Alnylam Pharmaceuticals: The RNAi Revolution

I. Introduction & Episode Setup

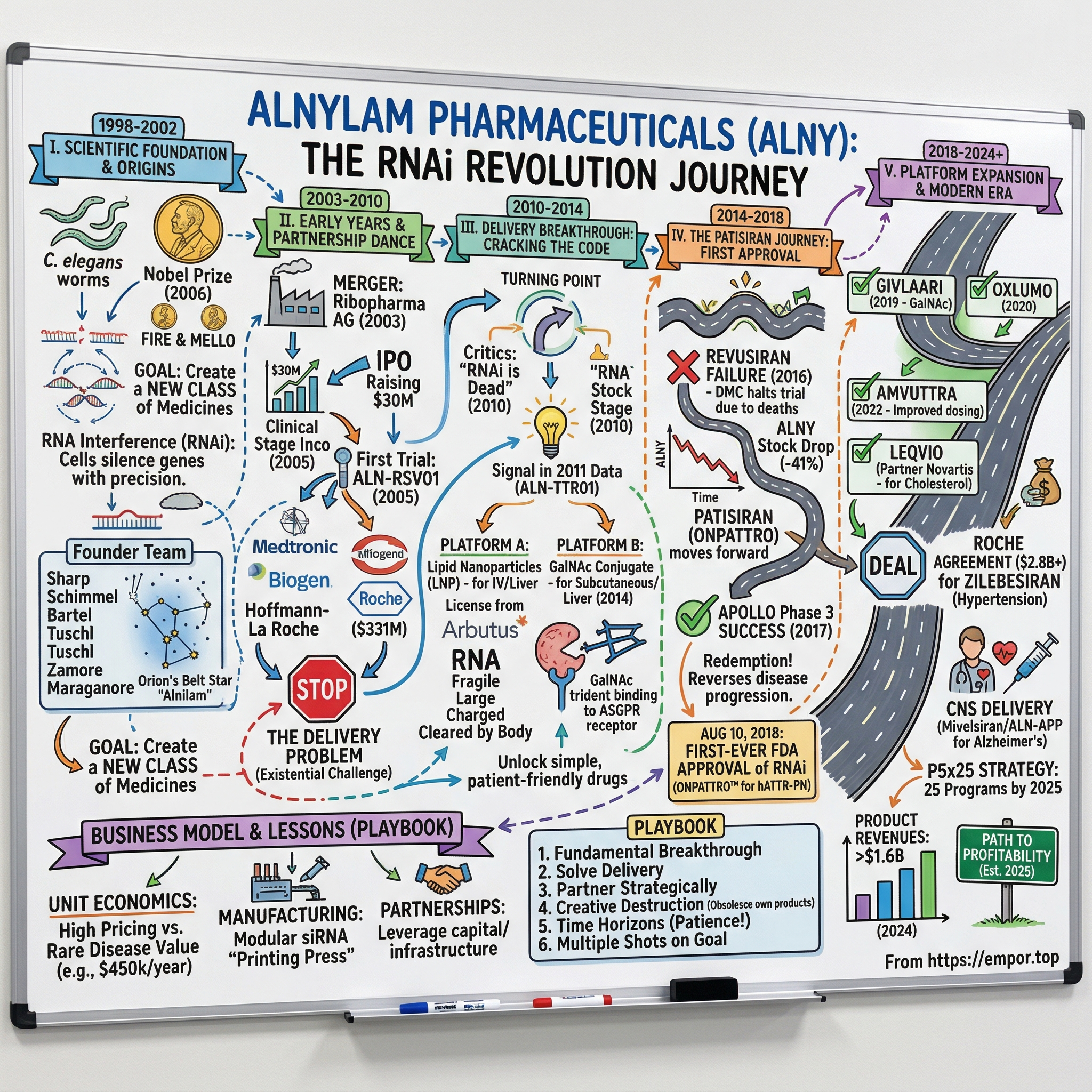

Picture this: Stockholm, December 2006. Two scientists, Andrew Fire and Craig Mello, stand before Swedish royalty to receive the Nobel Prize in Physiology or Medicine. Their discovery—RNA interference, or RNAi—had revealed one of nature's most elegant mechanisms: cells could use tiny RNA molecules to silence genes with surgical precision. In the audience, pharmaceutical executives and biotech entrepreneurs saw something else entirely: the birth of an entirely new class of medicines.

Four years earlier, in Cambridge, Massachusetts, a group of scientific luminaries had already bet their careers on this vision. Phillip Sharp, himself a Nobel laureate for discovering RNA splicing, joined forces with Paul Schimmel, David Bartel, Thomas Tuschl, and Phillip Zamore to found Alnylam Pharmaceuticals. They recruited John Maraganore, a seasoned pharma executive from Millennium Pharmaceuticals, as founding CEO. The company's name came from Alnilam, the middle star in Orion's belt—a navigational beacon that sailors had used for millennia to find their way across dark seas.

The central question wasn't whether RNAi worked—Fire and Mello had proven that. The question was whether anyone could transform this laboratory phenomenon into actual medicines. The challenge seemed almost insurmountable: how do you deliver large, charged RNA molecules across cell membranes? How do you keep them stable in the bloodstream? How do you ensure they reach the right tissues? Why this matters is remarkable: for the first time in pharmaceutical history, scientists could turn off disease-causing genes rather than treating their downstream effects. Think of it this way—traditional medicines are like mopping up water from an overflowing sink. RNAi therapeutics simply turn off the faucet. Our medicines use RNA interference to "silence" gene expression for specific proteins that have been discovered to cause or contribute to diseases. Our RNAi therapeutics act before unwanted proteins are made compared to many other classes of medicines which target proteins after they've been made.

On August 10, 2018, the Food and Drug Administration approved a landmark rare disease treatment—the first to rely on a Nobel-prize-winning technique known as RNA interference, which silences disease-causing genes. Alnylam Announces First-Ever FDA Approval of an RNAi Therapeutic, ONPATTRO™ (patisiran) for the Treatment of the Polyneuropathy of Hereditary Transthyretin-Mediated Amyloidosis in Adults. It had taken sixteen years, billions of dollars, and countless scientific breakthroughs to reach this moment. But the journey from Nobel Prize to approved medicine reveals something profound about modern drug development: sometimes the biggest innovations require not just brilliant science, but the courage to persist when everyone else has given up.

II. The Scientific Foundation & Origins (1998-2002)

The story begins not in a boardroom, but in a worm laboratory. In 1998, Andrew Fire at Stanford and Craig Mello at UMass Medical School were injecting tiny roundworms—C. elegans—with different types of RNA. What they discovered defied conventional wisdom: double-stranded RNA could silence specific genes with extraordinary precision. The worms would stop producing certain proteins entirely, as if someone had flipped a molecular switch to "off."

The implications were staggering. Every pharmaceutical company on Earth was trying to block disease-causing proteins after they were made. Fire and Mello had discovered nature's own mechanism for preventing those proteins from ever existing. Their work would win the 2006 Nobel Prize, but even before that recognition, a handful of visionaries saw the therapeutic potential.

Phillip Sharp's 1999 Genes & Development perspective sparks collaboration and experimentation among Alnylam's founders. Sharp, who had already won his own Nobel Prize in 1993 for discovering RNA splicing, published a perspective that would become the intellectual foundation for what followed. He wasn't just theorizing—he was evangelizing. Sharp began reaching out to the brightest minds in RNA biology: Paul Schimmel at Scripps, David Bartel and Phillip Zamore at UMass, and Thomas Tuschl at Max Planck.

Tuschl held the keys to the kingdom. Working in Germany, he had figured out how to make RNAi work in mammalian cells—a breakthrough that transformed Fire and Mello's worm discovery into something that could potentially treat human disease. His patents, known as Tuschl I and Tuschl II, would become the foundational intellectual property for the entire field.

In 2002, Alnylam was founded by scientists Phillip Sharp, Paul Schimmel, David Bartel, Thomas Tuschl, and Phillip Zamore, and by investors Christoph Westphal and John Kennedy Clarke; John Maraganore was the founding CEO. The company was named after Alnilam, a star in Orion's belt. The spelling was modified to make it unique.

The name choice revealed their ambition. Alnilam, the middle star in Orion's belt, has guided navigators for millennia—a steady light in the darkness. The founders saw themselves embarking on a similar journey into uncharted scientific territory. They would need that navigational metaphor; the path ahead was anything but clear.

John Maraganore brought something different to the founding team. While the scientists brought Nobel-caliber expertise, Maraganore brought battle scars from the biotech trenches. He'd been at Millennium Pharmaceuticals, watching it grow from startup to multi-billion dollar success. He understood what the scientists perhaps didn't fully grasp: turning great science into medicine requires not just brilliance, but stamina, capital, and an almost irrational persistence.

The founding vision was audacious: create an entirely new class of medicines based on RNAi. Not improve existing drugs. Not find better targets. Build something that had never existed before. While Alnylam was founded in 2002, our history began before then, when Alnylam's co-founder discovered that RNAi and siRNA could silence genes that cause disease. Since that historic discovery, Alnylam has continued to drive the RNAi Revolution® forward, pioneering a new class of medicines for patients in need.

Tuschl 1 and 2 patents in-licensed from MIT, Max Planck and Whitehead. These weren't just patents—they were the molecular blueprints for how to make small interfering RNA (siRNA) molecules that could work in human cells. Without them, RNAi therapeutics would remain a laboratory curiosity.

The scientific foundation was elegant in its simplicity, revolutionary in its implications. Our RNAi therapeutics mimic the RNA interference process by delivering specially designed small interfering RNA (siRNA) that, join with a protein complex already in the body called RISC (RNA-induced silencing complex), to target and degrade specific mRNA before they can deliver their instructions, by cleaving them like a pair of molecular scissors. But between this elegant mechanism and actual medicine lay a chasm that would take nearly two decades to cross.

III. The Early Years: Proof of Concept & Partnership Dance (2003-2010)

The year 2003 opened with a bang. In 2003, the firm merged with the German pharmaceutical company, Ribopharma AG. The newly formed company also received $24.6 million in funding from private-equity firms. This wasn't just an acquisition—it was a cultural collision. The Germans brought rigorous chemistry expertise and a methodical approach to drug development. The Americans brought Silicon Valley-style ambition and a willingness to fail fast. Maraganore had to merge not just corporate entities but scientific philosophies.

The real test came in 2004. Alnylam announced the pricing of its initial public offering of 5,000,000 shares of common stock at a price of $6.00 per share. Alnylam's common stock is expected to begin trading on May 28, 2004, on The Nasdaq National Market under the symbol "ALNY." The IPO raised approximately $30 million—decent money, but far from the war chest they'd need. The market's message was clear: prove it works before we believe.

First RNAi clinical program initiated (ALN-RSV01)—this milestone in 2005 marked the transition from laboratory to clinic. ALN-RSV01 targeted respiratory syncytial virus, a common infection that could be deadly in infants and the elderly. The drug would be delivered directly to the lungs via inhalation. It was a clever choice: local delivery avoided the biggest challenge of getting RNA molecules through the bloodstream to distant tissues.

In 2005, the company partnered with Medtronic to develop drug-device combinations to treat neurodegenerative disorders, and in 2006 with Biogen Idec to develop treatments of progressive multifocal leukoencephalopathy. In 2007, it entered into a nonexclusive alliance with Hoffmann-La Roche, in which Alnylam received $331 million in exchange for access to its technology platform.

The Roche deal was transformative—$331 million was real money that could fund years of research. But it came with strings. Roche wanted access to Alnylam's entire platform, not just specific programs. The negotiation revealed a fundamental tension: was Alnylam a product company that happened to have platform technology, or a platform company that would develop some of its own products?

Maraganore's strategy was to dance with everyone but marry no one. Each partnership brought not just capital but validation. When Medtronic signed on, it signaled that device companies saw potential. When Biogen joined, it meant neurological applications were credible. The partnership announcements became a form of scientific and commercial storytelling—each deal expanding the narrative of what RNAi could become.

But beneath the press releases lay a brutal reality: nothing was working well enough. The delivery problem wasn't just challenging—it was existential. RNA molecules are large, negatively charged, and fragile. Cell membranes are designed specifically to keep such molecules out. The body's immune system treats foreign RNA as an invader. The liver and kidneys rapidly clear RNA from circulation. Every biological system seemed designed to prevent RNAi therapeutics from working.

By 2008, the company had burned through hundreds of millions with little to show beyond proof-of-concept studies. Critics began calling RNAi the "emperor's new drugs"—beautiful science that would never translate to medicine. The 2008 financial crisis made everything worse. Biotech funding evaporated. Several competitors shut down or pivoted away from RNAi entirely.

IV. The Delivery Breakthrough: Cracking the Code (2010-2014)

The winter of 2010 marked rock bottom. Roche had terminated its partnership after spending hundreds of millions with little to show. Novartis had walked away. Merck shut down its RNAi subsidiary entirely. Industry observers began writing obituaries for the entire field. "RNAi is dead," became the refrain at biotech conferences.

Then came the data that changed everything. In 2011, Alnylam was testing ALN-TTR01, using lipid nanoparticles licensed from a Canadian company called Tekmira (later Arbutus). The initial results were noisy, disappointing. But one patient showed something remarkable—a clear RNAi signature, dramatic reduction in the target protein. Most companies would have seen failure. Maraganore saw a signal.

"Double down," he told his team. They refined the lipid formulation, optimized the ratios, tweaked the chemistry. By 2012, ALN-TTR02 was born. Alnylam Pharmaceuticals, Inc. presented clinical results from its Phase 1 clinical trial with ALN-TTR02, an RNAi therapeutic targeting transthyretin (TTR) for the treatment of TTR-mediated amyloidosis (ATTR), which utilizes Tekmira's lipid nanoparticle (LNP) technology and is manufactured by Tekmira.

Progress on that front, coupled with a 2012 licensing deal with Arbutus, finally gave Alnylam two delivery platforms from which to build its pipeline of clinical candidates around. The technology was elegant: Lipid nanoparticles (LNPs) are chemically synthesized multicomponent lipid formulations (~100 nm in size) encapsulating siRNA for delivery to the target tissue. En route to their destination, the siRNA encapsulated in LNPs are protected against degradation by ubiquitous nucleases.

Lipid nanoparticle technology licensed from Arbutus, which Alnylam uses to deliver patisiran, protects the nucleic acid molecules from degradation and helps clear passage through the cell membrane. It helps that patisiran's target, a disease known as hereditary ATTR amyloidosis, stems from a protein produced primarily in the liver. The organ, a common focus of drug development, has a large blood supply and a large proportion of anything injected into the bloodstream will end up there. With lipid nanoparticles as a delivery vehicle, Alnylam was able to get patisiran to the liver, where it could work to halt production of a protein known as TTR.

But lipid nanoparticles were only half the solution. They worked for intravenous delivery to the liver, but required pre-medication to prevent immune reactions and couldn't be self-administered. Alnylam needed something simpler, more patient-friendly.

Enter GalNAc—N-acetylgalactosamine. This sugar molecule binds specifically to receptors on liver cells called ASGPR (asialoglycoprotein receptors). The breakthrough wasn't just finding the right sugar—it was the trivalent design, three GalNAc molecules arranged like a molecular trident, binding with extraordinary affinity to liver cells. RNAi therapeutics utilizing GalNAc conjugate technology are administered subcutaneously. Our medicines GIVLAARI® (givosiran), OXLUMO® (lumasiran), AMVUTTRA® (vutrisiran), and Leqvio® (inclisiran)* utilize GalNAc conjugate delivery.

The GalNAc platform transformed everything. Suddenly, patients could inject themselves at home. The drugs lasted months in the body. Manufacturing became simpler and cheaper. By 2014, Alnylam had two viable delivery platforms and a pipeline of drugs advancing through clinical trials.

In 2014, Sanofi Genzyme acquired a 12 percent stake in Alnylam and increased its rights to several of the company's drugs for $700 million. In a separate transaction Alnylam announced that it had purchased Merck & Co.'s Sirna Therapeutics, for $25 million cash and $150 million in stock. The Sanofi deal was vindication—one of pharma's giants was betting big on RNAi again. The Sirna acquisition brought valuable intellectual property and eliminated a competitor.

V. The Patisiran Journey: First Approval (2014-2018)

The boardroom at Alnylam's Cambridge headquarters had witnessed many difficult moments, but October 5, 2016, was different. John Maraganore sat across from his leadership team, staring at data that would haunt him for years.

The DMC told Alnylam ($ALNY) that the "benefit-risk profile for revusiran no longer supported continued dosing," and the unblinded data later showed an "imbalance of mortality in the revusiran arm as compared to placebo," i.e., more patients died using revusiran than placebo. Eighteen (12.9%) patients on revusiran and 2 (3.0%) on placebo died during the on-treatment period.

The stock market's reaction was brutal and immediate. Alnylam was down 41% after hours last night when it made the shock announcement that testing of its hereditary ATTR amyloidosis med would be halted after more patients died on its treatment than on a dummy drug. Sixteen years of work, billions in investment, and the company's lead product had become toxic—literally.

"Patient safety comes first. We have stopped all dosing and are actively monitoring patients across revusiran studies to ensure their safety." Maraganore's words at the emergency investor call betrayed none of the devastation he felt. On the investor call, Maraganore was unable to detail just what had happened: "There is no current explanation for the cause of these findings, and we don't have all the answers that we would like to have and that you will ask of us."

But this wasn't Alnylam's first setback, and it wouldn't be the last. What mattered was what came next. Hidden in the company's pipeline was patisiran—using a different delivery technology, lipid nanoparticles instead of GalNAc conjugates. It had been progressing quietly through trials while revusiran grabbed headlines.

The science behind hATTR amyloidosis made it an ideal target for RNAi. The disease stems from misfolded transthyretin proteins that accumulate in nerves and organs, causing progressive damage and death within years of symptom onset. Stop the production of TTR in the liver, and you stop the disease. Simple in theory, devastating when it fails.

"All the evidence to date has been dispositive of any platform indications," he told investors at the JP Morgan event, pointing out also that revusiran was an earlier generation compound given at much higher doses than Alnylam's current programs. The company had to convince investors that revusiran's failure didn't condemn the entire platform.

Meanwhile, patisiran continued its march through the APOLLO trial—225 patients, 18 months of treatment, powered to detect even modest benefits. Unlike revusiran's GalNAc conjugate approach, patisiran used those lipid nanoparticles that had shown promise years earlier. The formulation required pre-medication and intravenous infusion every three weeks, but it worked.

September 2017 brought redemption. The APOLLO trial didn't just meet its primary endpoint—it demolished it. Patients on patisiran showed improvement in neuropathy scores while placebo patients deteriorated. Quality of life improved. Walking speed increased. The drug was actually reversing disease progression, not just slowing it.

Success of the trial, called APOLLO, spurred a 50% jump in the biotech's stock price, and is the first successful Phase 3 study for an RNAi drug. "Reaching this point, however, has taken Alnylam 15 years and more than $1.6 billion in R&D investment."

The path to approval accelerated. Alnylam filed with the FDA in December 2017, received priority review, and then came August 10, 2018—the day that changed everything.

VI. Platform Expansion & The GalNAc Era (2018-2021)

The approval of ONPATTRO in August 2018 wasn't an endpoint—it was a starting gun. Within 16 months, Alnylam would transform from a one-drug company to a multi-product powerhouse, each approval validating different aspects of the platform.

November 2019 brought the second act. FDA approval of GIVLAARI was received in less than four months after acceptance of the NDA. "GIVLAARI now becomes our second RNAi therapeutic to be approved in the last 16 months, and the world's first-ever GalNAc-conjugate RNA therapeutic to be approved, representing a watershed moment for a technology uniquely pioneered by Alnylam scientists."

GIVLAARI (givosiran) targeted acute hepatic porphyria, a devastating genetic disease causing excruciating abdominal pain attacks. In ENVISION, AHP patients on GIVLAARI experienced 70% (95% CI: 60%, 80%) fewer porphyria attacks compared to placebo. The drug proved GalNAc conjugates could work—subcutaneous injection, no pre-medication, targeting the liver with precision.

The momentum accelerated. The FDA approved Oxlumo for the treatment of PH1 to lower UOx levels in pediatric and adult patients in November 2020. OXLUMO (lumasiran) tackled primary hyperoxaluria type 1, a rare disease causing kidney stones and renal failure in children. Each approval expanded the addressable patient population and proved RNAi could treat different genetic defects.

But the real game-changer came with AMVUTTRA (vutrisiran), approved in 2022. This was patisiran 2.0—same disease, better drug. Using GalNAc conjugates instead of lipid nanoparticles meant subcutaneous injection every three months instead of intravenous infusion every three weeks. No pre-medication. Patient convenience transformed.

The increases are primarily due to growth from sales of AMVUTTRA driven by increased patient demand, partially offset by a decrease in sales of ONPATTRO due to patient switches to AMVUTTRA. The cannibalization was intentional—Alnylam was betting that a better patient experience would expand the total market, not just redistribute existing patients.

The chemistry breakthrough behind this expansion was ESC+—Enhanced Stabilization Chemistry Plus. Earlier siRNA molecules degraded quickly, requiring frequent dosing. ESC+ made the molecules more stable, extending duration to months. Some experimental drugs were showing activity for six months or even a year after a single dose.

Meanwhile, the validation of lipid nanoparticle technology had unexpected consequences. When COVID-19 struck, Pfizer-BioNTech and Moderna used LNP technology—the same basic approach Alnylam had pioneered—to deliver mRNA vaccines. Eventually, Alnylam developed the first lipid nanoparticles (LNPs) that could be used to encase RNA and deliver it into patient cells. LNPs were later used in the mRNA vaccines for Covid-19. The pandemic turned the world into inadvertent evangelists for RNA delivery technology.

The business model evolved with the pipeline. Achieved global net product revenues for GIVLAARI and OXLUMO for the fourth quarter of ... $33 million, respectively, representing 11% total Ultra-Rare quarterly growth compared to Q3 2023, and full year 2023 revenues of ... $110 million, respectively, representing 35% total Ultra-Rare annual growth compared to full year 2022. Each drug targeted a different rare disease, but shared manufacturing, regulatory expertise, and commercial infrastructure.

By 2021, Alnylam had five approved drugs, with a sixth—Leqvio (inclisiran) for cholesterol—approved through partner Novartis. On December 22, 2021, Novartis announced that the US Food and Drug Administration (FDA) approved Leqvio (inclisiran), a small interfering RNA (siRNA) therapy to lower low-density lipoprotein cholesterol. Leqvio is indicated in the United States as an adjunct to diet and maximally tolerated statin therapy for the treatment of adults with clinical atherosclerotic cardiovascular disease (ASCVD) or heterozygous familial hypercholesterolemia (HeFH) who require additional lowering of LDL-C. The Leqvio approval marked a crucial transition—from ultra-rare diseases affecting hundreds to prevalent conditions affecting millions.

VII. The Roche Deal & Hypertension Moonshot (2022-2024)

July 24, 2023, marked a watershed moment in Alnylam's evolution. Teresa Graham, Roche's pharmaceutical division chief, had flown to Cambridge with a team of executives. The Swiss pharma giant, one of the world's largest with 104,000 employees and a history dating to 1896, was about to make a massive bet on RNAi.

Alnylam Pharmaceuticals, Inc. (Nasdaq: ALNY), the leading RNAi therapeutics company, today announced it has entered into a strategic agreement with Roche to develop and commercialize zilebesiran, Alnylam's investigational RNAi therapeutic for the treatment of hypertension, which is currently in Phase 2 of development. The terms were staggering: Receive Development, Regulatory, and Sales Milestones, Including Substantial Near-Term Milestones, for a Potential Deal Value of up to $2.8 Billion, as well as an Equal Share of Profits and Losses in the United States and Royalties on Net Sales Outside the.

Zilebesiran represented something revolutionary—not just another blood pressure medication, but a fundamental reimagining of how to treat the world's most prevalent cardiovascular condition. Roche has a proven history of innovating and commercializing medicines building upon their extensive global footprint which may potentially enable zilebesiran to reach more patients with hypertension, a disease that affects more than 1.2 billion patients globally.

The science behind zilebesiran was elegant. Zilebesiran is an RNAi drug developed by Alnylam that targets liver-expressed angiotensinogen (AGT), and is currently in Phase II development. Zilebesiran is comprised of a small interfering RNA (siRNA) covalently linked to an N-acetyl galactosamine (GalNAc) ligand, which can bind specifically to protein receptors expressed on the surface of liver cells, thus achieving precise delivery.

Unlike approved treatments for hypertension that require patients to take daily pills, the experimental medicine is given as an injection every few months. A study published last week in the New England Journal of Medicine found that zilebesiran's benefits lasted over 24 weeks in an early-stage trial, raising the possibility that a shot could be administered twice a year.

The KARDIA clinical program would test whether this bold vision could become reality. The two higher doses of zilebesiran being trialed, 300 mg and 600 mg, both produced a more than 15-mmHg mean reduction in 24-hour systolic blood pressure (SBP) after three months compared to placebo, hitting the primary endpoint of the 394-adult KARDIA-1 trial.

"We are thrilled to announce this collaboration, as it combines Alnylam's proven track record in RNAi therapeutics with Roche's global commercial reach, commitment to innovation and desire to transform the landscape for patients with severe cardiovascular diseases," said Yvonne Greenstreet MBChB, Chief Executive Officer of Alnylam. "With this collaboration, we now can develop zilebesiran in a more robust way," specifically by having cardiovascular outcomes data available at the time of a potential launch.

The strategic brilliance of the deal lay in its structure. The new partnership gives the Swiss pharma full ex-U.S. rights to the drug and co-U.S. rights alongside Alnylam, in exchange for the $310 million plus up to $2.8 billion in potential milestone payments. The two companies will co-commercialize and split profits of the drug in the U.S., according to Monday's announcement. Alnylam will lead the joint development of the asset through its first indication, currently listed as hypertension, with both companies splitting costs.

Think about the market dynamics: More than one billion people worldwide live with hypertension.1 In the U.S. alone, approximately 47 percent of adults live with hypertension, with more than half of patients on medication remaining above the blood pressure (BP) target level. Almost half of patients with high blood pressure aren't able to lower it to target levels with current medicines, according to the journal. Despite lifestyle changes and several classes of drugs, Alnylam says on its website, fewer than 20 percent of people with hypertension have it under control.

The challenge wasn't just medical—it was behavioral. Medication adherence for hypertension is notoriously poor. Patients feel fine, so they skip doses. Side effects accumulate. Pills pile up. But an injection twice a year? That changes the entire treatment paradigm.

March 2024 brought further validation. The KARDIA-2 study enrolled 672 adults with mild to moderate hypertension who received either a 600-mg dose of the RNAi therapeutic zilebesiran or placebo on top of one of three approved hypertension meds—namely Pfizer's Norvasc, Daiichi Sankyo's Benicar or indapamide. Patients who received zilebesiran added to one of these standard-of-care meds "experienced a clinically and statistically significant reduction in systolic blood pressure" when assessed by 24-hour ambulatory blood pressure monitoring at a three-month assessment, Roche said in a March 5 release.

VIII. Modern Era: Pipeline & Platform Evolution (2024-Present)

The numbers tell a story of transformation at scale. "2024 was another year of impressive execution for Alnylam, generating product revenues of over $1.6 billion, reflecting growth of 33% compared to 2023." Net product revenues increased 30% and 33% at actual currency during the three and twelve months ended December 31, 2024, respectively, compared to the same periods in 2023.

The growth engine was AMVUTTRA. Achieved global net product revenues for ONPATTRO and AMVUTTRA for the fourth quarter of $56 million and $287 million, respectively, and $343 million combined, representing 35% total TTR growth compared to Q4 2023, and full year 2024 revenues of $253 million and $970 million, respectively, and $1,223 million combined, representing 34% total TTR growth compared to full year 2023.

But the modern era isn't just about financial metrics—it's about platform evolution. The increases are primarily due to growth from sales of AMVUTTRA driven by increased patient demand, partially offset by a decrease in sales of ONPATTRO due to patient switches to AMVUTTRA, as well as increased patients on GIVLAARI and OXLUMO therapies. The controlled cannibalization strategy was working exactly as planned.

The pipeline has become a hydra—cut off one program, two more emerge. "Furthermore, driven by our proven RNAi platform, we anticipate 2025 will bring major advancements in our pipeline and expect to have over 25 high-value programs in the clinic across diverse indications by the end of the year." The Alnylam P5x25 strategy—25 programs by 2025—represents ambition at industrial scale.

The most exciting frontier is CNS delivery. Today announced positive initial results from the multiple dose portion of the Phase 1 study of mivelsiran in patients with Alzheimer's disease. For two decades, the brain had been off-limits to RNAi therapeutics. The blood-brain barrier, evolution's fortress protecting our most vital organ, also blocked therapeutic RNA molecules. But using C16 conjugates and intrathecal delivery, Alnylam cracked the code.

ALN-APP, our investigational RNAi therapeutic targeting amyloid precursor protein in Phase 1 development (in collaboration with Regeneron Pharmaceuticals) for the treatment of Alzheimer's disease and cerebral amyloid angiopathy, utilizes C16 conjugate technology. ALN-APP is administered intrathecally (via an injection into the spinal cord). The implications are staggering—suddenly, neurodegenerative diseases from Alzheimer's to Huntington's become targetable.

The commercial performance reflects sophisticated market segmentation. Approximately 5.0% of the 21.6% of cost of goods sold as a percentage of net product revenues for the year ended December 31, 2023 was attributable to cancelled manufacturing commitments and the impairment of ONPATTRO inventory. These one-time charges in 2023 did not recur in 2024, resulting in the decrease in cost of goods sold as a percentage of net product revenues in 2024.

Competition has intensified. Ionis Pharmaceuticals, the antisense oligonucleotide pioneer, competes directly in several indications. Arrowhead Pharmaceuticals focuses on its own RNAi platform. Dicerna, before its acquisition by Novo Nordisk, was developing competing GalNAc conjugates. But Alnylam's first-mover advantage in approved drugs creates a flywheel effect—revenues fund research, research creates new drugs, new drugs generate more revenues.

The strategic positioning for 2025 reveals confidence. We expect 2025 will represent an important inflection point for our TTR franchise, with the potential launch of vutrisiran in ATTR-CM delivering significant topline growth as reflected in our net product sales guidance announced today. If we are successful in meeting this product revenue guidance, we anticipate achieving non-GAAP profitability in 2025.

IX. Business Model & Unit Economics

The journey from startup to profitability spans 22 years and approximately $2.5 billion in cumulative investment—a testament to both the difficulty of platform development and the patience of Alnylam's investors. Understanding the unit economics requires peeling back layers of complexity.

Start with pricing. ONPATTRO launched at approximately $450,000 per patient per year—shocking to health economists but rational when you consider the alternative: progressive nerve damage, disability, and death within 5-10 years. GIVLAARI and OXLUMO command similar prices for their ultra-rare indications. These aren't lifestyle drugs; they're the only options for desperate patients.

The pricing strategy reflects a sophisticated understanding of value-based healthcare. For a patient with hATTR amyloidosis, the alternative to ONPATTRO or AMVUTTRA isn't another drug—it's liver transplantation costing over $800,000 with significant mortality risk. Suddenly, $450,000 annually for a subcutaneous injection seems reasonable.

Manufacturing presents unique challenges and opportunities. Unlike small molecule drugs produced through chemical synthesis, RNAi therapeutics require complex biological manufacturing. The good news: once you've built the platform, making different siRNA molecules uses the same basic process. It's like having a printing press where changing the content requires only changing the template, not rebuilding the entire machine.

The partnership economics reveal strategic brilliance. The Roche deal alone—$310 million upfront, up to $2.8 billion in milestones—validates the platform while sharing development risk. Sanofi's earlier $700 million investment provided crucial capital during the lean years. Novartis commercializes Leqvio, generating royalties without Alnylam bearing commercial costs.

Think about the leverage in this model: Alnylam develops the core technology, partners handle much of the commercial infrastructure in specific territories or indications, and both share the upside. It's capital-efficient for a company that spent its first sixteen years burning cash.

The path to profitability accelerated dramatically with AMVUTTRA. Cost of goods sold as a percentage of net product revenues decreased during the twelve months ended December 31, 2024, indicating improving margins as volumes scale. The company projects non-GAAP operating profitability in 2025—a remarkable achievement for a company that lost $650 million as recently as 2020.

The royalty obligations create a complex web. Alnylam pays royalties to MIT, Max Planck, and others for foundational patents. It receives royalties from partners like Novartis. The company pays milestones to Arbutus for LNP technology while receiving milestones from Roche for zilebesiran. It's financial engineering meets molecular engineering.

X. Playbook: Lessons for Platform Companies

The Alnylam story offers a masterclass in building platform companies, with lessons that extend far beyond biotech.

Lesson 1: Build Around Fundamental Breakthroughs You can't fake platform technology. Fire and Mello's Nobel Prize wasn't just validation—it was proof of a fundamental biological mechanism. Alnylam didn't try to incrementally improve existing drugs; they built an entirely new modality. The lesson: platforms require genuine technical discontinuity.

Lesson 2: The Delivery Problem Is The Business Problem For over a decade, RNAi's potential was obvious but unrealizable because RNA molecules couldn't reach their targets. Alnylam's journey from 2002 to 2018 was essentially solving one problem: delivery. Over 80% of R&D investments went toward delivery efforts, with dozens of systems assessed and discarded in first decade. The breakthrough with LNPs and GalNAc conjugates unlocked everything else.

Lesson 3: Partner Strategically, But Keep The Core Alnylam's partnership dance—Roche, Sanofi, Novartis, Regeneron—provided capital and validation while maintaining control of the platform. They licensed products, not the underlying technology. Each deal expanded capabilities without diluting the core value. Compare this to companies that sell themselves too early or give away fundamental IP.

Lesson 4: Embrace Creative Destruction When AMVUTTRA began cannibalizing ONPATTRO sales, Alnylam didn't resist—they accelerated it. They understood that protecting yesterday's products at the expense of tomorrow's platform is a death spiral. The willingness to obsolete your own products before competitors do is crucial for platform longevity.

Lesson 5: Clinical Failures Are Data, Not Defeats The revusiran disaster could have ended Alnylam. Eighteen deaths, stock price collapse, existential questions about the platform's safety. But they treated it as data: what went wrong, what can we learn, how do we prevent recurrence? The investigation showed the issue was drug-specific, not platform-wide. That analytical rigor saved the company.

Lesson 6: Time Horizons Matter Sixteen years to first approval. Twenty-two years to profitability. Most investors can't handle these timescales. Alnylam succeeded because it attracted investors who understood platform development timelines. The lesson: match your capital sources to your development timeline, or you'll face impossible pressure to show premature results.

Lesson 7: Multiple Shots On Goal With 25+ programs in development, Alnylam has derisked the platform. Any individual program can fail without threatening the company. This portfolio approach—enabled by platform modularity—transforms drug development from binary bets to statistical probabilities.

XI. Analysis & Investment Case

The Bull Case: Alnylam sits at an inflection point where platform validation meets commercial scale. With six approved drugs generating $1.6 billion in revenues growing 33% annually, the company has achieved what decades of RNAi companies couldn't: turning Nobel Prize science into profitable medicine.

The ATTR-CM opportunity alone could double the company's revenue. With FDA approval expected in March 2025, AMVUTTRA would address a market 10x larger than ATTR-PN. Cardiomyopathy affects approximately 40,000 patients in the U.S. versus 3,000 for polyneuropathy. At current pricing, that's a $15+ billion market opportunity.

Zilebesiran represents a step-change in ambition. Moving from thousands of rare disease patients to millions with hypertension transforms Alnylam from niche player to pharmaceutical giant. With Roche's commercial muscle and twice-yearly dosing, zilebesiran could capture significant share of the $30+ billion hypertension market.

The platform advantages compound over time. Each approved drug validates the technology, making regulatory approval easier for subsequent programs. Manufacturing economies of scale reduce per-unit costs. Commercial infrastructure leverages across multiple products. It's the biotech equivalent of software's zero marginal cost.

The Bear Case: Competition is intensifying across every indication. Ionis has competing drugs approved or in development. Arrowhead claims superior delivery technology. Big pharma is either partnering with or acquiring RNAi companies. Alnylam's first-mover advantage erodes with each competitor approval.

Patent cliffs loom. The foundational Tuschl patents have already expired. LNP patents from Arbutus create ongoing royalty obligations and potential disputes. GalNAc conjugate patents will eventually expire, opening the technology to generics or biosimilars. Unlike small molecules where formulation changes can extend patent life, RNAi sequences are harder to modify without losing efficacy.

The delivery problem isn't fully solved. Despite breakthroughs, RNAi therapeutics still primarily target the liver. CNS delivery requires invasive intrathecal injection. Lung, kidney, and tumor delivery remain challenging. Each new tissue requires essentially starting over on delivery technology.

Pricing pressure will intensify as RNAi moves from ultra-rare to common diseases. Charging $450,000 annually for 3,000 patients is one thing; maintaining premium pricing for millions with hypertension is another. Payers will demand value demonstration, outcomes-based contracts, and competitive bidding.

Technology Moats and Defensibility: Alnylam's moat consists of multiple layers: deep expertise in siRNA design, proprietary delivery platforms, manufacturing know-how, regulatory expertise, and commercial infrastructure. But none are insurmountable. The core science is published, delivery technologies can be licensed or circumvented, and manufacturing can be outsourced.

The real moat is integration and execution. Alnylam has spent 22 years learning what doesn't work—knowledge that's hard to replicate. They've built relationships with regulators, payers, and physicians. They understand the subtleties of siRNA chemistry that determine success versus failure. It's tacit knowledge that can't be easily transferred.

Financial Trajectory: The path to sustainable profitability seems clear. Product revenues growing 30%+ annually, approaching $2 billion by 2025. Operating leverage increasing as platform costs spread across more products. The question isn't whether Alnylam becomes profitable, but how profitable.

XII. Looking Forward

The next decade will determine whether RNAi fulfills its revolutionary promise or remains a niche technology for rare diseases. The scientific challenges are substantial but surmountable. Oral delivery—the holy grail that would make RNA drugs as convenient as traditional pills—remains elusive but not impossible. Advances in ligand chemistry and nanoparticle engineering inch closer to this goal.

CNS penetration opens vast new territories. Alzheimer's, Parkinson's, Huntington's, ALS—diseases that have resisted decades of drug development become theoretically tractable with RNAi. The challenge isn't just delivery but selecting the right targets in complex neurodegenerative cascades.

The combination with gene editing technologies like CRISPR creates intriguing possibilities. RNAi for temporary gene silencing, CRISPR for permanent correction—together they could address genetic diseases from multiple angles. Alnylam's expertise in delivery could prove valuable for getting CRISPR components into cells.

The expansion into prevalent diseases will test everything. Can Alnylam maintain premium pricing? Will twice-yearly dosing overcome patient adherence challenges? Can they compete with entrenched pharma giants in primary care markets? The answers will determine whether Alnylam becomes a $100 billion company or remains a successful niche player.

Success by 2030 looks like this: 15-20 approved drugs across rare and common diseases. Annual revenues exceeding $10 billion. RNAi established as the third major drug modality alongside small molecules and antibodies. Delivery to most tissues solved. Oral formulations in late-stage development. The platform spawning entirely new approaches to previously intractable diseases.

The broader implications extend beyond Alnylam. If RNAi succeeds at scale, it validates the entire nucleic acid therapeutics field—antisense, mRNA, gene therapy. It proves that complex biological mechanisms can be harnessed as medicines. It opens the door to treating disease at the genetic level rather than symptomatic level.

The story that began with worms and wonder in 1998 has become one of modern medicine's most important narratives. Whether it ends with transformation or disappointment depends on execution, innovation, and a bit of luck. But after 22 years, $2.5 billion invested, and six drugs approved, betting against Alnylam seems increasingly risky.

What started as a star in Orion's belt—a navigational beacon for ancient mariners—has become a lodestar for modern medicine. The journey from Nobel Prize to commercial success took two decades, but the destination was worth the voyage. For patients with previously untreatable diseases, for investors who stayed the course, and for science itself, Alnylam represents something profound: proof that audacious scientific bets, pursued with persistence and precision, can change the world.

The RNAi revolution isn't coming. It's here.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube