Lamar Advertising Company: The Quiet Empire of America's Roadways

I. Introduction & Episode Roadmap

Picture a stretch of interstate highway anywhere in America—I-10 through the bayous of Louisiana, I-95 along the Eastern Seaboard, or I-75 cutting through Florida's tourist corridor. Every few miles, towering steel structures rise from the landscape, bearing messages about lawyers, fast food chains, upcoming attractions, and everything in between. Most drivers glance at these billboards without a second thought. Few realize they're looking at one of the most durable competitive moats in American business.

Founded in 1902, Lamar Advertising Company (Nasdaq: LAMR) is one of the largest outdoor advertising companies in the world with over 360,000 displays across the United States and Canada. The company that began as a poster business promoting vaudeville shows at a Pensacola opera house has become an $12.9 billion enterprise that controls roughly a quarter of America's billboard market—a remarkable concentration of power in a fragmented industry where the next thousand competitors combined barely match its scale.

The central question this analysis explores: How did a poster company from the Gulf Coast become America's largest billboard empire—and why can't anyone compete with them?

Lamar says it owns about 25% of the OOH market and boasts a diversified base of advertisers in the services, health care, restaurant, retail, automotive, insurance, and gaming categories. This puts Lamar meaningfully ahead of Clear Channel Outdoor and OUTFRONT Media, its two publicly traded rivals. But market share only hints at the real story. The more interesting dynamic lies in understanding why these market positions have proven so sticky over decades.

Several themes will emerge throughout this examination:

The Regulatory Moat: The Highway Beautification Act of 1965—legislation championed by Lady Bird Johnson to beautify America's roadways—paradoxically created an impenetrable barrier to entry that has protected incumbent billboard operators for sixty years. The law that sought to limit billboards effectively froze the competitive landscape in place.

Four Generations of Family Control: Even though it is a public company, Lamar remains a family business under the control of third and fourth generation family members of the Lamar and Reilly families. This continuity of leadership has enabled patient capital allocation decisions that publicly traded rivals with quarterly pressures struggle to match.

The Digital Transformation Bet: Lamar invented the large-format digital billboard in 2001, sparking an industry transformation that has generated exceptional returns on invested capital. Digital billboards accounted for 32% of the company's annual revenue in 2024, despite representing only 3% of total displays—a 10x revenue intensity that represents perhaps the most attractive reinvestment opportunity in the portfolio.

The REIT Conversion: In 2014, Lamar became the first outdoor advertising company to convert to a Real Estate Investment Trust structure, creating tax advantages that fundamentally altered the competitive dynamics of the industry.

For long-term investors, billboards remain one of the most misunderstood businesses in America. In an era obsessed with digital disruption, here sits a 123-year-old enterprise leveraging steel, concrete, and carefully positioned land parcels to generate exceptional returns. The business model has evolved from hand-painted signs to LED displays streaming real-time content, but the underlying economics—scarcity of premium locations, regulatory barriers to new supply, and the inescapable visibility of roadside advertising to mobile populations—remain as powerful as ever.

II. The Origins: Poster Advertising in the Age of Horses (1902-1925)

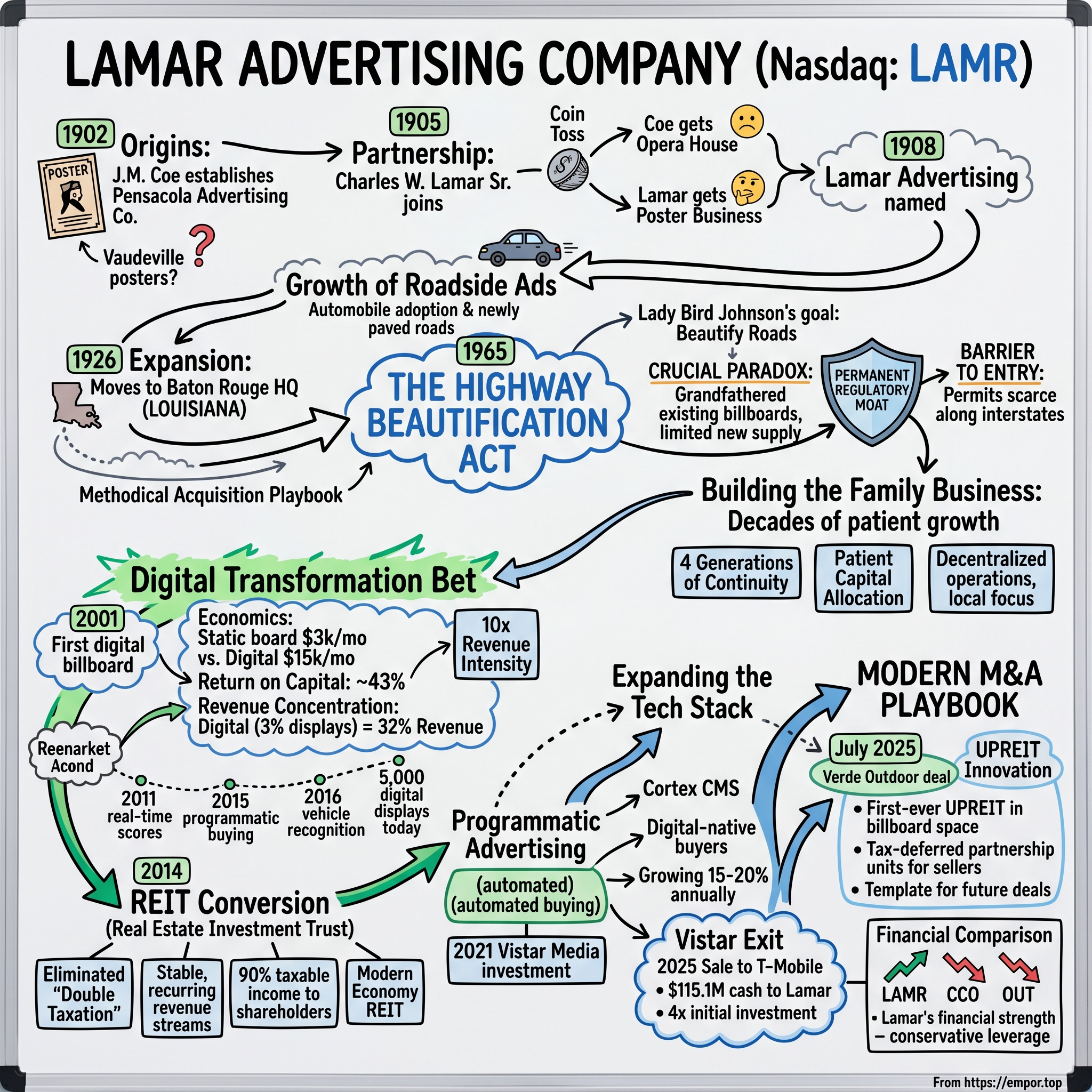

The story begins not with a billboard but with a vaudeville theater in the Florida panhandle. In 1902, Pensacola was a busy Gulf Coast port city, home to a naval air station and a thriving entertainment scene centered on the local opera house. Lamar Advertising Company traces its origins to 1902, when J.M. Coe established the Pensacola Advertising Company in Pensacola, Florida, initially focusing on promoting local attractions through poster advertising.

Coe's business was simple: he created and displayed posters advertising upcoming shows at the opera house. The posters were placed on what were then called "billboards"—nothing like the large, steel-frame structures used today. Then they were nothing more than town and city wall spaces used to advertise businesses or, just as often, upcoming public events.

The poster business was a relatively new industry. Just a decade earlier, in 1891, poster makers had created the Associated Bill Posters' Association, generally credited with being the nation's first association of advertisers. This nascent industry existed in a world still dominated by horse-drawn transportation, where advertising meant reaching pedestrians on city streets rather than drivers along highways.

In 1905, Charles W. Lamar Sr. entered into a partnership with Coe, expanding operations along the Gulf Coast region. Lamar was a prominent Pensacola businessman, serving as president of the American National Bank of Pensacola. The two men owned the opera house as well as the poster business.

Three years later came the coin flip that would determine the trajectory of an industry.

When the partners decided to break up in 1908, they used a coin toss to decide who would get what part of their mutual business. Coe won the more lucrative opera house and Lamar, who lost the coin toss, got the poster business. He named the new firm Lamar Advertising.

At the time, losing the coin toss must have seemed like bad luck. The opera house was the established, profitable business. The poster operation was secondary, worth perhaps $3,500 (approximately $120,000 in today's dollars). But Charles Lamar had inadvertently positioned himself at the intersection of two transformational forces: the automobile and the American road system.

Before the company's first decade of business ended, it became clear that the auto would soon replace the horse and buggy and that roads would be needed to accommodate it. By 1912, when Henry Ford introduced the Model-T, the nation had begun its love affair with the car. Lamar's response was to move into the new area of outdoor, roadside advertising.

This pivot was prescient. The Model T, priced within reach of middle-class Americans through Ford's assembly-line manufacturing, would transform the American landscape. Where pedestrians had once walked past wall posters, drivers now sped past structures positioned along newly paved roads. The billboard as we know it today—a large display visible from a highway—was being born.

The economics of this new medium were compelling from the start. Unlike newspaper advertisements that competed for attention on crowded pages, or radio spots that interrupted programming, roadside billboards commanded exclusive visual attention from captive audiences. A driver approaching at 40 miles per hour had no choice but to see what was displayed. The cost per impression was extraordinarily low, the reach was broad, and the message was impossible to skip.

By the early 1920s, Lamar Advertising had grown its presence in the poster advertising sector, particularly in Florida and nearby states, capitalizing on increasing automobile travel and roadside visibility.

The next major expansion came in 1926. Lamar and his two sons, Charles Lamar, Jr. and L.V. Lamar, purchased the Baton Rouge Poster Advertising Co., renaming it Lamar Advertising Co. This acquisition brought the company to Louisiana and established Baton Rouge as its permanent headquarters—a location from which it still operates nearly a century later.

The move to Baton Rouge was strategic. Louisiana was experiencing its own road-building boom, and Baton Rouge's position as the state capital ensured it would be a hub of both government activity and commercial development. The company was positioning itself to grow alongside America's expanding highway infrastructure.

For investors analyzing the origins of competitive advantage, the early Lamar story demonstrates a pattern that would repeat throughout the company's history: patient identification of structural trends (automobile adoption), quick pivots to capitalize on those trends (roadside advertising), and strategic acquisition of geographic footholds (the Baton Rouge expansion). These same dynamics continue to drive value creation today.

III. Building the Family Business: The Long Game (1926-1957)

The Great Depression tested countless American businesses, but Lamar Advertising demonstrated the resilience that would become its hallmark. Despite the Great Depression and the fact that Lamar's markets were in states with few paved roads, the company soon turned roadside advertising into its primary business. Like others in the industry, Lamar was aided by Outdoor Advertising Inc., an organization formed in 1931 to promote billboard sales nationwide.

During the 1930s Lamar slowly expanded the business, purchasing five outdoor advertising companies in Louisiana and Florida, areas where a paved road infrastructure was, like the company, rather slow to develop.

This methodical expansion strategy—acquiring smaller regional operators one at a time—established an acquisition playbook that Lamar would execute for the next nine decades. The company recognized early that outdoor advertising is fundamentally a local business with significant operating leverage. Each acquisition brought not just billboards but local market knowledge, advertiser relationships, and permitting expertise.

The challenges of early billboard advertising were considerable. Although it was a growth industry, the billboard advertising business was a tough one. In the industry's early years, many billboards had to be hand-painted on the actual display surfaces, a tedious process. Each new campaign required skilled workers to climb scaffolding and apply paint by hand—a labor-intensive operation far removed from today's digital displays that can be updated remotely in seconds.

In 1944, Lamar died, leaving the business to his son Charles, Jr. and his two daughters. The three siblings took over the management of the Louisiana and Florida operations of the now prosperous and growing family business.

The post-World War II period proved transformational for the outdoor advertising industry. Between 1940 and 1960, industry-wide yearly revenues increased from $44.7 million to more than $200 million. This growth was driven by the surge in automobile ownership as returning soldiers started families, moved to newly built suburbs, and drove the newly constructed highways connecting American cities.

The Interstate Highway System, authorized by President Eisenhower in 1956, would prove particularly important. This 41,000-mile network of limited-access highways created millions of new "impressions"—advertising industry parlance for the number of times an advertisement is viewed. Every car that rolled onto an interstate represented a captive audience with eyes on the road and limited alternatives for visual entertainment.

A new period of expansion for Lamar began in 1958 under the leadership of president and CEO Kevin Reilly, Sr. Reilly represented a third generation of family management of Lamar Advertising through his marriage to Charles Lamar, Sr.'s granddaughter, Ann Switzer Reilly. Under Reilly's leadership over the next 15 years, Lamar purchased an additional eight companies in Florida, Alabama, and Louisiana.

Kevin Reilly Sr.'s ascent to leadership deserves attention because it established the pattern of family continuity that persists today. Reilly was one of four children born to Gene and Molly Reilly in Boston, Massachusetts, where he attended the Roxbury Latin School. With assistance from a Reserve Officers Training Corps scholarship, he attended Harvard University, where he played varsity baseball and was voted Most Valuable Player during his senior year. After graduation, he served honorably for three years as a lieutenant in the United States Navy during the Korean War. In 1953, after only one year at Harvard Business School, he and his young wife, the former Ann Switzer, known as "DeeDee", relocated to Baton Rouge, where he was employed by her family's Lamar Advertising, then a small billboard company.

Reilly brought both Harvard credentials and military discipline to a family business that had operated informally for half a century. His leadership style combined aggressive acquisition with careful attention to operations—a balance that would define Lamar's approach through successive generations.

The late 1950s also brought the first significant federal regulation of the industry. In 1958, Congress passed the first outdoor advertising control legislation commonly known as the Bonus Act, PL 85-381. It was repealed and replaced by the Highway Beautification Act of 1965.

This initial regulatory framework established principles that would shape the industry's future: billboards could be located in commercial and industrial areas, states would develop compliance programs, and there would be compensation requirements for any forced removal. The seeds of the regulatory moat were being planted.

IV. The Highway Beautification Act: The Regulation That Created a Moat (1965)

In the annals of unintended consequences, few pieces of legislation rival the Highway Beautification Act of 1965. Championed by Lady Bird Johnson as part of her husband's Great Society agenda, the law sought to reduce visual clutter along America's highways. Instead, it created perhaps the most durable competitive moat in American advertising.

In 1965, the Lyndon B. Johnson Administration took action to enhance the beauty of America's roadways through the Highway Beautification Act (HBA), which was signed into law on October 22, 1965. The HBA sought to limit billboards, junkyards, and other visual clutter that impacted the appearance of interstate highways. Known as "Lady Bird's Law," the HBA is the most comprehensive piece of national legislation ever passed regarding outdoor advertising control in America.

The origins of the law reflected genuine concern about the aesthetic quality of American highways. In announcing an America the Beautiful initiative in January 1965, President Lyndon B. Johnson said: "I want to make sure that the America we see from these major highways is a beautiful America." The cornerstone of the initiative would be the Highway Beautification Act of 1965, which called for control of outdoor advertising, including removal of certain types of signs, along the Nation's growing Interstate System and the existing Federal-aid primary system.

Lady Bird Johnson made passage of the act a personal priority. The legislative process was contentious, with the advertising industry lobbying heavily. In the House of Representatives, the bill was assigned to the House Public Works Committee and reported back to the floor on September 22, 1965. However, due to pressure on members from special interest groups, the bill languished on the floor while its sponsors tried to garner support. At the urging of President Lyndon Johnson, the bill was passed by a vote of 245 to 138 at 1:00 am on October 8.

What the HBA Actually Does:

At the federal level, the Highway Beautification Act of 1965 (HBA, P. L. 89-285) controls outdoor advertising along 306,000 miles of Federal-Aid Primary, Interstate and National Highway System roads.

The HBA allows the location of billboards in commercial and industrial areas, mandates a state compliance program, requires the development of state standards, promotes the expeditious removal of illegal signs, and requires just compensation for takings.

In its finalized form, the Highway Beautification Act placed restrictions on the size, spacing, and lighting of roadside billboards, allowed the masking of junkyards or garbage dumps to preserve roadside beauty, and the authorization of use of the Highway Trust Fund for landscaping and recreation services within the right-of-way.

The Paradox—Regulation That Created Barriers:

Here's where the story gets interesting. The compromise that enabled passage of the HBA contained provisions that transformed it from a restriction on billboards into a protection for existing billboard operators.

In 1965, the outdoor advertising industry agreed to a compromise to limit the size, spacing, and lighting of billboards to what was "customary" use at the time of passage. The "freezing" of billboard size, spacing, and lighting was supposed to ensure that these characteristics could not become more visually intrusive than they were in 1965.

This "freezing" had a crucial consequence: it grandfathered existing billboards while making it extraordinarily difficult to construct new ones. The company benefits from high barriers to entry in the billboard industry due to restrictive local zoning regulations and the Highway Beautification Act, which limits new billboard construction along interstate highways.

The economic implications were profound. In a normal industry, high returns attract new entrants who compete away profits. In outdoor advertising post-1965, high returns could not attract meaningful new supply because permits for new billboards along federal highways were effectively unavailable. The existing inventory became increasingly valuable as demand grew while supply remained constrained.

While the law restricted billboards within 660 feet of these roads—allowing exceptions for on-site advertising and official signs—its provisions were significantly weakened due to lobbying from the advertising industry. As a result, many existing billboards were exempted and the effectiveness of the law was diminished.

Critics of the outdoor advertising industry have long noted this irony. Thirty-two years after its passage, the Act has become little more than a billboard protection program. On average, new billboards are twice as big as they were in 1965, and there are fifty percent more of them than 30 years ago when Lady Bird Johnson championed highway beautification.

The Supply Constraint:

For investors, the key insight is that the HBA transformed billboard inventory into something approximating a regulated monopoly. While newspapers, radio stations, television channels, and websites can all expand capacity to meet advertiser demand, billboard supply along federal highways has been largely frozen for sixty years.

This supply constraint operates at multiple levels:

- Federal restrictions limit billboard construction along the interstate system

- State regulations implement and often enhance federal requirements

- Local zoning ordinances add additional layers of restriction

- Environmental review processes can delay or block new construction

The cumulative effect is that obtaining a permit for a new billboard can take years of regulatory navigation—if it's possible at all. Existing permit holders face little threat of new competitive supply appearing nearby.

For Lamar, which has accumulated permits over 120+ years of operation, this regulatory framework represents an extraordinary competitive advantage. Lamar purchases or leases the real estate beneath its roadside billboards. It has nearly 60,000 landowner partners across the country and thousands of billboard permits.

Those permits, combined with the underlying land positions, constitute assets that would take decades and potentially billions of dollars for any competitor to replicate—if replication were even possible under current regulations.

V. The Reilly Era: A New Period of Expansion (1958-1996)

Kevin Reilly Sr.'s leadership established the management philosophy and acquisition strategy that Lamar continues to execute today. Under his direction, the company transformed from a regional Gulf Coast operator into a national force.

In 1973, the family restructured the business to better manage its growing complexity. The Lamar Corporation was formed to facilitate management of the operating companies. This holding company structure, with individual operating subsidiaries maintaining local autonomy, became a defining characteristic of Lamar's organizational philosophy.

In total, Lamar operates 94 outdoor advertising companies through its subsidiary network. Although its central management offices are housed in its 53,500-square-foot headquarters in downtown Baton Rouge, Louisiana, much local autonomy is allowed the managers of each of these companies, and they remain in charge of day-to-day company operations.

This decentralized approach reflected a fundamental insight about the outdoor advertising business: success depends on local relationships. The advertiser deciding whether to buy billboard space in Baton Rouge or Birmingham wants to work with someone who understands local traffic patterns, local businesses, and local competitive dynamics. Lamar's structure enabled national scale with local expertise.

In 1988, Lamar entered the interstate logo sign business, winning a contract from the State of Nebraska. Lamar has secured contracts in Ontario Province, Canada, and in 18 of the 22 states that allow private contractors to fabricate the signs. It is the primary provider of such services in the United States.

These logo signs—the blue displays near highway exits showing which gas stations, restaurants, and hotels are available—represent a different business model than traditional billboards. Rather than selling advertising space to the highest bidder, logo sign contracts involve agreements with state transportation departments to install and maintain signage that guides travelers to essential services. The business generates lower margins than traditional advertising but provides stable, recurring revenue with minimal customer concentration risk.

Kevin explains how, upon transitioning to the role of CEO in 1989, he took Lamar Advertising to soaring heights. The episode delves into the successes he achieved during his time, including the pivotal moment of taking the business public. Under Kevin's leadership, the company evolved from traditional paint-based advertising to embracing innovative technologies.

Kevin Reilly Jr. took over as CEO in 1989, representing the continuation of family leadership into its third generation. His brother Sean, father of current CEO Sean Reilly, also played a key role. Kevin Reilly Sr.'s three sons have also been key players for the company: Wendell was Chief Financial Officer from 1985 to 1989; Sean is the Chief Operating Officer and Kevin Reilly Jr. is now the President and Chief Executive Officer.

The family's intertwined leadership reflects an unusual corporate structure where blood ties and business objectives align. A controlling interest is owned by two families. CEO Kevin Reilly Jr. owns approximately 40 percent of the business, and Charles Lamar III and his sister, Mary Lee Lamar Dixon, great-grandchildren of the company's founder, own about 27 percent.

This concentration of ownership in founding family hands—unusual for a company of Lamar's size—has enabled patient, long-term decision-making. While competitors faced quarterly earnings pressure from dispersed institutional shareholders, Lamar could pursue multi-decade strategies like building digital infrastructure or making acquisitions that diluted near-term margins but created long-term value.

The typical entry-level job at Lamar is account executive, and just about every one of our general managers at Lamar started as account executives. The average tenure of a Lamar general manager is over 25 years, and the average tenure of a Lamar regional manager, of which there are six, is more than 35 years.

This extraordinary employee tenure reflects both the company's culture and its family ownership structure. When leadership thinks in generational terms rather than quarterly cycles, employees can build careers rather than optimize for short-term performance metrics. The result is deep institutional knowledge and strong advertiser relationships that compound over time.

VI. Going Public & The Acquisition Machine (1996-2010)

On August 2, 1996, Lamar Advertising Company began trading on the NASDAQ under the ticker symbol LAMR. Lamar Advertising went public on August 2, 1996, with an initial public offering price of approximately $19 per share on the NASDAQ under the ticker LAMR.

The IPO involved selling approximately 14% of the company's stock to the public, raising capital to fuel expansion while the founding families retained majority control through Class B shares with enhanced voting rights. The company employs a dual-class share structure, with Class A common stock held by public investors and Class B common stock, which carries 10 votes per share compared to one vote per Class A share, reserved exclusively for permitted holders including members of the founding Reilly family.

The Reilly family maintains significant influence through ownership of Class B shares, controlling approximately 62% of the total voting power of the company's outstanding capital stock as of December 31, 2024, enabling them to elect the entire board of directors and direct corporate policies.

This dual-class structure has proven crucial to Lamar's strategy. Unlike competitors beholden to dispersed shareholders demanding short-term returns, Lamar's controlling family can prioritize long-term value creation—a dynamic that has enabled patient capital allocation in digital infrastructure and strategic acquisitions.

Post-IPO, Lamar unleashed its acquisition strategy. Lamar undertook a vigorous acquisitions program in the 1990s, despite the fact that it faced some problems. A major, industrywide setback was the steady decline in the billboard advertising of tobacco products, which had begun in 1992. Leading tobacco companies, yielding to both governmental mandates and societal pressures, began a drastic reduction in their outdoor advertising, a policy that continued over the next several years. It cut fairly deep into the billboard advertising business and left many billboards blank. Recovery was slow.

The tobacco advertising decline forced the industry to diversify its customer base. Billboards that had long displayed Marlboro cowboys and Camel characters needed new advertisers. Lamar and its competitors pivoted toward local businesses, healthcare providers, automotive dealers, and quick-service restaurants—categories that remain the company's largest customer segments today.

The largest acquisition in company history came in 2001. In 2001, the company completed its largest acquisition to date by purchasing Chancellor Media's outdoor advertising division for $1.1 billion. This transformative deal significantly expanded Lamar's geographic footprint and market share.

In October 2004, Lamar swapped assets in South Carolina and Georgia to Fairway Outdoor Advertising, in exchange for the Palm Springs, CA; Fayetteville, NC; Rocky Mount, NC; and New Bern, NC assets. Later in November, Lamar acquired Obie Media Corporation of Eugene, Oregon, adding outdoor displays in Idaho, Oregon, and Washington.

The Obie Media acquisition demonstrated Lamar's strategy of expanding into new geographic markets through purchasing established regional operators. Rather than building billboard networks from scratch—a near-impossibility given regulatory constraints—Lamar grew by consolidating existing operators who had accumulated permits over decades.

The 2008 financial crisis tested the company's resilience. Outdoor advertising has proven sensitive to economic cycles, as marketing budgets typically face early cuts during recessions. Lamar responded with severe capital discipline: capex dropped from $198 million in fiscal 2008 to just $38.8 million in 2009 and $43.5 million in 2010. This flexibility—the ability to dramatically reduce investment during downturns—reflects the relatively low maintenance capital requirements of the billboard business.

In January 2016, Lamar purchased advertising rights in five major American markets from Clear Channel Outdoor for $458.5 million. This acquisition reinforced Lamar's strategy of building density in attractive markets rather than pursuing scale for its own sake.

The acquisition playbook that emerged from this period remains central to Lamar's strategy: identify well-run regional operators with attractive market positions, acquire them at reasonable valuations, integrate them into the Lamar operating system, and generate synergies through shared overhead and improved sell-through rates.

VII. Inflection Point #1: The Digital Billboard Revolution (2001-Present)

The most important strategic decision in Lamar's modern history occurred in Baton Rouge in 2001, when the company installed what it claims was the outdoor advertising industry's first large-format digital billboard.

The brainchild of former Lamar Vice President of Operations Bobby Switzer, the first digital billboard was conceived by Lamar and debuted in Baton Rouge in 2001. In the 20 years since, digital has transformed the Out of Home industry.

"The creation of that first digital billboard changed the entire ballgame for the Out of Home industry," Sean Reilly, CEO of Lamar Advertising Company, said. "It began the process of transforming Out of Home into the advanced, data-powered, technology-enabled, and measurable channel that it has become."

The economics of digital conversion are extraordinarily compelling. When we take down a static unit on average it's doing about $3,000 a month... replace that with digital unit that costs a little over $200,000... your revenue lift is give or take 5 or 6 times so you're going to do something in the neighborhood of $15,000 a month on that board.

A static to digital billboard conversion has a 43% return on capital.

This math deserves careful attention. A $200,000 investment that generates $15,000 monthly (versus $3,000 for the static alternative) produces $180,000 in annual revenue, implying roughly a 1-year payback on the incremental revenue and exceptional returns thereafter. Few capital investments in any industry offer such attractive profiles.

Why do digital billboards generate so much more revenue than static displays?

Unlike static billboards, digital billboards display advertising messages that rotate every six to eight seconds like a slideshow, with typically six to eight advertisers sharing the same billboard at any given time.

They're paying about $3,000 for the slot... but they don't have to pay the production and they can of course change their copy from their desktop at will and that flexibility is why they're willing to share space with other advertisers. So their absolute dollars in terms of the cost of the space stays about the same. Their cost per thousand impressions goes up.

From the advertiser's perspective, digital billboards offer flexibility that static displays cannot match. Campaigns can be updated instantly, creative can be day-parted (different messages for morning commuters versus evening traffic), and advertisers can respond in real-time to events. A restaurant can advertise breakfast specials at 7 AM and dinner deals at 5 PM. A retailer can promote a flash sale within hours of deciding to run it.

From Lamar's perspective, digital conversion transforms a single-occupancy asset into a multi-tenant property. The same physical location can generate revenue from eight advertisers simultaneously rather than one. While each individual advertiser pays roughly the same as they would for a static board, total revenue from that location increases 5-6x.

In just seven years following the debut of the first digital billboard, Lamar grew its digital network to 1,000 displays. Today, Lamar operates the largest network of large-format digital billboards in the United States with approximately 3,800 displays.

By 2024, that number had grown to approximately 5,000 digital displays. In addition to its more traditional out-of-home inventory, Lamar is proud to offer its customers the largest network of digital billboards in the United States with approximately 5,000 displays.

The revenue concentration is remarkable. Of Lamar's 159,000 billboards today, 5,000 (or roughly 3%) are digital. However, digital billboards accounted for 32% of the company's annual revenue in 2024, so there's significant potential for growth through conversions.

This disproportion—3% of units generating 32% of revenue—represents perhaps the most attractive feature of Lamar's current positioning. The company possesses 154,000 static billboards that could theoretically be converted to digital, each conversion generating 5-6x revenue uplift with 40%+ returns on capital.

In practice, the conversion opportunity is constrained by regulatory approvals and market demand. Lamar is targeting 350 digital conversions in 2025, potentially reaching 375. At this pace, the company has decades of attractive reinvestment opportunities ahead.

The digital transformation also created operational efficiencies. Lamar established a Network Operating Center in 2006 to monitor and support digital billboards nationwide, enabling centralized management of content updates, troubleshooting, and performance monitoring. 2006: Lamar forms the Network Operating Center which monitors and supports the company's digital billboards nationwide.

Subsequent milestones demonstrated expanding capabilities: - 2011: First real-time March Madness scores displayed on billboards - 2012: First user-generated digital billboard campaign - 2015: Digital inventory made available for programmatic buying - 2016: Vehicle recognition technology incorporated for Chevy campaign

For long-term investors, the digital transformation represents both a competitive moat and a long-duration growth opportunity. Lamar's first-mover advantage in digital—combined with its scale, permits, and geographic reach—has created capabilities that competitors would need years and billions of dollars to replicate.

VIII. Inflection Point #2: The REIT Conversion (2014)

In April 2014, after a multi-year review process, the IRS issued a private letter ruling approving Lamar's conversion to a Real Estate Investment Trust. The IRS approved the plan in a private letter ruling, and Lamar says its conversion is expected to be effective as of Jan. 1, 2014. The advertising giant underwent an internal corporate restructuring in 2013 so it would comply with REIT rules for the 2014 tax year.

Companies that qualify as REITs can reduce their tax burden and increase their cash flow as long as they distribute at least 90% of their annual taxable income to investors through dividends.

The REIT conversion transformed Lamar's tax structure fundamentally. As a C-corporation, Lamar paid corporate income taxes on profits, and shareholders paid taxes again when they received dividends—the classic "double taxation" problem. Real estate investment trusts don't have to pay corporate income taxes on profits as long as the trusts give at least 90 percent of profits to shareholders.

For shareholders, this meant more of each dollar of operating profit reached their pockets. For Lamar, it meant a lower cost of capital—the company could offer attractive yields to income-seeking investors while retaining enough capital for growth investments.

The strategic rationale extended beyond tax efficiency. Lamar is a modern economy REIT that generates revenues by leasing advertising space on billboards, buses, shelters, benches, logo plates, and in airport terminals. Lamar has grown to become one of the largest out of home (OOH) advertising companies in the world, with more than 360,000 displays across the United States and Canada.

Billboard companies qualify as REITs because their assets—the land under billboards and the structures themselves—constitute real property. Just as office REITs generate income by leasing office space and apartment REITs generate income by leasing residential units, billboard REITs generate income by leasing advertising space. The "tenant" happens to be an advertiser rather than a resident, but the underlying economics share important characteristics: long-term site control, capital-intensive physical assets, and recurring revenue streams.

Lamar's competitive advantages include its extensive geographic footprint across smaller and mid-sized markets where it often faces less competition, its early and continued investment in digital technology, and its REIT structure, which provides tax advantages not available to some competitors.

This last point deserves emphasis. Clear Channel Outdoor, Lamar's largest direct competitor, is not structured as a REIT. Interest totaled $404 million during 2024 which is 90% of cashflow from continuing operations at Clear Channel, reflecting a highly leveraged balance sheet that constrains strategic flexibility. Lamar's REIT structure, combined with more conservative leverage, provides meaningful competitive advantages in capital allocation.

Post-REIT Performance:

The REIT conversion has coincided with strong shareholder returns. Next year marks Lamar's 20th year operating as a REIT. Over this period, the company has delivered consistent dividend growth while continuing to invest in digital conversion and acquisitions.

Lamar Advertising's total dividend distribution for 2024 was $5.60 per share, paid across four quarterly distributions. LAMR's largest quarterly dividend payment in 2024 was $1.65 per share, distributed on December 30, 2024.

For income-focused investors, Lamar offers an unusual combination: high yield (currently around 5%) with dividend growth potential. Unlike many high-yield REITs that distribute most of their cash flow, Lamar retains capital for growth investments—primarily digital conversions and acquisitions—that should drive continued dividend increases.

IX. Inflection Point #3: Programmatic & The Tech Stack (2020s)

The latest chapter in Lamar's evolution involves embracing programmatic advertising technology—automated buying and selling of ad inventory through digital platforms. While programmatic buying revolutionized online advertising over the past decade, outdoor advertising lagged behind due to the physical nature of billboard inventory and the industry's historically fragmented structure.

Lamar's approach to this challenge centered on a strategic partnership with Vistar Media, a leading provider of programmatic technology for digital out-of-home advertising.

Vistar Media, the leading global provider of programmatic technology for digital out-of-home, announced a Series B funding round of $30M from Lamar Advertising Company (Nasdaq: LAMR).

"By providing capital to a clear leader in the programmatic space, Lamar is investing in the future of our industry and the next evolution of our compelling media channel," Lamar chief executive officer Sean Reilly said.

The $30 million investment, made in July 2021, gave Lamar a board seat at Vistar while maintaining Vistar's independence as a technology partner serving the broader industry. This structure allowed Lamar to benefit from programmatic innovation without the distraction of building technology capabilities in-house.

Lamar Advertising Company selected Vistar's content management software (CMS), Cortex, to power its network of digital out-of-home billboards across the U.S. The agreement follows a partnership forged in 2023 in which Lamar chose Vistar to run its Denver Transit DOOH network.

Lamar's entire national footprint of 5,000 digital billboards to run on Cortex, Vistar's CMS.

The strategic value of programmatic capabilities extends beyond technology. It positions Lamar to capture advertising dollars from digital-native buyers who are accustomed to purchasing inventory programmatically. Media agencies that allocate budgets across search, social, display, and video increasingly want to include out-of-home in their programmatic campaigns.

While Lamar's programmatic channel is relatively new and accounts for just 2% of its business, Reilly says it's a major growth area. The company's programmatic channel is growing 15% to 20% annually.

Programmatic revenue increased 70%. in Q3 2024, demonstrating the growth trajectory of this channel even from a small base.

In January 2025, T-Mobile announced its acquisition of Vistar Media. T-Mobile has entered an agreement to acquire digital-out-of-home media company Vistar Media for approximately $600 million through its T-Mobile Advertising Solutions business.

Lamar's 20% share of the sale price of $600 million comes to $120 million or four times Lamar's initial investment. Not a bad investment and a big cash infusion to an already cash strong company.

On February 3, 2025, T-Mobile USA, Inc. acquired 100% of Vistar Media Inc. In connection with the closing of the Sale, the Company received $115.1 million in cash as consideration for the sale of its 20% equity interest in Vistar Media.

The Vistar exit demonstrated both the value of Lamar's investment thesis and the strategic importance of programmatic technology to the broader advertising ecosystem. T-Mobile—a sophisticated technology company seeking to build its advertising business—paid a premium to acquire Vistar's capabilities.

"I'm excited about T-Mobile buying Vistar because T-Mobile is a really savvy company," Reilly explains. "They're very entrepreneurial, and they're the primary source of this rich data that can be used by our clients to help them more effectively buy our space."

For Lamar, the relationship with Vistar continues through the CMS and programmatic platform, now backed by T-Mobile's resources and data assets. The investment provided attractive financial returns while positioning Lamar to benefit from continued industry digitization.

X. The Modern Acquisition Playbook & UPREIT Innovation (2020s)

In July 2025, Lamar completed what it describes as the first-ever UPREIT transaction in the billboard industry—a milestone that may reshape how the company executes acquisitions going forward.

The transaction was enabled by Lamar's organization as an UPREIT, or Umbrella Partnership Real Estate Investment Trust. This structure allows Lamar to issue partnership units of Lamar LP to billboard owners on a tax-deferred basis.

"This deal represents a significant milestone for Lamar," said Sean Reilly, Lamar's Chief Executive Officer. "We're thrilled to have Ernie and the other Verde owners as partners, and we expect this UPREIT structure to become a template for future acquisitions with owners who want to diversify their asset bases in a tax-efficient manner."

The Verde Outdoor acquisition deserves detailed attention because it illustrates both the UPREIT mechanism and Lamar's acquisition strategy.

Closed on July 2, 2025, the deal adds over 1,500 billboard faces, including 80 digital displays, to Lamar's portfolio across 10 states, enhancing its presence in the Midwest, Southeast, and Mid-Atlantic regions. Verde Outdoor, founded in 2021 by Ernest C. Garcia II, grew rapidly through strategic acquisitions and organic development before partnering with Lamar.

Under traditional acquisition structures, sellers who receive cash or stock must recognize capital gains immediately and pay taxes. For founders of billboard companies who have held permits for decades, these tax bills can be substantial. The UPREIT structure solves this problem:

In this transaction, Verde contributed its assets to Lamar Advertising Limited Partnership ("Lamar LP"), the operating partnership subsidiary of Lamar that holds the Company's assets. In return, the owners of Verde received common units of Lamar LP, with each common unit of Lamar LP designed to track the value of a share of Lamar's Class A common stock. Holders of the Lamar LP common units receive cash distributions on each common unit in an amount equal to the per share dividend paid on Lamar's common stock. Common units of Lamar LP are convertible into cash or shares of Class A common stock of Lamar.

These units entitle them to the same cash distributions as common shareholders. Meanwhile, the tax on their gains will be deferred until the units are converted to cash or Lamar shares, a conversion that they trigger on their own timetable. The UPREIT is a really compelling option for sellers who like the outdoor business, but want to diversify their asset base in a tax efficient manner, all the while enjoying income from our distributions.

For Lamar, the UPREIT structure offers several advantages:

- Access to tax-sensitive sellers: Owners who would otherwise hold onto appreciated assets to avoid taxes may find UPREIT terms attractive

- Competitive differentiation: Competitors without UPREIT structures cannot offer equivalent terms

- Aligned incentives: Sellers who receive LP units remain economically invested in Lamar's success

- Capital efficiency: No immediate cash outlay reduces financing needs

The billboard sector is 90% fragmented, with countless small players owning prime locations. The UPREIT structure addresses two critical pain points: Tax Barriers: Traditional sales force sellers to pay taxes upfront, discouraging deals. Cost Efficiency: Buyers like Lamar avoid the dilution of issuing shares or the risk of debt-fueled purchases.

M&A Activity:

Through Q2, we had spent $87,000,000 in cash on 20 acquisitions, including a deal that we expect to close this morning, bringing the year to date total to approximately $110,000,000 in cash acquisitions. It's been an active year on the M and A front. In early July, meanwhile, we completed a milestone deal with the first ever UPREIT transaction in the billboard space. Our counterparty, Verde Outdoor, contributed their billboards in the Southeast, Northeast and Midwest to us. In return, we issued nearly 1,200,000 units in our operating partnership subsidiary to Verde's owners.

Lamar is targeting $150 million in acquisitions in 2025, focusing on smaller, high-quality deals. "It looks to me like we'll exceed that pretty easily," Reilly says. "There's a lot of activity." Lamar has a history of acquiring other outdoor ad companies to expand its reach and market share. "It's in our DNA to expand through M&A deals," he says. Reilly says the company's M&A activity is primarily funded through free cash flow. Typically, Lamar has around $150 million available annually after interest payments, capital expenditures, and distributions to expand its footprint through M&A.

XI. Leadership: Sean Reilly and the Fourth Generation

Sean Eugene Reilly represents the fourth generation of family leadership at Lamar—a continuity that distinguishes the company from virtually all publicly traded competitors.

Sean E. Reilly has served as Chief Executive Officer since February 2011 and as President since February 2020. Prior to becoming CEO, Mr. Reilly served as Chief Operating Officer and President of the Company's Outdoor Division. He began working with the Company in 1987 and served as a director of the Company from 1989 to 1996 and from 1999 until 2003. Mr. Reilly served in the Louisiana Legislature as a State Representative from 1988 to 1996.

"I'm forth generation working at Lamar," said Sean Reilly in his charming Louisiana accent. The company was originally founded by his mother's grandfather back in 1902 and is now one of the largest outdoor advertising companies in North America, with more than 325,000 displays across the United States, Canada and Puerto Rico. "I consider it my responsibility to pass this legacy on," he continued.

His background combines academic credentials with practical political experience. Sean Reilly received a B.A. from Harvard University in 1984 and a J.D. from Harvard Law School in 1989.

Joined Lamar Advertising in 1987 as Vice President of Mergers and Acquisitions, later serving as a director, COO and President of the Outdoor Division, then becoming CEO in February 2011 and President in February 2020. He began his journey at Lamar Advertising in 1987 as Vice President of Mergers and Acquisitions, marking the start of his long and distinguished tenure at the company.

His eight years in the Louisiana Legislature provided experience navigating regulatory environments—useful preparation for an industry where permitting relationships with state and local governments are essential to operations.

"We try to live by the golden rule at Lamar," Mr. Reilly said. This emphasis on values and culture pervades company communications. We live by the Golden Rule, and we operate with honesty and integrity in every aspect of our business. We are open with our employees, transparent with our customers and loyal to the communities in which we serve.

Under Reilly's leadership, Lamar has: - Completed the REIT conversion (2014) - Expanded the digital network from under 2,000 to over 5,000 displays - Invested in programmatic capabilities through the Vistar partnership - Pioneered the UPREIT structure for acquisitions - Navigated the COVID-19 pandemic and subsequent recovery

"When you talk about ad spend, 80% of our tenant base is local businesses," says Sean Reilly, president and CEO of Lamar, which was founded by his maternal great-grandfather. This focus on local advertisers—rather than national brand campaigns—reflects a strategic choice. Local advertisers tend to be stickier customers with less budget volatility than national campaigns that can shift quickly between media channels.

Kevin Reilly Jr. as Executive Chairman:

Kevin P. Reilly Jr., a third-generation family member in the company's leadership, has been Executive Chairman of the Board since February 2020, after serving as Chairman and previously as Chief Executive Officer from 1989 to 2011; he provides guidance on long-term strategy and governance. Reilly has been a director since February 1984.

The two Reillys—Kevin Jr. as Executive Chairman and Sean as CEO—provide continuity of family oversight while enabling day-to-day management transition. This succession planning, executed smoothly over multiple years, contrasts with the abrupt leadership changes that often destabilize family businesses.

XII. Competitive Position & Industry Dynamics

The U.S. outdoor advertising market features three significant publicly traded players: Lamar, Clear Channel Outdoor, and OUTFRONT Media. Their competitive positions and financial profiles differ meaningfully.

Market Share and Geographic Focus:

Lamar's more rural roadside billboard plant relies on national advertising for only 21% of revenue. Clear Channel Outdoor Americas plant in the US relies on national advertising for 35% of total revenues. OUTFRONT's urban billboard/transit plant relies on national advertising for 42% of total revenues.

Lamar billboards tend to be in smaller markets with lower revenues. OUTFRONT billboards tend to be in urban markets with higher revenues. Clear Channel billboards fall in the middle.

This geographic differentiation has strategic implications. Lamar's focus on smaller and mid-sized markets means less exposure to the volatility of national advertising budgets—which are typically the first to be cut during recessions—but also less access to premium pricing available in major DMAs like New York and Los Angeles.

Also setting Lamar apart is its strong concentration of billboards in small and mid-size U.S. markets.

Financial Comparison:

Lamar Advertising continued its trend of steady growth, reporting a 4.5% increase in total revenue for Q2 2024, which reached $539.1 million.

Clear Channel Outdoor reported a consolidated revenue of $637.2 million for Q2 2024, reflecting a 7.7% decline compared to the previous year. This decrease was largely influenced by the divestiture of the company's European operations, which had a significant impact on overall revenues. However, the Americas segment saw a 5.2% increase, bringing in $559 million. This growth was primarily driven by digital transformation efforts and a remarkable 21.4% increase in airport advertising revenue.

OUTFRONT Media reported a 4% increase in total revenue for Q2 2024, bringing the figure to $477.3 million. Billboard revenue grew by 2.3% to $360.2 million, driven by the company's ongoing focus on digital expansion and its strategic investments in transit advertising.

The key differentiator is financial health. Clear Channel Outdoor made few acquisitions during the past two years due to high leverage. Interest totaled $404 million during 2024 which is 90% of cashflow from continuing operations.

All of the out of home companies trail the S&P 500 poorer performance during and just after covid. The S&P is up 85% for the past five years, Lamar up 51%, OUTFRONT is down 28% and Clear Channel Outdoor is down 69%.

Lamar's conservative leverage—total debt around $3.2 billion with strong cash flow coverage—provides flexibility that heavily indebted competitors lack. This financial strength enables continued investment in digital conversion and strategic acquisitions while competitors manage debt loads.

Industry Growth:

The global billboard and outdoor advertising market size was estimated at USD 38.32 billion in 2024 and is projected to reach USD 60.81 billion by 2030, growing at a CAGR of 8.1% from 2025 to 2030.

The OOH industry's revenue surpassed $9 billion in 2024, the highest volume to date, according to the Out of Home Advertising Association of America (OAAA).

The outdoor advertising industry recovered strongly from the COVID-19 pandemic, which caused temporary but severe disruption as reduced driving and transit ridership depressed billboard viewership. Following the COVID-19 pandemic, which caused a 10.5% revenue decline to $1.57 billion in 2020 due to reduced mobility, Lamar experienced robust recovery driven by surging demand for digital out-of-home advertising. Revenues rebounded to $1.79 billion in 2021 (up 13.9%), $2.03 billion in 2022 (up 13.7%), $2.11 billion in 2023 (up 3.9%), and $2.21 billion in 2024 (up 4.6%).

XIII. Financial Performance & Capital Allocation

Lamar's financial results reflect the steady, cash-generative nature of the billboard business combined with disciplined capital allocation.

2024 Results:

Net revenue was $2.21 billion. Net income was $362.9 million. Adjusted EBITDA was $1.03 billion.

"Our revenue growth accelerated in the fourth quarter, aided by strength in political, local and programmatic. This allowed us to deliver full-year AFFO of $7.99 per share, above the top end of our revised guidance range," Lamar chief executive Sean Reilly said. "For 2025, we anticipate further growth in diluted AFFO, to a range of $8.13 to $8.28 per share."

Revenue Mix:

Lamar's largest revenue driver by far are its towering roadside billboards, strategically located along high-traffic expressways, highways, interstates, and primary arteries. These billboards account for around 88% of the company's revenues. Smaller portions come from interstate logo advertising (4% to 6%) and transit advertising (7%).

Capital Allocation Priorities:

The REIT structure requires distributing at least 90% of taxable income to shareholders as dividends. Lamar manages this requirement while retaining capital for growth through a combination of depreciation (non-cash charge that reduces taxable income below cash flow), modest debt utilization, and occasional equity issuance.

Reilly says the company's M&A activity is primarily funded through free cash flow. Typically, Lamar has around $150 million available annually after interest payments, capital expenditures, and distributions to expand its footprint through M&A.

Digital conversion represents the highest-return use of capital. Lamar is targeting 350 digital conversions in 2025, potentially reaching 375. At roughly $200,000 per conversion, this implies $70-75 million of annual digital capex generating 40%+ returns.

Dividend Policy:

The company made four quarterly distributions throughout 2024: March 28: $1.30 per share, June 28: $1.30 per share, September 30: $1.40 per share, December 30: $1.65 per share.

The rising quarterly dividend trajectory reflects management confidence in sustained cash flow growth. At current prices, Lamar offers a dividend yield around 5%—attractive for a company also investing in high-return growth opportunities.

Balance Sheet:

As of December 31, 2024, Lamar had $506.7 million in total liquidity that consisted of $457.2 million available for borrowing under its revolving senior credit facility and $49.5 million in cash and cash equivalents. There were $284.0 million in borrowings outstanding under the Company's revolving credit facility.

Total debt of approximately $3.2 billion represents a debt-to-EBITDA ratio around 3x—conservative for a REIT and well below levels that would constrain strategic flexibility.

XIV. Bull Case, Bear Case, and Strategic Assessment

Bull Case:

-

Regulatory moat is permanent: The Highway Beautification Act and local zoning regulations effectively prevent meaningful new supply. Existing permit holders benefit from scarcity that increases asset values over time.

-

Digital conversion runway: With only 3% of billboards converted to digital generating 32% of revenue, decades of high-return reinvestment opportunities remain. Each conversion generates 40%+ returns on capital.

-

UPREIT unlocks consolidation: The newly deployed UPREIT structure makes Lamar the most attractive acquirer for tax-sensitive sellers in a 90% fragmented industry. Accelerated consolidation could drive meaningful market share gains.

-

Local advertising resilience: The 80% local customer base is less cyclical than national brand advertising, providing stability through economic downturns.

-

Programmatic growth: Growing 15-20% annually from a small base, programmatic capabilities position Lamar to capture digital-native advertising budgets.

Bear Case:

-

Digital advertising competition: Online advertising continues taking share of total advertising spend. While outdoor has held relatively steady, long-term competitive position versus Google, Meta, and Amazon is uncertain.

-

Autonomous vehicles: Self-driving cars could fundamentally change the economics of roadside advertising. If passengers are looking at screens rather than the road, billboard impressions lose value.

-

Regulatory risk: Future environmental or aesthetic regulations could restrict billboard operations, though the strong lobbying position of the OAAA has historically protected the industry.

-

Interest rate sensitivity: As a REIT, Lamar competes with bonds and other income investments. Rising rates increase the cost of capital and may compress valuations.

-

Cyclicality: Despite local focus, outdoor advertising is economically sensitive. The 10.5% revenue decline in 2020 demonstrates vulnerability to severe downturns.

Porter's Five Forces Analysis:

-

Threat of New Entrants: Very Low. Regulatory barriers effectively eliminate new competition along federal highways. This is the business's primary moat.

-

Bargaining Power of Suppliers: Moderate. Landowners can demand higher rents at lease renewal, though Lamar's scale and long-term relationships provide negotiating leverage.

-

Bargaining Power of Buyers: Moderate. Advertisers have alternatives (digital, TV, radio, print), but outdoor's unique characteristics—high visibility, broad reach, unskippable impressions—limit substitution.

-

Threat of Substitutes: Moderate to High. Digital advertising offers precise targeting and measurability that outdoor cannot match. However, outdoor's "unskippable" nature provides unique value in an ad-blocking era.

-

Industry Rivalry: Moderate. Three public players plus fragmented regional operators. Competition is primarily on service quality and geographic coverage rather than price.

Hamilton Helmer's 7 Powers Assessment:

-

Scale Economies: Moderate. Central NOC and programmatic infrastructure create operating leverage, but local market dynamics limit benefits of national scale.

-

Network Effects: Low. Unlike platform businesses, billboard networks don't become more valuable as they grow.

-

Counter-Positioning: Moderate. Digital-native competitors would need to build physical infrastructure and navigate regulatory processes that take decades.

-

Switching Costs: Low to Moderate. Advertisers can shift between outdoor operators, though relationships and geographic coverage create friction.

-

Branding: Low. Advertisers care about locations and reach, not brand name of the billboard operator.

-

Cornered Resource: High. Permits and land positions accumulated over 120+ years cannot be replicated. This is the primary source of competitive advantage.

-

Process Power: Moderate. Decades of operational experience create execution advantages, particularly in regulatory navigation and local market knowledge.

Key Performance Indicators to Track:

For investors monitoring Lamar's ongoing performance, two metrics warrant particular attention:

-

Acquisition-Adjusted Revenue Growth: This metric adjusts for the impact of acquisitions to reveal organic growth trends. Management typically provides this figure in quarterly earnings releases. Consistent positive organic growth indicates healthy demand for outdoor advertising and effective pricing.

-

Digital Revenue as Percentage of Total Billboard Revenue: Currently at 32%, this metric tracks the progress of digital conversion—the company's highest-return capital allocation opportunity. Continued growth indicates successful execution of the digital strategy.

XV. Conclusion: The Quiet Empire Endures

In an era obsessed with disruption and digital transformation, Lamar Advertising represents an anachronism—a 123-year-old company whose core product, the roadside billboard, would be recognizable to Charles Lamar Sr. when he lost that coin flip in 1908.

Yet this apparent simplicity conceals a sophisticated business with remarkable competitive advantages. The regulatory framework that was supposed to beautify America's highways instead created an impenetrable moat protecting incumbent operators. The digital transformation that threatened to make physical advertising obsolete has instead created Lamar's most attractive reinvestment opportunity, with 40%+ returns on conversion capital. The REIT structure that might have been merely a tax optimization has become a competitive weapon, enabling UPREIT acquisitions that competitors cannot match.

As of December 31, 2024, the company's portfolio included approximately 159,000 billboard displays, with nearly 5,000 being digital, forming the largest digital billboard network in the U.S. Lamar also managed over 138,000 interstate logo signs in 23 states and Canada, as well as about 47,500 transit displays in urban areas.

The family ownership structure—now entering its fourth generation—has enabled patient capital allocation that quarterly-focused competitors struggle to match. When your great-great-grandfather founded the business, you can think in decades rather than quarters.

For long-term investors seeking exposure to a durable franchise with visible reinvestment opportunities, defensive characteristics, and meaningful yield, Lamar warrants consideration. The billboard business will never excite growth-focused investors, but for those who appreciate businesses with competitive advantages that compound quietly over decades, the Quiet Empire of America's Roadways offers something increasingly rare in public markets: a business model that has worked for over a century and shows few signs of stopping.

The question facing investors isn't whether billboards represent the future of advertising—they clearly don't in a world of programmatic digital targeting and personalized content. The question is whether the scarcity of premium roadside locations, combined with the unskippable nature of outdoor impressions and the continued growth of American road traffic, will sustain attractive returns for another generation. Based on the regulatory framework, digital conversion economics, and management's capital allocation track record, the case for yes remains compelling.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube