International Gemmological Institute: The Certification Empire Built on Trust

I. Introduction & Episode Roadmap

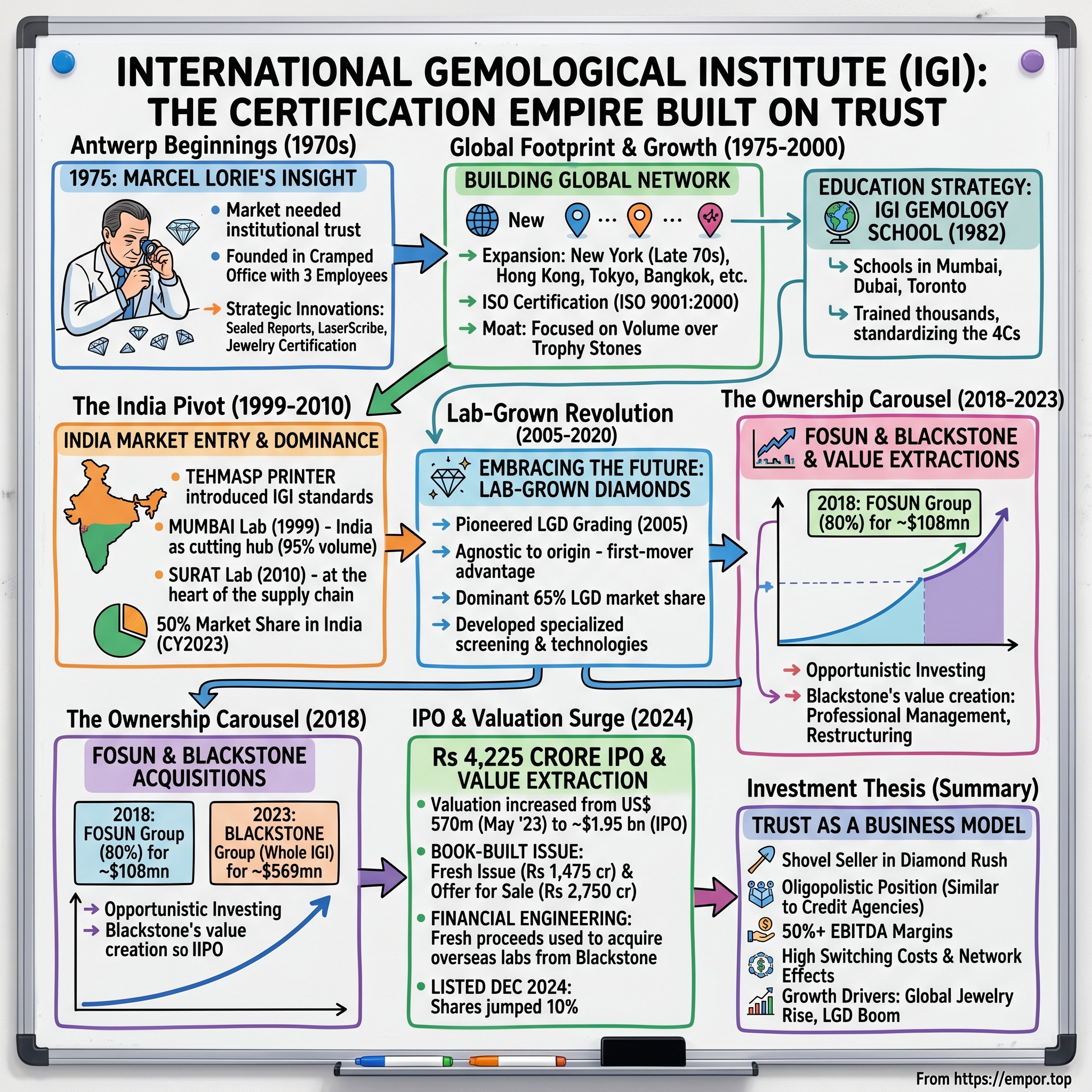

Picture this: A Belgian diamond trader in 1975 Antwerp, watching dealers squint through loupes at thousands of tiny diamonds, each transaction built on nothing but a handshake and reputation. Marcel Lorie saw something others missed—not the diamonds themselves, but the desperate need for trust in a market drowning in stones. What started as a three-person operation in a cramped office above Antwerp's diamond district would become the world's largest independent gemological certification empire, processing over 15 million pieces annually and commanding a market capitalization approaching $2 billion.

This is the story of International Gemmological Institute—IGI—a company that built its fortress not on diamonds, but on something far more valuable: institutional trust. While competitors fought over who could grade the biggest, most expensive stones, IGI quietly became the infrastructure layer for the entire global diamond industry, particularly in segments others ignored: smaller stones, finished jewelry, and eventually, the controversial world of lab-grown diamonds. The real story begins with a simple financial engineering masterstroke. Last year, Blackstone acquired IGI Group from Chinese investment firm Fosun and Roland Lorie of the founding family for $569 million. Fast forward just 18 months, and the upcoming IPO values IGI at Rs 165.5 billion (approximately US$ 1.95 billion), a significant increase from its valuation of US$ 570 million in May 2023. But here's where it gets interesting: IGI IPO is a book-built issue of Rs 4,225.00 crores, combining a fresh issue of 3.54 crore shares aggregating to Rs 1,475.00 crores and an offer for sale of 6.59 crore shares aggregating to Rs 2,750.00 crores.

When the dust settles, Blackstone will have orchestrated one of the most elegant value extraction plays in recent private equity history. They're selling parts of IGI to itself using public money, monetizing their stake through the Indian capital markets while maintaining control. The numbers tell a story that would make any financial engineer proud: a tripling of valuation in less than two years, all while the underlying business fundamentals remained largely unchanged.

But to understand how we got here—how a certification company became worth billions, how trust became a business model, and how India became the center of the global diamond universe—we need to go back to where it all began: the cobblestone streets of Antwerp in the 1970s, where a veteran diamond trader saw an opportunity that would reshape an entire industry.

II. The Diamond District Origins (1970s-1975)

The year is 1975. Antwerp's diamond district hums with activity as dealers from Mumbai, Tel Aviv, and New York crowd into cramped offices, examining stones through loupes, negotiating in a babel of languages. The Nixon Shock of 1971—when the U.S. abandoned the gold standard—has sent shockwaves through global markets. Suddenly, everyone wants tangible assets. Gold. Art. And especially diamonds.

In this chaos, Marcel Lorie, a 50-year-old veteran of the diamond trade, notices something peculiar. While the Gemological Institute of America (GIA) had introduced diamond certification back in 1934, by the mid-1970s they were still primarily focused on the trophy stones—those magnificent rocks above 2 carats that graced the fingers of Hollywood stars and oil sheikhs. But what about the millions of smaller diamonds flooding in from India's cutting centers? What about the finished jewelry that retailers were desperate to authenticate? Lorié founded IGI at the age of 50 and saw what others missed: a massive market gap. His goal was to create an independent gemological laboratory providing reliable, impartial, and accessible certification services for a broader range of diamonds, including smaller stones and finished jewelry. While GIA focused on the Tiffany diamonds of the world, millions of engagement rings, earrings, and pendants containing smaller stones went uncertified, their value determined by nothing more than a dealer's word.

The timing was perfect. Antwerp in the 1970s was experiencing a unique convergence. The city's historic position as a diamond trading hub—dating back to the 15th century—was being reinvigorated by a new wave of Indian diamond merchants. Antwerp, known as a historic hub for diamond trading due to its proximity to India, especially our beloved Surat, played a key role in the founding of IGI. The economic instability following the Nixon Shock had created unprecedented demand for tangible assets. Americans, traditionally the world's largest diamond consumers, were buying stones not just for romance but as a hedge against inflation.

IGI is founded in Antwerp, Belgium, by Marcel Lorie in 1975. But Marcel didn't just create another grading lab. He engineered three strategic innovations that would define IGI's trajectory for the next five decades:

First, IGI developed tamper-proof security-sealed reports for diamonds and colored stones. It launched the patented LaserScribe inscription system, which allowed unique identifiers to be inscribed on diamonds. These weren't just technical improvements—they were trust mechanisms, turning a subjective assessment into something that felt scientific, permanent, unquestionable.

Second, and perhaps most importantly, Becomes the first gemstone grading laboratory to issue Jewelry Identification Reports among it's global peers. While competitors focused on loose stones, IGI recognized that consumers didn't buy certificates—they bought jewelry. A grandmother's ring, a wedding band, a pair of earrings. By certifying finished pieces, IGI inserted itself into the emotional transaction between retailer and consumer.

The third innovation wouldn't fully reveal itself until 1982, but Marcel was already laying the groundwork: education as a growth strategy. He understood that certification was worthless unless people understood what they were certifying. The dealers, the retailers, the consumers—they all needed to speak the same language of the four Cs (cut, color, clarity, carat).

By the end of 1975, IGI operated from a modest office above Antwerp's diamond district with just three employees. Marcel, at 50, had bet his reputation and resources on a simple insight: in a market built on trust, the company that could institutionalize and scale that trust would become indispensable. He was right, but even he couldn't have imagined how right.

The foundation was set. Now came the hard part: convincing an industry that had operated on handshakes for centuries that they needed a piece of paper to do business. The journey from those three employees in Antwerp to a global certification empire was about to begin, and it would take IGI to places Marcel Lorie never imagined—from the cutting floors of Surat to the luxury malls of Shanghai, from traditional diamonds to laboratory-created stones that would upend the entire industry.

III. Building the Global Footprint (1975-2000)

The expansion began quietly. Opens new IGI laboratories in New York. It was the late 1970s, and Marcel Lorie faced a classic chicken-and-egg problem: dealers wouldn't use IGI certificates unless consumers demanded them, but consumers didn't know to demand something that barely existed. His solution was brilliant in its simplicity—don't sell to the dealers, educate them. Founded in Antwerp in 1982, the IGI Gemology School currently has branches in Mumbai, Cavalese, Dubai, and Toronto. This wasn't just another educational venture—it was strategic infrastructure building. Marcel understood that every graduate would become an evangelist for certification, spreading the gospel of the four Cs to jewelry stores from Brussels to Bangkok.

The curriculum was revolutionary for its practicality. The schools promote IGI's mission of education and knowledge by offering courses in polished diamonds, rough diamonds, colored stones, pearl grading, and jewelry design. IGI's prestigious gemology training courses attract thousands of diamond dealers and jewelers from 90 countries annually, with courses available in many languages. Unlike academic programs that focused on mineralogy and geology, IGI taught dealers how to grade, how to communicate value, and most importantly, how to sell certified stones at a premium.

By the mid-1980s, IGI had achieved something remarkable: ISO certification. The only ISO 9001:2000 certified international gemological organization, IGI adheres strictly to an internationally accepted system for diamond grading. This wasn't just about standards—it was about legitimacy. In an industry where trust was everything, ISO certification transformed IGI from a Belgian startup into an institution.

The expansion accelerated through the 1990s. Founded in Antwerp in 1975 by a staff of three, IGI has grown to include more than 450 professionals, spanning the globe with offices in New York City, Hong Kong, Tokyo, Bangkok, Dubai, Toronto, Los Angeles, Tel Aviv, and Mumbai. Each new office wasn't just a laboratory—it was a beachhead in a local market, a training center for local dealers, and most importantly, a trust mark that local consumers would come to recognize.

The strategic decisions during this period revealed Marcel's genius. While competitors chased prestige by certifying museum-quality stones, IGI focused on volume. They understood that the real money wasn't in grading the Hope Diamond—it was in certifying the millions of engagement rings sold at mall jewelry stores. By positioning themselves as the certification solution for the middle market, IGI built a moat that would prove nearly impossible to cross.

Opens new IGI laboratories and schools in Thailand and India. This expansion into Asia in the late 1990s would prove to be the company's most important strategic move. While Western markets were mature, Asia—particularly India—was about to explode. The stage was set for IGI's next act, one that would transform it from a successful certification company into an essential piece of global diamond infrastructure.

IV. The India Pivot & Market Entry (1999-2010)

The phone call came in 1998. Tehmasp Printer, a young diamond professional in Mumbai, was explaining to Marcel Lorie what everyone in the industry already knew but no one wanted to admit: India wasn't just cutting diamonds anymore—it was becoming the diamond industry. The numbers were staggering. India is the world's largest centre for cutting and polishing diamonds, accounting for approximately 95 per cent of the world's total polished diamonds by volume in CY2023.

But here was the problem: Indian diamonds, despite dominating global volume, traded at a discount. Why? Trust. Western buyers didn't trust Indian certification. Indian manufacturers didn't trust each other. The entire ecosystem operated on relationships and reputations that didn't scale. Printer saw the opportunity: become the trust layer for India's diamond revolution.

IGI is the largest independent certification and accreditation service provider in India, holding approximately a 50 per cent market share in terms of the number of certifications of diamonds, studded jewellery, and coloured stones for CY2023. But this dominance didn't happen overnight. When IGI opened its first Indian laboratory in Mumbai in 1999, they faced a market that was simultaneously desperate for their services and deeply skeptical of outsiders. The strategy was masterful. Rather than competing with local players, IGI positioned itself as the international standard that would help Indian diamonds command global prices. He has been with IGI for 24 years, most recently as Managing Director of IGI India, and was instrumental in introducing IGI's grading and certification practices to India's gemstone and jewelry industries. Tehmasp Printer didn't just open laboratories—he built an ecosystem.

The real breakthrough came with Surat. In April 2010, IGI opened a laboratory in Surat, its fifth diamond grading laboratory in India. Situated in the heart of Surat, India's diamond cutting and polishing capital, this institution is a symbol of excellence in the field of gemology. The Surat laboratory specializes in the certification of: Natural Diamonds: Precision evaluation of cut, clarity, color, and carat weight, supporting Surat's reputation as a leading hub for diamond manufacturing and export.

This wasn't just another office opening. Surat processes 90% of the world's diamonds by volume. Every diamond that passes through Surat eventually ends up in jewelry stores from Fifth Avenue to Shanghai's Nanjing Road. By establishing a presence there, IGI inserted itself into the global diamond supply chain at its most critical chokepoint.

The numbers from this period tell a story of exponential growth. IGI went from certifying thousands of stones annually in India to millions. They didn't just capture market share—they created the market. Before IGI, most small diamonds traded as commodities. After IGI, each stone had an identity, a grade, a certificate. This transformation added billions in value to India's diamond exports.

IGI is the largest independent certification and accreditation service provider in India, holding approximately a 50 per cent market share in terms of the number of certifications of diamonds, studded jewellery, and coloured stones for CY2023, IGI India said in a release. But perhaps the most strategic move during this period was one that wouldn't pay off for another decade: IGI's early embrace of what would become the most controversial topic in the diamond industry.

V. The Lab-Grown Diamond Revolution (2005-2020)

The meeting took place in 2004, in a nondescript conference room in Antwerp. Roland Lorie, who had taken over from his father Marcel, sat across from a delegation of scientists and entrepreneurs who claimed they could grow diamonds in a laboratory that were indistinguishable from natural ones. The diamond industry representatives in the room were skeptical, some openly hostile. Lab-grown diamonds were the industry's dirty secret—everyone knew they were coming, but nobody wanted to acknowledge them.

Roland made a decision that would define IGI's next two decades: embrace the future rather than fight it. IGI pioneered the grading of lab grown diamonds in 2005 and continues to lead the field today. While competitors like GIA initially refused to grade lab-grown diamonds or insisted on calling them "synthetic" (a term that made them sound fake), IGI treated them with the same rigor as natural stones.

The backlash was immediate and fierce. Traditional diamond dealers accused IGI of betraying the industry. De Beers, which had spent decades building the mythology around natural diamonds, was particularly incensed. But Roland and his team saw what others missed: lab-grown diamonds weren't competition for natural diamonds—they were an entirely new market. The numbers tell the story of IGI's prescience. IGI held a 42% share in studded jewelry certifications and led the LGD segment with a dominant 65% market share. While competitors scrambled to catch up, IGI had already built the infrastructure, trained the gemologists, and most importantly, educated the market on how to think about lab-grown diamonds.

The technology moat IGI built during this period was formidable. IGI screens every gemstone using state of the art technologies to determine naturally mined, laboratory grown or simulant origin. They developed proprietary detection systems that could identify lab-grown diamonds with near-perfect accuracy, even as the technology for creating these stones improved dramatically.

But the real genius was in the positioning. IGI didn't present lab-grown diamonds as fake or inferior—they graded them with the same rigor as natural stones. IGI pioneered the grading of lab grown diamonds in 2005 and continues to lead the field today. This legitimized the entire category, transforming lab-grown diamonds from curiosity to commodity.

The economics were transformative. Lab-grown diamonds typically sold for 30-40% less than natural equivalents, opening up entirely new market segments. Young couples who couldn't afford a natural diamond engagement ring could now buy a lab-grown alternative. Fashion jewelry that would have been prohibitively expensive with natural stones became accessible.

By 2020, the lab-grown diamond market had exploded from virtually nothing to billions in annual sales. And at the center of it all was IGI, certifying the vast majority of these stones, collecting fees on every certificate, building a recurring revenue stream that would make any software company envious. IGI was the first to offer certificates for lab diamonds and has a first-mover advantage in market share and sales volume.

The controversy never fully subsided. Natural diamond purists continued to view IGI with suspicion. But by then, it didn't matter. IGI had positioned itself perfectly for the future—agnostic about origin, focused on certification, making money whether diamonds came from the earth or a laboratory. They had become, in the truest sense, a shovel seller in the new diamond rush.

VI. The Ownership Carousel: Fosun to Blackstone (2018-2023)

The boardroom at Fosun's Shanghai headquarters in early 2018 was electric with possibility. Guo Guangchang, Fosun's billionaire founder, had a vision: transform his conglomerate into China's answer to Warren Buffett's Berkshire Hathaway, but with a focus on lifestyle and luxury brands that would appeal to China's exploding middle class. IGI fit perfectly into this narrative.

In 2018, China's Fosun Group purchased 80% of IGI Group for around $108mn. The logic seemed impeccable. China was becoming the world's largest luxury market. Chinese consumers were obsessed with diamonds as symbols of success and romance. And here was IGI, the infrastructure layer that could authenticate and legitimize every stone flowing into the Middle Kingdom.

But Fosun's timing was catastrophic. Within two years, COVID-19 would shut down global travel, devastate the luxury market, and trap Fosun in a liquidity crisis as Chinese regulators cracked down on overleveraged conglomerates. The diamond certification business, which required minimal capital and generated steady cash flows, suddenly looked like one of the few assets Fosun could sell quickly and profitably.

Enter Blackstone, the masters of opportunistic investing. In early 2023, as Fosun desperately needed liquidity, Blackstone's team saw an opportunity that went beyond a distressed sale. They saw a business with monopolistic characteristics trading at a fraction of its potential value.

Last year, Fosun and the other shareholders sold the whole IGI Group to private equity group Blackstone for $569mn. For Fosun, it was a face-saving exit—they more than quintupled their investment in five years. For Blackstone, it was the beginning of one of the most elegant value creation plays in recent private equity history.

The Blackstone playbook was executed with surgical precision. First, they brought in professional management. Blackstone has enhanced IGI's management team with several high-level appointments, including a new CFO, global CHRO, global CMO, and new country managers in the UAE and the USA. These weren't just any executives—they were operators who understood how to prepare a company for public markets. Second, and more audaciously, Blackstone began restructuring IGI's corporate structure with an eye toward the Indian public markets. The restructuring plan, which includes elevating Tehmasp Printer from Managing Director of IGI India to Global CEO, reflects Blackstone's intent to shift IGI's operational base to India. This wasn't just operational streamlining—it was preparation for one of the most sophisticated financial engineering plays in recent memory.

The consolidation strategy was masterful. In a strategic move that has raised eyebrows, Blackstone is seeking to leverage its upcoming IPO of International Gemmological Institute (India) Limited (IGI) to finance the acquisition of IGI's overseas businesses from itself. Think about that for a moment: Blackstone would use public market money to buy assets from itself, consolidating the global IGI business under the Indian entity while simultaneously cashing out part of their investment.

By late 2023, the transformation was complete. IGI had gone from a family-controlled, European-centric certification company to a professionally managed, India-focused global leader positioned for public markets. The valuation had nearly tripled in 18 months, not through operational improvements alone, but through financial restructuring, strategic repositioning, and perfect market timing.

VII. The IPO & Financial Engineering Masterclass (2024)

The conference room at Kotak Mahindra Capital's Mumbai headquarters in August 2024 was a study in controlled excitement. Investment bankers, lawyers, and Blackstone's deal team were putting the finishing touches on what would become one of the most audacious IPO structures in Indian capital markets history. The structure was breathtaking in its complexity. IGI IPO is a book-built issue of Rs 4,225.00 crores. The issue is a combination of fresh issue of 35.4 m shares aggregating to Rs 1,475.00 crores and offer for sale of 65.9 m shares aggregating to Rs 2,750.00 crores. But here's the genius: IGI India plans to use Rs. 1,300 crore from its Rs. 1,475 crore fresh IPO proceeds to acquire IGI Belgium and IGI Netherlands from Blackstone.

Let that sink in. Blackstone owns IGI Belgium and Netherlands. They're taking IGI India public. They're using the IPO proceeds—money from public investors—to have IGI India buy IGI Belgium and Netherlands from... Blackstone itself. It's a circular transaction of breathtaking elegance. IGI paid BCP Asia II Topco—a subsidiary of Blackstone—$88.4 million for the Netherlands lab and $70 million for the Belgium facility.

The timing was perfect. India's IPO market was red hot. Retail investors were desperate for quality listings. And here was IGI, a monopolistic business with 50% EBITDA margins, growing at 30% annually, available to the public for the first time. The anchor book was oversubscribed within hours, with marquee names like the Government of Singapore, Nomura, and ICICI Prudential fighting for allocations.

The valuation math was extraordinary. The upcoming IPO values IGI at Rs 165.5 bn (approximately US$ 1.95 billion), a significant increase from its valuation of US$ 570 m in May 2023. In just 18 months, Blackstone had engineered a value creation of over $1.3 billion, and they were still retaining 76% ownership post-IPO.

But the real masterstroke was the narrative. This wasn't positioned as a private equity exit—it was sold as the consolidation of a global leader under Indian management, tapping into nationalist sentiment about India's dominance in the diamond industry. Following the IPO, BCP Asia owns 76% of IGI. Blackstone wasn't leaving; they were doubling down, just with other people's money.

The December 20, 2024 listing day arrived with massive fanfare. The market responded favorably to the acquisition, with IGI shares jumping 10%. For Blackstone, it was mission accomplished: they had extracted over $300 million in cash while maintaining control, tripled their valuation, and positioned IGI for continued growth using public market capital.

VIII. The Business Model & Unit Economics

Walk into any IGI laboratory—whether in Surat, Antwerp, or New York—and you'll witness the same scene: rows of gemologists bent over microscopes, each examining stones that will pass through their hands in minutes but generate revenue for decades. This is the beauty of the certification business: high throughput, minimal capital requirements, and recurring revenue from an industry that never stops producing.

The numbers tell a story of operational excellence that would make any software CEO jealous. For the nine months ending September 2024, IGI India reported revenue of Rs 7.9 bn, compared to Rs 8.9 bn a year back. But here's the kicker: the margins. With EBITDA margins consistently above 50%, IGI operates more like a software company than a traditional services business.

Why such extraordinary margins? Start with the cost structure. Once you've invested in the equipment—microscopes, spectrometers, imaging systems—the marginal cost of certifying each additional stone is negligible. A gemologist can grade 20-30 stones per day. The equipment lasts for years. The only real variable cost is labor, and even that scales beautifully as gemologists become more experienced and efficient.

The pricing power is remarkable. IGI charges anywhere from $15 for a small melee diamond to several hundred dollars for a large stone or complex piece of jewelry. Customers rarely push back on price because the certificate typically adds 10-20% to the value of their inventory. For a jeweler selling a $5,000 ring, a $50 certificate that provides customer confidence is a rounding error.

As of the same date, IGI had over 7,500 customers located across 10 countries. In CY2023, IGI India was the largest independent certification and accreditation services provider in India, with a market share of about 50%. Globally, it is the second-largest independent certification and accreditation services provider based on revenue for CY2023, with a global market share of about 33%.

But the real genius of the model is the network effects. Every certificate IGI issues becomes a marketing tool. Consumers learn to look for the IGI logo. Retailers promote IGI certification as a selling point. Manufacturers need IGI certificates because their customers demand them. It's a virtuous cycle that compounds over time.

The education business amplifies these network effects. Each year, thousands of professionals and consumers enroll in the courses offered by IGI's School of Gemology. Whether your ambition is to become a more confident buyer, a diamond grader, jewelry designer, sales professional, or Graduate Gemologist, IGI's worldwide schools offer an unrivaled range of coursework. Every graduate becomes an ambassador for IGI certification, spreading the gospel of third-party verification throughout the industry.

The switching costs are prohibitive. Once a manufacturer's entire inventory is IGI-certified, switching to another lab means re-certifying everything, confusing customers, and potentially seeing inventory values decline. It worked with 9 of India's top 10 jewellery chains just last year. These aren't just customers—they're locked-in partners who couldn't leave if they wanted to.

Geographic diversification provides another layer of resilience. While ~75% of the group's business comes from India, IGI has strategically positioned labs in every major diamond trading hub. When COVID shut down India, Dubai picked up the slack. When China slowed, the US accelerated. It's a portfolio approach to a services business.

The lab-grown diamond boom has turbocharged this model. IGI pioneered the grading of lab grown diamonds in 2005 and continues to lead the field today. More complex than the analysis of most gemstones, IGI's lab grown diamond certification process demonstrates unparalleled expertise in the testing and documentation of loose stones and finished jewelry items undergoing lab grown diamond certification. As these stones flood the market—growing at 15-20% annually—IGI captures value from every single one that needs certification.

The capital efficiency is stunning. IGI can open a new laboratory for less than $1 million, and it typically reaches profitability within 12-18 months. Compare that to a diamond mine that requires billions in capital and a decade to develop. IGI is the ultimate asset-light business in an asset-heavy industry.

IX. Playbook: Trust as a Business

The playbook IGI has perfected over five decades is deceptively simple yet nearly impossible to replicate: become the trust layer for an entire industry, then monetize that trust at every transaction point. It's a strategy that transforms a commodity service into an economic moat wider than the Grand Canyon.

Consider the barriers to entry. Unlike miners or manufacturers who need heavy investments and infrastructure, IGI benefits from working with all players in the value chain by offering its expertise in certification. This makes IGI a "shovel seller" in the diamond industry's gold rush. Operating in an oligopolistic market, similar to credit rating agencies, IGI holds a strong global position with limited competition. Its business model is highly efficient that requires low ongoing investment.

The trust moat is built on three pillars. First, longevity—IGI has been certifying stones since 1975, building a reputation over generations. Second, consistency—an IGI certificate in Mumbai means exactly the same thing as one in New York. Third, ubiquity—with 31 laboratories worldwide, IGI is everywhere the diamond industry operates.

But here's what's brilliant: IGI doesn't just certify stones; it defines value. When IGI says a diamond is VVS1 clarity, that assessment becomes market reality. Traders quote prices based on IGI grades. Insurance companies assess claims using IGI certificates. It's not just providing a service—it's establishing the very language of commerce in diamonds.

The shovel-seller strategy is particularly elegant. During the California Gold Rush, the real winners weren't the miners but the merchants selling picks and shovels. Similarly, IGI profits regardless of diamond market cycles. Natural diamonds booming? IGI certifies them. Lab-grown diamonds disrupting the market? IGI certifies those too. Colored stones having a moment? IGI's there. The company is structurally positioned to benefit from any trend in the gemstone industry.

The operational leverage in this model is extraordinary. As volumes increase, costs barely budge. The same gemologist who grades 20 stones today can grade 25 tomorrow with minimal additional training. The same equipment that processes thousands of stones annually can handle tens of thousands with basic maintenance. Every incremental certificate drops almost entirely to the bottom line.

Private equity value creation in IGI's case went beyond financial engineering. Blackstone professionalized operations, upgraded technology, and most importantly, recognized that IGI's Indian operations were the crown jewel. By restructuring the company to center it in India—where 95% of the world's diamonds are processed—they aligned corporate structure with economic reality.

The India advantage extends beyond proximity to supply. Labor costs for skilled gemologists in India are a fraction of those in Belgium or the US, yet the quality is comparable or superior. Indian gemologists, trained in IGI's own schools, combine technical expertise with cultural understanding of a market where jewelry isn't just adornment but investment, tradition, and identity.

The recurring revenue nature of the business is often overlooked but crucial. Unlike a mine that depletes or a factory that obsolesces, IGI's service is needed in perpetuity. Every new diamond discovered, every stone recut, every piece of estate jewelry sold—they all need certification. It's a toll booth on the highway of the global diamond trade, and traffic only increases.

The technology investments Blackstone facilitated have created additional moats. IGI's detection systems for synthetic diamonds, their blockchain initiatives for certificate verification, and their AI-powered grading assistance tools aren't just operational improvements—they're barriers to entry that would cost competitors hundreds of millions to replicate.

X. Analysis & Investment Thesis

The bull case for IGI reads like a private equity dream. Start with the macro: global jewelry sales are expected to grow at 5-7% annually through 2030, driven by rising wealth in Asia, particularly India and China. The Indian jewelry market alone is projected to reach $100 billion by 2027. Every piece of that jewelry potentially needs certification.

Lab-grown diamonds represent an even more explosive opportunity. Currently 10% of the global diamond market, lab-grown stones are expected to reach 20-25% by 2030. IGI certification is believed to be the best certification for lab-grown diamonds. IGI works very fast and its certification prices are lower than that of the GIA. IGI gives specific grades like color and clarity for lab-grown diamonds. Most synthetic diamond manufacturers get their certification from IGI. As the undisputed leader in lab-grown certification with 65% market share, IGI is perfectly positioned to capture this growth.

The financial metrics are compelling. Trading at roughly 30x earnings post-IPO might seem rich, but consider: 50%+ EBITDA margins, 30%+ revenue growth, essentially zero capital requirements for growth, and a dominant market position in a fragmented industry. Find another business with these characteristics trading at a similar multiple—you won't.

But the bear case has teeth. For the nine months ending September 2024, IGI India reported revenue of Rs 7.9 bn, compared to Rs 8.9 bn a year back. This revenue decline, while potentially temporary, raises questions about growth sustainability. The natural diamond market faces serious headwinds. About 35% of the world's rough diamonds come from Russia, and international sanctions have created supply disruptions. Since nearly a fifth of IGI's revenue comes from certifying natural diamonds, any prolonged disruption could impact results.

Competition is evolving. GIA, long focused on high-end natural diamonds, is aggressively entering the lab-grown space. Both labs are deemed reliable, but the demand for GIA-graded diamonds has seen a spike since 2023, mainly because of their reliable branding. The US market shows a gradual shift towards GIA lab diamonds, while the global market maintains a strong preference for IGI lab diamonds. If GIA successfully challenges IGI's dominance in lab-grown certification, margin pressure is inevitable.

Technology risks loom larger than many investors realize. Blockchain-based certification could disintermediate traditional players. AI-powered grading systems might commoditize what's currently a skilled service. And if synthetic diamond detection becomes foolproof and portable, why would anyone need laboratory certification?

The China wildcard can't be ignored. Chinese labs are aggressively pricing services at 50-70% below IGI rates. While quality and trust currently protect IGI's position, history shows that Chinese competitors often move upmarket faster than expected. If a Chinese lab achieves international credibility, IGI's pricing power evaporates overnight.

Valuation concerns are legitimate. At current multiples, IGI is priced for perfection. Any disappointment—a slowdown in lab-grown adoption, successful competitive entry, regulatory changes—could trigger a significant re-rating. The fact that Blackstone is extracting value so early in the public market journey might signal their own concerns about peak valuation.

The regulatory landscape is evolving. Governments worldwide are increasingly focused on conflict diamonds, money laundering through jewelry, and disclosure requirements for synthetic stones. While IGI should benefit from increased regulation, compliance costs could escalate, and new requirements might favor local over international certifiers.

XI. Epilogue & Reflections

As we reach the end of this journey through IGI's remarkable transformation, several meta-lessons emerge that extend far beyond the diamond industry. This isn't just a story about certificates and gemstones—it's a masterclass in building and monetizing trust, creating infrastructure businesses in luxury markets, and the evolution of private equity value creation.

The infrastructure play in luxury markets reveals a fundamental truth: in industries built on aspiration and emotion, the companies that provide the rational layer often capture disproportionate value. IGI doesn't sell dreams; it validates them. While diamond miners and jewelry brands fight for consumer attention, IGI quietly taxes every transaction, providing the trust layer that makes the entire industry function.

What Blackstone saw that Fosun missed wasn't just operational improvement potential—it was a geographic arbitrage opportunity combined with a regulatory tailwind. Fosun, focused on Chinese luxury consumption, viewed IGI as a way to authenticate products for Chinese consumers. Blackstone recognized that the real value was in India, where production happens, not in China, where consumption occurs. By centering the business in India and taking it public there, Blackstone captured both operational efficiency and valuation multiple expansion.

The timing of Blackstone's exit—or partial exit—is instructive. Last year, Fosun and the other shareholders sold the whole IGI Group to private equity group Blackstone for $569mn - according to the IPO prospectus, Blackstone paid $393mn for IGI (India) and $176mn for IGI (Belgium) and IGI (Netherlands). Eighteen months later, they're taking it public at a $2 billion valuation while retaining 76% ownership. This isn't just financial engineering—it's recognition that the window for these valuations might not stay open forever.

The future of certification in a digital, blockchain world presents both opportunities and threats. IGI's physical certificates might seem anachronistic in an age of NFTs and digital verification. But trust isn't just about technology—it's about institutions, reputation, and accountability. IGI's challenge will be to digitize trust while maintaining the human expertise that justifies its existence.

For founders, IGI's story offers crucial lessons about building trust-based monopolies. Start by solving an information asymmetry problem. Focus on the unglamorous but essential parts of an industry. Build switching costs through education and ecosystem lock-in. And most importantly, position yourself as the infrastructure layer that enables others' success rather than competing with them.

The lab-grown diamond revolution that IGI pioneered certification for might ultimately be its biggest challenge. As lab-grown diamonds become commoditized, will certification matter as much? When you can produce a perfect diamond in a lab, does anyone need an expert to tell them it's perfect? IGI's bet is that trust always matters, that consumers will always want third-party validation, that the ceremony of certification is as important as the certificate itself.

The India story embedded in IGI's trajectory reflects a broader transformation. India isn't just the world's back office anymore—it's becoming the command center for global industries. IGI's restructuring to center itself in India while maintaining its Belgian heritage represents a template for how global businesses might evolve: Eastern operations, Western branding, worldwide reach.

The private equity playbook has evolved from leverage and cost-cutting to something far more sophisticated. Blackstone's handling of IGI shows the new model: operational transformation, geographic optimization, multiple expansion through public markets, and maintaining control while extracting value. It's financial engineering, yes, but built on genuine business improvement.

As IGI trades on public markets, its next chapter will be written by different forces—quarterly earnings pressure, retail investor sentiment, index inclusion dynamics. The company that spent 50 years building trust must now maintain it while satisfying the market's insatiable demand for growth. Whether IGI can balance these competing demands while navigating technological disruption and competitive threats will determine if this IPO marks the beginning of a new growth phase or the peak of a historic run.

The ultimate lesson might be this: in a world increasingly mediated by platforms and algorithms, the companies that can institutionalize and scale human judgment become paradoxically more valuable, not less. IGI doesn't just grade diamonds—it converts subjective assessment into objective reality, transforms stones into assets, and perhaps most importantly, turns doubt into confidence.

That transformation—from uncertainty to trust—might be the most valuable alchemy in business. And in that sense, IGI isn't really in the diamond business at all. It's in the confidence business, selling certainty in an uncertain world, one certificate at a time.

The story of IGI is far from over. But as Blackstone counts its returns and public investors place their bets, one thing is certain: the three-person operation Marcel Lorie started above Antwerp's diamond district in 1975 has become something he could never have imagined—a global trust machine, humming away in laboratories from Surat to New York, quietly underpinning an entire industry's value system.

And perhaps that's the most acquired lesson of all: the biggest opportunities often lie not in the spotlight of consumer brands or the drama of disruption, but in the quiet corners of commerce where trust is manufactured, standards are set, and value is defined. IGI found one of those corners and turned it into an empire. The question now is whether that empire can endure the harsh light of public markets and the relentless march of technological change.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube