TITAN: From Quartz Watches to Crown Jewel - India's Lifestyle Empire

I. Introduction & The Big Picture

The year is 1987. In a small watch shop in Chennai's T. Nagar, a customer holds up a sleek quartz watch with a futuristic design—something that looks like it belongs in a Tokyo showroom rather than an Indian marketplace. The shopkeeper, accustomed to selling sturdy but uninspiring HMT watches, watches nervously as the customer examines the piece. "Is this really made in India?" the customer asks, turning the watch over to reveal the TITAN logo. That moment of disbelief—that India could produce something world-class—would be repeated millions of times over the next four decades, not just with watches, but with jewellery, eyewear, and lifestyle accessories.

Today, TITAN Company Limited stands as a ₹3.1 trillion market cap colossus, generating ₹63,713 crore in revenue and commanding the aspirations of middle-class India. What started as a joint venture to make watches has morphed into something far more profound: India's definitive lifestyle empire. The numbers tell one story—85% of revenue now comes from jewellery, with an 8% market share in India's vast jewellery market. But the real story is how a company that began by challenging Swiss watchmakers ended up reorganizing entire sectors of Indian retail. The central question that haunts any analysis of TITAN is deceptively simple yet profoundly complex: How did a watch company, entering a market dominated by a government monopoly and Swiss prestige, transform itself into India's lifestyle colossus? The answer lies not in a single brilliant strategy but in a repeatable playbook of entering chaotic, unorganized markets and bringing order through trust, design, and retail excellence.

Consider the sheer audacity of TITAN's journey. The company now commands a market cap of ₹3,10,366 crore with revenue of ₹63,713 crore and profit of ₹3,713 crore. Jewellery dominates with 85% of revenue, and the company holds an 8% market share in India's jewellery market. But these numbers only hint at the deeper transformation. TITAN didn't just build a business; it rewired how Indians think about personal adornment, from the watch on their wrist to the jewellery in their wedding trousseau.

The genius of TITAN lies in recognizing a pattern that others missed: India's consumer markets were riddled with trust deficits. In watches, consumers either settled for functional but uninspiring domestic products or paid premiums for smuggled foreign goods. In jewellery, they navigated a maze of local jewelers with questionable purity standards. In eyewear, they endured clinical, joyless experiences. TITAN saw these not as separate problems but as variations of the same theme—and applied the same solution repeatedly.

This episode explores how a company born from a joint venture between the Tata Group and Tamil Nadu's government became the fifth largest integrated own brand watch manufacturer in the world, then pivoted to dominate jewellery, and ultimately built a portfolio spanning 16 brands across lifestyle categories. It's a story of patient capital meeting ambitious vision, of organizing the unorganized, and of building trust in markets where trust was the scarcest commodity.

The journey ahead takes us from the socialist constraints of 1980s India to the digital battlegrounds of today, from factory floors in Hosur to glittering showrooms in Dubai and New York. We'll examine how TITAN built moats in commodity businesses, why it succeeded where others failed, and what its astronomical valuation—trading at 26.7 times book value—tells us about India's consumption story.

II. The Tata Context & TITAN's Genesis (1984)

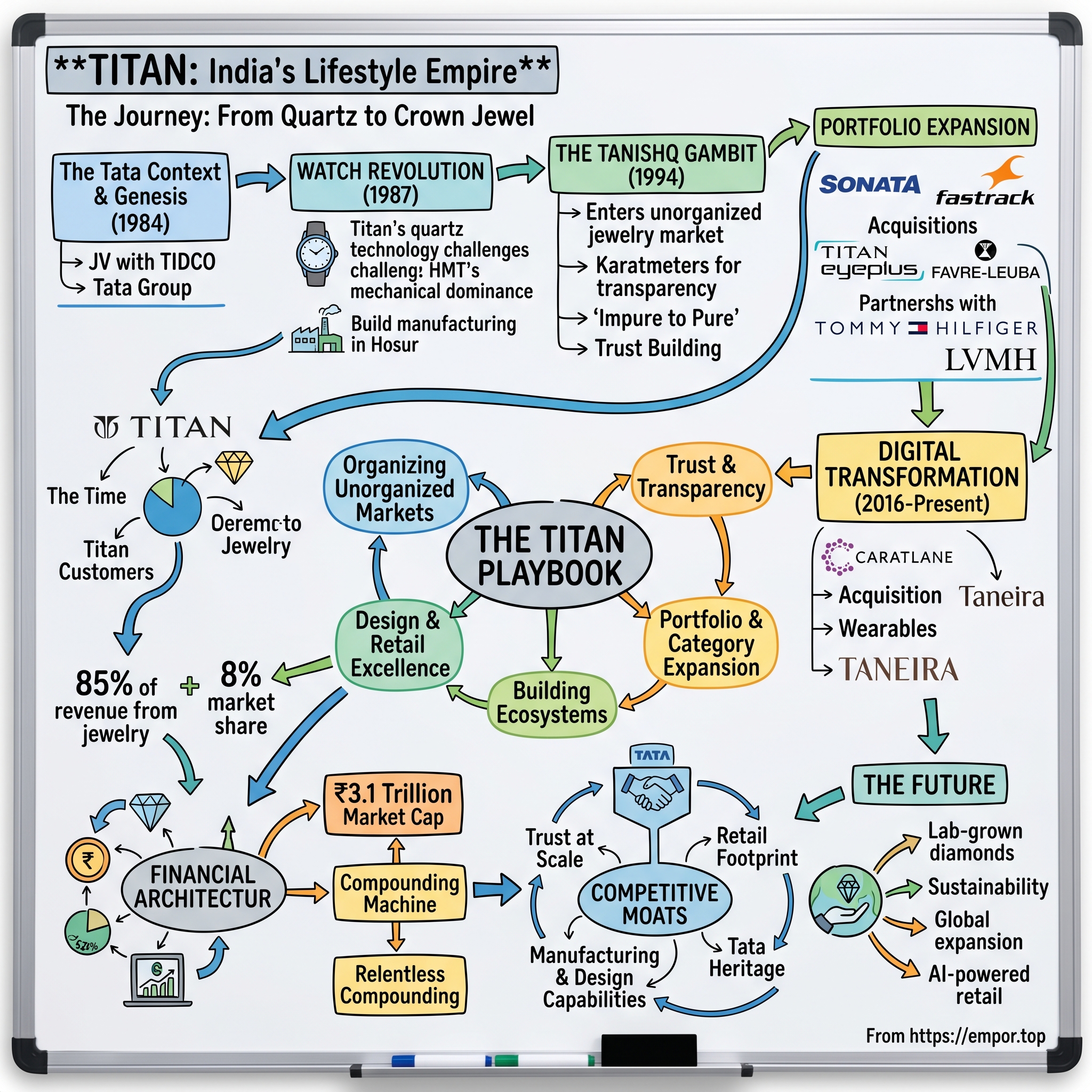

The conference room at Bombay House, the Tata Group headquarters, buzzed with skepticism in early 1984. J.R.D. Tata, then chairman of the conglomerate, listened as executives debated whether India could truly manufacture world-class watches. The prevailing wisdom was clear: Switzerland had centuries of watchmaking heritage, Japan had revolutionized quartz technology, and India had... HMT, a state-owned enterprise making functional but aesthetically challenged timepieces. Yet J.R.D., who had already proven India could build trucks, make steel, and run hotels at global standards, saw an opportunity where others saw impossibility. Established in 1984 as a joint venture between the Tata Group and Tamil Nadu Industrial Development Corporation (TIDCO), TITAN represented something far more ambitious than a simple business venture. It was an assertion that India could compete in precision manufacturing, that domestic brands could rival international ones, and that the Tata philosophy of nation-building through business could extend into new frontiers.

The partnership structure itself revealed the complexities of doing business in socialist India. Wary of opposition from civil servants in the central government, Tata's name was not associated with the project at the beginning. The initial JV agreement was entered into between TIDCO and Questar Investments, whose promoters included Xerxes Desai, who went on to become the first MD of Titan. After the central government gave its final nod, Questar was taken over by the Tatas via a rights issue. This elaborate corporate choreography—hiding the Tata name behind Questar until bureaucratic approval was secured—speaks volumes about the business environment of the era. The India that TITAN entered was a country where HMT Watches continued its monopoly in the 1980s. HMT, established in 1961 as a government-owned enterprise with technical assistance from Citizen of Japan, had become "Timekeeper to the Nation." Demand for the watches in the 1960s to the 1980s was huge, leading to waiting lists, which stretched for months. At the height of its popularity the brand was synonymous with watches in India. By 1991, HMT produced nearly seven million watches, more than all of its domestic rivals combined.

But HMT's dominance masked deep vulnerabilities. The company was wedded to mechanical watches, slow to embrace quartz technology, and hampered by the bureaucratic decision-making typical of state enterprises. HMT had been producing quartz watches in India since the 1970s but they were not popular at the time due to their relatively higher prices. Consequently HMT decided to continue its focus on producing more mechanical watches, not realizing that quartz technology was ahead of its time and would eventually dominate the market.

The choice of Tamil Nadu as TITAN's base was no accident. TIDCO, established in 1965, was looking for flagship projects that would bring manufacturing jobs to the state. The government of Tamil Nadu would own a 28% stake in TITAN—today worth roughly ₹87,000 crores, making it one of the most successful state government investments in Indian history. Even the name TITAN itself cleverly combined "Tata Industries" and "Tamil Nadu," cementing the partnership in the brand identity. But the real genius of TITAN's founding lay not in corporate structures but in human capital development. Faced with a severe shortage of skilled workers, teams of people scoured schools in small towns and remote villages in Tamil Nadu to persuade young students (17 and above) to take competitive aptitude and attitude tests; for every 100 that applied, three were selected.

Many of these workers had never left their homes and villages. TITAN didn't just hire them; it created an entire ecosystem. Titan even went to the extent of giving them housing and foster parents if the candidates were required to relocate. The company provided food, accommodation, and monthly remuneration during training—essentially building a small society around the factory in Hosur, then a sleepy town with a population of barely 20,000.

This investment in human capital would prove crucial. After three years of research, conceptualising designs and rigorous training, the first batchmakers were ready. Today, 1,600 people work in the manufacturing segment across five factories. What started as a necessity—training village youth to assemble watches—became a template for how TITAN would approach every new category: invest deeply in people, build capabilities from scratch, and create ecosystems rather than just factories.

The company also understood the importance of local pride. TITAN launched the 'Namma Tamil Nadu' watch series, paying homage to the state that had taken a leap of faith on this ambitious venture. This wasn't mere marketing; it was acknowledgment that TITAN's success was inseparable from Tamil Nadu's support. The partnership structure ensured that TITAN's chairman would always be an IAS officer nominated by the Tamil Nadu government—a unique governance model that balanced corporate efficiency with state oversight.

By 1987, when TITAN was ready to launch its first watches, it had spent three years and considerable capital without selling a single product. In an era when most businesses expected quick returns, TITAN and its backers were playing a fundamentally different game—one measured not in quarters but in decades. The stage was set for a revolution that would transform not just the watch industry but the very concept of Indian consumer brands.

III. The Watch Revolution (1984-1994)

The showrooms were packed. It was 1987, and something unprecedented was happening in Indian retail. Customers weren't just buying watches; they were clutching newspaper advertisements, pointing at specific models, demanding to see the exact timepiece from the print ads. In Mumbai's upscale stores, in Chennai's traditional markets, in Delhi's Connaught Place—everywhere, the same phenomenon repeated. Indians who had resigned themselves to functional but uninspiring HMT watches or paid premiums for smuggled foreign brands suddenly discovered a third option: world-class watches, made in India, that looked like they belonged in Geneva showrooms.

Titan Company Ltd brought about a paradigm shift in the Indian watch market when it introduced its futuristic quartz technology, complemented by international styling. This wasn't incremental improvement; it was category reinvention. While HMT continued to focus on mechanical watches, believing quartz to be a passing fad, TITAN bet everything on the technology that was revolutionizing global watchmaking.

The product strategy was audacious in its simplicity. TITAN watches blended international aesthetics with subtle Indian design elements—gold-plated dials that appealed to Indian preferences for gold, leather straps that signaled sophistication, and steel bracelets that promised durability. Each watch was a statement: India could produce products that matched global standards. The village Hosur, which had never heard of the Tatas or even remotely knew how battery-operated watches worked, was now making dazzling watches with varied features like gold plated dials with leather straps, steel and gold straps, and gold plated bracelets.

But having great products was only half the battle. Distribution in pre-liberalization India was a nightmare of permits, quotas, and entrenched networks. Traditional watch dealers were skeptical of this new entrant, comfortable with their existing HMT relationships. TITAN's response was revolutionary for its time: if the existing channels won't take you, build your own.

Titan roped in advertising ace Ogilvy and Mather who created beautiful print ads that prominently displayed these timepieces through its copy. This news spread like wildfire and it is said that consumers would walk in with newspaper cuttings to show the salesmen which watch they wanted to purchase. The advertising wasn't just selling watches; it was selling aspiration, modernity, and national pride simultaneously.

The manufacturing capabilities TITAN built were staggering for a startup. The journey began in 1987, out of a 15-acre factory located in Hosur, Tamil Nadu and three decades later, Titan stands proudly as one of the top five suppliers in the world delivering end-to-end solutions including quartz movement and mechanical watch movement for the horology industry. Within a few years, TITAN was manufacturing 15 million watches annually and had sold 150 million watches worldwide.

The brand-building playbook TITAN developed during this period would become its signature across categories. First, identify a market plagued by quality issues and trust deficits. Second, introduce technology and design that dramatically exceeds existing standards. Third, build distribution that controls the customer experience. Fourth, invest heavily in brand communication that positions the product as aspirational yet accessible.

By 1990, TITAN took another bold step. The year 1990 saw the launch of the brand's first independent showroom in Mumbai's Colaba area. It was inaugurated by Mr JRD Tata in the presence of Xerxes Desai as well as Mr AL Mudaliar, Chairman, TIDCO. This wasn't just a store; it was a temple to time, where watches were displayed like jewelry, where trained staff could explain quartz technology, where the buying experience itself became part of the product.

The competition with HMT during this period was fascinating. HMT still dominated with nearly seven million watches produced in 1991, more than all domestic rivals combined. But TITAN was winning the perception war. While HMT watches were gifts of necessity—for graduations, weddings, retirements—TITAN watches were becoming gifts of choice, symbols of modern India.

TITAN also understood segmentation before segmentation became a buzzword. After Sonata, a value brand of functionally styled watches at affordable prices, Titan Company reached out to the youth segment with Fastrack, its third brand, trendy and chic. Sonata targeted the mass market with functional watches at aggressive price points. The mainline TITAN brand occupied the premium space. This portfolio approach meant TITAN could fight HMT at every price point while maintaining distinct brand identities.

The results spoke for themselves. Titan Company Ltd is the fifth largest integrated own brand watch manufacturer in the world. The company has sold 150 million watches world over and manufactures over 15 million watches every year. In less than a decade, a company that didn't exist had become a global player, competing not just with domestic rivals but with international brands.

The watch revolution TITAN led wasn't just about replacing mechanical with quartz or domestic with stylish. It was about proving that Indian companies could innovate, that Indian manufacturing could achieve global standards, that Indian brands could command premium pricing. Every TITAN watch sold was a small victory against the narrative of Indian industrial mediocrity. The success in watches gave TITAN something invaluable: credibility. When the company announced in 1994 that it was entering the jewelry market, skeptics remembered what they had said about watches. Maybe, just maybe, TITAN could revolutionize another tradition-bound industry.

IV. The Tanishq Gambit: Entering Jewellery (1994-2005)

Bhaskar Bhat sat in his new corner office, staring at financial statements that told a story of unmitigated disaster. It was 1999, and he had just been appointed to lead TITAN's jewelry division—Tanishq—which had been bleeding money for five consecutive years. The losses were so severe that senior executives were resigning en masse, convinced that the jewelry venture was TITAN's first major strategic blunder. The board was restless, shareholders were questioning the diversification, and even within TITAN, there were whispers that Tanishq should be shut down before it damaged the parent brand.

The jewelry market TITAN entered in 1994 was nothing like watches. India's jewellery market has traditionally always been dominated by local independent jewellers, and even today around 70 percent of the market continues to be unorganised and fragmented. The relationship with the family jeweller endured for generations. Lack of transparency on purity, an ability to negotiate pricing, customised designs and personalised dealing resulted in customers having blind trust in the family jeweller and a sense of 'winning the transaction' every time they shopped. The journey into jewelry had actually begun with 18kt gold watches, but it wasn't until 1996 that Tanishq opened its first state-of-the-art factory and Karigar Park in Hosur. This facility represented something revolutionary in Indian jewelry manufacturing—organized production at scale with consistent quality standards. The term Tanishq itself was coined by Xerxes Desai by marrying the words 'Tan' meaning body and 'Nishk' meaning a gold ornament.

The initial strategy was fundamentally flawed. TITAN had decided to focus on 18-carat gold jewelry, believing Indian consumers would embrace the international standard. But gold jewellery in India was not just an ornament. Instead, it was considered an asset: a store of value and wealth. Hence, Indians always preferred the purer 22 carats over the 18 carats products. Till 2001, Titan tried absorbing Tanishq's losses which had mounted to 150 crores INR in the past 5 years.

The turning point came with what would become one of the most brilliant marketing coups in Indian business history: the Karatmeter revolution of 1997. The Karatmeter is a scientific instrument which uses X-rays to give an exact reading of the purity of gold. Due to its very high precision and fast result, X-ray analysis has been adopted by international agencies in India as part of the certification process used to hallmark gold.

Tanishq didn't just install these machines; they weaponized them. Armed with the Karatmeters, Tanishq ran an ad campaign where it offered its customers to bring their old jewellery and get its purity tested for free in their stores. The results were devastating for traditional jewelers: Almost 60% of the jewellery tested in the Karatmeters came out to be less pure than what the local jewellers had promised the customers.

But exposing the problem was only half the solution. Tanishq then launched the 'Impure to Pure' scheme—a masterstroke of strategic generosity. If a customer brought jewellery that was lower than 22 carats but higher than 19 carats pure, he/she could exchange it with Tanishq's 22-carat jewellery by just paying for the making charges. The math was brilliant: the upgrade cost Tanishq only about Rs 350 per customer, which they recovered through making charges, but the trust and loyalty generated was priceless.

The transformation under Bhaskar Bhat's leadership was remarkable. This scheme worked wonders for Tanishq. A lot of stores started doing almost 1 crore INR in daily sales. The company that McKinsey had recommended shutting down in 2002 was suddenly generating lines outside stores, with customers carrying their family jewelry to test and exchange.

The 'Tanishq Way of Life' retail programme represented another innovation. By 2005, Tanishq had built a network that would eventually grow to 400+ stores with 8,000+ retail sales officers. Each store wasn't just a point of sale but a temple to transparency, where the Karatmeter sat prominently, where every piece came with certification, where the buying experience itself became part of the value proposition.

TITAN had effectively started the concept of branded jewellery in India—a category that didn't exist before. In a market where jewelry buying was intensely personal, often involving the same family jeweler for generations, Tanishq had created a brand that people trusted more than their neighborhood goldsmith. The company achieved this not through advertising alone but through a systematic dismantling of the trust deficit that plagued the industry.

The patience required for this transformation cannot be overstated. From 1994 to 2000, Tanishq bled money while TITAN's board and shareholders questioned the strategy. The watch business was funding these losses, essentially subsidizing the creation of what would become TITAN's crown jewel. By 2005, when Tanishq finally turned the corner, it had fundamentally altered how Indians bought jewelry. The unorganized had been organized, the opaque made transparent, and a commodity had been transformed into a brand.

V. Portfolio Expansion: Building a Lifestyle Empire (1995-2015)

The boardroom at TITAN headquarters in 2005 witnessed an unusual debate. Fresh from turning Tanishq profitable after a decade of losses, the management team was proposing something radical: transform Fastrack from a sub-brand of watches into an independent lifestyle brand targeting urban youth. The finance team was skeptical—why risk diluting focus when jewelry was finally working? But CEO Bhaskar Bhat saw something others missed: TITAN's real capability wasn't making watches or jewelry; it was organizing unorganized markets and building trusted brands. Fastrack would be the proof.

The portfolio expansion that followed over the next decade wasn't random diversification—it was a systematic application of the TITAN playbook across adjacent categories. Each new venture followed the same pattern: identify a fragmented market with trust issues, introduce superior products with transparent practices, build exclusive retail experiences, and create distinct brand identities for different consumer segments.

Sonata, launched in the late 1990s, had already proven TITAN could play at different price points. Targeting the mass market with watches priced under ₹1,000, Sonata became the volume driver, selling functional watches at affordable prices while maintaining TITAN's quality standards. After Sonata, a value brand of functionally styled watches at affordable prices, Titan Company Ltd reached out to the youth segment with Fastrack, its third brand, trendy and chic. Fastrack was launched in 1998 as a sub-brand of Titan. It was spun off as an independent brand of watches targeting the urban youth in 2005. To become a fashion brand, Fastrack launched sunglasses in the same year and launched bags, belts and wallets in 2009. The transformation was remarkable—what started as a watch line became India's largest youth fashion brand, eventually claiming the title of being the largest sunglasses brand in the country.

The eyecare market presented another unorganized opportunity. In 2007, Titan established its prescription eyewear store chain called Titan Eyeplus. The Indian eyecare market lacked national players and had no real standard of optometry or service. TITAN's approach was characteristically systematic: partner with Sankara Nethralaya for training, implement 20-step zero-error eye tests by qualified optometrists, create an open-browse format that made eyewear shopping experiential rather than clinical. The division would eventually grow to 860+ stores across 384 towns and cities.

The international ambitions materialized in 2011 with a bold move. Titan acquired Swiss watchmaker Favre-Leuba in 2011 for €2 million to enter the European market. Favre-Leuba, founded in 1737, was one of Switzerland's oldest watch brands but had fallen on hard times. For TITAN, it represented not just European market access but validation—an Indian company owning a Swiss watch brand was a powerful statement about reversed colonial flows of capital and expertise. In 2013, Titan entered the fragrances segment with the brand Skinn and helmets category under the Fastrack brand. Titan Company launched the SKINN range of fine fragrances in 2013 and widened footprint in the personal lifestyle segment. The fragrances were created by world-class perfumers from Givaudan—the same house that created iconic fragrances like L'Air du Temps and Dior's J'adore. Although these perfumes are manufactured and bottled in France, every perfume is inspired by Indian stories and created after taking the Indian sensibilities into account.

The partnership strategy revealed TITAN's sophisticated approach to capabilities. In 2004, Titan signed an agreement with the Murjani Group to market and distribute the latter's Tommy Hilfiger watches in India. 2004, Titan partnered with LVMH to service the latter's watches in India through its service centres. These weren't just distribution deals; they were learning opportunities, ways to understand luxury retail and high-end service standards.

The Montblanc joint venture in 2014-2015 took this further. In 2015, Titan entered a joint venture to sell products of the Swiss luxury brand Montblanc through its retail outlets. Titan's equity share in Montblanc India Retail Private Limited is 49% and Montblanc Services B.V. holds 51%. This gave TITAN direct exposure to ultra-luxury retail, knowledge that would prove invaluable as it pushed Tanishq into higher price segments.

Each brand in the expanding portfolio served a strategic purpose. Sonata drove volumes and market penetration. Fastrack captured youth mindshare and built future customers. Tanishq generated the bulk of profits. Titan Edge showcased innovation capabilities. The international partnerships provided learning and credibility. Together, they created a portfolio that could address every segment, every price point, every occasion in an Indian consumer's life.

The manufacturing capabilities kept pace with brand expansion. TITAN's watch division was producing about 16 million watches per year, catering to customers across 32 countries. The company had 4000 employees spread across its integrated facility that included design, manufacturing and tool manufacturing. This wasn't just scale; it was integrated capabilities that few companies globally could match.

By 2015, TITAN had transformed from a watch company to a lifestyle conglomerate. The portfolio spanned watches, jewelry, eyewear, fragrances, and accessories. Each category had been entered using the same playbook: identify unorganized markets, introduce superior products, build trust through transparency, create memorable retail experiences. But the biggest test was yet to come—the digital revolution that would challenge every assumption about retail and consumer behavior.

VI. Digital Transformation & New Categories (2016-Present)

The emergency board meeting in early 2016 had one item on the agenda: CaratLane. The online jewelry startup had been burning cash, competing fiercely with other e-commerce players, and represented everything traditional jewelers feared about digital disruption. Yet TITAN's management was proposing to acquire a 62% stake for ₹357 crore. Board members who had watched TITAN painstakingly build Tanishq's offline presence over two decades questioned why they would now embrace a model that seemed to contradict everything they had built. The answer would reshape TITAN's future. In 2016, Titan acquired a 62% stake in CaratLane for ₹357 crore. At the time, CaratLane's revenues for 2015-16 were just ₹141 crore. Back in 2016, Titan's online jewellery business was negligible. As the division's CEO put it back then, "Revenues from the online medium is not even a decimal point for Tanishq, while Carat Lane is an online company."

CaratLane represented more than just an online play. Founded in 2008 to bridge the gap between exquisite jewellery meant for special occasions and everyday wear, the company had pioneered the concept of affordable, daily-wear diamond jewelry in India. Its marketplace model, working with vendors who supplied gems on request, was radically different from Tanishq's vertically integrated approach.

The transformation that followed was remarkable. In FY21, CaratLane reported its first profits. The company nearly doubled its store size within the next year. Revenue jumped 71% to ₹2,177 crore in FY23. By 2023, TITAN was so convinced of CaratLane's potential that it acquired the remaining stake for ₹4,621 crore, valuing the company at ₹17,000 crore—a 47x increase from the initial investment valuation.

Today, CaratLane stands as India's largest omni-channel jeweller, with a robust presence in more than 100 Indian cities through an extensive network of over 270+ retail stores. The integration wasn't just financial; it was strategic. CaratLane's tech-first approach influenced Tanishq's digital strategy, while Tanishq's brand trust accelerated CaratLane's offline expansion.

The wearables market presented another digital opportunity. In 2016, Titan entered the wearable devices market by introducing its smartwatch, Juxt, made through a collaboration with Hewlett-Packard. In 2017, the company launched a fitness tracker, named Gesture Band under its youth accessories brand, Fastrack. The company achieved a 7.4% market share in the wearable devices market by 2018.In 2017, Titan started its women's ethnic wear retail chain named Taneira. Conceived in 2017, Taneira was established with a vision to bring to life a symphonic medley of the old and new—an eclectic selection of contemporary designs on authentic, handwoven fibres from over hundred craft clusters across the country. The brand currently works with 200+ suppliers and has been defined by the discovery and revival of lost art forms, development of weaving clusters and artisan community.

Taneira represented TITAN applying its playbook to yet another unorganized market. The saree-making business is mostly disorganised. The management invested Rs 30 crore in building the supply chain for the first two stores, which included building relations with weavers and designers. The team travelled the length and breadth of India to bring under one roof a collection that includes mugas from Assam; cottons from Chettinad; tussars from Bhagalpur; ikats from Gujarat, Andhra Pradesh and Orissa; chikankari from Lucknow; classical Banarasi silks and kanjeevarams.

The merger of Gold Plus with Tanishq in 2018 consolidated TITAN's jewelry operations. In 2018, Titan merged its South India-focused jewellery brand Gold Plus with Tanishq. This wasn't just administrative tidiness; it was recognition that in jewelry, scale and brand concentration mattered more than portfolio diversity.

The most recent category expansion came in 2022. TITAN launched IRTH, a women's handbag brand, targeting ambitious revenue of ₹1,000 crore by FY28. This represented TITAN's confidence that its playbook could work even in categories dominated by international brands and fast fashion.

International expansion accelerated in this period. In November 2020, Titan opened its first overseas Tanishq store in Dubai. In 2023, the company entered the US market. These weren't vanity projects but strategic tests of whether TITAN's India-centric model could work globally.

The digital transformation wasn't just about new acquisitions or online sales. By FY25, 25% of sales were digitally influenced—customers researching online before buying offline, using virtual try-ons, or engaging through social media. The integration of online and offline had become seamless, with CaratLane's try-at-home service and Tanishq's virtual consultation blurring the boundaries between channels.

The numbers tell the transformation story. From a company that was primarily about watches in 2015, TITAN had become a true lifestyle conglomerate by 2024. With 38,000 people in the overall ecosystem, 16 brands, and over 2,000 retail stores, the company had successfully navigated the digital disruption that destroyed many traditional retailers. More importantly, it had proven that its core capability—organizing unorganized markets through trust and superior customer experience—remained relevant in the digital age.

VII. The TITAN Playbook: Organizing the Unorganized

In a glass conference room overlooking TITAN's Hosur factory, a team of executives studies a new market opportunity. The category is fragmented, quality standards are inconsistent, consumer trust is low, and traditional players resist change. For most companies, these would be red flags. For TITAN, they're green lights. Over four decades, the company has perfected a repeatable formula for entering and dominating such markets—a playbook so consistent that employees joke they could apply it blindfolded.

The TITAN playbook begins with a fundamental insight: India's consumer markets suffer not from lack of demand but from supply-side failures. Whether watches in 1987, jewellery in 1994, eyecare in 2007, or sarees in 2017, the pattern repeats—massive markets served poorly by fragmented, often unethical players who've never faced organized competition. TITAN's genius lies not in discovering these markets but in recognizing that the same solution works across categories.

Step one is always trust-building through radical transparency. In watches, it was offering international quality with clear pricing. In jewellery, the Karatmeter exposed widespread purity fraud. In eyecare, certified optometrists replaced untrained salespeople. In sarees, GI-tagging authenticated regional weaves. Each intervention seems category-specific but follows the same principle: make the invisible visible, the opaque transparent.

Step two involves technology and innovation as differentiators. TITAN doesn't just enter markets; it modernizes them. The company achieves 100-120% higher productivity than industry standards at its Karigar Centres through systematic training and modern equipment. When entering wearables, it didn't just import technology but collaborated with HP for local development. Even in traditional categories like sarees, technology plays a role—from inventory management systems that track thousands of SKUs to digital design tools that help weavers modernize patterns.

Step three focuses on retail excellence and experience design. TITAN doesn't just sell products; it creates destinations. A Tanishq store isn't merely a jewellery shop but a trust temple where the Karatmeter sits like an altar. A Taneira outlet showcases sarees like an art gallery. Titan Eye+ stores feel more like premium healthcare facilities than optical shops. This retail philosophy—that the experience is part of the product—predated the experience economy by decades.

Step four involves building ecosystems, not just businesses. When TITAN entered watches, it didn't just build a factory; it created vocational training programs, housing colonies, and supplier networks. In jewellery, it established Karigar Parks that formalized artisan employment. In sarees, it works with over 200 weaving clusters, providing design inputs, quality standards, and assured purchase agreements. This ecosystem approach creates competitive moats that are nearly impossible to replicate.

Step five deploys portfolio management across price points. In every category, TITAN operates multiple brands targeting different segments. In watches: Sonata for mass market, TITAN for premium, and Swiss brands for luxury. In jewellery: CaratLane for daily wear, Tanishq for occasions, Zoya for luxury. This portfolio approach allows TITAN to capture value across the entire market while maintaining distinct brand identities.

The manufacturing and operational excellence underlying this playbook is staggering. TITAN's watch division produces about 16 million watches annually with 4,000 employees across integrated facilities. The jewellery division operates multiple manufacturing units with productivity levels that set industry benchmarks. The company maintains 5,000+ retail stores across 2,200+ cities, with products available in 30+ countries.

But perhaps the most remarkable aspect of the TITAN playbook is its consistency across four decades and multiple categories. The same principles that worked in watches in 1987 work in handbags in 2022. This isn't luck or coincidence but the result of deep organizational learning. TITAN has institutionalized the process of entering unorganized markets, building trusted brands, and scaling operations.

The human capital strategy deserves special mention. TITAN employs 38,000 people directly and supports thousands more indirectly. But more than numbers, it's the company's approach to talent that stands out. From training village youth to become watchmakers to partnering with design schools for jewellery innovation, TITAN invests in creating capabilities that don't exist in the market.

The playbook also reveals TITAN's patience with profitability. Tanishq lost money for six years. CaratLane took five years to turn profitable. Taneira is still in investment mode. This patient capital approach, enabled by strong cash flows from mature businesses and the Tata Group's long-term orientation, allows TITAN to build categories rather than just enter them.

Critics might argue that the playbook is too India-specific, that it won't work in developed markets with organized retail and established brands. But TITAN's success suggests something deeper: that markets everywhere have trust deficits, that consumers universally value transparency, that superior retail experiences command premiums. The playbook isn't about India; it's about human psychology and market dynamics.

The sustainability of this approach faces new challenges. Digital natives don't have the trust deficits that TITAN historically addressed. Younger consumers value authenticity over authority, experiences over products, sustainability over scale. But TITAN's acquisition of CaratLane and digital transformation efforts suggest the playbook is evolving, not obsolete.

As TITAN looks ahead, the playbook provides both comfort and challenge. Comfort because the formula for entering new categories is proven. Challenge because each new market is more competitive, more digital, more global than the last. The question isn't whether the playbook works but whether it can evolve fast enough for the markets of tomorrow.

VIII. Financial Architecture & Performance

The numbers tell a story of relentless compounding. TITAN's market capitalization of ₹3,10,366 crore places it among India's top 20 companies, ahead of stalwarts like Maruti Suzuki and Nestle India. But the headline number obscures a more interesting narrative: how a company in mature categories like watches and jewellery maintains growth rates that would make tech startups envious.

Current metrics paint a picture of robust health: ₹3.1 trillion market cap, ₹63,713 crore revenue, ₹3,713 crore profit. The quarterly performance shows momentum continuing with revenue jumping 18.8% since last year same period to ₹15,032.00Cr in the Q4 2024-2025. The trailing twelve-month growth tells a consistent story of expansion well above India's GDP growth.

The segment concentration is both TITAN's strength and vulnerability. Jewellery contributes 85% of revenue, with the company holding an 8% market share in India's jewellery market. This concentration has intensified over the years—a decade ago, jewellery was 75% of revenue; two decades ago, it was less than 50%. The shift reflects both Tanishq's success and the relative maturity of the watch business.

The profitability metrics reveal operational excellence. Net profit jumped 12.97% year-over-year to ₹871.00Cr in Q4 2024-2025. But more impressive than absolute profits is the consistency—TITAN has delivered positive earnings growth for 15 of the last 17 years, through demonetization, GST implementation, and pandemic lockdowns.

Working capital management in the jewellery business deserves special attention. Jewellery is inherently working capital intensive—gold inventory, customer advances, and supplier credits create complex cash flow dynamics. TITAN manages this through innovative schemes like the Golden Harvest program, where customers pay monthly instalments before purchase, effectively providing interest-free working capital financing.

The capital allocation strategy reflects TITAN's evolution from a single-category manufacturer to a multi-brand conglomerate. Growth capex goes primarily to retail expansion—new stores for Tanishq, CaratLane, and Taneira. Maintenance capex supports manufacturing upgrades and technology infrastructure. M&A spending has accelerated, from the CaratLane acquisition to smaller tactical purchases. The company maintains a conservative balance sheet with minimal debt, providing flexibility for opportunistic investments.

The dividend policy remains conservative with a 0.36% yield and 29.24% payout ratio. This reflects TITAN's growth-first mentality—why return capital when you can compound it at 20%+ rates? The low dividend yield also signals management's confidence in reinvestment opportunities, a positive for long-term value creation.

The valuation metrics scream expensive by traditional measures. The stock trades at 26.7 times book value, a premium valuation even for a consumer franchise. The P/E ratio of 89x suggests the market is pricing in years of future growth. These multiples make sense only if you believe TITAN can sustain 15-20% earnings growth for the next decade—a bet on India's consumption story as much as TITAN's execution.

International revenue remains minimal despite global ambitions. Products reach 30+ countries, but international sales contribute less than 5% of revenue. This isn't necessarily negative—India's domestic market offers decades of growth runway. But it raises questions about TITAN's ability to compete globally, especially as Indian consumers become more sophisticated and demand global brands.

The financial architecture reveals strategic choices. Unlike asset-light franchising models, TITAN owns most of its retail stores, requiring significant capital but ensuring control over customer experience. Manufacturing remains largely in-house despite outsourcing trends, preserving quality control and margins. The company funds growth primarily through internal accruals rather than debt, maintaining financial flexibility.

Return metrics justify the premium valuation. Return on equity consistently exceeds 25%, remarkable for a capital-intensive retail business. Return on capital employed hovers around 30%, suggesting efficient capital deployment. These returns, sustained over decades, explain why TITAN trades at such premium multiples—the market recognizes a compounding machine.

The risk-return profile has evolved. Twenty years ago, TITAN was a turnaround story with binary outcomes. Ten years ago, it was a growth story with execution risk. Today, it's a quality compounder with valuation risk. The transformation from risky turnaround to expensive quality mirrors India's own economic evolution.

Analyst estimates suggest continued optimism. Consensus projects 18-20% earnings growth over the next three years, driven by jewellery store additions, CaratLane scaling, and category expansion. The street expects TITAN to reach ₹100,000 crore revenue by FY27, implying sustained market share gains across categories.

The financial story ultimately reflects TITAN's unique position in India's consumption landscape. It's simultaneously a play on gold prices (through jewellery), discretionary spending (through watches and accessories), and cultural evolution (through modern retail formats). This diversification within concentration—multiple ways to win within focused categories—explains both the premium valuation and sustained performance.

IX. Competitive Moats & Strategic Advantages

The moats around TITAN's business run deeper than financial statements suggest. In an era when digital disruption threatens every traditional retailer and D2C brands challenge established players, TITAN not only survives but thrives. Understanding why requires examining competitive advantages that compound over time rather than erode.

The first and most powerful moat is trust at scale. Titan's efforts are deeply rooted in the values of the Tata group, driving commitment to contribute meaningfully to society beyond business goals. In categories where purchase decisions involve significant financial and emotional investment—jewellery for weddings, watches for milestones, eyecare for health—trust becomes the primary currency. TITAN has built this trust over four decades through consistent delivery, transparent practices, and the Tata backing.

The manufacturing and design capabilities represent a tangible moat that's expensive and time-consuming to replicate. TITAN has grown to be the fifth largest integrated watch manufacturer in the world with a wide range of products and lifestyle brands. The company operates integrated manufacturing facilities for watches and jewellery, with proprietary designs and quality standards that set industry benchmarks. While competitors can outsource manufacturing, they can't replicate the quality consistency and design innovation that comes from vertical integration.

The retail footprint creates powerful network effects. With over 8,000 employees and about 38,000 in the overall Titan ecosystem, 16 brands and over 2,000 retail stores. But it's not just store count—it's store locations, trained staff, and customer relationships built over decades. A bride shopping for wedding jewellery at Tanishq isn't just buying gold; she's buying into an experience, a relationship, a lifecycle of purchases. This installed base of customers becomes a moat that deepens with time.

The portfolio approach creates strategic flexibility that single-brand competitors lack. When Tanishq faces margin pressure from gold prices, Fastrack or TITAN watches can compensate. When watch sales slow, jewellery drives growth. This diversification within focus—multiple brands in related categories—provides resilience without complexity.

Regulatory advantages, while not insurmountable, raise barriers for new entrants. TITAN's hallmarking certifications, GST compliance infrastructure, and relationships with regulatory bodies took years to build. In jewellery especially, where hallmarking is becoming mandatory, TITAN's early adoption provides competitive advantage.

The supplier ecosystem represents an underappreciated moat. TITAN doesn't just buy from suppliers; it develops them. The Karigar Parks for jewellery artisans, the weaver clusters for Taneira, the component suppliers for watches—these represent relationships and capabilities that can't be quickly replicated. New entrants must either accept higher costs or inferior quality while building similar ecosystems.

Customer acquisition costs that decrease over time create a powerful economic moat. While D2C brands spend 20-30% of revenue on digital marketing, TITAN's customer acquisition happens organically through store footfall, word-of-mouth, and lifecycle events. A customer acquired for a Fastrack watch in college becomes a TITAN watch buyer in their first job, a Tanishq customer for their wedding, and eventually a CaratLane regular for daily wear jewellery.

The data and insights accumulated over decades provide competitive intelligence that money can't buy. TITAN knows Indian consumers' jewellery buying patterns across regions, seasons, and life stages. It understands watch preferences by age, income, and occasion. This knowledge, encoded in everything from store locations to product designs, guides decisions in ways competitors can't match.

Brand equity in TITAN's categories transcends functional benefits. TITAN watches aren't just timepieces; they're coming-of-age gifts. Tanishq jewellery isn't just gold; it's wedding tradition modernized. These emotional associations, built through consistent execution and cultural integration, resist commoditization.

The talent pipeline, especially in specialized skills, creates human capital advantages. TITAN doesn't just hire jewellery designers or watchmakers; it creates them through training programs, partnerships with design schools, and apprenticeship systems. This talent development capability ensures quality while creating employee loyalty—many senior executives have spent entire careers at TITAN.

Scale economics in procurement, particularly in jewellery, provide cost advantages. TITAN's gold purchasing power, relationships with suppliers, and inventory management capabilities allow better pricing and terms than smaller competitors can achieve. In a business where 1-2% cost advantages matter, scale becomes decisive.

The innovation capability, often overlooked in traditional categories, drives differentiation. From the Karatmeter in jewellery to smart watches in wearables to GI-tagging in sarees, TITAN consistently introduces innovations that reshape categories. This isn't R&D for its own sake but innovation that solves real consumer problems.

Switching costs, while not insurmountable, create friction that favors TITAN. A Tanishq customer with years of purchase history, exchange benefits, and emotional associations doesn't easily switch to another jeweller. A company buying eyecare benefits from Titan Eye+ has integration costs that discourage switching.

The omnichannel capability, enhanced through the CaratLane acquisition, positions TITAN for digital-physical convergence. While pure-play online competitors struggle with trust in high-value categories and traditional retailers struggle with digital integration, TITAN operates seamlessly across channels.

Geographic advantages in manufacturing and sourcing provide cost benefits. The Hosur facilities benefit from Tamil Nadu's manufacturing ecosystem. The jewellery operations leverage India's gold trading infrastructure. The saree sourcing taps into centuries-old weaving clusters. These location-specific advantages are difficult for global competitors to replicate.

The moats compound rather than erode. Each new store strengthens the network effect. Each satisfied customer deepens brand equity. Each product innovation enhances capability advantages. This compounding of advantages over time explains why TITAN's competitive position strengthens rather than weakens despite intense competition.

X. Bear Case & Bull Case Analysis

Bear Case: The Risks That Keep Skeptics Awake

The valuation math has become stretched to breaking point. Trading at 26.7 times book value and with a P/E ratio of 89x, TITAN is priced for perfection. Any disappointment—a weak quarter, margin compression, slower store additions—could trigger a violent derating. History is littered with quality companies that remained great businesses while becoming terrible stocks due to valuation compression.

The jewellery concentration risk looms larger each year. With 85% of revenue from jewellery, TITAN is essentially a jewellery company with a watch and accessories portfolio. This concentration makes the company vulnerable to gold price volatility, regulatory changes in jewellery, or shifts in consumer preferences. If Indians' love affair with gold weakens—as has happened in developed markets—TITAN's entire investment thesis crumbles.

Digital disruption threatens the moats TITAN spent decades building. Younger consumers trust online reviews over brand heritage, prefer Instagram-native brands over traditional retailers, value sustainability over scale. D2C jewellery brands like GIVA and Melorra are growing rapidly with asset-light models and digital-first approaches. BlueStone raised significant capital to challenge Tanishq online. The question isn't whether digital brands will take share but how much and how fast.

Competition from online players intensifies daily. Amazon and Flipkart sell jewellery with aggressive pricing and convenience. International platforms like Etsy connect consumers directly with artisans, bypassing traditional retail. Chinese manufacturers offer fashion jewellery at price points TITAN can't match. While TITAN acquired CaratLane to address this threat, integration challenges and channel conflicts remain.

Gold price volatility creates unavoidable margin pressure. When gold prices rise rapidly, consumers defer purchases, hitting volumes. When prices fall, inventory losses hurt margins. TITAN has managed these cycles historically, but the jewellery business's increased dominance makes the company more vulnerable to gold price shocks than ever before.

Regulatory disruptions pose constant threats. Mandatory hallmarking, while beneficial long-term, creates short-term disruption. GST changes affect pricing and compliance costs. Import duty modifications impact competitive dynamics. State-level regulations on store operations add complexity. Each regulatory change, while manageable individually, cumulatively increases operational challenges.

International expansion has been slow and capital-intensive. Despite global ambitions, international revenue remains negligible. The Dubai and US store openings are more symbolic than substantial. Unlike Indian IT or pharma companies that conquered global markets, TITAN remains overwhelmingly India-dependent. This geographic concentration limits growth potential and increases country-specific risk.

Management succession poses medium-term uncertainty. The current leadership team has delivered exceptional results, but key executives are approaching retirement. While TITAN has strong bench strength, leadership transitions in complex retail businesses often bring execution challenges. The Tata Group's own leadership changes add another layer of uncertainty.

Category maturation in watches limits growth potential. The watch business, TITAN's origin story, faces structural headwinds. Smartphones have made watches less essential for timekeeping. Smartwatches cannibalize traditional watches. Fashion watches face intense competition from international brands. While TITAN has managed decline better than peers, the category's challenges are irreversible.

New category execution remains unproven. IRTH handbags, Taneira sarees, and fragrances are still subscale. The success rate in new categories is mixed—for every Tanishq, there might be multiple failures. The capital and management bandwidth invested in new categories could dilute focus on core businesses.

Bull Case: The Opportunity That Excites Believers

India's consumption story has barely begun. With per capita income still under $3,000, India's consumption boom lies ahead, not behind. As millions enter the middle class, demand for branded jewellery, watches, and accessories will explode. TITAN, with its established presence and brand trust, is perfectly positioned to capture this growth. The company's 8% jewellery market share could double as the organized sector grows from 30% to 60% penetration.

The organized retail penetration opportunity is massive. In jewellery, 70% of the market remains unorganized. In eyecare, organized players have less than 20% share. In sarees, organized retail is under 5%. TITAN's playbook of organizing unorganized markets has decades of runway. Each percentage point of market share gain in jewellery alone adds thousands of crores in revenue.

Ambitious growth targets suggest management confidence. The ₹1,000 crore handbag revenue target by FY28 implies new category success. Store addition plans—50+ Tanishq stores, 40+ CaratLane stores annually—indicate expansion momentum. International market entry, while early, opens new growth avenues. Management's track record of achieving ambitious targets provides credibility.

Digital transformation creates omnichannel advantages. In FY25, the company generated 25% digitally influenced sales. The CaratLane acquisition brings digital DNA into TITAN. The combination of TITAN's offline trust and CaratLane's online innovation creates a powerful omnichannel proposition that neither pure-play online nor traditional offline competitors can match.

International expansion potential remains untapped. The Indian diaspora globally represents a $100+ billion market opportunity. TITAN's brands resonate with Indians worldwide. The Dubai store's success demonstrates potential. As TITAN builds international operations capabilities, global expansion could surprise positively.

Adjacent category opportunities abound. TITAN has successfully entered watches, jewellery, eyecare, fragrances, and sarees. Each category entry refined the playbook. Potential categories—cosmetics, apparel, leather goods—offer similar dynamics of unorganized markets awaiting organization. TITAN's brand equity and retail presence provide launch advantages.

The demographic dividend favors TITAN disproportionately. India's median age of 28 means decades of consumption growth ahead. Young consumers entering life stages—first job, marriage, parenthood—trigger TITAN product purchases. The demographic pyramid ensures customer flow for decades.

Premiumization trends benefit TITAN's positioning. As incomes rise, consumers upgrade from unbranded to branded, from functional to aspirational. TITAN's portfolio from Sonata to Swiss watches, from CaratLane to Zoya, captures the entire premiumization journey. The margin expansion from premiumization offsets volume pressures.

Sustainability and ethical sourcing become competitive advantages. Younger consumers value responsible brands. TITAN's certified sourcing, artisan development, and sustainability initiatives resonate with conscious consumers. As ESG considerations influence purchase decisions, TITAN's four-decade track record provides authenticity that new brands can't match.

Technology integration in retail enhances competitive position. AR try-ons for jewellery, AI-powered recommendations, virtual consultations—TITAN is investing in technology that enhances rather than replaces physical retail. This tech-enabled human touch creates experiences pure-play digital or traditional players can't replicate.

The network effects strengthen with scale. Each new store makes the next store more valuable. Each new customer makes acquiring the next customer easier. Each new product makes the portfolio stronger. These network effects, already powerful, accelerate as TITAN scales.

Cultural tailwinds support TITAN's categories. Indian weddings are becoming grander, driving jewellery demand. Fashion consciousness is increasing, supporting watches and accessories. Health awareness is growing, benefiting eyecare. These cultural shifts align with TITAN's portfolio.

The Balanced View

The truth likely lies between extremes. TITAN is neither as vulnerable as bears suggest nor as invincible as bulls believe. The valuation is stretched but perhaps justified by quality and growth. The concentration risk is real but manageable given jewellery market dynamics. Digital disruption is a threat but also an opportunity TITAN is addressing.

For investors, the key question isn't whether TITAN is a good business—it demonstrably is—but whether it's a good investment at current valuations. The answer depends on time horizon, risk tolerance, and belief in India's consumption story. Short-term investors might find better risk-reward elsewhere. Long-term investors might view temporary valuation concerns as irrelevant given the compounding potential.

The bear case centers on valuation and disruption. The bull case rests on execution and expansion. History suggests betting against TITAN has been costly. Future suggests the easy gains are behind us. The investment decision ultimately comes down to whether you believe TITAN can continue organizing the unorganized profitably for another decade.

XI. The Future: What's Next for TITAN

The gemologist holds up a diamond that sparkles identically to a natural stone but costs 70% less. It's lab-grown, created in a reactor rather than mined from the earth, and it represents perhaps the biggest disruption facing TITAN's jewellery business. In TITAN's boardroom, executives debate not whether to embrace lab-grown diamonds but how quickly and at what scale. The decision will shape TITAN's next decade.

Lab-grown diamonds embody the disruptions ahead. Younger consumers, especially in the West, increasingly prefer them for ethical and environmental reasons. The technology is improving rapidly, costs are plummeting, and quality is indistinguishable from natural diamonds. For TITAN, which built Tanishq on trust and authenticity, lab-grown diamonds present a philosophical challenge. Embrace them and risk cannibalizing high-margin natural diamond sales. Ignore them and risk losing relevance with younger consumers.

The sustainability and ethical sourcing imperatives go beyond diamonds. Gen Z consumers scrutinize supply chains, carbon footprints, and labor practices. They want to know where gold is sourced, how artisans are treated, what happens to old jewellery. TITAN's four-decade track record of ethical practices provides credibility, but past reputation won't suffice. The company needs transparent, verifiable, continuous demonstration of sustainable practices.

Gen Z and millennial consumption patterns challenge every assumption TITAN has held. They rent rather than own, experience rather than possess, share rather than hoard. The traditional Indian model of accumulating gold jewellery as investment seems antiquated to a generation that invests in crypto and values minimalism. TITAN must reimagine its value proposition for consumers who might wear a Tanishq piece to a wedding but would never buy it.

Technology integration in retail will separate winners from losers. Virtual try-ons using AR, AI-powered personal styling, blockchain for supply chain transparency, NFTs for digital collectibles—these aren't futuristic concepts but current expectations. TITAN must integrate technology seamlessly while maintaining the human touch that differentiates its retail experience. The challenge is making technology invisible while making its benefits obvious.

Global luxury brand competition intensifies as India becomes attractive to international players. Cartier, Tiffany, and Bulgari are expanding aggressively in India. They bring centuries of heritage, global design capabilities, and luxury cache that TITAN can't match. While TITAN dominates the mass premium segment, the luxury segment—where margins and growth are highest—faces fierce competition.

New category expansion possibilities seem endless but require discipline. The success in watches, jewellery, and eyecare creates temptation to enter every lifestyle category. Cosmetics, apparel, leather goods, home decor—each seems logical given TITAN's retail presence and brand equity. But each new category dilutes focus, requires new capabilities, and risks the core business. The selection and sequencing of new categories will determine whether TITAN remains focused or becomes a conglomerate.

The next ₹10 trillion market cap journey requires different capabilities than the first ₹3 trillion. The growth ahead must come from new sources—international markets, new categories, digital channels, younger consumers. Each requires capabilities TITAN is building but hasn't mastered. The company that conquered India's traditional retail market must now conquer India's digital natives and global citizens.

Artificial intelligence will reshape retail in ways we're only beginning to understand. Predictive analytics for inventory management, personalized marketing at scale, automated customer service, dynamic pricing—AI applications will separate efficient retailers from the inefficient. TITAN's data advantage from millions of transactions provides training data for AI, but leveraging this requires technical capabilities traditionally outside TITAN's competence.

The metaverse and digital assets present opportunities and threats. Digital fashion, virtual jewellery, NFT collectibles—these might seem irrelevant to physical retailers, but they represent how younger consumers think about identity and status. TITAN must decide whether to participate in digital worlds or risk becoming irrelevant to digital natives.

Climate change will impact TITAN's business in unexpected ways. Gold mining becomes more difficult and expensive as environmental regulations tighten. Store operations face pressure to reduce energy consumption. Supply chains must adapt to extreme weather events. Consumers increasingly factor climate impact into purchase decisions. TITAN's response to climate change will affect both operations and brand perception.

The Chinese manufacturing challenge looms large. Chinese manufacturers are moving up the value chain from cheap fashion jewellery to sophisticated designs. They combine manufacturing scale, technology adoption, and aggressive pricing in ways Indian manufacturers struggle to match. TITAN's made-in-India positioning provides some protection, but quality and price matter more than origin to many consumers.

Demographic shifts create new customer segments. Single women buying jewellery for themselves rather than waiting for gifts. Men interested in jewellery beyond watches. Senior citizens with disposable income and time for experiences. Same-sex couples seeking wedding jewellery. Each segment requires different products, marketing, and retail approaches.

The healthcare convergence in eyecare presents expansion opportunities. Eye testing leads to health screening leads to wellness services. Titan Eye+ could evolve from optical retail to health services, leveraging store infrastructure and customer trust. This adjacent expansion leverages existing capabilities while opening new revenue streams.

Subscription and service models will complement product sales. Jewellery rental for occasions, watch servicing subscriptions, eyecare memberships—recurring revenue models provide predictability and deepen customer relationships. TITAN's installed base of customers provides a natural subscription opportunity, but execution requires different capabilities than transaction retail.

The partnership ecosystem will become more complex and critical. Technology partnerships for digital capabilities, brand partnerships for global expansion, supplier partnerships for sustainability, startup partnerships for innovation—TITAN must become a platform that orchestrates partnerships rather than a company that does everything internally.

The future ultimately depends on TITAN's ability to balance continuity with change. The core capabilities—building trust, organizing markets, retail excellence—remain relevant. But their application must evolve for digital natives, global markets, and new categories. TITAN must become a 100-year company that acts like a 10-year startup—maintaining institutional wisdom while embracing entrepreneurial energy.

XII. Key Lessons & Takeaways

The TITAN story, stripped of its specifics, reveals universal principles about building enduring businesses. These lessons transcend industries and geographies, offering insights for entrepreneurs, investors, and executives navigating their own market opportunities.

Patient Capital and Long-Term Thinking

TITAN's journey demonstrates that transformative businesses require patient capital and long-term thinking. Tanishq lost money for six years before turning profitable. CaratLane took five years to reach profitability. Taneira is still in investment mode. This patience—enabled by strong cash flows from mature businesses and the Tata Group's philosophy—allowed TITAN to build categories rather than just enter them. The lesson: category creation takes time, and companies that measure success in quarters will lose to those that measure in decades.

The Power of Trust in Consumer Brands

In an age of performance marketing and growth hacking, TITAN's success reminds us that trust remains the ultimate moat in consumer businesses. Trust isn't built through advertising but through consistent delivery over time. The Karatmeter didn't just test gold purity; it demonstrated TITAN's commitment to transparency. Every certified diamond, every zero-error eye test, every genuine leather strap builds trust incrementally. The compound effect of millions of trust-building interactions creates a moat that no amount of venture capital can replicate.

Organizing Unorganized Markets as a Strategy

TITAN's repeatable success across categories reveals a powerful strategy: organizing unorganized markets. The playbook—identify fragmented markets with trust deficits, introduce superior products with transparent practices, build exclusive retail experiences, create distinct brands for different segments—works across categories. This isn't about disruption in the Silicon Valley sense but about bringing order to chaos, standards to variability, trust to suspicion.

Portfolio Approach to Growth

TITAN's multi-brand strategy within categories provides resilience and growth options. Rather than stretching single brands across segments, TITAN creates distinct brands with clear positioning. Sonata doesn't dilute TITAN watches. CaratLane doesn't cannibalize Tanishq. This portfolio approach requires more investment and complexity but creates strategic flexibility and market coverage that single brands can't achieve.

Balancing Tradition with Innovation

TITAN succeeds by respecting tradition while embracing innovation. Tanishq honors Indian jewellery traditions while introducing modern designs. Taneira celebrates handloom heritage while applying contemporary retail. This balance—neither rejecting the past nor resisting the future—resonates with consumers navigating their own tradition-modernity tensions.

The Tata Way of Doing Business

TITAN's success is inseparable from its Tata heritage, with efforts deeply rooted in the values of the Tata group, driving commitment to contribute meaningfully to society beyond business goals. This isn't corporate social responsibility as marketing but business as social contribution. The decision to train village youth, develop artisan communities, support weaving clusters—these create shared value that benefits society while building competitive advantages.

Vertical Integration in the Right Places

While the business world celebrates asset-light models, TITAN demonstrates the value of selective vertical integration. Manufacturing watches and jewellery in-house ensures quality control. Operating retail stores directly guarantees customer experience. Training artisans creates capability advantages. The lesson: own what matters for differentiation, outsource what doesn't.

Building Ecosystems, Not Just Businesses

TITAN doesn't just build businesses; it builds ecosystems. The Karigar Parks for jewellers, weaver clusters for Taneira, supplier networks for watches—these ecosystems create mutual dependencies that benefit all participants. This ecosystem approach creates competitive moats while contributing to economic development.

The Importance of Retail Excellence

In an increasingly digital world, TITAN proves that physical retail still matters when done right. But retail excellence isn't about store count or square footage. It's about creating experiences that justify the journey, knowledge that adds value, relationships that endure. TITAN stores aren't points of sale but theaters of aspiration.

Timing Market Entry

TITAN's entry timing across categories reveals strategic patience. The company didn't rush into jewellery when flush with watch success but waited until it had learned retail. It didn't immediately launch online but acquired CaratLane when digital capabilities were critical. This patient timing—entering markets when ready, not when hot—increases success probability.

Managing Stakeholder Expectations

TITAN's ability to manage diverse stakeholders—government partners, public shareholders, employees, suppliers, customers—while maintaining strategic focus is remarkable. The Tamil Nadu government ownership could have created political interference. Public listing could have encouraged short-termism. Instead, TITAN aligned stakeholders around long-term value creation.

The Compound Effect of Incremental Improvements

TITAN's success comes not from revolutionary breakthroughs but from thousands of incremental improvements. Better store layouts, improved training programs, refined designs, enhanced systems—each improvement seems minor but compounds over decades. This Japanese-style continuous improvement, applied consistently, creates insurmountable advantages.

Brand Building in the Indian Context

TITAN demonstrates how to build aspirational yet accessible brands in India. The brands are modern but not Western, premium but not exclusive, global in quality but Indian in soul. This positioning—speaking to Indian aspirations without abandoning Indian values—resonates across demographics.

The Value of Corporate Heritage

In a world obsessed with startups, TITAN shows the value of corporate heritage. Four decades of operations create institutional knowledge, customer relationships, supplier networks, and brand equity that money can't buy. This heritage, properly leveraged, provides competitive advantages that new entrants can't replicate.

Evolution vs. Revolution

TITAN evolved rather than revolutionized markets. It didn't destroy traditional jewellers but organized them. It didn't eliminate watch dealers but upgraded them. This evolutionary approach faces less resistance, creates fewer enemies, and builds more sustainable advantages than revolutionary disruption.

The ultimate lesson from TITAN is that building enduring businesses requires more than strategy and capital. It requires patience to build trust, discipline to maintain focus, wisdom to balance competing demands, and courage to invest through uncertainty. These qualities, more than any specific tactic or technology, explain why TITAN transformed from a watch manufacturer to India's lifestyle empire.

For investors, TITAN teaches that quality compounds but valuation matters. For entrepreneurs, it demonstrates that organizing unorganized markets creates enormous value. For executives, it shows that sustainable success comes from building institutions, not just businesses. For India, it proves that domestic companies can build global-quality brands.

The TITAN story continues to unfold. New chapters on digital transformation, international expansion, and category evolution are being written. But the principles that guided the first ₹3 trillion in value creation will likely guide the next ₹10 trillion. In a business world obsessed with disruption and revolution, TITAN reminds us that patient execution of proven principles, adapted thoughtfully to changing contexts, creates the most enduring value.

As we close this exploration of TITAN's journey, one truth emerges clearly: great businesses aren't built in quarters or even years but in decades of consistent execution, continuous learning, and relentless focus on customer value. TITAN's transformation from a watch company to India's lifestyle empire isn't just a business success story—it's a masterclass in building institutions that endure.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube