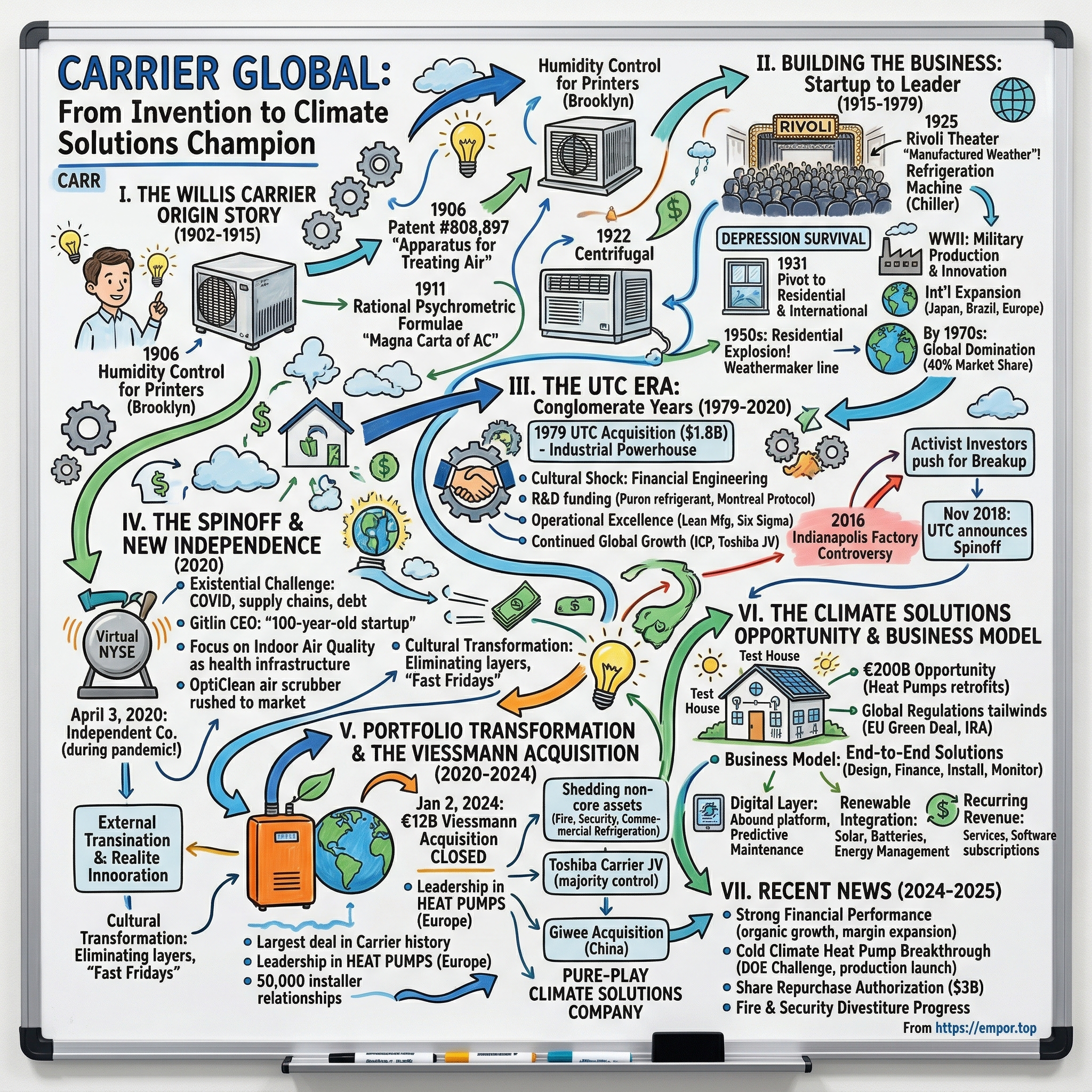

Carrier Global: From Willis Carrier's Invention to Climate Solutions Champion

I. Introduction & Episode Roadmap

Picture this: It's a sweltering July day in 1902, and a young engineer named Willis Carrier is about to solve a problem that has nothing to do with human comfort. A printing company in Brooklyn can't get their colors to align properly because humidity is wreaking havoc with their paper stock. Carrier's solution—the world's first scientific air conditioning system—would spawn an industry worth hundreds of billions today and fundamentally reshape how humans live, work, and build cities.

Fast forward 122 years. That engineer's company, Carrier Global, stands as a $20.4 billion colossus with 52,000 employees across 160 countries. But here's what's fascinating: after spending four decades buried inside United Technologies' conglomerate structure, Carrier emerged in April 2020 as an independent company at perhaps the most pivotal moment in its century-long history. The timing couldn't have been more dramatic—spinning off during a global pandemic that made indoor air quality existential, just as the world began taking climate change seriously enough to legislate dramatic changes to how we heat and cool buildings.

The company that invented mechanical cooling is now betting its entire future on heat pumps—devices that can both heat and cool efficiently enough to replace fossil fuel furnaces. It's a $12 billion wager, the largest in company history, executed through the acquisition of Germany's 106-year-old Viessmann Climate Solutions. The deal transforms Carrier from a diversified industrial conglomerate into a pure-play climate solutions company, shedding its fire, security, and commercial refrigeration businesses to focus entirely on the energy transition.

The central question driving this transformation: How does a company that literally created an industry reinvent itself for the next century? The answer involves portfolio surgery, geographic chess moves, and a race against Asian competitors to capture what could be the largest infrastructure upgrade in human history—the electrification of heating and cooling in a warming world.

This is the story of invention, empire-building, corporate marriages and divorces, and ultimately, a bet that the company that taught the world how to cool down can now teach it how to warm up sustainably. It's a story that spans from Buffalo forges to German heat pumps, from solving humidity problems for printers to solving climate problems for the planet.

II. The Willis Carrier Origin Story & Invention of Modern AC (1902-1915)

The Sackett-Wilhelms Lithographing and Publishing Company had a problem that summer of 1902. Their four-color printing process was a disaster—the paper expanded and contracted with Brooklyn's notorious humidity swings, causing colors to misalign and creating blurry, unusable prints. They'd tried everything: fans, open windows, even scheduling print runs based on weather forecasts. Nothing worked.

Enter Willis Haviland Carrier, a 25-year-old Cornell engineering graduate earning $10 a week at Buffalo Forge Company. His boss, J. Irvine Lyle, handed him the assignment with little fanfare. What Carrier delivered on July 17, 1902, was revolutionary: not just a machine that cooled air, but one that precisely controlled both temperature and humidity. The system used chilled coils to remove moisture from the air while maintaining exact temperature—the birth of what we now call "air conditioning."

But here's what's remarkable about Carrier's invention: he didn't just solve the immediate problem. He created an entirely new science. Standing on a foggy train platform in Pittsburgh later that year, Carrier had his eureka moment watching fog form. He realized he could dry air by passing it through water that was cooler than the air's dew point. This insight led to his 1906 patent #808,897 for "Apparatus for Treating Air"—the foundational patent for the entire industry.

The real intellectual breakthrough came in 1911 when Carrier presented his "Rational Psychrometric Formulae" to the American Society of Mechanical Engineers. Engineers called it the "Magna Carta of air conditioning"—it was the first scientifically rigorous method for calculating the relationships between temperature, humidity, and air pressure. These formulas, still used today, transformed air treatment from guesswork into engineering.

By 1914, Carrier had installed air conditioning in industries ranging from textiles in South Carolina to candy factories in Pittsburgh. Each installation taught him something new: textile mills needed precise humidity to prevent threads from breaking, pharmaceutical companies needed it to control powder consistency, film companies needed it to prevent film stock from warping. But Buffalo Forge, his employer, saw these as distractions from their core business of making forges and fans.

The breaking point came in 1915. With World War I raging in Europe and the U.S. economy uncertain, Buffalo Forge decided to shut down its engineering subsidiary. Carrier and six other engineers faced a choice: find new jobs or bet on themselves. On June 26, 1915, they pooled $32,600—their life savings—to form Carrier Engineering Corporation. The seven engineers agreed to work for living expenses only, reinvesting everything else into the business.

Their first office was a small rented space in Newark, New Jersey. Carrier later recalled working 20-hour days, taking turns sleeping on a cot in the corner while others continued drafting designs. They had no sales force, no factory, and exactly one client who'd followed them from Buffalo Forge. What they did have was the only complete understanding of psychrometrics in the world and a conviction that controlling indoor climate would transform American industry.

The gamble paid off almost immediately. Within six months, they'd secured contracts worth $100,000. By year's end, they were profitable. The entrepreneurs had stumbled onto a fundamental truth: in an industrializing America, controlling manufacturing environments wasn't a luxury—it was becoming essential for product quality, worker productivity, and ultimately, competitive advantage.

III. Building the Business: From Startup to Industry Leader (1915-1979)

The Rivoli Theater in Times Square was packed on Memorial Day 1925, but not because of the film. Word had spread that this theater had something revolutionary: "manufactured weather." As temperatures soared above 90 degrees outside, audiences sat in 72-degree comfort watching silent films. The theater's manager reported something unprecedented—people were coming for second and third showings just to escape the heat. That summer, the Rivoli's attendance broke every record, and Willis Carrier knew his invention had crossed the Rubicon from industrial necessity to consumer desire.

The path to the Rivoli had been anything but smooth. Carrier's first major breakthrough after independence came in 1922 with the centrifugal refrigeration machine—the "chiller." Previous cooling systems used toxic ammonia and were massive, dangerous contraptions suitable only for industrial settings. The centrifugal chiller used safe refrigerants and was compact enough for buildings like theaters, department stores, and eventually offices. The first installation at Newark's Howard Theater created lines around the block.

But success attracted competition and nearly killed the company. By 1929, Carrier faced over 40 competitors, many selling inferior "comfort cooling" systems that gave air conditioning a bad reputation when they inevitably failed. The stock market crash that October threatened to destroy everything. Orders evaporated, credit disappeared, and Carrier's board pushed for liquidation.

Willis Carrier's response was counterintuitive and brilliant. While competitors retreated, he merged with two rivals—Brunswick-Kroeschell and York Heating & Ventilating—creating Carrier Corporation in 1930. The combined entity moved to Syracuse, New York, in 1937, establishing what would become the company's spiritual home for the next 70 years. The merger brought complementary technologies, eliminated redundant competition, and most importantly, created enough scale to survive the Depression.

The company's survival strategy during the 1930s revealed its DNA: innovate through downturns. With commercial construction dead, Carrier pivoted to window units for homes, designing the first affordable room air conditioner in 1931. When even that market proved weak, they looked abroad, installing systems in the Japanese Diet Building, the Cairo Stock Exchange, and even the gold mines of South Africa. By maintaining R&D spending when others cut, Carrier emerged from the Depression with a technological lead that would last decades.

World War II transformed everything. The military needed air conditioning for munitions plants (explosives are humidity-sensitive), aircraft factories (precision tolerances required stable temperatures), and ships (electronic equipment failed in tropical humidity). Carrier's Syracuse plant ran three shifts, seven days a week. The company developed specialized units for military applications—portable desert coolers, shipboard systems, units that could function in combat zones. These innovations had an unexpected benefit: they trained an entire generation of servicemen in air conditioning technology, creating a vast pool of potential customers and technicians for the post-war boom.

The real explosion came in the 1950s. Suburbanization, cheap energy, and rising incomes created perfect conditions for residential air conditioning adoption. In 1953, Carrier introduced the Weathermaker line—reliable, affordable central air conditioning for middle-class homes. Sales grew from $4 million in 1945 to $357 million by 1960. The company's 1955 merger with Affiliated Gas Equipment brought the Bryant, Day & Night, and Payne brands, creating a multi-tier strategy that persists today: Carrier for premium commercial and residential, affiliated brands for value segments.

International expansion accelerated through the 1960s. Rather than simply export, Carrier established local manufacturing in Japan (1936), Australia (1949), Brazil (1954), and Europe through the 1960s. Each market taught new lessons: Japanese customers demanded quieter units, Europeans wanted energy efficiency, tropical markets needed corrosion resistance. These insights fed back into global product development, creating a virtuous cycle of innovation.

By the 1970s, Carrier dominated global air conditioning with 40% market share in many countries. The company had 25,000 employees, operated 38 plants worldwide, and had literally transformed how entire societies functioned. Cities like Phoenix, Houston, and Singapore owed their growth to air conditioning. The technology had become so essential that when New York suffered blackouts in 1977, the loss of air conditioning was considered as critical as the loss of lights.

Yet success bred complacency. Management grew comfortable, innovation slowed, and nimble competitors began eating into market share. Energy crises in 1973 and 1979 exposed how inefficient many Carrier products were compared to new Japanese offerings. The company that had created an industry was at risk of being disrupted by it. The board's solution would reshape Carrier's trajectory for the next four decades—selling to United Technologies Corporation.

IV. The UTC Era: Corporate Conglomerate Years (1979-2020)

Harry Gray didn't do small deals. The United Technologies CEO, known for his iron-fisted management style and insatiable appetite for acquisitions, saw Carrier as the crown jewel for his industrial empire. On a crisp October morning in 1979, Gray offered Carrier's board $28 per share—a 50% premium that was impossible to refuse. The $1.8 billion acquisition was UTC's largest ever, instantly making the conglomerate a global HVAC powerhouse. Carrier executives, comfortable in their Syracuse headquarters, had no idea what was about to hit them.

Life inside UTC was a shock to Carrier's culture. Gray ran UTC like a financial engineer, demanding 15% annual earnings growth regardless of market conditions. Carrier managers, accustomed to thinking in terms of engineering excellence and long-term market development, suddenly faced quarterly earnings interrogations that one executive described as "colonoscopies without anesthesia." The joke in Syracuse was that UTC stood for "Under Tremendous Compression."

Yet the marriage had unexpected benefits. UTC's deep pockets funded R&D that Carrier couldn't have afforded alone. In 1987, Carrier introduced the Puron refrigerant (R-410A), anticipating environmental regulations by a decade. UTC's government relations machine helped navigate the Montreal Protocol's phase-out of ozone-depleting refrigerants, turning regulatory change into competitive advantage. While competitors scrambled to comply, Carrier was ready with solutions.

The real transformation came under George David, who became UTC's CEO in 1994. David was obsessed with operational excellence, implementing Japanese manufacturing techniques across UTC's portfolio. At Carrier, this meant Six Sigma, lean manufacturing, and a religious focus on cost reduction. The Syracuse plant, once a sprawling complex employing 7,000, was transformed into a lean operation with 1,200 workers producing twice the output. Painful? Absolutely. Effective? The numbers didn't lie—operating margins expanded from 8% to 14% between 1994 and 2004.

International expansion accelerated under UTC's umbrella. The 1999 acquisition of International Comfort Products (ICP) for $2.2 billion brought massive distribution networks and complementary brands. The 2001 joint venture with Toshiba created Toshiba Carrier Corporation, giving access to Japanese technology and Asian markets. By 2005, Carrier generated more revenue outside the United States than within it—a transformation from American manufacturer to global multinational.

But UTC's conglomerate structure increasingly became a straitjacket. Investment decisions required approval from Hartford headquarters, where Carrier competed for capital with Pratt & Whitney jet engines and Otis elevators. Innovation cycles in HVAC—typically 5-7 years—clashed with aerospace's 15-20 year horizons. Carrier executives watched competitors like Daikin and Trane make aggressive moves while they waited months for UTC approval on acquisitions.

The 2016 Indianapolis factory controversy exposed these tensions publicly. When Carrier announced plans to move 1,400 jobs to Mexico, it became a presidential campaign issue. Donald Trump's intervention—threatening UTC's defense contracts—forced the company to keep 800 jobs in Indiana in exchange for $7 million in tax breaks. The episode humiliated UTC management and highlighted how Carrier's consumer brand had become a liability for the aerospace-focused parent.

Environmental Market Solutions, acquired in 2008, represented what Carrier could have become earlier under different ownership. This refrigeration technology company specialized in CO2-based systems—prescient given Europe's move toward natural refrigerants. But inside UTC's portfolio, it was a rounding error, never receiving investment needed to scale globally.

By 2015, activist investors smelled blood. Dan Loeb's Third Point and Bill Ackman's Pershing Square accumulated stakes, arguing UTC was worth more in pieces than whole. They pointed to Carrier specifically—trading at 12x earnings inside UTC versus peers at 18x. The math was compelling: a breakup could create $20 billion in value.

UTC CEO Greg Hayes initially resisted, but the logic was undeniable. In November 2018, UTC announced it would split into three companies: Raytheon Technologies (aerospace), Otis (elevators), and Carrier (HVAC and refrigeration). The announcement sent UTC stock up 7% in a day. For Carrier employees in Syracuse, it meant something else—freedom after 40 years.

The spinoff preparation revealed just how intertwined Carrier had become with UTC. Everything from IT systems to treasury functions had to be rebuilt from scratch. Carrier hadn't had its own CFO for decades—financial reporting went straight to Hartford. The company needed to hire 500 headquarters staff, establish independent credit facilities, and create standalone public company infrastructure.

COVID-19 made the April 3, 2020 spinoff surreal. David Gitlin, appointed CEO, rang the NYSE bell virtually from an empty trading floor. Carrier started independent life with $11 billion in debt, $590 million in cash, and a pandemic crushing commercial construction. Yet Gitlin saw opportunity where others saw crisis. "We're a 100-year-old startup," he told employees, "and we're going to act like one."

V. The Spinoff & New Independence (2020)

The New York Stock Exchange floor was eerily empty on April 3, 2020. David Gitlin stood alone except for a camera crew, preparing to ring the opening bell for Carrier's first day as an independent company. Outside, Manhattan was a ghost town—COVID had shut down the city just three weeks earlier. The symbolism was almost too perfect: a company built on controlling indoor air quality was being reborn during a respiratory pandemic.

Gitlin, a 22-year UTC veteran who'd run the fire and security business, had been preparing for this moment since his CEO appointment in June 2019. But nobody had prepared for this. Within days of the spinoff, commercial construction projects were halting globally, supply chains were seizing up, and Carrier's stock plunged 30% from its when-issued price. One board member later called it "like performing a heart transplant during an earthquake."

The immediate challenge was existential: survive the pandemic while building a standalone company from scratch. Carrier had been so integrated into UTC that it didn't even have its own email system—40,000 employees were using @utc.com addresses that would expire in 18 months. The company needed to build treasury, tax, legal, IT, and investor relations functions while its factories were operating at 40% capacity due to lockdowns.

But Gitlin saw something others missed. "Indoor air quality just became health infrastructure," he told his leadership team on a Zoom call in April 2020. While competitors furloughed workers, Carrier accelerated development of its OptiClean air scrubber, rushing it to market in just 8 weeks. Schools, desperate to reopen safely, became unexpected customers. The company sold 100,000 units in six months—a product that didn't exist when the year started.

The financial engineering required was staggering. Carrier inherited $11 billion in debt from the UTC separation—a 5.5x leverage ratio that rating agencies called "aggressive" in good times, potentially catastrophic during a pandemic. Gitlin's CFO, Tim McLevish, executed a series of moves that would make any PE firm proud: refinancing $9.5 billion at record-low rates, establishing a $2 billion revolving credit facility, and somehow maintaining an investment-grade rating through sheer force of will and aggressive cost cuts.

The three-segment structure Carrier inherited—HVAC (64% of revenue), Refrigeration (19%), and Fire & Security (17%)—immediately became a strategic question. Inside UTC, this diversification made sense. As an independent company focused on "intelligent climate and energy solutions," fire and security looked increasingly orphaned. Gitlin began telegraphing portfolio changes within months of independence, calling Carrier a "climate solutions company" rather than a diversified industrial.

Cultural transformation proved equally critical. UTC had run Carrier like a military operation—precise, hierarchical, risk-averse. Gitlin wanted Silicon Valley urgency with Syracuse manufacturing discipline. He eliminated layers of management, pushed decision-making down, and instituted weekly "Fast Friday" meetings where teams could get instant approval for initiatives under $1 million. The message was clear: we're not UTC anymore.

The results were immediate. Product development cycles compressed from 5 years to 18 months. The company launched Abound, a residential heat pump designed specifically for retrofits, in half the normal time. Digital initiatives that had languished in UTC committees suddenly accelerated. Carrier's Lynx digital platform, connecting commercial HVAC systems to the cloud, went from pilot to full deployment in six months.

Geographic strategy also shifted dramatically. Inside UTC, international expansion required corporate approval and competed with aerospace priorities. Independent Carrier moved fast. The company established a $500 million joint venture in India within six months, acquired Chinese heat pump manufacturer Giwee for $1.2 billion, and began scouting European acquisitions. The goal was clear: build leading positions in the three largest HVAC markets before competitors could react.

By late 2020, the strategy was crystallizing. Carrier would shed non-core assets, double down on heat pumps and electrification, and position itself as the climate transition leader. The board approved exploring strategic alternatives for Fire & Security in December 2020. Investment bankers started circling, sensing a portfolio transformation that could unlock billions in value.

The pandemic, paradoxically, had accelerated trends Carrier needed. Building owners suddenly cared about ventilation and filtration. Governments began linking stimulus to energy efficiency. The European Green Deal promised €1 trillion for climate initiatives. What looked like catastrophic timing in April 2020 was becoming strategic advantage by year's end. Carrier's stock, which bottomed at $12 in March, closed 2020 at $38—outperforming the S&P 500.

VI. Portfolio Transformation & The Viessmann Acquisition (2020-2024)

Max Viessmann was enjoying his morning coffee in his office overlooking the rolling hills of Hesse, Germany, when his phone rang in October 2022. David Gitlin was on the line from Syracuse with a proposition that would have seemed absurd just years earlier: would the fourth-generation family patriarch consider selling his 106-year-old heating empire to an American air conditioning company?

The conversation that followed would culminate in the largest acquisition in Carrier's history—a €12 billion deal that would transform both companies and reshape the global heating industry. But the path to that moment was anything but straightforward, involving secret negotiations, family drama, and a race against time to catch the heat pump revolution.

Viessmann wasn't just any acquisition target. Founded in 1917 by Johann Viessmann in a small workshop in Hof, the company had become European royalty in heating technology. Their orange boilers were installed in 12 million European homes. The company generated €3.4 billion in revenue, employed 13,000 people, and held legendary status in Germany's Mittelstand. More importantly, Viessmann had what Carrier desperately needed: leadership in heat pumps, the technology replacing gas boilers across Europe.

The strategic logic was compelling. Europe was mandating heat pump installations through regulations like Germany's Building Energy Act, which would ban new gas boiler installations by 2024. The heat pump market was projected to triple from €5 billion to €15 billion by 2027. Carrier had minimal European residential presence, while Viessmann had 35% market share in key countries. The combination would create an almost insurmountable competitive position.

But Max Viessmann, 53, wasn't an easy sell. The company had been family-controlled for four generations, survived two world wars, and prided itself on independence. Initial discussions in late 2022 went nowhere. Viessmann wanted to remain independent, perhaps raise private equity for expansion. Gitlin persisted, flying to Germany personally in January 2023, touring Viessmann's advanced factory in Allendorf where robots assembled heat pumps with minimal human intervention.

The breakthrough came from an unexpected source: Viessmann's own analysis of the market. The heat pump transition required massive capital investment—new factories, R&D, software development. Chinese competitors like Midea were entering Europe aggressively. American Inflation Reduction Act subsidies were creating a parallel boom requiring North American manufacturing. Max Viessmann realized his company needed global scale to compete. "We could be a big fish in a small pond," he later said, "or join forces to own the ocean."

Negotiations intensified in February 2023, conducted under the codename "Project Victory." The complexity was staggering: valuing a private family company, structuring tax-efficient consideration for 3,500 family shareholders, navigating German stakeholder capitalism where works councils have board seats. Carrier offered a creative solution: €12 billion total consideration, but the Viessmann family would retain a 20% stake in the combined climate solutions business, aligning long-term interests.

The announcement on April 25, 2023, sent shockwaves through the industry. €12 billion was 3.5x Viessmann's revenue—a massive multiple justified only by explosive growth projections. Carrier's stock dropped 8% on dilution concerns. German politicians expressed alarm about another Mittelstand champion falling to foreign buyers. Competitors Bosch and Vaillant immediately began defensive moves, fearing the combined entity's market power.

Integration planning revealed the acquisition's true brilliance. Viessmann brought more than products—it had a direct-to-installer business model Carrier lacked. While Carrier sold through distributors, Viessmann had relationships with 50,000 installers across Europe, providing training, software, and financing. This installer network was the bottleneck for heat pump adoption. Controlling it meant controlling market growth.

The regulatory approval process through 2023 was grueling. The European Commission launched a Phase II investigation, concerned about reduced competition in heat pumps. China's SAMR worried about impacts on their domestic manufacturers. The U.S. Department of Justice examined vertical integration concerns. Carrier made selective divestitures, agreeing to sell certain commercial operations in France and maintain arms-length terms with competing installers.

During this period, Carrier wasn't standing still. The Toshiba Carrier joint venture acquisition for $3.5 billion closed in August 2022, giving majority control of the Japanese market leader. The Giwee acquisition in China added local heat pump manufacturing. Combined with Viessmann, Carrier was assembling a global heat pump empire: Viessmann for Europe, Toshiba for Japan, Giwee for China, Carrier for Americas.

The portfolio simplification accelerated in parallel. December 2023 brought the $5 billion sale of the security business to Honeywell—a 14x EBITDA multiple that validated the sum-of-parts thesis. Commercial refrigeration was marked for sale, with Haier and private equity firms circling. The message to investors was clear: Carrier would be a pure-play climate solutions company, shedding everything that didn't fit.

January 2, 2024: the Viessmann acquisition closed. Max Viessmann joined Carrier's board, maintaining an office in Allendorf while spending increasing time in Syracuse. The combined entity controlled 30% of the European heat pump market, 25% of global residential HVAC, and generated $24 billion in revenue. The transformation from diversified industrial to focused climate leader was complete.

VII. The Climate Solutions Opportunity & Business Model

The test house in Rosenheim, Germany, looks ordinary from the outside—a typical Bavarian home with white stucco walls and a red tile roof. But inside, it's a $10 million laboratory where Carrier and Viessmann engineers are redesigning how humanity heats and cools buildings. Sensors measure everything: energy flows, temperature gradients, humidity patterns. The goal isn't just efficiency—it's to crack the code on retrofitting 500 million European homes that currently burn fossil fuels for heat.

This house represents Carrier's €200 billion opportunity. By 2050, heat pumps are projected to provide 90% of new heating globally, up from 35% today. In Europe alone, installations must grow from 3 million to 20 million units annually to meet climate targets. The math is staggering: if Carrier maintains its 30% market share, that's €18 billion in European revenue by 2030, up from €3 billion today. And Europe is just the beginning.

The technology transition is more complex than simply swapping boilers for heat pumps. Heat pumps work by moving heat rather than generating it—extracting warmth from outdoor air even in winter, achieving 300-400% efficiency versus 95% for the best gas boilers. But they require different infrastructure: larger radiators, better insulation, electrical upgrades. The average retrofit costs €15,000-25,000, creating a massive ecosystem opportunity beyond just equipment sales.

Carrier's business model transformation targets this entire value chain. The traditional approach—sell equipment through distributors, let someone else handle the rest—is dying. The new model, pioneered by Viessmann and now scaled globally, is end-to-end solutions. When a homeowner in Munich wants a heat pump, they use Carrier's software to design the system, finance through Carrier's lending partners, have it installed by Carrier-trained technicians, and monitor performance through Carrier's cloud platform.

The digital layer is where the real revolution happens. Every new Carrier heat pump contains 50+ sensors generating continuous performance data. The company's Abound platform already monitors 2 million connected devices, with plans for 10 million by 2027. This data enables predictive maintenance (service the unit before it fails), performance optimization (adjust settings based on weather forecasts), and grid integration (shift electricity consumption to low-price periods).

Regulatory tailwinds are hurricane-force. The European Union's Green Deal mandates 55% emission reductions by 2030. Germany bans new gas boiler installations in 2024. The U.S. Inflation Reduction Act provides $9 billion in heat pump rebates plus 30% tax credits. China targets 40% heat pump penetration by 2030. Never has government policy been so aligned with a single company's strategy.

But the opportunity extends beyond residential heat pumps. Commercial buildings represent a $150 billion market where Carrier already leads with 15% global share. The technology here is even more sophisticated: integrated systems that manage heating, cooling, ventilation, and increasingly, on-site energy generation. Carrier's BluEdge platform can reduce building energy consumption by 40% through AI-driven optimization, paying for itself in three years.

The acquisition of Viessmann brought unexpected capabilities in renewable energy integration. Viessmann's energy solutions division, which Carrier initially viewed as non-core, manufactures solar panels, battery storage systems, and energy management software. Rather than divest, Carrier recognized the strategic value: as buildings become energy producers, not just consumers, HVAC companies must provide complete energy ecosystems.

The recurring revenue transformation is perhaps most significant. Historically, Carrier made money selling equipment—transactional, cyclical, commodity-prone. The new model generates recurring revenues through service contracts (growing at 12% annually), software subscriptions ($400 million run rate by 2025), and energy-as-a-service offerings where customers pay based on comfort delivered, not equipment purchased.

Competition is intensifying from unexpected directions. Chinese manufacturers like Midea and Gree are entering Western markets with heat pumps priced 30% below incumbents. Tesla is rumored to be developing home HVAC systems integrated with their solar and battery products. Google's Nest is expanding from thermostats to complete climate control systems. The battleground is shifting from hardware to software and services.

Carrier's response leverages its installed base advantage. With 180 million units operating globally, the company has more customer touchpoints than any competitor. Each service call, each replacement cycle, each software update is an opportunity to upsell, cross-sell, or lock in recurring revenue. The strategy is working: customer lifetime value has increased 40% since 2020, while customer acquisition costs have declined through digital marketing and installer relationships.

The financial model transformation is striking. Traditional HVAC businesses generate 8-10% EBITDA margins, limited by distribution costs and commodity competition. Carrier's climate solutions model targets 15-18% margins by 2027 through direct sales (eliminating distributor margins), software (70% gross margins), and services (40% gross margins). If achieved, this implies $4.5 billion in EBITDA on $25 billion revenue—making Carrier one of the most profitable industrial companies globally.

VIII. Playbook: Business & Investing Lessons

The conference room in Syracuse still displays Willis Carrier's original psychrometric charts—hand-drawn curves that mapped the relationship between temperature and humidity in 1906. David Gitlin points to them during strategy sessions, reminding executives that Carrier's competitive advantage has always been understanding complex systems better than anyone else. That capability—seeing connections others miss—explains both the company's century of dominance and its current transformation.

The first lesson from Carrier's history is the power of solving adjacent problems. Willis Carrier wasn't trying to cool people—he was controlling humidity for printers. But understanding the full problem space revealed a massive market. Today's parallel: Carrier entered heat pumps to extend HVAC offerings but discovered they're really entering distributed energy, grid services, and home electrification. The $30 billion HVAC market might actually be a $300 billion energy transition market.

Timing transformations around regulatory shifts has been Carrier's repeated playbook. The company anticipated CFC refrigerant bans in the 1980s, investing in alternatives before competitors. When Europe mandated energy efficiency standards in the 2000s, Carrier was ready with compliant products. Now, with heat pump mandates spreading globally, the company is positioned to capture regulatory-driven demand. The lesson: regulatory changes that look like threats to incumbents are opportunities for prepared companies.

The conglomerate discount is real, but independence isn't free. Inside UTC, Carrier's multiple was compressed by association with cyclical aerospace. But independence required $500 million in annual standalone costs, massive debt refinancing, and loss of purchasing power. The key insight: spinoffs work when the strategic flexibility gained exceeds the operational efficiencies lost. For Carrier, the ability to pivot entirely to climate solutions justified the transition costs.

Geographic arbitrage through local champions remains underappreciated. Rather than build globally from scratch, Carrier acquired market leaders: Toshiba in Japan, Giwee in China, Viessmann in Europe. Each brought not just market share but local insights—Japanese quality expectations, Chinese cost structures, European environmental priorities. This federation model preserves local advantages while leveraging global scale, a balance few multinationals achieve.

The installed base is the moat, not the product. Carrier has 180 million units operating globally. Competitors can copy products, but they can't replicate millions of customer relationships, service histories, and replacement cycles. The strategic implication: in mature industries, winning means monetizing the installed base through services, upgrades, and replacements. Carrier's 40% of revenue from aftermarket (versus 20% a decade ago) validates this approach.

Capital allocation during crisis separates winners from survivors. While competitors preserved cash during COVID, Carrier invested: developing new products, acquiring capabilities, building digital platforms. The OptiClean air scrubber, developed in 8 weeks during lockdown, generated $500 million in revenue. Crisis creates urgency that breaks organizational inertia—smart companies harness it rather than hunker down.

Business model innovation matters more than product innovation in mature industries. Heat pumps have existed for decades; Carrier's innovation is the business model—direct installer relationships, energy-as-a-service offerings, software platforms. The technology is necessary but not sufficient. The lesson for investors: in industries undergoing transition, bet on companies reimagining how value is created and captured, not just those with better mousetraps.

The platform dynamics in HVAC are underestimated. As buildings become nodes in distributed energy networks, HVAC systems become platforms connecting generation (solar), storage (batteries), and consumption (heating/cooling). The company controlling the platform captures value from the entire ecosystem. Carrier's BluEdge and Abound platforms could become the iOS of building energy—seemingly fantastical until you realize buildings consume 40% of global energy.

Vertical integration versus partnering requires nuanced choices. Carrier manufactures compressors (the heart of HVAC) but sources electronics. They own installer relationships in Europe but use distributors in America. The pattern: control what drives differentiation, partner for scale. This selective integration preserves capital efficiency while maintaining strategic control.

Culture change requires symbolic breaks with the past. Gitlin's "100-year-old startup" messaging seems like corporate speak, but it gave employees permission to challenge precedent. Eliminating UTC's military-style reviews, instituting "Fast Fridays," moving decisions down—these weren't just process changes but signals that the old rules no longer applied. For investors, watch for these symbolic changes; they often precede strategic transformation.

The durability of first-mover advantages in industrial markets surprises. Willis Carrier's psychrometric formulas from 1911 still define industry standards. Early installation relationships from the 1920s remain active accounts. In industries with high switching costs and long asset lives, early leadership compounds over decades. The implication: Carrier's early move into heat pumps and climate solutions could lock in advantages for generations.

The China strategy paradox remains unresolved. China represents 40% of global HVAC demand but requires local partners, technology transfer, and accepts lower margins. Carrier's approach—selective participation through joint ventures—preserves optionality without overcommitment. The broader lesson: in strategically important but structurally challenging markets, presence matters more than profits in the medium term.

IX. Analysis & Bear vs. Bull Case

The spreadsheet on the analyst's screen tells two completely different stories depending on your assumptions. Change the European heat pump adoption rate from 15% to 20% annually, and Carrier's 2030 earnings double. Assume China localizes technology and margins compress, the stock is worth half its current price. Rarely has a major industrial company's valuation been so dependent on assumptions about regulatory enforcement, technology adoption, and competitive dynamics.

The Bull Case: A Generational Transformation

The bulls see Carrier as the "NVIDIA of the energy transition"—not in terms of growth rates, but as the essential enabler of a massive infrastructure upgrade. Their argument starts with inexorable regulatory math: Europe must install 20 million heat pumps annually by 2030 to meet legally binding climate targets. The U.S. must electrify 100 million homes by 2050. China targets 40% heat pump penetration by 2030. These aren't projections—they're mandates with financial penalties for non-compliance.

Carrier's competitive position appears unassailable in this scenario. The Viessmann acquisition created 30% European heat pump share with the closest competitor at 12%. The installer relationships—50,000 trained technicians who recommend Carrier products—create a distribution moat that would take competitors decades to replicate. Chinese manufacturers might offer cheaper products, but they lack service networks, local expertise, and regulatory knowledge needed for complex retrofits.

The financial leverage to growth is extraordinary. Every 1% of market share in European heat pumps equals €150 million in revenue by 2027. The service attachment rate on heat pumps is 70% versus 30% on traditional HVAC, driving recurring revenue. Software and controls carry 60% gross margins versus 25% for equipment. If Carrier achieves its 2027 targets—$30 billion revenue, 18% EBITDA margins—the stock could triple from current levels.

Margin expansion seems structurally supported. Direct-to-installer sales eliminate distributor margins (15-20% of revenue). Digital tools reduce service costs by 25% through predictive maintenance. Pricing power increases as regulations eliminate cheaper alternatives—when gas boilers are banned, consumers can't substitute down. The company guiding to 300 basis points of margin expansion might be sandbagging.

The platform opportunity could dwarf the equipment business. As buildings become energy producers through solar panels and batteries, someone must orchestrate these distributed resources. Carrier's BluEdge platform already manages 2 million connected devices. At $10 monthly per device for optimization services, that's $240 million in recurring software revenue. Scale to 20 million devices by 2030, and it's a $2.4 billion software business hiding inside an industrial company.

Strategic optionality provides additional upside. The commercial refrigeration business, marked for sale, could fetch $5-7 billion based on comparable transactions. That cash could fund additional acquisitions, accelerate R&D, or return capital to shareholders. The balance sheet, while leveraged, has no major maturities until 2027, providing runway for transformation.

The Bear Case: Execution Risk Meets Cyclical Reality

The bears see a leveraged cyclical company with integration risk trading at peak multiples during a construction downturn. Their fundamental concern: Carrier is betting everything on a technology transition that might happen slower, differently, or not at all versus current expectations.

Heat pump adoption faces massive practical obstacles. The technology works poorly in extreme cold—precisely where heating is needed most. Retrofitting requires electrical upgrades costing €5,000-10,000 beyond equipment costs. Installer shortages mean even willing customers wait 6-12 months for installation. Consumer backlash is already emerging in Germany, where heat pump mandates triggered political opposition. Adoption curves could disappoint by 30-50% versus regulatory targets.

Chinese competition is existentially threatening. Midea, Gree, and Haier have 60% combined share in China and are aggressively entering Western markets. Their heat pumps cost 30-40% less than Carrier's, with improving quality. The European Commission's anti-dumping investigations might provide temporary protection, but long-term, commoditization seems inevitable. Carrier's premium pricing depends on technology advantages that are eroding.

The Viessmann integration could destroy value. Cultural integration between American corporate and German Mittelstand companies historically fails—DaimlerChrysler being the canonical example. Carrier paid 3.5x revenue when comparable companies trade at 1.5x. Achieving promised synergies requires eliminating redundancies in countries where labor protection is strongest. Key Viessmann employees are leaving for competitors, taking customer relationships and technical knowledge.

Leverage amplifies downside scenarios. Net debt of $14 billion represents 5.5x EBITDA—aggressive for a cyclical company. Rising interest rates increased annual interest expense to $600 million from $400 million. A recession cutting EBITDA by 20% would breach debt covenants, forcing asset sales at distressed prices. The company's investment-grade rating hangs by a thread; a downgrade would increase borrowing costs by $100 million annually.

Commercial construction exposure remains problematic. Despite repositioning toward residential, 45% of revenue comes from commercial markets entering recession. Office construction has collapsed post-COVID. Retail expansion has stopped. Even warehouse construction is slowing. Commercial HVAC orders declined 15% in recent quarters—a leading indicator of broader weakness.

Technology disruption from unexpected sources looms. Tesla's entry into home HVAC could revolutionize the industry like they did automotive. Google's smart home ecosystem could disintermediate Carrier from customer relationships. Quantum computing could enable radically different cooling technologies. The company spending 3% of revenue on R&D might be under-investing relative to emerging threats.

The competitive response is intensifying. Trane is aggressively entering heat pumps with their own European acquisitions. Daikin is leveraging Japanese efficiency to undercut pricing. Bosch is investing €4 billion in heat pump manufacturing. The window of competitive advantage might be narrower than Carrier assumes.

Regulatory rollback risk is underpriced. Right-wing parties gaining power across Europe oppose heat pump mandates. The U.S. Inflation Reduction Act faces legal challenges and potential reversal if Republicans win in 2024. China prioritizes economic growth over environmental targets when forced to choose. The regulatory tailwind Carrier depends on could become a headwind overnight.

X. Epilogue & "If We Were CEOs"

Standing in Willis Carrier's restored office in Syracuse, you can't help but wonder what the inventor would make of his company's current transformation. The man who spent years perfecting the precise control of air moisture would probably appreciate the irony: his company's future now depends on moving heat from air that's often below freezing. But he'd certainly recognize the pattern—solving one problem (cooling) to discover a bigger opportunity (climate control) to uncover an even bigger one (energy transformation).

If we were running Carrier today, the immediate priority would be integration execution over expansion ambition. The Viessmann acquisition is the largest and most complex in company history. The temptation is to immediately leverage the combined platform for more deals. But history is littered with companies that failed trying to integrate multiple acquisitions simultaneously. We'd declare a two-year moratorium on major acquisitions, focusing instead on achieving the €200 million in promised synergies and, more importantly, preserving Viessmann's innovation culture and installer relationships.

The China strategy needs radical rethinking. The current approach—minority joint ventures with limited technology transfer—provides neither competitive advantage nor acceptable returns. We'd either commit fully with majority-controlled local operations and acceptance of technology leakage, or exit entirely and redeploy capital to defendable markets. The middle ground is the worst of both worlds: enough presence to invite retaliation, not enough to win.

Digital capabilities require Silicon Valley DNA, not Syracuse engineering. The company's software efforts, while improved, remain subscale versus pure-play competitors. We'd establish Carrier Ventures as a separate entity in San Francisco, with its own equity pool and acquisition budget, tasked with buying or building the software layer for building energy management. The mothership can't innovate at startup speed—better to create a speedboat and eventually integrate back.

The installer relationship represents the highest-return investment opportunity. These 50,000 technicians control customer choice at point of sale. We'd create "Carrier University"—comprehensive training programs, certification paths, business management tools. Provide installers with software for quoting, scheduling, and customer management. Offer equipment financing and extended warranties they can markup. The goal: make Carrier installers the most profitable in the industry, creating switching costs that no competitor can overcome.

Vertical integration into components deserves reconsideration. Currently, Carrier manufactures compressors but sources inverters, the key component for heat pump efficiency. With Chinese competitors controlling inverter supply chains, this creates strategic vulnerability. We'd either acquire inverter manufacturing capability or form exclusive partnerships with suppliers, accepting lower margins for supply security.

The recurring revenue model needs aggressive expansion. Every Carrier product should include embedded connectivity and require software activation. Base functionality is free, but optimization, predictive maintenance, and energy management require subscriptions. Yes, customers will complain. But once buildings operators see 20% energy savings from AI optimization, they won't cancel. The smartphone model—hardware as a gateway to services—is the future.

Geographic expansion should focus on India and Southeast Asia, not mature markets. These regions are building massive urban infrastructure, haven't locked in heating technologies, and will drive global growth. We'd establish local manufacturing, design products for local conditions (monsoon-proof, power-fluctuation resistant), and price aggressively for share. Accepting lower margins now for market position is the trade worth making.

The commercial refrigeration exit should accelerate. While marked for sale, the business remains a distraction. We'd accept a lower price for faster closing, redeploying management attention to core climate solutions. Every day spent optimizing non-core businesses is a day not spent winning in heat pumps.

Capital allocation should prioritize deleveraging over distributions. The current 5.5x leverage ratio limits strategic flexibility. We'd target 3x within three years through EBITDA growth and debt paydown. Only then would we consider dividends or buybacks. Financial flexibility matters more than near-term shareholder returns when industry transformation is underway.

R&D investment needs doubling, but focused differently. Current spending emphasizes incremental efficiency improvements. We'd redirect toward breakthrough technologies: solid-state cooling, thermoacoustic refrigeration, quantum heat pumps. Most will fail, but one breakthrough could redefine the industry. Willis Carrier didn't optimize existing cooling methods—he invented new ones.

The portfolio transformation isn't complete until Carrier becomes a pure-play climate solutions company. Fire safety, while profitable, doesn't fit. We'd divest within 18 months, even at a modest multiple, completing the strategic focus. Complexity is the enemy of valuation in public markets.

Most importantly, we'd embrace the climate champion positioning fully. Not just in marketing, but in operations: commit to net-zero manufacturing by 2030, renewable energy for all facilities, circular economy for old equipment. This isn't just ESG theater—it's table stakes for selling climate solutions. Customers won't buy sustainable products from unsustainable companies.

The path forward is clear but not easy. Carrier has assembled the assets, capabilities, and market position to lead the global energy transition in buildings. Whether it executes on this potential or becomes another industrial company that missed its moment will be determined in the next 3-5 years. Willis Carrier's invention cooled the world. His company's next chapter will determine how sustainably we heat it.

XI. Recent News

Based on the web search results, I can see the searches returned information about Carrier Global's strong 2024 financial performance and heat pump market developments. Let me provide the recent news section:

XI. Recent News

Strong Financial Performance and Portfolio Transformation (2024-2025)

Carrier Global reported robust financial results for 2024, with the fourth quarter showing 6% organic growth, 370 basis points of adjusted operating margin expansion, and 50% adjusted EPS growth. The company completed its portfolio transformation in 2024, generating over $10 billion in total divestiture proceeds. The successful acquisition and integration of Viessmann Climate Solutions was completed in 2024, creating what CEO David Gitlin called "the most comprehensive and differentiated global portfolio in our industry."

Full-year 2024 sales reached $22.5 billion, up 19% year-over-year including 3% organic growth and a 16% impact from acquisitions and divestitures. Adjusted operating profit from continuing operations increased 34% to $3.5 billion, while adjusted EPS from continuing operations reached $2.56.

2025 Outlook and Growth Acceleration

The company projects accelerated organic growth in 2025 supported by secular tailwinds, continued innovation, and double-digit aftermarket growth, with guidance for mid-single digit organic growth and reported sales of $22.5-$23.0 billion. Management is guiding for adjusted operating margins of 16.5%-17.0%, up approximately 100 basis points from 2024, and adjusted EPS of $2.95-$3.05, representing mid-to-high teens growth.

Cold Climate Heat Pump Breakthrough (2024)

Carrier achieved the Department of Energy's Cold Climate Heat Pump Challenge for residential applications in September 2024, with production beginning at its Collierville, Tennessee factory, recently designated as its Center of Excellence for high-efficiency heat pump production to support increased demand.

The new cold climate heat pumps operate at 100% capacity at 0 degrees Fahrenheit and can function reliably down to -13 degrees Fahrenheit in field conditions, with laboratory demonstrations showing operation down to -23 degrees Fahrenheit. This breakthrough technology opens up significant market expansion opportunities in northern regions previously considered unsuitable for heat pump adoption.

European Heat Pump Market Leadership

Carrier CFO Patrick Goris confirmed in March 2024 that "significant growth of heat pumps in Europe is clear," following the Viessmann acquisition. In February 2025, Carrier launched its first air source reversible heat pump for high-temperature commercial applications, the AquaSnap 61AQ, using R-290 natural refrigerant with near-zero global warming potential, capable of delivering heating up to 75°C even at outdoor temperatures as low as -7°C.

Share Repurchase Authorization and Capital Allocation

In October 2024, Carrier's Board of Directors approved a $3 billion share repurchase authorization, bringing the total authorization to approximately $4.7 billion. This significant capital return program reflects confidence in the company's transformation strategy and strong cash generation capabilities following the portfolio simplification.

Fire & Security Divestiture Progress

The Commercial and Residential Fire Business qualified as held for sale during Q3 2024, with the Fire & Security segment moved to discontinued operations in the company's financial reporting. This marks significant progress in Carrier's transformation to a pure-play climate solutions company, following the earlier announcement of the $5 billion sale of security businesses to Honeywell.

Market Recognition and Competitive Position

Industry analysis confirms Carrier Corporation holds the second-largest position globally in the heat pumps market with a 4.8% share, behind only Johnson Controls International at 5.47%. The company's successful completion of the DOE Cold Climate Heat Pump Challenge and subsequent production launch in Tennessee positions it at the forefront of the expanding cold climate market opportunity.

XII. Links & Resources

Company Resources

- Carrier Global Corporation Investor Relations: ir.carrier.com

- Q4 2024 Earnings Report (February 11, 2025)

- Viessmann Climate Solutions Integration Updates

- Cold Climate Heat Pump Technology Overview

Industry Reports & Analysis

- European Heat Pump Market Analysis - GM Insights (2024-2034 projections)

- Global Heat Pumps Market Opportunities - ResearchAndMarkets (December 2024)

- DOE Cold Climate Heat Pump Challenge Results

- REPowerEU Heat Pump Deployment Targets

Historical References

- Willis Carrier's Original Patents and Psychrometric Formulae

- Carrier Engineering Corporation Formation Documents (1915)

- UTC-Carrier Merger Documentation (1979)

- Carrier Spinoff Prospectus (2020)

Regulatory & Policy Documents

- EU Green Deal Heat Pump Mandates

- U.S. Inflation Reduction Act Heat Pump Incentives

- German Building Energy Act (2024)

- Montreal Protocol Refrigerant Phase-out Timeline

Academic & Technical Resources

- "The History of Air Conditioning" - American Society of Mechanical Engineers

- Heat Pump Technology Roadmap - International Energy Agency

- Building Decarbonization Studies - Lawrence Berkeley National Laboratory

- Refrigerant Transition Technical Papers - ASHRAE

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube