TD Power Systems: India's Hidden Power Generator Champion

I. Introduction & Episode Roadmap

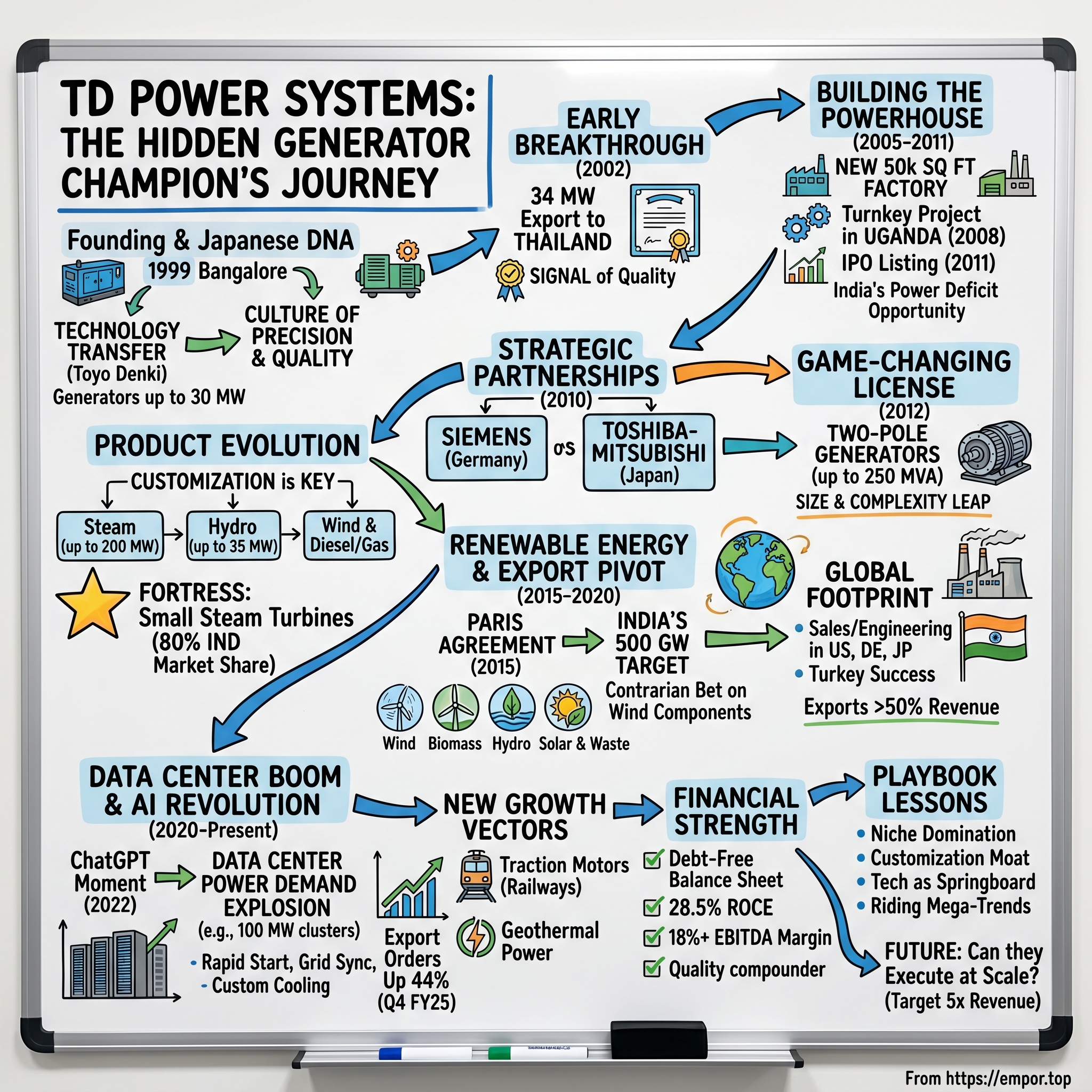

Picture this: In a nondescript industrial estate on the outskirts of Bangalore, engineers huddle over blueprints for a 200-megawatt generator—a machine so large it could power a small city. The company they work for isn't General Electric, Siemens, or any of the industrial giants you'd expect. It's TD Power Systems, a name most investors have never heard of, despite its ₹7,385 crore market cap and debt-free balance sheet that would make any CFO jealous.

Here's the hook that caught our attention: How did a 25-year-old Indian company, started with Japanese technology transfer, become a global leader in generators up to 200 MW? More intriguingly, how did they carve out an estimated 80% market share in small steam turbine generators (up to 52 MW) while competing against both local behemoth BHEL and global MNCs?

TD Power Systems represents something fascinating in the Indian industrial landscape—a company that took the classic emerging market playbook of technology transfer and licensing, then flipped it into genuine technological capability and global competitiveness. They're not just assembling foreign designs anymore; they're custom-engineering solutions for data centers in Virginia, wind farms in Turkey, and hydro plants in Uganda.

What makes this story particularly compelling right now is the confluence of mega-trends TDPS is riding. The AI boom has created unprecedented demand for data center power generation. India's ambitious 500 GW renewable energy target by 2030 is driving domestic orders. Global industrial capex is resurging after years of underinvestment. And somehow, this Bangalore-based manufacturer is positioned at the intersection of all three.

The numbers tell a story of acceleration: Consolidated net profit jumped 47.5% to ₹174.58 crore in FY25, with revenue climbing 27.8% to ₹1,278 crore. Export orders surged 44.77% year-over-year, while domestic orders rose 39.24%. Management's FY26 guidance of ₹1,500 crore already looks conservative, with whispers of an upward revision coming.

But this isn't just a momentum story. It's a masterclass in how to build a global industrial champion from an emerging market, navigate technology partnerships without becoming dependent, and maintain pricing power in a commoditized industry through customization and engineering excellence. Let's dive into how a company named after Toyo Denki—its Japanese technology partner—became India's answer to the global power generation oligopoly.

II. The Founding Story & Japanese Connection (1999-2005)

The late 1990s in Bangalore were electric with possibility. The Y2K boom had put Indian engineering talent on the global map, but while everyone obsessed over software, a different kind of opportunity was taking shape in the industrial sector. India's power deficit was chronic—blackouts were routine, industrial growth was constrained, and the state-owned BHEL couldn't keep up with demand.

On April 16, 1999, TD Power Systems Private Limited was incorporated in Bangalore. The founding team wasn't starting from scratch—they had something more valuable than capital: a technology transfer agreement with Toyo Denki, a Japanese firm with decades of experience in generator manufacturing. The "TD" in the company name literally stood for Toyo Denki, a refreshingly honest acknowledgment of where the technical DNA came from.

The Japanese connection wasn't accidental. By 2001, the partnership had deepened, with Toyo Denki transferring technology for generators up to 30 MW capacity. This wasn't just about blueprints and specifications—it was about absorbing an entire manufacturing philosophy. Japanese industrial culture, with its obsession over quality, continuous improvement (kaizen), and respect for engineering precision, would fundamentally shape TD Power Systems' DNA.

Consider the context: India in 2001 was still reeling from economic sanctions after the 1998 nuclear tests. Foreign technology transfer wasn't just business strategy—it was almost an act of industrial diplomacy. The Japanese, unlike their Western counterparts, were willing to share real technology, not just outdated designs. They saw India not as a threat but as a complementary manufacturing base.

The early team at TDPS understood something crucial: in the generator business, credibility is everything. When you're selling a machine that costs millions and is expected to run continuously for decades, customers don't experiment with unknowns. They needed a proof point, something that would signal they weren't just another Indian engineering firm trying to reverse-engineer foreign technology.

That proof point came in 2002 with their first major triumph: a 34 MW generator export to Thailand. Think about the audacity of this—a three-year-old Indian company, in an industry dominated by century-old giants, winning an export order to another Asian market. The Thailand order wasn't just about the revenue; it was a signal that TDPS could compete on quality and delivery, not just price.

The founding team, including Nikhil Kumar who would later become Managing Director, spent these early years in an almost monastic devotion to learning. They weren't content being assemblers of Japanese designs. Every project was dissected, every failure analyzed, every customer complaint treated as a learning opportunity. The Japanese partners noticed—this wasn't the typical licensor-licensee relationship where the local partner just wanted to slap a foreign brand on locally made products.

By 2005, TDPS had built something remarkable: a 50,000 square foot manufacturing facility in Dabaspet, near Bangalore, with the capability to produce generators that actually worked reliably in Indian conditions—extreme heat, dust, voltage fluctuations, and maintenance neglect. They had taken Japanese precision and adapted it to Indian realities.

Building credibility meant taking on the established order. BHEL, the state-owned behemoth, had a near-monopoly in large generators. Global players like GE and Siemens dominated the high-end segment. But TDPS found a sweet spot—the 5-50 MW range where customers needed customization, local support, and competitive pricing. They weren't trying to build the biggest generators; they were building the right generators for emerging market realities.

The philosophical divide between TDPS and its competitors was stark. While others pursued scale and standardization, TDPS embraced customization. Each generator was essentially a bespoke solution, engineered for specific customer requirements. This approach was more expensive, required deeper engineering capabilities, and made manufacturing more complex. But it also created switching costs and customer loyalty that pure price competition couldn't break.

As 2005 drew to a close, the company stood at an inflection point. They had proven they could absorb and adapt foreign technology. They had won credibility in export markets. They had found a defensible niche. The question now was whether they could scale beyond being a successful small player into something more ambitious—a true manufacturing powerhouse.

III. Building the Manufacturing Powerhouse (2005-2011)

The year 2008 marked a watershed moment, not for what happened in Bangalore's factories, but 4,000 kilometers away in Uganda. TD Power Systems had just commissioned its first overseas turnkey project—a 16.5 MW steam turbine power plant in a country most Indian companies wouldn't even consider. While the world was melting down in the global financial crisis, TDPS was proving it could not just manufacture generators, but execute complete power projects in frontier markets.

The Uganda project was emblematic of a larger strategic shift. Management realized that to truly compete globally, they needed to move up the value chain from component supplier to solution provider. In Uganda, they weren't just shipping a generator; they were responsible for design, procurement, installation, and commissioning. When the plant successfully came online, it sent a powerful signal: an Indian company could deliver complex infrastructure in Africa, competing directly with Chinese and Western firms.

But the real coup came in 2010 with dual partnerships that would fundamentally alter TDPS's trajectory. First came Siemens AG, the German industrial giant. Then Toshiba-Mitsubishi, the Japanese powerhouse. These weren't mere vendor relationships or casual technical collaborations. These were strategic partnerships where global giants were essentially endorsing TDPS as a trusted manufacturer for their supply chains.

The Siemens relationship deserves special attention. In the generator business, Siemens is royalty—150 years of engineering excellence, patents numbering in the thousands, installations in every major economy. For them to partner with a relatively unknown Indian firm wasn't charity; it was cold, calculated business logic. Siemens needed manufacturing capacity in Asia for cost competitiveness, but more importantly, they needed a partner who could maintain their quality standards. TDPS had proven they could.

Inside the company, the decision to go public was fiercely debated. The founding team, led by Nikhil Kumar who had risen through the ranks, understood that competing globally required capital—not just for machines and factories, but for working capital, R&D, and the ability to take on larger projects. But timing mattered enormously. The Indian capital markets in 2011 were skeptical of manufacturing stories. Software was sexy; industrial companies were seen as slow-growth, capital-intensive dinosaurs.

On September 8, 2011, TD Power Systems listed on both the BSE and NSE. The IPO wasn't a blockbuster—this wasn't a tech unicorn promising to change the world. It was a manufacturing company with real revenues, actual profits, and tangible assets. The pitch to investors was straightforward: India's power deficit wasn't going away, global energy demand would only grow, and TDPS had the technology partnerships and manufacturing capability to capture this opportunity.

The market's initial reception was lukewarm, but management didn't need validation from day traders. They needed patient capital for what came next. Just months after the IPO, in 2012, came the game-changing announcement: Siemens had licensed TDPS to manufacture two-pole generators up to 250 MVA. To understand the significance, consider that most of TDPS's existing portfolio was below 50 MW. This license was like a regional airline suddenly getting certification to fly intercontinental routes.

The Siemens license wasn't just about size; it was about technology complexity. Two-pole generators spin at 3,000 or 3,600 RPM (depending on grid frequency), compared to multi-pole generators that spin slower. The engineering challenges—balancing, vibration control, material stress—increase exponentially. That Siemens trusted TDPS with this technology was a massive vote of confidence.

Manufacturing these larger generators required a fundamental rethinking of production processes. The Dabaspet facility, impressive as it was, couldn't handle 250 MVA machines. The company embarked on a carefully orchestrated capacity expansion, adding specialized equipment like vacuum pressure impregnation (VPI) systems for insulation, dynamic balancing machines for rotors weighing several tons, and testing facilities that could simulate full-load conditions.

The cultural transformation during this period was equally important. The company was transitioning from an entrepreneurial, hustle-based culture to something more systematic and process-driven. Japanese influence was evident in the implementation of Total Productive Maintenance (TPM), 5S methodology, and just-in-time manufacturing principles. But unlike many Indian companies that blindly copied foreign management techniques, TDPS adapted them to local realities.

Quality control became an obsession. In the generator business, a single failure could destroy decades of reputation-building. TDPS implemented testing protocols that went beyond customer requirements. Every generator underwent a battery of tests—insulation resistance, high voltage, temperature rise, vibration, noise—with results meticulously documented. When customers visited the facility, they weren't just shown the manufacturing floor; they were walked through the quality processes, test certificates, and failure analysis systems.

The human capital story during this period is often overlooked but crucial. TDPS wasn't competing with IT companies for India's top engineering talent—they were competing for a different breed of engineer, ones who wanted to build physical products, who got excited about magnetic flux and rotor dynamics. The company established partnerships with engineering colleges, created apprenticeship programs, and more importantly, sent engineers to Germany and Japan for training.

Financial discipline during this expansion phase set TDPS apart from peers who gorged on debt during the 2005-2011 credit boom. Despite massive capital requirements for machinery and facilities, the company maintained conservative leverage ratios. This wasn't financial timidity—it was strategic patience. Management understood that in cyclical industries, the companies that survive downturns are those that don't overextend during booms.

By the end of 2011, TD Power Systems had transformed from a technology licensee to a legitimate manufacturing powerhouse. They had blue-chip technology partners, proven execution capability in international markets, and a public market currency for future growth. But the real test was coming: Could they leverage these capabilities to capture the massive opportunities emerging in renewable energy and meet the exploding power demands of the digital economy?

IV. The Product Portfolio Evolution

Walk into TD Power Systems' design center, and you'll find something unusual for an Indian manufacturing company: engineers debating the magnetic properties of grain-oriented silicon steel with the passion most reserve for cricket matches. This isn't just technical minutiae—it's the key to understanding how TDPS built a product portfolio that spans from 1 MW diesel generators for remote telecom towers to 200 MW behemoths for combined-cycle power plants.

The evolution of TDPS's product portfolio reads like a careful chess game, each move calculated to build on existing capabilities while opening new markets. By 2012, they had four distinct product verticals: generators for steam turbines (up to 200 MW), hydro turbines (up to 35 MW), diesel and gas engines (up to 20 MW), and increasingly important—customized generators for wind turbines.

The strategic brilliance lay not in the breadth but in the deliberate focus on customization. While competitors pursued economies of scale through standardization, TDPS went the opposite direction. Every generator was essentially engineered to order, optimized for specific operating conditions, fuel types, altitude, ambient temperature, and grid requirements. This approach was more expensive and complex but created a powerful moat.

Consider a typical customer scenario: A sugar mill in Brazil needs a 15 MW generator for their cogeneration plant, burning bagasse (sugar cane waste). The operating environment is hot, humid, with frequent load variations as the mill's power demand fluctuates. A standard generator might work, but TDPS would design one specifically for these conditions—modified cooling systems for tropical humidity, special insulation for temperature variations, and rotor dynamics optimized for the load profile. The result? Higher efficiency, longer life, and a customer who becomes deeply embedded with TDPS's engineering team.

This customization capability didn't happen overnight. It required building deep domain expertise across multiple technologies. Steam turbine generators operate on the Rankine cycle, converting high-pressure steam into rotational energy. Hydro generators work with water turbines, dealing with very different speed and torque characteristics. Gas engine generators must handle rapid start-stops and load variations. Wind turbine generators face unique challenges—variable speed operation, grid synchronization issues, and extreme weather conditions.

The wind turbine generator business deserves special attention. As India embarked on ambitious renewable energy targets, TDPS made a contrarian bet. While everyone rushed into solar panels and wind turbine manufacturing, TDPS focused on a critical but overlooked component—the generators inside wind turbines. These aren't simple machines; modern wind turbine generators must handle variable speed operation, convert fluctuating wind energy into stable grid power, and survive 20 years of continuous operation in harsh conditions.

TDPS developed capabilities in both doubly-fed induction generators (DFIG) and permanent magnet generators (PMG) for wind applications. The technical challenges were formidable—managing harmonics, ensuring grid code compliance across different countries, and achieving efficiency levels that made economic sense given the intermittent nature of wind. But by 2015, they had become a trusted supplier to major wind turbine OEMs, both in India and globally.

The small steam turbine generator segment (up to 52 MW) became TDPS's fortress. Here, they achieved an estimated 80% market share in India—a dominance that seems almost monopolistic. How did they achieve this? It wasn't through predatory pricing or regulatory capture. Instead, they understood that small steam turbine applications—biomass plants, industrial cogeneration, waste-to-energy facilities—required extensive customization and local support that global giants couldn't economically provide.

The technology partnerships played a crucial role in portfolio development. The Siemens license for two-pole generators opened doors to higher-speed applications—critical for combined-cycle gas turbine plants where efficiency is paramount. The Japanese partnerships brought expertise in materials science—special steel alloys for rotors, advanced insulation materials, innovative cooling designs. But TDPS didn't just implement foreign technology; they adapted and improved it.

One example of indigenous innovation: TDPS developed a modular stator design that allowed them to manufacture generators in segments, transport them separately, and assemble them on-site. This solved a massive logistics problem in India where transporting oversized equipment through narrow roads and weak bridges was often impossible. Global competitors with monolithic designs couldn't match this flexibility.

The move into traction motors around 2018 represented a logical adjacency. Motors and generators are essentially the same machine operating in reverse—one converts electrical energy to mechanical, the other mechanical to electrical. TDPS leveraged their electromagnetic design capabilities to enter the railway traction motor market, eventually winning a ₹300 crore contract for European railways—a testament to their quality and competitiveness.

Testing capabilities became a differentiator. TDPS invested in full-load testing facilities that could simulate actual operating conditions. When a customer ordered a 50 MW generator, TDPS could test it at full capacity, measuring efficiency, temperature rise, vibration, and harmonics. Competitors often relied on calculation and partial testing. This real-world validation became a powerful selling point, especially for risk-averse customers in critical applications.

The product portfolio evolution also reflected changing market dynamics. As distributed generation became more prevalent, TDPS developed smaller, more flexible generators suitable for microgrids and industrial captive power plants. As data centers proliferated, they engineered generators optimized for the unique requirements of backup power—rapid start capability, parallel operation, and fuel flexibility.

Materials innovation became increasingly important. TDPS worked with steel suppliers to develop specialized electrical steels with lower core losses. They experimented with advanced composites for insulation systems that could withstand higher temperatures, enabling more compact designs. They pioneered the use of vacuum pressure impregnation for smaller generators, a technology typically reserved for larger machines, improving reliability and lifespan.

The portfolio strategy wasn't without risks. Customization meant higher engineering costs, longer lead times, and complex inventory management. Every project required detailed engineering, often involving multiple iterations with customers. The company had to maintain expertise across multiple technologies, requiring continuous training and development. But these challenges became competitive advantages—barriers that commoditized manufacturers couldn't easily overcome.

By 2020, TD Power Systems had built something remarkable: a product portfolio that spanned nearly every power generation application except nuclear, with deep engineering capabilities that allowed them to compete on value, not just price. They had become the preferred choice for applications requiring customization, local support, and engineering excellence—a position that would prove invaluable as the world entered an unprecedented period of power demand growth driven by digitalization and energy transition.

V. The Renewable Energy & Export Pivot (2015-2020)

The Paris Agreement was signed in December 2015, and while diplomats celebrated in champagne, engineers at TD Power Systems were recalibrating their entire strategic outlook. India had just committed to installing 175 GW of renewable energy by 2022, later raised to 500 GW by 2030. For a company that had built its reputation on conventional power generation, this could have been an existential threat. Instead, TDPS turned it into their greatest opportunity.

The renewable pivot wasn't a sudden revelation—it was a calculated transformation that had been brewing since 2013. Management recognized that renewable energy wasn't just about solar panels and wind turbine blades; it required an entire ecosystem of supporting infrastructure. Wind farms needed specialized generators. Solar plants required backup power systems. Hydro projects demanded custom solutions for varying head and flow conditions. And crucially, all of this renewable capacity would need grid stabilization equipment—an area where rotating machines still played a critical role.

The export strategy during this period was equally deliberate. While Indian manufacturers typically followed a predictable progression—dominate locally, then export to similar emerging markets—TDPS did something counterintuitive. They targeted developed markets with the most stringent quality requirements: Europe, Japan, and North America. The logic was simple but bold: if you can meet German engineering standards or Japanese quality requirements, every other market becomes accessible. The export numbers during this period tell the story. TDPS supplied wind turbine generators (WTGs) for windmill manufacturers, offering three solutions: permanent magnet generators (PMG), synchronous generators, and doubly-fed induction generators (DFIG). PMGs use strong magnets on the rotor to induce current, eliminating the need for external excitation; TDPS's entry into PMGs aligned with the industry trend for direct-drive wind turbines. The synchronous and DFIG options catered to geared turbines—DFIGs are widely used in modern wind turbines for their variable-speed, constant-frequency capability. By having multiple technologies, TDPS could serve different wind OEM preferences. These generators were designed for high torque at relatively low RPM and had to withstand environmental stresses (temperature, offshore or desert conditions).

The strategic brilliance wasn't just in the product development but in the timing. While competitors were still debating whether renewables were a fad or the future, TDPS had already positioned itself as a critical supplier to wind turbine OEMs. They understood that regardless of which company made the turbine blades or towers, everyone needed generators—and not generic ones, but customized solutions for specific wind conditions, grid codes, and operational requirements.

The export strategy crystallized around 2017 when management made a conscious decision to reduce dependence on the Indian market's cyclicality. They established sales offices in strategic locations—Japan for the Asian market, USA for North America, and Germany as the gateway to Europe. But these weren't just sales outposts; they were engineering centers where local teams could work directly with customers on specifications, ensuring TDPS's generators met local grid codes and environmental requirements.

Turkey emerged as an unexpected success story. Despite regulatory challenges and political uncertainty, TDPS built strong relationships with Turkish wind farm developers and turbine manufacturers. The key was their willingness to localize—not just in manufacturing but in understanding Turkish grid requirements, seismic conditions, and maintenance practices. When competitors treated Turkey as just another emerging market, TDPS treated it as a strategic priority.

The numbers from this period validate the strategy. Export revenues grew from roughly 30% of total sales in 2015 to over 50% by 2020. More importantly, export orders commanded better margins—international customers were willing to pay premiums for proven reliability and engineering support. The domestic market remained important for volume, but exports drove profitability.

TDPS committed to green energy solutions and environmental responsibility, with machines effectively harnessing wind, biomass, water, solar & waste to generate renewable energy. The company offered sustainable solutions for hydropower, with hydro turbine generators designed as per customer requirements, ensuring high reliability and performance. Their manufacturing facilities for wind turbine generators delivered high-quality products with high operational efficiency.

The renewable pivot also forced internal transformation. Engineers who had spent careers optimizing steam turbine generators had to learn about permanent magnet materials, power electronics, and grid integration challenges. The company invested heavily in simulation software, allowing them to model generator performance under varying wind conditions without expensive physical prototypes. They built specialized test facilities that could simulate the unique stresses of renewable applications—rapid speed variations, grid disturbances, and extreme weather conditions.

One fascinating development was the biomass generator business. While the world obsessed over solar and wind, TDPS quietly became a leader in generators for biomass power plants. Sugar mills in Brazil burning bagasse, rice mills in Southeast Asia using husks, municipal waste-to-energy plants in Europe—all needed specialized generators that could handle the unique characteristics of biomass combustion. Their turbo generators were designed to run on energy derived from municipal solid waste including bagasse, biogas, syngas, and biofuel.

The financial discipline during this expansion deserves recognition. While peers leveraged up to fund renewable ventures, TDPS maintained its debt-free status. Every expansion was funded through internal accruals, every new product development carefully staged to match cash generation. This wasn't financial conservatism—it was strategic patience, understanding that renewable energy markets could be volatile and maintaining flexibility was crucial.

Customer relationships evolved from transactional to strategic during this period. Major wind turbine OEMs didn't just buy generators; they co-developed solutions. TDPS engineers would be embedded in customer design teams, working on next-generation turbines years before commercial production. This deep integration created switching costs that went beyond economics—it was about shared knowledge, trust, and aligned innovation roadmaps.

The global footprint expansion wasn't just about sales. TDPS established a vast network of 57 service providers across 6 continents, helping address customer needs with high precision and agility. Service capability became a differentiator—the ability to dispatch technicians to a wind farm in Patagonia or a hydro plant in Indonesia within 48 hours. In the generator business, where downtime costs thousands of dollars per hour, service responsiveness could be more valuable than product features.

By 2020, TD Power Systems had successfully transformed from an India-centric conventional power equipment manufacturer to a global renewable energy enabler. The pandemic year, which devastated many industrial companies, actually validated TDPS's strategy. While fossil fuel projects stalled, renewable energy installations continued, driven by government commitments and improving economics. TDPS was perfectly positioned for what would come next—an unprecedented boom in power demand driven by the digital economy's insatiable appetite for electricity.

VI. The Data Center Boom & New Growth Vectors (2020-Present)

The ChatGPT moment arrived in November 2022, but for TD Power Systems, the AI revolution had been building since 2020. Every large language model training run, every cryptocurrency mining operation, every video streaming service expanding its content delivery network—all of it required massive amounts of reliable power. And behind that power, increasingly, were TDPS generators humming away in data centers from Virginia to Singapore.

The numbers are staggering: a single state-of-the-art AI training cluster can consume 100 MW of power—equivalent to a small city. Microsoft's recent deal for Three Mile Island's nuclear output, Google's investments in geothermal power, Amazon's renewable energy commitments—all point to the same reality: the digital economy's growth is fundamentally constrained by power availability. For TDPS, this represented not just an opportunity but a generational shift in demand dynamics. The Q4 FY25 numbers confirmed the acceleration: Order inflows jumped 42.7% to Rs 413.4 crore in Q4 FY25. Exports order inflows stood at Rs 258.7 crore, up 44.77% YoY, while domestic order inflows was at Rs 154.7 crore, up 39.24% YoY. But behind these aggregate numbers was a fundamental shift in customer composition. Data center operators, who barely registered five years ago, were now driving a significant portion of demand.

The unique requirements of data center power generation played perfectly to TDPS's strengths. Data centers need generators that can start within seconds, synchronize seamlessly with the grid, operate in parallel with multiple units, and run continuously during grid outages. More critically, they need customization—generators optimized for specific fuel types (diesel, natural gas, hydrogen), altitude conditions, and acoustic requirements (many data centers are near urban areas where noise regulations are strict).

TDPS's approach to the data center market was characteristically strategic. Rather than competing on price for commodity backup generators, they focused on mission-critical applications—hyperscale facilities where even seconds of downtime could cost millions. They developed specialized cooling systems for generators operating in the hot exhaust environment of data center mechanical yards. They engineered control systems that could manage load sharing across dozens of parallel generators. They even developed "island mode" capabilities, allowing data centers to operate completely independently from the grid during extended outages.

The geographic expansion during this period was deliberate and focused. Traction motor contracts from Germany, U.S., CIS to contribute in FY26 and scale sharply in FY27–28. The UK expansion was particularly strategic—not just a sales office but a full design center, announced in late 2023. The UK-based R&D hub will enable TDPS to enter large machine segments (40–100 MW) — potential to tap OEM partnerships and new verticals (nuclear, utility-scale).

The traction motor business, which seemed like a distraction when first announced, suddenly made perfect sense in the context of electrification. FY25 saw the first ₹50 Cr motor order and ₹316 Cr traction order book. Railways worldwide were electrifying, driven by decarbonization targets and improving battery technology. TDPS's electromagnetic design capabilities transferred naturally to traction motors, and their relationships with European engineering firms opened doors to lucrative railway contracts.

The operational expansion to support this growth was carefully orchestrated. Third manufacturing plant comes online in Q2 FY26, unlocking capacity to scale to ₹1,800–2,300 Cr revenue over the next 2–3 years. This wasn't just about adding floor space; it was about building capabilities for larger, more complex machines. The new facility included specialized equipment for manufacturing generators above 100 MW, automated winding machines for improved consistency, and advanced testing facilities that could simulate grid disturbances and transient conditions.

One fascinating development was the entry into geothermal power generation. Delay in Phase 2 geothermal deal (~1,000 MW U.S. project) — not closed in FY25; expected decision in FY26. Geothermal presented unique challenges—generators operating in corrosive environments, with variable steam quality and frequent thermal cycling. But it also offered massive opportunities as tech companies sought 24/7 clean power for their data centers. TDPS developed specialized materials and coatings for geothermal applications, positioning themselves as one of the few suppliers capable of meeting these demanding requirements.

The integration of AI and advanced analytics into product development marked a significant evolution. TDPS began using machine learning models to optimize generator designs, predicting performance under thousands of operating scenarios without physical prototypes. They developed predictive maintenance algorithms that could identify potential failures weeks in advance, a critical capability for data center operators who couldn't afford unexpected downtime.

Financial performance during this period validated the strategy. The company's consolidated net profit jumped 47.5% to Rs 174.58 crore in FY25. Revenue from operations increased 27.8% to Rs 1,278.76 crore in FY25. More importantly, margins expanded despite inflationary pressures—EBITDA margin improved by 430 bps to 20.7% in Q4 FY25—demonstrating pricing power and operational efficiency improvements.

The order book composition told the story of transformation. 67% of order inflows from export markets like U.S., Europe, Turkey, CIS. Gas turbine generators, particularly for combined-cycle plants supporting renewable grids, saw explosive growth. Orders from international gas engine OEMs worth ₹142 crore reflected the global shift toward distributed generation and grid stabilization.

Supply chain management became a critical capability during this period. The global semiconductor shortage, copper price volatility, and shipping disruptions could have derailed growth. But TDPS's strategy of maintaining strategic inventory—High inventory buildup (copper/steel) impacted FY25 operating cash flow, though strategic in nature—proved prescient. While competitors faced delivery delays, TDPS maintained on-time performance, strengthening customer relationships.

The strategic exit from certain markets also demonstrated discipline. Planned exit from Turkey post FY25 due to regulatory overreach; minor impact on P&L. Rather than fighting unwinnable regulatory battles, management chose to redeploy resources to more promising markets. This wasn't retreat; it was strategic focus.

Customer concentration risk, always a concern in B2B manufacturing, was actively managed. No single customer accounted for more than 15% of revenues. The customer base spanned industries—power generation, oil & gas, data centers, railways—and geographies, providing resilience against sector-specific downturns. Long-term framework agreements with major OEMs provided revenue visibility while maintaining flexibility to capture spot opportunities.

The investment in human capital during this period was substantial but often overlooked. TDPS hired AI specialists to work alongside traditional electrical engineers. They brought in supply chain experts from automotive companies to implement just-in-time manufacturing. They recruited service engineers globally, building local capabilities in key markets. The company's headcount grew, but more importantly, its capability set expanded dramatically.

Looking at the FY26 guidance of ₹1,500 crore—The company said that the initial top line guidance for FY26 is Rs 1,500 crore. The order inflow rate strongly suggests that upward revision in guidance is highly likely by end of next quarter—it seems conservative given the momentum. But this conservatism has been a TDPS hallmark—under-promise and over-deliver, building credibility through consistent execution rather than aggressive targets.

As we enter the back half of 2025, TD Power Systems stands at an inflection point. The convergence of AI-driven power demand, renewable energy expansion, and industrial reshoring creates unprecedented opportunities. The company that started as a technology licensee has become a critical enabler of the global energy transition, with the capabilities, relationships, and financial strength to capture this generational opportunity.

VII. Financial Performance & Unit Economics

The spreadsheet warriors at investment banks often miss what makes TD Power Systems' financials truly remarkable. It's not just the headline numbers—though a 47.5% jump in consolidated net profit to ₹174.58 crore in FY25, with revenue climbing 27.8% to ₹1,278 crore certainly catches attention. It's the underlying unit economics and capital efficiency that reveal a business model more akin to a specialized engineering firm than a traditional heavy manufacturer.

Start with the balance sheet, where the most important number might be what's not there: debt. In an industry where competitors routinely operate at 2-3x debt-to-equity ratios, TDPS has maintained a virtually debt-free status for over a decade. This isn't financial timidity—it's strategic flexibility. When copper prices spike or a large order requires working capital, TDPS doesn't need banker approval to act. When acquisition opportunities arise, they can move without leverage constraints.

The return metrics tell the real story. 28.5% ROCE, 22% ROE in FY25—numbers that would make software companies envious, achieved in capital-intensive manufacturing. How? The answer lies in the business model's hidden leverage: engineering intensity creates pricing power, customization drives customer stickiness, and service revenues provide high-margin recurring income.

Working capital management in a custom manufacturing business is notoriously difficult, yet TDPS has developed a sophisticated approach. Receivables rose to ₹437 Cr; ~20% above 90 days due to March-end invoicing and back-loaded collection cycle. While this might alarm some analysts, it reflects the reality of dealing with utility customers and large OEMs who pay slowly but surely. The company has never faced a significant bad debt write-off—a testament to customer quality and credit management.

The margin trajectory deserves special attention. EBITDA margin improved by 430 bps to 20.7% in Q4 FY25, reaching levels typically associated with specialized industrial software or precision instruments, not heavy electrical equipment. This margin expansion wasn't driven by price increases alone—it came from mix improvement (more exports, larger generators), operational efficiency (automation, lean manufacturing), and service revenue growth.

Consider the unit economics of a typical generator sale. A 50 MW steam turbine generator might sell for ₹15-20 crore, with material costs (copper, steel, insulation) accounting for 60-65%, direct labor 5-7%, and engineering/design 8-10%. That leaves 18-27% for overhead and profit—but the real value creation happens post-sale. Installation supervision, commissioning, annual maintenance contracts, and eventual refurbishment can generate another 30-40% of the initial sale price over the generator's 20-30 year life.

The capital allocation framework reflects a deep understanding of business economics. Annual capex runs at 8-10% of revenues—enough to support growth without diluting returns. Capital discipline and ~₹200 Cr cash buffer for self-funded expansion means growth is internally funded, avoiding the dilution treadmill that traps many industrial companies.

Inventory management presents unique challenges in custom manufacturing. High inventory buildup (copper/steel) impacted FY25 operating cash flow, though strategic in nature. TDPS maintains strategic stocks of key materials—electrical steel, copper wire, specialized insulation—to hedge against price volatility and ensure delivery commitments. This inventory isn't working capital trapped in inefficiency; it's a strategic asset that enables rapid response to customer requirements.

The shift in revenue mix tells a profitability story. Export revenues, now representing over 60% of total sales, command 300-500 basis points higher margins than domestic sales. Why? International customers value reliability and service support more than initial price. They're willing to pay premiums for proven track records, comprehensive documentation, and global service networks. A generator failure in a Norwegian wind farm or Texas data center costs far more than the price differential between suppliers.

Fixed cost absorption has improved dramatically with scale. The same engineering team that could design 10 generators annually five years ago now handles 30-40 projects, thanks to design automation, modular architectures, and accumulated expertise. Testing facilities that sat idle between projects now run continuously, serving both production and third-party certification needs. The Dabaspet factory that once struggled to achieve single-shift utilization now runs two full shifts with selective weekend operations.

The cash conversion cycle reveals operational excellence. Despite the working capital intensity of custom manufacturing, TDPS maintains a cash conversion cycle of 120-140 days—remarkable for an industry where 180-200 days is common. This efficiency comes from milestone-based billing (advance, dispatch, installation, commissioning), aggressive collection follow-up, and strategic vendor partnerships that allow favorable payment terms.

Service revenue economics deserve special mention. While contributing only 10-12% of total revenues, service activities generate 25-30% margins and require minimal capital investment. A field service engineer visiting a wind farm for annual maintenance might generate ₹5-10 lakhs in billing with direct costs of ₹2-3 lakhs. More importantly, service relationships create switching costs—customers become dependent on TDPS's expertise for maintenance, modifications, and troubleshooting.

The R&D spending pattern reflects strategic priorities. At 2-3% of revenues, it might seem modest compared to technology companies. But this spending is highly targeted—electromagnetic design software, materials research, testing capabilities. Every rupee of R&D spending is directed toward customer-specific solutions rather than blue-sky research. The payoff comes in the ability to win high-margin custom projects that commodity manufacturers can't execute.

Geographic profitability varies significantly. European orders, with their stringent quality requirements and comprehensive documentation needs, actually generate highest margins due to pricing premiums. Middle Eastern projects, despite payment delays, offer good profitability due to lower competitive intensity. Domestic orders, while lower margin, provide volume for fixed cost absorption and local market credibility.

The capital structure evolution reflects growing confidence. The dividend payout has increased progressively—Board recommended a final dividend of Rs 0.65 per equity share—while maintaining sufficient retained earnings for growth. The company has resisted the temptation to leverage up for acquisitions or aggressive expansion, understanding that financial flexibility is more valuable than short-term EPS accretion.

Looking at peer comparison, TDPS trades at premium valuations—The market is valuing TDPS as a quality compounder with sustained margin leadership and capital efficiency — pricing in near-term earnings growth and execution stability. But the premium seems justified given superior returns, debt-free status, and exposure to structural growth themes.

The FY26 outlook provides a window into future economics. Initial top line guidance for FY26 is Rs 1,500 crore. The order inflow rate strongly suggests that upward revision in guidance is highly likely. With the third plant coming online and 18%+ EBITDA margin profile, with long-term stability, the company is positioned for operating leverage expansion.

The unit economics story ultimately comes down to this: TDPS has transformed commodity manufacturing into specialized engineering, where customer relationships, technical expertise, and service capabilities matter more than production capacity. It's a business model that generates software-like returns from hardware manufacturing—a rare achievement in Indian industry.

VIII. Management & Corporate Governance

Nikhil Kumar doesn't fit the typical mold of an Indian manufacturing CEO. When you meet him, the first thing you notice isn't the Harvard executive education credentials or the 20+ years at TDPS—it's the obsessive attention to technical detail combined with strategic thinking usually found in Silicon Valley boardrooms. The company's board approved the re-appointment of Nikhil Kumar as managing director for a further term of five years commencing January 17, 2026 to January 16, 2031, a vote of confidence that speaks volumes about his leadership through multiple business cycles.

Kumar's journey with TDPS began as a founding member in 1999, but his real imprint on the company started when he became Managing Director in 2012. Unlike professional CEOs parachuted in to run established businesses, Kumar grew up with the company, understanding its technical DNA while developing the strategic vision to take it global. His approach—humble about achievements, paranoid about competition, obsessive about quality—reflects both the Japanese influence from the early Toyo Denki days and his own engineering-first philosophy.

The board composition tells a story of evolution from promoter-driven to professionally governed. Promoter holding has decreased over last quarter: -6.34%, Promoter Holding: 26.9%. This reduction isn't distress selling—it's strategic dilution to bring in institutional investors and improve liquidity. The promoter group understands that professional governance and broad shareholding are prerequisites for the next phase of growth.

What sets TDPS's governance apart is the balance between entrepreneurial agility and institutional discipline. Board meetings don't just rubber-stamp management decisions; they involve genuine debate about technology choices, market entry strategies, and capital allocation. Independent directors include former customers who understand the industry, technologists who can evaluate R&D investments, and financial experts who ensure capital discipline.

The organizational culture is a unique blend of Indian jugaad (innovative problem-solving), Japanese kaizen (continuous improvement), and German engineering precision. Walk through the Dabaspet factory, and you'll see quality circles discussing microscopic improvements in winding techniques, while engineers debate electromagnetic field optimization with the passion of sports fans. This isn't manufactured corporate culture—it's genuine technical obsession.

Kumar's leadership style emphasizes empowerment with accountability. Department heads have significant autonomy in operational decisions but face rigorous monthly reviews where every variance is dissected. The company maintains a startup-like atmosphere despite its size—engineers can walk into Kumar's office with ideas, and promising concepts get resources quickly. But there's also ruthless prioritization; projects that don't show results get killed fast.

The approach to talent management reflects long-term thinking. TDPS doesn't just hire; it builds careers. Engineers join fresh from college and spend years rotating through design, manufacturing, testing, and field service. By the time they reach senior positions, they understand every aspect of the business. This internal development creates deep institutional knowledge—critical in a business where customer relationships and technical expertise span decades.

Compensation philosophy balances market competitiveness with internal equity. While TDPS can't match IT industry salaries, it offers something more valuable to a certain type of engineer: the opportunity to work on complex, physical products that power the world. Stock options, though modest compared to startups, create long-term alignment. The real retention tool is the work itself—solving problems that matter.

The company's approach to stakeholder management is refreshingly transparent. Quarterly earnings calls don't just present numbers; management discusses technical challenges, explains strategic choices, and admits mistakes. When the Turkey exit was announced—Planned exit from Turkey post FY25 due to regulatory overreach—management clearly explained the rationale rather than burying it in footnotes.

Risk management isn't delegated to a compliance function; it's embedded in operational DNA. Every major order undergoes technical risk assessment—can we deliver on specifications, what are the penalty clauses, how does this affect other commitments? Financial risks are managed conservatively—foreign exchange hedging, credit insurance, advance payments. But the company also takes calculated strategic risks, like entering new product categories or challenging incumbents in developed markets.

The approach to M&A reflects discipline over empire-building. Despite numerous opportunities and banker pitches, TDPS has avoided the acquisition trap that ensnares many successful mid-sized companies. Kumar's philosophy is clear: organic growth we can control; acquisitions introduce variables we can't. The focus remains on building capabilities internally rather than buying problems externally.

Corporate social responsibility isn't just compliance checkbox-ticking. The company runs serious skill development programs, training local youth in electrical and mechanical trades. Many graduates join TDPS; others find employment elsewhere, creating a skilled ecosystem around Bangalore's manufacturing corridor. Environmental initiatives focus on practical improvements—reducing copper waste, recycling insulation materials, optimizing energy consumption—rather than glamorous but ineffective programs.

The governance framework handles related-party transactions with textbook discipline. All such transactions undergo independent director review, are benchmarked against market rates, and disclosed transparently. The promoter family has gradually professionalized their involvement—from operational management to strategic oversight—a transition many Indian companies struggle with.

Succession planning, often a weakness in founder-led companies, appears robust. Kumar's re-appointment for five years provides continuity, but the next generation of leaders is clearly visible. The heads of engineering, manufacturing, and international business have grown with the company and understand its culture. The transition, when it comes, should be smooth rather than disruptive.

The board's approach to capital allocation deserves special mention. Despite the temptation to chase growth through aggressive expansion or acquisitions, they've maintained discipline. Capital discipline and ~₹200 Cr cash buffer for self-funded expansion reflects a philosophy of sustainable growth over headline-grabbing announcements.

Information security and intellectual property protection, critical in a technology-intensive business, receive board-level attention. The company has implemented sophisticated systems to protect design data, customer information, and proprietary processes. But the real protection comes from embedded knowledge—the accumulated expertise in thousands of engineers' heads that can't be easily replicated.

The handling of the COVID-19 crisis revealed management character. While many companies used the pandemic as an excuse for poor performance, TDPS maintained operations, protected jobs, and supported suppliers through the crisis. The company provided salary advances, medical support, and even oxygen concentrators for employees' families. This wasn't just corporate altruism—it was recognition that human capital is the real asset.

Looking at institutional ownership patterns, the evolution is striking. From virtually no institutional holding a decade ago, marquee domestic mutual funds and emerging market specialists now hold significant stakes. This isn't just passive index inclusion; these are active managers who've done deep diligence and bet on management execution.

The communication strategy balances transparency with competitive discretion. While financial performance is disclosed comprehensively, technical details and customer specifics are carefully protected. Management understands that in a B2B business, information asymmetry is a competitive advantage.

As TDPS enters its next phase—targeting ₹2,000+ crore revenues, expanding globally, entering new product categories—governance will be tested. Can the company maintain its entrepreneurial edge while implementing institutional processes? Can it preserve its engineering culture while scaling operations? Can Kumar and his team navigate the transition from successful mid-size company to industrial champion? The five-year reappointment suggests the board believes they can.

IX. Playbook: Business & Investing Lessons

TD Power Systems' journey from technology licensee to global competitor offers a masterclass in emerging market industrial strategy. The playbook isn't about disruption or blitzscaling—it's about patient capability building, strategic positioning, and exploiting structural advantages that emerge from being in the right place at the right time with the right capabilities.

Lesson 1: Technology Transfer as a Springboard, Not a Crutch

Most companies that start with foreign technology transfer remain perpetual licensees, paying royalties while never developing independent capabilities. TDPS flipped this model. They used the Toyo Denki partnership to learn fundamental principles, then built upon that foundation with indigenous innovation. The key was viewing technology transfer not as outsourced R&D but as accelerated learning. Within a decade, they were designing generators that their original partners couldn't produce.

Lesson 2: The Power of Niches Within Large Markets

The global generator market is worth hundreds of billions, but TDPS didn't try to compete everywhere. They identified specific niches—small steam turbine generators, customized wind turbine solutions, tropical climate adaptations—where global giants couldn't economically compete and local players lacked technical capability. By dominating these niches (like their 80% market share in small steam turbine generators), they built a fortress before expanding into adjacent areas.

Lesson 3: Custom Manufacturing as a Moat

In an era obsessed with standardization and platform economics, TDPS went the opposite direction. Every generator is essentially a custom product, engineered for specific requirements. This creates multiple moats: engineering expertise that takes years to develop, customer relationships that deepen with each project, and switching costs that make customers reluctant to change suppliers. The inability to achieve traditional economies of scale becomes an advantage—it keeps commodity manufacturers out.

Lesson 4: Building Global from India—Beyond Labor Arbitrage

The conventional wisdom for Indian companies going global was leverage cheap labor for cost advantage. TDPS competed on engineering capability, customization flexibility, and service responsiveness. 67% of order inflows from export markets didn't come from being cheapest but from solving problems others couldn't or wouldn't. They understood that competing with Siemens on price was futile; competing on willingness to customize for a Norwegian wind farm's specific needs was winnable.

Lesson 5: Capital Allocation Without Debt—The Compound Effect

The decision to remain debt-free seemed overcautious when interest rates were low and peers were leveraging up. But it provided strategic flexibility that compounded over time. No debt meant no covenants restricting strategic choices. It meant surviving downturns without distressed asset sales. It meant negotiating from strength with customers and suppliers. 28.5% ROCE wasn't achieved despite being debt-free; it was achieved because of it.

Lesson 6: Riding Multiple Secular Trends Simultaneously

TDPS positioned itself at the intersection of multiple mega-trends: renewable energy transition, data center explosion, industrial reshoring, and infrastructure modernization. This wasn't luck—it was deliberate portfolio construction. When wind power slowed, data centers accelerated. When domestic orders weakened, exports surged. This diversification across correlated but non-identical trends provided resilience and growth optionality.

Lesson 7: Technical Partnerships Without Dependence

The relationships with Siemens, Toshiba-Mitsubishi, and others could have created dependence. Instead, TDPS structured them as capability-building exercises. Each partnership brought specific technology or market access, but TDPS maintained independent R&D, developed proprietary designs, and built direct customer relationships. Partners became force multipliers, not crutches.

Lesson 8: The Service Revenue Stream Hidden in Hardware

Manufacturing companies often view service as a necessary evil—costly support required to sell products. TDPS understood that service was a high-margin, recurring revenue stream that created customer lock-in. A generator sold once generates service revenue for decades. The installed base becomes an annuity that funds growth while providing market intelligence about customer needs and competitor activities.

Lesson 9: Why Being Boring Can Be Beautiful

In an investment world obsessed with disruption, TDPS represents something different—steady execution in an essential industry. Generators aren't sexy, but every kilowatt of global electricity passes through one. This "boring" business generated 47.5% profit growth because demand is structural, not cyclical. The lesson: sometimes the best investments are in companies making products that will definitely be needed in 20 years.

Lesson 10: Culture as Sustainable Competitive Advantage

The hybrid culture—Indian entrepreneurialism, Japanese quality obsession, German engineering precision—wasn't designed; it evolved. But once established, it became nearly impossible to replicate. Competitors could copy products, match prices, even poach employees. But they couldn't replicate two decades of accumulated culture that makes engineers voluntarily work weekends to solve customer problems.

Lesson 11: The Platform Dynamics in Traditional Manufacturing

While TDPS isn't a platform business in the tech sense, it exhibits platform characteristics. Each new customer relationship makes the company more valuable to other customers (shared learning, improved designs). Each new product category leverages existing capabilities while adding new ones. The business becomes more valuable as it scales—classic network effects in an unexpected industry.

Lesson 12: Timing Market Entry—Fast Follower Advantage

TDPS rarely pioneered new technologies but excelled at rapid commercialization once technologies proved viable. They entered wind turbine generators after the technology stabilized. They moved into data center applications after demand patterns clarified. This fast-follower strategy avoided pioneer risks while capturing growth opportunities.

For Investors: Pattern Recognition

The TDPS pattern—technology transfer leading to indigenous capability, niche domination before expansion, export success validating quality—appears repeatedly in emerging market success stories. Identifying companies in the early stages of this pattern, before market recognition, offers asymmetric returns.

For Operators: Sustainable Growth Architecture

The TDPS model shows how to build sustainable competitive advantages in traditional industries: focus on customer problems not products, build capabilities not just capacity, maintain financial flexibility over aggressive growth, and create cultures that compound knowledge over time.

The Meta-Lesson: Convergence Creates Opportunity

The biggest opportunities emerge at convergence points—where multiple trends intersect, creating demand that didn't previously exist. Data centers needing renewable power, wind farms requiring grid stabilization, distributed generation supporting electric vehicle charging—these convergences create new markets for those positioned to capture them.

X. Analysis & Bear vs. Bull Case

The investment case for TD Power Systems sits at a fascinating juncture where compelling structural growth drivers meet legitimate execution concerns. Let's dissect both sides with the rigor this story deserves.

The Bull Case: Structural Tailwinds Meeting Execution Excellence

The bulls start with an almost irrefutable premise: electricity demand is entering a super-cycle not seen since the original electrification era. AI data centers alone could add 500-1000 TWh of global electricity demand by 2030—equivalent to adding another Japan to the global grid. Every watt of this power needs generation equipment, and TDPS sits squarely in the sweet spot of 10-200 MW generators where demand is exploding.

The export momentum validates the quality argument. Exports order inflows stood at Rs 258.7 crore, up 44.77% YoY in an environment where customers can choose any global supplier. European and American customers aren't choosing TDPS for price—they're choosing them for engineering capability and customization flexibility that established players won't provide.

India's 500 GW renewable target by 2030 isn't just political rhetoric—it's backed by policy, capital, and necessity. Even achieving 70% of this target would require thousands of generators for wind, hydro, and biomass applications. TDPS's dominant position in small steam turbine generators and growing presence in wind applications positions them as a direct beneficiary.

The balance sheet provides unusual resilience for a capital-intensive manufacturer. Zero debt in an industry where 2-3x leverage is normal means TDPS can weather downturns, fund growth internally, and act opportunistically when competitors face distress. Capital discipline and ~₹200 Cr cash buffer provides firepower for expansion without dilution.

Margin expansion potential remains underappreciated. 18%+ EBITDA margin profile could expand further as: service revenues grow from the expanding installed base, product mix shifts toward higher-value exports and large generators, and the new UK R&D center enables entry into 100+ MW segments. Operating leverage from the third plant could add 200-300 basis points to margins.

The management track record speaks for itself. Five consecutive years of 20%+ growth, consistent margin improvement, successful technology partnerships, and disciplined capital allocation. Re-appointment of Nikhil Kumar as MD for five years provides continuity and confidence.

Valuation, while not cheap, seems reasonable for the quality and growth. At current levels, the market values TDPS at a premium to traditional industrials but a discount to specialized engineering companies—arguably the right comparable set given their business model evolution.

The Bear Case: Execution Risks in a Cyclical Industry

Bears point to uncomfortable realities hidden in the growth narrative. Domestic order inflow weak at just 4% YoY growth suggests the India story might be overhyped. If the domestic market, contributing 40% of revenues, remains weak while competition intensifies, margin pressure could emerge quickly.

The working capital deterioration deserves scrutiny. Receivables rose to ₹437 Cr; ~20% above 90 days and elevated inventory and receivables due to steel/copper stocking could signal either aggressive revenue recognition or deteriorating customer quality. If cash conversion doesn't normalize, ROCE could decline despite profit growth.

Geographic concentration risks are materializing. Planned exit from Turkey post FY25 due to regulatory overreach shows that international expansion isn't without risks. If regulatory challenges emerge in other markets or protectionist policies favor local suppliers, the export growth story could unravel.

Chinese competition looms large. While TDPS has successfully competed against Western giants, Chinese manufacturers are different—willing to accept lower margins, backed by state support, and increasingly capable technically. If Chinese players seriously target TDPS's niches, pricing pressure could be severe.

Technology disruption risks are real. Battery storage improving faster than expected could reduce need for backup generators. Direct renewable-to-hydrogen production could bypass traditional generation. Solid-state transformers could change power distribution architecture. While these are longer-term risks, they could impact valuation multiples sooner.

The new business ventures carry execution risk. Motors and traction have lower margins initially. If they scale faster than high-margin generator exports, blended EBITDA margin may compress below 18%. Entering new product categories while maintaining quality and delivery in core businesses is notoriously difficult.

Customer concentration, while managed, exists. Loss of a major OEM relationship or a large project cancellation could impact near-term results significantly. The custom manufacturing model means each order is essentially a project risk.

The Balanced View: Probabilistic Outcomes

Base Case (60% probability): TDPS executes on its ₹1,500 crore FY26 guidance, margins stabilize around 18-20%, and growth continues at 20-25% annually. The stock delivers 15-20% annual returns, in line with earnings growth.

Bull Case (25% probability): Geothermal Phase 2 (U.S.), data center projects, and European grid orders accelerate beyond expectations. AI power demand creates generator shortage. Margins expand to 22-24%, growth accelerates to 30%+, and the stock re-rates to specialized engineering multiples, delivering 30-40% annual returns.

Bear Case (15% probability): China competition intensifies, domestic market remains weak, and working capital issues persist. Growth slows to 10-15%, margins compress to 15-16%, and the stock de-rates to traditional industrial multiples, resulting in 20-30% downside.

Key Monitorables for Investors

The smart money should watch several key indicators beyond headline numbers:

-

Order Book Quality: Not just growth but composition—geography mix, customer concentration, and margin profile of new orders.

-

Cash Conversion: If cash conversion doesn't normalize by Q2 FY26, ROCE may soften. Watch days sales outstanding and inventory turns closely.

-

Export Market Dynamics: Regulatory changes, local content requirements, and competitive intensity in key export markets.

-

Technology Partnerships: New collaborations or extensions of existing ones signal capability expansion and market access.

-

Capacity Utilization: The third plant's ramp-up pace will determine whether growth targets are achievable.

-

Service Revenue Growth: Expansion of high-margin service revenues indicates installed base monetization and customer stickiness.

The Verdict: Quality at a Premium, But Justified

TD Power Systems represents a rare combination in Indian markets—a manufacturing company with software-like economics, global competitiveness, and exposure to structural growth themes. The bears raise valid concerns, but the bulls have momentum, execution track record, and secular tailwinds on their side.

For long-term investors willing to stomach near-term volatility, TDPS offers exposure to the electrification megatrend through a proven operator with conservative financial management. The premium valuation reflects quality and growth potential, but isn't egregious given the business characteristics.

The key insight: this isn't just a cyclical industrial play riding temporary demand strength. It's a structural beneficiary of the global energy transition with the capabilities, culture, and capital structure to compound value over decades. In a market obsessed with the next quarter, that's exactly the kind of business that creates wealth over time.

XI. Epilogue & "What Would We Do?"

Standing at the threshold of what could be the most significant energy infrastructure build-out in human history, TD Power Systems faces a defining question: Can a company that built its success on patient capability building and conservative financial management capture the explosive opportunities ahead without losing its soul?

The path to becoming a $10 billion company—roughly 5x from current revenues—isn't fantastical. If global electricity demand grows 3-4% annually (conservative given AI and electrification trends) and TDPS maintains its market share while expanding into adjacent segments, the math works. But the real question isn't whether the opportunity exists—it's whether TDPS can execute at scale while maintaining the quality, culture, and capital discipline that got them here.

If we were running TDPS, the strategic priorities would be clear but challenging:

Geographic Expansion—Beyond Sales Offices

The UK R&D center is a start, but true globalization requires more. We'd establish manufacturing capabilities in key markets—not to chase labor costs but to be closer to customers, navigate local content requirements, and de-risk supply chains. A generator assembly facility in the US serving data center customers, a service center in the Middle East for the massive renewable build-out, perhaps even a partnership in Africa where power infrastructure needs are greatest. Each expansion would be self-funded, milestone-based, and reversible if conditions change.

The M&A Question—Strategic Additions, Not Empire Building

Despite the historical aversion to acquisitions, selective M&A could accelerate capability building. We wouldn't buy another generator manufacturer—that's just buying market share. Instead, we'd look for specialized capabilities: a power electronics firm to strengthen grid integration capabilities, a materials science company working on next-generation insulation, or a digital twin software company for predictive maintenance. Small, technology-focused acquisitions that plug capability gaps and can be integrated without cultural disruption.

The Energy Storage Integration

Batteries aren't replacing generators; they're complementing them. The hybrid power systems of the future will seamlessly integrate generation, storage, and grid management. TDPS should develop capabilities in generator-battery integration, providing complete power solutions rather than standalone generators. Partner with battery manufacturers, develop control systems, and become the system integrator for hybrid power installations.

Digital Transformation—But the Right Kind

Not digital for digital's sake, but targeted applications that enhance core capabilities. AI-powered design optimization to reduce engineering time from weeks to days. Digital twins of every generator sold, enabling predictive maintenance and performance optimization. Blockchain-based service records ensuring authenticity and maintaining asset value. The goal: become the most technically sophisticated generator company, not the most digitally visible.

The Human Capital Investment

The constraint on growth isn't capital or market demand—it's human capability. We'd 10x the investment in training, creating a TDPS University that becomes the global center of excellence for generator technology. Partner with IITs and international universities for research programs. Create an alumni network that becomes a competitive advantage—former TDPS engineers in customer organizations becoming advocates for the company.

The Service Revolution

The installed base of thousands of generators is an undermonetized asset. We'd create TDPS Service Corporation, a separate entity with its own P&L and growth targets. Offer performance guarantees, efficiency optimization programs, and lifecycle extension services. Use IoT sensors and predictive analytics to shift from reactive to proactive maintenance. The goal: service revenues should equal product revenues within a decade.

The Sustainability Imperative

As ESG considerations become paramount, TDPS should lead in sustainable manufacturing. Develop circular economy practices—refurbishing old generators, recycling rare earth materials, designing for disassembly. Create the industry's first carbon-neutral generator, even if initially at a loss. The marketing value and customer preference shift would more than compensate.

Capital Structure Evolution

The debt-free status has been a strength, but strategic use of leverage could accelerate growth without significantly increasing risk. We'd consider sustainable bonds for green energy projects, export credit facilities for international expansion, and perhaps strategic equity raises for transformational investments. The key: maintain financial flexibility while optimizing capital costs.

The Platform Play

TDPS has linear economics—more sales require more resources. We'd explore platform opportunities: a marketplace for used generators, a financing platform for small renewable projects, or a training platform for generator technicians globally. These capital-light, high-margin businesses could leverage TDPS's reputation while creating new revenue streams.

The Next Decade: Three Scenarios

Scenario 1: The Conservative Path Continue current strategy, grow organically at 20-25%, maintain margins, and become a solid ₹5,000 crore company by 2035. Safe, predictable, but potentially missing the generational opportunity.

Scenario 2: The Aggressive Expansion Lever up, acquire aggressively, expand globally, and shoot for ₹20,000 crore by 2035. Higher risk, potential for spectacular success or failure.

Scenario 3: The Balanced Transformation Our preferred path—selective expansion, strategic partnerships, service revolution, and platform elements. Target ₹10,000-12,000 crore by 2035 while maintaining cultural and financial strengths.

Final Reflections

TD Power Systems represents something increasingly rare in modern business—a company that creates genuine value through engineering excellence, customer focus, and patient execution. In a world of unicorns and blitzscaling, TDPS is the tortoise that might actually win the race.

The company stands at an inflection point where decades of capability building meets unprecedented market opportunity. The choices made in the next 2-3 years will determine whether TDPS becomes a footnote in Indian industrial history or a global champion that powers the sustainable energy future.

For investors, the question isn't whether TDPS is a good company—it clearly is. The question is whether current valuations adequately reflect the optionality embedded in the business. A company with proven execution, conservative balance sheet, and exposure to multiple structural growth drivers rarely comes at a discount.

For the broader Indian economy, TDPS represents what's possible when patient capital meets engineering excellence and strategic thinking. If India is to become a developed economy, it needs hundreds of companies like TDPS—globally competitive, technically sophisticated, and financially disciplined.

The generators humming in data centers, wind farms, and power plants around the world are testament to a simple truth: in the race to electrify everything, someone needs to make the machines that make the electricity. TD Power Systems has spent 25 years preparing for this moment. The next decade will reveal whether they can seize it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube