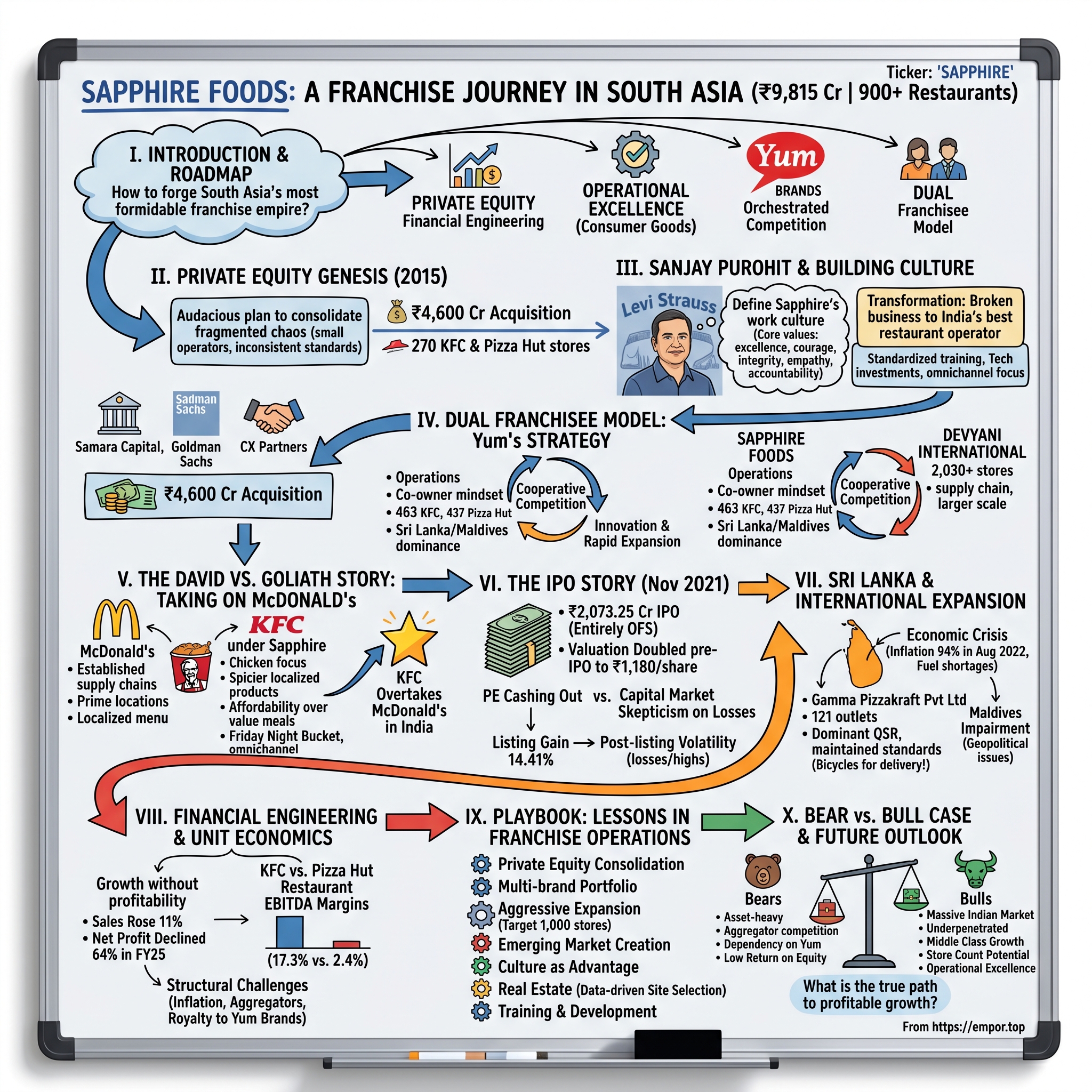

Sapphire Foods: The Franchise Empire That Conquered South Asia

I. Introduction & Episode Roadmap

Picture this: It's 2015, and India's quick-service restaurant landscape is a patchwork quilt of small operators, each running a handful of KFC or Pizza Hut outlets with wildly different standards, systems, and cultures. Enter a consortium of private equity firms—Samara Capital, Goldman Sachs, and CX Partners—with an audacious plan: consolidate this chaos into a single powerhouse. Today, that bet has transformed into Sapphire Foods India Limited, a ₹9,815 crore behemoth operating over 900 restaurants across three iconic brands.

The question that should fascinate any student of business is deceptively simple: How does one take eight disparate restaurant businesses—each with its own operational quirks, vendor relationships, and organizational culture—and forge them into South Asia's most formidable franchise empire? The answer involves a unique cocktail of private equity financial engineering, operational excellence borrowed from consumer goods, and a counterintuitive strategy of competing against your own sister franchisee.

This is a story about transformation at scale. It's about how Yum Brands orchestrated competition between its own franchisees to accelerate growth. It's about navigating economic crises in Sri Lanka while maintaining market leadership. And ultimately, it's about whether the traditional QSR franchise model can survive the onslaught of cloud kitchens and food aggregators in emerging markets.

What makes Sapphire particularly fascinating is its dual identity: part private equity rollup, part operational excellence machine. Unlike the typical PE playbook of financial engineering and cost-cutting, Sapphire's journey required something far more difficult—building a unified culture from scratch while simultaneously scaling at breakneck speed. The company that emerged from this crucible now runs KFC outlets that generate higher average unit volumes than many developed markets, operates Pizza Hut's most successful international market in Sri Lanka, and has quietly become a case study in how to build a multi-country, multi-brand QSR platform in emerging markets.

II. The Private Equity Genesis Story (2015)

The year 2015 marked a watershed moment in Indian QSR history, though few recognized it at the time. Across conference rooms in Mumbai and Singapore, private equity partners were drawing up plans for what would become one of the most ambitious restaurant consolidations ever attempted in an emerging market. The target wasn't a single distressed chain or an underperforming brand—it was an entire ecosystem of franchise operators that had grown organically, haphazardly, over two decades. The company was formally established in September 2015, through the acquisition of approximately 270 KFC and Pizza Hut stores across India and Sri Lanka by a consortium of private equity firms. The fragmented landscape they inherited was staggering in its complexity—eight different businesses, each with its own operational systems, vendor relationships, and management cultures, all suddenly forced under one corporate umbrella.

To understand the audacity of this consolidation, consider the pre-2015 reality: India's QSR franchise ecosystem was a cottage industry masquerading as organized retail. Individual franchisees might operate five to fifteen outlets, each running their own procurement, maintaining separate IT systems, and negotiating individually with landlords. Quality standards varied wildly—a KFC in Mumbai might deliver an entirely different experience than one in Chennai, not by design but by default. This fragmentation was Yum's Achilles heel in India, preventing the brand consistency and operational leverage that made their model successful in developed markets.

The private equity consortium—led by Samara Capital with Goldman Sachs and CX Partners as co-investors—saw opportunity where others saw chaos. Their thesis was elegantly simple yet operationally complex: consolidate the fragmented franchisees, standardize operations, achieve scale economies, and create a platform capable of rapid, profitable expansion. The ₹4,600 crore acquisition wasn't just buying restaurants; it was buying the right to reshape an entire market.

What made this particularly interesting from Yum's perspective was their deliberate orchestration of the consolidation. Rather than forcing consolidation themselves—which would have required significant capital and management bandwidth—they essentially outsourced the heavy lifting to private equity. Yum needed scale players who could maintain brand standards, invest in growth, and provide the operational consistency that individual franchisees couldn't deliver. The fragmented franchise model had reached its natural limits; what India's growing QSR market demanded was industrial-scale execution.

The timing was no accident. India's organized food services market was at an inflection point in 2015—smartphone penetration was accelerating, disposable incomes were rising, and urban consumers were increasingly comfortable with Western QSR brands. The private equity firms weren't just consolidating restaurants; they were betting on a fundamental shift in Indian consumption patterns. The question was whether they could build the operational capability to capture this opportunity before the window closed.

III. Sanjay Purohit & Building a Culture from Chaos

When Sanjay Purohit walked into Sapphire Foods' makeshift headquarters in late 2015, he wasn't inheriting a company—he was inheriting chaos masquerading as consolidation. Eight different businesses, acquired over a matter of months, each with their own operational DNA, vendor relationships, and deeply entrenched work cultures. The mechanical engineer turned IIM-Bangalore alumnus, fresh from transforming Levi Strauss India, faced a challenge that would have broken most executives: forge a unified identity from this operational Tower of Babel.

"Sapphire Foods had only just come into existence when Sanjay, formerly of Levi Strauss and Cadbury India, came on board. It was really up to me to charter the aspirations of what we wanted to achieve, what the culture would look like, what operating levers we wanted to chase and what our core purpose would be." The task wasn't just operational—it was fundamentally existential. What would Sapphire Foods stand for? How could it compete not just with other QSR operators but with the established narrative that India was too price-sensitive, too vegetarian, too traditional for Western QSR brands to truly scale?

Purohit's approach was counterintuitive for a private equity-backed rollup. Rather than immediately focusing on cost synergies and financial engineering—the typical PE playbook—he started with culture. On his very first day, he presented the fledgling team with five core values: excellence, courage, integrity, empathy, and accountability. These weren't corporate platitudes; they were operational imperatives. Excellence meant standardizing operations across hundreds of outlets that had never followed common procedures. Courage meant challenging Yum's global playbook when it didn't fit Indian realities. Integrity meant building trust with franchisees who had just sold their life's work to faceless private equity firms.

"That was roughly 250 restaurants at the time. It was also eight different cultures. People were used to different operating environments. The first thing I had to do was define the Sapphire Foods work culture, and that's something that stems from the basic values underlying the business." The integration challenge was staggering. Some acquired operations ran on paper-based inventory systems; others had rudimentary IT but incompatible platforms. Quality standards varied wildly—one franchisee's "fresh" might mean daily preparation, another's might mean weekly. Customer service protocols, pricing strategies, vendor relationships—everything needed harmonization without disrupting daily operations serving millions of customers.

What made Purohit particularly effective was his consumer goods background. At Cadbury India, he had learned how to build brands that resonated with Indian consumers while maintaining global standards. At Levi Strauss, he had mastered the art of retail execution in a market where organized retail was still nascent. This wasn't the typical QSR executive who had grown up in the industry; this was an outsider who saw opportunities where others saw constraints.

"From the beginning, when we acquired a broken business, our aspiration has been that one day we could become India's best restaurant operator." The audacity of this vision cannot be overstated. Here was a cobbled-together collection of franchises, operating in a market where McDonald's had a two-decade head start, where Domino's had cracked the delivery code, where local chains like Haldiram's dominated the value segment. Yet Purohit wasn't content with being a competent operator; he wanted to be the best.

The transformation started with basics that would seem trivial but were revolutionary in the Indian QSR context. Standardized training programs that took team members from different operational backgrounds and created a unified service culture. Technology investments that gave real-time visibility into inventory, sales, and customer feedback across hundreds of locations. Most importantly, a performance management system that rewarded not just financial metrics but adherence to the new cultural values.

Within eighteen months, the eight different cultures had begun to coalesce into something distinctive—not quite the American efficiency of McDonald's, not quite the local flexibility of independent operators, but something uniquely Sapphire. Store managers who had operated as independent fiefdoms under previous owners now shared best practices in WhatsApp groups. Supply chain executives who had negotiated individually with vendors now leveraged collective scale to drive better terms. Marketing teams that had run hyperlocal campaigns now coordinated national brand-building initiatives.

The real test came when Purohit made his first major strategic bet: that Indian consumers were ready for premium QSR experiences, not just value offerings. While competitors raced to the bottom with ₹99 meal deals, Sapphire began investing in store ambiance, premium ingredients, and service quality. "Brands that stand for something distinct always win. And his instinct was right: both KFC and Pizza Hut have done better than well – they've bucked global trends." This wasn't just operational excellence; it was a fundamental reimagining of what QSR could be in India.

IV. The Dual Franchisee Model: Understanding Yum's India Strategy

The dual franchisee model that Yum employs in India is perhaps the most misunderstood aspect of the country's QSR landscape. On the surface, it seems counterintuitive—why would a global brand deliberately create competition between its own franchisees? The answer reveals a sophisticated understanding of market dynamics that most Western brands miss when entering India.

Sapphire Foods and Devyani International are two franchisees for Yum Brands in India. Yum Brands follows a dual franchisee system in India, similar to McDonald's. This wasn't an accident or an artifact of messy expansion—it was deliberate strategy. Yum recognized that India's vast geography, diverse consumer preferences, and complex regulatory environment made a single franchisee model risky. By maintaining two major operators, they created internal competition that drove innovation, operational excellence, and rapid expansion.

The territorial allocation between Sapphire and Devyani reads like a medieval map of kingdoms. As of Q2FY25, company owned and operated 463 KFC restaurants in India and Maldives, 437 Pizza Hut restaurants in India, Sri Lanka, and the Maldives, and 9 Taco Bell restaurants in Sri Lanka. Meanwhile, Devyani International operates more than 2,030 stores across brands in over 280 cities in India, Thailand, Nigeria and Nepal. The overlap and competition happen at the brand level within India—both operate KFC and Pizza Hut outlets, sometimes in the same cities, creating a fascinating dynamic of cooperative competition.

The genius of this model becomes apparent when you examine the results. Rather than cannibalizing each other, the competition has driven both franchisees to excel. Devyani, backed by the RJ Corp conglomerate with its PepsiCo bottling operations, brought supply chain expertise and capital depth. Sapphire, with its private equity backing and focus on operational excellence, brought professional management and aggressive expansion strategies. The result? India became one of Yum's fastest-growing markets globally, with KFC overtaking McDonald's—something that seemed impossible a decade ago.

What's particularly fascinating is how each franchisee developed distinct operational philosophies despite running the same brands. Unlike Devyani, Sapphire operates with a co-owner mindset, focusing on store-level execution, advanced operational tools, and disciplined capital allocation. This differentiation in approach created a natural experiment in franchise operations—Yum could observe which strategies worked better in different contexts and encourage cross-pollination of best practices.

The recent speculation about consolidation adds another layer to this story. Yum Brands is reportedly exploring the possibility of merging its two key franchise partners in India, Devyani International and Sapphire Foods India. Sources suggest that Yum Brands is facilitating discussions that may lead to Sapphire Foods merging into Devyani International. If true, this would mark the end of an era—the dual franchisee model having served its purpose of rapid expansion and market education, now potentially giving way to consolidated scale economics.

The financial dynamics of this competition are revealing. Devyani's market capitalization is at 213.2 billion Indian rupees ($2.50 billion), while Sapphire's stood at 107.2 billion rupees. Despite operating similar brands in overlapping markets, the market values Devyani at nearly twice Sapphire's worth—a reflection of its larger scale, broader geographic footprint, and perhaps the strategic value of its conglomerate backing.

It is Sri Lanka's Largest International QSR chain with 121 outlets in 52 cities. This international expansion showcases another dimension of the dual franchisee strategy—while both operators competed in India, Sapphire carved out a near-monopoly in Sri Lanka, becoming the dominant QSR player in a market that most global brands had written off as too small or too risky.

The operational metrics tell a story of intense competition driving performance. Sapphire reported a 6% sequential decline in KFC and 13% sequential decline in Pizza Hut's average daily sales for the quarter ended March, while Devyani's KFC same-store sales saw a decline of 6.1% in the fourth quarter year-on-year. These parallel struggles suggest that the challenges facing Indian QSR aren't franchisee-specific but systemic—inflation, changing consumer preferences, and the rise of food aggregators affecting both operators equally.

V. The David vs. Goliath Story: Taking on McDonald's

The narrative of KFC overtaking McDonald's in India reads like a classic underdog story, except the underdog was backed by sophisticated private equity operators and armed with a secret weapon: fried chicken that actually appealed to Indian palates. "When Sapphire started, KFC in India was significantly smaller than McDonald's. Today, it's much larger, and as we continue to optimise our stores and increase our market share, that growth will continue."

This transformation didn't happen overnight. When Sapphire took over in 2015, McDonald's had a two-decade head start in India, with established supply chains, prime real estate locations, and deep brand recognition. The golden arches were synonymous with Western fast food in Indian cities. KFC, by contrast, was seen as a niche player—appealing to non-vegetarian consumers in a country where vegetarian options often determined QSR success.

The breakthrough came from a counterintuitive insight: rather than trying to out-vegetarian McDonald's, which had masterfully created localized offerings like the McAloo Tikki burger, KFC doubled down on its core competency—chicken. But not just any chicken. Sapphire's team recognized that Indian consumers had sophisticated palates when it came to chicken preparation. The standard global KFC recipe, while successful elsewhere, needed significant adaptation.

Product localization became Sapphire's obsession. They introduced spice levels that would make Colonel Sanders sweat—the Fiery Grilled chicken, the Nashville Hot variants adapted for Indian heat tolerance, and rice bowls that transformed KFC from a snack destination to a meal solution. "brands that stand for something distinct always win". And his instinct was right: both KFC and Pizza Hut have done better than well – they've bucked global trends.

The marketing strategy was equally audacious. While McDonald's positioned itself as a family restaurant—safe, predictable, vegetarian-friendly—KFC embraced its identity as the destination for serious chicken lovers. The "Finger Lickin' Good" tagline wasn't just translated; it was weaponized. Campaigns featuring Bollywood celebrities devouring chicken with unabashed enthusiasm broke through the cultural hesitation around meat consumption in public spaces.

But perhaps the most crucial factor was Sapphire's operational excellence in delivery and takeaway—capabilities that would prove prescient when the pandemic hit. While McDonald's had focused on the dine-in experience with its PlayPlaces and birthday party offerings, Sapphire invested heavily in kitchen design optimized for delivery, packaging that maintained product quality during transport, and partnerships with emerging food aggregators.

The omnichannel revolution that Sapphire pioneered deserves special attention. By 2019, before anyone had heard of COVID-19, Sapphire was already operating on the assumption that the future of QSR in India would be dramatically different from the West. They recognized that Indian consumers, particularly millennials, were leapfrogging traditional consumption patterns. Why build massive dine-in restaurants when customers increasingly wanted food delivered to their offices or homes?

This bet on delivery and digital ordering created a virtuous cycle. Better delivery performance led to higher ratings on aggregator platforms, which drove more orders, which justified further investment in delivery-optimized stores. By the time the pandemic forced everyone into delivery mode, Sapphire's KFC outlets were already running a well-oiled machine while competitors scrambled to adapt.

The numbers tell the story of this dramatic reversal. McDonald's is perhaps the most potent competitor in the fast food restaurant chain business. It is often ranked as number one in most of the aspects revolving around this particular industry including, sales volume; customers served in a month, number of stores globally as well as the total revenue generated. Yet in India, KFC's rise under Sapphire's management has been nothing short of remarkable.

The pricing strategy was another masterstroke. Rather than competing with McDonald's on value meals, Sapphire positioned KFC as affordable indulgence. A KFC meal might cost 20-30% more than a McDonald's equivalent, but it delivered a protein-heavy, flavor-forward experience that justified the premium. This wasn't about being cheap; it was about being worth it.

Marketing campaigns reflected this confidence. The "Friday Night Bucket" became a cultural phenomenon, transforming KFC from a restaurant into a social ritual. Office teams ordering KFC for late-night work sessions, families gathering around a bucket for weekend cricket matches—Sapphire didn't just sell chicken; they sold moments.

VI. The IPO Story: Peak Valuation or Perfect Timing? (2021)

The Sapphire Foods IPO of November 2021 was a masterclass in private equity timing—or perhaps a cautionary tale about Indian capital markets' appetite for loss-making growth stories. The numbers alone tell a remarkable story: Sapphire Foods IPO is a bookbuilding of ₹2,073.25 crores. The issue is entirely an offer for sale of 1.76 crore shares. Not a single rupee would go to the company—this was pure exit, the private equity firms cashing out after six years of value creation.

The pre-IPO maneuvering deserves scrutiny. On 5th Aug 2021, company issued shares at Rs. 505 per share and Rs. 544 per share to promoters Sapphire Food Mauritius and Edelweiss Fund respectively, both of which are among the selling shareholders in OFS. Three months later, these same shareholders were selling to public investors at ₹1,180 per share—more than double what they had just paid. This wasn't illegal, but it raised eyebrows about corporate governance and fairness to incoming shareholders.

The timing seemed perfect on paper. India's QSR sector was roaring back from COVID lockdowns, Devyani International had recently listed successfully, and there was genuine excitement about consumption stories. In Q3 FY22, Sapphire Foods achieved its highest ever quarterly sales, EBITDA margin, profit after tax and new restaurant additions. Revenue increased YoY by 52 per cent to Rs 508 cr, and EBITDA stood at Rs 115 cr, representing a growth of 43.2 per cent YoY. Profit after tax was Rs 51 crore, compared to Rs 3 crore in Q3 FY21.

Yet the valuation math was challenging. Devyani International which has same franchise of KFC, Pizza Hut etc as that of Sapphire, it available at ~18000 Cr Mcap on 1100 Crores revenue. So, Mcap/Sales = 16x. While, Sapphire with almost same revenue is coming up at ~7500 Cr of Mcap. This valuation discount might have seemed like an opportunity, but it also reflected market skepticism about Sapphire's growth trajectory versus its sister franchisee.

Sapphire Foods IPO bidding started from November 9, 2021 and ended on November 11, 2021. The allotment for Sapphire Foods IPO was finalized on Tuesday, November 16, 2021. The shares got listed on BSE, NSE on November 18, 2021. The listing was positive—shares opened at ₹1,350, delivering a 14.41% listing gain. For a brief moment, it seemed the private equity firms had timed their exit perfectly.

The stock hit a low of Rs 974 per share within a few days of listing but then reached a high of Rs 1,435 on February 14, 2022. As of April 8, 2022, the stock closed at Rs 1,353, about 14.7 per cent higher than its issue price of Rs 1,180. This volatility in the early months reflected the market's struggle to value a company that was simultaneously showing explosive growth and persistent losses.

The IPO structure—pure OFS with no primary component—sent a clear message: the private equity investors believed they had maximized value and it was time to exit. Company gains nothing as IPO is pure OFS, but outgoing investors benefit at the cost of company and incoming investor. Shares may have been allotted for whatever reason, but present OFS price of 2x last transaction price, barely 3 months ago is unjustified.

What's particularly interesting is how the IPO crystallized the private equity playbook. In six years, Samara Capital and its partners had consolidated a fragmented industry, brought in professional management, scaled operations from 270 to 450+ restaurants, and achieved operational metrics that impressed even global Yum executives. The IPO valuation of ₹7,500 crores on an initial investment of roughly ₹4,600 crores (plus subsequent capital infusions) represented a decent but not spectacular return—especially considering the operational heavy lifting involved.

The market's subsequent treatment of Sapphire shares reveals the challenge of being a pure-play franchisee in public markets. Unlike Jubilant FoodWorks with its Domino's monopoly, or Westlife with its McDonald's exclusivity, Sapphire faced constant comparison with Devyani—same brands, similar markets, but different valuations. Investors struggled to understand why they should pay different multiples for what appeared to be similar businesses.

VII. Sri Lanka & International Expansion: The Untold Story

The Sri Lankan operations of Sapphire Foods read like a business school case study in resilience—or perhaps denial. While the country descended into its worst economic crisis since independence in 1948, with inflation rising as result of high food prices, and pandemic restrictions in tourism which further decreased the country's income, Sapphire's Pizza Hut outlets somehow maintained their position as the country's dominant QSR brand.

Gamma Pizzakraft Lanka Pvt Ltd, a subsidiary of Sapphire Foods India Limited, has been successfully operating in Sri Lanka since 1993. This wasn't a recent adventure—Sapphire had inherited operations that predated even the Indian business, creating an interesting dynamic where the "subsidiary" had more operational history than the parent. By 2021, Sapphire had become Sri Lanka's Largest International QSR chain with 121 outlets in 52 cities.

The timing of Sapphire's IPO in November 2021 now seems either prescient or incredibly fortunate. In September 2021, the government announced an economic emergency, as the situation was further aggravated by the falling national currency exchange rate. Within months of Sapphire raising capital and the private equity firms exiting, Sri Lanka would experience currency devaluation that would have decimated returns had they waited.

The 2022 crisis tested every assumption about operating in emerging markets. Prices of most food items have been on a steady rise since the last quarter of 2021 and reached a new record high in August 2022, with the year-on-year food inflation rate at nearly 94 percent. Imagine trying to maintain QSR operations when your input costs are doubling every year, your customers' purchasing power is evaporating, and basic supplies like cooking oil and wheat are subject to rationing.

While the Sri Lanka business is delivering strong financial performance in local currency terms, the currency devaluation of LKR will have an impact while consolidating accounts at the entity level in Indian currency. This corporate understatement masks an operational nightmare. The Sri Lankan rupee lost over 80% of its value against the dollar in 2022. Every pizza sold, every piece of equipment imported, every royalty payment to Yum—all became exercises in foreign exchange gymnastics.

Yet somehow, Sapphire's Sri Lankan operations didn't just survive—they maintained market leadership. The competency and experience of the leadership team and their decades of experience in the brand/ business have enabled the business to navigate through the current turbulence. The secret was counterintuitive: while competitors retreated, Sapphire doubled down on maintaining quality and availability. When fuel shortages made delivery impossible for most restaurants, Sapphire's teams found ways to keep operating, sometimes using bicycles for delivery when petrol wasn't available.

The supply chain story is particularly remarkable. On 28 June 2022, the government suspended fuel sales to non-essential vehicles. Only buses, trains, and vehicles used for medical services and transporting food could obtain fuel. Sapphire had to completely reimagine its logistics—consolidating deliveries, working with local suppliers despite quality variations, and sometimes air-freighting critical ingredients from India at extraordinary cost to maintain menu consistency.

The human dimension of this crisis management often gets overlooked. Sapphire's Sri Lankan employees were dealing with Food inflation is alarmingly high at 57.4 percent in June 2022. Steeply increasing food prices have crippled the population's ability to put sufficient and nutritious food on the table. The majority of assessed households (61 percent) are regularly employing food-based coping strategies such as eating less preferred and less nutritious food, and reducing the amount of food they eat. Yet they continued showing up for work, serving customers, maintaining standards. The company implemented emergency support programs—providing meals, salary advances, and even helping employees' families with essential supplies.

What's fascinating is how the crisis actually strengthened Sapphire's competitive position in some ways. International competitors without deep local knowledge struggled to navigate the rapidly changing regulations, currency controls, and supply constraints. Local operators lacked the financial depth to weather the storm. Sapphire, with its Indian parent's support and operational expertise gained from operating in challenging markets, occupied a sweet spot—international standards with local resilience.

The Maldives expansion, often overshadowed by the Sri Lankan crisis, tells its own story. Operating QSR outlets on islands where everything must be imported, where the customer base fluctuates dramatically with tourism seasons, and where a single restaurant might serve an entire atoll, required completely different operational models. The fact that Sapphire persisted in these markets when pure financial logic suggested retreat speaks to a long-term vision that most public market investors struggle to appreciate.

VIII. Financial Engineering & Unit Economics

The financial architecture of Sapphire Foods reveals a business caught between the demands of rapid expansion and the realities of thin margins—a classic QSR dilemma amplified by emerging market complexities. Net profit declined 25.10% to Rs 1.79 crore in Q4 2025. For the full year, net profit declined 63.55% to Rs 19.25 crore. Sales rose 11.09% to Rs 2881.86 crore in the year ended March 2025. These numbers tell a story of growth without profitability, scale without margin expansion—the curse of the franchisee model in inflationary times.

The unit economics reveal why QSR franchising is simultaneously attractive and treacherous. KFC Revenue grew by 11% YoY, with a restaurant EBITDA margin of 17.3%. Pizza Hut revenue increased by 5% YoY, but restaurant EBITDA margin declined to 2.4%. The stark difference between KFC's healthy margins and Pizza Hut's near-breakeven operations explains Sapphire's strategic focus. Each KFC outlet functions as a cash generation machine; each Pizza Hut outlet is essentially a strategic placeholder, maintaining market presence while hoping for operational improvements.

Store-level economics in the Indian context defy global QSR norms. While a typical McDonald's in the US might generate $2-3 million in annual sales, Sapphire's outlets operate at a fraction of those volumes. The payback period for a new KFC outlet in India ranges from 3-4 years—acceptable by emerging market standards but challenging when capital costs are high and competitive intensity is increasing. The company's ability to maintain 17.3% restaurant EBITDA margins at KFC despite these constraints showcases operational excellence.

Capital allocation between brands reveals management's strategic priorities. During FY25, Sapphire opened 73 new KFC restaurants while being far more selective with Pizza Hut expansion. This isn't just following success—it's a deliberate strategy to maximize returns on invested capital. Each new KFC outlet represents approximately ₹2-2.5 crores in capital expenditure, while Pizza Hut outlets, often larger with dine-in focus, require ₹3-3.5 crores. With KFC generating nearly 7x the restaurant-level EBITDA of Pizza Hut, the math is straightforward.

Working capital management in franchising presents unique challenges. Sapphire must maintain inventory levels across hundreds of outlets, manage credit terms with suppliers, and handle the cash conversion cycle of a business where customers pay immediately but suppliers expect 30-60 day payment terms. The company's negative working capital position—essentially using supplier credit to fund operations—is both a strength and a vulnerability. It provides free financing but requires maintaining strong supplier relationships and creditworthiness.

Revenue increased YoY by 52 per cent to Rs 508 cr in Q3 FY22, and EBITDA stood at Rs 115 cr, representing a growth of 43.2 per cent YoY. Profit after tax was Rs 51 crore, compared to Rs 3 crore in Q3 FY21. These were the glory days post-IPO, when revenge spending post-COVID lockdowns drove extraordinary growth. The subsequent normalization has been brutal—a reminder that QSR economics are fundamentally tied to consumer discretionary spending.

The financial engineering employed by Sapphire goes beyond simple franchising. The company operates a hub-and-spoke supply chain model, with centralized procurement driving 5-7% cost advantages versus independent operators. Technology investments in inventory management and demand forecasting reduce waste—critical when gross margins hover around 65-70% and every percentage point of efficiency drops directly to the bottom line.

The recent financial performance reveals structural challenges. Sapphire Foods India Ltd's net profit margin fell -33.4% since last year same period to 0.25% in the Q4 2024-2025. On a quarterly growth basis, Sapphire Foods India Ltd has generated -84.18% fall in its net profit margins since last 3-months. These aren't just bad quarters; they're symptoms of a business model under pressure from multiple directions—food inflation, wage increases, and changing consumer preferences toward value offerings.

Royalty structures add another layer of complexity. Sapphire pays Yum Brands approximately 5-6% of gross sales as franchise fees, plus 4-5% for marketing fund contributions. This 10% off-the-top burden means Sapphire needs to generate exceptional operational efficiency just to achieve mediocre net margins. It's the price of playing with global brands, but in a market where local competitors operate without such burdens, it creates a permanent disadvantage.

The impairment story from Maldives operations deserves attention. Maldives business (2 KFC & Pizza Hut each, ~ 0.4% of overall revenue) has struggled for the past 1 year and sales is down by 57% YoY due to continuing geopolitical situation. This has resulted in the business incurring losses and hence as a prudent approach, we have taken an impairment (non-cash) of Rs 114 million in Q2FY25. This write-off, while small in absolute terms, represents the hidden cost of international expansion—markets that seem attractive on paper can become financial sinkholes when geopolitical or economic conditions shift.

IX. Playbook: Lessons in Franchise Operations

The Sapphire Foods playbook represents a masterclass in how private equity can create value through operational transformation rather than financial engineering alone. The consolidation of eight disparate franchise operations into a unified platform wasn't just about achieving scale—it was about creating a replicable system that could expand efficiently across diverse markets.

The private equity consolidation playbook started with a fundamental insight: the QSR industry in India was structurally inefficient. Small franchisees couldn't negotiate favorable terms with suppliers, couldn't invest in technology, couldn't attract top talent. By rolling up these subscale operators, Samara Capital and its partners didn't just buy restaurants—they bought the opportunity to professionalize an entire sector.

Multi-brand portfolio management emerged as a critical capability. Unlike single-brand operators who rise and fall with one concept's fortunes, Sapphire built expertise in managing multiple brands with different positioning, customer bases, and operational requirements. KFC appeals to protein-seeking millennials, Pizza Hut targets families and groups, Taco Bell represents future optionality. Each brand requires different marketing strategies, menu innovations, and real estate strategies, yet all must share common back-end infrastructure to achieve economies of scale.

At the current pace of expansion, Sanjay hopes to reach over 1,000 stores in the next two or three years. This aggressive expansion target isn't just about growth for growth's sake—it's about achieving the critical mass necessary to negotiate better terms with landlords, justify technology investments, and spread fixed costs across a larger base. In QSR economics, scale isn't just an advantage; it's a survival requirement.

Emerging market QSR dynamics differ fundamentally from developed markets. In the US, QSR growth comes from market share battles and same-store sales growth. In India, it's about market creation—converting street food consumers to organized QSR, teaching consumers to value consistency and hygiene over just taste and price. Sapphire's playbook recognized this distinction, investing heavily in market education and brand building rather than just store expansion.

Culture as competitive advantage sounds like management consultant speak, but in Sapphire's case, it's measurably real. The company's employee turnover rates are significantly lower than industry averages—critical in a business where service quality directly impacts customer experience. The integration of eight different organizational cultures into one cohesive unit, while maintaining operational continuity, stands as one of the most underappreciated achievements of the Sapphire story.

Supply chain localization strategies deserve particular attention. While global QSR brands typically mandate specific suppliers and ingredients, Sapphire negotiated flexibility to source locally where possible. This wasn't just about cost savings—though local sourcing can reduce costs by 20-30%—it was about supply chain resilience. When global supply chains broke during COVID, Sapphire's local supplier relationships kept restaurants operational while competitors struggled with stockouts.

The technology stack Sapphire built represents another crucial element of the playbook. Rather than relying on Yum's global systems, which were often overengineered for emerging markets, Sapphire developed India-specific solutions. Point-of-sale systems that work with intermittent internet connectivity, inventory management systems that account for power outages, delivery integration platforms that work with local aggregators—each innovation addressed real operational challenges.

The real estate strategy evolved from opportunistic to scientific. Early franchisees chose locations based on gut feel and relationships. Sapphire introduced data-driven site selection, analyzing foot traffic patterns, demographic data, competition density, and delivery radius potential. This reduced the failure rate of new outlets from industry-standard 15-20% to under 5%—each avoided closure saving ₹2-3 crores in sunk costs.

Training and development programs became a cornerstone of the operational model. Sapphire established dedicated training centers where new employees undergo intensive programs before being deployed to restaurants. This investment in human capital—unusual for QSR operators who typically view frontline staff as commoditized labor—created a differentiated service experience that customers noticed and rewarded with repeat visits.

The franchise relationship management with Yum represents a delicate balance. While Sapphire must adhere to global brand standards, it negotiated significant autonomy in areas like menu localization, pricing, and marketing. This flexibility—hard-won through demonstrating operational excellence and market knowledge—allowed Sapphire to adapt global brands to local realities without diluting brand equity.

Marketing efficiency became another competitive advantage. Rather than simply deploying Yum's global campaigns, Sapphire created India-specific marketing that resonated with local consumers. The cost per customer acquisition through targeted digital marketing was fraction of traditional media spending, allowing Sapphire to build brand awareness efficiently despite limited marketing budgets.

X. Bear vs. Bull Case & Future Outlook

The investment case for Sapphire Foods splits sharply between those who see structural challenges and those who believe in the long-term QSR opportunity in India. The bears point to undeniable financial weakness: Company has low interest coverage ratio. Company has a low return on equity of 8.23% over last 3 years. These aren't metrics that inspire confidence, especially when combined with declining profitability despite revenue growth.

The bear case starts with brutal mathematics. QSR penetration in India might be low, but that doesn't guarantee profitable growth. Competition from aggregators and cloud kitchens has fundamentally changed unit economics. Why pay rent for prime real estate when a cloud kitchen in a back alley can deliver the same product at 30% lower cost? Why invest in dine-in ambiance when 70% of orders are delivered? The asset-heavy QSR model looks increasingly antiquated in the age of asset-light digital natives.

Margin pressure from inflation represents another structural headwind. Food and labor costs, typically 60-65% of QSR revenues, have inflated faster than menu prices. Consumers resist price increases above 5-7% annually, but input costs have risen 10-12%. This margin compression isn't cyclical—it's structural, reflecting India's transition from cheap labor to middle-income economy. The days of ₹50 meals delivered profitably are ending.

Dependency on Yum brands creates strategic vulnerability. Sapphire doesn't own its brands; it rents them. If Yum decides to change strategy, implement direct operations, or squeeze franchisees harder on royalties, Sapphire has limited recourse. The recent speculation about consolidation with Devyani International suggests even Yum recognizes the current structure's limitations.

The technology disruption threat looms large. New-age brands like EatSure, Rebel Foods, and others operate cloud kitchens serving multiple virtual brands from single locations. Their unit economics are fundamentally different—no front-of-house staff, no prime real estate, no dine-in infrastructure. They can undercut traditional QSR pricing while maintaining better margins. Sapphire's response has been to increase delivery focus, but this cannibilizes higher-margin dine-in sales.

Food services market in India is projected to grow at a CAGR of 8.0% from financial year 2020 to financial year 2025, and is expected to reach Rs. 6,211 billion by financial year 2025. The bull case rests on this massive market opportunity. Even capturing a small share of incremental growth could double Sapphire's business. India's QSR penetration remains a fraction of China's or Brazil's—there's simply enormous headroom for growth.

The operational excellence track record provides confidence. Despite challenging conditions—COVID lockdowns, Sri Lankan economic crisis, inflation—Sapphire has consistently executed. Management has demonstrated ability to navigate crises, adapt to changing consumer preferences, and maintain operational standards. This execution capability is rare and valuable in emerging markets.

Multi-country diversification, often criticized as complexity, actually provides resilience. When India locked down during COVID, Sri Lanka operations continued. When Sri Lanka faced economic crisis, India operations provided stability. This portfolio approach to geography mirrors the multi-brand strategy—diversification reducing concentration risk.

The underpenetrated QSR market in India represents genuine long-term opportunity. India adds 10-12 million people to its middle class annually. Each represents a potential QSR consumer who will graduate from street food to organized chains. The demographic dividend—median age of 28 versus 38 in China and 45 in Japan—suggests decades of consumption growth ahead.

Store expansion potential remains significant. India has approximately 5,000 QSR outlets per billion population versus 50,000 in the US. Even reaching China's penetration levels would require 10x current store count. Sapphire's target of 1,000 stores represents just scratching the surface of long-term potential.

The balance sheet strength, often overlooked, provides strategic flexibility. Unlike leveraged competitors, Sapphire can weather short-term pressures without financial distress. This patient capital approach—investing through cycles rather than retreating during downturns—creates competitive advantage over time.

XI. Epilogue & Reflections

"We're a two-brand asset, but they're powerhouse brands with the scale and profitability to expand even further." Sanjay Purohit's confident assertion captures both the strength and limitation of the Sapphire Foods story. This is a business built on borrowed brands, operating in markets with structural challenges, yet somehow transforming into one of South Asia's most formidable restaurant operators.

What this story teaches about franchising in emerging markets is nuanced. Success requires more than just licensing global brands and following playbooks. It demands deep local knowledge, operational excellence that exceeds global standards, and the financial resilience to weather crises that would bankrupt operators in stable markets. Sapphire didn't succeed by being a good franchisee—it succeeded by being a better operator than the franchisor itself in these markets.

The role of private equity in restaurant consolidation emerges as more complex than simple financial engineering. Samara Capital and partners didn't just provide capital—they provided the strategic vision to consolidate a fragmented industry, the operational expertise to integrate disparate businesses, and the patience to build value over years rather than quarters. This patient capital approach, unusual in private equity, was essential given the long-term nature of QSR brand building.

Key surprises and counterintuitive insights abound. Who would have predicted that Sri Lanka, in the midst of its worst economic crisis, would maintain QSR operations while developed markets struggled? That KFC would overtake McDonald's in India? That a rollup of struggling franchisees would achieve operational metrics exceeding global standards? These outcomes challenge conventional wisdom about emerging market investments.

The unresolved tension between growth and profitability remains. Sapphire has proven it can scale—from 270 to nearly 1,000 restaurants. It has proven it can operate efficiently—maintaining standards across diverse markets. What it hasn't proven is the ability to generate consistent, attractive returns for shareholders. The stock market's lukewarm reception reflects this uncertainty.

Perhaps the most profound insight is about market creation versus market share capture. In developed markets, QSR competition is zero-sum—McDonald's gain is Burger King's loss. In India, Sapphire isn't just competing for existing QSR consumers; it's converting street food patrons, home diners, and traditional restaurant goers to the QSR format. This market creation opportunity, if successfully captured, could sustain decades of growth.

The human dimension deserves final reflection. Behind the financial metrics and strategic analyses are thousands of employees—from corporate executives to restaurant crew members—who built this enterprise. Their ability to maintain service standards during COVID lockdowns, economic crises, and operational challenges represents the true foundation of Sapphire's success. No amount of private equity capital or strategic brilliance succeeds without execution excellence at the front lines.

Looking forward, Sapphire Foods stands at an inflection point. The easy growth from store additions is ending; same-store sales growth must accelerate. The protective moat of operational complexity is eroding as competitors professionalize. The tailwind of QSR adoption is moderating as penetration increases. Success in the next chapter requires different capabilities—digital excellence, menu innovation, and perhaps most critically, the ability to generate profits while growing.

The Sapphire Foods story ultimately raises more questions than it answers. Can franchisees create sustainable value when they don't own their brands? Can operational excellence overcome structural economic challenges? Can emerging market QSR operators achieve developed market valuations? These questions extend beyond Sapphire to challenge our understanding of how global business models adapt to local realities—and whether such adaptations can create lasting value for all stakeholders involved.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube