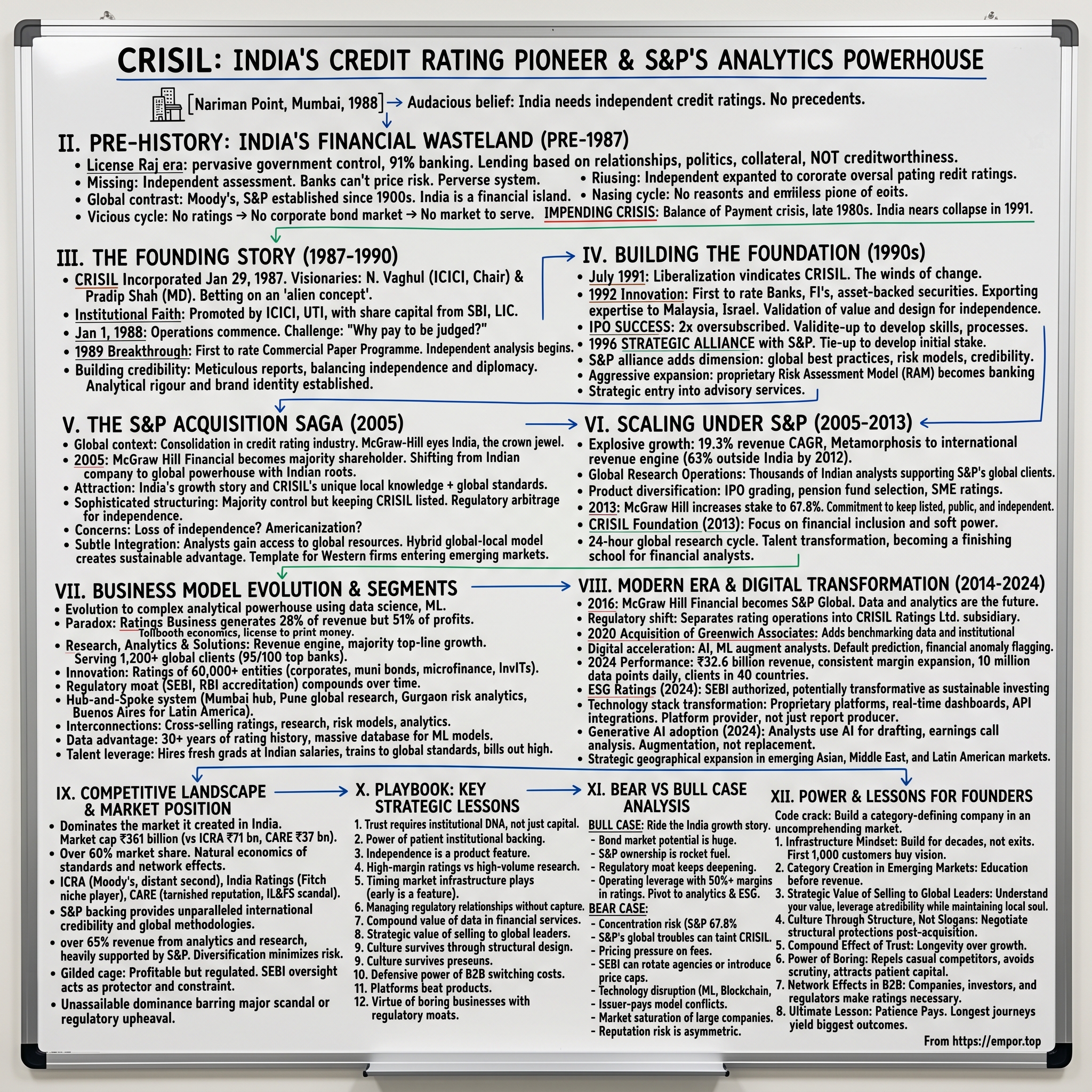

CRISIL: India's Credit Rating Pioneer and S&P's Analytics Powerhouse

I. Introduction & Cold Open

Picture this: January 1988, Nariman Point, Mumbai. In a modest office overlooking the Arabian Sea, a small team of analysts sits hunched over financial statements, building something that doesn't yet exist in India—a systematic way to judge creditworthiness. No templates from New York or London to copy. No precedents in Indian markets. Just the audacious belief that a country emerging from decades of socialist planning needs what the West has had since 1909: independent credit ratings.

That team would become CRISIL—Credit Rating Information Services of India Limited. Today, with a market capitalization of ₹37,436 crores and revenues exceeding ₹3,381 crores, CRISIL stands as India's largest credit rating agency and a global analytics powerhouse. But here's the twist that makes this story remarkable: while most emerging market financial infrastructure companies struggle to scale beyond their borders, CRISIL managed something extraordinary. It caught the attention of S&P Global, which acquired majority control in 2005, transforming a local ratings agency into a critical node in the global financial information network. This isn't just another financial infrastructure story. It's the tale of how a developing economy built its own credit architecture, how global capital recognized that infrastructure's value, and how—against all odds—the marriage between a local pioneer and a global giant actually worked. While most acquisition stories in emerging markets end with either corporate indigestion or cultural erosion, CRISIL managed to maintain its Indian identity while scaling globally. Today, with a market cap of ₹38,075 crores and revenue of ₹3,381 crores, it stands as testament to what happens when local expertise meets global ambition at exactly the right moment.

The company's journey from that Nariman Point office to becoming S&P Global's crown jewel in Asia is a masterclass in timing, execution, and the art of building trust in markets where trust itself is currency. Its ratings business, while contributing only 28% of revenues, generates 51% of total profits—a testament to the pricing power that comes from being the gold standard in credit assessment.

As we unpack this story, we'll explore how CRISIL navigated India's License Raj, survived the skepticism of a market that didn't understand credit ratings, leveraged liberalization to explosive growth, and ultimately caught the eye of one of Wall Street's most prestigious names. It's a story about infrastructure, yes, but more fundamentally, it's about how financial trust gets built in emerging markets—one rating at a time.

II. Pre-History: India's Financial Markets Pre-1987

To understand why CRISIL's founding was revolutionary, you need to first grasp the financial wasteland that was India before 1987. Imagine walking into a State Bank of India branch in 1985. The loan officer sits behind a massive wooden desk, files stacked ceiling-high, making lending decisions based on... what exactly? Relationships. Political connections. The size of the collateral. But actual creditworthiness? That was anyone's guess.

This was the License Raj era—that suffocating period from 1947 to 1991 when the Indian government controlled virtually every aspect of economic life through an elaborate system of licenses, regulations, and red tape. Want to expand your factory? Get a license. Import raw materials? Another license. The joke went that you needed a permit to get a permit. In this environment, capital allocation wasn't about risk and return; it was about who you knew in the corridors of power. The banking sector epitomized this dysfunction. In 1969, Indira Gandhi nationalized 14 major commercial banks, followed by six more in 1980. By the second round of nationalizations, the Government of India controlled around 91% of the banking business. Banks weren't financial institutions in any modern sense—they were extensions of government policy, directed to lend to "priority sectors" regardless of creditworthiness. Interest rates were fixed by bureaucrats, not markets. Risk assessment was a foreign concept.

The absence of credit ratings created a particularly perverse system. Without independent assessment of creditworthiness, lending decisions relied on crude proxies: the size of your factory, your family name, which politician vouched for you. This wasn't just inefficient—it was dangerous. Banks couldn't price risk because they couldn't measure it. Bad loans accumulated like toxic waste, hidden in the ledgers of state-owned banks that knew they'd be bailed out anyway.

Consider the international context. While India struggled with this financial medievalism, the rest of the world had long since developed sophisticated credit assessment mechanisms. Moody's had been rating bonds since 1909. Standard & Poor's traced its roots to 1860. By the 1980s, these agencies were integral to global capital markets, enabling the flow of trillions of dollars based on standardized risk assessments. India, meanwhile, remained a financial island, cut off from global capital flows by its own regulatory walls.

The corporate bond market—that vital alternative to bank lending that exists in every developed economy—was essentially non-existent. Why would anyone buy a corporate bond when you couldn't assess the issuer's creditworthiness? The result was a vicious cycle: companies couldn't access capital markets because there were no ratings, and there were no ratings because there was no market to serve.

The Balance of Payment crisis arose in the 1970s and worsened towards the end of 1980s, bringing India to the verge of collapse in 1991. With foreign exchange reserves at just $1.2 billion in January 1991—barely enough to cover three weeks of essential imports—India was weeks away from defaulting.

Yet even in this stifling environment, whispers of change were beginning. A small group of reformers within the government and financial institutions understood that India couldn't remain isolated forever. They studied how South Korea had built its credit infrastructure, how Malaysia was developing its capital markets. They knew that when—not if—India opened up, it would need the financial plumbing that other countries took for granted.

The stage was being set for something unprecedented: the creation of a credit rating agency in a country where the very concept of market-determined credit risk was alien. It would require not just technical expertise but a leap of faith—that India's businesses, starved of proper capital allocation for decades, were ready for the harsh light of independent credit assessment. That leap would come from an unlikely alliance of institutions that understood a fundamental truth: you can't build a modern economy on a foundation of financial guesswork.

III. The Founding Story (1987-1990)

The boardroom at ICICI's headquarters, January 29, 1987. N. Vaghul, the visionary banker who would later transform ICICI into a financial supermarket, sits across from Pradip Shah, a young financial wizard with an architect's mind for building institutions. They're signing papers that will give birth to Credit Rating Information Services of India Limited—CRISIL. The moment is heavy with both promise and uncertainty. As Vaghul would later recall, they were launching "an idea far ahead of its times" in a country that didn't yet understand why it needed credit ratings.

CRISIL was incorporated on January 29, 1987, promoted by the erstwhile ICICI Ltd along with UTI and other financial institutions, with N. Vaghul as first Chairman and Pradip Shah as first Managing Director. The shareholding structure itself told a story of institutional faith: share capital came from SBI, LIC and United India Insurance Company. This wasn't just private sector entrepreneurship—it was a coalition of India's financial establishment betting on an alien concept.

Shah, who would become the founding managing director, brought a unique perspective. Unlike the traditional bankers surrounding him, he understood that India's financial markets needed architecture, not just capital. He had studied how rating agencies functioned in developed markets and recognized a fundamental truth: you can't have efficient capital allocation without independent risk assessment. But translating that vision into reality in 1980s India would prove nearly impossible.

CRISIL commenced operations on January 1, 1988, but the business environment was far from promising—lending rates were fixed, India had no corporate bond market, and credit rating was an idea far ahead of its times. Imagine trying to sell ice to Eskimos, except the Eskimos don't know what ice is and aren't sure they need it. That was CRISIL's challenge.

The early days were brutal. Shah and his small team would visit company after company, explaining what a credit rating was, why it mattered, only to be met with puzzled looks or outright hostility. "Why should we pay someone to judge us?" was a common refrain. Companies saw ratings as unnecessary scrutiny in a market where lending decisions were already made through relationships and government directives. Banks, comfortable in their state-owned cocoons, saw no need for external assessment of credit risk.

The breakthrough came in 1989, modest but symbolically massive: CRISIL became the first rating organization to evaluate the Commercial Paper Programme. Commercial paper—short-term debt instruments—represented a tiny corner of India's financial markets, but it was a start. For the first time, an Indian company's creditworthiness was being assessed not by government diktat or banking relationships, but by independent analysis.

CRISIL launched the 'CrisilCard Service' to provide comprehensive information and analytical opinion on India's corporate entities, and despite initial lack of market acceptance, its operations became well established, acquiring brand identity with a reputation for analytical rigour and independence.

Building credibility required more than just technical competence—it demanded a delicate balance between independence and diplomacy. Shah understood that CRISIL couldn't afford to be seen as either too harsh (alienating potential clients) or too lenient (losing credibility). Every rating decision in those early years wasn't just an assessment of credit risk; it was a precedent that would shape how Indian markets understood creditworthiness.

The team Shah assembled was deliberately eclectic—economists, chartered accountants, even engineers—bringing diverse perspectives to credit analysis. They developed methodologies from scratch, adapting international best practices to Indian realities. How do you rate a company in a market where financial disclosure is minimal? How do you assess management quality in family-run businesses where succession planning is taboo? These weren't questions with textbook answers.

Vaghul's role as chairman provided crucial cover. His reputation as a reformist banker who had modernized Bank of India gave CRISIL institutional credibility it desperately needed. When skeptics questioned why India needed credit ratings, Vaghul could point to his experience seeing how the absence of proper risk assessment had led to mounting bad loans in the banking system. He wasn't just chairman in name—he was CRISIL's chief evangelist to a skeptical establishment.

The company operated on a shoestring budget, with analysts working out of cramped offices, often sharing desks. But what they lacked in resources, they made up in missionary zeal. These weren't just employees building a business; they were financial revolutionaries trying to drag India's capital markets into modernity. Every rating report was meticulously crafted, knowing that a single mistake could destroy the credibility they were painstakingly building.

By 1990, against all odds, CRISIL had established itself as more than just a curiosity. It had rated its first bonds, evaluated its first commercial paper programs, and—most importantly—begun to change how Indian businesses thought about creditworthiness. The company that started as "an idea far ahead of its times" was slowly pulling India's financial markets into the future. The foundation was set for what would become an explosive growth story, perfectly timed with India's impending economic liberalization.

IV. Building the Foundation (1990s)

July 1991: The monsoon clouds gathering over Mumbai carried more than rain—they brought the winds of economic change. Finance Minister Manmohan Singh had just presented his watershed budget, dismantling four decades of socialist planning. For CRISIL, struggling to convince a skeptical market about the value of credit ratings, liberalization wasn't just good news—it was vindication. The company that had been "far ahead of its times" suddenly found time catching up.

The transformation was immediate and dramatic. In 1992, CRISIL became the first to rate Banks & financial institutions' asset-backed securities—a market that simply didn't exist before liberalization. This wasn't just another product launch; it was CRISIL creating the infrastructure for entirely new asset classes. As foreign investors began eyeing Indian markets, they needed something familiar—credit ratings that spoke their language. CRISIL was the only translator available.

That same year, something remarkable happened that validated CRISIL's growing reputation: the company offers technical assistance and training to help set up Rating Agency Malaysia Berhad, and MAALOT—the Israeli securities rating company. Think about that—a four-year-old Indian company, operating in a market that barely understood credit ratings, was now exporting its expertise internationally. This wasn't just business development; it was a powerful signal that CRISIL had developed genuine intellectual property worth sharing. But the real breakthrough came with CRISIL's IPO: a whopping success—its 20,00,000 shares, sold at a premium of Rs.40 per share, were oversubscribed by 2.47 times. This wasn't just a capital-raising exercise; it was validation from the market that CRISIL had built something valuable. The oversubscription meant investors were literally fighting to own a piece of India's credit rating infrastructure.

The IPO's success had deeper implications. CRISIL was now a public company with thousands of shareholders watching its every move. This public ownership created an additional layer of independence—any attempt to compromise ratings for business gain would face scrutiny not just from regulators but from minority shareholders. It was a masterstroke in institutional design.

Then came 1996, a watershed year that would define CRISIL's trajectory for decades: CRISIL forges a strategic business alliance with Standard & Poor's (S&P) Ratings Group. The tie-up was part of CRISIL's strategy to develop its skills and processes. This wasn't just a handshake agreement—it was CRISIL recognizing that to be world-class, it needed world-class partners.

The relationship was further strengthened in 1997 when McGraw Hill Financial acquired its initial 9.68% equity stake in CRISIL. The alliance with the world's leading rating agency added a new dimension to CRISIL's methodologies, providing exposure to international rating markets and S&P's rating processes.

The S&P alliance transformed CRISIL in ways both visible and subtle. Suddenly, CRISIL analysts had access to global best practices, sophisticated risk models, and—perhaps most importantly—credibility with international investors who were beginning to eye India as liberalization gained momentum. When a foreign institutional investor looked at a CRISIL rating, they saw the imprimatur of S&P's methodology behind it.

The decade also saw CRISIL's aggressive product expansion. In 1998, CRISIL's proprietary Risk Assessment Model (RAM) became the banking industry standard—a remarkable achievement for a company that was barely a decade old. Banks that once resisted the very concept of external ratings were now using CRISIL's models as their internal risk management framework.

CRISIL also began its transformation from pure ratings into adjacent businesses. The company diversified its business portfolio with a strategic entry into advisory services, winning its first major mandate in the infrastructure policy advisory domain. This wasn't mission creep—it was strategic expansion into areas where CRISIL's analytical capabilities could create value beyond just rating debt instruments.

The internationalization of expertise continued throughout the decade. The technical assistance to Malaysia and Israel wasn't just consultancy work—it was CRISIL exporting India's financial innovation to other emerging markets. Think about the audacity: a company from a country that didn't have credit ratings until 1988 was now teaching other nations how to build their credit infrastructure.

By decade's end, CRISIL had fundamentally altered India's financial landscape. It had created not just a business but an entire ecosystem—investors who relied on ratings, companies that sought them, regulators who mandated them, and competitors who emerged to challenge CRISIL's dominance. The company that started as "an idea far ahead of its times" had successfully dragged Indian capital markets into the present, setting the stage for what would become an explosive growth story in the new millennium.

V. The S&P Acquisition Saga (2005)

The boardroom at McGraw-Hill's Manhattan headquarters, early 2005. Harold McGraw III, the patrician CEO of the publishing-turned-financial-services giant, is reviewing a presentation about emerging markets. One slide keeps appearing: India's GDP growth projections, the explosion in corporate bond issuances, the need for credit infrastructure. The message is clear—whoever owns India's rating infrastructure will control a critical gateway to one of the world's fastest-growing economies. That company, McGraw-Hill's team has concluded, is CRISIL.

In 2005, McGraw Hill Financial became CRISIL's majority shareholder, culminating the strategic alliance that began in 1996. While the exact financial details of the 2005 transaction weren't publicly disclosed, what we know is that this represented a fundamental shift in CRISIL's trajectory—from an Indian company with international partnerships to a global company with Indian roots.

The global context is crucial here. By 2005, the credit rating industry was consolidating worldwide. Moody's had gone public in 2000 and was aggressively acquiring. Fitch had been bought by Fimalac. The industry was becoming a global oligopoly, and McGraw-Hill understood that to compete, S&P needed dominant positions in emerging markets. India, with its booming economy and underdeveloped capital markets, represented the crown jewel of emerging market opportunities.

Why did S&P want CRISIL so badly? First, the India growth story was becoming impossible to ignore. GDP was growing at 8-9% annually. Foreign institutional investors were pouring money into Indian markets. Corporate India was beginning to access international capital markets. Every one of these trends required credit ratings, and CRISIL had a virtual monopoly on the infrastructure.

Second, CRISIL offered something unique: deep local knowledge combined with global standards. You couldn't just parachute S&P analysts into Mumbai and expect them to rate Indian companies. Understanding Indian business groups, the nuances of priority sector lending, the implications of monsoons on agricultural credits—this required indigenous expertise that would take decades to build from scratch.

The deal mechanics revealed sophisticated structuring. McGraw-Hill didn't attempt a full buyout initially—that would have triggered regulatory concerns and potentially damaged CRISIL's carefully cultivated independence. Instead, they took majority control while keeping CRISIL listed, maintaining the fiction of independence while securing economic control. This wasn't just financial engineering; it was regulatory arbitrage at its finest.

The impact on independence raised immediate concerns. How could CRISIL claim to be independent when it was majority-owned by an American corporation? The rating agency that had built its reputation on being India's own was now controlled from New York. Critics worried about conflicts of interest—would CRISIL favor companies that were also S&P clients globally? Would rating standards be imposed from Manhattan without understanding Indian realities?

Yet remarkably, CRISIL managed to maintain its Indian identity post-acquisition. The management remained largely Indian. The rating committees continued to operate independently. S&P was smart enough to recognize that CRISIL's value lay precisely in its local credibility—Americanizing it would destroy the very asset they had purchased.

The integration was subtle but powerful. CRISIL analysts gained access to S&P's global resources—sophisticated risk models, sector expertise, training programs. When rating an Indian infrastructure company, they could tap into S&P's experience rating similar companies in Brazil or South Africa. This wasn't just knowledge transfer; it was the creation of a global-local hybrid that neither company could have built independently.

For McGraw-Hill, CRISIL became a gateway to the entire South Asian market. Through CRISIL, S&P could offer global investors a credible window into Indian credit markets. When Reliance wanted to issue international bonds, having a CRISIL rating that met S&P standards became a powerful calling card. The acquisition wasn't just about buying a rating agency; it was about controlling a critical node in the global flow of capital to emerging markets.

The precedent this set was profound. Other global financial services firms took notice—if McGraw-Hill could successfully acquire and integrate an Indian financial infrastructure company, why couldn't they? The CRISIL acquisition became a template for how Western financial giants could enter emerging markets not as colonizers but as partners, maintaining local credibility while providing global connectivity.

By keeping CRISIL publicly listed with minority shareholders, McGraw-Hill also created a unique governance structure. The minority shareholders, including many Indian institutions, acted as a check on any attempt to compromise CRISIL's independence. This wasn't corporate social responsibility; it was clever structuring that aligned incentives—McGraw-Hill needed CRISIL to remain credible to remain valuable.

VI. Scaling Under S&P (2005-2013)

The transformation was immediate and dramatic. Within months of S&P taking majority control, CRISIL's offices in Mumbai began to buzz with a different energy. Young analysts who had been rating Indian textile companies were suddenly on calls with New York, discussing methodologies for rating collateralized debt obligations. The company that had spent two decades building India's credit infrastructure was now being groomed for a much larger stage.

The numbers tell a story of explosive growth: revenue increased at a compound annual growth rate of 19.3% over five years. By 2012, CRISIL had total sales of INR 9,777 million, with 63% generated outside India. Think about that transformation—a company founded to serve Indian capital markets was now earning the majority of its revenue from international clients. This wasn't just growth; it was metamorphosis.

The international expansion followed a brilliant strategy: leverage India's cost advantage to serve global clients. CRISIL set up what would become one of the world's largest financial research operations, with thousands of analysts in India supporting S&P's global operations. When a portfolio manager in London needed analysis of European bank earnings, that work was increasingly being done by CRISIL analysts in Mumbai or Pune, trained to global standards but costing a fraction of London salaries.

Product diversification accelerated beyond traditional ratings. CRISIL launched IPO grading services, providing independent assessments of new public issues. The Pension Fund Regulatory and Development Authority awarded CRISIL a prestigious mandate to assist in selecting fund managers under the New Pension Scheme. Small and Medium Enterprise (SME) ratings were introduced to serve specialized needs of the SME sector. Each new product leveraged the same core competency—turning data into judgment—but applied it to new markets.

In 2013, McGraw Hill Financial announced increasing its stake to 67.8% from 52.8%, acquiring 10,623,059 equity shares for INR 12.9 billion or $214 million. The offer of INR 1,210 per share represented a premium of 29% to the closing share price and 12% to CRISIL's all-time high. This wasn't desperation buying; it was McGraw-Hill doubling down on a winner.

Harold McGraw III's statement was revealing: "We intend to keep CRISIL a listed public, independent company to maintain the company's leadership and essential role across the Indian economy." This wasn't corporate speak—it was recognition that CRISIL's value lay precisely in its independence and Indian identity.

The creation of CRISIL Foundation in 2013 was more than corporate social responsibility—it was strategic positioning. By focusing on financial inclusion and policy research, the Foundation reinforced CRISIL's role as not just a rating agency but a critical piece of India's financial architecture. This soft power would prove invaluable in maintaining regulatory relationships and public trust.

The global delivery model that emerged during this period was revolutionary. CRISIL created a 24-hour research cycle—work would begin in India, continue in London, and finish in New York, following the sun. This wasn't just about cost arbitrage; it was about creating a seamless global research platform that no competitor could easily replicate.

The talent transformation was equally dramatic. CRISIL began recruiting from India's top engineering and business schools, offering them global careers without leaving India. The company became a finishing school for financial analysts—young Indians who joined CRISIL would emerge trained to global standards, often poached by investment banks and private equity firms. This talent ecosystem became self-reinforcing: the best graduates wanted to work where the best graduates worked.

By 2013, CRISIL had achieved something remarkable: it had become simultaneously more Indian and more global. Its ratings were the gold standard in India, required by regulators and trusted by investors. Yet it was also a critical part of S&P's global infrastructure, processing research and analytics for the world's largest financial institutions. This dual identity—Indian enough to be trusted locally, global enough to be valued internationally—became CRISIL's sustainable competitive advantage. The company that had started as an "idea far ahead of its times" was now setting the pace for everyone else.

VII. Business Model Evolution & Segments

Walk into CRISIL's headquarters in Mumbai's Powai district today, and you'll find something that would puzzle a visitor from the 1990s. Yes, there are still rating analysts poring over financial statements, but they're outnumbered by data scientists, software engineers, and quantitative analysts building machine learning models. The company that made its name rating Indian corporate bonds has evolved into something far more complex—and far more profitable.

The numbers reveal a fascinating paradox: the Ratings Business generates 28% of revenues but delivers 51% of profits. This isn't just good margins; it's the economics of a tollbooth on a highway everyone must use. Once SEBI mandates that certain instruments must be rated, once investors demand ratings before investing, CRISIL essentially owns a license to print money. The marginal cost of issuing one more rating is minimal, but the pricing power is enormous.

The Research, Analytics & Solutions segment, while less profitable on a percentage basis, has become the revenue engine, driving the majority of top-line growth. This business serves over 1,200 clients globally, including 95 of the world's 100 largest banks. When JP Morgan needs someone to analyze thousands of European corporate earnings reports, they turn to CRISIL. When a private equity firm needs to evaluate Indian infrastructure assets, CRISIL provides the analysis.

Innovation in the ratings business has been constant: CRISIL now rates over 60,000 entities, from traditional corporates to municipal bonds, from microfinance institutions to complex structured products like InvITs (Infrastructure Investment Trusts). Each new product category requires developing new methodologies, training analysts, educating the market—but once established, becomes another recurring revenue stream.

The regulatory moat deserves special attention. CRISIL operates under accreditation from both SEBI and RBI, licenses that are nearly impossible for new entrants to obtain. This isn't just bureaucratic protection; regulators need rating agencies they can trust, with long track records and proven methodologies. Every year CRISIL operates successfully, this moat becomes deeper.

The geographic expansion strategy has been subtle but effective. Rather than trying to compete with S&P in developed markets, CRISIL focused on serving global clients who need emerging market expertise. A hedge fund in Greenwich, Connecticut might use S&P for rating U.S. corporates, but when they need someone to analyze Indian banks or Chinese real estate developers, they turn to CRISIL's specialized emerging market teams.

The global delivery model operates on a hub-and-spoke system. Mumbai remains the mothership, but CRISIL has built specialized centers of excellence: Pune for global research, Gurgaon for risk analytics, Buenos Aires for Latin American markets. This isn't just about cost—it's about building deep, specialized expertise that clients can't replicate in-house.

The business model's beauty lies in its interconnections. A corporate client who comes for a credit rating might also need research services. A bank using CRISIL's risk models might also subscribe to its industry research. An investor relying on CRISIL ratings might also purchase customized analytics. Each product reinforces the others, creating switching costs that make clients sticky.

The innovation pipeline reveals where CRISIL sees its future. Environmental, Social, and Governance (ESG) ratings, approved by SEBI in 2024, represent a massive new market. As sustainable investing goes mainstream, every company will need ESG ratings just as they need credit ratings today. CRISIL's early mover advantage here could replicate its dominance in traditional ratings.

The data advantage compounds over time. With over three decades of rating history, CRISIL possesses one of the most comprehensive databases of Indian corporate credit performance. This data becomes the training set for machine learning models, the basis for predictive analytics, the foundation for risk models. New entrants can't buy this history; they have to build it year by year.

Pricing power remains robust despite competition. CRISIL can charge premium prices because switching costs are high—investors have learned to interpret CRISIL ratings, regulators have built rules around them, and issuers have established relationships with rating committees. This isn't monopolistic exploitation; it's the economics of a network where everyone benefits from standardization.

The talent leverage model is particularly clever. CRISIL hires fresh graduates at Indian salaries, trains them to global standards, and bills them out at rates that would make a Manhattan consultant jealous. The employees win (global exposure, rapid learning), the clients win (high-quality work at reasonable prices), and CRISIL wins (enormous margins on human capital).

By 2024, CRISIL has evolved from a single-product company rating Indian bonds to a diversified analytical powerhouse serving global markets. Yet the core business model remains unchanged: transform data into judgment, judgment into trust, and trust into recurring revenues. It's a formula that has worked for three decades and shows no signs of breaking.

VIII. Modern Era & Digital Transformation (2014-2024)

February 2016 marked a symbolic transition: McGraw Hill Financial officially changed its name to S&P Global, acknowledging that the ratings business had become more valuable than the publishing empire that spawned it. For CRISIL, this meant being part of a pure-play financial intelligence company rather than a conglomerate. The message was clear: data and analytics were the future, and CRISIL was at the center of that future.

The regulatory landscape shifted dramatically. SEBI's new regulations required the separation of rating operations into a wholly-owned subsidiary, CRISIL Ratings Ltd. This wasn't bureaucratic hassle—it was about preventing conflicts of interest between ratings and consulting services. CRISIL adapted smoothly, using the restructuring to actually strengthen governance and independence.

The 2020 acquisition of Greenwich Associates LLC for an undisclosed amount (market estimates suggested around $550 million) was CRISIL's boldest move yet. Greenwich brought proprietary benchmarking data and deep relationships with institutional investors—exactly the kind of high-value, sticky revenue streams that complement ratings. This wasn't just buying revenue; it was buying relationships that take decades to build.

Digital transformation accelerated during the COVID-19 pandemic, but CRISIL had been preparing for years. The company invested heavily in artificial intelligence and machine learning, not to replace analysts but to augment them. When rating a company, algorithms now flag anomalies in financial statements, identify peer comparisons, and predict default probabilities—but human judgment still makes the final call.

The 2024 performance shows the strategy working: revenues of ₹32.6 billion, with consistent margin expansion despite investing heavily in technology. The company processes over 10 million data points daily, runs thousands of risk models, and delivers insights to clients across 40 countries. This scale would have been unimaginable with traditional analyst-driven models.

ESG ratings emerged as the next frontier. With SEBI approval in April 2024, CRISIL became one of the few entities authorized to provide ESG scores in India. This isn't just another product—it's potentially as transformative as credit ratings were in 1988. As sustainable investing goes mainstream, every company, fund, and financial instrument will need ESG assessment.

The sustainable finance focus goes beyond ratings. CRISIL now advises governments on green bond frameworks, helps companies develop sustainability strategies, and provides climate risk analytics to insurers. This positions CRISIL at the intersection of finance and sustainability—exactly where the next decade's growth will emerge.

The technology stack transformation has been profound. CRISIL built proprietary platforms that clients can access directly—no more emailing PDF reports. Real-time dashboards, API integrations, automated alerts—the company transformed from a report producer to a platform provider. This isn't just better service; it's creating switching costs that lock in clients.

Generative AI adoption, accelerated in 2024, is changing the game again. CRISIL's analysts now use AI to draft initial research reports, analyze earnings calls, and extract insights from thousands of documents. What once took weeks now takes hours. But CRISIL is careful to position AI as augmentation, not replacement—the "CRISIL judgment" remains the product clients pay for.

The geographic footprint evolved strategically. While maintaining India as the core, CRISIL expanded in markets where it had unique advantages: other emerging Asian markets where Indian expertise translates, the Middle East where infrastructure financing booms, and Latin America where S&P connections open doors. This isn't empire building; it's careful expansion where competitive advantages exist.

The competitive response has been interesting. Indian competitors like ICRA (Moody's subsidiary) and CARE have grown, but CRISIL maintains its premium positioning. International players struggle to compete in India without local presence. Fintech startups promising to "disrupt ratings with AI" have learned that trust can't be algorithmic—it must be earned over decades.

The partnership ecosystem expanded beyond S&P. CRISIL now collaborates with technology providers, data vendors, and even competitors on certain products. The company learned that in the platform economy, sometimes competition and cooperation aren't mutually exclusive.

The talent strategy evolved to match digital demands. CRISIL now hires as many technologists as financial analysts. The company established partnerships with IITs and IIMs, creating specialized courses in credit analysis and risk management. This isn't just recruitment; it's building the next generation of the talent ecosystem.

Looking at 2024 revenue composition, the transformation is complete: while ratings remain the profit engine, the company now generates significant revenues from subscriptions (recurring), platforms (scalable), and advisory (high-value). This diversification doesn't dilute focus—each business reinforces the core franchise of turning data into trusted judgment.

The modern CRISIL is unrecognizable from its 1988 origins, yet the mission remains unchanged: making markets function better through independent analysis. The tools have evolved from spreadsheets to AI, the market has expanded from Mumbai to the world, but the core value proposition endures—in markets built on trust, CRISIL remains the keeper of that trust.

IX. Competitive Landscape & Market Position

Stand at the 26th floor of CRISIL House in Mumbai's Powai district and look out across the city's financial landscape. To the south, in Bandra-Kurla Complex, sits ICRA's offices—Moody's Indian subsidiary watching every move CRISIL makes. Further south in Fort, CARE Ratings plots its comeback from reputational damage. And scattered across the city, smaller players like India Ratings (Fitch's arm) and Brickwork Ratings fight for scraps. This geography tells the story of Indian credit rating—a market CRISIL created and still dominates.

CRISIL's market cap of Rs 361 billion is almost five times bigger than ICRA (Rs 71 bn) and ten times bigger than CARE Ratings (Rs 37 bn), with market share of over 60%. This isn't just market leadership; it's market dominance that compounds on itself.

The first-mover advantage from 1987 created network effects that are nearly impossible to overcome. Every year CRISIL operates, its rating history becomes more valuable. Every company it rates adds to its database. Every investor who learns to interpret CRISIL ratings becomes less likely to switch. This isn't monopolistic behavior—it's the natural economics of standards. Just as QWERTY keyboards persist despite better alternatives, CRISIL ratings persist because everyone has learned to use them.

CRISIL vs ICRA represents the classic battle between first-mover and deep pockets. ICRA, 52% owned by Moody's, has the backing of a global giant and access to sophisticated methodologies. Yet it remains a distant second, unable to overcome CRISIL's three-year head start and deeper market relationships. ICRA focuses on niches like structured finance where Moody's expertise provides genuine differentiation, but in the bread-and-butter corporate rating business, CRISIL's dominance remains unchallenged.

CARE Ratings tells a cautionary tale. Once a credible challenger, CARE's reputation was damaged by involvement in high-profile scandals such as IL&FS, DHFL, ZEE, and RCOM, significantly tarnishing the credibility of their credit rating processes. The market is unforgiving—one bad rating can destroy decades of credibility. Over the last five years, CARE's revenue grew by just 4%, while its profitability declined by 25%.

India Ratings, backed by Fitch, occupies an interesting niche. Rather than competing head-on with CRISIL in corporate ratings, it focuses on sectors where Fitch's global expertise matters—infrastructure, structured finance, financial institutions. This strategy of competing where you have advantage, not where the market is largest, shows sophisticated thinking but limits growth potential.

The S&P Global backing provides CRISIL advantages beyond capital. When Indian companies want to access international markets, a CRISIL rating that meets S&P standards carries weight. When foreign investors evaluate Indian credits, they trust CRISIL's methodology because it mirrors what they know from S&P. This creates a virtuous cycle—international credibility drives domestic dominance, which reinforces international credibility.

For CRISIL, a significant portion of its revenue (over 65%) comes from its analytics and research business, heavily supported by S&P. This diversification is critical—while CARE and ICRA remain largely dependent on ratings revenues, CRISIL has built multiple revenue streams that reduce dependence on any single business line.

Local vs global dynamics create interesting tensions. Pure domestic players argue they better understand Indian business realities—the importance of promoter reputation, the impact of monsoons, the nuances of priority sector lending. But markets have spoken: investors prefer the global standards and methodologies that CRISIL (via S&P) and ICRA (via Moody's) provide. Local knowledge matters, but global credibility matters more.

The regulatory environment under SEBI oversight acts as both protector and constraint. SEBI accreditation requirements make new entry nearly impossible—you need track record to get accreditation, but you need accreditation to build track record. This protects incumbents but also subjects them to strict oversight. SEBI can mandate rating categories, set pricing caps, and investigate conflicts of interest. It's a gilded cage—profitable but constrained.

Network effects in the rating business are subtle but powerful. A company rated AAA by CRISIL can reference that rating in every investor presentation, loan negotiation, and bond issuance. Changing to another agency means re-educating every stakeholder about what the new rating means. These switching costs aren't monetary—they're cognitive, and therefore even more powerful.

The competitive dynamics reveal a market in equilibrium. CRISIL dominates but can't abuse that dominance without regulatory backlash. Competitors survive by finding niches but can't challenge the core franchise. New entrants are essentially locked out. International players can't enter without local partners. It's a market structure that rewards the incumbent while providing just enough competition to avoid regulatory intervention.

Looking forward, the competitive landscape seems frozen. Barring major scandals or regulatory upheaval, CRISIL's dominance appears unassailable. The question isn't whether CRISIL will maintain leadership, but whether the rating business itself will remain relevant as alternative assessment methods emerge. But even there, CRISIL's diversification into analytics, ESG ratings, and risk advisory suggests it's preparing for a world beyond traditional credit ratings.

X. Playbook: Key Strategic Lessons

If you wanted to build the next CRISIL—to create critical financial infrastructure in an emerging market—what would the playbook look like? The answer isn't found in MBA textbooks but in the subtle moves CRISIL made over three decades, decisions that seemed small at the time but compounded into an unassailable moat.

Lesson 1: Building trust in emerging markets requires institutional DNA, not just capital. CRISIL wasn't started by entrepreneurs in a garage but by ICICI, UTI, SBI, and LIC—the Mount Rushmore of Indian financial institutions. This wasn't about money (though that helped); it was about borrowed credibility. In markets where trust is scarce, you can't build it from scratch—you must inherit it from institutions that already possess it.

Lesson 2: The power of patient institutional backing. Most startups die from impatience—VCs want returns in 5-7 years. CRISIL's institutional sponsors understood they were building infrastructure, not just a business. They could afford to lose money for years while educating the market about credit ratings. This patient capital is the secret weapon of category-creating companies in emerging markets.

Lesson 3: Independence is a product feature, not just governance. CRISIL understood that its value lay in independence. Every time it resisted pressure to inflate a rating, every time it downgraded a powerful company, it was building its true product—trust. The S&P acquisition could have destroyed this, but both parties understood that CRISIL's independence was its value. Destroying independence would be like Coca-Cola changing its formula.

Lesson 4: High-margin ratings vs high-volume research—the portfolio approach. CRISIL built a brilliant portfolio: ratings for margins (28% of revenue but 51% of profits) and research for growth. This wasn't diversification for its own sake but strategic design—the high margins from ratings funded expansion into lower-margin but scalable businesses. It's the same strategy Amazon used with AWS funding retail expansion.

Lesson 5: Timing market infrastructure plays. CRISIL launched in 1987, four years before liberalization, which seems early. But infrastructure must precede the market it serves. By the time India liberalized in 1991, CRISIL had worked out its methodologies, built its reputation, and educated the market. When demand exploded, CRISIL was the only game in town. Being early is a feature, not a bug, in infrastructure plays.

Lesson 6: Managing regulatory relationships without capture. CRISIL maintains a delicate dance with regulators—close enough to influence policy, independent enough to avoid capture. The company helps SEBI design regulations, provides technical expertise, and acts as the de facto standard setter. But it never crosses the line into regulatory capture that would destroy its credibility. This balance is perhaps the hardest aspect of building financial infrastructure.

Lesson 7: The compound value of data in financial services. Every rating CRISIL issues adds to a database that goes back to 1988. This historical data becomes the training set for risk models, the benchmark for new ratings, the basis for research. New entrants can copy methodologies, hire talent, even get regulatory approval—but they can't copy 35 years of data. In financial services, data compounds like interest.

Lesson 8: Strategic value of selling to global leaders. The S&P acquisition wasn't a sellout—it was strategic leverage. CRISIL gained global credibility, methodological sophistication, and access to international markets while maintaining operational independence. The lesson: in winner-take-all markets, aligning with global leaders can be more valuable than remaining independent.

Lesson 9: Culture survives ownership changes through structural design. Despite majority ownership by S&P, CRISIL maintains its Indian DNA. How? Through careful structural design—keeping the company publicly listed, maintaining Indian management, preserving independent rating committees. Culture isn't preserved through promises but through structures that make cultural change costly.

Lesson 10: The defensive power of switching costs in B2B markets. CRISIL's real moat isn't regulatory approval or brand—it's the cognitive switching cost of moving to another rating agency. Every investor who has learned to interpret CRISIL ratings, every banker who has built models around them, every company that has educated stakeholders about their CRISIL rating—they all become defenders of the status quo. These cognitive switching costs are more powerful than any contract.

Lesson 11: Platforms beat products in financial infrastructure. CRISIL evolved from a rating agency (product) to a platform that others build upon. Banks use CRISIL ratings in their risk models. Regulators reference them in rules. Investors incorporate them in mandates. Once you become the platform others build upon, displacement becomes nearly impossible.

Lesson 12: The virtue of boring businesses with regulatory moats. Credit rating isn't sexy. It doesn't have the excitement of fintech or crypto. But this boring nature is a feature—it doesn't attract excessive competition, regulatory scrutiny, or disruption attempts. The best infrastructure businesses are boring enough to be ignored but critical enough to be irreplaceable.

The CRISIL playbook isn't about building a unicorn—it's about building infrastructure that becomes so embedded in the market fabric that its absence becomes unthinkable. It's about playing a game where time is your friend, where every year of operation deepens your moat, where patience is rewarded with monopoly-like economics. In a world obsessed with disruption, CRISIL reminds us that some things are better built to last than built to exit.

XI. Bear vs Bull Case Analysis

Walk into any institutional investor's office in Mumbai and ask about CRISIL, and you'll get two violently different takes—often from the same person. The bull sees India's financial infrastructure play of the century. The bear sees a sunset industry facing technological obsolescence. Both are right, which is what makes CRISIL fascinating.

The Bull Case: Riding the India Growth Story

Start with the macro: India's corporate bond market is still just 17% of GDP versus 123% in the US. As this gap closes over coming decades, every basis point of growth requires credit ratings. CRISIL owns the tollbooth on this highway. The math is compelling—if India's bond market merely doubles as a percentage of GDP, CRISIL's addressable market quadruples.

The S&P Global ownership isn't baggage—it's rocket fuel. As Indian companies increasingly access global markets, they need ratings that international investors understand. CRISIL provides Indian credibility with S&P methodology. No competitor can replicate this combination. It's like owning the only translator in a room where two languages are being spoken.

The regulatory moat keeps deepening. Every year, SEBI adds new requirements for ratings—municipal bonds, infrastructure investment trusts, ESG scores. Each mandate is essentially a license for CRISIL to print money. The regulator has become CRISIL's unofficial sales force, mandating demand for its products.

Operating leverage is beautiful in this business. The marginal cost of one more rating approaches zero, but pricing remains robust. As volumes grow, margins expand. CRISIL's EBITDA margins in the ratings business exceed 50%. Find another business with those economics that isn't software or drugs.

The pivot to analytics and ESG is working. These aren't desperate attempts at diversification—they're natural extensions leveraging the same core competency of turning data into judgment. ESG ratings could be as big as credit ratings within a decade. CRISIL has first-mover advantage in a market that doesn't exist yet.

International expansion through the S&P network provides optionality. CRISIL isn't trying to rate US corporates, but it's becoming the go-to source for emerging market expertise. A hedge fund in Connecticut analyzing Indian banks doesn't call Goldman Sachs—they call CRISIL.

The Bear Case: Concentration Risk and Technological Disruption

Start with ownership concentration: S&P owns 67.8%. If S&P decides to integrate CRISIL more tightly, minority shareholders have no recourse. If S&P gets into regulatory trouble globally (remember the 2008 financial crisis lawsuits), CRISIL gets tainted by association. You're not just betting on CRISIL—you're betting on S&P's governance.

Competitive pressure on pricing is real and growing. SEBI periodically reviews rating fees, and there's constant pressure to cap prices. As the market matures, commoditization is inevitable. Look at what happened to audit fees—the same could happen to rating fees.

Regulatory changes are a double-edged sword. Yes, SEBI mandates create demand, but SEBI can also destroy economics overnight. One regulation separating ratings from advisory already forced restructuring. What if SEBI mandates rotating rating agencies? Or introduces price caps? Regulatory giveth, and regulatory taketh away.

Technology disruption lurks everywhere. Machine learning models can increasingly predict defaults better than human analysts. Blockchain promises to make financial data transparent without intermediaries. Alternative data sources—satellite imagery, social media sentiment, transaction data—provide real-time insights versus quarterly rating reviews. The rating agency model looks increasingly antiquated.

Conflicts of interest remain unresolved. The issuer-pays model is fundamentally flawed—rating agencies are paid by the companies they rate. Every attempt to fix this (investor-pays, regulator-pays) has failed, but that doesn't mean the current model is sustainable. One major scandal could trigger regulatory overhaul.

Market saturation is approaching. Most large Indian companies are already rated. Growth must come from smaller companies (lower fees), new products (unproven economics), or international markets (fierce competition). The easy growth is behind CRISIL.

Reputation risk is asymmetric. It takes decades to build credibility but one bad rating to destroy it. Ask CARE about IL&FS. Ask Moody's about 2008. In a business built on trust, reputation risk is existential risk.

The Nuanced Reality

The truth, as always, lies between extremes. CRISIL is neither the perfect monopoly bulls imagine nor the disruption target bears fear. It's a mature business with monopoly-like characteristics in a growing but increasingly regulated market.

The India opportunity is real but will unfold over decades, not quarters. Patient investors will be rewarded; traders will be frustrated. The S&P relationship is net positive but comes with governance overhead that pure-play Indian companies don't face.

Technology will transform the rating business but probably not destroy it. Just as equity research survived the internet, ratings will survive AI—transformed but not replaced. The need for independent judgment in credit markets is permanent; the method of delivering that judgment will evolve.

The most likely scenario: CRISIL remains dominant in Indian ratings while successfully pivoting to higher-growth adjacencies like ESG and analytics. Returns will be solid but not spectacular—think 12-15% annual returns, not 25%+. It's a widows-and-orphans stock dressed up as a growth story.

For investors, CRISIL represents a bet on Indian financial deepening with downside protection from regulatory moats. It's not without risks, but the risk-reward remains favorable for those who understand they're buying infrastructure, not innovation.

XII. Power & Lessons for Founders

Sit down with any founder building in emerging markets, and eventually the conversation turns to CRISIL. Not because they want to build a rating agency, but because CRISIL cracked the code on something fundamental: how to build a category-defining company in a market that doesn't yet understand the category. The lessons transcend industry.

The Infrastructure Mindset: Building for Decades, Not Exits

Most founders think in funding rounds and exit multiples. CRISIL's founders thought in decades and market development. When Pradip Shah pitched rating services to skeptical CFOs in 1988, he wasn't selling a product—he was evangelizing a concept. This requires a different kind of patience, what venture capitalists call "missionary" versus "mercenary" founders. But here's what VCs miss: in emerging markets, missionaries build monopolies.

The lesson for founders: if you're building infrastructure in an emerging market, your competition isn't other startups—it's the status quo. Your first thousand customers won't buy your product; they'll buy into your vision of how the market should work. Price accordingly. CRISIL could have underpriced to gain adoption but chose to price for value, even when that meant slower initial growth. Cheap infrastructure becomes weak infrastructure.

Category Creation in Emerging Markets: Education Before Revenue

CRISIL spent its first years educating the market about what ratings were, why they mattered, how to use them. This wasn't marketing—it was market creation. They published research, conducted seminars, trained bankers, advised regulators. Revenue was a byproduct of education, not the goal.

Modern founders can learn from this sequencing. Uber didn't start by optimizing unit economics—it started by teaching people to trust strangers' cars. Airbnb didn't begin with dynamic pricing—it began by normalizing staying in strangers' homes. In emerging markets, the education phase is even longer because you're not just changing behavior—you're creating it.

Strategic Value of Selling to Global Leaders

When McGraw-Hill approached CRISIL, conventional wisdom said "stay independent." But CRISIL understood something profound: in winner-take-all markets, independence is overrated. What matters is strategic leverage. S&P didn't just bring capital—it brought credibility that would have taken decades to build independently.

The lesson isn't "sell out early" but "understand your strategic value." If you've built critical infrastructure in an emerging market, you're valuable to global players who need that infrastructure to expand. But—and this is critical—you're only valuable if you maintain what made you special. CRISIL kept its Indian identity, management, and independence post-acquisition. It sold ownership but not soul.

Culture Through Structure, Not Slogans

Every acquisition promises to "maintain the culture." Most fail. CRISIL succeeded because it built structural protections: staying publicly listed (accountability to minority shareholders), keeping Indian management (operational independence), maintaining separate rating committees (decision independence). Culture wasn't preserved through promises but through architecture that made cultural change expensive.

Founders facing acquisition should study this playbook. Don't negotiate for cultural promises—negotiate for structural protections. Keep the company listed if possible. Maintain separate boards or committees for critical decisions. Create reporting lines that preserve autonomy. Make it structurally difficult, not just politically incorrect, to destroy what you've built.

The Compound Effect of Trust

In businesses built on trust—financial services, healthcare, education—time is your friend in a way it isn't in technology. Every year CRISIL operated without scandal added to its trust bank account. This trust compounds like interest, creating a moat that deepens with time rather than erodes.

Founders in trust-based businesses should optimize for longevity over growth. Better to grow 20% annually for 20 years than 100% for 5 years followed by collapse. This requires resisting the venture capital growth-at-all-costs mentality. It means saying no to revenue that could compromise trust. It means playing a different game than your Silicon Valley peers.

The Power of Boring

CRISIL is boring. Credit ratings are boring. Financial infrastructure is boring. This boring nature is a superpower—it repels casual competitors, avoids regulatory scrutiny, and attracts patient capital. Exciting businesses attract competition; boring businesses build monopolies.

The next great emerging market fortunes won't be built in sexy spaces like social media or e-commerce—those will be won by global giants. They'll be built in boring infrastructure plays that require deep local knowledge and regulatory navigation: credit bureaus, commodity exchanges, bond markets, clearing houses. Boring is beautiful if you're building for decades.

Network Effects in B2B Markets

Consumer network effects are obvious—more Facebook users make Facebook more valuable. B2B network effects are subtle but powerful. Every company CRISIL rates makes its ratings more valuable (comparison data). Every investor using CRISIL ratings makes them more necessary (market standard). Every regulation referencing CRISIL ratings makes them more embedded (structural lock-in).

Founders should design for these multi-sided network effects from day one. Don't just acquire customers—make customers need each other through your platform. Don't just serve regulators—become embedded in regulations. Don't just provide data—become the standard others reference.

The Ultimate Lesson: Patience Pays

In a world of overnight unicorns and quick flips, CRISIL reminds us that the biggest outcomes come from the longest journeys. It took 18 years from founding to S&P acquisition. It took another decade to build the analytics business. It's taking another decade to build ESG ratings. Each phase built on the last, creating compounding value that no competitor can quickly replicate.

For founders, the message is clear: if you're building infrastructure in an emerging market, think in decades. If you're creating a new category, prepare for years of education before revenue. If you're building on trust, optimize for longevity over growth. And if you have the patience for this journey, the rewards are monopoly-like economics in markets too boring for Silicon Valley to care about.

That's the ultimate CRISIL lesson: in emerging markets, patience isn't just a virtue—it's a strategy.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube