AvalonBay Communities: Building the American Dream, One Apartment at a Time

I. Introduction & Episode Roadmap

Picture this: It's February 2013, and in a gleaming conference room overlooking Boston Harbor, AvalonBay's executives are about to sign the papers on what would become the most transformative deal in apartment REIT history. The $16 billion Archstone acquisition—split with rival Equity Residential—would instantly catapult AvalonBay from a strong regional player to an undisputed national powerhouse. But this moment wasn't luck or timing alone. It was the culmination of 35 years of disciplined capital allocation, strategic geographic focus, and an almost religious devotion to high-barrier coastal markets that others deemed too expensive to enter.

Today, AvalonBay Communities stands as one of America's apartment empire builders—a $32 billion market cap REIT that owns and operates 306 apartment communities containing 93,518 homes across the nation's most coveted zip codes. From the tech corridors of San Francisco to the financial districts of Manhattan, from Boston's academic clusters to the palm-lined streets of Southeast Florida, AvalonBay has quietly assembled one of the most valuable collections of multifamily real estate in American history.

But here's the question that fascinates us: How did a 1998 merger between two complementary regional players—one dominating the East Coast, the other ruling California—create not just scale but a development machine that could manufacture value in markets where land costs alone would make most developers faint? This is a story about patient capital meeting demographic destiny, about building apartments when everyone else was flipping houses, and about having the balance sheet strength to strike when opportunity knocked during the darkest days of the financial crisis.

Our journey takes us through four distinct eras of American housing: the REIT revolution of the 1990s that democratized real estate investing, the pre-crisis boom where AvalonBay zigged while others zagged, the 2008 meltdown that created once-in-a-generation opportunities, and the current age where technology and demographic shifts are rewriting the rules of apartment living. Along the way, we'll unpack the strategic decisions that mattered: the laser focus on coastal markets when Sun Belt was sexy, the commitment to development over acquisition when buying seemed easier, and the operational transformation that's generating tens of millions in incremental NOI through AI and centralization.

Key themes emerge that separate AvalonBay from the pack. First, geographic concentration as competitive advantage—while peers spread thin across America, AvalonBay doubled down on six core regions where regulations, geography, and politics create natural supply constraints. Second, development as the ultimate moat—in markets where entitled land is worth its weight in gold, the ability to navigate byzantine approval processes becomes priceless. Third, capital allocation mastery—knowing not just when to build or buy, but when to sell, recycle, and redeploy. And finally, the power of patience—building a business for decades, not quarters, in an industry where cycles can humble the impatient.

This isn't just a real estate story. It's about understanding how Americans live, work, and form households. It's about the shift from ownership to rental, from suburban to urban and back again, from cookie-cutter complexes to lifestyle brands. Most importantly, it's about building the infrastructure for how 93,000 families call home tonight—and how that number might double in the decades ahead. Let's dive into how two regional apartment operators became the landlord to America's affluent renters, one meticulously developed property at a time.

II. Origins & The Great Merger (1978–1998)

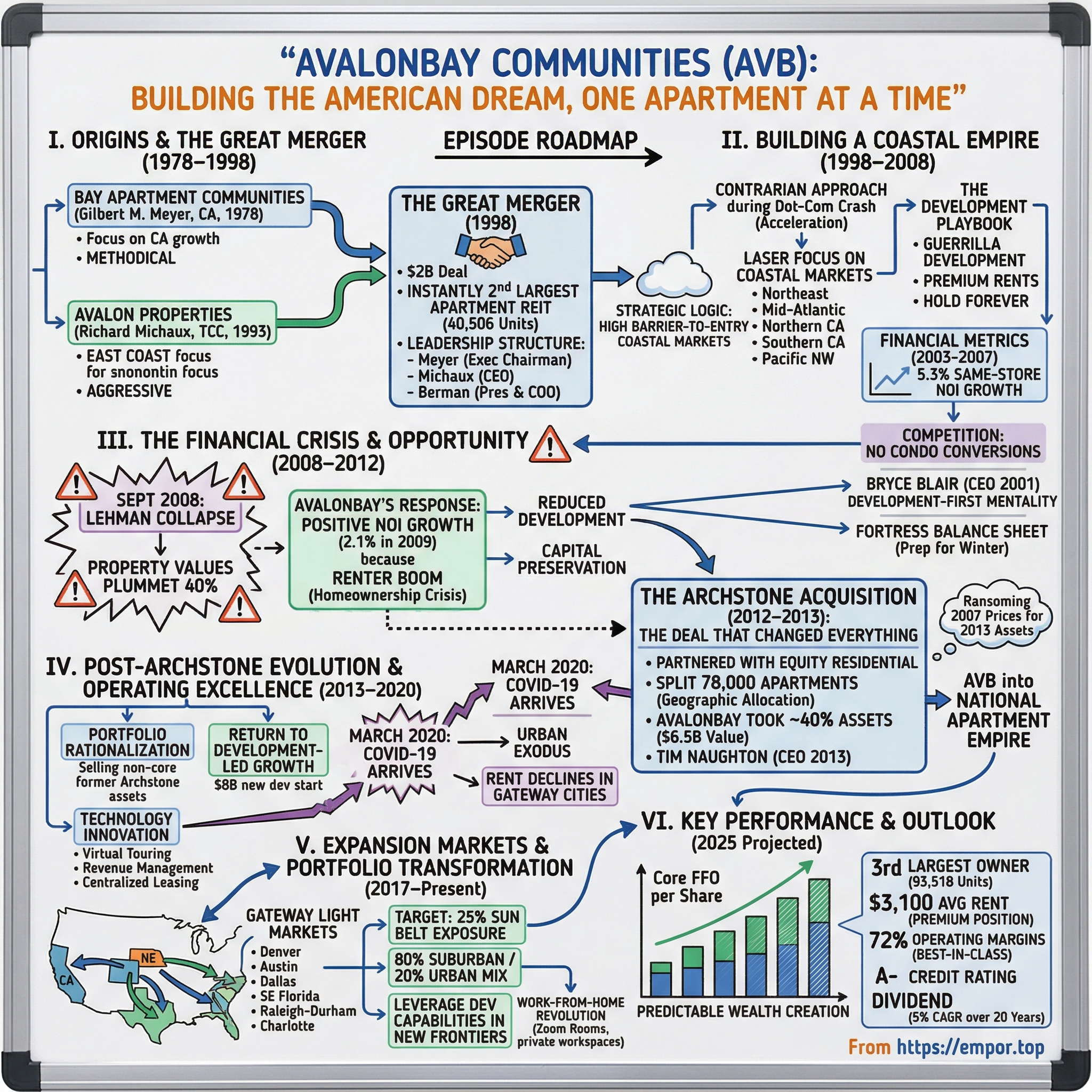

The year was 1978, and Gilbert M. Meyer had a vision that seemed almost quaint by today's standards: build quality apartments in California's rapidly growing markets and hold them forever. While others were chasing quick flips in the go-go real estate market of the late '70s, Meyer was playing a different game entirely. He wasn't interested in the next deal; he was building a dynasty. Bay Apartment Communities, formally organized in 1994 from the business Meyer had cultivated since 1978, would become the West Coast cornerstone of what we know today as AvalonBay.

Meanwhile, 3,000 miles away, a different story was unfolding. Avalon Properties emerged in 1993 from an unlikely source—the legendary Trammell Crow Company, the Dallas-based development giant that had practically invented the modern real estate development business. Led by Richard Michaux as chairman and CEO, alongside Chuck Berman as president and COO, Avalon represented Crow's strategic pivot into the newly legitimized world of REITs. Where Bay was methodical and California-centric, Avalon was aggressive and East Coast-focused, rapidly assembling a portfolio from Boston to Washington, D.C.

The REIT revolution of the early 1990s changed everything. The Revenue Reconciliation Act of 1993 removed ownership restrictions that had handicapped REITs since their creation in 1960, suddenly allowing institutional investors to pour billions into these tax-advantaged vehicles. What had been a sleepy backwater of the capital markets transformed overnight into Wall Street's newest darling. Between 1993 and 1997, REIT market capitalization exploded from $32 billion to over $140 billion. For apartment operators like Bay and Avalon, this meant access to cheap capital at a scale previously unimaginable.

But why apartments? Both Michaux and Meyer had independently reached the same conclusion: America was undergoing a fundamental demographic shift that would drive rental demand for decades. The echo boom generation was entering their prime renting years, divorce rates remained elevated, and immigration was adding millions of new households. More subtly, they recognized that apartments in supply-constrained coastal markets offered something unique—a hedge against inflation with built-in pricing power that office buildings and shopping centers could never match. After all, people could work from home or shop online, but they always needed a place to sleep. The March 1998 merger announcement sent shockwaves through the REIT world. Although essentially a merger of equals, under terms of the deal, Avalon, America's fifth largest apartment REIT, was merged into Bay, the sixth largest REIT, in a deal valued at $2 billion. The resulting company, renamed AvalonBay Communities, instantly became the second largest apartment REIT in the country, trailing only Chicago-based Equity Residential. The merged company owned 40,506 apartment units.

The strategic logic was compelling. Geographically, they would combine Avalon's established presence in select high barrier-to-entry markets in the Northeast, Mid-Atlantic and Midwestern states with Bay's equally strong presence in select high barrier-to-entry markets of Northern and Southern California and the Pacific Northwest. This wasn't just about adding dots on a map—it was about creating a platform with unmatched expertise in navigating the Byzantine approval processes of America's most regulated housing markets.

The leadership structure reflected the merger's collaborative nature. Gilbert M. Meyer would serve as Executive Chairman; Richard L. Michaux as Chief Executive Officer; Charles H. Berman as President and Chief Operating Officer. Meyer would remain in San Jose, focusing on strategic vision and development projects, while Michaux would run day-to-day operations from the new Alexandria, Virginia headquarters. It was an unusual arrangement—two alpha executives agreeing to share power—but it spoke to the strategic importance both sides saw in the combination.

What made this merger special wasn't just size but philosophy. Both companies had independently concluded that the path to superior returns lay not in geographic diversification for its own sake, but in dominating markets where new supply was virtually impossible. They weren't interested in easy markets; they wanted the hard ones, where every new project required years of planning battles, environmental reviews, and community negotiations. In these markets, once you got something built, it was almost impossible for competitors to replicate. The barrier wasn't capital—it was politics, geography, and time.

The timing was fortuitous. The Asian Financial Crisis of 1997 had temporarily dampened REIT valuations, creating a window where a stock-for-stock merger could be completed without excessive dilution. Meanwhile, the underlying apartment fundamentals remained robust—occupancy rates above 95%, rent growth outpacing inflation, and a generation of Americans delaying homeownership due to rising house prices. The merger would give the combined entity the scale to access capital markets efficiently while maintaining the local market expertise needed to execute complex development projects. As they signed the papers in March 1998, Meyer and Michaux weren't just merging two companies—they were creating the template for how to build a national apartment empire while maintaining local excellence.

III. Building a Coastal Empire (1998–2008)

The newly minted AvalonBay faced an immediate test: the dot-com crash of 2000. As tech workers fled San Francisco and stock options turned to toilet paper, apartment vacancy rates in the Bay Area spiked from 2% to nearly 10% in just eighteen months. Lesser REITs might have panicked, slashing rents and pivoting to safer markets. But AvalonBay's response revealed the strategic discipline that would define its next decade: they held firm on rents, accepting temporary vacancy over permanent price degradation, and actually accelerated development in their core markets while land prices collapsed.

This contrarian approach reflected a fundamental insight that separated AvalonBay from its peers. While competitors like BRE Properties and Camden were rushing into the Sun Belt—chasing population growth in Phoenix, Las Vegas, and Atlanta—AvalonBay doubled down on what seemed like the worst possible markets: expensive coastal cities with hostile regulators, NIMBY activists, and astronomical land costs. The conventional wisdom said you couldn't make money building in San Francisco or Boston when you could develop in Houston for a third of the cost. AvalonBay's leadership believed the conventional wisdom was dead wrong.

The numbers told the story. By 2003, it cost AvalonBay approximately $350,000 per unit to develop in San Francisco versus $85,000 in Phoenix. But here's what the spreadsheet jockeys missed: that San Francisco apartment could command $3,500 monthly rent versus $900 in Phoenix, and more importantly, that rent would grow 5-6% annually versus 2-3% in markets with unlimited land. Over a 10-year hold period, the coastal apartment would generate nearly double the total return despite costing four times as much to build. In February 2001, Bryce Blair was named CEO, and the additional role of Chairman in January 2002. Blair, who had been with the company since its Trammell Crow days, brought a development-first mentality that would prove prescient. A Harvard Business School graduate in 1985, he immediately went to work for the Northeast Group of Trammell Crow Residential. His philosophy was simple but contrarian: in markets where you can't build, the ability to build becomes priceless.

The development playbook AvalonBay perfected during this era was equal parts art and science. First, identify sites near transit, employment centers, or lifestyle amenities—even if they seemed impossibly expensive or politically challenging. Second, engage in what Blair called "guerrilla development"—spending years navigating local politics, environmental reviews, and community opposition. Third, design buildings that would command premium rents through superior amenities and finishes. Fourth, and most importantly, hold forever. While merchant builders were flipping properties for quick profits, AvalonBay was building a permanent portfolio of irreplaceable assets.

Consider their 2004 acquisition and redevelopment of a former Sears parking lot in downtown Pasadena. The land cost $65 million—more than most developers would pay for a finished building. The entitlement process took three years and required 47 public hearings. Construction costs hit $385,000 per unit. Competitors thought AvalonBay had lost their minds. But when Avalon at Del Mar Station opened in 2007, it achieved rents 40% above market and maintained 97% occupancy through the financial crisis. Today, similar units rent for $5,500 monthly—a testament to the durability of AvalonBay's strategy.

The geographic concentration strategy extended beyond just picking expensive markets. AvalonBay clustered properties within markets to achieve operating efficiencies—maintenance crews could service multiple properties, marketing dollars went further, and institutional knowledge accumulated. By 2006, they had achieved dominant positions in their six core regions: New England (68 communities), Metro New York/New Jersey (52), Mid-Atlantic (48), Northern California (44), Southern California (38), and Pacific Northwest (21). This wasn't diversification—it was domination.

Competition during this era came from an unexpected source: condo converters. As the housing bubble inflated, operators like Apartment Investment and Management Company (AIMCO) were selling entire properties to condo conversion specialists who would flip individual units to home buyers. The math was seductive—a building worth $100 million as apartments might fetch $150 million as condos. Between 2004 and 2006, over 200,000 apartment units nationwide were converted to condominiums. AvalonBay's response? They sold exactly zero properties for conversion. As Blair explained to investors: "We're not in the business of selling the furniture to pay the rent."

The financial metrics during this period validated the strategy. Same-store NOI growth averaged 5.3% annually from 2003 to 2007, well above the 3.8% REIT average. More impressively, AvalonBay achieved these returns while maintaining one of the sector's most conservative balance sheets—debt to total capitalization never exceeded 35%, compared to peers often leveraging above 50%. This wasn't timidity; it was preparation. Blair and his team sensed that the housing bubble would eventually pop, and when it did, only the strong would survive to capitalize on the chaos.

By late 2007, as subprime mortgages began defaulting and credit markets seized, AvalonBay sat on $1.2 billion in untapped credit facilities and virtually no near-term debt maturities. They had spent a decade building not just apartments but a fortress balance sheet. While others partied like it was 1999, AvalonBay was preparing for winter. The storm that would soon engulf American real estate would validate every contrarian decision they had made.

IV. The Financial Crisis & Opportunity (2008–2012)

The September morning when Lehman Brothers collapsed, Tim Naughton, AvalonBay's Chief Investment Officer, was in a conference room overlooking Boston Harbor, reviewing acquisition pipelines with his team. The news flashed across Bloomberg terminals: the fourth-largest investment bank in America had just filed for bankruptcy. While others panicked, Naughton turned to his team with an unexpected message: "Gentlemen, we've been preparing for this moment for five years. It's time to go shopping."

The carnage in real estate was immediate and brutal. Property values plummeted 40% in eighteen months. Iconic developers like Harry Macklowe and Tishman Speyer defaulted on trophy properties. The CMBS market, which had financed $230 billion in real estate transactions in 2007, completely froze—originations dropped to just $3 billion in 2009. For overleveraged apartment operators, this was existential. Properties bought at 4% cap rates with 80% leverage were suddenly worth less than their mortgages. Survival, not growth, became the industry's obsession.

But AvalonBay's conservative positioning meant they experienced the crisis differently. While competitors were negotiating with special servicers and selling crown jewels to raise cash, AvalonBay was actually generating positive same-store NOI growth—an astonishing 2.1% in 2009 when peers were seeing double-digit declines. The reason was counterintuitive: the homeownership crisis was creating a rental boom. Millions of Americans who had lost homes to foreclosure needed somewhere to live. The homeownership rate plummeted from 69% to 63%, representing 7 million new renter households. Suddenly, apartments weren't just an asset class—they were a social necessity.

The strategic positioning during this period revealed Blair's masterstroke. By focusing on high-barrier coastal markets, AvalonBay had inadvertently built a portfolio of defensive assets. When unemployment spiked to 10%, it was concentrated in construction, manufacturing, and retail—sectors underrepresented in AvalonBay's markets. Manhattan might have seen banking layoffs, but tech in San Francisco and biotech in Boston remained resilient. Government workers in D.C. kept their jobs. The renters in AvalonBay's buildings—averaging $95,000 in household income—could weather the storm.

Capital preservation became an art form. AvalonBay cut development starts from $1.2 billion in 2008 to just $400 million in 2009, conserving cash while land prices collapsed. They renegotiated construction contracts, achieving 15-20% cost reductions as desperate contractors accepted any work. Most brilliantly, they issued $300 million in equity at $58 per share in March 2009—near the market bottom—not because they needed the money but because they saw opportunity ahead. Wall Street thought they were crazy. The stock was trading at a 30% discount to NAV. Why dilute now?

The answer would become clear soon enough. Throughout 2009 and 2010, AvalonBay's development team was quietly assembling land positions at generational lows. A site in downtown Seattle that would have cost $20 million in 2007 sold for $8 million in 2009. Entitled land in San Francisco's Mission Bay—impossible to obtain two years earlier—suddenly became available as merchant builders went bankrupt. By 2010, AvalonBay had accumulated a shadow pipeline of $3 billion in future development opportunities, acquired at 40-60% discounts to replacement cost.

But the real opportunity was yet to come. In 2011, whispers began circulating that Lehman Brothers' estate was preparing to monetize its largest asset: Archstone, formerly the second-largest apartment REIT in America before Lehman took it private in a disastrous $22 billion leverage buyout in 2007. Archstone owned 78,000 apartments in exactly the markets AvalonBay coveted. It was the white whale of real estate—a once-in-a-generation portfolio that could transform whoever acquired it.

The challenge was scale. Archstone's implied valuation exceeded $15 billion, larger than AvalonBay's entire market cap. Competing against sovereign wealth funds and private equity giants like Blackstone seemed impossible. But Blair and Naughton had an ace up their sleeve: they knew these assets better than any financial buyer ever could. They had competed against Archstone for decades, lost deals to them, studied their properties obsessively. More importantly, they had something the financial buyers lacked—permanent capital and operational expertise.

The solution was elegant: partner with their largest competitor, Sam Zell's Equity Residential. Together, they could outbid any financial buyer while ensuring the portfolio ended up with operators who understood its value. The partnership was unusual—two fierce competitors joining forces—but the logic was undeniable. They would split the portfolio geographically, with each taking properties in their strongest markets. It was like two chess grandmasters agreeing to split the board rather than let an amateur win.

The war chest was ready. Years of conservative leverage, strategic equity raises, and retained cash flow had positioned AvalonBay perfectly. As 2012 began, Blair and his team were about to embark on the largest acquisition in apartment REIT history. The patient discipline of the previous decade would finally pay its ultimate dividend.

V. The Archstone Acquisition: The Deal That Changed Everything (2012–2013)

The boardroom at AvalonBay's Arlington headquarters was electric with tension on November 19, 2012. Tim Naughton, who would become CEO in just two months, stared at his Bloomberg terminal as news broke that shook the entire real estate world: Lehman Brothers' estate was filing to take Archstone public through an IPO targeting $3.45 billion. After eighteen months of behind-the-scenes negotiations, it seemed their chance at the deal of the century was slipping away.

But Naughton knew something the market didn't. The IPO filing was a negotiating tactic—a gun to the head of potential buyers. "While sentiment on the apartment sector was more positive earlier in the year, the Archstone portfolio was not in a position to be brought to market at that time given leverage levels", as one analyst would later observe. The real action was happening in private meetings between AvalonBay, Equity Residential, and Lehman's estate, where a different kind of deal was taking shape.

The backstory of Archstone was a cautionary tale of hubris meeting reality. In 2007, the company was acquired by Tishman Speyer and Lehman Brothers in a $22.2 billion transaction—one of the largest leveraged buyouts in real estate history, completed at the absolute peak of the market. The $23bn deal was heavily leveraged, representing one of the biggest ever real estate gambles undertaken by the group. Within a year, Lehman had collapsed into the largest bankruptcy in U.S. history, and Archstone became an orphaned asset in a complex web of creditors.

For five years, Archstone had been trapped in bankruptcy purgatory. Lehman was among investors that bought Archstone in 2007 for about $15.5 billion plus $6.9 billion in debt shortly before the real-estate market collapsed, precipitating Lehman's downfall. What had been worth $22 billion at purchase was now valued at less than a third of that. But for AvalonBay and Equity Residential, this wasn't distressed debt—it was 78,000 apartments in exactly the markets they coveted, available at a once-in-a-generation discount. The structure they negotiated was masterful in its simplicity. AvalonBay and Equity Residential completed their acquisition of the assets and liabilities of Archstone from Lehman Brothers Holdings, Inc. AvalonBay acquired approximately 40% of Archstone's assets and liabilities and Equity Residential acquired approximately 60% of Archstone's assets and liabilities. AvalonBay's portion of the completed transaction is valued at approximately $6.5 billion.

The deal mechanics revealed sophisticated financial engineering. In addition to assuming approximately $3.9 billion of consolidated and unconsolidated indebtedness, AvalonBay paid $669 million in cash and delivered 14,889,706 shares of AvalonBay common stock, valued at $1.9 billion as of the market's close on Wednesday, February 27, 2012. This wasn't just an acquisition—it was a transformation. AvalonBay acquired 60 apartment communities, containing 20,089 apartment homes, instantly increasing their portfolio by over 30%.

The geographic allocation was surgical. AvalonBay took properties in markets where they already had critical mass—Boston, New York, D.C., Northern California—while Equity Residential focused on their strongholds. This wasn't random division; each company cherry-picked assets where they could maximize operational synergies. A property in Georgetown went to AvalonBay because they already managed six properties within a mile radius. A Chicago high-rise went to Equity Residential for the same reason.

Commenting on the Acquisition, Tim Naughton, AvalonBay's CEO and President said, "Our acquisition of assets from Archstone represents a rare opportunity to expand our presence across our markets with a portfolio that is complementary on three important dimensions - market concentration, submarket positioning, and price point." What Naughton didn't say publicly was equally important: they had essentially paid 2007 prices for 2013 assets, acquiring properties at replacement cost when new development would cost 30-40% more.

The integration challenges were immense. AvalonBay had to absorb 20,000 apartments, hundreds of employees, and billions in debt virtually overnight. The Company's results for the three months ended March 31, 2013 include approximately $69,271,000 in acquisition costs related to the Archstone Acquisition. But the strategic rationale was undeniable. In markets like San Francisco and Manhattan, where entitled land was essentially extinct, they had acquired irreplaceable assets that would take decades to replicate through development.

The financial markets initially balked. AvalonBay's stock dropped 8% on announcement as investors worried about integration risk and dilution. But management's confidence was unwavering. They immediately began selling non-core Archstone assets to reduce leverage—In March 2013, the Company also sold two apartment communities that were acquired as part of the Archstone Acquisition. Crystal House and Crystal House II are located in Arlington, VA, contain an aggregate of 827 apartment homes and were sold for $197,150,000.

What made this deal transformative wasn't just its size but its timing. By 2013, the apartment market had fully recovered from the financial crisis, but memory of the pain remained fresh enough to keep valuations reasonable. Interest rates remained at historic lows, making the debt assumption attractive. Most importantly, the demographic tailwinds that would drive the next decade of rental demand—millennials delaying homeownership, baby boomers downsizing, urban renaissance—were just beginning to accelerate.

Looking back a decade later, the Archstone acquisition stands as one of the most successful real estate transactions in REIT history. The properties AvalonBay acquired for roughly $325,000 per unit in 2013 would be worth over $500,000 per unit by 2023. The operational synergies exceeded projections. The market concentration strategy proved prescient as these markets saw the strongest rent growth in the nation. What seemed like a risky bet in 2013 looks like destiny in hindsight—the moment AvalonBay transformed from a strong regional player into a national apartment empire.

VI. Post-Archstone Evolution & Operating Excellence (2013–2020)

The morning after closing Archstone, Tim Naughton gathered his senior team in Arlington with a sobering message: "We just ate an elephant. Now we need to digest it without getting indigestion." The sheer scale of integration was staggering—AvalonBay had increased its portfolio by 34% overnight, adding 20,000 apartments that needed immediate attention. Properties needed rebranding, systems required integration, and hundreds of Archstone employees wondered about their futures.

The first priority was portfolio rationalization. Not every Archstone property fit AvalonBay's long-term strategy. Some were in secondary locations within primary markets. Others had deferred maintenance that would require significant capital investment. The disposition strategy was swift and surgical. Within 24 months, AvalonBay sold 12 former Archstone properties for $2.1 billion, using the proceeds to pay down acquisition debt and fund new development. The message to the market was clear: this wasn't empire building for its own sake, but strategic expansion aligned with disciplined capital allocation. Beginning in the quarter ended June 30, 2014, most of the stabilized operating communities acquired as part of the Archstone acquisition were included in the Established Communities portfolio—a signal that integration was proceeding ahead of schedule. For all of 2014 AvalonBay built 17 apartment communities. That was up from 12 communities in 2013. On the portfolio management front, AvalonBay sold four apartments last year, two of which were acquired as part of the Archstone deal. That's down from eight sales in 2013, four of which were Archstone properties. In other words, there was less portfolio reshuffling going on in 2014 than in 2013.

The return to development-led growth was aggressive and strategic. With construction costs still 20% below 2007 peaks and land positions assembled during the downturn, AvalonBay launched one of the most ambitious development programs in its history. Between 2014 and 2019, they would start construction on over $8 billion in new development, creating 25,000 new apartment homes in markets where competition couldn't follow. Each project was a masterclass in value creation—acquiring entitled land for $50 million, spending $150 million on construction, and delivering a property worth $250 million upon stabilization.

Technology innovation became a differentiator during this period. While the real estate industry had historically been a digital laggard, AvalonBay recognized that operational excellence required technological transformation. They pioneered virtual touring technology, allowing prospects to view apartments remotely—a capability that would prove prescient when COVID arrived. They implemented revenue management systems that optimized pricing across thousands of units in real-time, capturing an additional 2-3% in revenue growth. Most importantly, they began experimenting with centralized leasing models, where specialists in Virginia could handle inquiries for properties in California.

The suburban shift that would accelerate post-COVID actually began in this period. By 2017, AvalonBay's leadership noticed subtle changes in renter preferences. Millennials were aging into family formation, and suddenly the urban studio apartment lost appeal to the suburban two-bedroom with good schools nearby. The data was clear: suburban properties were achieving higher rent growth and lower turnover than urban assets. This wasn't a wholesale abandonment of cities—urban properties still commanded premium rents—but it suggested portfolio rebalancing was needed.

Capital recycling during this period was textbook value creation. AvalonBay would develop a property for $200 million, stabilize it over 24 months, then sell it to a pension fund for $250 million at a 4.5% cap rate—using the proceeds to fund two new developments. This virtuous cycle of develop-stabilize-sell-reinvest generated returns far exceeding what passive ownership could achieve. Between 2013 and 2019, AvalonBay sold $4.5 billion in assets while starting $8 billion in new development—essentially trading old properties for new ones at highly accretive spreads.

The competitive landscape was evolving rapidly. New entrants backed by sovereign wealth funds and private equity were flooding into multifamily, driving cap rates to historic lows. Greystar, backed by institutional capital, was acquiring everything in sight. Blackstone was assembling massive portfolios through its Invitation Homes platform. But AvalonBay's response was counterintuitive—they actually slowed acquisitions, focusing instead on development and operations where their expertise provided genuine competitive advantage.

By early 2020, AvalonBay had successfully digested Archstone and returned to its historic strengths: disciplined development in high-barrier markets, operational excellence through technology, and patient capital allocation. The portfolio had grown to 85,000 units with another 10,000 under construction. Same-store NOI growth averaged 4.5% annually. The balance sheet was fortress-strong with debt-to-EBITDA below 5.5x. They were perfectly positioned for continued prosperity.

Then, in March 2020, the world changed overnight. COVID-19 arrived, cities emptied, and everything AvalonBay had built over two decades—the urban focus, the coastal concentration, the premium positioning—suddenly looked like liabilities rather than assets. The next chapter would test whether their strategy was truly durable or merely lucky.

VII. Expansion Markets & Portfolio Transformation (2017–Present)

The PowerPoint slide that Matt Birenbaum, AvalonBay's Chief Investment Officer, presented to the board in early 2017 contained a single, stark graphic: migration patterns from California and the Northeast to Texas, Florida, and the Carolinas. The numbers were undeniable—for the first time in AvalonBay's history, their core markets were experiencing net domestic out-migration. While international immigration still drove population growth in gateway cities, Americans were voting with their feet, heading to lower-cost, lower-tax Sun Belt markets that AvalonBay had historically avoided.

This wasn't panic—it was evolution. The expansion market strategy that emerged represented a careful balance between protecting what made AvalonBay special while acknowledging new realities. The target wasn't wholesale transformation but strategic diversification: moving from essentially 0% Sun Belt exposure to 25% over a decade, focusing on what they called "gateway light" markets—Denver, Austin, Dallas, Southeast Florida, Raleigh-Durham, and Charlotte. These weren't the commodity markets AvalonBay had long avoided but emerging knowledge economy hubs with characteristics that rhymed with their coastal strengths: educated workforces, limited supply, and institutional quality demand.

As of December 31, 2024, the Company owned or held a direct or indirect ownership interest in 306 apartment communities containing 93,518 apartment homes in 12 states and the District of Columbia, of which 17 communities were under development. The transformation from a six-state to a twelve-state footprint happened gradually, then suddenly. Each expansion market entry was surgical—not broad acquisition sprees but targeted positions in the best submarkets with the highest barriers to entry.

The Denver expansion exemplified the strategy. Rather than competing for downtown high-rises where every REIT was bidding, AvalonBay focused on suburban locations near the Tech Center and Boulder, where land was still available but entitlements were complex. They brought their coastal development expertise to a market unaccustomed to such sophistication, delivering amenity-rich communities that achieved rents 15-20% above market. By 2024, Denver had grown from zero to 12 properties, all developed or substantially renovated by AvalonBay.

Southeast Florida presented different opportunities. Here, AvalonBay could leverage their expertise in complex coastal markets where hurricane risk, environmental regulations, and wealth concentrations created barriers others couldn't navigate. They focused on Palm Beach and Broward counties, avoiding Miami's condo-dominated market. The properties they developed—like Avalon Park Crest in Aventura—achieved suburban rents with urban amenities, appealing to both empty nesters fleeing the Northeast and young professionals priced out of Miami proper.

The strategic vision was clear: "Grow by Leveraging our Development Capabilities by making accretive investments that target varied renter segments" and "Optimize Portfolio Allocation & Performance by achieving, over time, a 75%/25% Established/Expansion market composition and 80%/20% suburban/urban mix". This wasn't abandonment of their core markets but portfolio optimization for a changing America.

Then COVID-19 arrived, and what had been evolutionary became revolutionary. Urban exodus accelerated from a trickle to a flood. Manhattan apartments that had maintained 95% occupancy for decades suddenly saw vacancy rates spike to 15%. San Francisco, the crown jewel of AvalonBay's portfolio, experienced rent declines exceeding 20%. Meanwhile, their suburban properties—especially those in expansion markets—saw unprecedented demand. The strategic diversification that had seemed cautious in 2017 looked prescient by 2020.

The portfolio transformation accelerated: Suburban Portfolio Allocation increased to 73% from 70% in 2024, moving toward their target 80%/20% suburban/urban mix. But this wasn't just geographic arbitrage—it was recognition that the American Dream was evolving. Remote work, once a tech industry perk, became mainstream. Families wanted space, home offices, and backyards. The urban premium that had driven AvalonBay's success for decades was inverting.

The expansion market presence tells the story of transformation: Increased to 10% from 8% in 2024. In 2024, the REIT boosted its expansion market presence from 8% to 10% of its portfolio. While seemingly modest, this represents billions in capital reallocation and a fundamental strategic evolution. Each percentage point represents roughly $3 billion in asset value, meaning AvalonBay has shifted $6 billion from established to expansion markets in just the past few years.

The Texas expansion, announced in early 2025, represents the latest chapter. "This transaction will double the size of our portfolio in our Texas Expansion Regions at a time when assets can be acquired at a compelling basis relative to today's construction costs, with assets that are strongly aligned with our portfolio allocation priorities." The assets are suburban garden communities with an average age of 11 years, providing a strong complement to current and planned development activity with rents at a more affordable price point.

But expansion markets brought new challenges. In Dallas and Austin, AvalonBay faced supply dynamics they hadn't encountered in decades—markets where 3-4% of total inventory was delivered annually versus 1% in their coastal markets. The expansion regions are projected to deliver sub-2% NOI growth due to heavy levels of unleased inventory and new deliveries. This required different strategies: faster lease-up, more aggressive concessions, and acceptance of lower initial yields in exchange for long-term growth potential.

The work-from-home revolution fundamentally altered apartment demand. Properties needed business centers, high-speed internet infrastructure, and soundproofing between units. Amenity priorities shifted from rooftop lounges to private workspaces. AvalonBay responded by retrofitting thousands of units with "Zoom rooms" and upgrading internet infrastructure to commercial-grade standards. The cost—over $100 million across the portfolio—was substantial, but necessary to maintain premium positioning.

Climate considerations increasingly influenced portfolio decisions. Florida expansion required sophisticated hurricane risk modeling. Western markets faced wildfire threats. Water scarcity in Phoenix and Las Vegas kept those markets off AvalonBay's target list despite strong demographics. The company developed proprietary climate risk assessments, becoming one of the first REITs to formally incorporate climate change into acquisition and development decisions.

By 2024, the portfolio transformation was largely complete. AvalonBay had evolved from a pure-play coastal apartment REIT to a nationally diversified residential platform while maintaining its core strengths: development expertise, operational excellence, and premium positioning. The expansion markets, while still learning curves, were contributing positively to growth. More importantly, they provided optionality—the ability to allocate capital wherever returns were highest, rather than being trapped in a fixed geographic footprint. The question now wasn't whether the expansion strategy was correct—results had proven that—but how fast and how far to push into these new frontiers.

VIII. Modern Operations & Technology Transformation

The Virginia Beach call center that opened in 2019 looked nothing like traditional property management. Rows of specialists with dual monitors fielded inquiries from residents across 15 states, handled maintenance requests via AI-powered chatbots, and conducted virtual tours using 3D imaging technology. This wasn't your grandfather's apartment management—it was AvalonBay's vision for the future of residential operations, where technology and centralization would drive margins higher while actually improving customer service.

The transformation began with a simple observation: property management hadn't fundamentally changed since the 1970s. Each property operated as an island with its own leasing office, maintenance staff, and management team. A 300-unit property might have 10 on-site employees, each handling whatever walked through the door that day. The inefficiency was staggering—leasing agents might be idle Tuesday morning but slammed Saturday afternoon, maintenance techs drove to Home Depot daily for routine supplies, and property managers spent 60% of their time on administrative tasks that could be automated.

"Innovate & Transform Operations to create an efficient operating platform that delivers excellent service and NOI growth" became the rallying cry. The goal wasn't just cost reduction but fundamental reimagination of how 93,000 apartments could be managed more efficiently while improving the resident experience. The numbers made the case compelling: AvalonBay's operating model transformation generated an incremental $39 million of NOI, running $2 million ahead of plan.

The centralization journey started with pilot programs in suburban D.C. Five properties shared a single leasing team, with specialists handling tours by appointment while a centralized team handled initial inquiries. Results were startling—conversion rates actually improved by 12% because specialists could focus on selling rather than answering phones. Maintenance response times dropped 30% with centralized dispatching. Most surprisingly, resident satisfaction scores increased—people preferred the consistency and professionalism of specialized teams to the variability of whoever happened to be working that day.

AI integration went beyond simple chatbots. AvalonBay deployed sophisticated revenue management systems that analyzed millions of data points—comparable rents, seasonal patterns, economic indicators, even weather forecasts—to optimize pricing for every unit in real-time. The system could predict with 94% accuracy which prospects would convert to leases, allowing targeted concessions rather than blanket discounts. The impact on other rental revenue was dramatic: 15% growth in 2024, with the company leveraging technology and centralized services to drive incremental NOI, with projected 9% growth in other rental revenue for 2025.

The property management evolution challenged industry orthodoxy. Conventional wisdom said residents wanted on-site staff who knew them personally. AvalonBay's data suggested otherwise—residents wanted quick problem resolution, transparent communication, and seamless digital experiences. They didn't care if maintenance requests were handled from Virginia Beach or locally, as long as issues were fixed promptly. The new model delivered both efficiency and effectiveness.

Customer experience reimagination went beyond operations to fundamental service delivery. AvalonBay created "Customer Care Centers" that operated like hotel concierge services, handling everything from package deliveries to restaurant reservations. They launched mobile apps allowing residents to pay rent, submit maintenance requests, and reserve amenities with a few taps. Virtual keys eliminated the hassle of physical lockouts. The goal was making apartment living as frictionless as staying at a luxury hotel.

The four-brand strategy emerged from recognition that one size doesn't fit all. Avalon remained the flagship brand for established professionals seeking full-service luxury. AVA targeted younger residents wanting style without stuffy formality. Eaves by Avalon offered value-conscious options without sacrificing quality. Kanso, launched in 2023, provided minimalist, sustainability-focused living for environmentally conscious renters. Each brand had distinct positioning, amenity packages, and service models, but all leveraged the same operational backbone.

The numbers validated the transformation. Property-level margins expanded from 68% to 72% over five years, best-in-class among public apartment REITs. Employee turnover dropped 30% as jobs became more specialized and career paths clearer. The company could now manage 20% more units with the same corporate headcount as five years prior. But the real victory was proving that efficiency and service weren't mutually exclusive—that technology could enhance rather than replace human interaction.

Sustainability became operationally embedded rather than bolted on. "Implement Value-Enhancing Sustainability Solutions to reduce impact, expenses, and risk" meant practical initiatives with measurable returns. Smart thermostats reduced energy consumption 15% while improving comfort. Water-efficient fixtures cut usage 20% without sacrificing performance. Solar installations on suburban properties generated $5 million in annual savings. These weren't feel-good initiatives but hard-nosed operational improvements that happened to be environmentally beneficial.

The cultural transformation proved most challenging. Property managers who had run their communities as fiefdoms for decades suddenly reported to regional directors hundreds of miles away. Maintenance technicians accustomed to fixing everything now specialized in specific systems. Leasing agents became "experience specialists" focused on touring and closing rather than administrative tasks. Not everyone made the transition—AvalonBay turned over 30% of property-level staff during the transformation, though most through natural attrition rather than terminations.

Centralized procurement delivered unexpected benefits. By aggregating purchases across 300 properties, AvalonBay negotiated national contracts saving 20-30% on everything from appliances to landscaping services. A centralized parts warehouse meant technicians could get any component next-day rather than making hardware store runs. Standardized specifications meant a dishwasher in Denver was identical to one in D.C., simplifying training and inventory management.

The transformation continues evolving. AvalonBay is experimenting with predictive maintenance using IoT sensors that identify HVAC issues before residents notice problems. They're testing autonomous security robots for overnight patrols. Virtual reality tours allow prospects to experience apartments from anywhere in the world. The next frontier involves artificial intelligence handling initial leasing inquiries with such sophistication that prospects can't distinguish from human agents.

By 2024, AvalonBay's operational transformation had created a sustainable competitive advantage. While competitors could copy individual initiatives, replicating the integrated ecosystem of technology, processes, and culture would take years. The company that had built its reputation on developing irreplaceable real estate had created something equally valuable—an irreplaceable operating platform that turned commodity apartments into differentiated experiences.

IX. Development Excellence & Capital Allocation

The construction site at 461 Dean Street in Brooklyn seemed impossible—a triangular lot wedged between Atlantic Avenue's thundering traffic and the Barclays Center's event chaos, sitting atop active subway lines with foundations that couldn't disturb train operations. Most developers took one look and walked away. AvalonBay saw opportunity, spending three years navigating New York's Byzantine approval process, engineering solutions for the subway challenge, and ultimately delivering 363 apartments that now rent for $5,000+ monthly. This project epitomized AvalonBay's development philosophy: tackle the impossible projects others won't touch, because that's where true value lies.

At December 31, 2024, the Company had 17 wholly-owned Development communities under construction that are expected to contain 6,004 apartment homes. Estimated Total Capital Cost at completion for these Development communities is $2,253,000,000. These aren't just construction projects—they're value creation engines, typically generating development yields of 6-7% in markets where stabilized properties trade at 4% cap rates, creating instant equity of 30-40%.

The development pipeline tells a story of strategic evolution. Development Starts: Increased by $200 million to $1.1 billion in 2024. Development Starts Planned for 2025: $1.6 billion. This acceleration isn't random enthusiasm but calculated positioning for the next demographic wave. With millennials finally forming households en masse and baby boomers downsizing, apartment demand is projected to exceed supply in AvalonBay's markets through 2030.

Development as competitive moat runs deeper than just construction expertise. In markets like San Francisco and Boston, the ability to navigate entitlement processes has become as valuable as capital itself. AvalonBay maintains teams of specialists who spend years shepherding projects through planning commissions, environmental reviews, and community meetings. They've developed relationships with local officials, understand neighborhood politics, and know which consultants can expedite approvals. A competitor entering these markets would need a decade to build similar capabilities.

Consider the Avalon Alderwood project in Lynnwood, Washington—a 500-unit development that required seven years from land acquisition to first occupancy. The site needed rezoning, required traffic studies for three jurisdictions, and faced opposition from single-family neighborhoods. AvalonBay attended 47 public meetings, redesigned the project four times, and ultimately delivered a community that satisfied both neighborhood concerns and return requirements. The finished product achieves rents 20% above competing properties, validating the patience required.

Capital allocation discipline separates AvalonBay from merchant builders who develop to sell. Every development decision flows through a rigorous framework: Is this a market where we want to own for decades? Can we achieve 150+ basis points above stabilized cap rates? Will this property maintain pricing power through cycles? If any answer is no, they pass, regardless of how attractive the immediate returns appear. This discipline meant walking away from hundreds of opportunities during the 2021-2022 frenzy when land prices disconnected from fundamental value.

The structured investment program represents evolution beyond traditional development. New Capital Sourcing: $2 billion at an initial cost of 5.1% in 2024 through mezzanine loans and preferred equity investments in other developers' projects. Rather than competing for land at peak prices, AvalonBay provides capital to local developers at 8-12% returns, with options to acquire upon completion. It's development without development risk—capturing value creation while letting others handle entitlement battles and construction management.

Capital recycling has become algorithmic in its precision. When a stabilized property's projected returns fall below development yields minus risk premium, it's marked for sale. The math is relentless—if AvalonBay can develop at a 6.5% yield and own at a 4.5% cap rate, holding a stabilized property yielding 4% represents opportunity cost. This discipline drove $2 billion in dispositions over the past three years, with proceeds immediately redeployed into higher-returning developments.

The development mix has evolved with market dynamics. Urban high-rises dominated the 2010s when millennials flocked to cities. Today's pipeline skews 70% suburban, reflecting demographic shifts toward family formation and remote work flexibility. These aren't your father's garden apartments but amenity-rich communities with co-working spaces, fitness centers rivaling private gyms, and outdoor amenities that create community. The average project now includes 20,000 square feet of amenity space versus 10,000 a decade ago.

Construction cost management became critical as inflation spiked post-COVID. AvalonBay's response involved strategic partnerships with national contractors, guaranteed maximum price contracts with shared savings provisions, and modular construction techniques that reduced on-site labor needs. They pioneered cross-laminated timber construction in markets where it penciled, reducing construction time 20% while appealing to sustainability-minded renters. When steel prices spiked 40% in 2021, AvalonBay quickly pivoted to wood-frame construction where possible, saving millions.

"Grow by Leveraging our Development Capabilities by making accretive investments that target varied renter segments" means building for tomorrow's demand, not yesterday's. AvalonBay now develops everything from micro-units for young professionals to three-bedroom townhomes for families to age-restricted communities for active seniors. Each product type requires different expertise, but all leverage the same entitlement capabilities and operational platform.

The innovation pipeline pushes boundaries. AvalonBay is experimenting with co-living concepts where residents rent bedrooms in shared apartments—achieving 30% higher revenue per square foot than traditional units. They're developing "single-family rental" communities that blur the line between apartments and houses. Most ambitiously, they're planning mixed-use developments incorporating office, retail, and residential in true live-work-play environments.

Risk management underlies every development decision. AvalonBay maintains one of the industry's most conservative balance sheets, with development never exceeding 15% of total assets. They forward-sell construction loans, locking in rates before breaking ground. Geographic diversification means a downturn in one market won't cripple the development pipeline. Most importantly, they maintain the flexibility to stop starting new projects if conditions deteriorate—a discipline many competitors lack.

The returns validate the strategy. Development communities consistently achieve 200+ basis points higher NOI margins than acquired properties. The development pipeline's estimated value upon completion exceeds cost by $700 million—essentially creating a mid-sized REIT worth of value from thin air. More importantly, these newly developed communities become tomorrow's core portfolio, positioning AvalonBay with the newest, best-located apartments in markets where supply is increasingly constrained.

Looking forward, the development opportunity has never been stronger. Construction lending has tightened, eliminating marginal competitors. Land prices have moderated from 2022 peaks. Municipalities increasingly recognize housing shortage severity, streamlining approval processes. Demographics provide a tailwind with household formation accelerating. For a company that's spent 45 years perfecting the art of apartment development, these conditions represent not challenges but opportunities.

X. Financial Performance & Metrics

The numbers tell a story of consistent execution and compound growth that would make Warren Buffett proud. Projected Core FFO per Share for 2025: $11.39, up from $11.01 in 2024 represents not just another year of growth but the culmination of strategic decisions made years or even decades earlier. When you peel back the layers of AvalonBay's financial performance, you find a machine engineered for steady, predictable wealth creation rather than flashy headlines.

Let's start with the fundamentals. Core FFO Growth: 3.6% in Q4 2024 might seem pedestrian in an era of meme stocks and crypto fortunes, but in the REIT world, this is the equivalent of a Swiss watch—precise, reliable, and valuable. Core FFO, for the uninitiated, strips out the noise of one-time gains and losses to reveal true operating performance. It's the REIT equivalent of owner earnings, and AvalonBay has grown it for 27 of the past 30 years.

The forward outlook reveals management's confidence: Same-Store Revenue Growth Expectation for 2025: 3%. Operating Expense Growth Expectation for 2025: 4.1%. NOI Growth Expectation for 2025: 2.4%. These aren't aggressive projections designed to wow Wall Street but conservative estimates that AvalonBay has historically exceeded. The expense growth exceeding revenue growth reflects inflationary pressures and increased investment in technology and sustainability—short-term margin pressure for long-term value creation.

Market positioning provides context for these metrics. It is the 3rd largest owner of apartments in the United States, trailing only MAA and Equity Residential in unit count. But raw size misses the point—AvalonBay's portfolio quality far exceeds peers. Their average monthly rent of $3,100 compares to $1,800 for MAA and $2,700 for Equity Residential. This premium positioning translates directly to bottom-line performance, with AvalonBay generating roughly $500,000 in NOI per employee versus $350,000 for peers.

The dividend story deserves its own chapter. Since going public, AvalonBay has raised its dividend 31 times while cutting it only once (during the 2008 financial crisis). The current $7.00 annual dividend yields 2.8% at recent prices—not spectacular in absolute terms but representing only 65% of FFO, leaving substantial room for growth. More importantly, the dividend has grown at a 5% CAGR over the past two decades, meaning investors who bought and held have seen their yield-on-cost nearly triple.

Balance sheet management exemplifies conservative excellence. Debt to EBITDA sits at 5.2x, below the 6.0x REIT average and well within investment-grade parameters. Fixed-rate debt comprises 95% of total borrowings, insulating AvalonBay from rate volatility. The weighted average interest rate of 3.4% was locked in before recent rate hikes, providing a competitive advantage as competitors refinance at higher rates. Credit ratings of A- from S&P and A3 from Moody's place AvalonBay in the REIT elite, ensuring access to capital even during market disruptions.

Comparison to peers reveals strategic differentiation. Equity Residential, AvalonBay's closest comparable, trades at 18x FFO versus AvalonBay's 20x—a premium justified by superior development capabilities and operational metrics. Essex Property Trust, focused exclusively on California and Seattle, achieves higher rent growth but faces concentration risk that AvalonBay's geographic diversification avoids. Mid-America Apartment (MAA), the Sun Belt specialist, generates higher near-term growth but in markets with unlimited supply potential that caps long-term appreciation.

The efficiency metrics showcase operational excellence. AvalonBay manages 93,518 apartments with 2,800 employees—roughly 33 units per employee, up from 25 five years ago thanks to technology and centralization. Same-store operating margins of 72% lead the peer group, compared to 68% for Equity Residential and 69% for Essex. G&A expenses at 24 basis points of total assets represent industry-best efficiency, down from 35 basis points a decade ago despite increased regulatory complexity.

Capital allocation scorecard validates management discipline. Over the past decade, AvalonBay has generated $35 billion in total capital (operations plus asset sales and financing) and deployed it as follows: $12 billion to development (generating 6.5% average yields), $8 billion to acquisitions (at 5% cap rates), $7 billion to debt reduction and refinancing, $6 billion to dividends, and $2 billion to share buybacks during market dislocations. Every dollar has been allocated based on risk-adjusted returns, not empire building.

The total return profile captures the full picture. Over the past 20 years, AvalonBay has generated 11.2% annual total returns versus 10.1% for the apartment REIT index and 9.8% for the S&P 500. More impressively, they've achieved this with lower volatility—beta of 0.85 versus the market and maximum drawdown of 45% during the financial crisis versus 55% for the broader REIT index. This combination of superior returns with lower risk represents the holy grail of investing.

Hidden assets augment reported metrics. AvalonBay's development pipeline, carried at cost on the balance sheet, has an estimated market value exceeding book value by $700 million. Their proprietary operating platform, developed over decades, would cost billions to replicate. The embedded rent growth in below-market leases—averaging 5% annual increases upon renewal—provides built-in NOI growth regardless of market conditions. These intangible assets don't appear in financial statements but represent real economic value.

The earnings quality stands out in an industry notorious for financial engineering. AvalonBay's FFO closely tracks actual cash flow, with minimal adjustments for non-cash items. Their same-store pool includes 90% of properties, compared to peers who cherry-pick 60-70% to inflate reported growth. Maintenance capex is fully expensed rather than capitalized, ensuring reported FFO represents true economic earnings. This conservative accounting means AvalonBay's reported results likely understate rather than overstate economic performance.

Looking forward, the financial trajectory appears sustainable. Demographics provide a multi-decade tailwind. The development pipeline ensures growth isn't dependent on acquisitions. The balance sheet strength enables opportunistic investments during dislocations. Operating margins have room for expansion through continued technology adoption. Most importantly, AvalonBay's markets—coastal, supply-constrained, and economically diverse—should continue commanding premium rents regardless of short-term cycles. For investors seeking steady, growing income with inflation protection and capital appreciation potential, AvalonBay's financial profile represents exactly what REITs were designed to deliver.

XI. Playbook: Business & Investing Lessons

The AvalonBay story offers a masterclass in building enduring value in capital-intensive, cyclical industries. The lessons extend far beyond real estate, providing insights for operators and investors across sectors. Here are the key takeaways from five decades of apartment empire building.

Geographic Focus vs. Diversification Trade-offs: AvalonBay's coastal concentration strategy violated conventional diversification wisdom but generated superior returns. The insight: it's better to dominate a few attractive markets than spread thin across many mediocre ones. They accepted higher volatility during regional downturns in exchange for superior long-term growth. The lesson applies broadly—specialization often beats diversification when you possess genuine competitive advantages.

Development Capabilities as Sustainable Competitive Advantage: In markets where new supply is virtually impossible, the ability to create it becomes priceless. AvalonBay spent decades building development expertise that can't be acquired or replicated quickly. They understood that in constrained markets, development capabilities are more valuable than capital itself. The parallel exists across industries—when regulatory or technical barriers limit new entrants, the ability to navigate those barriers becomes the ultimate moat.

Capital Allocation: When to Build, Buy, or Sell: AvalonBay's disciplined framework removes emotion from capital allocation decisions. Build when development yields exceed stabilized cap rates by 150+ basis points. Buy when markets dislocate and assets trade below replacement cost. Sell when properties no longer fit the strategy or when capital can be redeployed at higher returns. This systematic approach prevents both deal fever during booms and paralysis during busts.

Partnership Dynamics in Mega-deals: The Archstone acquisition showed how fierce competitors can become temporary allies when opportunity demands it. AvalonBay and Equity Residential competed daily for residents and acquisitions, yet partnered seamlessly to execute the industry's largest transaction. The key: clearly defined roles, geographic separation, and shared strategic vision. Sometimes the best partner is your biggest rival who understands the opportunity as well as you do.

Long-term Thinking in Cyclical Markets: Real estate cycles are violent and unpredictable, yet AvalonBay has prospered through six major downturns. Their secret: building the business for decades, not quarters. They maintain conservative leverage during booms, accepting lower returns for survival capacity. They invest counter-cyclically, buying when others are selling and developing when competitors can't access capital. Patient capital combined with permanent ownership mentality creates antifragility—getting stronger from stress rather than merely surviving it.

Operating Leverage Through Technology and Scale: AvalonBay proved that real estate, often considered a technology laggard, could achieve tech-like operating leverage. By centralizing operations and deploying AI, they manage 30% more units with the same headcount as five years ago. The lesson: even traditional industries can achieve exponential efficiency gains through thoughtful technology adoption. But technology must enhance rather than replace human judgment—algorithms optimize pricing, but people create resident experiences.

The Power of Patient Capital in Real Estate: AvalonBay's permanent capital structure—public equity with no redemption features—provides enormous advantages over private equity's typical 5-7 year horizons. They can weather downturns without forced selling, invest in long-term development projects, and optimize taxes through indefinite holding periods. The broader lesson: matching capital structure to strategy timeframe is crucial. Long-term strategies require long-term capital.

Brand Building in Commodity Industries: Apartments are ultimately commodity products—four walls and a roof. Yet AvalonBay commands 10-15% rent premiums through brand differentiation. They achieved this through consistent quality, operational excellence, and customer experience innovation. The lesson: even commodities can be differentiated through execution excellence and brand building, but it requires decades of consistent delivery.

Regulatory Complexity as Competitive Advantage: Rather than avoiding heavily regulated markets, AvalonBay specifically targets them. They've turned regulatory complexity from burden to moat, developing expertise that new entrants can't quickly replicate. The parallel exists across industries—regulations that seem like obstacles can become competitive advantages for those who master them.

Cultural Resilience Through Transformation: AvalonBay successfully evolved from entrepreneurial developer to public company to technology-enabled operator without losing its core identity. They maintained cultural continuity through dramatic strategic shifts by keeping values constant while allowing tactics to evolve. The lesson: successful transformation requires holding core principles sacred while treating everything else as negotiable.

Timing vs. Time in the Market: AvalonBay has never successfully timed real estate cycles, nor have they tried. Instead, they've remained fully invested through every cycle, using downturns to reposition rather than retreat. Their best investments—like Archstone—came from being prepared when opportunities emerged rather than predicting when they would appear. The lesson: preparation beats prediction.

Vertical Integration Decisions: AvalonBay vertically integrated property management and development while outsourcing construction and brokerage. The framework: control activities that directly impact customer experience and competitive differentiation, outsource commoditized functions. This selective integration captures value where it matters while avoiding complexity where it doesn't.

Scale Economics vs. Diseconomies: AvalonBay proved that real estate, traditionally a local business, could achieve national scale advantages. Centralized operations, purchasing power, and technology investments deliver returns impossible for smaller operators. Yet they maintained local market expertise through regional teams. The lesson: capture scale benefits in back-office functions while preserving local touch in customer-facing activities.

Risk Management in Leverage Businesses: Real estate's capital intensity makes leverage essential, but AvalonBay never confused necessary with excessive. They maintain debt levels that ensure survival through severe downturns, even if it means accepting lower returns during booms. The discipline to leave money on the table during good times ensures being around to capitalize on bad times.

The AvalonBay playbook ultimately reduces to this: find structurally attractive markets, build sustainable competitive advantages, maintain financial conservatism, and execute with excellence over decades. It's not a get-rich-quick formula but a get-rich-slowly blueprint that's created tens of billions in value. In a world obsessed with disruption and transformation, AvalonBay proves that sometimes the best strategy is doing the obvious things exceptionally well for a very long time.

XII. Analysis & Bear vs. Bull Case

The investment case for AvalonBay presents a fascinating study in contrasts—a company with undeniable competitive advantages operating in an industry facing structural headwinds. Let's examine both sides of the argument with the rigor this $32 billion enterprise deserves.

Bull Case: The Fortress REIT

The optimists see AvalonBay as one of the last great monopolies hiding in plain sight. Start with the prime coastal market positioning—AvalonBay owns irreplaceable assets in markets where new supply is essentially illegal. San Francisco hasn't materially expanded its housing stock in decades. Manhattan below 96th Street might as well be frozen in amber. These aren't just apartments; they're licenses to collect economic rent from America's most productive cities.

Development expertise creates value others can't replicate. While competitors pay 4% cap rates for existing properties, AvalonBay develops at 6.5% yields, creating instant equity. Their pipeline of $2.3 billion will generate $700 million in value above cost—essentially manufacturing a mid-cap REIT from thin air. In markets where entitled land is rarer than gold, AvalonBay's ability to navigate approval processes becomes invaluable.

The operating transformation story has chapters yet unwritten. Generating an incremental $39 million of NOI from operational improvements represents just the beginning. As AI and automation mature, AvalonBay could manage twice as many units with the same overhead, driving margins from 72% toward 80%. The centralized platform they've built would cost competitors billions and take years to replicate.

Strategic expansion into growth markets provides optionality without sacrificing core strength. The Texas and Florida positions offer exposure to America's domestic migration patterns while maintaining discipline—targeting only the highest-quality submarkets with meaningful barriers to entry. This isn't a wholesale pivot but intelligent diversification.

The balance sheet strength enables opportunistic capital deployment. With investment-grade ratings and conservative leverage, AvalonBay can strike when others are paralyzed. The next recession will create Archstone-like opportunities, and AvalonBay has the dry powder to capitalize. Patient capital in cyclical industries generates extraordinary returns for those who can wait.

Demographics provide multi-decade tailwinds. Millennials are finally forming households en masse, creating 1.2 million new renter households annually. Baby boomers are downsizing from suburban mansions to urban apartments. Immigration, despite political volatility, continues adding residents to gateway cities. The American housing shortage—estimated at 4-7 million units—won't be solved this decade, ensuring pricing power for existing landlords.

Bear Case: The Disruption Ahead

The skeptics see gathering storm clouds that AvalonBay's historical excellence can't disperse. Start with the expansion regions, which are projected to deliver sub-2% growth due to heavy levels of unleased inventory and new deliveries. AvalonBay is walking into a supply buzz saw in Texas and Florida, where developers can deliver thousands of units annually. Their coastal expertise doesn't translate to markets where land is plentiful and approvals are easy.

Regulatory risks loom larger than ever. AvalonBay faces regulatory risks in certain markets, which could impact future investment decisions and portfolio optimization. Rent control initiatives in California, New York, and Oregon threaten the fundamental investment thesis. Progressive cities increasingly view landlords as villains, not housing providers. The political climate has shifted from benign neglect to active hostility toward property owners.

Coastal market exposure to tech sector volatility represents concentrated risk. AvalonBay's premium rents depend on tech workers earning $200,000+ salaries. But tech layoffs have accelerated, AI threatens white-collar jobs, and remote work enables geographic arbitrage. The moat around coastal cities is eroding as knowledge workers realize they can earn San Francisco salaries while living in Austin.

Rising interest rates impact development returns fundamentally. Construction loans that cost 3% in 2021 now price at 7-8%. The development spread that justified AvalonBay's entire strategy has compressed from 250 basis points to barely 100. If rates stay elevated, the development machine that drives growth grinds to a halt.

Competition from single-family rentals represents a new threat. Institutional investors have assembled massive SFR portfolios offering the space and privacy apartments can't match. For the same $3,500 monthly payment, residents can rent a house with a yard versus a two-bedroom apartment. The American Dream of homeownership might be dead, but the desire for single-family living isn't.

Climate change poses existential risks to coastal portfolios. Rising sea levels threaten properties from Miami to Boston. Wildfire risk makes California insurance increasingly expensive or unavailable. Hurricanes are strengthening and reaching further north. AvalonBay's geographic concentration in climate-vulnerable regions represents unhedgeable risk.

Technology disruption could commoditize AvalonBay's advantages. Opendoor and similar platforms make home transactions as easy as apartment rentals. Co-living startups offer flexibility apartments can't match. Airbnb enables property owners to achieve apartment-like returns from single-family homes. The very concept of traditional apartment living faces disruption from multiple angles.

Work-from-home permanently reduces apartment demand in expensive cities. If professionals only commute twice weekly, living an hour from the office becomes tolerable. The premium for proximity evaporates when proximity doesn't matter. AvalonBay's urban portfolios were built for a daily commute world that may never fully return.

The Verdict: Synthesis and Probability Weighting

The truth, as usual, lies between extremes. AvalonBay faces real challenges that will compress returns from historical levels. But their competitive advantages—irreplaceable assets, development expertise, operational excellence, and balance sheet strength—remain durable even if diminished.

The highest probability scenario sees AvalonBay generating 7-9% annual total returns over the next decade—below the 11% historical average but well above bond yields. Coastal markets will grow slowly but steadily. Expansion markets will disappoint initially but provide long-term growth. Technology will enhance operations without revolutionizing the industry. Demographics will support demand despite headwinds.

The key risk isn't catastrophic failure but gradual commoditization. AvalonBay's moats are wide but slowly filling. Their premium valuation assumes continued excellence, leaving little room for error. For conservative investors seeking inflation-protected yield, AvalonBay remains attractive. For growth investors expecting double-digit returns, look elsewhere.

Ultimately, AvalonBay represents a bet on American urban dynamism. If cities remain centers of innovation and opportunity, AvalonBay prospers. If the future is distributed and digital, their coastal fortresses become expensive prisons. The company that built an empire on geographic concentration now faces its greatest test: evolving without abandoning what made them special. The next decade will determine whether AvalonBay's transformation preserves their premium position or merely manages decline. The smart money should probably bet on the former, but hedge for the latter.

XIII. Epilogue & "If We Were CEOs"

Standing on the observation deck of AvalonBay's newest Seattle high-rise, watching ferries cross Puget Sound while Mount Rainier looms in the distance, you can't help but wonder: What would Gilbert Meyer think of the empire his Bay Apartment Communities helped create? The scrappy California developer who started with a few garden apartments in 1978 probably couldn't have imagined a $32 billion colossus managing nearly 100,000 homes across America. Yet here we are, at an inflection point where AvalonBay's next chapter might diverge as dramatically from its past as a smartphone differs from a rotary dial.

The future of American housing presents both existential challenges and generational opportunities. The affordability crisis has reached breaking point—median home prices now exceed 7x median income versus the historical 3x ratio. An entire generation faces permanent rentership, not by choice but necessity. This creates unprecedented demand for rental housing but also political pressure for rent control, public housing investment, and regulatory intervention. AvalonBay must navigate between capitalizing on scarcity and avoiding becoming the poster child for housing inequality.

Climate change isn't a distant threat but present reality reshaping portfolio strategy. AvalonBay's coastal concentration, once its greatest strength, increasingly looks like a liability. Rising sea levels threaten properties from Miami to Boston. Wildfire smoke makes Bay Area summers unbearable. Hurricanes strengthen and reach further north each year. "Implement Value-Enhancing Sustainability Solutions to reduce impact, expenses, and risk" understates the transformation required—this isn't about LED lightbulbs but fundamental portfolio reconstruction.