Atlas Copco: The Swedish Titan Building Tomorrow's Industry

I. Introduction & Episode Roadmap

Picture this: Deep beneath the Swiss Alps, engineers are boring through solid granite to create the Gotthard Base Tunnel—at 57 kilometers, the world's longest railway tunnel. The drilling equipment powering through that ancient rock? Atlas Copco. Meanwhile, 8,000 kilometers away in a pristine semiconductor fab in Taiwan, the same company's vacuum pumps are creating the near-perfect void necessary to etch transistors just 3 nanometers wide onto silicon wafers. And in a Tesla Gigafactory, their precision tools are assembling the electric vehicles of tomorrow.

This is Atlas Copco—a 150-year-old Swedish industrial giant that most people have never heard of, yet whose technology touches nearly every aspect of modern life. With over $20 billion in revenue and operations spanning 180 countries, this company has mastered the art of being everywhere while remaining invisible.

How does a railway equipment manufacturer founded in 1873 Stockholm become the backbone of semiconductor manufacturing in 2024? How does a company survive multiple existential crises, two world wars, and countless economic cycles to emerge stronger each time? And perhaps most intriguingly—how does a Swedish industrial conglomerate built on compressed air become essential to the AI revolution?

The Atlas Copco story isn't just about industrial equipment. It's a masterclass in portfolio management, a testament to Swedish capitalism's unique model, and a case study in how patient capital and engineering excellence can compound over centuries. It's about the Wallenberg dynasty—Sweden's most powerful business family—and their multi-generational bet on industrial technology. It's about knowing when to buy, when to build, and crucially, when to split apart what you've spent decades assembling.

Today's journey takes us from the gaslit boardrooms of 1870s Stockholm to the clean rooms of modern semiconductor fabs. We'll explore how Atlas Copco built, acquired, and sometimes divested its way to becoming one of the world's most successful industrial companies. We'll examine the Swedish Method that revolutionized mining, the vacuum acquisitions that positioned them for the semiconductor boom, and the bold decision to split the company in 2018—walking away from their mining heritage to focus on tomorrow's industries.

This is also a story about transformation at scale. About a company that has reinvented itself multiple times: from Atlas to Atlas Diesel to Atlas Copco, from railway equipment to rock drills to compressors to vacuum pumps. Each transformation required not just technical innovation but the courage to abandon what made you successful yesterday for what will make you essential tomorrow.

As we navigate through Atlas Copco's remarkable journey, we'll uncover the playbook that has made this company a compounding machine: radical decentralization that pushes decision-making to the front lines, an acquisition strategy that has integrated over 100 companies, and a service model that transforms one-time equipment sales into recurring revenue streams. We'll see how boring B2B businesses—the picks and shovels of the industrial world—can generate extraordinary returns over time.

II. Origins & The Wallenberg Foundation (1873-1920s)

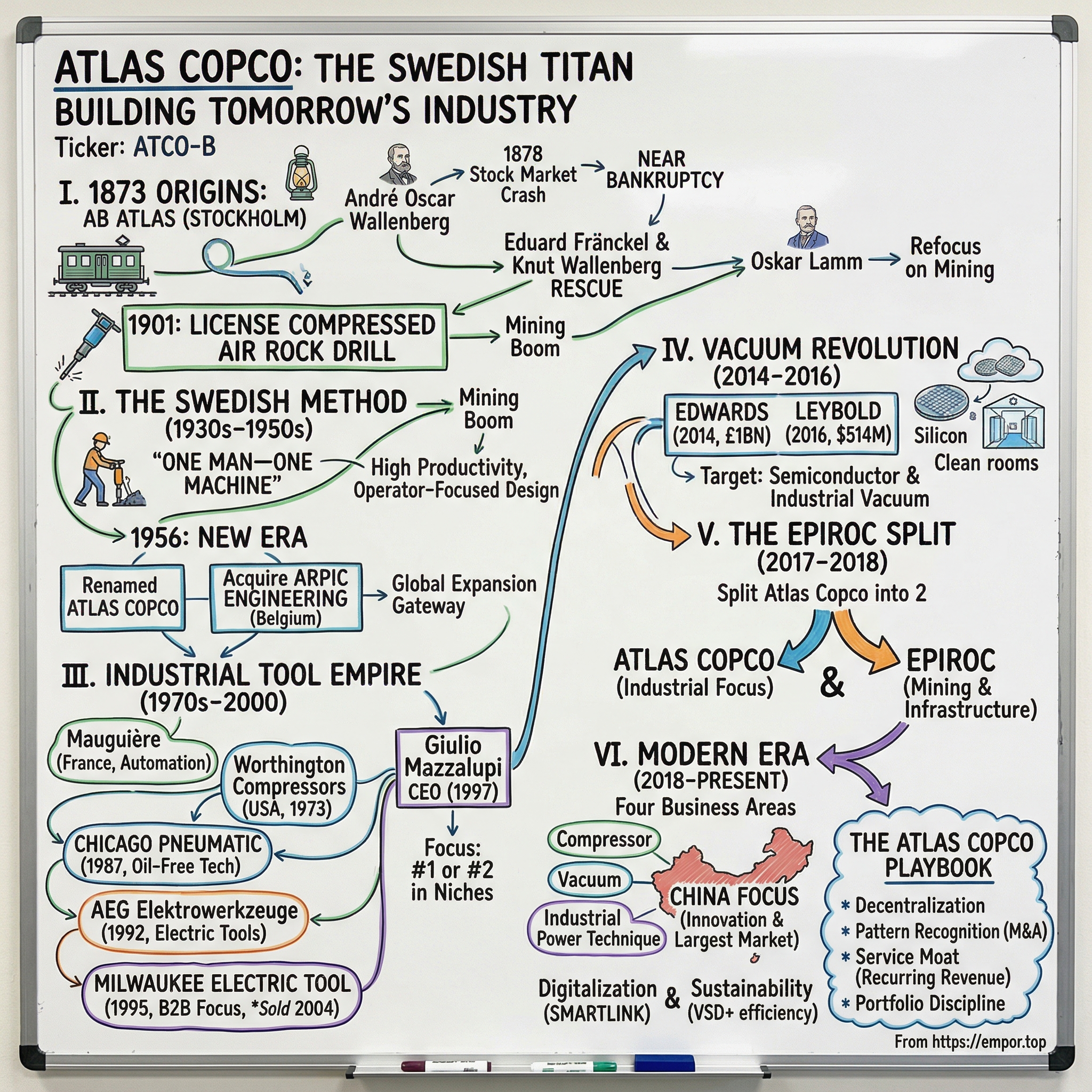

The gas lamps of Stockholm flickered in the February cold of 1873 as André Oscar Wallenberg, at just 56 years old but already one of Sweden's most prominent bankers, gathered with three partners in a modest office. Sweden was experiencing its first industrial boom, railways were being laid across the nation's harsh terrain, and Wallenberg saw opportunity where others saw only frozen wilderness and granite mountains. That night, they signed the papers creating AB Atlas—named after the Greek Titan condemned to hold up the heavens for eternity.

The name choice wasn't accidental. Wallenberg envisioned a company that would literally support the weight of Sweden's industrial transformation. The initial focus was pragmatic: manufacturing railway equipment for Statens Järnvägar (Swedish State Railways). Sweden needed to connect its iron ore deposits in the north with ports in the south, and every meter of track required switches, signals, and rolling stock.

The early years were promising. Atlas quickly established itself as a reliable supplier, its workshops in Stockholm humming with activity. Engineers from across Europe visited to study their designs. By 1877, the company had expanded beyond railway equipment into heating systems and machine tools. Revenue grew steadily, and Wallenberg's reputation as a visionary industrialist seemed secure.

Then came 1878.

The Stockholm stock market crashed with a violence that shocked even seasoned financiers. Banks failed overnight. Construction projects—including most of Sweden's ambitious railway expansion—ground to a halt. Atlas, which had borrowed heavily to finance its growth, found itself with warehouses full of railway equipment that nobody wanted to buy. The company that was supposed to hold up Sweden's industrial heavens was instead being crushed under the weight of its own ambitions.

By 1880, bankruptcy seemed inevitable. André Oscar Wallenberg, whose personal fortune was tied to the company, faced ruin. But here emerged the first glimpse of what would become the Wallenberg dynasty's defining characteristic: the ability to think in decades, not quarters.

Enter Eduard Fränckel, a German-Jewish engineer who had earned André Oscar's trust, and more importantly, his nephew Knut Wallenberg, who would later found the Wallenberg industrial empire. Together, they orchestrated a rescue that would establish a pattern repeated throughout Atlas's history. They brought in fresh capital from the extended Wallenberg network, restructured the company's debts, and most radically, brought in outside management.

The savior was Oskar Lamm, a brilliant engineer with a reputation for turning around distressed industrial companies. Lamm's first act was symbolic but powerful: he renamed the company Nya Atlas—New Atlas—signaling a break from the past. His second act was more practical: he slashed costs, sold off non-core assets, and refocused on the company's most profitable products.

But Lamm's real genius lay in recognizing that Sweden's industrial future wasn't in railways but in mining. The country sat atop vast deposits of iron ore, but extracting it from the frozen ground required new technology. In 1901, Lamm made a decision that would transform Atlas forever: he licensed the production rights for a new type of rock drill powered by compressed air.

The compressed air drill was revolutionary. Unlike steam-powered equipment, it could operate in confined spaces without suffocating workers. Unlike manual drilling, it could bore through granite at ten times the speed. Lamm saw immediately that this wasn't just a product—it was a platform. Once you had compressed air infrastructure in a mine, you could power ventilation systems, hoists, and eventually, entire automated processes.

By 1917, with World War I raging and demand for Swedish iron ore at historic highs, the company made another pivotal transformation. It merged with Diesel Motorer, a company producing diesel engines, and renamed itself AB Atlas Diesel. The logic was elegant: diesel engines could power air compressors in remote locations where electrical infrastructure didn't exist. The company now had an integrated solution for mining anywhere in the world.

The Wallenberg influence during this period extended far beyond capital. The family's network opened doors across Europe. When Atlas Diesel needed to license technology from German or American companies, a Wallenberg introduction smoothed the way. When the company needed long-term contracts with mining companies, the family's reputation for honoring agreements—even when disadvantageous—proved invaluable.

Marcus Wallenberg Sr., who joined the board in 1916, embodied this long-term thinking. In board meetings, he would often ask: "What will this decision look like in twenty years?" This question, simple as it sounds, would guide Atlas through the turbulent decades ahead. It meant investing in research during recessions, maintaining customer relationships even when unprofitable, and most importantly, building a culture that thought beyond the next quarterly earnings report.

The 1920s brought both opportunity and challenge. The post-war reconstruction boom created massive demand for compressed air equipment, but competition intensified as American and German manufacturers entered the Swedish market. Atlas Diesel's response was characteristically Swedish: rather than compete on price, they would compete on reliability and innovation. The company established one of Europe's first industrial research laboratories, staffed with PhDs from the Royal Institute of Technology.

This period also saw the emergence of what would become Atlas's most important cultural principle: decentralization. As the company expanded across Sweden and into Norway and Finland, headquarters realized that local managers understood their markets better than executives in Stockholm. Rather than impose central control, Atlas Diesel gave significant autonomy to regional operations. This principle—that whoever is closest to the problem is best positioned to solve it—would become a cornerstone of the company's management philosophy.

By the late 1920s, Atlas Diesel had transformed from a near-bankrupt railway equipment manufacturer into one of Europe's leading compressed air companies. Revenue had grown twenty-fold since Lamm's rescue. The company employed over 2,000 people. Most importantly, it had established the three pillars that would support its growth for the next century: patient capital from the Wallenberg family, a focus on technical excellence, and a decentralized structure that encouraged entrepreneurship.

As the 1920s drew to a close, Atlas Diesel stood at another crossroads. The company had conquered the Nordic market, but the real opportunity lay beyond Sweden's borders. The question was how to expand internationally while maintaining the company's Swedish soul.

III. The Swedish Method & Global Expansion (1930s-1960s)

The year was 1936, and deep in the Kiruna iron mine—the world's largest underground ore extraction operation—something extraordinary was happening. A single miner, Gustaf Andersson, stood before a wall of solid magnetite, operating a pneumatic drill rig that would have required three men just five years earlier. This was the Swedish Method in action: "One man—one machine." While American and Soviet mines still relied on teams of workers manually positioning heavy equipment, Atlas Diesel had engineered lightweight, aluminum-alloy drill rigs that transformed mining from brute force into precision engineering.

The Swedish Method wasn't just about the equipment—it was a philosophy that would propel Atlas Diesel from a regional player into a global force. The concept emerged from Sweden's unique labor dynamics: high wages, strong unions, and a chronic worker shortage that forced companies to maximize productivity rather than simply adding more bodies. Where American mining companies could throw hundreds of workers at a problem, Swedish operations had to make each worker exponentially more productive.

Erik Johnsson, who became managing director in 1935, understood this dynamic intimately. A former mining engineer himself, Johnsson had spent months underground studying how workers actually used equipment—not how engineers assumed they used it. He noticed that most accidents and inefficiencies came from equipment that fought against human physiology rather than working with it. His mandate to Atlas Diesel's engineers was revolutionary for its time: design for the operator first, the rock second.

The results were dramatic. By 1938, Swedish mines using Atlas Diesel equipment reported productivity gains of 300% per worker compared to traditional methods. The Grängesberg mine became a pilgrimage site for mining engineers worldwide, who came to witness single operators controlling sophisticated drill rigs via pneumatic controls, achieving precision that teams of workers couldn't match elsewhere.

World War II, paradoxically, accelerated Atlas Diesel's international expansion. As a neutral country, Sweden could trade with both Allied and Axis powers, though carefully and with significant restrictions. Atlas Diesel equipment found its way into mines across Europe, often through complex transactions involving Swiss intermediaries and creative payment arrangements. The company's reputation for reliability became legendary—Atlas Diesel compressors kept running in conditions that destroyed competitors' equipment.

But the real transformation came in 1956, a year that would define Atlas's trajectory for the next half-century. The company's board, led by Marcus Wallenberg Jr.—known as "Dodde" to distinguish him from his father—made two decisions that seemed unrelated but were actually part of a grand strategy.

First, they renamed the company Atlas Copco, derived from Compagnie Pneumatique Commerciale, the Belgian company they had acquired. The name change signaled a shift from Swedish industrialist to global player. "Diesel" was yesterday; "Copco" suggested cosmopolitan sophistication and international ambition.

Second, and more importantly, they acquired the remainder of Arpic Engineering in Belgium. This wasn't just another acquisition—it was Atlas Copco's first major international production facility. The Antwerp factory would eventually manufacture the majority of the company's compressor production, but its real value was strategic. Belgium provided access to the European Economic Community (precursor to the EU), sophisticated supply chains, and most crucially, a gateway to Africa's booming mining sector.

The Arpic acquisition revealed Atlas Copco's emerging M&A philosophy: don't just buy companies, buy capabilities and market access. The Belgian operation came with something Stockholm couldn't replicate: deep relationships with mining companies operating in the Congo, South Africa, and Rhodesia. Within two years, Atlas Copco equipment was operating in copper mines across the African Copper Belt, a market that would drive growth for the next two decades.

The international expansion accelerated with remarkable precision. The UK subsidiary, established in 1919, was revitalized with new capital and management. Canada became the beachhead for North America, with Atlas Copco (Canada) Ltd. established in 1948. But the real prize was the United States.

The American market in the 1950s was dominated by Ingersoll Rand and Gardner Denver—giants with decades-old relationships and massive production capabilities. Atlas Copco's approach was surgical rather than frontal. Instead of competing across the board, they identified specific niches where Swedish engineering provided genuine advantage: lightweight rock drills for narrow-vein mining, specialized compressors for chemical processing, and precision pneumatic tools for aerospace manufacturing.

By 1955, Atlas Copco controlled nearly half the North American market for lightweight rock drills—a segment the American giants had ignored as too small. This foothold strategy would become another element of the Atlas Copco playbook: enter markets through specialized niches, then expand adjacently.

The 1960 acquisition of Craelius, a Swedish manufacturer of diamond drilling equipment, exemplified this approach. Craelius brought proprietary technology for exploration drilling—the process of extracting core samples to assess ore deposits. This wasn't a large market, but it was strategic: mining companies that used Craelius equipment for exploration often standardized on Atlas Copco equipment for production. The acquisition made Atlas Copco indispensable at every stage of the mining lifecycle.

The global expansion created organizational challenges that would have destroyed a more rigid company. By 1960, Atlas Copco operated in over 50 countries, each with unique regulations, labor practices, and customer expectations. The solution came from the company's Swedish DNA: radical decentralization combined with strong cultural values.

Each country operation was run as a semi-autonomous unit, with local management making virtually all operational decisions. The Swedish headquarters focused on three things: capital allocation, technology development, and culture. This wasn't the American model of detailed quarterly targets and standardized processes. Instead, it was trust-based management—what Wallenberg called "freedom with responsibility."

The cultural element was crucial. Atlas Copco didn't try to make its Egyptian operations Swedish, but it did insist on certain non-negotiable principles: technical excellence, long-term thinking, and absolute integrity in customer relationships. Managers were rotated through Stockholm not for training in procedures but for immersion in values.

This approach produced remarkable innovations. The Australian subsidiary, facing unique challenges in desert mining, developed dust suppression systems that became global products. The Indian operation, dealing with extreme monsoon conditions, created waterproofing techniques adopted worldwide. Innovation flowed not from headquarters to periphery but in all directions simultaneously.

The financial results vindicated the strategy. Between 1950 and 1965, Atlas Copco's revenue grew from 50 million SEK to over 500 million SEK. More importantly, international sales surpassed domestic Swedish sales for the first time in 1958. The company that had nearly died as a Swedish railway equipment manufacturer had been reborn as a global industrial power.

But success brought new challenges. The company's structure—dozens of semi-autonomous units producing hundreds of product variations—was becoming unwieldy. Competition was intensifying as Japanese manufacturers entered global markets with high-quality, lower-cost alternatives. Most pressingly, the core mining market was showing signs of maturation.

As the 1960s drew to a close, Atlas Copco faced a strategic inflection point. The company could continue as a successful but increasingly commoditized equipment manufacturer, or it could transform again. The choice they made—to become not just an equipment supplier but an industrial tools empire—would require the largest acquisition spree in the company's history.

IV. The Industrial Tool Empire (1970s-2000)

The boardroom at Atlas Copco's Stockholm headquarters was thick with cigarette smoke on that March morning in 1987. Tom Wachtmeister, the aristocratic CEO known for his perfectly pressed suits and old-world manners, stood before a map of the United States with a single company logo circled in red: Chicago Pneumatic. "Gentlemen," he said in his precise English, "we are about to swallow a company older than our own." The tension was palpable—Chicago Pneumatic wasn't just any acquisition; it was an American industrial icon, founded in 1889, with revenue nearly matching Atlas Copco's entire tools division.

The path to that moment had begun nearly two decades earlier with a series of strategic moves that transformed Atlas Copco from a mining-focused equipment maker into a diversified industrial powerhouse. The 1970s had started with the acquisition of French compressor manufacturer Mauguière, a deal that seemed modest at the time but proved transformational. Mauguière didn't just bring production capacity; it brought something more valuable—deep relationships with European manufacturers who were automating their assembly lines.

The automation trend was reshaping manufacturing globally. Car factories that once employed thousands of workers with hand tools were installing robotic assembly lines requiring sophisticated pneumatic systems. Atlas Copco's management, led by the visionary Erik Johnsson until 1975, recognized that industrial tools would follow the same trajectory as mining equipment: from simple mechanical devices to integrated systems.

The American market remained the ultimate prize, and Atlas Copco's strengthening of its U.S. position through the acquisition of Worthington Compressors in 1973 was a masterclass in strategic patience. Worthington was struggling, having lost market share to more nimble competitors. Wall Street saw a dying industrial dinosaur; Atlas Copco saw an undervalued platform with 2,000 skilled workers, established distribution channels, and most importantly, relationships with every major American manufacturer.

The integration of Worthington revealed what would become Atlas Copco's secret weapon in M&A: they didn't integrate, at least not in the traditional sense. While American acquirers typically imposed standardized systems and processes, Atlas Copco took a different approach. They kept Worthington's management, maintained the brand, and even retained separate product lines that competed with Atlas Copco's own offerings. The only changes were subtle but powerful: access to Swedish R&D, patient capital for long-term investments, and most importantly, a culture that celebrated engineering excellence over quarterly earnings.

Within five years, Worthington's profitability had tripled. The transformation wasn't driven by cost-cutting or synergies—the standard private equity playbook—but by releasing the entrepreneurial energy that corporate bureaucracy had suppressed. Engineers who had been told for years that their ideas were too expensive suddenly found themselves with development budgets. Sales representatives who knew their customers' needs intimately were empowered to customize solutions rather than push standardized products.

But it was the Chicago Pneumatic acquisition in 1987 that truly announced Atlas Copco's ambitions. The $160 million deal was enormous by Swedish standards—newspapers in Stockholm questioned whether a Swedish company could successfully manage such a large American operation. The skeptics didn't understand Atlas Copco's game.

Chicago Pneumatic brought three critical assets. First, its "CP" brand was globally recognized—in many markets, pneumatic tools were simply called "CPs" regardless of manufacturer. Second, the company's installed base included virtually every automotive assembly plant in North America. Third, and most importantly, Chicago Pneumatic had recently developed revolutionary oil-free technology that eliminated contamination in sensitive applications like food processing and pharmaceutical manufacturing.

The integration—or rather, the deliberate non-integration—of Chicago Pneumatic became a Harvard Business School case study. Atlas Copco kept CP's headquarters in New York, retained its entire management team, and even expanded its R&D budget. The only visible change was access to Atlas Copco's global distribution network. Within 18 months, CP tools were being sold in 40 new countries.

The 1990s brought a new challenge and opportunity: electrification. Pneumatic tools had dominated industrial applications for decades, but electric tools were becoming more powerful and precise. Rather than resist the trend, Atlas Copco embraced it through two transformative acquisitions.

The 1992 purchase of AEG Elektrowerkzeuge from the struggling German conglomerate AEG was opportunistic. AEG was in financial distress and needed to raise cash quickly. Atlas Copco paid 425 million Deutsche Marks for a business that German competitors had valued at twice that amount just years earlier. But what looked like a financial arbitrage was actually strategic positioning—AEG's electric tools were perfectly suited for the light assembly work that was growing fastest in manufacturing.

The 1995 acquisition of Milwaukee Electric Tool for $650 million was even bolder. Milwaukee was an American icon, its red tools as recognizable as Coca-Cola in construction sites across America. The company had been passed between financial owners who had under-invested in innovation while milking the brand. Atlas Copco saw what others missed: Milwaukee's reputation for durability created customer loyalty that transcended rational purchasing decisions. Construction workers would pay premium prices for tools they trusted their lives to.

Under Atlas Copco's ownership, Milwaukee flourished. R&D spending doubled, new product launches accelerated, and most importantly, the company's culture of "Nothing but Heavy Duty" was not just preserved but celebrated. Sales grew from $400 million to over $1 billion by 2004.

Then, in a move that shocked industry observers, Atlas Copco sold Milwaukee to Techtronic Industries for $2.3 billion in 2004—a 3.5x return in less than a decade. The sale wasn't driven by poor performance; Milwaukee was thriving. Instead, it reflected a strategic insight: the professional power tools market was diverging from industrial assembly systems. Consumer-facing brands required different capabilities than B2B industrial equipment. Atlas Copco chose focus over empire.

The appointment of Giulio Mazzalupi as CEO in 1997 marked another inflection point. The first non-Swedish CEO in the company's history, Mazzalupi was an Italian engineer who had run Atlas Copco's compressor division. His outsider perspective challenged sacred cows while respecting what made the company unique. Under his leadership, Atlas Copco doubled down on industrial applications while systematically exiting consumer-adjacent markets.

The Milwaukee sale exemplified Mazzalupi's philosophy: "We must be number one or number two in chosen niches, or we exit." This wasn't Jack Welch-style corporate brutalism but strategic clarity. The proceeds from Milwaukee were immediately redeployed into acquisitions of specialized industrial companies—businesses with 70% market shares in narrow niches like semiconductor fabrication tools or natural gas compression systems.

By 2000, Atlas Copco had completed over 100 acquisitions, creating the world's largest industrial tools and assembly systems empire. The company's revenue had grown from 2 billion SEK in 1970 to over 50 billion SEK. More impressively, return on capital employed consistently exceeded 20%, extraordinary for an industrial company.

The M&A machine had also created something invaluable: pattern recognition. Atlas Copco could evaluate an acquisition target in weeks, not months. They knew which red flags mattered (customer concentration, deferred maintenance) and which didn't (outdated IT systems, redundant product lines). They had developed a playbook for post-acquisition value creation that was simultaneously systematic and flexible.

But as the new millennium began, Atlas Copco's leadership recognized that the next wave of growth wouldn't come from traditional industrial markets. The future lay in the ultra-high-precision world of semiconductor manufacturing, where maintaining a perfect vacuum was as critical as compressed air in a mine. The company that had built an empire on pressure was about to make an enormous bet on its absence.

V. The Vacuum Revolution: Edwards & Leybold (2014-2016)

The cleanroom at Intel's Fab 32 in Chandler, Arizona hummed with an otherworldly silence in January 2014. Inside, hundreds of vacuum pumps maintained the near-perfect void necessary for extreme ultraviolet lithography—the bleeding-edge technology that would enable the next generation of computer chips. These weren't Atlas Copco pumps. They were Edwards pumps, and within weeks, Atlas Copco would purchase Edwards Ltd for £1 billion, fundamentally transforming itself from an industrial equipment company into a critical enabler of the digital revolution.

The timing seemed counterintuitive. Atlas, which employs around 40,000 people worldwide, had faced a troubling time in its mining division in recent years. Indeed, the financial crisis had helped to create a particularly volatile global market for commodities. Iron ore prices had collapsed from $180 per ton in 2011 to below $50. Mining companies were slashing capital expenditures. The division that had defined Atlas Copco for a century was suddenly its biggest liability.

But CEO Ronnie Leten, a Belgian engineer who had joined Atlas Copco in 1997 and risen through the compressor division, saw opportunity where others saw crisis. The semiconductor industry was experiencing unprecedented growth, driven by smartphones, cloud computing, and the early stirrings of artificial intelligence. Every new chip fab required thousands of vacuum pumps, and more importantly, continuous service and upgrades. "Edwards is a technology leader with a well developed structure and solid customer relationships in industries we know well. It is a great fit for Atlas Copco," said Ronnie Leten, president and chief executive officer of Atlas. "The vacuum solutions market is growing and has similar characteristics to our existing industrial businesses"

Edwards is a technology and market leader in sophisticated vacuum products and abatement solutions. The products and services are integral to manufacturing processes, such as for semiconductors and flat panel displays, and are used within an increasingly diverse range of industrial applications. But Edwards wasn't just any vacuum company—it was vacuum royalty, with a history stretching back to 1919 when F.D. Edwards founded the company in London. In its initial years, Edwards Vacuum imported vacuum equipment from Germany's Leybold—a relationship that would prove ironically prescient.

The Edwards acquisition was structured with characteristic Atlas Copco sophistication. Under the terms of the merger agreement, a subsidiary of Atlas Copco would acquire Edwards for a per-share consideration of up to US$10.50, which included a fixed cash payment of US$9.25 at closing and an additional payment of up to US$1.25 per share post-closing, depending on Edwards' achievement of 2013 revenue within the range of £587.5 million to £650 million and achievement of a related Adjusted EBITDA target within the range of £113.9 million to £145 million. The earnout structure aligned interests and demonstrated Atlas Copco's confidence in Edwards' trajectory.

Upon completion of the transaction, a new Vacuum Solutions Division was formed within the Atlas Copco Compressor Technique business area, with headquarters in Crawley, UK. This wasn't just an organizational detail—it signaled Atlas Copco's commitment to maintaining Edwards' identity and expertise. The Swedish company had learned from decades of acquisitions that destroying the acquired company's culture was the fastest way to destroy its value.

The integration of Edwards proceeded with surgical precision. Atlas Copco retained Edwards' management team, maintained its brand identity, and actually increased R&D spending. The only visible changes were access to Atlas Copco's global service network and patient capital for long-term investments. Edwards purchased Brooks Automation's CTI-Cryogenics and Polycold branded cryopump operations based in Chelmsford and Monterrey for US$675 million in 2018, expanding its technological capabilities in ultra-low temperature applications critical for quantum computing and advanced materials research.

But Leten and his team weren't finished. They recognized that the vacuum industry, like many mature industrial sectors, was consolidating around a few global players. To truly dominate, Atlas Copco needed to make another transformative move.

That opportunity came in November 2015, when Oerlikon Corporation, the Swiss industrial conglomerate, announced it was refocusing on core businesses. Among the assets for sale was Leybold Vacuum—the same German company that Edwards had once imported equipment from, now a €358 million revenue business with 1,600 employees and technology leadership in industrial vacuum applications.

Atlas Copco agreed to acquire Leybold Vacuum, part of Oerlikon Corporation, for $514m, with the transaction to be completed in the first half of 2016. The price seemed steep for a business with lower margins than Edwards, but Atlas Copco's leadership saw something others missed: complementary technology portfolios. Where Edwards excelled in semiconductor and high-tech applications, Leybold dominated industrial processes like metallurgy, coating, and food packaging.

"With this acquisition, Atlas Copco trusts the strengths of the vacuum specialists at Leybold, founded in 1850, who will keep their traditional and well-known brand in the market. The technological know-how and the innovative spirit of Leybold will complement our vacuum portfolio and strengthen our market presence, contributing to our customers' success," says Geert Follens, President of the Atlas Copco Vacuum Solutions Division

The Leybold acquisition closed on September 1, 2016, exactly as planned. Effective Sept. 1, 2016, Atlas Copco AB owns the former Oerlikon Leybold Vacuum GmbH, renamed Leybold GmbH and now part of the Vacuum Solutions Division. Like Edwards, Leybold maintained its brand, its headquarters in Cologne, and its distinctive culture. Atlas Copco had learned that in highly technical businesses, the real assets walked out the door every evening—keeping them engaged was more important than any synergy.

The strategic logic of the vacuum revolution became clear when examining the numbers. In 2013, before the Edwards acquisition, Atlas Copco's exposure to semiconductor and electronics markets was minimal. By 2017, after integrating Edwards and Leybold, the Vacuum Solutions division generated over €2 billion in revenue with EBITDA margins exceeding 25%—significantly higher than the traditional compressor business.

More importantly, the business model was fundamentally different from mining equipment. Semiconductor fabs required constant service, upgrades, and replacement parts. A single production interruption could cost millions in lost output, making reliability paramount. Atlas Copco's vacuum pumps became mission-critical infrastructure, creating switching costs that made customers incredibly sticky. Service revenues, which provided predictable, high-margin recurring income, grew to represent over 40% of the division's total revenue.

The timing proved prescient. The semiconductor industry entered a super-cycle driven by artificial intelligence, 5G deployment, and accelerated digitalization during the COVID-19 pandemic. Every new chip fab—whether TSMC's facilities in Arizona or Samsung's expansion in Texas—required thousands of vacuum pumps. Atlas Copco found itself as one of only three companies globally capable of supplying the full spectrum of vacuum technology required for advanced semiconductor manufacturing.

The vacuum revolution also demonstrated Atlas Copco's evolution as a capital allocator. Rather than pursuing growth for growth's sake, the company had made targeted bets on structurally growing markets with high barriers to entry. They paid premium prices—approximately 15x EBITDA for Edwards—but gained irreplaceable market positions. The alternative—building these capabilities organically—would have taken decades and likely failed given the deep customer relationships and application knowledge required.

Standing on the shoulders of these two vacuum giants—Edwards with its semiconductor expertise and Leybold with its industrial applications—Atlas Copco had transformed itself from a cyclical mining equipment supplier into an essential enabler of the digital economy. The company that had nearly died making railway equipment in the 1880s was now indispensable to manufacturing the chips powering the 21st century's technological revolution.

But even as the vacuum division flourished, Atlas Copco's board was contemplating an even bolder move—one that would challenge the very identity of the company.

VI. The Epiroc Split: Focus Through Division (2017-2018)

The January 16, 2017 board meeting at Atlas Copco's Stockholm headquarters lasted twelve hours. Outside, snow fell steadily on the Sickla industrial district, but inside, the temperature was rising. Board chairman Hans Stråberg, the former CEO of Electrolux who had engineered that company's own transformation, stood before a simple slide showing two diverging arrows. One pointed up and to the right—labeled "Industrial Customers." The other moved in volatile waves—labeled "Mining & Infrastructure." After 144 years as one company, Atlas Copco was about to perform corporate surgery on itself.

The proposal was radical: split Atlas Copco into two independent, publicly traded companies. Atlas Copco would retain the compressor, vacuum, industrial, and power technique divisions. A new company, Epiroc (from "epirrhoe," Greek for "on rock"), would take the mining and rock excavation business—the very business that had saved Atlas from bankruptcy in 1901, that had driven its international expansion, that still generated nearly 40% of group revenue.

The logic was compelling but painful. The mining business operated on fundamentally different cycles than industrial equipment. When commodity prices crashed, mining companies could delay equipment purchases for years. But semiconductor fabs needed vacuum pumps regardless of copper prices. Industrial manufacturers required compressed air whether or not iron ore was trading at $50 or $150 per ton. The volatility of mining was obscuring the stability and growth of the industrial businesses, depressing Atlas Copco's valuation multiple.

Mats Rahmström, who had become CEO in April 2017 after running the industrial technique division, understood both sides intimately. In private conversations with board members, he used a medical analogy: "We're not amputating a diseased limb. We're separating conjoined twins, both healthy, both with bright futures, but each constrained by their connection to the other."

The announcement on January 16, 2017 sent shockwaves through the Swedish business community. Dagens Industri, Sweden's leading business daily, ran a headline asking "Is Nothing Sacred?" The mining equipment business wasn't just profitable—it was highly profitable, with EBITDA margins exceeding 20%. The division had revolutionary products like the Boomer face drilling rigs and Scooptram loaders that dominated their markets. Why destroy what worked?

The answer lay in Atlas Copco's deepest cultural DNA: the willingness to sacrifice the comfortable present for the transformative future. The board's analysis showed that focused pure-play companies traded at premium valuations compared to conglomerates. More importantly, each business could optimize its capital structure, R&D investments, and acquisition strategy for its specific market dynamics.

The execution complexity was staggering. Epiroc and Atlas Copco shared everything: IT systems, manufacturing facilities, sales offices, even cafeterias. In India, the same salesperson might sell both mining drills and industrial compressors. In Chile, the same service technician might maintain equipment in both copper mines and food processing plants. Separating these intertwined operations without disrupting customer relationships required surgical precision.

Helena Hedblom, appointed to lead Epiroc as CEO, became the architect of this separation. A 20-year Atlas Copco veteran who had run mining operations in multiple countries, Hedblom understood that Epiroc needed its own identity from day one. "We're not the mining division of Atlas Copco anymore," she told employees at town halls across the globe. "We're Epiroc. We're writing our own story."

The separation process revealed just how integrated the businesses had become. Atlas Copco operated 180 shared customer centers globally. Each needed to be evaluated: would it go to Atlas Copco, Epiroc, or be split? The companies ultimately decided on a pragmatic approach—in mining-dominant countries like Chile and Peru, Epiroc took the infrastructure. In manufacturing hubs like Germany and China, Atlas Copco retained control. In mixed markets, they literally divided buildings, with separate entrances and branding.

The IT separation alone cost over 500 million SEK. Atlas Copco had operated on a single SAP instance globally. Now that needed to become two, with historical data appropriately divided, security protocols established, and business continuity ensured. The project employed over 500 IT professionals for 18 months, working around the clock to ensure that on day one, both companies could invoice customers, pay suppliers, and operate independently.

But the human element proved most challenging. Employees who had spent entire careers at Atlas Copco suddenly had to choose—or were assigned to—either company. The mining equipment division employed 13,000 people globally. Many had deep relationships with colleagues who would remain at Atlas Copco. The companies instituted generous policies allowing employees to transfer between companies for the first year, recognizing that forced separations could destroy valuable institutional knowledge.

The financial engineering was equally complex. Epiroc would inherit approximately 2 billion SEK in debt, a conservative level given its cash generation capabilities. But how to divide pension obligations? Ongoing legal disputes? Long-term customer contracts that covered both mining and industrial equipment? Each issue required negotiation, documentation, and regulatory approval.

The Swedish tax authorities initially threatened to treat the spinoff as a taxable event, which would have destroyed billions in shareholder value. After months of negotiation and legal arguments, Atlas Copco secured a ruling that shareholders who received Epiroc shares wouldn't face immediate tax consequences—a critical victory that preserved the transaction's economics.

On June 18, 2018, Epiroc began trading on Nasdaq Stockholm. Atlas Copco shareholders received one Epiroc share for every Atlas Copco share they owned—a clean, tax-efficient distribution. The market's reaction was immediate and positive. Within six months, the combined market capitalization of Atlas Copco and Epiroc exceeded the pre-announcement value by over 30%.

The split's success went beyond financial metrics. Epiroc, freed from being overshadowed by Atlas Copco's industrial businesses, could tell its own story to investors. The company positioned itself as a technology leader in mining automation and electrification—themes that resonated with ESG-focused investors. Epiroc's battery-electric mining equipment, developed in partnership with Swedish battery maker Northvolt, suddenly got the attention it deserved.

Meanwhile, Atlas Copco emerged as a pure-play industrial technology company. Without the mining division's volatility, its financial profile looked remarkably stable: organic growth averaging 8% annually, ROCE exceeding 30%, and over 35% of revenues from recurring service. The company's multiple expanded from 15x EBITDA to over 20x within 18 months of the split.

The cultural impact was equally profound. Both companies, freed from compromise and internal competition for resources, accelerated innovation. Epiroc launched 18 new products in its first year as an independent company. Atlas Copco doubled down on vacuum technology, acquiring four specialized vacuum companies in 2019 alone.

The Epiroc split became a Harvard Business School case study in strategic focus. It demonstrated that sometimes the best way to create value isn't through addition but subtraction. It showed that emotional attachment to history—even profitable history—shouldn't override strategic logic. Most importantly, it proved that a 145-year-old company could still make radical changes when markets demanded them.

The split also revealed the Wallenberg sphere's evolution. The family's investment vehicle, Investor AB, supported the split despite the execution risks, maintaining significant stakes in both companies. This patient capital, willing to endure short-term uncertainty for long-term value creation, enabled a transformation that quarterly-focused shareholders might have blocked.

As 2018 drew to a close, both companies were thriving independently. Epiroc was winning major contracts for mine automation. Atlas Copco was expanding its semiconductor vacuum business as chip demand soared. The twins, finally separated, were each growing faster than they ever could have while conjoined. The courage to divide had multiplied value—a paradox that would define Atlas Copco's next chapter.

VII. Modern Era: Four Business Areas & China Focus (2018-Present)

The conference room at Atlas Copco's new Shanghai innovation center bristled with tension in March 2022. Outside, the city was entering its strictest COVID lockdown, but inside, regional president Frank Zhang was presenting numbers that defied the chaos: China sales up 23% year-over-year, local R&D staff doubled to 400 engineers, and three new manufacturing facilities under construction. "While the world sees China risk," Zhang told the executive team via video link, "we see China opportunity."

Post-Epiroc, Atlas Copco had reorganized into four focused business areas, each operating as a mini-conglomerate with its own P&L responsibility, capital allocation authority, and strategic direction. Compressor Technique, the historical core, generated 45% of revenues. Vacuum Technique, turbocharged by the Edwards and Leybold acquisitions, contributed 20%. Industrial Technique, manufacturing assembly tools and industrial power tools, provided 20%. Power Technique, offering portable compressors, generators, and light towers, rounded out the portfolio at 15%.

But the real transformation was geographic. Asia/Oceania had become 39% of revenues, Americas 29%, Europe 27%, and Africa/Middle East 5% as of 2022. China alone represented nearly 20% of group sales, making it Atlas Copco's largest single market—larger than the United States, larger than Germany, larger even than Sweden.

The China strategy wasn't just about following demand. Atlas Copco recognized that China was transitioning from the world's factory to the world's innovator. Chinese semiconductor fabs weren't just assembling chips designed elsewhere—they were pushing the boundaries of manufacturing technology. Chinese electric vehicle manufacturers weren't copying Tesla—they were pioneering new battery technologies and production methods. To serve these customers, Atlas Copco needed to innovate in China, for China, and increasingly, from China to the world.

The Wuxi factory, opened in 2019, exemplified this approach. Rather than simply assembling products designed in Sweden, Wuxi developed entirely new compressor lines optimized for Chinese industrial applications. The GA 90-160 VSD+ series, designed specifically for the volatile power conditions common in Chinese factories, became a global bestseller. Chinese innovation was flowing back to Stockholm.

The semiconductor vacuum business showcased this bidirectional innovation flow. When SMIC and other Chinese chip manufacturers faced technology restrictions, they needed vacuum solutions optimized for their specific equipment and processes. Atlas Copco's Shanghai team developed customized solutions that didn't violate export controls but maximized performance within constraints. These innovations proved valuable for second-tier fabs globally, creating an unexpected market opportunity.

The service transformation accelerated in the modern era. 36% of revenues came from services including spare parts, maintenance, repairs, and consumables. But this understated the strategic importance. Service revenues grew faster than equipment sales, generated higher margins, and most critically, created customer stickiness. A semiconductor fab using Atlas Copco vacuum pumps typically signed 10-year service agreements. These contracts provided predictable cash flows that smoothed cyclical equipment sales.

Digital technology enabled new service models. Atlas Copco's SMARTLINK system connected over 100,000 compressors and vacuum pumps globally, monitoring performance in real-time. When a compressor in a Brazilian food processing plant showed early signs of bearing wear, technicians arrived with replacement parts before failure occurred. This predictive maintenance capability transformed Atlas Copco from equipment supplier to operational partner.

The sustainability imperative reshaped product development. Industrial companies faced mounting pressure to reduce energy consumption and carbon emissions. Atlas Copco's variable speed drive (VSD) compressors, which adjusted motor speed to match air demand, reduced energy consumption by up to 50% compared to fixed-speed alternatives. In an era of rising energy costs and carbon taxes, efficiency became the primary selling point.

The company's organizational structure evolved to balance global scale with local entrepreneurship. Each business area operated dozens of divisions, each focused on specific technologies or customer segments. The Semiconductor division within Vacuum Technique operated differently from the Scientific Vacuum division, even though they shared underlying technologies. This radical decentralization—what Atlas Copco called "the federation model"—allowed each unit to optimize for its specific market dynamics.

In 2024, Vagner Rego became CEO, having first joined the company in 1996. Rego, a Brazilian engineer who had run operations in South America, Asia, and Europe, embodied Atlas Copco's global character. His appointment signaled continuity—he was a 28-year company veteran—but also change. Unlike his Swedish predecessors, Rego spent his first months as CEO in China, India, and the United States, not Stockholm.

The acquisition engine continued humming, but with surgical precision. Between 2018 and 2024, Atlas Copco acquired 23 companies, each fitting specific capability gaps. The 2021 acquisition of Seepex, a German progressive cavity pump manufacturer, added technology for handling viscous fluids in chemical processing. The 2023 purchase of Geveke, a Dutch compressor service company, doubled Atlas Copco's service presence in the Benelux region. Each deal was small enough to integrate smoothly but strategic enough to matter.

The industrial technique division's evolution demonstrated Atlas Copco's ability to ride technology waves. As automotive manufacturing shifted from internal combustion to electric vehicles, assembly requirements changed dramatically. Electric motors required different torque specifications than engines. Battery packs needed specialized joining technologies. Atlas Copco's Chicago Pneumatic and Atlas Copco Tools brands developed entirely new product lines for EV manufacturing, turning potential disruption into opportunity.

The market's perception of Atlas Copco transformed post-Epiroc. Without mining's volatility, investors could appreciate the company's subscription-like business model. The stock traded at valuation multiples typically reserved for software companies, not industrial manufacturers. The company's market capitalization exceeded 500 billion SEK by 2024, making it one of Europe's most valuable industrial companies.

But challenges emerged alongside opportunities. China's "dual circulation" policy pushed for domestic self-sufficiency in critical technologies. Local competitors like Kaishan and Hanbell were moving upmarket, offering products that matched Atlas Copco's performance at lower prices. The company responded by localizing more production, increasing Chinese suppliers, and most importantly, embedding deeper into customers' operations through service and digitalization.

Geopolitical tensions added complexity. Technology export restrictions limited what Atlas Copco could sell to certain Chinese customers. The company navigated carefully, establishing clear compliance protocols while maintaining customer relationships. Some cynics called it "strategic ambiguity," but Atlas Copco preferred "principled pragmatism."

The Power Technique division found unexpected growth in energy transition applications. Portable power was essential for renewable energy construction—wind farms and solar installations required temporary power during construction. The division's battery-powered light towers and generators, developed for environmental regulations in European cities, found global markets as construction sites worldwide faced emission restrictions.

Innovation investment reached record levels, with R&D spending exceeding 3.5 billion SEK annually. But innovation wasn't just about products. Atlas Copco pioneered new business models like "air-as-a-service," where customers paid for compressed air consumption rather than buying compressors. This model, piloted in Belgium and scaled globally, transformed capital expenditure into operating expense, making Atlas Copco's solutions accessible to smaller customers.

The modern Atlas Copco defied easy categorization. It was a Swedish company that generated most revenue outside Sweden. An industrial company with tech-like margins. A 150-year-old firm that acted like a startup in its approach to innovation. This paradoxical nature—traditional yet transformative, global yet local, diversified yet focused—became its competitive advantage in an increasingly complex world.

VIII. The Atlas Copco Playbook

Marcus Wallenberg Jr. had a saying that became scripture at Atlas Copco: "To exist is not enough." This philosophy, inherited from his grandfather and passed to successive generations of managers, created a corporate culture unique even by Swedish standards. The Atlas Copco playbook wasn't written in any manual—it was embedded in thousands of decisions, acquisitions, and innovations over 150 years. Yet its principles were remarkably consistent.

Decentralization as Competitive Advantage

The principle was simple but radical: whoever is closest to the challenge is most likely to figure out a solution. While American corporations in the 1980s and 1990s centralized for efficiency, Atlas Copco moved in the opposite direction. By 2024, the company operated over 40 divisions, each run as an independent business with its own president, R&D budget, and P&L responsibility.

This wasn't delegation—it was designed autonomy. Division presidents could approve capital expenditures up to 50 million SEK without headquarters approval. They could hire, fire, and set salaries within broad guidelines. They could even develop products that competed with other Atlas Copco divisions. The only non-negotiables were ethical standards, safety protocols, and financial reporting accuracy.

The magic happened at the edges. When the Australian mining division faced unique dust problems in iron ore operations, they didn't wait for Stockholm to develop a solution. Local engineers created water mist systems that became global products. When the Indian compressor division needed equipment that could handle 50°C ambient temperatures and monsoon humidity, they designed it themselves. These innovations would never have emerged from centralized R&D.

But decentralization without coordination would be chaos. Atlas Copco solved this through what they called "the network effect." Division presidents met quarterly, not to receive orders but to share experiences. If the Brazilian team figured out how to reduce service costs by 20%, that knowledge spread organically. If the Chinese team developed a new sales approach for semiconductor customers, colleagues in Taiwan and Korea learned about it over dinner, not through PowerPoint.

The Acquisition Machine: Pattern Recognition at Scale

By 2024, Atlas Copco had completed over 200 acquisitions. Most failed acquisitions destroy value through integration problems, culture clashes, or overpayment. Atlas Copco's success rate exceeded 80%—extraordinary in the M&A world. The secret wasn't genius but pattern recognition developed over decades.

The evaluation process was standardized but flexible. Every target was assessed on seven dimensions: technology differentiation, customer relationships, service potential, cultural fit, management quality, integration complexity, and value creation potential. But these weren't weighted formulas—they were conversation starters. The real decisions happened when experienced managers asked, "Does this feel like Leybold or Milwaukee?"

Due diligence focused on the non-obvious. While investment bankers scrutinized financial statements, Atlas Copco engineers visited customer sites. How did users actually interact with the products? What problems weren't being solved? Where was the informal knowledge—the tricks experienced operators knew but weren't documented? This customer-back approach revealed value that spreadsheets missed.

The integration philosophy was counterintuitive: don't integrate, at least not immediately. Acquired companies kept their names, their offices, often their entire management teams. Chicago Pneumatic still operated as Chicago Pneumatic forty years after acquisition. Edwards remained Edwards. This preserved the entrepreneurial energy that made these companies attractive in the first place.

Value creation came through patient capability building. Atlas Copco provided capital for R&D that previous owners couldn't afford. They opened distribution channels that small companies couldn't access. They shared technologies across divisions without forcing standardization. A vacuum pump innovation at Edwards might inspire a compressor improvement at Worthington, but nobody mandated the cross-pollination.

The discipline to walk away distinguished Atlas Copco from deal-hungry competitors. For every acquisition completed, ten were rejected after initial evaluation. The company maintained a "never chase" policy—if bidding became emotional, Atlas Copco withdrew. They lost some attractive targets but avoided the winner's curse that plagued aggressive acquirers.

Service as Moat: The Recurring Revenue Revolution

Equipment sales were episodic—a customer might buy compressors every decade. Service was continuous—filters needed replacement, bearings wore out, technology required updates. Atlas Copco transformed this mundane reality into competitive advantage.

The insight was behavioral, not technical. Maintenance managers cared more about avoiding downtime than minimizing costs. A semiconductor fab losing production for an hour could lose millions. A food processing plant with a compressor failure might scrap entire batches. For these customers, Atlas Copco's value proposition wasn't equipment but reliability.

Service contracts became sophisticated risk-transfer mechanisms. Instead of selling spare parts, Atlas Copco guaranteed uptime. If equipment failed despite proper maintenance, Atlas Copco paid penalties. This aligned incentives—Atlas Copco was motivated to prevent problems, not just fix them. Customers paid premiums for this peace of mind.

The installed base became a data goldmine. With over 500,000 pieces of equipment in the field, Atlas Copco could identify patterns invisible to individual customers. They knew that certain compressor models in chemical plants needed bearing replacement after 8,000 hours. They recognized early indicators of seal failure in vacuum pumps. This knowledge, accumulated over decades, created switching costs that no competitor could overcome.

Swedish Industrial Excellence: The Cultural Advantage

Swedish capitalism operated differently from Anglo-American or Asian models. The focus wasn't quarterly earnings but generational wealth creation. The stakeholders weren't just shareholders but employees, communities, and society. This sounds like corporate propaganda, but at Atlas Copco, it drove concrete decisions.

The company never had significant layoffs, even during severe downturns. The 2008 financial crisis saw revenue drop 25%, but instead of mass firings, Atlas Copco reduced working hours, cut executive pay, and eliminated dividends. When recovery came, experienced workers were ready to capture growth. Competitors who had cut deeply struggled to rebuild capabilities.

Long-term thinking enabled investments that wouldn't pay off for years. The vacuum technology build-out required billions in investment before generating significant returns. The sustainability focus—developing energy-efficient products when energy was cheap—seemed irrational to analysts but proved prescient when carbon taxes and energy costs soared.

The engineering culture went beyond products to processes. Swedish engineers obsessed over incremental improvements. Making a compressor 2% more efficient might seem trivial, but across thousands of units running continuously, the energy savings were enormous. This patient perfectionism, mocked by some as slow, created products that lasted decades and customers who never switched.

Portfolio Management: The Courage to Cut

Atlas Copco's greatest strategic moments involved subtraction, not addition. Selling Milwaukee when it was thriving. Spinning off Epiroc at peak profitability. Exiting product lines that were profitable but non-strategic. This unsentimental portfolio management distinguished Atlas Copco from industrial conglomerates that hoarded assets.

The framework was elegant: be number one or two in chosen niches, or exit. But "niche" was carefully defined—not broad markets like "compressors" but specific applications like "oil-free air for pharmaceutical manufacturing." In these focused segments, Atlas Copco could achieve 40-50% market share and pricing power that broad-market players never enjoyed.

The exit discipline was as rigorous as acquisition discipline. Every five years, each division underwent strategic review. Was it still core? Could Atlas Copco add unique value? Would another owner be better positioned? These weren't theoretical exercises—divisions generating hundreds of millions in revenue were regularly divested if they didn't fit the strategic focus.

The Wallenberg Influence: Patient Capital's Compounding Power

The Wallenberg family's influence, exercised through Investor AB, provided stability unique among global industrial companies. Controlling roughly 20% of votes but only 5% of capital, the family could think in decades while public markets obsessed over quarters.

This wasn't passive ownership. Wallenberg representatives on the board asked tough questions, demanded performance, and occasionally forced leadership changes. But they also provided air cover for long-term investments, supported strategic transformations, and most importantly, maintained consistent strategic direction across CEO transitions.

The multi-generational perspective enabled Atlas Copco to survive existential threats that would have destroyed companies with impatient owners. The 1880s bankruptcy. The 1930s depression. The 2008 financial crisis. Each time, the Wallenberg commitment provided both capital and confidence to persist through darkness.

Global-Local Balance: The Federation Model

Atlas Copco operated in 180 countries but felt local in each one. This wasn't marketing spin but operational reality. The Mexican operation was run by Mexicans, sold products designed for Mexican conditions, and contributed to Mexican communities. Yet it was unmistakably part of Atlas Copco, sharing technologies, values, and ambitions with colleagues worldwide.

The balance was maintained through careful tension. Global functions—treasury, basic R&D, ethics—were centralized. Local functions—sales, service, application engineering—were decentralized. The boundaries were constantly negotiated, never fixed. This dynamic equilibrium prevented both chaotic fragmentation and stifling centralization.

The federation model created resilience through redundancy. If one country operation struggled, others compensated. If one technology faced disruption, others provided growth. This portfolio effect, operating across geographies, technologies, and customers, smoothed volatility that destroyed more focused competitors.

The playbook's genius wasn't any single element but how they reinforced each other. Decentralization enabled successful acquisitions. Service focus supported premium pricing. Swedish values attracted patient capital. Portfolio discipline maintained strategic focus. Each principle strengthened the others, creating a system more powerful than its components.

IX. Bear vs. Bull Case & Competitive Analysis

The Bull Case: Secular Tailwinds and Competitive Moats

The bull thesis for Atlas Copco rests on three pillars that seem almost too perfect for skeptical investors. First, the semiconductor vacuum business has transformed from a nice-to-have into an existential necessity for the global economy. Every AI chip, every smartphone processor, every automotive semiconductor requires the ultra-high vacuum that only Atlas Copco, Pfeiffer Vacuum, and a handful of others can provide. With semiconductor content increasing in everything from refrigerators to rockets, this isn't a cycle—it's a secular shift.

The math is compelling. A single advanced semiconductor fab costs $20 billion to build and requires thousands of vacuum pumps, each costing between $50,000 and $500,000. More importantly, these pumps need continuous service, spare parts, and eventual replacement. Atlas Copco estimates that every dollar of equipment sales generates three dollars of lifetime service revenue. With over 50 new fabs planned globally through 2030, the vacuum division alone could double revenues.

The second pillar—industrial compressor dominance—seems mundane but proves remarkably resilient. Compressed air powers 90% of all manufacturing processes. It's the fourth utility after electricity, water, and gas. Atlas Copco's installed base of over 300,000 compressors creates switching costs that border on prohibitive. Replacing an Atlas Copco compressor with a competitor's requires retraining technicians, establishing new service relationships, and risking production downtime. For what potential benefit? Maybe 5% lower equipment cost that's offset by higher lifecycle expenses.

The service revenue resilience can't be overstated. During the 2008 financial crisis, equipment orders collapsed 40%, but service revenues declined only 8%. During COVID-19, equipment sales dropped 15% while service fell just 3%. This stability comes from the non-discretionary nature of maintenance—you can defer buying a new compressor, but you can't skip replacing filters unless you want catastrophic failure.

The third pillar—sustainability regulations—transforms Atlas Copco from vendor to strategic partner. The EU's carbon border adjustment mechanism, China's dual carbon goals, and corporate net-zero commitments all require dramatic improvements in industrial energy efficiency. Atlas Copco's VSD+ compressors reduce energy consumption by up to 50%. For energy-intensive industries, the payback period is often under two years. This isn't green washing—it's green economics.

The valuation multiple expansion story remains intact. Industrial technology companies with 35%+ service revenue mix typically trade at 20-25x EBITDA. Atlas Copco trades at approximately 22x, but bulls argue this understates the quality. The company's ROCE exceeds 30%, far above peers. Organic growth averages 6-8% annually without heroic assumptions. The dividend has grown for 15 consecutive years. This isn't just an industrial company—it's a compounder hiding in plain sight.

The Bear Case: Cyclical Risks and Structural Challenges

The bear case begins with an uncomfortable truth: Atlas Copco has never been tested by a prolonged semiconductor downturn coinciding with an industrial recession. The vacuum division's meteoric growth assumes semiconductor capital expenditure continues its upward trajectory. But physics and economics suggest otherwise. Moore's Law is slowing, requiring exponentially more investment for marginally better chips. At some point, the cost-benefit breaks.

China dependency creates existential risk that bulls underappreciate. Nearly 20% of revenues come from China, but the exposure is actually higher—many components for "European" or "American" sales originate in China. If geopolitical tensions escalate to technology embargoes or financial sanctions, Atlas Copco faces impossible choices. Serve Chinese customers and risk Western sanctions, or abandon China and lose not just revenue but global supply chains.

The competitive landscape is intensifying in ways Atlas Copco hasn't faced before. Chinese competitors like Kaishan and Hanbell aren't just copying—they're innovating. Their compressors match Atlas Copco's efficiency at 60% of the price. They're winning contracts in Southeast Asia, Africa, and increasingly, Europe. The standard defense—"customers pay for reliability"—assumes past patterns persist. But as Chinese quality improves and price gaps widen, that assumption weakens.

Valuation multiples embed perfection that reality rarely delivers. At 22x EBITDA and 35x earnings, Atlas Copco trades at premiums typically reserved for software companies or luxury brands. But this is industrial equipment exposed to cycles, competition, and technological disruption. The multiple expansion story—from 15x to 22x since Epiroc—likely reverses during the next downturn. A reversion to historical averages implies 30% downside.

The technology transition risk gets insufficient attention. Electric vehicles require fewer pneumatic tools for assembly than internal combustion engines—fewer parts, simpler construction. Additive manufacturing (3D printing) could eliminate many machining processes that require compressed air. Quantum computing might revolutionize semiconductor manufacturing in ways that obsolete current vacuum technology. Atlas Copco's R&D spending, while substantial, might be fighting yesterday's war.

Climate transition creates stranded asset risk. Atlas Copco's power technique division sells diesel generators and compressors to oil and gas customers. These products generate strong margins but face existential threats from electrification and renewable energy. The company talks about sustainable solutions, but 30% of revenues still come from carbon-intensive applications. As regulations tighten and financing disappears for fossil fuel projects, this revenue stream erodes.

Competitive Dynamics: The Oligopoly Under Pressure

The competitive landscape resembles a comfortable oligopoly under increasing attack. In vacuum technology, Atlas Copco (via Edwards and Leybold) controls approximately 35% of the semiconductor vacuum market. Pfeiffer Vacuum holds 25%, and Japanese players like Ebara and Shimadzu split another 30%. This cozy arrangement enabled rational pricing and stable margins for decades.

But ASML's dominance in lithography equipment creates customer concentration risk. ASML specifies which vacuum pumps work with their systems. If ASML decided to develop proprietary vacuum technology or partner exclusively with one supplier, Atlas Copco's semiconductor exposure becomes a liability. The customer you can't afford to lose is the customer who controls you.

In industrial compressors, the landscape is fragmenting. Ingersoll Rand remains formidable, especially in North America. Gardner Denver (now part of Ingersoll Rand) brings scale and aggression. But the real threat comes from regional champions. Germany's Kaeser Kompressoren dominates the German Mittelstand. Italy's Ceccato and Mattei own their local markets. These aren't global threats individually, but collectively they're eroding Atlas Copco's pricing power.

The service competition is evolving from OEM-dominated to independent providers. Third-party service companies offer Atlas Copco compressor maintenance at 70% of Atlas Copco's price. They source spare parts from China, hire former Atlas Copco technicians, and increasingly, use predictive analytics that match OEM capabilities. The service moat that bulls celebrate might be shallower than assumed.

Digital threats loom larger than traditional competition. If Amazon Business or Alibaba.com creates marketplaces for industrial equipment and service, the direct customer relationships Atlas Copco spent 150 years building become intermediated. If AI-powered predictive maintenance becomes commoditized through platforms like IBM's Maximo or SAP's Asset Management, Atlas Copco's service differentiation erodes.

Capital Allocation: The Ultimate Differentiator

Atlas Copco's capital allocation excellence provides the strongest rebuttal to bear arguments. Over the past decade, the company generated ROCE exceeding 30% while investing aggressively in R&D and acquisitions. This isn't financial engineering—it's operational excellence that creates compounding value.

The dividend policy exemplifies this discipline. Atlas Copco targets 50% of earnings as dividends, providing reliable income while retaining capital for growth. The dividend has never been cut, even during severe downturns. This consistency attracts long-term investors who provide stability during volatile periods. The shareholder base—Wallenberg family, Swedish pension funds, Norwegian sovereign wealth—thinks in decades, not quarters.

The acquisition strategy remains disciplined despite having significant firepower. Net debt/EBITDA sits below 1x, providing 20+ billion SEK in acquisition capacity. But management resists empire building. Recent acquisitions average €100-200 million—bolt-ons that enhance capabilities without transformation risk. The Epiroc spin-off proved management will shrink to grow when strategy demands.

The Verdict: Quality at a Premium Price

The investment case for Atlas Copco reduces to a single question: do you believe quality persists? The bulls see a company with 150 years of compounding excellence, protected by switching costs, service relationships, and technical capabilities that take decades to build. They're buying the picks and shovels of the 21st century—the boring but essential equipment that enables everything from AI chips to electric vehicles.

The bears see peak multiple on peak margins in peak industries. They're selling the assumption that past is prologue, that Chinese competition remains inferior, that semiconductor growth continues indefinitely. They believe mean reversion applies even to exceptional companies.

The truth, as always, lies between extremes. Atlas Copco is genuinely exceptional—the financials, market positions, and corporate culture prove that. But exceptional companies at exceptional valuations often deliver ordinary returns. The margin of safety that value investors demand doesn't exist at current prices.

For long-term investors who believe in secular growth of semiconductors, industrial automation, and sustainability, Atlas Copco provides exposure with lower risk than pure-plays. For value investors seeking bargains, the stock requires patience—waiting for the next downturn when quality becomes temporarily cheap. For momentum traders, the trend remains favorable but increasingly vulnerable to disappointment.

X. Epilogue & Lessons for the Future

In the winter of 2024, as snow falls once again on Stockholm's Sickla district, Atlas Copco stands as a paradox resolved. The company that began making railway equipment for a nation of 4 million people now provides essential technology for 8 billion. The firm that nearly died in the 1880s has survived and thrived through three centuries. The industrial giant that split itself in half emerged twice as valuable.

What does Atlas Copco teach us about industrial conglomerates in the 21st century? First, that focus and diversification aren't opposites but complements when properly structured. Atlas Copco is highly diversified across geographies, end markets, and technologies, yet laser-focused on a single theme: providing mission-critical equipment and services for industrial processes. This isn't the conglomerate model of unrelated businesses sharing only capital. It's strategic coherence disguised as portfolio diversity.

The power of focus through division—exemplified by the Epiroc split—challenges conventional wisdom about corporate breakups. Most spinoffs are defensive, forced by activists or distress. Atlas Copco's split was offensive, initiated at peak performance to unlock greater potential. The lesson isn't that all companies should split, but that sacred cows—even profitable ones—shouldn't be sacred. If division creates more value than combination, emotional attachment to unity becomes expensive nostalgia.

The boring B2B lesson might be most important for investors. While markets obsess over consumer brands, social media platforms, and disruptive technologies, companies like Atlas Copco compound wealth through mundane excellence. Compressed air isn't sexy. Vacuum pumps don't generate headlines. But the returns—30% ROCE sustained over decades—exceed what most "exciting" companies ever achieve. The lesson: boring businesses with pricing power, switching costs, and service revenue can create extraordinary returns.

The Swedish model offers an alternative to both American shareholder capitalism and Asian state capitalism. The Wallenberg family's multi-generational ownership, combined with professional management and public market discipline, creates unique advantages. Patient capital enables long-term thinking. Professional management ensures competence. Public markets enforce discipline. This triangular structure—family, management, markets—might be the optimal governance model for industrial companies.

Looking forward, Atlas Copco faces transformations that dwarf past challenges. The energy transition isn't just about efficient compressors—it's about reimagining industrial processes. Artificial intelligence isn't just driving semiconductor demand—it's revolutionizing how equipment is designed, manufactured, and serviced. China's evolution from customer to competitor isn't just a market shift—it's a fundamental restructuring of global industry.

The automation opportunity could be Atlas Copco's next transformation. As factories become lights-out operations run by robots, the demands on industrial equipment change fundamentally. Predictive maintenance becomes autonomous maintenance. Service technicians become data scientists. Equipment sales become outcome guarantees. Atlas Copco's vast installed base and service relationships position it to lead or be disrupted by this shift.

Sustainability pressures will intensify, not abate. Carbon taxes, water scarcity, and circular economy mandates will reshape industrial economics. Atlas Copco's efficiency focus aligns with these trends, but incremental improvement might not suffice. The company that revolutionized mining with lightweight aluminum drills might need to revolutionize manufacturing with technologies not yet invented.