Waste Connections: Building the Third-Largest Waste Empire

I. Introduction & Episode Roadmap

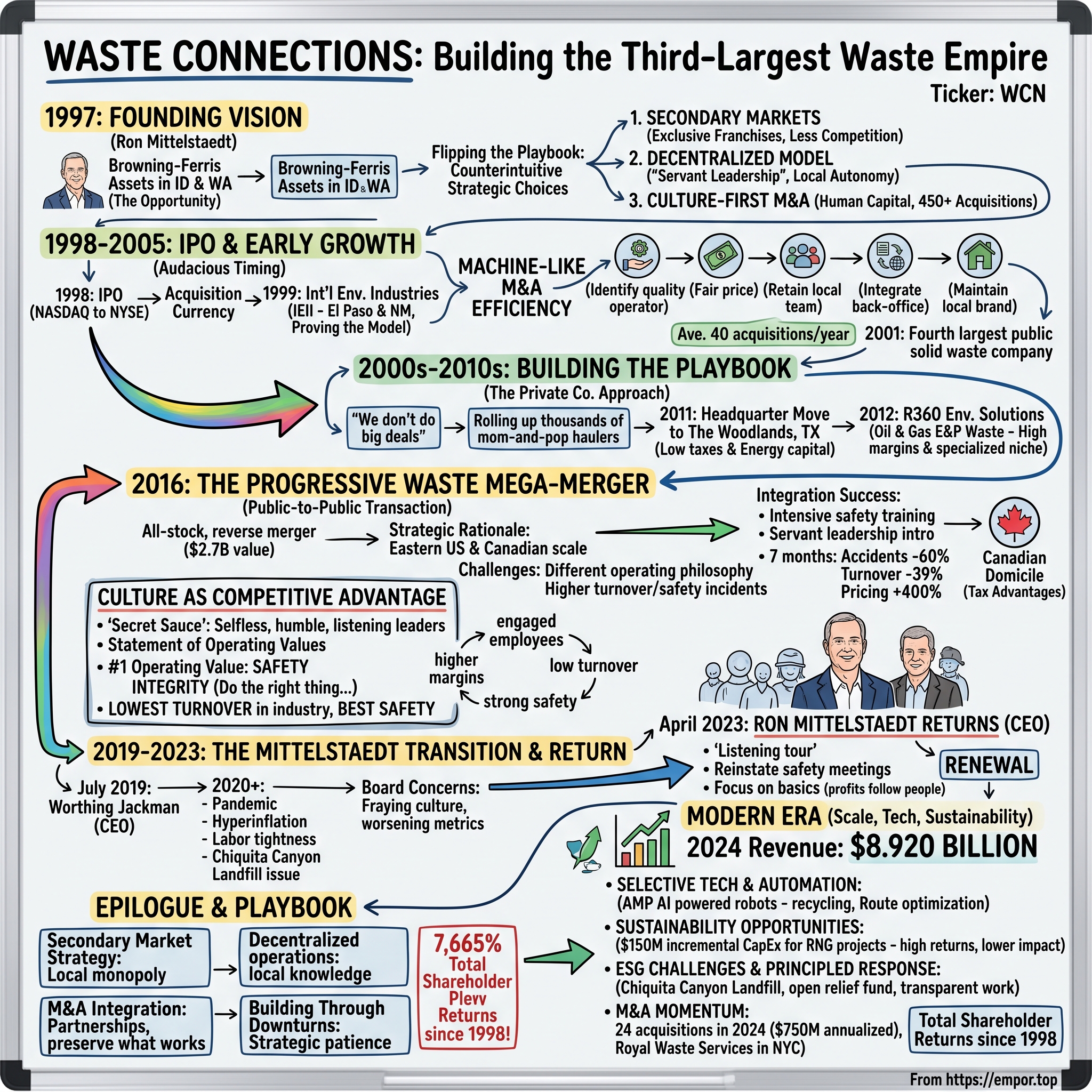

Picture this: It's 1997, and a young executive named Ron Mittelstaedt is sitting in a conference room, having just learned that Browning-Ferris Industries—one of the waste management giants where he cut his teeth—is divesting assets in Idaho and Washington. Most would see a fire sale. Mittelstaedt saw the foundation of an empire.

Twenty-seven years later, that opportunistic bid has morphed into Waste Connections, generating revenue of $8.920 billion in 2024 with expectations for 2025 financial outlook including revenue from $9.45 billion to $9.60 billion and adjusted EBITDA of $3.12 billion to $3.2 billion. It is the third largest waste management company in North America, trailing only industry behemoths Waste Management and Republic Services.

But here's what makes this story fascinating: While its larger rivals built their empires through brute-force consolidation in major metropolitan markets, Waste Connections took the road less traveled. The company is "known for being the most profitable company in the industry by far" and "the fastest-growing company in the industry by far". How did a startup founded in 1997 become a $9+ billion waste empire through 450+ acquisitions?

The answer lies in three counterintuitive strategic choices that would define the company: a laser focus on secondary markets where they could secure exclusive franchises rather than compete head-to-head with the giants, a radically decentralized operating model built on "servant leadership" rather than command-and-control hierarchies, and a culture-first approach to M&A that prioritized human capital over financial engineering.

This is the story of how Waste Connections built the third-largest waste empire in North America—not by following the playbook, but by rewriting it entirely. We'll explore the founding vision, the rapid-fire IPO, the relentless acquisition machine, the transformative Progressive Waste merger, and the cultural secret sauce that makes it all work. Along the way, we'll unpack the business lessons that matter for investors: why boring businesses with network effects can be extraordinary investments, how culture can be a sustainable competitive advantage, and what it really takes to successfully integrate 450+ acquisitions.

II. The Founding Story & Ron Mittelstaedt's Vision

Ron Mittelstaedt's path to waste management royalty began, improbably, in the air freight business. A graduate of the University of California at Santa Barbara, where he earned a bachelor of science degree in economics at the age of 20, Mittelstaedt joined the transportation industry after completing his studies. He spent roughly three years working for Airborne Express in New York City, before being selected to manage the company's operations in San Francisco.

The San Francisco move would prove pivotal. It was there that Mittelstaedt first encountered the waste disposal industry—not as an employee, but as an observer of an industry ripe for disruption. The waste business in the late 1980s was dominated by a handful of giants engaged in a land-grab strategy, prioritizing scale over profitability, market share over margins.

In 1988, at age 26, Mittelstaedt made the leap. He joined Browning-Ferris Industries, one of the industry titans, starting as a sales manager charged with overseeing the company's commercial and industrial selling activity in the Sacramento Valley. Within two years, he earned a promotion to general manager of the Sacramento area operations. He later served as Division Vice President of Northern California, overseeing the San Jose market, and as District Manager of BFI's operations in Sacramento and surrounding areas.

Working inside Browning-Ferris was like getting a PhD in how the waste industry operated—and more importantly, how it didn't. Mittelstaedt watched as the company pursued growth at any cost, engaging in bruising competition in major markets where multiple haulers fought over the same customers. Margins were compressed, service suffered, and the human element was often forgotten in the pursuit of tonnage and market share.

After Browning-Ferris, Mittelstaedt's career took him through other industry giants. As Regional Vice President of USA Waste Services, Inc. from November 1993 to January 1997, he was responsible for all operations in 16 states and Canada. He then served as a Consultant and Executive Vice President of United Waste Systems, Inc. from January 1997 to August 1997, where he was responsible for corporate development for all states west of Colorado.

Each stop reinforced the same lesson: The industry's conventional wisdom was broken. The biggest players were so focused on conquering major metropolitan markets that they ignored thousands of smaller communities. They were so obsessed with centralized control that local managers had no autonomy. They were so fixated on financial metrics that they forgot their employees were human beings.

Then came July 1997. Mittelstaedt heard that Browning-Ferris had decided to sell its operations in Idaho and Washington to raise capital. He heard about the proposed divestiture in July 1997 and quickly decided that he wanted to buy the properties. He submitted a bid in August and assembled a management team to lead the company that would control the Browning-Ferris assets. Mittelstaedt solicited the help of former colleagues at Browning Ferris, as well as several executives who worked for USA Waste Services.

The founding team was small but experienced: James Cutler, Brad Bishop, Frank Cutler and Ron Mittelstaedt. Mittelstaedt turned to the task of raising the money needed to make his company a viable corporate entity. He raised $8.5 million in private capital from his business contacts and invested his own money into the concern, ranking as the largest single investor.

By September 30, 1997, Waste Connections was officially born. But this wasn't just another waste company. From day one, Mittelstaedt articulated a radically different vision—one that would flip the industry's conventional playbook on its head.

First, instead of fighting over Los Angeles or New York, Waste Connections would target secondary and tertiary markets—places like Yakima, Washington, or Midland, Texas. These markets were too small for the giants to care about but large enough to support a profitable business, especially if you could secure exclusive franchise agreements.

Second, instead of managing everything from corporate headquarters, Waste Connections would push decision-making down to local managers. Mittelstaedt believed that "culture is the great differentiator amongst companies in all businesses" and focused on foundational pillars including the belief that culture "gives us a common language within the company".

Third, and perhaps most radically, the company would put culture first. Not as a nice-to-have, but as the core competitive advantage. This wasn't feel-good corporate speak—it was a calculated strategy based on a simple insight: in a local service business, the quality of your people determines the quality of your service, and the quality of your service determines your ability to maintain pricing power and exclusive contracts.

Not long after its formation, Waste Connections earned the reputation as a fast-growing company destined for national prominence, a fitting description for a company founded by a young, fast-rising executive headed for national recognition himself. Within just six months of founding, the results were already impressive. The company had successfully integrated a number of waste disposal firms across five states. Through nine collections operations, three transfer stations, one landfill, and one recycling facility, the company served approximately 140,000 commercial, industrial, and residential customers.

The post-Browning-Ferris vision was taking shape: learning from the giants, but doing everything differently. Where they zigged, Waste Connections would zag. And the market was about to take notice.

III. The IPO & Early Growth Strategy (1998–2005)

Speed was the name of the game. While most companies spend years preparing for an IPO, Waste Connections sprinted to the public markets with the urgency of a startup that knew its window of opportunity wouldn't stay open forever. Within about a year of its founding the company decided to go public, launching its IPO in May 1998. Waste Connections went public not long after its founding, trading on the NASDAQ from May 23, 1998, until 2003, when the company moved over to the New York Stock Exchange (NYSE).

The timing was audacious. Less than eight months old, with barely $8.5 million in initial capital, Waste Connections was asking public market investors to bet on a vision that contradicted everything Wall Street thought it knew about the waste industry. The conventional wisdom said you needed scale in major markets. Mittelstaedt was building a company focused on places most investors couldn't find on a map.

But the IPO proceeds gave Waste Connections something crucial: acquisition currency. And Mittelstaedt was about to deploy it with machine-like efficiency.

In October 1998, the company signed a definitive merger agreement with four waste collection companies in Washington. The companies--Murrey's Disposal Company, Inc.; American Disposal Company, Inc.; D.M. Disposal Co.; and Tacoma Recycling Company, Inc.--were collectively known as The Murrey Companies. This wasn't just an acquisition—it was a statement of intent. The Murrey Companies brought critical mass in Washington State and validated Waste Connections' thesis that quality regional operators were eager for a liquidity event.

Then came the move that would transform Waste Connections from a Pacific Northwest regional player into a force to be reckoned with. In August 1999, the company purchased International Environmental Industries Inc. (IEII), an operator of four landfills and three collection operations in markets surrounding El Paso and southern New Mexico. Waste Connections' net income, a measure of how successfully the company integrated its new assets, soared, jumping from $9.2 million in 1999 to $28.2 million.

The IEII acquisition wasn't just about the numbers—it was about proving the model could work outside the company's backyard. El Paso and southern New Mexico were classic Waste Connections markets: secondary cities where the company could establish dominant positions without engaging in brutal price wars with Waste Management or Republic Services.

The market loved what it saw. In 2000, Waste Connections' stock ranked as the top performer in the environmental sector, appreciating 129 percent. Although Waste Connections' pace of expansion slowed in 2000, the vitality of the company intensified decidedly.

What made Waste Connections' early acquisition strategy so distinctive wasn't just what they bought, but how they bought it. While competitors focused on large, public company transactions that grabbed headlines, Waste Connections was quietly rolling up the thousands of mom-and-pop haulers that dotted the American landscape. These weren't sexy deals that would make the front page of the Wall Street Journal, but they were incredibly strategic.

Consider the math: A small hauler in a secondary market might have exclusive franchise agreements with local municipalities, own a permitted landfill (increasingly difficult to replicate due to environmental regulations), and generate $5-10 million in revenue. Waste Connections could acquire these businesses at 5-6x EBITDA, implement basic operational improvements, achieve cost synergies through route density, and suddenly that same business would be worth 8-10x EBITDA as part of a larger platform.

The secondary market thesis was elegant in its simplicity. Major markets like Los Angeles or Chicago had multiple large haulers competing aggressively on price. But in a place like Bend, Oregon, or Casper, Wyoming, Waste Connections could often become the only game in town through exclusive municipal contracts. These contracts typically ran 5-10 years and included automatic price escalators tied to inflation. It was like owning a mini-monopoly with built-in pricing power.

Waste Connections adopted a pace of expansion that averaged nearly 40 acquisitions a year during its first four years of business. Each acquisition followed a similar playbook: identify a quality operator in a secondary market, pay a fair price that allowed the seller to feel good about the transaction, retain local management and employees who knew the market, integrate back-office functions to achieve cost savings, and maintain the local brand and relationships that made the business successful in the first place.

By 2001, the results spoke for themselves. Between the company's IPO and August 2001, roughly 135 private businesses were acquired, giving Waste Connections a customer base of nearly 800,000. Four years after its creation, the company ranked as the fourth largest, publicly-owned solid waste company in the United States, larger than the four companies ranking fifth through eighth combined.

The company's footprint had expanded dramatically from its Pacific Northwest roots. Operations now stretched from California to Texas, from Montana to New Mexico. But unlike its larger competitors who managed these far-flung operations from centralized headquarters, Waste Connections maintained its decentralized model. Local managers had real authority to make decisions, set pricing, and manage customer relationships. Corporate headquarters in Folsom, California, remained lean, focusing on capital allocation, acquisition integration, and maintaining the culture.

According to the company's calculations, there were approximately 2,000 private solid waste companies located west of the Mississippi. Mittelstaedt and his team estimated there were roughly 450 companies suitable for inclusion within Waste Connections' operations. The years ahead promised to see the acquisition and integration of these companies into one of the industry's powerhouses.

The path was clear: while the giants battled over market share in major metros, Waste Connections would methodically consolidate the thousands of smaller markets they ignored. It was a strategy that required patience, discipline, and exceptional execution. But for investors who understood the power of compounding and network effects, it was becoming clear that Waste Connections was building something special—one small acquisition at a time.

IV. Building Through Acquisitions: The Private Company Playbook (2000s–2010s)

"We don't do big deals," Ron Mittelstaedt would tell anyone who asked about Waste Connections' M&A strategy. It was a curious statement from the CEO of a company that had completed hundreds of acquisitions. But it captured something essential about how Waste Connections thought about growth. The company has "grown through acquisitions, mostly of private companies, over the last 19-plus years. We've done 450 to 470 private company acquisitions. We've only done one public-to-public transaction ever".

This wasn't just a preference—it was a philosophy rooted in deep understanding of what makes acquisitions succeed or fail. Public company deals are complex, heavily negotiated affairs with investment bankers, lawyers, and publicity. Private company acquisitions, especially in the waste industry, are intensely personal transactions where the seller is often handing over a business they've built over decades.

The Waste Connections approach to these private deals was unlike anything else in the industry. Where others sent in corporate development teams with spreadsheets and term sheets, Waste Connections sent operators who spoke the language of the business. The conversation wasn't about EBITDA multiples and working capital adjustments—it was about taking care of employees, maintaining relationships with customers, and preserving the seller's legacy in the community.

The move to Texas in 2011 marked a pivotal moment in this acquisition-driven strategy. In December 2011, the company announced that it was moving its headquarters from Folsom, CA to The Woodlands, Texas, a suburb of Houston. Chief Executive Officer, Ron Mittelstaedt, cited California's high taxes and dysfunctional legislature as key reasons for the move.

But the Texas relocation was about more than just taxes. Houston was the energy capital of America, and Waste Connections saw an opportunity that others missed. In September 2012, it acquired R360 Environmental Solutions, a Texas waste company specializing in the oil industry. This wasn't traditional municipal solid waste—it was exploration and production (E&P) waste from oil and gas drilling, a specialized niche with higher margins and significant growth potential as fracking technology unlocked new energy reserves across Texas, North Dakota, and other states.

The R360 acquisition exemplified the evolution of Waste Connections' strategy. They weren't just consolidating traditional waste markets anymore; they were identifying adjacent opportunities where their operational expertise and acquisition capabilities could create value. E&P waste required different equipment, different disposal methods, and different customer relationships. But the fundamental business model—providing essential services with high barriers to entry—remained the same.

Throughout the 2000s and early 2010s, Waste Connections refined its acquisition machine to near-perfection. The company developed a systematic approach to identifying, evaluating, and integrating targets. They maintained relationships with hundreds of potential sellers, sometimes for years, waiting for the right moment when the owner was ready to sell. They had learned that forcing a timeline rarely worked—better to be patient and let the seller come to them.

The integration process was equally sophisticated. Within days of closing, Waste Connections would deploy an integration team—not to slash costs and fire employees, but to understand what made the acquired company successful and preserve those elements while adding value where possible. Back-office functions like accounting, billing, and regulatory compliance would be centralized to achieve economies of scale. Safety programs would be immediately upgraded to Waste Connections' standards. But customer-facing operations remained local.

The numbers told the story of this disciplined approach. Between 2005 and 2015, Waste Connections completed over 200 acquisitions, adding billions in revenue. But more importantly, they maintained industry-leading margins and returns on invested capital. While competitors struggled with integration challenges and cultural clashes from their mega-mergers, Waste Connections quietly compounded value through its steady stream of tuck-in acquisitions.

One of the most underappreciated aspects of this strategy was its capital efficiency. Large public company deals often required significant leverage, integration costs, and management distraction. Waste Connections' smaller deals could be funded from free cash flow, integrated by regional teams who had done it dozens of times before, and immediately accretive to earnings. It was a virtuous cycle: strong operations generated cash flow, cash flow funded acquisitions, acquisitions increased density and margins, which generated more cash flow.

The culture-first approach to M&A integration set Waste Connections apart. Where other acquirers imposed their systems and processes from day one, Waste Connections took time to understand what worked in each local market. They recognized that the truck driver who had been running the same route for 15 years knew more about those customers than any corporate executive ever would. The office manager who had been handling billing for two decades had relationships that couldn't be replicated.

This respect for local knowledge and relationships paid dividends in employee retention. While the industry averaged 30-40% driver turnover, acquired companies that joined Waste Connections often saw turnover rates drop significantly after the acquisition. Drivers appreciated the better equipment, improved safety programs, and enhanced benefits. But more than that, they appreciated being treated with respect by a company that valued their contribution.

By 2015, Waste Connections had built an acquisition machine unlike anything else in the industry. They weren't doing the biggest deals or making the biggest headlines. But they were methodically consolidating an industry one small market at a time, creating enormous value for shareholders while maintaining the entrepreneurial spirit that made them successful in the first place. The stage was set for their biggest move yet—one that would test everything they had learned about acquisitions, integration, and culture.

V. The Progressive Waste Mega-Merger (2016)

On January 19, 2016, the waste industry woke up to shocking news. Waste Connections and Progressive Waste Solutions—the third and fourth largest players in North America—were merging in an all-stock transaction. The all-stock, reverse merger transaction provides an implied exchange ratio of 0.4815 of a share of Waste Connections stock for each share of Progressive Waste stock. Based on Friday's closing price of $24.55 per share, that puts the deal's value at about $2.7 billion.

This wasn't just another acquisition. This was Waste Connections departing from its carefully cultivated playbook of small, private company deals to swallow a public company nearly its own size. Progressive Waste brought significant operations in Eastern Canada and the eastern United States—markets where Waste Connections had limited presence. The strategic logic was compelling, but the execution risk was enormous.

When the deal is completed Waste Connections shareholders will own about 70 percent of the combined company, and Progressive Waste shareholders will own about 30 percent. But the real story wasn't in the ownership percentages—it was in the structure. This was engineered as a reverse merger with a Canadian domicile, a clever bit of financial engineering that would reduce the combined company's tax rate while maintaining operational headquarters in Texas.

The numbers were staggering. The merged company has a pro-forma revenue of $4.1 billion USD. The newly combined company will have 273 collection operations, 132 transfer stations, 93 landfills, 71 recycling facilities, 24 saltwater disposal wells, and 20 exploration and production treatment facilities. Overnight, Waste Connections would nearly double in size, cementing its position as a clear number three in the industry behind Waste Management and Republic Services.

But Ron Mittelstaedt knew that size alone meant nothing if they couldn't maintain their culture and operational excellence. In announcing the deal, he said "We are extremely excited to welcome Progressive Waste into the Waste Connections family and believe the combination will be quite compelling to our collective employees, shareholders and other stakeholders. Under our leadership, we believe we can instill the corporate culture, safety focus, operational excellence and accountability that have served us so well and which we believe are necessary for long-term success within Progressive Waste's complementary markets".

The Progressive Waste integration would be the ultimate test of Waste Connections' vaunted culture. Progressive was a roll-up itself, assembled from numerous acquisitions across Canada and the eastern United States. It had a different operating philosophy, more centralized management, and critically, significantly higher employee turnover and safety incident rates than Waste Connections.

The integration began immediately after the June 1, 2016 closing. But instead of the typical post-merger playbook of immediate cost cuts and layoffs, Waste Connections took a different approach. They started with safety and culture. Every Progressive Waste location received intensive safety training. Waste Connections' servant leadership philosophy was introduced not as a corporate mandate but as an invitation to a different way of operating.

The financial engineering of the deal was masterful. The new company began trading on both the Toronto Stock Exchange and New York Stock Exchange under the symbol "WCN", but the Canadian domicile provided significant tax advantages. The combined company's effective tax rate dropped from the high 30s to the mid-20s, freeing up hundreds of millions in cash flow for reinvestment and shareholder returns.

But the real story of the Progressive merger wasn't financial—it was operational. Within seven months of the acquisition, accidents were down 60 percent, turnover was down 39 percent and customers' annual price invested has improved almost 400 percent. "Those are pretty significant changes on a $2 billion revenue company in a seven-and-a-half month period".

The transformation of Progressive's operations validated everything Waste Connections believed about the power of culture. When you treat drivers with respect, give them modern equipment, invest in their safety, and empower local managers to make decisions, magical things happen. Routes become more efficient. Customer service improves. Safety incidents decline. Employees stop looking for other jobs.

The Progressive merger also brought Waste Connections something it had been lacking: scale in Eastern markets and a significant presence in Canada. Progressive reported owning or operating 121 collection operations, 66 transfer stations, 30 landfills and 40 MRFs in the eastern U.S. and six Canadian provinces. These assets complemented Waste Connections' western U.S. focus perfectly, creating a truly North American footprint.

Integration challenges certainly existed. Some Progressive managers, accustomed to centralized decision-making, struggled with the autonomy Waste Connections provided. Some markets required significant capital investment to bring facilities up to Waste Connections' standards. And melding two public companies' systems and processes was far more complex than integrating a small private hauler.

But by any measure, the Progressive merger was a stunning success. Within 18 months, the combined company was generating margins that exceeded either predecessor company's standalone performance. Employee turnover and safety metrics continued to improve. And perhaps most importantly, Waste Connections proved it could execute a transformational deal without losing its cultural soul.

The Progressive merger marked Waste Connections' evolution from a successful regional consolidator to a true industry powerhouse. They had proven they could play the big-deal game when the opportunity was right, while maintaining the operational excellence and cultural values that made them special. It was a masterclass in M&A execution that would set the stage for the next phase of growth.

VI. Culture as Competitive Advantage

Walk into any Waste Connections facility, from a transfer station in rural Montana to corporate headquarters in Texas, and you'll likely hear the same phrase: "servant leadership." It's not a buzzword or a management fad. As one employee explains, "Servant Leadership is not a program, or a training class or a motto. It is at the core of how we operate and, frankly, it's our 'secret sauce'. Leaders who are selfless, humble, who listen to and care for their employees and who get results through empowering others are the leaders that succeed at Waste Connections. And those leaders and their employees are what have allowed Waste Connections to succeed".

In an industry often characterized by blue-collar grit and command-and-control management, Waste Connections' servant leadership philosophy seems almost radical. But the numbers suggest it's anything but soft. The company is "known for having the lowest turnover in the industry, and...the best safety in the industry". In an industry where driver turnover routinely exceeds 30% annually, Waste Connections consistently maintains rates below 15%.

The company's Statement of Operating Values isn't just corporate wallpaper. It's a living document that drives daily decisions. Safety is the #1 Operating Value, with the company believing that "the development of our managers and supervisors into Servant Leaders and our ability to instill this commitment-based, safety-driven culture across our broader employee base" drives success.

The integrity principle is particularly revealing of how the company thinks. As leadership explains it: What they define as integrity is "to do the right thing at the right time for the right reason and, when in doubt, do them in that order. We want people to know that if the right thing is not the best thing for the company, do the right thing, and we will deal with the consequences".

This might sound like corporate idealism, but it translates into hard business results. When drivers feel respected and empowered, they take better care of equipment, reducing maintenance costs. When local managers have real decision-making authority, they respond faster to customer needs, improving retention. When safety truly is the top priority, insurance costs decline and productivity improves.

The decentralized operations model is inextricably linked to this cultural philosophy. The company operates under "a decentralized, servant leadership-based culture" where "local leaders...have the responsibility to make operating decisions" in "what we would argue, is truly a local business". This isn't delegation by necessity—it's empowerment by design.

Consider how this plays out in practice. A district manager in Odessa, Texas doesn't need to call headquarters to approve a new route, adjust pricing for a longtime customer facing hardship, or invest in equipment that will improve safety. They have the authority and the responsibility to make those calls. Corporate provides support, resources, and accountability, but not micromanagement.

The company reinforces this culture through systematic programs. They offer servant-leadership classes where "we like the dialogue you get when everyone is in the classroom" and "servant-leadership surveys to hold our leaders accountable" because "it's good for our front-line employees to know that we are listening".

But perhaps the most powerful cultural reinforcement comes from the top. Ron Mittelstaedt doesn't just preach servant leadership—he lives it. Stories abound of the CEO visiting drivers at 4 AM to understand their challenges, spending days at transfer stations learning operations from the ground up, and personally calling employees who've achieved safety milestones.

This cultural advantage becomes particularly powerful in M&A integration. When Waste Connections acquires a company, they don't send in consultants to cut costs. They send in operators who've lived the servant leadership philosophy. As Mittelstaedt explains about acquired companies: "Employee turnover is higher in acquired companies, often reaching 30-35% initially due to our rigorous safety standards. However, our core company turnover is much lower, indicating strong retention overall".

The safety transformation at acquired companies is particularly striking. Progressive Waste's Canadian operations provide a compelling example. After the acquisition, "Its safety program is focused on extreme and personal one-on-one engagement with the result that total incident rates went from a high of 53.8 in 2016 down to 6.2 through May 2021". That's not incremental improvement—that's transformation.

The cultural philosophy extends beyond employees to community engagement. The company runs programs like an annual Christmas bike-building drive where "employees, families and friends assemble thousands of bicycles for local charities, first responders and military bases" with "an estimated 50,000 bikes" donated to date, and a charity golf event that "raises more than $1,000,000 each year for charities supporting at-risk youth".

What makes Waste Connections' culture truly remarkable is its durability at scale. Many companies lose their cultural edge as they grow. Waste Connections has managed to maintain and even strengthen its culture while growing from a startup to a $9 billion enterprise. As they note in their annual report: "We're sticking to a model that has served us well for over 27 years".

The financial markets have taken notice. Waste Connections' overall culture is rated A+ based on ratings from employees. More importantly, this cultural excellence translates directly to financial performance. Companies with engaged employees, low turnover, and strong safety records generate higher margins, better returns on capital, and more sustainable growth.

In an industry where the service is commoditized and the technology is mature, culture becomes the ultimate differentiator. Waste Connections has proven that in the unglamorous business of hauling trash, how you treat people matters as much as how efficiently you run routes. It's a lesson that extends far beyond the waste industry: in any people-intensive business, culture isn't just a nice-to-have—it's the foundation of sustainable competitive advantage.

VII. The Mittelstaedt Transition and Return (2019–2023)

The announcement in July 2019 sent shockwaves through the waste industry: Ron Mittelstaedt, the founder and driving force behind Waste Connections for 22 years, was stepping back from the CEO role. Mittelstaedt transitioned to the position of Executive Chairman of the Board of Directors, having served as the Company's Chief Executive Officer from 1997 until July 2019.

His successor seemed like a natural choice. Worthing Jackman had been with the company since acting as its investment banker during the 1997 founding. He officially joined Waste Connections in 2003, became CFO in 2004, and was promoted to president in 2018. Jackman knew the business inside and out, had been instrumental in executing the company's M&A strategy, and had Mittelstaedt's full endorsement.

The timing of the transition seemed optimal. Waste Connections was firing on all cylinders, having successfully integrated Progressive Waste and continuing its acquisition momentum. The company had clear strategic direction, strong market positions, and a deep bench of operational talent. As Jackman said during his first earnings call as CEO-designate: "I wouldn't say anyone's skipping a beat. I think you see it's a testament to the organization that [Ron] has put together that you've seen the results that we're printing right now".

For a while, the transition appeared seamless. The company continued executing its playbook, completing acquisitions, expanding margins, and generating strong cash flow. Jackman brought his own strengths to the role, particularly in capital markets and financial strategy. The stock price continued its upward trajectory, and investors seemed comfortable with the leadership change.

But then came 2020, and with it, challenges no one could have anticipated. The COVID-19 pandemic disrupted every aspect of the waste business. Commercial collection volumes plummeted as businesses closed. Residential volumes spiked as people stayed home. Labor markets tightened dramatically as stimulus payments and enhanced unemployment benefits made it harder to recruit and retain drivers. Supply chains fractured, making it difficult to obtain trucks and equipment.

Jackman and his team navigated these unprecedented challenges competently. The company maintained profitability, protected employees, and continued serving customers through the worst of the pandemic. But as the months wore on, cracks began to appear. Employee turnover, which had been industry-leading low, began to creep higher. Safety metrics, while still strong, showed signs of deterioration. The company's cultural edge—that intangible servant leadership magic that Mittelstaedt had cultivated—seemed to be fraying at the edges.

The challenges weren't entirely pandemic-related. Inflation surged to 40-year highs, driving up costs for fuel, labor, and equipment. Competition for drivers intensified as e-commerce growth created alternative employment opportunities. Environmental regulations tightened, requiring costly investments in cleaner trucks and enhanced landfill monitoring. The Chiquita Canyon landfill in California developed operational issues that would eventually require early closure and hundreds of millions in remediation costs.

Through it all, Jackman maintained a steady hand, delivering solid if unspectacular results. But for a company accustomed to industry-leading performance, solid wasn't enough. Behind the scenes, the board of directors was growing concerned. The company's cultural metrics—employee engagement scores, turnover rates, safety statistics—were all trending in the wrong direction. The acquisition pipeline, while still active, lacked the momentum of earlier years.

Then, on April 23, 2023, came another shocking announcement. Ronald J. Mittelstaedt, the Executive Chairman of the Company, has been appointed President and Chief Executive Officer of the Company, effective April 23, 2023. Mr. Mittelstaedt succeeds Worthing F. Jackman in this role.

The carefully worded press release couldn't hide the reality: this was not a planned succession. Mittelstaedt's statement was gracious but pointed: "We thank Worthing for his work and dedication on behalf of Waste Connections for the last 19 years, including the last four as CEO. These last four years, with the pandemic and hyperinflation, have been challenging for leadership in all industries, and Worthing has done a yeoman's job in leading us through this period. We are grateful for all that Worthing has done for the company, its stakeholders and the communities that we serve. His extensive efforts have helped shape the company we are today, and we all wish him well in his future endeavors".

Mittelstaedt's return was more than just a leadership change—it was a statement that Waste Connections was returning to its roots. In his first comments as returning CEO, Mittelstaedt was clear about priorities: "I'm excited to return to this role to serve our 23,000 employees and focus our efforts on servant leadership, our decentralized operating structure and delivering exceptional results in all areas".

The impact was almost immediate. Mittelstaedt embarked on a listening tour, visiting operations across the company's footprint. He reinstated regular safety meetings, reinvigorated the servant leadership training programs, and refocused on the basics that had made Waste Connections successful. The message was clear: profits follow people, not the other way around.

As the company noted in its 2023 annual report: "2023 was a year of renewal for Waste Connections, with a return to our leadership roots to reinforce our commitment to a decentralized operating model supported by a servant leadership-driven culture. Along with the addition of a geographic segment to accommodate our outsized growth from recent years, we modified certain leadership roles and responsibilities to more closely align, reposition and reinvigorate our team and 'double down' on our commitment to human capital. We've gotten back to the basics that are fundamental to implementing the differentiated strategy that has driven our exemplary track record of value creation for 26 years".

The results of Mittelstaedt's return spoke volumes. By Q4 2024, employee turnover had reached "multi-year lows" and the company was "delivering on our commitments and once again driving industry-leading results". The acquisition machine roared back to life. Safety metrics improved dramatically. The servant leadership culture that had seemed to be slipping away was suddenly vibrant again.

The Mittelstaedt transition and return offers profound lessons about leadership, culture, and the difficulty of succession in founder-led companies. Even the most capable successor can struggle to maintain the ineffable qualities that make a culture special. Sometimes, returning to the source—bringing back the founder who embodies the values and vision—is necessary to reset and refocus. For Waste Connections, Mittelstaedt's return wasn't a step backward; it was a reaffirmation of what made them exceptional in the first place.

VIII. Modern Era: Scale, Technology & Sustainability (2020s–Today)

The Waste Connections of 2024 operates at a scale Ron Mittelstaedt could barely have imagined when he founded the company in 1997. Full year 2024 revenue reached $8.920 billion, the company serves approximately nine million customers across 46 states and six Canadian provinces, and employs nearly 24,000 people. But what's remarkable isn't the size—it's that the company has maintained its entrepreneurial edge and cultural distinctiveness while becoming an industry giant.

The modern era has been defined by record acquisition activity that makes even Waste Connections' historically aggressive pace look modest. The company completed 24 acquisitions in 2024 and 13 in 2023. The 2024 acquisitions added $750 million in annualized revenues to Waste Connections. This isn't desperation or growth for growth's sake—it's opportunistic execution of the same playbook that's worked for nearly three decades.

The crown jewel of recent acquisitions was Royal Waste Services in New York City. The Royal Waste Services acquisition entrenches Waste Connections as one of the largest commercial waste companies in New York City. This marked a strategic evolution—Waste Connections was no longer avoiding major metros entirely but entering them selectively when they could establish strong positions without engaging in irrational competition.

But the most intriguing development in the modern era isn't about traditional waste—it's about technology and sustainability. Waste Connections is partnered with AMP to use AMP's AI powered robots which facilitate recycling. Waste Connections recycled 2.21 million tons in 2023, and is planning to expand capacity by contracting AMP to build and operate an entirely new MRF in Commerce City, Colorado.

The AMP partnership represents a fascinating evolution in how Waste Connections thinks about technology. They're not trying to become a tech company or chase the latest fad. Instead, they're selectively adopting technologies that enhance their core operations. AI-powered sorting robots improve recycling economics, making previously marginal facilities profitable. Route optimization software reduces fuel costs and improves customer service. Automated truck technology enhances safety without replacing drivers.

The renewable natural gas (RNG) opportunity at landfills has become a significant value driver. When organic waste decomposes in landfills, it produces methane—a potent greenhouse gas. Waste Connections captures this gas and converts it into pipeline-quality renewable natural gas that can power vehicles or heat homes. The company is investing an incremental $150 million in capital expenditures in 2024 for renewable natural gas projects. These projects generate attractive returns while reducing environmental impact—a win-win that appeals to both investors and regulators.

The company has also navigated significant ESG challenges, particularly the Chiquita Canyon landfill situation in California. In March 2024, Waste Connections opened a relief fund to residents to pay to mitigate noxious fumes that leaked from their Chiquita Canyon Landfill. The company states that at least $25 million will be available through the fund, and that they distributed air purifiers to the residents. The closure resulted in a $116.1 million write-down and $480.8 million in closure and post-closure liabilities.

The Chiquita Canyon situation could have been a corporate disaster—environmental liability, regulatory scrutiny, community outrage. But Waste Connections' response demonstrated the power of their values-based approach. They didn't deny, deflect, or delay. They acknowledged the problem, committed resources to fix it, and worked transparently with regulators and the community. It was expensive and painful, but it preserved trust and demonstrated that their integrity principle wasn't just words on paper.

Financial performance in the modern era has been exceptional, even by Waste Connections' high standards. Full year 2024 adjusted EBITDA reached $2.902 billion, up 15% year-over-year, with a margin of 32.5%. These are industry-leading margins, well above larger competitors despite Waste Connections' focus on secondary markets that theoretically should be less efficient.

The company's Q4 2024 results and 2025 outlook demonstrate continued momentum. As Mittelstaedt noted: "Q4 provided a solid finish to a year of extraordinary accomplishments for Waste Connections both financially, with double-digit growth in both revenue and adjusted EBITDA, and operationally, with accelerating improvements in employee engagement and retention". The company highlighted that "Our differentiated results in 2024 include 100 basis points adjusted EBITDA margin expansion for industry-leading margin of 32.5% led by 7% solid waste core price complemented by outsized acquisition contribution".

Looking forward, the company is positioning for the $10 billion revenue milestone. The 2025 outlook projects revenue of $9.45 billion to $9.60 billion, putting the company within striking distance of this psychological barrier. But management is careful to emphasize that scale isn't the goal—it's the byproduct of executing their strategy.

The modern era has also seen continued refinement of the company's capital allocation strategy. With year-end leverage of less than 2.7 times, the strength of the balance sheet provides "tremendous optionality to fund outsized acquisition activity and invest in sustainability-related projects, along with an increasing return of capital to shareholders". This financial flexibility is crucial—it allows Waste Connections to be opportunistic on acquisitions without overleveraging, invest in long-term projects like RNG without sacrificing near-term results, and return excess capital to shareholders through dividends and buybacks.

Perhaps most importantly, the modern era has validated that Waste Connections' model is not only sustainable but increasingly relevant. As environmental regulations tighten, their operational excellence becomes more valuable. As labor markets remain tight, their culture-first approach to employee retention becomes a bigger competitive advantage. As technology evolves, their selective adoption strategy allows them to benefit without betting the company on unproven concepts.

The company's 2024 achievements were particularly noteworthy: "Most importantly, our continued focus on human capital resulted in multi-year lows for employee turnover, now down over one thousand basis points from 2022". In an industry where finding and keeping qualified drivers is the biggest operational challenge, this improvement in retention is worth hundreds of millions in reduced training costs, improved safety, and better customer service.

The modern Waste Connections is a paradox: a $9 billion company that operates like a collection of small businesses, a technology adopter that remains fundamentally people-focused, a consolidator that preserves entrepreneurial culture. They've proven that you can achieve massive scale without losing your soul, that you can be both profitable and principled, that sometimes the old ways—treating people with respect, keeping your promises, focusing on the long term—are actually the most innovative strategies of all.

IX. Playbook: Business & Investing Lessons

After nearly three decades of building Waste Connections from a startup to a $9 billion enterprise, what are the enduring lessons for operators and investors? The playbook that emerges is both counterintuitive and remarkably consistent.

The Secondary Market Strategy: The Power of Being the Only Game in Town

Waste Connections' focus on secondary markets wasn't just about avoiding competition—it was about understanding the fundamental economics of the waste business. In a major metropolitan area, multiple haulers compete for the same commercial contracts, driving prices down to commodity levels. But in a secondary market with an exclusive municipal franchise, Waste Connections essentially operates a local monopoly with automatic price escalators.

Consider the math: A exclusive franchise in a city of 50,000 might generate $10 million in annual revenue with 35% EBITDA margins. The contract runs 7-10 years with CPI-based price increases. Customer churn is essentially zero. Capital requirements are modest—a few trucks, some containers. The return on invested capital can exceed 20%. Now multiply this by hundreds of similar markets across North America.

This strategy requires patience and discipline. You can't force your way into these markets—you have to wait for the right opportunity, build relationships with local officials, and prove you're a reliable long-term partner. But once established, these positions are nearly impregnable. A competitor would need to wait years for the contract to expire, then convince the municipality to switch from a proven operator. It rarely happens.

Decentralized vs. Centralized Operations: Trust but Verify

The decentralized model is harder to execute than most realize. It requires hiring managers you trust, giving them real authority, and accepting that some decisions won't be perfect. The temptation to centralize—especially as you scale—is enormous. Technology makes it easier than ever to monitor and control everything from headquarters.

But Waste Connections understood something profound: in a local service business, local knowledge matters more than corporate consistency. The manager in Boise knows her market, customers, and employees better than any executive in Texas ever could. Give her the tools, training, and accountability framework, then get out of the way.

This doesn't mean anarchy. Waste Connections maintains strict standards for safety, financial reporting, and customer service. But within those guardrails, local managers have remarkable autonomy. They can adjust pricing, modify routes, invest in equipment, and make hiring decisions without corporate approval. This speed and flexibility is a massive competitive advantage in a business where customer needs can change daily.

Culture as a Moat: The Compound Effect of Treating People Well

The servant leadership philosophy sounds soft, but it creates hard economic value. When driver turnover is 15% instead of 35%, you save millions in recruiting and training costs. When safety incidents decline 50%, insurance premiums drop and productivity increases. When employees are engaged, they take better care of equipment, provide better customer service, and generate more ideas for improvement.

But culture only works if it's authentic and consistent. You can't preach servant leadership then treat people as expendable. You can't claim safety is the top priority then pressure drivers to skip pre-trip inspections. As leadership notes, culture is defined by "who we hire, fire, and promote"—not by mission statements or training programs.

M&A Integration Excellence: The 450+ Deal Machine

Waste Connections' M&A success comes from treating acquisitions as partnerships, not conquests. They understand that selling a business—especially a family business built over generations—is intensely emotional. The seller wants to know their employees will be treated well, their customers served properly, their community relationships maintained.

The integration philosophy is "preserve what works, improve what doesn't." Keep the local brand if it has value. Retain the management team if they're effective. Maintain customer relationships that have been built over decades. But upgrade safety programs immediately. Centralize back-office functions for efficiency. Provide better benefits and career opportunities for employees.

This patient approach means integration takes longer and costs more initially. But it results in better employee retention, customer retention, and ultimately, returns on investment. Of the 450+ acquisitions Waste Connections has completed, virtually all remain part of the company today, contributing to its success.

Capital Allocation Discipline: The Power of Saying No

For all their acquisition activity, Waste Connections has been remarkably disciplined about what they won't do. They won't overpay for assets, even if it means losing deals to competitors. They won't enter markets where they can't establish strong positions. They won't pursue growth that sacrifices margins or returns.

This discipline extends to managing the balance sheet. Even after record acquisition spending, leverage remains below 2.7x, providing flexibility for future opportunities. They've avoided the trap that ensnared many competitors: overleveraging to fund acquisitions, then being forced to cut investment when markets turn.

Tax-Efficient Structures: The Canadian Domicile Advantage

The Progressive Waste merger's Canadian structure was financial engineering at its finest. By domiciling in Canada while maintaining U.S. operations, Waste Connections reduced its tax rate by roughly 10 percentage points. On $2.9 billion of EBITDA, that's nearly $300 million in annual tax savings—money that can be reinvested in growth or returned to shareholders.

But this wasn't just opportunistic tax avoidance. The Canadian operations provided geographic diversification, exposure to different commodity prices, and access to new markets. The structure made strategic sense beyond the tax benefits.

Building Through Downturns: Opportunistic Timing

Waste Connections' biggest opportunities have come during difficult periods. The 2008-2009 financial crisis, the 2014-2016 oil collapse, the 2020 pandemic—each created distress for smaller operators and opportunities for Waste Connections to acquire quality assets at reasonable prices.

This requires maintaining financial flexibility during good times—avoiding excessive leverage, generating strong free cash flow, maintaining access to capital markets. When others are forced sellers, Waste Connections can be a patient buyer. It's a simple strategy but difficult to execute—it requires resisting the pressure to overpay during frothy markets.

The playbook lessons converge on a central insight: in a mature, essential service industry, sustainable competitive advantage comes not from revolutionary technology or brilliant strategy, but from consistent execution of fundamentals. Treat people well. Keep your promises. Think long-term. Stay disciplined. The compound effect of doing these things well for decades creates extraordinary value. Waste Connections is living proof.

X. Analysis & Bear vs. Bull Case

As Waste Connections approaches $10 billion in revenue, investors face a classic dilemma: Is this a mature business approaching its limits, or a compound success story with years of growth ahead? The bull and bear cases are both compelling.

Bull Case: The Compound Machine Keeps Running

The bulls see Waste Connections as Warren Buffett's ideal business: simple, predictable, and possessing durable competitive advantages. Start with the industry-leading margins. At 32.5% EBITDA margins, Waste Connections significantly outperforms larger competitors Waste Management (~28%) and Republic Services (~29%). This isn't temporary—it's structural, driven by their focus on exclusive markets, superior employee retention, and decentralized operating model.

The M&A runway remains vast. Despite completing 450+ acquisitions, Waste Connections estimates thousands of private haulers remain in North America. The company has "a robust acquisition pipeline, with over $75 million in annualized revenue already closed or signed for 2025". As environmental regulations tighten and technology requirements increase, smaller operators will increasingly need to sell to larger platforms. Waste Connections is the natural buyer—they have the reputation, the capital, and most importantly, the culture that makes sellers comfortable.

The secondary market dominance is nearly unassailable. Once Waste Connections secures an exclusive franchise, it's extraordinarily difficult for competitors to dislodge them. These aren't commodity contracts won on price—they're long-term partnerships based on reliability and trust. The switching costs for municipalities are high, both financially and politically.

Free cash flow generation is exceptional and improving. 2024 adjusted free cash flow reached $1.218 billion, and management guides to over $1.3 billion in 2025. This cash funds acquisitions, growth investments, and shareholder returns without requiring leverage. It's a self-funding growth machine.

The cultural advantages are widening, not narrowing. With employee turnover at "multi-year lows" after dropping "over one thousand basis points from 2022", Waste Connections is pulling away from competitors struggling with driver shortages and retention. In a tight labor market, this advantage is worth hundreds of basis points of margin.

Technology and sustainability create new growth vectors. Renewable natural gas, AI-powered recycling, route optimization—these aren't science projects but real businesses generating attractive returns. As ESG considerations become more important, Waste Connections' operational excellence positions them to benefit from stricter environmental standards.

Bear Case: The Challenges Mount

The bears acknowledge Waste Connections' execution but worry about structural headwinds. Start with valuation. At roughly 25x forward earnings and 14x EBITDA, Waste Connections trades at a significant premium to peers. This premium assumes continued exceptional execution—any stumble could trigger multiple compression.

Integration risks are rising with the pace of acquisitions. Completing 24 acquisitions in 2024 worth $750 million in annualized revenue stretches even Waste Connections' proven integration capabilities. Each acquisition requires management attention, capital investment, and cultural alignment. The law of large numbers suggests some will disappoint.

Commodity price exposure remains significant despite operational excellence. Recycling commodity prices, fuel costs, and natural gas values all impact profitability. The company faces "headwinds from declining commodity values, RINs, and FX rates, impacting margins". While Waste Connections manages these risks better than peers, they can't eliminate them entirely.

Regulatory and environmental liabilities loom large. The Chiquita Canyon situation demonstrates how quickly environmental issues can become financial disasters. The landfill closure resulted in over $600 million in charges and cash outlays. With nearly 100 landfills in operation, similar issues could emerge elsewhere.

Competition from larger players entering secondary markets is a growing threat. As Waste Management and Republic Services exhaust growth opportunities in major metros, they're increasingly looking at secondary markets—Waste Connections' traditional stronghold. Their scale advantages in procurement, technology, and capital access could challenge Waste Connections' dominance.

Volume headwinds persist despite pricing power. Q4 2024 solid waste volumes declined 2.7%, reflecting both economic softness and strategic shedding of unprofitable business. While focusing on price over volume makes sense, persistent volume declines could eventually pressure revenue growth.

Competitive Positioning: David Among Goliaths

Compared to Waste Management (market cap ~$90 billion) and Republic Services (~$65 billion), Waste Connections (~$45 billion) remains the smaller player. But size isn't everything in waste. Waste Connections generates higher margins, better returns on capital, and faster organic growth than its larger peers.

The competitive dynamics are fascinating. Waste Management dominates major metros and large national accounts. Republic Services focuses on large markets and vertical integration. Waste Connections owns secondary markets and specialized niches. There's overlap, but less direct competition than you might expect.

Future Catalysts and Risks

Looking forward, several factors could drive outperformance. Accelerating inflation makes CPI-linked contracts more valuable. Infrastructure spending increases construction waste volumes. Tightening environmental regulations favor operational excellence. Continued labor shortages benefit companies with superior retention.

But risks abound. A recession could pressure volumes and pricing. Rising interest rates could make acquisitions more expensive. Technology disruption—autonomous vehicles, waste-to-energy innovations—could change industry economics. ESG pressures could require massive capital investment with uncertain returns.

The Verdict: Quality at a Premium

The investment case for Waste Connections ultimately comes down to whether you believe quality is worth paying for. This isn't a value stock trading at 10x earnings. It's a premium business trading at a premium multiple. The company has earned that premium through decades of exceptional execution, but maintaining it requires continued outperformance.

For long-term investors who appreciate compound stories, Waste Connections remains compelling despite the valuation. The business model is simple and durable. The competitive advantages are real and widening. The management team has proven they can adapt and execute through various cycles. And the runway for continued consolidation and margin expansion remains long.

For value investors or those worried about near-term headwinds, the risk-reward is less attractive. Any disappointment—integration challenges, environmental issues, margin compression—could trigger a sharp correction from current valuations. And with the macro environment uncertain, those risks feel elevated.

Perhaps the best framework is to think of Waste Connections as you would any high-quality compounder: wonderful business, exceptional management, but price matters. At current valuations, the margin of safety is thin. But for investors with long time horizons who understand the power of compound returns, Waste Connections remains one of the best operators in one of the best industries. Sometimes, paying up for quality is the best investment you can make.

XI. Epilogue & "What Would We Do?"

Standing at the threshold of $10 billion in revenue, Waste Connections faces the perpetual challenge of successful companies: how to maintain entrepreneurial energy while operating at institutional scale. The path forward requires balancing growth ambitions with operational excellence, cultural preservation with necessary evolution.

The Path to $10+ Billion and Beyond

The arithmetic to $10 billion is straightforward. With 2025 revenue guidance of $9.45-9.60 billion, Waste Connections will likely cross this milestone within the year through a combination of organic pricing growth (historically 4-6% annually), modest volume growth as the economy stabilizes, and continued acquisitions. But the more interesting question isn't when they'll hit $10 billion—it's what happens at $15 or $20 billion.

The company's addressable market remains enormous. Of the estimated 10,000+ private waste companies in North America, perhaps 2,000-3,000 fit Waste Connections' acquisition criteria. Even after 450+ deals, they've only consolidated a fraction of the opportunity. Add in the growing E&P waste market, expansion into recycling and organics processing, and international opportunities, and the runway extends for decades.

Technology and Automation Opportunities

While Waste Connections has been selective about technology adoption, several innovations could transform operations over the next decade. Autonomous vehicles—particularly for fixed commercial routes—could address driver shortages while improving safety. Advanced routing algorithms using real-time traffic and service data could optimize collection efficiency. IoT sensors in containers could enable dynamic routing based on actual fill levels rather than fixed schedules.

The company's partnership with AMP for AI-powered recycling, including a new MRF in Commerce City, Colorado scheduled to open in 2026, represents just the beginning. As recycling technology improves, previously uneconomical materials become profitable to process. Chemical recycling could unlock value from plastics currently sent to landfills. Organics processing could generate renewable natural gas at scale.

But Waste Connections' approach to technology will likely remain pragmatic. They won't be first movers or bleeding-edge adopters. They'll let others prove concepts, then selectively implement technologies that enhance their core operations without fundamentally changing their business model.

International Expansion Possibilities

With successful operations in Canada demonstrating their ability to operate outside the United States, international expansion becomes intriguing. Markets like Australia, the UK, or Chile share characteristics that fit Waste Connections' model: developed economies with fragmented waste industries, stable regulatory environments, and opportunities for consolidation.

But international expansion would require careful consideration. Different regulatory regimes, labor laws, and business cultures create complexity. The company's decentralized model and servant leadership culture might not translate directly. Most likely, any international expansion would come through partnership or acquisition of an existing platform rather than organic entry.

ESG Leadership Opportunities

Environmental considerations are evolving from compliance requirements to competitive advantages. Waste Connections is well-positioned to lead here. Their safety record, employee treatment, and operational excellence already exceed industry standards. But there's opportunity to go further.

Imagine Waste Connections as the first major hauler to achieve carbon neutrality through a combination of electric vehicles, renewable natural gas from landfills, and carbon sequestration. Or leading the industry in diverting waste from landfills through advanced recycling and organics processing. These initiatives require capital, but they generate returns—both financial and reputational.

The company's $150 million investment in renewable natural gas projects in 2024 suggests management understands this opportunity. As ESG considerations increasingly influence customer decisions and access to capital, operational excellence becomes even more valuable.

Final Reflections: Building Differentiation in a Commodity Industry

The Waste Connections story offers profound lessons that extend far beyond the waste industry. In a commoditized service business with mature technology and rational competition, they've generated extraordinary returns through operational excellence, cultural differentiation, and disciplined capital allocation.

The servant leadership philosophy that sounds soft in theory creates hard competitive advantages in practice. The decentralized model that seems risky actually reduces risk by empowering those closest to customers. The focus on secondary markets that appears limiting actually creates more durable competitive positions than fighting over major metros.

Perhaps most importantly, Waste Connections proves that how you do business matters as much as what business you're in. By treating employees with respect, keeping promises to customers, and thinking long-term, they've built one of the great compound stories in American business.

What Would We Do?

If we were running Waste Connections today, we'd focus on three priorities:

First, double down on human capital. With labor remaining the biggest constraint and competitive advantage, we'd invest even more in employee development, safety, and retention. This might mean industry-leading wages, enhanced benefits, or innovative programs like employee ownership. The ROI on reducing turnover from 15% to 10% would dwarf any technology investment.

Second, build the platform for the next generation. This means selective technology adoption that enhances rather than replaces human workers, expansion into adjacent services that leverage existing capabilities, and perhaps most importantly, developing the next generation of servant leaders who will carry the culture forward.

Third, maintain strategic patience. The temptation at $10 billion revenue will be to accelerate growth through larger deals, new markets, or aggressive expansion. But Waste Connections' success has come from discipline—saying no to bad deals, avoiding markets where they can't win, focusing on sustainable returns rather than headline growth.

The path from $10 billion to $20 billion won't be linear. There will be setbacks—economic downturns, integration challenges, environmental issues. But for a company that's navigated nearly three decades of change while maintaining its cultural core, these are manageable challenges.

In an industry where the service is essential, the barriers to entry are high, and the competitive dynamics are rational, Waste Connections has built something remarkable: a compound machine that generates predictable returns while treating all stakeholders—employees, customers, communities, shareholders—with respect.

Looking at Total Shareholder Returns, the company's "long-term outperformance of sector and market indices has delivered returns of 7,665% since going public in May 1998". Those returns weren't generated through financial engineering or lucky bets. They came from thousands of small decisions, executed well, compounded over time.

That's the real lesson of Waste Connections: in business, as in life, the fundamentals matter. Treat people well. Keep your promises. Think long-term. Execute consistently. Do these things for decades, and extraordinary outcomes become almost inevitable. It's a playbook that works in any industry, but it requires something rare: the discipline to stick with it when others chase shortcuts, and the patience to let compound returns work their magic.

XII. Recent News

The most recent developments at Waste Connections reinforce the themes that have defined the company for nearly three decades: disciplined growth, operational excellence, and a return to cultural fundamentals under Ron Mittelstaedt's renewed leadership.

Q4 2024 results exceeded expectations with revenue of $2.260 billion and the company delivering "a solid finish to a year of extraordinary accomplishments for Waste Connections both financially, with double-digit growth in both revenue and adjusted EBITDA, and operationally, with accelerating improvements in employee engagement and retention".

The 2025 outlook suggests continued momentum. Revenue is projected at $9.45 billion to $9.60 billion with adjusted EBITDA of $3.12 billion to $3.2 billion, implying margins of 33% to 33.3%. Adjusted free cash flow is expected to reach $1.3 billion to $1.35 billion.

Recent acquisition activity continues at a torrid pace. The company completed 24 acquisitions in 2024 adding $750 million in annualized revenues, with notable acquisitions including Royal Waste Services which "entrenches Waste Connections as one of the largest commercial waste companies in New York City".

Looking ahead, management remains optimistic about both organic growth and acquisition opportunities. Mittelstaedt noted the company is "well-positioned for another year of outsized growth in 2025 from price-led organic solid waste growth, with improving commodities and ongoing acquisition activity positioning us at or above the high end of our range of potential outcomes".

The transformation under Mittelstaedt's return continues to bear fruit, with the company achieving what many thought impossible: returning to its cultural roots while operating at unprecedented scale. As Waste Connections approaches the $10 billion revenue milestone, it does so not as a bloated giant but as a collection of entrepreneurial businesses united by common values and uncommon execution.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube