BitMine Immersion Technologies: From Shell Company to Ethereum Treasury Titan

The Setup: A $26 Million Company Becomes an $11 Billion Digital Asset Powerhouse

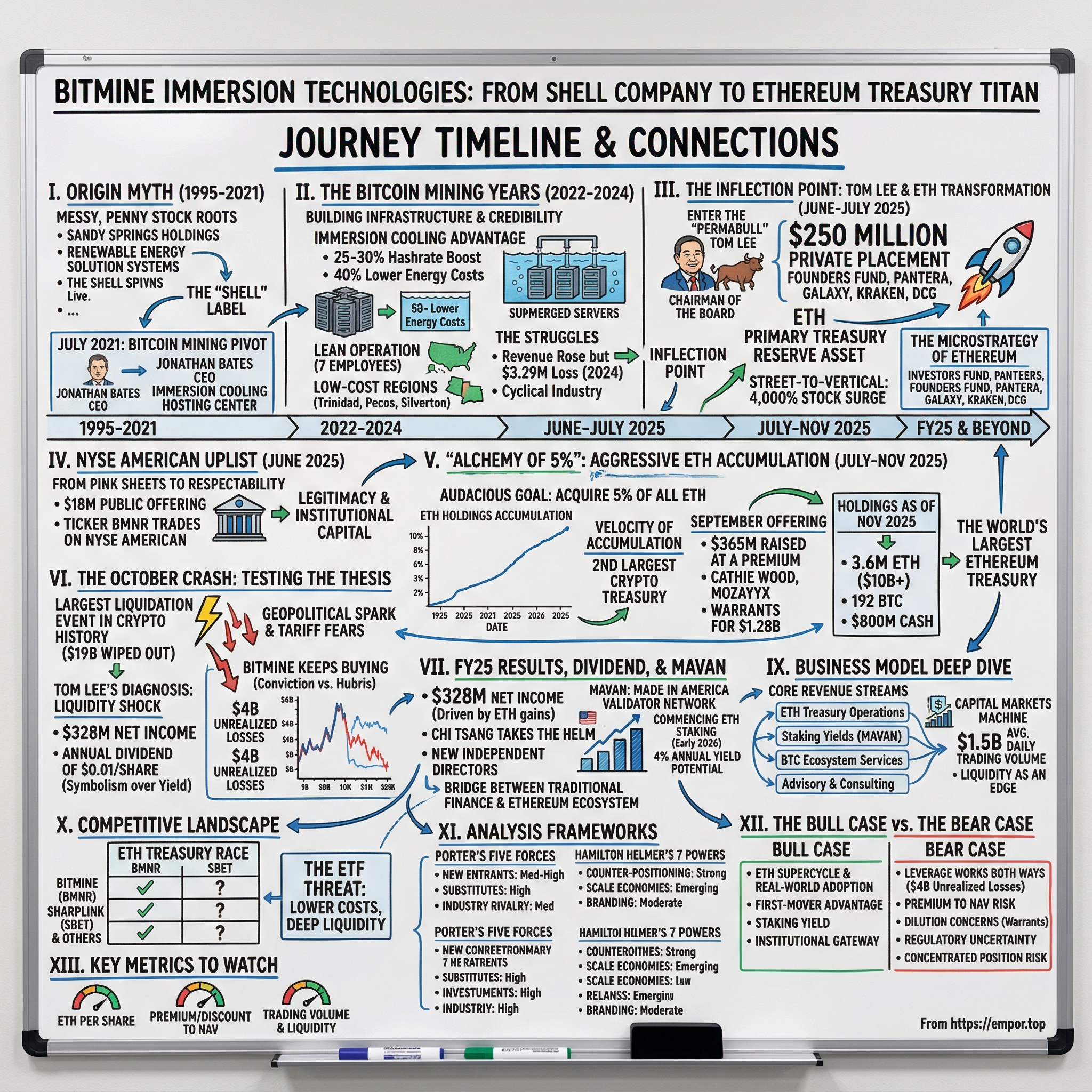

It’s late June 2025. BitMine Immersion Technologies is a small, Las Vegas-based company with a market cap of roughly $26 million—an immersion-cooled Bitcoin miner that, to most of Wall Street, might as well not exist. The stock is down about 45% on the year, hovering around $4.

And then, in a single announcement, everything changes.

On June 30, 2025, BitMine revealed a $250 million private placement led by MOZAYYX, backed by a lineup that reads like a who’s who of crypto and venture: Peter Thiel’s Founders Fund, Pantera Capital, FalconX, Galaxy Digital, Kraken, DCG, and Republic Digital. The deal was expected to close around July 3.

But the money wasn’t the headline. The headline was the person attached to it.

Thomas Lee—Fundstrat founder and CIO—was named Chairman of the Board, effective immediately. A high-profile Wall Street strategist was stepping into a company that had been living in the small-cap shadows, and he was bringing something far more valuable than capital: legitimacy.

The market reacted like it had just been introduced to a new kind of trade. Over the following days, BMNR went vertical—ripping from the low single digits to as high as $160. While Ethereum itself moved only about 10% over that stretch, BitMine’s stock surged nearly 4,000%.

In a week, a $26 million afterthought started trading like a $10 billion idea.

So what, exactly, did investors think they were buying? And why did a sleepy miner suddenly look like the future of corporate treasury strategy—right at the moment traditional finance and crypto began to blur into the same story?

I. The Origin Myth: From Shell Company to Crypto Dreams (1995–2021)

The Ghost of Corporate Past

Every reinvention story wants a clean, heroic origin. BitMine’s is the opposite: messy, technical, and very “penny stock.”

Yes, the company traces its roots to August 16, 1995, and today it’s headquartered in Las Vegas. But that date doesn’t describe a steady march toward greatness. It describes a corporate entity that spent years as little more than a public wrapper—reshuffled, renamed, and repurposed through a series of restructurings that only make sense if you’ve lived inside SEC filings.

Over time, the company carried multiple identities, including Sandy Springs Holdings Inc. and Renewable Energy Solution Systems. At various points it pointed itself at entirely different industries—clean energy solutions, telecommunications, solar installations. Under the Sandy Springs Holdings banner, it described its business as providing solar electric installations for commercial, government, and telecommunications customers, as well as large residences.

But the more important label wasn’t “solar” or “telecom.” It was “shell.”

In the microcap world, a shell company is a publicly traded structure with minimal real operations—valuable not for what it does, but for what it can become. Shells are often used in reverse-merger plays: instead of a traditional IPO, a new business can step into the public listing and effectively “go public” by taking over the shell.

Sandy Springs Holdings was shaped by exactly that kind of machinery. A Delaware reorganization created a clean structure through a multi-entity merger setup. RESS of Delaware and Sandy Springs Holdings Inc. were incorporated in Delaware on November 20, 2019, alongside other entities involved in the reorganization, including RESS Merger Corporation and Renewable Energy Solution Systems.

And then, buried in plain sight in the filings, is the blunt truth: prior to a change of control to new directors, the company was a shell company.

Not a struggling operator. Not an underdog. A shell—waiting for a story.

The Bitcoin Mining Pivot

That story finally arrives in July 2021, when new management was appointed with a specific mission: build a hosting center for Bitcoin mining computers, primarily using immersion cooling technology, and mine Bitcoin for the company’s own account.

Jonathan Bates emerged as the leader of this pivot, becoming CEO and Chairman. The timing made sense. The 2021 bull market had turned mining into an arms race, and the industry was rapidly professionalizing. Infrastructure mattered. Efficiency mattered. Cooling mattered.

The rebrand followed soon after. On March 3, 2022, FINRA approved the company’s name change from Sandy Springs Holdings, Inc. to BitMine Immersion Technologies, Inc., along with a new ticker symbol: BMNR.

It wasn’t just a cosmetic reset. The name staked out a specific bet—that BitMine wouldn’t be “another miner,” but a miner built around immersion cooling. A real piece of technology, a real operational edge, and the first foundation of credibility in a company that, until recently, was mostly paperwork.

II. The Bitcoin Mining Years: Building Infrastructure and Credibility (2022–2024)

The Science of Staying Cool

If BitMine was going to be taken seriously as a miner, it needed a real edge. Its pitch was immersion cooling.

Immersion cooling works exactly like it sounds: you submerge computer components, sometimes entire servers, in a specialized liquid that conducts heat but not electricity. That liquid—called a dielectric coolant—pulls heat away far more efficiently than air ever could.

And in Bitcoin mining, heat is the enemy. Mining rigs run flat-out solving cryptographic puzzles, and they throw off enormous thermal load while doing it. Traditional air cooling means giant warehouses, loud fans, costly HVAC, and a meaningful chunk of your power bill spent not on mining—but on preventing your mining equipment from cooking itself.

Immersion changes that equation. It can be dramatically more efficient than air cooling, with estimates putting power usage effectiveness around 1.05. A cooler, more stable environment can also extend machine lifespan—some estimates say by 30% or more.

BitMine said its immersion setup delivered a 25–30% hashrate boost, roughly 40% lower energy costs, and near-silent operations. Not a marketing flourish—a very specific attempt to build an advantage in a business where efficiency is everything.

Building a Business in Low-Cost Regions

Cooling is only half the mining story. The other half is power.

BitMine set up operations in low-cost energy regions: Trinidad, Pecos (Texas), and Silverton (Texas). The logic was straightforward. Trinidad offered access to inexpensive natural gas. Texas, with its deregulated power market and abundant energy generation, had become one of the world’s major magnets for crypto mining.

But BitMine wasn’t trying to outspend the giants. Its model was designed to be capital-efficient: pass through some or all fixed costs to hosting clients, then take a percentage of the Bitcoin mined through profit-sharing agreements. Instead of betting the company on massive upfront infrastructure, it tried to build something lighter—hosting plus some exposure to the upside of mined coins.

It landed its first client on a three-year hosting agreement and, by the second quarter of fiscal 2022, became revenue positive.

A Lean Operation

For most miners, “building infrastructure” conjures images of sprawling campuses and huge teams. BitMine did it with seven employees.

Seven people managing operations spread across multiple locations tells you what this company was trying to be: asset-light, partner-driven, operationally tight. Lease equipment. Work with hosting arrangements. Focus on efficiency. Avoid the kind of capex that can bury a small miner the moment the cycle turns.

The company positioned itself around immersion cooling, modern ASIC hardware, and flexible leasing—tools meant to scale quickly and adapt when the market shifted, without being trapped under the fixed costs that crush weaker operators.

The Struggles

Even with a technical edge, scale still mattered—and BitMine struggled to reach it.

In 2024, revenue rose to $3.31 million from $645,278 the year prior, but the company still lost $3.29 million. The growth was real, but it was coming off a tiny base, and profitability stayed out of reach.

That wasn’t just a BitMine problem. The mining business is cyclical and unforgiving. Bitcoin halving events periodically cut rewards in half, squeezing margins across the board. Competition kept intensifying as larger, better-capitalized miners expanded and negotiated ever-better power economics.

For a small player, the pressure built fast. If mining was increasingly a game of scale and cheapest power, where did that leave a lean, niche miner—especially one that had just spent years trying to prove it was a real operating company at all?

III. The Inflection Point: Tom Lee and the Ethereum Transformation (June–July 2025)

Enter the Permabull

If BitMine’s first act was about immersion cooling and surviving as a tiny miner, its second act began with a single name: Tom Lee.

Lee is a Wall Street strategist and media fixture—an American entrepreneur, financial analyst, strategist, investor, and a familiar face on CNBC’s Fast Money, Tech Check, Halftime Report, and Closing Bell. He was born in Westland, Michigan, the third of four children of Korean immigrant parents. His father was a retired psychiatrist; his mother went from homemaker to Subway franchise owner.

He studied economics at the University of Pennsylvania’s Wharton School, concentrating in finance and accounting, joined Delta Upsilon, and became a CFA charterholder. Professionally, he built credibility the old-fashioned way: years inside big banks and big research. He served as J.P. Morgan’s Chief Equity Strategist from 2007 to 2014, after working as a Managing Director at Salomon Smith Barney.

In 2014, he co-founded Fundstrat Global Advisors, a research firm serving clients in more than two dozen countries. And in crypto—where most traditional strategists either laughed early or arrived late—Lee was unusually early. In 2017, he published a report, “A Framework for Valuing Bitcoin as a Substitute for Gold,” arguing Bitcoin could take share from gold as a store of value.

Over time, that combination—traditional Wall Street résumé plus public conviction—earned him a particular reputation: the “permabull.” Sometimes right, sometimes early, always optimistic, and always loud enough for markets to hear.

That’s exactly why his arrival at BitMine mattered.

The $250 Million Private Placement

BitMine announced it had priced and signed a private placement to sell 55,555,556 shares of common stock at $4.50 per share, for expected gross proceeds of about $250 million. The deal was led by MOZAYYX, with participation from a lineup that made BitMine instantly feel bigger than its balance sheet: Founders Fund, Pantera, FalconX, Republic Digital, Kraken, Galaxy Digital, DCG, Diametric Capital, Occam Crest Management, Graticule (GAMA), GSR, and Tom Lee himself.

The roster did more than provide capital—it signaled what BitMine was becoming. Founders Fund brought Silicon Valley gravity. Pantera brought crypto-native institutional heft. Galaxy, Kraken, and DCG plugged BitMine into the core plumbing of the digital-asset world.

And then BitMine said the quiet part out loud: ETH would serve as the company’s primary treasury reserve asset.

Thomas Lee, newly appointed Chairman of the Board of Directors, framed it as a reflection of where finance was headed: “This transaction includes the highest quality investors across trad-fi and crypto venture capital, properly reflecting the rapid and continued convergence of traditional financial services and crypto.”

Put differently: BitMine wasn’t just raising money. It was switching identities.

At the time, BitMine was a crypto mining company with a market cap around $26 million—raising nearly ten times its entire value in one shot. On July 9, 2025, BitMine announced the private placement had closed, funded in a combination of cash and crypto, to implement its Ethereum treasury strategy.

The MicroStrategy of Ethereum

The strategy wasn’t subtle. BitMine was positioning itself as the MicroStrategy of Ethereum—an operating company that becomes, in practice, a publicly traded vehicle for accumulating a crypto asset.

But Ethereum offered a twist that Bitcoin doesn’t: once you hold ETH, you can potentially put it to work. BitMine emphasized that an ETH treasury position creates access to native protocol-level activities on Ethereum, including staking and decentralized finance mechanisms.

Lee’s broader thesis tied Ethereum to the most visible real-world crypto use case: stablecoins. “Stablecoins have proven to be the ‘chatGPT’ of crypto, leading to rapid adoption by consumers, merchants and financial services providers,” he said. He pointed to Treasury Secretary Scott Bessent’s view that the stablecoin market could reasonably reach $2 trillion from around $250 billion, and argued Ethereum mattered because “Ethereum is the blockchain where the majority of stablecoin payments are transacted and thus, ETH should benefit from this growth.”

Internally, BitMine also set a simple scoreboard: increase the value of ETH held per share. The company said it could do that through reinvesting cash flows, capital markets activity, and changes in the price of ETH itself.

The Market Reacts

Then the stock did what stocks do when the story suddenly becomes bigger than the business.

BitMine Immersion Technologies (NYSE AMERICAN:BMNR) surged more than 690% in Monday’s trading after the private placement announcement. From the June 30 news that it would raise funds primarily to increase Ethereum holdings, the stock ran from about $4 to roughly $135 in short order—more than a 30-fold move.

The velocity was the point. In days, BitMine went from an obscure, single-digit miner to a triple-digit, headline-making proxy for Ethereum exposure—wrapped in a listed U.S. equity, and now stamped with Tom Lee’s name.

IV. The NYSE American Uplist: Legitimacy at Last (June 2025)

From Pink Sheets to Respectability

BitMine’s transformation didn’t start with Tom Lee. It started with something far less exciting, but just as essential: getting itself onto a real exchange.

In early June 2025—just weeks before the Ethereum pivot—BitMine priced an underwritten public offering: 2,250,000 shares at $8.00 per share, raising about $18 million in gross proceeds before fees and expenses. The underwriters also received a 45-day option to buy up to 337,500 additional shares to cover over-allotments. The deal was expected to close on June 6, 2025, subject to the usual conditions.

Alongside the raise came the bigger milestone: BitMine’s common stock was approved for listing on the NYSE American. On June 5, 2025, those newly sold shares started trading there under the same ticker—BMNR.

This wasn’t paperwork. It was a passport.

Moving from the OTC markets to a national exchange put BitMine in front of a much larger pool of capital. Many institutions can’t touch OTC names, no matter the story. The uplist made BitMine “buyable” to an entirely different class of investor—and it gave the company the credibility and liquidity it would soon need in bulk.

CEO Jonathan Bates called it a major milestone that would increase visibility, broaden the investor base, and improve liquidity. And at the time, the plan was still straightforward: the $18 million offering was used to purchase Bitcoin as part of an initial treasury strategy. Bates pointed to the coming acceleration, saying the private placement would ramp BitMine’s treasury holdings shortly after its first treasury purchase on June 9, 2025.

But within weeks, “treasury strategy” was about to mean something else entirely.

V. The "Alchemy of 5%": Aggressive ETH Accumulation (July–November 2025)

An Audacious Goal

Tom Lee didn’t come to BitMine to build a respectable ETH position.

He came to build a stake so large it would be impossible to ignore.

The company said it would use the new capital to make Ethereum its primary treasury reserve asset—scaling its ETH holdings by more than sixteen times. But the real headline was the ambition behind it: acquire 5% of all ETH in existence.

Lee dubbed it the “alchemy of 5%,” framing it as more than a portfolio choice. If BitMine could amass that much ETH, it wouldn’t just be an Ethereum proxy stock. It would be a meaningful player inside the ecosystem itself.

In Lee’s words: “We increased our cash holdings to $389 million and acquired 82,353 ETH tokens over the past week pushing our ETH holdings to 3.4 million, or 2.8% of the supply of ETH. We are now more than halfway towards our initial pursuit of the 'alchemy of 5%' of ETH.”

Velocity of Accumulation

Then came the part that made even crypto markets do a double-take: the speed.

Since July, BitMine acquired roughly 3.5 million ETH, becoming the second-largest crypto treasury, behind only Michael Saylor’s Strategy. Week after week, it kept buying—at one point adding another 110,288 ETH, worth nearly $400 million at the time, pushing total holdings to more than 3.5 million ETH, around 2.9% of total supply.

Strategy still sat on top in absolute size. But BitMine’s pace started to feel like a different kind of weapon—one that made the lead look, if not vulnerable, at least no longer unthinkable.

The September Offering: Capital at a Premium

In September, BitMine went back to the markets for more fuel—and pulled off something that almost never happens in equity fundraising.

It entered a securities purchase agreement with an institutional investor to sell about 5.22 million shares at $70 per share, plus warrants for up to roughly 10.4 million additional shares with an $87.50 strike price. The $70 price represented about a 14% premium to the stock’s September 19 close. The warrants were exercisable upon issuance and expired on March 22, 2027.

The common stock sale was expected to bring in about $365.24 million in gross proceeds before fees and expenses. If the warrants were exercised for cash, they could add another roughly $913 million—bringing potential total proceeds to about $1.28 billion.

The takeaway wasn’t the mechanics. It was the signal.

Most companies have to discount stock to convince investors to fund them. BitMine raised at a premium—because investors weren’t buying a mining business. They were buying a liquid, listed path to ETH exposure, and they were willing to pay up for it.

The company said the proceeds would primarily go toward increasing its Ethereum holdings, in service of the 5% goal. The round was backed by high-profile names, including ARK’s Cathie Wood, MOZAYYX, and Founders Fund.

The Holdings as of November 2025

By November 23 at 7:30pm ET, BitMine reported a balance sheet that would have sounded absurd just months earlier: 3,629,701 ETH valued at $2,840 per ETH (Coinbase), 192 BTC, a $38 million stake in Eightco Holdings (NASDAQ: ORBS) under “moonshots,” and $800 million in unencumbered cash.

That ETH position represented about 3.0% of total Ethereum supply—roughly two-thirds of the way to the “alchemy of 5%.” BitMine now reigned as the largest Ethereum treasury in the world, and the #2 global crypto treasury overall, behind Strategy.

Five months earlier, this was a $26 million microcap miner trying to prove it belonged on a real exchange.

Now it was sitting on more than $10 billion worth of Ethereum, and sprinting toward a target that sounded less like treasury management and more like a corporate takeover of a monetary network.

VI. The October Crash: Testing the Thesis

The Largest Liquidation Event in Crypto History

October 10, 2025 was the kind of day crypto traders talk about in before-and-after terms.

What started as a normal Friday session unraveled into what CoinGlass later tagged as the largest liquidation event it had ever tracked: about $19 billion in leveraged positions wiped out in roughly 24 hours, across Bitcoin, Ethereum, and everything downstream of them.

The spark was geopolitical. A podium announcement reignited trade-war fears: “Starting November 1, the United States will impose a 100% tariff on all Chinese imports.” Risk assets flinched immediately. The S&P 500 dropped more than 2%, and crypto—built on leverage and momentum—fell through the floor.

Bitcoin slid sharply, Ethereum followed, and many altcoins got hit hardest, with some down 60–90% at the worst of it. In the span of hours, nearly $1 trillion in crypto market cap was erased.

Tom Lee's Diagnosis

Tom Lee’s take wasn’t that Ethereum had broken. It was that the market’s plumbing had.

He argued the real damage was in liquidity—specifically, that a major market maker may have taken losses in the crash and then pulled back from providing liquidity. When that happens, the market gets thinner, spreads widen, and every wave of selling hits harder because there’s less standing in the way to absorb it.

“Crypto prices continue to suffer as the drop in market liquidity and function since October 10, which was the largest ever single day liquidation event in the history of crypto,” Lee said. He pointed to 2022’s post-FTX liquidity shock as a precedent, arguing that even severe dislocations can clear—and that recoveries can come quickly once liquidity returns.

BitMine Keeps Buying

This was the moment BitMine’s strategy stopped being a PowerPoint and became a test of nerve.

As the broader digital asset treasury sector pulled back—many firms pausing purchases, pivoting to share buybacks, or even selling assets—BitMine kept leaning in. Over one week, the company bought 69,822 ETH, taking total holdings to about 3.63 million tokens, roughly 3% of total ETH supply.

It was a striking decision given the backdrop: analysts estimated BitMine was sitting on around $4 billion in unrealized losses on its ETH position at the time. Buying into that kind of drawdown reads one of two ways—conviction or hubris—and markets don’t hand you the answer immediately.

The Unrealized Losses

The paper losses were brutal. Ether had fallen nearly 40% from its August peak during the correction, and BitMine—built to be a leveraged proxy for ETH exposure—felt it from both directions: the asset down, and sentiment down.

Even after the additional purchases, BitMine’s stock kept sliding. On November 24, BMNR traded around $26, still roughly 84% below its July peak of $161.

And the volatility wasn’t subtle. Over the past year, the shares ranged from $3.20 at the low to $161 at the high—an almost unbelievable swing for what, not long ago, was a tiny mining company trying to get taken seriously.

VII. FY25 Results, Dividend, and the MAVAN Network

Record Earnings—But What Do They Mean?

BitMine reported full-year fiscal 2025 net income of $328,161,370, with fully diluted EPS of $13.39 per share. It also declared an annual dividend of $0.01 per BMNR share.

On paper, those are jaw-dropping numbers for a company that, just a year earlier, generated only $3.31 million in revenue. But there’s an important asterisk: the profits were driven overwhelmingly by mark-to-market gains on its Ethereum holdings—accounting gains that can reverse just as quickly when crypto prices move the other way.

In other words, the income statement suddenly looked like a powerhouse. But the engine under the hood was still the same thesis: BitMine’s financial destiny was tethered to ETH.

A Dividend? Really?

A $0.01 annual dividend is tiny—more symbolic than lucrative. Still, in crypto, symbolism matters.

BitMine said it was the first large-cap crypto company to declare an annual dividend. And that’s the real message: this wasn’t about yield. It was about positioning. By paying even a token dividend, BitMine was trying to place itself in a different mental category—not just a volatile proxy for ETH, but something closer to a crypto-native financial company that can return capital to shareholders.

MAVAN: The Staking Infrastructure

The next step was to make the ETH do more than sit on the balance sheet.

“The company is well positioned in 2026 and we look forward to commencing ETH staking with our MAVAN, or Made in America Validator Network, in early calendar 2026,” said Thomas “Tom” Lee, Chairman of BitMine.

BitMine selected three top staking providers for a focused pilot, testing capabilities as it advanced and scaled its own dedicated staking infrastructure: the Made-in-America Validator Network (MAVAN).

MAVAN was BitMine’s attempt to turn an enormous ETH position into a productive asset—earning yield through Ethereum’s proof-of-stake system. With staking yields hovering around 4% annually, even a few percentage points start to matter when your holdings are measured in the tens of billions.

VIII. Leadership Transition: Chi Tsang Takes the Helm

The Old Guard Steps Back

“Building BitMine from the ground up to become an NYSE listed company, and then the world’s largest holder of Ethereum, has been a remarkable journey,” former CEO Jonathan Bates said. “I’m proud of what our team has achieved, and I have complete confidence that Tom and BitMine’s new leadership will carry that momentum as it continues to grow.”

With that, Bates stepped aside—and BitMine handed the CEO role to Chi Tsang, with Tom Lee as chairman and the Ethereum-treasury strategy now firmly in motion. At the same time, the company refreshed its board, adding three new members with backgrounds spanning traditional finance, asset management, and law.

The New Guard Arrives

Tsang took over as CEO as BitMine added three independent directors: Robert Sechan, Olivia Howe, and Jason Edgeworth. Sechan is the founder of NewEdge Capital Group and CEO of NewEdge Wealth. Edgeworth is an asset manager for JPD Family Holdings. Howe is Chief Legal Officer at RigUp.

Tsang framed the moment as bigger than BitMine—or even crypto. “The transformation and innovation now facing Wall Street through blockchain and Ethereum mirror the explosion of opportunity that mobile phones and the internet unleashed on telecoms and technology in the 1990s,” he said. “With its substantial Ethereum holdings and credibility with both Wall Street and the Ethereum ecosystem, BitMine is positioned to become a leading financial institution.”

Lee was even more explicit about what the leadership shift was meant to signal. “Our new CEO and Board members bring a unique blend of experience, insight, and leadership across technology, DeFi and financial services, enabling BitMine to further position itself as the bridge between traditional capital markets and the supercycle Ethereum ecosystem,” he said.

IX. Business Model Deep Dive: How BitMine Makes Money

The Core Revenue Streams

By late 2025, BitMine wasn’t really “a miner” anymore. It was a public company with an Ethereum-dominated balance sheet—and a grab bag of crypto-adjacent businesses meant to support, finance, and justify that treasury strategy.

On paper, the company operated across several lanes: ETH treasury operations; BTC ecosystem services like consulting, advisory work, and equipment leasing; facilitating and optimizing third-party power and hosting arrangements; and disciplined BTC treasury management, all while winding down proprietary self-mining exposure and deferring new site buildouts.

BitMine acquired digital assets through a mix of Bitcoin mining operations and capital raises. And alongside whatever mining footprint remained, it offered synthetic Bitcoin mining exposure, advisory services for businesses seeking Bitcoin-denominated revenues, and general cryptocurrency consulting.

In other words: the operating business existed, but the treasury strategy was the main event.

The Economics of the Treasury Strategy

The model underneath it all was straightforward: raise capital, buy crypto, and let the balance sheet expand or contract with the market.

In practice, BitMine’s earnings power came from four places:

- Mark-to-market gains on its ETH holdings (the dominant factor behind its FY25 net income)

- Staking yields once MAVAN launches (with the company pointing to roughly 4% or more annually on staked ETH)

- Legacy mining operations (still there, but no longer the center of gravity)

- Advisory and consulting services (early-stage, but positioned as a growth area)

That mix is important, because it clarifies what BitMine was selling investors: not stable operating cash flows, but a liquid, equity-wrapped way to own and potentially earn on ETH.

The Capital Markets Machine

The real differentiator wasn’t mining tech or consulting. It was BitMine’s access to capital—because once a company can reliably raise money, it can keep buying, keep compounding, and keep pushing the “ETH-per-share” story.

By this point, BMNR had become one of the most actively traded stocks in the U.S., with about $1.4 billion in average daily dollar volume over five days, ranking it around the high 40s nationally.

That liquidity became its edge. For institutions that wanted large-scale Ethereum exposure through a regulated U.S. equity, the menu was short. BitMine’s trading volume made it possible to build real positions without immediately blowing out the price—turning the stock itself into a kind of capital markets flywheel that could fund the next round of ETH accumulation.

X. The Competitive Landscape: BitMine vs. SharpLink and Others

The Ethereum Treasury Race

BitMine isn’t the only company that looked at MicroStrategy’s Bitcoin playbook and thought: what if we did this with Ethereum?

SharpLink Gaming (SBET), a Nasdaq-listed company that previously focused on sports betting marketing, pivoted into an Ethereum treasury strategy and emerged as the world’s second-largest corporate ETH holder. It reported holdings of 740,760 ETH—worth more than $3.15 billion—behind BitMine Immersion, which was sitting on more than 1.7 million ETH. And SharpLink didn’t just buy ETH; it brought in Ethereum royalty. Joseph Lubin, Ethereum co-founder and ConsenSys CEO, became Chairman and strategic advisor.

And the field didn’t stop there. Other names—like Bit Digital—also announced pivots to the same basic model in June.

The pattern is hard to miss. A new category is forming in public markets: companies racing to become the “MicroStrategy of Ethereum,” offering investors an equity wrapper around ETH accumulation.

BitMine vs. SharpLink: Key Differences

The two leading contenders sell different flavors of the same idea.

SharpLink has leaned into steady ETH accumulation and staking yield—more like a yield-oriented ETH vehicle that many observers see as potentially less volatile. BitMine, by contrast, has gone for speed and scale: rapid accumulation, major Wall Street backers, and a legacy mining footprint that reinforces its crypto identity. That posture makes BMNR feel like the higher-risk, higher-reward version of the trade, while SBET may be more attractive to investors looking for a slower, more deliberate path.

Lubin’s Ethereum pedigree and a disciplined approach give SBET a sense of long-term alignment with the ecosystem. BitMine—once a Bitcoin miner, now an ETH treasury company—has chosen the more aggressive route. At the time, it said its ETH holdings were worth over $7.5 billion, making it the largest ETH treasury globally.

XI. Porter's Five Forces Analysis

1. Threat of New Entrants: MEDIUM-HIGH

In theory, the barrier to a crypto treasury strategy is almost laughably low. Any public company can wake up tomorrow, announce an “ETH treasury,” and start buying.

In practice, the moat shows up fast:

- Capital requirements: Getting to “billions of dollars of ETH” is a capital markets game, not a crypto game.

- Institutional credibility: Tom Lee’s name and network unlocked funding and counterparties most small public companies can’t access.

- First-mover advantage: BitMine had already amassed roughly 3% of ETH supply, making it hard for latecomers to matter at the same scale.

- Liquidity: Executing and financing purchases at this size requires real trading, execution, and operational infrastructure.

2. Bargaining Power of Suppliers: LOW

BitMine wasn’t dependent on a single doorway into the market. It lined up partnerships with FalconX, Kraken, and Galaxy Digital, and it already had custody relationships with BitGo and Fidelity Digital.

ETH itself is broadly available across exchanges and OTC desks, which keeps supplier power low. If one provider becomes expensive or constrained, BitMine can route around them. And on the custody side, institutional-grade options have multiplied—good for safety and compliance, but also a sign that custody is becoming more standardized.

3. Bargaining Power of Buyers: LOW-MEDIUM

Here, the “buyers” are investors using BMNR as a proxy for Ethereum exposure.

They do have choices: buy ETH directly, buy spot Ethereum ETFs, or buy other ETH-treasury names. But BitMine’s pitch is that it isn’t just another wrapper. It’s scale, speed, and a level of institutional credibility that—at least during its run—made it feel like the main venue for the trade.

4. Threat of Substitutes: HIGH

This is the pressure point.

- Direct ETH ownership (no corporate wrapper, no premium)

- Spot Ethereum ETFs (simpler access, less friction)

- Other Ethereum treasury companies (SharpLink, Bit Digital)

- DeFi yield strategies (for investors comfortable operating on-chain)

If investors can get the exposure they want more cleanly elsewhere, BMNR’s value proposition gets harder to defend—especially when the stock swings away from NAV.

5. Industry Rivalry: MEDIUM

The real competition isn’t just other corporate treasuries. It’s the ETF complex.

Ethereum ETFs collectively held over 5.7 million ETH, versus about 1.75 million ETH across publicly traded corporate treasuries combined. In other words, the center of gravity for “equity-like ETH exposure” is still ETFs, not treasury companies.

And ETFs come with structural advantages: generally lower costs, no premium or discount to NAV dynamics in the same way, and deep liquidity.

So while BitMine may headline the corporate treasury race, it’s ultimately competing for investor capital against the simplest alternative on the board: the ETF.

XII. Hamilton Helmer's 7 Powers Framework

Which "Powers" Does BitMine Possess?

1. Scale Economies: EMERGING

With roughly 3% of ETH supply on its balance sheet, BitMine had reached a size where its buying—and eventually any selling—could start to matter at the margin. That scale can cut both ways: it can create influence and execution advantages on the way in, and real friction on the way out.

2. Network Effects: WEAK

BitMine doesn’t have classic network effects. More shareholders don’t make the “product” better for existing shareholders—if anything, raising more equity to buy more ETH can dilute ownership.

3. Counter-Positioning: STRONG

In the market’s imagination, Tom Lee had become to Ethereum what Michael Saylor is to Bitcoin. And with BitMine now the #2 crypto treasury company by size, the bet wasn’t just on ETH—it was on the maverick chairman behind the curtain.

BitMine positioned itself as a go-to institutional vehicle for Ethereum exposure. For many traditional investors constrained from holding spot crypto directly, BMNR offered a listed, U.S.-regulated on-ramp. Meanwhile, ETFs couldn’t simply “become BitMine” without abandoning the ETF structure and taking on an operating-company balance sheet, capital markets strategy, and all the messiness that comes with it.

4. Switching Costs: WEAK

There’s little stickiness here. Investors can sell BMNR and buy ETH directly—or buy an ETH ETF—without meaningful friction. There are no structural switching costs keeping them in.

5. Branding: MODERATE

Tom Lee’s public profile and constant media presence gave BitMine something most small-cap crypto companies can’t buy: instant awareness and a sense of legitimacy. But “permabull” is a double-edged sword—magnetic when the thesis is working, and easy to dismiss when it isn’t.

6. Cornered Resource: WEAK-MODERATE

A multi-million ETH position starts to look like something more than “just holdings,” especially if BitMine kept marching toward the 5% target. At that kind of concentration, the company could become a uniquely significant stakeholder in the Ethereum ecosystem—though “influence” is not the same thing as control.

7. Process Power: EMERGING

BitMine’s real operational edge showed up in the mechanics: raising capital—sometimes at a premium—and turning it into massive ETH purchases quickly. The partnerships with FalconX, Galaxy Digital, Kraken, and others didn’t just add logos; they created a repeatable pipeline for execution, custody, and scale that would be hard for copycats to assemble overnight.

XIII. The Bull Case

Why This Could Work Spectacularly

- Ethereum's Supercycle Thesis

The optimistic version of this story starts with a simple premise: Ethereum is still early in its next wave of real-world adoption.

BitMine—and Tom Lee in particular—has pointed to multiple tailwinds stacking up at once: the upcoming Fusaka upgrade, the continued surge in stablecoins, and the accelerating push to tokenize real-world assets like stocks, bonds, and real estate on Ethereum.

Lee’s framing is that tokenization isn’t just about slicing assets into smaller pieces or trading them 24/7. It’s a structural change in how assets can be packaged and sold. “Tokenization is a major unlock for asset markets as it is more than just fractionalization or 24/7 liquidity. It is the innovation driven by factorization of an asset by time, product or geography. This in turn will provide great market transparency for issuers and investors,” Lee said.

He also argues that policy is finally catching up. In BitMine’s telling, the GENIUS Act and the SEC’s Project Crypto could be watershed moments for financial services in 2025—comparable in impact to the U.S. ending Bretton Woods and taking the dollar off the gold standard on August 15, 1971. That 1971 shift helped set the stage for the modern Wall Street giants and the financial and payments rails that dominate today. BitMine’s bet is that a similar “rules-of-the-road” moment could push more finance onto Ethereum’s rails.

- First-Mover Advantage

BitMine moved early—and moved aggressively—before “Ethereum treasury company” became a crowded trade.

By late 2025, it had established itself as the dominant ETH-treasury name and the holder of the second-largest crypto treasury overall, with total holdings of $13.2 billion, trailing only Michael Saylor’s Strategy.

- Staking Yield Optionality

If Bitcoin treasury companies are basically pure price bets, Ethereum introduces a new lever: yield.

BitMine’s MAVAN network is designed to turn its ETH from a static balance-sheet asset into something that can generate ongoing income through staking—revenue that doesn’t require ETH to go up tomorrow. At roughly 4% yields on more than $10 billion of ETH, that could translate into hundreds of millions in annual income.

- Institutional Gateway

BitMine’s pitch isn’t just ETH exposure—it’s a version of ETH exposure that fits inside traditional market plumbing.

Tom Lee brings credibility and institutional attention that most crypto-native companies can’t manufacture. And while the company’s center of gravity has shifted to treasury strategy, BitMine still points to its roots as an operating business: immersion-cooled mining technology it says boosts hashrate by 25–30%, cuts energy costs by about 40%, and runs quietly—positioned to produce a steady flow of revenue alongside the balance-sheet strategy.

XIV. The Bear Case

Why This Could End Badly

1. Leverage Works Both Ways

BitMine kept buying even while it was sitting on roughly $4 billion in unrealized losses on its ETH position. That’s the trade in one sentence.

When ETH rises, BMNR can feel like a rocket ship: the balance sheet inflates, the story gets louder, the stock can outrun the asset. But when ETH falls, the same machinery runs in reverse. Losses stack up quickly, sentiment turns, and the equity can drop harder than ETH itself. The paper loss wasn’t just a red number—it was proof of how unforgiving this structure can be.

2. Premium to NAV Risk

For all the talk of staking and “ETH-per-share,” BitMine’s underlying business has a history of operational losses from the mining era. And its valuation has often reflected expectation rather than earnings power, including a very high price-to-sales multiple compared to the sector.

That matters because the stock doesn’t always trade like a simple claim on the ETH it holds. If BMNR trades at a premium to net asset value, investors are paying more than the underlying ETH is worth. In a euphoric market, that premium can persist. In a fearful one, it can vanish overnight—and sometimes flip into a discount, trapping shareholders in the worst possible version of the trade.

3. Dilution Concerns

BitMine’s growth engine is capital markets. That’s also its Achilles’ heel.

The September deal wasn’t just a common stock sale; it also came with warrants for up to 10.44 million additional shares at an $87.50 strike price, with the company noting total potential proceeds of about $1.28 billion if exercised. That’s a lot of future share count hanging over the stock.

Issuing stock can be accretive when shares trade above NAV. But it still dilutes existing owners. And if the market ever stops rewarding the strategy with a premium valuation, the company’s ability to fund more ETH purchases gets constrained—right when it would most want flexibility.

4. Regulatory Uncertainty

Even with the GENIUS Act in place, crypto regulation is still a moving target. A shift in tax treatment, securities classification, or the rules around staking could hit BitMine directly—not just the price of ETH, but the company’s ability to generate yield and operate its strategy as advertised.

5. Concentrated Position Risk

Owning about 3% of ETH supply isn’t just a flex. It’s a risk profile.

At that size, any meaningful decision—especially selling—can move the market against you. And because the position is so visible, BitMine’s reputation becomes entangled with broader Ethereum narratives: governance disputes, ecosystem controversy, or even just changing institutional sentiment. The stake is massive enough to matter, but also too large to unwind quickly without paying for the privilege.

XV. Key Metrics to Watch

If you want to understand BitMine’s story from here—and not just react to the latest ETH candle—there are three KPIs that matter most.

1. ETH Per Share

BitMine has effectively told investors what scoreboard it plans to play on: ETH per share.

The goal is simple in theory—grow the amount of ETH backing each share over time. In practice, it’s the cleanest way to tell whether BitMine’s capital raises and treasury purchases are helping existing shareholders or quietly diluting them.

If ETH per share rises faster than ETH itself, the company is compounding value. If it rises more slowly—or falls—then shareholders are getting diluted, even if the total ETH pile is getting bigger.

2. Premium/Discount to NAV

BMNR isn’t just a claim on a pile of ETH. It trades like a story. And the quickest way to measure how much the market believes that story is the premium or discount to net asset value per share.

A persistent premium usually means investors think management can do something more than “buy and hold”—raise capital efficiently, execute well, maybe generate yield through staking, and keep growing ETH per share. A discount is the market’s way of saying: we’d rather own the ETH directly.

3. Trading Volume and Liquidity

BitMine has leaned heavily into one advantage that most would-be treasury companies never achieve: liquidity.

The company has pointed to BMNR trading with roughly $1.5 billion in average daily dollar volume over five days, ranking around #60 among U.S.-listed stocks. That kind of volume isn’t trivia—it’s part of the engine. Liquidity makes the stock usable for institutions, and it helps BitMine keep tapping capital markets when it wants to buy more ETH.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube