Alkermes: The Drug Delivery Pioneer That Became a Neuroscience Powerhouse

The Quiet Giant You've Probably Never Heard Of

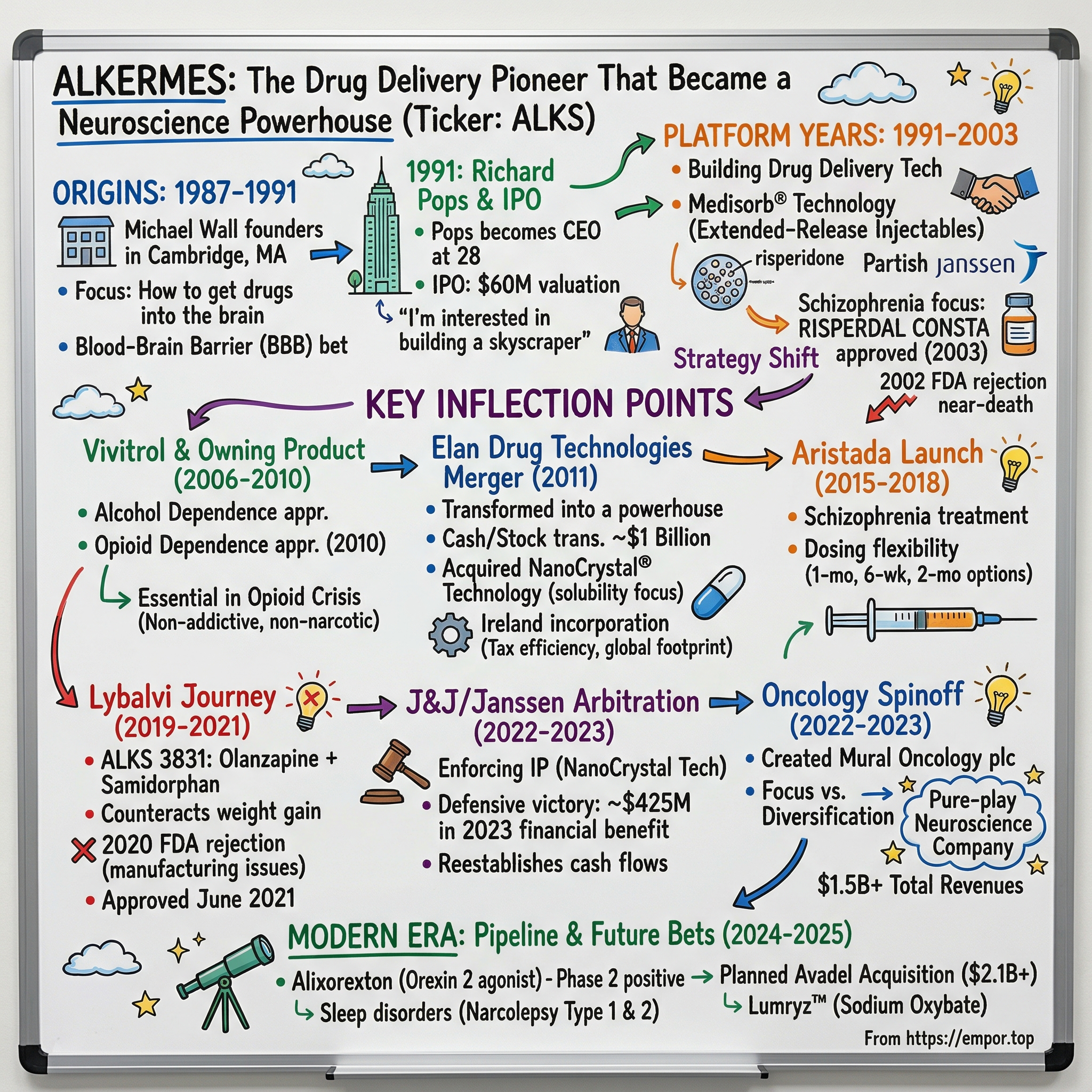

In the gleaming laboratories of Cambridge, Massachusetts, in the late 1980s, a small band of scientists and financiers were placing a contrarian bet on one of medicine's most frustrating problems: how to get drugs into the brain. While the rest of the biotech world rushed toward recombinant proteins and the molecular biology revolution, Alkermes was obsessing over the blood-brain barrier—that exquisitely selective fortress that keeps most therapeutic molecules out of the central nervous system.

Today, Alkermes commands total revenues of $1.56 billion, with net sales of proprietary products increasing approximately 18% year-over-year and GAAP net income from continuing operations of $372 million. The company has transformed from a tiny 1987 startup focused on drug delivery into what CEO Richard Pops calls "a highly profitable, pure-play neuroscience company" with more than 2,000 employees spread across operations on both sides of the Atlantic.

The central question of this story is deceptively simple: How did a company founded to solve someone else's drug delivery problems become a fully integrated pharmaceutical powerhouse with its own blockbuster products? The answer involves multiple near-death experiences, a transformational merger, a dramatic arbitration victory, and one of the longest CEO tenures in American corporate history.

This is a story about the power of long-acting injectables in psychiatric care—where medication adherence is the number one challenge—and about what happens when a platform company decides it wants to own its own destiny.

Origins: The Blood-Brain Barrier Bet (1987-1991)

Picture the late 1980s biotech landscape: Genentech had proven that engineered proteins could become blockbuster drugs. Amgen was racing toward erythropoietin. The entire industry was focused on what molecules to make, not how to deliver them. Into this environment stepped Michael Wall with an utterly counterintuitive thesis.

The company was founded in 1987 by Michael Wall. Wall was a founder of Flow Laboratories and Centocor, one of America's first biotechs—a man who had seen the biotech revolution from its inception and understood both its promise and its limitations.

Wall's insight was simple but profound: drugs are only as good as their ability to reach their targets. Alkermes was focused on trying to understand how the blood-brain barrier worked. At the time, there were only about 20 employees.

The blood-brain barrier is one of evolution's most elegant inventions—a network of tightly-packed cells lining the brain's blood vessels that prevents most substances from freely entering the central nervous system. It protects the brain from toxins and pathogens, but it also keeps out most therapeutic molecules. In the 1990s, there was a lot of excitement about the brain. In particular, many people were interested in neurotrophic factors in the brain that could lead to regeneration of neurons, opening up the possibility of treating neurological issues such as stroke or Alzheimer's disease. The problem was that proteins are big and don't get into the brain. This spurred Wall's initial premise for building Alkermes.

Wall understood something crucial: while everyone else was trying to make better molecules, Alkermes could become the gatekeeper—the company that understood how to get any molecule where it needed to go. It was a platform play before that term became fashionable in Silicon Valley.

The company's original focus was drug delivery, not drug development. This distinction would prove enormously important: Alkermes wasn't trying to discover new medicines but rather to make existing medicines work better. It was lower risk than de novo drug discovery, and it created a natural partnership model with larger pharmaceutical companies.

The biotech funding landscape of the late 1980s was fertile but also treacherous. The industry was young, and investors were still learning to evaluate companies that might not generate revenue for a decade or more. Drug delivery, with its more predictable development timelines and clearer regulatory pathway, offered a somewhat safer bet for venture capital—even if the ultimate upside was more modest than a breakthrough therapeutic.

But Wall wasn't planning to stay small, and he had his eye on someone who could help him build something truly substantial.

Richard Pops & the IPO (1991)

In 1991, a 28-year-old named Richard Pops received an unusual job offer. He had been working in New York, "involved with a group in New York trying to understand and develop novel financial structures to bankroll biotechnology companies." It was there that he made the acquaintance of Michael Wall.

"He was a really insightful, nonconformist type of fellow who wasn't afraid of doing things that hadn't been done before, and I suppose he saw something in me that wasn't obvious to me or anybody else," Pops later recalled.

When Wall first approached Pops about working at Alkermes, he didn't even tell him what the job was. Pops was intrigued by the idea of working with someone like Wall, as he was considered one of biotech's founding fathers. But it was only after several interviews, discussions, and dinners that Pops finally asked what job it was that Wall wanted him to do. "When he said 'CEO,' I laughed and told him to stop joking around," Pops recalls.

But Wall was serious. And once Pops agreed, Wall gave him remarkable latitude. "We can do whatever you want," Pops recalls Wall saying. "We can build it a little bit, package it up, and sell it to a pharmaceutical company, or we can build a 'skyscraper.'" Pops responded, "Well, the reason I'm coming on is that I'm interested in building a skyscraper."

Pops would need that ambition almost immediately. "I was a 28-year-old first-time CEO without a deep understanding of the whole company. Had I been put in a position of running an organization of 1,000 people back then, that would have been a recipe for failure." His first huge challenge came almost immediately—the company decided to go public that year.

"I smile thinking about it, because I believe it was at my first board meeting when we decided to go public," he explains. So, in July of 1991, Alkermes launched its IPO, which Pops recalls being rather modest by today's standards at a $60 million pre-money valuation. "We raised a bit of money, and that started the ball rolling on being able to expand our activities."

The IPO date was July 16, 1991. For context, that $60 million valuation seems almost quaint now—a rounding error by today's standards—but it represented a significant vote of confidence in a company with no commercial products and a business model built on becoming essential to others.

The dual business model that emerged under Pops would define Alkermes for the next two decades. The company would pursue neuroscience applications because of its focus on the brain, while simultaneously developing next-generation drug delivery capabilities. This diversification became one of Pops's core business philosophies—a hedge against the binary outcomes that often define biotech companies.

What's remarkable about Pops's tenure is its longevity. He is "not only one of the longest tenured CEOs in biopharma, but probably one of the top five most-tenured American CEOs of publicly traded companies." That three-decade run has given Alkermes a strategic consistency that's rare in an industry where executive churn is endemic.

The Platform Years: Building Drug Delivery Technology (1991-2003)

The 1990s were foundational years for Alkermes, a time when the company was building the technological infrastructure that would power its future. At the center of this work was Medisorb® technology—a system for creating extended-release injectables that would become the company's first commercial success.

The technology is elegant in its conception. Using proprietary Medisorb® drug-delivery technology developed by Alkermes, the RISPERDAL CONSTA formulation encapsulates risperidone in microspheres made of a biodegradable polymer, which are suspended in a water-based solution and injected into the muscle. Laboratory and clinical research has shown that the microspheres gradually degrade at a set rate to provide therapeutic blood levels of the drug in the bloodstream for an extended period. The polymer from which the microspheres are made breaks down into two naturally occurring compounds that are then eliminated by the body.

This might sound like technical jargon, but the practical implications were profound for psychiatric care. Schizophrenia patients often struggle with medication adherence—as many as 75 percent of patients with schizophrenia have difficulty taking their oral medication on a regular basis. Every missed dose increases the risk of relapse, hospitalization, and the devastating cascade of consequences that follow. A long-acting injectable that delivers consistent medication levels for weeks at a time doesn't just improve convenience—it fundamentally changes the treatment paradigm.

Alkermes pursued a partnership model, licensing its technology to Big Pharma companies that had the commercial infrastructure to bring products to market. The most important of these partnerships was with Johnson & Johnson's Janssen subsidiary.

On October 29, 2003, the FDA approved RISPERDAL® CONSTA® ((risperidone) long-acting injection) for the treatment of schizophrenia. Risperdal Consta is administered once every two weeks, rather than daily, for the management of schizophrenia. Until now, long-acting injection formulations of antipsychotics have been available only for older, conventional treatments.

This was the first and only long-acting atypical antipsychotic medication approved for use in schizophrenia at the time—a genuine first-in-class product. Under the partnership structure, Janssen-Cilag was responsible for worldwide sales and marketing of the product. Alkermes was responsible for worldwide manufacturing and received manufacturing fees and royalties on product sales.

The partnership model had clear advantages: Alkermes could leverage Janssen's global commercial capabilities without building its own sales force, generating revenue while continuing to invest in R&D. But it also had limitations. Every dollar of royalty revenue was a fraction of what Alkermes could have earned by owning and commercializing products itself.

The path to RISPERDAL CONSTA approval wasn't smooth. In 2002, J&J received a letter of rejection from the FDA for RISPERDAL CONSTA, which Alkermes was manufacturing. That news sent Alkermes stock plummeting nearly 70 percent. This was an extremely challenging period for the company.

This near-catastrophe became a teaching moment that Pops has revisited repeatedly. "A number of years ago, professors from the MIT Sloan School of Management approached me about writing a case study for two courses about a moment when something calamitous happened," he shares. "Then there's a day when Pops shows up to class, and on that day one of the students plays the role of Alkermes CEO at that point. The student CEO gives a presentation to describe the problem, while the rest of the class represents the company's board members, and together they determine a plan of action. After about an hour, the real Richard Pops is then invited to share what actually happened."

The company ultimately navigated through the regulatory issues, and RISPERDAL CONSTA launched successfully. But the experience highlighted both the risks and the dependencies inherent in the partnership model. Alkermes was at the mercy of its partners' regulatory execution and commercial priorities.

By the mid-2000s, Pops was increasingly focused on a strategic question: Could Alkermes transition from being a technology platform company to owning its own proprietary products?

KEY INFLECTION POINT #1: Vivitrol & Owning the Product (2006-2010)

The first major test of Alkermes's ability to own its own destiny came with Vivitrol—a product that would also become unexpectedly essential during America's opioid crisis.

On April 13, 2006, the FDA approved VIVITROL™ (naltrexone for extended-release injectable suspension) for the treatment of alcohol dependence. VIVITROL, the first and only once-monthly injectable medication for alcohol dependence, is indicated for alcohol dependent patients who are able to abstain from drinking in an outpatient setting and are not actively drinking when initiating treatment.

Unlike RISPERDAL CONSTA, which Janssen commercialized, Vivitrol represented a different strategic approach. Based on a joint commercialization agreement signed in June 2005, Cephalon had primary responsibility for the marketing and sales of VIVITROL and Alkermes was responsible for manufacturing VIVITROL. Under the terms of the agreement, Alkermes received a milestone payment of $110 million from Cephalon upon the FDA approval.

VIVITROL is the first and only once-monthly, extended-release injectable medication for the treatment of alcohol dependence. The proprietary Medisorb® drug delivery technology in VIVITROL enables the medication to be gradually released into the body at a controlled rate over a one-month time period.

The partnership with Cephalon represented a hybrid model—Alkermes maintained significant economic interest and manufacturing control while outsourcing the expensive and challenging task of building a specialty sales force for addiction medicine. But over time, Alkermes would take increasing control of the product's commercial destiny.

The second act for Vivitrol proved even more significant. On October 12, 2010, the FDA approved VIVITROL® for the prevention of relapse to opioid dependence, following opioid detoxification. VIVITROL is now the first and only non-narcotic, non-addictive, once-monthly medication approved for the treatment of opioid dependence. VIVITROL was approved by the FDA in 2006 for the treatment of alcohol dependence.

The timing of this expanded indication would prove prescient. America was entering the full bloom of its opioid epidemic, and Vivitrol—as a non-narcotic, non-addictive treatment—offered something crucial: a way to help patients maintain recovery without introducing another addictive substance.

"Opioid dependence is a growing disease and we believe that VIVITROL offers physicians and their patients a whole new approach, as the only long-acting, non-addictive treatment for opioid dependence," stated Richard Pops, Chief Executive Officer of Alkermes. "We look forward to helping to improve the lives of patients with this chronic and debilitating condition."

Vivitrol became essential infrastructure in the fight against opioid addiction—used in treatment centers, prisons, and drug courts across the country. Its unique properties made it particularly valuable for patients transitioning out of institutional settings, where the risk of relapse and fatal overdose is highest.

The strategic significance of Vivitrol extended beyond its commercial success. It represented Alkermes's first major step toward building its own commercial organization—a capability that would become increasingly important as the company evolved beyond pure platform licensing.

For investors, Vivitrol demonstrated that Alkermes could successfully commercialize a product, even if the commercial model was initially through partnership. It also revealed the company's ability to identify therapeutic areas—like addiction—where long-acting injectables could make a genuine clinical difference and where the company's expertise could translate into sustained competitive advantage.

KEY INFLECTION POINT #2: The Elan Drug Technologies Merger (2011)

If there is a single transaction that transformed Alkermes from an interesting specialty company into a genuine pharmaceutical powerhouse, it was the 2011 merger with Elan Drug Technologies.

In May 2011, Alkermes, Inc. and Elan Corporation, plc announced the execution of a definitive agreement under which Alkermes would merge with Elan Drug Technologies (EDT), the profitable, world-class drug formulation and manufacturing business unit of Elan, in a cash and stock transaction currently valued at approximately $960 million.

Alkermes and EDT would be combined under a new holding company incorporated in Ireland. This newly created company would be named Alkermes plc.

The strategic logic was compelling on multiple dimensions. The combined Alkermes would start life with 25 commercialized products, pro forma annual revenues of some $450 million, and a strong CNS-focused pipeline of in-house and partnered products in clinical development. Drug formulation capabilities would include EDT's oral controlled-release technologies and NanoCrystal® platform for poorly water-soluble drug compounds, together with Alkermes' long-acting injectable drug expertise.

The NanoCrystal technology acquisition deserves particular attention. EDT had been working on, and perfecting, its NanoCrystal technology, which essentially is a milling technique that breaks down drug crystal sizes to less than 2,000 nanometers. This seemingly small, simple solution addresses at least one major problem facing the pharmaceutical industry today: Poor solubility of drugs. Elan says its NanoCrystal technology is currently used in five commercialized products, including Invega Sustenna, an extended-release injectable suspension for schizophrenia approved by the FDA and marketed by Janssen in the United States.

But more than just gaining latter-stage drug development and production capabilities—including such EDT novelties as NanoCrystal technology for poorly water soluble drugs and proprietary technologies for oral controlled-release drugs—CEO Richard Pops now oversaw a well-equipped global manufacturing network. The combined operation includes GMP facilities in Wilmington, OH, Gainesville, GA and Athlone, Ireland.

"The merger will be financially transformative and create a profitable, global biopharmaceutical company with a diversified CNS product portfolio and a strong foundation for growth," stated Richard Pops. "Both companies have a proven track record as innovators. This merger will bring the scale and resources for strategic and balanced investment across the whole product continuum, from R&D innovation to clinical development, to world-class manufacturing and commercial expansion."

The merger was completed in September 2011, following the approval of the merger by Alkermes, Inc. shareholders on Sept. 8, 2011. Under the terms of the business combination agreement, Elan received $500 million in cash and 31.9 million ordinary shares of Alkermes plc, representing approximately 25% of Alkermes plc. Based on the closing share price of Alkermes, Inc. on Thursday, Sept. 15, 2011 of $16.52, this represented a total transaction value of approximately $1.0 billion.

The Dublin headquarters and Ireland manufacturing footprint had significant tax implications. Ireland's 12.5% corporate tax rate—roughly two-thirds lower than U.S. rates at the time—made the merged company substantially more tax-efficient. This wasn't a pure tax inversion; the combination had genuine operational substance, but the tax benefits were material.

More importantly, the increased cash flow enabled Alkermes to fundamentally shift its business model. The company had made the transition from being a drug delivery company driven by collaborations to a research-based company, to a partnering and royalty-based company, and now had the resources to become a proprietary products-based company with its own U.S. commercial operations.

For investors, the Elan merger represented a true category change. Before the deal, Alkermes was essentially a specialty services company—valuable, but with limited upside. After the deal, it had the scale, capabilities, and financial resources to compete as a mid-cap pharmaceutical company with diversified revenue streams and proprietary growth opportunities.

KEY INFLECTION POINT #3: Aristada Launch & Long-Acting Injectable Leadership (2015-2018)

With the Elan acquisition integrated and cash flow strengthening, Alkermes was ready to expand its proprietary product portfolio in schizophrenia—this time, competing in the same market where it had long served as a supplier to Janssen.

On October 5, 2015, Alkermes announced that the U.S. Food and Drug Administration (FDA) had approved ARISTADA™ (aripiprazole lauroxil) extended-release injectable suspension for the treatment of schizophrenia. ARISTADA is the first atypical antipsychotic with once-monthly and six-week dosing options for delivering and maintaining therapeutic levels of medication in the body through an injection.

FDA approval of ARISTADA was based on a proven safety and efficacy profile, including data from a randomized, double-blind, placebo-controlled, phase 3 study in 623 patients with schizophrenia.

ARISTADA's product profile offered genuine differentiation. In June 2018, the FDA approved two-month ARISTADA® (aripiprazole lauroxil) extended-release injectable suspension for the treatment of schizophrenia. ARISTADA is now FDA-approved in four doses and three dosing duration options (441 mg, 662 mg or 882 mg once monthly, 882 mg once every six weeks and 1064 mg once every two months) and can be initiated at any dose or interval, offering an unprecedented range of flexibility to patients and healthcare providers.

The flexibility was clinically meaningful. "The newly approved two-month ARISTADA gives people living with schizophrenia an option to treat their symptoms with only six injections per year." For patients struggling with the burden of frequent medical appointments, this represented a genuine improvement in quality of life.

"The formulation also means that Aristada can be sold as a liquid in prefilled syringes, unlike Otsuka's Abilify Maintena, which comes as a powder that must be reconstituted before administration. 'You basically put on the needle, shake it quickly, and then inject,' said Alkermes' chief financial officer, Jim Frates. 'Bringing a new, easy-to-use, flexible dosage form of aripiprazole is something physicians and patients are going to benefit from.'"

The competitive dynamics were notable. Alkermes was now competing directly with Janssen (J&J) in the long-acting injectable space while still serving as their manufacturing partner for RISPERDAL CONSTA and receiving royalties on the INVEGA products utilizing NanoCrystal technology. This "co-opetition" arrangement—simultaneously cooperating and competing—required careful management of relationships and clear delineation of intellectual property.

Aristada would cost about $1,500 a month, comparable to other long-acting antipsychotics. The pricing reflected Alkermes's strategy of competing on product attributes rather than price—the company believed that the dosing flexibility and ease of administration justified premium positioning.

By 2018, Alkermes had assembled a portfolio of proprietary commercial products generating substantial revenue, a technology platform that continued to produce royalty streams from partner products, and manufacturing capabilities that served both internal needs and partner requirements. The company was no longer just a platform—it was a fully integrated pharmaceutical company with multiple revenue engines.

KEY INFLECTION POINT #4: The Lybalvi Journey (2019-2021)

The development and approval of Lybalvi represented both Alkermes's scientific ambition and the regulatory gauntlet that pharmaceutical development can become.

The ALKS 3831 development program pursued an innovative approach: combining olanzapine—one of the most effective but also most problematic antipsychotics due to weight gain—with samidorphan, an opioid receptor antagonist designed to counteract the metabolic side effects.

The FDA approved Lybalvi for the treatment of schizophrenia and bipolar I disorder in June 2021. The drug has been commercially available by prescription in the US since October 2021.

Lybalvi® (olanzapine and samidorphan) is an oral atypical antipsychotic drug indicated for the treatment of adults with schizophrenia and bipolar I disorder. The drug is used as a maintenance monotherapy or for the acute treatment of manic or mixed episodes, either as a monotherapy or as an adjunctive therapy with lithium or valproate.

The FDA's approval of Lybalvi was based on the results of the ENLIGHTEN clinical development programme. In the ENLIGHTEN-1 study, Lybalvi's antipsychotic efficacy, safety and tolerability were assessed and compared to placebo for four weeks in 403 patients experiencing an acute exacerbation of schizophrenia. The study met its primary endpoint.

But the path to approval was far from smooth. The 2020 FDA rejection became one of the more memorable regulatory dramas in recent pharmaceutical history.

The Food and Drug Administration handed Alkermes a setback, citing manufacturing issues in refusing to approve the company's new schizophrenia medicine. Alkermes emphasized the agency raised no issues with data in the company's application for the drug, known as ALKS 3831, and hadn't requested any new studies. The FDA singled out tablet coating problems with specific development batches of the drug that have since been resolved, the company said. Data are available to address the FDA concerns, and the company is preparing a submission for regulators, Alkermes said. Chief Medical Officer Craig Hopkinson added the company sees "a clear path to resolution."

Tuesday's approval announcement came six and a half months after the FDA rejected Lybalvi because of manufacturing issues. That decision proved surprising, especially since a group of FDA advisors had just recently voted in favor of the drug. That decision proved surprising, especially since a group of FDA advisors had just recently voted in favor of the drug. While the agency isn't required to follow its advisors' recommendations, it typically does.

When the FDA's Psychopharmacologic Drugs Advisory Committee and Drug Safety and Risk Management Advisory Committee met last October to discuss Lybalvi, they voted 15-1, with one abstention, that the drug was effective and prevented weight gain. But by an 11-6 vote, experts were divided on whether a label warning would sufficiently capture the risks. The approval comes after the FDA sent a complete response letter (CRL) to the drug company in November of last year over concerns at a manufacturing site in the production of Lybalvi.

The commercial challenge was real but manageable. Chief financial officer Todd Nichols told investors that even though the US market for antipsychotic drugs is 90% generic, branded products still account for a $3 billion market, showing that there is an opportunity for products that can show a clear benefit over established therapies.

Speaking on a conference call, Alkermes CEO Richard Pops noted that the average schizophrenia or bipolar disorder patient switches therapies five times over a lifetime in the search of the medication offering the best balance of efficacy and tolerable side effects. The company believes Lybalvi can capture market share as patients make these switches.

Lybalvi's importance extends beyond its immediate commercial prospects. It represents Alkermes's ability to develop novel combination products—not just reformulations of existing drugs—and navigate the complex regulatory terrain that such innovation requires. The manufacturing issues that caused the initial rejection also prompted the company to strengthen its quality systems, lessons that would pay dividends in future development programs.

KEY INFLECTION POINT #5: The J&J/Janssen Arbitration Battle (2022-2023)

Few events better illustrate the value of robust licensing agreements than Alkermes's arbitration battle with Johnson & Johnson's Janssen subsidiary—a dispute that ultimately added hundreds of millions of dollars to the company's bottom line.

The conflict centered on the NanoCrystal technology that Alkermes had acquired through the Elan merger. Alkermes commenced binding arbitration proceedings in respect of two license agreements with Janssen Pharmaceutica N.V., a subsidiary of Johnson & Johnson. Under these agreements, Janssen received access and rights to Alkermes' small particle pharmaceutical compound technology, known as NanoCrystal® Technology, which enabled a number of successful products, such as INVEGA SUSTENNA®, INVEGA TRINZA®, INVEGA HAFYERA® and CABENUVA®. Janssen partially terminated the agreements in the United States effective as of February 2022. The purpose of the arbitration is to settle, among other things, whether, notwithstanding its partial termination of the agreements, Janssen has a continuing obligation to pay royalties on sales in the United States of products developed under the agreements.

Janssen refused to pay any royalties required by the agreements in the United States since the effective date of the partial terminations. Alkermes strongly disagreed with Janssen's position and contended that it continues to owe royalties. Alkermes remained committed to enforcing its contractual rights and addressing any unauthorized use of its intellectual property.

The stakes were enormous. J&J's Invega franchise accounted for $4.1 billion in sales in 2022, including $2.7 billion in the U.S.

The arbitration ruling decisively favored Alkermes. On May 31, 2023, Alkermes received a final award from the arbitral tribunal in its arbitration proceedings with Janssen Pharmaceutica N.V. In connection with the Final Award, the company raised its financial expectations for 2023 by approximately $425 million, which includes back royalties of approximately $194 million (inclusive of interest through March 15, 2023) related to 2022 U.S. net sales of the long-acting INVEGA® products and CABENUVA® that the company has now received from Janssen, and anticipated royalty revenues related to 2023 global net sales of these products. In addition, the company is entitled to future royalty revenues from Janssen related to these products in 2024 and beyond.

"From the outset, we believed strongly that Janssen was not entitled to cease paying royalties due to Alkermes on sales of these products," said Richard Pops, Chief Executive Officer of Alkermes. "This outcome reestablishes significant cash flows to Alkermes, provides strategic capital to our balance sheet and strengthens our longer-term financial profile by clarifying the distinct royalty term for each product covered by the license agreements."

The Final Award provided, among other things, that: while Janssen may terminate the license agreements, it may not continue to sell Products developed during the term of the license agreements without paying royalties pursuant to the terms of the respective agreements; back royalties related to U.S. sales in 2022 of approximately $194 million (inclusive of interest through March 15, 2023) are due to Alkermes from Janssen under the two agreements; and a separate Know-How Royalty term applies for each of INVEGA SUSTENNA®, INVEGA TRINZA® and INVEGA HAFYERA®.

The arbitration victory demonstrated the enduring value of the intellectual property Alkermes had acquired through the Elan merger. It also highlighted the importance of carefully drafted licensing agreements and the willingness to enforce contractual rights even against large and powerful partners.

For investors, the Janssen arbitration illustrated both a risk and an opportunity in Alkermes's business model. The risk: royalty streams can be disputed and interrupted, creating earnings volatility. The opportunity: well-structured agreements backed by genuine intellectual property can generate substantial long-term cash flows that survive changes in partner strategy.

KEY INFLECTION POINT #6: The Oncology Spinoff & Pure-Play Transformation (2022-2023)

The decision to spin off Alkermes's oncology business into a separate company called Mural Oncology represented a fundamental strategic choice: focus versus diversification.

On November 15, 2023, Alkermes announced that it had completed the separation of its oncology business into Mural Oncology plc (Mural Oncology), a new, independent, publicly traded company. Alkermes is now a pure-play, profitable neuroscience company that will continue its work to develop innovative medicines for people living with difficult-to-treat psychiatric and neurological disorders.

"The separation of our oncology business was an important element of our strategy to transform Alkermes into a pure-play neuroscience company with the potential to generate strong profitability and cash flow. With a topline driven by the growth of our proprietary commercial products, proven drug development capabilities, and an important pipeline opportunity..."

The new company, Mural Oncology, would continue registrational studies of its IL-2 cytokine in melanoma and ovarian cancer utilizing a $275 million cash runway expected to take them to the end of 2025. Mural Oncology began trading on the Nasdaq, with Alkermes shareholders receiving a share of Mural for every 10 shares of Alkermes. Mural launched with $275 million, which is expected to fund it through the fourth quarter of 2025.

"Spinning off Alkermes' oncology business by creating Mural Oncology, a public company, was a big undertaking given the IRS and SEC regulations," Pops said, but the cancer business deserved its own capital, instead of sharing with the neuroscience arm of the business. Moreover, Alkermes now has "a really clear story," Pops said. "It's a pure-play neuroscience company that has a billion dollars of revenue and growing."

The financial implications were immediate. The separation is associated with an anticipated reduction in operating expenses of approximately $20 million during the last six weeks of 2023, primarily consisting of Research and Development expenses. Net income according to generally accepted accounting principles in the U.S. (GAAP) was now expected to be in the range of $250 million to $280 million, revised from the prior expectation of $225 million to $265 million.

The spinoff reflected a broader evolution in Pops's thinking about corporate strategy. After decades of building diversified capabilities, the company was now betting that strategic clarity—being a pure-play neuroscience company—would be more valuable than the diversification that had previously been a core philosophy.

Now independent Mural Oncology focuses on advancing a pipeline of engineered cytokines for cancer, while Alkermes has recast itself as a "pure-play" neuroscience company. Richard Pops maintained his position as CEO of Alkermes. Mural Oncology is led by Caroline Loew.

For investors, the spinoff crystallized a clear investment thesis: Alkermes is now a focused bet on neuroscience, with established commercial products generating substantial cash flow and a pipeline of development candidates targeting significant unmet needs in sleep medicine and beyond. The oncology exposure—with its different risk profile and capital requirements—now sits in a separate vehicle for investors who want that exposure.

The Modern Era: Pipeline & Future Bets (2024-2025)

With its transformation complete, Alkermes entered 2025 with a focused strategy and what management believes is the most promising pipeline opportunity in the company's history.

"2024 was Alkermes' strongest year of financial and operational performance to date. Financially, we generated more than $1 billion in revenue from our proprietary commercial product portfolio, delivered EBITDA from continuing operations of approximately $452 million, repurchased $200 million of the company's ordinary shares, retired approximately $290 million of debt and ended the year debt-free with approximately $825 million of cash and investments on the balance sheet."

"2024 marked the completion of a multi-year effort to transition the business into a highly profitable, pure-play neuroscience company. We enter 2025 with a diversified portfolio of proprietary commercial products generating substantial profitability and an advancing development pipeline that represents a significant value creation opportunity in one of the most exciting potential new therapeutic categories in neuroscience," said Richard Pops, Chief Executive Officer of Alkermes.

The orexin 2 receptor agonist opportunity (alixorexton) represents Alkermes's most ambitious pipeline bet. Alkermes announced positive topline results from the randomized double-blind treatment period of the Vibrance-1 phase 2 study evaluating alixorexton in patients with narcolepsy type 1 (NT1). Alixorexton, formerly referred to as ALKS 2680, is the company's novel, investigational, oral orexin 2 receptor (OX2R) agonist in phase 2 development as a once-daily treatment for NT1, narcolepsy type 2 (NT2) and idiopathic hypersomnia (IH). In Vibrance-1, alixorexton met the primary endpoint across all doses tested, demonstrating statistically significant, clinically meaningful and dose-dependent improvements from baseline compared to placebo in wakefulness on the Maintenance of Wakefulness Test (MWT).

In November 2025, Alkermes announced positive topline results from the Vibrance-2 dose-ranging phase 2 study evaluating alixorexton in patients with narcolepsy type 2 (NT2). Alixorexton is the First Oral Orexin 2 Receptor Agonist to Demonstrate Efficacy in a Large Phase 2 Study in Patients With Narcolepsy Type 2, Supporting Advancement to Phase 3. Alixorexton Met the Study's Dual Primary Endpoints, Demonstrating Statistically Significant and Clinically Meaningful Improvements in Wakefulness and Excessive Daytime Sleepiness Compared to Placebo in Patients With Narcolepsy Type 2.

Alkermes' alixorexton has become the first drug in the orexin 2 receptor agonist class to show efficacy in phase 2 trials involving patients with both main subtypes of sleep disorder narcolepsy.

Alkermes plans to initiate the alixorexton narcolepsy global phase 3 program in the first quarter of 2026.

The proposed acquisition of Avadel Pharmaceuticals represents another major growth driver. Alkermes entered into a definitive agreement under which Alkermes will acquire Avadel, a commercial-stage biopharmaceutical company, for total transaction consideration of up to $20.00 per share in cash, which values Avadel at approximately $2.1 billion. The transaction has been approved by the boards of directors of both companies and is expected to close in the first quarter of 2026. The planned acquisition adds Avadel's FDA-approved product, LUMRYZ™ (sodium oxybate) for the treatment of cataplexy or excessive daytime sleepiness in patients over 7 years of age with narcolepsy, to Alkermes' commercial portfolio.

"This transaction represents a pivotal step in Alkermes' strategic evolution. With the acquisition of Avadel, we are able to accelerate our commercial entry into the sleep medicine market at a critical inflection point as we prepare to advance alixorexton into a phase 3 program in narcolepsy."

In November 2025, the companies reached agreement on the terms of an increased recommended offer under which Alkermes will acquire Avadel for total transaction consideration of up to $22.50 per share, consisting of $21.00 in cash and one non-transferable contingent value right entitling holders to a potential additional cash payment of $1.50 per share, contingent upon final FDA LUMRYZ™ Approval for the treatment of idiopathic hypersomnia in adults by the end of 2028.

Last month, at the World Sleep 2025 Congress, Alkermes presented promising phase 2 results for its sleep disorder asset alixorexton and touted the long-acting orexin 2 receptor agonist as the first drug in its class to "demonstrate clinically meaningful and statistically significant impact on wakefulness, cognition and fatigue with once-daily dosing." Alkermes plans to initiate a phase 3 trial of alixorexton in narcolepsy in 2026's first quarter. By the time it potentially gains approval later in the decade, Alkermes expects to have a significant presence in the market, thanks to its commercialization of Lumryz through the proposed Avadel buyout.

Playbook: Business & Investing Lessons

The Platform-to-Product Evolution

Alkermes's journey from drug delivery platform to integrated pharmaceutical company offers a masterclass in strategic evolution. The key insight: platform businesses can generate steady returns, but the really transformational value creation happens when you own the products, not just the enabling technology.

The transition wasn't overnight—it took decades, multiple acquisitions, and a willingness to build entirely new capabilities in commercial operations, regulatory affairs, and clinical development. Most platform companies never make this leap; those that do often stumble in execution. Alkermes succeeded because it maintained financial discipline, made strategically complementary acquisitions (Elan, potentially Avadel), and developed products in therapeutic areas where its core competencies in long-acting formulations could drive genuine clinical differentiation.

Long-Acting Injectable Dominance in Psychiatry

The company built its franchise on a simple clinical insight: medication adherence is the Achilles heel of psychiatric treatment. Patients with schizophrenia, bipolar disorder, and addiction struggle to take daily medications consistently, and every gap in treatment increases the risk of relapse, hospitalization, and tragic outcomes.

Long-acting injectables solve this problem structurally—a monthly or bi-monthly injection administered by healthcare professionals ensures consistent drug levels regardless of patient behavior. This isn't just a convenience feature; it's a clinical necessity that changes treatment paradigms.

Alkermes became the leading developer and manufacturer of these formulations, creating competitive moats through manufacturing complexity, regulatory expertise, and clinical data demonstrating outcomes advantages.

IP Defense Matters

The Janssen arbitration demonstrated that intellectual property rights are only as valuable as your willingness to defend them. Alkermes inherited the NanoCrystal technology through the Elan acquisition and then had to fight to preserve the royalty streams that technology generated. The $425 million revenue lift from the arbitration victory represented return on both the original acquisition investment and the legal resources deployed in defense.

For investors, this highlights the importance of understanding not just what IP a company owns, but whether it has the financial resources and legal capabilities to enforce those rights against well-resourced adversaries.

Bull & Bear Cases: Framework for Analysis

Bull Case

Orexin Platform Potential: Alixorexton's positive Phase 2 results in both narcolepsy type 1 and type 2 position it as a potential first-in-class once-daily oral therapy for sleep disorders. The orexin pathway represents fundamental biology regulating wakefulness, suggesting potential applications beyond narcolepsy into broader hypersomnolence disorders. With Takeda's competing orexin agonist also showing promise, investor attention has validated the therapeutic category while demonstrating substantial market opportunity.

Avadel Acquisition Synergies: The acquisition of Lumryz provides immediate commercial infrastructure and revenue in the sleep medicine market—precisely where alixorexton will eventually compete. Rather than building from scratch, Alkermes can leverage Avadel's specialized sales force and payer relationships. The $275 million in expected 2025 Lumryz revenue provides a solid base while alixorexton advances through Phase 3.

Cash Generation & Balance Sheet Strength: Debt-free status with approximately $825 million in cash gives Alkermes substantial optionality. The company can fund Phase 3 trials, execute the Avadel acquisition, and pursue additional pipeline opportunities without dilutive financing.

Porter's 5 Forces Analysis: - Barriers to Entry: High. Long-acting injectable manufacturing is technically demanding with significant capital requirements and regulatory hurdles. - Supplier Power: Moderate. Alkermes controls its own manufacturing, reducing dependence on external suppliers. - Buyer Power: Moderate to High. Payers exercise significant pricing pressure in psychiatric markets, but clinical differentiation can command premium positioning. - Substitute Threat: Moderate. Generic oral medications dominate the market by volume, but long-acting injectables offer distinct clinical advantages for adherence-challenged patients. - Competitive Rivalry: Moderate. The long-acting injectable space has limited competitors, though J&J/Janssen remains formidable.

Hamilton Helmer's 7 Powers: - Process Power: Strong. Alkermes's Medisorb and NanoCrystal technologies represent proprietary manufacturing processes that competitors cannot easily replicate. - Switching Costs: Moderate. Once patients are stabilized on a particular long-acting injectable, switching introduces risk and requires careful clinical management. - Counter-Positioning: Present in the orexin space. As a mid-cap company, Alkermes can pursue novel therapeutic categories that larger pharma companies may view as too small or risky.

Bear Case

Pipeline Concentration Risk: The bull case hinges heavily on alixorexton success. Phase 3 failure would eliminate the company's primary pipeline growth driver and likely result in significant multiple contraction.

Competitive Intensity in Orexin: Takeda's orexin program is more advanced, with Phase 3 data already in hand. If Takeda reaches market first, alixorexton may face significantly higher commercial hurdles despite potential differentiation on dosing convenience.

Royalty Stream Erosion: The Janssen royalties that were successfully defended through arbitration are time-limited. INVEGA SUSTENNA royalties ended in August 2024, and other product royalties will expire through 2030-2036. Proprietary product growth must offset declining royalty revenue.

Generic Competition: Vivitrol faces potential generic competition starting in 2027 under settlement agreements with Teva and Amneal. This long-established product may face significant price erosion that impacts overall margins.

Avadel Execution Risk: The acquisition, while strategically compelling, requires successful integration of a commercial organization while simultaneously preparing for potential alixorexton launch. Integration challenges or Lumryz sales underperformance could prove costly.

Key Performance Indicators to Track

For long-term investors monitoring Alkermes, three metrics deserve particular attention:

1. Lybalvi Prescription Growth Rate: Lybalvi represents the company's core commercial growth engine in psychiatry. Quarter-over-quarter prescription growth demonstrates market acceptance, payer access progress, and commercial execution capability. Management has invested heavily in direct-to-consumer advertising and sales force expansion; prescription trends reveal whether these investments are generating returns.

2. Alixorexton Clinical Milestones: Given the pipeline concentration in orexin biology, every clinical readout for alixorexton carries substantial information value. Watch for Phase 3 trial initiations (expected Q1 2026), enrollment progress, interim safety data, and regulatory interactions. Success or failure in the Vibrance program will likely determine the stock's direction more than any other single factor.

3. Proprietary Product Revenue Growth vs. Royalty Revenue Decline: Alkermes is in the midst of a revenue source transition—from a mix of proprietary and royalty/manufacturing revenue to increasingly proprietary-dominated. The rate at which proprietary product growth outpaces royalty erosion will determine whether total revenue can continue expanding through the transition period.

Regulatory & Legal Considerations

Generic Competition Settlements: Alkermes has entered settlement agreements that will permit generic Vivitrol competition beginning January 2027 for Teva and slightly later for Amneal. The trajectory of Vivitrol revenue erosion once generics enter will impact overall profitability.

Orexin Regulatory Pathway: The FDA regulatory pathway for orexin agonists is being established in real-time as both Alkermes and Takeda advance programs. Any guidance changes or safety concerns that emerge across the class could affect development timelines or label restrictions.

Avadel Acquisition Closing: The Avadel transaction remains subject to regulatory approvals and shareholder votes. The competing bid from Lundbeck, while ultimately unsuccessful in changing Avadel's recommendation, introduced transaction risk that may persist until closing.

Conclusion

Alkermes's nearly four-decade journey from a 20-person startup studying the blood-brain barrier to a profitable neuroscience company with $1.5 billion in annual revenue offers several enduring lessons.

First, platform companies can transition to integrated product companies, but it takes decades of patient capital allocation, strategically sound acquisitions, and willingness to build entirely new organizational capabilities. Most platform companies never make this leap.

Second, technical moats in pharmaceutical manufacturing—the ability to produce complex formulations like long-acting injectables that competitors cannot easily replicate—can generate sustained competitive advantage. Unlike molecule patents that expire, manufacturing expertise compounds over time.

Third, therapeutic focus eventually trumps diversification. After years of pursuing both neuroscience and oncology, Alkermes concluded that clarity of strategic identity—being the pure-play neuroscience company—was more valuable than portfolio diversification. The market seems to agree; the stock has performed well since the Mural spinoff.

The next chapter of Alkermes's story will be written by alixorexton. If the drug succeeds in Phase 3 and reaches market, Alkermes could emerge as a leader in the emerging orexin therapeutic category—a potential multi-billion dollar market addressing fundamental disorders of wakefulness. If it fails, the company remains a profitable neuroscience franchise but without the growth catalyst that would justify meaningful multiple expansion.

For Richard Pops, now in his 34th year as CEO, alixorexton represents perhaps the last major strategic bet of his tenure. Success would validate a career spent building manufacturing platforms, fighting IP battles, and patiently transitioning from technology provider to pharmaceutical company. It would also provide a fitting capstone to one of the longest and most successful CEO runs in biotechnology history.

The skyscraper that Pops told Michael Wall he wanted to build in 1991 now stands—profitable, focused, and reaching for new heights in sleep medicine. Whether it adds additional floors or faces structural challenges depends on clinical data yet to be generated. That's the inherent uncertainty of pharmaceutical investing, and it's why Alkermes remains one of the most interesting strategic stories in the industry.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube