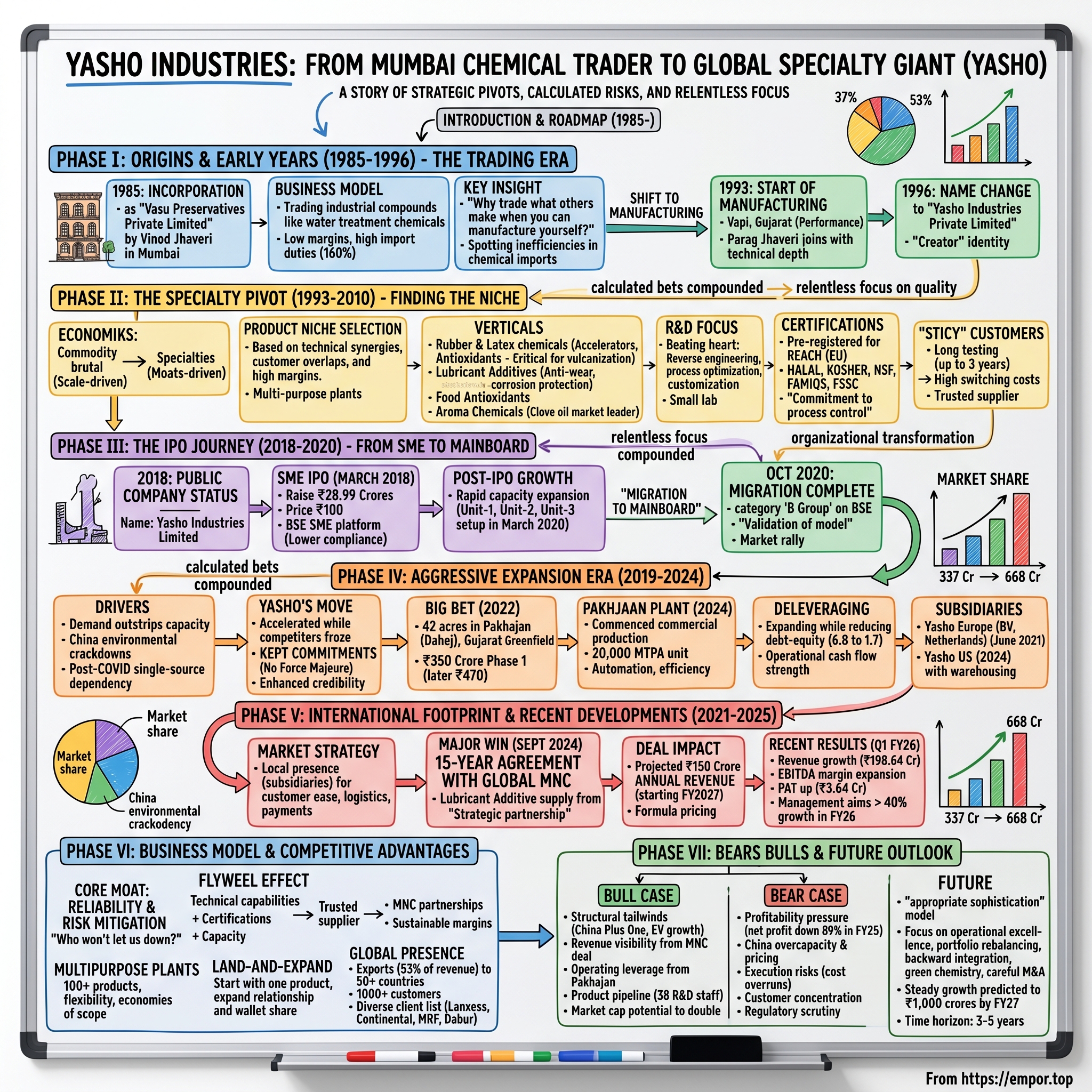

Yasho Industries: From Mumbai Chemical Trader to Global Specialty Giant

I. Introduction & Episode Roadmap

Picture the bustling chemical bazaars of Mumbai in 1985. The air thick with the scent of industrial compounds, traders haggling over import prices that carried punitive duties as high as 160%. In a modest office somewhere in this maze of commerce, a middle-aged businessman named Vinod Jhaveri was wrestling with a fundamental question that would reshape his family's destiny: Why keep trading what others make when you could manufacture it yourself?

This wasn't just idle speculation. Yasho Industries is a Mumbai-based Specialty chemicals manufacturer which was incorporated in 1985 by Mr. Vinod Jhaveri, starting life as Vasu Preservatives Private Limited—a name that hinted at preservation but would soon give way to transformation. What began as a small chemical trading operation would, over four decades, morph into a global specialty chemicals powerhouse with operations spanning continents.

Today, Yasho Industries commands a market capitalization of Rs 2,042 crore, a far cry from its humble beginnings. The company manufactures 148 products across five business verticals, serves over 1,000 clients in more than 50 countries, and has just commenced production at a massive 20,000 MTPA facility spread across 42 acres in Gujarat. But the real story isn't in these numbers—it's in the strategic pivots, calculated risks, and relentless focus that transformed a Mumbai trading firm into a specialty chemicals champion.

What makes Yasho's journey particularly compelling for students of business strategy is how it navigated three critical transitions that most emerging market companies struggle with: the shift from trading to manufacturing, the leap from commodities to specialties, and the migration from SME obscurity to mainboard visibility. Each transition carried existential risks. Each required fundamentally different capabilities. And each, as we'll explore, offers a masterclass in industrial transformation.

This is also a story about timing—about reading the tea leaves of global supply chains before they became obvious. When China's environmental crackdowns began disrupting global chemical supplies, Yasho was already expanding capacity. When COVID-19 exposed the fragility of single-source dependencies, Yasho's credibility got enhanced as it kept its delivery commitments while competitors declared force majeure. And when multinational corporations began desperately seeking alternative suppliers outside China, Yasho had already built the technical capabilities and certifications they demanded.

But perhaps most intriguingly, this is a narrative about the power of patient capital and technical depth in an industry where both are prerequisites for survival. In a sector where product development cycles stretch three years, where customer approvals can take even longer, and where a single quality failure can destroy decades of reputation, the Jhaveri family built a business designed for the long game. Three generations now work in the company—a rarity in an industry known for either quick exits or spectacular failures.

As we dive deep into Yasho's evolution, we'll uncover the playbook for building a specialty chemicals business in emerging markets: How do you compete with Chinese manufacturers who enjoy massive scale advantages? How do you convince Fortune 500 companies to trust a supplier from Vapi, Gujarat? How do you finance capital-intensive expansions while maintaining family control? And perhaps most crucially—how do you spot the inflection points that separate winners from also-rans in the brutal world of industrial chemicals?

The answers, as we'll discover, lie not in any single brilliant strategy, but in a series of calculated bets that compounded over time. From the decision to focus on import substitution in the 1990s to the recent signing of a 15-year contract with a global MNC worth Rs 150 crore annually, each move built upon the last, creating a flywheel that's now spinning faster than ever.

II. Origins & Early Years: The Trading Era (1985-1996)

The monsoons had just retreated from Mumbai when Yasho Industries Limited was incorporated in October 1985 as "Vasu Preservatives Private Limited" under the provisions of Companies Act, 1956. In those days, Vinod Jhaveri wasn't thinking about global supply chains or specialty chemicals. When Yasho was launched, the Jhaveris were in the business of water treatment chemicals—a pragmatic choice in a city where industrial growth was outpacing infrastructure.

The name "Vasu Preservatives" itself tells a story of modest ambitions. This wasn't a company born with grandiose visions of chemical empires. It was a trading operation, buying and selling what others produced, operating in the shadows of established players like Hindustan Unilever and the chemical giants of Europe. The margins were thin, the competition fierce, and the barriers to entry virtually non-existent. Anyone with a phone line and a rolodex could become a chemical trader in 1980s Mumbai.

But Jhaveri possessed something that set him apart from the hundreds of other traders crowding Mumbai's chemical markets—an intuitive understanding of the inefficiencies plaguing India's chemical imports. In those days, the import duty was as high as 150 percent to 160 percent. These punitive tariffs created a peculiar market dynamic: imported chemicals were essential for India's growing industries, yet their prices were artificially inflated by government policy. It was a classic arbitrage opportunity waiting to be exploited.

The early years were about survival more than strategy. Vasu Preservatives operated from modest premises, with Jhaveri personally managing relationships with both suppliers and customers. The business model was straightforward: source chemicals from international suppliers, navigate the byzantine import regulations, and distribute to local manufacturers who needed these inputs but couldn't justify direct imports. It was unglamorous work, but it provided something invaluable—a front-row seat to understanding which chemicals Indian industry desperately needed and couldn't source domestically.

By the early 1990s, patterns began emerging from the chaos of orders and invoices. Certain chemicals appeared repeatedly—specialty compounds used in rubber processing, additives for lubricants, antioxidants for food preservation. These weren't commodity chemicals that any large plant could churn out. They required specific technical knowledge, precise quality control, and often, proprietary processes. More importantly, the customers buying these chemicals weren't price-shopping commodity buyers—they were quality-conscious manufacturers for whom these chemicals were critical inputs.

The transformation from trader to manufacturer didn't happen overnight. After Parag joined in the 90s, the company decided to set up a chemical production plant for manufacturing speciality chemicals as import substitutes. Parag, armed with a Master's degree in Chemistry from Mumbai University, brought technical depth that complemented his father's commercial acumen. This father-son combination—commerce meets chemistry—would become the cornerstone of Yasho's evolution.

The name was changed to Yasho Industries Private Limited on May 17, 1996—a seemingly minor administrative detail that signaled a major strategic shift. The company was no longer just preserving or trading; it was creating. The new name carried no baggage, no limitations. It was a blank canvas on which to paint industrial ambitions.

The decision to abandon pure trading for manufacturing wasn't without risks. Trading required minimal capital—you could operate on credit, turning over inventory without major investments. Manufacturing, especially in chemicals, demanded significant upfront capital for land, equipment, and regulatory compliance. It meant dealing with pollution control boards, factory inspections, and the thousand headaches that come with running an industrial operation. For a family business with limited resources, it was a bet-the-company moment.

Yet the logic was compelling. Every chemical Jhaveri had traded revealed the same truth: Indian manufacturers were paying exorbitant prices for imported specialties that could, in theory, be produced locally. The technical barriers were real but not insurmountable. The regulatory requirements were onerous but manageable. And most crucially, the first-mover advantages were substantial—whoever cracked the code for local production of these import substitutes would enjoy years of pricing power before competition caught up.

The location choice was critical. Manufacturing units are strategically located within 200 kilometres from JNPT Port, at GIDC, Vapi, Gujarat. Vapi wasn't Mumbai—it lacked the sophistication, the infrastructure, the talent pool. But it had something Mumbai didn't: space for chemical plants, a business-friendly state government, and crucially, proximity to ports for both importing raw materials and eventually, exporting finished products. It was a location chosen not for what it was, but for what it could become.

The transition period from 1993 to 1996 was Yasho's chrysalis phase. Within the world of fine chemicals, Yasho Industries Limited manufactures performance chemicals for industries as diverse as Rubber & Latex, Food & Flavors, Perfumery, Lubricants and other Specialty applications since 1993. The company was simultaneously operating as a trader while building manufacturing capabilities—a delicate balance that required funding ongoing operations while investing every spare rupee into the nascent production facilities.

By 1996, when the name officially changed to Yasho Industries, the die was cast. The company had made its choice: it would no longer be content as a middleman in India's chemical supply chain. It would become a creator, a manufacturer, a company that added tangible value rather than just facilitating transactions. The trading DNA would never fully disappear—it would manifest in deep customer relationships and acute market sensing—but it would now be supplemented by something more substantial: the ability to actually make what customers needed.

III. The Specialty Pivot: Finding the Niche (1993-2010)

The economics of commodity chemicals are brutal. Scale is everything, margins are measured in basis points, and the largest player usually wins by crushing everyone else on cost. In 1993, as Yasho's first manufacturing operations came online in Vapi, this reality hit hard. The company could produce basic chemicals, yes, but so could dozens of others. Competing with established giants on their turf was a recipe for mediocrity at best, bankruptcy at worst.

The pivot to specialties wasn't a eureka moment—it was a gradual recognition born from customer interactions and market feedback. The company started operations with aromatic chemicals and specialty chemicals. In 2000, the company started manufacturing rubber chemicals and lubricant additives which are used in rubber processing industries. Each product category told its own story of market opportunity and technical challenge.

Take rubber chemicals, for instance. The rubber chemicals manufactured by Yasho industries are accelerators, antioxidants and co-agents. These are critical and essential chemicals which accelerate the sulphur cross linking reaction (vulcanization) and impart desired physical properties to rubber products and enable manufacturing of products on a large scale at an optimum cost. This wasn't just mixing compounds—it was chemistry that directly impacted the performance of tires, conveyor belts, and countless rubber products that modern life depends upon.

The technical complexity served as a natural moat. Accelerators are also classified as Primary or Secondary accelerators based on the role they play in a given compound. Generally, Thiazoles and Sulfenamide accelerators play a role of being Primary Accelerators due to their characteristics such as good processing safety, a broad vulcanization plateau and optimum cross link density. The basic accelerators such as Guanidines, Thiurams, and Dithiocarbamates etc are used as Secondary accelerators to activate the primary accelerators. This wasn't knowledge you could Google or learn from a textbook—it required deep understanding of polymer chemistry and years of practical experience.

The lubricant additives market presented a different opportunity. Lubricants are used to reduce friction and wear, dissipate heat from critical parts of equipment, remove and suspend deposits that may affect performance and protect metal surface damage from degradation and corrosion. Base oils themselves perform most of the functions of lubricants. Additives are needed when a lubricant's base oil doesn't provide all the properties the application requires. They typically range between 0.1 to 30 percent of the oil volume, depending on the machine. Small percentages, massive impact—the perfect specialty chemical dynamic.

Building capabilities in these niches required more than just equipment. Mr. Parag Jhaveri, Managing Director and CEO. Mr. Parag Jhaveri has a Master of Science degree in Chemistry from Mumbai University. He has over three decades of experience in the chemical industry. He played a key role in ensuring the robust growth of the organisation with oversight over the functions of sales, finance, R&D and marketing along with our founder promoter. Technical leadership wasn't just helpful—it was existential.

The R&D function, initially just Parag and a handful of chemists working in a makeshift lab, became the beating heart of the transformation. They weren't trying to discover new molecules—that was the domain of companies with hundred-million-dollar research budgets. Instead, they focused on reverse engineering, process optimization, and most crucially, customization for Indian conditions. A rubber accelerator that worked perfectly in European factories might fail in the heat and humidity of Indian plants. These adaptations became Yasho's calling card.

Customer acquisition in specialties followed a completely different playbook than commodity sales. Players intending to enter need to invest in product development and testing time periods are as high as 3 years. The time taken to identify a product niche, master quality, build credibility with customers, acts as a moat. 10 years after entering Lubricant Additives, Yasho only has ~84 Cr Revenue in this segment in FY22. The long gestation periods scared away financial investors and impatient competitors alike.

But the Jhaveris understood something fundamental about specialty chemicals: once you're in, you're sticky. A tire manufacturer who approves your rubber accelerator won't switch suppliers to save a few percentage points. The testing costs, the risk of production disruption, the regulatory re-approvals—all create massive switching costs. This wasn't selling commodities where customers switched suppliers for a rupee per kilogram difference. This was becoming embedded in customers' production processes.

The product portfolio expansion followed a deliberate logic. The company has four business verticals with the highest revenue contribution from rubber chemicals. Rubber chemicals, Lubricant additives and specialty chemicals together contribute 59% of total revenues and the rest is from antioxidants and aroma chemical business. Going forward the company expects the revenue contribution from rubber, lubricant and specialty will be 65-70% of total revenues. Each vertical was chosen for its technical synergies, customer overlaps, and margin profiles.

The aroma chemicals business showcased another dimension of the specialty pivot. The company manufactures clove oil and its derivatives in the segment and is a market leader for these products. The aroma chemicals are used by F&F companies in the formulation of flavours and fragrances. From industrial rubber to fine fragrances—it seemed schizophrenic, but there was method to the madness. The same extraction and purification technologies, the same quality control processes, the same customer emphasis on consistency and purity.

International certifications became crucial differentiators. The Company has pre-registered certain products under REACH (Registration, Evaluation, Authorization and Restriction of Chemicals) Regulation. The Company exports some of its products to European countries and hence it has pre-registered certain products under REACH Regulation. REACH pre-registration wasn't just paperwork—it was a multi-year, multi-crore investment that most Indian chemical companies couldn't or wouldn't make.

The certification arsenal grew: The Company has received various certifications confirming its products to be in line with National and International Standards i.e. HALAL Certifications, STAR KOSHER Certifications, NSF Certifications, FAMIQS Certification, FSSC Certification. Each certificate opened new markets, new customers, new possibilities. A kosher certification might seem irrelevant for industrial chemicals, but it signaled something deeper—a commitment to process control and documentation that sophisticated buyers valued.

By 2010, the transformation was complete. Yasho was no longer a trader who happened to manufacture, or a commodity producer seeking better margins. It had become a specialty chemical company with deep technical capabilities, sticky customer relationships, and products that commanded premium pricing. The foundation was set for the next phase of growth—taking this specialty expertise to public markets.

IV. The IPO Journey: From SME Platform to Mainboard (2018-2020)

The conference room at Aryaman Financial Services buzzed with nervous energy in late 2017. Across the table, three generations of the Jhaveri family wrestled with a decision that would fundamentally alter their company's trajectory. Going public meant scrutiny, compliance burdens, and partial loss of control. But it also meant access to capital for the ambitious expansion plans percolating in Parag's mind. After decades of bootstrapped growth, Yasho needed external capital to compete at the next level.

The status changed to a Public Company and name of the Company was changed to "Yasho Industries Limited" on February 19, 2018. The legal transformation preceded the market debut by just a month—a compressed timeline that suggested urgent capital needs or a favorable market window, perhaps both.

The IPO structure was modest by any standard. Yasho Industries IPO is a SME IPO of 2899200 equity shares of the face value of ₹10 aggregating up to ₹28.99 Crores. The issue is priced at ₹ 100 per share. The minimum order quantity is 1200. The IPO opens on March 19, 2018, and closes on March 21, 2018. At just under 29 crores, this wasn't a blockbuster issue seeking headlines. It was a pragmatic capital raise from a company that had always been conservative with external financing.

The SME platform choice was telling. Rather than shooting for the mainboard with its institutional investors and stringent requirements, Yasho chose the path of less resistance. The BSE SME platform meant lower compliance costs, less scrutiny, and most importantly, the ability to tell their story to investors who understood smaller companies. It was crawling before walking, learning the public market ropes without betting everything.

The March 2018 IPO timing proved fortuitous. The Indian equity markets were still in a bull run, specialty chemical stocks were gaining recognition as a thematic play on China's environmental crackdowns, and retail investors were hungry for new stories. But the response was lukewarm—the issue subscribed just 1.11 times, barely crossing the finish line. This wasn't a hot IPO with investors clamoring for allocations. It was a workmanlike debut that achieved its primary objective: raising growth capital.

Listed on BSE SME on April 2, 2018. Listed at ₹101.25 per share—a mere 1.25% premium to the issue price. In IPO terms, this was practically flat, suggesting the investment bankers had priced it almost perfectly, leaving little on the table. For retail investors accustomed to listing day pops, it was disappointing. For the Jhaveris, who were playing a longer game, it was irrelevant.

The immediate post-IPO period tested the company's public market readiness. Yasho Industries had a capacity of 5,500 mtpa at the time of listing on the BSE small exchange in 2018. Over the past three years it has doubled capacities. The capital raised was immediately deployed into capacity expansion—Unit I enhancement of 850 MT in 2018-19, Unit-2 commissioning with 1550 MT in 2019-20, and Unit-3 setup in March 2020. This wasn't financial engineering or M&A adventures. It was blocking and tackling—more capacity to serve more customers.

The SME platform years were about proving the model to public market investors. Quarterly results, investor calls, annual reports—all the paraphernalia of being a listed company had to be mastered while simultaneously running a complex chemical manufacturing operation. The company learned to communicate its story, to translate technical achievements into financial metrics that investors could understand.

By mid-2020, Yasho had outgrown the SME platform. The company was listed on the BSE SME exchange in 2018 and graduated to the main board in FY21. The mainboard migration wasn't just about prestige—it was about access. Institutional investors, foreign funds, and larger domestic mutual funds couldn't invest in SME platform stocks due to mandate restrictions. The mainboard opened these funding channels.

The stocks will be admitted to dealings in the category 'B Group' on the BSE Mainboard platform from Thursday 29th October 2020. October 29, 2020—barely two and a half years after the IPO. The migration criteria were stringent: consistent profitability, minimum market capitalization, adequate public shareholding. That Yasho qualified so quickly validated the business model's robustness.

The migration timing was particularly astute. October 2020 was peak COVID disruption—global supply chains were snarled, Chinese chemical supplies were erratic, and customers were desperately seeking alternative suppliers. Parag Jhaveri, Chairman and Managing Director, Yasho Industries Limited said, "We are extremely delighted to inform about the company's milestone of migrating from the BSE SME platform to the BSE Mainboard. We received the in-principle approval from BSE and listed on the Mainboard by completing all the necessary listing formalities. I would like to thank our customers, shareholders, and other stakeholders for the confidence they have shown in Yasho over the years".

The market response to the mainboard migration was dramatic. The Rs10 paid up shares of the company, which were moving in the range of Rs150-160 in November 2020 would soon embark on a spectacular rally. This wasn't just multiple expansion from increased visibility—it was recognition that Yasho was positioned perfectly for the post-COVID reshaping of global chemical supply chains.

The governance improvements that came with mainboard listing were substantial. Independent directors with industry expertise joined the board. Quarterly investor calls became more sophisticated. The company began providing detailed segment-wise performance metrics. This transparency, initially seen as a compliance burden, became a competitive advantage—customers could see the financial strength behind their supplier.

The public market journey also brought unexpected benefits. Employee stock options became a powerful retention tool. The listed stock price provided a daily market validation of strategy. Bank financing became easier and cheaper with the enhanced disclosure and governance standards. The same conservatism that had made the IPO modest in size now showed as consistent performance that built investor trust.

Yet the most important outcome of the IPO-to-mainboard journey wasn't the capital raised or the institutional recognition—it was the organizational transformation. Yasho had evolved from a closely-held family business to a professionally-run public company without losing the entrepreneurial edge that had driven its growth. The Jhaveris still controlled the company with 67.99% shareholding, but they now operated with the discipline and transparency that public markets demanded.

The two-and-a-half-year journey from SME listing to mainboard migration became a template that other specialty chemical companies would follow. Start small on the SME platform, prove the model, build capabilities, then graduate to the mainboard when ready. It was patient capital markets evolution—very different from the venture-backed, grow-at-all-costs model that dominated technology startups, but perfectly suited for industrial companies that measured progress in years, not quarters.

V. Aggressive Expansion Era (2019-2024)

The spreadsheet on Parag Jhaveri's laptop told a story of constrained ambition. Customer inquiries Yasho couldn't fulfill. Orders declined due to capacity limitations. Long-term contracts unsigned because buyers needed supply assurance the company couldn't provide. By 2019, Yasho had a different problem than most chemical companies—too much demand, too little capacity. The conservative capacity additions of the past wouldn't suffice for the opportunity ahead.

In 2018-19, the Company's Unit I production capacity was enhanced by 850 MT. The Company commissioned production at Unit-2 facility, with additional 1550 MT to the capacity for industrial and lubricant chemicals in 2019-20. These expansions, funded by the IPO proceeds, were just appetizers. The main course was about to begin.

The board meeting in March 2020 was supposed to be routine. Then COVID hit. Markets crashed, lockdowns loomed, and every business plan seemed obsolete. Yet in this chaos, the Jhaveris saw opportunity. While competitors froze capital spending, Yasho accelerated. Unit-3 was set up in March 2020, right as the world shut down. It was contrarian, risky, and ultimately, brilliant.

The pandemic revealed the fragility of global chemical supply chains with brutal clarity. Due to supply chain issues during Covid and subsequently in 2021 and 2022, many chemical manufacturers declared force majeure on their contracts with customers. Force majeure—the legal escape clause that allowed suppliers to abandon delivery commitments during extraordinary circumstances. For chemical buyers, it was a nightmare scenario. Production lines shut down for want of critical additives. Contracts meant nothing when suppliers couldn't or wouldn't deliver.

But Yasho didn't invoke force majeure. The company stretched operations, juggled logistics, and somehow kept supplies flowing. This reliability during chaos would prove more valuable than any marketing campaign or sales pitch. Covid disruptions provided Yasho a foot in the door. Yasho's credibility got enhanced as it kept its delivery commitments. Trust, that most ephemeral of business assets, was being accumulated at compound rates.

The real ambition revealed itself in 2022. Yasho Industries Limited has acquired Land aggregating to about 42.14 acres, at Pakhajan Village, Bharuch, Gujarat for future expansion of the manufacturing plant. Forty-two acres. To put this in perspective, their existing three units in Vapi operated from a fraction of this space. This wasn't incremental expansion—this was transformation.

The Board of Directors of the Company has approved a capital expenditure of Rs350 crore in Phase 1 for its greenfield project at Pakhajan (Dahej), Gujarat. The company intends to manufacture lubricant additives and rubber chemicals with a total capacity of 15500 MT per annum in phase 1 at this new facility. Post expansion, the total manufacturing capacity will increase from 11,000 MTPA to 26,500 MTPA. The numbers were staggering—more than doubling capacity in one shot.

The Pakhajan location wasn't random. Dahej had emerged as a chemical manufacturing hub, with better infrastructure than the aging GIDC estates. Proximity to ports remained crucial, but now supplemented by dedicated chemical logistics infrastructure. Environmental clearances, always a challenge in chemical manufacturing, were streamlined in these designated zones. It was choosing the future over the familiar.

Capital allocation during this period showed remarkable discipline despite the aggressive capacity expansion. The company has, over the years, been using a part of the profit in paring debt, which stood at Rs116 crore as on 31 March 2021. The debt equity ratio has been trending downwards. In FY17 it was 6.8, which was brought to 3.8 in FY18, 2.9 in FY29 and further scaled down to 2.5 in FY20 and 1.7 in FY21. Expanding while deleveraging—a rare combination that demonstrated operational cash flow strength.

The execution of Pakhajan was a masterclass in project management. Yasho Industries Limited, a leading Indian company manufacturing specialty and fine chemicals, has commenced commercial production at its Pakhajan Plant in Dahej, Gujarat. Spread over 42 acres, the 20,000 MTPA unit has been set up at an approximate cost of Rs. 470 crore. This increase is on account of enhanced scope of automation done to improve efficiency levels, increased capacity by around 15% and inflationary factors. The cost overrun from 400 to 470 crores would normally signal execution issues. Here, it indicated scope expansion—more automation, more capacity, better economics.

The international expansion paralleled domestic capacity growth. The Company incorporated a wholly owned subsidiary company in Netherlands viz. Yasho Industries Europe B.V. on June 29, 2021. This wasn't vanity—European customers wanted local entities for easier contracting, better payment terms, and regulatory comfort. The subsidiary served as a stock point, reducing delivery times and cementing customer relationships.

The US expansion followed similar logic. In FY 2024, Company has set up a wholly-owned subsidiary in US in 2024. But unlike the European subsidiary which focused on distribution, the US presence included warehousing capabilities. American customers, accustomed to just-in-time delivery, wouldn't tolerate six-week shipping times from India. Local inventory was table stakes for serious suppliers.

R&D expansion during this period was equally dramatic. The R&D team has been strengthened from 6 people in 2019 to 38 people in 2023. A six-fold increase in research staff signaled ambitions beyond process optimization. The company was moving up the value chain, developing new products rather than just manufacturing what others had invented.

The capacity expansion wasn't just about volume—it was about capability. The Pakhajan facility incorporated automation levels unprecedented in Yasho's history. Reactor designs allowing for multiple products. Quality control systems that exceeded customer requirements. Environmental management infrastructure that anticipated future regulations rather than just meeting current ones. This was building for the next decade, not the next quarter.

Customer conversations during this period revealed the strategy's wisdom. We foresee a reasonable demand for our products in the market on account of our ability to manufacture quality products and our reliability. The enhanced capacity will also allow us to approach large multinational consumers who we could not approach in the past due to limited capacity. Capacity wasn't just about serving existing demand—it was about qualifying for opportunities previously out of reach.

The financial performance during the expansion years validated the strategy, albeit with volatility. Revenue grew from 337.98 crores at IPO to 668.50 crores in FY24. But profitability was erratic—net profit declined 89.45% to Rs 6.11 crore in the year ended March 2025 as against Rs 57.94 crore during the previous year ended March 2024. The margin pressure came from multiple sources: competitive pricing from Chinese imports, raw material volatility, and the operating leverage working in reverse during demand softness.

Yet the Jhaveris weren't managing for quarterly earnings. Yasho is doing more Cap ex in the period FY 22-FY 24 (400 Cr) than it has done cumulatively in the first 25 years of its existence (GFA FY 23 is 280 Cr). This statistic captures the transformation's magnitude—more investment in three years than in the previous quarter-century. It was a bet that the specialty chemical industry's structural growth would eventually overwhelm temporary margin pressures.

The expansion era also saw important governance changes. Professional managers joined the leadership team. The company has announced the appointment of Chirag Shah as the new CFO and KMP for the company, effective from 18 February 2025. Bringing in outside talent with two decades of experience signaled the complexity of managing a company that had outgrown its family business roots while retaining family control.

VI. International Footprint & Recent Developments (2021-2025)

The video call connected three continents—Mumbai, Amsterdam, and New Jersey. On screen, Yasho's newly hired European sales director was explaining why a major lubricant manufacturer wouldn't even consider Asian suppliers without local presence. "They want to visit a warehouse, meet a team, have someone who understands their time zone and their language," he emphasized. It was 2021, and Yasho was learning that technical capabilities alone wouldn't crack developed markets.

In 2021-22, the Company incorporated a wholly owned subsidiary company in Netherlands viz. Yasho Industries Europe B.V. on June 29, 2021. The Netherlands wasn't chosen for its tulips or windmills, but for its strategic position as Europe's logistics hub. Rotterdam's port, Europe's largest, handled much of the continent's chemical imports. Dutch regulatory efficiency meant faster company formation and easier compliance. And perhaps most importantly, a Netherlands entity provided comfort to European customers wary of direct dealings with Indian suppliers.

The European subsidiary started lean—initially just a registered office and a small warehouse operation. But its impact was immediate. Contract negotiations that previously stalled on payment terms and legal jurisdiction suddenly progressed. European customers could pay a European entity in euros, avoiding currency hedging complexities. Disputes, should they arise, would be handled under familiar EU law rather than Indian commercial courts. These might seem like minor details, but in the risk-averse world of chemical procurement, they mattered enormously.

The US expansion followed a different playbook. Our US warehouse is now operational. Unlike Europe, where the subsidiary primarily facilitated transactions, the American operation included physical infrastructure. US chemical buyers, accustomed to next-day delivery from domestic suppliers, wouldn't tolerate trans-Pacific shipping times. The warehouse meant Yasho could promise delivery in days, not weeks—table stakes for competing with established suppliers.

But the crown jewel of this period was neither European presence nor American warehousing. In September 2024, Yasho announced something that would reshape its next decade: Yasho Industries Limited, a manufacturer and supplier of specialty chemicals, has signed a long-term agreement for a period of 15 years with a global MNC for the supply of a lubricant additive. This material will be supplied from our Pakhajan facility for a period of 15 years.

The deal's structure was as important as its duration. The company shall receive an advance to build the facility. The MNC customer—whose identity remains undisclosed—would fund the capacity creation. This wasn't just a supply agreement; it was a partnership. The customer was putting skin in the game, ensuring Yasho could deliver while reducing their own capital requirements.

This deal is projected to generate approximately Rs 150 crore in annual revenue, with supply expected to begin by the end of the fiscal year 2027. To contextualize: this single contract would represent roughly 20% of Yasho's current revenues. But more than the financial impact, it validated Yasho's evolution from opportunistic supplier to strategic partner for global corporations.

The deal's genesis revealed how far Yasho had traveled. Yasho has credibility with customers as can be seen from its blue-chip customer list (Lanxess, Michelin, Huntsman) and that it has always operated close to peak utilizations. This credibility enjoyed a further boost during Covid when it could ship products when its competitors struggled. The MNC contract wasn't won on price—Chinese competitors could always go lower. It was won on reliability, a currency more valuable than any cost advantage.

The sales price will be based on an agreed upon formula with our customer. We will be setting up the facility to build the plant in the next 12 to 18 months. We expect supply to start sometime by Q4 FY 27. Formula pricing—another sophistication marker. Rather than negotiating prices annually or quarterly, both parties agreed to a transparent mechanism tied to raw material costs. It removed pricing friction while ensuring sustainable margins for Yasho and predictable costs for the customer.

The international expansion wasn't without challenges. The consolidated results showed the strain: Yasho Industries Ltd's net profit fell -71.96% since last year same period to ₹5.03Cr in the Q4 2024-2025. Setting up international operations, hiring local teams, maintaining inventory in multiple geographies—all required upfront investment before revenue materialized. The J-curve of international expansion was playing out in real-time.

Yet the strategic logic remained sound. Yasho is also banking on its global presence, with exports contributing a significant 61% of revenue. Despite shipping challenges, export volumes have continued to grow, signalling robust demand across markets. The international subsidiaries weren't just about serving existing export markets better—they were about accessing customers who wouldn't consider a purely India-based supplier.

The Pakhajan facility's commissioning in 2024 marked another milestone. Parag Jhaveri, Managing Director & CEO said, "We are pleased to announce the commencement of commercial production at our new facility, marking a significant advancement in our journey of growth. Spread across 42acres, this expansive facility represents our commitment to expanding our operational footprint and enhancing our production capabilities". The facility wasn't just bigger—it was better. Automation levels that reduced labor dependency. Environmental systems that exceeded current regulations. Flexibility to produce multiple products without extensive changeovers.

The customer portfolio evolution during this period told its own story. From primarily Indian companies and trading houses, Yasho now served diverse clients like Dabur India, Wacker, HP, Indian Oil, Balmer Lawrie, Continental Tyres, MRF, JK, Apollo and Lanxess. The mix—Indian consumer goods companies, German specialty chemical giants, tire manufacturers, oil companies—showcased the breadth of applications for Yasho's products.

Market dynamics during 2024-25 presented both challenges and opportunities. China is currently contributing to 75% of global rubber chemicals supply although their domestic demand does not exceed 35% of the global demand. This structural imbalance—China producing far more than it consumed—created persistent pricing pressure. But it also meant any disruption to Chinese supply would create immediate opportunities for alternative suppliers like Yasho.

The recent quarterly results showed green shoots despite headline challenges. Total Revenue: Rs 19,901.56 lakh compared to Rs 17,495.27 lakh during Q1FY25, change 13.75%. EBITDA: Rs 3,386.86 lakh compared to Rs 2,382.96 lakh during Q1FY25, change 42.13%. PAT: Rs 364.46 lakh compared to Rs -246.18 lakh during Q1FY25. The return to profitability and EBITDA expansion suggested operational improvements were bearing fruit.

Management commentary reflected cautious optimism. Parag Jhaveri, Managing Director & CEO said: "The global chemical industry continues to remain volatile. We continue to face pressure on selling prices due to the current global uncertainty. We are confident to achieve > 40% growth in FY26". Forty percent growth might seem aggressive given current challenges, but with Pakhajan ramping up and the MNC contract approaching commercialization, the targets appeared achievable.

VII. Business Model & Competitive Advantages

Walk into any large chemical company's purchasing department and you'll find a vendor evaluation matrix. Price, quality, delivery, technical support—all rated and weighted. But dig deeper into how purchasing managers actually make decisions, and you'll discover something else entirely: risk mitigation. In specialty chemicals, where a bad batch can shut down a production line or trigger a product recall, the question isn't "who's cheapest?" but "who won't let us down?" This psychology sits at the heart of Yasho's business model.

The company's customer base tells this story eloquently. Over 1,000 clients across 50+ countries, ranging from local soap manufacturers to Fortune 500 multinationals. The marquee names jump off the page: Dabur, Continental, Hindustan Petroleum, Apollo Tyres, CEAT, Adani Wilmar, MRF. But it's the customer behavior that's truly revealing. For any B2B company, credibility is the hardest to establish. No customer will give long term volume commitments unless they have seen a working plant which can deliver quality at scale. Hence, one needs to invest ahead of time to demonstrate commitment, reliability, and ability to deliver at significantly higher scale. However, credibility scales exponentially once trust is established. It makes no sense for customers to cultivate a strategic supplier and then give it a non-material share of their business as that creates needless complexity without de-risking.

This trust-based model manifests in fascinating ways. Take the export percentage—53% of revenues from international markets. In commodity chemicals, exports usually mean competing on price in spot markets. But Yasho's exports follow a different pattern. Long-term contracts, formula-based pricing, technical collaboration agreements. These aren't transactional relationships where customers constantly shop for better prices. They're partnerships where switching costs—both economic and operational—create natural stickiness.

The product portfolio architecture reveals strategic thinking refined over decades. Five verticals—aroma chemicals, food antioxidants, rubber chemicals, lubricant additives, and specialty chemicals—might seem random to casual observers. But there's an elegant logic underneath. Our engineering and process teams have designed multipurpose plants which allows us to manufacture more than 100 products and fulfill our customer's quality and volume requirements. Multipurpose plants mean the same reactor that produces a rubber accelerator on Monday can manufacture a food antioxidant on Thursday. This flexibility is kryptonite to focused single-product competitors.

The technical moats deserve special attention. On the other hand, Buyers are very fragmented. There are over 800 brands selling lubricants and about 10 of them have about ~50% market share with the balance shared between the others. What makes things interesting is that many Lube Additive players compete with their customers as they have interests across the value chain. This is the opportunity for Yasho as small brands lack supply security. Yasho doesn't compete with its customers—a strategic choice that opens doors closed to vertically integrated competitors.

The certification portfolio functions as both shield and sword. REACH pre-registration for Europe, HALAL for Middle Eastern markets, KOSHER for specific customer requirements, NSF for food-contact applications, FSSC for food safety. Each certification costs lakhs to obtain and years to maintain. But together, they create a regulatory moat that's nearly impossible for new entrants to quickly replicate. A Chinese competitor might match Yasho's prices, but can they provide REACH-registered products with HALAL certification and NSF approval? The combination complexity becomes prohibitive.

R&D capabilities have evolved from basic quality control to genuine innovation. The DSIR-certified R&D facility isn't just a compliance checkbox—it provides tax benefits that improve project economics. The evolution from 6 to 38 R&D staff represents more than headcount growth. It's the difference between reverse engineering existing products and developing novel solutions. When a customer approaches with a specific performance requirement—a rubber additive that works at extreme temperatures, a lubricant component that extends oil life—Yasho can now say "we'll develop it" rather than "we don't make that."

The import substitution angle provides natural protection in domestic markets. When a product carries 20-30% import duties, transportation costs, and 60-90 day lead times, local manufacturing enjoys substantial advantages even at similar production costs. But Yasho layers additional value: local inventory, technical support in local languages, payment terms in rupees, and crucially, the ability to supply smaller lots that importers won't handle. An SME tire manufacturer in Tamil Nadu can't buy a 20-ton container of rubber accelerator from China, but they can buy 500 kg from Yasho with 7-day delivery.

Geographic positioning amplifies these advantages. The manufacturing facilities located in Vapi, Gujarat is 200 km from the port which allows us to serve customers throughout the globe. This isn't just about logistics efficiency. It's about balancing import of raw materials with export of finished goods, optimizing container utilization, and maintaining the flexibility to serve both domestic and international markets without preference or penalty.

The working capital model reveals operational sophistication. Chemical manufacturing typically requires substantial working capital—raw materials purchased on cash, finished goods sold on credit. But Yasho's model shows interesting variations. Export sales often come with letters of credit, improving cash conversion. The 15-year MNC contract includes customer advances for capacity building. Long-term contracts enable better raw material planning, reducing inventory requirements. These incremental improvements compound into superior return on capital employed.

Competitive dynamics in specialty chemicals differ markedly from commodities. Lubricant Additive 1 is a USD 15 B market where Yasho has <0.1% market share. Rubber Chemicals is a USD 5 B export opportunity where Yasho has <1% market share (China at 27%). Plastic Additives/stabilizers 2 which are a USD 500M export opportunity where Yasho has <1% market share (China 8%). The minuscule market shares might seem concerning, but they represent enormous headroom. Yasho doesn't need to dethrone market leaders—growing from 1% to 2% market share doubles the business.

The customer acquisition strategy follows a land-and-expand model reminiscent of enterprise software. Start with one product, prove reliability, then gradually expand the relationship. A rubber manufacturer might begin buying accelerators, then add antioxidants, then lubricant additives for their machinery. Each additional product increases switching costs and relationship depth. The 1,000+ customer base provides diversification, but the focus on expanding share of wallet with existing customers drives growth efficiency.

Sustainability initiatives, often dismissed as compliance overhead, create competitive advantages. Effluent treatment capabilities that exceed regulations become selling points to environmentally conscious customers. Energy efficiency improvements reduce costs while earning carbon credits. Zero liquid discharge systems, expensive to implement, signal long-term commitment that fly-by-night competitors can't match. In specialty chemicals, where customers conduct supplier audits, these capabilities become table stakes for multinational corporations.

VIII. Financial Performance & Market Dynamics

The Nifty Specialty Chemicals Index tells a story of boom, bust, and bewilderment. From 2020 to 2021, specialty chemical stocks were market darlings—China supply disruptions, global supply chain realignment, the "China Plus One" narrative. Every specialty chemical company, regardless of merit, saw valuations soar. Then came the reckoning. Chinese capacity returned with a vengeance, global demand softened, and the same stocks that had multiplied became wealth destroyers. Against this backdrop, Yasho's financial journey offers lessons in both operational excellence and market psychology.

The stock price trajectory reads like a thriller. From the IPO price of ₹100 in April 2018 to ₹101.25 on listing—a pedestrian start. The SME platform years saw steady appreciation, reaching ₹150-160 by late 2020. Then came the mainboard migration and the specialty chemical mania. Any report that there is a company whose share prices have shot up 7.7 times in the span of 12 months would probably be met with disbelief and raised eyebrows. The Rs10 paid up shares of the company, which were moving in the range of Rs150-160 in November 2020 rocketed to over ₹1,200 by November 2021.

The ascent continued, peaking around ₹2,330 before reality intruded. Today, the stock trades around ₹1,700-1,800—still a 17-fold return from IPO, but down 25% from peaks. This volatility isn't just about Yasho—it reflects the sector's fundamental challenge. Specialty chemicals sit at the intersection of global trade, environmental regulation, and industrial demand. When any of these factors shift, valuations whipsaw accordingly.

Quarterly financial performance tells a more nuanced story than stock prices suggest. The company's consolidated net profit was at Rs 3.64 crore in Q1 FY26 as against net loss of Rs 2.46 crore in Q1 FY25. Net sales jumped 13.9% year on year to Rs 198.64 crore in Q1 FY26. Revenue growth continues, but profitability remains under pressure. This disconnect—growing revenues, shrinking margins—plagues the entire sector.

The margin pressure has multiple villains. Chinese oversupply tops the list. When competitors dump products at marginal cost, pricing discipline becomes impossible. Raw material volatility adds another layer—petroleum derivatives, the building blocks of most chemicals, fluctuate with oil prices. Currency movements compound the challenge. With 60%+ revenues from exports but costs largely in rupees, exchange rate movements directly impact margins. A 2% rupee appreciation can wipe out quarterly profits.

Yet focusing solely on recent margin pressure misses the longer arc. From FY18 revenues of ₹338 crores to FY24's ₹668 crores, Yasho nearly doubled its top line in six years. This growth came despite COVID disruptions, Chinese competition, and raw material inflation. The revenue resilience suggests the business model's fundamental strength even as profitability faces headwinds.

The balance sheet evolution reveals strategic priorities. In FY17 it was 6.8, which was brought to 3.8 in FY18, 2.9 in FY29 and further scaled down to 2.5 in FY20 and 1.7 in FY21. The debt-equity ratio's steady decline even during aggressive capacity expansion shows remarkable capital discipline. This conservative leverage provides flexibility—the ability to weather downturns without financial distress and capitalize on opportunities without dilution.

Working capital management presents ongoing challenges. Chemical manufacturing inherently requires substantial working capital—raw material inventory, work-in-progress across multiple products, finished goods awaiting shipment. The international expansion added complexity. Maintaining inventory in European and US warehouses ties up capital but enables faster customer service. It's a classic trade-off between efficiency and effectiveness.

The shareholder structure has evolved interestingly. Promoter holding in Yasho Industries Ltd has gone down to 67.99 per cent as of Jun 2025 from 71.92 per cent as of Dec 2024. The gradual promoter stake reduction suggests either profit booking or strategic stake sales to institutional investors. Foreign institutional investors raised their stake from 1.41% to 7.24%, while retail investors hold 24.25%. Ace investor Ashish Kacholia owns 3.9% as of March 2025. Kacholia's presence—he's known for identifying multibaggers early—provides validation and visibility.

The recent quarterly numbers show operational improvements despite headline challenges. EBITDA margins expanded from 13.6% to 17% year-on-year in Q1 FY26. This margin expansion during a period of intense competition suggests operational efficiencies are kicking in. The Pakhajan facility's automation, scale economies, and better product mix likely drive these improvements.

Management commentary provides insight into near-term expectations. Despite these challenges, we are confident to achieve 40-50% revenue growth in FY 26 while maintaining current margins. This guidance seems aggressive given current market conditions. But with Pakhajan operating at 50% utilization and ramping up, the US warehouse operational, and the MNC contract approaching commercialization, the targets appear achievable.

The capital allocation framework has matured considerably. From FY22-24, Yasho invested ₹400 crores in capex—more than the company's cumulative investment in its first 25 years. This front-loaded investment positions the company for the next growth phase. With major capacity expansion complete, future cash flows can fund growth without massive additional investment.

Market perception remains mixed. At ₹1,700-1,800 per share, the stock trades at a P/E of 170+—seemingly expensive for a manufacturing company. But the earnings are temporarily depressed. On normalized margins, the valuation appears more reasonable. The market seems to be looking through current challenges to future potential—the operating leverage from Pakhajan, the MNC contract's revenue visibility, the structural growth in specialty chemicals.

The competitive dynamics continue evolving. There is a large Opportunity for Yasho to take share of global supply chains in Industrial Chemicals. Starting market shares are low. The China Plus One narrative may have faded from headlines, but the underlying logic remains. Global customers learned painful lessons about single-source dependencies. They may not abandon Chinese suppliers entirely, but they're actively cultivating alternatives. Yasho, with proven reliability and expanding capacity, stands to benefit from this rebalancing.

Commodity cost pressures present both challenge and opportunity. When raw material prices spike, smaller competitors struggle to finance inventory. Their distress becomes Yasho's opportunity—to gain market share, acquire customers, potentially even acquire assets. The strong balance sheet and banking relationships become competitive weapons during industry stress.

IX. Playbook: Lessons for Chemical Industry Entrepreneurs

The conference room at IIT Chemical Engineering's entrepreneurship cell was packed. Aspiring chemical industry entrepreneurs, armed with technical degrees and startup dreams, peppered the panel with questions. "How do you compete with China?" asked one. "Where do you find initial customers?" wondered another. The panelist, a veteran who'd built and sold a specialty chemical company, paused before answering: "Study Yasho Industries. They made every transition you'll need to make."

Lesson 1: The Trading-to-Manufacturing Bridge Most chemical entrepreneurs face an impossible choice: start as traders with minimal capital but no differentiation, or jump straight into manufacturing with massive capital requirements but no market knowledge. Yasho's playbook offers a third way. Begin trading to understand market dynamics, identify product gaps, build customer relationships. Use trading profits to fund initial manufacturing. Then gradually shift the mix from trading to manufacturing. This bridge strategy reduces risk while building capabilities.

The key insight: trading isn't just about working capital management—it's market research that pays for itself. Every import order reveals pricing dynamics, quality specifications, customer pain points. Every customer complaint about imports—delivery delays, minimum order quantities, payment terms—becomes a manufacturing opportunity. The trading years aren't wasted time; they're paid education.

Lesson 2: The Specialty Selection Framework Not all specialties are created equal. Yasho's product selection reveals consistent patterns. First, products with technical complexity that creates barriers to entry. Rubber accelerators require understanding of polymer chemistry. Food antioxidants demand regulatory expertise. Second, products where India has raw material advantages or proximity to raw materials. Third, products serving industries with presence in India—tire manufacturing, food processing, lubricant blending.

The anti-pattern is equally instructive. Avoid products where scale is everything, where technology changes rapidly, or where customers can easily backward integrate. Yasho doesn't make base chemicals that any refinery can produce. They don't chase pharmaceutical intermediates where patents and rapid obsolescence destroy returns. They focus on the boring middle—products essential enough that customers need reliable supply, complex enough that not everyone can make them, but not so specialized that the market becomes tiny.

Lesson 3: The Certification Accumulation Strategy The Company has received various certifications confirming its products to be in line with National and International Standards i.e. HALAL Certifications, STAR KOSHER Certifications, NSF Certifications, FAMIQS Certification, FSSC Certification. Each certification seems minor individually, but collectively they create a formidable moat. A competitor might match one or two, but matching all becomes prohibitively expensive and time-consuming.

The sequencing matters. Start with basic quality certifications (ISO 9001) that improve internal processes. Add industry-specific certifications that open customer doors. Layer market-access certifications (REACH for Europe) that competitors struggle to match. Finally, add nice-to-have certifications that signal sophistication. This staged approach spreads costs while progressively building competitive advantages.

Lesson 4: The Capital-Light to Capital-Intensive Transition The temptation for successful chemical traders is to immediately build world-scale plants. Yasho's journey suggests patience. Start with small, multipurpose facilities. Prove the model, generate cash flows, build credibility. Only then undertake major expansions. The Pakhajan investment—₹470 crores—came only after decades of capability building and years of public market scrutiny.

This transition timing is crucial. Too early, and you lack the capabilities to utilize the capacity efficiently. Too late, and growth opportunities pass you by. Yasho timed it for when they had proven demand (customers they couldn't serve), proven capabilities (successful operation of existing plants), and access to capital (post mainboard migration). All three conditions were necessary; any two insufficient.

Lesson 5: The Customer Concentration Balance With 1,000+ customers across 50+ countries, Yasho appears highly diversified. But dig deeper—the top customers likely contribute disproportionate revenues. This concentration isn't necessarily bad if managed properly. Large customers provide volume, stability, and credibility. They push you to improve, to meet international standards, to innovate. But dependence is dangerous.

Yasho's approach: use large customers as capability developers, not revenue dependencies. The MNC contract for ₹150 crores annually is significant but not existential. It's large enough to justify dedicated capacity but not so large that losing it would cripple the company. This balance—concentrated enough for efficiency, diversified enough for resilience—is the sweet spot.

Lesson 6: The Working Capital Optimization Playbook Chemical manufacturing is working capital intensive, but not all working capital is equal. Yasho's model shows how to optimize each component. Raw materials: build supplier relationships that provide credit terms. Work-in-process: design multipurpose plants that reduce changeover inventory. Finished goods: locate warehouses near customers to reduce in-transit inventory. Receivables: use letters of credit for exports, maintain strict credit discipline domestically.

The international subsidiaries add complexity but also opportunity. European customers paying a Dutch entity in euros eliminates currency risk and accelerates collections. The US warehouse enables smaller, more frequent shipments, reducing customer inventory requirements and increasing stickiness. These structural improvements to working capital are more sustainable than simply squeezing payment terms.

Lesson 7: The R&D Investment Philosophy There is a visible step up in R&D efforts for future products. The R&D team has been strengthened from 6 people in 2019 to 38 people in 2023. But this isn't R&D for its own sake. Yasho doesn't pursue Nobel prizes or breakthrough molecules. Their R&D focuses on practical outcomes: process optimization to reduce costs, product customization for specific customers, application development to expand addressable markets.

The DSIR certification provides tax benefits, but more importantly, it forces discipline. Documented processes, measurable outcomes, regular audits. This structure transforms R&D from cost center to profit contributor. When customers need modifications, Yasho can quote development costs confidently. When regulations change, they can adapt formulations quickly. This responsive R&D model suits specialty chemicals better than breakthrough innovation.

Lesson 8: The Capital Market Navigation Strategy The progression from SME listing to mainboard migration offers a template for other industrial companies. Don't rush to mainboard—use SME platform to learn public market disciplines. Build track record, improve governance, demonstrate consistent performance. Only then migrate to access institutional capital.

Post-migration, resist the temptation to grow for growth's sake. Yasho could have used its elevated valuations to make acquisitions, enter new geographies, or diversify into adjacent industries. Instead, they stuck to their knitting—expanding capacity in known products, deepening existing customer relationships, building on proven capabilities. This discipline, boring as it seems, creates sustainable value.

X. Bear vs. Bull Case & Future Outlook

The Bull Case: Structural Tailwinds and Strategic Positioning

The optimists see Yasho at an inflection point. Start with the macro picture: global specialty chemicals market growing at 5-6% annually, faster in emerging applications like electric vehicle lubricants and sustainable rubber compounds. Layer the China Plus One dynamic—not the headlines, but the quiet reality of procurement managers diversifying supplier bases. Add India's manufacturing push, infrastructure improvements, and chemical park development. The structural tailwinds are powerful and persistent.

The company-specific catalysts are even more compelling. Yasho Industries Limited, a manufacturer and supplier of specialty chemicals, has signed a long-term agreement for a period of 15 years with a global MNC for the supply of a lubricant additive. This deal is projected to generate approximately Rs 150 crore in annual revenue. This single contract provides revenue visibility rare in chemical manufacturing. It validates Yasho's technical capabilities, provides cash flow certainty for debt servicing, and most importantly, signals to other MNCs that Yasho is a credible long-term partner.

The capacity expansion math is straightforward. Post expansion, the total manufacturing capacity will increase from 11,000 MTPA to 26,500 MTPA with a revenue potential of Rs500 crore to Rs550 crore in Phase 1 at full capacity utilisation. With current revenues around ₹670 crores from 11,000 MTPA capacity, the additional 15,500 MTPA could theoretically double revenues. Even at 70% utilization and current pricing, Pakhajan alone could add ₹400+ crores to the top line.

The operational leverage story excites investors most. Specialty chemicals have high fixed costs—depreciation, maintenance, quality control, R&D. These costs don't scale linearly with production. As Pakhajan ramps up, the fixed cost per unit drops dramatically. If Yasho can maintain current EBITDA margins of 17% while doubling revenues, absolute EBITDA could reach ₹200+ crores. At a reasonable multiple, the market cap could double from current levels.

International expansion provides another growth vector. The European subsidiary is still subscale, the US operations just beginning. As these operations mature, they could contribute 20-30% of revenues while improving margins through better pricing and reduced logistics costs. The ability to serve global customers locally transforms Yasho from an Indian exporter to a global supplier—a rerating catalyst when it materializes.

The product pipeline offers hidden optionality. With 38 R&D professionals and a new state-of-the-art laboratory coming online in October 2025, Yasho can accelerate new product development. Each successful product launch expands the addressable market, deepens customer relationships, and improves margins. The specialty chemical industry rewards innovation with premium pricing—a dynamic Yasho is positioned to exploit.

The Bear Case: Structural Challenges and Execution Risks

The skeptics see red flags everywhere. Start with the recent performance: net profit declined 89.45% to Rs 6.11 crore in the year ended March 2025 as against Rs 57.94 crore during the previous year ended March 2024. Yes, revenues grew, but what use is growth without profitability? The margin collapse suggests either structural challenges or execution failures—neither inspiring confidence.

China remains the 800-pound gorilla. China is currently contributing to 75% of global rubber chemicals supply although their domestic demand does not exceed 35% of the global demand. This massive overcapacity won't disappear overnight. Chinese manufacturers, backed by state support and operating at scales Yasho can't match, can sustain losses longer than Yasho can remain solvent. Every uptick in pricing brings more Chinese capacity online, capping margin recovery.

The execution track record raises questions. The Pakhajan project overran by ₹70 crores—nearly 18% above budget. While management attributed this to scope expansion and automation, cost overruns suggest either poor planning or weak project management. With more expansion planned, can investors trust execution capabilities?

Customer concentration, despite 1,000+ clients, remains concerning. The new MNC contract will contribute 20%+ of revenues. Large customers have negotiating leverage, demanding price reductions, extended payment terms, and dedicated capacity. As Yasho becomes more dependent on a few large contracts, margins could face structural pressure.

The competitive landscape is intensifying. Other Indian specialty chemical companies are expanding aggressively. Global majors are establishing Indian operations. Chinese companies are setting up plants in India to circumvent tariffs. The window of opportunity from supply chain diversification may be shorter than bulls anticipate. Yasho's first-mover advantages in certain products are eroding as competition catches up.

Working capital requirements could strain finances. As revenues double, working capital needs could increase by ₹200+ crores. While the MNC contract includes advances, other growth will require funding. With limited cash generation currently, this could mean more debt or dilutive equity raises—neither attractive for existing shareholders.

Regulatory risks lurk beneath the surface. Chemical manufacturing faces increasing environmental scrutiny. Single pollution violations can shut plants for months. As Yasho expands, regulatory compliance becomes more complex and costly. The European REACH regulations are tightening, potentially requiring expensive retesting and registration. Any regulatory misstep could derail growth plans.

The Probabilistic Path Forward

Reality likely lies between these extremes. Yasho has demonstrated resilience through multiple cycles—the 2008 financial crisis, COVID-19, the current China oversupply situation. This suggests a business model more robust than bears acknowledge but less dominant than bulls hope.

The most probable scenario: steady but unspectacular growth. Revenues could reach ₹1,000 crores by FY27 as Pakhajan ramps and the MNC contract commercializes. Margins might stabilize around 15% EBITDA—below historical peaks but above current troughs. This would generate ₹150 crores EBITDA, supporting a ₹3,000-3,500 crore market cap at sector multiples. Decent returns, but not the multibagger some expect.

The key variables to monitor: Pakhajan utilization rates, which signal demand reality versus management optimism. Working capital cycles, which reveal operational efficiency or stress. R&D commercialization success, which indicates innovation capabilities. And critically, the next large contract announcement—evidence that the MNC deal wasn't a one-off but part of a pattern.

The time horizon matters enormously. Over the next 12-18 months, China oversupply and margin pressure likely persist. Bears could be right temporarily. But over 3-5 years, the structural growth in specialty chemicals, Yasho's expanded capacity, and customer relationships position it well. Bulls might ultimately prevail, but patience will be tested.

XI. Epilogue: What Would We Do?

Standing in Yasho's boardroom today, looking at the chess pieces on the board, what moves would we make? The company has capacity, capabilities, and customer relationships. It has survived the brutal margin compression of 2024-25. The foundation is solid, but the structure needs reinforcement.

Priority 1: Operational Excellence Over Growth The temptation after massive capacity expansion is to chase volume at any cost. Resist. Focus instead on operational excellence at Pakhajan. Achieve 70% utilization at target margins before considering Phase 2 expansion. Use automation investments to reduce costs by 10-15%. Implement Toyota Production System principles—eliminate waste, reduce changeovers, improve yield. Boring? Yes. Essential? Absolutely.

Priority 2: Customer Portfolio Rebalancing The MNC contract is wonderful but dangerous if it creates dependency. Actively cultivate 5-10 similar relationships with global corporations. Target customers in defensive industries—food, healthcare, consumer goods—that are less cyclically exposed than automotive or construction. Build redundancy in the customer base before the market forces it.

Priority 3: Backward Integration, Selectively The margin pressure from raw material volatility suggests selective backward integration. Don't try to make everything—that's a capital allocation disaster. But identify 2-3 critical raw materials that constitute 40%+ of costs and evaluate make-versus-buy. Even partial backward integration can provide negotiating leverage with suppliers.

Priority 4: Green Chemistry Initiative Sustainability is shifting from nice-to-have to must-have. Launch a green chemistry initiative—not for PR, but for competitive advantage. Develop bio-based alternatives to petroleum-derived products. Create closed-loop processes that eliminate waste. Partner with customers on sustainability goals. This positions Yasho for the next decade, not just the next quarter.

Priority 5: M&A, But Carefully With the balance sheet stabilizing and operations maturing, consider bolt-on acquisitions. Not transformative deals that distract management, but small acquisitions that bring specific capabilities: a product line, a customer relationship, a technology. Pay reasonable multiples, integrate carefully, and ensure cultural fit. The specialty chemical industry has many subscale players struggling with compliance costs—opportunity for consolidation at attractive prices.

Priority 6: Capital Allocation Discipline The next few years will generate substantial cash as Pakhajan ramps and the MNC contract kicks in. Resist the empire-building temptation. Return excess cash to shareholders through dividends or buybacks when the stock is cheap. Maintain debt at conservative levels—the chemical industry is too volatile for aggressive leverage. Signal capital allocation discipline to attract quality investors.

Final Reflections

Yasho Industries represents something increasingly rare in Indian business—a manufacturing company that actually manufactures, a family business professionalizing without losing its entrepreneurial edge, a small company competing globally without losing its roots. The journey from Vasu Preservatives to a ₹2,000 crore market cap company wasn't preordained. It required vision, persistence, and not a small amount of luck.

For students of business strategy, Yasho offers rich lessons. The importance of timing—entering specialty chemicals just as India's manufacturing competitiveness improved. The value of patience—taking decades to build capabilities rather than rushing into capacity expansion. The power of focus—resisting diversification temptations to deepen expertise in chosen niches.

But perhaps the most important lesson is about industrial transformation in emerging markets. Yasho didn't try to out-innovate BASF or outscale Sinopec. It found a middle path—sophisticated enough to serve global customers, nimble enough to adapt to local conditions, scaled enough to compete but not so large as to lose flexibility. This model—call it "appropriate sophistication"—might be the template for industrial champions in emerging markets.

The next chapter remains unwritten. Will Yasho become India's specialty chemical champion, growing to ₹10,000+ crores revenue? Will Chinese competition force consolidation, making Yasho an acquisition target? Will the third generation—Dishit Jhaveri already working in R&D—take the company in entirely new directions? These questions await answers.

What's certain is that Yasho's story is far from over. In an industry where success requires thinking in decades, not quarters, Yasho has just completed its first act. The stage is set, the actors are in place, and the audience—customers, investors, competitors—watches with interest. Whether the next act is triumph or tragedy depends on decisions being made today in Mumbai offices and Vapi laboratories.

For investors, entrepreneurs, and students of business, Yasho Industries offers a living case study in industrial transformation. It's a reminder that in the physical world of atoms and molecules, competitive advantages are built slowly but can endure for generations. In an era obsessed with digital disruption and asset-light models, there's something reassuring about a company that makes real things for real customers solving real problems.

The specialty chemicals industry will continue evolving. New technologies, changing regulations, shifting supply chains—all will create challenges and opportunities. But companies like Yasho, with technical depth, customer relationships, and patient capital, are positioned to not just survive but thrive. The journey from Mumbai chemical trader to global specialty giant is complete. The journey to whatever comes next has just begun.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube