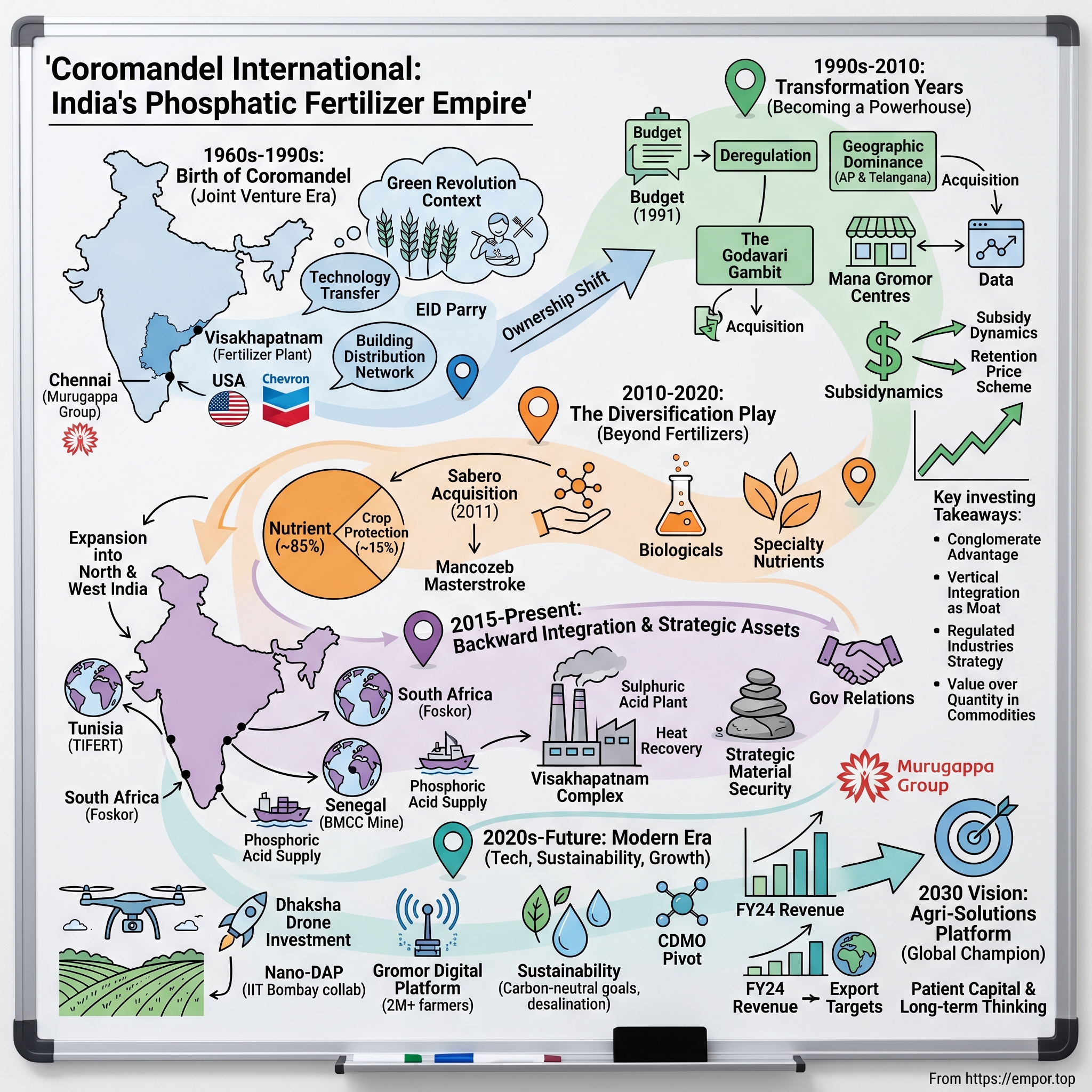

Coromandel International: The Phosphatic Fertilizer Empire of India

I. Introduction & Episode Roadmap

The year is 1965. India is staring down a food crisis that threatens to unravel the young nation. The monsoons have failed—again. Ships carrying PL-480 wheat from America dock at Indian ports like life rafts thrown to a drowning man. Prime Minister Lal Bahadur Shastri calls for Indians to skip one meal a week. In the corridors of power, a terrifying question echoes: Can India feed itself, or will it forever remain what American diplomats cruelly call "a basket case"?

Meanwhile, in the southern city of Chennai, a different story is unfolding. Inside the offices of the Murugappa Group—a conglomerate that had already survived the Burma exodus, two world wars, and Partition—executives are plotting something audacious. They're not thinking about importing food. They're thinking about the soil itself. What if India could manufacture its own fertilizers at scale? What if the answer to feeding a billion people wasn't more imports, but better chemistry? Today, that dream has crystallized into something extraordinary. Coromandel International Limited, one of India's leading fertilizer manufacturers, reported a gross revenue of some 223.08 billion Indian rupees in fiscal year 2024. It is the 2nd largest phosphatic seller in India and largest single super phosphate (SSP) seller with a market share of ~15%. But numbers alone don't capture the transformation. This is a story of how a trading house built an empire from phosphorus and nitrogen, how a family business became a national champion, and how India learned to feed itself.

The big question hovering over this narrative: How did a 1960s joint venture—started when India couldn't even produce basic fertilizers—evolve into a vertically integrated agricultural powerhouse that touches every aspect of Indian farming? It's a playbook worth studying, especially for anyone interested in how companies navigate regulated industries, manage government relationships, and build competitive moats in commodity businesses.

Episode Structure

We'll trace this journey through distinct eras: from the Murugappa Group's century-old foundation through Burma's money markets, to the joint venture years when American technology met Indian ambition, through liberalization's opportunities, and into today's high-tech precision agriculture revolution. Along the way, we'll uncover strategic moves that seem obvious in hindsight but required tremendous conviction at the time—backward integration into phosphoric acid, the crop protection acquisitions, the retail network buildout.

This isn't just another conglomerate expansion story. It's about understanding India's agricultural transformation through the lens of one company that helped engineer it. Ready? Let's begin where all great business stories do—with a family fleeing crisis and discovering opportunity.

II. The Murugappa Legacy & Foundation

Picture this: It's 1900, and a young Tamil Chettiar businessman named A.M. Murugappa is boarding a steamer from the Madras coast, bound for Rangoon. In his pocket, perhaps a handful of British pounds and a mental ledger of contacts. Burma—then the rice bowl of Asia—is booming under British rule. The teak forests are being harvested, the rice paddies expanded, the ruby mines excavated. And someone needs to finance it all.

The foundation for the Murugappa Group was laid by Dewan Bahadur A.M. Murugappa Chettiar who established a money-lending and banking business in 1900, first in Moulmein, Burma (now Myanmar) and then spreading to British Malaya, Ceylon, Dutch East Indies. This wasn't just opportunistic expansion—it was following the Tamil Chettiar diaspora's ancient trade routes, where trust-based lending networks had operated for centuries. The Chettiars were India's original venture capitalists, financing everything from temple construction to shipping ventures across Southeast Asia.

The early decades saw remarkable diversification. Between 1915-1934, the group diversified into textiles, rubber plantations, insurance, and stock broking, expanding presence to Malaya, Vietnam, and Ceylon. Think about the audacity here—while Europe was destroying itself in World War I, the Murugappas were quietly building a pan-Asian financial empire. They weren't just lending money; they were taking equity stakes, buying plantations, vertically integrating.

Then came the moment that would define the group's character forever. In the 1930s the business was moved back to India, with the group shifting assets before the Japanese invasion of Burma in World War II. This wasn't retreat—it was prescient redeployment. While other Indian businesses in Burma lost everything to the Japanese occupation, the Murugappas had already pivoted, bringing capital and expertise back to build India's industrial base.

The Industrial Pivot

What happened next was quintessentially Murugappa: they didn't just park their Burma profits in safe government bonds. They went all-in on manufacturing. Steel furniture. Emery paper. Bicycles. By 1947, as India gained independence, they established Coromandel Engineering Company Limited. In 1949, they collaborated with Tube Investments Limited, UK, to establish TI Cycles of India Limited, a renowned bicycle manufacturer.

But here's what makes the Murugappa story different from other business houses of that era. While the Birlas and Tatas were building heavy industry with government licenses, the Murugappas focused on what economists call "appropriate technology"—products that India's emerging middle class actually needed and could afford. A bicycle wasn't just transportation; it was economic mobility for millions.

The Values Architecture

In 1953, the AMM Charities Trust was founded, showcasing the Group's commitment to social responsibility and philanthropy. This wasn't corporate social responsibility as window dressing—this was baked into the DNA from the start. The Murugappa philosophy was simple: business wasn't separate from nation-building; it was the mechanism for it.

By the time the third generation took charge in the 1960s, the group had evolved a unique governance structure. Unlike other family conglomerates that often imploded in succession battles, the Murugappas created what they called a "family board"—professional management with family oversight, meritocracy within bloodlines. Decisions were collective, profits were reinvested, and no single family member could dominate.

The Numbers Tell the Story

Fast forward to today: The Group has 29 businesses including 10 companies listed on the NSE and BSE, with their net worth estimated at ₹85,000 Crore (9.8 Billion USD) in 2024. In October 2024, the Murugappa family were ranked 26th on the Forbes list of India's 100 richest tycoons, with a net worth of $10.1 billion.

But what's remarkable isn't the size—it's the portfolio construction. The Group has presence in several segments including abrasives, auto components, bicycles, sugar, farm inputs, fertilisers, plantations, bioproducts and nutraceuticals. Notice the pattern? Every business touches India's real economy. Nothing speculative, nothing purely financial. It's Warren Buffett's "circle of competence" philosophy, executed with Tamil prudence.

The Agricultural Imperative

Which brings us to the crucial question: Why fertilizers? Why did a group that could have stuck to profitable light engineering and financial services decide, in the early 1960s, to enter one of the most capital-intensive, government-regulated, technically complex industries in India?

The answer lay in what the Murugappas saw that others missed. India's population was exploding—from 361 million in 1951 to 439 million by 1961. Agricultural productivity was stagnant. The country was one failed monsoon away from famine. And here was a business that could simultaneously generate returns and prevent starvation. For a group whose motto was nation-building through business, what could be more compelling?

So What for Investors: The Murugappa foundation story reveals a crucial insight about successful conglomerates: patient capital combined with operational excellence can compound over decades. The group's focus on sectors critical to India's development—rather than quick-return ventures—created both defensive moats and offensive growth options. Modern investors evaluating Coromandel should understand that this DNA of long-term thinking and willingness to make decade-long bets remains embedded in the company's capital allocation framework. As we'll see next, this patient capital advantage would prove decisive when Coromandel needed to invest heavily in phosphatic fertilizer capacity during India's Green Revolution—a bet that would take years to pay off but would ultimately create one of India's most formidable agricultural franchises.

III. Birth of Coromandel: The Joint Venture Era (1960s–1990s)

The telegram arrived at the Murugappa Group headquarters in Chennai on a humid morning in early 1961. "American partners confirmed. Stop. Phosphatic fertilizer project approved. Stop. India's future begins now."

That future had been germinating since the late 1950s, when two American giants—International Minerals and Chemical Corporation (IMC) and Chevron Chemical Company—began scouting Asia for fertilizer manufacturing opportunities. They found willing partners in EID Parry, the Murugappa Group's sugar and chemicals arm that had a unique claim to fame: it had manufactured fertilizers for the first time in the Indian subcontinent back in 1906. But this new venture would be something entirely different—a bet that India could industrialize its agriculture before starvation overtook its population growth.

The Perfect Storm

By the 1960s, India's low agricultural productivity led to food grain shortages that were more severe than those of other developing countries. The production of food within India was insufficient in the years from 1947 to 1960 as there was a growing population. Food availability was only 417 g per day per person. The situation was so dire that Prime Minister Lal Bahadur Shastri famously asked Indians to skip one meal a week. Ships carrying American PL-480 wheat—disparagingly called the "ship-to-mouth" existence—were India's lifeline.

The company was founded in the early 1960s by IMC and Chevron Companies and EID Parry. But why would American chemical companies venture into Indian agriculture? The answer lay in a convergence of interests. For IMC and Chevron, it was market expansion—they saw a billion future customers for agricultural chemicals. For the Indian government, it was survival. For the Murugappa Group, it was the opportunity to build a business that could simultaneously generate returns and prevent famine.

The joint venture structure was carefully crafted. The Americans brought technology—the know-how to manufacture complex phosphatic fertilizers that Indian soil desperately needed. The Murugappas brought local knowledge, government relationships, and most importantly, the patience to navigate India's byzantine regulatory environment. Complex fertilizer plant commissioned at Visakhapatnam became the first major milestone, a facility that would become the backbone of South India's agricultural transformation.

Technology Transfer: The Real Revolution

What made Coromandel different wasn't just the manufacturing—it was the chemistry. Indian soils, depleted by centuries of cultivation without replenishment, were particularly deficient in phosphorus. Traditional farming used organic manure, but while India had abundant manure from its cows, it produced almost no chemical fertilizer. It had to start spending heavily to import and subsidize fertilizer.

The Visakhapatnam plant, commissioned in 1967, was a marvel of 1960s industrial engineering. Picture massive reaction vessels where rock phosphate imported from Morocco was treated with sulphuric acid to create phosphoric acid, then ammoniated to produce complex fertilizers. The plant could produce multiple grades—16-20-0, 14-35-14, 20-20-0—numbers that became as familiar to Indian farmers as their children's names.

But technology transfer is never just about machinery. It's about knowledge systems. Coromandel sent Indian engineers to American plants, where they learned not just how to operate equipment but how to think about soil chemistry, nutrient management, and agricultural productivity. These engineers returned as evangelists for scientific farming.

The Green Revolution Context

The Green Revolution in India was initiated in the 1960s by introducing high-yielding varieties of rice and wheat to increase food production in order to alleviate hunger and poverty. The HYVs of wheat and rice were tested by the Indian scientists in 1962 and 1964 respectively. Later, these tested varieties were introduced throughout the nation during the crop year of 1965–1966. Thus, the Green Revolution involved the use of HYVs of wheat and rice and adoption of new agricultural practices involving the use of chemical fertilizers, pesticides, tractors, controlled water supply to crops.

Here's what most histories miss: the Green Revolution wasn't just about seeds. The new dwarf wheat varieties from Mexico and IR-8 rice from the Philippines were designed to absorb massive amounts of nutrients without lodging (falling over). The HYVs had 20% more grain than its earlier cultivars and were more responsive to the nitrogen fertilizers. Without fertilizers, these seeds were worthless. With fertilizers, they were miraculous.

Coromandel found itself at the epicenter of this transformation. In 1966 India imported 18,000 tons of new Mexican wheat seeds. Wheat output in India surged from 12 million tons in 1965 to 20 million tons in 1970. Every ton of increased grain production required proportional increases in fertilizer consumption. Coromandel's production couldn't keep pace with demand.

The Ownership Evolution

The joint venture structure that birthed Coromandel was always meant to be temporary. As the company matured and Indian engineers mastered the technology, the ownership evolved. Chevron Corporation Group California Chemical Company divested its share in Coromandel International to EID Parry. Then came the pivotal moment: International Minerals and Chemical Corporation (IMC) divested its share in Coromandel International to EID Parry. Following this sale Coromandel Fertilisers Limited (present day Coromandel International) became a Group company.

This wasn't just a financial transaction—it was a declaration of technological independence. The Murugappa Group had successfully absorbed, adapted, and improved upon American technology. They were no longer junior partners; they were masters of their domain.

Building the Network

Manufacturing fertilizer is one challenge; getting it to millions of small farmers is another entirely. In the 1970s and 1980s, Coromandel built one of India's most sophisticated agricultural distribution networks. This wasn't Amazon-style logistics—this was creating supply chains where none existed, building warehouses in districts that barely had roads, training dealers who couldn't read English but understood soil chemistry better than PhDs.

The company pioneered the concept of "agronomic marketing"—not just selling fertilizer but educating farmers on optimal usage. Coromandel's field officers became legendary figures in rural India, carrying soil testing kits and crop charts, speaking local dialects, understanding local cropping patterns. They weren't salesmen; they were agricultural extension officers with a commercial mandate.

The Subsidy Trap

Here's where the story gets complicated. The Indian government, desperate to boost agricultural production, began heavily subsidizing fertilizers. What seemed like good policy created perverse incentives. The farmers say they must use three times as much fertilizer as they used to, to produce the same amount of crops. The soil, addicted to chemical inputs, required ever-increasing doses to maintain yields.

For Coromandel, subsidies were both blessing and curse. They guaranteed demand—farmers would buy as much subsidized fertilizer as they could get. But they also meant government control over pricing, distribution, and even production decisions. The company had to master not just chemistry and logistics but also the arcane art of subsidy management, maintaining relationships with bureaucrats who could make or break profitability with a policy circular.

Scaling Up: The 1980s Expansion

By the 1980s, Coromandel had proven the model. The Visakhapatnam plant was running at full capacity. Demand was insatiable. The company embarked on aggressive expansion, but with a twist—instead of just building more plants, they began acquiring struggling fertilizer units.

Expansion of Complex fertiliser capacity at Visakhapatnam marked the beginning of a new phase. The company wasn't just growing; it was consolidating India's fragmented fertilizer industry. Each acquisition brought new challenges—outdated technology, demoralized workforces, accumulated losses. But it also brought strategic assets: manufacturing licenses (gold in India's license raj), distribution networks, and most importantly, market share.

Innovation Under Constraints

Working within India's regulatory framework required constant innovation. When the government limited imports of rock phosphate, Coromandel pioneered the use of indigenous low-grade rock. When environmental regulations tightened, they developed processes to reduce effluents. When farmers complained about fertilizer quality, they introduced branded products with quality guarantees.

The company's R&D efforts in the 1980s and 1990s focused not on breakthrough innovation but on incremental improvements that mattered in the Indian context: fertilizers that worked in alkaline soils, grades optimized for specific crops, coatings that prevented caking in humid storage conditions. This wasn't Silicon Valley-style disruption; it was patient, methodical improvement.

So What for Investors: The joint venture era reveals a crucial pattern: successful emerging market companies often begin as technology importers but create value through localization and distribution excellence. Coromandel's ability to transform from a foreign joint venture into a domestic champion—while navigating complex stakeholder relationships including foreign partners, government regulators, and millions of small farmers—demonstrates the importance of "political capital" alongside financial and human capital. Modern investors should note that the company's early focus on building hard-to-replicate assets (manufacturing licenses, distribution networks, farmer relationships) rather than pursuing quick profits created the foundation for decades of competitive advantage. The transition from foreign to domestic ownership, completed without operational disruption, also shows the Murugappa Group's exceptional execution capabilities in complex transactions.

IV. The Transformation Years: Becoming a Powerhouse (1990s–2010)

July 24, 1991. Finance Minister Manmohan Singh rises in Parliament to deliver the most consequential budget speech in Indian history. "No power on earth can stop an idea whose time has come," he declares, quoting Victor Hugo. For Coromandel International, watching from their headquarters in Secunderabad, this wasn't just political theater—it was the starting gun for a transformation that would redefine Indian agriculture.

The crisis that precipitated these reforms was severe. The fiscal deficit had ballooned to over 8% of GDP, foreign exchange reserves had dwindled to a point where they could barely cover three weeks of imports, and inflation was soaring. As part of a bailout deal with the IMF, India was forced to pledge 20 tonnes of gold to Union Bank of Switzerland and 47 tonnes to the Bank of England and Bank of Japan. The humiliation of shipping gold reserves abroad shocked the nation into action.

The New Playing Field

The reforms specified deregulation, increased foreign direct investment, liberalisation of the trade regime, reforming domestic interest rates, strengthening capital markets (stock exchanges), and initiating public enterprise reform (selling off public enterprises). For a company like Coromandel, operating in the heavily regulated fertilizer sector, every one of these changes mattered.

The immediate impact on agriculture was paradoxical. As the government reduced subsidies on fertilizers, pesticides, and electricity, farmers faced increasing production expenses. The phased reduction of fertilizer subsidies led to significantly higher prices for nutrients essential to crop production. Yet demand for fertilizers didn't collapse—it transformed. Farmers began demanding not just any fertilizer, but the right fertilizer for their specific soil and crop combinations.

Coromandel's leadership, under the Murugappa Group's strategic guidance, saw opportunity where others saw chaos. While competitors lobbied for protection, Coromandel invested in differentiation. The company accelerated its R&D efforts, developing unique grade fertilizers tailored to specific regional soil conditions. It has ~40% share in the unique grade fertilizer sales in India—a position built during these turbulent years.

Geographic Dominance Strategy

The 1990s marked Coromandel's shift from being a manufacturer to becoming a regional powerhouse. The company identified Andhra Pradesh and Telangana as its fortress markets—regions where it would build unassailable competitive positions. It has a leading position in the states of Andhra Pradesh and Telangana; India's largest complex-fertiliser markets.

This wasn't random selection. These states were at the forefront of India's agricultural transformation, with progressive farmers willing to invest in productivity. The Krishna and Godavari river deltas provided ideal conditions for intensive agriculture. State governments were supportive of private sector participation. And critically, Coromandel already had manufacturing assets and distribution networks in place.

The company's strategy was multi-pronged: dominate manufacturing capacity, control distribution channels, build farmer loyalty through service, and create switching costs through customized products. By 2000, farmers in these regions didn't ask for "fertilizer"—they asked for "Gromor" and "Paramfos," Coromandel's flagship brands.

The Godavari Gambit

In the late 1990s, an opportunity emerged that would double Coromandel's size overnight. Godavari Fertilizers & Chemicals Limited, a joint venture between the Andhra Pradesh government and IFFCO (Indian Farmers Fertiliser Cooperative), was struggling. Despite having modern plants and strategic locations, the company was bleeding cash, caught between government inefficiency and cooperative politics.

In July, Government of Andhra Pradesh divested its share in Godavari Fertilizers & Chemicals Limited to Coromandel International. The acquisition, completed in stages through the early 2000s, was transformative. Investment in Godavari Fertilisers and Chemicals Ltd becoming the 2nd largest Phosphatic fertiliser player in the country.

The integration of Godavari wasn't just about adding capacity. Coromandel had to merge two different cultures—a government PSU mindset with private sector dynamism. They retrained workers, modernized plants, and most importantly, connected Godavari's assets to Coromandel's distribution network. Within three years, the acquired plants were operating at higher efficiency than Coromandel's original facilities.

Technology and Product Innovation

The late 1990s and early 2000s saw Coromandel make crucial technology partnerships. The company wasn't trying to invent new chemistry—phosphorus is phosphorus. Instead, they focused on application technology and product formulation.

Complex fertilizers became the growth driver. Unlike straight fertilizers (containing single nutrients), complex fertilizers provided balanced nutrition with nitrogen, phosphorus, and potassium in single granules. This meant uniform distribution, better absorption, and higher yields. Coromandel developed grades specifically for cotton in Gujarat, rice in the Godavari delta, and groundnut in Andhra Pradesh's Rayalaseema region.

The company also pioneered coated fertilizers in India—products where nutrients were released slowly, matching crop requirements and reducing losses. This wasn't breakthrough science, but it required sophisticated manufacturing processes and quality control that few Indian companies could match.

The Retail Revolution

Started its first rural retail store in Andhra. Today, company operates ~750 stores in Andhra, Telangana, Karnataka and Maharashtra. But calling these "stores" misses the point. Coromandel's Mana Gromor Centres were agricultural solution hubs—places where farmers could get soil tested, buy inputs, access credit, and receive agronomic advice.

Each center was strategically located to serve a cluster of villages, typically positioned at mandal (sub-district) headquarters where farmers came for other purposes. The stores stocked not just Coromandel fertilizers but also seeds, pesticides, farm implements—everything except competing fertilizers. They became data collection points, gathering intelligence on cropping patterns, pest attacks, and farmer preferences that fed back into product development.

The retail network solved multiple problems simultaneously. It reduced dependence on traditional dealers who often played brands against each other. It provided direct farmer contact, building brand loyalty. It enabled bundled selling—fertilizers with pesticides, seeds with nutrients. And critically, it provided a distribution channel for the specialty products that would drive future growth.

Managing Subsidy Dynamics

Throughout the 1990s and 2000s, Coromandel became a master at navigating India's complex fertilizer subsidy regime. The government's Retention Price Scheme (later replaced by the New Pricing Scheme) meant that companies were reimbursed based on their cost of production plus a nominal return. This created perverse incentives—efficient producers were penalized while inefficient ones were protected.

Coromandel's response was sophisticated. Instead of fighting the system, they optimized within it. They located plants to minimize logistics costs under the freight subsidy rules. They timed capacity additions to coincide with policy windows. They maintained flexibility to switch between products based on subsidy economics. And most cleverly, they used subsidy-supported commodity products to pull through non-subsidized specialty products.

The company also became adept at managing subsidy receivables—the delays between selling subsidized fertilizers and receiving government reimbursement. This required sophisticated working capital management and strong banking relationships, capabilities that became competitive advantages.

Brand Building in Commodities

How do you build a brand in a commodity business where the government controls prices and products are chemically identical? Coromandel's answer was to brand the experience, not just the product.

"Gromor" became synonymous with quality assurance—farmers trusted that every bag contained what the label promised. "Paramfos" stood for phosphatic nutrition. These weren't just names; they were promises backed by consistent quality, reliable availability, and responsive service.

The company invested heavily in below-the-line marketing—field demonstrations, farmer meetings, village-level campaigns. They sponsored agricultural fairs, supported progressive farmers, and created farmer clubs. By 2009, when the company changed its name to Coromandel International with a new logo, the transformation from manufacturer to solutions provider was complete.

The 2008 Crisis and Recovery

The global financial crisis of 2008 coincided with a spike in international fertilizer prices. Phosphoric acid prices shot up from $400 per ton to over $2,000. The Indian government, facing fiscal pressures, delayed subsidy payments. Many fertilizer companies faced existential crises.

Coromandel not only survived but emerged stronger. Their diversified product portfolio provided resilience. Strong farmer relationships meant continued offtake even at higher prices. Most importantly, the crisis accelerated industry consolidation, with weaker players exiting or seeking buyers. Coromandel was perfectly positioned to acquire distressed assets and expand market share.

So What for Investors: The transformation years demonstrate how regulatory transitions create opportunities for prepared operators. Coromandel's strategy of building regional dominance rather than pursuing national spread created defensible market positions with pricing power even in a regulated industry. The company's investment in retail infrastructure during the 2000s—when most competitors focused solely on manufacturing—created a direct-to-farmer channel that now provides competitive advantages in data collection, brand building, and new product introduction. The successful integration of Godavari Fertilizers shows management's M&A execution capabilities, a skill that would prove valuable in subsequent acquisitions. For modern investors, this period highlights how companies operating in regulated industries can create value through operational excellence and strategic positioning rather than regulatory arbitrage.

V. The Diversification Play: Beyond Fertilizers (2010–2020)

The boardroom at Coromandel's Secunderabad headquarters was tense on a May morning in 2011. The company's leadership team was about to make their boldest move yet—a ₹452 crore bet that would either transform them into an integrated agricultural solutions provider or saddle them with an underperforming asset in an unfamiliar business.

The target was Sabero Organics Gujarat Limited, a Mumbai-based crop protection company that on paper looked troubled—operating at just 40% capacity utilization, bleeding market share, with a stock price that had been languishing. But Kapil Mehan, Coromandel's Managing Director, saw something others missed: a company with 240 product registrations across 50 countries, state-of-the-art manufacturing facilities, and most crucially, technical expertise in molecules that perfectly complemented Coromandel's portfolio.

The Strategic Rationale

The company's business is divided among 2 main segments i.e. nutrient and other allied products (~85% of revenues) and crop protection (~15% of revenues). This revenue split revealed both Coromandel's strength and vulnerability—dominant in fertilizers but dangerously dependent on government-controlled, subsidy-driven products. The crop protection market, in contrast, was deregulated, growing at 10-12% annually, with pricing power and export potential.

In May 2011, Coromandel International Ltd (CIL) acquired 74% stake in Sabero Organics Gujarat Limited (SOGL) for Rs 452 crore. This includes acquisition of entire 42.2% stake held by promoters in SOGL. The deal valued the company at Rs 672 crore, 14.3 times EBITDA—a multiple that raised eyebrows. But Mehan's logic was compelling: the acquisition catapults CIL into one of the top five players in the country's Rs 8,000-crore pesticides market, which was growing at an average rate of 10-12 per cent a year.

The Integration Challenge

Sabero Organics is a leading producer and supplier of a variety of fungicides, herbicides, insecticides and specialty chemicals and is a significant player in Mancozeb fungicide in global markets. The Company has manufacturing operations in Gujarat and markets its products in India and abroad. Current Turnover of the Company is Rs. 413 Crores in FY 11, out of which the exports contribute about Rs. 220 Crores.

The integration wasn't just about combining balance sheets. Sabero's culture was that of a technical manufacturing company—focused on chemistry and production efficiency. Coromandel's strength was in marketing and distribution—understanding farmers, building relationships, creating pull for products. Merging these cultures required delicate handling.

Sabero was unable to utilise more than 40 per cent of its manufacturing base due to lack of adequate marketing network. "With our (CIL) marketing capabilities, we will be able to ramp up capacity utilisation faster," Mehan said. This wasn't corporate speak—it was a precise diagnosis of the problem and solution.

Within 18 months, Sabero's capacity utilization jumped from 40% to over 70%. Coromandel pushed Sabero's products through its 750+ retail stores, bundled them with fertilizers, and leveraged farmer relationships built over decades. Meanwhile, Sabero's technical team developed new formulations tailored to Indian conditions, moving beyond commodity molecules to specialized products with higher margins.

The Mancozeb Masterstroke

Sabero's crown jewel was its position in Mancozeb, a broad-spectrum fungicide critical for protecting fruits and vegetables. It is 3rd largest manufacturer of mancozeb globally and exports accounts for ~37% of revenues of the business. Coromandel recognized that global agricultural chemical supply chains were shifting. Chinese manufacturers, facing environmental regulations, were curtailing production. Indian companies with clean manufacturing processes and global registrations could capture this opportunity.

Coromandel invested in upgrading Sabero's Gujarat plant to meet international environmental standards—not just compliance, but exceeding requirements to become the supplier of choice for global agrochemical majors. They expanded the product portfolio beyond Mancozeb into other fungicides and herbicides where similar dynamics were playing out.

Building the Biologicals Business

The 2010s saw growing concern about chemical residues in food and environmental damage from pesticides. Organic farming was moving from niche to mainstream. Coromandel, with its finger on the pulse of Indian agriculture, saw this trend early.

It is a leading manufacturer of azadirachtin in the world with ~65% export share. This wasn't achieved overnight. Coromandel had been quietly building capabilities in biological crop protection for years, but the Sabero acquisition provided the scale and technical expertise to accelerate.

The company's approach to biologicals was pragmatic rather than ideological. They positioned bio-pesticides not as replacements for chemicals but as complements—part of integrated pest management that reduced chemical usage while maintaining yields. This resonated with farmers who wanted to reduce costs and meet increasingly stringent residue requirements for export crops.

Specialty Nutrients: The Hidden Gem

While crop protection grabbed headlines, Coromandel was quietly building another growth engine: specialty nutrients. These weren't your grandfather's fertilizers—they were sophisticated products like water-soluble fertilizers for drip irrigation, micronutrient formulations for specific deficiencies, and organic fertilizers for premium crops.

The specialty nutrients business leveraged the same distribution infrastructure as traditional fertilizers but with vastly superior economics. Gross margins on specialty products were 25-30% versus 8-10% for subsidized fertilizers. More importantly, these products created stickiness—farmers who saw results from customized nutrition solutions rarely switched back to generic products.

Retail as Platform

Started its first rural retail store in Andhra. Today, company operates ~750 stores in Andhra, Telangana, Karnataka and Maharashtra. But these weren't just stores—they were platforms for cross-selling, data collection, and farmer engagement.

Each Mana Gromor Centre became a hub for the complete Coromandel portfolio. A farmer coming for fertilizer would learn about crop protection. Someone buying pesticides would get soil tested for nutrient deficiencies. The stores also offered credit, insurance, and even farm equipment rentals—creating multiple touchpoints and revenue streams.

The retail network generated invaluable data. Coromandel knew what farmers were planting, when they were planting, what problems they faced, what products they used. This information fed back into product development, inventory planning, and marketing strategies. In an industry where most companies were flying blind, Coromandel had ground-level intelligence.

Technology Partnerships

The 2010s also saw Coromandel actively seeking technology partnerships to differentiate its products. Signed up with Shell for micronized sulfur technology and introduced slow release sulfur fertilizers - a first in India. This wasn't just licensing—it was technology absorption and adaptation.

The Shell Thiogro technology allowed Coromandel to manufacture Sulphur Enhanced Fertilizers (SEF) that addressed India's widespread sulphur deficiency—a problem that had emerged as intensive cultivation depleted soil micronutrients. The technology involved coating urea with elemental sulphur and polymers, creating a product that released nutrients slowly while providing essential sulphur.

Similarly, partnerships with Japanese and European companies brought expertise in formulation technology, allowing Coromandel to develop products with better shelf life, easier application, and improved efficacy. These weren't revolutionary innovations but incremental improvements that mattered in the field.

Geographic Expansion

While maintaining dominance in South India, Coromandel began systematic geographic expansion. Strengthened Single Super Phosphate portfolio in West & North India through acquisition of Liberty Phosphates—a strategic move to enter markets where it had been historically weak.

The Liberty Phosphate acquisition in 2013 brought manufacturing facilities in Uttar Pradesh and Madhya Pradesh, along with established dealer networks in North and West India. Single Super Phosphate (SSP), while less sophisticated than complex fertilizers, was crucial for crops like oilseeds and pulses grown in rain-fed areas. Overall, it is the 2nd largest phosphatic seller in India and largest single super phosphate (SSP) seller with a market share of ~15%.

The Export Opportunity

By the mid-2010s, Coromandel's crop protection business had developed significant export capabilities. Exports for crop protection business contributed 45% in FY15 as against less than 10% in FY11 mainly due to SOGL's acquisition—a transformation achieved through systematic market development.

The company targeted regulated markets in Latin America, Southeast Asia, and Africa—regions with similar cropping patterns to India but without domestic manufacturing capabilities. They invested in product registrations, a slow and expensive process that created barriers to entry. They established local partnerships for distribution and technical support. And crucially, they maintained quality standards that met international requirements.

Financial Transformation

The diversification strategy fundamentally changed Coromandel's financial profile. Revenue from NonSubsidy business contributes 18% of CIL's sales (FY15). Non-Subsidy EBITDA share at CIL has improved from 23% in FY09 to 34% in H1 FY16. This wasn't just revenue diversification—it was margin expansion and risk reduction.

Non-subsidy businesses provided cushion against policy changes, reduced working capital requirements (no subsidy receivables), and most importantly, gave Coromandel pricing power it never had in fertilizers. The company could now optimize its product mix based on profitability rather than just volume.

So What for Investors: The diversification decade demonstrates the value of patient capital allocation in building new capabilities. Coromandel's move into crop protection and specialty products—segments with 2-3x the margins of commodity fertilizers—transformed the company's return profile while reducing regulatory risk. The Sabero acquisition, though expensive at 14x EBITDA, proved transformative by providing technical capabilities that would have taken decades to build organically. The retail network investment, initially dilutive to returns, created a distribution moat and data advantage that competitors still struggle to replicate. Modern investors should note that the company's non-subsidy revenue share has become a key metric for evaluating business quality and resilience. The export success in crop protection also shows that Indian companies can compete globally in specialty chemicals when they combine low-cost manufacturing with registration expertise and quality standards.

VI. Backward Integration & Strategic Assets (2015–Present)

The boardroom in Chennai was silent as A. Vellayan, Executive Chairman of the Murugappa Group, studied the numbers. It was 2015, and global phosphate prices had just crashed from $2,000 per ton to under $500. Most Indian fertilizer companies were celebrating—cheaper imports meant better margins. But Vellayan saw a trap.

"Gentlemen," he said, "we're one geopolitical crisis away from disaster. Morocco controls 70% of global phosphate reserves. China is restricting exports. We need to own the rocks, not just rent them."

This wasn't paranoia—it was pattern recognition. Coromandel had lived through multiple commodity cycles, seen suppliers break contracts when prices spiked, watched competitors shut plants when raw materials became unavailable. The company's leadership decided on a radical strategy: backward integrate all the way to the mines.

The Phosphoric Acid Imperative

Phosphoric acid is to fertilizers what silicon is to semiconductors—the critical input that determines everything else. Without reliable phosphoric acid supply, you can't manufacture DAP or complex fertilizers. And phosphoric acid comes from treating rock phosphate with sulphuric acid—both imported commodities for India.

Coromandel has strategic tie up with leading integrated players like Tifert (Tunisia) and Foskor (South Africa) for meeting its phosphoric acid requirements. But tie-ups weren't ownership. When markets tightened, contracts could be renegotiated, shipments delayed, prices increased. The company needed equity stakes, board seats, guaranteed offtake agreements.

The Foskor investment was particularly strategic. Coromandel holds 14% equity in Foskor, providing supply security and flexibility with regards to phosphoric acid requirement. The Acid Plant, situated at Richards Bay, KwaZulu-Natal, has a capacity to manufacture 7.2 lakh tons high quality merchant grade acid with low cadmium content. This wasn't just about volume—cadmium content mattered. European regulations were tightening on heavy metal content in fertilizers. Low-cadmium phosphoric acid commanded premium prices and would become mandatory for exports.

The Tunisia Gambit

The more audacious move was Tunisia. In 2013, Coromandel International Limited and GSFC hold 15% share each in a 498 million USD project—Tunisian Indian Fertilisers (TIFERT)—with balance 70% being held by GCT and CPG, both Tunisian government entities. TIFERT Plant will consume around 1.4 million tons of Tunisian phosphate rock per year, producing 360,000 tons of phosphoric acid annually.

This wasn't just a supply agreement—it was industrial diplomacy. The plant was originally scheduled to be commissioned in 2011. But the project was delayed due to some internal developments in Tunisia—a euphemism for the Arab Spring that toppled the government. While other investors fled, Coromandel stayed, earning goodwill that would prove invaluable.

The Company and GSFC have entered into an agreement with the TIFERT to import all the production of phosphoric acid directly to India on a long term basis. This meant 180,000 tons annually of guaranteed phosphoric acid supply for Coromandel, shipped directly from La Skhira Port to Kakinada. No middlemen, no traders, no price speculation.

The Senegal Bet

By 2022, Coromandel was ready for the next leap—owning the rocks themselves. The target was Baobab Mining and Chemicals Corporation (BMCC), a rock phosphate mining company located in Senegal, Africa. The acquisition will be at an outlay of $19.6 million (about Rs 150 crore) for 45% equity stake, besides a loan infusion of $9.7 million into BMCC for capital projects and expansion.

Senegal wasn't random selection. West African phosphate was low in cadmium, crucial for meeting environmental standards. The logistics worked—ships from Dakar could reach both Indian coasts. Most importantly, Senegal was politically stable with mining-friendly policies.

BMCC has stabilised its operations and commenced active production from 2021. This investment will help in strengthening Coromandel International's backward integration and ensure long term supply security of the key raw material. The company now had direct access to 500,000 tons annually of rock phosphate—enough to produce 150,000 tons of phosphoric acid.

Domestic Integration Push

While securing international supply chains, Coromandel also pushed domestic backward integration. Completed backward integration projects in 2019, expanding phosphoric acid factory capacity by 2020. The strategy was to create multiple supply options—imported rock processed domestically, imported phosphoric acid, and equity stakes in overseas production.

The crown jewel was the Visakhapatnam complex. The board of agri-solutions provider Coromandel International Ltd has given its nod to set up phosphoric and sulphuric acid plants towards backward integration capabilities. The plant has been set up with an investment of INR 400 Crores with the production capacity of 1,650 metric tonnes per day.

Sulphuric Acid: The Other Bottleneck

Phosphoric acid production requires massive amounts of sulphuric acid—about 3 tons for every ton of phosphoric acid. India imports most of its sulphur, but Coromandel decided to at least control the conversion process.

With this, Coromandel's Sulphuric acid capacity will increase to 11 lakh tonnes per annum from 6 lakh tonnes per annum, supporting its requirement towards downstream processes involving Phosphoric acid and Phosphatic Fertilizer production. The Plant is designed with Double Conversion and Double Absorption (DCDA) process with a 5 bed Catalyst Converter—technology that ensured 99.7% conversion efficiency and minimal emissions.

The plant wasn't just about capacity—it was about integration. Steam generated from the Sulphuric acid plant will be used for captive power generation. Heat from the exothermic reaction powered other processes. Even the dilute acid streams were recovered and recycled. This wasn't just manufacturing; it was industrial ecosystem design.

The Kakinada Mega Complex

The Kakinada transformation represents the culmination of Coromandel's backward integration strategy. In January 2024, we had announced Sulphuric acid (2000 TPD) and Phosphoric acid (650 TPD) plants at Kakinada and the projects are progressing as per plan and are likely to be commissioned by early 2026, thereby making all of the company's fertilizer manufacturing sites backward integrated and reducing their dependence on imports.

With a capacity of around 2 million tons, Coromandel's Kakinada plant is the India's second largest phosphatic fertiliser facility and contributes close to 15% of nation's NPK fertilizer output. With the new facilities, the plant will become one of the world's most integrated fertilizer complexes—from acid to granulation under one roof.

Technology Leadership

The technology choices for these plants reveal Coromandel's sophistication. The proposed 650 ton per day (tpd) Phosphoric Acid facility is designed with advanced DA-HF (Dihydrate Attack-Hemihydrate Filtration) process technology. This isn't standard technology—it's a cutting-edge process that increases phosphoric acid recovery from rock by 3-4%, reduces energy consumption, and produces higher quality acid.

Coromandel signed contracts with technology partners M/s Prayon, Belgium for DA-HF process technology for phosphoric acid manufacturing and with M/s MECS, USA for DCDA process technology for sulphuric acid manufacturing. These weren't lowest-bid vendors—they were global technology leaders whose processes would meet the most stringent environmental standards.

The Financial Architecture

The economics of backward integration are complex. With an estimated outlay of Rs 1000 crores, the project is expected to be commissioned in two years' time—a massive capital commitment that would take years to recover. But Coromandel's analysis went beyond simple payback calculations.

This will enhance Company's backward integration capacities and provide stable supplies of phosphoric acid for its fertiliser manufacturing by replacing more than 50% of Kakinada plant's imported acid requirement. At current import prices, this meant annual savings of ₹500-600 crores. But the real value was in supply security—the ability to continue operations when global supply chains disrupted.

Strategic Raw Material Security

Coromandel's approach to raw material security was multi-layered. Direct equity stakes in mines (Senegal), joint ventures for acid production (Tunisia), long-term supply agreements (South Africa), and domestic production capacity created redundancy. If one source failed, others could compensate.

The company is also exploring investment support from the State and Central Governments, which can improve the project viability and ensure supply security for key raw materials used in fertiliser manufacturing. This wasn't just seeking subsidies—it was aligning corporate strategy with national priorities.

Environmental Integration

Modern chemical plants can't just be efficient—they must be sustainable. The Plant is designed to meet one of the lowest emission standards globally. Steam generated from the Sulphuric acid plant will be used for captive power generation. The Kakinada complex even included a modern desalination plant, which will recycle sea water for usage in operations.

This wasn't greenwashing. It was recognizing that environmental compliance would become increasingly stringent and that companies with clean operations would have competitive advantages in accessing capital, obtaining permits, and maintaining social license to operate.

The Scale Game

Enhancement of granulation capacity by 7.5 lakh tons per annum for manufacture of complex and unique fertilizers at Kakinada, Andhra Pradesh, taking the total production capacity of the Kakinada site to 30 lakh tons. This would make Kakinada one of the largest single-location fertilizer complexes globally.

Scale mattered for multiple reasons. Fixed costs could be spread over larger volumes. Purchasing power for raw materials increased. Logistics became more efficient with full shiploads. Most importantly, scale created bargaining power with both suppliers and customers.

Managing Complexity

Running integrated chemical complexes requires exceptional operational capability. A disruption in sulphuric acid production affects phosphoric acid, which affects fertilizer granulation. Quality variations in rock phosphate impact acid quality, which affects final product specifications. Energy balance, water management, waste treatment—everything is interconnected.

Coromandel developed sophisticated process control systems, with automated DCS (Distributed Control Systems) managing the complex interactions. But technology was only part of the solution. The company invested heavily in training operators, creating a cadre of chemical engineers who understood not just their unit operations but the entire integrated complex.

The Innovation Pipeline

Backward integration wasn't just about securing today's raw materials—it was about enabling tomorrow's innovations. With captive acid production, Coromandel could experiment with different grades, develop customized products, and respond quickly to market needs without depending on external suppliers' willingness to customize.

The company began developing specialty phosphates for industrial applications, food-grade phosphates for exports, and technical-grade acids for other chemical processes. Each of these higher-value products leveraged the same raw material base but generated superior margins.

So What for Investors: The backward integration strategy reveals how capital-intensive industries can create competitive moats through vertical integration. Coromandel's systematic approach—starting with supply agreements, moving to equity stakes, and finally to captive production—minimized risk while building capabilities. The ₹1,000 crore Kakinada investment might seem expensive, but it transforms the company from a converter (dependent on raw material availability and pricing) to an integrated producer with control over its destiny. The focus on environmental compliance and technology leadership positions the company for a future where sustainability becomes a competitive differentiator. For investors, the key metrics to watch are the percentage of captive raw material production, the spread between integrated and non-integrated players' margins, and the company's ability to maintain operations during global supply disruptions. The successful execution of this strategy suggests management's capability to handle complex, multi-year capital projects—a competency that will be crucial as the company enters new businesses like CDMO and specialty chemicals.

VII. Modern Era: Technology, Sustainability & Growth (2020–Present)

The future of farming arrived not in Silicon Valley but in a field outside Warangal, Telangana, in 2021. A drone, no larger than a coffee table, hovered precisely three meters above a cotton crop, its rotors creating a perfect downwash that opened the plant canopy. In sixteen minutes, it had sprayed an entire acre with nano-DAP—a product that didn't exist five years ago, applied by a technology that was illegal in India until recently, operated by a farmer who had never used a computer until last year.

This scene encapsulates Coromandel's transformation in the 2020s—from a fertilizer manufacturer to an agricultural technology company. 18 manufacturing facilities across India now produce not just chemicals but solutions. The retail network of 900+ stores creating access to quality agri products has become platforms for digital services. And most remarkably, the company is pioneering products at the intersection of nanotechnology and agriculture.

The Nano Revolution

Coromandel has successfully developed a nanotechnology-based fertiliser, Nano DAP, from its R&D centre based at IIT Bombay. This wasn't incremental innovation—it was reimagining how nutrients are delivered to plants. Traditional DAP contains 46% phosphate and 18% nitrogen in crystalline form. Nano DAP contains the same nutrients in particles 30,000 times smaller than the width of human hair.

The implications are staggering. A 500ml bottle of nano DAP replaces a 50kg bag of conventional DAP. Application rates drop from 100kg per acre to 250ml. Transportation costs plummet. Storage becomes trivial. Most importantly, nutrient use efficiency jumps from 30% to over 80%—meaning less fertilizer achieves better results.

The development process took five years of collaboration between Coromandel's R&D team and IIT Bombay's Department of Chemical Engineering. The challenge wasn't just creating nano particles—that's relatively straightforward. The challenge was creating stable nano particles that remained in suspension, didn't agglomerate, survived field conditions, and actually improved plant uptake.

The Digital Agriculture Platform

Modern farming generates data—soil moisture, weather patterns, pest infestations, crop growth stages. Coromandel recognized that whoever controlled this data flow would control the future of agriculture. The company's digital initiatives, launched under the "Gromor Digital" brand, aimed to become the operating system for Indian farming.

The platform started simply—SMS advisories to farmers about weather and pest alerts. But it quickly evolved into a sophisticated system integrating satellite imagery, IoT sensors, and machine learning algorithms. Farmers could upload photos of diseased leaves and receive instant diagnosis and treatment recommendations. The system tracked individual fields, remembered cropping history, and provided personalized advice.

By 2024, over 2 million farmers were registered on the platform. But the real value wasn't in user numbers—it was in data. Coromandel knew what farmers were planting, when they were planting, what problems they faced, what products they used. This information fed into demand forecasting, inventory planning, and product development.

Drone Services: Coromandel Increases Stake in Dhaksha Unmanned Systems

Coromandel International Limited, through its subsidiary Coromandel Technology Limited (CTL), announced acquisition of an additional 7% stake in Chennai-based drone manufacturer Dhaksha Unmanned Systems Private Limited. Coromandel will invest INR 150 crores through fresh issue of shares to increase its overall shareholding in Dhaksha to 58%.

This wasn't just an investment—it was a strategic bet on the future of farming. Dhaksha is targeting sales of 3,500 drones out of a total industry sales of 10,000 units this year. The company has its manufacturing facility at Sholavaram near Chennai, which can produce around 40 drones per shift or 12,000 drones per year.

Gromor Drive: Drones as a Service

Currently operational in seven key states Andhra Pradesh, Telangana, Karnataka, Tamil Nadu, Maharashtra, Madhya Pradesh and Uttar Pradesh, Gromor Drive's operations are supported by RPTO-trained pilots. The service has covered 16,000+ acres of farmland through drone-led spraying—the first fertilizer company to achieve this milestone.

The economics are compelling. Drone technology is recorded to offer a remarkable efficiency boost for agriculture spraying services, covering up to 30 acres per day, while reducing water consumption by a staggering 90%. A drone can spray an acre in 15 minutes versus 4 hours manually. Chemical usage drops by 30% due to precision application. Most importantly, farmers avoid direct exposure to pesticides.

Coromandel's approach was unique. Instead of selling drones to farmers who couldn't afford or maintain them, they offered drone spraying as a service. Farmers paid per acre, making it accessible even to smallholders. The company trained local youth as drone pilots, creating rural employment. And they integrated drone services with their retail stores, creating a complete solution ecosystem.

The CDMO Pivot and Crop Protection Expansion

The Board in its meeting held today approved the company's plan to expand its operations in Crop Protection Chemicals and foray into Contract Development & Manufacturing Organisation (CDMO) business. Coromandel plans to invest Rs. 1,000 crores over the next two years in the above businesses.

This announcement in March 2023 marked Coromandel's most ambitious strategic pivot. Entry into CDMO business is a strategic portfolio choice where Coromandel can leverage its expertise in handling complex chemistries at commercial scale and strong development capabilities across various chemistries.

The CDMO opportunity was created by global supply chain realignments. Chinese chemical companies, facing environmental crackdowns and rising costs, were exiting certain molecules. Global agrochemical majors needed alternative suppliers who could meet quality standards, handle complex chemistries, and maintain confidentiality. Coromandel, with its manufacturing infrastructure and technical capabilities, was perfectly positioned.

The company's approach to CDMO is differentiated. Instead of competing on cost alone, they focus on complex, multi-step syntheses where technical expertise matters more than labor costs. They target molecules going off-patent, where innovator companies need manufacturing partners for their generic strategies. And they leverage their registration expertise to offer not just manufacturing but regulatory support.

The NACL Acquisition

2025: Acquired 53% stake in NACL Industries—a move that accelerated the CDMO strategy. NACL brought complementary capabilities: different chemistry expertise, established customer relationships, and most importantly, GMP-certified facilities that could manufacture pharmaceutical intermediates.

The integration strategy is sophisticated. Combining CIL's extensive distribution network and industry expertise with NACL's manufacturing infrastructure, strong domestic brand presence, global partnerships (including CDMO relationships), and R&D capabilities will drive faster commercialization of new products.

Sustainability as Strategy

Modern agriculture faces a paradox: it must produce more food while reducing environmental impact. Coromandel's sustainability initiatives aren't corporate greenwashing—they're strategic positioning for a carbon-constrained future.

The company's organic fertilizer business, initially a regulatory compliance exercise, has become a growth driver. Urban compost plants process city waste into agricultural inputs. Neem-based bio-pesticides leverage India's traditional knowledge with modern formulation technology. These products command premium prices and face less regulatory scrutiny.

Water management has become central to operations. The desalination plant at Visakhapatnam doesn't just ensure water security—it demonstrates to regulators and communities that the company can operate without depleting local resources. Rainwater harvesting, effluent treatment, and zero liquid discharge aren't costs; they're investments in operational continuity.

The Global Export Play

Nano fertilizers and global export journey represents Coromandel's ambition to become a global player. The company isn't just exporting commodities—it's exporting innovation. Nano DAP has received interest from Africa, Southeast Asia, and Latin America, regions facing similar agricultural challenges as India.

The export strategy leverages India's unique position. Labor costs are competitive with China. Technical capabilities match developed markets. Regulatory expertise from navigating India's complex system translates globally. And critically, India's diplomatic non-alignment means access to markets closed to Chinese or Western companies.

Financial Performance and Capital Allocation

Current financial performance: FY24-25 revenue at Rs. 24,428 Cr, up 10% YoY demonstrates the strategy's success. But the real story is in the changing revenue mix. Non-subsidy businesses now contribute over 30% of revenues with significantly higher margins.

Capital allocation has become more sophisticated. The company maintains dividend payout while investing in growth. Capacity expansion: As mentioned in Q2FY25, Coromandel's board approved capital projects amounting to ~Rs.800 crore. But equally important is investment in intangibles—R&D, brand building, farmer education, digital platforms.

Building for 2030

Planned foray into CDMO business with INR 1,000 crore investment positions Coromandel for the next decade. The vision is clear: become an integrated agricultural solutions company that happens to make fertilizers, rather than a fertilizer company trying to diversify.

The company is placing multiple bets: precision agriculture through drones and digital platforms, specialty chemicals through CDMO, sustainability through biologicals and nano-technology, and global expansion through exports. Not all will succeed, but the portfolio approach ensures resilience.

So What for Investors: The modern era transformation shows how traditional manufacturing companies can reinvent themselves through technology adoption and business model innovation. Coromandel's investments in drones, nano-technology, and digital platforms—while dilutive to near-term returns—position the company for secular trends like precision agriculture and sustainable farming. The CDMO pivot, with planned Rs 1,000 crore investment targeting 16-18% EBITDA margins, could transform the company's financial profile by adding a high-margin, asset-light business stream. The NACL acquisition at 53% stake demonstrates management's ability to execute complex M&A even in the current cycle. For investors, key monitorables include the pace of non-subsidy revenue growth, success in CDMO customer acquisition, and the commercial viability of innovations like nano-fertilizers. The company's evolution from a commodity manufacturer to a technology-enabled solutions provider suggests potential for multiple expansion as the market recognizes this transformation.

VIII. Market Position & Competitive Dynamics

The conference room at the Fertiliser Association of India's annual meeting in New Delhi buzzed with nervous energy. It was February 2024, and the industry faced an existential question: How do you compete when your biggest competitor isn't a company but a cooperative backed by millions of farmers?

IFFCO (Indian Farmers Fertiliser Cooperative) and KRIBHCO (Krishak Bharati Cooperative) together controlled over 35% of India's fertilizer market. They had patient capital from farmer-members, political support across party lines, and a distribution network that reached every village. Private players like Coromandel had to be twice as good just to stay even.

Yet somehow, Coromandel had carved out a unique position. Second-largest player in phosphatic fertiliser industry in India with Improved NPK & DAP market share to 17.2%. More remarkably, Top position as single largest producer of SSP with 13.8% market share. How did a private company outmaneuver cooperatives with seemingly insurmountable advantages?

The Cooperative Challenge

Understanding Indian fertilizer markets requires understanding cooperatives. IFFCO, established in 1967, isn't just a company—it's a movement. With 36,000 member cooperatives representing 55 million farmers, it combines the efficiency of corporate operations with the legitimacy of farmer ownership. When IFFCO enters a market, it doesn't just bring products; it brings votes.

KRIBHCO operates similarly, while state-level cooperatives like GSFC (Gujarat State Fertilizers & Chemicals) dominate regional markets. These aren't commercial enterprises optimizing for profit; they're quasi-governmental entities balancing social objectives with business sustainability.

The cooperatives' advantages are structural. They access subsidized credit from cooperative banks. Their dealer networks double as political organizations. Their brands carry the implicit endorsement of farmer solidarity. When choosing between identical products, farmers naturally prefer buying from "their" cooperative.

Coromandel's Differentiation Strategy

Coromandel couldn't beat cooperatives at their own game, so they changed the game. While cooperatives focused on volume and standard products, Coromandel specialized. It has ~40% share in the unique grade fertilizer sales in India—products tailored for specific crops and soil conditions that cooperatives' centralized manufacturing couldn't efficiently produce.

It has a leading position in the states of Andhra Pradesh and Telangana; India's largest complex-fertiliser markets. This geographic concentration wasn't weakness but strength. By dominating specific regions, Coromandel achieved economies of scale in distribution, built deeper farmer relationships, and could respond quickly to local needs.

The retail strategy was particularly clever. Started its first rural retail store in Andhra. Today, company operates ~750 stores in Andhra, Telangana, Karnataka and Maharashtra. These weren't just sales points but service centers. While cooperative outlets often operated part-time from village cooperative offices, Coromandel's stores were professional operations offering soil testing, credit, and agronomic advice.

The Quality Premium

In commoditized markets, Coromandel created differentiation through quality consistency. Farmers discovered that while all DAP should theoretically be identical, Coromandel's products had uniform granule size (better for mechanical spreading), lower moisture content (longer shelf life), and consistent nutrient levels (predictable results).

This quality premium allowed Coromandel to compete even when cooperatives offered lower prices. A 2% price premium meant nothing if crop yields improved by 5%. The company reinforced this through aggressive branding—"Gromor" and "Paramfos" became synonymous with quality in their stronghold markets.

Technology as Moat

Where cooperatives moved slowly due to their democratic decision-making, Coromandel moved fast. The company introduced new products every season, launched digital services while cooperatives still used paper ledgers, and deployed drones while competitors debated their utility.

It is a leading manufacturer of azadirachtin in the world with ~65% export share. This wasn't a market cooperatives even recognized as important initially. By the time they did, Coromandel had locked up raw material supplies, perfected extraction technology, and established global customer relationships.

Global Context and Competition

The Asia-Pacific region emerges as the primary market for DAP fertilizer, commanding a substantial share of global consumption, with China and India collectively accounting for over three-quarters of regional DAP usage. In this massive market, Coromandel competed not just with Indian players but with global giants.

International competitors like Mosaic (USA), OCP (Morocco), and PhosAgro (Russia) had advantages in raw material access. Chinese producers like Sinofert had scale. Middle Eastern players had access to cheap natural gas for nitrogen fertilizers. Yet Coromandel held its ground through local knowledge and relationships.

The global fertilizer industry is oligopolistic at the production level but fragmented at distribution. Global phosphate fertilizer market at $61.63 billion in 2021 is dominated by a handful of producers who control phosphate rock resources. But selling to millions of small farmers requires local presence, cultural understanding, and trust—areas where Coromandel excelled.

Government Relations: The Hidden Differentiator

In a heavily regulated industry, government relations capability becomes a competitive advantage. Coromandel mastered the art of policy navigation—never confrontational but always engaged. The company's executives served on government committees, provided technical expertise for policy formulation, and built relationships across the political spectrum.

This paid dividends in multiple ways. When subsidy payments delayed, Coromandel had the relationships to expedite processing. When new regulations were drafted, they had input into the process. When special allocations were made for disaster relief, Coromandel was positioned to participate.

The Distribution Battle

Distribution in rural India is about more than logistics—it's about relationships. Coromandel's 20,000+ dealer network wasn't built overnight. Each dealer relationship was cultivated over years, often decades. The company didn't just supply products; it provided credit, training, and support through crop failures and family emergencies.

The dealer network became self-reinforcing. Established dealers discouraged new entrants. They pushed Coromandel products even when competitors offered higher margins. They provided market intelligence that helped the company anticipate demand and adjust production.

Innovation in Marketing

While cooperatives relied on their institutional legitimacy, Coromandel innovated in farmer engagement. The company pioneered demonstration plots—fields where farmers could see results before committing. They organized farmer meetings that were part education, part social event. They created farmer clubs that built community while building brand loyalty.

The company's marketing wasn't just about selling products but about changing behavior. They educated farmers on soil health, promoted balanced nutrition over excessive urea use, and introduced concepts like micronutrient management. This positioned Coromandel not as a vendor but as a partner in prosperity.

Competitive Response Capability

When competitors launched new products, Coromandel responded within seasons, not years. When Chinese imports of specialty fertilizers increased, the company quickly developed import-substitution products. When organic farming gained traction, they acquired capabilities rather than dismissing the trend.

This agility came from decentralized decision-making. Regional managers had authority to adapt products, pricing, and promotion to local conditions. The corporate center set strategy, but execution was local. This contrasted with cooperatives' centralized structure where every decision required committee approval.

The Sustainability Advantage

As environmental concerns grew, Coromandel's investments in sustainable products became competitive advantages. Bio-pesticides, organic fertilizers, and nano-technology weren't just new products—they were entry tickets to premium markets that conventional players couldn't access.

Younger farmers, more educated and environmentally conscious, increasingly preferred suppliers who offered sustainable solutions. Coromandel's early investments in these areas positioned them as the progressive choice, attracting farmers who might otherwise default to cooperatives.

Managing Channel Conflict

Operating both retail stores and dealer networks created potential channel conflict. Coromandel managed this by clear segmentation—retail stores in semi-urban areas, dealers in rural markets. Stores offered services dealers couldn't provide, while dealers maintained relationships stores couldn't replicate.

The company also innovated in channel partnership. Dealers weren't just distributors but business partners. They received training, credit support, and exclusive territories. Many dealer businesses grew alongside Coromandel, creating aligned interests that transcended transactional relationships.

Future Competitive Dynamics

The competitive landscape is evolving rapidly. Digital platforms threaten traditional distribution. Global supply chain disruptions favor integrated players. Environmental regulations advantage companies with clean technology. In each trend, Coromandel is positioned favorably.

But new challenges emerge. Startup companies offering precision agriculture solutions compete for farmer attention. E-commerce platforms like BigHaat and AgroStar challenge traditional distribution. Global giants eye India's growing market. The competitive advantages that worked for decades may not work for the next decade.

So What for Investors: Coromandel's market position reveals the importance of regional dominance over national presence in fragmented markets. The company's strategy of controlling 40% of unique grade fertilizers while maintaining just 17% overall market share demonstrates profitable niching within commodity markets. The structural challenge from cooperatives (35%+ market share) is actually a hidden blessing—it prevents aggressive price competition while allowing private players to focus on value-added segments. The company's ability to maintain premium pricing through brand strength and service quality in a subsidy-controlled market suggests pricing power that could expand as subsidies eventually rationalize. For investors, key competitive metrics to monitor include market share in unique grades (currently 40%), regional dominance indicators in South India, and the relative growth rates of private players versus cooperatives. The company's successful competition against both subsidized cooperatives and global giants validates its moat durability.

IX. Playbook: Business & Investing Lessons

The Conglomerate Advantage: Patient Capital and Long-term Thinking

The Murugappa Group's century-old philosophy provided Coromandel with a crucial advantage: the ability to think in decades, not quarters. When the company invested ₹1,000 crores in backward integration projects that would take years to generate returns, they didn't face activist investor pressure or quarterly earnings calls questioning the ROI.

This patient capital advantage manifests in multiple ways. The group could fund Coromandel's losses during the integration of Godavari Fertilizers, support the decade-long development of nano-fertilizers, and absorb the initial losses from retail store expansion. Independent companies would have struggled to justify these investments to public markets focused on immediate returns.

But the conglomerate advantage goes beyond capital. The Murugappa Group's diversification across engineering, financial services, and agriculture created knowledge spillovers. Tube Investments' manufacturing expertise informed Coromandel's operational excellence. Cholamandalam Finance's rural networks provided market intelligence. The group's collective government relations capability opened doors no single company could access.

Vertical Integration as a Moat in Commodity Business

Coromandel's systematic backward integration—from trading to manufacturing to raw material production to mining—demonstrates how commodity businesses can build moats. Each step up the value chain reduced dependency, increased margins, and most importantly, ensured supply security during disruptions.

The integration wasn't pursued blindly. The company carefully evaluated make-versus-buy decisions at each stage. They integrated into phosphoric acid production when import dependence became a strategic vulnerability. They acquired mining assets when raw material quality became a differentiator. But they didn't integrate into shipping or sulphur mining where they lacked competitive advantage.

The lesson for commodity businesses: vertical integration creates value only when it solves strategic vulnerabilities or creates operational advantages. Integration for its own sake destroys value through capital inefficiency and operational complexity.

Managing Government Relations and Subsidy Dynamics

In regulated industries, government relations capability is as important as operational excellence. Coromandel's approach—engaged but not entangled, supportive but not subservient—provides a template for managing government stakeholders.