Amgen: The Biotechnology Pioneer

I. Introduction & Episode Roadmap

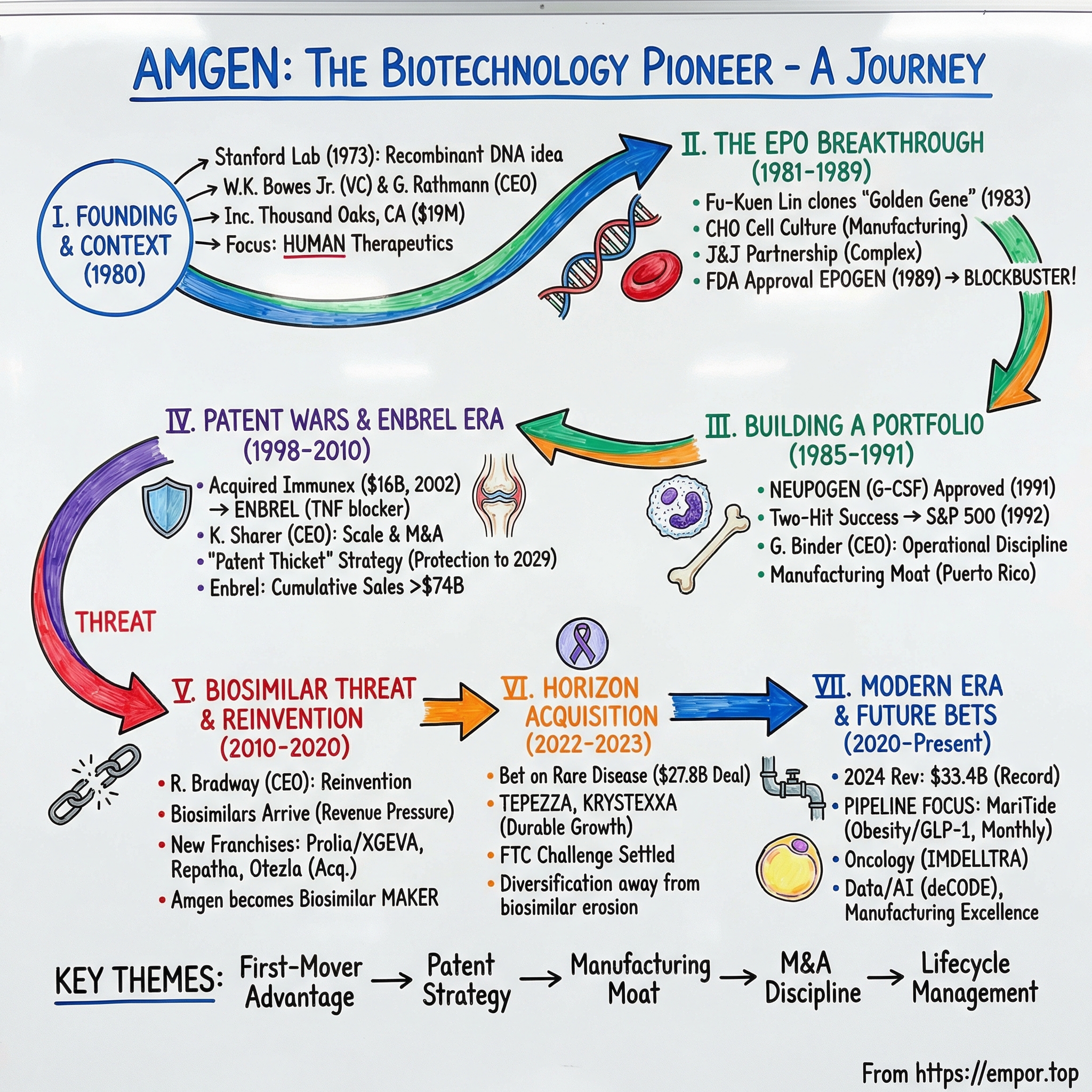

Picture this: It's 1983, and in a cramped laboratory in Thousand Oaks, California, a scientist named Fu-Kuen Lin is hunched over a microscope at 2 AM, searching for a single gene fragment among 1.5 million pieces of human DNA. It's like finding not just a needle in a haystack, but a specific atom within that needle. Two years later, when Lin finally isolates the erythropoietin gene, he doesn't just create a drug—he births an entire industry. That discovery would generate over $100 billion in revenue and transform Amgen from a venture-backed startup into the world's largest independent biotechnology company.

Today, Amgen stands as a colossus in the biotech landscape, headquartered still in Thousand Oaks, ranked 18th among the world's largest biomedical companies by revenue. The numbers tell a story of dominance: Prolia/XGEVA generating $6.7 billion, Enbrel pulling in $3.3 billion, and Repatha adding $2.3 billion to the company's 2024 revenues. But those numbers obscure the real question that should fascinate any student of business history: How did a company that nearly ran out of cash in its early years become the first to create a blockbuster biologic drug and then sustain that leadership for over four decades? The story of Amgen reads like a Silicon Valley fairytale, except the heroes wear lab coats instead of hoodies, and their garage was actually a legitimate research facility in Thousand Oaks. This is a tale of scientific audacity, patent warfare, and the transformation of human proteins into a pharmaceutical empire worth over $150 billion. It's about how a company that started with $19 million and a prayer became the world's largest independent biotechnology company, generating $33.4 billion in revenue in 2024.

The fundamental question isn't just how Amgen succeeded—plenty of biotech companies have had breakthrough drugs. It's how they've sustained that success for over four decades, navigating patent cliffs, biosimilar threats, and technological disruptions while maintaining their position at the apex of the industry. This is the story of first-mover advantage crystallized into corporate dominance, of how being first to market with a biologic drug created compounding advantages that persist to this day.

Our journey spans from the birth of recombinant DNA technology to the modern era of obesity drugs and AI-driven drug discovery. We'll explore the patent strategies that extended drug monopolies for decades, the M&A playbook that turned acquisitions into growth engines, and the manufacturing excellence that became a competitive moat. Along the way, we'll meet the scientists who found needles in genetic haystacks, the executives who bet billions on unproven technologies, and the lawyers who built patent fortresses around molecular structures.

The narrative arc follows four major themes. First, the power of platform technologies—how Amgen's early focus on recombinant DNA created capabilities that spawned multiple blockbusters. Second, the art of lifecycle management—extending patent protection through legal creativity and incremental innovation. Third, the strategic pivot from pure biologics player to diversified biopharma powerhouse. And fourth, the perpetual tension between innovation and competition, as Amgen simultaneously defends against biosimilars while becoming a biosimilar manufacturer itself.

What emerges is not just a corporate history but a masterclass in building sustainable competitive advantages in one of the world's most challenging industries. It's about turning scientific breakthroughs into business empires, and more importantly, maintaining that empire when the original magic starts to fade.

II. The Biotech Revolution & Founding Context

The year was 1979, and biology was having its transistor moment. Just three years earlier, Genentech had been founded in a San Francisco garage, promising to turn bacteria into tiny pharmaceutical factories. The scientific community was skeptical—many believed that manipulating DNA to produce human proteins was either impossible or decades away from commercialization. But by 1978, Genentech had successfully used recombinant DNA technology to produce human insulin in bacteria, proving the doubters wrong and igniting a gold rush in molecular biology.

Enter William K. "Bill" Bowes Jr., a venture capitalist with an unusual combination of deep pockets and deeper patience. Bowes wasn't your typical Silicon Valley financier—he understood that biotechnology required a different investment thesis than semiconductors or software. Where tech startups might pivot in months, biotech companies needed years just to validate their basic science. Bowes had been watching Genentech's progress closely and recognized an opportunity: while everyone was rushing to copy Genentech's insulin success, he would build something more ambitious—a company focused on producing complex human proteins that the body couldn't make enough of on its own.

On April 8, 1980, Applied Molecular Genetics Inc.—soon shortened to the more pronounceable AMGen—was officially incorporated in Thousand Oaks, California. The location was strategic rather than accidental. Thousand Oaks sat in a sweet spot between three major research universities: UCLA, Caltech, and UC Santa Barbara. This wasn't just about proximity to talent; it was about being close enough to collaborate but far enough away to avoid the bidding wars for scientists that were already erupting in the San Francisco Bay Area.

The initial funding was substantial for its time: $19 million from a consortium of venture capital firms and two major corporations. This wasn't garage startup money—it was a serious bet on an unproven industry. The investors included some of the smartest money in venture capital, but what distinguished this founding was the immediate focus on building scientific credibility. Before hiring a single bench scientist, the founders assembled a scientific advisory board that read like a who's who of molecular biology.

The advisory board's composition revealed the company's ambitions. Norman Davidson from Caltech was a pioneer in DNA research. Leroy Hood would later invent the automated DNA sequencer. Marvin Caruthers had developed methods for synthesizing DNA. These weren't just prestigious names for the letterhead—they were active participants who would guide the company's scientific strategy. The message was clear: Amgen intended to be a serious scientific enterprise, not just a commercial venture riding the biotech wave.

But scientific advisors don't run companies. For that, Bowes and his partners made a recruitment that would define Amgen's trajectory: they hired George Rathmann away from Abbott Laboratories. Rathmann wasn't an obvious choice—at 52, he was older than the typical startup CEO, and his experience was in traditional pharmaceuticals, not biotechnology. But that was precisely the point. While other biotech startups were led by scientists trying to learn business or businesspeople trying to understand science, Rathmann brought something different: deep experience in taking drugs from laboratory to market.

At Abbott, Rathmann had been vice president of research and development in the diagnostics division. He understood FDA regulations, manufacturing at scale, and the complex dance of pharmaceutical marketing. More importantly, he had a philosophy about biotechnology that differed from the prevailing wisdom. While Genentech was focused on copying existing drugs like insulin and growth hormone using their new technology, Rathmann believed the real opportunity lay in creating entirely new therapeutic proteins—molecules that didn't exist as drugs because they couldn't be extracted from natural sources in sufficient quantities.

Rathmann officially joined as president and CEO in October 1980, and immediately set about building a culture that would become Amgen's secret weapon. He instituted what he called "management by walking around," spending hours in the labs talking to scientists about their work. But this wasn't just executive theater—Rathmann had a PhD in physical chemistry from Princeton and could engage with the science at a deep level. Scientists recall him asking probing questions that often led to breakthrough insights.

The company began operations in earnest in 1981, moving into a 24,000-square-foot facility that seemed impossibly large for their initial team of fewer than 50 employees. But Rathmann was thinking ahead. He structured the research organization into small, autonomous teams—each focused on a different protein target but sharing core technologies and insights. This modular approach would prove crucial when some projects failed (as most did in biotech) while others succeeded beyond anyone's imagination.

The early research strategy was both focused and opportunistic. The team would scan the scientific literature for proteins that met three criteria: they had clear therapeutic potential, they were impossible or impractical to extract from natural sources, and their genes hadn't already been claimed by competitors. It was a needle-in-haystack approach, but with multiple teams searching different haystacks simultaneously.

The initial scientific staff was an eclectic mix of fresh PhDs eager to work at the cutting edge and experienced researchers who had grown frustrated with the bureaucracy of big pharma. The company culture that emerged was part academic laboratory, part startup, and part pharmaceutical company—a hybrid that shouldn't have worked but somehow did. Friday afternoon beer hours coexisted with rigorous FDA documentation standards. Casual dress codes accompanied serious discussions about clinical trial design.

One early employee recalled the atmosphere as "controlled chaos with a purpose." Projects would start and stop based on preliminary data. Resources would shift dramatically from one team to another based on promising results. But through it all, Rathmann maintained focus on the ultimate goal: getting therapeutic proteins to patients. This wasn't research for research's sake—every experiment had to answer the question, "How does this get us closer to a drug?"

The technical challenges were staggering. Recombinant DNA technology was still in its infancy. The tools that modern biotech takes for granted—automated sequencers, commercial cloning vectors, optimized expression systems—didn't exist. Everything had to be built from scratch. Want to sequence a gene? That meant running gel after gel, reading bands by eye, often getting just 20-30 base pairs per day. Need to express a protein? First figure out which promoters work, which signal sequences to use, how to prevent the bacteria from chewing up your precious product.

But perhaps the biggest challenge was choosing which proteins to pursue. The human body produces thousands of proteins, but which ones would make good drugs? The team developed a systematic approach: they would focus on proteins that were already known to have biological activity, that were produced in very small quantities naturally, and that addressed serious medical needs with limited treatment options. This led them to focus on growth factors and hormones—molecules that controlled fundamental biological processes like blood cell production and immune response.

By late 1982, the company had multiple projects underway, but resources were burning fast. The initial $19 million sounded like a lot, but with no products and no revenue, the runway was finite. Rathmann made a crucial decision: rather than pursuing the safer path of developing biosimilar versions of existing drugs, Amgen would go all-in on novel proteins. It was a bet-the-company strategy that would either establish them as leaders or leave them as a footnote in biotech history.

The stage was set for what would become one of the most dramatic discoveries in biotechnology history. In the labs of Thousand Oaks, a team led by a quiet, determined scientist named Fu-Kuen Lin was about to embark on a quest that would transform not just Amgen, but the entire pharmaceutical industry. They were hunting for the gene that produced erythropoietin, a protein that stimulated red blood cell production. Success would mean helping millions of kidney disease patients avoid transfusions. Failure would likely mean the end of Amgen as an independent company. The clock was ticking, competitors were circling, and the odds were astronomical.

III. The EPO Breakthrough: Finding the Golden Gene (1981–1989)

Fu-Kuen Lin didn't look like someone about to change medical history. Soft-spoken and methodical, he had joined Amgen in 1981 fresh from his postdoctoral work at UC Davis. Lin was assigned to what many considered a quixotic project: finding and cloning the gene for erythropoietin (EPO), a hormone produced by the kidneys that stimulates red blood cell production. The medical need was clear—kidney dialysis patients often suffered from severe anemia because their damaged kidneys couldn't produce enough EPO. But the technical challenge was staggering.

Consider the mathematics of the problem: the human genome contains roughly 3 billion base pairs of DNA, divided among 20,000-25,000 genes. In 1981, only a handful of human genes had been successfully cloned. Lin's task was to find one specific gene—about 5,000 base pairs long—somewhere in that vast genetic ocean. Worse, EPO was produced in such tiny quantities that isolating enough protein to study was nearly impossible. Previous attempts to extract EPO from human urine had yielded micrograms from thousands of gallons—barely enough to study, nowhere near enough to reverse-engineer the gene.

Lin's approach was elegant in its simplicity but brutal in its execution. He would create a "library" of human DNA fragments, breaking the entire genome into millions of pieces and inserting each piece into bacteria. Then he would screen these bacterial colonies one by one, looking for the one in 1.5 million that contained the EPO gene. It was like trying to find a specific sentence in all the books in the Library of Congress, except the sentence was written in a language you barely understood and you had to check each book by hand.

The screening process was mind-numbing. Lin and his small team would plate out bacterial colonies, transfer them to filters, break them open to expose their DNA, and then probe with radioactive markers that might—might—stick to EPO sequences. Each screening cycle took days and could check perhaps a few thousand colonies. Do the math: at that rate, screening 1.5 million colonies would take years. And that assumed the gene was even in the library, that their probes would work, and that they would recognize success when they saw it.

Meanwhile, Amgen was burning through cash. By June 1983, with no products and mounting expenses, the company went public, raising nearly $40 million. The IPO prospectus was remarkably honest about the risks: "The Company has not generated any revenues from product sales... There can be no assurance that the Company's research and development efforts will be successful." Wall Street was skeptical but intrigued. Genentech had gone public three years earlier and seen its stock price soar. Maybe Amgen would be the next biotechnology success story.

The IPO bought time but increased pressure. Public investors wanted results, not promises about revolutionary science. Rathmann was spending increasing amounts of time on the road, explaining to analysts why finding the EPO gene was worth the wait. Inside Amgen, there were debates about whether to abandon EPO for more achievable targets. But Lin pressed on with quiet determination.

The breakthrough came not from brilliance but from persistence. In late 1983, after screening hundreds of thousands of colonies, Lin's team found a weak but reproducible signal. It wasn't the whole gene—just a fragment—but it was enough. They used that fragment as a new probe, screened another library, and found a larger piece. Then another. Like assembling a jigsaw puzzle where you didn't know what the final picture looked like, they slowly reconstructed the entire EPO gene.

But finding the gene was only the beginning. Now they had to make it work—to convince bacteria to produce human EPO in quantities sufficient for clinical trials. This introduced a new set of challenges. Human proteins are decorated with sugar molecules that bacteria can't add. Would EPO work without these modifications? The protein had to fold correctly, maintain stability, and retain biological activity. Each of these requirements could have been a deal-breaker.

The competitive landscape was heating up. Genetics Institute, a Boston-based rival, was also hunting for EPO. They had deeper pockets, more scientists, and connections to major pharmaceutical companies. If they beat Amgen to market, all of Lin's work would be worthless. The race wasn't just about science anymore—it was about speed, patents, and strategic partnerships.

In 1984, Amgen made a crucial decision that would haunt them for decades: they partnered with Johnson & Johnson to develop and market EPO. The deal seemed logical at the time. J&J had the clinical development expertise, regulatory know-how, and marketing muscle that Amgen lacked. In exchange for these capabilities, Amgen granted J&J rights to sell EPO for all uses except dialysis in the United States, and all uses outside the United States except China and Japan. It was like giving away the kingdom to keep the castle, but Rathmann felt they had no choice.

The clinical trials began in 1985, and the results were spectacular. Dialysis patients who had required regular blood transfusions suddenly didn't need them anymore. Their energy returned, their quality of life improved dramatically. One patient described it as "getting my life back." The medical community was stunned—this wasn't just an incremental improvement but a fundamental change in how chronic kidney disease could be managed.

But success in the clinic didn't mean success in the courts. Genetics Institute had also cloned EPO and filed their own patents. What followed was one of the most complex and costly patent battles in biotechnology history. The central question: who had invented EPO first, and what exactly had they invented? Was it the gene sequence? The protein? The method of production? The legal arguments were as complex as the science.

The patent litigation would drag on for years, consuming millions in legal fees and creating uncertainty that depressed Amgen's stock price. At one point, a judge ruled that Genetics Institute's patents were valid, sending Amgen shares plummeting. The company's entire future hung on appeals and legal technicalities. Scientists who should have been developing new drugs were instead giving depositions and testifying in court.

Finally, in 1989, the FDA approved Epogen (Amgen's brand name for EPO) for treating anemia in chronic kidney disease patients. It was the first recombinant human protein approved for a major therapeutic indication. The initial sales projections were conservative—maybe $100-200 million annually. The reality exceeded everyone's wildest dreams. Epogen became the first biotechnology blockbuster, eventually generating over $2 billion annually for Amgen alone.

But the sweetest victory was still to come. In 1991, after years of legal wrangling, the courts ultimately upheld Amgen's EPO patents. Genetics Institute was forced to license the technology, paying royalties on their own EPO sales. The patent protection would last until 2004 in the U.S., giving Amgen a 15-year monopoly on one of medicine's most important drugs.

The success of EPO transformed Amgen from a speculative biotech startup into a profitable pharmaceutical company. Revenue grew from essentially zero in 1988 to over $1 billion by 1992. The company's market capitalization soared. More importantly, EPO validated the entire biotechnology industry's promise: you could indeed engineer bacteria to produce human proteins, and those proteins could become transformative medicines.

Yet the EPO story also contained the seeds of future challenges. The J&J partnership, necessary for initial success, would become a source of constant friction as both companies fought over market boundaries and usage rights. The patent battles, while ultimately successful, demonstrated how vulnerable biotech companies were to legal challenges. And the very success of EPO created expectations that would be difficult to replicate—investors now expected every Amgen drug to be a blockbuster.

The lessons from EPO would shape Amgen's strategy for decades. First, own your intellectual property completely and defend it aggressively. Second, be careful about partnerships—what seems necessary today might become a constraint tomorrow. Third, focus on proteins with clear, unmet medical needs where the therapeutic benefit is undeniable. And finally, invest in manufacturing and quality control—the ability to produce complex proteins at scale would become as important as discovering them.

As the 1980s drew to a close, Amgen was no longer a startup but not yet a pharmaceutical giant. They had proven they could develop a breakthrough drug, but could they do it again? In the labs of Thousand Oaks, another team had been working on a different growth factor, one that stimulated white blood cell production. Their success would determine whether Amgen was a one-hit wonder or a sustainable innovation engine.

IV. Building a Portfolio: Neupogen and the Second Act (1985–1991)

While Fu-Kuen Lin was hunting for EPO in one corner of Amgen's labs, Larry Souza was chasing an equally elusive quarry in another. Souza, a molecular biologist who had joined Amgen in 1982, was tasked with finding granulocyte colony-stimulating factor (G-CSF), a protein that stimulated the production of neutrophils—the white blood cells that form the body's first line of defense against infection. The medical implications were profound: cancer patients undergoing chemotherapy often suffered from dangerously low neutrophil counts, leaving them vulnerable to life-threatening infections. Many cancer deaths weren't from the cancer itself but from infections that overwhelmed depleted immune systems.

Souza's challenge differed from Lin's in crucial ways. While EPO was produced primarily in the kidneys, G-CSF was made in multiple cell types in tiny quantities. There was no concentrated source to study, no clear tissue to mine for genetic material. Souza had to be creative. He developed a novel screening approach using cancer cell lines that produced slightly higher levels of G-CSF, painstakingly purifying enough protein to create antibodies that could recognize it. These antibodies became his divining rods, tools to search through genetic libraries for the G-CSF gene.

The work proceeded in parallel with the EPO project, creating an internal competition that pushed both teams harder. Souza later recalled the atmosphere as "intensely collaborative competition"—teams shared techniques and insights but raced to be first. Coffee machines became impromptu conference rooms where scientists debated strategies at 2 AM. The parking lot was never empty. Marriages strained. But there was a shared sense that they were doing something historic.

By 1985, Souza's team had successfully cloned G-CSF, but now faced a different challenge than Lin's group. While EPO had a clear patient population (dialysis patients) and a simple endpoint (increased red blood cells), G-CSF's market was less defined. Which cancer patients would benefit? When should it be administered? How would oncologists, notoriously conservative about changing treatment protocols, be convinced to add another drug to already complex chemotherapy regimens?

This period also marked a crucial leadership transition at Amgen. George Rathmann, having successfully guided the company through its pioneering phase, was increasingly focused on strategic partnerships and financing. The board wanted someone with experience scaling operations and managing a commercial organization. In 1988, they found their answer in Gordon Binder, a Harvard MBA who had been Amgen's CFO since 1982.

Binder's ascension to CEO marked a shift from Amgen as a research boutique to Amgen as a commercial enterprise. Where Rathmann had managed by walking the labs, Binder managed by walking Wall Street. He understood that Amgen's future depended not just on scientific innovation but on financial innovation—using cash from EPO to fund research while maintaining profitability. It was a delicate balance that most biotech companies failed to achieve.

On February 21, 1991, the FDA approved Neupogen (filgrastim), Amgen's brand of G-CSF. The clinical trials had shown remarkable results: cancer patients receiving Neupogen had significantly fewer infections, shorter hospital stays, and could maintain their chemotherapy schedules instead of having treatments delayed due to low blood counts. Oncologists, initially skeptical, became believers when they saw patients who previously would have been hospitalized sailing through chemotherapy.

The commercial success was immediate. Neupogen generated $260 million in its first full year, exceeding even optimistic projections. Combined with EPO, Amgen now had two blockbuster biologics, a feat no other biotech company had achieved. By 1992, combined sales of Epogen and Neupogen exceeded $1 billion, and on January 2, 1992, Amgen joined the S&P 500—a remarkable achievement for a company that had been founded just twelve years earlier.

But success brought new challenges. Manufacturing biological drugs at scale was vastly more complex than making traditional pharmaceuticals. Proteins had to be produced in living cells, purified through dozens of steps, and maintained in precise conditions. A slight variation in temperature, pH, or processing time could render an entire batch worthless. Amgen needed industrial-scale manufacturing capabilities that didn't exist anywhere in the world.

The company embarked on an ambitious expansion, building what would become the crown jewel of biologics manufacturing in Puerto Rico. The facility, opened in 1991, wasn't just big—it was revolutionary in its approach to quality control. Every step was monitored, documented, and validated. The joke among employees was that Amgen made two products: drugs and paperwork, and it wasn't clear which weighed more. But this obsessive attention to quality would become a crucial competitive advantage.

The Puerto Rico facility also represented a strategic bet on manufacturing as a core competency. While other biotech companies outsourced production, Amgen believed that the ability to manufacture complex proteins at scale was as important as discovering them. They were right. When competitors eventually developed similar drugs, many struggled with manufacturing consistency, giving Amgen an edge in reliability that translated to market dominance.

Binder also recognized that Amgen needed to expand beyond blood cell growth factors. The company initiated research programs in neuroscience, inflammation, and metabolic diseases. Not all would succeed—the graveyard of failed projects grew steadily—but the strategy of multiple shots on goal increased the odds of finding the next blockbuster. The research budget ballooned from $50 million in 1988 to over $200 million by 1992, funded entirely by profits from EPO and Neupogen.

The company culture was evolving too. The scrappy startup where everyone knew everyone was becoming a corporation with thousands of employees. Binder instituted more formal management structures, performance reviews, and strategic planning processes. Some old-timers grumbled about bureaucracy, but the changes were necessary. You couldn't run a billion-dollar company like a graduate student lab.

One crucial decision during this period was to maintain independence. Throughout the early 1990s, big pharmaceutical companies came calling with acquisition offers. The numbers were tempting—multiples of Amgen's market value. But Binder and the board believed that remaining independent was crucial to maintaining the innovative culture that had produced EPO and Neupogen. They would partner when necessary but never surrender control.

This independence came at a cost. Without a big pharma parent, Amgen had to build every capability from scratch: clinical development, regulatory affairs, manufacturing, marketing, and distribution. Each required massive investment and carried execution risk. Many biotech companies that tried to go it alone failed at this transition. Amgen succeeded through a combination of disciplined execution, deep pockets from their successful drugs, and a bit of luck.

The international expansion was particularly challenging. Each country had different regulatory requirements, reimbursement systems, and medical practices. Amgen couldn't simply export the U.S. model; they had to adapt to local conditions while maintaining global quality standards. The company established subsidiaries across Europe and Asia, each requiring significant investment before generating returns.

By the end of 1992, Amgen had achieved what seemed impossible just a decade earlier: they were a profitable, growing, independent biotechnology company with multiple blockbuster drugs. Revenue approached $1.5 billion. The company employed over 2,500 people. The stock price had increased fifty-fold since the IPO. Fortune magazine added them to the Fortune 500 list, the first biotech company to achieve that distinction.

But success had also attracted attention from competitors. Genetics Institute, Johnson & Johnson, and others were developing their own versions of EPO and G-CSF for markets outside Amgen's patents. Generic drug manufacturers were beginning to ask whether biological drugs could be copied like traditional pharmaceuticals. And new biotechnology companies, inspired by Amgen's success, were targeting similar proteins with potentially superior properties.

The question facing Amgen as they entered the mid-1990s was how to sustain growth when their foundational patents would eventually expire. The answer would come from an unexpected source: a small biotechnology company in Seattle that had developed a revolutionary treatment for rheumatoid arthritis. The ensuing acquisition and patent strategy would demonstrate that in biotechnology, sometimes the best innovations come from knowing what to buy and how to protect it.

V. The Patent Wars & Enbrel Era (1998–2010)

The fax machine in Amgen's legal department wouldn't stop buzzing on the morning of March 15, 1998. Patent infringement lawsuits were arriving from multiple jurisdictions, each claiming that Immunex Corporation's new drug, Enbrel, violated intellectual property owned by competitors. The drug hadn't even been approved yet, but the legal battles had already begun. This was the new reality of biotechnology: the war for market dominance was fought as much in courtrooms as in laboratories.

Enbrel received FDA approval on November 2, 1998, marking a revolution in treating rheumatoid arthritis. Unlike traditional treatments that broadly suppressed the immune system, Enbrel specifically targeted tumor necrosis factor (TNF), a protein that drove inflammation in autoimmune diseases. Patients who had been crippled by arthritis were suddenly able to walk, work, and live normal lives. The medical community hailed it as one of the most significant advances in rheumatology in decades.

But Immunex, the Seattle-based company that developed Enbrel, was overwhelmed by success. Demand far exceeded their manufacturing capacity, creating shortages that left desperate patients unable to access the drug. By 2001, Immunex was in crisis. They couldn't build manufacturing facilities fast enough, their stock price was volatile, and larger competitors were circling like sharks. The company needed a savior, and Amgen saw an opportunity.

The courtship between Amgen and Immunex was complicated by a third party: American Home Products (later Wyeth), which owned marketing rights to Enbrel and had a contentious relationship with Immunex. Any acquisition would require not just buying Immunex but also negotiating with Wyeth. Kevin Sharer, who had succeeded Gordon Binder as CEO in 2000, saw this complexity not as an obstacle but as an opportunity. If Amgen could navigate the three-way negotiation, they would acquire not just a drug but a monopoly position in a massive market.

Sharer was a different breed of biotech CEO. A former nuclear submarine officer and McKinsey consultant, he brought military discipline and strategic thinking to Amgen. Where his predecessors had been scientists or financial engineers, Sharer was a strategist who understood that in the pharmaceutical industry, controlling intellectual property was as important as discovering new drugs.

The Immunex acquisition, completed in 2002 for $16 billion, was the largest in biotechnology history at the time. But the real story wasn't the price tag—it was what Amgen did next. They immediately set about constructing what industry insiders would later call the "Enbrel patent thicket," a web of interconnected patents that would protect the drug long after its original composition patent expired.

Here's how the strategy worked: Amgen filed patents not just on Enbrel itself but on methods of manufacturing it, methods of administering it, specific formulations, dosing regimens, and even particular patient populations. Each patent might only provide narrow protection, but together they created a nearly impenetrable barrier to competition. A biosimilar manufacturer might be able to work around one or two patents, but not dozens.

The manufacturing problem that had plagued Immunex became Amgen's opportunity to demonstrate their operational excellence. Within months of the acquisition, Amgen's Rhode Island facility was producing Enbrel at scales Immunex never achieved. The shortage crisis ended, and sales soared. By 2004, Enbrel was generating over $2 billion annually, validating the acquisition price that many analysts had called excessive.

But the patent strategy was just beginning. Amgen's legal team, now numbering in the hundreds, pursued what they called "patent lifecycle management." As original patents neared expiration, they would file new applications based on ongoing research. Discovered that Enbrel worked better with a particular injection device? Patent it. Found that a specific dosing schedule improved outcomes? Patent it. Identified biomarkers that predicted treatment response? Patent those too.

The approach was controversial. Critics argued that Amgen was gaming the system, using legal technicalities to extend monopolies on essential medicines. Patient advocacy groups complained about high prices maintained through artificial patent barriers. But Amgen argued they were simply protecting legitimate innovations and the investments required to develop and manufacture complex biological drugs.

The real test came from biosimilar manufacturers. Unlike traditional generic drugs, which are chemically identical to the original, biosimilars are highly similar but not identical biological products. The regulatory pathway for biosimilars was unclear in the early 2000s, giving Amgen time to strengthen their patent fortress. When the FDA finally established biosimilar regulations in 2010, Amgen was ready.

Samsung Bioepis, a Korean biosimilar manufacturer, thought they had found a way around Enbrel's patents. They developed a biosimilar version and prepared to launch in the U.S. market. Amgen's response was swift and brutal: they filed lawsuits in multiple jurisdictions, challenged Samsung's manufacturing processes, and questioned the similarity of their product. The legal costs for Samsung mounted into the hundreds of millions.

But Amgen's masterstroke came through a negotiation rather than litigation. In 2015, they reached a settlement with Samsung that appeared to be a compromise: Samsung could launch their Enbrel biosimilar in Europe in 2016 but couldn't enter the U.S. market until 2029. On the surface, Samsung got market access. In reality, Amgen had just extended Enbrel's U.S. monopoly by another decade beyond the original patent expiration.

The Enbrel patent strategy became a template that Amgen would apply to their entire portfolio. Each successful drug would be surrounded by layers of patent protection. Manufacturing processes would be kept as trade secrets. Partnerships would be structured to maintain control over intellectual property. The legal department became as important as the research department in maintaining competitive advantage.

During this period, Amgen also expanded Enbrel's approved uses beyond rheumatoid arthritis to include psoriatic arthritis, ankylosing spondylitis, and psoriasis. Each new indication required clinical trials and regulatory approval but also justified premium pricing and extended market exclusivity. The drug that started as a treatment for one condition became a platform for treating multiple inflammatory diseases.

The financial impact was staggering. Enbrel's cumulative sales exceeded $50 billion by 2010, making it one of the most successful drugs in pharmaceutical history. The patent strategy ensured that even as other TNF inhibitors entered the market—Abbott's Humira, Johnson & Johnson's Remicade—Enbrel maintained its market share through superior patent protection and manufacturing reliability.

Kevin Sharer's tenure as CEO from 2000 to 2012 marked Amgen's transformation from a biotechnology pioneer to a pharmaceutical powerhouse. Revenue grew from $3.6 billion to over $17 billion. The company's market capitalization exceeded $70 billion. But more importantly, Amgen had proven that biotechnology companies could compete with traditional pharmaceutical giants not just in innovation but in commercial execution and strategic maneuvering.

The Enbrel experience also taught Amgen about the importance of inflammation as a therapeutic area. The biological pathways that drove rheumatoid arthritis were involved in dozens of other conditions. This insight would drive research investments for the next decade, leading to new drugs targeting different aspects of the inflammatory cascade. The company that had started with blood cell growth factors was becoming a leader in immunology.

Yet success bred complacency. By 2010, Amgen's growth was slowing. The company had become dependent on a handful of blockbuster drugs, all facing eventual patent expiration. Biosimilar manufacturers were becoming more sophisticated, finding ways around patent thickets. Regulators were under pressure to increase competition and lower drug prices. The strategies that had worked for two decades were reaching their limits.

The next phase of Amgen's evolution would require a different approach. Rather than just defending existing franchises, the company would need to discover or acquire entirely new platforms. The era of Robert Bradway, who would become CEO in 2012, would be defined by bold acquisitions, geographic expansion, and a race to develop the next generation of breakthrough medicines. The patent warrior would need to become an innovation engine once again.

VI. The Biosimilar Threat & Reinvention (2010–2020)

Robert Bradway walked into Amgen's boardroom on his first day as CEO in May 2012 with a stark message: "The patent cliff is real, and it's coming for us." The former Morgan Stanley banker turned biotech executive had spent his first years at Amgen as CFO watching the company's financial projections, and what he saw was troubling. Bradway became chief executive officer in May 2012, inheriting a company that looked successful on the surface—$17 billion in revenue, strong profits—but faced an existential crisis beneath.

The numbers told the story. Epogen, once Amgen's crown jewel, was already facing biosimilar competition in Europe. Neupogen patents would expire by 2015. Even the seemingly impregnable Enbrel fortress would eventually fall. For a company that had built its success on a handful of blockbuster biologics protected by patents, the next decade looked like a slow-motion train wreck. Bradway's response would be to fundamentally reimagine what Amgen could be: not just a defender of old franchises but an aggressor in new markets. The first major victory in this new era had actually been achieved just before Bradway took the helm. On June 1, 2010, the FDA approved Prolia (denosumab) for the treatment of postmenopausal women with osteoporosis at high risk for fracture. Prolia represented a new model for Amgen: a drug that required twice-yearly administration rather than weekly or monthly dosing, creating a different relationship with patients and physicians. Prolia was the first and only approved therapy that specifically targeted RANK Ligand, an essential regulator of osteoclasts (the cells that break down bone)

. The six-month regimen also created better compliance rates and convenience for patients compared to weekly or daily injections that characterized most osteoporosis treatments.

But Prolia was more than just a new drug—it represented Amgen's strategic pivot beyond its traditional hematology and nephrology strongholds. The company built an entirely new commercial infrastructure to target endocrinologists and primary care physicians, markets where Amgen had limited presence. The drug's success was immediate, generating $884 million in its first full year and eventually becoming one of Amgen's most important growth drivers.

Bradway's most immediate challenge was the biosimilar threat to Neupogen. In 2012, Sandoz filed for approval of the first biosimilar version in Europe. Rather than just defend, Bradway made a counterintuitive decision: Amgen would become a biosimilar manufacturer itself. The logic was elegant—who better to make biosimilar versions of complex biologics than the company that invented the originals? In 2014, Amgen launched its biosimilars unit, eventually developing biosimilar versions of competitors' drugs including Humira and Avastin.

This dual strategy—defending against biosimilars while creating them—confused Wall Street initially but proved brilliant over time. By 2015, when Sandoz's Zarxio became the first biosimilar approved in the U.S., Amgen had already shifted most Neupogen users to Neulasta, a longer-acting version with stronger patent protection. Meanwhile, their biosimilar division was preparing to launch competing versions of blockbusters from other companies.

The cardiovascular opportunity emerged from Amgen's deep understanding of human genetics. Scientists had discovered that people with naturally occurring mutations in the PCSK9 gene had extremely low cholesterol levels and rarely developed heart disease. Amgen's researchers developed Repatha (evolocumab), a monoclonal antibody that mimicked these protective mutations. When the FDA approved Repatha in August 2015, it offered hope to patients who couldn't tolerate statins or achieve adequate cholesterol reduction with existing therapies.

But Repatha's launch illustrated the new challenges facing innovative biologics. Despite clear clinical benefits, insurance companies balked at the $14,000 annual price tag. Prior authorization requirements created barriers for physicians, and many patients couldn't access the drug despite medical need. Amgen was forced to cut Repatha's list price by 60% in 2018, acknowledging that the traditional pricing model for specialty biologics was breaking down under payer pressure.

The acquisition of Otezla from Bristol Myers Squibb for $13.4 billion in 2019 marked another strategic pivot. Otezla wasn't a biologic but a small molecule drug for psoriasis and psoriatic arthritis. The acquisition was opportunistic—Bristol Myers was required to divest Otezla to complete its merger with Celgene—but it gave Amgen an immediately profitable asset with limited biosimilar risk.

The deal also demonstrated Bradway's disciplined approach to capital allocation. While other companies were paying astronomical premiums for speculative assets, Amgen bought a proven drug with growing sales at a reasonable multiple. Otezla generated $2.2 billion in revenue in its first full year under Amgen ownership, validating the acquisition thesis.

As the decade progressed, Amgen's transformation accelerated. The company expanded aggressively in China, partnering with local companies to navigate regulatory complexities. They invested heavily in next-generation manufacturing technologies, including continuous processing and single-use bioreactors that could reduce production costs by 50%. The research organization was restructured around four therapeutic areas: oncology, cardiovascular disease, inflammation, and neuroscience.

The neuroscience bet was particularly bold. Brain diseases had become a graveyard for pharmaceutical companies, with failure rates exceeding 95%. But Amgen believed their expertise in large molecule biologics could succeed where small molecules had failed. They developed innovative delivery technologies to get proteins across the blood-brain barrier and initiated programs in Alzheimer's, Parkinson's, and migraine.

AIMOVIG (erenumab), approved in May 2018, validated this strategy. As the first FDA-approved treatment specifically designed to prevent migraines, it opened an entirely new market. The drug worked by blocking the calcitonin gene-related peptide receptor, a target identified through genetic studies of migraine patients. Within two years, AIMOVIG was generating over $400 million annually despite intense competition from similar drugs.

But the boldest move of the Bradway era would come in 2022. On December 12, 2022, Amgen announced it would acquire Horizon Therapeutics for $116.50 per share in cash, representing a transaction equity value of approximately $27.8 billion. It was Amgen's largest acquisition ever, dwarfing even the Immunex deal twenty years earlier.

VII. The Horizon Acquisition: Betting Big on Rare Disease (2022–2023)

The boardroom at Amgen's Thousand Oaks headquarters was unusually crowded on the morning of December 11, 2022. Investment bankers from Goldman Sachs, lawyers from Sullivan & Cromwell, and Amgen's entire executive team had gathered for what CFO Peter Griffith called "the most important decision in Amgen's recent history." On the table was a proposal to acquire Horizon Therapeutics for nearly $28 billion—a price that would consume most of Amgen's financial flexibility and bet the company's future on rare diseases.

The opportunity had emerged suddenly. Horizon, an Irish company with most operations in Chicago, had built a portfolio of treatments for rare inflammatory and autoimmune conditions. The acquisition would add first-in-class medicines such as TEPEZZA (teprotumumab-trbw), KRYSTEXXA (pegloticase) and UPLIZNA (inebilizumab-cdon). But Horizon was also being courted by Johnson & Johnson and Sanofi, both offering similar valuations. The bidding war threatened to push the price even higher.

Bradway's analysis was characteristically thorough. TEPEZZA, indicated for the treatment of Thyroid Eye Disease regardless of Thyroid Eye Disease activity or duration, addressed a condition affecting 20,000 Americans annually with no other FDA-approved treatments. The drug had generated $1.9 billion in 2022 despite being launched just two years earlier. KRYSTEXXA treated chronic refractory gout, another rare condition with limited options. Together, these drugs could generate $5-6 billion annually at peak.

But the strategic rationale went beyond individual products. Horizon had mastered the rare disease commercial model—small, specialized sales forces calling on a limited number of expert physicians. This was completely different from Amgen's approach of large sales teams targeting broad physician populations. Acquiring Horizon would give Amgen capabilities that would take years to build organically.

The FTC's intervention in May 2023 shocked no one who understood the Biden administration's aggressive antitrust stance. The FTC filed a complaint in the U.S. District Court for the Northern District of Illinois to block the proposed transaction. The complaint stated that the deal would give Amgen the ability and incentive to foreclose rivals to Tepezza and Krystexxa, and would entrench their monopoly positions by substituting Amgen's broad portfolio for Horizon's smaller portfolio, thus raising entry barriers.

The FTC's theory was novel and controversial. They argued that Amgen could "bundle" Horizon's drugs with their existing portfolio, offering discounts to insurance companies that favored Horizon products over potential competitors. Amgen pointed out they were unaware of any prior acquisition that had been blocked under a bundling theory.

The legal battle that followed was intense but brief. Amgen's lawyers argued that the FTC's concerns were entirely speculative, that there were no current competitors to TEPEZZA or KRYSTEXXA to foreclose, and that the companies' portfolios addressed completely different diseases. Behind the scenes, settlement negotiations proceeded in parallel with trial preparation.

On September 1, 2023, Amgen and the FTC reached a proposed consent order that included unprecedented restrictions. As part of a nationwide settlement, the FTC and attorneys general from six states—California, Illinois, Minnesota, New York, Washington, and Wisconsin—agreed to dismiss the federal court preliminary injunction action.

Under the final consent order, Amgen was prohibited from bundling an Amgen product with either Tepezza or Krystexxa. In addition, Amgen could not condition any product rebate or contract term related to an Amgen product on the sale or positioning of either drug. Amgen was also barred from using any product rebate or contract term to exclude or disadvantage any product that would compete with Tepezza or Krystexxa.

The restrictions were painful but manageable. Amgen had never intended to bundle the products—the rare disease market operated on different dynamics than primary care drugs. What mattered was that the deal could close. On October 6, 2023, Amgen announced it had completed its acquisition of Horizon Therapeutics for $116.50 per share in cash.

The integration proceeded with military precision. Rather than immediately merging operations, Amgen maintained Horizon as a semi-autonomous unit, preserving the specialized commercial capabilities that made the company successful. Key Horizon executives were retained with generous retention packages. The rare disease sales force continued operating independently, maintaining the personalized relationships with specialist physicians.

Early results vindicated the strategy. In Q4 2023, Horizon products generated over $1 billion in quarterly revenue for the first time. TEPEZZA continued its rapid growth trajectory, with demand exceeding manufacturing capacity. Amgen's global infrastructure accelerated Horizon's international expansion, launching products in markets where Horizon lacked presence.

But the Horizon acquisition's importance extended beyond financial metrics. It represented a fundamental shift in Amgen's strategic identity. For forty years, the company had focused on common diseases affecting millions—anemia, neutropenia, osteoporosis, high cholesterol. Now they were embracing the opposite approach: ultra-rare diseases affecting thousands, requiring different development strategies, regulatory pathways, and commercial models.

The rare disease pivot also aligned with broader industry trends. As traditional blockbuster markets became increasingly competitive and price-pressured, rare diseases offered a different value proposition. Smaller patient populations meant less competition. Regulatory agencies provided expedited pathways and longer exclusivity periods. Most importantly, payers were generally willing to reimburse high prices for transformative treatments addressing severe unmet needs.

The acquisition transformed Amgen's financial profile. "Robust growth in sales and earnings throughout 2024 reflects the momentum of our business," Bradway noted in the Q4 2024 earnings call. For the fourth quarter, total revenues increased 11% to $9.1 billion. Product sales grew 11%, primarily driven by 14% volume growth.

The Horizon deal brought in seven products already approved in the U.S. along with a healthy pipeline of assets in clinical trials. Demand for key drugs—Tepezza, Krystexxa and Uplizna—increased second-quarter 2023 revenues by 8% to $945 million. Tepezza alone generated $445.5 million in sales in Q2 2023.

The successful integration of Horizon also demonstrated Amgen's evolved M&A capabilities. Unlike the Immunex acquisition twenty years earlier, which took years to fully integrate, Horizon was contributing meaningfully to growth within quarters. The company had learned how to preserve entrepreneurial culture within a large corporate structure, maintaining the agility that made smaller biotechs successful.

VIII. Modern Era: Pipeline & Future Bets (2020–Present)

In 2024, Amgen's transformation reached a crescendo. "Robust growth in sales and earnings throughout 2024 reflects the momentum of our business," Bradway announced during the full-year earnings call. "With strong performance globally, we are investing heavily in our rapidly advancing pipeline to deliver innovative therapies across our four therapeutic areas." Total revenues for 2024 grew 19% to a record $33.4 billion, driven by 23% volume growth.

But the headline number that captured Wall Street's attention was MariTide, Amgen's entry into the obesity gold rush that had transformed pharmaceutical markets. In people living with obesity without Type 2 diabetes, MariTide demonstrated up to ~20% average weight loss at week 52 without a plateau. For those with Type 2 diabetes, the drug achieved up to ~17% average weight loss and lowered average HbA1c by up to 2.2 percentage points.

MariTide represented a different approach than competitors Wegovy and Zepbound. As a bispecific antibody-peptide conjugate, it acted as both a GLP-1 receptor agonist and GIPR antagonist. This dual mechanism, combined with its long half-life, allowed for monthly or less frequent dosing—a potential game-changer in a market where current drugs require weekly injections.

The obesity opportunity was massive—analysts projected the global market could reach $150 billion by 2030. But MariTide's differentiation went beyond convenience. The drug demonstrated robust improvements in cardiometabolic parameters, including blood pressure, triglycerides, and high-sensitivity C-reactive protein. For Amgen, success in obesity could transform the company's growth trajectory for the next decade.

Yet Wall Street's reaction to the Phase 2 data was mixed. Shares fell about 5% when results were announced, as the 20% weight loss fell at the lower end of expectations, with some analysts hoping for up to 25%. Mizuho analyst Jared Holz noted that investors remained more confident in Eli Lilly and Novo Nordisk as market leaders, suggesting Amgen could be a "distant third/fourth player" since MariTide wouldn't enter the market until around 2027.

The challenges in obesity highlighted the competitive intensity of modern pharmaceutical development. Being first mattered less than being best, and being best required not just efficacy but also safety, convenience, manufacturing capacity, and payer acceptance. Amgen's response was characteristically thorough: the company initiated the MARITIME Phase 3 program, one of the most comprehensive clinical development efforts in obesity history.

The MARITIME program included two freshly launched trials with primary endpoints measuring percent change from baseline in body weight at 72 weeks. The program was expected to include additional Phase 3 trials in cardiovascular disease, heart failure, kidney disease and obstructive sleep apnea.

Beyond obesity, Amgen's pipeline reflected a company comfortable taking big swings in difficult therapeutic areas. In oncology, the company was pioneering bispecific T-cell engagers, essentially creating synthetic immune synapses that forced T-cells to recognize and destroy cancer cells. IMDELLTRA (tarlatamab), approved for small cell lung cancer, represented the first of potentially dozens of such molecules.

The company's approach to oncology had evolved from traditional chemotherapy to precision immunotherapy. Rather than carpet-bombing cancer cells and hoping for the best, Amgen's new drugs acted like guided missiles, using the body's immune system as the delivery vehicle. BLINCYTO, their pioneering bispecific for acute lymphoblastic leukemia, had shown that the approach could deliver dramatic responses in cancers that had resisted everything else.

The numbers validated the strategy. Ten products delivered at least double-digit sales growth in Q4 2024, including Repatha, BLINCYTO, TEZSPIRE, EVENITY, and TAVNEOS. Each represented a different therapeutic approach—PCSK9 inhibition for cardiovascular disease, bispecific T-cell engagement for cancer, TSLP inhibition for asthma, sclerostin inhibition for osteoporosis, and complement C5a receptor inhibition for vasculitis.

Manufacturing innovation continued to provide competitive advantage. Amgen's new facility in Ohio represented the future of biologics production: smaller, more flexible, using single-use technologies that could switch between products without lengthy changeover times. The company claimed their next-generation manufacturing could reduce costs by 50% while improving quality and reducing environmental impact.

The biosimilars business, once viewed skeptically by investors, had become a meaningful contributor. AMJEVITA (adalimumab), Amgen's biosimilar to Humira, captured significant market share within months of launch. The company's biosimilar portfolio generated over $3 billion annually, providing a hedge against the patent expirations of their own originator biologics.

But perhaps the most intriguing developments were in Amgen's approach to drug discovery itself. The company had embraced artificial intelligence and machine learning not as buzzwords but as fundamental tools. Their partnership with Generate Biomedicines aimed to design entirely new proteins from scratch, using AI to predict structures that would bind to disease targets previously considered undruggable.

The computational approach extended to clinical trials. Amgen was pioneering "digital twins"—computer simulations of patients that could predict drug responses based on genetic, proteomic, and clinical data. This could reduce the size and duration of clinical trials while improving success rates. Early applications in oncology trials had reduced enrollment requirements by 30% while maintaining statistical power.

Geographic expansion accelerated, particularly in China. Despite geopolitical tensions, Amgen committed to building local manufacturing and research capabilities. The company's China revenue exceeded $2 billion in 2024, growing at 30% annually. Twenty drugs were in development specifically for Chinese patients, addressing genetic variations and disease patterns unique to Asian populations.

The integration of digital health represented another frontier. Amgen wasn't just making drugs but creating comprehensive disease management platforms. For osteoporosis, they developed apps that reminded patients about injections, tracked bone density improvements, and connected patients with specialists. These digital tools improved adherence rates by 40%, translating directly to better outcomes and higher sales.

External recognition validated the transformation. In 2024, Amgen was named one of the "World's Most Innovative Companies" by Fast Company and one of "America's Best Large Employers" by Forbes. These accolades reflected not just business success but cultural evolution—from a California biotech to a global healthcare leader.

Yet challenges loomed. The Enbrel patent cliff approaching in 2029 would eliminate billions in high-margin revenue. Biosimilar competition was intensifying for Prolia and other key products. The regulatory environment was becoming more demanding, with agencies requiring larger trials and real-world evidence. Drug pricing remained under political pressure globally.

The company's response was to accelerate innovation while maintaining financial discipline. R&D spending exceeded $5 billion annually, but every program underwent rigorous scrutiny. Projects that missed milestones were quickly terminated. Resources shifted rapidly to promising areas. The culture balanced entrepreneurial risk-taking with pharmaceutical rigor.

As 2025 began, Amgen stood at an inflection point. The company that started by cloning a single gene now operated at the intersection of biology, chemistry, and computation. The next decade would determine whether Amgen could maintain its pioneering spirit while managing the complexities of a $180 billion market capitalization company.

IX. Playbook: Business & Investing Lessons

The conference room at Harvard Business School was packed beyond capacity as Robert Bradway concluded his guest lecture. A student raised her hand: "Mr. Bradway, if you had to distill Amgen's success into key principles that other companies could apply, what would they be?" Bradway smiled. "I'd need more than this hour, but let me try to synthesize forty-five years of lessons."

First-Mover Advantage in Platform Technologies

Amgen's history demonstrates that in biotechnology, being first with a platform technology creates compounding advantages that can last decades. When Fu-Kuen Lin cloned EPO, Amgen didn't just get a drug—they gained expertise in recombinant protein production that spawned multiple blockbusters. This expertise became a moat that competitors couldn't easily cross.

The lesson extends beyond biotech. Companies that pioneer fundamental technologies—Amazon with cloud computing, Tesla with electric vehicle platforms—create capabilities that generate returns far beyond the initial investment. The key is recognizing which technologies are truly platforms versus mere products. Platforms enable multiple applications; products solve single problems.

The Patent Strategy Paradox

Amgen's approach to intellectual property reveals a counterintuitive truth: the best patent strategy often involves filing many weak patents rather than relying on a few strong ones. The Enbrel patent thicket—dozens of interconnected patents covering manufacturing methods, formulations, and uses—proved more defensible than any single composition patent.

This "death by a thousand cuts" approach to patent protection works because challenging multiple patents is exponentially more expensive than challenging one. Each patent might be vulnerable individually, but collectively they create prohibitive legal costs for biosimilar manufacturers. Samsung Bioepis spent hundreds of millions challenging Enbrel patents before ultimately settling for a 2029 U.S. launch date.

The M&A Discipline Matrix

Amgen's acquisition history reveals clear patterns about when to buy versus build. The company acquired when they needed: (1) established commercial infrastructure in new therapeutic areas (Immunex for rheumatology), (2) late-stage or approved products with clear value propositions (Horizon for rare diseases), or (3) capabilities that would take too long to develop internally (Otezla for immediate revenue).

Conversely, Amgen built internally when dealing with: (1) platform technologies where their expertise provided advantage, (2) early-stage research where integration risks outweighed benefits, or (3) manufacturing capabilities that represented core competitive advantages. This disciplined approach avoided the value destruction that plagued many pharmaceutical M&A deals.

Managing the Patent Cliff Through Portfolio Architecture

Every successful drug company eventually faces patent cliffs, but Amgen's experience shows how thoughtful portfolio construction can minimize impact. The key is maintaining a balanced mix of: (1) protected franchises with extended exclusivity, (2) growing products in early lifecycle stages, (3) pipeline assets approaching commercialization, and (4) defensive plays like biosimilars.

When Epogen faced biosimilar competition, Aranesp was growing. As Neupogen patents expired, Neulasta was ascending. When Enbrel's cliff approaches in 2029, MariTide and the rare disease portfolio should be peaking. This orchestrated succession requires thinking in decades, not quarters—a discipline most companies lack.

The Manufacturing Moat

Amgen's investment in manufacturing excellence, initially seen as capital inefficiency, proved to be one of their strongest competitive advantages. Biological drugs aren't like small molecules where the product is defined by chemical structure. With biologics, "the process is the product"—minor variations in manufacturing can dramatically affect safety and efficacy.

By maintaining control over manufacturing and continuously innovating production technologies, Amgen created barriers that pure research companies couldn't match. When competitors' biosimilars faced manufacturing problems, Amgen's products maintained consistent quality. This reliability premium justified higher prices and maintained market share even against cheaper alternatives.

Capital Allocation in High-Risk R&D

Amgen's approach to R&D investment offers lessons in managing high-risk, high-reward portfolios. The company maintains a "shots on goal" philosophy—pursuing multiple approaches to major diseases rather than betting everything on single programs. But within this diversification, resource allocation is ruthlessly Darwinian. Programs that miss predetermined milestones are terminated quickly, with resources immediately redeployed to more promising efforts.

This combination of diversification and discipline is crucial in industries where success rates are low but payoffs are massive. The temptation is either to concentrate bets (risking catastrophic failure) or to spread resources too thin (ensuring mediocrity). Amgen's model shows how to balance these extremes.

The Biosimilar Hedge Strategy

Amgen's decision to become both a defender against and manufacturer of biosimilars represents sophisticated strategic thinking. By developing biosimilars to competitors' drugs, Amgen gained intelligence about the challenges facing their own products. By defending against biosimilars with patent thickets and lifecycle management, they learned what strategies actually worked.

This dual positioning also created optionality. If biosimilars became dominant, Amgen was positioned to win. If originator biologics maintained premium pricing, Amgen benefited there too. This hedging approach sacrificed some upside for significant downside protection—a rational trade in an uncertain regulatory environment.

Building Regulatory Expertise as Strategic Asset

Amgen's regulatory capabilities, built over decades of FDA interactions, became as important as their scientific expertise. The company didn't just comply with regulations—they shaped them. Amgen executives served on FDA advisory committees, contributed to regulatory guidance documents, and pioneered new approval pathways.

This regulatory fluency provided multiple advantages: faster approvals, better anticipation of agency concerns, and ability to navigate complex global requirements. While competitors struggled with regulatory delays, Amgen consistently achieved first-cycle approvals. In pharmaceuticals, where time to market can be worth billions, regulatory expertise translates directly to financial value.

The Platform-to-Franchise Evolution

Amgen's evolution from platform technologies (recombinant proteins) to therapeutic franchises (inflammation, cardiovascular, oncology) illustrates a crucial transition in corporate development. Platforms provide initial differentiation but eventually commoditize. Franchises—deep expertise in specific disease areas—create sustainable competitive advantages.

The transition requires different capabilities. Platform companies need great scientists; franchise companies need great clinicians. Platform companies focus on technology; franchise companies focus on patients. Amgen's successful navigation of this transition, while many biotech companies failed, provides a roadmap for other technology-driven companies facing similar evolution.

The Innovation Productivity Paradox

Despite massive increases in R&D spending, pharmaceutical industry productivity has declined for decades—a phenomenon known as Eroom's Law (Moore's Law backwards). Amgen's response reveals potential solutions: (1) focus on genetically validated targets where human biology provides proof-of-concept, (2) use biomarkers to identify responsive patient populations early, (3) terminate failing programs quickly to preserve resources, and (4) leverage external innovation through partnerships and acquisitions.

This approach requires accepting that most programs will fail while ensuring that successes are large enough to compensate. It's a venture capital mindset applied to internal R&D—a difficult cultural shift for companies accustomed to avoiding failure rather than embracing it as necessary for breakthrough innovation.

X. Analysis & Bear vs. Bull Case

The investment committee at a major pension fund was in its sixth hour of debate. On the wall, two columns laid out the case for and against a major position in Amgen. The fund's healthcare analyst summarized: "This isn't just about whether Amgen is a good company—it clearly is. The question is whether it's a good investment at current valuations given the opportunities and risks ahead."

Bull Case: The Transformation Story

The optimistic scenario for Amgen rests on multiple pillars, each reinforcing the others. First, the company's dominant position in multiple therapeutic areas provides pricing power and competitive insulation. In osteoporosis, Prolia and EVENITY control over 60% of the biologic market. In cancer supportive care, Neulasta maintains leadership despite biosimilar competition. Even mature products like Enbrel continue generating billions in cash flow.

The MariTide opportunity alone could transform Amgen's growth trajectory. With demonstrated 20% weight loss without plateau and monthly dosing, MariTide could capture significant share in a $150 billion obesity market. The comprehensive MARITIME Phase 3 program across obesity and related conditions positions Amgen to become a major player in metabolic diseases.

The Horizon acquisition is already exceeding expectations. Product sales grew 11% in Q4 2024, primarily driven by 14% volume growth. Excluding Horizon sales, product sales still grew 10%, driven by 15% volume growth. This suggests both successful integration and continued strength in the core business.

Manufacturing excellence provides sustainable advantage. Amgen's biologics production capabilities, refined over four decades, enable consistent quality and supply reliability that newer entrants can't match. This manufacturing moat becomes more valuable as biologics increase in complexity and regulators raise quality standards.

The company's financial strength enables continued investment while returning capital to shareholders. With over $9 billion in cash and strong free cash flow generation, Amgen can fund internal R&D, pursue acquisitions, and maintain dividend growth simultaneously. The 6% dividend increase in 2024 marked the 13th consecutive year of raises.

Geographic expansion, particularly in China, offers substantial growth potential. With only 10% of revenues from the world's second-largest pharmaceutical market, Amgen has room to grow internationally. Their localization strategy—building manufacturing and R&D in China—positions them better than companies relying purely on exports.

The biosimilars business provides both offense and defense. While generating over $3 billion annually from biosimilars of competitors' drugs, Amgen also gains intelligence about challenges facing their own products. This dual positioning creates optionality regardless of how the biosimilar market evolves.

Bear Case: The Maturity Trap

The pessimistic view starts with Amgen's dependence on aging franchises facing inevitable decline. Enbrel's 2029 patent cliff will eliminate approximately $3 billion in high-margin revenue. Prolia faces biosimilar competition by 2026. Even with lifecycle management, these losses will be difficult to offset.

The obesity market opportunity might be overhyped for Amgen specifically. MariTide won't reach market until around 2027, by which time Novo Nordisk and Eli Lilly will have established dominant positions. Next-generation obesity drugs from these leaders could obsolete MariTide before it achieves meaningful penetration.

Pricing pressures continue intensifying globally. The Inflation Reduction Act enables Medicare to negotiate drug prices directly, potentially reducing revenues for Amgen's products treating elderly populations. European governments are demanding larger rebates. Even in the U.S., pharmacy benefit managers are extracting higher discounts.

The Horizon acquisition, while successful so far, carries integration risks. Rare disease markets operate differently from Amgen's traditional businesses, requiring specialized capabilities that could be disrupted by integration. The $27.8 billion price tag requires near-perfect execution to generate acceptable returns.

Competition in biosimilars is intensifying from companies with lower cost structures. Samsung Bioepis, Coherus, and others can offer biosimilars at prices that challenge Amgen's margins. As more biosimilars enter the market, pricing power erodes for both originators and biosimilar manufacturers.

R&D productivity remains challenging despite massive investment. Amgen spends over $5 billion annually on R&D, but breakthrough innovations have become increasingly rare. The industry-wide decline in research productivity affects Amgen as much as any company.

Regulatory risks are mounting. The FTC's intervention in the Horizon deal signals increased antitrust scrutiny of pharmaceutical M&A. FDA requirements for larger, longer clinical trials increase development costs and risks. Post-marketing safety surveillance has become more stringent, potentially leading to restrictions or withdrawals.

Financial Metrics Analysis

Amgen trades at approximately 15x forward earnings, a premium to large pharmaceutical companies but a discount to high-growth biotechs. This valuation reflects the market's view of Amgen as a hybrid—more innovative than traditional pharma but more mature than pure biotech.

The company's return on invested capital has averaged 15% over the past five years, well above the cost of capital but below the 20%+ returns during the blockbuster era. This decline reflects both competitive pressures and the increasing capital intensity of drug development.

Free cash flow yield of approximately 5% provides support for the current dividend while funding growth investments. However, debt levels increased substantially with the Horizon acquisition, reducing financial flexibility for future deals.

Competitive Positioning

Compared to Roche, Amgen has better patent protection but less oncology depth. Versus Novartis, Amgen has stronger biologics capabilities but weaker small molecule expertise. Against Gilead, Amgen offers more diversification but potentially lower growth. Relative to Regeneron, Amgen provides more stability but less innovation upside.

The company's unique position—larger than most biotechs but more focused than big pharma—creates both advantages and challenges. Amgen can pursue opportunities too large for smaller companies but too risky for pharmaceutical giants. However, this middle ground also means competing against focused specialists and diversified giants simultaneously.

Scenario Analysis

In the optimistic scenario, MariTide becomes a $10 billion drug, Horizon products reach $6 billion in peak sales, and the core portfolio declines gradually. This could drive revenues to $45 billion by 2030 with expanding margins from manufacturing efficiency.

The base case assumes MariTide achieves $5 billion peak sales, Horizon grows modestly, and key products face biosimilar erosion. Revenues reach $38 billion by 2030 with stable margins as efficiency gains offset pricing pressure.

The pessimistic scenario sees MariTide failing to differentiate, Horizon integration issues, and rapid biosimilar penetration. Revenues stagnate around $30 billion with declining margins from competitive pressure.

XI. Epilogue & "If We Were CEOs"

The Amgen boardroom in January 2025 looked out over the same Thousand Oaks hills where Fu-Kuen Lin had searched for the EPO gene four decades earlier. But everything else had changed. The company that started with 50 employees now employed 24,000 globally. The single product hope had become a portfolio generating over $33 billion annually. The California startup had evolved into a multinational pharmaceutical enterprise.

If we were taking the CEO chair today, several strategic imperatives would demand immediate attention:

Accelerate the Digital Transformation

While Amgen has made progress in computational drug discovery, the company remains behind leaders like Recursion Pharmaceuticals or Insitro in applying AI to drug development. We would establish a separate digital therapeutics division with Silicon Valley culture and compensation, tasked with reimagining every aspect of drug discovery and development through computational approaches.

This means going beyond using AI for target identification. We would create digital twins of entire disease pathways, simulate clinical trials before running them, and develop AI-powered diagnostic companions for every drug. The goal: reduce development time by 50% and improve success rates from 10% to 25% within five years.

Restructure for the Post-Blockbuster Era

The blockbuster model that built Amgen is dying. Future growth will come from portfolios of specialized medicines for targeted populations. We would reorganize Amgen into semi-autonomous therapeutic area units, each with its own P&L responsibility, development budget, and commercial strategy.