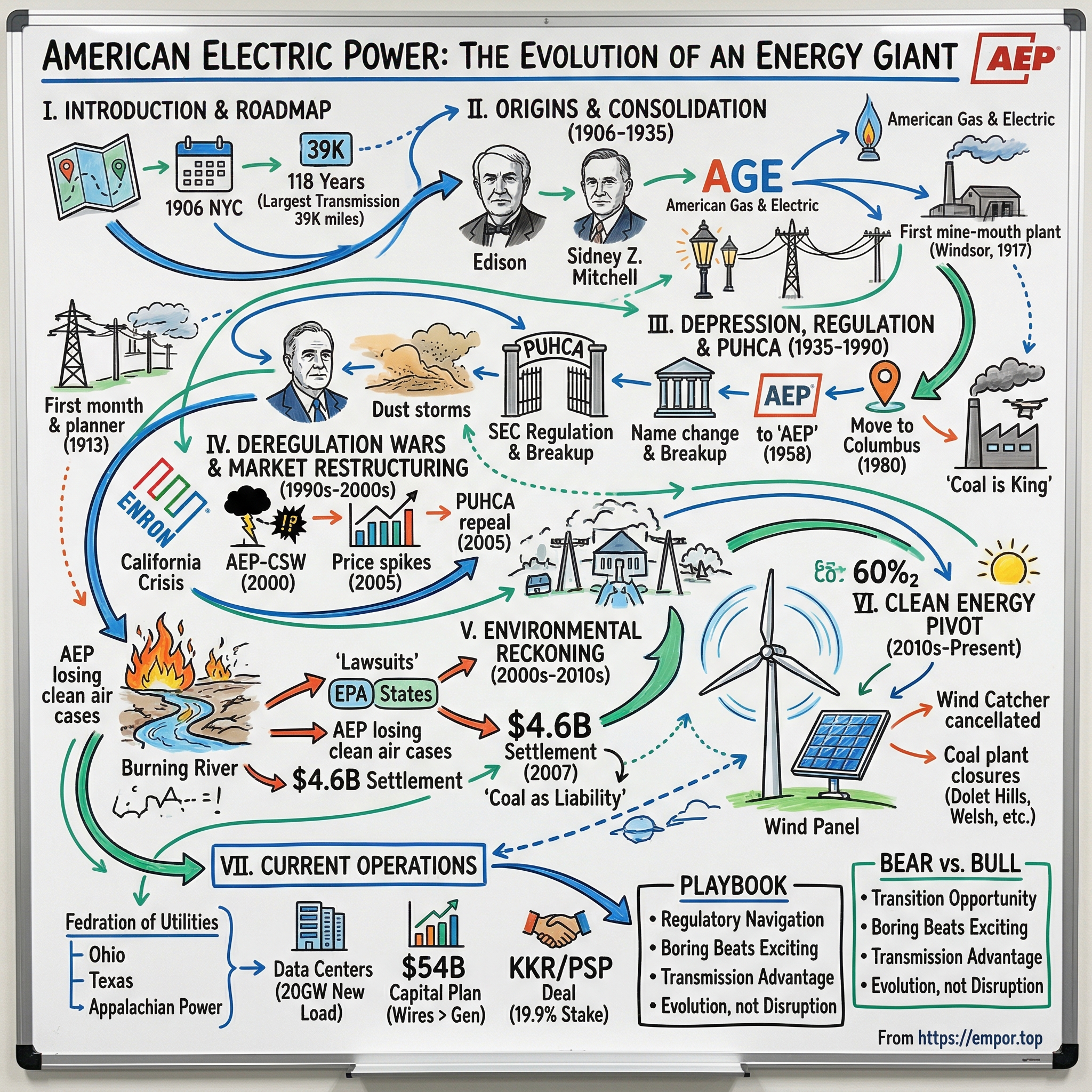

American Electric Power: The Evolution of an Energy Giant

I. Introduction & Episode Roadmap

Picture this: December 1906, New York City. The electric age is barely two decades old. Gas lamps still illuminate most American streets, but in a Manhattan boardroom, three men are architecting what would become the backbone of American power. Sidney Z. Mitchell, a protégé of Thomas Edison himself, sits across from financiers Richard Breed and Harrison Williams. They're not just starting another utility company—they're envisioning an empire that would light up the heartland.

Fast forward 118 years. American Electric Power now commands the nation's largest electricity transmission system—39,000 miles of high-voltage lines that could circle the Earth one and a half times. The company serves over 5 million customers across 11 states, wielding nearly 38,000 megawatts of generating capacity. To put that in perspective, that's enough power to supply every home in California during peak summer demand.

But here's the fascinating paradox: How did a company born in the era of unregulated monopolies not just survive but thrive through trust-busting, the Great Depression, wartime controls, deregulation wars, environmental lawsuits, and now, the existential challenge of decarbonization? The answer reveals fundamental truths about American capitalism, the nature of essential services, and why some companies become too important to fail.

This is a story of reinvention through regulation—a seemingly contradictory narrative where government constraints actually created competitive moats. It's about how a coal-burning giant is attempting to transform into a renewable energy company while still keeping the lights on for 10% of America's Eastern grid. Most importantly, it's a masterclass in navigating the impossible trilemma that defines modern utilities: keeping power reliable, affordable, and increasingly, sustainable.

We'll trace AEP's evolution from Edison's shadow through the regulatory labyrinth of the 20th century, into the deregulation experiments that nearly broke the industry, and finally to today's precarious position straddling the old carbon economy and the new energy future. Along the way, we'll uncover why utilities keep returning to regulated models after flirting with free markets, how transmission lines became more valuable than power plants, and what happens when a century-old business model collides with Silicon Valley-style disruption.

The chapters ahead reveal not just corporate history but the hidden architecture of American power—literally and figuratively. Because to understand AEP is to understand how America electrified itself, why your power bill looks the way it does, and where the $2 trillion energy transition might actually lead.

II. Origins & The Age of Consolidation (1906–1935)

December nights in the frozen heartland, 1906. While most Americans still lived by candlelight and gas lamps, Sidney Z. Mitchell was sketching electrical grids on napkins in Manhattan restaurants. The story of American Electric Power (AEP) began on December 20, 1906, when it was founded as American Gas and Electric Company (AGE). But this wasn't just another utility startup—it was the beginning of an empire that would wire America.

An 1883 graduate of the U.S. Naval Academy, Mitchell had installed the first incandescent electric lighting system on a U.S. naval vessel while stationed aboard the U.S.S. Trenton. After leaving the navy in 1885, Mitchell had met Thomas Edison and started working for him in New York City. This wasn't just a job change; it was an apprenticeship with the wizard of electricity himself. In New York, Sidney Mitchell heard from two school friends about the opportunity for organizing electric light companies under Edison licenses. He went to see Thomas A. Edison, who, impressed by the young man's enthusiasm, hired him to work in the Goerck Street factory to learn about construction, testing, and shipping of generators and to attend a night school Edison conducted for training electrical engineers. Sidney Mitchell also learned the basics of distributing electricity by working as a laborer for one of New York's leading contractors. The young man and the young electric industry were to grow up together.

The timing was everything. As president of the United States from 1901 to 1907, Theodore Roosevelt denounced such business combinations. By 1906, however, Roosevelt had come to believe that, with proper government regulation, the consolidation of businesses could be beneficial to the public interest. This shift in political winds created the perfect moment for consolidation.

Richard E. Breed, Harrison Williams, and Sidney Z. Mitchell met in 1906 to consider forming a holding company to buy the 23 small companies held by Electric Company of America, a failing venture whose directors hadn't grasped the economics of the emerging industry. After some negotiation, Electric Company of America agreed to sell its assets for $6.28 million to American Gas & Electric Company (AG & E). The sale was completed in January of 1907, with Breed and Williams as board directors of AG & E, Mitchell as chairman, and Henry L. Doherty--later to begin his own chain of electric companies--as president until 1910, when Breed stepped in.

What they acquired was a disaster. The acquired companies were a varied lot, including nine utilities in Pennsylvania; four in New Jersey; and two each in New York, West Virginia, Illinois, Indiana, and Ohio. They supplied services including electricity, gas, water, steam, and ice. For the most part, the companies' service was poor, their rates high, and their equipment faulty. Customers desiring service often had to invest in the company since the operating company lacked financing to extend its lines.

Mitchell understood something his contemporaries missed: electricity wasn't just another commodity—it was infrastructure that would reshape civilization. His strategy was surgical. By 1910 Mitchell had sold all of the gas properties included in the original acquisitions, a policy the company consistently followed in later years. He also sold some electric companies that could not be merged readily into a unified system. The largest of these isolated AG & E operations was in Rockford, Illinois. Retaining the companies in Marion and Muncie, Indiana; Bridgeport, Ohio; Atlantic City, New Jersey; and Scranton, Pennsylvania, Mitchell began acquiring smaller, adjoining companies consolidating their operations and extending their lines into neighboring communities.

The real breakthrough came in building connections. Having created several core markets in which to expand, AG & E began to construct long-range transmission lines to tie its properties together. An early step in consolidation was the construction of a 32-mile-long tie-line between Muncie and Marion. This wasn't just wire stringing—it was the physical manifestation of a new business model: economies of scale through interconnection.

Then came 1917, the year that changed everything. The nation's first major "mine-mouth" power plant, the Windsor Plant near Wheeling, W.Va., which began operating in 1917; the nation's first long-distance high-voltage transmission line, a 138-kilovolt (kV) line, also completed in 1917. These weren't incremental improvements—they were paradigm shifts. The mine-mouth plant concept meant building generation right at the coal source, eliminating transportation costs. The high-voltage transmission line meant power could travel hundreds of miles efficiently, turning regional utilities into interstate empires.

Mitchell's philosophy was deceptively simple but revolutionary for its time. "The only way that I know to make money in the public-utility business today, is by following the large volume of business, low cost of operation, low cost of money, low rates to the customers, and small margin of profit idea". This wasn't the robber baron playbook of squeezing customers for maximum profit—it was infrastructure capitalism, where scale and efficiency created value for everyone.

The results spoke volumes. AG&E had increased the number of kilowatt hours it provided from 53 million in 1907 to 427 million in 1917. In a decade, they'd grown eight-fold, not through price gouging but through relentless expansion and operational excellence.

By the 1920s, Mitchell's consolidation machine was in full swing. The company expanded beyond its Midwest base, acquiring properties in Virginia, West Virginia, and Kentucky by 1926. Each acquisition wasn't just about adding customers—it was about creating an interconnected system where power could flow from where it was cheapest to generate to where it was most needed.

The Edison connection ran deeper than just Mitchell. One such man was Samuel Insull, another Edison protégé who was revolutionizing the industry in Chicago with demand-based pricing and massive steam turbines. These Edison alumni weren't competing so much as collectively inventing the modern utility industry, each taking different approaches to the same fundamental challenge: how to electrify America profitably.

What made AG&E different was its focus on transmission—the highways of electricity. While others focused on generation or local distribution, Mitchell understood that whoever controlled the transmission lines controlled the industry. Those early high-voltage lines weren't just infrastructure; they were the moat that would protect AG&E's business model for the next century.

As the 1920s roared on, AG&E became a consolidation powerhouse. The company wasn't just buying utilities; it was creating America's first truly integrated power system. By interconnecting previously isolated systems, AG&E could balance load across regions, share generation reserves, and achieve economies of scale that standalone utilities couldn't match.

The genius was in the network effects. Each new connection made the entire system more valuable. A power plant failure in Ohio could be backed up by generation in Indiana. Excess nighttime capacity in one region could serve industrial demand in another. This wasn't just operational efficiency—it was the birth of grid reliability as we know it today.

But storm clouds were gathering. By the early 1930s, utility holding companies had become empires unto themselves. By the late 1920s, 10 holding companies controlled 75 percent of the American electricity industry. The stage was set for a confrontation between the utility magnates and a new political force that would reshape the industry forever: Franklin Delano Roosevelt and his New Deal.

III. Depression, Regulation & The PUHCA Era (1935–1990)

The sky was falling in 1932. Not metaphorically—literally, as dust storms blackened the Midwest while the nation's economy collapsed. For American Gas & Electric, the threat wasn't dust but Washington. By 1932, eight of the largest utility holding companies controlled 73 percent of the investor-owned electric industry. Three companies alone controlled half the entire U.S. utility business. AG&E, now one of the giants, had become exactly what Progressive reformers feared: an interstate empire beyond the reach of any single state regulator.

Enter Franklin Delano Roosevelt, carrying a grudge and a plan. The grudge came from his battles with utility magnates as Governor of New York. The plan would reshape American capitalism. On March 12, 1935, President Franklin D. Roosevelt released a report he commissioned by the National Power Policy Committee. This report became the template for the PUHCA.

The Wheeler-Rayburn bill, introduced in February 1935, wasn't just regulation—it was dismemberment. The Public Utility Holding Company Act of 1935 (PUHCA), also known as the Wheeler-Rayburn Act, was a US federal law giving the Securities and Exchange Commission authority to regulate, license, and break up electric utility holding companies. It limited holding company operations to a single state, thus subjecting them to effective state regulation. It also broke up any holding companies with more than two tiers, forcing divestitures so that each became a single integrated system serving a limited geographic area.

The political battle was vicious. The political battle over its passage was one of the bitterest of the New Deal, and was followed by eleven years of legal appeals by holding companies led by the Electric Bond and Share Company, which finally completed its breakup in 1961. Utility executives deployed every weapon: lawsuits, lobbying, even fake telegrams to Congress. But on August 26, 1935, Roosevelt signed PUHCA into law, fundamentally altering the trajectory of American utilities.

For AG&E, PUHCA meant existential choices. The law's geographic restrictions threatened to tear apart the interstate system Mitchell had spent three decades building. Another purpose of the PUHCA was to keep utility holding companies engaged in regulated businesses from also engaging in unregulated businesses. The company had to choose: break apart voluntarily or fight and risk being broken apart punitively.

Mitchell, now in his seventies, chose adaptation over confrontation. While Electric Bond & Share fought PUHCA in courts for decades, AG&E quietly restructured. The company divested non-contiguous properties, simplified its corporate structure, and most importantly, consolidated its operations in a connected service territory spanning from Michigan to Virginia. This wasn't retreat—it was strategic consolidation.

The transformation accelerated under new leadership. Mitchell's role in shaping federal regulation hadn't gone unnoticed—he had been instrumental in establishing the principles upon which was based the Federal Power Act of 1920. This regulatory savvy would prove invaluable as AG&E navigated the PUHCA maze.

Then came 1958, a year of symbolic rebirth. In 1958, American Gas and Electric Company officially changed its name to American Electric Power (AEP). The name change wasn't cosmetic—it reflected a fundamental shift. No longer a gas and electric conglomerate, AEP was now a pure-play electric utility, focused on what it did best: generating and transmitting power at massive scale.

The post-PUHCA decades saw AEP perfect the regulated monopoly playbook. Unable to expand geographically, the company went deep instead of wide. It built the nation's first 345-kilovolt transmission line in 1953, then the world's first 765-kilovolt line in 1969. These weren't just engineering achievements—they were competitive moats disguised as infrastructure.

The genius of AEP's strategy was turning regulatory constraints into advantages. State regulation meant guaranteed returns on capital investment. The more AEP invested in generation and transmission, the larger its rate base, the higher its allowed profits. It was capitalism with training wheels—competition was illegal, profits were guaranteed, and all you had to do was keep the lights on.

Coal became AEP's fuel of choice, not just for economic reasons but for strategic ones. The company's service territory sat atop some of America's richest coal seams. By building massive coal plants at the mine mouth—avoiding transportation costs—AEP could generate electricity cheaper than almost anyone. The 1973 Amos Plant in West Virginia, with its 1,300-megawatt units, became the world's largest coal-fired generator. Environmental consequences? That was tomorrow's problem.

The 1980 headquarters move from New York to Columbus, Ohio, was more than geographic. In 1980 AEP acquired Columbus and Southern Ohio Electric Company, located in the middle of its operating system, and moved its headquarters to Columbus, then the largest city it served. This wasn't just about being closer to operations—it was about cultural transformation. New York was finance; Columbus was engineering. New York was about deals; Columbus was about kilowatts.

In 1979, American Electric Power (AEP) confirmed the company would be moving their headquarters from New York City to Columbus, Ohio. This move was part of the 1968 acquisition deal to merge with the Columbus and Southern Ohio Electric Co (C&SOE). The move also reflected a deeper truth: AEP had become fundamentally a Midwest and Appalachian company, serving the industrial heartland with coal-fired power.

But the 1980s brought challenges that even regulatory protection couldn't prevent. By 1982, however, a recession severely affecting industry in AEP's territories caused a drop in industrial sales of 18 percent. Sales to other utilities declined by 20 percent. The rust belt was rusting, and AEP's biggest customers—steel, aluminum, chemicals—were shrinking or shutting down.

The company's response revealed both its strengths and limitations. Unable to grow through geographic expansion (thanks to PUHCA), unable to diversify into non-utility businesses (also thanks to PUHCA), AEP doubled down on what it could control: operational efficiency and transmission dominance. The company became obsessed with heat rates, capacity factors, and interconnection agreements—the mundane metrics that determined profitability in a regulated world.

Yet within these constraints, AEP thrived. By 1990, it had built the nation's largest transmission network, operated some of its most efficient coal plants, and delivered power more reliably than almost any other major utility. The company had turned PUHCA's prison into a palace, regulatory constraints into competitive advantages.

The irony was inescapable. PUHCA was designed to break up utility empires and limit their power. But for companies like AEP that adapted rather than fought, it created protected fiefdoms—regulated monopolies with guaranteed profits and captive customers. The law meant to increase competition had instead eliminated it, at least within service territories.

As the 1990s dawned, however, winds of change were stirring. In Washington, a new generation of policymakers, influenced by Reagan-era deregulation, began questioning whether PUHCA's protections were protections at all—or chains holding back innovation and efficiency. In California and Texas, experiments with electricity markets were beginning. The age of the regulated monopoly, which had seemed permanent, was about to face its greatest test.

IV. Deregulation Wars & Market Restructuring (1990s–2000s)

The lights went out in Houston on October 19, 1992. Not from a blackout, but from Enron's victory party. Kenneth Lay's energy trading giant had just secured the passage of the Energy Policy Act, and champagne corks were popping like miniature power surges. Removes obstacles to wholesale power competition in the Public Utilities Holding Company Act (PUHCA). Title III of the 1992 Energy Policy Act addresses alternative fuels. The law had done exactly what Enron wanted: Amends the Federal Power Act regarding FERC's wheeling authority to permit any person generating electric energy for sale for resale to apply to FERC for an order requiring a transmitting utility to provide transmission services to the applicant. Specifies general requirements for issuance of such an order.

This wasn't deregulation—it was selective liberation. The 1992 Energy Policy Act removed PUHCA obstacles but kept crucial protections in place. The Energy Policy Act of 1992, effective October 24, 1992, (102nd Congress H.R.776.ENR, abbreviated as EPACT92) is a United States government act. It was passed by Congress and set goals, created mandates, and amended utility laws to increase clean energy use and improve overall energy efficiency in the United States. The Act consists of twenty-seven titles detailing various measures designed to lessen the nation's dependence on imported energy, provide incentives for clean and renewable energy, and promote energy conservation in buildings. It reformed the Public Utility Holding Company Act of 1935 (PUHCA) to help small utility companies stay competitive with larger utilities and amended the Public Utility Regulatory Policies Act (PURPA) of 1978, broadening the range of resource choices for utility companies and outlined new rate-making standards.

For AEP, watching from Columbus, this represented both threat and opportunity. The company had spent decades perfecting the regulated monopoly model. Now merchant generators could build plants anywhere, traders could buy and sell power like pork bellies, and transmission access—AEP's crown jewel—had to be offered to competitors. The Energy Policy Act of 1992 (EPAct) laid the initial foundation for the eventual deregulation of the North American electricity market. The OASIS concept was originally conceived with the Energy Policy Act of 1992, and formalized in 1996 through Federal Energy Regulatory Commission (FERC) Orders 888 and 889.

AEP's response was characteristically bold: if you can't beat them, buy them. The company began eyeing Central and South West Corporation (CSW), a Dallas-based utility giant serving Texas, Oklahoma, Louisiana, and Arkansas. This wasn't just geographic expansion—it was strategic positioning for the coming market wars. CSW brought access to Texas's deregulated market, natural gas assets, and most importantly, trading expertise.

The merger negotiations began in 1997, but this wasn't a typical utility deal. On June 15, 2000, the merger between AEP & CSW took effect. For every 1 share of CSW stock, the CSW shareholder received .6 shares of AEP; for example, 100 shares of CSW stock would equate to 60 shares of AEP stock. On the day of the merger, AEP closed at $35 per share and CSW closed at $20.9375. The $10 billion transaction would create America's largest electricity company—a behemoth stretching from Virginia to the Mexican border.

But timing, as they say, is everything. As AEP and CSW navigated regulatory approvals through 1999 and 2000, California's electricity market was melting down in spectacular fashion. The 2000–2001 California electricity crisis, also known as the Western U.S. energy crisis of 2000 and 2001, was a period during which the U.S. state of California had a shortage of electricity supply, caused by market manipulations and capped retail electricity prices. The state suffered from multiple large-scale blackouts, one of the state's largest energy companies collapsed, and the economic fall-out greatly harmed Governor Gray Davis's standing.

The California crisis was deregulation's Chernobyl moment. On the state level, part of California's deregulation process, which was promoted as a means of increasing competition, was also influenced by lobbying from Enron, and began in 1996 when California became the first state to deregulate its electricity market. Energy deregulation put the three companies that distribute electricity into a tough situation. Energy deregulation policy froze or capped the existing price of energy that the three energy distributors could charge. Deregulating the producers of energy did not lower the cost of energy. Deregulation did not encourage new producers to create more power and drive down prices. Instead, with increasing demand for electricity, the producers of energy charged more for electricity. The producers used moments of spike energy production to inflate the price of energy. In January 2001, energy producers began shutting down plants to increase prices.

Enron's traders had turned California's market into a casino, using strategies with names that sounded like video game moves: "Fat Boy", "Death Star", "Forney Perpetual Loop", "Wheel Out", "Ricochet", "Ping Pong", "Black Widow", "Big Foot", "Red Congo", "Cong Catcher" and "Get Shorty". In a letter sent from David Fabian to Senator Boxer in 2002, it was alleged that: "There is a single connection between northern and southern California's power grids. I heard that Enron traders purposely overbooked that line, then caused others to need it. Next, by California's free-market rules, Enron was allowed to price-gouge at will."

The numbers were staggering. This caused an 800% increase in wholesale prices from April 2000 to December 2000. In 1999, the first full year of deregulation, California expenditures on wholesale electricity had totaled $7.4 billion. Just one year later, those costs rose 277 percent, to $27.1 billion. In 2001, wholesale prices remained at the exorbitantly high level of $26.7 billion.

For AEP executives watching from Columbus, California was both cautionary tale and competitive opportunity. While West Coast utilities hemorrhaged billions, AEP's regulated operations churned out steady profits. Five of AEP's eleven states—Arkansas, Ohio, Texas, Virginia, and West Virginia—were experimenting with customer choice and market-based pricing. But AEP had learned from California's mistakes: maintain generation assets, keep transmission control, and never, ever, sell forward without owning the underlying power.

The merger with CSW closed on June 15, 2000, right as California's crisis peaked. American Electric Power (NYSE: AEP) and Central and South West Corp. (NYSE: CSR) completed their merger today, creating a national leader in electricity generation, trading and distribution. But regulatory approval came with strings. On August 31, 2004, American Electric Power Company's $10 billion acquisition of the Central and South West Corporation was approved. The delay between merger completion and final approval reflected deep regulatory anxiety about concentration in power markets.

AEP had to navigate a federal court challenge to its PUHCA compliance. The Commission issued an order on August 30, 2004, in the case involving the merger of American Electric Power Company, Inc. (AEP) and Central and South West Corporation (CSW) that was remanded to the Commission from the U.S. Court of Appeals for the District of Columbia (276 F. 3d 609 (D.C. Cir. The company's solution was elegant: create separate holding companies for regulated versus non-regulated operations, structurally unbundling its six operating companies while maintaining operational integration.

The 2005 Energy Policy Act finally delivered what the industry had sought for decades: The Energy Policy Act of 2005 repealed the PUHCA under George W. Bush. After 70 years, the law that had defined American utilities was gone. But by then, the damage from California's crisis had fundamentally shifted the deregulation narrative.

States that had rushed toward competitive markets in the 1990s began pulling back. Retail choice programs stalled or reversed. The promised consumer savings from competition never materialized—in fact, According to a 2007 study of Department of Energy data by Power in the Public Interest, retail electricity prices rose much more from 1999 to 2007 in states that adopted deregulation than in those that did not.

For AEP, the deregulation wars taught valuable lessons. Markets could create opportunities, but transmission—not trading—was where real value lay. The company began selling off merchant generation assets and unregulated businesses, returning to its roots as an integrated utility. The future wasn't about competing in commodity markets; it was about owning the wires that everyone needed to reach those markets.

As one AEP executive reflected years later: "California taught us that you can deregulate generation, you can create markets for energy, but someone still has to keep the lights on. And whoever controls the transmission system controls the game."

The irony was complete. A movement that began as an assault on utility monopolies had instead reinforced the value of integration, reliability, and yes, regulation. AEP emerged from the deregulation wars larger, stronger, and more convinced than ever that boring, steady, regulated returns beat casino capitalism every time.

V. Environmental Reckoning & Regulatory Battles (2000s–2010s)

The river was burning. Again. On November 3, 1999, not the Cuyahoga this time, but a river of lawsuits flowing toward Columbus. NRDC filed suit against AEP in 1999 under the Clean Air Act for violations at a number of its coal-fired electric power plants. The Environmental Protection Agency, a dozen environmental groups and eight states — Connecticut, Maryland, Massachusetts, New Hampshire, New Jersey, New York, Rhode Island and Vermont — brought the lawsuit against the company in 1999. They accused the company of rebuilding coal-fired power plants without installing pollution controls as required under the Clean Air Act.

The charges were damning: As a result of its Clean Air Act violations, AEP emitted illegal amounts of harmful nitrogen oxides and deadly sulfur dioxide pollution at plants in Indiana, Kentucky, Ohio, Virginia and West Virginia for over two decades. This wasn't just paperwork violations—it was environmental catastrophe in slow motion.

The numbers told a story of industrial-scale pollution that would have made 19th-century robber barons blush. The Political Economy Research Institute ranks American Electric Power 55th among corporations emitting airborne pollutants in the United States. The ranking is based on the quantity (2,240,000,000 pounds (1,020,000 t) in 2018) of toxic air released, as well as the toxicity and population exposure of the emissions. Major pollutants include sulfuric and hydrochloric acids, and chromium, manganese and nickel compounds.

For AEP, which had spent decades perfecting the art of regulatory compliance, the lawsuit represented an existential threat. The company's coal fleet—the source of its competitive advantage—had become its greatest liability. The plants in question weren't minor facilities; they were the backbone of AEP's generation portfolio, massive coal-burning behemoths that had powered American industry for generations.

The legal battle dragged on for eight years, a war of attrition fought in courtrooms and conference rooms. AEP's defense was simple: they hadn't violated the Clean Air Act because the modifications to their plants were "routine maintenance," not major upgrades requiring pollution controls. It was a semantic argument with billions at stake.

But the science was catching up with the semantics. Climate change was moving from academic debate to public consciousness. Al Gore's "An Inconvenient Truth" hit theaters in 2006. The Supreme Court ruled in Massachusetts v. EPA that greenhouse gases were pollutants. The political winds had shifted against coal.

Finally, on October 9, 2007, AEP surrendered—though they called it a settlement. The terms were staggering: AEP has agreed to spend $4.6 billion on pollution control equipment and pay fines. The $4.6 billion settlement represents the largest of its kind in the history of the Clean Air Act and the most money an energy company has ever agreed to put towards new pollution controls. AEP also agreed to pay an additional $15 million civil penalty, which is the highest penalty paid by any electric utility in settlement of a New Source Review case, and also fund $60 million in environmental mitigation projects. American Electric Power has agreed to cut 813,000 tons of air pollutants annually at an estimated cost of more than $4.6 billion, pay a $15 million penalty, and spend $60 million on projects to mitigate the adverse effects of its past excess emissions.

This is the single largest environmental enforcement settlement in history by several measures. For example, it is the largest settlement in terms of the value of injunctive relief, and will result in the largest amount of emission reduction from stationary sources, such as power plants and factories.

The settlement covered 16 plants across five states, representing the heart of AEP's coal fleet. In 2006, sulfur dioxide (SO2) emissions at these 16 plants totaled 828,000 tons per year. By 2018, these AEP emissions will be reduced to 174,000 tons per year, continuing in perpetuity. This SO2 reduction -- from a single settlement -- is more than the SO2 emitted from most states (45 out of 50).

CEO Michael Morris tried to spin it as victory: "It eliminates the potentially significant financial risk of pursuing the litigation to its conclusion while still achieving the environmental improvements that both we and the government want," Morris said in a statement. But everyone knew the truth: AEP had lost, and lost big.

The environmental groups were less diplomatic. Sandy Buchanan, executive director of Ohio Citizen Action, one of the groups that brought the 1999 lawsuit said "Citizens of the five states and our downwind neighbors have just won an unprecedented public health victory. We regret that it took eight years and a legal two-by-four to get AEP's attention."

The settlement forced AEP to install scrubbers, selective catalytic reduction systems, and other pollution controls on its coal plants—technologies the company had resisted for decades. The equipment was expensive not just to install but to operate, adding costs to every megawatt of coal-fired power. Suddenly, AEP's competitive advantage—cheap coal power—wasn't so cheap anymore.

But pollution controls were just the beginning of AEP's environmental challenges. The company still operated the Donald C. Cook nuclear plant in Michigan, which AEP owns and operates the Donald C. Cook nuclear power plant. This accounts for 6% of the generation portfolio. While nuclear didn't emit air pollutants, it came with its own environmental and safety concerns.

Meanwhile, a new threat was emerging: distributed solar. Homeowners were starting to install rooftop panels, generating their own power and selling excess back to the grid. For a company built on centralized generation and transmission, this was heresy. AEP's initial response was resistance—lobbying for laws that made distributed solar less economical, arguing that solar customers weren't paying their fair share for grid maintenance.

The company also faced the challenge of stranded costs. As environmental regulations tightened and natural gas prices fell, many of AEP's coal plants became economically unviable. But these plants represented billions in invested capital that hadn't been fully depreciated. Who would pay for these stranded assets—shareholders or ratepayers?

State regulators generally sided with ratepayers, forcing AEP to absorb losses on uneconomic coal plants. The company began a strategic retreat, announcing coal plant retirements and conversions. Some plants, like the Zimmer facility in Ohio, were converted from nuclear to coal and then considered for conversion to natural gas—a three-generation fossil fuel family tree.

The environmental reckoning wasn't just about air pollution. AEP also bought much of the town of Cheshire, Ohio, where the Gavin Power Plant is located, due to pollution issues. The company literally had to purchase an entire town rather than clean up its act—a dystopian solution to an environmental problem.

By the 2010s, AEP faced a new reality. Coal was no longer king; it was a liability. Natural gas was cheaper and cleaner. Renewables were becoming competitive without subsidies. And public opinion had turned decisively against coal. The company that had built its empire on Appalachian coal now had to figure out how to dismantle that empire profitably.

The transformation wouldn't be easy. AEP's entire business model—from its generation fleet to its transmission system to its regulatory relationships—had been optimized for coal. Now it all had to change. The company began investing in wind and solar, but tentatively, almost reluctantly, like a heavyweight boxer trying to learn ballet.

The irony was inescapable. AEP had spent a century perfecting the art of burning coal efficiently. Now its greatest challenge was learning how not to burn coal at all. The company that had powered America's industrial rise now had to power its sustainable future—or become a relic of the carbon age.

VI. The Clean Energy Pivot (2010s–Present)

The boardroom in Columbus had changed. February 2018. Gone were the coal-dusted ledgers and transmission maps. In their place: carbon projections, renewable portfolios, and a document that would have made Sidney Mitchell's head spin—"Strategic Vision for a Clean Energy Future."

CEO Nicholas Akins was announcing what seemed impossible for a company built on Appalachian coal: 60% carbon dioxide reduction from 2000 levels by 2030, 80% by 2050. The irony wasn't lost on anyone. AEP, which had spent a century perfecting the art of burning coal, was now promising to stop.

"Our customers want us to partner with them to provide cleaner energy and new technologies while continuing to provide reliable, affordable energy," Akins said. "Our investors want us to protect their investment in our company, deliver attractive returns and manage climate-related risk."

The numbers behind this pivot were staggering. AEP planned to add 3,065 megawatts of solar generation and 5,295 MW of wind generation to its portfolio by 2030. The company's largest planned renewable energy investment was the $4.5 billion, 2,000-megawatt Wind Catcher Energy Connection project in Oklahoma, which, if approved, would be the largest contiguous wind farm in the United States.

Wind Catcher represented everything about AEP's clean energy ambitions—and everything that could go wrong. It was being developed by Invenergy in association with General Electric (GE), as part of the $4.5 billion renewable project Wind Catcher Energy Connection, which also included the construction of a dedicated generation tie-line. The scale was unprecedented for a utility that had built its empire on coal.

But the project faced fierce opposition. Wind Catcher faced opposition from Americans for Prosperity, which was founded by the Koch Brothers, and the Windfall Coalition, whose co-founders include energy executive Harold Hamm. They were making their cases in states where the oil and gas industry has substantial influence.

The death blow came from Texas. On July 27, 2018, American Electric Power canceled the Wind Catcher project as a result of the Public Utility Commission of Texas' July 26 decision to deny approval of the project. Texas regulators rejected it on the grounds that its $3 billion price tag and the need for a new $1.6 billion transmission line put too much financial risk on Swepco ratepayers.

"We are disappointed that we will not be able to move forward with Wind Catcher, which was a great opportunity to provide more clean energy, lower electricity costs and a more diverse energy resource mix for our customers," Akins said. The cancellation was a setback, but not a surrender.

The reality of AEP's clean energy transition was more complex than press releases suggested. AEP's generation capacity was currently 47 percent fueled by coal, down from 70 percent in 2005. The company's natural gas capacity was 27 percent compared to 19 percent in 2005, and its renewable generation capacity was 13 percent compared to four percent in 2005.

But the future mix revealed the challenge. AEP expected that its future generating capacity through 2030 would be 28% coal and 25% natural gas. Only 37% would come from solar, wind, hydro and pumped storage, with the remainder coming from nuclear (7%) or being met through energy efficiency and demand response (3%). Even in 2030, more than half of AEP's power would still come from fossil fuels.

The financial realities were driving strategic shifts. In 2022, AEP made a surprising decision: sell its unregulated renewable assets. In August 2023, American Electric Power completed the sale of its 1,365-megawatt unregulated, contracted renewables portfolio to IRG Acquisition Holdings, a partnership owned by Invenergy, CDPQ and funds managed by Blackstone Infrastructure, at an enterprise value of $1.5 billion including project debt. AEP netted approximately $1.2 billion in cash after taxes, transaction fees and other customary adjustments.

"This sale is part of our strategy to streamline and de-risk the business and focus on our regulated operations," said Julie Sloat, AEP president and chief executive officer. The company that had once embraced deregulation was retreating to the safety of regulated returns.

The capital plans revealed where AEP was really placing its bets. The company planned to invest $40 billion in capital from 2023 through 2027, allocating $26 billion to transmission and distribution operations and $9 billion in regulated renewable generation. The message was clear: wires, not generation, would drive the future.

By 2025, the capital requirements had grown even larger. AEP's five-year capital plan included $54 billion from 2025 through 2029 for distribution and transmission investments across its footprint. The scale was breathtaking—more than the entire market capitalization of many Fortune 500 companies.

On the ground, the transition was happening in smaller, more tangible ways. AEP rolled out an electric vehicle infrastructure incentive program in its Ohio service territory, providing $10 million for up to 375 EV public charging stations. It was a modest investment compared to the billions flowing into transmission, but it represented a fundamental shift: AEP was no longer just generating power, but enabling new ways to use it.

Customer sentiment was driving some of these changes. A study commissioned by AEP Ohio found that 86 percent of its residential customers wanted the utility to make greater use of renewable energy, and 77 percent were willing to pay more for it. The social license that had allowed AEP to burn coal for a century was expiring.

Yet the tensions were obvious. Morgan Stanley analysts found that AEP stood to gain the most in earnings of all investor-owned utilities from decarbonization, with an earnings accretion potential of 14% by 2025. Based on an asset-by-asset analysis, the report found that 94% of AEP's 124 GW of regulated coal plants would be rendered uneconomic by 2024, primarily by lower-cost wind energy.

The company kept accelerating its targets. In 2019, AEP cut carbon dioxide emissions faster than anticipated and revised its 2030 reduction target to 70 percent from 2000 levels, up from its previous target of 60 percent reduction. By 2022, the ambition grew further: AEP committed to reaching an 80% reduction in carbon dioxide emissions from 2005 levels by 2030 and achieving net zero by 2045.

But every announcement of coal plant closures came with political and economic consequences. By 2020, AEP planned to retire the 650-MW Dolet Hills Station in Louisiana by 2021; the 469-MW Northeastern Unit 3 in Oklahoma by 2026; the 1.1-GW Rockport Unit 1 in Indiana by 2028; AEP's 595-MW portion of the Cardinal Plant in Ohio by 2030; the 580-MW Pirkey Plant in Texas in 2023; and cease using coal at the 1.05-GW Welsh Plant in Texas in 2028.

Each closure meant lost jobs, reduced tax revenue, and stranded assets. The communities that had powered America's industrial rise were being left behind in its clean energy transition. AEP tried to manage the politics, but the economics were inexorable.

The transformation wasn't just about swapping coal for solar. It was about reimagining the entire business model. "Nearly all of our capital will be allocated to our regulated businesses, and 90% of our future investment will focus on wires and renewables," Sloat said. "Our high-growth transmission business has a long runway of investment opportunities focused on improving system performance, increasing reliability and resiliency and enhancing market efficiency".

The great irony of AEP's clean energy pivot was that it reinforced, rather than challenged, the fundamental structure Mitchell had created over a century ago. Transmission—those high-voltage lines first strung in 1917—remained the moat. Whether carrying coal power or wind energy, the wires were what mattered.

As 2024 drew to a close, AEP stood at a crossroads familiar to any century-old company: how to honor the past while embracing the future. The coal plants that had defined AEP were becoming liabilities. The renewable future promised growth but required massive capital and political navigation. And through it all, 5 million customers still expected the lights to turn on every time they flipped a switch.

The clean energy pivot wasn't really a pivot at all—it was an evolution, forced by economics, enabled by technology, and constrained by the realities of keeping the grid running. AEP wasn't becoming a different company; it was becoming what it had always been: the invisible infrastructure of American power, adapting to survive another century.

VII. Current Operations & Market Position

The numbers tell a story of industrial scale that's hard to comprehend. AEP's nearly 16,000 employees operate and maintain the nation's largest electric transmission system with 40,000 line miles, along with more than 225,000 miles of distribution lines to deliver energy to 5.6 million customers in 11 states. To put that in perspective, AEP's transmission lines alone could circle the Earth more than one and a half times. Add the distribution lines, and you could reach the moon.

But scale alone doesn't capture AEP's market position in 2024. The company sits at the intersection of America's energy past and future, managing a portfolio that would make any CFO lose sleep: approximately 29,000 megawatts of diverse generating capacity, ranging from aging coal plants to cutting-edge renewables.

The operating structure reflects a century of acquisitions, regulations, and geographic expansion. AEP isn't one company but a federation of utilities, each with its own regulatory relationships, customer base, and operational challenges. AEP's family of companies includes utilities AEP Ohio, AEP Texas, Appalachian Power (in Virginia and West Virginia), AEP Appalachian Power (in Tennessee), Indiana Michigan Power, Kentucky Power, Public Service Company of Oklahoma, and Southwestern Electric Power Company (in Arkansas, Louisiana, east Texas and the Texas Panhandle).

Each subsidiary operates like a feudal fiefdom within the AEP empire. AEP Ohio serves Columbus and the industrial heartland. AEP Texas manages the complexities of the ERCOT market. Appalachian Power navigates the politics of coal country. Indiana Michigan Power balances rust belt decline with data center growth. Each faces different regulators, different politics, different economics—yet all must contribute to the parent company's financial targets.

The financial performance tells a story of steady execution in a volatile world. The company has been hitting its marks with the precision of a Swiss watch. In 2023, AEP's utilities combined for a 9.1% return on equity, with the company expecting that to increase to 9.4% through higher rates in states like Louisiana, Virginia and Oklahoma.

These returns might seem modest compared to tech stocks or crypto, but in the utility world, they're gold. Regulated returns, approved by state commissions, guaranteed by monopoly service territories. It's the same business model Sidney Mitchell pioneered, refined for the 21st century.

The growth story is even more compelling. Weather-normalized electric sales at AEP's utilities climbed 2.8% in 2022, the best annual load growth in 15 years, partly driven by a 4.5% jump in industrial sales. After decades of flat or declining demand, electricity consumption is surging again.

The driver? Data centers. The digital economy's insatiable appetite for power is transforming AEP's service territories from rust belt relics to silicon suburbs. In 2024, AEP experienced significant load growth in its commercial class, largely due to economic development in Indiana, Ohio and Texas. The company anticipates 8-9% annual total retail load growth from 2025-2027 and ultimately expects to serve more than 20 gigawatts of new load by the end of the decade.

Twenty gigawatts of new load. That's equivalent to adding the entire electricity consumption of a country like Sweden to AEP's system. Customer agreements are secured for 24 gigawatts of new load by end of decade. The data center boom isn't coming—it's here.

But serving this growth requires massive investment. AEP's $54 billion, five-year capital plan supports this opportunity as the company builds infrastructure. Further, as the company continues to review the full scope of infrastructure needs, it is evaluating $10 billion of potential incremental investment across its service territory and regional transmission grids.

Competition in AEP's markets varies wildly by state and service type. In Ohio and Texas, retail choice means customers can shop for their power supplier, though AEP still owns the wires. In other states, AEP maintains traditional vertically integrated monopolies. This patchwork of market structures requires different strategies, different skills, different relationships.

The transmission business remains AEP's crown jewel and competitive moat. "We operate the nation's largest extra-high voltage transmission system that serves as America's energy backbone. Our unique experience building and operating extra-high voltage lines has positioned us as an ideal partner to expand the grid to deliver reliable power".

In February 2024, this expertise paid off. AEP, through its Transource Energy joint venture, and in collaboration with other regional utilities, was selected by the PJM board to complete projects totaling $1.7 billion. These aren't just construction projects—they're licenses to print money for decades, with regulated returns on every dollar invested.

The Texas operation shows how AEP adapts to different markets. In April 2024, AEP Texas received approval from the Public Utility Commission of Texas to construct one of the first 765-kilovolt transmission line projects in the state. Additionally, the commission approved AEP Texas' proposed grid resiliency plans. In the wild west of Texas electricity markets, transmission is the steady business.

Customer preferences are evolving faster than the grid itself. 86% of AEP's residential customers want more renewable energy, and 77% are willing to pay more for it. This social pressure is reshaping investment decisions, regulatory filings, and corporate strategy. The customers who once didn't care where their power came from now demand to know—and increasingly, to choose.

The regulatory relationships across 11 states create both complexity and opportunity. Each state commission has different priorities, different politics, different processes. Kentucky wants jobs. Ohio wants reliability. Texas wants markets. Virginia wants clean energy. AEP must be all things to all regulators, a political chameleon adapting to local colors while maintaining corporate coherence.

The company's response to these challenges has been creative financing. In January 2025, AEP announced a definitive agreement for KKR and PSP Investments to acquire a 19.9% equity interest in the company's Ohio and Indiana & Michigan Transmission Companies for $2.82 billion. The transaction multiple of 30.3 times LTM P/E is highly attractive and is a significant premium to AEP's current stock price.

This deal represents financial engineering at its finest—selling minority stakes in regulated assets at premium valuations to fund new growth. These transactions are equivalent to issuing common stock at approximately $140 per share, a premium to AEP's current share price.

Meanwhile, operational excellence remains the daily challenge. Keeping the lights on for 5.6 million customers across 11 states isn't a given—it's a 24/7 operational marathon. Storm response, vegetation management, equipment replacement, cyber security—the mundane work that never makes headlines unless it fails.

The company has also been streamlining its portfolio. Beyond selling unregulated renewables, AEP has been evaluating its retail energy business and working to complete the sale of Kentucky Power to Liberty Utilities. This isn't retreat—it's focus, concentrating on the regulated utility model that has sustained AEP for over a century.

Industrial customers remain the backbone of AEP's load, even as their mix changes. The aluminum smelters and steel mills that once defined AEP's service territory are being replaced by data centers, battery plants, and logistics hubs. The electrons flow to different customers, but the fundamental business—delivering reliable power at scale—remains unchanged.

The utility operates in an environment of constant technological change while maintaining infrastructure that must last decades. Smart meters, distributed resources, electric vehicles, battery storage—each innovation must be integrated into a grid designed in Edison's era and built in Mitchell's.

Today's AEP is a paradox: a 118-year-old startup, a regulated innovator, a monopoly competitor. It operates at the intersection of the possible and the practical, the profitable and the political. The company that once powered America's industrial age must now enable its digital future, all while maintaining the delicate balance of reliability, affordability, and increasingly, sustainability.

As one senior executive noted privately: "We're not in the electricity business anymore. We're in the reliability business. The electrons are just the product—what we really sell is the confidence that the lights will always turn on."

VIII. Playbook: Business & Strategic Lessons

The art of regulatory navigation might be AEP's greatest corporate competency, honed over 118 years of working with everyone from Teddy Roosevelt's trust busters to today's climate hawks. The playbook reads like Machiavelli wrote it for utilities: never fight regulators directly, always give them victories they can claim, and remember that today's adversary is tomorrow's partner.

Consider how AEP handled the 2007 Clean Air Act settlement. They could have fought for years, spending hundreds of millions on lawyers. Instead, they settled for $4.6 billion in equipment upgrades—equipment that went straight into their rate base, earning regulated returns for decades. They turned a penalty into a profit center. That's not compliance; that's judo.

The company's approach to working with 11 state commissions plus FERC resembles a complex chess game played simultaneously on multiple boards. Each state wants to feel special, heard, prioritized. Ohio commissioners care about jobs and economic development. Virginia wants clean energy leadership. Texas demands market efficiency. AEP gives each what they want while maintaining a coherent corporate strategy—a political ballet performed in regulatory hearing rooms.

Capital allocation in regulated versus competitive markets reveals another strategic lesson: boring beats exciting every time. AEP spent years chasing deregulated market opportunities, building merchant plants, trading power. What did they learn? Regulated returns might be capped, but they're guaranteed. Competitive markets offer upside, but also bankruptcy risk. By 2023, AEP had sold off its unregulated renewables and refocused entirely on regulated utilities. The lesson: in infrastructure, predictability trumps possibility.

Managing the energy trilemma—reliability, affordability, and sustainability—requires accepting that you can't maximize all three simultaneously. AEP's approach has been to prioritize reliability above all else. As one executive explained: "You can survive angry environmentalists. You can survive rate increases. You can't survive a blackout." This hierarchy drives every operational decision, from generation planning to tree trimming budgets.

The transmission advantage explains why AEP's strategy has shifted from generation to wires. Generation assets become obsolete—coal plants close, nuclear plants age out, even wind turbines eventually need replacement. But transmission lines, properly maintained, last nearly forever. And crucially, whoever owns the transmission controls market access. It's the bridge everyone must cross, collecting tolls in perpetuity.

The lessons from deregulation are particularly instructive. When markets work: they drive efficiency, innovation, and customer choice. When markets fail: California 2000, Texas 2021, price spikes that destroy political support overnight. AEP learned that partial deregulation is worse than either full regulation or full competition. You get the worst of both worlds—market volatility without market efficiency, regulatory burden without regulatory protection.

Portfolio theory for utilities isn't like portfolio theory for hedge funds. It's not about maximizing returns but about minimizing catastrophic failure. AEP maintains a diverse generation mix not because it's optimal but because it's resilient. Coal provides baseload when gas prices spike. Gas responds quickly when wind stops blowing. Renewables provide fuel cost certainty. Nuclear runs regardless of weather. This redundancy is expensive but essential—insurance against the unthinkable.

The challenge of stranded assets offers a masterclass in political economy. AEP has billions invested in coal plants that are becoming uneconomic. The accounting says write them off. The politics says that means rate increases and job losses. The solution? Gradual retirement, securitization, finding ways to spread the pain over time and stakeholders. It's financial engineering meets political theater.

Perhaps the most counterintuitive lesson: utilities keep returning to regulated models after deregulation experiments because monopolies, properly regulated, can be more efficient than competitive markets for essential infrastructure. Competition works for widgets and websites. But for assets that take decades to build and must run reliably 24/7/365, the transaction costs of markets can exceed their efficiency gains.

The regulatory compact—utilities get monopolies in exchange for serving everyone at regulated rates—seems archaic in the age of Uber and Amazon. But it solves a fundamental problem: how to ensure universal service when some customers are profitable and others aren't. Cherry-picking profitable customers works in telecom. In electricity, it means grandma freezes in winter because serving her rural home isn't economic.

AEP's experience shows that the best regulatory strategy is to make regulators look good. Propose programs that let commissioners claim credit for job creation, emissions reduction, or rate stability. Never surprise them. Never embarrass them. Always give them an out. The company that masters this dance can turn regulation from a constraint into a competitive advantage.

The infrastructure investment paradox reveals itself in AEP's capital plans. The more you spend, the more you earn (through regulated returns), but the higher rates go, risking political backlash. The art is finding the sweet spot—enough investment to maintain reliability and earn returns, not so much that customers revolt. It's a balance AEP has maintained for over a century.

Risk management in utilities differs fundamentally from other industries. A tech company can fail fast and pivot. A bank can hedge with derivatives. But utilities must maintain physical assets that can't be easily moved, replaced, or abandoned. AEP's risk management focuses on optionality—maintaining multiple paths forward without committing irrevocably to any single future.

The lesson on technological change: adopt slowly but thoroughly. AEP wasn't first to renewables, smart meters, or electric vehicle charging. But when they move, they move at scale. Let others debug the technology and take the regulatory arrows. Then deploy proven solutions across millions of customers. It's not innovative, but it works.

Customer relations in a monopoly require a different playbook. Customers can't leave, so the temptation is to ignore them. But ignored customers become political opponents, funding solar panels, supporting municipalization, demanding regulatory intervention. AEP learned to treat captive customers like voluntary ones—not because they have to, but because it's cheaper than fighting them.

The balance between centralization and decentralization remains an ongoing challenge. Centralize too much, and you lose local knowledge and relationships. Decentralize too much, and you lose economies of scale and coordination. AEP's federal structure—autonomous subsidiaries within a coordinated holding company—isn't elegant, but it works.

Perhaps the meta-lesson from AEP's playbook: in essential infrastructure, success comes not from disruption but from evolution. The companies that survive centuries don't do so by constantly reinventing themselves but by gradually adapting to new realities while maintaining core capabilities. AEP in 2024 would be recognizable to Sidney Mitchell—still moving electrons from where they're generated to where they're needed, just with different sources and smarter systems.

The ultimate strategic lesson might be this: in the utility business, there are no permanent victories, only permanent relationships. Technology changes, regulations shift, politics swing, but the need for reliable electricity remains constant. The companies that thrive are those that understand they're not in the electricity business—they're in the trust business. Every electron delivered reinforces or erodes that trust. After 118 years, AEP is still here because they've never forgotten that fundamental truth.

IX. Bear vs. Bull Case & Future Outlook

The Bull Case:

The optimists see AEP as a coiled spring, ready to capture unprecedented value from the energy transition. Start with the Morgan Stanley analysis that made Wall Street sit up straight: AEP stood to gain the most in earnings of all investor-owned utilities from decarbonization, with an earnings accretion potential of 14% by 2025. Based on an asset-by-asset analysis, 94% of AEP's 124 GW of regulated coal plants would be rendered uneconomic by 2024, primarily by lower-cost wind energy.

This isn't disaster—it's opportunity. Every coal plant retirement creates regulatory justification for new investment. Every dollar spent on renewables goes into the rate base, earning regulated returns for decades. The energy transition isn't a threat to AEP's business model; it's the greatest capital deployment opportunity in the company's history.

The transmission buildout opportunity alone could transform AEP's economics. The company already operates the nation's largest transmission network, and the renewable transition requires massive new transmission investment. Wind farms in Oklahoma need to reach cities in Ohio. Solar in Texas needs to flow to factories in Indiana. Every electron from renewable sources needs more transmission than coal or gas because renewable resources are location-dependent. AEP owns the highways; everyone else just wants to drive on them.

Data center demand represents a generational growth opportunity. Customer agreements secured for 24 gigawatts of new load by end of decade isn't just growth—it's transformation. This is equivalent to adding several major cities to AEP's service territory. And unlike residential customers who increasingly add rooftop solar, data centers need industrial-scale, hyper-reliable power that only utilities can provide.

The federal policy tailwinds are hurricane-force. The Infrastructure Investment and Jobs Act, the Inflation Reduction Act, the CHIPS Act—collectively, they represent trillions in federal support for exactly what AEP does: build and operate electrical infrastructure. Production tax credits for renewables, investment tax credits for transmission, grants for grid modernization—it's Christmas morning for utilities, and AEP is perfectly positioned to capture more than its share.

The regulatory environment has never been more favorable. State commissions understand that massive investment is needed for the energy transition. They're approving rate increases that would have been politically impossible a decade ago. The social license to spend and earn has been renewed and expanded.

Financial engineering is creating value beyond traditional utility returns. The KKR/PSP transmission deal valued those assets at 30 times earnings—multiples that make tech companies jealous. If AEP can monetize more infrastructure at similar valuations while maintaining operational control, shareholder value could soar.

The reshoring and reindustrialization narrative plays directly to AEP's geographic strengths. Its service territory spans the American industrial heartland—exactly where companies are building new factories to reduce supply chain dependence on Asia. Every semiconductor fab, every battery plant, every reshored manufacturer needs reliable, affordable power. AEP is their only option.

The Bear Case:

The pessimists see existential threats lurking behind every transformer. Start with the coal problem. Despite all the renewable rhetoric, 28% of AEP's generation capacity will still be coal in 2030. That's not just stranded assets—it's stranded politics. Every coal plant closure means lost jobs, reduced tax revenue, and angry communities in states where AEP needs regulatory approval for rate increases.

Execution risk on the capital plan is enormous. $54 billion in five years isn't just spending—it's building. Supply chain constraints, skilled labor shortages, permitting delays, contractor failures—any could derail the plan. And unlike tech companies that can delay product launches, utilities must deliver power every second of every day while rebuilding the entire system.

Regulatory lag and ROE compression could strangle returns. Regulators approve investments based on yesterday's capital costs but returns are earned in tomorrow's operating environment. With interest rates volatile and construction costs soaring, AEP could find itself earning 6% returns on investments that cost 8% to finance.

Competition from distributed resources isn't slowing—it's accelerating. Every rooftop solar panel, every home battery, every community microgrid reduces demand for utility power. The death spiral—fewer customers paying for the same fixed infrastructure—isn't theoretical anymore. It's happening in California, Hawaii, and could spread to AEP's territory as solar costs continue falling.

Climate litigation represents an unknowable but potentially catastrophic risk. AEP has been among the largest carbon emitters for decades. As climate attribution science improves and legal theories evolve, utilities could face tobacco-style litigation. The company ranked 55th among corporations emitting airborne pollutants in the United States, with 2.24 billion pounds in 2018. Those are big numbers for plaintiff attorneys to wave in front of juries.

The pace of technological change could obsolete traditional utilities entirely. If solid-state batteries achieve projected cost reductions, if hydrogen becomes economically viable, if fusion finally works—any could make the grid as AEP knows it irrelevant. The company would own the equivalent of railroad tracks in the age of airlines.

Political risk is rising, not falling. Public power movements, municipalization efforts, and social justice campaigns targeting utility disconnections are gaining momentum. The regulatory compact that has protected utilities for a century is under assault from both left and right—socialists wanting public power, libertarians wanting market competition.

Environmental liabilities beyond carbon lurk in every coal ash pond, every contaminated site, every chemical spill. The bill for a century of industrial-scale pollution hasn't been fully tallied, but it's coming due. And unlike carbon, which can be addressed through transition, legacy contamination requires cash remediation.

Customer affordability is reaching breaking points. Industrial customers are already seeing double-digit rate increases. Residential customers are choosing between heating and eating. The social license to raise rates indefinitely doesn't exist, but the capital plan requires exactly that.

The Synthesis:

The truth, as always, lies between the extremes. AEP faces both generational opportunities and existential challenges. The company's future likely depends on three critical factors:

First, execution excellence. Can AEP actually build $54 billion worth of infrastructure on time and on budget? The company's track record suggests yes, but the scale is unprecedented.

Second, regulatory navigation. Can AEP maintain constructive relationships across 11 states while pushing through necessary rate increases? The political skills that got them this far will be tested like never before.

Third, technological adaptation. Can a 118-year-old company built for centralized generation adapt to a distributed, digital, decarbonized future? The answer will determine whether AEP thrives for another century or becomes the Kodak of utilities.

The most likely scenario: AEP muddles through magnificently, as it always has. The company will capture enough of the upside to satisfy investors while avoiding enough of the downside to survive. It won't be the highest performing utility or the most innovative, but it will be there, reliably delivering electrons, collecting regulated returns, and adapting just fast enough to stay relevant.

The bear case assumes disruption; the bull case assumes transformation. Reality suggests evolution—slow, steady, profitable evolution. After 118 years, betting against AEP's survival instincts seems foolish. But betting on spectacular returns seems equally naive. The company's future, like its past, will likely be measured in steady dividends and stable returns—boring, essential, and ultimately, successful.

X. Epilogue: The Next Chapter

The conference room in Columbus, 2024. Outside, construction crews are installing electric vehicle chargers in the parking garage. Inside, executives debate small modular reactors and green hydrogen. On the wall, portraits: Sidney Mitchell, who built the empire; Nicholas Akins, who began the transition; and space for whoever comes next. The history of American Electric Power is still being written.

The irony of re-regulation after the deregulation wars is almost Shakespearean. AEP spent the 1990s and 2000s pursuing competitive markets, building merchant plants, trading power like a commodity. Now, in 2024, the company has retreated entirely to regulated utilities. The market experiment didn't fail—it proved that for essential infrastructure, regulated monopolies might actually be the most efficient structure. Competition works for smartphones and sneakers, not for assets that take decades to build and must run every second forever.

Can traditional utilities survive the distributed energy revolution? That's the trillion-dollar question. Every Tesla Powerwall, every rooftop solar panel, every community microgrid chips away at the centralized model AEP has perfected. But the data center boom suggests a different future—one where distributed resources serve homes while utilities serve the digital infrastructure that increasingly runs the world. AEP might lose residential customers to solar but gain data centers that consume the equivalent of small cities.

The transmission bottleneck problem is AEP's advantage wrapped in a national crisis. America needs to triple its transmission capacity to achieve renewable energy goals. That sounds like a problem, but for the company that owns more high-voltage transmission than anyone else, it's an opportunity. The bottleneck isn't a bug in AEP's business model—it's a feature. Scarcity creates value, and transmission capacity is becoming the scarcest commodity in the energy transition.

Climate resilience and grid hardening imperatives are reshaping capital allocation. It's not enough to deliver power—the grid must withstand Category 5 hurricanes, polar vortexes, cyberattacks, and solar storms. Every dollar spent on resilience goes into the rate base, earning regulated returns. Climate change isn't just driving decarbonization; it's driving a massive infrastructure upgrade cycle that could sustain utilities for decades.

What would an acquisition or breakup look like? The question haunts every utility conference. Could Amazon buy AEP to power its data centers? Could the company be split into transmission and distribution entities? The regulatory barriers are immense, but in an era where Tesla makes cars and rockets, where Amazon delivers groceries and runs the CIA's cloud, traditional boundaries are dissolving. AEP's collection of state-regulated utilities might be worth more apart than together—or might be priceless to a tech giant needing guaranteed power for the AI age.

The key lessons for energy transition investors are sobering but valuable. First, the transition will take longer and cost more than anyone expects. Second, incumbents like AEP have massive advantages—regulatory relationships, operational expertise, and balance sheets that can sustain decades-long capital programs. Third, the boring investments—transmission, distribution, grid modernization—will likely generate better risk-adjusted returns than sexy bets on breakthrough technologies.

XI. Recent News & Developments

The drumbeat of announcements in 2024 and 2025 shows a company in motion. In January 2025, AEP announced the $2.82 billion minority interest sale of its Ohio and Indiana Michigan transmission companies to KKR and PSP Investments—financial engineering that funds growth while maintaining control.

Late 2024 brought innovation through necessity: AEP announced an agreement with Bloom Energy to acquire up to 1 gigawatt of fuel cells to enable data center customers to expand while transmission infrastructure is built. AEP Ohio filed with regulators for approval to install the first 100 megawatts. It's a bridge technology for a bridge moment—keeping customers while building permanent infrastructure.

Looking ahead, AEP expects to announce a new, five-year capital plan of approximately $70 billion. Seventy billion. That's more than the market cap of General Motors, Ford, or dozens of other Fortune 500 companies—all to rebuild the invisible infrastructure that makes modern life possible.

The regulatory wins keep coming. Grid modernization in Ohio, transmission approvals in Texas, renewable additions across the footprint. Each approval is another brick in the foundation of AEP's next century.

XII. Final Analysis

American Electric Power stands as a monument to American industrial capitalism—not the disruptive, move-fast-and-break-things variety, but the slow, steady, build-things-that-last kind. For 118 years, the company has done one thing: deliver electrons from where they're generated to where they're needed. The sources change, the technology evolves, the regulations shift, but the fundamental mission remains.

The company's transformation from coal giant to renewable developer isn't really a transformation at all—it's an adaptation, like a river changing course but still flowing to the sea. AEP will likely never be the most innovative utility or the fastest growing or the most beloved. But it will probably be there in another century, still moving electrons, still earning regulated returns, still powering whatever comes next in the American experiment.

The story of AEP is the story of American infrastructure—built by visionaries, sustained by engineers, regulated by politicians, and taken for granted by everyone else until the lights go out. It's a story of monopoly and competition, innovation and inertia, public service and private profit. Most of all, it's a story that's still being written, one electron at a time, one rate case at a time, one transformation at a time.

As Sidney Mitchell might recognize if he walked into AEP's headquarters today, the tools have changed but the task hasn't: keep the lights on, earn a fair return, and survive whatever comes next. After 118 years, American Electric Power has mastered that formula. The next century will test whether that's still enough.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube