Amphenol Corporation: The Interconnect Empire

I. Introduction & Cold Open

Picture this: Inside a massive data center in Northern Virginia, rows upon rows of NVIDIA H100 GPUs hum with barely contained power, training the next generation of AI models. Each GPU cluster—worth millions of dollars—depends on thousands of high-speed connectors carrying data at 224 gigabits per second. A single faulty connection could bring down an entire rack. The company that makes many of these mission-critical connectors? A 92-year-old firm that started by making radio tube sockets during the Great Depression.

How did a Chicago entrepreneur's phenolic plastic innovation in 1932 become the essential infrastructure powering the AI revolution? The answer lies in one of the most successful yet underappreciated business stories in American capitalism: Amphenol Corporation.

In 2024, Amphenol generated $15.22 billion in revenue—a 21.25% increase from the previous year's $12.55 billion. Earnings reached $2.42 billion, up 25.73%. These aren't the numbers of a sleepy industrial conglomerate. They're the metrics of a company experiencing hypergrowth at near-century age, riding every major technology wave while most investors barely notice.

Walk through your day and you're surrounded by Amphenol products, though you'll never see their logo. The Lightning connector in your iPhone? Often Amphenol. The wiring harness in your Tesla? Amphenol. The tactical communications system in an F-35 fighter jet? Amphenol. The fiber optic cables bringing 5G to your neighborhood? Probably Amphenol. The company has achieved something remarkable: complete ubiquity with near-total invisibility.

This is the story of how a Depression-era startup became a $90 billion market cap giant by mastering one deceptively simple principle: when everyone else fights to build the flashy end products, become the indispensable supplier of the unglamorous components that make everything work. It's a playbook of radical decentralization, relentless acquisition, and the patient compound growth that comes from being everywhere while appearing nowhere.

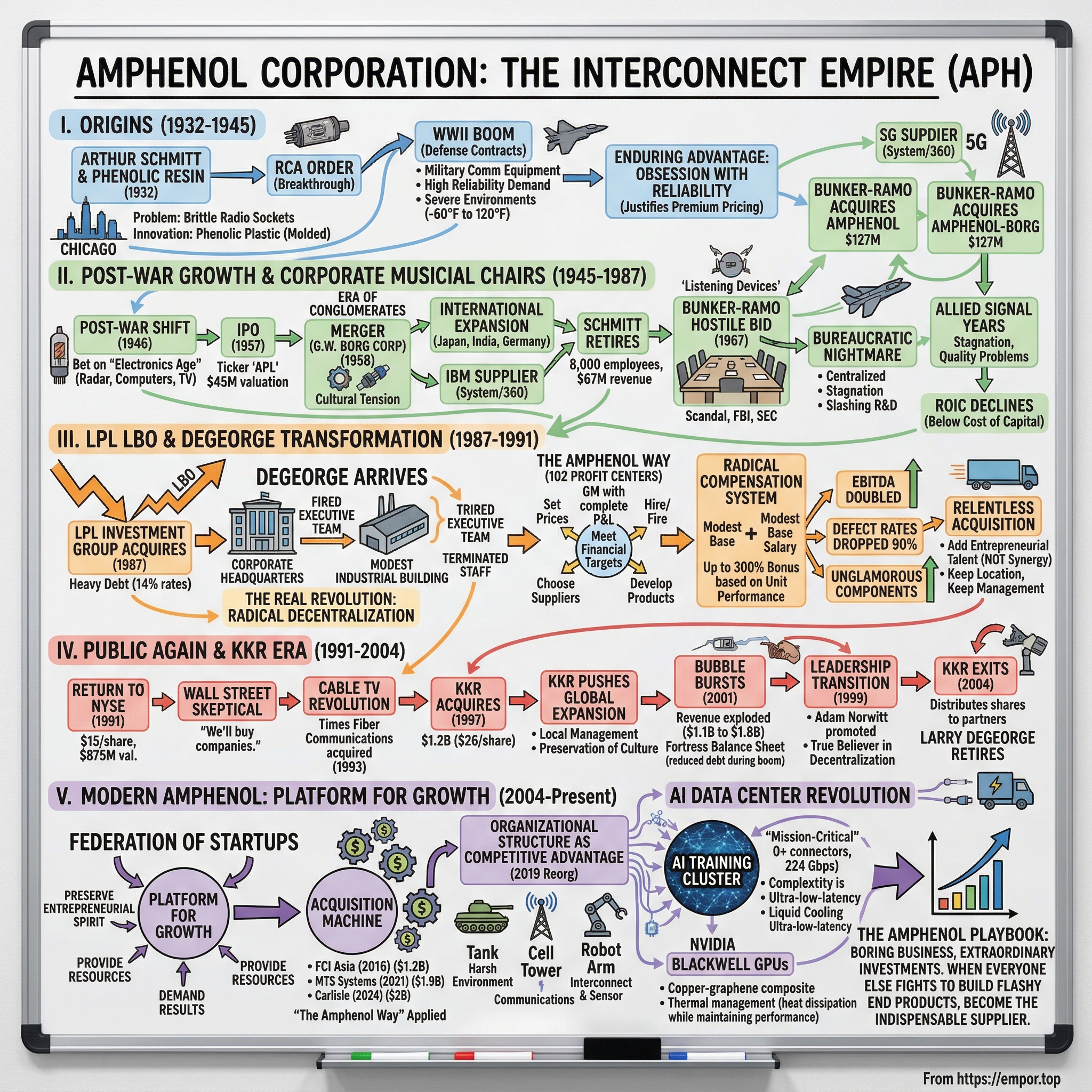

II. Origins: Arthur Schmitt & The Phenolic Revolution (1932-1945)

The year was 1932. Banks were failing at a rate of 40 per day. Unemployment hit 23.6%. In Chicago, breadlines stretched for blocks. It was, by any measure, the worst possible time to start a manufacturing company. Arthur J. Schmitt thought otherwise.

Schmitt wasn't an engineer by training—he was an entrepreneur who understood materials. He'd noticed something others hadn't: the radio industry, one of the few bright spots in the Depression economy, had a component problem. Radio tube sockets were made from ceramic, which was brittle, expensive to manufacture, and prone to cracking during assembly. Schmitt had been experimenting with a new material called phenolic resin—an early plastic that could be molded into complex shapes while maintaining excellent electrical insulation properties.

The American Phenolic Corporation opened its doors in a modest Chicago facility with a radical proposition: replace ceramic with plastic. The industry scoffed. Plastic was for toys and trinkets, not serious electrical components. But Schmitt had done his homework. Phenolic wasn't just cheaper than ceramic—it was actually better. It could be molded with integrated features that ceramic couldn't achieve, reducing assembly steps. It was more resistant to shock and vibration. Most importantly, it could be manufactured at scale using injection molding, dramatically reducing per-unit costs.

The breakthrough came when RCA, the General Electric of the radio age, placed an initial order. RCA's engineers had tested Schmitt's phenolic sockets and found them superior to ceramic in every metric that mattered. Word spread quickly through the tight-knit community of radio manufacturers clustered around Chicago and the East Coast. Within eighteen months, American Phenolic had captured 15% of the radio socket market.

But it was December 7, 1941, that transformed American Phenolic from a successful component supplier into a critical defense contractor. The attack on Pearl Harbor created an immediate and insatiable demand for military communications equipment. Every fighter plane needed dozens of electrical connectors. Every field radio required reliable sockets that could withstand jungle humidity and desert sand. Every naval vessel bristled with communications gear that demanded components that wouldn't fail under enemy fire.

The War Department quickly identified American Phenolic as one of the few companies with both the technology and manufacturing capability to meet these demands. Military contracts poured in, but they came with strict requirements: components had to meet specifications that were orders of magnitude more demanding than civilian applications. A radio in someone's living room might face dust; a radio in a B-17 bomber faced temperature swings from -60°F to 120°F, constant vibration, and the concussive force of anti-aircraft fire.

Schmitt's response revealed the entrepreneurial agility that would define Amphenol's culture for decades. Rather than simply scaling existing products, he embedded engineers directly with military units to understand their needs firsthand. When pilots complained that connectors were failing at high altitudes, American Phenolic developed new formulations that maintained flexibility at extreme temperatures. When naval officers reported corrosion problems in Pacific operations, the company created revolutionary sealed connectors that could withstand salt spray.

By 1944, American Phenolic had grown from 50 employees to over 2,000. The company operated three shifts, seven days a week. Revenue increased forty-fold. But more importantly, the company had learned something invaluable: in the connector business, reliability wasn't just a selling point—it was everything. A failed connector in a consumer radio meant static; a failed connector in a military application meant death.

This wartime experience created what would become Amphenol's enduring competitive advantage: an obsession with reliability that justified premium pricing. While competitors would later try to compete on cost, Amphenol had learned that customers would pay significantly more for connectors they could trust with their lives—literally in military applications, figuratively in commercial ones.

III. Post-War Growth & Corporate Musical Chairs (1945-1967)

The end of World War II should have been catastrophic for American Phenolic. Military contracts evaporated overnight. The company's revenue dropped 75% in six months. Thousands of defense contractors went bankrupt in what economists called the "reconversion recession." But Arthur Schmitt had anticipated this cliff and prepared for something that seemed impossible in 1945: the electronics age.

While his competitors retreated to pre-war product lines, Schmitt made a contrarian bet. He believed that the technologies developed during the war—radar, advanced communications, early computers—would transform civilian life. In 1946, he incorporated a new division called Amphenol Electronics Corporation, a portmanteau of "American Phenolic." This wasn't just a rebranding exercise; it was a declaration of intent to move beyond simple connectors into sophisticated electronic components.

The bet paid off faster than even Schmitt anticipated. By 1950, television manufacturing was exploding, with production increasing from 7,000 sets in 1946 to 7.3 million in 1950. Each television required dozens of specialized connectors. The Korean War brought a new wave of military contracts, but this time Amphenol wasn't dependent on them—civilian applications now represented 60% of revenue.

The company's growth trajectory was staggering. By 1956, annual sales reached $27.3 million with profits of $1.3 million—a net margin that would make modern manufacturers envious. Schmitt decided it was time to tap public markets. In 1957, he listed the newly renamed Amphenol Electronics Corporation on the New York Stock Exchange under the ticker "APL." The IPO valued the company at $45 million, making Schmitt one of Chicago's wealthiest industrialists.

But Schmitt wasn't content with organic growth. The late 1950s were the era of the conglomerate, when financial engineering was seen as the path to unlimited growth. In 1958, Amphenol merged with G.W. Borg Corporation, creating Amphenol-Borg Corporation. The logic seemed sound: Borg brought automotive components and mechanical systems that complemented Amphenol's electronic expertise. The combined company would be a one-stop shop for the increasingly electronic automobile.

The merger revealed a fundamental tension that would plague Amphenol for the next decade. Borg's culture was traditional Midwest manufacturing—hierarchical, process-driven, focused on cost reduction. Amphenol's culture was entrepreneurial and engineering-driven, willing to sacrifice margin for innovation. The two organizations never truly integrated, operating as parallel companies under a single corporate umbrella.

Despite cultural challenges, Schmitt pushed international expansion aggressively. By 1964, Amphenol-Borg had established joint ventures in Japan with Daiichi Electric and in India with the Birla Group. The company acquired Tuchel-Kontakt in Heilbronn, Germany, gaining a foothold in the European market just as the Common Market was reducing trade barriers. Most strategically, Amphenol acquired Cadre Industries in Endicott, New York—a coup that made Amphenol a major supplier to IBM just as the computer giant was launching System/360, the product line that would define enterprise computing for a generation.

When Arthur Schmitt retired in 1964 at age 71, he left behind a company that bore little resemblance to the Depression-era startup he'd founded. Amphenol-Borg had 8,000 employees across four continents, generated $67 million in annual revenue, and held over 400 patents. But Schmitt's departure created a power vacuum that would soon be filled in the most dramatic way possible.

The takeover battle of 1967 reads like a corporate thriller. Bunker-Ramo Corporation, a technology conglomerate with defense and computing divisions, launched a hostile bid for Amphenol-Borg in January. Amphenol's board initially rejected the offer, claiming Bunker-Ramo was using "strong-arm tactics." Then things got strange. In March, Amphenol executives discovered listening devices in the boardroom. Private investigators traced the bugs to operatives allegedly connected to Bunker-Ramo, though the company denied involvement.

The scandal exploded across the business press. The SEC launched an investigation. The FBI got involved. Amphenol's stock price gyrated wildly as investors tried to parse rumor from fact. Behind the scenes, a different dynamic was playing out: Amphenol's board, exhausted by months of fighting and concerned about lawsuits from shareholders, began to see merit in Bunker-Ramo's offer. The defense contractor was offering a 40% premium and promised to maintain Amphenol's autonomy.

In September 1967, the board capitulated. Bunker-Ramo acquired Amphenol-Borg for $127 million—nearly triple its IPO valuation a decade earlier. The bugging scandal was quietly settled out of court. Arthur Schmitt, watching from retirement, reportedly told friends he was "heartbroken" to see his company lose its independence. He had no idea how much worse things would get.

IV. The Bunker-Ramo Era & Allied Signal Years (1967-1987)

The marriage between Bunker-Ramo and Amphenol was doomed from the start. Bunker-Ramo CEO Simon Ramo—the "Ramo" in the company name and co-founder of aerospace giant TRW—was a brilliant engineer but a disaster as a conglomerate manager. He believed that synergies between Amphenol's connectors and Bunker-Ramo's defense electronics would create a vertically integrated powerhouse. Instead, he created a bureaucratic nightmare.

Within months, Amphenol's entrepreneurial culture began to suffocate under layers of corporate oversight. Every product decision required approval from Bunker-Ramo headquarters in Canoga Park, California. Pricing changes needed three signatures. New product development, which had always been Amphenol's lifeblood, slowed to a crawl as engineers spent more time writing justification memos than designing connectors.

The market noticed. Between 1968 and 1973, Amphenol's market share in commercial connectors dropped from 18% to 12%. Competitors like AMP Incorporated and Molex, still independent and agile, grabbed share by being faster to market with new designs. The company that had pioneered phenolic connectors was now a laggard in adopting new materials like advanced thermoplastics.

Yet paradoxically, this era produced one of Amphenol's most important innovations: the MIL-DTL-38999 cylindrical connector. Developed at the Bendix Corporation facility in Sidney, New York (which Bunker-Ramo had acquired and folded into Amphenol), the 38999 became the standard for military aerospace applications. Even today, every fighter jet, military helicopter, and tactical communication system uses descendants of this design. The 38999 epitomized Amphenol's historic strength: creating products so reliable that they became industry standards, generating decades of high-margin replacement revenue.

By 1977, Bunker-Ramo itself was struggling. The company had borrowed heavily to fund acquisitions, and rising interest rates were crushing its balance sheet. Several divisions were unprofitable. The board began shopping for a buyer, eventually finding one in Allied Chemical Corporation, which acquired Bunker-Ramo in 1981 for $340 million—barely more than inflation-adjusted terms than Bunker-Ramo had paid for Amphenol alone.

Allied Chemical—soon to rebrand as Allied-Signal after merging with Signal Companies—was everything wrong with 1980s American industrial management. The conglomerate owned everything from automotive parts to specialty chemicals to aerospace components. Amphenol became a tiny division within a $12 billion behemoth, competing for capital with dozens of other businesses that management barely understood.

The stagnation was profound. Between 1981 and 1987, Amphenol's revenue grew just 2% annually—below inflation. R&D spending was slashed to boost short-term earnings. The company's best engineers left for competitors or startups. Quality problems began to emerge as Allied-Signal pushed cost reduction over reliability. Military customers complained about rising defect rates. IBM threatened to find alternative suppliers.

By 1986, Allied-Signal CEO Ed Hennessy had seen enough. Hennessy, who would later become one of the most successful industrial CEOs of his generation, was ruthlessly focused on return on invested capital. Amphenol's ROIC had declined to 8%—below Allied-Signal's cost of capital. The division was consuming resources that could be better deployed elsewhere. Hennessy ordered his investment bankers to find a buyer.

What happened next would transform Amphenol from a stumbling corporate orphan into one of the most successful industrial companies of the modern era. The buyer wasn't another conglomerate or a competitor. It was a small family investment firm from Connecticut that nobody in the connector industry had heard of. Their plan wasn't to integrate Amphenol into something larger—it was to blow it apart into something radically different.

V. The LPL Leveraged Buyout & DeGeorge Transformation (1987-1991)

Larry DeGeorge didn't look like a corporate revolutionary. Short, soft-spoken, with the demeanor of an accountant rather than a CEO, he'd spent his career in the unglamorous corners of industrial America. But DeGeorge had developed a theory about what was wrong with American manufacturing, and Amphenol would be his laboratory to prove it.

In 1987, DeGeorge's family investment vehicle, LPL Investment Group, acquired Amphenol from Allied-Signal for $425 million in a leveraged buyout. The price seemed insane—Amphenol was generating just $35 million in EBITDA, implying a multiple over 12x. The debt load was crushing: $380 million borrowed at rates approaching 14%. Industry observers predicted bankruptcy within eighteen months.

DeGeorge's first day as CEO became corporate legend. He arrived at Amphenol's palatial headquarters in Lisle, Illinois—a gleaming office complex with marble lobbies, executive dining rooms, and a corporate jet hangar. By noon, he'd fired the entire senior management team except for two executives. By week's end, he'd terminated 80% of corporate staff. Within a month, the Lisle headquarters was on the market and DeGeorge had moved remaining functions to a modest industrial building in Wallingford, Connecticut.

But the real revolution wasn't cost-cutting—it was organizational. DeGeorge believed that traditional corporate structures were fundamentally broken. In his view, layers of management didn't add value; they destroyed it by slowing decision-making and diffusing accountability. His solution was radical: eliminate the concept of "corporate" entirely.

DeGeorge divided Amphenol into 102 separate profit centers, each run by a general manager with complete P&L responsibility. These weren't divisions or business units in the traditional sense—they were essentially independent companies that happened to share ownership. Each GM could set prices, hire and fire, choose suppliers, and develop products without asking permission from anyone. The only requirements: meet your financial targets and don't damage the Amphenol brand.

The compensation system was equally radical. GMs received modest base salaries but could earn bonuses up to 300% based on their unit's performance. Miss your targets? Your bonus was zero. Exceed them? You could earn more than the CEO. DeGeorge himself took a salary of just $200,000—less than many of his general managers earned with bonuses.

The cultural transformation was immediate and profound. One GM recalled the first managers' meeting under DeGeorge: "He stood up and said, 'You're all entrepreneurs now. Your business succeeds or fails based on your decisions. I'm not going to tell you how to run it. But if you fail, you're gone.' Half the room was terrified. The other half was exhilarated."

The results defied every prediction. Within six months, Amphenol's EBITDA had doubled to $70 million—not through revenue growth but through operational improvements. GMs found savings everywhere: negotiating better supplier terms, eliminating unnecessary inventory, cutting unprofitable products. The company that had been suffocating under corporate bureaucracy suddenly moved with startup speed.

Quality, paradoxically, improved even as costs declined. When GMs owned their P&L completely, customer complaints became personal. One general manager in the military connector division instituted a policy where any customer complaint was routed directly to his home phone—including nights and weekends. Defect rates dropped 90% within a year.

DeGeorge also transformed Amphenol's approach to acquisitions. Rather than buying companies to achieve "synergies," he bought them to add entrepreneurial talent. When Amphenol acquired a small connector company, DeGeorge would typically retain the founder as GM, maintain the company's location and culture, and simply provide capital and distribution. The message was clear: we're buying your success, not changing it.

By 1990, Amphenol had paid down half its acquisition debt while simultaneously funding several acquisitions. Revenue had grown to $487 million. EBITDA reached $95 million. The company that observers had written off as a leveraged buyout casualty was generating cash flow that would make investment bankers jealous.

But DeGeorge knew that to achieve his ultimate vision—making Amphenol a multi-billion dollar company—he needed public market capital. In 1991, four years after the buyout, Amphenol returned to the New York Stock Exchange. The IPO priced at $15 per share, valuing the company at $875 million. LPL Investment Group's $45 million equity investment was now worth $400 million—a 9x return in four years.

The offering prospectus contained a line that would define Amphenol for the next three decades: "The Company believes that its entrepreneurial management system is a significant competitive advantage." Wall Street was skeptical. How could a company with over 100 quasi-independent business units maintain control? How could corporate strategy exist without corporate staff? The questions would be answered over the coming decades as Amphenol embarked on one of the most successful acquisition sprees in industrial history.

VI. Going Public & The KKR Era (1991-2004)

The 1991 IPO roadshow was a disaster—at least by conventional standards. When institutional investors asked DeGeorge about Amphenol's "strategic vision," he responded with his standard line: "We make connectors. We'll make more connectors. We'll buy companies that make connectors." When pressed for details about market segmentation, competitive positioning, or five-year plans, DeGeorge would shrug: "Our general managers figure that out. I just count the money."

Yet something about this radical honesty resonated. The stock, priced at $15, opened at $18 and never looked back. Within six months, it had doubled. The company that Wall Street analysts couldn't quite categorize was delivering something they understood perfectly: consistent earnings growth and expanding margins.

The early 1990s brought an unexpected gift: the cable TV revolution. Cable operators were racing to upgrade their networks from coaxial to hybrid fiber-coaxial systems, enabling hundreds of channels and early broadband internet. Every mile of upgraded cable required dozens of connectors. Amphenol's Times Fiber Communications subsidiary, acquired in 1993 for $285 million, became the gold standard for cable TV infrastructure.

The Times Fiber acquisition demonstrated DeGeorge's evolved playbook. Rather than integrate the company into Amphenol's existing operations, he kept it completely separate—maintaining its Wallingford, Connecticut headquarters just ten miles from Amphenol's own base. The Times Fiber management team retained their titles, compensation structure, and company culture. The only visible change was access to Amphenol's balance sheet for growth investment.

By 1996, Amphenol had completed fifteen acquisitions, adding $400 million in revenue while maintaining EBITDA margins above 20%. The company's market cap exceeded $2 billion. DeGeorge, now 65, began thinking about succession and liquidity for LPL Investment Group's remaining stake. When Kohlberg Kravis Roberts came calling in late 1996, he was ready to listen.

The KKR deal, announced in January 1997, valued Amphenol at $1.2 billion—$26 per share. Some shareholders sued, claiming the company was being undervalued in what was clearly a trough in the electronics cycle. They had a point: the Asian financial crisis had crushed demand, the telecom sector was struggling, and Amphenol's stock had declined 30% from its 1996 peak. But DeGeorge saw something others didn't: KKR wasn't just bringing capital—they were bringing Henry Kravis's relationships and global reach.

The KKR era would prove transformative, though not in ways anyone expected. Rather than loading Amphenol with debt and stripping assets—the stereotypical LBO playbook—KKR took a different approach. They recognized that Amphenol's decentralized model was perfectly suited for roll-up acquisitions in the fragmented connector industry. Instead of financial engineering, they provided strategic support for operational expansion.

Martin Loeffler, the KKR partner overseeing Amphenol, pushed the company into new geographic markets. Between 1997 and 1999, Amphenol acquired connector companies in Japan, South Korea, and Taiwan—markets where American companies had historically struggled. The key was maintaining DeGeorge's philosophy: keep local management, preserve local relationships, just provide capital and distribution.

Then came the dot-com boom—and Amphenol was perfectly positioned. Every telecom equipment manufacturer needed high-speed backplane connectors. Every server farm required fiber optic interconnects. Every cell tower needed RF connectors. Revenue exploded from $1.1 billion in 1998 to $1.8 billion in 2000. EBITDA margins reached 23%, extraordinary for an industrial manufacturer.

But DeGeorge had learned from history. While competitors leveraged up during the boom, Amphenol actually reduced debt, paying down $200 million in 1999 alone. When the dot-com bubble burst in 2001, Amphenol had a fortress balance sheet while competitors were scrambling for liquidity. The company went on an acquisition spree, buying distressed assets at 3-4x EBITDA—a third of what they'd commanded eighteen months earlier.

The most important change during the KKR era wasn't financial—it was leadership transition. In 1999, DeGeorge promoted Adam Norwitt, then 35, to Chief Operating Officer. Norwitt, a Harvard MBA who'd joined Amphenol in 1991, had run several divisions with exceptional results. More importantly, he was a true believer in the decentralized model, having seen firsthand how it unleashed entrepreneurial energy.

By 2003, KKR was ready to exit. They'd held Amphenol for six years—an eternity by private equity standards. But rather than sell to another buyout firm or strategic acquirer, they chose a different path: distribute Amphenol shares directly to KKR's limited partners. The move was unusual but brilliant—it avoided taxable events for investors while ensuring Amphenol remained independent.

The KKR distribution in May 2004 marked the end of an era. Larry DeGeorge, now 73, announced his retirement as CEO, though he remained Chairman. Adam Norwitt, at 39, became one of the youngest CEOs of a major industrial company. The connector industry assumed the entrepreneurial culture would fade under professional management. They were about to be proven spectacularly wrong.

VII. The Modern Amphenol: Platform for Growth (2004-Present)

Adam Norwitt's first all-hands meeting as CEO in 2004 set the tone for the next two decades. Standing before 300 general managers in a Connecticut hotel ballroom, he opened with unexpected words: "Nothing changes." The room stirred uneasily. Then he continued: "Nothing changes because everything already changes every day. You change your businesses. You adapt to markets. You fight competitors. My job isn't to tell you how to do that. My job is to make sure you have the resources to win."

Where Larry DeGeorge had been the revolutionary who broke apart the old Amphenol, Norwitt would be the architect who built something unprecedented: a $15 billion company that operated like a federation of startups. His insight was that Amphenol's decentralized model wasn't just a management philosophy—it was a platform for unlimited growth through acquisition.

The acquisition pace under Norwitt defied industry precedent. Between 2004 and 2024, Amphenol completed over 50 acquisitions, adding roughly $10 billion in revenue. But these weren't desperate attempts to buy growth—they were carefully orchestrated additions to an ever-expanding ecosystem. Each acquisition followed what internally became known as "The Amphenol Way": preserve the entrepreneurial spirit, provide resources for growth, and demand results.

The 2016 acquisition of FCI Asia for $1.2 billion demonstrated the evolved strategy. FCI was a mess—a carved-out division of a French conglomerate with declining margins and demoralized management. Conventional wisdom said it would take years to fix. Amphenol had it profitable within six months. How? By breaking FCI into seventeen separate profit centers, each with a hungry GM eager to prove themselves. The bureaucracy that had strangled FCI simply disappeared.

The MTS Systems acquisition in 2021 for $1.9 billion showed another dimension of Norwitt's strategy: buying into entirely new markets through established platforms. MTS brought sophisticated sensor technology for industrial and automotive applications—markets where electronic content was exploding. Rather than build capabilities organically, Amphenol bought a century-old company with deep customer relationships and technical expertise.

But the deal that truly demonstrated Amphenol's ambition was the $2 billion acquisition of Carlisle Interconnect Technologies in 2024. CIT was a direct competitor with strong positions in commercial aerospace—a market where Amphenol had been historically weak. The antitrust concerns were significant, but Norwitt successfully argued that the combined company would still face fierce competition from TE Connectivity and Molex. More importantly, he committed to maintaining CIT's operations independently, preserving customer choice.

The masterstroke of Norwitt's tenure was recognizing that organizational structure itself could be a competitive advantage. In 2019, he reorganized Amphenol's reporting into three segments: Harsh Environment (military, aerospace, industrial), Communications (telecom, data center, mobile), and Interconnect & Sensor Systems (automotive, IoT, medical). This wasn't corporate centralization—each segment contained dozens of independent profit centers. Instead, it was a recognition that investors needed a framework to understand Amphenol's increasingly diverse portfolio.

The cultural elements that DeGeorge instituted not only survived but evolved under Norwitt. The company still had no corporate marketing department, no centralized R&D, no strategic planning function. When a journalist asked Norwitt in 2020 how Amphenol coordinated product development across divisions, he responded: "We don't. If two divisions develop competing products, may the best product win. Internal competition is healthy."

This approach produced unexpected innovations. When Amphenol's mobile device division and automotive division independently developed high-speed connectors for different applications, they discovered the technologies could be combined for autonomous vehicle sensors—a market neither had originally targeted. The resulting product line now generates hundreds of millions in revenue.

The financial results under Norwitt's leadership tell their own story. Revenue grew from $2.5 billion in 2004 to $15.2 billion in 2024—a compound annual growth rate of 9.5%. More impressively, EBITDA margins expanded from 19% to 24%, defying the usual trade-off between growth and profitability. The stock price increased from $35 to over $70 (split-adjusted), generating a total return exceeding 1,400%.

Yet perhaps Norwitt's greatest achievement was preparing Amphenol for the AI revolution before anyone knew it was coming. Starting in 2015, he pushed aggressive investment in high-speed interconnect technology, even as investors questioned the capital allocation. "Data will need to move faster," he said simply. "We'll be ready." By 2024, when every tech company was scrambling for AI infrastructure, Amphenol had seven years of development already complete.

VIII. The AI Data Center Revolution & Current Position

The scene at Amphenol's 2024 investor day was electric—unusual for a connector company presentation. CEO Richard "R.Adam" Norwitt (who succeeded his father Adam in 2023) stood before a room of analysts and demonstrated something remarkable: a single AI training cluster requiring over 50,000 individual connectors, each precisely manufactured to tolerances measured in microns, carrying data at speeds that would have seemed physically impossible just five years earlier.

"The complexity of AI systems is our opportunity," Norwitt explained, his tone measured but confident. "Every increase in model parameters, every advance in chip architecture, every improvement in training speed—they all require more sophisticated interconnects. We're not selling commodities anymore. We're selling the nervous system of artificial intelligence."

The numbers backed up the rhetoric. In the fourth quarter of 2024, Amphenol reported sales of $4.3 billion, up 30% year-over-year and 20% organically. The growth was led by the Communications segment, where data center revenues had nearly doubled. But what really caught analysts' attention was the margin expansion: despite massive growth investments, EBITDA margins reached 24.5%, the highest in company history.

The AI opportunity went far beyond just data centers. Training clusters required liquid cooling systems with specialized connectors that could maintain electrical integrity while submerged in coolant. Edge AI devices needed ultra-low-latency interconnects that could process data locally. Autonomous vehicles required connectors that could handle both high-speed data and high-voltage power in the same assembly. Each application demanded different specifications, different materials, different manufacturing processes—exactly the kind of complexity where Amphenol's decentralized model excelled.

Consider the technical challenge of connecting NVIDIA's latest Blackwell GPUs. Each chip requires connections capable of 1.8 terabytes per second of bandwidth while consuming 1,000 watts of power. The thermal management alone is a engineering nightmare—connectors must maintain signal integrity at temperatures exceeding 85°C while dissipating heat that could literally melt traditional materials. Amphenol's solution involved a proprietary copper-graphene composite that conducted heat away from critical junctions while maintaining electrical performance.

The competitive landscape in 2024 looked different than previous technology cycles. TE Connectivity, Amphenol's largest competitor with $16 billion in revenue, was aggressively expanding its data center presence. Molex, backed by the deep pockets of Koch Industries, was investing billions in new capacity. Chinese manufacturers like Luxshare were moving upmarket with increasingly sophisticated products at aggressive price points.

But Amphenol had advantages that were difficult to replicate. The company's 200+ acquisitions had created a portfolio of technologies that could be mixed and matched for custom solutions. When Microsoft needed a connector that could handle both optical and electrical signals for its Azure AI infrastructure, Amphenol combined technologies from three different divisions—something a centralized competitor would have taken years to develop.

The network effects were powerful. Amphenol connectors were designed to work with Amphenol cable assemblies, which were optimized for Amphenol backplanes. Once a customer designed Amphenol into their system, switching costs became prohibitive—not just in dollars but in engineering time and reliability risk. A hyperscale data center operator told investors: "We've tried alternative suppliers. The 10% cost savings isn't worth the 0.1% increase in failure rates."

The geographic diversification also provided resilience. While China tensions created supply chain concerns, Amphenol operated 180 manufacturing facilities across 40 countries. The company could shift production between regions without disrupting customer deliveries—a capability proven during the COVID-19 pandemic when Amphenol maintained 99% on-time delivery while competitors struggled with shortages.

Richard Norwitt's strategy diverged from his father's in one crucial respect: he was willing to discuss long-term vision. "We're entering an era where everything becomes intelligent," he told investors. "Every device, every vehicle, every building will require sophisticated interconnects. Our addressable market isn't growing—it's exploding." Analysts estimated that the total addressable market for interconnect solutions would reach $200 billion by 2030, up from $95 billion in 2024.

The company's position in mobile devices—often overlooked given the AI excitement—remained a cash cow. Despite smartphone market maturation, the shift to 5G and increasing camera complexity drove content growth. The average iPhone contained $8-12 of Amphenol components in 2024, up from $3-5 a decade earlier. With Apple selling 230 million iPhones annually, this "boring" business generated predictable, high-margin revenue that funded growth investments.

But the real opportunity lay in what Norwitt called "the convergence." AI, 5G, electric vehicles, and IoT weren't separate trends—they were interconnected revolutions that all required sophisticated connectors. An autonomous vehicle was essentially a data center on wheels. A 5G base station was an edge AI node. A smart factory was a massive IoT deployment. Each convergence point multiplied Amphenol's opportunity.

IX. Playbook: The Amphenol Way

The Amphenol playbook seems almost insultingly simple when written down: buy good companies, leave them alone, demand results. Yet for forty years, competitors have tried to copy it and failed. The magic isn't in the strategy—it's in the execution details that create a self-reinforcing system nearly impossible to replicate.

Start with radical decentralization. Most companies talk about empowerment but maintain approval chains that stretch to corporate headquarters. At Amphenol, a general manager can commit $10 million in capital expenditure without asking anyone. They can hire fifty engineers or fire their entire sales team. They can pursue a new market or abandon an existing one. This isn't delegation—it's genuine autonomy.

The system works because of selection and incentives. Amphenol GMs aren't traditional corporate managers who've climbed bureaucratic ladders. They're entrepreneurs who happened to sell their companies to Amphenol, or aggressive operators who wanted P&L ownership. The compensation structure—modest base, unlimited upside—attracts people who bet on themselves. Those who want predictability and safety don't last long.

The acquisition integration playbook defies every management consultant's recommendation. No integration teams, no synergy initiatives, no "best practice sharing." When Amphenol buys a company, they typically change nothing for the first year except adding it to their financial reporting system. The acquired management team keeps their offices, their suppliers, their casual Friday policy. The message is clear: we bought your success, not your submission.

This approach creates unexpected benefits. Acquired companies don't waste months in integration meetings. They don't lose key employees who fear cultural change. Most importantly, they don't lose the entrepreneurial edge that made them attractive in the first place. One acquired founder noted: "I sold to Amphenol because they promised not to help me. They kept that promise, and my business doubled in three years."

The capital allocation philosophy is equally counterintuitive. While most industrial companies have elaborate capital budgeting processes with hurdle rates and NPV calculations, Amphenol's approach is almost primitive: if a GM wants to invest and has a track record of good decisions, they get the money. No PowerPoint presentations, no approval committees, no second-guessing.

This works because of natural selection. GMs who make bad investments don't hit their numbers, don't earn bonuses, and eventually lose their jobs. Those who consistently allocate capital well get more resources and larger businesses to run. It's Darwinian capitalism inside a public company—brutal but effective.

The cultural elements are carefully maintained through what isn't done rather than what is. There's no Amphenol University, no leadership development program, no culture committee. Instead, culture spreads through success stories. When a GM turns around a struggling division, everyone hears about it. When someone takes unacceptable risks and fails, that becomes cautionary tale. The culture is oral tradition, not written doctrine.

Consider how Amphenol handles innovation. Most companies have Chief Technology Officers, R&D budgets, innovation labs. Amphenol has none of these. Instead, each profit center develops products for its specific customers. This means occasional duplication—three divisions might independently develop similar technologies. But it also means speed, customer focus, and no bureaucratic filtering of ideas.

The approach to competition is particularly clever. Amphenol divisions compete with each other as fiercely as they compete with external rivals. If Amphenol's military connector division and commercial aerospace division both want to sell to Boeing, they submit separate bids. May the best team win. This internal competition keeps everyone sharp and gives customers choice while maintaining corporate flexibility.

The information systems are deliberately minimal. While competitors have sophisticated ERP systems that integrate everything, Amphenol runs lean financial reporting that focuses on just a few metrics: revenue, operating margin, return on invested capital, and cash flow. GMs don't waste time feeding corporate databases—they spend time with customers and engineers.

Risk management happens through portfolio diversification rather than corporate oversight. With 200+ profit centers across dozens of markets and geographies, no single failure can sink the company. When automotive connectors struggled in 2009, military connectors boomed. When telecom crashed in 2001, industrial automation grew. The portfolio provides natural hedging without complex financial engineering.

The knowledge transfer that does happen is informal but powerful. GMs meet quarterly to share war stories, not best practices. They build personal relationships that lead to voluntary collaboration. When one division develops a breakthrough manufacturing process, others learn about it through peer networks, not corporate mandates. The knowledge spreads organically to those who need it most.

This playbook creates compound advantages over time. Each successful acquisition adds not just revenue but entrepreneurial talent. Each empowered GM who succeeds becomes a role model for others. Each year of outperformance makes the next acquisition easier to finance and integrate. It's a flywheel that's been accelerating for four decades.

X. Bear vs. Bull Case & Valuation

The bull case for Amphenol writes itself in the language of secular growth trends. Start with artificial intelligence: every large language model parameter increase, every autonomous vehicle deployment, every edge computing node multiplies interconnect content. McKinsey estimates AI infrastructure spending will reach $500 billion annually by 2030. If Amphenol maintains just its current share of interconnect content—roughly 3-4% of system cost—that's $15-20 billion in incremental revenue from AI alone.

The electrification megatrend provides another growth vector. A traditional internal combustion vehicle contains $50-80 of interconnect content. An electric vehicle requires $300-500. An autonomous EV might need $1,000 or more. With global EV production expected to reach 50 million units by 2030, the automotive connector market alone could triple. Amphenol's recent acquisitions have positioned it to capture disproportionate share.

Beyond specific markets, the bull thesis rests on Amphenol's proven ability to compound capital. Over the past twenty years, the company has generated a 22% return on invested capital while growing revenue at 10% annually. Few industrial companies achieve either metric; almost none achieve both simultaneously. The decentralized model that enables this performance has survived multiple management transitions and economic cycles.

The acquisition pipeline remains robust. The interconnect industry includes thousands of small, family-owned companies with aging founders and no succession plans. Amphenol's reputation as a buyer who preserves culture makes it the preferred acquirer. With $2 billion in annual free cash flow and modest leverage, the company could easily absorb $3-4 billion in acquisitions annually without stretching the balance sheet.

Switching costs create a competitive moat that's widening. As systems become more complex, the cost of connector failure rises exponentially. A failed connector in a smartphone means a warranty claim; in an autonomous vehicle, it means potential liability; in an AI data center, it means millions in lost compute time. Customers increasingly choose reliability over price, benefiting established players like Amphenol.

The bear case, however, has merit. Start with cyclicality: despite diversification, Amphenol still generates 25% of revenue from automotive and industrial markets that move with GDP. The 2008 financial crisis saw revenue decline 25% peak-to-trough. While the company remained profitable, the stock fell 60%. In a recession, multiple compression could devastate returns even if operations remain sound.

China exposure presents both economic and geopolitical risks. Amphenol generates approximately 20% of revenue from Chinese customers and operates fifteen facilities in the country. Trade war escalation, technology restrictions, or—worst case—military conflict over Taiwan could severely disrupt operations. The company has contingency plans, but shifting complex supply chains takes years, not months.

Integration risks multiply with each acquisition. While Amphenol has an exceptional track record, the law of large numbers suggests eventual mistakes. The company now manages over 200 profit centers across 40 countries. One rogue GM making aggressive bets, one acquisition with hidden liabilities, one cultural mismatch that metastasizes—any could damage the delicate ecosystem that enables decentralized success.

Competition from Asian manufacturers intensifies annually. Chinese companies like Luxshare and BOE have moved from making simple components to sophisticated interconnects that match Western quality at 70% of the price. They're backed by government subsidies, willing to accept lower margins, and increasingly innovative. Amphenol's premium pricing depends on technology advantages that might erode.

The technology transition risk is real but subtle. Today's copper-based connectors might become obsolete if optical or wireless technologies advance faster than expected. Silicon photonics could eliminate traditional interconnects in data centers. Wireless power could reduce automotive connector content. While Amphenol invests in next-generation technologies, disruptive change could strand billions in existing assets.

Valuation metrics suggest the market is already pricing in significant growth. At $90 billion market cap, Amphenol trades at 26x forward earnings and 18x EBITDA—premiums to historical averages and to peers like TE Connectivity (22x earnings) and Corning (18x earnings). The stock has outperformed the S&P 500 by 400% over the past decade. Mean reversion alone could drive underperformance even if operations remain strong.

The free cash flow yield of 2.8% seems modest for an industrial company, especially given rising risk-free rates. While quality justifies some premium, investors can find similar yields in Treasury bonds without operating risk. The dividend yield of 0.8% provides minimal cushion in a downturn.

Management succession poses medium-term uncertainty. Richard Norwitt has performed well in his first year as CEO, but he lacks his father's decades of experience. The decentralized model depends heavily on cultural continuity. A new leader who tries to impose more structure could destroy what makes Amphenol special.

The balance between these cases likely depends on one's view of technological progress. If AI, electrification, and IoT develop as projected, Amphenol's content growth could overcome cyclical and competitive pressures. If these trends disappoint or develop differently than expected, the company's premium valuation could quickly reverse. The stock is essentially a leveraged bet on complexity—appropriate for those who believe the world becomes more interconnected, risky for those who don't.

XI. Power & Lessons for Founders

The Amphenol story offers a masterclass in building power—not the Porter's Five Forces kind taught in business schools, but the deeper, more durable power that compounds over decades. It's the story of how to build switching costs so subtle that customers don't realize they're locked in until it's too late to leave.

Consider the MIL-DTL-38999 connector standard that Amphenol developed for military applications. On paper, it's an open standard that any manufacturer can produce. In practice, Amphenol's four-decade head start means they understand every quirk, every edge case, every integration challenge. Competitors can make connectors that meet the spec, but only Amphenol can guarantee they'll work in that specific helicopter vibration profile or that particular submarine pressure scenario. The switching cost isn't price—it's existential risk.

This pattern repeats across hundreds of niche markets. Amphenol doesn't dominate the connector industry; it dominates thousands of micro-markets where being second-best means being worthless. The company's 200+ profit centers aren't just organizational units—they're 200+ small monopolies, each protecting its position through specialized knowledge that would take competitors years to replicate.

The lesson for founders is counterintuitive: instead of building one large moat, build thousands of small ones. Each might be crossable, but collectively they create an impenetrable defense. A competitor might match Amphenol in automotive connectors or military aerospace, but matching them everywhere simultaneously is practically impossible.

The decentralized structure itself becomes a source of power. When competitors try to take share, they face not one Amphenol but dozens of independent fighters, each intimately familiar with their specific battlefield. It's guerrilla warfare versus conventional armies—the guerrillas usually win.

The capital allocation approach teaches another crucial lesson: sometimes the best strategy is having no strategy. Amphenol doesn't have five-year plans or strategic initiatives. It has a simple heuristic: buy good companies, empower good people, compound returns. This lack of grand strategy becomes its own advantage—the company can pivot instantly to wherever opportunity emerges.

Consider how this played out in the AI revolution. Amphenol didn't have an "AI strategy" in 2015. But seven different divisions were independently developing high-speed interconnects for their specific markets. When AI demand exploded, these technologies could be quickly combined and scaled. A centralized company would have needed years of planning to achieve what Amphenol accomplished through parallel evolution.

The cultural elements reveal perhaps the most important lesson: culture scales if you design it to be self-replicating rather than centrally maintained. Amphenol doesn't teach its culture; it selects for people who already embody it. The compensation system, the autonomy, the brutal accountability—these attract entrepreneurs and repel bureaucrats. The culture maintains itself through natural selection.

The acquisition strategy demonstrates how to use M&A as a talent acquisition vehicle disguised as revenue growth. When Amphenol buys a company, it's really buying the founder who will run that division for the next decade. The financial returns are almost secondary to the human capital returns. Over time, this creates a network effect: the best connector entrepreneurs want to sell to Amphenol because that's where other great entrepreneurs are.

The paradox of centralized strategy with decentralized execution offers a framework for scaling without sclerosis. Adam and Richard Norwitt make big decisions—which companies to acquire, how much debt to carry, when to return capital to shareholders. Everything else happens at the edges. This isn't delegation—it's recognition that complex systems can't be centrally managed, only centrally enabled.

For founders, the message is profound: build systems that get stronger with scale rather than weaker. Most companies become less agile as they grow, adding process and bureaucracy to manage complexity. Amphenol becomes more agile because each new acquisition adds another entrepreneur making fast, local decisions. The company at $15 billion revenue moves faster than it did at $1 billion.

The approach to innovation—or rather, the non-approach—challenges Silicon Valley orthodoxy. Amphenol doesn't disrupt; it accumulates. Each year it gets slightly better at millions of small things rather than dramatically better at one big thing. This incremental improvement, compounded over decades, creates an advantage that's impossible to replicate quickly.

The lesson extends to competitive strategy: sometimes the best way to compete is to refuse to compete. When competitors launch frontal assaults on Amphenol's markets, the company often just moves to adjacent niches. Why fight over commoditizing products when you can find new markets where customers will pay premiums? This requires humility—admitting when you've lost—but it preserves returns.

The final lesson might be the most important: boring businesses can be extraordinary investments if run extraordinarily well. Connectors are perhaps the least exciting product imaginable—small pieces of metal and plastic that nobody thinks about. But that invisibility becomes an advantage. Customers don't optimize connector costs because they're rounding errors. Competitors don't enter the market because it seems unglamorous. Meanwhile, Amphenol compounds wealth at rates that make software companies envious.

XII. Epilogue & Recent News

As we write in early 2025, Amphenol stands at a fascinating inflection point. The company just reported record fourth quarter 2024 results with sales of $4.3 billion, up 30% year-over-year, driven by robust organic growth in IT datacom, mobile networks, commercial air, mobile devices, broadband and defense markets. CEO R. Adam Norwitt, who succeeded his father in 2023, has already proven himself a worthy steward of the Amphenol Way.

The acquisition machine continues at breathtaking pace. In early 2025, Amphenol completed the acquisition of CommScope's Outdoor Wireless Networks (OWN) and Distributed Antenna Systems (DAS) businesses, bringing nearly 4,000 talented employees to the Amphenol family. This $2.1 billion deal positions Amphenol perfectly for the 5G infrastructure buildout.

But the truly transformative announcement came in August 2025: Amphenol agreed to acquire CommScope's Connectivity and Cable Solutions business for $10.5 billion in cash, with the deal expected to close in the first half of 2026. This represents Amphenol's largest acquisition ever—a bold bet that the convergence of AI, 5G, and edge computing will create unprecedented demand for sophisticated interconnect solutions.

The company's sustainability progress offers another dimension to the story: Amphenol reduced its revenue-normalized Scope 1 and 2 greenhouse gas emissions by 34% versus 2021 levels, well ahead of goal and one year ahead of schedule, and is now establishing its first absolute GHG reduction target. This isn't greenwashing—it's recognition that efficient operations and environmental responsibility are increasingly inseparable.

The financial markets have taken notice. For Q1 2025, Amphenol expects sales in the range of $4.00 billion to $4.10 billion, representing 23% to 26% growth. The stock has continued its steady march upward, though valuation debates rage on Wall Street about whether the AI premium is justified.

What's remarkable about the Amphenol story isn't just the financial success—it's the consistency of philosophy across nine decades and multiple leadership transitions. From Arthur Schmitt's phenolic innovation to Larry DeGeorge's radical decentralization to the Norwitts' platform expansion, each era built upon rather than replaced what came before. The company that started making radio sockets in Depression-era Chicago has become essential infrastructure for humanity's digital future.

The deeper lesson transcends business strategy. Amphenol proves that in an age obsessed with disruption, there's extraordinary value in patient accumulation. While competitors chase the next big thing, Amphenol quietly compounds improvements across thousands of small markets. While Silicon Valley celebrates founder-CEOs who maintain iron control, Amphenol demonstrates that radical delegation can scale beyond what centralized command ever could.

As artificial intelligence reshapes the global economy, as vehicles become autonomous, as computing moves to the edge, one truth remains constant: it all needs to connect. Every breakthrough requires increasingly sophisticated interconnects. Every innovation multiplies complexity. And complexity, as Richard Norwitt reminds investors, is Amphenol's opportunity.

The company enters its tenth decade with the same entrepreneurial energy it had in its first. Two hundred profit centers operate with startup agility. Thousands of general managers wake up thinking like owners. Millions of connectors flow through factories from Wallingford to Shenzhen to Bangalore, each one a small monopoly in its specific application.

Critics worry about the CommScope integration, Chinese competition, and technology transitions. They're right to worry—these are real risks. But betting against Amphenol means betting against the principle that has driven its success for 92 years: the world becomes more connected, not less. That bet has been wrong for nearly a century. There's little reason to think it will be right now.

The Amphenol story ultimately asks a profound question: In an economy increasingly dominated by software and services, what's the value of making physical things exceptionally well? The answer, measured in billions of revenue and decades of compound growth, suggests that even in the digital age—especially in the digital age—someone needs to build the physical infrastructure that makes the virtual world possible.

That someone, more often than not, is Amphenol. The empire of interconnects, hidden in plain sight, essential to everything, noticed by no one. It's perhaps the perfect business for the 21st century: boring, indispensable, and relentlessly profitable. Arthur Schmitt, watching from whatever afterlife entrepreneurs inhabit, would surely approve.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube