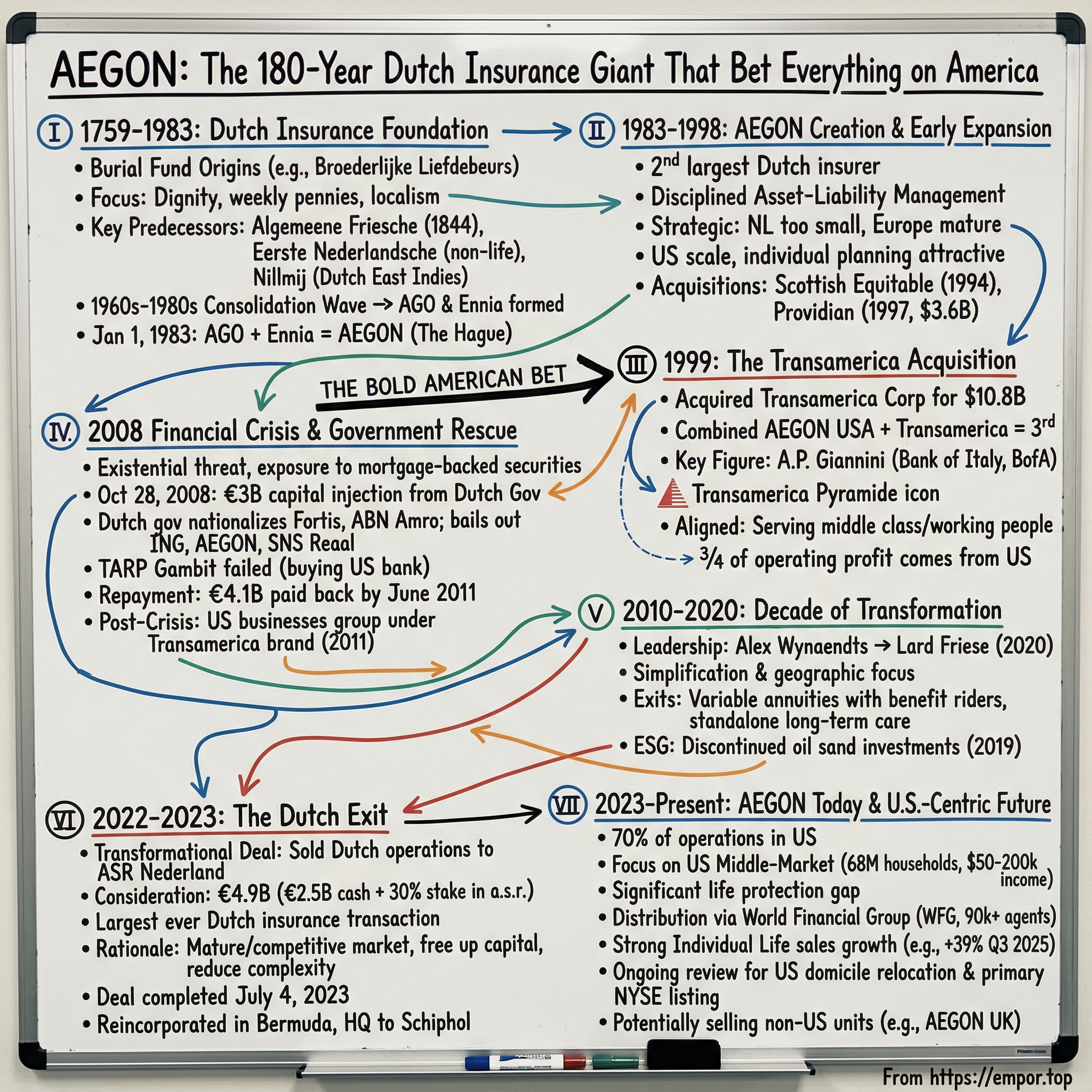

AEGON: The 180-Year Dutch Insurance Giant That Bet Everything on America

I. Introduction & Episode Roadmap

In the shadow of Amsterdam's 17th-century canals, where the world's first stock exchange once traded, a quiet revolution in financial services has been unfolding. A company whose roots stretch back to 1759—when Dutch burial funds collected weekly pennies from working families—now stands poised to abandon its European heritage entirely and become, for all practical purposes, an American corporation.

Aegon, a Dutch insurance firm, is currently evaluating the prospect of relocating its head office and legal domicile to the US. The consideration reflects the US's contribution to Aegon's business, accounting for around 70% of its operations and being integral to the company's long-term growth plans.

The central narrative here is nothing short of remarkable: how did a company named after the initials of old Dutch insurers—companies with names like Algemeene Friesche, Groot-Noordhollandsche, and Olveh—end up with 70% of its business in middle-market America?

Aegon Ltd. is a Dutch public company for life insurance, pensions and asset management. Aegon was founded in 1983 from the merger of AGO Holding N.V. and Ennia N.V. But the real story begins much earlier, in burial funds serving Friesland's provincial civil servants, and crescendos with a $10.8 billion acquisition that changed everything.

At Aegon's Capital Markets Day on December 10, 2025, the company will provide an update on its strategy and financial targets, and announce the outcome of its ongoing review regarding a potential relocation of its legal domicile and head office to the United States.

This is the story of Aegon: from burial funds to Transamerica, through the 2008 crucible, the 2022-2023 Dutch exit, and into an uncertain but potentially transformative American future.

II. The Dutch Insurance Foundation (1759-1983)

The Burial Fund Origins

Picture the Netherlands in 1759. The Dutch Golden Age had faded, but Amsterdam remained Europe's financial center. In the cobblestoned city of Haarlem, something quietly revolutionary was taking shape—the Broederlijke Liefdebeurs, or "Fraternal Fund of Love," one of Aegon's earliest predecessors.

These burial funds emerged from a distinctly Dutch anxiety: the prospect of a pauper's funeral. In an era before social safety nets, a city-provided burial was a mark of shame, reserved for the destitute. The burial funds—begrafenisfondsen—offered dignity in death for those who could afford weekly pennies but not much more.

The model was elegantly simple. Statutes limited each fund to operate within a single Dutch province—a localism that would define Dutch insurance for centuries. Collectors went door to door, gathering premiums from working families. Low premiums appealed to ordinary people, though fixed payments didn't always guarantee a fixed death benefit. In one particularly humane tradition, burial funds insured young children free of charge.

The Key Predecessor Companies

Among this patchwork of provincial protections, several companies would eventually merge into what became Aegon.

Aegon was founded in 1983 from the merger of AGO Holding N.V. (created by the merger of Algemeene Friesche, Groot-Noordhollandsche and Olveh in 1968) and Ennia N.V. (formed by the merger of Eerste Nederlandsche and Nillmij in 1969).

The oldest predecessor was Algemeene Friesche, created by two civil servants in the northern Dutch province of Friesland in 1844. In a nation where water management had long required collective action, organizing collective financial protection came naturally. Friesland's insurance pioneers brought the same cooperative spirit to mortality risk that their ancestors had brought to dike maintenance.

Meanwhile, Eerste Nederlandsche pioneered something new: non-life coverage. The company introduced accident insurance to the Netherlands around 1880, a concept its founder brought back from England, where the Industrial Revolution had created new categories of workplace danger and corresponding financial products.

Nillmij took a different path entirely, putting down roots in the Dutch East Indies starting in 1859. Serving civil servants and military personnel in what is now Indonesia, Nillmij represented Dutch insurance's imperial reach—and its entanglement with colonial administration.

The Olveh, founded in 1877, began as a self-help organization for civil servants, patterned after a successful Austrian union. Its goals were quintessentially mutual: reduce the cost of living, provide security through consumer cooperatives, savings plans, and life insurance.

The Consolidation Wave

By the 1960s, the logic of consolidation had become irresistible. European market liberalization loomed on the horizon. Scale would be necessary to compete. The next 140 years of fragmented Dutch insurance would compress into two decades of mergers.

In 1968, Algemeene Friesche, Groot-Noordhollandsche, and Olveh merged to form AGO. A year later, Eerste Nederlandsche, Nieuwe Eerste Nederlandsche, and Nillmij combined into Ennia. These two insurance giants circled each other for fifteen years before the final consolidation.

On January 1, 1983, in The Hague, AGO and Ennia merged to create Aegon. The name itself—made up of initials from major predecessors—reflected its roots while functioning as an exportable brand designed for international expansion. The locally managed structure aimed to help the company compete in an increasingly internationalized market.

For investors, the burial fund origins matter because they reveal Aegon's DNA: disciplined asset-liability management, long-dated investing for pensions and life insurance, and a mission to serve working people rather than just the wealthy. These principles would guide—and sometimes constrain—the company for the next four decades.

III. The AEGON Creation & Early Expansion (1983-1998)

The 1983 Merger

When Aegon emerged on that New Year's Day in 1983, it was already the second-largest insurer in the Netherlands. The board-driven merger combined life, non-life, and pensions franchises, creating diversification that could cushion against sector-specific shocks while building the scale necessary for European competition.

The initial model emphasized what would become Aegon's calling card: disciplined asset-liability management. Life insurers and pension providers face a unique challenge—they collect premiums today against liabilities that may come due decades hence. The Dutch had long experience matching long-dated assets to long-dated liabilities, a skill that would prove invaluable in markets where others chased short-term returns.

Amsterdam's public equity markets provided the financing for expansion. The combined balance sheets created capacity for growth. The question was: where to grow?

Strategic Rationale for Consolidation

The answer, increasingly, was America.

The Netherlands, despite its sophisticated financial culture, was simply too small. Even as the second-largest Dutch insurer, Aegon faced limited domestic growth potential in a mature market. European liberalization promised eventual access to continental neighbors, but those markets were equally mature and fiercely contested by domestic incumbents.

The United States offered something different: sheer scale. With 250 million people in the 1980s, fragmented state-level regulation, and a culture of individual financial planning, America represented the greatest opportunity in global insurance.

Early International Expansion

Aegon acquired Scottish Equitable in 1994. This established a durable U.K. position in pensions and savings, adding scale in workplace and retail retirement markets while diversifying revenue outside the Netherlands.

In 1998, it formed Stonebridge International Insurance Ltd to create and market a range of personal insurance products, providing accident, health and unemployment cover.

But the real story of the 1980s and 1990s was America. By the late 1980s, Aegon initiated U.S. expansion through targeted acquisitions of life insurers. The company bought Louisville, Kentucky-based Providian Corp. in 1997 for $3.6 billion, building distribution capability that would later enable scale in the American market.

The company, which also bought the insurance business of Providian Corp. in 1997 for $3.6 billion, is focusing increasingly on life insurance and retirement-savings vehicles.

The strategy was clear: use Dutch capital discipline and long-term orientation to build an American insurance empire. By decade's end, Aegon was ready for the move that would define its next quarter-century.

IV. The Transamerica Acquisition: The Bold American Bet (1999)

Transamerica's Storied History

To understand the 1999 acquisition, one must first understand Transamerica—and to understand Transamerica, one must begin with one of the most remarkable bankers in American history.

Amadeo Pietro Giannini, also known as A. P. Giannini, was an American banker who founded the Bank of Italy, which eventually became Bank of America. Giannini is credited as the inventor of many modern banking practices. Most notably, Giannini was one of the first bankers to offer banking services to middle-class Americans, mainly Italian immigrants, rather than only the upper class.

Giannini founded the Bank of Italy in the Jackson Square neighborhood of San Francisco on October 17, 1904. The bank was based in a converted saloon as an institution for the "little fellow." It was a new bank for the hardworking immigrants other banks would not serve.

Then came the earthquake. After a disastrous earthquake and subsequent fires levelled much of the city in 1906, Giannini set up a temporary bank immediately, collecting deposits, making loans, and proclaiming to all that San Francisco would rise from the ashes. He based his business on openness and trust, making his reputation by helping the city rebuild.

A liberal in a conservative field, Giannini and his bank helped nurture the motion picture and wine industries in California. He loaned Walt Disney the funds to produce "Snow White", the first full length animated motion picture. In the depths of the Depression, he bought the bonds that financed the construction of the Golden Gate Bridge.

Giannini founded another company, Transamerica Corporation, as a holding company for his various interests, including Occidental Life Insurance Company.

After creating a holding company, Transamerica Corporation (1928), for his banking interests, he merged the Bank of Italy and the Bank of America of California in 1930, resulting in the Bank of America National Trust and Savings Association.

The company became a diversified conglomerate over the decades, including the film distributor United Artists, Trans International Airlines, and Budget Rent-a-Car. In 1972, the company completed construction of the iconic Transamerica Pyramid skyscraper in San Francisco, which served as its headquarters for many years and remains depicted in its logo today.

In 1981, Transamerica sold United Artists to Tracinda Corporation. Transamerica was eventually reduced to three main product divisions: insurance, investments, and retirement planning.

The Deal

In February 1999, the long-rumored deal finally came.

European insurer Aegon N.V. agreed Thursday to acquire Transamerica Corp. for $10.8 billion in stock, cash and debt, as the Dutch-based company moved to bolster its life insurance business in the United States.

Aegon NV, a big, Netherlands-based insurer with U.S. headquarters in Baltimore, agreed to pay $10.8 billion to acquire Transamerica Corp., the San Francisco insurer famous for its pyramid-shaped building. If sealed as planned that summer, the deal would be the second-largest U.S. life insurance marriage in history, behind American International Group Inc.'s $18.2 billion acquisition of SunAmerica Inc. It would create the third-biggest U.S. life insurer.

Aegon will pay $9.7 billion - 70 percent stock and 30 percent cash - and assume $1.1 billion in debt. That represents a $78 a share price, or a 34.5 percent premium over Transamerica's closing price.

Donald Shepard, then CEO of Aegon USA, said "It makes us a much stronger company. We never had a very strong brand name in the U.S., and this gives us one. We like the fit very much." The acquisition got its start when Shepard called Transamerica CEO Frank Herringer and the two met in a Houston restaurant.

Strategic Impact

The merger, completed in July 1999, combined the operations of AEGON USA and Transamerica to form the third largest U.S. life insurer. The two, operating among the AEGON Americas Companies division, had combined assets of $131.6 billion.

This bold move catapulted Aegon into the top tier of global insurers and made the U.S. market central to its strategy and financial performance. It fundamentally altered the company's geographic balance and scale. By the end of the transaction, Aegon went from a mid-sized European player to a truly transatlantic giant.

The acquisition was also, in hindsight, a cultural bet. Giannini's vision—banking and insurance for the "little fellow"—aligned naturally with Aegon's burial fund origins. Both traditions emphasized serving working people, not just the wealthy. This philosophical alignment would prove prescient when, decades later, Aegon would target America's underserved middle market.

The Netherlands-based Aegon, which currently owns U.S. life insurer Transamerica, derives three-quarters of its operating profit from the United States.

For investors evaluating Aegon today, the Transamerica acquisition remains the defining transaction—the bet that transformed a regional Dutch insurer into a global player, but also the commitment that now pulls the company toward American domicile.

V. The 2008 Financial Crisis: Near-Death and Government Rescue

The Crisis Hits

The global financial crisis that erupted in 2008 posed an existential threat to Aegon. Like many insurers, the company had exposure to mortgage-backed securities and other risky assets whose values collapsed as the crisis unfolded.

On October 28, 2008, the Dutch government and De Nederlandsche Bank agreed to give Aegon a €3 billion capital injection to create a capital buffer in exchange for convertible bonds due to the effects of the 2008 financial crisis.

Aegon already got a €3 billion ($3.785 billion) capital injection from the Dutch government last month to strengthen a capital base eroded by investment losses and exposure to risky assets.

The Dutch Financial System Under Stress

Aegon was not alone. The crisis swept through the Dutch financial sector with devastating force.

The crisis began in 2007 and forced the government to nationalize Fortis and ABN Amro banks and issue loans of almost €14 billion (about US$18 billion) to global financial services company ING, life insurance and pension group Aegon, and financial services group SNS Reaal.

In addition to bailing out ING and Aegon, the government nationalized the Dutch operations of ABN Amro, the country's largest retail bank, along with those of Belgium's Fortis in early October.

The Netherlands, despite its image as a stable, consensus-driven economy, found its entire financial sector on the brink. Amsterdam's centuries-old reputation as a financial center hung in the balance.

AEGON's TARP Ambitions

In a desperate and creative gambit, Aegon explored accessing American bailout funds as well.

Dutch insurer Aegon NV said it may buy Maryland-based thrift Suburban Federal Savings Bank, to qualify Aegon for the government TARP bailout program. "This is part of our strategy to ensure Aegon has the strongest capital position possible."

The insurer will have to repay the Dutch government at a premium or pay a steep 8.5 interest rate to use the cash, opening an arbitrage opportunity if U.S. TARP funds are cheaper. "The capital of Aegon is totally unchanged," Aegon's CFO Streppel said. "I don't need more money but I might replace a part of the €3 billion with U.S. funds."

A Dutch insurer's experimental bid to tap the U.S. government for bailout cash looks doomed to failure. Aegon NV said it was mulling buying a small U.S. bank to qualify for potentially more than $1 billion in U.S. government support.

The TARP gambit ultimately failed. Foreign insurers were barred from using the fund, and the regulatory backlash would have been severe regardless. Politicians were unlikely to allow companies to arbitrage between rescue funds.

The Repayment

The Dutch government's rescue came with strings attached—and a steep price.

On June 15, 2011, Aegon fulfilled its key objective of repurchasing all of the €3 billion core capital securities issued to the Dutch State. The total amount Aegon has paid to the Dutch State amounts to €4.1 billion. Of this amount, €3 billion covered the original issue of core capital securities, while an additional €1.1 billion was paid in premium and interest.

The company was required by the Dutch government to refrain from spending money to promote its brand or products until it repaid the loan. AEGON in June completed the repurchase of the securities. The company repaid a total of $5.8 billion, including $1.5 billion in premium and interest.

Post-Crisis Consolidation

With the government debt finally repaid, Aegon moved to simplify its American operations.

On August 3, 2011, Aegon USA announced that all its various businesses will be grouped under a single brand name: Transamerica. Transamerica's key businesses are life insurance, investments and retirement.

Mark Mullin, president and CEO of AEGON USA LLC, said the change to Transamerica recognizes the ongoing support from its corporate parent and the achievements of founding companies. "We are unifying our brand, leveraging our experience and embracing the best of where we came from. We are positioning ourselves for opportunities from a place of strength, security and confidence."

For investors, the 2008 crisis revealed both Aegon's vulnerability and its resilience. The company survived, repaid its obligations at a premium, and emerged with a simplified structure. But the experience also demonstrated the risks of complex, leveraged financial institutions—and planted seeds for the geographic simplification that would come a decade later.

VI. The Decade of Transformation (2010-2020)

Leadership Transitions

The post-crisis years brought leadership change. On April 23, 2008, Alex Wynaendts succeeded the retiring Donald J. Shepard as chairman of the executive board and CEO of Aegon N.V. Wynaendts would guide the company through the crisis aftermath and into a new strategic era.

On May 15, 2020, Lard Friese (former CEO of NN Group) succeeded Alex Wynaendts as the CEO of Aegon N.V.

Mr. Friese joins Aegon from NN Group where he was Chief Executive Officer. He has close to 30 years' experience in the financial services industry, including at Aegon between 1993 and 2003.

Lard Friese earned a Master of Law degree at the University of Utrecht. He has worked most of his professional career in the insurance industry, including ten years at Aegon between 1993 and 2003. He was employed by ING as from 2008, where he held various positions.

Friese's return to Aegon—a company where he had spent a decade early in his career—brought a leader who understood both the organization and the broader transformation underway in European insurance. His track record at NN Group suggested an appetite for strategic repositioning.

Strategic Repositioning

The 2010s were marked by continuous simplification and geographic focus. Sales of non-core assets and reduced equity risk exposure enabled the company to navigate lingering eurozone volatility while positioning for growth in key markets.

In December 2020, Aegon announced a strategic overhaul aimed at simplifying its operations by concentrating on three core markets—the United States, the United Kingdom, and the Netherlands.

Product Exits

In December 2020, Transamerica announced it would no longer sell variable annuities with benefit riders and fixed index annuities and is also exiting the standalone long-term care market.

These exits reflected hard-won lessons from the crisis. Variable annuities with complex guarantees had proven capital-intensive and volatile. Long-term care insurance had become a notorious source of losses across the industry as Americans lived longer than actuaries had predicted. Rather than continue wrestling with these troubled lines, Aegon chose to exit and redeploy capital elsewhere.

ESG Considerations

In June 2018, AEGON was criticized by Greenpeace for its investments in oil sand companies and pipelines. Aegon reacted by stating that it was developing a new policy with regards to the oil and gas sector. In 2019, they decided to discontinue their oil sand investments.

The Greenpeace criticism illustrated growing pressure on institutional investors to consider environmental, social, and governance factors. For a long-duration investor like Aegon—whose liabilities stretch decades into the future—climate risk was not merely reputational but fundamentally material to asset-liability matching.

For investors, the decade of transformation showed management's willingness to make difficult decisions: exiting underperforming lines, simplifying structures, and eventually preparing for far more dramatic geographic repositioning.

VII. The 2022-2023 Dutch Exit: Selling the Homeland

The Transformational Deal

On October 27, 2022, Aegon announced what many observers considered unthinkable: the company would sell its Dutch operations—the business that had existed since 1759—to smaller rival ASR Nederland.

Aegon agreed to a conditional deal for a total consideration of €4.9 billion ($4.9 billion), ASR Nederland said in a statement. Dutch insurance giant Aegon will receive a 30% stake in a.s.r. and €2.5 billion in cash proceeds from the deal.

"This is going to be a powerhouse company" on the Dutch market, Aegon Chief Executive Officer Lard Friese told reporters in a video call.

This transaction deserves recognition as the largest European insurance transaction in 2023 and the largest-ever insurance transaction in the Dutch market.

Strategic Rationale

Why sell the homeland? The answer lay in Aegon's geographic imbalance. With over 70% of operations in the United States, maintaining a fully owned Dutch insurance business created complexity without commensurate benefits. The Dutch market was mature, intensely competitive, and required dedicated capital and management attention.

The deal is part of Aegon's strategy to free up capital from mature markets and accelerate growth in businesses outside the Netherlands.

"Customers of both companies will benefit from a more diversified product offering and strong distribution," said Aegon's Chief Executive Officer Lard Friese.

The combination created a stronger competitor to NN Group, the market leader in Netherlands insurance. By taking a 29.99% stake rather than full exit, Aegon retained exposure to Dutch market upside while dramatically simplifying its structure.

Deal Completion

After the Netherlands Authority for Consumers and Markets (ACM), De Nederlandsche Bank (DNB) and the European Central Bank gave the go-ahead, the transaction was realised on 4 July 2023.

Aegon has concluded a previously announced deal to merge its Dutch pension, life and non-life insurance, banking and mortgage origination portfolios with its smaller rival a.s.r. As part of the deal, Aegon has received a 29.99% stake in a.s.r and €2.2bn in cash proceeds.

Aegon CEO Lard Friese said: "The completion of this transaction marks a major milestone in Aegon's history and in our long-term ambition to create leaders in investments, protection, and retirement solutions. The combination creates the number two insurance company in the Netherlands."

Reincorporation

Following the sale, Aegon no longer operated a regulated insurance business in the Netherlands. The logical next step followed swiftly.

Subsequently, AEGON reincorporated in Bermuda.

Earlier this year, Aegon moved its headquarters from The Hague to Schiphol, while keeping the legal seat in Bermuda, a step taken after the sale of its Dutch insurance operations to ASR in 2023. That deal meant Aegon was no longer under the supervision of De Nederlandsche Bank.

For investors, the Dutch exit represents perhaps the most dramatic strategic pivot in Aegon's history. A company with roots stretching back 264 years chose to exit its home market entirely, retaining only a minority financial stake. This is not normal corporate behavior—it suggests management conviction that the future lies elsewhere.

VIII. AEGON Today & The U.S.-Centric Future (2023-Present)

Current Financial Profile

As of late 2025, Aegon has transformed into a fundamentally different company than it was just five years ago.

Aegon delivered on its increased guidance for Operating Capital Generation (OCG) of EUR 1.2 billion for 2024, while its main business units remained well capitalized. The company also generated an IFRS operating result of EUR 1.5 billion.

On the basis of 2024 performance, the company proposed a final dividend of 19 eurocents per share. This will result in a total dividend paid for the full-year 2024 of 35 eurocents, up 17% compared with 2023, and means we are on our way to achieve our target of around 40 eurocents per share over 2025.

The company's operating result was EUR 845 million in H1 2025, up 19% compared to last year.

U.S. Dominance

"Over the past years, Aegon's U.S. operations — which make up approximately 70 percent of Aegon's activities — have become the company's most important market and are central to its strategy and long-term growth," CEO Lard Friese said during the presentation of half-year results.

During the third quarter of 2025, Transamerica continued to make progress in executing its strategy to grow its business by focusing on middle-market America, targeted through agency distribution and the workplace. New Individual Life sales increased by 39%.

Transamerica's Growth Strategy

Transamerica aims to accelerate its growth and build America's leading middle market life insurance and retirement company. This rapidly growing market, representing 68 million middle income households, is the largest in the US and is relatively underserved by the financial services industry.

The middle market includes approximately 68 million households (~52% of total US households) with USD 50-200 thousand yearly income. About 40% of households are diverse, and the market has a USD ~3 trillion Life protection gap with higher likelihood of customers to purchase insurance.

Transamerica is targeting approximately USD 750 million of annual new life sales in Individual Life by 2027.

New Individual Life sales increased by 13% to a new record-high level in H1 2025, driven by all distribution channels. World Financial Group (WFG), Transamerica's affiliated distribution network of independent agents, continued to increase its number of licensed agents.

World Financial Group provides resources for over 85,000 independent agents in the United States and Canada.

WFG's number of licensed agents grew to 90,315, reflecting successful recruiting and improved retention.

Recent Performance

Continued strong commercial momentum in US Strategic Assets: Individual Life sales are up 39% compared with the prior year period, while World Financial Group's (WFG) sales and US Retirement Plans account balances also increase.

Business growth and favorable markets drove a 10% increase in the total account balances in Retirement Plans over the last year. Account balances for the mid-sized plans segment increased by 15% due to favorable market movements, as well as overall net inflows.

Potential U.S. Relocation

Alongside the publication of its H1 2025 results, Aegon announces the start of a review of a possible relocation of its legal domicile and headquarters to the US. This would simplify the corporate structure by aligning the legal domicile, tax residence, accounting standards, and regulatory framework with the geographic area where Aegon conducts the majority of its business, CEO Lard Friese said.

This comprehensive review will examine the implications of a potential relocation, including the impact on all of Aegon's stakeholders, and making its NYSE listing its primary listing alongside its Euronext listing. If Aegon decides to proceed with such a relocation, the transition is expected to take two to three years.

Aegon is considering a divestment strategy outside of the US as part of a review aimed at sharpening business focus on its largest market. The Dutch insurer is working with financial advisers to assess which international units could be sold. Aegon UK, responsible for administering retirement accounts, is among the divisions being examined for a potential sale.

If the relocation goes forward, it would add Aegon to the list of multinationals that have departed the Netherlands in recent years, following Shell and Unilever.

For investors, the potential U.S. relocation represents the logical culmination of two decades of strategic evolution. From Transamerica acquisition to Dutch exit to potential American redomicile, the arc bends consistently toward simplification around the company's dominant market.

IX. Business Model Deep Dive

Current Operating Structure

Aegon is an international financial services holding company. Aegon's ambition is to build leading businesses that offer their customers investment, protection, and retirement solutions. Aegon's portfolio of businesses includes fully owned businesses in the United States and United Kingdom, and a global asset manager. Aegon also creates value by combining its international expertise with strong local partners via insurance joint-ventures in Spain & Portugal, China, and Brazil, and via asset management partnerships in France and China. In addition, Aegon owns a Bermuda-based life insurer and generates value via a strategic shareholding in a market leading Dutch insurance and pensions company. Aegon's purpose of helping people live their best lives runs through all its activities.

Key Business Lines

Transamerica (U.S.): The crown jewel, representing 70% of group operations. Transamerica focuses on life insurance, retirement solutions, and employee benefits, with particular emphasis on the underserved middle market.

World Financial Group (WFG) is a multi-level marketing financial and insurance services company based in Johns Creek, Georgia, which sells investment, insurance, and various other financial products through a network of distributors in the United States, Canada, and Puerto Rico. It is wholly owned by Dutch life insurance multinational Aegon and operates primarily under the Transamerica brand.

Aegon UK: Focuses on platform-based retirement and savings products. As noted, this division is reportedly under review for potential sale.

Aegon Asset Management: Aegon AM is an active global asset management firm comprised of four global investment platforms: Fixed Income, Real Assets, Equities and Multi-Asset & Solutions. Across platforms, they share a common belief in fundamental, research-driven active management, underpinned by effective risk management.

The Assets under Management (AuM) at Aegon Investment Management B.V. remained flat from EUR 120.6 billion to EUR 120.5 billion in the first half of 2025.

International Joint Ventures: Partnerships in Spain & Portugal (with Banco Santander), China (with CNOOC), and Brazil provide geographic diversification without full capital commitment.

Strategic Stakes: The 29.99% stake in a.s.r. provides ongoing exposure to the Dutch market, now reduced to approximately 24% following share sales in late 2025.

The Middle Market Opportunity

The strategic focus on America's middle market deserves particular attention because it represents Aegon's core thesis about where value can be created.

McKinsey research indicates that mass-market millennials, mass-market Generation Xers, and middle-market baby boomers represent the next horizon of growth for the life insurance industry. Among the 68 million such households in the United States, 57 percent do not own individual life insurance.

This is a staggering statistic. More than half of America's middle-income households lack individual life insurance coverage—despite recognizing the need. The industry has historically found it uneconomical to serve this segment through traditional distribution channels; the commission economics simply don't work for smaller policies sold to cost-conscious consumers.

Transamerica's answer is WFG: a network of over 85,000 independent agents who often come from the communities they serve. Many WFG agents work part-time, building their businesses alongside other careers. The model creates reach into communities that traditional insurance distribution has struggled to penetrate.

X. Investment Analysis: Bull & Bear Cases

The Bull Case

Geographic Focus Creates Operational Leverage: By concentrating on the U.S. market, Aegon can optimize its capital allocation, regulatory compliance, and management attention. The complexity costs of managing multiple jurisdictions disappear.

Middle Market Represents Structural Growth: With 68 million households underserved and demographic tailwinds from retiring baby boomers, Transamerica is positioned in a growing segment rather than fighting for share in saturated affluent markets.

Capital Returns Accelerating: The company's commitment to share buybacks (€400 million ongoing) and dividend growth demonstrates confidence in sustainable cash generation.

Aegon announced an interim dividend of 19 euro cents for 2025, representing a year-on-year increase of 19%, and increased its currently ongoing share buyback to EUR 400 million from the previously announced EUR 200 million.

Simplified Structure Improves Transparency: The transition to U.S. GAAP and potential U.S. domicile would make Aegon more comparable to American peers and potentially more attractive to U.S.-focused institutional investors.

The Bear Case

Execution Risk on U.S. Relocation: A 2-3 year transition to U.S. domicile creates execution risk and potential regulatory hurdles. Management distraction is real, and unexpected complications could arise.

The transition period (2–3 years) could disrupt short-term earnings, and regulatory hurdles—such as approval from Dutch and U.S. authorities—must be navigated. Additionally, the U.S. insurance market is highly competitive, with legacy players and fintech disruptors vying for market share.

WFG Model Controversy: In October 2025, WFG was ordered by the San Francisco County Superior Court to pay $65 million to settle a class action lawsuit over allegations of "misclassifying its sales agents as independent contractors". Multi-level marketing structures face ongoing regulatory and reputational scrutiny.

Financial Assets Drag: Transamerica carries a legacy book of variable annuities, fixed annuities, and long-term care insurance that consumes capital while running off. On March 31, 2025, Financial Assets had USD 3.6 billion of capital employed, an increase of USD 0.2 billion compared with the end of 2024.

Competition in the U.S. Market: The industry's three largest companies, Mass Mutual, Northwestern Mutual and New York Life, have a significant presence in this industry. The level of competition is high and steady in the Life Insurance & Annuities industry in the United States.

Porter's Five Forces Analysis

Threat of New Entrants (Medium): The insurance industry requires significant capital and regulatory approval, creating barriers. However, insurtech startups are attempting to disrupt distribution, particularly in the middle market that Aegon targets.

Bargaining Power of Buyers (Medium-High): Life insurance is increasingly commoditized, with consumers comparing quotes online. However, the middle market often lacks financial sophistication, reducing their bargaining leverage.

Bargaining Power of Suppliers (Low): Insurers are primarily capital providers; their main "suppliers" are reinsurers and capital markets, where Aegon has scale advantages.

Threat of Substitutes (Medium): Alternative savings vehicles (401(k)s, IRAs, taxable investment accounts) compete for customer wallet share. The cash value of life insurance faces competition from other investment products.

Competitive Rivalry (High): The U.S. life insurance market is mature with many established competitors. Differentiation is difficult, leading to price competition and margin pressure.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Modest. Insurance has some scale benefits in spreading fixed costs, but unit economics don't dramatically improve with size.

Network Effects: Present in WFG's agent network. More agents create more training capacity and peer support, potentially reinforcing recruitment. However, this is not a strong network effect comparable to platforms.

Counter-Positioning: Aegon's middle-market focus could represent counter-positioning—incumbents may be reluctant to cannibalize their affluent-market business model to compete effectively.

Switching Costs: Moderate for policyholders, who face surrender charges and re-underwriting hassles when changing insurers.

Branding: Transamerica's brand carries significant awareness in the U.S., enhanced by its iconic pyramid imagery and Giannini heritage.

Cornered Resource: None apparent. Insurance is fundamentally commoditized.

Process Power: Possible. Transamerica's claims to superior underwriting, particularly through its "fully digital underwriting platform," could represent process advantages if genuinely more efficient.

XI. Key Metrics to Watch

For investors tracking Aegon's ongoing performance, three KPIs deserve particular attention:

1. Operating Capital Generation (OCG)

OCG measures the capital generated by business units before holding company expenses. It is the company's primary cash flow metric and the source of dividends and buybacks. The 2025 target of approximately EUR 1.2 billion represents management's commitment; tracking actual OCG against this target reveals execution quality.

2. WFG Licensed Agent Count and Productivity

With WFG at the heart of Transamerica's middle-market strategy, agent count (currently ~90,000) and productivity metrics matter enormously. Agent growth without productivity growth would suggest recruiting struggles to generate profitable activity. The company discloses "multi-ticket agents" (those who have sold more than one policy in the last 12 months) as a quality indicator.

3. U.S. Individual Life New Sales

Transamerica is targeting approximately USD 750 million of annual new life sales in Individual Life by 2027. Tracking progress toward this target—and the trajectory required to achieve it—reveals whether the middle-market thesis is translating into actual business growth.

XII. Risks and Regulatory Considerations

Material Legal/Regulatory Overhangs

WFG Independent Contractor Litigation: The $65 million settlement in October 2025 may not be the final word on agent classification issues. Similar cases have proliferated across industries that rely on independent contractor models.

Cross-Border Regulatory Complexity: Until the U.S. relocation is complete (if it proceeds), Aegon remains subject to oversight from multiple jurisdictions including Bermuda, the Netherlands (via the a.s.r. stake), and all 50 U.S. states.

Life Insurance Reserving: Long-duration products like life insurance involve significant actuarial judgment. Mortality, lapse, and interest rate assumptions all affect reserves. The company's annual assumption updates have caused earnings volatility.

Accounting Judgments

Contractual Service Margin (CSM): Under IFRS 17, the CSM represents deferred profit from insurance contracts. Aegon reports CSM alongside shareholders' equity as part of "valuation equity." Investors should understand that CSM is an accounting construct—actual cash realization depends on future experience.

Variable Annuity Hedging: Transamerica's legacy variable annuity book requires complex derivatives hedging. Hedge effectiveness affects reported earnings and capital.

XIII. Conclusion: A Company in Transition

Aegon stands at an inflection point unlike any in its 180-year history. From Dutch burial funds to transatlantic insurance giant, the company has continuously adapted to changing markets and opportunities. The potential U.S. relocation represents the logical endpoint of a strategic journey that began with the Transamerica acquisition in 1999.

The December 10, 2025 Capital Markets Day will likely provide clarity on whether Aegon's future is American in domicile as well as operations. For long-term fundamental investors, the key questions are:

- Can Transamerica execute on its middle-market growth thesis?

- Will the WFG distribution model scale profitably and sustainably?

- Can management navigate the complexity of corporate relocation without operational disruption?

In an analyst call in November 2025, Aegon CEO Lard Friese said: "Our aim is to build Transamerica into America's leading middle-market life insurance and retirement company."

That ambition—to be America's leading middle-market insurer—represents both the opportunity and the challenge. In a market where established players dominate and insurtechs disrupt, Aegon's combination of Dutch discipline and American distribution may prove either a winning formula or a cultural collision.

What is certain is that the company founded to prevent pauper's funerals in 18th-century Haarlem has traveled an extraordinary distance—geographically, strategically, and philosophically. The next chapter is being written now.

Key Dates for Investors: - December 10, 2025: Capital Markets Day (U.S. relocation decision expected) - June 12, 2025: Annual General Meeting - Q1-Q2 2028 (estimated): Potential U.S. relocation completion if approved

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube