P N Gadgil Jewellers: The 192-Year Journey from Sangli to Nasdaq Dreams

I. Introduction & Setup

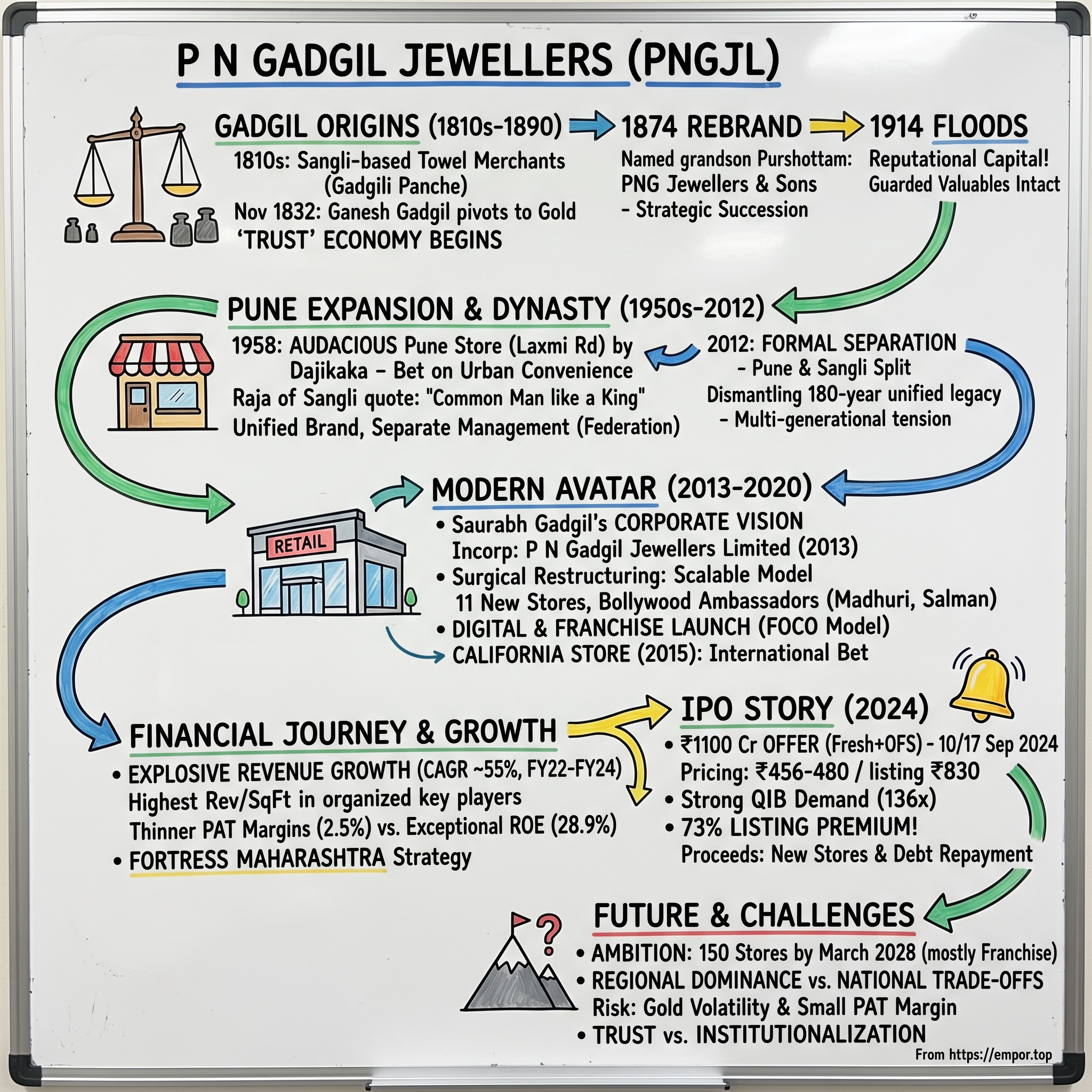

Picture this: A narrow lane in Sangli, Maharashtra, 1832. The air thick with the scent of marigolds and incense from nearby temples. A young man named Ganesh Gadgil carefully weighs gold on a traditional balance scale, his eyes sharp with the precision that would define six generations of jewellers after him. Little did he know that the small shop he was opening that November day would one day ring the opening bell at the National Stock Exchange, commanding a market value of nearly ₹8,000 crores.

The story of P N Gadgil Jewellers isn't just another corporate chronicle—it's a masterclass in how Indian family businesses navigate the treacherous waters between tradition and modernity. Here's the puzzle that makes this tale worth telling: How does a 192-year-old jewellery house, born in pre-independence India when trust was built through generations of face-to-face transactions, transform itself into a publicly-traded retail powerhouse while keeping its soul intact?

Most heritage brands face an existential crisis when they modernize. They either cling too tightly to tradition and become irrelevant, or they abandon their roots and lose what made them special. PNG, as customers lovingly call it, seems to have found a third way—one that involves family feuds, strategic splits, technological leaps, and a franchise model that would make any quick-service restaurant chain envious.

What unfolds is a journey from towel merchants to Maharashtra's jewellery kings, from handwritten ledgers to NSE listings, from a single shop in Sangli to 53 outlets spanning the state. It's a story of how gold became more than a commodity—it became a currency of trust passed down through generations like a family heirloom.

II. The Gadgil Origins: From Towels to Gold (1810s-1890)

The transformation from towels to gold deserves the kind of origin story that Silicon Valley startups dream about—except this one actually happened, 190 years before the first iPhone was sold.

In the early 19th century, the Gadgil family moved from a small village called Trimbak in Malvan Tehsil to Sangli, where patriarch Narayanrao Vasudeorao Gadgil sold towels under the brand "Gadgili Panche." These weren't just any towels—they had achieved something approaching brand status in pre-independence India, when most commerce happened through word-of-mouth and family reputation.

But it was Narayanrao's son, Ganesh, who would pivot the family business in a direction that would define the next six generations. Ganesh learned the jewellery business under the guidance of Mr. Modak, a family of jewellers with roots in Konkan, and after gaining hands-on experience, decided to start his own jewellery business.

On November 29, 1832, Ganesh set foot in the jewellery business with "Ganesh Narayan Gadgil," his own jewellery business. The date would become sacred in company lore—marked not just as a founding moment but as the beginning of a trust economy that would survive British colonial rule, two world wars, Indian independence, economic liberalization, and eventually, an NSE listing.

The early decades weren't about rapid scaling or market dominance—concepts that didn't exist in 1830s Sangli. Instead, Ganesh built his business on something more fundamental: the ability to accurately assess gold purity in an era before hallmarking, the discipline to maintain consistent weights when scales were crude, and the integrity to return deposits even when documentation was minimal.

Ganesh was blessed with three sons—Ramchandra, Narayan, and Gopal—all of whom assisted him in his business, with Narayan (called Bal Nana) continuing the family enterprise with the help of Bhulukaka Abhyankar, building up a reputation through hard work and excellent customer rapport.

The 1874 rebrand tells us something crucial about how Indian family businesses think about legacy. After the birth of his eldest grandson in 1874, Gadgil changed the name to P. N. Gadgil Jewellers & Sons, believing that his grandson's name, Purshottam, would bring good fortune. This wasn't just superstition—it was strategic succession planning, Maharashtra-style. By naming the business after his grandson, Ganesh was essentially IPO-ing the family's reputation, making it clear that this enterprise would outlive any single generation.

The trust capital built during this period would prove invaluable during one of Sangli's darkest moments. The floods of 1914 saw people leaving Sangli in droves for safer grounds, and while departing, they kept their valuables with Bal Nana in his shop. On their return, they were surprised to find their belongings intact! In modern terms, this was PNG's first major crisis management success—no insurance claims, no legal contracts, just pure reputational capital at work.

The three sons—Purshottam, Ganesh Pant, and Vasudev—went on to earn a name for themselves and their enterprise within a span of 4 decades between 1880 and 1920. Following Ganesh's death in 1890, the business didn't fragment as many family enterprises do. Instead, it evolved into something more sophisticated—a multi-branch family conglomerate before the term was invented.

III. The Pune Expansion & Family Dynamics (1950s-2012)

The year 1958 marks PNG's most consequential strategic decision—one that would determine whether this would remain a regional heritage brand or evolve into something bigger. The protagonist of this transformation wasn't supposed to be a businessman at all.

Anant Gadgil, who was born in a farm on September 11, 1915 while the family sought refuge there to escape the plague that year, had worked in the Gadgils' shop in Sangli for 20 long years. Twenty years of apprenticeship—imagine that in today's world where people switch jobs every two years. This wasn't just learning the business; it was absorbing the DNA of trust-based commerce that would prove crucial when he decided to make his move.

The Pune decision was audacious for its time. In 1958, he and his cousin, the son of Vishwanath Gadgil, established a new retail outlet in Pune under the name P. N. Gadgil Jewellers & Company, located on Laxmi Road. But here's what makes this fascinating: "Back then, all the jewellers were based in the Sonya Maruti area and people could not understand why I wanted to set up my shop up on Laxmi Road, which had just been constructed then."

This wasn't just geographic expansion—it was a bet on urban planning and demographic shifts. Anant, who would later be known affectionately as Dajikaka, chose Laxmi Road because it was close to the Peth areas, the traditional residential neighborhoods. He was essentially betting that customers would prefer convenience over tradition, that they would choose a modern storefront over the crowded traditional jewellery market.

The management structure that emerged reveals how Indian family businesses handle growth without fragmenting. The Pune branch was managed by Anant, Vishwanath Gadgil, and Laxman Gadgil, while the Sangli branch was overseen by Hari, the son of Vasudev Gadgil, and Shankar, Anant's elder brother. This wasn't a split—it was a federation, with each branch maintaining the PNG brand while operating with relative autonomy.

What's remarkable is how the Raja of Sangli captured the essence of PNG's business philosophy in 1958: "They treat me like a common man and the common man like a King, basically with the same sincerity and that is the secret of their success". This wasn't just flattery—it was identifying a core competitive advantage that would matter even more in post-independence, democratic India.

The Pune branch's success validated Anant's contrarian bet. Within years, Many people now tell me that we have been responsible in bringing Sonya Maruti to Laxmi Road. In other words, PNG didn't just join the market—it moved the market. This is the kind of market-making power that modern retail chains spend millions trying to achieve.

But success brought its own complications. For over five decades, the Pune and Sangli branches operated as a unified brand with separate management structures—a delicate balance that worked as long as family relationships remained harmonious. The cracks began to show as the business grew and new generations entered the picture.

In 2012, the Pune and Sangli branches formally separated, with the Pune operations continuing under the name P. N. Gadgil & Company. This wasn't just a business split—it was the dismantling of an 180-year-old unified legacy. The demerger created multiple PNG entities, each claiming lineage to the original 1832 founding, each carrying forward the trust capital built over generations, but now as competitors rather than collaborators.

The separation reveals a fundamental tension in family businesses: how do you scale trust? The original PNG model worked because customers knew the Gadgil family personally, or at least knew of them. But as the business expanded, as new stores opened, as family branches diverged, maintaining that personal connection became increasingly difficult. The 2012 split wasn't just about business disagreements—it was about the impossibility of maintaining unified family governance across multiple generations and geographies.

IV. The Modern Avatar: Saurabh Gadgil's Corporate Vision (2013-2020)

The post-2012 demerger period represents PNG's most dramatic transformation—from a traditional family-run jewellery business to a modern corporate entity with Silicon Valley-style ambitions. The architect of this metamorphosis was Saurabh Gadgil, born in Pune into the family of jeweler-businessman Vidyadhar Gadgil, whose grandfather Dajikaka had started the Pune branch in 1958.

Saurabh joined his family-owned business, PNG Jewellers, in 1998 when the company operated as a partnership firm. Think about that timing—1998 was when India's economy was just beginning to feel the effects of liberalization, when organized retail was still a foreign concept, when family businesses were starting to question whether their traditional models could survive in a globalizing world.

For 16 years, Saurabh observed, learned, and waited. Then came 2014—the inflection point. After Anant Gadgil's death in 2014, his son and grandson, including Saurabh Gadgil, inherited a portion of the business. This wasn't just inheritance; it was an opportunity to reimagine what a 182-year-old jewellery business could become.

The restructuring that followed was surgical in its precision. He later restructured the organization into a corporate entity and oversaw its geographic expansion into cities including Pune, Nashik, and Kolhapur, as well as international markets such as the UAE and the United States. This wasn't just about opening new stores—it was about building a scalable business model that could work beyond the traditional trust radius of the Gadgil family name.

The incorporation of P N Gadgil Jewellers Limited in 2013 marked the formal beginning of this transformation. But what's fascinating is how Saurabh balanced modernization with tradition. After the death of his grandfather, Anant Gadgil (colloquially known as Dajikaka), in 2014, the company added 11 new retail locations. This rapid expansion would have been unthinkable in the old model where each store was personally overseen by a family member.

The celebrity strategy reveals Saurabh's understanding of modern brand building. During Gadgil's tenure, PNG Jewellers engaged Bollywood actors Madhuri Dixit, Raveena Tandon, and Salman Khan as brand ambassadors. This wasn't just about star power—it was about transferring trust from family reputation to celebrity endorsement, making PNG relevant to a generation that didn't personally know the Gadgil family.

In 2014, the company began operating a diamond manufacturing facility in Mumbai—a crucial vertical integration move that would improve margins and quality control. This was PNG entering the supply chain game, moving from pure retail to manufacturing-retail integration.

The franchise model introduction was perhaps the most radical departure from tradition. All stores are operated and managed by us, with 23 stores owned by us and 10 stores operated by franchisees under the Franchisee Owned and Company Operated ("FOCO") model. The FOCO model is brilliant in its simplicity—franchisees bring capital and local connections, PNG brings brand, systems, and inventory management. It's asset-light expansion with quality control.

In 2015, he partnered with actress Preity Zinta to open a P N Gadhil store in Fremont, California, and launched the Being Human Jewellery line in association with Salman Khan's charitable brand. The California store wasn't just international expansion—it was a bet on the Indian diaspora's desire for authentic Indian jewellery with modern retail experience.

The digital transformation during this period was comprehensive. E-commerce platforms, mobile apps, virtual try-ons—PNG was essentially building a tech stack that would make it competitive with any modern retail chain. This wasn't your grandfather's jewellery store anymore; it was becoming an omnichannel retail operation that happened to sell jewellery.

By 2020, the transformation was complete. What had started as a traditional family business was now a modern corporate entity with professional management, celebrity endorsements, franchise operations, international presence, and digital capabilities. The stage was set for the next big leap—going public.

V. The Business Model: Manufacturing to Retail Integration

To understand PNG's business model is to understand how jewellery retail actually works—and why most people get it wrong. This isn't a high-margin luxury goods business like watches or handbags. It's essentially a commodity transformation business with razor-thin margins, where trust is the product and gold is merely the medium.

The PNG group's presence in gold, silver and diamond jewellery business, introducing Temple Motifs, Contemporary Jewellery designs, Light Weight, Daily Wear and Designer Collections, reveals the first layer of sophistication. This isn't just about selling gold bars in pretty shapes—it's about understanding the psychological and cultural needs of Indian consumers across life stages and occasions.

The product portfolio architecture is worth dissecting. PNG operates across gold, silver, platinum, and diamond categories with multiple sub-brands—eight for gold jewellery collections, two for diamond jewellery, and two for platinum jewellery as of December 2023. Each sub-brand serves a specific customer segment or occasion: Saptam for traditional ceremonies, Swarajya for cultural pride, Rings of Love for modern romance, The Golden Katha for craftsmanship connoisseurs, Flip for the younger demographic, Litestyle for daily wear, Pratha for heritage designs, and Yoddha for statement pieces.

This portfolio strategy isn't random—it's a sophisticated response to the democratization of jewellery consumption in India. As middle-class incomes rise, jewellery purchasing has shifted from purely investment-driven (buy gold, store it) to consumption-driven (wear it, flaunt it, express yourself). PNG is essentially running multiple brands under one trust umbrella.

The store format economics reveal the operational sophistication. As of 2025, the company reported operating 53 outlets, of which 41 were company-owned and 12 franchise-operated. These outlets covered a combined retail area of over 145,000 square feet. The breakdown is telling: 19 large format stores (2,500+ sq ft), 11 medium format (1,000-2,500 sq ft), and 3 small format (less than 1,000 sq ft).

Each format serves a different purpose. Large format stores in prime locations act as brand flagships—they're experience centers where families spend hours selecting wedding jewellery. Medium format stores balance selection with accessibility. Small format stores are essentially brand outposts, maintaining presence in emerging micro-markets.

The FOCO (Franchisee Owned, Company Operated) model deserves special attention. Unlike typical franchise models where the franchisee runs operations, PNG maintains operational control while the franchisee provides capital and local connections. This gives PNG the benefits of asset-light expansion while maintaining quality control—crucial in a trust-based business where one bad customer experience can destroy decades of reputation.

Revenue composition tells the real story of transformation. The company's franchise operations segment, contributing 15.7% to its total revenue, grew 109% in Q1FY26, compared to the year-ago period. Its other segments, including B2B and corporate sales, contributed 10.1% to its total revenue The dramatic shift from B2B to retail—with retail now at 81.5%—represents a fundamental reimagining of the business model.

B2B jewellery business is essentially a working capital game with minimal margins. You're selling to other jewellers who know exactly what gold costs and will squeeze every basis point. Retail, on the other hand, allows for making charges (labor costs), design premiums, and most importantly, customer relationships that drive repeat purchases.

The manufacturing integration story starts with the diamond facility in Mumbai, established in 2014. This wasn't just backward integration—it was a margin expansion play. Diamond jewellery offers significantly higher margins than plain gold jewellery because the value addition is higher and price discovery is more opaque. By controlling diamond sourcing and cutting, PNG captured margins that would otherwise go to intermediaries.

The company's e-commerce business, representing 3.9% of total revenue, surged 126% YoY during the quarter under review, showcasing its "successful digital expansion and increasing online customer engagement". While 3.9% might seem small, the 126% growth rate suggests PNG is finally cracking the code on selling high-value jewellery online—no mean feat in a category where touch-and-feel has traditionally been paramount.

The working capital intensity of the business model is both its biggest challenge and its natural moat. Jewellery retail requires massive inventory investment—you need to stock enough variety to give customers choice, but every piece on display is essentially dead capital until sold. This capital intensity keeps fly-by-night operators out but also limits how fast even established players can grow.

What's brilliant about PNG's model is how it uses trust to accelerate inventory turns. Customers often buy jewellery for future events (weddings planned months ahead), allowing PNG to optimize inventory based on forward orders. The old jewellery exchange programs essentially provide cheap sourcing of raw material while deepening customer relationships.

The business model's evolution from 2013 to 2020 represents a masterclass in how traditional businesses can modernize without losing their essence. PNG didn't abandon its heritage—it institutionalized it, scaled it, and gave it a contemporary expression that resonates with both 60-year-old mothers-in-law and 25-year-old brides.

VI. The IPO Story & Market Entry (2024)

September 10, 2024. The opening bell at the Bombay Stock Exchange. Saurabh Gadgil, sixth-generation jeweller turned corporate chieftain, watches as the ticker symbol PNGJL appears on screens across India's financial markets. The culmination of 192 years of family enterprise crystallized into a four-letter code that institutional investors could punch into their Bloomberg terminals.

The IPO of ₹1100 Cr launched on 10-09-2024 to 12-09-2024 and the shares listed on BSE, NSE on 17-09-2024. But the real story isn't in these dates—it's in what happened between announcement and listing, a period that revealed whether Indian investors believed in PNG's transformation story.

The structure of the offering was telling: a fresh issue of equity shares approximately Rs 850 crore and an offer for sale (OFS) of equity shares of upto Rs 250 crore by promoter SVG Business Trust. The 850 crore fresh issue would fund expansion, while the 250 crore OFS allowed early investors some liquidity—a balanced approach that suggested confidence rather than exit.

The pricing strategy was crucial. At ₹456-480 per share, PNG was asking for a PE of 42.2x—aggressive for a retailer but arguably justified for a growing franchise model with 192 years of brand equity. The minimum lot size of 31 shares meant retail investors needed to commit at least ₹14,880—not prohibitive, but enough to ensure serious participation.

Then came the subscription window, and the market delivered its verdict with remarkable clarity. PNG Jewellers witnessed strong demand from investors in its Rs 1,100 crore IPO with oversubscription to the tune of 59.41x. The IPO received an oversubscription of 59.41x, driven by the portion of Qualified Institutional Buyers(QIBs) that oversubscribed by whopping 136.85x. Non Institutional Investors (NII) and Retail Individual Investors (RIIs) portions oversubscribed by 56.09x and 16.58x respectively.

The QIB oversubscription of 136.85x deserves special attention. These are the smartest money managers in India—mutual funds, insurance companies, foreign institutional investors. Their overwhelming interest suggested they saw something beyond just another regional jeweller going public. They saw a platform play in a fragmenting market, a trusted brand in a trust-deficit category, a franchise model in a capital-intensive business.

The grey market premium (GMP) added another layer of validation. As per Investo Grain, P N Gadgil Jewellers IPO last GMP is ₹345, last updated Sep 13th 2024 11:27 PM. With the price band of 480.00, P N Gadgil Jewellers IPO's estimated listing price is ₹825 (cap price + today's GMP). A GMP of ₹345 on an issue price of ₹480 implied a 72% premium—the grey market was essentially saying PNG was worth 50% more than what the company was asking.

September 17, 2024. Listing day. The moment of truth.

The public issue of P N Gadgil Jewellers IPO (PNGJL,544256) was offered at ₹480.00 per share and the ipo was listed at ₹830.00. It has delivered listing gain of 72.92%. As the minimum lot size was 31 shares, the IPO has offered Rs 10850.00 per lot return on listing.

The 73% listing premium was spectacular by any measure. To put this in context, most IPOs consider a 10-15% pop successful. PNG's debut suggested the market believed the company had deliberately underpriced itself—either out of conservatism or to ensure a successful listing that would create positive momentum.

But then came the reality check. After opening at a premium of 73-74% on BSE and NSE, the P N Gadgil Jewellers overall gains on the exchanges were between 75-77% before the stock corrected to end in red. The stock price ended at Rs 792.80 apiece, down by 4.94% compared to the listing price of Rs 834 apiece on BSE.

This intraday reversal—from 77% gains to closing in the red versus listing price—revealed the two-sided nature of PNG's market entry. Yes, there was enormous interest, but there was also profit-booking pressure from investors who had made 70%+ returns in a week. The correction was healthy, even necessary—it separated the flippers from the believers.

The capital allocation strategy revealed through IPO proceeds tells us where management sees opportunity. The Company proposes to utilize the Net Proceeds towards funding the following objects: Funding expenditure towards setting up 12 new stores in Maharashtra (New Stores); Repayment or pre-payment, in full or part, of certain borrowings availed by the Company; and General corporate purposes.

Twelve new stores might seem modest, but in the jewellery business, each store is a significant capital commitment. More importantly, the focus on Maharashtra reveals a depth-over-breadth strategy—dominate the home market before expanding nationally. The debt repayment component would improve return ratios and reduce interest burden, crucial for a working capital-intensive business.

The post-IPO market cap of approximately ₹7,800 crores placed PNG in an interesting position. Not large enough to compete with Titan (market cap over ₹2,00,000 crores) on scale, but large enough to have access to capital markets for growth. Not small enough to be a takeover target, but not so large that growth wouldn't move the needle.

What the IPO really achieved was optionality. With public currency, PNG could now pursue acquisitions of smaller regional chains. With improved visibility, they could attract better franchise partners. With quarterly scrutiny, management would be forced to professionalize further. With employee stock options, they could attract talent from larger competitors.

The IPO timing was also strategic. Gold prices were near all-time highs, creating wealth effect for existing inventory. The Indian wedding market was recovering post-COVID. Organized retail was gaining share from unorganized players due to GST and hallmarking requirements. PNG went public at possibly the best time in a decade for an organized jewellery player.

But perhaps the most interesting aspect of the IPO was what it meant for the family. Post-IPO, Saurabh Vidyadhar Gadgil, Radhika Saurabh Gadgil, and SVG Business Trust are the promoters of the company, maintaining 83.1% shareholding. This high promoter holding sent a clear message—the family wasn't cashing out; they were inviting public investors to join their journey.

VII. Competition & Market Position

Second-largest organized jewellery player in Maharashtra as of January 2024, and the fastest growing jewellery brand amongst the key organized jewellery players in India, based on the revenue growth between Fiscal 2022 and Fiscal 2024. These superlatives matter, but they also hide a more nuanced competitive reality.

The Indian jewellery market is a ₹5-6 lakh crore behemoth where organized players control just 35% of the market—up from 20% in FY19. Tanishq, Titan's crown jewel, entered the scene in the early 2000s and revolutionised how people shopped for jewellery by building trust. Tanishq noticed that India's jewellery market was mostly unorganised — about 95%, to be exact.

In this transforming landscape, PNG occupies a fascinating middle ground. Titan holds 3.2% of the organised jewellery market in India, which is led by Kalyan Jewellers India Pvt. While this data point seems to contradict Titan's perceived dominance, it reveals how fragmented even the organized segment remains. Tanishq has enjoyed higher margins because of the higher share of diamond-studded jewellery in its product mix and market share owing to its expansive presence with 475 stores across India than most of its rivals.

The competitive dynamics are shifting rapidly. Since last year, at least three new regional brands—West Bengal's Senco Gold and Kerala's Kalyan Jewellers and Malabar Gold & Diamonds—have popped up around Tanishq stores. Kalyan Jewellers has been gaining market share through expanding its store network by 70% to 217 stores within the last two years.

PNG's Maharashtra fortress strategy starts to make sense in this context. Maharashtra leads the retail spending in India and accounted for approximately 15% of the overall retail spend on jewellery in India in Fiscal 2023. Rather than dilute focus by going national immediately, PNG is doubling down on dominating India's wealthiest state—a market larger than most countries' entire jewellery sectors.

The CAGR story is particularly impressive. Its CAGR for revenue from operations for the period between Fiscal 2022 and Fiscal 2024 was 54.63%. The company achieved an EBITDA growth of 39.78% between Fiscal 2022 and Fiscal 2024, which is the second highest in key organized jewellery players in India. This isn't just growth—it's explosive expansion that suggests PNG found a formula that resonates.

It also had the highest revenue per square feet in Fiscal 2024 among the key organized jewellery players in India. This metric is crucial—it suggests PNG stores are more productive than Tanishq's or Kalyan's, possibly due to better locations, superior customer service, or more effective merchandising.

The competitive responses reveal how seriously rivals take PNG. These newer brands are not just entering the market but also using Titan's own playbook to outshine it. The playbook—trust, transparency, certification, celebrity endorsements, mall presence—has become table stakes. The question is who executes better.

Organised players like Tanishq, Reliance Jewels, Kalyan Jewellers and others expanding their presence in malls. Jewellery storefronts in malls are becoming quite the crowd-pullers. These stores now take up nearly 5% of total mall space, a significant jump from just 1% two years ago. PNG's large-format store strategy aligns perfectly with this mall-ification of jewellery retail.

The diamond disruption adds another layer of competition. Kalyan's share of diamond-studded jewellery increased to 30% in the first quarter of the current fiscal year 2025 from 22% in the year ended March 2022. This shift to studded jewellery isn't just about product mix—it's about margin expansion. Diamond jewellery carries 15-20% margins versus 8-12% for plain gold.

Regional champions are proving formidable. While sales of GRT Jewellers and Tanishq stood at Rs 24,000 crore and Rs 23,000 crore, respectively, in the fiscal year 2022, that of Malabar were at Rs 32,000 crore. These aren't David vs. Goliath stories—these are Goliath vs. Goliath battles where PNG, despite its heritage, is actually the smaller player nationally.

The advertising arms race shows how competitive the market has become. Top branded jewellery chain Titan Company Limited increased its advertising expenditure from Rs380mn (US$6mn) in 2015 to Rs2,080mn (US$28.3mn) in 2021. Over the same period, Kalyan Jewellers increased its spend on advertising from Rs700mn (US$11mn) to Rs920mn (US$12.5mn). PNG's celebrity strategy with Madhuri Dixit and Salman Khan is its attempt to match this firepower without Titan's marketing budget.

What's PNG's competitive moat then? It's not scale (Titan wins), it's not national presence (Kalyan and Malabar win), it's not just heritage (every regional player claims that). PNG's moat is the depth of trust in Maharashtra specifically—multi-generational relationships where grandmothers, mothers, and daughters all buy from PNG, where the brand is woven into the cultural fabric of Maharashtrian life events.

The question isn't whether PNG can compete—it clearly can, as evidenced by its growth metrics. The question is whether its Maharashtra-first strategy will create an unassailable local fortress that generates enough cash flow to fund national expansion, or whether national players will eventually erode its home advantage through sheer scale and marketing might.

VIII. Financial Deep Dive

The numbers tell a story of transformation, but you have to read between the lines to understand what's really happening at PNG.

Revenue increased from Rs 2,555.63 crore in FY22 to Rs 6,110.94 crore in FY24, while PAT increased from Rs 69.51 crore to Rs 154.34 crore. That's a 139% revenue increase in two years—the kind of growth that software companies dream about but jewellery retailers rarely achieve. The CAGR for revenue from operations for the period between Fiscal 2022 and Fiscal 2024 was 54.63%.

But here's where it gets interesting: Operating profit margins witnessed a fall and down at 4.4% in FY24 as against 2.8% in FY23. Wait, margins improved but they're still at 4.4%? In the jewellery business, these aren't margins—they're rounding errors. This reveals the fundamental challenge of jewellery retail: you're essentially a logistics company moving gold from refineries to consumers, taking a small cut for the service.

The real story is in the return ratios. Return on Equity (ROE) improved and stood at 28.9% during FY24, from 25.1% during FY23. Return on Capital Employed (ROCE) improved and stood at 40.8% during FY24, from 33.0% during FY23. These are exceptional numbers—most retailers would kill for a 20% ROE, and PNG is delivering nearly 30%.

How do you generate 29% ROE with 4.4% operating margins? The answer lies in the turnover game. PNG had the highest revenue per square feet in Fiscal 2024 among the key organized jewellery players in India. Every square foot of retail space is sweated to generate maximum revenue. This is retail excellence—not through margin expansion but through operational efficiency.

The working capital story deserves special attention. P N Gadgil stands out for its excellent management of working capital and inventory, with 51 working capital days and 63 inventory days, much better than Kalyan and Senco. In a business where inventory is literally gold bars and diamond stones, managing 63 inventory days means PNG is turning its gold 5.8 times a year—remarkable for a category where customers often take months to make purchase decisions.

Net profit margins during the year grew from 2.1% in FY23 to 2.5% in FY24. That 40 basis point improvement might seem trivial, but on a ₹6,000 crore revenue base, it translates to ₹24 crores of additional profit. In the jewellery business, basis points matter because the volumes are so large.

The cash flow dynamics reveal the working capital intensity of the business. Cash flow from operating activities (CFO) during FY24 stood at Rs 63 million on a YoY basis. Yes, you read that right—a ₹6,000 crore revenue business generated just ₹6.3 crores in operating cash flow. This isn't a red flag; it's the nature of a rapidly growing jewellery business where every rupee of growth requires working capital investment.

The balance sheet transformation is striking. Current assets rose 44% and stood at Rs 12 billion, while fixed assets rose 15% and stood at Rs 3 billion in FY24. The 4:1 ratio of current to fixed assets shows this is fundamentally an inventory business, not a real estate play. Unlike mall retailers who sink capital into store build-outs, PNG's capital is in the gold and diamonds sitting in their stores.

Geographical concentration adds another dimension to the financial analysis. About 68% of its total FY24 revenue came from Pune, making it vulnerable to regional disruptions. This concentration is both a strength (deep market penetration) and a weakness (limited diversification). From an investor perspective, you're essentially betting on the continued prosperity of Pune's affluent class.

The peer comparison is revealing. While its sales and profits are smaller than companies like Kalyan and Senco Gold, P N Gadgil shows strong financial efficiency, with a high ROE (28.88%) and RoCE (27.31%). However, its profit margins are thinner, with an EBITDA margin of 4.54% and a PAT margin of 2.53%, lower than its peers who have margins between 3-8%.

This margin differential isn't necessarily bad—it could reflect PNG's competitive pricing strategy to gain market share, or its focus on high-turnover plain gold jewellery versus higher-margin studded pieces. The fact that PNG generates superior returns despite lower margins suggests operational excellence that competitors haven't matched.

The dividend policy, or lack thereof, is telling. The company has not declared any dividends for the reported periods. This isn't stinginess—it's capital allocation discipline. In a business growing at 50%+ CAGR, every rupee retained can generate 30% ROE. Paying dividends would be value-destructive when you can reinvest at such high returns.

Finance costs increased by 30.6% YoY, reflecting the working capital expansion needed to fund growth. In the jewellery business, you essentially need to buy inventory (gold) upfront and wait for customers to buy it. The 30% increase in finance costs on 139% revenue growth shows improving working capital efficiency—PNG is funding more revenue with proportionally less debt.

The IPO valuation at 42.2x P/E seemed rich, but post-listing, the P/E ratio, at the current price of Rs 707.6, stands at 62.2 times. The market is essentially saying PNG's growth story is worth a 50% premium to IPO pricing. Whether this is euphoria or justified optimism depends on PNG's ability to maintain its growth trajectory while improving margins.

IX. Growth Strategy & Future Challenges

The ambition is staggering: PNG plans to open 25 stores in FY26 with a Rs 400–500 crore investment, targeting 150 stores by March 2028 via owned and franchise formats. From 53 stores to 150 in four years—that's essentially tripling the store count, requiring PNG to open a new store every 10 days for the next four years.

But here's what makes this expansion strategy sophisticated: During our IPO journey last year, we clearly articulated our approach to expansion: it must be strategic, profitable and meaningful. That word "profitable" is crucial—PNG isn't chasing growth for growth's sake. Each store needs to be accretive to returns from day one.

The geographic strategy reveals a fundamental shift. The expansion strategy will center on key growth markets such as Maharashtra, where the company maintains a leadership position, as well as high-potential regions like Uttar Pradesh and Madhya Pradesh. This isn't just geographic expansion—it's following the money trail of India's economic development. UP and MP represent massive untapped markets with rising disposable incomes but limited organized jewellery presence.

The localization strategy shows deep market understanding. Our aim is to offer approximately 70 per cent jewellery specifically curated for local market preferences, including a significant focus on studded jewellery segments like kundan, polki, diamonds, and precious gemstones, reflecting its strong demand identified in central and northern India. The remaining 30 per cent will comprise PNG's classic and bestselling designs. This 70-30 split is brilliant—enough localization to feel relevant, enough standardization to maintain operational efficiency.

The Litestyle sub-brand launch targeting younger consumers reveals PNG's attempt to solve the generational challenge. Consumer preferences are evolving towards lightweight and studded jewelry, prompting an expansion of retail presence. Young Indians don't want their grandmother's heavy gold sets—they want Instagram-worthy pieces they can actually afford and wear daily.

The franchise acceleration is remarkable. Revenue contribution from franchise operations rose 109% YoY, accounting for 15.7% of Q1 FY26 revenue. The FOCO model is proving its worth—franchisees are bringing capital and local connections while PNG maintains operational control. This allows PNG to expand faster than pure company-owned growth would permit while maintaining quality standards.

Digital transformation continues to surprise. E-commerce jumped 126% to contribute 3.9%. While still small in absolute terms, the growth rate suggests PNG is finally cracking the code on selling high-value jewellery online—possibly through virtual try-ons, easy EMI options, or leveraging trust in the PNG brand to overcome the touch-and-feel barrier.

The festive performance validates the strategy. The company recorded its highest-ever single-day festive sales on Akshaya Tritiya, achieving ₹1,395.3 million, a 35.1% increase from the previous year. In the jewellery business, festivals are everything—they drive 40-50% of annual sales. PNG's ability to capture increasing festive wallet share suggests strong brand resonance.

But challenges loom large. Gold price volatility remains the elephant in the room. When gold prices rise, demand typically falls as customers wait for corrections. PNG needs to manage this through innovative schemes, exchange programs, and possibly lightweight jewellery that maintains affordability despite high gold prices.

Competition is intensifying. Kalyan Jewellers is eyeing over 25% revenue growth in the 2026 financial year, plans to open 160 new exclusive brand outlets. Every major player is expanding aggressively, fighting for the same prime retail locations, the same customers, the same talent pool. PNG's 25 stores per year looks modest compared to Kalyan's 160.

The working capital challenge will intensify with expansion. Each new store requires ₹15-20 crores of inventory investment. 25 new stores means ₹375-500 crores locked in inventory alone, not counting store fit-outs, staff, marketing. This is why the IPO proceeds and operational cash flow generation become crucial.

Regional concentration risk persists. About 68% of its total FY24 revenue came from Pune. Even with expansion into UP and MP, Maharashtra will likely contribute 50%+ of revenues for years. Any economic slowdown in Maharashtra, any regional disruption, could disproportionately impact PNG.

The talent challenge is underappreciated. Each store needs trained staff who understand jewellery, can build customer relationships, can handle high-value transactions. Finding and training such talent in new markets where PNG has no brand presence will be challenging.

The same-store sales growth of 8% is respectable but not spectacular. As the store base matures, PNG will need to drive higher SSSG to maintain overall growth momentum. This requires constant innovation in products, marketing, and customer experience.

The make-or-buy decision on manufacturing adds complexity. PNG operates a diamond facility in Mumbai but sources most gold jewellery from karigars (artisans). As volumes grow, should PNG integrate further backward? Or stay asset-light and focus on retail?

Consumer financing is becoming crucial. Young consumers want to buy jewellery but can't afford lump-sum payments. PNG's ability to offer attractive EMI schemes, possibly through fintech partnerships, could be a differentiator.

The sustainability angle is emerging. Younger consumers care about ethical sourcing, conflict-free diamonds, recycled gold. PNG's 192-year heritage gives it credibility, but it needs to articulate its sustainability story better.

Technology adoption remains critical. From inventory management systems that optimize stock across stores to AI-powered design recommendations, PNG needs to continue investing in technology to remain competitive.

The multi-generational opportunity is unique to PNG. Many of our loyal patrons spanning multiple generations have migrated and settled across central and northern India. These diaspora customers become brand ambassadors in new markets—a natural advantage that new-age brands can't replicate.

X. Playbook: Lessons from a 192-Year Journey

The PNG story isn't just about one company—it's a masterclass in how family businesses can navigate the treacherous journey from tradition to modernity without losing their soul. The lessons embedded in this 192-year journey read like a playbook for any business trying to build enduring value.

Lesson 1: Trust as Currency In 1914, when flood victims returned to find their valuables intact at PNG's Sangli store, they discovered something more valuable than gold—absolute trust. This isn't just a heartwarming anecdote; it's the foundation of a business model. In the jewellery business, you're not selling products; you're selling trust. Every transaction is essentially a customer saying, "I trust you with my life savings." PNG understood this when modern MBAs were still centuries away from being born.

The trust economy works differently than the transaction economy. Trust compounds—each satisfied customer becomes a walking testimonial, each generation that buys from you makes the next generation more likely to do the same. But trust is also fragile—one incident of selling impure gold, one broken promise, and decades of reputation can evaporate.

Lesson 2: The Art of Family Business Transitions Most family businesses die in the third generation. PNG is in its sixth, going on seventh. How? The answer lies in how they've handled succession. The 1874 decision to rename the business after grandson Purshottam wasn't nepotism—it was strategic succession planning, making it clear that the business would outlive any individual.

The 2012 split between Pune and Sangli branches could have been a disaster. Instead, both branches thrived separately. Sometimes, the best way to preserve a family legacy is to divide it thoughtfully rather than forcing unity that breeds resentment. PNG chose pragmatism over dogma.

The transition from Anant (Dajikaka) to Saurabh represents another model—from patriarch to professional. Saurabh joined in 1998 but didn't take charge until 2014. Sixteen years of apprenticeship in your own family business—that's patience modern corporations could learn from.

Lesson 3: Regional Dominance vs. National Expansion Trade-offs PNG's Maharashtra-first strategy challenges conventional wisdom about scale. While competitors rushed to plant flags nationally, PNG chose depth over breadth. Second-largest organized jewellery player in Maharashtra might not sound as impressive as "national player," but it's more profitable.

Regional dominance creates a virtuous cycle: deeper customer relationships → better understanding of local preferences → more targeted inventory → higher inventory turns → better returns → more capital for local expansion. It's the In-N-Out Burger model applied to Indian jewellery.

The risk, of course, is concentration. But PNG's response—gradual expansion into adjacent markets (UP, MP) with similar cultural contexts—shows how to expand without losing focus. They're not trying to sell Tamil Nadu-style temple jewellery in Punjab.

Lesson 4: Managing Commodity Risk in a Consumer Business Jewellery retail is a bizarre business—you're selling a consumer product where 90% of the cost is a volatile commodity (gold). Imagine if Apple's iPhone costs fluctuated 20% monthly based on silicon prices. That's PNG's reality.

PNG's approach—focus on making charges, design premiums, and inventory turns rather than gold price speculation—shows maturity. They're not trying to be commodity traders; they're trying to be value-added retailers. The shift from B2B (low margin, high volume) to retail (higher margin, lower volume) reflects this philosophy.

Lesson 5: Brand Heritage as Competitive Moat In an age where startups talk about "building brand," PNG has 192 years of it. But heritage can be a double-edged sword—it can mean trustworthy or it can mean outdated. PNG's genius was in making heritage feel contemporary.

The celebrity endorsements (Madhuri Dixit, Salman Khan) weren't about abandoning tradition—they were about making tradition aspirational for a new generation. The sub-brands (Litestyle for youngsters, Swarajya for patriots) show how to segment without fragmenting the master brand.

Lesson 6: The Franchise Model in Luxury Retail Franchising luxury seems oxymoronic—how do you maintain premium positioning when you don't control the stores? PNG's FOCO model squares this circle. Franchisees own the real estate and provide capital, but PNG controls operations.

This isn't the McDonald's model where franchisees run everything. It's more like the Apple Store model where every detail is controlled centrally. The 109% growth in franchise revenues validates this approach—franchisees are voting with their capital that the model works.

Lesson 7: Digital Transformation Without Digital Destruction Many traditional retailers were destroyed by e-commerce. PNG's 126% e-commerce growth shows adaptation, but at 3.9% of revenues, it shows restraint. They understand that jewellery buying is still primarily an offline, emotional, family experience.

PNG's digital strategy isn't about moving sales online—it's about using digital to enhance offline. Virtual try-ons drive store visits. WhatsApp catalogs enable browsing before buying. The website builds trust before the transaction. It's omnichannel done right.

Lesson 8: The Capital Allocation Masterclass No dividends despite profits. 83% promoter holding post-IPO. Debt repayment prioritized from IPO proceeds. These aren't random decisions—they reflect sophisticated capital allocation.

When you can reinvest at 30% ROE, paying dividends is value destructive. When you're growing at 50% CAGR, diluting promoter holding too much removes skin in the game. When interest costs eat into margins, debt repayment is the highest return investment.

Lesson 9: Culture as Strategy "They treat me like a common man and the common man like a King"—the Raja of Sangli's 1958 observation captures PNG's cultural secret. In a status-conscious society, PNG's egalitarian service model was revolutionary.

This isn't just good customer service—it's a political statement about post-independence India where merit matters more than birthright. It's a business model that says every customer's money is equally green. In a country with vast income inequality, this positioning is both moral and profitable.

Lesson 10: The Institutionalization of Trust The biggest challenge for any family business is institutionalizing what came naturally to founders. How do you teach a 25-year-old store manager to care about customer relationships the way the founder's family did?

PNG's answer: systems and processes that embed values. The FOCO model ensures quality control. The company-operated structure ensures consistent service. The sub-brand architecture ensures targeted offerings. The IPO governance ensures professional management. Trust is no longer person-dependent—it's process-dependent.

These lessons transcend jewellery retail. They apply to any business trying to build long-term value in a short-term world, any family business trying to professionalize without losing its soul, any regional player wondering whether to go national. PNG's playbook isn't just about selling gold—it's about turning tradition into sustainable competitive advantage.

XI. Bull vs. Bear Case

Bull Case: The Decade of PNG

The bull case for PNG starts with a simple observation: India's jewellery market is undergoing a once-in-a-generation transformation from unorganized to organized retail, and PNG is perfectly positioned to capture disproportionate value from this shift.

Consider the macro backdrop: organized jewellery currently represents just 35% of the market, up from 20% five years ago. If this trend continues—and there's every reason to believe it will accelerate with GST compliance, hallmarking requirements, and changing consumer preferences—organized players could capture 50-60% share within a decade. That's roughly ₹2-3 lakh crores of market share up for grabs.

PNG's 192-year heritage provides an unfair advantage in this land grab. While new-age brands spend millions building trust, PNG inherits it. Multi-generational customer relationships mean lower customer acquisition costs, higher lifetime values, and natural word-of-mouth marketing that money can't buy.

The franchise model breakthrough changes PNG's growth trajectory. With 109% growth in franchise revenues and the FOCO model proven, PNG can now expand at Silicon Valley speeds with Marwari capital efficiency. Each successful franchise becomes a case study attracting more franchisees—a virtuous cycle that could see PNG adding 50+ stores annually within 2-3 years.

Maharashtra's economic dominance provides a fortress of cash flow. As India's richest state contributing 15% of national GDP, Maharashtra's jewellery market alone is larger than most countries'. PNG's leadership position here provides stable cash flows to fund national expansion without diluting margins through excessive competition.

The operational metrics suggest PNG has cracked the code: highest revenue per square foot among organized players, 63-day inventory turns versus 100+ for competitors, 30% ROE despite 4% operating margins. This operational excellence creates a flywheel—better metrics → more capital → faster expansion → greater scale benefits → even better metrics.

Young Indian consumers represent a generational opportunity. The Litestyle sub-brand targeting millennials and Gen Z could be PNG's Trojan horse into national markets. These consumers care less about which state a brand comes from and more about design, affordability, and social media appeal.

The technology investments are starting to pay off. 126% e-commerce growth suggests PNG is finally bridging the online-offline divide. As AR/VR technology improves, virtual try-ons could make PNG accessible to millions of consumers far from physical stores.

Financial leverage is declining. Using IPO proceeds for debt repayment means more profits flow to the bottom line. Combined with improving margins from the shift to retail and studded jewellery, PNG could see PAT margins expand from 2.5% to 4-5% over five years—effectively doubling profits even without revenue growth.

The management quality under Saurabh Gadgil has been proven. From partnership to corporation, from single-city to multi-state, from family-run to professionally-managed—every transition has been handled expertly. This execution track record suggests future challenges will be similarly navigated.

If PNG executes its 150-store plan by FY28, maintains 25-30% revenue CAGR, expands into 3-4 new states successfully, and margins expand even modestly, the company could be worth ₹25,000-30,000 crores within five years—a 3-4x return from current levels.

Bear Case: The Challenges Ahead

The bear case starts with a sobering reality: PNG is a subscale player in a bruising battle against giants. Titan has ₹2,00,000 crore market cap and pan-India presence. Kalyan is adding 160 stores annually. In this war of attrition, PNG's ₹8,000 crore market cap and regional concentration look vulnerable.

The Maharashtra concentration is a ticking time bomb. 68% revenue from Pune alone means any local disruption—economic slowdown, political instability, competitive intensity—could devastate PNG. The recent Shiv Sena split and political uncertainty in Maharashtra should worry investors more than they apparently do.

Gold price volatility could destroy demand. Gold has rallied from ₹40,000 to ₹70,000 per 10 grams in recent years. If prices correct 20-30%, customers will defer purchases waiting for further falls. If prices spike another 50%, affordability will collapse. PNG has no control over its primary raw material cost.

The margin structure remains concerning. 2.5% PAT margins mean there's no room for error. One inventory write-down, one failed store expansion, one competitive pricing war, and profits could evaporate. Competitors with deeper pockets can sustain losses longer than PNG can sustain competition.

Execution risk in new markets is significant. PNG has thrived in Maharashtra where everyone knows the brand. In UP or MP, PNG is nobody—just another jewellery store. Building brand awareness, customer trust, and operational excellence in new markets typically takes years and burns cash.

The working capital intensity limits growth. Each new store needs ₹15-20 crore inventory investment. 150 stores means ₹2,250-3,000 crores locked in inventory. PNG's current net worth is ₹500 crores. The math doesn't work without massive equity dilution or dangerous leverage.

Technology disruption could blindside PNG. What if a tech-first player like BlueStone or Melorra figures out online jewellery? What if Reliance leverages its retail footprint to offer jewellery at predatory prices? What if Chinese lab-grown diamonds destroy natural diamond demand? PNG's traditional model has no answer to these disruptions.

Management depth beyond the family is untested. Yes, Saurabh has done well, but PNG is still essentially a family enterprise. As the company scales, it needs professional managers who can think strategically, execute flawlessly, and navigate complexity. The bench strength isn't proven.

Regulatory risks loom large. The government's frequent changes to gold import duties, GST rates, and hallmarking requirements create constant uncertainty. One adverse regulation—say, a wealth tax on jewellery purchases—could cripple demand overnight.

The franchise model could backfire. Franchisees are partners when times are good but can become liabilities when times are tough. If gold prices crash and franchisees face losses, they might abandon stores, refuse inventory purchases, or damage the brand through poor service.

The IPO valuation at 62x P/E prices in perfection. Any earnings disappointment, any growth slowdown, any margin compression, and the stock could halve. The 73% listing pop has created expectations that PNG must now live up to quarter after quarter.

Consumer preferences are shifting to experiences over possessions. Young Indians increasingly prefer travel, dining, and entertainment over traditional jewellery. The cultural importance of gold is declining with each generation. PNG's entire business model assumes this trend reverses or stabilizes.

The Verdict

The bull-bear debate ultimately comes down to time horizon and risk tolerance. Over a 10-year period, the bull case seems stronger—India's jewellery market will formalize, organized players will win, and PNG's heritage positions it well. But the next 2-3 years could be volatile as PNG navigates expansion challenges, competitive pressures, and market cycles.

For believers in the India consumption story, PNG offers a differentiated play on rising affluence and cultural continuity. For skeptics, it's a subscale regional player in a brutal industry with structural challenges. The truth, as always, lies somewhere in between.

XII. Epilogue & Final Thoughts

Standing at the crossroads of its 193rd year, P N Gadgil Jewellers embodies the eternal paradox of Indian business: how to honor the past while embracing the future, how to remain local while going global, how to stay family while becoming corporate.

The transformation from Ganesh Gadgil's single shop in 1832 Sangli to Saurabh Gadgil's IPO in 2024 Mumbai isn't just a business success story—it's a meditation on what endures and what evolves in the endless churn of commerce. Gold, that immutable element, has been the constant. Everything else—the customers, the stores, the systems, even the family structures—has shapeshifted with time.

What would you do as CEO of PNG today? The answer isn't obvious. Push too hard on expansion and you risk destroying the operational excellence that makes PNG special. Move too slowly and you cede ground to aggressive competitors who won't show similar restraint. Focus too much on technology and you lose the human touch that defines PNG. Ignore technology and you become irrelevant to digital natives.

The strategic choices facing PNG mirror those facing India itself: How do you modernize without westernizing? How do you scale without losing soul? How do you compete globally while remaining rooted locally? There are no MBA case studies with clear answers, no consultants with proven playbooks.

Perhaps the answer lies in PNG's own history. The company has survived the Maratha Empire's decline, British colonialism, two world wars, independence, partition, economic liberalization, and demonetization. Each crisis forced adaptation without abandonment of core values. Each generation added its own layer to the palimpsest while preserving what came before.

The listing on NSE wasn't an ending—it was another beginning. Public market scrutiny will force PNG to be more transparent, more efficient, more growth-oriented. Quarterly earnings calls will replace family meetings as the rhythm of business. Professional managers will increasingly outnumber family members. The PNG of 2034 will be as different from today's PNG as today's is from 1832's.

Yet something essential will likely persist—call it culture, call it values, call it DNA. The trust that survived the 1914 floods, the egalitarian service that impressed the Raja of Sangli, the craftsmanship that turns metal into memory—these intangibles can't be replicated by competitors, can't be disrupted by technology, can't be destroyed by market cycles.

The jewellery business, at its core, is about marking life's moments—births, marriages, anniversaries, achievements. PNG has been witness to six generations of such moments. In a world accelerating toward digital everything, there's something profoundly grounding about a business that measures time in generations, not quarters.

For investors, PNG represents a bet on continuity in an age of disruption. For competitors, it's a reminder that heritage and modernity need not be mutually exclusive. For family businesses everywhere, it's proof that professionalization doesn't require abandoning family values. For India, it's a testament to enterprise that predates the nation itself.

The story of PNG Jewellers doesn't end with an IPO or a market cap or a store count. It continues every time a young couple walks into a PNG store to buy their first piece of jewellery together, every time a mother passes down a PNG necklace to her daughter, every time trust is chosen over transaction.

In the end, PNG's greatest achievement isn't surviving 192 years—it's remaining relevant for the next 192. The path forward won't be easy. The challenges are real, the competition is fierce, the market is unforgiving. But if history is any guide, PNG will adapt, evolve, and endure.

Because that's what family businesses do. They play the long game in a short-term world. They build for generations in a market obsessed with quarters. They create value that transcends valuation.

The bells at the Bombay Stock Exchange will ring for many IPOs. But few will carry the weight of history that PNG brings. Few will represent such a seamless blend of tradition and ambition. Few will embody the Indian business story quite so completely.

As we close this deep dive into PNG Jewellers, one thing becomes clear: this isn't just a company selling jewellery. It's a 192-year-old startup, a family corporation, a traditional disruptor, a local multinational. It's all the contradictions that make Indian business fascinating, all the paradoxes that make family enterprises unique, all the tensions that make transformation necessary.

The next chapter of PNG's story is being written now—in board rooms and stores, in factories and franchises, in Maharashtra and beyond. Whether it becomes a case study in successful transformation or a cautionary tale of ambition exceeding capability remains to be seen.

But one suspects that 50 years from now, 100 years from now, there will still be a PNG Jewellers. The form may change, the structure may evolve, the geography may expand. But the essence—trust, craftsmanship, relationships—will endure.

Because some things are more precious than gold. And PNG, after 192 years, knows exactly what they are.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube