Merus N.V.: The Bispecific Antibody Pioneer

How a Dutch Biotech Built the Platform That Rewrote Cancer Treatment—And Earned an $8 Billion Exit

I. Introduction: The Twenty-Year Overnight Success

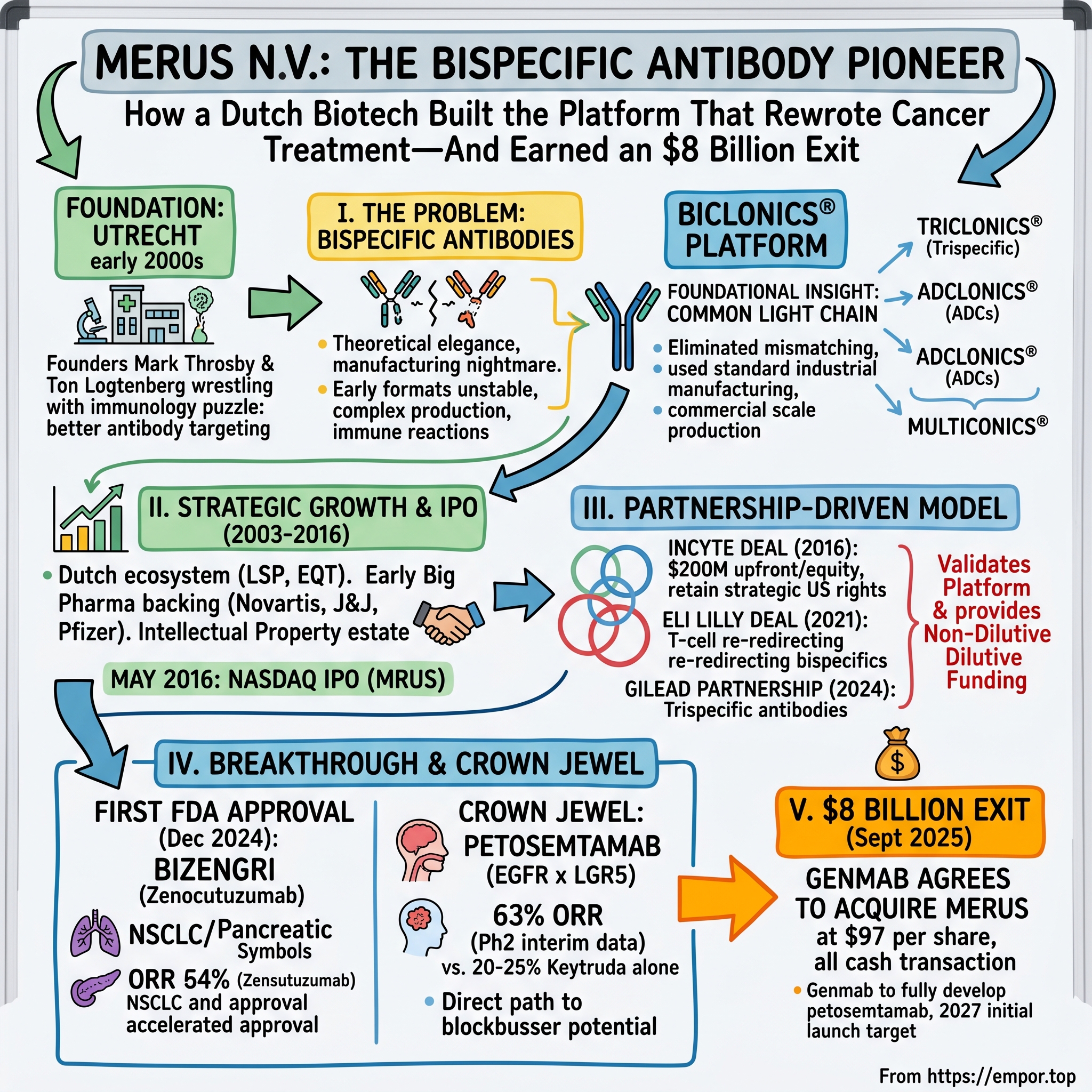

Picture Utrecht in the early 2000s: a medieval Dutch city of winding canals and towering church spires, home to the Netherlands' largest university and an unexpectedly fierce biotech scene. In an unremarkable laboratory building on Uppsalalaan, a handful of scientists were wrestling with one of immunology's most vexing puzzles—how to build a better antibody.

The human immune system produces antibodies with exquisite precision, each one designed to target a single enemy. But what if you could create an antibody that hits two targets at once? It sounds elegant in theory. Bispecific antibodies reduce the likelihood of unintended effects on healthy cells that express only one of the two targets, because the monovalent binding by one arm of the bispecific antibody alone has no functional consequences. In practice, it was a manufacturing nightmare. Earlier bispecific formats produced unstable molecules, required exotic production methods, and often triggered dangerous immune reactions.

Merus N.V. was founded in 2003 by Mark Throsby and Ton Logtenberg in Utrecht, the Netherlands. The company was established with the vision of developing innovative bispecific antibody therapeutics for the treatment of cancer. What followed was two decades of patient platform-building, scientific pivots, near-death experiences, partnership deals worth billions in potential milestones, and ultimately, one of the largest European biotech acquisitions in history.

In September 2025, Genmab agreed to acquire Merus for USD 97.00 per share in an all-cash transaction representing a transaction value of approximately USD 8.0 billion. This was one of the largest acquisitions of a European biotech company to date.

The Merus story is fundamentally about platform versus product thinking in biotech—how building a technology engine that generates multiple candidates can be more valuable than betting everything on a single drug. It's about the Dutch biotech advantage: world-class academic science, favorable regulatory environments, and a talent pool that punches far above its weight. Most importantly, it's about timing: knowing when to partner, when to retain rights, and when to sell.

II. The Science Foundation: Understanding Bispecific Antibodies

Before understanding Merus's triumph, you need to understand why bispecific antibodies matter—and why they were so hard to make.

Traditional monoclonal antibodies revolutionized cancer treatment starting in the 1990s. Drugs like Herceptin (trastuzumab) showed that you could target specific proteins on tumor cells and achieve remarkable therapeutic effects. But cancer is cunning. Tumors evolve resistance. They downregulate target proteins, activate bypass pathways, and hide from single-agent therapies.

Unlike standard monoclonal antibodies, which generally target a single antigen, bispecific antibodies have unique capabilities by engaging several targets, allowing for innovative therapeutic modes of action and improved efficacy in treating various disorders.

The most exciting application is T-cell engagement. Bispecific antibodies are bioengineered molecules designed to simultaneously recognize and bind to two different antigens or epitopes. Unlike monoclonal antibodies that target a single antigen, bispecific antibodies can link a disease-related antigen (such as one found on cancer cells) to another molecule—often a T-cell—thus redirecting immune cells to attack malignant tissues with heightened precision.

But there was a fundamental engineering problem. Antibodies are composed of two heavy chains and two light chains. When you try to produce a bispecific—which needs different heavy and light chains on each arm—you get a statistical mess of mismatched pairs. Early bispecific formats were either small fragments with poor pharmacokinetics, required complex chemical linking steps, or had manufacturing yields so low that commercial production was impractical.

Merus uses a suite of proprietary technologies to generate its Biclonics bispecific antibodies, which have a full-length IgG format that retains the favorable features associated with conventional mAbs, such as a long half-life, low immunogenicity, and use of the standard process for mAb manufacturing. The proprietary transgenic mouse MeMo is used to generate large panels of diverse and high-quality human antibodies characterized by a common light chain.

The "common light chain" was Merus's foundational insight. Merus overcomes the potential for mispairing during the generation of bispecific antibodies by combining common light chain antigen-binding fragment (Fab) regions with CH3 electrostatic engineering in the crystallizable fragment (Fc) region to efficiently drive the formation of the heterodimer.

In practical terms, this means Merus could use standard industrial manufacturing—the same equipment, the same processes, the same quality controls used for regular monoclonal antibodies—to produce full-length bispecifics at commercial scale. This was a massive competitive advantage that would prove decisive.

The global bispecific antibodies market size was valued at USD 5.51 billion in 2024 and is projected to grow from USD 6.58 billion in 2025 to USD 20.14 billion by 2033, growing at a CAGR of 15.49% during the forecast period. Some estimates are even more aggressive, with projections reaching hundreds of billions by the mid-2030s. Merus positioned itself at the center of this explosion.

III. Founding & Early Years: The Academic-to-Commercial Transition (2003–2015)

Ton Logtenberg was not a first-time founder. He was the founder and CEO of U-BiSys, a Dutch biotechnology company that merged with Introgene to become Crucell N.V., serving as its Chief Scientific Officer. Crucell was acquired by Johnson & Johnson for $2.4 billion in 2011. That exit gave Logtenberg both capital and credibility to pursue his next venture.

The founding team included key scientists and entrepreneurs: Ton Logtenberg, Mark Throsby, Alexander B. M. Brinkman, Victor Schut, and Hans van Eenennaam. Their expertise in antibody engineering was central to the company's creation.

Before joining Merus, Mark Throsby was Director Antibody Discovery at Crucell NV, where he was responsible for initiation of projects in viral and bacterial diseases leading to successful clinical development programs and licensing deals. The Crucell connection was more than coincidental—it represented a transfer of institutional knowledge about how to build antibody therapeutics from idea to clinic.

Merus' founding technology was based on the development of full-length human IgG bispecific antibodies, which would later evolve into their proprietary Biclonics® platform. This platform was designed to overcome the manufacturing challenges and structural limitations of earlier bispecific antibody formats.

In its early years, Merus focused on building its technological foundation and securing initial funding. The company raised its first significant venture capital in 2006, followed by additional financing rounds to support its growing pipeline.

A key early round was the Series A financing in 2007, which raised €14.5 million (approximately $19 million at the time), enabling the advancement of its proprietary Biclonics® technology platform. This was substantial seed capital for a European biotech at the time, reflecting investor confidence in both the science and the team.

LSP co-led the Series B financing of Merus in 2010 and actively supported the company in further financings in subsequent years. The Dutch life sciences investment ecosystem—led by LSP, EQT Life Sciences (formerly part of LSP), and others—would prove crucial to Merus's development. EQT Life Sciences has been an investor in Merus since 2010, supporting the Company at board level in its growth from a start-up company to a NASDAQ-listed clinical-stage biotech with multiple late-stage oncology assets.

By 2010, Merus had established its core Biclonics® technology platform and began advancing its first candidates toward clinical development.

The early validation came from partners, not products. The cancer specialist listed Novartis, Johnson & Johnson and Pfizer among its largest investors. When Big Pharma puts money into your company, it signals confidence in your technology. But it also creates a complicated dynamic: these same companies might become competitors, partners, or acquirers.

Patent protection was essential. The company built an extensive intellectual property estate around its core innovations—not just the antibodies themselves, but the methods for generating, screening, and manufacturing them. This patent portfolio would become a key asset in every partnership negotiation.

IV. The IPO & Strategic Pivot (2016)

By 2015, Merus had a proven platform and early-stage candidates but needed capital for the expensive clinical trials ahead. The company initially targeted a $100 million IPO.

Utrecht, the Netherlands-based Merus first talked up the prospect of a Nasdaq IPO during the go-go month of April 2015. At that time, the $100 million it was aiming for was on the low side of the sums being proposed and raised by fellow oncology biotechs.

But biotech markets are notoriously fickle. By the time Merus formalized its plan to go public in October, the tide had turned, leaving a clutch of biotechs on the outside looking in through the then-closed IPO window.

The company showed financial discipline. Having raised €72.8 million in a private round in August, Merus was better equipped than some to ride out the downturn in sentiment toward biotech.

On May 19, 2016, Merus was successfully listed on the NASDAQ stock exchange after the pricing of 5.5 million new shares at $10.00 per share, successfully raising $55 million in an initial public offering. The stock traded under the symbol "MRUS."

In honor of the occasion, Ton Logtenberg, Ph.D, Chief Executive Officer, rang the Closing Bell at the Nasdaq MarketSite in Times Square.

LSP was very proud that Merus succeeded in the current challenging market conditions to raise significant capital from a very strong group of leading investors and was one of the few European biotech companies that successfully achieved a listing on NASDAQ.

Merus had commitments from existing institutional investors to buy $32.5 million of the IPO shares. Bay City Capital, Aglaia Oncology Fund, Sofinnova Venture Partners, Novo A/S and LSP sat alongside the Big Pharma trio on the list of Merus' main investors.

The reduced raise was actually a strategic pivot. Instead of trying to fund everything internally, Merus would leverage partnerships to advance programs while retaining rights to its most promising assets. This hybrid model—platform plays generating partnership revenue while wholly-owned programs potentially generate blockbuster returns—would define the company's strategy for the next decade.

The strategic Nasdaq IPO in 2016 provided essential capital to advance multiple candidates into and through clinical trials simultaneously. It increased visibility and offered liquidity, crucial steps for a development-stage biotech company.

V. The Partnership-Driven Model & Key Inflection Points (2016–2021)

Just seven months after the IPO, Merus secured a deal that transformed its financial position.

The Incyte Deal (December 2016)

On December 21, 2016, Incyte Corporation and Merus N.V. announced that they have entered into a global, strategic collaboration agreement focused on the research, discovery and development of bispecific antibodies utilizing Merus' proprietary Biclonics® technology platform.

Under the terms of the collaboration, Incyte agreed to pay Merus an upfront payment of $120 million. In addition, Incyte agreed to purchase 3.2 million shares of Merus stock at $25 per share, for a total equity investment of $80 million. The parties agreed to collaborate on the development and commercialization of up to 11 bispecific antibody programs.

That's $200 million for a company that had raised $55 million in its IPO just months earlier. The deal validated the platform and provided non-dilutive funding for years of R&D.

The Collaboration and License Agreement grants Incyte the exclusive rights for up to eleven bispecific antibody research programs, including two of Merus current preclinical immuno-oncology discovery programs.

Critically, Merus retained strategic rights. For one current preclinical program, Merus will retain all rights to develop and commercialize approved products in the United States, and Incyte will develop and commercialize approved products arising from the program outside the United States.

"By virtue of a unique ability to simultaneously engage multiple protein targets, we believe bispecific antibodies have the potential to play an important role in the future of biotherapeutics," said Reid Huber, Ph.D., Incyte's Chief Scientific Officer. "This collaboration with Merus expands our large molecule discovery capabilities into an innovation-rich area of research."

The Ono Pharmaceutical Partnership

In April 2014, Merus and Ono entered into a research and license agreement to jointly develop bispecific antibody therapies for undisclosed targets. Ono received worldwide exclusive rights to develop, manufacture, and commercialize the resulting products developed through the collaboration. Merus received an upfront payment, and is eligible to receive milestones and sales royalties.

In March 2018, Ono exercised its option under the April 2014 agreement to enter into a new research and license agreement utilizing Merus proprietary Biclonics® technology platform to generate a bispecific antibody that binds to a combination of targets.

The Eli Lilly Deal (January 2021)

Loxo Oncology at Lilly, a research and development group of Eli Lilly and Company, and Merus N.V., announced a research collaboration and exclusive license agreement that will leverage Merus' proprietary Biclonics® platform along with the scientific and rational drug design expertise of Loxo Oncology at Lilly to research and develop up to three CD3-engaging T-cell re-directing bispecific antibody therapies. Under the terms of the agreement, Merus will lead discovery and early stage research activities while Loxo Oncology at Lilly will be responsible for additional research, development and commercialization activities. Merus received an upfront cash payment of $40 million, as well as an equity investment by Lilly of $20 million in Merus common shares.

Merus is also eligible to receive up to $540 million in potential development and commercialization milestones per product, for a total of up to approximately $1.6 billion for three products, as well as tiered royalties ranging from the mid-single to low-double digits on product sales.

"The collaboration with Loxo Oncology at Lilly and their world class research capabilities opens up exciting possibilities for Merus' Biclonics® platform," said Bill Lundberg, MD., President and Chief Executive Officer at Merus. "Our CD3 T-cell engager platform includes over 175 novel and diverse anti-CD3 common light chain antibodies across a wide range of affinities and attributes and enables functional screening of large libraries for optimal performance."

The pattern across these deals was consistent: Merus provided platform access and early-stage research capabilities, partners provided capital and late-stage development/commercialization expertise. Merus retained strategic rights where possible and always protected its most advanced wholly-owned programs.

VI. Platform Evolution: From Biclonics to Multiclonics

While partnership deals generated non-dilutive funding, Merus continued expanding its technological capabilities.

The core Biclonics® platform for bispecific antibodies was joined by the Triclonics® platform for trispecific antibodies. The Triclonics® or trispecific platform provides the unique opportunity to design antibodies capable of simultaneously binding to three targets at once.

The company branded these collective capabilities as Multiclonics®. Merus is a clinical-stage oncology company developing bi/tri-specific antibodies. Multiclonics® are manufactured using industry standard processes and have been observed in preclinical and clinical studies to have several of the same features of conventional human monoclonal antibodies, such as long half-life and low immunogenicity.

The Gilead Partnership (March 2024)

Gilead Sciences, Inc. and Merus N.V. announced a research collaboration, option and license agreement to discover novel dual tumor-associated antigens (TAA) targeting trispecific antibodies. Gilead and Merus agreed to collaborate on the use of Merus' proprietary Triclonics® platform along with Gilead's oncology expertise to research and develop multiple, separate preclinical research programs.

Gilead paid an upfront, non-refundable payment of $56 million and $25 million equity investment. The collaboration includes at least two, but may include up to three preclinical research programs.

If Gilead exercises its license option for all Programs, Merus will receive up to a total of approximately $1.5 billion across all three programs and potential royalties.

Importantly, this collaboration represents the first for Merus' proprietary Triclonics platform.

The Biohaven ADC Collaboration (January 2025)

In January 2025, Biohaven Ltd. and Merus N.V. announced a research collaboration and license agreement to co-develop three novel bispecific antibody drug conjugates (ADCs), leveraging Merus' leading Biclonics® technology platform, and Biohaven's next-generation ADC conjugation and payload platform technologies.

Under the terms of the agreement, Biohaven is responsible for the preclinical ADC generation of three Merus bispecific antibodies under mutually agreed research plans. The agreement includes two Merus bispecific programs generated using the Biclonics® platform, and one program under preclinical research by Merus.

"We're excited to collaborate with Biohaven, leveraging their broad range of linker/payload and conjugation technologies, and expertise with the research and development of ADCs, to rapidly advance bispecific antibody candidate ADCs based on the Merus Biclonics® platform," said Peter B. Silverman, Chief Operating Officer of Merus.

This represented Merus's expansion into ADClonics®—the combination of bispecific antibodies with antibody-drug conjugate technology. The platform was continuously evolving to address new therapeutic modalities.

VII. The BIZENGRI Breakthrough: First FDA Approval (December 2024)

After two decades of platform development, Merus finally achieved regulatory validation.

On December 4, 2024, the Food and Drug Administration granted accelerated approval to zenocutuzumab-zbco (Bizengri, Merus N.V.) for adults with advanced, unresectable, or metastatic non-small cell lung cancer (NSCLC) harboring a neuregulin 1 (NRG1) gene fusion with disease progression on or after prior systemic therapy, or advanced, unresectable, or metastatic pancreatic adenocarcinoma harboring a NRG1 gene fusion with disease progression on or after prior systemic therapy.

This represents the first FDA approval of a systemic therapy for patients with NSCLC or pancreatic adenocarcinoma harboring an NRG1 gene fusion.

This groundbreaking approval makes Zenocutuzumab the first HER3-targeting antibody to reach the market and the 13th bispecific antibody approved by the FDA.

The science behind BIZENGRI is elegant. Bizengri is a Biclonics® bispecific antibody that utilizes the Merus Dock & Block® mechanism to bind to the extracellular domains of HER2 and HER3 expressed on the surface of cells, including tumor cells, inhibiting HER2:HER3 dimerization and preventing NRG1 binding to HER3. It works in the treatment of NRG1+ cancers by inhibiting oncogenic signaling pathways, leading to inhibition of tumor cell proliferation and blocking tumor cell survival.

The ORR was 33% (95% CI, 22%-46%) and 40% (95% CI, 23%-59%) in the NRG1+ NSCLC (n=64) and NRG1+ PDAC (n=30) cohorts, respectively.

For context: NRG1 fusions are rare—found in perhaps 0.1-0.3% of cancers—but the patients who have them previously had no targeted treatment options. NRG1 gene fusions are rare but potent oncogenic genomic events observed in specific cancer types, including NSCLC and PDAC. However, treatment options for patients with NRG1 fusion-positive (NRG1+) cancers were extremely limited.

This application was granted priority review, breakthrough designation, and orphan drug designation. The "accelerated approval" pathway—based on response rate rather than survival data—allowed Merus to reach patients faster, though continued approval may require confirmatory trials.

"The FDA approval of BIZENGRI® marks an important milestone for patients with pancreatic adenocarcinoma or NSCLC that is advanced unresectable or metastatic and harbors the NRG1 gene fusion. I have seen firsthand how treatment with BIZENGRI® can deliver clinically meaningful outcomes for patients," said Alison Schram, MD, an attending medical oncologist at Memorial Sloan Kettering Cancer Center and a principal investigator for the ongoing eNRGy trial.

The commercial path for BIZENGRI involved a partnership with Partner Therapeutics for U.S. commercialization, allowing Merus to focus resources on its larger opportunity: petosemtamab.

VIII. Petosemtamab: The Crown Jewel & Path to Acquisition

While BIZENGRI validated the platform, petosemtamab (MCLA-158) was always the asset that could transform Merus into a commercial powerhouse—or attract a major acquirer.

Petosemtamab, or MCLA-158, is a Biclonics® low-fucose human full-length IgG1 antibody targeting the epidermal growth factor receptor (EGFR) and the leucine-rich repeat containing G-protein-coupled receptor 5 (LGR5).

The drug's mechanism is multifaceted. By targeting both EGFR (overexpressed in many solid tumors) and LGR5 (a marker of cancer stem cells), petosemtamab can simultaneously block tumor growth signals, drive internalization and degradation of EGFR on cancer cells, and enhance immune-mediated killing through ADCC (antibody-dependent cellular cytotoxicity).

The target indication—head and neck squamous cell carcinoma (HNSCC)—represents a substantial market opportunity. The head and neck squamous cell carcinoma market size was valued at USD 2.37 billion in 2024 and is likely to exceed USD 7.08 billion by the end of 2037, expanding at over 8.7% CAGR during the forecast period.

According to Global Cancer Observatory (GLOBOCAN), the incidence of HNSCC continues to rise and is anticipated to increase by 30% (that is, 1.08 million new cases annually) by 2030.

The current standard of care—pembrolizumab (Keytruda) for PD-L1+ patients—has limitations. Many patients don't respond, and those who do often progress within a year. The Phase 2 data for petosemtamab in combination with pembrolizumab generated enormous excitement.

"By essentially every metric, we believe these interim data are significantly better than pembrolizumab monotherapy, the control arm of our ongoing phase 3 trial, and underscores the opportunity petosemtamab holds to become a new standard of care, if approved, in head and neck cancer," said Bill Lundberg, M.D., President, Chief Executive Officer of Merus.

Merus provided updated interim clinical data from the phase 2 trial of petosemtamab with pembrolizumab as 1L treatment for PD-L1+ (CPS≥1) r/m HNSCC at the 2025 American Society of Clinical Oncology® (ASCO®) Annual Meeting, demonstrating a 63% response rate among 43 evaluable patients and a 79% overall survival rate at 12 months.

To put this in context: pembrolizumab monotherapy achieves response rates around 20-25% in first-line HNSCC. A 63% response rate with petosemtamab plus pembrolizumab—if replicated in Phase 3—would represent a transformational improvement.

Petosemtamab is an EGFRxLGR5 bispecific antibody with the potential to be both first- and best-in-class in head and neck cancer. It has been granted two Breakthrough Therapy Designations (BTD) by the U.S. Food and Drug Administration (FDA) for first- and second-line plus head and neck cancer indications.

Merus is currently running two Phase 3 trials in first- and second/third line head and neck cancer, with topline interim readout of one or both trials anticipated in 2026. Based on Genmab's experience in late-stage development and excellence in commercial execution, Genmab anticipates the potential for the initial launch of petosemtamab in 2027, subject to clinical results and regulatory approvals.

The LiGeR-HN1 trial is a phase 3, open-label, randomized trial comparing the efficacy and safety of petosemtamab plus pembrolizumab vs pembrolizumab.

The LiGeR-HN2 trial is a phase 3 open-label, randomized trial comparing the efficacy and safety of petosemtamab vs. investigator's choice of monotherapy treatment including cetuximab, methotrexate, or docetaxel.

This dual-track Phase 3 strategy positioned Merus for potential approval in multiple treatment settings—exactly the kind of comprehensive development program that makes a company attractive to acquirers.

IX. The Genmab Acquisition: The $8 Billion Exit

On September 29, 2025, the endgame arrived.

Antibody drug specialist Genmab on Monday agreed to acquire Dutch biotechnology company Merus in an $8 billion deal centered around a drug that's shown potential treating head and neck cancer.

Per deal terms, Genmab will pay $97 per share in cash to acquire Merus, representing a 41% premium to the biotech's closing price on Friday of about $68. The deal hands Genmab a drug called petosemtamab that's in late-stage testing for head and neck cancer.

The transaction has been unanimously approved by the Boards of Directors of both companies. A wholly owned subsidiary of Genmab will commence a tender offer for 100% of Merus' common shares, which is anticipated to close by early in the first quarter of 2026.

Consideration is expected to be funded through a combination of cash on hand and approximately $5.5 billion of non-convertible debt financing. Genmab has obtained a funding commitment from Morgan Stanley Senior Funding, Inc. for this amount.

Why Genmab?

Genmab is itself a remarkable antibody company. The asset adds to a large portfolio of antibody drugs for Genmab, which codeveloped the multiple myeloma therapy Darzalex with Johnson & Johnson, the cervical cancer medicine Tivdak with Seagen and the lymphoma drug Epkinly with AbbVie.

Genmab, which had long developed drugs under partnerships with larger companies, is now pursuing a strategy of developing and commercializing medications it fully owns.

The company has recently started turning to deals to boost its pipeline. Last year, it paid $1.8 billion to acquire antibody-drug conjugate developer ProfoundBio.

The strategic logic was clear. Genmab also intends to broaden and accelerate petosemtamab's development with potential expansion into earlier lines of therapy. Following its initial anticipated approval, Genmab believes that petosemtamab will be accretive to EBITDA with at least one-billion-dollar annual sales potential by 2029, with multi-billion-dollar annual revenue potential thereafter.

William Blair analyst Matt Phipps is projecting $3 billion to $4 billion in annual peak sales in head and neck cancer alone.

In a note sent to investors, William Blair analyst Matt Phipps said an acquisition was the likely path for Merus, but the firm expected such a deal would not come until peto's Phase 3 readout in 2026.

The deal came earlier than many expected—before Phase 3 data—reflecting Genmab's confidence in the Phase 2 results and desire to acquire before the asset was fully de-risked (and therefore more expensive).

John de Koning, Partner at EQT and former board member at Merus, said: "It has been a great honor to support Merus from its early beginnings to a NASDAQ-listed clinical-stage biotech with more than 300 employees. The acquisition agreement with Genmab highlights the strength of Merus' innovative platform and pipeline and is a testament to the team's vision and leadership."

X. Business Model & Financial Evolution

Merus's business model evolved across three phases:

Phase 1: Platform Development (2003-2016) Focus on building the Biclonics® technology, securing patents, and achieving proof-of-concept in preclinical models. Funding came from venture capital and pharma strategic investments.

Phase 2: Partnership-Driven Expansion (2016-2024) After the IPO, Merus used partnerships to fund R&D while retaining rights to its most promising programs. Merus N.V. reported $25.6 million in collaboration revenue for Q1 2024 while simultaneously investing $70.0 million in research and development within the same quarter.

This model—spending more on R&D than generating in revenue—is typical for clinical-stage biotechs. The key metric is whether the company can fund itself to key value-creation milestones.

With significant progress reported in trials for petosemtamab and zenocutuzumab, and maintaining a robust cash position near $1.1 billion as of March 31, 2024, Merus held approximately $1.0 billion in cash, cash equivalents, and marketable securities as of September 30, 2024.

Phase 3: Commercial Transition (2024-2025) BIZENGRI's approval marked the beginning of commercial operations, though the license agreement with Partner Therapeutics meant Merus wouldn't build its own U.S. sales force for that product. The company was positioning to commercialize petosemtamab more directly—until the Genmab acquisition changed the trajectory.

As of the most recent data, Merus employs approximately 291 people and has a market capitalization of approximately $7.119B.

XI. Playbook: Business & Investing Lessons

Platform vs. Product Thinking

Merus demonstrates the power of platform companies in biotech. By developing the Biclonics® technology rather than betting everything on a single drug, Merus could: - Generate multiple clinical candidates with different risk/reward profiles - License early-stage programs for non-dilutive capital while retaining later-stage assets - Continuously improve the underlying technology - Pivot when individual programs failed (as they did with MCLA-117 in leukemia)

Non-Dilutive Funding Strategy

The partnership progression—Incyte ($200M), Eli Lilly ($60M + $1.6B potential), Gilead ($81M + $1.5B potential)—provided hundreds of millions in non-dilutive capital. This preserved equity value for shareholders while funding expensive clinical development.

Focused Clinical Strategy

Rather than pursuing broad indications, Merus targeted specific biomarkers (NRG1 fusions for BIZENGRI) or specific cancer types (HNSCC for petosemtamab). This focus enabled: - Smaller, faster clinical trials - Regulatory pathways like breakthrough therapy designation and accelerated approval - Clearer differentiation from competitors

The Dutch Biotech Ecosystem

Merus benefited from Utrecht's strong academic life sciences community, European venture capital networks (LSP, EQT), and talent pools experienced in antibody engineering (many from the Crucell diaspora). The Netherlands' favorable regulatory environment and central European location also helped.

Timing the Exit

Genmab's acquisition came at an interesting moment—after Phase 2 de-risking but before Phase 3 readout. This timing reflected: - Genmab's desire to acquire before complete de-risking increased the price - Merus's recognition that commercializing petosemtamab globally would require either major dilution or partnership - The broader M&A environment favoring deals

XII. Competitive Landscape & Strategic Analysis

Porter's Five Forces

Threat of New Entrants: MODERATE-HIGH Bispecific antibodies require sophisticated platforms, extensive patent portfolios, and years of optimization. However, the space is attracting significant investment. As of January 2025, ClinicalTrials.gov indicates that over 319 bispecific antibody drug candidates are in various stages of development worldwide.

Bargaining Power of Suppliers: LOW Merus's manufacturing approach—using standard monoclonal antibody production processes—meant abundant CMO (contract manufacturing organization) capacity and competitive pricing.

Bargaining Power of Buyers: MODERATE Oncology products command premium pricing due to life-or-death stakes and limited alternatives. Breakthrough therapy designations and orphan drug status (for BIZENGRI) enhance pricing power.

Threat of Substitutes: HIGH The competitive landscape includes CAR-T therapies, checkpoint inhibitors, and other immunotherapy modalities. In head and neck cancer specifically, Merck's pembrolizumab is the dominant standard of care.

Industry Rivalry: HIGH The bispecific antibody space is rapidly evolving with heightened competition among biotech giants and emerging players. Leading companies are prioritizing next-generation platforms for greater safety, flexibility, and efficacy.

Hamilton's 7 Powers Framework

Counter-Positioning: STRONG Merus's full-length IgG format for bispecifics was a counter-position to earlier approaches. Legacy players using fragment-based or chemically linked bispecifics couldn't easily adopt Merus's approach without rebuilding their platforms.

Cornered Resource: STRONG The proprietary MeMo transgenic mouse platform, common light chain technology, and extensive patent estate around bispecific generation and screening methods represent genuine cornered resources.

Process Power: STRONG The high-throughput functional screening approach—generating thousands of candidates and selecting the best—is a process advantage. This enables rapid optimization and identification of molecules with unique biological properties.

Scale Economies: WEAK As a clinical-stage company, Merus didn't benefit significantly from manufacturing scale. However, the standard production processes reduced the capital intensity of scaling.

Network Effects: WEAK Drug development lacks traditional network effects, though reputation and clinical trial networks provide modest advantages.

Switching Costs: MODERATE (Post-Approval) Once physicians become familiar with a therapy and patients respond well, switching costs emerge. Petosemtamab's combination with pembrolizumab leverages an existing standard of care, potentially reducing adoption barriers.

Branding: WEAK B2B focus on physician/payer buyers limits consumer branding. However, breakthrough therapy designations and FDA approval create professional reputation.

XIII. Key Metrics for Ongoing Monitoring

For investors tracking companies in the bispecific antibody space, three KPIs matter most:

1. Clinical Trial Progression Rate The percentage of candidates advancing from one clinical phase to the next. Industry average is roughly 30% Phase 1 to Phase 2, 30% Phase 2 to Phase 3, and 50% Phase 3 to approval. Companies consistently beating these averages demonstrate superior target selection and platform performance.

2. Partnership Economics Track the ratio of upfront payments to total potential deal value. Higher upfront percentages signal partner confidence. Also monitor option exercise rates—when partners choose to advance programs past initial research phases, it validates the platform.

3. Response Rates in Registrational Trials For individual programs, overall response rate (ORR) and duration of response (DoR) in Phase 2 studies predict Phase 3 success probability. Petosemtamab's 63% ORR in combination with pembrolizumab—versus approximately 25% for pembrolizumab alone—represents the kind of step-change improvement that typically succeeds in registrational trials.

XIV. Risk Factors & Regulatory Considerations

Accelerated Approval Contingencies BIZENGRI's indications are approved under accelerated approval based on overall response rate (ORR) and duration of response (DOR). Continued approval for these indications may be contingent upon verification and description of clinical benefit in a confirmatory trial(s).

The FDA can withdraw accelerated approvals if confirmatory trials fail or are not completed. This creates ongoing regulatory risk.

Phase 3 Execution Risk Petosemtamab's Phase 3 trials are ongoing. LiGeR-HN1 and LiGeR-HN2 are enrolling and expected to be substantially enrolled by year-end 2025. Positive Phase 2 data doesn't guarantee Phase 3 success—many promising drugs fail in larger, randomized trials.

Manufacturing Complexity While Merus uses standard processes, biologic manufacturing remains complex. Any issues with contract manufacturers could delay clinical development or commercial supply.

Competitive Dynamics Over 400 clinical/preclinical bispecific antibody candidates are being evaluated by over 120 drug developers worldwide. Competition is intensifying across the space.

Acquisition Integration Risk Following the Genmab acquisition, integration challenges could affect development timelines or key personnel retention.

XV. Looking Ahead: The Next Chapter

The Merus story ends—at least as an independent company—with the Genmab acquisition. But the broader implications continue.

While Merus' drug showed potential in Phase 2, those findings will need to be duplicated in a late-stage study comparing a petosemtamab-Keytruda combination to Keytruda alone. Results are expected in 2026.

Genmab said Monday that the drug could eventually book $1 billion in yearly sales by 2029 and have multibillion-dollar annual sales potential afterwards.

The bispecific antibody field—which Merus helped pioneer—is entering its commercial adolescence. Till date, fifteen bispecific antibodies have been approved for therapeutic use. That number will likely triple or quadruple in the next decade.

Merus demonstrated that European biotech can compete at the highest levels. That a small team from Utrecht could build a technology platform worthy of an $8 billion acquisition speaks to the globalization of biotech innovation.

Most importantly, Merus proved that the partnership-driven, platform-first model can work. By retaining rights to its crown jewels while licensing earlier-stage programs, Merus captured the upside of its best assets while funding development with non-dilutive capital.

The twenty-year journey from a university lab to an $8 billion exit wasn't linear. There were funding crises, failed programs, market crashes, and pandemic disruptions. But the core thesis—that full-length bispecific antibodies would transform cancer treatment—proved correct.

For the thousands of patients who may one day benefit from petosemtamab, the story is just beginning. For the founders, investors, and employees who built Merus, it's a remarkable vindication of the long game in biotech. And for the industry watching, it's a playbook worth studying: build the platform, protect the optionality, time the partnerships, and know when to hand off the baton.

Myth vs. Reality

| Myth | Reality |

|---|---|

| "Bispecific antibodies are a new concept" | The concept dates to the 1960s; Merus's innovation was making them manufacturable at scale |

| "European biotechs can't compete with US companies" | Merus achieved FDA approval and an $8B exit while headquartered in the Netherlands |

| "Partnership deals mean giving away the farm" | Merus retained rights to BIZENGRI and petosemtamab while partnering early-stage programs |

| "Phase 2 data predicts Phase 3 success" | Only about 30% of oncology drugs succeed in Phase 3; petosemtamab's 63% ORR is encouraging but not guaranteed |

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube