Symphony Limited: The World's Largest Air Cooler Story

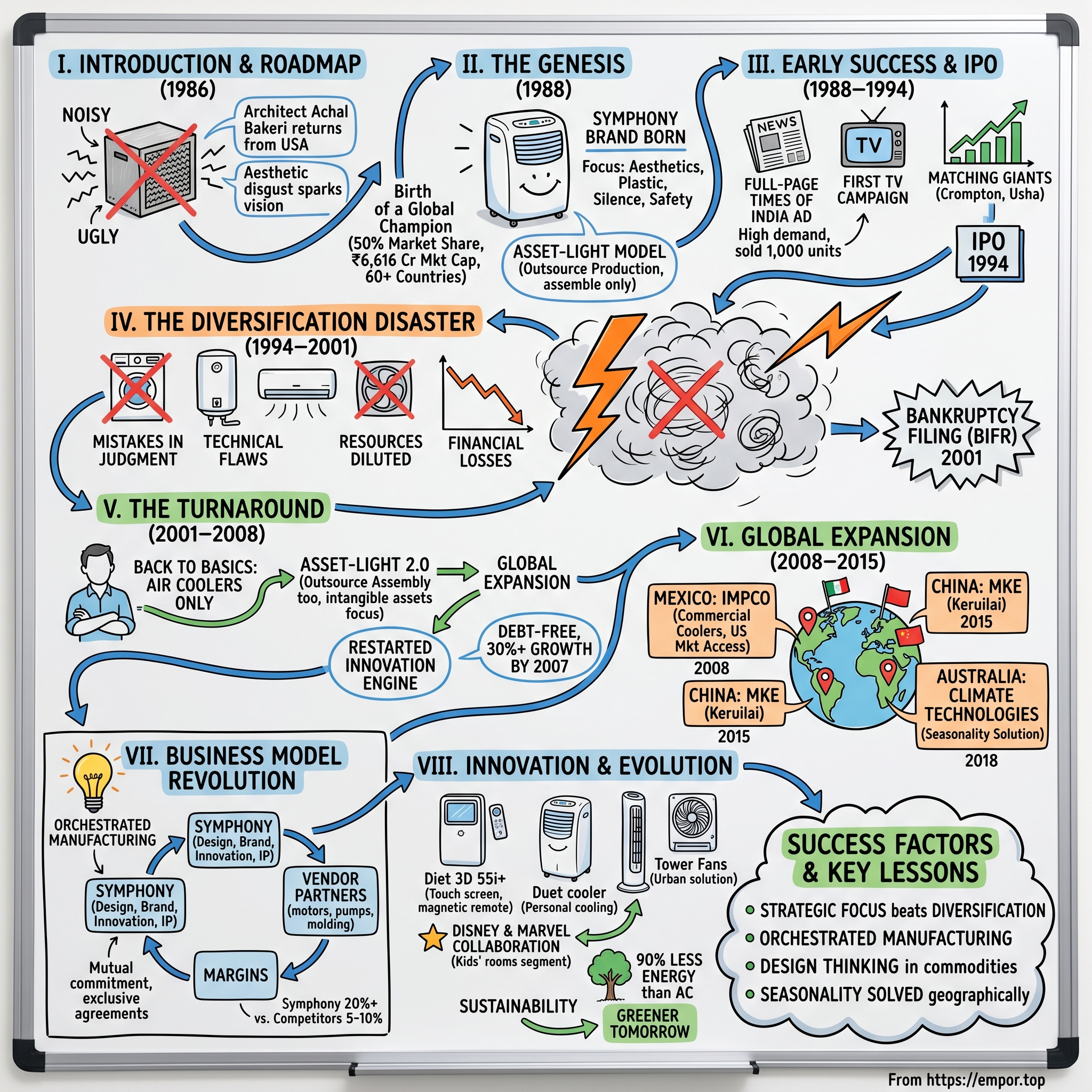

I. Introduction & Episode Roadmap

Picture this: A young architect returns from America in 1986, walks into his family's prosperous Ahmedabad home, and stares at an ugly, noisy metal box humming in the corner—an air cooler that looks like it belongs in a factory, not a living room. That moment of aesthetic disgust would spawn a company that today commands 50% of India's organized air cooler market and sells to Walmart, Home Depot, and customers across 60 countries.

Symphony Limited stands as an unlikely global champion. With a market cap of ₹6,616 crores, it's the world's largest air cooler manufacturer—a title that sounds almost quaint in an era of AI and semiconductors. Yet this is precisely what makes Symphony fascinating: while everyone chased software and services, Achal Bakeri built a manufacturing empire without owning a single factory. While competitors diversified into every appliance imaginable, Symphony learned through near-death that focus beats diversification every time.

The numbers tell a story of resurrection: From bankruptcy proceedings in 2001 with net losses exceeding revenues, to a 91,000% stock price appreciation over the following decade. How does a company selling what many consider a poor man's air conditioner become one of India's most successful consumer businesses?

This is a story about three profound business insights. First, that design thinking can transform commoditized markets—Symphony didn't just make air coolers; it reimagined them as lifestyle products. Second, that asset-light manufacturing isn't an oxymoron—the company generates 20%+ margins while outsourcing everything from production to assembly. Third, and most painfully learned, that strategic focus trumps diversification, even when every advisor tells you otherwise.

The themes we'll explore mirror the classic Acquired playbook: founder conviction in the face of existential crisis, the power of vertical integration (or in Symphony's case, radical dis-integration), and how emerging market entrepreneurs can build global champions. But there's a twist—this isn't about network effects or software margins. It's about making physical products for the bottom of the pyramid profitably, at scale, across continents.

II. The Genesis: Achal Bakeri's Architectural Vision (1986–1988)

Achal Bakeri wasn't supposed to be in the air cooler business. Son of successful real estate developer Anil Bakeri, he'd followed the prescribed path for ambitious Gujarati business families: architecture degree from the prestigious CEPT University in Ahmedabad, then an MBA from USC in Los Angeles. The plan was simple—get world-class education, return home, join the family business, build on what father created.

But when the 26-year-old returned to Ahmedabad in 1986, something felt off. "I wasn't adding any value," Bakeri would later recall. His father's real estate business was established, successful, running smoothly. The son with American degrees and architectural sensibilities found himself shuffling papers in an enterprise that didn't need transformation. The existential question every second-generation entrepreneur faces stared back at him: How do you prove yourself when your predecessor has already won?

The answer came from an unexpected source—aesthetic revulsion. Indian homes in the 1980s, even affluent ones, had a contradiction at their heart. Families would spend lakhs on marble flooring and designer furniture, then stick an industrial-looking metal air cooler in the corner that looked like it escaped from a factory floor. These machines were functional eyesores: prone to rust, dangerously close to electrocuting users when water met worn wiring, and producing a drone that made conversation difficult.

One evening, Bakeri complained about their home's cooler to his father. Anil Bakeri, in what would become a pivotal moment of reverse psychology, challenged his son: "If you think they're so ugly and problematic, why don't you make a better one? "The challenge became an obsession. Bakeri spent weeks studying the problem with an architect's eye and an entrepreneur's urgency. He launched Symphony in 1988 to bring aesthetics to the world of air coolers, albeit on a budget. The existing products had fundamental design flaws: "The existing air coolers were noisy, ugly, would rust very soon, and one could even be electrocuted," Bakeri recalled. His solution was radical for the time—use plastic instead of metal, make them look like air conditioners rather than industrial equipment, focus on silence and safety.

In February 1988, Bakeri started Symphony Limited in Ahmedabad with a seed capital of INR 100,000. He borrowed an additional ₹7 lakh from his father—not a handout, but a loan that carried the weight of expectation. The company initially operated as Sanskrut Comfort Systems Ltd. (SCS), manufacturing under the 'Symphony' brand name.

The design philosophy was revolutionary in its simplicity. While competitors saw air coolers as purely functional devices for the poor, Bakeri saw them as lifestyle products waiting to be reimagined. "We used plastic and the final product looked like a 1.5-tonne AC." By March 1988, they had six prototypes ready—sleek, quiet machines that wouldn't look out of place in a middle-class drawing room.

What's remarkable about Bakeri's approach was the immediate adoption of an asset-light model. Yet, it never manufactured coolers. "Manufacturing is a capital and management intensive process, and we thought it better to outsource it to specialised vendors," Bakeri said. Sanskrut would only assemble the various components into an air cooler under the Symphony brand. This wasn't born from sophisticated business school strategy—it was pragmatic entrepreneurship. With limited capital and no manufacturing experience, outsourcing wasn't just smart; it was survival.

The architect in Bakeri understood something his competitors missed: in India's aspirational middle class, aesthetics matter as much as functionality. A cooler wasn't just beating the heat; it was a statement about who you were and who you wanted to become. This insight would drive Symphony's growth for the next three decades, but first, it had to survive its own success.

III. Early Success & The IPO Years (1988–1994)

The summer of 1988 would test whether Bakeri's aesthetic gamble could translate into commercial success. Bakeri launched his product under the Symphony brand at Rs 4,300 a unit, putting out a full-page advertisement in India's largest-selling English-language newspapers, The Times of India. This was a time when ACs were selling at Rs 35,000 a unit and local air coolers at Rs 2,000.

The pricing strategy was audacious—more than double the cost of traditional coolers but a fraction of an air conditioner's price. Symphony positioned itself in the no-man's land between aspiration and affordability. The full-page Times of India advertisement wasn't just marketing; it was a statement of intent. Here was a startup declaring itself a premium brand from day one.

By the summer of 1988, demand had steadily grown and the company had sold 1,000 units, raking in Rs 40 lakh in sales. For context, this represented nearly 10% market share in the organized segment within the first season—unprecedented for a new entrant. For any new entrepreneur, especially in the product category, selling off all the units from the first batch can be overwhelming; however, Bakeri sold the entire lot by the end of the first summer of his business inception. Then later in the year 1990, Symphony aired its first TV campaign. The decision to invest in television advertising just two years after launch—when most startups were barely breaking even—showed Bakeri's understanding that building a consumer brand required reaching beyond newspaper readers. The TV campaign positioned Symphony not as a cheaper alternative to air conditioners but as a smarter choice for Indian conditions.

Within 2-3 years, Symphony was matching giants like Crompton Greaves, Usha, and Polar in the air cooler category. These were companies with decades of history, vast distribution networks, and deep pockets. Yet here was a startup from Ahmedabad competing on equal terms. The secret wasn't just better design—it was the entire business model.

The asset-light approach that would later become Symphony's defining characteristic was there from the beginning. While competitors built factories and hired thousands of workers, Symphony orchestrated a network of specialized vendors. Each component—motors, pumps, plastic molding—was outsourced to firms that did only that, ensuring both quality and cost efficiency. Symphony became the conductor of an industrial orchestra, creating harmony without owning the instruments.

Symphony went public in the year 1994 and was also listed at Bombay, Ahmedabad and Delhi stock exchanges. The IPO represented validation—six years from startup to public company, competing with established giants, all while maintaining the asset-light model that conventional wisdom said couldn't work in manufacturing.

The market's response was enthusiastic. Here was a company growing at 40-50% annually, with margins that defied industry norms, in a category everyone understood. Air coolers weren't sexy, but in a country where summer temperatures regularly exceeded 45°C and electricity was expensive and unreliable, they were essential. Symphony had found the sweet spot between necessity and aspiration.

Symphony's business was growing by leaps and bounds in the 90s and by the late 90s it had also crossed international boundaries. But success would breed its own challenges. The same advisors and bankers who celebrated the IPO began asking uncomfortable questions: What happens during monsoons when nobody buys coolers? How do you grow when you've already captured significant market share? Why limit yourself to one product when you have brand recognition and distribution?

These questions would lead Symphony down a path that nearly destroyed everything Bakeri had built. The diversification disaster that followed would become a textbook case of how strategic focus matters more than strategic optionality.

IV. The Diversification Disaster (1994–2001)

The advice came from everywhere—investment bankers, consultants, even well-meaning board members. "Air coolers are a seasonal product," Bakeri believed, hoping that foraying into other categories would help him scale his business. The logic seemed irrefutable: Symphony had built a brand, established distribution, proven its innovation capabilities. Why not leverage these assets across multiple categories?

The expansion began methodically, then accelerated into chaos. Symphony added washing machines, water heaters, air conditioners, and exhaust fans, among others to its portfolio, but none of them clicked with the market. Each new category seemed to make strategic sense. Geysers and room heaters for winter would balance the summer-heavy cooler sales. Washing machines would leverage relationships with the same dealers. Water purifiers capitalized on the growing health consciousness of India's middle class.

But Bakeri's explanation reveals a deeper problem: "The products were way ahead of their time. An entrepreneur can dream big, but you know it takes a while for dreams to materialise and everything can't happen overnight. And so probably they were mistakes in judgment getting into too many products at that time. We were a small company then and we did not have the resources."

The technical flaws multiplied across categories. The washing machines had innovative features but couldn't match the reliability of established brands. The water purifiers used cutting-edge technology that service centers couldn't repair. Each product launch divided management attention, diluted marketing budgets, confused dealers who had come to trust Symphony for cooling.

The financial hemorrhaging accelerated through the late 1990s. Inventory piled up in warehouses—unsold heaters during warm winters, washing machines that dealers refused to stock. The company built a large factory to manufacture these diverse products, abandoning the asset-light model that had been its strength. Fixed costs ballooned while revenues stagnated.

By 2001, the numbers told a story of complete collapse. In 1994 Symphony got listed on the Bombay Stock Exchange but a series of events and some mistakes in judgment and execution led to Symphony filing for bankruptcy in 2001. For the year ending June 2002, Symphony reported a net loss of ₹31 crore on total income of just ₹28 crore—losing more money than it brought in. The company that had IPO'd as a growth story seven years earlier was now technically insolvent.

The stock price reflected the disaster—Symphony became a penny stock, trading at a fraction of its IPO price. The company was referred to the Board for Industrial and Financial Reconstruction (BIFR), India's mechanism for dealing with sick companies. For most firms, BIFR referral was a death sentence, a prelude to liquidation.

The personal toll on Bakeri was crushing. Friends advised him to declare bankruptcy and walk away. Others suggested he swallow his pride and join his father's real estate business. Some even recommended leaving the country to escape the shame. "I had built this company from scratch and I couldn't watch it sink," said Bakeri.

The easiest path would have been liquidation. Sell the assets, pay what creditors you could, move on. Bakeri had his family's business to fall back on. He was still young enough to start over. No one would have blamed him—90% of startups fail, and Symphony had at least tasted success before falling.

But something in Bakeri refused to quit. Perhaps it was the memory of those first 1,000 units selling out in summer 1988. Perhaps it was pride—the architect who'd reimagined an entire category couldn't accept such an ungraceful exit. Or perhaps it was simpler: Symphony was his identity, and walking away meant admitting that identity was false.

"Stemming losses was our priority. We exhausted our inventory and ceased manufacturing operations in the other categories. In time, we exited and refocused on the business of air cooling." The turnaround would require not just returning to air coolers, but reimagining the entire business model from first principles. What emerged would be even more radical than the original Symphony—and far more successful.

V. The Turnaround: Back to Basics (2001–2008)

The boardroom at Symphony's Ahmedabad headquarters in 2002 must have felt like a wake. Creditors demanding payment, employees wondering about their futures, and at the center, Achal Bakeri facing the ruins of his entrepreneurial dream. The conventional playbook for BIFR companies was simple: massive layoffs, asset sales, and if lucky, acquisition by a competitor for spare parts.

Bakeri chose a different path. "In 2003, Symphony decided to approach the Indian government's Board for Industrial and Financial Reconstruction that helps sick companies restructure their businesses. The company began to revamp its business model and engage with more distributors. It began to outsource even the assembling of products and went back to being just an air cooler maker."

The restructuring was brutal in its simplicity. Between 2002 and 2004, Symphony exited all other categories and resumed its focus on air coolers. Every geyser, washing machine, and water purifier in inventory was sold at whatever price the market would bear. The large factory built during the diversification years—once seen as a symbol of Symphony's ambitions—was shut down. Even the assembly operations were outsourced.

What emerged was a company that barely resembled a traditional manufacturer. Symphony now owned almost nothing tangible—no factories, no assembly lines, minimal inventory. The company's primary assets were intangible: designs, patents, brand value, and relationships. Financial analysts struggled to categorize it. Was it a manufacturer without manufacturing? A brand licensing company? Something entirely new?

"In diverting our attention to diversification, we had stopped innovating. Although air coolers were still profitable, the business had stagnated. To rectify the situation, we developed new air-cooling products and moved to distribute these products internationally."

The innovation engine restarted with vengeance. Instead of spreading R&D across multiple categories, Symphony concentrated everything on cooling. New models emerged—coolers with remote controls, coolers that looked indistinguishable from air conditioners, portable coolers for small spaces. Each innovation targeted a specific customer pain point identified during the dark years.

The distribution strategy transformed completely. By 2008, Symphony also began to focus more on its distributor and dealer base. From about 100 distributors in 2007, it has 800 today, while the dealer number grew to over 20,000 in 2016, from 3,000 in 2007. Rather than trying to push multiple products through confused channels, Symphony made its dealers specialists in cooling. Training programs, better margins, and exclusive territories turned dealers into evangelists.

The international expansion that began during this period wasn't about escape—it was about validation. If Symphony could compete globally with its India-designed, India-made (through outsourcing) products, it would prove the model's robustness. The company began exhibiting at international trade shows, surprising attendees with coolers that looked nothing like the industrial boxes they expected.

The financial model that emerged was unprecedented in Indian manufacturing. With virtually no fixed assets, Symphony's capital requirements were minimal. Working capital needs were managed through dealer advances and vendor credit. The company generated cash from operations even while growing rapidly. This wasn't just asset-light—it was asset-invisible.

By 2007, the transformation was complete. Symphony had emerged from BIFR supervision, was debt-free, and growing at 30%+ annually. The company that nearly died from trying to do everything had been reborn by doing one thing exceptionally well. But Bakeri knew that to truly vindicate the model, Symphony needed to prove it could scale globally.

The opportunity would come from an unexpected source—a struggling American company that had pioneered commercial air cooling but lost its way. The acquisition of IMPCO would mark Symphony's transformation from Indian survivor to global champion, validating everything Bakeri had learned through failure.

VI. Global Expansion: The IMPCO Acquisition & Beyond (2008–2015)

The call came in 2006—International Metal Products Company (IMPCO), a pioneer in commercial air cooling based in Mexico, was for sale. Founded by Adam Goettl, the man who invented modern air coolers, IMPCO had opened its first manufacturing plant in Monterrey, Mexico in 1955. By the 1990s, after changing hands multiple times through McGraw-Edison, Arvin Industries, and others, the company was drowning in debt and operational chaos.

In 2006, Symphony acquired the Mexican holdings of International Metal Products Company (IMPCO). The acquisition price was remarkable: Symphony acquired the Mexican assets of the International Metal Products Company (IMPCO) which was founded by Adam Goettl, the man who invented air coolers for $650,000. For context, this was less than Symphony's quarterly profit at the time—a distressed asset price for a company with enormous strategic value.

Why would Symphony, having barely survived its own near-death experience, acquire another troubled company? Bakeri's answer revealed hard-won wisdom: IMPCO, however, was a loss making company and was on the verge of bankruptcy. But Symphony's BIFR experience gave them unique insight—they knew how to restructure broken businesses, having done it to themselves.

The strategic logic was compelling. IMPCO, based in Mexico manufactured industrial coolers that complemented Symphony's product line. Additionally, the acquisition provided Symphony access to the US market. While Symphony dominated residential cooling in India, IMPCO had technology and relationships in commercial cooling—factories, warehouses, outdoor venues. The companies were perfectly complementary.

On taking over IMPCO, Symphony dealt with several issues like financial crisis, operational inefficiencies, low employee productivity, IMPCO's poor brand image, lack of product innovation and weak sales and distribution. The turnaround playbook Symphony applied was familiar: streamline operations, focus on core products, rebuild distributor relationships, restart innovation.

But the real breakthrough came from cross-pollination. With this collaboration, Achal Bakeri realized that IMPCO's large commercial air coolers could be deployed to India too. In 2010, Symphony introduced Industrial coolers in Indian market. Meanwhile, Symphony's residential cooling expertise and cost-efficient Indian manufacturing (through its outsourcing network) made IMPCO products competitive again in North America.

The results vindicated the strategy. Leading air cooler maker Symphony Ltd has managed to turn around its Mexican subsidiary Impco, a company it had acquired in 2009 to get into the industrial cooler business. The acquisition opened doors to major American retailers—Walmart, Home Depot, Sears—who would never have considered an unknown Indian brand but were happy to work with IMPCO, now backed by Symphony's innovation and manufacturing capabilities.

The distribution explosion that followed was unprecedented. From about 100 distributors in 2007, it has 800 today, while the dealer number grew to over 20,000 in 2016, from 3,000 in 2007. The IMPCO acquisition had given Symphony credibility that no amount of marketing could have bought.

Emboldened by the IMPCO success, Symphony continued its international expansion. In the year 2015, Symphony announced acquisition of Chinese air cooler company Munters Keruilai Air Treatment Equipment (Guangdong) Co. Ltd. (MKE) that owns the brand Keruilai, for Rs 1.5 cr. They signed an equity transfer agreement with the shareholders of MKE to acquire 100 per cent of their equity share capital. This marked Symphony's entry into the China market which is the second largest air cooler market in the world after India.

The China acquisition was even more audacious than IMPCO. China wasn't just a market—it was Symphony's primary competition in global markets. By acquiring a local player, Symphony gained not just market access but insight into Chinese manufacturing and design approaches. Besides, losses at its Chinese subsidiary Guangdong Symphony Keruilai Air Coolers (GSK) have also been halved.

The masterstroke came in 2018. Further in 2018, Symphony announced its agreement to purchase 95% equity stake in Climate Technologies, an Australian manufacturer of cooling and heating products. The deal was signed as an opportunity to reduce business risks as a result of opposite winter and summer seasons in India and Australia. The acquisition was executed at a valuation range of A$40–44 million.

The Australian acquisition solved Symphony's eternal challenge—seasonality. When India entered monsoon season and cooler sales plummeted, Australia was heading into summer. The geographic diversification that Symphony had sought through product diversification in the 1990s was finally achieved through international expansion.

By 2015, the transformation was complete. Symphony's 25-30 percent of the turnover comes from international market as it covers Mexico, Europe, United States, West Asia and South-East Asia. The company that couldn't sell washing machines in Gujarat was now selling air coolers to Americans, Mexicans, Chinese, and Australians. The local had become global, but more importantly, the global expansion had made Symphony stronger locally.

VII. The Business Model Revolution

By 2014, Symphony's business model had evolved into something unprecedented in global manufacturing. Symphony (SYML) is the largest Air Cooler company in India, with 50% value market share in the organized market. This dominance wasn't achieved through traditional economies of scale—Symphony owned virtually no manufacturing assets. Instead, it had perfected what could be called "orchestrated manufacturing."

The numbers defied conventional business logic. SYML outsources 100% of its domestic production. It has tied up with OEMs supplying to the Auto industry and have surplus capacity and bandwidth to meet SYML's requirements. These OEMs work exclusively for SYML in the Air Cooler industry and can increase production through new lines at minimum cost. SYML has a monthly purchase order agreement with the OEMs, which gives it flexibility to manage inventory in case of a bad summer.

This wasn't simple contract manufacturing. Symphony had created a symbiotic ecosystem where vendors invested in Symphony-specific capabilities while Symphony focused entirely on design, innovation, and brand building. The financial implications were staggering—while competitors struggled with 5-10% margins, Symphony consistently delivered 20%+ operating margins.

The market structure itself favored Symphony's approach. Further, a large part of the cooler industry is unorganized at 80% (4m units) which makes the market potential for organized players (1m units) even larger. SYML, being the pioneer in the industry and holding a 50% market share, is best placed to capture this growth. The unorganized sector couldn't match Symphony's innovation pace or distribution reach, while organized competitors couldn't match its cost structure.

Revenue growth reflected this dominance. From ₹238 crore in 2010-11, Symphony reached ₹466.39 crore by 2014, representing a CAGR exceeding 40%. International operations contributed significantly—Symphony's 25-30 percent of the turnover comes from international market as it covers Mexico, Europe, United States, West Asia and South-East Asia.

The intellectual property portfolio became a moat. As of 9M25, the company holds 97+ designs, 20+ copyrights, 55+ patents(22 applied in FY24), and 417+ trademarks, with 27.5+ million air coolers sold worldwide. Each patent represented not just technical innovation but market understanding—coolers designed for Mumbai's humidity differed from those for Delhi's dry heat.

Distribution reached unprecedented scale. Symphony through Impco has tied up with large retailers like Walmart, Home Depot, Lowes, Famsa, Costco, etc in North America its residential air coolers. Due to limited presence in countries outside North America, SYML is aggressively looking to forge relationships with players globally. Recently, its tie up with Carrefour in Indonesia to offer its residential coolers to its customers goes in this direction.

The IMPCO synergy deserves special attention. Symphony's Surat SEZ facility didn't manufacture—it coordinated vendors who supplied to IMPCO's specifications. These products, designed in India but meeting American standards, were then exported through IMPCO's established channels. The result: Indian engineering reaching American homes through Mexican distribution.

What emerged was a new paradigm for emerging market manufacturing. Symphony proved you didn't need massive capital investments to build a global manufacturing business. You needed design excellence, distribution strength, and the ability to orchestrate a network of specialized partners. The company that nearly died trying to be everything had succeeded by owning almost nothing—except the customer relationship and the innovation process.

VIII. Product Innovation & Market Evolution

The Symphony showroom in Ahmedabad tells a story of evolution. From the original plastic boxes that replaced metal coolers in 1988 to today's IoT-enabled, voice-controlled cooling systems, each product generation reflects changing Indian aspirations. But the real innovation isn't in features—it's in understanding use cases that air conditioning manufacturers miss.

There is a compelling advantage of air cooler over air conditioners is that they consume less electricity. Number two, coolers are portable, you can simply place the same cooler in different places at your home. Coolers can also be used outdoors. These aren't just product benefits—they're lifestyle enablers for India's middle class, where electricity costs matter and outdoor living is central to social life.

The market opportunity remains massive despite Symphony's dominance. While 54% of Indian households live in hot and dry climatic conditions, only about 8% own Air Coolers. Thus, the market potential for Air Coolers in India is huge. This penetration gap represents not just sales potential but an innovation imperative—why haven't 92% of potential customers bought coolers? Symphony's answer has been relentless product innovation. Recent innovations include the Tabletop Duet cooler—a personal cooling device that sits on kitchen counters without disturbing cooking flames. The Diet 3D 55i+ range features automatic pop-up touch screen control and magnetic remote control, bringing smartphone-like interfaces to cooling. These aren't incremental improvements but category redefinitions.

The COVID pandemic accelerated another transformation. During the pandemic, Symphony further diversified with an omnichannel approach and launched its D2C wing. Direct-to-consumer wasn't just another sales channel—it provided real-time customer feedback that traditional distribution couldn't match. Symphony discovered use cases they never imagined: home offices needing silent cooling during video calls, urban apartments using coolers as air purifiers. The Disney collaboration exemplified Symphony's evolution. India's most loved and trusted air cooler brand, Symphony Limited has launched the country's first-ever Disney and Marvel-themed air coolers to give a respite from the scorching summer heat and add panache to your homes. Featuring Disney's beloved characters Frozen's Elsa and Anna, Princesses' Cinderella and fan favorite Marvel's Iron Man and Spider-Man; these coolers are packed with aesthetic appeal, innovation, and technology. In the summer of 2022 we scaled up our D2C business and at the same time we collaborated with Disney to launch a new air cooler collection for kids rooms.

This wasn't just slapping cartoon characters on products. Symphony recognized that children's rooms represented an underserved segment—parents wanted cooling solutions that were safe, quiet, and aesthetically pleasing for kids' spaces. The Disney coolers featured sleep modes, child-safe designs, and became conversation pieces rather than appliances to hide.

New categories emerged from understanding adjacencies. Symphony recently introduced residential tower fans—essentially coolers minus the water component. For urban apartments where water management is challenging, these provided Symphony-quality air circulation without the complexity of evaporative cooling.

The market dynamics continue to favor Symphony's innovation-led approach. The current market size stands at 7 million units worth ₹3,000 crore domestically, with expectations to reach 10 million units. Yet the unorganized sector still represents 70-80% of volumes, creating massive opportunity for conversion to branded products. Globally (excluding China), the market represents another ₹4,000 crore opportunity.

There is a compelling advantage of air cooler over air conditioners is that they consume less electricity. Number two, coolers are portable, you can simply place the same cooler in different places at your home. Coolers can also be used outdoors. These advantages become more pronounced as electricity costs rise and environmental consciousness grows. Air coolers consume 90% less electricity than air conditioners—a critical factor as India faces both power shortages and climate commitments.

The innovation pipeline reflects Symphony's understanding that cooling isn't just about temperature—it's about lifestyle enablement. Whether it's a kitchen cooler that doesn't disturb gas flames, a silent cooler for work-from-home professionals, or Disney-themed coolers that make children excited about their rooms, Symphony has transformed a commodity into a design statement.

IX. Playbook: Business & Investing Lessons

The Symphony story offers a masterclass in contrarian business building. While Silicon Valley preaches "move fast and break things," Symphony's journey suggests "focus deeply and build deliberately" might be equally valid. The lessons aren't just for emerging market entrepreneurs—they challenge fundamental assumptions about how modern businesses should be built.

The Focus Paradox: Symphony's near-death experience with diversification reveals a profound truth—focus isn't about doing one thing, it's about solving one problem completely. "An entrepreneur can dream big, but you know it takes a while for dreams to materialise and everything can't happen overnight. And so probably they were mistakes in judgment getting into too many products at that time." The company that tried to solve seasonal revenue through product diversification nearly died. The company that solved it through geographic diversification thrived.

Consider the timeline: 1994-2001 pursuing multiple product categories led to bankruptcy. 2006-2018 pursuing multiple geographies led to global dominance. Same problem (seasonality), different solutions, opposite outcomes. The lesson? Horizontal expansion within your core competency beats vertical expansion outside it.

Asset-Light Excellence: Symphony proves you can build a manufacturing powerhouse without manufacturing. SYML outsources 100% of its domestic production. It has tied up with OEMs supplying to the Auto industry and have surplus capacity and bandwidth to meet SYML's requirements. These OEMs work exclusively for SYML in the Air Cooler industry and can increase production through new lines at minimum cost. SYML has a monthly purchase order agreement with the OEMs, which gives it flexibility to manage inventory in case of a bad summer.

This isn't simple outsourcing—it's orchestrated manufacturing. Symphony controls the design, owns the customer relationship, manages the brand, but lets specialists handle production. The result: 20%+ operating margins in a business where competitors struggle to reach 10%. The model requires deep supplier relationships and rigorous quality control, but eliminates capital intensity.

Founder Conviction vs. Market Consensus: Every advisor told Bakeri to diversify. Every banker questioned the seasonal business model. The market valued Symphony as a penny stock. Yet "I had built this company from scratch and I couldn't watch it sink." This isn't stubborn founder syndrome—it's the difference between knowing your business and knowing about your business.

The 91,000% stock appreciation over 10 years wasn't luck—it was the market finally understanding what Bakeri always knew: in a country where 92% of hot/dry climate households don't own coolers, you don't need diversification. You need better coolers.

Design Thinking in Commoditized Markets: Symphony didn't innovate through technology breakthroughs—they innovated through design empathy. Understanding that coolers were eyesores led to aesthetic revolution. Recognizing that metal rusts and conducts electricity led to plastic adoption. Observing families on scooters didn't lead to cheaper coolers—it led to aspirational ones.

Emerging Market Arbitrage: Symphony exploited a unique arbitrage—global companies ignored air coolers (too small a market), while local companies couldn't innovate (too fragmented). By becoming the only focused, innovative, global player in the category, Symphony captured value that neither multinationals nor local players could access.

The Seasonality Solution: Most seasonal businesses try to smooth revenues through adjacent products. Symphony tried this and failed spectacularly. The successful solution was geographic smoothing—when India's monsoon arrives, Australia needs cooling. When Mexico's winter comes, Middle East summers begin. Same product, different markets, consistent revenue.

Capital Allocation Mastery: Post-2001, Symphony's capital allocation has been exemplary. No large factories, minimal working capital, strategic acquisitions at distressed prices (IMPCO for $650,000, MKE for ₹1.5 crore). The recent buyback of ₹71.4 crore at ₹2,500 per share shows confidence in intrinsic value.

"Failure can teach what lifetime of success cannot" - Achal Bakeri's observation captures Symphony's deepest lesson. The diversification disaster wasn't a detour—it was education. Without the BIFR experience, Symphony might never have developed the discipline that made it dominant. Without the near-death experience, the asset-light model might have remained theoretical.

For investors, Symphony represents a paradox: a manufacturing company that doesn't manufacture, a seasonal business with year-round revenues, an emerging market company with developed market margins. These contradictions aren't weaknesses—they're the moats that competitors can't cross.

X. Analysis & Bear vs. Bull Case

Bull Case: The Dominant Incumbent with Structural Tailwinds

Symphony's investment thesis rests on multiple structural advantages that compound over time. Start with market position: Symphony (SYML) is the largest Air Cooler company in India, with 50% value market share in the organized market. In most industries, 50% market share would invite regulatory scrutiny. In air coolers, it barely scratches the surface—the organized segment itself represents only 20% of total market volumes.

The TAM expansion opportunity is staggering. While 54% of Indian households live in hot and dry climatic conditions, only about 8% own Air Coolers. Thus, the market potential for Air Coolers in India is huge. This isn't speculative demand—it's basic physics. As temperatures rise and incomes grow, cooling shifts from luxury to necessity. With 143 million households in hot/dry climates and only 11 million owning coolers, the runway extends for decades.

The asset-light model creates a virtuous cycle. Without factory investments, Symphony can focus R&D spending on innovation rather than maintenance. The 97+ designs, 20+ copyrights, 55+ patents(22 applied in FY24), and 417+ trademarks, with 27.5+ million air coolers sold worldwide represent competitive advantages that grow stronger each year. Competitors must match this innovation while also building manufacturing—an almost impossible dual mandate.

Geographic diversification has finally solved the seasonality puzzle. With operations across 60 countries and opposite-season markets like Australia, Symphony achieves what product diversification couldn't: stable revenues without complexity. The model is proven—international markets contribute 25-30% of revenues and growing.

Climate change, paradoxically, strengthens Symphony's position. Rising temperatures increase cooling demand. Growing environmental consciousness favors evaporative cooling over energy-intensive air conditioning. Government focus on sustainable cooling solutions aligns with Symphony's core product. The company that started as an aesthetic choice has become an environmental imperative.

The financial metrics support premium valuation. Debt-free balance sheet, 20%+ operating margins, minimal capital requirements for growth, strong cash generation—these aren't temporary achievements but structural characteristics of the business model. The recent buyback at ₹2,500 per share signals management's confidence in intrinsic value.

Bear Case: Growth Deceleration and Structural Threats

The bearish perspective begins with recent performance. The company has delivered a poor sales growth of 7.40% over past five years. For a company in a supposedly under-penetrated market with dominant share, single-digit growth raises questions. Is the TAM real or theoretical? Are there hidden barriers to adoption that Symphony can't overcome?

The air conditioning threat looms larger each year. As India's per-capita income rises, the aspiration isn't for better coolers—it's for air conditioners. AC prices have fallen dramatically while electricity availability has improved. The same middle-class emergence that should drive cooler adoption might leapfrog directly to AC ownership, similar to how mobile phones killed landline expansion.

Unorganized competition remains resilient. Despite Symphony's innovation and brand strength, 70-80% of the market remains unorganized. Local manufacturers offer products at 50% of Symphony's price. For price-sensitive consumers, a basic cooling function might matter more than aesthetic appeal or IoT connectivity. The premium that Symphony commands could become a liability in price-conscious markets.

Single product concentration creates existential risk. Unlike diversified appliance companies, Symphony's entire fortune depends on air coolers. A breakthrough in AC technology, dramatic electricity cost reduction, or alternative cooling solutions could obsolete the entire category. The company that nearly died from diversification might be equally vulnerable from concentration.

Seasonal business risks persist despite geographic expansion. Unseasonal rains, cooler summers, or climate pattern changes can devastate single-year performance. While geographic diversification helps, India still represents the core market. One bad Indian summer can't be fully offset by Australian or Mexican sales.

The innovation edge might be narrowing. While Symphony holds numerous patents, the basic evaporative cooling technology hasn't fundamentally changed. Competitors can copy designs, match features, and offer similar products at lower prices. In commoditizing markets, innovation advantages tend to erode over time.

Market saturation in metros poses growth challenges. Urban markets, Symphony's traditional strength, show signs of saturation. Rural penetration requires different distribution models, price points, and product features. The company optimized for urban middle-class customers might struggle with rural mass-market dynamics.

The Verdict: Exceptional Business, Uncertain Growth

Symphony represents a fascinating investment paradox—an exceptional business model facing uncertain growth prospects. The company's transformation from bankruptcy to global dominance demonstrates execution excellence. The asset-light model, dominant market position, and innovation capabilities create substantial moats.

Yet the growth deceleration can't be ignored. Whether this represents temporary headwinds or structural challenges remains unclear. The bull case assumes TAM conversion accelerates; the bear case suspects it might never materialize at expected rates.

For long-term investors, Symphony offers a compelling risk-reward. The downside seems limited given the asset-light model and cash generation. The upside could be substantial if even a fraction of the TAM converts to organized, branded products. But expecting the explosive growth of the past decade might be unrealistic.

The investment decision ultimately depends on one's view of India's consumption trajectory. If you believe millions of Indian households will upgrade from suffering through summer to affordable cooling, Symphony stands to benefit disproportionately. If you believe they'll wait for AC prices to fall further or continue buying unbranded products, Symphony's premium valuation looks stretched.

XI. Epilogue & Recent Developments

Standing in Symphony's Ahmedabad headquarters today, you see a company that has traveled an extraordinary arc. From Achal Bakeri's aesthetic revolt against ugly coolers to commanding 18% global market share in 2025 with a strong presence in over 60 countries, the journey validates an unconventional approach to building a global manufacturing business.

The current numbers tell a story of sustained dominance despite challenges. Market cap stands at ₹6,512 crore, with revenue at ₹1,189 crore and profit at ₹167 crore. The stock trades at 8.56 times book value—neither cheap nor excessive for a company with Symphony's characteristics. Promoter holding remains steady at 73.4%, signaling the Bakeri family's continued confidence despite having multiple opportunities to cash out at peak valuations.

The recent share buyback deserves attention. The Business recently finished its share repurchasing program, spending Rs.71.4 crore to buy 2,85,600 shares at a price of 2500 each. In a market where many companies pursue growth at any cost, Symphony's decision to return capital demonstrates discipline. The buyback price of ₹2,500 compared to current levels suggests management sees intrinsic value above market price.

Climate change has transformed from threat to opportunity. Rising global temperatures—average global temperature has risen by 1.3°C above pre-industrial levels—create inexorable demand for cooling solutions. But the energy cost of cooling could cripple developing nations if met entirely through air conditioning. Symphony's evaporative cooling, using 90% less energy than AC, positions it as a climate adaptation solution rather than just a consumer product.

The sustainability angle grows more compelling each year. Symphony air coolers reduce carbon footprint that's equivalent to planting 14 trees per year and are engineered for a greener and cooler tomorrow. As governments implement carbon taxes and efficiency standards, Symphony's products shift from budget alternatives to policy solutions. The company that started by making coolers beautiful now makes them essential for sustainable development.

Recent market dynamics favor Symphony's positioning. In 2025, the Asia Pacific region continues to dominate the global air cooler market, accounting for 67% of the total demand. This high demand is attributed to the region's hot and humid climate, coupled with rapid urbanization and increasing disposable incomes. India leads the pack with an annual demand of 8.5 million units, followed closely by China at 7.2 million units.

The transformation isn't complete. Symphony recently opened subsidiaries in Brazil, expanding into Latin America's largest market. The U.S. operation shows particular promise—The U.S. market, for instance, has seen a 15% year-on-year increase in demand for smart air coolers equipped with features like remote control operation and IoT connectivity. American consumers, traditionally AC-focused, are discovering evaporative cooling for outdoor spaces, garages, and workshops.

What would success look like in 10 years? If Symphony achieves even 30% penetration in India's hot/dry climate households, it would mean selling to 43 million homes versus 11 million today—a 4x expansion. If the organized segment captures 50% share from unorganized players, Symphony's addressable market doubles again. Add international expansion, commercial cooling adoption, and climate-driven demand, and Symphony could be a ₹50,000 crore company.

The risks remain real. AC prices continue falling, Chinese competitors grow aggressive, and climate patterns might shift unexpectedly. But Symphony has survived bankruptcy, thrived through crises, and built a business model that turns conventional manufacturing wisdom upside down. The company that nearly died trying to be everything has found prosperity in being the world's best at one thing.

Achal Bakeri, now in his 60s, has built something remarkable—a global manufacturing champion that owns no factories, a seasonal business with year-round revenues, an emerging market company with developed market margins. Symphony's story isn't just about air coolers. It's about the power of focus, the value of design thinking, and the possibility of building world-class businesses from India.

The architect who set out to make air coolers beautiful has built something more valuable—a business model for the future. In a world where asset-light, sustainable, and focused businesses command premiums, Symphony looks less like a traditional manufacturer and more like a glimpse of what 21st-century manufacturing might become. The journey from ₹1 lakh seed capital to global market leadership proves that in business, as in architecture, the most enduring structures are often the simplest.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube