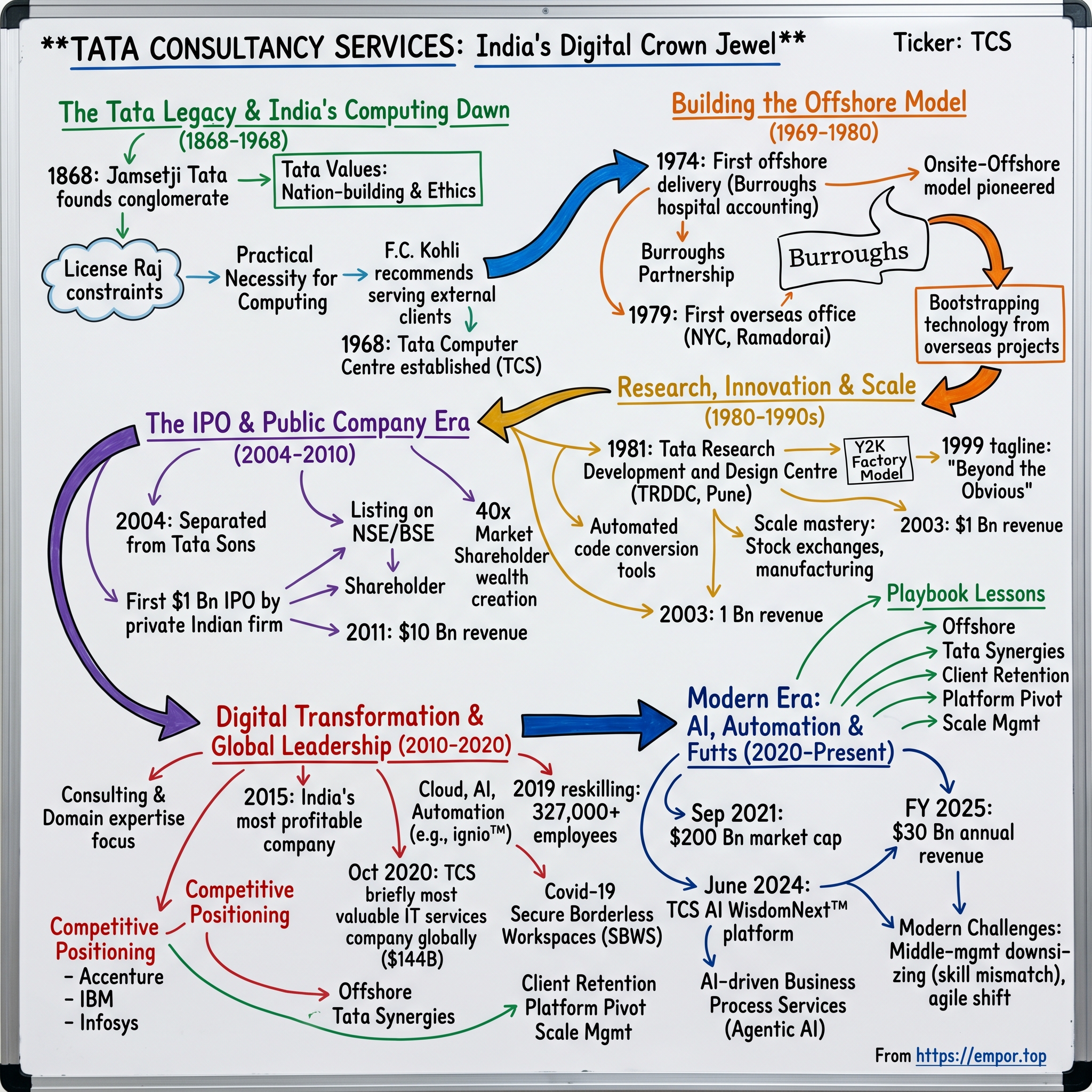

Tata Consultancy Services: India's Digital Crown Jewel

Introduction & Episode Roadmap

The story of Tata Consultancy Services reads like a meticulously crafted business thriller, one where a small division processing punched cards in 1968 transforms into India's most valuable company with a market capitalization exceeding ₹16 lakh crore. With over 600,000 employees spread across 46 countries, TCS has become synonymous with India's rise as a global technology powerhouse. But the journey from manual data processing to artificial intelligence leadership wasn't just about technological evolution—it was about reimagining how global business itself could be conducted.

The question that drives this narrative isn't simply how TCS grew, but how it fundamentally rewrote the rules of the technology services industry. In October 2020, when TCS briefly surpassed Accenture to become the world's most valuable IT services company at $144 billion, it marked not just a corporate milestone but the culmination of a 52-year journey that paralleled India's own transformation from a closed economy to a digital services superpower.

This is a story of three distinct revolutions: India's economic liberalization, the global IT services explosion, and the digital transformation era. Each phase demanded different strategies, different leadership styles, and different bets on the future. The company that began by helping Tata Steel manage its inventory would eventually advise Fortune 500 CEOs on their digital strategies, manage the technology infrastructure of global banks, and help governments reimagine citizen services.

What makes TCS particularly fascinating is how it maintained its cultural DNA while scaling to unprecedented heights. The Tata values of nation-building and ethical business practices, inherited from a 156-year-old conglomerate founded during British colonial rule, somehow translated seamlessly into Silicon Valley boardrooms and European banking centers. This wasn't just about outsourcing or cost arbitrage—it was about creating an entirely new business model that would be copied by hundreds of companies but never quite replicated with the same success.

The themes that emerge from TCS's story—the power of patient capital, the advantage of emerging market innovation, the importance of investing ahead of the curve, and the delicate balance between growth and values—offer lessons that extend far beyond the technology industry. As we stand at another inflection point with artificial intelligence threatening to disrupt the very foundations of the IT services industry, understanding how TCS navigated previous technological disruptions becomes even more critical.

The Tata Legacy & India's Computing Dawn (1868–1968)

The roots of TCS stretch back to 1868, when Jamsetji Nusserwanji Tata founded what would become India's largest conglomerate with a trading company in Mumbai. Jamsetji's vision was audacious for its time: he believed Indian businesses could compete globally while contributing to nation-building. This philosophy of combining profit with purpose would become the genetic code of every Tata enterprise, including the technology services company that wouldn't be born for another century.

By the 1960s, the Tata Group had already established itself as India's industrial backbone. Tata Steel was Asia's first integrated steel plant, Tata Power was pioneering hydroelectric projects, and Tata Motors was manufacturing trucks and buses. But India's post-independence economy was struggling with what would later be called the "License Raj"—a complex system of licenses, regulations, and red tape that made business expansion nearly impossible. Foreign exchange was scarce, imports were restricted, and technology transfer was viewed with suspicion.

It was in this constrained environment that India's computing journey began. The country's first computer, a British-made HEC-2M, arrived at the Indian Statistical Institute in Kolkata in 1955. By the mid-1960s, only about a dozen computers existed in the entire nation, mostly in government research institutions. The private sector's access to computing was virtually non-existent, and when companies needed data processing, they had to rely on manual methods or expensive time-sharing arrangements with the few available machines.

The Tata Group's entry into computing was driven by practical necessity rather than grand vision. In 1966, Tata Sons, the group's holding company, was grappling with the administrative complexity of managing dozens of companies across diverse industries. The group needed better ways to handle accounting, inventory management, and data processing. Initially, they considered purchasing computer time from existing installations, but the costs were prohibitive and availability limited.

The breakthrough came through an unlikely source: Faqir Chand Kohli, a young engineer who had joined Tata Electric Companies in 1951. Kohli had spent time at MIT in the early 1950s, where he had been exposed to early computing machines. By the mid-1960s, he had risen through the ranks to become deputy general manager at Tata Electric and was known for his systematic thinking and technological curiosity. When Tata Sons began exploring computing options, Kohli was asked to evaluate the feasibility of establishing an in-house computing division.

Kohli's recommendation was bold: instead of just meeting the Tata Group's internal needs, why not create a division that could serve external clients as well? He argued that the economies of scale would justify the investment in expensive computing equipment, and the external revenue would help subsidize the group's own computing needs. More importantly, he saw an opportunity to build India's indigenous computing capability at a time when the country was almost entirely dependent on foreign technology.

In 1968, Tata Sons established the Tata Computer Centre as a division within the company. The initial team consisted of just twelve people, including Kohli and a handful of engineers recruited from India's premier engineering institutions. The division's first computer was an ICL 1903, imported from the UK at considerable expense and bureaucratic effort. The machine, which would seem primitive by today's standards, was housed in a specially constructed air-conditioned room at Bombay House, the Tata Group's headquarters.

The early projects were modest but significant. The first major assignment was developing a payroll system for Tata Steel, which employed over 40,000 people and was struggling with manual payroll processing. The team also developed an inventory management system for Tata Engineering and Locomotive Company (now Tata Motors) and a reconciliation system for the Central Bank of India. These projects required the team to work closely with clients to understand their business processes, a practice that would become a hallmark of TCS's approach.

What distinguished the Tata Computer Centre from other early computing initiatives in India was its focus on developing local expertise rather than depending on foreign consultants. Kohli instituted a rigorous training program, sending engineers to ICL facilities in the UK and later to Burroughs Corporation in the US. But the goal was always to bring the knowledge back and adapt it to Indian conditions. This emphasis on knowledge transfer and localization would prove crucial in the coming decades.

The late 1960s also saw the centre experimenting with what would later be called "systems integration." Instead of just writing code, the team was designing entire business processes, selecting appropriate hardware, developing custom software, and training client personnel. This end-to-end approach was unusual for the time and reflected Kohli's belief that computing was not just about technology but about transforming how businesses operated.

By 1968, when Tata Computer Centre was formally incorporated as Tata Consultancy Services, the foundation for India's IT revolution had been laid. The new company had a dozen clients, mostly from within the Tata Group but increasingly from outside. Revenue was modest—just a few crore rupees—but the expertise being built was invaluable. The team had learned to work with multiple hardware platforms, had developed competence in various programming languages, and most importantly, had begun to understand how to apply technology to solve business problems.

The timing of TCS's establishment was fortuitous in ways that wouldn't become apparent for years. The late 1960s saw the beginning of the global shift from hardware-centric to software-centric computing. IBM's decision to unbundle software from hardware in 1969 created the independent software industry. Meanwhile, the rise of minicomputers was making computing accessible to smaller organizations. TCS was positioned to ride both waves, though the journey would require navigating India's challenging regulatory environment and overcoming skepticism about an Indian company's ability to compete globally.

The seeds planted in those early years—the emphasis on training and knowledge building, the focus on business transformation rather than just technology implementation, the commitment to indigenous capability development, and the patient, long-term approach inherited from the Tata Group—would all prove crucial as TCS embarked on its next phase: proving that software development could be successfully delivered from thousands of miles away.

Building the Offshore Model (1969–1980)

The 1970s marked a pivotal decade that would reshape not just TCS but the entire global IT services industry. When TCS won a project to convert a hospital accounting system from Burroughs Medium Systems COBOL to Burroughs Small Systems COBOL, they faced an extraordinary challenge: they didn't have a Burroughs computer. The team built an in-house tool to write the code and then shipped it to the US, creating the first offshore delivery project. This wasn't just technical ingenuity—it was the birth of a business model that would generate trillions of dollars in value over the next five decades.

The company pioneered the global delivery model for IT services with its first offshore client in 1974. Burroughs Corporation wanted healthcare software that would be packaged with their computers. Kohli convinced them that Burroughs and TCS could work together, and the two signed what can be called the first IT outsourcing contract of India for US$24,000. The audacity of this project cannot be overstated. TCS didn't have a single Burroughs machine then. It was a giant leap of faith to deliver the software package without compatible hardware. But TCS went ahead and developed the whole system on an available ICL computer (acquired from Life Insurance Corporation when its communist unions had prevented its use perceiving a threat to their jobs).

The technical solution was brilliant in its simplicity and prescient in its implications. The Hospital Accounting system conversion from a Burroughs Medium Systems COBOL to a Burroughs Small Systems COBOL—which the TCS team managed without a Burroughs computer, using a filter in assembly language on their ICL 1903 to parse the source code—was historic for being the first recorded instance of an offshore software delivery, done using automation, 45 years ago. This filter essentially acted as a cross-compiler, translating code written for one system to run on another—a technique that would become fundamental to software portability and platform independence.

The success of this project opened doors that had been previously unimaginable for an Indian company. This year marked the start of TCS' partnership with Burroughs to distribute and support Burroughs products in India and to build software for export to various Burroughs units and clients across the world. The partnership was more than a commercial arrangement; it was a knowledge transfer mechanism that would accelerate TCS's technical capabilities exponentially. Engineers were sent to Burroughs facilities in Detroit and other locations, where they learned not just programming but also American business practices, project management methodologies, and client interaction protocols.

By 1975, TCS was ready to take on more complex projects. S Mahalingam—then a young chartered accountant who was part of a six-member team of coders based in Mumbai with two members onsite—wrote specifications for a financial accounting software package for Burroughs computers, which was sold to a couple of building societies in the UK. It was TCS' first-ever project involving the complete software development lifecycle. This marked a crucial evolution from simple coding tasks to end-to-end software development, including requirements gathering, design, implementation, testing, and deployment.

The onsite-offshore model that TCS pioneered during this period was revolutionary in several ways. First, it addressed the visa and immigration challenges that made it difficult for Indian engineers to work in the US for extended periods. By keeping the bulk of the development team in India and sending only a small contingent to the client site, TCS could circumvent these restrictions while maintaining close client contact. Second, the model leveraged time zone differences to create what would later be called "follow-the-sun" development, where work could progress continuously as teams in different time zones handed off tasks to each other.

The economic logic was equally compelling. Indian engineers, even the best graduates from IITs and other premier institutions, were earning a fraction of what their American counterparts made. But this wasn't just about labor arbitrage. The offshore model allowed TCS to invest in training, infrastructure, and process improvements that would have been impossible if they were competing on a purely onsite basis. They could afford to have redundant teams, extensive documentation, and rigorous quality control processes—luxuries that high-cost locations couldn't justify.

In 1979, TCS established its first sales office in New York, headed by S Ramadorai. One of the first major clients was the Institutional Group Information Corporation (IGIC). IGIC, a data centre for ten banks which catered to two million customers in the US, assigned TCS the task of maintaining and upgrading its computer systems. The IGIC project was transformational for several reasons. It was TCS's first large-scale engagement with the American financial services industry, a sector that would become its largest vertical. It also introduced TCS to the complexities of mission-critical systems—the IGIC systems processed millions of transactions daily, and any downtime could cost millions of dollars.

The project required TCS to master IBM mainframe technology, which was becoming the standard for large enterprises. Kohli wanted to build technological capability through overseas projects and transfer it back to India—an approach TCS management referred to as 'bootstrapping' and continued to apply till 1990 when Indian economy opened up. This bootstrapping strategy was sophisticated. In the 1970s, Kohli could foresee the decline of Burroughs business and felt the need to acquaint his TCS team to IBM machines. Eventually, the team gained so much proficiency in software building on both frameworks that TCS accepted a US-based bank consortium's project to migrate their software from Burroughs to IBM. In mid-1980s, when several companies were migrating from Burroughs to IBM, TCS capitalized on its dual expertise and grabbed those opportunities.

The learning curve was steep and sometimes painful. Early projects often ran over budget and schedule as the team grappled with communication challenges, cultural differences, and the complexities of distributed development. Conference calls were expensive and often of poor quality. Documentation had to be exceptionally detailed since face-to-face clarifications were rare. The team developed elaborate protocols for code reviews, testing, and deployment to ensure quality despite the geographic separation.

But these challenges forced TCS to develop capabilities that would become competitive advantages. They created sophisticated project management frameworks that could track distributed teams' progress in real-time. They invested heavily in documentation and knowledge management systems, ensuring that expertise gained in one project could be leveraged across the organization. They developed cultural training programs to help engineers understand not just the technical requirements but also the business context of their American and European clients.

In 1979, TCS set up its first overseas sales office in New York, headed by S Ramadorai, and bagged their first and largest offshore project out of the Delhi office for Swiss National Bank (SNB). The project teams realized the value of meticulous planning to meet deadlines with precision and emphasis on quality. The Swiss National Bank project was particularly significant because it demonstrated that TCS could handle projects for the most demanding clients in the world. Swiss banks were known for their exacting standards and conservative approach to technology adoption. Success with SNB opened doors to other European financial institutions and established TCS's reputation for reliability and quality.

The infrastructure challenges of this period cannot be understated. International communication relied on telex machines and expensive international phone calls. Sending code or documentation required physical shipment of magnetic tapes or punched cards, which could take days or weeks. The team had to be extraordinarily disciplined about version control and change management since rolling back changes or fixing bugs required another round of international shipping. Power outages were common in India, requiring backup generators and careful scheduling of critical work. The Indian government's import restrictions made it difficult to acquire the latest hardware and software tools, forcing the team to innovate with whatever was available.

Despite these constraints, or perhaps because of them, TCS developed a culture of frugal innovation that would serve it well in future decades. Engineers learned to write highly optimized code because computing resources were scarce. They developed robust testing procedures because fixing bugs after deployment was expensive and time-consuming. They created detailed documentation because knowledge transfer couldn't rely on informal conversations. These practices, born of necessity, would later be codified into methodologies like the Capability Maturity Model (CMM) that TCS would champion in the 1990s.

By late 1980s, the company was the largest consultancy outfit in India, bigger than the next 10 software companies put together. But size alone doesn't capture the transformation that had occurred. In just over a decade, TCS had proven that software development could be successfully delivered from halfway around the world, that Indian engineers could compete with the best in the world, and that the combination of low costs, high quality, and round-the-clock development could create a compelling value proposition for global clients.

The foundation laid in the 1970s—the technical capabilities, the client relationships, the delivery processes, and most importantly, the confidence that Indian companies could compete globally—would prove invaluable as TCS entered the 1980s. The next decade would bring new challenges: increased competition from other Indian companies copying the offshore model, the need to move up the value chain from coding to design and consulting, and the imperative to build a global brand. But the blueprint had been established. The offshore model wasn't just about cost savings; it was about reimagining how global business could be conducted in an increasingly connected world.

Research, Innovation & Scale (1980–1990s)

The 1980s would prove to be TCS's crucible decade, where theoretical concepts about offshore delivery were transformed into industrial-scale operations. The decade began with a bold vision that would seem audacious even by today's standards. On October 8, 1981, the Tata Research Development and Design Centre was inaugurated at 1 Mangaldas Road, Pune, on the campus of the Tata Management Training Centre (TMTC). TRDDC was established as a software research centre in Pune, India, by Tata Group's TCS in 1981. This wasn't just another development center—it was India's first dedicated software research facility, an investment in the future at a time when most Indian companies were struggling to meet immediate delivery commitments.

The creation of TRDDC represented a fundamental shift in how TCS viewed itself. Under F.C. Kohli's leadership, the company was making a statement: Indian companies could not just execute projects designed elsewhere but could innovate at the cutting edge of computer science. The facility was headed by E.C. Subbarao, a prominent materials scientist from IIT Kanpur, who began applying computational materials engineering for Tata Steel, which then dominated the group's business. Indeed, research in TCS was joined at the hip with business from its inception. Soon Kesav V. Nori joined TRDDC from TIFR and began adapting compiler technology to TCS' fledgling software services business, successfully automating many of the conversion projects that TCS won through the 1980s.

The decision to house TRDDC in Pune was strategic and purposeful. Pune had the twin benefit of being almost a metro and a centre for higher education with many academic institutions and research laboratories. The location also kept it separate from the day-to-day functioning of TCS, which Mr Kohli thought was important. This physical separation was crucial—it allowed researchers to work on long-term projects without the pressure of immediate billability, a luxury few service companies could afford.

The timing of TRDDC's establishment coincided with significant technological shifts globally. The personal computer revolution was beginning, with IBM launching its PC in 1981. Object-oriented programming was emerging as a new paradigm. Relational databases were becoming commercially viable. Networks were evolving from proprietary protocols to more open standards. TRDDC positioned TCS to not just react to these changes but to anticipate and shape them.

Tools and processes developed at TRDDC helped TCS accomplish some of its most challenging projects in the early days: scaling millions of transactions for stock exchanges and clearing and settlement systems, developing a factory model for the Y2K problem, or automating large-scale manufacturing processes. One of TRDDC's earliest breakthroughs was in automated code conversion. As companies worldwide grappled with migrating legacy systems to newer platforms, TRDDC developed tools that could automatically analyze source code, identify patterns, and generate equivalent code for different platforms. This wasn't just find-and-replace; it involved deep semantic analysis and sophisticated transformation rules.

The scale and complexity of creating an end-to-end advanced system to manage customer relationships for Western Trust and Savings Limited (WTSL) in 1981, which involved 135-person-years' effort, gave TCS an in-depth knowledge of the retail banking sector, the know-how to execute large projects, and mastery over IBM mainframe technology. This project was significant not just for its size but for its scope. TCS wasn't just coding to specifications; they were designing the entire system architecture, defining business processes, and creating a complete banking solution that would process millions of transactions daily.

In 1981, TCS created India's first client-dedicated offshore development centre, established for Tandem. The Tandem ODC (Offshore Development Center) model would become the template for thousands of similar centers across India over the next decades. The concept was elegantly simple: create a secure, dedicated facility that functioned as an extension of the client's own development team. The ODC would have dedicated communication lines, follow the client's development processes, and often even observe the client's work hours despite the time difference.

But execution was complex. Each ODC required significant upfront investment in infrastructure, training, and security. TCS had to convince clients that their intellectual property would be safe thousands of miles away in a country many executives had never visited. They had to demonstrate that the quality of work would match or exceed what could be done locally. And they had to manage the human challenges of distributed teams long before video conferencing or instant messaging existed.

Between 1982-88, TCS saw an explosion of new technological inventions. These included the Advanced Data Dictionary (ADDICT), a global repository of project information with a vast and advanced nomenclature, giving users a holistic view of a project; the Falcon (Fast Access Local Computer Network), the first fault-tolerant, multi-user, multitasking Windows-type capability; and Casepac, a computer-aided software engineering tool for IBM mainframes. These weren't academic exercises—each tool emerged from real project needs and was refined through actual deployment.

Some of the tools grew into products and platforms, including Quartz (later BaNCS), MasterCraft, Rule Engines, and in recent years, ignio™ and digital twins. The evolution of these tools into products marked another transition for TCS. The company was learning to productize its innovations, creating repeatable solutions that could be deployed across multiple clients. This was particularly important in the financial services sector, where TCS was building deep domain expertise.

By 1987, the IBM mainframe Centre of Excellence was set up in Chennai with the installation of the imported IBM 3090 mainframe, making it the largest mainframe site in India for several years, thereby opening up IBM mainframe business opportunities for TCS. The acquisition of this mainframe was itself a story of persistence and ingenuity. Import restrictions made it nearly impossible to bring such equipment into India. TCS had to navigate complex bureaucracy, demonstrate national interest, and even commit to training government personnel to get the necessary approvals.

The Chennai center became a training ground for thousands of Indian engineers who would go on to become the backbone of the global IT industry. The IBM 3090 wasn't just a computer; it was a statement of intent. TCS could now bid for the largest, most complex projects in the world, confident that they had the infrastructure to deliver. The center ran 24/7, with multiple shifts of programmers working on projects for clients across time zones.

In the late 1980s, TCS was awarded a large, complex development project by SEGA, the Swiss financial depository, clearing and settlement organization. The SECOM project for SIS SegaInterSettle was groundbreaking in its complexity. It wasn't just about processing transactions; it was about creating a real-time system that could handle the settlement of securities trades with zero tolerance for errors. A single bug could potentially cause millions of dollars in losses. The project required TCS to understand not just technology but also the intricate details of Swiss securities law, international banking regulations, and complex financial instruments.

The success of SECOM opened doors across European financial markets. TCS followed this up with System X for the Canadian Depository System and also automated the Johannesburg Stock Exchange. Each of these projects added to TCS's reputation as a company that could handle mission-critical systems for the world's most demanding clients. The company was no longer competing on cost alone; it was winning projects based on technical capability and domain expertise.

The talent development initiatives of this period were equally impressive. TCS established elaborate training programs that went far beyond technical skills. Engineers learned about international business practices, financial markets, and industry-specific regulations. The company created career paths that allowed engineers to specialize in particular domains or technologies, building deep expertise that could command premium rates. The investment in people was substantial—new hires often underwent six months of training before being assigned to projects, an expense that few companies could justify.

The quality focus intensified during this period. TCS began implementing rigorous software engineering practices, inspired by methodologies developed at TRDDC. Code reviews became mandatory. Testing protocols were standardized. Documentation requirements were enforced religiously. These practices, which seemed bureaucratic to some, proved their worth when TCS became one of the first companies to achieve higher levels of the Capability Maturity Model (CMM) certification in the 1990s.

The business model evolution during the 1980s was subtle but significant. TCS moved from body-shopping (providing individual contractors) to project-based work to managed services. Each evolution required new capabilities and offered better margins. By the end of the decade, TCS was managing entire IT departments for some clients, taking responsibility not just for development but for operations, maintenance, and continuous improvement.

The geographic expansion accelerated. From a single office in New York, TCS expanded to multiple US cities, established a presence in the UK and continental Europe, and began exploring opportunities in Asia-Pacific. Each new geography brought unique challenges—different business cultures, regulatory requirements, and competitive landscapes. TCS learned to adapt its delivery model to local conditions while maintaining global standards.

In its first few years, TRDDC's Process Engineering Lab built: an award-winning TB testing kit; eco-friendly cements that use soda ash and recyclable waste. The TRDDC mission did not limit itself to computer science or information technology. The proficiency in innovation with materials was displayed further with 'Sujal'. TRDDC had been working on rice husk for several applications including tiles, construction material and a water purifier. An ash-based water filter that used rice husk, Sujal delivered clean and safe drinking water and helped improved the health of many villagers in India as part of TCS' CSR efforts. These non-IT innovations demonstrated the breadth of TCS's research ambitions and its commitment to social impact, a value inherited from the Tata Group's nation-building ethos.

The 1990s began with India's economic liberalization in 1991, a watershed moment that would transform TCS and the entire Indian IT industry. The dismantling of the License Raj, the opening up of the economy to foreign investment, and the gradual relaxation of import restrictions created new opportunities and challenges. Competition intensified as new players like Infosys and Wipro expanded aggressively. Multinational corporations like IBM and Accenture, which had largely ignored India, began establishing operations there.

But TCS was well-prepared for this new era. The capabilities built during the 1980s—the research infrastructure, the quality processes, the global delivery network, the domain expertise, and most importantly, the confidence to compete with anyone—positioned the company to not just survive but thrive in the liberalized economy. The approaching Y2K crisis would provide an unexpected catalyst, but TCS's transformation from an Indian company doing international business to a truly global corporation was already well underway.

Anticipating the Y2K bug and the introduction of the unified European currency (Euro), Tata Consultancy Services developed a factory model for Y2K conversion. The company also created software tools to automate the conversion process and facilitate implementation by third-party developers and clients. The factory model wasn't just about scale; it was about industrializing software development. TCS created specialized tools that could scan millions of lines of code, identify date-related fields, and automatically convert them to Y2K-compliant formats. The company established dedicated Y2K factories in multiple Indian cities, each capable of processing enormous volumes of code with assembly-line efficiency.

The numbers were staggering. By 1999, TCS had remediated over 300 million lines of code for more than 700 clients. The company had deployed over 15,000 engineers on Y2K projects, making it one of the largest coordinated software efforts in history. The revenue impact was transformational—Y2K projects contributed over $500 million in revenues in the late 1990s, providing the capital needed for TCS's next phase of growth. More importantly, Y2K proved to skeptical Western corporations that Indian companies could handle their most critical systems. The successful transition through December 31, 1999, without major incidents involving TCS-remediated systems, cemented the company's reputation for reliability.

In late 1999, TCS introduced Decision Support System (DSS) solutions to the domestic market. In 1999, the company also registered its first tagline, "Beyond the Obvious." This tagline captured TCS's evolution from a services provider to a strategic partner that could help clients reimagine their businesses. The company was no longer content with just executing projects; it wanted to help define them.

The IPO & Public Company Era (2004–2010)

The transformation of TCS from a division of Tata Sons to a publicly traded company in 2004 marked not just a corporate milestone but a watershed moment for Indian capital markets. In 2004, TCS made history with the first $1 billion initial public offering (IPO) by a private-sector company in India. The corporatization process began on April 1, 2004, when TCS was formally separated from Tata Sons and established as an independent entity. This restructuring, which had been contemplated for years, was finally triggered by the recognition that TCS needed access to capital markets to fund its ambitious growth plans and provide liquidity to its parent company.

TCS was corporatized into a separate company with effect from 1st April 2004. Following a hugely successful IPO in July 2004, it was listed on the NSE and BSE, in India, on August 25, 2004. The IPO structure was meticulously designed to balance multiple objectives. Public Issue of 55452600 Equity Shares of Re. 1 each for cash at a price of Rs. 850 per Equity Share aggregating Rs. 4713.47 crore, consisting of a Fresh Issue of 22775000 Equity Shares of Re. 1 each by Tata Consultancy Services. This represented a combination of fresh capital raising for the company and an offer for sale by existing shareholders, primarily Tata Sons.

The IPO price band was set between Rs 775 and Rs 900. The final price of Rs 850 was determined through a book-building process that saw overwhelming demand from institutional investors globally. The IPO was oversubscribed multiple times, with foreign institutional investors particularly eager to get exposure to India's IT services sector. The enthusiasm wasn't misplaced—TCS represented not just a company but a proxy for India's entire knowledge economy transformation.

TCS was listed on August 25, 2004, at Rs 1,076, a 26% premium to the issue price of Rs 850 per share. The strong listing day performance reflected market confidence, but few could have predicted the wealth creation that would follow. In 20 years, the company's m-cap has seen exorbitant gains and has moved from Rs 41,000 crore to now top Rs 16.4 lakh crore. This 40-fold increase in market capitalization would make TCS one of the most successful wealth creators in Indian corporate history.

The IPO proceeds were deployed strategically. The fresh capital wasn't needed for immediate operations—TCS was already highly profitable and cash-generative. Instead, the funds were used to strengthen the balance sheet, invest in new delivery centers, fund acquisitions, and most importantly, signal to global clients that TCS was now a transparent, well-governed public company subject to rigorous disclosure norms. This last point was crucial for winning large deals from Fortune 500 companies who were increasingly scrutinizing their vendors' financial stability and governance practices.

The immediate post-IPO period saw TCS accelerate its transformation from a services company to a strategic partner for global enterprises. Revenue growth, which had been strong in the pre-IPO years, accelerated further. The company crossed $1 billion in revenues even before the IPO, but the pace of growth post-listing was remarkable. Its headcount grew from 33,774 in FY04 to a staggering 606,998 as of June 30, 2024. This 18-fold increase in workforce reflected not just organic growth but a fundamental scaling of ambition.

Geographic expansion was equally impressive. At the time of its IPO, TCS had a presence in 32 countries and delivery centres in 10. Today, the company operates in 55 countries, with over 300 offices and more than 200 delivery centres. Each new geography represented not just a sales office but often included delivery centers, innovation labs, and local hiring to meet client requirements for onshore presence. The company was evolving from an offshore provider to a global delivery network that could seamlessly blend onshore, nearshore, and offshore resources.

The public company discipline brought unexpected benefits. Quarterly earnings calls forced management to articulate strategy clearly and consistently. The scrutiny from analysts and investors pushed the company to improve operational metrics continuously. Return on equity, operating margins, and utilization rates became not just internal metrics but public scorecards. This transparency, initially seen as a burden by some in management, proved to be a competitive advantage as clients increasingly preferred working with financially transparent partners.

The period from 2004 to 2010 saw several strategic initiatives that would define TCS's future trajectory. In July 2005, Tata Infotech, which was until then a different IT subsidiary of Tata Sons, merged with TCS in a stock swap deal. This consolidation brought additional capabilities in product engineering and telecom services while eliminating internal competition within the Tata Group. Later that year, TCS changed its tagline from "Beyond the Obvious" to "Experience Certainty". This new tagline reflected a shift in positioning—from innovation and creativity to reliability and predictability, qualities that resonated with risk-averse enterprise clients.

The company's approach to shareholder returns established it as a model for Indian corporates. TCS has been returning cash to shareholders consistently from the time of listing, through interim dividends every quarter, final dividends at the year-end and an occasional special dividend. This consistent dividend policy, unusual for a growth company, reflected the Tata Group's philosophy of sharing prosperity with all stakeholders. It also attracted a different class of investors—those seeking steady income along with capital appreciation.

The bonus share issuances further enhanced shareholder value. The first instance occurred on 16th June 2009, when the company issued a 1:1 bonus, effectively doubling the number of shares held by each investor. Nearly a decade later, on 31st May 2018, TCS repeated this generous gesture, issuing another 1:1 bonus. These bonus issues, while not creating economic value per se, improved liquidity and made the stock more accessible to retail investors, broadening the shareholder base.

In 2006, TCS developed an ERP system for the Indian Railway Catering and Tourism Corporation. By 2008, its e-business operations were generating over US$500 million in annual revenue. These domestic projects, while smaller than international engagements, were strategically important. They demonstrated TCS's commitment to India's development, built relationships with government agencies that would prove valuable for future projects, and served as references for similar work in other emerging markets.

The financial crisis of 2008-09 tested TCS's resilience as a public company. While revenues and profits continued to grow, the pace slowed considerably. The stock price fell sharply along with global markets. Some analysts questioned whether the offshore model would survive as clients cut IT budgets and brought work in-house. But TCS's response demonstrated the strength of its business model. Instead of cutting costs indiscriminately, the company invested in training, developed new service lines around cost optimization, and actually gained market share as competitors struggled.

The period also saw TCS make strategic bets on emerging technologies and business models. In 2011, TCS entered the small and medium enterprises market with cloud-based solutions. This was a departure from the company's traditional focus on large enterprises, but management recognized that cloud computing would democratize access to enterprise software, creating opportunities in previously unaddressable market segments. The TCS iON platform, launched for small and medium businesses, would eventually serve hundreds of thousands of users and establish the company as a credible player in the SaaS market.

On the final trading day of 2011, it surpassed RIL to achieve the highest market capitalization of any India-based company. In the 2011–12 fiscal year, TCS achieved annual revenues exceeding US$10 billion for the first time. Crossing $10 billion in revenues was more than a psychological milestone. It put TCS in an exclusive club of global IT services companies, alongside IBM, Accenture, and a handful of others. The achievement came just eight years after the IPO when revenues were around $2 billion, representing a five-fold growth that few companies of this size achieve.

TCS's mcap crossed $100 billion in 2018, 13.5 years after the IPO. It took only four more years to double its mcap to $200 billion. This acceleration in value creation reflected not just financial performance but the market's recognition of TCS's strategic positioning for the digital era. The company had successfully navigated the transition from labor arbitrage to capability-led growth, from offshore delivery to global presence, from IT services to business transformation.

The governance standards established during this period set benchmarks for Indian corporates. Independent directors brought global perspectives and challenged management thinking. Audit committees ensured financial integrity. Compensation committees aligned executive pay with long-term value creation. These weren't just compliance requirements but genuine efforts to build a world-class institution that could outlive its founders.

For individual investors who participated in the IPO, the returns were extraordinary. With 28 shares now in their portfolio, the value of the investment stands at about Rs 1,27,400 (Rs 4,550 x 28 shares). What began as a Rs 5,950 investment in 2004 has transformed into a sum over 21 times that amount, highlighting the power of long-term investing. But beyond individual wealth creation, TCS's public listing created a template for Indian companies aspiring to global leadership—demonstrating that transparency, governance, and consistent execution could create enormous value for all stakeholders.

Digital Transformation & Global Leadership (2010–2020)

The decade from 2010 to 2020 would prove to be TCS's most transformative period, as the company evolved from a traditional IT services provider to a digital transformation partner for the world's largest enterprises. This wasn't merely growth—it was metamorphosis. The company that had built its reputation on operational excellence and cost efficiency now positioned itself at the forefront of technological disruption, helping clients navigate cloud computing, artificial intelligence, and the fundamental reimagination of business models.

The journey began with strategic foresight that preceded market recognition by years. In 2011, when cloud computing was still viewed with skepticism by many enterprises, TCS entered the small and medium enterprises market with cloud-based solutions. The launch of TCS iON represented more than product diversification—it was a fundamental rethinking of how technology could be delivered and consumed. Instead of the traditional model of large, multi-year implementations, iON offered pay-per-use functionality that could be deployed in weeks. This platform would eventually serve hundreds of thousands of small businesses and educational institutions, creating a new revenue stream while building capabilities that would prove invaluable for enterprise cloud transformations.

In 2013, the company moved from 13th to 10th place on the list of global IT services companies by revenue. This ascent wasn't just about size—it reflected TCS's evolution from an offshore provider to a peer of companies like IBM and Accenture. The transformation required massive investments in consulting capabilities, domain expertise, and local presence in key markets. TCS began hiring management consultants from top-tier firms, technology architects from Silicon Valley companies, and industry experts from the sectors they served. The goal was ambitious: to sit across the table from CEOs and boards, not just IT departments.

In July 2014, it became the first Indian company to exceed ₹5 trillion (US$81.93 billion) in market capitalization. This milestone reflected investor confidence in TCS's ability to navigate the shift from labor arbitrage to innovation-led growth. The market recognized that digital transformation wasn't a threat to TCS's business model but an opportunity for even greater value creation. Companies needed partners who could help them reimagine their businesses for the digital age, and TCS had positioned itself perfectly for this role.

In January 2015, TCS became India's most profitable company, ending Reliance Industries Limited's 23-year streak. This achievement was particularly significant because it represented the triumph of knowledge work over traditional industry. A services company, with no physical products or natural resources, had become more profitable than oil refineries and petrochemical plants. It validated the vision of those who had argued that India's future lay in its intellectual capital rather than its natural resources.

The period saw TCS making strategic technology bets that would define its future. Cloud computing evolved from experimental pilots to mission-critical implementations. TCS didn't just help clients migrate applications to the cloud; they reimagined entire business processes for cloud-native architectures. The company developed deep partnerships with all major cloud providers—Amazon Web Services, Microsoft Azure, and Google Cloud Platform—while maintaining the flexibility to work across platforms. By 2019, cloud-related revenues were growing at over 30% annually, far outpacing overall company growth.

Artificial intelligence and automation became central to TCS's value proposition. The company's approach was pragmatic rather than futuristic. Instead of chasing artificial general intelligence, TCS focused on applying machine learning to specific business problems: predicting customer churn, optimizing supply chains, automating document processing. The MFDM™ framework which integrates Automation, Analytics and AI has been central to many core transformation deals. This Machine First Delivery Model wasn't just about cost reduction—it was about augmenting human capabilities and enabling new business models.

The development of ignio™, TCS's cognitive automation platform, exemplified this approach. Rather than replacing human workers wholesale, ignio focused on automating repetitive tasks and predicting system failures before they occurred. After many years of field deployment 'under the radar,' ignio would become a standalone business unit, generating hundreds of millions in revenue and transforming how enterprises thought about IT operations. The platform's ability to self-heal IT systems and predict outages resonated with enterprises struggling with increasingly complex technology landscapes.

In January 2017, TCS announced a partnership with Aurus, a payments technology company, to deliver payment solutions for retailers through TCS OmniStore, a pioneering unified store commerce platform. This wasn't just a technology partnership—it represented TCS's evolution into industry-specific platform development. Rather than just implementing others' software, TCS was creating its own intellectual property tailored to specific industry needs. The retail platform integrated online and offline channels, enabling retailers to compete with Amazon while maintaining their physical presence.

The same year, TCS China entered into a joint venture with the Chinese government. This bold move into the world's largest market required navigating complex geopolitical dynamics and regulatory requirements. The joint venture model, where TCS partnered with local entities, became a template for entering other challenging markets. It demonstrated TCS's ability to adapt its business model to local conditions while maintaining global standards.

Geographic expansion during this period was strategic rather than opportunistic. Growth was led by Europe (+15.9%) and MEA (+10.8%). The European market, in particular, became a showcase for TCS's transformation capabilities. Our participation in the growth and transformation spends of our customers is most evident in our sustained success in Continental Europe where our revenues have more than doubled in the last five years. European clients, often more conservative than their American counterparts, valued TCS's combination of technical expertise, process discipline, and competitive pricing.

The focus on digital transformation wasn't just external—TCS underwent its own digital metamorphosis. The company launched comprehensive reskilling programs to prepare its workforce for the digital era. By the end of 2019, TCS had trained 327,000+ employees in digital technologies. This wasn't token training but intensive skill development in areas like cloud architecture, data science, and agile methodologies. The Digital Learning platform offered multi-layered and multi-device learning formats, allowing employees to learn at their own pace while balancing project commitments.

The transformation of TCS's business mix was dramatic. Digital services, which barely existed at the beginning of the decade, grew to represent over 30% of revenues by 2020. More importantly, these services commanded higher margins and created deeper client relationships. A cloud migration project often led to application modernization, which led to data analytics implementations, which led to AI initiatives. TCS was no longer just a vendor but an innovation partner embedded in clients' strategic initiatives.

On 8 October 2020, TCS surpassed Accenture in market capitalization, becoming the world's most valuable IT company with a market capitalization of over $144 billion. This moment was fleeting—market capitalizations fluctuate daily—but symbolically powerful. An Indian company, started as a division processing punched cards, had become more valuable than the consulting giant that had defined the industry for decades. It validated the offshore model, the focus on engineering excellence, and the patient, long-term approach that characterized TCS's journey.

The COVID-19 pandemic that began in early 2020 became an unexpected accelerator of digital transformation. Years of digital adoption were compressed into months as businesses scrambled to enable remote work, digitize customer interactions, and build resilience into their operations. TCS's Secure Borderless Workspaces (SBWS) model, which the company had been developing for years, suddenly became mission-critical. Within weeks, TCS had transitioned over 400,000 employees to remote work, maintaining productivity and security while demonstrating the feasibility of distributed work at scale.

95% of the deals won by TCS between October 2020 and October 2021 were for its cloud and SaaS platforms. This statistic captured the fundamental shift in how enterprises were thinking about technology. The debate was no longer whether to move to the cloud but how quickly and comprehensively to do so. TCS's role evolved from implementing cloud migrations to architecting entire digital ecosystems that could scale dynamically, integrate seamlessly, and evolve continuously.

The company's thought leadership during this period was notable. The Business 4.0™ framework articulated how enterprises could leverage technology to achieve mass personalization, create exponential value, and embrace risk. Unlike academic frameworks, Business 4.0 was grounded in practical experience from thousands of client engagements. It provided a roadmap for digital transformation that resonated with business leaders struggling to navigate technological disruption.

In 2021, TCS underwent a millennial rebranding, and the company updated its tagline from "Experience Certainty" to "Building on Belief". This wasn't just cosmetic—it reflected a fundamental shift in how TCS viewed its role. "Experience Certainty" had emphasized reliability and predictability, crucial qualities for an IT services provider. "Building on Belief" signaled ambition, innovation, and partnership in creating the future. It acknowledged that in an era of constant change, success required not just execution but imagination and courage.

The platforms and products business, including its SaaS-based platforms, is valued at approximately $3 billion. This evolution from services to products represented a crucial diversification of TCS's business model. Products like BaNCS in banking, iON for small businesses, and industry-specific platforms generated recurring revenues, created competitive moats, and captured a larger share of value creation. Unlike services, which scaled linearly with people, products could scale exponentially with minimal incremental cost.

By 2020, TCS had fundamentally redefined what an IT services company could be. Revenue had grown from approximately $8 billion in 2010 to over $22 billion in 2020, but the transformation went far beyond financial metrics. The company had evolved from a provider of technical services to a partner in business transformation. It had shifted from labor arbitrage to innovation leadership. It had progressed from offshore delivery to global presence. Most importantly, it had demonstrated that companies from emerging markets could not just participate in technological revolutions but lead them.

Modern Era: AI, Automation & Future Bets (2020–Present)

The modern era of TCS, from 2020 to the present, represents both the culmination of decades of strategic positioning and the beginning of an entirely new chapter defined by artificial intelligence, automation, and unprecedented market dynamics. In September 2021, TCS recorded a market capitalization of US$200 billion, becoming the first Indian IT company to achieve this valuation. This milestone wasn't just symbolic—it represented the market's recognition that TCS had successfully navigated the transition from labor arbitrage to innovation leadership, from offshore delivery to global presence, and from IT services to business transformation partner.

The achievement was particularly remarkable given the context. It took nearly 13.5 years to get to $100 billion market cap, while the next $ 100 billion took 3.5 years, or a third of the time, a company executive stated. This acceleration reflected not just financial performance but a fundamental shift in how investors valued technology services companies. The pandemic had demonstrated that digital transformation wasn't optional but existential, and companies like TCS that could enable this transformation commanded premium valuations.

K Krithivasan, Chief Executive Officer and Managing Director, said "We are pleased to cross the $30 Billion in annual revenues and achieve a strong order book for the second consecutive quarter. The FY 2025 milestone of $30 billion in revenue represented a remarkable journey from the $1 billion achieved in 2003. But the composition of this revenue told an even more compelling story. Digital services, which barely existed a decade earlier, now dominated the portfolio. Cloud migrations, data analytics, artificial intelligence implementations, and cybersecurity services commanded higher margins and created deeper client relationships than traditional application development and maintenance.

The launch of TCS AI WisdomNext™ in June 2024 exemplified the company's strategic evolution. TCS AI WisdomNext™ is a platform that aggregates multiple generative AI (GenAI) and cloud services into a unified interface. It offers ready-to-deploy solution blueprints for rapid enterprise adoption of GenAI solutions. This wasn't just another product launch—it represented TCS's ambition to be at the forefront of the generative AI revolution that was transforming every industry.

The platform addressed a critical challenge facing enterprises: the bewildering array of AI models and tools available in the market. TCS AI WisdomNext helps businesses choose the right models and simplify the design of new business solutions using GenAI tools. It also enables businesses to reuse pre-existing components to accelerate the design. By aggregating multiple AI services into a single interface, TCS was positioning itself as the orchestrator of enterprise AI adoption, a role that could generate billions in revenue as companies scrambled to implement AI capabilities.

Early implementations demonstrated the platform's potential. Examples include fast-tracking sales for an outdoor advertising company in the US, with real-time inventory availability and quote generation with maps Integration; enhancing productivity and efficiency across the application migration and modernization lifecycle for a leading American insurance provider; and enhancing customer experience through a smart mortgage-assistant for a leading bank in the UK. These weren't proof-of-concepts but production deployments generating real business value.

The scale of TCS's AI ambitions was reflected in its training initiatives. The company had trained over 550,000 employees in basic AI skills and over 100,000 in advanced capabilities. This massive reskilling effort, perhaps the largest in corporate history, demonstrated TCS's commitment to AI-led transformation. But it also revealed the challenges of such a transition, as not all employees could successfully make the leap to new technologies.

The financial performance during this period reflected both opportunities and challenges. FY 25 Revenue $30.18 Bn, Growth +3.8% YoY, + 4.2% in CC showed respectable but not spectacular growth. The company was navigating a complex environment where clients were simultaneously excited about AI's potential and cautious about implementation costs and risks. Deal sizes in AI remained relatively small compared to traditional IT services, though the pipeline was growing rapidly.

Geographic performance showed interesting patterns. Growth led by strong double-digit growth in Regional Markets: + 37.2% YoY demonstrated TCS's success in diversifying beyond traditional markets. However, North America, which represented about 50% of revenues, showed signs of softness as enterprises reassessed their technology spending in an uncertain economic environment.

The partnership ecosystem evolved significantly during this period. TCS deepened relationships with all major cloud providers—Amazon Web Services, Microsoft Azure, and Google Cloud Platform—while maintaining platform neutrality. Announced strategic partnership with Google Cloud to enhance its AI and GenAI offerings for customers in the communication, media, and information services industry. These partnerships went beyond reselling or implementation; they involved co-innovation and joint solution development.

The business process services evolution was particularly noteworthy. This quarter we saw a good number of deals in Business Process services led by F&A, HR and CX practices. Key demand themes were AI driven transformation, operating model transformation, and first-time outsourcing. We are investing in building an Agentic AI farm with over 150 agents across F&A, Supply Chain, Sourcing & Procurement, HR and CX, to enable customers in their journey towards "Autonomous GBS". This represented a fundamental reimagination of business process outsourcing, from human-delivered services to AI-augmented operations.

The TCS AI for Business Study shows that 40% of the executives surveyed felt their companies needed to make many changes to take advantage of AI. This gap between AI's potential and enterprises' readiness created both opportunity and challenge for TCS. The company needed to not just implement technology but help clients transform their organizations, processes, and cultures to leverage AI effectively.

However, the modern era also brought unprecedented challenges. In July 2025, TCS announced that it would downsize its global workforce by 2%, or about 12,000 employees, primarily from middle- and senior-level positions, with CEO K. Krithivasan citing a "skill mismatch" as the reason. This announcement sent shockwaves through the industry, as TCS had historically been known for job security and minimal layoffs.

The CEO's explanation was revealing. Speaking to Moneycontrol, Krithivasan said, "This is not because of AI delivering 20% productivity gains. The layoffs are due to a skill mismatch and the inability to redeploy certain employees within the company's evolving business model. The clarification was important—this wasn't about AI replacing humans but about the changing nature of work requiring different skills.

He explained that some employees, particularly at senior levels, are finding it difficult to transition into more technology-focused roles. While TCS has invested heavily in AI training — over 5.5 lakh employees trained in basic AI and 1 lakh in advanced skills — reskilling has not always translated into redeployment, especially for senior professionals. This highlighted a harsh reality: in the AI era, experience alone wasn't enough; continuous learning and adaptation were essential.

The structural changes within TCS reflected broader industry trends. TCS is also undergoing a major structural shift, moving from the traditional "waterfall" project management model to a more agile, product-centric approach. This transition required not just new technical skills but a fundamental change in mindset—from sequential, documentation-heavy processes to iterative, collaborative development.

The new HR policies introduced during this period signaled a shift in how TCS managed its workforce. Recently, TCS revised its HR norms, mandating a minimum of 225 billable days in a year and reducing bench time to a maximum of 35 days. These changes reflected the pressure to maintain utilization rates and profitability in an environment where clients were demanding more value for their spending.

The support provided to affected employees demonstrated TCS's attempt to balance business needs with its values. Employees affected by this move will receive their due notice period compensation along with an additional severance package. TCS will also provide extended insurance coverage and outplacement support to help affected staff transition smoothly into new roles outside the company. This approach, while compassionate, couldn't fully mitigate the impact on employee morale and the company's reputation as a stable employer.

Looking at brand valuation, TCS continued to strengthen its position globally. 17 Jul - TCS ranked 20th in Brand Finance Tech 100, valued at $21.3B, highlighting AI leadership and global brand growth. The brand value of $21.3 billion positioned TCS as the second most valuable global IT services brand, a remarkable achievement for a company that started as a division of an Indian conglomerate.

The competitive landscape during this period became increasingly complex. Traditional competitors like Accenture, IBM, Infosys, and Wipro remained formidable, but new challenges emerged from multiple directions. Cloud providers like Amazon and Microsoft were moving up the value chain into consulting and implementation. AI-native startups were offering specialized solutions that competed with specific TCS offerings. Global systems integrators were investing heavily in AI capabilities. Even clients were building internal AI teams, potentially reducing their dependence on external partners.

The cybersecurity focus intensified during this period. This quarter, we continued to see good traction for Cybersecurity services. Our clients focused on Managed Detection & Response (MDR), Identity and Access Management and Governance, Risk & Compliance (GRC). We had good traction in Network Security, Cloud Security and GenAI for Cybersecurity. As digital transformation accelerated, security became not just a technical requirement but a business imperative, and TCS positioned itself as a trusted partner in this critical area.

The platform strategy continued to evolve beyond traditional IT services. In October 2021, N. Ganapathy Subramaniam, the COO of TCS, announced that its platforms and products business, including its SaaS-based platforms, is valued at approximately $3 billion. He noted that 95% of the deals won by TCS between October 2020 and October 2021 were for its cloud and SaaS platforms. This shift from services to platforms represented a fundamental change in business model—from linear growth tied to headcount to potentially exponential growth through software leverage.

The research and innovation investments continued to pay dividends. With 19 innovation labs across three countries and partnerships with leading universities and startups, TCS maintained its position at the cutting edge of technology development. The focus areas—quantum computing, blockchain, Internet of Things, edge computing, and of course, artificial intelligence—positioned the company for the next waves of technological disruption.

As we stand in 2025, TCS faces perhaps its most critical inflection point since the Y2K era. The generative AI revolution promises to fundamentally transform how software is developed, deployed, and maintained. The traditional model of large teams working on multi-year projects is giving way to AI-augmented development where smaller teams can achieve more in less time. The question isn't whether this transformation will happen but how quickly and comprehensively.

The recent workforce adjustments, while painful, reflect TCS's recognition that the future requires different capabilities than the past. The company that built its success on managing large-scale human resources must now excel at human-AI collaboration. The organization that perfected the offshore delivery model must now master the art of AI-augmented services. The firm that became synonymous with operational excellence must now become known for innovation and transformation.

Yet, the fundamental strengths that brought TCS to this point remain relevant. The company's engineering heritage, its process discipline, its client relationships built over decades, its financial strength, and most importantly, its ability to execute at scale—these remain powerful differentiators. The question is whether TCS can leverage these strengths while transforming fast enough to remain relevant in an AI-dominated future.

Playbook: Business & Operating Lessons

The TCS playbook represents one of the most successful business model innovations in modern corporate history. Over five decades, the company has developed and refined strategies that transformed not just TCS but the entire global technology services industry. These lessons, extracted from thousands of client engagements and millions of person-years of experience, offer insights that extend far beyond the IT services sector.

The offshore/onshore model that TCS pioneered remains its most significant contribution to global business. What began as a necessity—Indian engineers couldn't easily get visas to work in the US—evolved into a sophisticated global delivery network that fundamentally changed how services are delivered. The model wasn't simply about cost arbitrage, though the 3-5x cost differential certainly helped. It was about creating a 24-hour development cycle where work progressed continuously as teams in different time zones handed off tasks. A problem identified in New York at 6 PM could be worked on in Mumbai through the night and have a solution ready by 9 AM Eastern Time.

The sophistication of this model went far beyond time zones and cost savings. TCS developed elaborate frameworks for knowledge transfer, quality assurance, and project management that made distributed development not just feasible but often superior to co-located teams. The company created detailed documentation standards that allowed engineers who had never met to collaborate seamlessly. They developed communication protocols that minimized misunderstandings despite cultural and linguistic differences. They built security frameworks that protected client intellectual property across multiple jurisdictions.

But perhaps the most innovative aspect was the flexibility built into the model. TCS could dynamically adjust the onshore-offshore mix based on project phases, client preferences, and regulatory requirements. During requirements gathering and design phases, more people would be onshore. During development and testing, the bulk of work would shift offshore. For production support, a follow-the-sun model ensured 24/7 coverage. This flexibility allowed TCS to optimize both cost and effectiveness for each engagement.

The Tata Group synergies provided advantages that standalone IT services companies couldn't match. Access to Tata's relationships opened doors that would have remained closed to a pure-play technology company. When TCS pitched to a global automotive company, they could leverage Tata Motors' credibility in the industry. When pursuing opportunities in steel or chemicals, Tata Steel and Tata Chemicals provided domain expertise and references. The Tata brand, built over 150 years, conveyed trust and stability that resonated particularly in conservative industries and emerging markets.

The ethical business practices inherited from the Tata Group became a significant differentiator, especially in markets where corruption was endemic. TCS's refusal to pay bribes, even when it meant losing business, earned respect from global clients who valued integrity. The company's commitment to corporate social responsibility—from education initiatives to healthcare programs—aligned with the values of progressive corporations. This ethical foundation also helped in attracting and retaining talent, as employees took pride in working for a company that stood for something beyond profits.

Client retention strategies at TCS went far beyond delivering projects on time and budget. The company invested in understanding clients' businesses deeply, often knowing their systems better than the clients themselves. Multi-decade relationships were built on this foundation of trust and expertise. TCS account managers weren't just selling services; they were advising on business strategy, identifying opportunities for improvement, and sometimes warning clients about risks they hadn't seen.

The company's approach to client relationships was distinctly long-term. TCS would often accept lower margins on initial projects to establish relationships, confident that the lifetime value of the client would justify the investment. They would proactively invest in building capabilities specific to a client's needs, sometimes years before those capabilities generated revenue. This patient approach, possible because of the Tata Group's long-term orientation, created switching costs that made client defection rare.

Scale management at TCS—operating as India's fourth-largest employer with over 600,000 employees—required innovations in human resource management that have become case studies in business schools. The company's training infrastructure rivals that of major universities, with dedicated campuses, thousands of trainers, and comprehensive curricula covering both technical and soft skills. New hires undergo months of training before being assigned to projects, an investment few companies can match.

The performance management system evolved to handle the complexity of managing such a large, distributed workforce. The company developed sophisticated metrics to track utilization, productivity, and quality across projects, technologies, and geographies. Career paths were clearly defined, allowing employees to see how they could progress from programmer to architect to project manager to executive. The promotion system, while sometimes criticized for being slow, ensured that those who rose through ranks were thoroughly prepared for increased responsibilities.

Innovation investments at TCS challenged the conventional wisdom that services companies couldn't be innovation leaders. The 19 labs, university partnerships, and startup ecosystem weren't just window dressing—they generated real intellectual property and differentiated capabilities. The research wasn't academic but applied, focused on solving real business problems. When TRDDC developed automated code conversion tools in the 1980s, it was responding to actual client needs. When they created water purification systems using rice husk, it addressed both social needs and demonstrated the breadth of their innovation capabilities.

The innovation model at TCS was particularly clever in how it balanced long-term research with immediate business needs. Researchers were encouraged to work on fundamental problems, but they were also embedded in business units where they could see real-world applications. This bi-directional flow of knowledge—from research to business and from business to research—ensured that innovation remained grounded in practical reality while still pushing boundaries.

Capital allocation at TCS reflected a disciplined approach that balanced growth, profitability, and shareholder returns. Despite being in a people-intensive business, the company maintained industry-leading return on equity by carefully managing working capital and avoiding expensive acquisitions. The consistent dividend policy—paying out quarterly dividends since listing—demonstrated confidence in cash generation while maintaining sufficient capital for growth investments.

The company's approach to acquisitions was notably conservative. Unlike peers who made large, transformational acquisitions, TCS preferred organic growth supplemented by small, strategic acquisitions that brought specific capabilities or client relationships. This discipline helped TCS avoid the integration challenges and goodwill write-offs that plagued aggressive acquirers. When TCS did acquire, like the purchase of Citigroup's BPO operations in India, it was done with clear strategic rationale and careful integration planning.

The platform pivot represented a fundamental evolution in TCS's business model. Products like BaNCS in banking, iON for small businesses, and industry-specific platforms weren't just additional revenue streams—they represented a move up the value chain. Unlike services, which scaled linearly with people, platforms could scale exponentially with minimal incremental cost. A platform developed for one bank could be deployed to hundreds with customization, generating recurring revenue with high margins.

The platform strategy also changed client relationships. Instead of being one of many vendors, TCS became embedded in clients' operations through its platforms. Switching costs increased dramatically when a bank ran its core operations on BaNCS or a retailer managed its stores through TCS OmniStore. The platform approach also accelerated implementation times—what once took years of custom development could be deployed in months using pre-built components.

The Location Independent Agile delivery model represented the next evolution of the offshore model for the cloud era. Instead of fixed offshore development centers, TCS created a fluid model where talent could be accessed from anywhere. Engineers in Brazil could collaborate with designers in Poland and testers in India, all working on a project for a client in Japan. This model, tested during COVID-19 and refined since, offers even greater flexibility and access to global talent.

The agile transformation within TCS demonstrated the company's ability to reinvent itself despite its size. Moving from waterfall to agile methodologies required not just training but fundamental changes in how projects were structured, managed, and delivered. The company had to reorganize from horizontal functions (development, testing, support) to vertical, cross-functional teams. Contracts had to shift from fixed-scope to outcome-based. Client relationships had to evolve from vendor-customer to partnership. This transformation, still ongoing, shows that even 600,000-person organizations can change if the will and vision exist.

Risk management at TCS reflected hard-learned lessons from decades of global operations. The company developed sophisticated frameworks for managing currency risk, regulatory compliance, data security, and business continuity. Multiple delivery centers ensured that natural disasters, political instability, or pandemic lockdowns in one location wouldn't disrupt client services. Contracts included carefully crafted clauses that protected against scope creep while maintaining flexibility. The legal and compliance infrastructure, often seen as overhead, proved its value repeatedly in avoiding costly disputes and regulatory penalties.

The knowledge management systems at TCS turned individual expertise into organizational capability. Best practices from one project were documented and shared across the organization. Reusable components were catalogued and made available to all teams. Lessons learned from failures were analyzed and incorporated into methodologies. This systematic approach to knowledge management meant that TCS's capabilities grew exponentially with experience, creating a compounding advantage over competitors.