ALKEM Laboratories: The Indian Pharma Underdog That Built an Empire

I. Introduction & Episode Roadmap

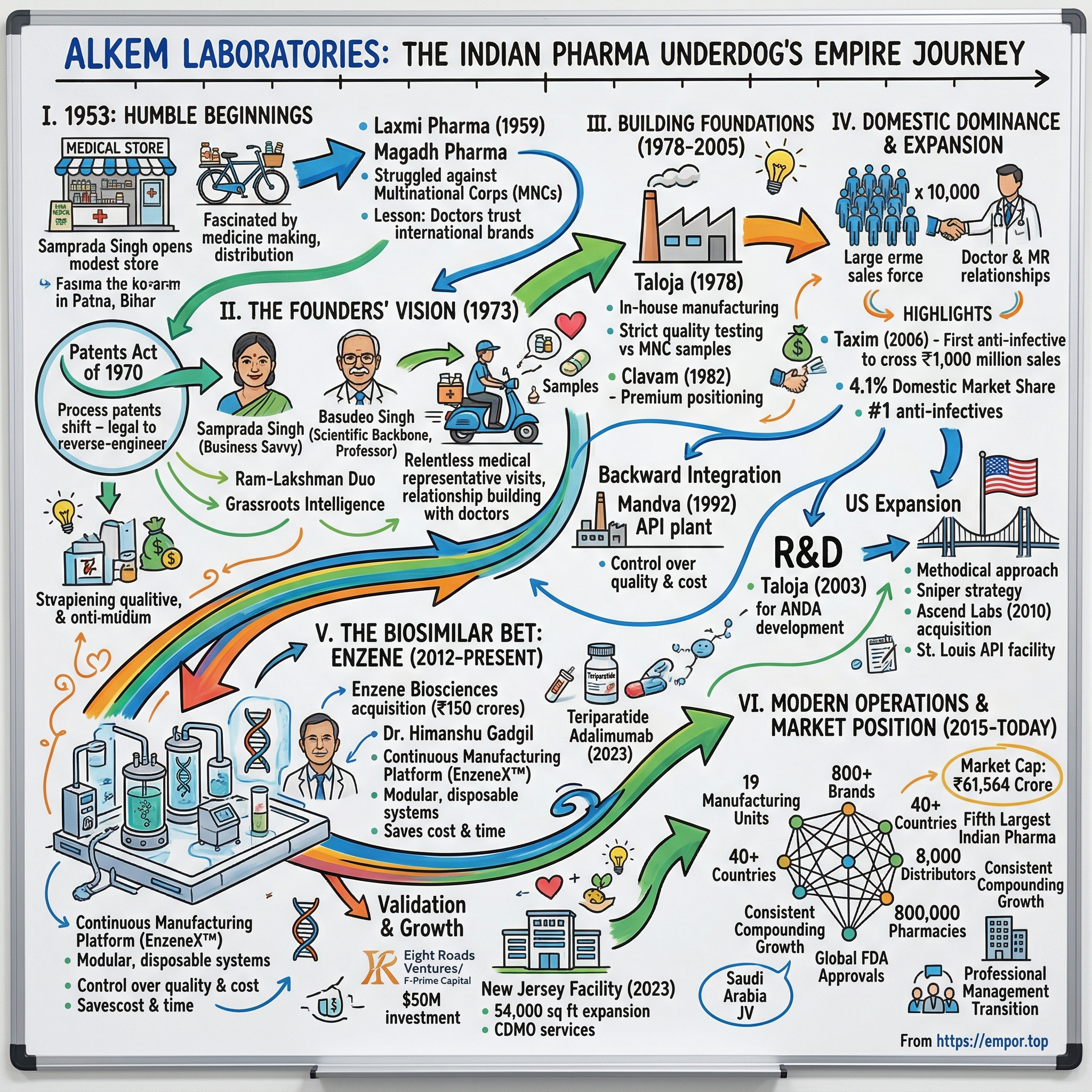

Picture this: It's 2015, and the Indian pharmaceutical market is witnessing one of its most anticipated IPOs. A company founded by two brothers from Bihar—one a former medical store owner, the other a university professor—is about to list at a valuation exceeding ₹12,000 crore. The bidding frenzy is palpable. Investment bankers are projecting this as the pharmaceutical event of the year. Yet most international investors have never heard of ALKEM Laboratories.

Fast forward to today: ALKEM commands the fifth-largest position in India's domestic pharmaceutical market with a 4.1% share, operates 19 manufacturing facilities, exports to over 40 countries, and maintains an iron grip on the anti-infectives segment where it reigns as the undisputed leader. Its market capitalization hovers around ₹61,564 crore—a testament to four decades of methodical empire-building in one of the world's most competitive pharmaceutical markets.

But here's what makes this story extraordinary: Unlike Sun Pharma's aggressive acquisition playbook or Dr. Reddy's early pivot to global generics, ALKEM built its fortress brick by brick through the unglamorous work of medical representative visits, doctor relationships, and a laser focus on branded generics in India. No flashy Silicon Valley–style disruption. No breathtaking M&A headlines in the early years. Just relentless execution in the trenches of Indian healthcare.

The central question driving this narrative isn't just how two brothers from Bihar built a pharmaceutical giant—it's how they did it while competing against both multinational behemoths with century-old legacies and nimble Indian upstarts backed by private equity. How did a company that started delivering medicines on bicycles in Patna end up developing biosimilars that compete with Big Pharma's biologics? And perhaps most intriguingly: Why did a family-controlled business that could have remained private forever choose to go public at the peak of the market?

This is the story of ALKEM Laboratories—a masterclass in building competitive advantages through patience, relationships, and an uncanny ability to spot market transitions before they become obvious. It's about understanding that in Indian pharma, brand equity with doctors matters more than patent portfolios, that trust beats technology in emerging markets, and that sometimes the best strategy is to let others chase the shiny objects while you quietly dominate the segments that actually make money.

Over the next several hours, we'll trace ALKEM's journey from Samprada Singh's first medical store in 1953 to the company's current position as a pharmaceutical powerhouse. We'll explore the strategic decisions that shaped its trajectory: the early bet on anti-infectives when others chased lifestyle drugs, the calculated entry into biosimilars through Enzene, the perfectly timed IPO that gave early investors legendary returns, and the ongoing transformation into a global player with manufacturing facilities from Dabhasa to New Jersey.

But this isn't just a corporate history lesson. It's a playbook for building enduring businesses in emerging markets, where relationships trump algorithms, where regulatory complexity creates moats, and where family businesses can outmaneuver professional managers through sheer long-term thinking. We'll examine how ALKEM navigated India's byzantine drug pricing controls, built a 10,000-person sales force that visits 400,000 doctors monthly, and why its Taxim brand became the first anti-infective in Indian pharmaceutical history to cross ₹1,000 million in sales.

We'll also confront the uncomfortable questions: Can ALKEM maintain its domestic dominance as Indian healthcare digitizes? Will its biosimilar bet through Enzene pay off against global giants with deeper pockets? And in a market increasingly dominated by chronic therapies, can a company built on acute care medications reinvent itself?

The structure ahead unfolds chronologically but thematically—each section revealing not just what happened, but why it mattered and what it teaches us about building pharmaceutical empires in emerging markets. From the founding struggles in Bihar to the gleaming manufacturing facilities of today, from handshake deals with distributors to algorithm-driven supply chains, from a medical store in 1953 to a company treating millions of patients globally.

This is that story—one that demonstrates that in business, as in medicine, sometimes the best cure isn't the newest drug but the one that reliably works, is accessible to millions, and is backed by decades of trust. Welcome to the ALKEM story.

II. The Founders' Journey: From Medical Store to Manufacturing

The year was 1953, and independent India was just six years old. In this nascent nation still finding its economic feet, a young man named Samprada Singh opened a modest medical store in Bihar. It was an unremarkable beginning—thousands of such stores dotted the Indian landscape. But Singh possessed something that set him apart: an obsessive fascination with not just selling medicines but understanding how they were made, distributed, and ultimately reached patients. He would spend hours studying drug formulations, questioning suppliers about manufacturing processes, and observing which medicines doctors prescribed most frequently.

By 1959, Singh had saved enough capital to take his first entrepreneurial leap, founding Laxmi Pharma. The venture was ambitious for its time—moving from retail to manufacturing in an era when the Indian pharmaceutical industry was dominated by multinational corporations like Glaxo, Pfizer, and Hoechst. These giants controlled over 80% of the market, wielding advantages in technology, capital, and brand recognition that seemed insurmountable. Singh's Laxmi Pharma struggled against these headwinds, but each failure became a lesson. He learned that competing on price alone was futile; Indian doctors, trained in Western medical schools, inherently trusted international brands.

The pattern repeated with his next venture, Magadh Pharma in Patna—another attempt to crack the manufacturing code that ended in disappointment. But Singh was nothing if not persistent. In 1970, he established Aristo Labs, and this time something clicked, though not entirely. The company gained traction in regional markets, but partnership disputes and capital constraints prevented it from scaling. These serial ventures might seem like failures, but they were actually reconnaissance missions. Singh was mapping the terrain, understanding distribution networks, building relationships with suppliers, and most importantly, identifying the gaps that a nimble Indian company could exploit.

The pivotal moment arrived in 1973. India had just passed the Patents Act of 1970, which recognized only process patents, not product patents, for pharmaceuticals. This meant Indian companies could legally reverse-engineer drugs patented abroad by developing alternative manufacturing processes. It was a seismic shift that would eventually transform India into the "pharmacy of the world," but in 1973, few recognized its full implications. Samprada Singh did. He founded Alkem Laboratories, naming it after his two children—a deeply personal touch that signaled this wasn't just another business venture but a legacy project.

But Singh knew he couldn't do it alone. He needed someone who understood the science as deeply as he understood the market. Enter his younger brother, Basudeo Singh—a man whose life trajectory seemed destined for academia, not entrepreneurship. Basudeo was a professor at Patna University, teaching pharmaceutical sciences to eager students. He had the comfortable life of an academic—respect, stability, intellectual stimulation. Yet when Samprada called, presenting his vision of an Indian pharmaceutical company that could compete with multinationals, Basudeo made a decision that would alter both their destinies. He resigned from his professorship and joined Alkem as its scientific backbone.

The contrast between the brothers was striking and complementary. Samprada was the street-smart entrepreneur who could read market dynamics like a chess grandmaster. Basudeo brought academic rigor and technical expertise. Together, they formed what employees would later call the "Ram-Lakshman" duo—a reference to the legendary brothers from the Hindu epic Ramayana, inseparable in their mission. But their roles often defied conventional expectations. Despite his professorial background, it was Basudeo who took charge of building distributor relationships, personally delivering stock to pharmacies across Mumbai and Gujarat.

Picture this: A former university professor, who once lectured to halls full of students, now navigating the chaotic streets of Mumbai on a scooter, pharmaceutical samples packed in carriers, visiting pharmacy after pharmacy. The humility was strategic. In Indian business culture, especially in the 1970s, relationships were everything. When pharmacy owners saw that a founder-director was personally ensuring their supplies, it built trust that no advertising campaign could match. Basudeo would often spend hours with distributors, not just discussing business but understanding their challenges, their customer complaints, their inventory management struggles. This grassroots intelligence became ALKEM's early warning system for market shifts.

The early product portfolio was deliberately unglamorous—basic antibiotics, pain relievers, and gastrointestinal drugs. While multinational competitors focused on patented molecules and lifestyle drugs for urban elites, the Singh brothers targeted the masses. They understood a fundamental truth about Indian healthcare: volume beats margin when you're serving a billion people. An antibiotic that could treat common infections at an affordable price would outsell a sophisticated cardiovascular drug accessible only to the wealthy.

But the real breakthrough in building distributor loyalty came through an innovative credit system. Unlike multinationals that demanded upfront payments or offered standard 30-day credits, ALKEM introduced flexible payment terms based on seasonal cash flows and local market dynamics. During monsoon months when infection rates soared, they extended credit periods, knowing distributors would need larger inventories. This wasn't just financial engineering; it was empathy translated into business practice.

By 1975, ALKEM had established a network of 50 distributors across Maharashtra and Gujarat. Each relationship was cultivated personally by one of the Singh brothers. They maintained detailed notes on every distributor—their family situations, business challenges, even their children's educational pursuits. Years later, when ALKEM had grown into a pharmaceutical giant, old distributors would recall how Basudeo Singh had attended their children's weddings or how Samprada Singh had helped them through business crises with extended credit lines.

The company's first manufacturing facility was actually a rented space in Andheri, Mumbai—a 2,000-square-foot unit that could barely be called a factory. The equipment was second-hand, purchased from a defunct pharmaceutical company. The staff consisted of twelve people, including the Singh brothers. Production runs were small, quality control was manual, and every batch was personally inspected by Basudeo. But what they lacked in scale, they compensated with consistency. ALKEM's drugs might not have had the premium packaging of multinational brands, but they worked reliably.

The philosophy that emerged during these foundational years would define ALKEM for decades: "Sanjeevani for Millions." Unlike the mythical herb from Ramayana that could revive the dead, ALKEM's sanjeevani was about keeping millions healthy through affordable, accessible medications. It wasn't trying to cure cancer or develop breakthrough therapies. It was ensuring that a daily wage laborer in Bihar could afford antibiotics for his child's fever or that a farmer in Gujarat could treat his chronic gastritis without selling his livestock.

As 1977 drew to a close, the Singh brothers made a decision that would transform ALKEM from a trading company with small-scale manufacturing into a serious pharmaceutical player. They acquired land in Taloja, near Mumbai, for their first dedicated manufacturing facility. The location was strategic—close enough to Mumbai for logistics and talent acquisition, but far enough to afford large land parcels for future expansion. The funding came from a combination of retained earnings and loans against personal guarantees by both brothers. They were betting everything on ALKEM's future.

The transition from traders to manufacturers, from a medical store to a pharmaceutical company, from academic theory to business practice—it all crystallized in this period. The Singh brothers had learned that in Indian pharma, success wasn't about breakthrough innovation or patent protection. It was about execution, relationships, and an unwavering focus on what Indian patients actually needed versus what global pharmaceutical companies thought they should want. This foundation, built on countless scooter rides, personal relationships, and affordable medicines, would support ALKEM's transformation into one of India's pharmaceutical giants.

III. Building the Foundation: Manufacturing & Brand Development (1978-2005)

The Taloja facility that opened in 1978 was modest by any standard—a single production line, basic tablet compression machines, and a quality control lab that doubled as Basudeo Singh's personal office. But for the Singh brothers, it represented sovereignty. No longer were they dependent on third-party manufacturers or constrained by others' production schedules. The first product off the line was an amoxicillin formulation, chosen deliberately. Antibiotics were the workhorses of Indian medicine—prescribed millions of times daily across the country's vast network of clinics and hospitals. If ALKEM could establish credibility in antibiotics, everything else would follow.

The early days at Taloja were characterized by a hands-on intensity that would become ALKEM legend. Basudeo Singh would arrive at 6 AM, checking the previous night's production logs before the first shift began. He instituted a practice that seemed eccentric then but proved prescient: every batch of medicines was tested not just for regulatory compliance but against samples from multinational competitors. The goal wasn't just to meet standards but to match or exceed what Glaxo or Pfizer offered, at a fraction of the cost. Workers recall him tasting oral suspensions himself, checking for palatability—because if children wouldn't take the medicine, therapeutic efficacy was irrelevant.

By 1982, ALKEM had introduced its first major branded generic: Clavam, a combination of amoxicillin and clavulanic acid. The timing was impeccable. Indian doctors were just becoming aware of antibiotic resistance, and combination therapies were seen as the solution. But ALKEM's masterstroke wasn't the product itself—several companies offered similar formulations. It was the brand-building strategy that followed. Instead of competing on price, ALKEM positioned Clavam as a premium antibiotic, pricing it just 10% below multinational equivalents while investing heavily in medical education.

The company pioneered what it called "scientific promotion"—sending medical representatives not just to sell but to educate. ALKEM's med reps carried detailed clinical studies, resistance patterns data, and treatment protocols. They organized continuing medical education (CME) programs for doctors, bringing specialists from Mumbai and Delhi to tier-2 and tier-3 cities. A pediatrician in Nashik or a general practitioner in Surat suddenly had access to the same information as their metropolitan counterparts. The psychological effect was profound: ALKEM wasn't just another pharmaceutical company; it was a knowledge partner.

The year 1992 marked ALKEM's second major manufacturing leap with the Mandva facility in Gujarat. Unlike Taloja, which focused on finished formulations, Mandva was conceived as a backward integration project. The facility would manufacture active pharmaceutical ingredients (APIs), the raw materials that form the heart of any medicine. This was a capital-intensive, technically complex undertaking that many Indian pharmaceutical companies avoided, preferring to import APIs from China. But the Singh brothers understood that API manufacturing was about control—control over quality, supply chains, and ultimately, margins.

The Mandva investment nearly broke the company. Construction costs overran by 40%, equipment installation faced repeated delays, and the technical expertise required was scarce in India. ALKEM recruited scientists from public sector undertakings like Hindustan Antibiotics Limited, offering them salaries that raised eyebrows in the industry. But the gamble paid off. By 1994, Mandva was producing not just APIs for ALKEM's own formulations but also supplying other Indian pharmaceutical companies. The facility gave ALKEM a cost advantage that competitors couldn't match—while others faced API price fluctuations and supply uncertainties, ALKEM's costs were predictable and controlled.

The period from 1995 to 2000 witnessed ALKEM's transformation from a manufacturer to a brand powerhouse. The company introduced Taxim, a cefixime antibiotic that would become its flagship product. The Taxim launch exemplified ALKEM's evolved marketing sophistication. Instead of targeting all doctors, they identified and mapped the top 1,000 physicians in each therapeutic area across India. These "super prescribers" received personalized attention—regular visits from senior medical representatives, invitations to international conferences, and first access to new clinical data. The strategy was resource-intensive but effective. When a leading physician in Mumbai or Chennai prescribed Taxim, dozens of junior doctors followed suit.

The year 2003 brought another strategic pivot with the establishment of ALKEM's R&D facility at Taloja, specifically designed for ANDA (Abbreviated New Drug Application) development. This was ALKEM's first serious foray into the regulated markets of the United States. The facility represented a cultural shift as much as a technical one. ANDA development required reverse-engineering complex molecules, proving bioequivalence, and navigating the FDA's labyrinthine regulatory requirements. ALKEM hired regulatory experts from Dr. Reddy's and Ranbaxy, companies that had pioneered the Indian assault on the US generics market.

But what truly distinguished ALKEM during this period was its ability to build enduring brand equity in a market where generics were supposed to be commodities. By 2005, the company had created a portfolio of power brands that doctors prescribed by name, not molecule. Taxim for respiratory infections, Clavam for resistant bacteria, Pan for acid reflux—these weren't just medicines but trusted allies in a physician's therapeutic arsenal. The brands commanded premium pricing despite being generics, a paradox that confounded multinational competitors who couldn't understand why Indian doctors remained loyal to ALKEM's brands even when cheaper alternatives existed.

The numbers told the story: By 2006, Taxim became the first anti-infective drug in Indian pharmaceutical history to cross ₹1,000 million in domestic sales. This wasn't just a financial milestone but a psychological breakthrough. It proved that an Indian company could build brands as powerful as any multinational's, that doctors would prescribe based on trust rather than just international pedigree. The achievement was celebrated at ALKEM with characteristic modesty—a small function at the Taloja facility where Samprada Singh, now in his seventies, reminded employees that ₹1,000 million meant nothing if it didn't translate to millions of patients treated effectively.

The company's approach to manufacturing quality during this period deserves special attention. While regulatory compliance was table stakes, ALKEM went beyond. They implemented what they called "patient-backward integration"—every manufacturing decision was evaluated based on its impact on the end patient. This meant choosing excipients that improved palatability even if they cost more, investing in packaging that maintained drug stability in India's harsh climate despite cheaper alternatives being available, and maintaining buffer stocks to ensure no prescription went unfilled due to supply shortages.

An illustrative example: In 2004, a contamination issue at a competitor's facility led to a nationwide shortage of certain antibiotics. While other companies saw an opportunity to raise prices, ALKEM increased production at Taloja and Mandva, maintaining prices while ensuring supply to even remote areas. The decision cost millions in overtime and logistics, but it cemented ALKEM's reputation among distributors and doctors as a reliable partner. Years later, when ALKEM launched new products, this goodwill translated into immediate market acceptance.

The period also saw ALKEM's first tentative international steps. Exports began to Nepal, Sri Lanka, and African countries—markets similar to India in disease profiles and purchasing power. These weren't lucrative markets by global standards, but they served as learning laboratories. ALKEM discovered that its India-developed formulations—designed for tropical stability, palatability for children, and affordable pricing—were perfectly suited for developing markets worldwide. A pediatric suspension formulated for Indian children worked equally well in Nigeria. An anti-malarial developed for Indian patients found ready acceptance in Southeast Asia.

By 2005, ALKEM had evolved from a single-product, single-facility operation into a complex pharmaceutical enterprise. Five manufacturing facilities, over 300 products, presence in 15 countries, and a field force of 3,000 medical representatives. But more importantly, it had developed intangible assets that no balance sheet could capture: relationships with 200,000 doctors who prescribed ALKEM brands reflexively, trust among 8,000 distributors who knew ALKEM would never leave them stranded, and a manufacturing culture where quality wasn't a department but a religion.

The foundation was complete. ALKEM was no longer just competing with multinationals; in many therapeutic segments, it was beating them. The company that had started with second-hand equipment in a rented facility now operated FDA-approved plants producing medicines for developed markets. The transformation from trader to manufacturer to brand-builder was complete. What remained was the leap from domestic champion to global player—a journey that would require not just capital and capability but the courage to compete in markets where being Indian was a liability, not an asset.

IV. The Growth Engine: Domestic Dominance & US Expansion (2007-2014)

The filing of ALKEM's first ANDA for Amlodipine in 2007 might seem like a routine regulatory submission, but within the company's Mumbai headquarters, it represented a watershed moment. The US generic market was the holy grail of Indian pharma—a $100 billion opportunity where Indian companies' cost advantages could translate into massive profits. But it was also a graveyard of ambitions, littered with companies that had underestimated the FDA's exacting standards or the brutal price competition among generic manufacturers. ALKEM's approach would be different: methodical, selective, and built on its domestic fortress rather than betting everything on American success.

The Amlodipine ANDA approval in 2009 validated the strategy. This wasn't a complex molecule or a difficult-to-manufacture product. It was a straightforward antihypertensive, chosen precisely because ALKEM could leverage its existing manufacturing expertise while learning the intricacies of FDA regulations. The first shipment to the US—10,000 bottles sent to a distributor in New Jersey—was modest by industry standards. But for ALKEM employees who gathered at Taloja to watch the container being sealed, it represented their company's arrival on the global stage.

What happened next would define ALKEM's international strategy for the next decade. Rather than chase every generic opportunity in the US market, the company adopted what it internally called the "sniper approach"—targeting specific products where it could maintain margins above 40%, even after brutal price competition. This meant avoiding blockbuster generics where 20 Indian companies would compete, driving prices to commodity levels. Instead, ALKEM focused on complex formulations, combination products, and niche therapeutic areas where its R&D capabilities provided genuine differentiation.

The 2010 acquisition of Ascend Laboratories in the US for approximately $35 million was ALKEM's first major international M&A transaction. Ascend wasn't a trophy asset—it was a modest company with 12 approved ANDAs and a small sales team. But it provided what ALKEM desperately needed: a front-end presence in the US market. No longer would ALKEM be dependent on third-party distributors who controlled customer relationships. Ascend's team, though small, understood American pharmacy chains, insurance formularies, and the complex web of rebates and discounts that characterized US pharmaceutical distribution.

The integration of Ascend revealed ALKEM's operational sophistication. Rather than imposing Indian management practices on the US team, ALKEM adopted a "federal structure"—Ascend maintained operational autonomy while ALKEM provided product pipeline and manufacturing support. The American team was incentivized based on profitability, not just revenue, aligning their interests with ALKEM's margin-focused strategy. Within two years, Ascend's revenue had doubled, not through new product launches but by better commercial execution of existing products.

2012 emerged as ALKEM's annus mirabilis—a year of transformative acquisitions that would reshape its future. The purchase of an API manufacturing facility in the US was strategic chess playing at its finest. While other Indian companies were building massive API facilities in India to serve global markets, ALKEM recognized that having US-based manufacturing provided intangible advantages—faster regulatory approvals, "Made in USA" labeling that some customers preferred, and proximity to customers for just-in-time delivery. The facility, located in St. Louis, specialized in controlled substances APIs, a niche where regulatory barriers limited competition.

But the year's most prescient move was the acquisition of Enzene Biosciences for approximately ₹150 crores. In 2012, biosimilars were still largely theoretical in India—complex biological drugs that few Indian companies had the expertise to develop or manufacture. The global biosimilar market was dominated by companies like Sandoz and Celltrion, with development costs running into hundreds of millions of dollars per product. Enzene, founded by scientist Himanshu Gadgil, had spent years developing capabilities in mammalian cell culture, protein characterization, and biological manufacturing—competencies that traditional pharmaceutical companies like ALKEM lacked.

The Enzene acquisition was initially met with skepticism by analysts. Why was ALKEM, successful in simple generics, venturing into the complex world of biosimilars where even Big Pharma struggled? The answer lay in ALKEM's reading of long-term market dynamics. Biological drugs would soon represent 50% of global pharmaceutical sales. Patents on blockbuster biologics worth $100 billion would expire by 2020. And critically, biosimilars weren't commodities like small-molecule generics—they required sophisticated development and manufacturing capabilities that created genuine barriers to entry. It was a bet on the future, financed by the cash flows from ALKEM's dominant domestic business.

The 2014 acquisition of the "Clindac-A" brand from Galderma marked ALKEM's entry into dermatology, but more importantly, it demonstrated the company's evolved M&A capabilities. Clindac-A was a well-established brand for acne treatment, with sales of approximately ₹150 crores. ALKEM paid a significant premium—₹340 crores—that raised eyebrows. But within 18 months, ALKEM had doubled the brand's sales through superior execution. They expanded the sales force calling on dermatologists, launched line extensions for different acne severities, and critically, reduced prices by 20% to expand market access. The playbook was classic ALKEM: acquire established brands, improve execution, expand access, and drive volume growth.

During this period, ALKEM's domestic business wasn't just growing; it was establishing dominance in key therapeutic segments. The anti-infectives portfolio, anchored by Taxim and Clavam, commanded a 15% market share in India. To put this in perspective: in a market with over 10,000 pharmaceutical companies, where the top player rarely exceeded 7% share in any segment, ALKEM's position in anti-infectives was unprecedented. The company achieved this through what competitors grudgingly admired as "perfect execution"—consistent product availability, uniform pricing across markets, and relationships with virtually every physician who prescribed antibiotics regularly.

The numbers from this period tell a story of explosive growth funded by operational excellence. Clavam crossed the ₹2,000 million mark in domestic sales in 2014, making it one of India's largest pharmaceutical brands. But unlike companies that achieved such scale through aggressive price cuts or trade margin manipulation, ALKEM's growth was "physician-driven"—doctors prescribed because they trusted the brand, not because they received higher incentives. This was validated by independent prescription audit data that showed ALKEM brands had among the highest "prescription loyalty" scores in the industry.

The field force expansion during 2007-2014 was remarkable in its scale and sophistication. ALKEM grew from 3,000 to 6,000 medical representatives, but this wasn't just numerical growth. The company implemented one of the industry's most sophisticated training programs, partnering with the Indian Institute of Management Ahmedabad to develop a curriculum that combined pharmaceutical knowledge with business acumen. Medical representatives weren't just trained to detail products; they were taught to understand physician prescribing patterns, patient demographics, and local disease epidemiology.

Technology adoption accelerated during this period, though in typically ALKEM fashion—practical rather than flashy. The company implemented a tablet-based customer relationship management system that tracked every doctor interaction, prescription pattern, and competitive activity. But unlike competitors who used such systems for surveillance, ALKEM positioned it as an enablement tool. Medical representatives could access clinical studies, drug interaction databases, and treatment guidelines in real-time during doctor visits. The system also identified "white spaces"—doctors who should be prescribing ALKEM products based on their patient profiles but weren't, enabling targeted intervention.

The international expansion beyond the US deserves attention. ALKEM entered Australia, the Philippines, and Chile—markets chosen not randomly but through careful analysis. These were countries with growing generic penetration, stable regulatory environments, and disease profiles where ALKEM's product portfolio had relevance. The approach to each market was customized. In Australia, ALKEM partnered with local companies for distribution. In the Philippines, it established its own subsidiary. In Chile, it acquired a small local player to gain immediate market access. This flexibility—the willingness to adapt strategy to local conditions rather than forcing a one-size-fits-all approach—distinguished ALKEM from Indian peers who often failed in international markets through rigid execution.

By 2014, ALKEM had achieved what seemed impossible a decade earlier. US revenue exceeded $200 million, international operations contributed 25% of total revenue, and the domestic business generated enough cash to fund all expansion without significant debt. The company that had started with a single ANDA filing in 2007 now had 40 approved ANDAs with another 50 pending. The biosimilars pipeline through Enzene included six molecules in various stages of development. The domestic business, far from being cannibalized by international expansion, had strengthened—market share increased across all key therapeutic areas.

But perhaps the most significant achievement wasn't captured in financial statements. ALKEM had successfully managed a transition that destroyed many family-owned Indian businesses—from entrepreneur-driven to professionally managed, from domestic to global, from generic manufacturer to innovation-oriented, all while maintaining the cultural values and operational discipline that defined its early years. The company was ready for its next act: accessing capital markets to fund the next phase of growth. The IPO preparations that began in late 2014 would culminate in one of Indian pharma's most successful public offerings.

V. The IPO Story: Going Public at Peak Valuation (2015)

The boardroom at ALKEM's Mumbai headquarters in early 2015 witnessed heated debates that would determine the company's trajectory for decades. The Singh family, which had built ALKEM without external capital for 42 years, was contemplating the unthinkable—diluting their ownership through an initial public offering. Samprada Singh, now 82, listened quietly as investment bankers from Kotak Mahindra, Citigroup, and Morgan Stanley presented their pitch decks, each promising to achieve the highest possible valuation. But for the patriarch, the IPO wasn't about maximizing proceeds; it was about institutional permanence, ensuring ALKEM would outlive its founders.

The timing seemed perfect, almost suspiciously so. India's stock markets were at historic highs, driven by foreign institutional investor inflows betting on the Modi government's reform agenda. The pharmaceutical sector was particularly hot—Sun Pharma had just completed its acquisition of Ranbaxy, creating a $4 billion entity. Dr. Reddy's was trading at premium valuations based on its US pipeline. The narrative around Indian pharma as the "pharmacy to the world" had never been stronger. Yet ALKEM's bankers knew they faced a unique challenge: selling a company that was overwhelmingly domestic-focused to investors obsessed with US generic opportunities.

The pre-IPO roadshows revealed this tension starkly. In conference rooms from Boston to Singapore, fund managers peppered ALKEM's management with the same questions: Why was 75% of revenue still from India when peers derived majority revenues from international markets? How could ALKEM justify premium valuations when its US presence was subscale compared to Sun or Dr. Reddy's? The management team, led by CEO Sandeep Singh (Samprada's son), had rehearsed their response: ALKEM wasn't trying to be another Sun Pharma. It was building a different model—dominating the world's fastest-growing pharmaceutical market while selectively participating in international opportunities.

The equity story that emerged was compelling in its contrarian logic. While competitors fought price wars in commoditized US generics, ALKEM enjoyed 20%+ EBITDA margins in India through branded generics. While others spent billions acquiring distressed assets, ALKEM generated 15%+ organic growth through field force expansion and new product launches. The company's return on equity exceeded 25%, among the highest in global pharma, achieved without the leverage that characterized peers' balance sheets. The message was clear: ALKEM was the pure-play bet on Indian healthcare consumption.

The IPO pricing discussions in November 2015 revealed the delicate balance between ambition and pragmatism. The bankers initially proposed a price band of ₹875-900, valuing ALKEM at approximately ₹10,000 crores. But the Singh family, demonstrating the long-term thinking that characterized their entire journey, pushed for a higher price of ₹1,050. This wasn't greed—it was strategic. A higher IPO price meant less dilution for the same capital raised, preserving family control while accessing public markets. After weeks of negotiation, the final price was set at ₹1,050, implying a valuation of ₹12,200 crores—among the highest ever for an Indian pharmaceutical IPO.

December 8, 2015, marked the opening of the IPO subscription window. What followed was a masterclass in investment banking orchestration. The qualified institutional buyer (QIB) portion was subscribed 8.5 times, with marquee names like Government of Singapore, Fidelity, and Aberdeen Asset Management placing large orders. But the real story was in the retail participation—over 200,000 individual investors applied, making it one of the most widely distributed pharmaceutical IPOs in Indian history. The grey market premium—the unofficial trading that occurs before listing—touched ₹200, suggesting strong post-listing performance.

The allocation process revealed ALKEM's priorities. While regulations mandated specific allocations to different investor categories, the company ensured its 10,000+ employees received preference in the employee quota. Distributors and doctors who had been associated with ALKEM for decades were quietly guided through the application process, ensuring they participated in the wealth creation. This wasn't just about spreading ownership; it was about aligning stakeholders with ALKEM's long-term success.

December 23, 2015—listing day—arrived with palpable anticipation. The opening bell at the Bombay Stock Exchange was rung by Basudeo Singh, now 78, who had delivered medicines on his scooter four decades earlier. The stock opened at ₹1,550, a 48% premium to the issue price, and touched ₹1,600 during the day before closing at ₹1,530. The single-day gain created wealth of approximately ₹2,000 crores for pre-IPO shareholders. But amid the celebration, Samprada Singh's message to employees was characteristically measured: "The market's judgment today is based on our past. Our job is to justify it through future performance."

The IPO proceeds of ₹1,349.61 crores were earmarked with surgical precision. Unlike many IPOs that are primarily offer-for-sale (OFS) where existing shareholders cash out, ALKEM's IPO included a significant fresh issue component. ₹800 crores was allocated for capital expenditure—new manufacturing facilities, R&D expansion, and critically, the biosimilar infrastructure for Enzene. ₹300 crores was designated for working capital as ALKEM planned to expand its field force to 10,000 representatives. The remaining proceeds would strengthen the balance sheet, providing dry powder for opportunistic acquisitions.

What the IPO documents revealed about ALKEM's business was as interesting as what they concealed. The prospectus disclosed that ALKEM's top 10 brands contributed 40% of domestic revenue—a concentration that would concern investors in other industries but was actually conservative by pharma standards where companies often had 60% concentration. The R&D spend at 6% of revenues was lower than peers who spent 8-10%, but ALKEM's R&D productivity—measured by new product launches per R&D dollar—was industry-leading. The company had 650 product registrations pending across 40 countries, suggesting a robust future pipeline.

The post-IPO shareholding structure was carefully crafted to maintain family control while ensuring adequate public float. The Singh family retained 51.8% stake, enough for absolute control but not so high as to concern minority shareholders about governance. Interestingly, the family created a trust structure for their holdings, ensuring smooth succession planning and preventing future family disputes that had destroyed many Indian business houses. International investors held 22%, domestic institutions 15%, and retail investors 11%—a balanced mix that ensured diverse perspectives in shareholder meetings.

The immediate post-IPO period tested ALKEM's communication with public markets. In the first earnings call in February 2016, analysts grilled management on everything from US FDA inspection outcomes to the sustainability of domestic growth rates. Sandeep Singh and CFO Rajesh Dubey demonstrated remarkable poise, providing detailed guidance without over-promising, acknowledging challenges while articulating solutions. The stock responded positively, crossing ₹1,700 by March 2016, validating the IPO pricing that some had considered aggressive.

The IPO's success had ripple effects beyond ALKEM. It demonstrated that investors would pay premium valuations for high-quality domestic pharma franchises, not just US generic plays. It encouraged other family-owned pharmaceutical companies to consider public listings. Within the company, it created a culture of quarterly accountability that, while initially uncomfortable for an organization used to thinking in years not quarters, ultimately improved operational discipline. The employee stock options granted post-IPO aligned middle management with shareholder value creation in ways that salary and bonuses never could.

But perhaps the IPO's most profound impact was psychological. For 42 years, ALKEM had operated in the shadows of larger, listed competitors. Now it was subjected to the same scrutiny, held to the same standards, and remarkably, found superior on many metrics. The validation wasn't just financial; it was existential. The company that had started in a medical store in Bihar was now worth more than many multinational pharma subsidiaries in India. The Singh brothers' vision of building an institution, not just a business, had been realized.

Looking back, the timing of ALKEM's IPO appears prescient. The company went public at peak valuations just before the Indian pharmaceutical sector entered a challenging period with US FDA issues, pricing pressure, and domestic regulatory changes. Had ALKEM waited even six months, the valuation would have been significantly lower. This wasn't luck—it was the same strategic timing that had characterized ALKEM's entire journey, from entering anti-infectives before the antibiotic boom to acquiring Enzene before the biosimilar wave. The IPO proceeds would fund the next chapter of growth, particularly the biosimilar bet that would define ALKEM's future.

VI. The Biosimilars Bet: Enzene & Future Growth (2012-Present)

When the Singh brothers acquired Enzene Biosciences in 2012 for approximately ₹150 crores, the biotechnology world collectively scratched its head. Here was ALKEM, a company that had built its empire on simple tablets and syrups, suddenly venturing into the rarefied world of monoclonal antibodies and recombinant proteins. The acquisition price seemed modest, but the technical complexity was staggering. Biosimilars weren't just difficult to make; they were nearly impossible to make profitably. Even pharmaceutical giants like Pfizer and Merck had struggled in this space, often abandoning biosimilar programs after burning through hundreds of millions in development costs.

The founder of Enzene, Dr. Himanshu Gadgil, was a different breed of entrepreneur than typically found in Indian pharma. A PhD from the Institute of Chemical Technology in Mumbai, he had spent years at Genentech in California, working on the cutting edge of biological manufacturing. When he returned to India in 2009 to start Enzene, his vision wasn't to build another biosimilar company but to reimagine how biological drugs were manufactured. His obsession: continuous manufacturing, a concept that had revolutionized industries from petrochemicals to semiconductors but remained elusive in biologics.

The early years under ALKEM ownership were characterized by patient capital deployment and strategic restraint. While competitors rushed to launch biosimilars in India's loosely regulated market, Enzene spent four years perfecting its manufacturing platform. The company's Pune facility, which began operations in 2019, looked nothing like a traditional biologics plant. Instead of massive stainless-steel bioreactors that could hold 20,000 liters, Enzene installed modular, disposable systems that operated continuously, producing the same output with a footprint 90% smaller than conventional facilities.

The technology breakthrough came through Enzene's development of what it branded EnzeneX™—a fully integrated continuous manufacturing platform that could take a process from cell culture to purified drug substance without the traditional batch interruptions. This continuous manufacturing technology platform promised to reduce costs significantly for biosimilar production, addressing the fundamental economic challenge that had stymied the industry. Where traditional biosimilar manufacturing required $100-200 million facilities and years of construction, Enzene's approach could be deployed in months at a fraction of the cost.

But technology alone doesn't create a business. ALKEM's contribution was commercialization expertise and deep pockets for clinical trials. The Indian biosimilar market, while less regulated than the US or Europe, still required extensive clinical studies to prove similarity to originator biologics. Each trial cost ₹50-100 crores and took 2-3 years to complete. ALKEM funded these systematically, treating Enzene not as a speculative venture but as a long-term strategic bet on the future of medicine.

The validation began arriving in waves. Enzene partnered with ALKEM to launch a teriparatide biosimilar for osteoporosis treatment, demonstrating the subsidiary's capability to tackle complex peptide therapeutics. But the real breakthrough came with the company's aggressive launch cadence starting in 2021. Within 18 months, Enzene launched four biosimilars, a pace that would have been impossible with traditional manufacturing approaches.

The February 2023 launch of adalimumab biosimilar (ENZ-129) for treating ankylosing spondylitis and rheumatoid arthritis marked a technical and commercial milestone. Adalimumab, originally marketed as Humira by AbbVie, was the world's best-selling drug with peak sales exceeding $20 billion annually. Creating a biosimilar version required not just copying the molecule but replicating its complex glycosylation patterns, ensuring identical pharmacokinetics, and proving clinical equivalence. This was Enzene's first commercial launch using its continuous manufacturing technology, validating years of platform development.

The strategic masterstroke came in 2022 when Enzene raised $50 million (approximately ₹408 crores) from Eight Roads Ventures and F-Prime Capital. This wasn't just capital; it was validation from two of the world's most sophisticated healthcare investors. Eight Roads, managing $8 billion in assets globally, and F-Prime Capital, with $5.3 billion under management, don't invest in science projects. They invest in companies poised to disrupt global markets.

The investment terms revealed ALKEM's strategic sophistication. Rather than selling a majority stake or spinning off Enzene entirely, ALKEM retained 92% ownership while giving investors just enough equity to align interests. The valuation wasn't disclosed, but industry sources suggested it exceeded ₹5,000 crores—a 30x return on ALKEM's initial investment in just ten years. More importantly, the investors brought global networks and expertise in scaling biotechnology companies, capabilities ALKEM couldn't develop internally.

The international expansion strategy that followed was audacious in scope yet pragmatic in execution. In June 2023, Enzene announced a $50 million investment in a manufacturing facility near Princeton, New Jersey. This wasn't just another plant; it was a statement of intent. The facility would be the first US manufacturing site for the company and one of the only biologics-focused continuous manufacturing bases established by an Indian firm in the US.

The New Jersey location was chosen with characteristic ALKEM thoroughness. Princeton's biotech corridor provided access to talent from pharmaceutical giants and startups alike. The 54,000 square feet facility would host multiple manufacturing lines using the EnzeneX™ platform. But what made this investment remarkable was its timing—launched just as the US government was incentivizing domestic pharmaceutical manufacturing through the BIOSECURE Act and other initiatives aimed at reducing dependence on China.

By 2024, Enzene expanded the facility further, adding 26,000 square feet for additional drug substance manufacturing suites, laboratories, and warehouse space. The expansion happened before the facility was even operational, driven by what the company described as "strong demand from U.S.-based small- and medium-sized innovators." This wasn't speculative capacity building; it was responding to committed customer contracts.

The CDMO (Contract Development and Manufacturing Organization) strategy represented another layer of sophistication. Rather than just producing its own biosimilars, Enzene positioned itself as a partner to global biotech companies that had promising molecules but lacked manufacturing capabilities. The continuous manufacturing platform became a differentiator—offering faster timelines, lower costs, and smaller batch sizes that were perfect for clinical trials and orphan drugs where traditional large-scale manufacturing was uneconomical.

The partnerships that emerged validated this approach. In December 2021, UK's Theramex entered an agreement with Enzene to develop, register, and commercialize a tocilizumab biosimilar. Lupin collaborated with Enzene to launch Cetuxa®, the first Indian biosimilar of cetuximab for head and neck cancer. These weren't just manufacturing agreements; they were strategic alliances where Enzene's technical capabilities complemented partners' commercial expertise.

The clinical development capabilities deserve special attention. ALKEM Managing Director Sandeep Singh indicated the company intended to initiate global clinical trials for its denosumab biosimilar to achieve FDA approval and US commercialization. This represented a fundamental shift in ambition—from serving India's price-sensitive market to competing in the world's most regulated and lucrative pharmaceutical market.

The talent strategy underpinning this expansion was quintessentially ALKEM—blend global expertise with Indian execution. Dr. Gadgil remained CEO, providing technical continuity, while ALKEM recruited commercial leaders from global CDMOs. The New Jersey facility planned to hire 300 employees, a mix of American bioprocess engineers and Indian scientists on international assignments. This cross-pollination of expertise created a unique culture—Silicon Valley innovation meets Mumbai hustle.

The financial performance validated the strategy. While ALKEM doesn't break out Enzene's financials separately, the subsidiary's contribution to the parent's growth was evident. ALKEM's consolidated revenue growth accelerated post-2020, driven partially by biosimilar sales. More importantly, Enzene opened new customer segments—large global pharmaceutical companies that would never have considered ALKEM as a partner for their complex biological molecules.

The continuous manufacturing platform's implications extended beyond cost reduction. Traditional batch manufacturing of biologics required extensive quality testing between steps, adding weeks to production timelines. Enzene's continuous process reduced a six-month manufacturing cycle to six weeks. For biosimilars of cancer drugs where patient access was literally life-or-death, this time compression had profound humanitarian implications beyond commercial benefits.

The regulatory strategy showed remarkable sophistication. Rather than choosing between Indian standards and global requirements, Enzene built its processes to meet the highest global standards from day one. The Pune facility was designed to be FDA-compliant even before the company had concrete plans for US commercialization. This forward-thinking approach meant that when opportunities arose, Enzene could move quickly without retrofitting facilities or revalidating processes.

Sandeep Singh, ALKEM's MD, noted that the company had "invested significantly in building a world-class biotech company through Enzene" and that their confidence was "justified by series of biosimilar launches". This wasn't corporate rhetoric; it was acknowledgment that the biosimilar bet had transformed ALKEM from a traditional pharmaceutical company into a biotechnology player.

The competitive implications were profound. While Indian pharmaceutical giants like Sun Pharma and Dr. Reddy's had also entered biosimilars, most relied on partnerships or acquisitions of existing facilities. ALKEM, through Enzene, had built capabilities organically, creating deeper technical knowledge and greater strategic flexibility. When Big Pharma eventually came looking for biosimilar partners in India, Enzene would be uniquely positioned—combining Indian cost advantages with global quality standards and proven US manufacturing capabilities.

Looking ahead, Enzene's pipeline suggested even greater ambitions. Beyond biosimilars of existing drugs, the company was developing novel biologics—original molecules that could command premium pricing and patent protection. The same continuous manufacturing platform that made biosimilars economical could accelerate novel drug development, potentially positioning Enzene as India's first global biotechnology innovator.

The transformation from a ₹150 crore acquisition to a potential ₹5,000+ crore valuation in a decade represented more than financial success. It validated ALKEM's ability to identify technological discontinuities and invest ahead of the curve. While competitors chased immediate returns in crowded generic markets, ALKEM had quietly built a biotechnology platform that could define its next 50 years. The journey from tablets to antibodies, from Taloja to New Jersey, from copying molecules to creating them—it all started with the recognition that the future of medicine would be biological, and ALKEM needed to be ready.

VII. Modern Operations & Market Position (2015-Today)

The morning of August 13, 2025, witnessed something remarkable at ALKEM's Mumbai headquarters. The stock had jumped 7% in early trading, touching ₹5,400—not because of a breakthrough drug approval or a mega-acquisition, but because the company had reported another quarter of steady, predictable growth. Q1 FY26 results showed net profit surging 107% quarter-on-quarter, with the stock making a day high of ₹5,205.45 per share, up 7.5% from the previous close. In an era when pharmaceutical investors chase binary events and moonshot molecules, ALKEM's consistent execution had become its own form of disruption.

The scale of modern ALKEM operations defies easy comprehension. The company operates 19 manufacturing units, maintains 800 brands, and has a business footprint across 40 countries. But numbers alone don't capture the operational complexity. Every day, 10,000 medical representatives fan out across India, visiting 400,000 doctors monthly. The logistics network ensures that medicines reach 8,000 distributors who serve 800,000 retail pharmacies. This isn't just distribution; it's a cardiovascular system pumping pharmaceutical products to every corner of India.

ALKEM holds a 4.1% market share in the Indian domestic formulation market as of 9M FY25, making it the 5th largest pharmaceutical company in India, maintaining its #1 position in anti-infectives with a strong presence in gastrointestinal, pain management, vitamins, minerals, and nutrients segments while expanding in chronic therapies. This market position, built over decades, creates a moat that new entrants—despite deeper pockets or superior technology—find impossible to breach.

The domestic business remains ALKEM's fortress. In Q1 FY26, India sales grew 12% year-on-year to ₹2,265 crores, demonstrating that even in a mature market, execution excellence drives growth. The company's ability to grow faster than the Indian Pharmaceutical Market (IPM) consistently—8.4% versus IPM's 8.7% in recent quarters—reflects not market expansion but market share capture. Every basis point of share gained represents millions of prescriptions shifted from competitors, each one a vote of confidence from a doctor who chose ALKEM's brand over alternatives.

The evolution of ALKEM's therapeutic mix reveals strategic sophistication. While anti-infectives remain the crown jewel, the company has systematically expanded into chronic therapies—diabetes, cardiology, neurology—where patient lifetime value exceeds acute treatments by orders of magnitude. The Pulmocare division, launched in 2021 to target respiratory ailments, exemplifies this evolution. Rather than competing head-on with established players, ALKEM identified underserved segments within respiratory care and built focused teams to address them.

The international expansion milestones tell their own story: US revenue crossing $200 million in 2018, and total company revenue surpassing $1 billion in 2019. These weren't vanity metrics but validation that ALKEM could compete globally while maintaining domestic dominance. The US business, built methodically through the Ascend platform, now contributes meaningful profits rather than just revenue. With 40 approved ANDAs and another 50 pending, the pipeline ensures steady growth without the boom-bust cycles that characterize commodity generics.

The manufacturing footprint has evolved from production capacity to competitive advantage. ALKEM's facilities possess regulatory approvals from USFDA, MHRA-UK, TGA-Australia, ANVISA-Brazil, WHO-Geneva, TPD-Health Canada, and various African, Asian and CIS countries. Each approval represents years of quality system improvements, documentation protocols, and cultural transformation. The ability to supply regulated markets from India-based facilities provides cost advantages that US or European manufacturers cannot match.

Technology adoption at ALKEM follows a pragmatic philosophy—digitize where it adds value, maintain human touch where relationships matter. The company has introduced electronic logbooks and batch cards in international manufacturing plants, reducing manual transcription errors and improving traceability. But in the field, where medical representatives meet doctors, technology augments rather than replaces human interaction. Tablets provide real-time access to clinical data and competitive intelligence, but the representative's ability to build trust remains paramount.

The quality culture deserves special mention. With over 3,000 people in production teams working alongside quality teams, ALKEM has institutionalized a "zero-defect" mindset that goes beyond regulatory compliance. Each manufacturing unit operates its own quality control unit, ensuring problems are caught at source rather than downstream. This distributed quality architecture—expensive and complex to maintain—prevents the catastrophic recalls that have destroyed pharmaceutical companies' reputations overnight.

Recognition has followed performance: in 2022, Clavam reached ₹6 billion in sales, and ALKEM was honored as "Pharma Company of the Year" at the ET India Pharma World Awards, ranking 31st among India's best companies to work for. These accolades matter less for vanity than for talent acquisition. In India's competitive pharmaceutical job market, being recognized as a top employer attracts the scientists, managers, and sales professionals who drive innovation and growth.

The recent strategic moves signal ALKEM's next chapter. The company will establish a subsidiary in Saudi Arabia, with ALKEM holding 51% stake and local partner Abdulaziz Alsheikh holding 49%, focusing on manufacturing, importing, marketing, and distributing pharmaceutical and nutraceutical products. This isn't just market entry; it's a template for expansion into Middle Eastern markets where local partnerships are mandatory but fraught with execution risks. ALKEM's approach—majority control with meaningful local participation—balances control with local expertise.

The New Jersey expansion represents another level of ambition. Enzene's facility, initially planned at 54,000 square feet, expanded by another 26,000 square feet even before opening, adding drug substance manufacturing suites, laboratories, and warehouse space, with the site expected to be operational by June 2024. The expansion before operational launch—driven by customer pre-commitments—validates the continuous manufacturing platform's commercial appeal.

The field force evolution from 3,000 in 2005 to 10,000 today represents more than numerical growth. Each representative undergoes months of training, not just on product knowledge but on understanding disease pathophysiology, treatment protocols, and patient psychology. The investment in human capital—often dismissed as old-fashioned in the digital age—creates relationships that apps and algorithms cannot replicate. When a doctor prescribes ALKEM's brand, they're not just choosing a molecule; they're trusting a relationship built over years of consistent interaction.

Financial discipline underpins operational excellence. Despite aggressive expansion, ALKEM maintains one of the industry's strongest balance sheets—minimal debt, consistent cash generation, and return on equity exceeding 25%. This financial strength provides strategic flexibility. When opportunities arise—whether acquiring brands, building facilities, or entering new markets—ALKEM can move quickly without financial engineering or dilutive fundraising.

The innovation pipeline, while less visible than commercial operations, positions ALKEM for long-term growth. Beyond the 50 pending ANDAs for the US market, the company has 650 product registrations pending across 40 countries. Each registration represents a future revenue stream, carefully selected based on competitive dynamics, manufacturing complexity, and margin potential. This isn't a scattershot approach but systematic portfolio construction.

Market performance tells its own story: with a market capitalization of ₹61,564 crore, the company has delivered sales growth of 9.21% over five years. While analysts might characterize this as "poor" growth, it represents sustainable, profitable expansion in an industry where many chase growth at any cost. ALKEM's philosophy—grow steadily, maintain margins, preserve culture—might seem conservative, but it has created more shareholder value than many "high-growth" competitors who burned cash chasing revenue.

The operational complexity hidden behind these numbers is staggering. Consider a single product's journey: raw materials sourced from qualified suppliers, manufactured in climate-controlled facilities, tested at multiple stages, packaged for stability in tropical conditions, distributed through temperature-controlled supply chains, and ultimately dispensed to patients. Multiply this by 800 brands across multiple markets, and the orchestration required becomes apparent. That ALKEM executes this daily, with minimal stockouts or quality issues, represents operational excellence at scale.

Looking forward, ALKEM faces the classic innovator's dilemma. The domestic branded generics business that built the company faces pricing pressure and digital disruption. The US generics market offers growth but at lower margins. Biosimilars promise high returns but require massive investments with uncertain outcomes. International expansion provides diversification but adds complexity. Navigating these trade-offs while maintaining the operational excellence that defines ALKEM will determine whether the company remains a domestic champion or evolves into a global pharmaceutical force.

The transformation from 2015's IPO to today's operations reveals an organization that has successfully managed the transition from family-owned to professionally-managed while maintaining entrepreneurial agility. The company that once delivered medicines on scooters now operates FDA-approved facilities supplying global markets. Yet at its core, ALKEM remains what it always was: a company obsessed with operational excellence, believing that in pharmaceuticals, as in medicine, consistent execution beats sporadic brilliance. In a world chasing the next blockbuster drug, ALKEM's success comes from doing ordinary things extraordinarily well, repeatedly, at scale.

VIII. Playbook: Business Lessons & Strategy Analysis

The ALKEM story reveals a counterintuitive truth about pharmaceutical success: in markets where everyone chases innovation, operational excellence becomes the ultimate differentiator. The company's playbook, refined over five decades, offers lessons that extend beyond pharma into any industry where trust, distribution, and execution determine winners.

The Branded Generics Paradox

ALKEM's core insight was recognizing that in India, brands matter more than molecules. While Western markets treat generics as commodities differentiated only by price, Indian doctors prescribe by brand name, not chemical composition. This cultural quirk—rooted in medical education where professors taught using brand names and reinforced by patients who request specific brands—created an opportunity for value creation in supposedly commoditized products.

The genius lay in execution. ALKEM didn't just slap brands on generic molecules; it built emotional equity. Taxim wasn't just cefixime; it was the antibiotic doctors trusted for pediatric infections. Clavam wasn't just amoxicillin-clavulanate; it was the combination that worked when simple amoxicillin failed. These brands commanded 30-40% price premiums over identical molecules from other manufacturers—a pricing power that would baffle Western pharmaceutical executives.

The strategy required patience. Building brand equity in pharmaceuticals takes years of consistent quality, reliable supply, and thousands of doctor interactions. ALKEM resisted the temptation to launch hundreds of "me-too" brands, instead focusing on a portfolio of power brands that could sustain multi-decade growth. Today, the top 10 brands contribute 40% of domestic revenue—concentration that provides economies of scale in promotion and distribution.

The Medical Representative as Strategic Asset

In an era of digital marketing and AI-driven targeting, ALKEM's investment in human field force seems anachronistic. Yet the 10,000 medical representatives represent the company's most defensible moat. Each representative visits 8-10 doctors daily, armed not just with product samples but with clinical knowledge, competitive intelligence, and problem-solving capability.

The key insight: pharmaceutical selling in India isn't transactional but relational. Doctors don't just evaluate efficacy and price; they consider trust, reliability, and support. When a medical representative helps a doctor navigate insurance paperwork, arranges a consultation with a specialist, or provides samples for indigent patients, they're building switching costs that no digital platform can overcome.

ALKEM's field force strategy differs from competitors in crucial ways. Rather than rotating representatives frequently to prevent relationship capture, ALKEM encourages long-term assignments. Some representatives have called on the same doctors for decades, becoming trusted advisors rather than salespeople. This continuity creates institutional knowledge—understanding which doctor prefers which formulation, who treats which patient population, what concerns keep them awake at night.

The training investment is substantial. New representatives undergo three months of initial training, followed by continuous education throughout their careers. They learn not just pharmacology but psychology, not just products but patient outcomes. The result: ALKEM representatives are viewed as knowledge partners, not product pushers.

Capital Allocation Discipline

ALKEM's capital allocation framework reveals strategic discipline rare in family-controlled businesses. The company follows a clear hierarchy: first, invest in organic growth through field force expansion and product development; second, acquire strategic assets that fill portfolio gaps; third, build new capabilities like biosimilars; and only then, return capital to shareholders.

The M&A track record demonstrates this discipline. Unlike peers who pursued transformational deals, ALKEM made targeted acquisitions—Ascend for US front-end, Enzene for biosimilars, Clindac-A for dermatology entry. Each deal was sized to be digestible, priced to ensure returns exceeded cost of capital, and integrated to preserve value. The company walked away from numerous opportunities that didn't meet these criteria, including several high-profile auctions where emotional bidding drove prices beyond rational levels.

The international expansion strategy followed similar logic. Rather than betting everything on US generics like many peers, ALKEM treated international markets as portfolio options. Investments were staged, with each market proving itself before receiving additional capital. This optionality approach—small initial investments with right to expand—limited downside while preserving upside.

Managing the Acute vs. Chronic Transition

ALKEM built its fortune on acute therapies—antibiotics, analgesics, gastrointestinals—where treatment duration is short but volume is high. As Indian disease profiles shifted toward chronic conditions—diabetes, hypertension, depression—the company faced a strategic challenge: how to compete in chronic therapies without abandoning acute care strengths.

The solution was organizational ambidexterity. Rather than forcing the entire organization to pivot, ALKEM created dedicated chronic care divisions with distinct metrics, incentives, and cultures. The acute care business continued optimizing for prescription volume and distribution reach. The chronic divisions focused on patient adherence, lifetime value, and specialist relationships.

This dual structure prevented the organizational antibodies that typically reject new business models. Acute care representatives weren't threatened by chronic divisions; they operated in parallel universes. Resources weren't diverted from profitable acute products to fund speculative chronic launches. The result: ALKEM maintained acute care dominance while systematically building chronic franchises.

The Biosimilar Platform Bet

The Enzene acquisition and subsequent development represents ALKEM's biggest strategic bet—not just financially but philosophically. Moving from small molecules to large molecules, from chemical synthesis to biological manufacturing, from branded generics to cutting-edge biosimilars required capabilities that couldn't be bought; they had to be built.

The strategic logic was compelling. Biosimilars offer the margin profile of innovative drugs with the market access of generics. The technical barriers limit competition to a handful of capable players. The continuous manufacturing platform provides cost advantages that even Big Pharma struggles to match. If successful, Enzene could transform ALKEM from a domestic champion to a global biotechnology player.

But execution risk was substantial. Biosimilar development costs run into hundreds of millions, with no guarantee of success. Regulatory requirements are complex and evolving. Commercial models differ fundamentally from small-molecule generics. ALKEM mitigated these risks through patience—spending years perfecting the platform before launching products—and partnerships that provided technical expertise and market access.

Innovation Through Execution

ALKEM's approach to innovation challenges conventional wisdom. Rather than pursuing novel drug discovery or breakthrough technologies, the company innovates through execution—finding new ways to manufacture, distribute, and commercialize existing molecules. This "incremental innovation" might seem mundane, but it creates sustainable competitive advantages.

Consider ALKEM's approach to pediatric formulations. While competitors offered standard suspensions that children often rejected, ALKEM invested in palatability research, developing flavors and textures that improved compliance. This wasn't patentable innovation, but it drove prescription preference among pediatricians who struggled with adherence.

Similarly, in tropical stability. ALKEM developed formulations that remained stable in India's heat and humidity without refrigeration—critical for rural distribution. Again, not breakthrough science, but solving real problems that improved patient access and outcomes.

The Family Business Advantage

Conventional wisdom suggests family-controlled businesses suffer from nepotism, short-termism, and governance challenges. ALKEM inverted these weaknesses into strengths. Family control enabled long-term thinking—investing in biosimilars with 10-year payoffs, building brands over decades, maintaining quality even when cutting corners would boost short-term profits.

The succession planning was exemplary. Rather than forcing children into leadership, the Singh family professionalized management while maintaining strategic control. They hired external talent for critical roles, created independent boards with real power, and institutionalized decision-making processes. When leadership passed to the second generation, it was based on merit and preparation, not birthright.

The family's continued ownership—maintaining 51.8% post-IPO—aligned their interests with minority shareholders. Unlike professional managers optimizing for quarterly earnings, the Singh family thought in generations. This long-term orientation enabled investments that public market pressure might have prevented.

Managing Stakeholder Complexity

ALKEM's stakeholder management reveals sophisticated understanding of Indian pharmaceutical dynamics. The company maintains distinct strategies for different stakeholders: doctors receive education and support; distributors get flexible credit terms and reliable supply; regulators see transparent compliance and proactive engagement; employees enjoy stability and growth opportunities; investors receive consistent returns without surprises.

The balance is delicate. Pushing too hard on distributor margins alienates channel partners. Excessive doctor incentives invite regulatory scrutiny. Cost-cutting that compromises quality destroys decades of trust. ALKEM navigates these tensions through clear prioritization: patient outcomes first, sustainable relationships second, short-term profits last.

Building Trust at Scale

Perhaps ALKEM's greatest achievement is building trust at industrial scale. In an industry plagued by quality scandals, spurious drugs, and ethical lapses, ALKEM maintained reputation across millions of transactions. This wasn't accident but architecture—systems designed to prevent failure rather than just detect it.

Quality control provides an example. Rather than centralized testing that creates bottlenecks, ALKEM distributed quality responsibility throughout operations. Every manufacturing unit, every batch, every step has embedded quality checks. The cost is higher, the complexity greater, but the result is consistent quality that doctors trust implicitly.

The lesson extends beyond pharma: in industries where trust determines success, investing in systems that prevent trust breaches pays exponential returns. The cost of maintaining trust is fraction of the cost of rebuilding it after failure.

These lessons from ALKEM's playbook—building brands in commoditized markets, investing in human relationships in digital ages, maintaining discipline amid opportunities, managing complexity through focused execution—apply broadly. They demonstrate that in business, as in medicine, success comes not from miraculous cures but from doing ordinary things extraordinarily well, consistently, at scale. The ALKEM way might not be glamorous, but five decades of success suggest it works.

IX. Bear vs. Bull Case

Bear Case: The Structural Headwinds

The bear case against ALKEM starts with a troubling statistic: sales growth of just 9.21% over the past five years. In an industry where double-digit growth was once table stakes, this deceleration signals deeper structural challenges that no amount of operational excellence can overcome.

The core problem is market maturation. India's pharmaceutical market, while still growing, has lost its explosive character. The easy wins—expanding coverage to untapped geographies, introducing established molecules to new patient populations—are largely exhausted. What remains is grinding market share battles where every prescription gained costs more than the last. ALKEM's dominant position in anti-infectives, rather than being an asset, becomes a burden. When you already command 15% market share in a therapeutic area, where does growth come from?

The pricing environment compounds these challenges. The Indian government's expansion of price controls under the National List of Essential Medicines (NLEM) directly impacts ALKEM's portfolio. Anti-infectives, gastrointestinals, and analgesics—ALKEM's traditional strengths—face maximum price regulations. While the company has navigated previous price controls, the cumulative effect is margin compression that operational efficiency cannot fully offset. The recent push for generic prescription by name rather than brand threatens the entire branded generics model that ALKEM pioneered.

Competition has intensified from unexpected quarters. Digital pharmacies like PharmEasy and 1mg are disintermediating traditional distribution channels, offering consumers direct access to medicines at discounted prices. These platforms promote generic alternatives to branded products, showing consumers that ALKEM's Taxim and a generic cefixime are molecularly identical. For younger, urban consumers comfortable with digital commerce, brand loyalty evaporates when presented with 30-40% savings.