Varun Beverages: From Jaipur Bottler to PepsiCo's Global Champion

I. Introduction & Episode Roadmap

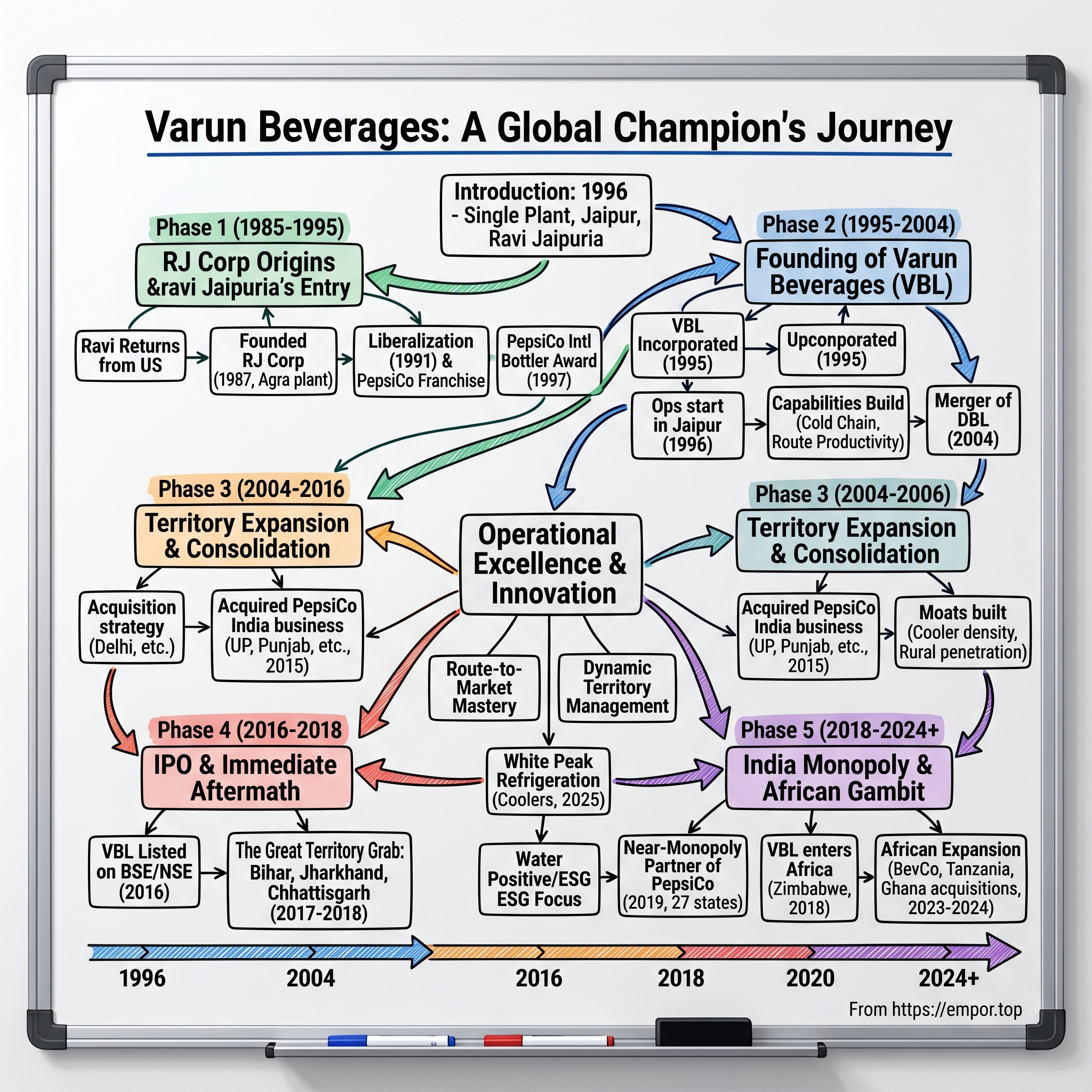

Picture this: A single bottling plant in Jaipur, 1996. The machines hum as they fill glass bottles with dark, fizzy liquid—Pepsi-Cola, the American challenger in India's newly liberalized economy. The man overseeing operations isn't thinking about becoming a beverage empire. Ravi Jaipuria is simply trying to make his piece of the family bottling business work. Fast forward to 2024: that same business, now called Varun Beverages Limited, controls PepsiCo's bottling across 27 of India's 29 states and is rapidly conquering Africa. Market capitalization? ₹1,60,914 crore. Annual revenue? ₹21,078 crore.

How does a regional bottler become one of the largest franchise partners of a Fortune 500 company globally? How do you build a business that PepsiCo itself couldn't—or wouldn't—build? And perhaps most intriguingly, how do you create such value while essentially selling someone else's product?

This is the story of territory consolidation as competitive advantage, of operational excellence at massive scale, and of a uniquely Indian approach to building a global beverage business. It's about understanding that in the consumer goods world, the company that controls the last mile often controls the profit pool. It's about Ravi Jaipuria's three-decade journey from inheriting a slice of the family bottling concern to building one of India's most valuable consumer companies.

We'll trace VBL's evolution through five distinct phases: the scrappy early days as RJ Corp fighting in India's cola wars; the methodical territory expansion across North India; the transformative 2017-2018 period when VBL essentially monopolized PepsiCo's India operations; the bold African gambit that's defining its next decade; and the operational innovations that make it all work. Along the way, we'll unpack the strategic decisions, the market dynamics, and the execution capabilities that transformed a commodity bottling operation into a compounding machine.

The themes that emerge aren't just about beverages. They're about the power of focus in an age of diversification, about building moats through operational excellence rather than technology, and about the surprising value creation possible in "boring" businesses. Because while tech unicorns grab headlines, Varun Beverages has quietly built something arguably more impressive: a business that turns sugar, water, and carbon dioxide into one of India's great wealth creation stories.

II. The RJ Corp Origins & Ravi Jaipuria's Entry (1985–1995)

The monsoon of 1985 brought more than rain to Delhi. It brought Ravi Jaipuria home from America, armed with a business degree and the peculiar confidence that comes from studying abroad while your family's fortunes are shifting back home. He studied business management in the United States and returned to India in 1985, joining the family business as a bottler for Pepsi-Cola. But the India he returned to wasn't the one he'd left. The License Raj was creaking under its own weight, and whispers of liberalization were beginning to circulate in Delhi's business circles.

The Jaipuria family had deep roots in North India's business ecosystem. His father, Chunilal Jaipuria, was a prominent figure in the textile industry, co-founding one of India's largest woolen mills. But textiles were yesterday's game. The future, as young Ravi saw it, lay in satisfying India's emerging consumer class—a demographic that didn't quite exist yet but would soon explode into being.

The pivotal moment came in 1987. He founded RJ Corp after receiving part of the family's bottling business from his father. In 1987 Chunni Lal divided the business among his three sons. Ravi got one bottling plant in Agra as his share. One plant in Agra—hardly the foundation of an empire. But Jaipuria saw what others didn't: India was about to open up, and when it did, the country would be thirsty.

The real transformation came in 1991, the year India embraced economic liberalization and PepsiCo entered the Indian market. Jaipuria became a franchisee of PepsiCo in 1991. Two years after PepsiCo entered India, he switched allegiances and has stayed with Pepsi since. This wasn't just changing suppliers; it was betting on globalization itself. While Coca-Cola had been kicked out of India in 1977 and wouldn't return until 1993, Pepsi had cleverly entered through a joint venture, positioning itself as the cola of new India.

RJ Corp was founded in 1992 by Ravi Jaipuria. By 1993, the company had formalized its relationship with PepsiCo, becoming what would eventually grow into the largest distributor of Pepsi products in India. The timing was exquisite—India's GDP was beginning its historic climb, and with it, discretionary spending on beverages.

What distinguished Jaipuria from other bottlers wasn't just ambition—it was execution. Mr. Ravi Jaipuria has an established reputation as an entrepreneur and business leader and is the only Indian to receive PepsiCo's International Bottler of the Year award, which was awarded in 1997. Think about that: within six years of partnering with PepsiCo, an Indian bottler with a single plant had become their global standard-bearer. He was awarded the Bottler of the Year by PepsiCo in 1999, receiving the award from former US President George H. W. Bush.

The late 1990s were a masterclass in aggressive expansion. While competitors focused on metros, Jaipuria was building distribution networks in Tier 2 and Tier 3 cities. His philosophy was simple but profound: carbonated soft drinks aren't a luxury product in India; they're an aspiration product. Price them right, distribute them everywhere, and you transform sugar water into social mobility.

In the same year, he joined the family bottling business, which primarily involved bottling for Pepsi-Cola, after losing close family members in the Kanishka air crash. Personal tragedy had accelerated his entry into the business, but it also seemed to sharpen his focus. While his brothers—who also received parts of the bottling business—remained regional players, Ravi was thinking nationally, then internationally.

The competitive landscape of the early 1990s was brutal. Parle's Thums Up dominated with over 60% market share, local brands like Campa Cola had loyal followings, and here was Pepsi—foreign, expensive, and new. But Jaipuria understood something crucial: he wasn't really selling cola. He was selling modernity. Every Pepsi bottle that left his Agra plant was a tiny ambassador for globalized India.

By 1995, RJ Corp had proven the model worked. Revenue was climbing, PepsiCo was impressed, and Jaipuria was ready for his next move. That move would be Varun Beverages—incorporated in 1995 as a subsidiary of RJ Corp, and named after founder Ravi Jaipuria's son. But that's getting ahead of our story. What matters here is understanding the foundation: a family business transformed into a professional operation, a local bottler thinking globally, and perfect timing meeting relentless execution.

The irony wasn't lost on industry observers. While multinational corporations spent millions on market research trying to crack the Indian consumer code, a Marwari businessman from Delhi had figured it out with one plant in Agra: give Indians quality at the right price, be everywhere they shop, and never, ever compromise on distribution. It sounds simple. It was anything but.

III. Founding of Varun Beverages & Early Operations (1995–2004)

The summer of 1995 brought a new kind of heat to Indian boardrooms. Liberalization was in full swing, consumer spending was accelerating, and Ravi Jaipuria was ready to institutionalize what had been a family operation. The company was incorporated in 1995 as a subsidiary of RJ Corp, and named after founder Ravi Jaipuria's son. Varun Beverages Limited wasn't just another corporate entity—it was a statement of intent. Naming it after his son signaled this was being built for generations.

In 1996, VBL kickstarted its operations in Jaipur. Following its growth journey, it planted its seeds of ambition in Alwar, Jodhpur, and Kosi in 1999. The choice of Jaipur as the first plant location was strategic brilliance disguised as geographic convenience. Rajasthan's tourism boom meant hotels, restaurants, and retail outlets proliferating—perfect training grounds for a bottling operation learning to scale.

But the real story of this period wasn't the plants or the territories. It was the systematic building of capabilities that would later enable exponential growth. While competitors focused on maximizing margins from existing territories, Jaipuria was investing in three critical areas that seemed excessive at the time: cold chain infrastructure, rural distribution networks, and what he called "route productivity"—essentially, the science of making every delivery truck journey profitable.

The numbers from this period tell a story of patient capital deployment. Between 1996 and 2004, VBL wasn't chasing headlines or market share wars. They were building what would become India's most efficient beverage distribution machine. Each new plant wasn't just additional capacity; it was a node in an increasingly sophisticated logistics network that could respond to demand spikes, seasonal variations, and the peculiar challenges of Indian retail.

In 2004, the company underwent a significant evolution with the merger of DBL, marking a pivotal moment in its history. Then, in 2012, VBIL joined forces with VBL, shaping a stronger and more dynamic entity. Merger of DBL with the company pursuant to the order of High Court of Delhi dated October 6, 2004. These weren't just corporate restructurings—they were consolidations of the various entities Jaipuria had built to serve different territories and product lines.

VBL has been associated with PepsiCo since the 1990s and have over two and half decades consolidated its business association with PepsiCo, increasing the number of licensed territories and sub-territories covered by the Company, producing and distributing a wider range of PepsiCo beverages, introducing various SKUs in the portfolio, and expanding the distribution network.

The relationship with PepsiCo during this period evolved from transactional to strategic. While other bottlers treated the franchise agreement as a vendor relationship, Jaipuria approached it as a partnership. He invested ahead of demand, built capabilities PepsiCo didn't mandate, and most importantly, delivered consistent volume growth even during challenging periods like the 2003 pesticide controversy that rocked the cola industry.

Consider the operational philosophy that emerged during these formative years. Most FMCG companies in India were still thinking about urban markets as their primary battlefield. Jaipuria was already building what he called "the capillary network"—reaching into rural India where a 200ml bottle of Pepsi wasn't just a beverage but an affordable luxury, a reward after a hard day's work.

The technology investments during this period seem prescient in hindsight. While the dot-com bubble was bursting globally, VBL was implementing SAP systems, GPS tracking for delivery vehicles, and automated inventory management—infrastructure that would seem standard today but was revolutionary for an Indian bottler in 2004.

There's a telling anecdote from this period. During a plant visit in 2003, a PepsiCo executive reportedly asked Jaipuria why he was building such large warehouses when current demand didn't justify them. Jaipuria's response: "I'm not building for today's India. I'm building for the India that's coming." That India would arrive sooner than anyone expected.

The financial discipline during these early years deserves special mention. While the business was capital-intensive—each new plant required crores in investment—Jaipuria maintained a conservative debt-to-equity ratio. He understood that in the bottling business, financial stress could compromise quality, and quality issues could terminate a franchise agreement. This conservative approach would later enable aggressive expansion when opportunities arose.

By 2004, VBL had evolved from a single-plant operation to a regional powerhouse with manufacturing facilities across North India, a distribution network reaching thousands of retail outlets, and most importantly, a reputation for operational excellence that made PepsiCo view them not just as a bottler but as a strategic partner in the Indian market.

The foundation was set. The capabilities were built. The team was in place. What came next would transform VBL from a successful regional player into a national champion. But that transformation would require not just capital and ambition, but perfect timing and flawless execution.

IV. Territory Expansion & Consolidation Phase (2004–2016)

The boardroom at RJ Corp's Gurgaon headquarters had seen many meetings, but none quite like the one in early 2004. Ravi Jaipuria stood before a wall-mounted map of India, red pins marking existing territories, blue ones representing opportunities. "We're playing checkers while the market demands chess," he told his leadership team. The next twelve years would prove him right in ways even he couldn't have imagined.

Merger of DBL with our Company pursuant to the order of High Court of Delhi dated October 6, 2004 marked the beginning of VBL's transformation from a collection of regional operations into an integrated national player. Devyani Beverages Limited (DBL) wasn't just another entity—it held critical manufacturing assets and distribution rights that would unlock economies of scale Jaipuria had been chasing for years.

The genius of the 2004-2016 period wasn't aggressive expansion—it was methodical consolidation. While competitors were distracted by the retail boom and mall culture explosion, Jaipuria was quietly stitching together a distribution network that would become unassailable. Each acquisition, each new territory, was chosen not for its immediate profitability but for its strategic value in completing the puzzle.

Merger of VBIL with our Company pursuant to the order of High Court of Delhi dated March 12, 2013 represented another critical milestone. Varun Beverages International Limited brought with it not just international operations but also institutional credibility—Standard Chartered Private Equity had invested in VBIL, validating Jaipuria's vision to sophisticated capital markets.

The numbers tell a compelling story of operational leverage. By 2013, VBL had transformed from a North India-centric bottler to a pan-Indian force. The company acquired the business of manufacturing and marketing of soft drink beverages and syrup mix in Delhi, India—PepsiCo's most important market in the country. This wasn't just a territory acquisition; it was a signal that VBL had graduated from regional partner to national champion.

But the real acceleration came in 2015. Through a series of lightning-fast acquisitions, VBL acquired PepsiCo India's business across Uttar Pradesh, Uttarakhand, Himachal Pradesh, Haryana, and Chandigarh. The speed of integration was breathtaking—plants that had operated independently for decades were brought into VBL's systems within quarters, not years.

As of April 30, 2016, they operated 16 production facilities across India and five production facilities in their international licensed territories. The distribution infrastructure had scaled proportionally: 57 depots and 1,389 delivery vehicles in India, with another 6 depots and 342 vehicles internationally. These weren't just numbers—they represented the circulatory system of a beverage empire.

The decision to go public crystallized in 2016. As of March 31, 2016, the company holds franchises for various PepsiCo products across 17 states and two union territories in India. The timing was deliberate. GST implementation was on the horizon, which would transform India's fragmented market into a single economic zone—perfect for a company with national distribution. Consumption patterns were evolving, with rural India beginning to adopt urban consumption habits. And most importantly, VBL had reached a scale where public markets could provide the capital for the next phase of growth.

The operational philosophy that emerged during this period deserves examination. While most FMCG companies obsessed over marketing and brand building, VBL focused on what Jaipuria called "the three pillars of profitability": route optimization, cooler density, and SKU velocity. Every truck route was mapped and optimized. Every retail outlet was evaluated for cooler placement. Every SKU's performance was tracked daily.

Consider the cooler strategy alone. By 2016, VBL had deployed tens of thousands of coolers across its territories. But these weren't just refrigeration units—they were brand ambassadors, point-of-sale advertisements, and competitive barriers rolled into one. A retailer with a Pepsi cooler was less likely to stock Coca-Cola. It was territorial marking at its most sophisticated.

The technology investments during this period were transformative. VBL implemented one of India's most advanced supply chain management systems, allowing real-time visibility from production to retail. Predictive analytics helped anticipate demand spikes during festivals and cricket matches. Automated ordering systems reduced stockouts while minimizing inventory carrying costs.

The relationship with PepsiCo evolved significantly during this period. VBL wasn't just a bottler anymore—it was PepsiCo's strategic partner in India. When PepsiCo wanted to launch new products, VBL's distribution network made it possible. When PepsiCo needed to respond to competitive threats, VBL's operational agility delivered results. The partnership had become symbiotic.

Financial discipline remained paramount even as growth accelerated. Despite massive capital expenditure on new plants and equipment, VBL maintained healthy cash flows through working capital optimization. The company negotiated better payment terms with retailers while securing favorable credit from suppliers. It was financial engineering at its most practical.

The human capital story of this period is equally impressive. VBL built one of India's most sophisticated sales organizations, with thousands of feet-on-street salespeople equipped with handheld devices for real-time order capture. Training programs transformed truck drivers into brand ambassadors. Plant managers were rotated across facilities to spread best practices.

By early 2016, the company had reached an inflection point. The foundation was complete, the capabilities were proven, and the market opportunity was massive. But to capture it would require capital—lots of it. The decision to tap public markets wasn't just about money; it was about institutionalizing what had been built and preparing for the next phase of growth.

The IPO preparation revealed the true extent of VBL's transformation. Due diligence uncovered a company that had quietly built competitive advantages that would take competitors years to replicate. The distribution network alone—reaching hundreds of thousands of retail outlets—represented billions in replacement cost. The manufacturing facilities were state-of-the-art. The systems and processes were world-class.

As 2016 drew to a close, VBL stood ready for its public market debut. The company that had started with a single plant in Agra now controlled vast swathes of India's beverage distribution. But this was just the beginning. The real transformation—the move from regional champion to national monopoly—was about to begin.

V. The IPO & Immediate Aftermath (2016–2017)

The IPO opens on October 26, 2016, and closes on October 28, 2016. Shares got listed on BSE, NSE on November 8, 2016. Between those dates lay seventy-two hours that would transform Varun Beverages from a closely-held family business into one of India's most valuable beverage companies. The issue is priced at ₹445 per share, a number that would soon seem quaint given what was to come.

The IPO roadshow had been exhausting but enlightening. Ravi Jaipuria and his team crisscrossed from Mumbai to Singapore, London to New York, telling the VBL story to institutional investors. The pitch was simple but powerful: India's per capita consumption of soft drinks was 44 servings per year versus 1,496 in Mexico and 394 in the US. The headroom for growth wasn't just significant—it was generational.

Varun Beverages IPO is a bookbuilding of ₹1,112.50 crores. The issue is a combination of fresh issue of 1.50 crore shares aggregating to ₹667.50 crores and offer for sale of 1.00 crore shares aggregating to ₹445.00 crores. The structure was telling—while the Jaipuria family was willing to dilute for growth capital, they were only selling a small portion of their holdings. This wasn't an exit; it was an acceleration.

The market context matters. October 2016 was a peculiar time for Indian capital markets. The economy was humming, but uncertainty loomed—demonetization would be announced just weeks after VBL's listing. Yet institutional investors saw in VBL something rare: a proxy play on India's consumption story without the execution risk of building brands from scratch.

The subscription numbers revealed massive institutional appetite. QIBs (Qualified Institutional Buyers) oversubscribed their portion multiple times. But retail participation was lukewarm—the idea of investing in a bottler rather than the brand owner seemed counterintuitive to many individual investors. They would later regret this assessment.

Varun Beverages IPO listed at a listing price of 461.90 against the offer price of 445.00. A modest 3.8% premium that hardly hinted at the wealth creation to come. The first day's trading was volatile—the stock touched ₹495 before closing near the listing price. The market was still making up its mind about VBL's value proposition.

What happened next caught everyone off guard. On November 8, 2016—the very day VBL listed—Prime Minister Modi announced demonetization. Overnight, 86% of India's currency became invalid. The consumption sector went into shock. Discretionary spending collapsed. For a company that had just raised capital for aggressive expansion, the timing couldn't have been worse.

But Jaipuria's response revealed the operational DNA that set VBL apart. Within days, the company had recalibrated its entire cash collection mechanism. Digital payment systems were fast-tracked at distributors. Credit terms were extended for trusted retailers. Most importantly, VBL used the disruption to grab market share from smaller, less capitalized competitors who couldn't weather the cash crunch.

The post-IPO period also marked a subtle but significant shift in corporate governance. Public listing brought scrutiny, quarterly earnings calls, and institutional investors asking tough questions. The family-run business had to evolve into a professionally managed corporation while retaining the entrepreneurial agility that had driven its success.

On 23 February 2017, VBL increased its stake in Zambia subsidiary to 90% from 60%. VBL has been successfully running the Zambia operations since its acquisition in 2016. The increase in stake reflects the Company's confidence in the future growth prospects of the subsidiary. This was VBL's first significant move as a listed company—not a splashy Indian acquisition but a quiet consolidation of an African operation. It signaled where Jaipuria saw the future.

The financial metrics post-IPO told a story of disciplined capital allocation. The fresh capital raised—approximately ₹667 crores—was deployed methodically. Debt was paid down, improving the balance sheet. New production lines were added in existing plants, increasing capacity utilization. But the big moves—the territory acquisitions that would transform VBL's footprint—were still being negotiated behind closed doors.

Institutional ownership patterns evolved rapidly. Marquee foreign institutional investors began accumulating positions, attracted by VBL's unique characteristics: asset-heavy enough to create barriers to entry, yet asset-light in brand building costs; tied to a global MNC yet independently managed; exposed to Indian consumption yet naturally hedged through geographic diversification.

The operational improvements post-IPO were less visible but equally important. Listed company discipline forced standardization across plants. Reporting systems were upgraded. Procurement was centralized. These seemingly mundane changes would prove critical when VBL embarked on its massive territory expansion—integrating new acquisitions would be far easier with standardized systems.

Communication with PepsiCo also evolved post-listing. VBL was no longer just a large bottler—it was a publicly listed partner whose stock price reflected, in part, PepsiCo's success in India. This created interesting dynamics. PepsiCo needed VBL to succeed for its own strategic objectives. VBL needed PepsiCo's brands to remain relevant. The partnership deepened from necessity to mutual dependence.

The stock's performance in the months following the IPO was uninspiring. It traded in a narrow range, occasionally dipping below the issue price. Retail investors who had received allotments were disappointed. Business newspapers largely ignored it. VBL was, in market parlance, "dead money"—a stock going nowhere while the broader market rallied.

But beneath this calm surface, Jaipuria and his team were engineering something spectacular. Negotiations with PepsiCo India for additional territories were advancing. Due diligence teams were crawling through bottling plants in Bihar, Jharkhand, and Chhattisgarh. The financing was being arranged. The integration plans were being drafted.

The contrast between market perception and business reality was stark. While the stock languished, the business was firing on all cylinders. Volumes were growing despite demonetization. Market share was increasing. New products were being launched. The disconnect wouldn't last long.

As 2017 progressed, whispers began circulating in the market. VBL was planning something big. The stock began stirring from its slumber. Trading volumes picked up. The smart money was positioning itself.

The IPO had achieved its primary objective—providing growth capital and institutional credibility. But its greater achievement was transforming VBL's currency. As a listed company with liquid stock, VBL could now contemplate acquisitions that would have been impossible as a private company. The stock wasn't just equity—it was acquisition currency.

By late 2017, the foundation was set for VBL's great leap forward. The company had public market credibility, a strong balance sheet, operational excellence, and most importantly, PepsiCo's trust to handle larger territories. The transformation from regional bottler to national powerhouse was about to begin. The market had no idea what was coming.

VI. The Great Territory Grab: Bihar, Jharkhand & Chhattisgarh (2017–2018)

The conference room at PepsiCo India's Gurgaon headquarters crackled with tension on a humid January morning in 2018. Across the table from VBL's negotiation team sat PepsiCo executives who knew they were about to fundamentally reshape India's beverage landscape. The documents being signed weren't just territory transfers—they were the keys to the kingdom.

The Board of Directors of Varun Beverages at its meeting held on 17 January 2018 considered and approved to acquire franchisee rights for PepsiCo India's previously franchised sub-territory in the State of Bihar. Bihar—population 125 million, per capita soft drink consumption less than 10% of the national average. To most, it looked like a challenging market. To Jaipuria, it looked like the 1990s all over again—massive untapped potential waiting for the right execution.

On 11 January 2018, Varun Beverages announced that it has concluded the acquisition of PepsiCo India's previously franchised rights for the state of Chhattisgarh. Just six days before Bihar. The speed was intentional—moving so fast that competitors couldn't respond, regulators couldn't object, and the market couldn't fully process what was happening.

Varun Beverages Limited concludes the acquisition of PepsiCo India's previously franchised sub territory in the State of Jharkhand along with one manufacturing unit at Jamshedpur. The Jamshedpur plant was strategic gold—a modern facility in the heart of India's industrial belt, perfectly positioned to serve not just Jharkhand but the entire eastern corridor.

The strategic logic was compelling. These three states—Bihar, Jharkhand, and Chhattisgarh—represented 200 million people, roughly 15% of India's population. But they contributed less than 5% of India's soft drink consumption. The math was simple: bring consumption up to even half the national average, and you'd essentially create a new market the size of many countries.

But the real genius wasn't in acquiring territories—it was in the sequencing. VBL didn't go after the most attractive markets first. Instead, they targeted the most strategic ones. These eastern states bordered VBL's existing territories, creating contiguous operations that dramatically reduced logistics costs. A truck leaving the Jamshedpur plant could now serve Bihar, Jharkhand, West Bengal, and Odisha without crossing into a competitor's territory.

The integration playbook developed during this period would become VBL's secret weapon. Within 48 hours of takeover, VBL teams would arrive at acquired facilities. Week one: assess and audit. Week two: implement VBL's systems. Week three: retrain staff. Week four: relaunch with improved service levels. The speed was breathtaking—territories that had operated independently for decades were transformed in months.

Acquired PepsiCo's India sub-territories in the State of Jharkhand (with manufacturing facilities), Chhattisgarh and Bihar. The 2018 annual report's simple line understated the magnitude of what had been achieved. VBL had essentially eliminated competition in eastern India. Every bottle of Pepsi sold from Patna to Raipur now generated margins for VBL.

The operational challenges were immense. Bihar's infrastructure was notoriously difficult—poor roads, unreliable power, complex political economy. Jharkhand's industrial markets had different dynamics than VBL's traditional consumer markets. Chhattisgarh's vast rural expanse required completely different distribution strategies. Yet VBL cracked each code, often by empowering local teams who understood ground realities.

Consider the Bihar strategy. Instead of imposing Delhi-style distribution, VBL created a hub-and-spoke model suited to Bihar's village economy. Smaller vehicles for rural routes. Credit programs for small retailers. Local hiring to navigate social dynamics. Within six months, VBL had more points of sale in Bihar than the previous franchisee had built in years.

The financial impact was immediate and dramatic. These acquisitions weren't immediately profitable—integration costs, infrastructure investments, and market development expenses weighed on margins. But the market understood the long-term value. The stock began its march upward, as investors recognized that VBL was building an unassailable moat.

PepsiCo's perspective during this period is fascinating. Why would a global giant hand over critical territories to a single bottler? The answer lay in execution. VBL had proven it could deliver volume growth that PepsiCo's own operations or smaller franchisees couldn't match. For PepsiCo, consolidating with VBL meant faster market development, better competition with Coca-Cola, and ironically, more control through a single, capable partner.

The competitive response—or lack thereof—was telling. Coca-Cola's bottling system in India remained fragmented among multiple franchisees. While VBL was consolidating territories, Coca-Cola's bottlers were fighting turf wars. The structural advantage VBL was building would prove insurmountable.

The technology investments during this period were crucial. VBL deployed advanced route-planning software that optimized delivery routes daily based on demand patterns. IoT sensors on coolers provided real-time temperature and stock data. A centralized command center in Gurgaon could monitor operations across Bihar, Jharkhand, and Chhattisgarh in real-time.

Human capital management was equally sophisticated. VBL retained most employees from acquired operations but retrained them extensively. The message was clear: you're not working for a new company; you're joining a winning team. Performance incentives were restructured to align with VBL's aggressive growth targets. The cultural integration was as important as operational integration.

The supply chain transformation was remarkable. VBL standardized procurement across all territories, leveraging scale for better pricing on everything from sugar to bottle caps. Manufacturing processes were harmonized—a bottle produced in Jamshedpur was identical to one from Jaipur. This standardization enabled flexibility—demand spikes in one region could be served from another.

By March 2018, the transformation was complete. PepsiCo's largest bottler outside the US acquired rights for 5 states in central & east India and Zimbabwe in 2018. VBL now controlled a contiguous territory stretching from Punjab to West Bengal, from the Himalayas to the Deccan Plateau. The company that had started with one plant in Agra now had the largest integrated bottling operation in India.

The numbers told the story. Post-acquisition, VBL controlled territories representing over 60% of India's population. But more importantly, these were territories with the highest growth potential—underpenetrated markets where consumption could double or triple in the coming decade.

The market's reaction was swift and decisive. The stock, which had languished around ₹400-500 since the IPO, began its historic run. Institutional investors who had been skeptical about the bottling business model suddenly understood: VBL wasn't just a bottler—it was building India's beverage infrastructure monopoly.

As 2018 drew to a close, Jaipuria's vision was becoming reality. The eastern expansion wasn't just successful—it was transformative. VBL had proven it could acquire, integrate, and improve operations at a pace and scale nobody had imagined possible.

But this was still just the beginning. Whispers in the market suggested VBL was eyeing the biggest prize of all: the wealthy states of South and West India. If VBL could capture Maharashtra, Gujarat, Karnataka—the heart of India's consumption economy—it would complete its transformation from bottler to beverage emperor. The stage was set for the final act of consolidation.

VII. Becoming India's Beverage Monopoly (2018–2022)

The morning of February 14, 2019, was supposed to be about romance and roses, but in VBL's boardroom, it was about consummating the deal of the decade. The documents spread across the conference table would transform VBL from a major player into something unprecedented in global bottling: a near-monopoly franchise partner of a Fortune 500 beverage giant.

After the deal, Varun Beverages would have 27 out of 29 states under its fold – barring Jammu & Kashmir and Sikkim. The firm already has bottling rights for 21 states – including the fast-growing seven northeastern states – and two union territories – Delhi-NCR and Chandigarh. The acquisition of South and West India territories from PepsiCo wasn't just expansion—it was coronation.

As of 2019, Varun Beverages is PepsiCo bottler in 27 states and 7 union territories of India. The simplicity of that statement belies its revolutionary nature. Never before had a single bottler controlled such a vast territory for a global beverage brand. Not in India, not anywhere.

The strategic logic was irrefutable. Until 2019, PepsiCo ran its own bottling and distribution unit in the south and west zones of India. But at some point, PepsiCo probably just thought, "Hey, VBL can run it in India better than us!" The decision wasn't made lightly—these were PepsiCo's crown jewel territories: Maharashtra with Mumbai, Karnataka with Bangalore, Gujarat with its industrial might, Tamil Nadu with Chennai. Yet PepsiCo chose to hand them over to VBL.

Responsible for over 90% of PepsiCo's total sales volumes throughout India. This wasn't just market dominance—it was market definition. Every Pepsi consumed from Kashmir to Kanyakumari (except in Jammu & Kashmir and Sikkim) now passed through VBL's supply chain. The company that started with one plant in Agra had become synonymous with PepsiCo in India.

The numbers during this period tell a story of explosive growth meeting operational excellence. VBL's share of PepsiCo beverages volume sales increased from ~ 26% in Fiscal 2011 to ~90% now. A 3.5x increase in market share within a single country for a global brand—unprecedented in the annals of franchise history.

But territory was just the beginning. In 2022, VBL entered into an agreement to manufacture Kurkure Puffcorn for PepsiCo India Holdings. This wasn't beverage bottling—this was food manufacturing. VBL was no longer just PepsiCo's bottler; it was becoming PepsiCo's entire operations partner in India.

The product portfolio evolution was remarkable. In 2022, 70% volumes came from selling Carbonated Soft Drinks, 23% volumes came from selling packages of drinking water, and the rest 7% volumes came from selling Non-Carbonated Beverages. But within these categories lay massive complexity—over 50 SKUs across multiple price points, package sizes, and flavor profiles. Managing this portfolio across India's diverse market required logistics capabilities that would make Amazon envious.

Consider the scale achieved by 2022. Over 3.8 million outlets and 40 factories across India and Africa. To put this in perspective, VBL could reach more retail points in India than most FMCG companies could even identify. The company had become India's capillary distribution network for beverages.

The relationship with PepsiCo during this period evolved into something unique in global business. VBL is a Pepsi monopoly really. But it wasn't a monopoly in the traditional sense—it was earned through superior execution. PepsiCo could theoretically revoke territories, but practically, VBL had become irreplaceable. The switching costs—operational, financial, and strategic—were prohibitive.

Manufacturing scale-up during this period was breathtaking. VBL added capacity equivalent to its entire 2016 footprint every 18 months. New plants came online with clockwork precision. Existing plants were expanded and modernized. The company was building tomorrow's capacity today, confident that consumption would catch up.

The technology transformation was equally impressive. VBL deployed AI-powered demand forecasting that could predict consumption patterns down to the SKU level for specific pin codes. IoT sensors monitored everything from production line efficiency to truck fuel consumption. A war room in Gurgaon tracked real-time sales data from millions of transactions daily.

Human capital evolution kept pace with physical expansion. VBL's workforce grew from thousands to tens of thousands, but more importantly, its composition changed. Data scientists worked alongside plant operators. Supply chain experts collaborated with rural sales teams. The company was building capabilities for a digital future while maintaining the relationship-based selling that worked in Indian markets.

The competitive dynamics during this period were fascinating. While VBL was consolidating PepsiCo's operations, Coca-Cola's response was fragmented. Hindustan Coca-Cola Beverages (HCCB) remained a wholly-owned subsidiary, unable to match VBL's entrepreneurial agility. Other Coca-Cola franchisees operated in silos, lacking VBL's scale advantages. The structural disadvantage was becoming insurmountable.

Financial performance reflected operational excellence. Revenue grew from ₹8,250 crore in FY2022-23 to ₹16,042.58 crore in 2023, up 21.8 per cent. But more impressive than topline growth was margin expansion despite inflationary pressures. VBL was demonstrating pricing power—the holy grail of the bottling business.

The market's recognition was swift and decisive. The stock, which had traded around ₹400-500 post-IPO, crossed ₹1,000 in early 2022. Shares rose to a high of about ₹1,020 in early 2022. The one-year return on equity (ROE) stood at approximately 20%. Institutional ownership increased dramatically as global funds recognized VBL's unique position.

Rural penetration strategies during this period deserve special attention. While urban India was saturated with beverage options, rural India remained vastly underpenetrated. VBL's approach wasn't to wait for rural income growth—it was to create affordability through innovation. Smaller pack sizes, localized distribution, and village-level entrepreneurship programs brought Pepsi to India's hinterlands.

The sustainability narrative also evolved. ESG wasn't just compliance for VBL—it was competitive advantage. Water conservation initiatives reduced costs. Solar installations provided energy security. Plastic recycling programs built community goodwill. The company was proving that sustainability and profitability weren't mutually exclusive.

Product innovation accelerated. While VBL didn't own brands, it influenced PepsiCo's India portfolio significantly. Sting energy drink's success was largely due to VBL's distribution muscle. Regional flavors were introduced based on VBL's market intelligence. The student had become the teacher in understanding Indian consumers.

The organizational culture that emerged during this period was unique. Despite becoming a near-monopoly, VBL maintained entrepreneurial hunger. Complacency was actively fought through aggressive targets, performance incentives, and a constant reminder that Coca-Cola was still the market leader by volume. The company operated like a challenger despite being dominant in its space.

International expansion provided additional growth vectors. Operations in Nepal, Sri Lanka, Morocco, Zambia, and Zimbabwe weren't just geographic diversification—they were laboratories for capabilities that could be reimported to India. Lessons from Africa's informal retail informed India's rural strategy. Sri Lankan automation improved Indian plant efficiency.

By 2022's end, VBL had achieved something remarkable. It had built a business that was simultaneously asset-heavy (plants, trucks, coolers) and asset-light (no brand ownership, minimal marketing spend). It had created value through operational excellence rather than financial engineering. It had become indispensable to a global giant while maintaining independence.

The transformation was complete. VBL was no longer a bottler—it was India's beverage infrastructure. Every competitor, every new entrant, every global brand looking at India had to reckon with VBL's dominance. The moat wasn't just wide; it was getting wider every day.

But even as VBL celebrated its Indian dominance, Jaipuria's eyes were on the horizon. Africa beckoned with its billion-plus population, low per-capita consumption, and fragmented market structure. The playbook perfected in India was ready for export. The next chapter of growth was about to begin.

VIII. The African Gambit: International Expansion (2016–2024)

The boardroom on the 42nd floor of Sandton's tallest tower commanded a view of Johannesburg's skyline—a fitting vantage point for the deal that would reshape Africa's beverage landscape. On a December morning in 2023, as the African summer sun blazed outside, Ravi Jaipuria signed documents that would extend VBL's empire from the Himalayas to Table Mountain.

In December 2023, Varun Beverages acquired PepsiCo's South African bottler Bevco for ₹1,320 crore (about ZAR 3 billion). The acquisition wasn't just about entering South Africa—it was about establishing a beachhead for conquering an entire continent. Africa, with its 1.4 billion people and soft drink consumption at a fraction of global averages, represented the next frontier.

The African strategy had actually begun years earlier, almost quietly. Early international moves: Nepal, Sri Lanka, Morocco, Zambia, Zimbabwe—each market a learning laboratory, each operation a test of VBL's ability to export its India playbook. But these were appetizers. South Africa was the main course.

Varun Beverages' subsidiary in Zimbabwe started Commercial Production at a Greenfield facility for Pepsico's products with effect from 16 February 2018. Starting from scratch in Zimbabwe took courage—the country's economic volatility would have scared away most investors. But Jaipuria saw opportunity where others saw risk. Within years, VBL controlled 50% of Zimbabwe's soft drink market.

During 2021, incorporated a new company 'Varun Beverages RDC SAS' in Democratic Republic of Congo. The DRC—population 100 million, per capita soft drink consumption less than 5% of South Africa's. It was India 1995 all over again, except with more complexity: multiple languages, challenging infrastructure, political uncertainty. Yet VBL pressed forward, understanding that first-mover advantage in Africa could be as valuable as their India monopoly.

The BevCo acquisition changed everything. BevCo holds franchise rights from PepsiCo in South Africa, Lesotho and Eswatini. It also has distribution rights for Namibia and Botswana. Overnight, VBL gained access to Southern Africa's economic engine. But more importantly, BevCo came with something VBL had never owned before: local brands. Refreshhh, Reboost, Coo-ee, and JIVE weren't global giants, but they were authentically African, providing pricing flexibility and market segmentation options VBL couldn't achieve with PepsiCo brands alone.

The most recent acquisition was Sbc Tanzania, acquired on November 12, 2024, for $155M. In November 2024, announced acquisitions of SBC Beverages Tanzania Limited for ₹1304 crore, SBC Beverages Ghana Limited for ₹127 crore. These weren't random acquisitions—they were chess moves. Tanzania's strategic location made it a distribution hub for East Africa. Ghana provided entry into West Africa's rapidly growing economies.

The numbers revealed the scale of ambition. SBCT operates five manufacturing facilities with 12 beverage manufacturing lines, located in Dar-es-Salaam, Mbeya, Arusha, and Mwanza. This wasn't just buying market access—it was acquiring industrial infrastructure that would take decades to build organically.

The strategic rationale for Africa focus went beyond simple math of population and low per-capita consumption. Africa offered what India no longer could: greenfield growth opportunity. In India, VBL was increasingly fighting for market share in a mature market. In Africa, they were creating markets.

Consider the operational challenges VBL had to solve. African markets were more fragmented than India—different currencies, regulations, languages, and consumer preferences. Supply chains were complex, with some landlocked countries requiring products to transit through multiple borders. Yet VBL's India experience proved invaluable. They'd solved for complexity before.

The technology deployment in Africa was leapfrogging what VBL had done in India. Instead of replicating India's evolution from manual to digital, African operations went straight to mobile-first, cloud-native systems. Sales teams used smartphones with custom apps. Inventory management was real-time from day one. It was India 2.0, built with lessons learned.

Local talent development became crucial. Unlike India, where VBL could transfer experienced managers between states sharing similar cultures, Africa required genuine localization. VBL invested heavily in training programs, creating a generation of African beverage industry professionals. The approach built goodwill and reduced execution risk.

The relationship with PepsiCo in Africa differed from India. In India, VBL had gradually earned PepsiCo's trust over decades. In Africa, VBL arrived with credibility pre-established. PepsiCo was eager to have VBL replicate its India success in markets where Coca-Cola dominated. The the company acquired 100% share capital of SBC Tanzania Limited and SBC Beverages Ghana Limited respectively, making them the wholly owned subsidiary of the Company effective on November 13, 2024—all with PepsiCo's blessing.

Financial structuring of African operations showed sophistication. VBL didn't just replicate its India model; it adapted to local realities. In countries with currency volatility, contracts were dollar-denominated. In markets with limited banking infrastructure, mobile money systems were integrated. Each market got a customized approach while maintaining standardized reporting to Gurgaon.

The competitive dynamics in Africa were fascinating. Coca-Cola had first-mover advantage in most markets, but their operations were often through local bottlers lacking VBL's scale and sophistication. VBL brought Indian efficiency to African markets—lower costs, better service, faster innovation. It was David versus Goliath, except David had perfected his slingshot in India.

Product strategy in Africa required careful calibration. While global brands like Pepsi had cache, price points needed localization. VBL introduced smaller pack sizes, making products affordable for daily wage earners. They also leveraged local brands from BevCo, creating a portfolio spanning from premium to value segments.

Infrastructure investments were massive but strategic. VBL wasn't just building plants; they were building ecosystems. Training centers for retailers. Cooler assembly facilities. Logistics hubs. Each investment created switching costs that would protect market share for decades.

The sustainability narrative in Africa was different from India. In markets where basic infrastructure was still developing, VBL could build sustainability in from the start. Solar-powered plants in areas with unreliable grids. Water recycling systems in water-stressed regions. These weren't just CSR initiatives—they were competitive advantages.

Risk management in Africa required new frameworks. Political risk insurance. Currency hedging strategies. Local partnership structures that aligned interests while protecting VBL's investments. The company that had mastered operational risk in India was learning to master geopolitical risk in Africa.

The organizational structure evolved to manage this complexity. Regional headquarters were established in key cities. Reporting lines balanced local autonomy with central control. The management information systems that tracked every bottle in India were adapted to track every crate across Africa.

Cultural adaptation went beyond business practices. VBL learned to navigate tribal dynamics in some markets, religious considerations in others. Marketing campaigns that worked in Hindu-majority India or Muslim-majority Morocco might fail in Christian-majority Zimbabwe. Each market required deep cultural intelligence.

Supply chain complexity in Africa made India look simple. Raw materials might come from Europe, packaging from Asia, with finished products distributed across borders with different tariff regimes. VBL's solution was radical localization—building supply chains within Africa rather than importing from India.

The human story behind African expansion was compelling. Indian executives who'd built careers in Rajasthan found themselves in Rwanda. African managers trained in Johannesburg were deployed to Delhi. VBL was building not just a business but a bridge between two continents with shared colonial histories and emerging market dynamics.

By 2024, the African strategy was validated. International operations contributed over 20% of revenues with higher growth rates than India. More importantly, Africa provided optionality—if India growth slowed, Africa could pick up the slack. If currency movements favored exports, capacity could be shifted.

Looking forward, VBL's African footprint positioned it uniquely. As African Continental Free Trade Area (AfCFTA) reduces barriers, VBL's multi-country presence becomes even more valuable. The company that had mastered the world's most complex single market—India—was now mastering the world's most complex continental market.

The transformation was remarkable. The same company that started with one plant in Agra now operated from the Mediterranean to the Indian Ocean, from the Atlantic to the Red Sea. Varun Beverages, the second largest bottler of PepsiCo beverages, recently acquired BevCo and expanded across Africa, proving that the India playbook could be globalized.

But even as VBL celebrated its African success, the next chapter was being written. Operational excellence had driven growth so far, but maintaining that growth would require something more: innovation, technology, and a manufacturing revolution that would redefine what it meant to be a bottler.

IX. Operational Excellence & Manufacturing Innovation

The numbers stop you in your tracks: Over 3.8 million outlets and 40 factories across India and Africa. With over 3.8 million outlets and 40 manufacturing facilities in 6 countries, VBL had built something unprecedented—a real-time neural network connecting village kirana stores to global supply chains, rural retailers to urban factories, African markets to Indian innovation centers.

Walk into VBL's Kosi plant at 4 AM and you'll witness a ballet of automation that would make Toyota envious. Bottles move through production lines at 600 per minute, each one tracked, quality-checked, and coded. But the real magic isn't the speed—it's the flexibility. The same line producing 2-liter Pepsi bottles at dawn switches to 200ml Slice pouches by noon, then to Aquafina by evening. Changeover time: under 30 minutes. Industry standard: 2-4 hours.

The technology story begins with an insight Jaipuria had in 2019: VBL wasn't really in the bottling business—it was in the logistics business with a bottling problem. Once you understand that, everything changes. The factories become nodes. The trucks become mobile warehouses. The coolers become point-of-sale data terminals. The entire operation transforms into a massive, distributed computing system where the product happens to be beverages.

Consider the route-to-market innovation. Every morning, 2,600 company-owned vehicles and thousands more contracted trucks fan out across India and Africa. But these aren't just delivery vehicles—they're data collection machines. Each driver's handheld device captures real-time sales data, competitive intelligence, cooler temperatures, and stock levels. By noon, Gurgaon headquarters knows more about beverage consumption patterns than most governments know about their economies.

The supply chain mastery goes deeper. VBL pioneered what they call "dynamic territory management"—using machine learning to redraw delivery routes daily based on demand predictions, traffic patterns, weather forecasts, and even local events. A cricket match in Bangalore triggers inventory redeployment before the first ball is bowled. A heatwave forecast in Bihar activates production surge protocols 72 hours in advance.

Technology investments transformed every aspect of operations. AI-powered demand forecasting reduced stockouts by 60% while cutting inventory carrying costs by 30%. IoT sensors on production lines predict maintenance needs before breakdowns occur—unplanned downtime dropped 80% in three years. Computer vision systems check bottle fill levels and cap placement at speeds human inspectors couldn't dream of matching.

But the crown jewel of operational excellence is the Integrated Business Planning (IBP) system. Every Monday, algorithms crunch data from millions of transactions, weather patterns, social media sentiment, competitor activities, and economic indicators to generate production plans for the next 13 weeks. These plans cascade automatically to procurement, manufacturing, and logistics teams. Human intervention is needed only for exceptions.

The sustainability initiatives aren't just good PR—they're operational advantages. Solar installations provide 30% of energy needs while insulating from grid volatility. Water recycling reduces costs and ensures production continuity in water-stressed areas. Plastic recycling programs create a circular economy that reduces raw material costs while building community goodwill.

ESG focus has become a competitive moat. When governments introduce environmental regulations, VBL is already compliant. When customers demand sustainability reports, VBL has the data ready. When communities protest industrial water usage, VBL's conservation credentials provide social license to operate.

The visicooler manufacturing integration (2025) represents the next evolution. VBL incorporated White Peak Refrigeration Pvt Ltd on Sep 4, 2025 to manufacture visicoolers and refrigeration equipment. Why should a bottler make refrigerators? Because coolers aren't just refrigerators—they're the last mile of the cold chain, the point of impulse purchase, the billboards that happen to keep drinks cold. By manufacturing coolers, VBL controls product presentation, ensures quality, captures margins, and most importantly, creates switching costs for retailers.

Manufacturing innovation extends beyond traditional metrics. VBL pioneered "micro-factories"—small, modular production units that can be deployed in remote locations. These units, producing 50-100 bottles per minute, make economic sense in markets too small for traditional plants. They're VBL's answer to the last-mile problem in manufacturing.

Quality control systems blend high-tech with high-touch. While spectrometers analyze syrup consistency and gas chromatographs check CO2 levels, VBL maintains teams of human tasters who sample products every hour. Because ultimately, technology can measure everything except whether something tastes right to a consumer in rural Rajasthan or urban Rwanda.

The distribution network deserves special attention. Those 3.8 million outlets aren't just customers—they're partners. VBL's "Retailer Development Programs" train shop owners in inventory management, display optimization, and customer service. The company provides interest-free cooler loans, signage support, and even helps with store renovations. The result: retailer loyalty that competitors can't buy.

Automation hasn't replaced humans—it's amplified them. VBL employs over 50,000 people directly and supports hundreds of thousands more indirectly. But today's VBL employee is different. The company runs one of India's largest corporate training programs, spending 2% of revenues on capability building. Plant operators learn six sigma. Drivers study customer service. Sales teams master data analytics.

The backward integration strategy goes beyond coolers. VBL manufactures preforms, crowns, and plastic closures in-house. This isn't just about capturing margins—it's about supply chain security. When COVID disrupted global supply chains, VBL kept producing because it controlled critical inputs.

Energy management showcases operational sophistication. VBL's plants consume massive amounts of power, but through a combination of efficient equipment, heat recovery systems, and optimized processes, energy consumption per case has dropped 40% since 2016. The company's newest plants are carbon-neutral from day one.

Water stewardship is existential for a beverage company. VBL has achieved "water positive" status—returning more water to communities than it uses in production. Rainwater harvesting, watershed management, and community water projects aren't CSR afterthoughts—they're integrated into operational planning.

The logistics network operates like a Swiss watch. Hub-and-spoke models minimize transportation costs. Cross-docking facilities reduce handling. Route optimization algorithms ensure trucks run full. The result: distribution costs as a percentage of revenue that are among the lowest in the global bottling industry.

Innovation labs in Gurgaon and Johannesburg experiment constantly. New package formats for price-conscious consumers. Concentrate formulations that reduce sugar while maintaining taste. Production processes that cut costs without compromising quality. This isn't R&D for its own sake—every innovation must deliver measurable operational improvement.

Digital transformation permeates everything. Sales teams use tablets with augmented reality apps to show retailers optimal product placement. Maintenance crews use mixed reality headsets for equipment repairs. Finance teams use blockchain for supplier payments. VBL isn't a tech company, but it uses technology like one.

The predictive maintenance program deserves special mention. Using sensors, analytics, and machine learning, VBL predicts equipment failures weeks in advance. Maintenance is scheduled during planned downtime. Parts are ordered just-in-time. The result: equipment uptime rates exceeding 95%, world-class by any standard.

Safety isn't just a priority—it's a precondition. VBL's plants have achieved millions of hours without lost-time injuries. This isn't luck—it's the result of systematic safety culture, continuous training, and investment in safety equipment. Safe operations are efficient operations.

The quality assurance system is multilayered. Raw material testing at receipt. In-process checks during production. Finished product analysis before shipping. Market quality monitoring after sale. Any deviation triggers immediate investigation. VBL's quality metrics exceed PepsiCo's global standards.

Flexibility in manufacturing has become a core competency. The same plant can produce carbonated drinks, juices, water, and now snacks. Seasonal demand swings are managed through temporary capacity additions. New product launches happen in weeks, not months. This agility is a competitive weapon.

The vendor development program creates ecosystems. VBL doesn't just buy from suppliers—it develops them. Technical assistance, quality training, financing support, and long-term contracts help suppliers grow with VBL. The result: a supplier network that's invested in VBL's success.

Cost optimization never stops. Despite inflation, VBL's cost per case has remained flat through continuous improvement. Energy efficiency, material optimization, process improvement, and automation offset input cost increases. This operational leverage drives margin expansion even in inflationary environments.

The environmental management system goes beyond compliance. VBL's plants are biodiversity positive, with green belts exceeding built areas. Waste is minimized, recycled, or converted to energy. Air emissions are below detection limits. These aren't costs—they're investments in operational longevity.

Knowledge management ensures best practices spread quickly. An innovation in Zambia is implemented in Rajasthan within quarters. A quality improvement in Karnataka cascades to Morocco. VBL operates as a learning organization where knowledge is the most valuable currency.

The future of manufacturing at VBL is already visible. Lights-out factories operated by AI. Drone delivery to remote retailers. 3D-printed bottles customized for local preferences. Biotechnology producing sweeteners on-site. The company that mastered traditional manufacturing is reinventing manufacturing itself.

But operational excellence isn't an end—it's a means. Every efficiency gained, every cost saved, every innovation implemented serves one purpose: delivering beverages to consumers at the right price, right place, and right time. In that mission, VBL has built an operational machine that's become the envy of the industry.

As impressive as the operations are, they're just the foundation. The real value creation comes from how VBL deploys this operational excellence to capture market opportunities, expand portfolios, and navigate competitive dynamics. That story—of products, markets, and competition—reveals how operational excellence translates into market dominance.

X. Product Portfolio Evolution & Market Dynamics

The portfolio tells a story of transformation. In 2022, 70% volumes came from selling Carbonated Soft Drinks, 23% volumes came from selling packages of drinking water, and the rest 7% volumes came from selling Non-Carbonated Beverages. But those percentages hide a revolution in how Indians consume beverages—a revolution VBL both rode and shaped.

Start with the crown jewels: Carbonated soft drinks – ~70% of volumes, including Pepsi, Mountain Dew, Mirinda, 7UP, Sting and Evervess. Each brand isn't just a product—it's a carefully positioned solution to a specific consumer need. Pepsi for mainstream refreshment. Mountain Dew for youth energy. Mirinda for colorful celebration. 7UP for digestive comfort. Sting for intense stimulation. The portfolio architecture is deliberate, comprehensive, and devastatingly effective.

The real story isn't the brands—it's how VBL made them accessible. In 2010, a 300ml Pepsi cost ₹10-12, affordable for urban middle class but out of reach for rural India. VBL's innovation wasn't creating new products—it was reimagining price architecture. ₹5 for a 200ml returnable glass bottle. ₹10 for a 250ml PET. ₹20 for a 600ml. Suddenly, Pepsi wasn't a luxury—it was an affordable indulgence.

Non-carbonated beverages and packaged water – ~30% volumes, covering Tropicana, Gatorade, Aquafina and others. This segment's growth trajectory reveals VBL's strategic evolution. Aquafina addressed water safety concerns in urban India. Tropicana captured the health-conscious consumer. Gatorade targeted the fitness boom. Each addition wasn't reactive—it was anticipatory, launched just as consumer trends emerged.

Competition with Coca-Cola system in India plays out like a chess match where VBL controls more squares but Coca-Cola holds the center. Coca-Cola leads with roughly 50% market share versus PepsiCo's 35%, but VBL's operational excellence means PepsiCo products often have better availability, cooler presence, and pricing flexibility. The battle isn't for dominance—it's for profitable growth.

The competitive dynamics are fascinating. Coca-Cola's fragmented bottling system—multiple franchisees with varying capabilities—faces VBL's unified machine. When Coca-Cola launches a promotion in Maharashtra, three different bottlers must coordinate. When PepsiCo promotes in Maharashtra, VBL executes seamlessly. This structural advantage compounds over time.

Pricing power and market share gains reflect a sophisticated understanding of Indian price psychology. VBL doesn't just cut prices—it creates price architectures that expand consumption. A ₹10 Pepsi isn't competing with a ₹10 Coke—it's competing with ₹5 local brands, ₹3 flavored water, or simply not consuming anything. By making the price ladder granular, VBL expanded the market rather than just fighting for share.

Rural penetration strategies deserve special attention. Urban India drinks 100+ servings per capita annually. Rural India? Less than 20. VBL saw this not as a challenge but as an opportunity worth thousands of crores. The approach was methodical: start with block headquarters, expand to large villages, then peripheral areas. Build distribution through local entrepreneurs. Create affordable price points. Educate about product safety and quality.

The innovation in rural wasn't just distribution—it was communication. VBL's rural activation programs—cricket tournaments, festival sponsorships, school programs—built brand awareness where traditional media didn't reach. Mobile video vans showed Bollywood movies with product placement. Local influencers became brand ambassadors. Rural wasn't treated as urban-lite but as a distinct market requiring distinct strategies.

Product localization went beyond pricing. Flavor profiles were adjusted for regional preferences—sweeter in South India, more carbonated in North India. Package sizes reflected consumption patterns—larger bottles where extended families dominate, smaller ones in nuclear family markets. Even cooling standards varied—extra cold in hot climates, moderate in temperate zones.

The Sting phenomenon deserves special mention. Launched as an energy drink in a market dominated by Red Bull's premium positioning, Sting was positioned as the "mass energy" solution. Priced at ₹20 versus Red Bull's ₹100+, Sting created a new category. VBL's distribution muscle put Sting in 2 million outlets within two years. Today, Sting contributes ~10% of volumes with higher margins than traditional CSDs.

Snacks integration marked a paradigm shift. In 2022, VBL entered into an agreement to manufacture Kurkure Puffcorn for PepsiCo India Holdings. This wasn't diversification—it was convergence. The same trucks delivering beverages could carry snacks. The same retailers stocking drinks could sell snacks. The same consumers buying Pepsi would purchase Kurkure. Synergies weren't theoretical—they were immediate and measurable.

The water business reveals strategic patience. Aquafina operates in a commoditized category where differentiation is minimal. Yet VBL built a ₹2,000+ crore business through execution excellence. Consistent quality when competitors faced contamination issues. Reliable availability when others faced stockouts. Premium positioning at commodity prices. Water became a trust business, and VBL earned that trust.

Juice represents the future. As India becomes health-conscious, carbonated drinks face headwinds. VBL's response isn't defensive—it's offensive. Tropicana's range expanded from basic orange to exotic fruits. Slice transformed from mango drink to fruit platform. New launches like Frutz targeted specific occasions. The juice portfolio isn't cannibalizing CSDs—it's capturing new consumption moments.

Gatorade showcases category creation. Sports drinks barely existed in India before VBL's push. Through cricket sponsorships, gym partnerships, and marathon associations, VBL built a category from scratch. Gatorade isn't competing with Pepsi—it's creating its own space in hydration and performance.

Private label strategy remains minimal but strategic. While VBL manufactures some retailer brands, it's selective. The focus remains on PepsiCo brands where margins and control are higher. Private label is tactical—maintaining retailer relationships without compromising core brand focus.

Portfolio gaps are deliberately maintained. VBL doesn't play in alcohol, dairy, or hot beverages—categories that would dilute focus or create channel conflicts. The discipline to say no is as important as the ambition to say yes.

Premiumization is accelerating. While volumes come from mass products, value growth increasingly comes from premium variants. Pepsi Black for zero-calorie seekers. Tropicana Essentials for health enthusiasts. Gatorade Sports for serious athletes. Premium doesn't mean niche—at VBL's scale, 1% of the market is still millions of consumers.

Channel strategy evolved with retail modernization. Modern trade requires different products than traditional retail. E-commerce needs different packaging than physical stores. VBL doesn't just adapt—it leads, creating channel-specific products that maximize each format's potential.

Digital engagement transformed marketing efficiency. VBL doesn't own brands, but it influences their perception through retail execution. QR codes on bottles drive digital engagement. Social media campaigns amplify retail promotions. Digital isn't separate from physical—it's integrated into every consumer touchpoint.

Seasonal management became science. Summer isn't just peak season—it's 60% of annual volumes compressed into four months. VBL's response: pre-season inventory building, temporary capacity additions, extended operating hours, and dynamic pricing. What could be chaos becomes choreographed execution.

Competition isn't just Coca-Cola anymore. Regional brands, ethnic drinks, health beverages, and even tea/coffee compete for share of throat. VBL's response isn't confrontation—it's envelope expansion. Make the pie bigger rather than fight for slices.

Market share gains tell the execution story. In acquired territories, VBL typically gains 5-10% market share within two years through better availability, superior cooling, and aggressive pricing. Share gains come not from marketing magic but operational excellence.

Future portfolio evolution is visible. Plant-based beverages for sustainability seekers. Functional drinks for health optimization. Personalized nutrition for individual needs. VBL isn't waiting for these trends—it's preparing infrastructure to capture them when they emerge.

The portfolio strategy reveals sophisticated thinking. This isn't about selling sugar water—it's about owning consumption occasions. Morning hydration. Afternoon refreshment. Evening energy. Celebration enhancement. Sports recovery. Every moment a consumer might want a beverage, VBL has a solution.

But products are only as good as their financial performance. The real test of VBL's strategy isn't market share or volume growth—it's value creation. The financial story reveals how operational excellence and portfolio optimization translate into shareholder returns.

XI. Financial Performance & Capital Allocation

The transformation is staggering. From ₹445 IPO price to current levels, the stock's journey mirrors the business transformation. Revenue of approximately ₹8,250 crore for the fiscal year 2022-2023 grew to Net revenue of Rs 16,042.58 crore, up 21.8 per cent in 2023, then to Revenue: 21,078 Cr, Profit: 2,881 Cr by 2024. These aren't just numbers—they're validation of a strategy executed flawlessly.

Stock performance: From ₹445 IPO price to current levels tells only part of the story. The real narrative is value creation through compounding. A ₹1 lakh investment at IPO would be worth over ₹10 lakhs today, excluding dividends. But this wasn't a smooth ride—the stock languished post-IPO, surged during territory acquisitions, consolidated during integration, then exploded as the market recognized the monopoly VBL had built.

Shares rose to a high of about ₹1,020 in early 2022. The one-year return on equity (ROE) stood at approximately 20%. But these headline numbers obscure the underlying drivers. ROE expansion came not from financial leverage but operational leverage—fixed costs spread over growing volumes, resulting in margin expansion despite inflationary pressures.

Capital structure evolution reveals sophisticated financial management. Post-IPO, VBL had minimal debt. Territory acquisitions were funded through internal accruals and strategic debt. The 2024 QIP raising ₹7,500 crore wasn't desperation—it was opportunistic, funding African expansion while maintaining balance sheet strength. Debt-to-EBITDA never exceeded 2x, remarkable for a capital-intensive business.

Dividend policy balanced growth and returns. While reinvestment dominated—necessary given expansion opportunities—VBL maintained consistent dividends, signaling confidence in cash generation. The dividend payout ratio of 15-20% reflected optimal capital allocation: enough to reward shareholders, not so much to constrain growth.

Working capital management deserves special attention. In a business with seasonal demand and extended credit terms, working capital can destroy returns. VBL's solution: negative working capital in peak season through advance payments from distributors, vendor financing, and optimized inventory turns. Cash conversion cycles improved from 45 days to under 30 days despite business complexity increasing.

The revenue growth trajectory—CAGR exceeding 25% over five years—came from multiple drivers. Volume growth contributed 15-18%. Price increases added 5-7%. Mix improvement from premiumization contributed 3-5%. New territories provided the remainder. This wasn't one-dimensional growth but multi-factorial expansion.

Margin evolution tells the operational excellence story. Gross margins expanded despite commodity inflation through procurement efficiency and pricing power. EBITDA margins improved from high teens to mid-twenties through operating leverage. Net margins doubled from 5-6% to 13-14% through interest cost reduction and tax optimization.

Geographic revenue mix evolved strategically. India contributed 80%+ historically but is trending toward 75% as international operations scale. This isn't de-prioritizing India—absolute India revenues continue growing. It's portfolio diversification, reducing single-market risk while maintaining growth momentum.

Segment profitability reveals strategic choices. CSDs generate highest absolute profits given volumes. Water has lowest margins but builds retailer relationships. Juices have highest margins but lower volumes. Snacks are margin-accretive but capital-intensive. The portfolio isn't optimized for any single metric but for system economics.

Capital allocation decisions reflect long-term thinking. Maintenance capex runs 3-4% of revenues—industry-leading efficiency. Growth capex varies with opportunity but averages 8-10% of revenues. M&A spending is opportunistic but disciplined—every acquisition must be accretive within 18 months. No diversification beyond core competencies.

The QIP in 2024 raising ₹7,500 crore was masterfully timed. Markets were receptive. Valuations were reasonable. Growth opportunities were visible. The dilution was minimal given market cap expansion. Proceeds went toward debt reduction and strategic acquisitions, not speculation.

Cash flow characteristics reveal business quality. Operating cash flows consistently exceed net profit, indicating real earnings, not accounting profits. Free cash flow generation funds growth without excessive leverage. Even during rapid expansion, VBL remained cash-generative—the hallmark of a great business.

Tax optimization through manufacturing incentives, SEZ benefits, and strategic structuring reduced effective tax rates below statutory rates. But VBL avoided aggressive tax planning that could create regulatory risk. The approach was optimization, not evasion.

Currency management in international operations showed sophistication. Natural hedging through local cost structures. Financial hedging for net exposures. Strategic pricing to pass through currency impacts. The goal wasn't eliminating currency risk but managing it intelligently.