Trent Limited: India's Fast Fashion Revolution

I. Introduction & Cold Open

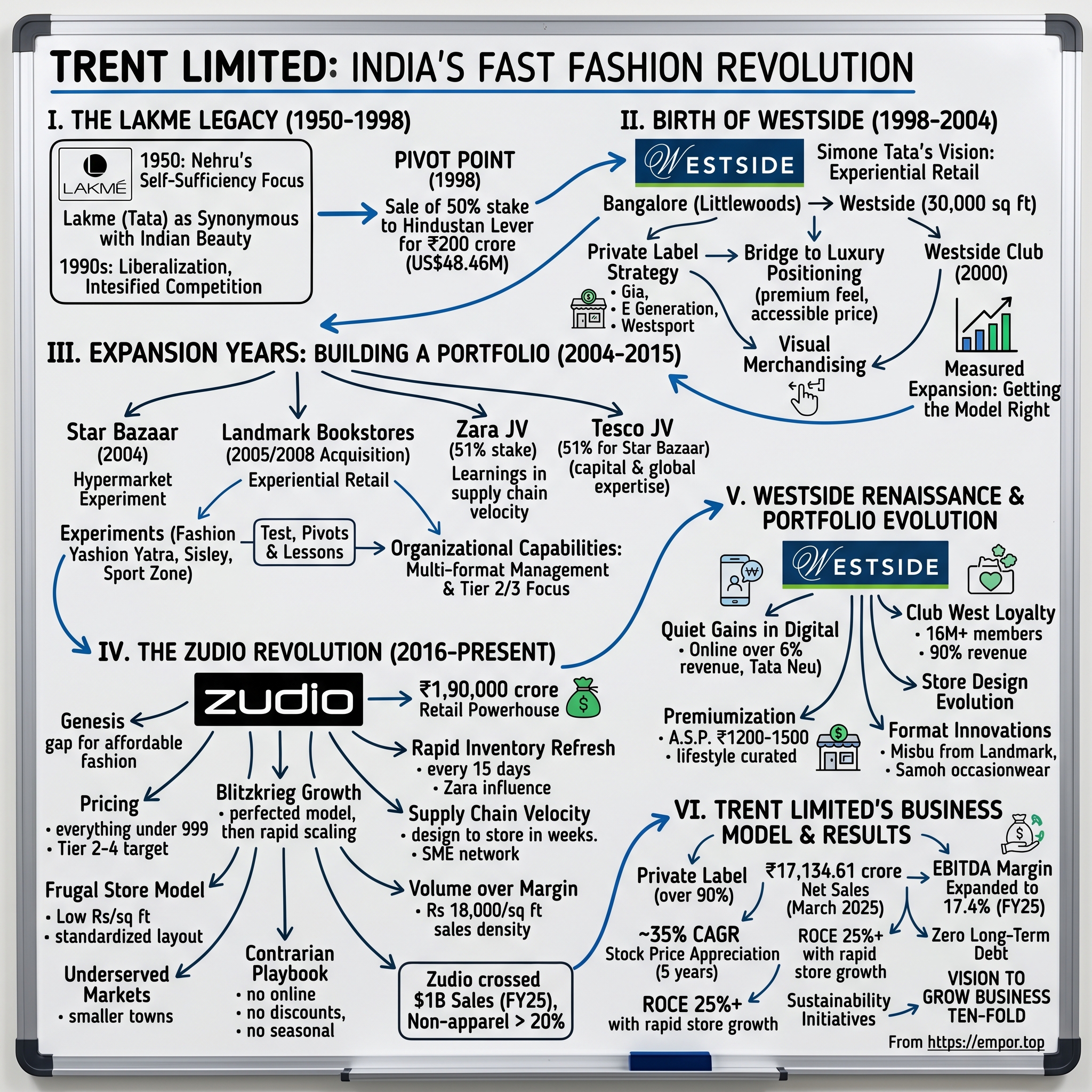

The Indian retail landscape tells many stories of ambition and failure, but few are as compelling as Trent Limited's transformation from a cosmetics divestment into a ₹1,90,000 crore retail powerhouse. As of March 2025, Zudio had 765 stores across 235 cities, growing at a pace that would make even global fast fashion giants envious. In FY25, Zudio crossed a billion dollars in sales with lifestyle, and non-apparel accounting for over 20% of the revenues.

Here's the paradox that confounds traditional retail wisdom: Zudio operates without an online presence, offers no discounts, and doesn't follow seasonal trends. Yet it has become the fastest-growing fashion retail chain in India, opening stores at a breathtaking pace while maintaining impressive unit economics. This accelerated expansion has had a direct and substantial impact on the company's revenue. Trent's revenue has surged, exhibiting a robust CAGR of 34% over the last five years.

The numbers tell only part of the story. Behind Trent's success lies a contrarian playbook that challenges every assumption about modern retail. While competitors chase online dominance and seasonal collections, Trent has built its empire on physical stores, everyday fashion, and an obsessive focus on value. This is not just another retail success story—it's a masterclass in understanding India's evolving consumer psyche and building for Bharat, not just the metros.

What makes Trent's journey particularly fascinating is its origin story. Born from the sale of Lakmé Cosmetics to Hindustan Lever, the company emerged with ₹200 crore and a vision that would reshape Indian retail. From that modest beginning, Trent has created multiple successful formats, survived the e-commerce onslaught, and emerged as one of India's most valuable retail companies. The stock has been an exceptional performer, with the stock price appreciating at ~35% CAGR in the last five years, creating enormous wealth for shareholders who believed in the physical retail story when everyone else was betting on digital.

Today, Trent operates over 1,000 stores across its formats, serves more than 100 million customers annually, and continues to expand at a pace that defies conventional retail wisdom. The company's ability to generate high returns on capital while maintaining rapid growth has made it a darling of both retail enthusiasts and financial markets. Yet, as we'll explore, the path here wasn't straightforward, and the road ahead presents both enormous opportunities and significant challenges.

II. The Lakme Legacy & Tata Context

The story of Trent Ltd begins with a historical backdrop in post-independence India. Around 1950, India's Prime Minister, Jawaharlal Nehru, was focused on reducing foreign exchange expenditure and promoting self-sufficiency across various sectors. At that time, the Indian market was heavily reliant on imported cosmetics, leading to a substantial outflow of foreign exchange.

This economic nationalism created the perfect conditions for Indian brands to flourish. The Tata Group, always attuned to national priorities, had built Lakmé into one of India's most successful cosmetics brands over nearly five decades. Named after the French opera by Léo Delibes, Lakmé had become synonymous with Indian beauty, pioneering everything from the country's first fashion shows to establishing beauty salons across major cities.

By the late 1990s, however, the Indian economy had liberalized, and global competition was intensifying. The Tatas faced a strategic crossroads with Lakmé. The cosmetics business, while successful, required significant capital investment to compete with multinational giants entering the Indian market. Meanwhile, the group sensed an even bigger opportunity emerging in organized retail—a sector that was virtually non-existent in India at the time.

In 1998, the Tatas sold off their 50% stake in Lakmé Cosmetics to Hindustan Lever for ₹200 crore (US$48.46 million), and created Trent with the proceeds from the sale. Simone Tata, the chairperson of Lakmé, went on to head Trent. This wasn't just a financial transaction; it was a strategic pivot that would define the next chapter of Tata's consumer business ambitions.

Simone Tata, the Swiss-born wife of Naval Tata, brought a unique perspective to the venture. Having successfully built Lakmé's retail presence through exclusive stores and salons, she understood the importance of creating experiential retail environments. Her vision for Trent wasn't just about selling products—it was about creating destinations where Indian consumers could discover global trends adapted for local sensibilities.

The timing of this transformation was crucial. India in 1998 was at an inflection point. Economic liberalization had created a growing middle class with disposable income and aspirational consumption patterns. Yet, the retail infrastructure remained largely traditional—dominated by small, unorganized players with limited product ranges and inconsistent quality. The opportunity to create modern retail formats was enormous, but so were the challenges.

The Tata Group's backing provided more than just financial muscle. It brought credibility, access to prime real estate through group companies, and most importantly, a long-term perspective that would prove crucial in the capital-intensive, slow-burn business of physical retail. Unlike many entrepreneurs who would enter and exit Indian retail over the next two decades, the Tatas were playing an infinite game.

The choice to focus on apparel and lifestyle wasn't accidental. The team recognized that fashion retail had several advantages: high gross margins, frequent purchase cycles, and the ability to build private labels that could offer both differentiation and better economics. Moreover, apparel retail allowed for creativity and constant newness—elements that would become central to Trent's strategy.

The transition from cosmetics to retail also reflected a deeper understanding of Indian consumer evolution. While Lakmé had educated Indian women about beauty and self-expression, Trent would democratize fashion, making contemporary styles accessible to a much broader audience. This mission—to bring affordable, aspirational fashion to Indian consumers—would remain constant even as the company evolved through different formats and strategies.

The initial capital from the Lakmé sale might have seemed modest for launching a retail revolution, but it forced discipline and focus. Every store opening, every inventory decision, and every hiring choice had to be carefully considered. This capital constraint, rather than being a limitation, instilled a culture of efficiency and innovation that would become Trent's hallmark.

As 1998 drew to a close, the pieces were in place. The capital was secured, the leadership was committed, and the market opportunity was clear. What remained was execution—turning vision into reality in a market where modern retail was still an alien concept for most Indians. The first Westside store would soon open its doors, marking the beginning of a retail journey that would span decades and transform how Indians shop for fashion.

III. Birth of Westside: The Foundation Years (1998-2004)

The company began operations in 1998, after acquiring the only store of Littlewoods in Bangalore and renaming the store "Westside". The choice of Bangalore as the starting point was strategic—the IT capital of India had a young, educated, and increasingly affluent population that was receptive to new retail concepts. The acquired Littlewoods store gave Trent a ready platform to experiment with its vision of modern Indian retail.

The early Westside stores were revolutionary for their time. Spanning 15,000 to 30,000 square feet, they offered an unprecedented shopping experience in India. Air-conditioned environments, organized displays, trial rooms with proper lighting, and courteous staff trained in customer service—these might seem basic today, but in 1998, they represented a quantum leap from the traditional retail experience Indians were accustomed to.

The private label strategy emerged as Westside's defining characteristic from day one. Rather than simply aggregating other brands, Trent chose to design and develop its own labels in-house. This wasn't just about better margins; it was about control—control over design, quality, pricing, and most importantly, the ability to respond quickly to Indian consumer preferences. Labels like Gia for women's ethnic wear, Westsport for activewear, and E Generation for youth fashion were created to cater to specific customer segments.

Building these private labels required capabilities that didn't exist in Indian retail at the time. Trent had to create design teams that understood both global trends and Indian sensibilities. They needed to develop supply chains that could deliver quality at accessible price points. Most challenging of all, they had to educate consumers to trust store brands in a market where branded meant national or international labels.

The merchandising philosophy that emerged during these foundation years would define Trent for decades to come. The company adopted what they called the "bridge to luxury" positioning—offering products that looked and felt premium but were priced accessibly. A Westside shirt might have the design elements of international brands but at a third of the price. This sweet spot between aspiration and affordability would become Trent's signature.

Store design played a crucial role in establishing Westside's identity. Each store was laid out to encourage discovery, with clear sections for different categories but enough flexibility for cross-shopping. The emphasis on visual merchandising—something largely absent in Indian retail then—helped products sell themselves. Window displays were changed regularly, mannequins were dressed to inspire complete looks, and the stores maintained a consistent aesthetic that made them instantly recognizable.

The human element was equally important. Trent invested heavily in training its store staff, importing best practices from international retail but adapting them for Indian contexts. The goal wasn't aggressive selling but rather helpful assistance. Staff were trained to understand products, suggest combinations, and most importantly, give customers space to browse—a novel concept in a market where shopkeepers traditionally showed products from behind counters.

Technology adoption, while modest by today's standards, was progressive for its time. Westside was among the first Indian retailers to implement proper inventory management systems, use barcoding for all products, and maintain centralized databases of sales patterns. This data-driven approach, unusual in Indian retail then, helped optimize inventory and identify trending products quickly.

The challenges during these early years were immense. Real estate was expensive and difficult to secure, especially in prime locations. Mall culture was nascent, and standalone stores required significant investment in infrastructure. Suppliers were skeptical of private label strategies and needed constant hand-holding to maintain quality standards. Perhaps most challenging was changing consumer behavior—convincing Indians that shopping could be a leisure activity, not just a functional necessity.

Between FY18 and FY23, this measured approach gave way to a more robust expansion, with Trent's store count more than tripling from 147 to 566 within a mere five years. But in these foundation years, growth was deliberately measured. Trent opened only a handful of stores annually, focusing on getting the model right rather than rapid expansion. Each new store was a learning laboratory, with lessons from customer feedback, sales patterns, and operational challenges incorporated into the next opening.

The financial performance during these early years was modest but encouraging. While the company wasn't generating significant profits, same-store sales growth was healthy, and customer retention rates were high. The Westside Club, launched in 2000, began building a loyal customer base that would provide the foundation for future growth. Members received exclusive previews, special discounts, and personalized communication—creating an emotional connection beyond transactional relationships.

By 2004, Westside had established itself as a recognized brand in Indian retail. With about 20 stores across major cities, it had proven that Indians were ready for modern retail formats. The private label strategy was working, with over 85% of sales coming from in-house brands. Customer satisfaction scores were high, and the brand had developed a distinctive identity in a market that was beginning to attract serious competition.

The success of Westside during these foundation years validated several hypotheses. First, Indian consumers were willing to pay for better shopping experiences. Second, private labels could compete with established brands if backed by quality and design. Third, physical retail in India had enormous potential despite the challenges of real estate and infrastructure. These lessons would prove invaluable as Trent prepared to expand its portfolio beyond the flagship Westside format.

As 2004 ended, Trent stood at another inflection point. The single-format strategy had worked well, but the Indian retail opportunity was too large and diverse for one concept to capture. The company was ready to experiment with new formats, each targeting different customer segments and shopping occasions. The next phase of growth would test Trent's ability to manage multiple brands while maintaining the operational excellence that had become its hallmark.

IV. The Expansion Years: Building a Portfolio (2004-2015)

Trent operated only Westside stores until 2004, when it opened its first Star Bazaar hypermarket in Ahmedabad. This marked a fundamental shift in Trent's strategy—from fashion-focused retail to multi-format operations. The hypermarket format represented both an opportunity and a challenge. While fashion retail had proven successful, the grocery and general merchandise space offered significantly larger market potential but with different economics and operational requirements.

Star Bazaar was conceptualized as a hypermarket that would bring organized retail to the food and grocery segment. The format combined groceries, fresh produce, household items, and general merchandise under one roof, spanning 30,000 to 50,000 square feet. The vision was to offer the convenience of one-stop shopping with the trust and quality assurance of the Tata brand. However, the hypermarket business proved to be far more complex than fashion retail, with thin margins, high wastage in fresh produce, and intense competition from local kirana stores that offered home delivery and credit.

In 2005, Trent acquired a 76% controlling stake in Landmark Bookstores, a Chennai-based privately owned books and music retailer, and completed 100% acquisition in April 2008. Landmark brought with it a different customer segment—educated, affluent consumers who valued intellectual and cultural products. The chain of bookstores, with their coffee shops and event spaces, had created community hubs in cities like Chennai and Bangalore. For Trent, this acquisition represented an entry into experiential retail and an opportunity to diversify beyond fashion and groceries.

The mid-2000s saw Trent experimenting with multiple formats, each targeting specific market opportunities. Fashion Yatra, a value fashion format, was launched to compete in the growing discount retail segment. Sisley, through a franchise arrangement with Benetton, brought international fashion to Indian consumers. The company also explored branded fashion retail through distribution agreements, though these experiments would eventually be discontinued as Trent refined its focus on private labels.

In 2014, Tesco acquired a 50% stake in Star Bazaar for £85 million and became a joint venture partner. This partnership brought much-needed capital and expertise to the struggling hypermarket business. Tesco's global experience in food retail, particularly in supply chain management and private label development, helped improve Star Bazaar's operations. The partnership also validated Trent's potential in food retail, even as the format continued to face profitability challenges.

The period also saw Trent's first serious engagement with international fashion brands. A joint venture with Inditex brought Zara to India, with Trent holding a 51% stake in the Indian operations. This partnership provided invaluable insights into fast fashion operations—from supply chain velocity to inventory management to store refresh rates. The learnings from operating Zara stores would later prove crucial in developing Trent's own fast fashion format.

After the establishment of the joint venture, Star Bazaar started supermarket format Star Market and small convenience store format Star Daily, but discontinued the latter by early 2018 when it began its online grocery service called StarQuik. In 2015, Trent entered into a partnership with Sonae to open and operate Sport Zone outlets in India, but the venture was later dissolved. These experiments, while not all successful, demonstrated Trent's willingness to test new concepts and quickly pivot when results didn't meet expectations.

The expansion years weren't without their challenges. The 2008 global financial crisis impacted consumer spending and made capital more expensive. Real estate costs continued to rise, making expansion capital-intensive. Competition intensified as international brands entered India directly and domestic players like Future Group and Reliance Retail scaled rapidly. The hypermarket business, in particular, struggled with profitability as operational costs remained high while price competition was intense.

During this period, Westside continued its steady expansion, reaching about 70 stores by 2015. The format refined its positioning, moving slightly upmarket to differentiate from emerging value players. The private label portfolio expanded to cover virtually every category—from cosmetics to home furnishings. The Westside Club grew to over 3 million members, providing valuable customer data and loyalty that competitors struggled to replicate.

The organizational capabilities built during these expansion years would prove crucial for future success. Trent developed expertise in multi-format management, learning to balance different business models with varying economics. The supply chain infrastructure expanded to handle diverse product categories—from fashion to fresh produce. The company also built a strong talent pipeline, with many executives who started during this period later leading key initiatives.

Technology adoption accelerated during these years, though Trent remained primarily focused on physical retail. Point-of-sale systems were upgraded, inventory management became more sophisticated, and customer relationship management tools were deployed to better understand shopping patterns. However, unlike some competitors who were making big bets on e-commerce, Trent maintained its focus on store expansion and operational excellence.

The financial performance during the expansion years was mixed. While Westside continued to deliver steady growth and improving margins, the newer formats struggled to achieve profitability. The company's overall margins were pressured by the investment in new formats and the losses from experimental ventures. However, the patient capital from the Tata Group allowed Trent to take a long-term view, focusing on learning and capability building rather than short-term profits.

An important development during this period was the increasing focus on tier 2 and tier 3 cities. As metro markets became saturated and expensive, Trent began exploring smaller cities where organized retail was still nascent. This expansion into smaller markets would later become a key competitive advantage, particularly for the value fashion format that was taking shape in the company's innovation labs.

The partnership approach that Trent adopted during these years—whether with Tesco, Inditex, or Benetton—demonstrated a pragmatic strategy of learning from global leaders while maintaining control over core operations. These partnerships brought technical expertise, operational best practices, and in some cases, capital, accelerating Trent's learning curve in new formats and categories.

By 2015, Trent had transformed from a single-format retailer to a multi-format player with presence across fashion, books, sports, and grocery retail. Not all experiments had succeeded, but each had contributed valuable lessons. The company had built robust operational capabilities, established strong vendor relationships, and most importantly, developed a deep understanding of Indian consumers across different segments and geographies.

The stage was now set for Trent's most ambitious move yet. The learnings from operating Zara, the insights from Fashion Yatra's value experiments, and the operational excellence developed at Westside would all converge in a new format that would revolutionize Indian fashion retail. As 2016 approached, the company was preparing to launch Zudio—a format that would combine fast fashion velocity with Indian value expectations, creating a new paradigm in retail that would capture the imagination of millions of Indian consumers.

V. The Zudio Revolution: Cracking the Code (2016-Present)

In 2016, Trent opened its first Zudio store in Bangalore. Over the subsequent years, the number of Zudio stores grew at a faster rate than Trent's flagship format Westside, driven by high turnover of Zudio's relatively inexpensive fast fashion clothing. The location wasn't random—it was the same spot where Westside had opened its first store in 1998, a symbolic gesture that suggested Trent believed this new format would be equally transformational.

The genesis of Zudio came from a simple but powerful insight: there was a massive market of Indian consumers who wanted fashionable clothing but couldn't afford Westside's price points. Trent Limited identified this gap between consumer desire and Westside's offerings—a gap where demand for affordable fashion was not being met by the existing market. In response, Trent launched Zudio, a brand specifically designed to cater to this vast and growing segment. Zudio aimed to offer quality apparel at more accessible price points, effectively capturing the attention of a cost-conscious yet style-aware population.

The Zudio model was radically different from anything in Indian retail. Zudio's competitive pricing strategy is at the heart of its success. It has a very attractive pricing proposition where you will get everything under 999. This pricing specifically targets the audience in Tier 2 to 4 cities, who prioritize affordable fashion over brand names. But low prices alone don't explain Zudio's explosive growth. The secret lay in a combination of operational innovations that created a virtuous cycle of high velocity, low costs, and rapid expansion.

In the first couple of years, they tested the waters. Zudio expanded to only 7 standalone stores. But once they realized that the value fashion idea was working, they went on a blitzkrieg. The initial slow expansion was deliberate—Trent was perfecting the model, understanding unit economics, and building supply chain capabilities. Once the formula was proven, the expansion was breathtaking.

The operational philosophy behind Zudio was revolutionary for Indian retail. Zudio didn't spend much money trying to make the stores look fancy. It had to simply look cool and that could be done with cheaper fittings, lighting, mirrors and trial rooms. It spends roughly around Rs 1,800 per sq. ft, compared to Rs 5,500 per sq. ft for Zara. And by concentrating on 'ignored' retail locations, it could keep rents low too. This frugal approach to store development meant rapid rollout was financially viable.

For Zudio, they leveraged the established infrastructure of Star supermarket stores. Trent meticulously assessed product viability before inaugurating their first independent Zudio store in FY18. This period of careful evaluation of store economics has led to a low rate of store closures, consistent sales per square foot, and an impressive return on capital employed (ROCE). The discipline in site selection and format standardization created a replicable model that could be scaled rapidly.

The inventory management approach at Zudio broke conventional retail wisdom. Zudio might have taken a leaf out of Zara's book for this one. Zara has one of the highest inventory refresh rates in the fast fashion industry. And Zudio decided to do that too. The brand refreshes its inventory every 15 days and maybe Trent picked up this trick after being on Zara's India board. This rapid refresh rate meant customers had a reason to visit frequently, driving footfalls and creating a sense of urgency in purchase decisions.

The supply chain that powers Zudio represents one of Trent's greatest achievements. Working with a network of small and medium manufacturers across India, Zudio created a system that could deliver new styles from design to store in weeks, not months. The company's decades of experience in private label development for Westside provided the foundation, but Zudio pushed the boundaries of speed and efficiency. Small batch production, quick testing of styles, and rapid scaling of successful products became the norm.

Because Zudio's ASP is close to ₹500, the profit margins are lower than Westside. So the only way to compensate for that is by pumping out large volumes. For instance, let's look at a popular metric in retail stores called sales density. Think of this as how much revenue is generated per square foot in a store. And for Zudio, this comes to around ₹18,000 per square foot. For Westside, it's just ₹12,000. The higher the better because it shows that the floor space is being used more efficiently.

The geographic expansion strategy for Zudio was particularly astute. Especially in smaller towns. As an article in the Financial Express put it, "[Zudio's expansion is] putting smaller towns such as Vapi and Godhra in Gujarat, Muzaffarpur in Bihar, Rudrapur in Uttarakhand, Dibrugarh in Assam, Khammam in Telangana, Thrissur and Pattambi in Kerala, Davanagare in Karnataka, Hanumangarh in Rajasthan and Sangli and Solapur in Maharashtra on the retail map." By focusing on underserved markets, Zudio faced less competition and lower real estate costs while tapping into pent-up demand for organized fashion retail.

The product strategy at Zudio deserves special attention. Unlike typical value retailers who offer last season's styles or lower quality products, Zudio focused on current trends at accessible prices. The design team, leveraging insights from Westside and Zara operations, created products that looked contemporary but were engineered for cost efficiency. Simple construction techniques, efficient fabric utilization, and standardized components across styles helped maintain low costs without compromising on appearance.

Zudio does not have an online presence, they don't do discounts, and they don't have seasonal clothing. So how is it able to survive in this highly competitive market? These apparent weaknesses are actually strategic choices. No online presence means no channel conflict and lower operational complexity. No discounts mean consistent margins and no training customers to wait for sales. No seasonal clothing means no inventory write-offs and consistent product flow throughout the year.

The customer experience at Zudio, while basic, hits all the right notes for its target audience. Stores are well-lit, air-conditioned, and organized. Trial rooms are functional. Staff are helpful but not intrusive. The checkout process is quick. For customers in tier 2 and tier 3 cities, many experiencing organized retail for the first time, this represents a massive upgrade from traditional shopping experiences.

Trent Ltd employed capital for a new Zudio store between Rs 3-4 crore in FY25. This capital efficiency is remarkable—a new store pays back its investment typically within 18-24 months, generating attractive returns on capital employed. This efficiency enabled rapid expansion without straining the balance sheet or requiring massive external funding.

The financial performance of Zudio has been spectacular. Zudio has over 450 stores as of today while Westside is only at 227. And Zudio already contributes to over 56% of Trent's fashion revenues. Mind you, it was just 16% in FY20. The format has not just grown rapidly but has become the primary growth driver for Trent.

In FY25, the company opened 244 stores under the Zudio brand and had 38.4% revenue growth at ₹17,134.6 crore (USD 2.06 billion approximately). This pace of expansion is unprecedented in Indian retail, particularly for a format that maintains positive unit economics from day one.

The impact of Zudio extends beyond Trent's financial statements. The format has democratized fashion for millions of Indians who previously had limited access to trendy, affordable clothing. It has created employment in smaller cities, supported hundreds of small manufacturers, and proven that physical retail can thrive in the digital age with the right value proposition.

Competition has taken notice. Just a few months ago, Shein made its comeback in India through Reliance after a five year break. And it isn't stopping there. Reliance also has big plans for Yousta, its affordable fashion brand, with a bold target of 1,000+ stores. Sure, Yousta had only about 55 stores as of October 2024, but the intent is clear. However, Zudio's first-mover advantage, operational excellence, and deep understanding of tier 2/3 markets provide significant competitive moats.

Recent challenges have emerged as the format matures. Kotak Institutional Equities pointed out a potential issue: store cannibalisation. Zudio's breakneck expansion led to overlapping locations. Basically, stores opening up in the same pin codes. That means they ended up eating into each other's sales, keeping revenue growth flat even though new stores were mushrooming. This suggests that even Zudio's remarkable model has limits to growth velocity.

Looking ahead, Zudio's evolution continues. The format is expanding categories beyond apparel into footwear, accessories, and home products. In 2024, the company began operating internationally with the opening of a Zudio store in Dubai, testing whether the model can work beyond Indian borders. The challenge will be maintaining the magic formula of value, velocity, and volume as the format scales beyond 1,000 stores.

VI. The Westside Renaissance & Portfolio Evolution

While Zudio captured headlines with its explosive growth, Westside quietly underwent its own transformation, evolving from Trent's flagship format into a premium lifestyle destination. The success of Zudio, rather than cannibalizing Westside, actually freed it to move upmarket and focus on a different customer segment—one seeking quality, design, and a superior shopping experience over rock-bottom prices.

The digital transformation of Westside marked a significant strategic shift. Westside has been making quiet gains in the digital space. Online sales through westside.com and the Tata Neu platform grew by 45% year on year in the first nine months of FY25. Online now makes up over 6% of Westside's total revenue. This digital growth came without the massive marketing spend typical of e-commerce players, leveraging instead the brand equity built over two decades and integration with the Tata Group's super-app strategy.

The Club West loyalty program emerged as a powerful competitive advantage. By 2024, the program had grown to over 16 million members, with these loyal customers accounting for 90% of revenues. The program went beyond traditional points and discounts, offering exclusive previews, personalized styling services, and curated experiences that deepened emotional connections with the brand. Members received birthday vouchers, anniversary rewards, and access to limited edition collections, creating a sense of belonging that transcended transactional relationships.

Westside.com and Tata Neu continue to witness traction and grow profitably. In Q1FY26, online revenues grew by 35 per cent and contributed to over 6 per cent of Westside revenues. This omnichannel approach, where online and offline experiences seamlessly integrated, positioned Westside uniquely in a market where most players struggled to balance digital and physical retail.

The product portfolio at Westside underwent significant premiumization. While maintaining its core private label strategy, the quality of fabrics, construction, and design sophistication increased substantially. The average selling price at Westside grew to ₹1,200-1,500, nearly three times that of Zudio, reflecting both the premium positioning and the customer's willingness to pay for perceived value. Categories like home furnishing, personal care, and accessories expanded, transforming Westside from an apparel retailer to a lifestyle curator.

The store design evolution reflected this premium shift. New Westside stores featured enhanced visual merchandising, dedicated brand shops within stores, and experiential zones for categories like beauty and home. The fitting rooms were upgraded with better lighting and spacious designs. Some stores introduced personal shopping services and alteration facilities, services that justified premium pricing and enhanced customer loyalty.

Beyond Westside and Zudio, Trent's portfolio strategy continued to evolve with targeted format innovations. After the outbreak of COVID-19, Trent repositioned Landmark Bookstores as a beauty and accessories retailer called Misbu. This transformation demonstrated Trent's ability to pivot quickly in response to market changes, converting an underperforming asset into a growth opportunity in the booming beauty segment.

In 2023, the company started occasionwear chain, Samoh, targeting the large and growing ethnic and occasion wear market. Samoh represented Trent's entry into a segment dominated by traditional players and ethnic specialists. The format leveraged Trent's design capabilities and supply chain efficiency to offer contemporary ethnic wear at competitive prices, filling a gap between mass-market ethnic retailers and premium designer brands.

The Star Bazaar transformation under the Tesco partnership yielded mixed results but valuable lessons. The hypermarket format evolved into a more focused grocery and fresh produce destination, with private labels accounting for over 30% of sales. The venture into online grocery through StarQuik, while eventually discontinued, provided insights into the complexities of grocery e-commerce and quick commerce that would inform future strategies.

Analysts believe Zudio could achieve Westside's levels of profitability in the medium term, given the scale of the business and the improvements in the unit economics. This convergence of profitability profiles across formats suggested that Trent had cracked the code on operating multiple formats efficiently while maintaining distinct positioning for each.

The organizational structure evolved to support this multi-format strategy. Each format operated with significant autonomy in merchandising and marketing while sharing common back-end infrastructure like supply chain, technology, and finance. This hub-and-spoke model allowed for entrepreneurial energy at the format level while capturing economies of scale at the corporate level. Cross-pollination of talent between formats ensured best practices spread quickly across the organization.

Technology adoption accelerated across all formats, though always in service of physical retail rather than as a replacement. Advanced analytics helped optimize inventory across the network. RFID technology improved stock accuracy and reduced shrinkage. Mobile apps for store staff enhanced customer service capabilities. Yet, Trent resisted the temptation to over-invest in technology, maintaining focus on retail fundamentals of product, price, and experience.

The vendor ecosystem that supported Trent's multiple formats became increasingly sophisticated. Long-term partnerships with manufacturers, many exclusive to Trent, ensured quality and cost advantages. The company's vendor financing programs helped smaller suppliers scale operations. Regular capability building workshops upgraded vendor skills in areas like sustainable manufacturing and quality control. This collaborative approach created a win-win ecosystem that competitors found difficult to replicate.

Sustainability initiatives, while not headline-grabbing, became embedded in operations. Westside introduced eco-friendly product lines using organic cotton and recycled materials. Store designs incorporated energy-efficient lighting and cooling systems. Packaging moved toward biodegradable materials. These initiatives, while adding some costs, resonated with increasingly conscious consumers and aligned with Tata Group values.

The real estate strategy evolved to support different format requirements. While Zudio could thrive in secondary locations, Westside required prime mall positions or high-street locations. The company's relationships with developers, built over decades, provided access to quality locations at competitive terms. The ability to commit to multiple stores across formats made Trent an attractive anchor tenant for new developments.

International expansion, tested with Zudio's Dubai store, opened new growth avenues. The Middle East and Southeast Asian markets, with large Indian diaspora populations and similar climate conditions, presented natural expansion opportunities. However, Trent approached international expansion cautiously, focusing first on perfecting the India model before aggressive overseas expansion.

The financial impact of this portfolio evolution was significant. While Zudio drove volume growth, Westside and other formats contributed to margin expansion. The diversified portfolio reduced dependence on any single format and provided resilience against market disruptions. Different formats appealed to different customer segments, maximizing Trent's addressable market and share of wallet.

Operating from over 1,000 large-format fashion stores, we have engaged with more than 100 million customers," P. Venkatesalu, Trent's Managing Director said. This scale, achieved through multiple complementary formats rather than a single concept, created competitive advantages in sourcing, real estate negotiations, and brand recognition that would be difficult for new entrants to replicate.

VII. Business Model Deep Dive

The business model that powers Trent's success is deceptively simple on the surface but remarkably sophisticated in execution. At its core lies a private label strategy that has evolved into one of the most successful in global retail, with over 90% of products sold across all formats being exclusive Trent brands. This isn't just about better margins—it's about complete control over the value chain from design to retail.

The economics of private label retail at Trent's scale create powerful competitive advantages. When a customer buys a shirt at Westside or Zudio, Trent captures not just the retail margin but also the brand margin that would typically go to an external supplier. Gross margins in the range of 50-55% for fashion products compare favorably with global retailers, but in the Indian context where branded apparel retailers operate at 35-40% gross margins, this advantage is substantial.

The design and product development process represents a core competency that took decades to build. Trent employs over 300 designers and product developers across formats, creating thousands of new styles annually. The design philosophy balances global trends with Indian preferences—a Western silhouette might be adapted with Indian-friendly necklines, or international color trends modified for Indian skin tones and climate conditions. This localization of global fashion, done at scale and speed, is nearly impossible for international brands to replicate.

Trent Ltd employed capital for a new Zudio store between Rs 3-4 crore in FY25. This capital efficiency is remarkable when compared to other retailers who might spend Rs 8-10 crore for similar-sized stores. The lean store model involves standardized layouts, modular fixtures that can be reused, and minimal customization. This allows Trent to open stores rapidly without straining capital resources, achieving payback periods of 18-24 months compared to industry standards of 3-4 years.

The working capital management at Trent defies retail conventions. Despite being in fashion retail where inventory obsolescence is a constant risk, Trent maintains inventory turns of 4-5 times annually at Zudio, comparable to global fast fashion leaders. This is achieved through small batch production, quick response to sales data, and a willingness to stock out rather than overstock. The company's mantra is "it's better to lose a sale than to mark down inventory," a discipline that maintains margins and brand perception.

The supply chain architecture supporting Trent's operations is a marvel of complexity management. The company works with over 500 vendors across India, from large factories to small workshop clusters. This distributed manufacturing model provides several advantages: risk diversification, ability to produce small batches economically, and access to specialized skills in different regions. Tamil Nadu clusters might specialize in knits, while Delhi NCR excels in Western wear, and Kolkata in ethnic products.

The vendor financing ecosystem Trent has created deserves special attention. Many small vendors lack working capital to scale operations. Trent's vendor financing programs, often in partnership with banks, provide capital at competitive rates. In return, Trent gets dedicated capacity, better prices, and first access to production slots. This symbiotic relationship, built over years of trust, creates switching costs for both parties and acts as a competitive moat.

Quality control in a distributed manufacturing system with hundreds of vendors could be a nightmare, but Trent has institutionalized processes that ensure consistency. Random quality audits, vendor rating systems, and technology-enabled tracking ensure standards are maintained. Vendors are classified into tiers based on performance, with top performers getting more business and better terms. This carrot-and-stick approach has created a culture of quality across the supply ecosystem.

The merchandising strategy varies significantly across formats but follows common principles. Fast-moving basics in standard sizes form the foundation, ensuring consistent footfalls and cash generation. Fashion products in smaller quantities create excitement and urgency. The mix is carefully calibrated—Zudio might have 70% basics and 30% fashion, while Westside could be 50-50. This portfolio approach balances risk and reward while maintaining inventory freshness.

Pricing architecture at Trent is both art and science. Price points are carefully chosen to create clear value perception—Zudio's sub-₹999 positioning isn't arbitrary but based on extensive consumer research showing psychological barriers at the ₹1,000 mark for value-conscious consumers. Within each format, price laddering ensures products at multiple price points, maximizing customer capture across income segments.

The anti-promotional stance, particularly at Zudio, represents a fundamental business philosophy. Zudio does not have an online presence, they don't do discounts, and they don't have seasonal clothing. By maintaining consistent pricing, Trent trains customers to buy at full price, protecting margins and avoiding the discount spiral that plagues many retailers. This requires confidence in product and pricing, and the discipline to accept short-term sales losses for long-term margin protection.

Store operations at Trent achieve efficiency through standardization and technology. Each format has detailed standard operating procedures covering everything from visual merchandising to customer service protocols. Store staff are cross-trained across functions, providing flexibility in deployment. Technology like automated replenishment systems and mobile POS devices enhance efficiency without compromising the human touch that differentiates physical retail.

The real estate strategy balances growth with prudence. Trent typically signs 9-15 year leases with rent escalation clauses, providing long-term visibility while protecting against inflation. The company's reputation as a reliable tenant who drives footfalls gives it negotiating leverage. In many tier 2/3 cities, Trent is often the anchor tenant that makes a retail development viable, extracting favorable terms in exchange for this anchor role.

Data analytics, while not Trent's primary differentiator, plays an increasingly important role. Sales data is analyzed daily to identify trends, with successful styles quickly reordered and failures discontinued. Customer data from loyalty programs informs product development and marketing strategies. However, Trent avoids the trap of over-reliance on data, maintaining space for merchant intuition and creative risk-taking.

The capital allocation framework at Trent prioritizes organic growth over acquisitions. The company's history shows a preference for building formats internally rather than buying existing chains. When acquisitions are made, like Landmark, they're typically transformed rather than run as-is. This build-versus-buy philosophy ensures cultural alignment and operational consistency but requires patience and long-term thinking.

Return on capital employed (ROCE) has emerged as a key metric driving decision-making. The foreign brokerage said Trent has balanced doubling its Zudio store count over FY23-25 with improving its return ratios to 25 per cent-plus levels. This focus on returns, not just growth, distinguishes Trent from retailers who prioritize market share over profitability.

The cash generation characteristics of the business model provide strategic flexibility. Negative working capital at Zudio—where inventory turns quickly and suppliers are paid on credit terms—means growth is largely self-funding. This cash generation has allowed Trent to fund expansion without significant debt or equity dilution, maintaining the balance sheet strength that provides resilience during downturns.

Risk management is embedded in the business model through diversification across formats, geographies, and price points. No single store or region contributes disproportionately to revenues. The multi-format strategy ensures exposure to different customer segments with varying economic sensitivities. This portfolio approach provides stability while individual formats might face temporary challenges.

The sustainable competitive advantages emerge from the interplay of these elements rather than any single factor. The combination of private label expertise, efficient operations, strong vendor relationships, and patient capital creates a system that's difficult to replicate. Competitors might copy individual elements—store designs, price points, or even products—but recreating the entire ecosystem requires time, capital, and capabilities that few possess.

VIII. Financials & Performance Analysis

Net sales reached Rs 17,134.61 crore in March 2025, a substantial increase from Rs 12,375.11 crore in March 2024 and Rs 8,242.02 crore in March 2023. Operating profit (PBDIT) also demonstrated a positive trend, rising to Rs 2,977.01 crore in March 2025. These numbers reflect not just growth but an acceleration that few retailers globally have achieved at this scale.

The revenue trajectory tells a story of compound excellence. Growing from Rs 8,242 crore to Rs 17,134 crore in just two years represents a CAGR of over 44%, extraordinary for a retailer operating primarily physical stores in an era supposedly dominated by e-commerce. This growth came not from acquisitions or financial engineering but from organic store expansion and same-store sales growth, making it particularly valuable from an investment perspective.

Margin evolution reveals operational leverage at work. Despite rapid expansion which typically pressures margins, Trent has maintained and even improved profitability metrics. EBITDA margins expanded from 15.3% in FY23 to 17.4% in FY25, demonstrating that scale benefits are flowing through to the bottom line. This margin expansion while growing at breakneck speed defies retail gravity and speaks to the strength of the business model.

The company's revenue rose 19.8% to ₹4,781 crore in Q1 FY26, up from ₹3,992 crore in Q1 FY25. Profit after tax (PAT) increased by 23.5% to ₹423 crore, compared to ₹342 crore in the same period last year. EBITDA stood at ₹838 crore, a 37.1% jump from ₹611 crore in Q1 FY25, while EBITDA margin improved by 220 basis points, reaching 17.5%. The Q1 FY26 results demonstrate that the momentum continues, with margins expanding even as the base grows larger.

Stock market performance has reflected this operational excellence. Trent has been an exceptional performer with the stock price appreciating at ~35% CAGR in the last five years. A Rs 100 investment in Trent five years ago would be worth approximately Rs 450 today, outperforming not just the broader market but most growth stocks globally. This wealth creation has made Trent a poster child for the India consumption story.

The valuation metrics tell a nuanced story. Trading at a P/E ratio of over 150 times, Trent is priced for perfection. This premium valuation reflects market confidence in future growth but also creates vulnerability to any disappointment. The PEG ratio, considering the growth rates, suggests the valuation might be justified if execution continues, but there's little room for error.

Comparative analysis with global peers provides perspective. Zara's parent Inditex trades at 25 times earnings, H&M at 15 times, and Fast Retailing (Uniqlo) at 35 times. Even high-growth players like Shein (private) are valued at lower multiples based on funding rounds. Trent's premium reflects both the India opportunity and execution excellence but also suggests markets are extrapolating current growth rates far into the future.

The unit economics breakdown reveals the model's attractiveness. A typical Zudio store generates Rs 15-20 crore in annual revenues on an investment of Rs 3-4 crore. With EBITDA margins of 15-18% at store level, each store contributes Rs 2.5-3.5 crore in EBITDA annually. This translates to cash payback in under two years and IRRs exceeding 35%, metrics that few retail formats globally can match.

Working capital dynamics provide a crucial competitive advantage. Inventory days at around 75-80 for Zudio compare favorably with industry standards of 120-150 days. Creditor days of 60-70 partially offset inventory investment. The negative working capital at Zudio means growth is self-funding—a critical advantage in capital-intensive retail. This efficient capital structure allows aggressive expansion without proportional capital needs.

Segment-wise performance shows portfolio strength. While Zudio drives volume growth with 60%+ revenue growth, Westside contributes stability with 15-20% growth and higher margins. The Star business, while smaller, is approaching breakeven after years of losses. This portfolio balance provides both growth and stability, reducing dependence on any single format's performance.

Return metrics have shown consistent improvement. Return on Equity (ROE) has expanded from 18% in FY21 to 28% in FY25, reflecting both operational improvements and efficient capital deployment. Return on Capital Employed (ROCE) at 30%+ places Trent among the best-performing retailers globally. These returns, sustained while growing rapidly, demonstrate the model's robustness.

Capital expenditure patterns reveal disciplined growth. Annual capex of Rs 800-1,000 crore funds 200+ new stores plus renovations and technology investments. This capex intensity of 5-6% of sales is modest for a retailer in expansion mode. The ability to fund this entirely from internal accruals without debt demonstrates cash generation strength.

The debt-free status provides strategic flexibility. Zero long-term debt on the balance sheet is unusual for a rapidly growing retailer. This conservative capital structure provides resilience during downturns and flexibility for opportunistic expansion. The strong balance sheet also supports vendor financing programs critical for supply chain management.

Cash flow analysis reveals quality of earnings. Operating cash flow consistently exceeds reported profits, indicating high earnings quality. Free cash flow after capex remains positive despite aggressive expansion, a rare achievement in growth retail. This cash generation funds dividends while maintaining growth investment, balancing stakeholder interests.

Quarterly volatility has increased recently, concerning some investors. However, brokerages remain cautious due to slowing like-for-like (LFL) growth, rich valuations, and concerns about future growth trajectory. The Q4 FY25 results showing slower growth sparked a correction, reminding investors that even exceptional businesses face periodic challenges.

Geographic revenue distribution shows increasing diversification. While western India contributes 35-40% of revenues, growth in southern and northern regions is faster. Tier 2/3 cities now contribute over 40% of revenues versus 25% five years ago. This geographic diversification reduces regional economic sensitivity while tapping into India's consumption democratization.

Category performance within stores shows expansion beyond core apparel. Non-apparel categories—footwear, accessories, beauty, home—now contribute 20-25% of revenues versus 10-15% five years ago. These categories often carry higher margins and increase transaction values, contributing disproportionately to profitability growth.

The impact of GST and other regulatory changes has been well-managed. The shift to organized retail accelerated post-GST as unorganized players struggled with compliance. Trent's systems and processes, built over decades, allowed seamless transition while gaining market share from struggling competitors. This regulatory advantage continues as compliance requirements increase.

Seasonality patterns are less pronounced than typical fashion retail. The absence of seasonal inventory at Zudio smooths revenue patterns. Festival seasons still drive higher sales, but the base business remains steady throughout the year. This reduced seasonality improves inventory management and cash flow predictability.

Investment in technology, while measured, is increasing. Annual technology spend of Rs 100-150 crore focuses on operational efficiency rather than customer-facing innovation. Investments in data analytics, supply chain systems, and store operations technology improve productivity without the massive capital requirements of e-commerce platforms.

Dividend policy reflects confidence in cash generation. Regular dividend payments, while modest in yield terms given the high stock price, signal management confidence in sustainable cash flows. The ability to fund growth and return cash to shareholders simultaneously is rare in growth retail.

Looking at peer comparison within India, Trent's metrics stand out. Reliance Retail, while larger in revenue, operates at lower margins due to grocery exposure. Aditya Birla Fashion struggles with profitability despite strong brands. Future Group's bankruptcy highlights the risks of aggressive debt-funded expansion. Trent's combination of growth, profitability, and balance sheet strength is unique in Indian retail.

The sustainability of these financial metrics is the key question for investors. Can Trent maintain 30%+ growth rates as the base expands? Will margins sustain as competition intensifies? Can return ratios remain elevated as the easy markets get saturated? These questions will determine whether current valuations are justified or excessive.

IX. Competition & Market Dynamics

The Indian retail landscape has undergone seismic shifts over the past decade, evolving from a fragmented, unorganized market to one where organized players increasingly dominate. The total retail market, valued at over $900 billion, remains predominantly unorganized at 88%, but the organized segment is growing at 20-25% annually versus 10-12% for traditional retail. Within this transformation, Trent has emerged as a unique player, competing effectively against both domestic giants and international entrants.

Reliance Retail, with revenues exceeding Rs 2,30,000 crore, is the 800-pound gorilla in Indian retail. Its multi-format strategy spans grocery, fashion, electronics, and petroleum retail. In fashion specifically, Reliance's Trends format operates over 2,000 stores, making it Zudio's most direct competitor. Just a few months ago, Shein made its comeback in India through Reliance after a five year break. And it isn't stopping there. Reliance also has big plans for Yousta, its affordable fashion brand, with a bold target of 1,000+ stores. Despite Reliance's scale and resources, Trent has maintained its growth trajectory, suggesting room for multiple players in India's vast market.

The Future Group's spectacular collapse in 2021-22 provided both validation and opportunity for Trent's strategy. Future's debt-fueled expansion and complex corporate structure ultimately led to insolvency, with assets acquired by Reliance. The failure highlighted the risks of aggressive expansion without operational excellence and the importance of balance sheet strength—areas where Trent excels. The market share vacated by Future's formats like Brand Factory and FBB was partially captured by Trent, accelerating growth.

International fashion retailers have had mixed success in India. Zara, H&M, Uniqlo, and Gap have all entered with fanfare but struggled to scale beyond metros. High real estate costs, import duties on non-local production, and difficulty in adapting to Indian preferences have constrained growth. Their premium positioning also limits addressable market size. Trent's partnership with Inditex for Zara provided insider knowledge of international retail while avoiding direct competition through distinct positioning.

E-commerce players, led by Amazon and Flipkart, were supposed to disrupt physical retail, but fashion has proven resilient. Online fashion penetration remains under 15% despite heavy discounting and marketing spend. The tactile nature of apparel shopping, immediate gratification of physical retail, and trust issues with online quality have limited e-commerce growth. Myntra, Flipkart's fashion platform, despite years of investment, generates revenues comparable to Trent while burning cash, validating Trent's physical-first strategy.

Goldman Sachs said the relaunch of Shein has been allowed by the Indian government on condition that it will source all products only from India, and make sure all consumer data remains in India. A meaningful scale up of a value fast fashion business requires several years of supply chain investments, Goldman Sachs said. This local sourcing requirement significantly alters Shein's business model, potentially negating its cost advantages from Chinese manufacturing.

Regional players provide competition in specific markets but lack national scale. Chennai's Saravana Stores, Bangalore's Shoppers Stop, and Punjab's Monte Carlo have strong local presence but haven't successfully expanded nationally. Their regional focus and traditional business models make them vulnerable to organized players like Trent who bring modern retail practices and national brand appeal.

The unorganized sector, while declining in share, remains formidable in absolute terms. Small shops offer personalized service, credit facilities, and proximity that organized retail cannot match. However, GST implementation, rising real estate costs, and changing consumer preferences steadily shift advantages toward organized players. Trent's value positioning at Zudio particularly appeals to consumers upgrading from unorganized retail.

New-age D2C brands, while grabbing headlines, haven't significantly impacted Trent's business. Brands like Bewakoof, Souled Store, and others remain subscale, burning cash to acquire customers online. Their lack of physical presence limits market reach, while customer acquisition costs make profitability elusive. Some are now exploring physical retail, validating Trent's omnichannel approach.

The competitive dynamics vary significantly by geography. Metros face intense competition with multiple players vying for premium real estate and affluent consumers. Tier 2/3 cities, where Trent has focused expansion, have less competition and lower operational costs. Rural markets remain largely untapped by organized players, representing future opportunity.

Price competition has intensified but hasn't triggered a race to the bottom. Zudio sharply targets a price point of Rs 999 and below. Apparel market above Rs 999 is not part of Zudio's TAM. This clear positioning allows Zudio to avoid direct price competition with players targeting different segments. The no-discount policy also prevents margin erosion from promotional intensity.

Supply chain capabilities have become a key differentiator. Fast fashion requires rapid response to trends, requiring sophisticated supply chain management. Trent's two-decade experience in private label development provides advantages in vendor relationships, quality control, and speed to market that new entrants cannot easily replicate. The distributed manufacturing model across hundreds of vendors provides flexibility and risk mitigation.

Real estate competition has intensified as retailers expand rapidly. Prime locations in metros command high rents and are often unavailable. Trent's relationships with developers, built over decades, provide access to quality locations. The multi-format strategy also provides flexibility—if Westside cannot get viable terms, Zudio might still work in the same location at lower rents.

Technology disruption, while a constant threat, hasn't materialized as expected in fashion retail. AR/VR for virtual trials, AI for personalization, and automation in stores remain experimental. Consumers still prefer physical shopping for fashion, and technology has primarily enhanced rather than replaced traditional retail. Trent's measured technology adoption focuses on operational efficiency rather than customer-facing innovation.

The talent war in retail has intensified with multiple players expanding simultaneously. Experienced store managers, merchandisers, and supply chain professionals command premium salaries. Trent's reputation as a stable, professionally run organization helps attract talent, but retention remains challenging as competitors poach aggressively. The company's investment in training and development creates internal pipelines but also makes employees attractive to competitors.

Market dynamics are shifting toward consolidation. Smaller regional players struggle to compete with national chains on price, selection, and experience. The next decade will likely see further consolidation, with 5-6 national players dominating organized retail. Trent's strong position, backed by Tata Group resources and reputation, positions it well for this consolidation phase.

Consumer behavior evolution favors organized retail. Increasing disposable incomes, urbanization, and exposure to global trends drive demand for fashion retail. The youth demographic, comfortable with brands and modern formats, represents a growing customer base. Social media influence accelerates trend adoption, benefiting fast fashion players who can quickly respond to viral trends.

Regulatory changes generally favor organized players. GST simplified inter-state commerce while increasing compliance burden on small players. E-commerce regulations limiting deep discounting and exclusive launches level the playing field with physical retail. Labor law reforms, while increasing costs, are manageable for organized players with proper systems.

The competitive moat around Trent's business model continues to widen. The combination of operational excellence, supply chain capabilities, real estate relationships, and brand equity creates barriers that money alone cannot overcome. It believes Trent's supply chain and design capabilities, built with years of experience of Indian design sensibilities, are difficult to replicate. Macquarie said Trent's proven ability to balance fashion risk with profitability through frequent style drops, and its expansion through owned/franchisee stores, have aided its performance.

X. Bear Case & Challenges

Goldman Sachs downgrades Trent Ltd. to 'neutral' and reduces its price target to ₹5,500 due to unexpected cannibalisation effects. Shares might trade at current levels until market conditions shift. This recent downgrade from one of Wall Street's most influential firms highlights growing concerns about Trent's ability to sustain its remarkable growth trajectory.

The cannibalization issue is becoming increasingly apparent as Trent's store density increases. The investment bank noted that while Zudio store additions remain robust, sales throughput has been moderating and has missed expectations for two consecutive quarters. Goldman Sachs believes higher-than-expected sales cannibalization is the likely culprit as Zudio adds significant retail area in towns that already have numerous stores. When multiple Zudio stores operate in the same catchment area, they compete for the same customers, leading to lower sales per store even as total store count grows.

The math of cannibalization is particularly concerning for a retailer valued on growth metrics. If same-store sales growth slows from 10% to 5% due to cannibalization, and new stores generate 20% lower revenues than expected due to nearby existing stores, the overall growth algorithm breaks down. Goldman Sachs cut its FY26-28 sales estimates by 5-9% and earnings per share forecasts by 8-13%, reflecting the slower pace of market share gains than previously anticipated.

Store saturation represents a longer-term but equally serious challenge. Macquarie sees scope to expand Zudio given its current store count of 700 against Reliance Trends' 2,000-plus stores. While this comparison suggests room for growth, it ignores crucial differences in positioning and market dynamics. Trends operates across price points while Zudio's sub-₹999 positioning limits its addressable market. The pace of store additions—200+ annually—cannot continue indefinitely without hitting saturation limits.

Execution risks multiply with scale. Managing 1,000+ stores across hundreds of cities requires operational excellence that becomes increasingly difficult to maintain. Each new store in a smaller town requires training staff who may have never worked in organized retail. Maintaining product quality across hundreds of vendors becomes more challenging as volumes grow. The supply chain complexity of delivering fresh fashion to remote locations tests logistics capabilities.

Management succession poses questions about continuity. While the current leadership has delivered exceptional results, the next generation of leaders must maintain the culture and operational discipline that made Trent successful. The Tata Group's governance structure provides stability, but retail is ultimately an execution business where leadership quality directly impacts performance.

Competition is intensifying from both expected and unexpected quarters. Sure, Yousta had only about 55 stores as of October 2024, but the intent is clear. The fast fashion game is heating up, and investors are watching closely. Reliance's entry into value fashion with Yousta, backed by deep pockets and retail infrastructure, represents a formidable challenge. If Reliance decides to accept losses to gain market share—a strategy it has employed in other sectors—Trent could face severe pricing pressure.

The online disruption threat, while manageable so far, could accelerate. The foreign brokerage's interactions with industry participants made it believe that a typical value retail customer has higher propensity of returns when shopping online than an average customer. However, as logistics infrastructure improves and return policies become more customer-friendly, online fashion could gain share. Trent's minimal online presence, while a strength today, could become a vulnerability if consumer behavior shifts rapidly.

Macroeconomic sensitivity could impact growth. While fashion is relatively resilient, a significant economic slowdown would affect discretionary spending. Trent's value positioning provides some protection, but fashion remains a postponable purchase during economic stress. The company's high valuation multiple leaves little room for error if growth slows even temporarily.

Real estate availability and costs pose ongoing challenges. As Trent expands into smaller cities, finding appropriate locations becomes harder. Many tier 3 cities lack organized retail infrastructure, requiring standalone stores with higher capital costs. In metros, prime real estate is either unavailable or prohibitively expensive. Rising rent costs, typically 8-10% annual escalations, pressure margins over time.

The talent constraint could limit growth quality if not quantity. Finding and training store managers, merchandisers, and supply chain professionals for 200+ new stores annually is challenging. Quality dilution is a real risk—one poorly managed store can damage brand reputation built over years. The cost of talent is also rising faster than inflation as retailers compete for limited experienced professionals.

Fashion risk remains inherent in the business model. While Trent has successfully predicted trends so far, fashion is inherently unpredictable. A few seasons of missing trends could lead to inventory buildup and markdowns. The no-discount policy, while protecting margins, also means less flexibility to clear slow-moving inventory.

Supply chain vulnerabilities could disrupt operations. Dependence on hundreds of small vendors creates quality and delivery risks. A major vendor bankruptcy, quality issue, or labor dispute could disrupt product flow. Climate change impacts on cotton production, increasing compliance requirements, and rising labor costs all pressure the supply chain.

Regulatory changes could impact business models. Potential e-commerce regulations favoring online players, changes in labor laws increasing costs, or environmental regulations requiring expensive compliance could pressure margins. The recent discussions about data localization and privacy laws add complexity and costs.

Brand perception risks exist despite current strength. Zudio's low-price positioning, while driving volume, could limit brand evolution. If consumers begin associating the brand with "cheap" rather than "value," moving upmarket becomes difficult. Westside faces the opposite challenge—premium positioning limits volume growth potential.

The international expansion wildcard adds complexity. While the Dubai store represents opportunity, international expansion requires different capabilities. Managing currency risks, understanding new markets, and competing with established local players all add risks. The distraction of international expansion could also impact domestic execution.

Valuation risks are perhaps most immediate for investors. Another thing is that investors are willing to pay an arm and a leg for the stock — the P/E ratio is at a whopping 150 times. At these valuations, any disappointment triggers sharp corrections. The stock's volatility has increased, with 5-10% daily moves becoming common around results or news flow.

ESG concerns, while not immediate threats, could impact long-term perception. Fast fashion globally faces criticism for environmental impact and labor practices. While Trent has better practices than many competitors, the sector's reputation could impact valuations and consumer behavior, particularly among younger, environmentally conscious consumers.

The "growth trap" represents a subtle but serious risk. The pressure to maintain high growth rates to justify valuations could lead to poor decisions—expanding too quickly, compromising on store quality, or entering unsuitable markets. The history of retail is littered with companies that destroyed value by growing for growth's sake.

System risk from overdependence on a few key executives or processes exists. If crucial individuals leave or key systems fail, the impact could be significant. The centralized buying model, while efficient, creates vulnerability if decision-making fails. The private label focus means no fallback on external brands if internal design fails.

These challenges don't negate Trent's achievements or potential, but they highlight the complexity of sustaining exceptional performance in retail. The bear case essentially argues that Trent's best days of easy growth are behind it, and the future will require navigating increasingly difficult trade-offs between growth, profitability, and market share. For investors paying premium valuations, these risks deserve careful consideration.

XI. Bull Case & Future Vision

The bull case for Trent rests on a fundamental truth: India's apparel market represents one of the world's last great untapped retail opportunities. With a market size exceeding $100 billion and organized retail penetration at just 12%, the runway for growth extends decades, not years. Trent, having cracked the code for serving Indian consumers across price points and geographies, is uniquely positioned to capture a disproportionate share of this opportunity.

It added 244 stores in FY 2024–25, now totaling 765 stores across 235 cities, including two international stores. This pace of expansion, while impressive, represents just the beginning. India has over 600 districts and 4,000 towns with populations exceeding 20,000. Even assuming only half are viable for organized retail, Trent's current presence barely scratches the surface. The potential for 5,000+ stores across formats isn't fantasy—it's a conservative estimate based on population density and consumption patterns.

The demographic dividend powering India's consumption story is only beginning to play out. With 65% of the population under 35 and rising income levels, the cohort entering peak consumption years is massive. These digital natives, exposed to global trends through social media but rooted in Indian values, represent Trent's ideal customers. They want fashion that's contemporary yet appropriate for Indian contexts, affordable yet aspirational—exactly what Trent delivers.

Noel Tata, chairman of Trent Ltd., and Tata Trusts reminded his vision was to grow the business ten-fold, noting that the revenue run rate had already doubled over the past two years. A ten-fold growth from current levels would put Trent at Rs 1,70,000 crore in revenues, which might seem audacious but is achievable given India's retail growth trajectory. If organized retail grows at 20% annually and Trent maintains or gains share, this vision becomes mathematical reality rather than aspiration.

The category expansion opportunity within existing formats provides another growth vector. In FY25, Zudio crossed a billion dollars in sales with lifestyle, and non-apparel accounting for over 20% of the revenues. This 20% could easily become 40% as categories like footwear, accessories, beauty, and home develop. Each category addition increases transaction values and visit frequency while leveraging existing store infrastructure.

International expansion, currently nascent, could become significant. The Middle East and Southeast Asia represent $50+ billion in apparel markets with significant Indian diaspora populations. If Trent can successfully adapt its model for these markets—and early indications from Dubai are positive—international could contribute 10-15% of revenues within a decade. This isn't about becoming a global retailer overnight but systematically expanding into natural adjacencies.

The Tata ecosystem provides competitive advantages that are underappreciated. Tata Neu, the group's super app, is gaining traction with millions of users. As it scales, it becomes a customer acquisition channel for Westside without the typical e-commerce customer acquisition costs. Tata's real estate arm provides access to prime properties. The group's reputation opens doors that remain closed to competitors.

Technology adoption, while measured so far, could accelerate growth. Unlike pure-play e-commerce players burning cash on customer acquisition, Trent can leverage its store network for omnichannel fulfillment. Click-and-collect, store-to-home delivery, and inventory visibility across channels could enhance customer experience without massive technology investment. The 1,000+ stores become mini-fulfillment centers, providing faster delivery than centralized e-commerce warehouses.

The supply chain moat continues to deepen with scale. Each year, Trent's vendor relationships strengthen, production capabilities expand, and logistics networks become more efficient. A meaningful scale up of a value fast fashion business requires several years of supply chain investments, Goldman Sachs said. Competitors starting today face a multi-year journey to reach Trent's current capabilities, by which time Trent will have moved further ahead.

Market share gains seem inevitable given competitive dynamics. The unorganized sector continues to cede share due to GST compliance, rising real estate costs, and changing consumer preferences. Among organized players, Trent's execution excellence and financial strength position it to gain share. The Future Group's collapse created a vacuum that Trent is filling. Smaller regional players lack resources to compete nationally.