Dow Inc.: From Brine to Global Materials Science Giant

I. Introduction & Episode Roadmap

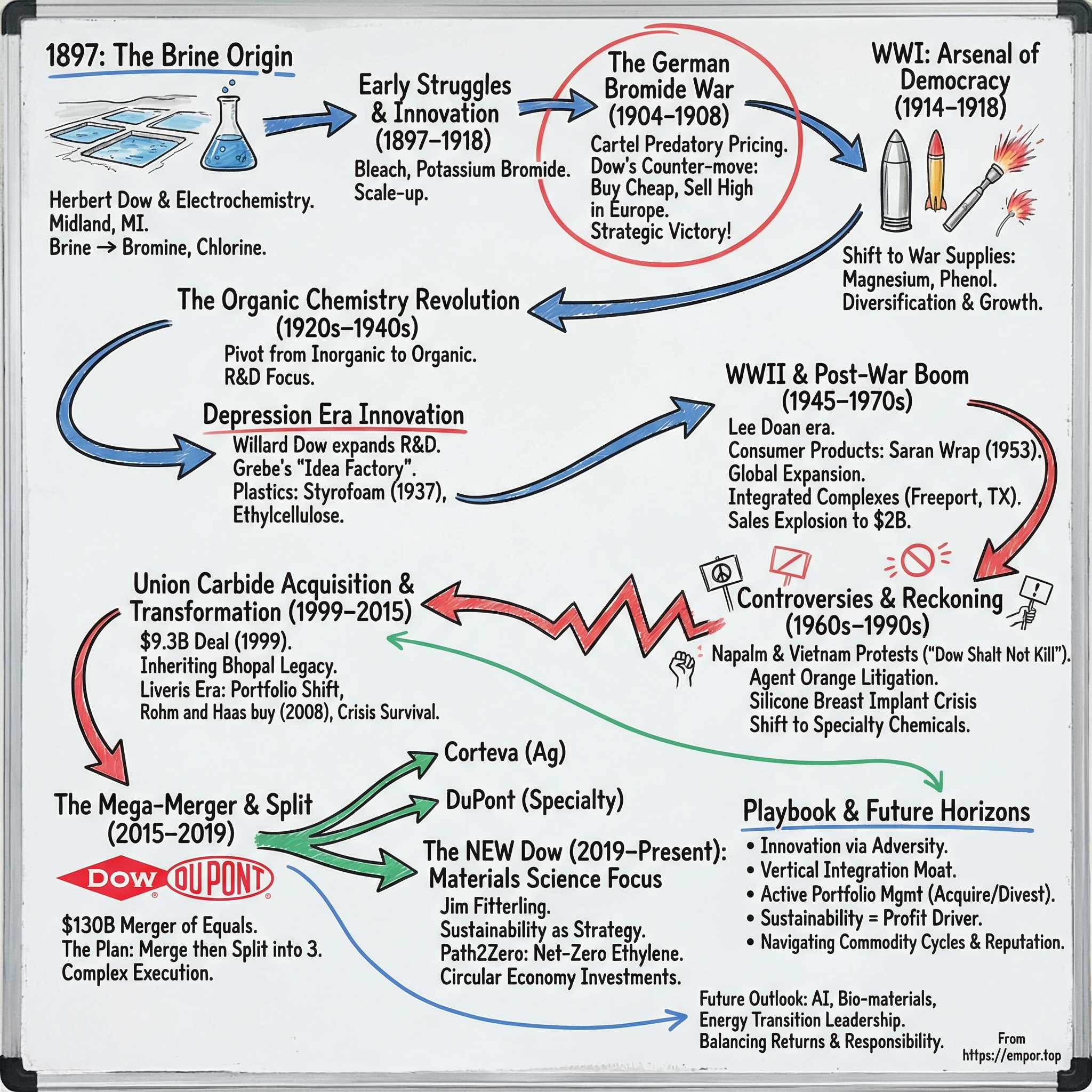

Picture this: A 31-year-old chemist in 1897 Michigan, staring at pools of underground brine that everyone else considers worthless saltwater. Herbert Henry Dow sees something different—he sees bromine, chlorine, and the building blocks of an empire. Fast forward 127 years, and that vision has morphed into Dow Inc., a $43 billion materials science colossus with manufacturing tentacles stretching across 31 countries and employing 35,900 people who wake up every morning to transform basic chemistry into the materials that define modern life.

How exactly did a lone inventor extracting bromine from Michigan brine build one of the world's largest chemical companies? How did a firm that started with bleach and potassium bromide evolve into a corporation whose products touch virtually every aspect of human existence—from the insulation in your walls to the plastics in your car to the packaging protecting your food?

This is a story of relentless innovation through adversity. It's about a company that turned World War I shortages into opportunities, transformed Depression-era desperation into R&D breakthroughs, and somehow navigated the treacherous waters of producing both life-saving medicines and controversial wartime chemicals. It's about strategic chess moves that would make any McKinsey consultant jealous—from outsmarting German cartels in the early 1900s to engineering one of the most complex corporate restructurings in history with the DowDuPont mega-merger.

We'll explore how Dow pioneered the integrated chemical complex model that became the industry standard, why they chose to inherit Union Carbide's Bhopal legacy, and how they're now attempting to lead the chemical industry's sustainability transformation while maintaining returns that keep Wall Street happy. Along the way, we'll unpack the strategic playbook that allowed Dow to survive and thrive through multiple existential crises, from environmental lawsuits to commodity price collapses to Chinese competition.

The themes that emerge are striking: innovation as a survival mechanism, vertical integration as competitive moat, portfolio transformation as perpetual motion, and the eternal tension between profitability and responsibility. This isn't just a corporate history—it's a masterclass in industrial strategy, chemical engineering, and the art of corporate reinvention. Buckle up for a journey from brine pools to boardrooms, from bromine to billions.

II. Herbert Dow's Origin Story & Early Innovation (1897–1918)

The Electrochemical Pioneer

In 1890, the Case School of Applied Science in Cleveland had a problem student. Herbert Henry Dow kept skipping classes—not to party or slack off, but to conduct unauthorized chemistry experiments in abandoned buildings around campus. His professors thought he was wasting his talent. Little did they know he was laying the groundwork for a chemical empire.

Dow's obsession wasn't random. Growing up in Cleveland, he'd become fascinated with the vast brine deposits beneath Michigan—ancient underground seas trapped in rock formations, loaded with chemicals that nobody knew how to extract economically. While his classmates studied textbook chemistry, Dow was inventing electrolytic cells in secret, convinced he could use electricity to liberate valuable chemicals from brine more efficiently than anyone had imagined.

His breakthrough came in 1891, just after graduation. On January 4, 1891, Herbert H. Dow succeeded in producing bromine electrolytically from central Michigan's rich brine resources. He had invented the Dow process, a method of bromine extraction using electrolysis to oxidize bromide to bromine. Instead of the traditional method that required expensive fuel to evaporate brine and multiple distillation steps, his electrolytic cell was the earliest devoted specifically to chemical manufacture.

The locals in Midland called him "Crazy Dow"—this fresh-faced 24-year-old who claimed he could extract a fortune from saltwater. He worked with makeshift resources—a rented mill building in Midland, Michigan, and a second-hand 15-volt generator turned by an old steam engine. But Dow's "craziness" was calculated genius. Dow became the world's most efficient bromine manufacturer through his successful application of electrochemistry.

The Company Takes Shape

By 1897, when he established The Dow Chemical Company, he had sufficient experience and financial backing to enter the world market for bromine. The early years were lean—the company originally sold only bleach and potassium bromide. But Dow was relentless in scaling up production. By 1902, just five years after founding, the company achieved a bleach output of 72 tons per day—a staggering volume for a startup operating from rural Michigan.

What made Dow different wasn't just his chemistry—it was his business philosophy. While other chemical companies focused on perfecting single products, Dow saw his brine wells as treasure chests of multiple chemicals waiting to be extracted. As he had predicted, Dow found many other uses for brine, and developed methods of extracting caustic soda, calcium, magnesium, and other minerals from it. Within twenty years, Dow had become a major producer of agricultural chemicals, elemental chlorine, phenol and other dyestuffs, and magnesium metal.

The German Bromide War: A Masterclass in Strategic Jujitsu

The story that best captures Herbert Dow's genius isn't about chemistry—it's about economic warfare. At the time, the German government supported a bromine cartel, Deutsche Bromkonvention, which had a near-monopoly on the supply of bromine, which they sold in the US for 49 cents per pound. Dow's company sold bromine in the United States for 36 cents per pound.

In 1904 Dow defied the cartel by beginning to export his bromine at its cheaper price to England. A few months later, an angry Bromkonvention representative visited Dow in his office and reminded him to cease exporting his bromine. Unafraid, Dow continued exporting to England and Japan.

The Germans' response was swift and brutal. The German cartel retaliated by dumping the US market with bromine at 15 cents a pound in an effort to put him out of business. This was predatory pricing at its most aggressive—selling at less than one-third of their normal price, accepting massive losses to destroy a competitor.

But here's where Dow's brilliance shines. Unable to compete with this predatory pricing in the U.S., Dow instructed his agents to buy up hundreds of thousands of pounds of the German bromine locally at the low price. The Dow company repackaged the bromine and exported it to Europe, selling it even to German companies at 27 cents a pound.

Think about the audacity of this move. Dow was buying German bromine at 15 cents in America and selling it back to Germans at 27 cents in Europe—an 80% markup using their own product against them. The cartel, having expected Dow to go out of business, was unable to comprehend what was driving the enormous demand for bromine in the U.S., and where all the cheap imported bromine dumping their market was coming from. They suspected their own members of violating their price-fixing agreement.

The cartel continued to slash prices on their bromine in the U.S., first to 12 cents a pound, and then to 10.5 cents per pound. The cartel finally caught on to Dow's tactic and realized that they could not keep selling below cost. They then increased their prices worldwide. Dow had won. A small American startup had outmaneuvered the mighty German chemical cartel through sheer strategic brilliance.

World War I: From Outsider to Arsenal of Democracy

When World War I erupted in 1914, it created both crisis and opportunity for Dow. The United States suddenly found itself cut off from German chemical supplies—and Germany had been the world's undisputed chemical leader. The federal government turned to Herbert Dow with an urgent question: Could he replace German imports?

Dow's answer transformed his company from a regional bromine producer into a strategic national asset. During World War I, Dow supplied many war materials that the United States had previously imported from Germany. The company pivoted with remarkable speed, producing magnesium for incendiary flares that lit up no-man's land, monochlorobenzene and phenol for explosives that armed American doughboys, and bromine for both medicines and tear gas.

The numbers tell the story of this transformation: By 1918, 90 percent of Dow's production was geared toward the war effort. This wasn't just business—it was a complete reinvention of the company's identity. Dow went from being "Crazy Dow" extracting bromine from brine to being an essential component of American military capability.

The war years also accelerated Dow's diversification strategy. Each new military requirement forced the company to innovate, to find new ways to extract and combine chemicals from their Michigan brine. The knowledge gained during these years—working under pressure, at scale, with life-or-death stakes—would lay the foundation for Dow's post-war expansion into consumer chemicals and materials science. The company that emerged from World War I was fundamentally different from the one that entered it: battle-tested, diversified, and ready to help build the American Century.

III. The Organic Chemistry Revolution (1920s–1940s)

The Pivot to Organic Chemistry

In 1920, Herbert Dow made a decision that would define his company's next century: He looked at the booming automobile industry in nearby Detroit, at the explosion of consumer goods, at the revolution in synthetic materials happening in German laboratories, and declared that Dow Chemical's future lay not in extracting inorganic chemicals from brine, but in building complex organic molecules that could transform American life.

This wasn't an obvious move. Dow had built his fortune on electrochemistry and inorganic compounds. Organic chemistry—the manipulation of carbon-based molecules—was largely a German specialty, protected by patents, trade secrets, and decades of expertise. But Dow saw opportunity where others saw obstacles. If World War I had taught him anything, it was that American dependence on German chemistry was a strategic vulnerability that needed to be fixed.

The shift required massive investment in research at a time when most chemical companies were content to manufacture commodities. Dow hired organic chemists from universities, built new laboratories, and gave his researchers something rare in corporate America: permission to fail. He understood that organic chemistry was about patient experimentation, about trying thousands of combinations to find the one that worked.

Innovation During the Depression

When Herbert Dow died suddenly in October 1930—just weeks after the stock market crash that triggered the Great Depression—the company faced an existential choice. Herbert's son, Willard H. Dow, just 33 years old, took the helm of a company whose sales were collapsing along with the global economy. Chemical prices plummeted. Customers canceled orders. Banks called in loans.

Most companies responded to the Depression by slashing research budgets, firing scientists, and hunkering down to survive. Willard Dow did the opposite. In what seemed like madness at the time, he expanded Dow's research operations, reasoning that the Depression had created a buyer's market for scientific talent. While competitors laid off their best chemists, Dow hired them. While other companies canceled research projects, Dow launched new ones. This contrarian strategy worked brilliantly. Dow invested heavily in research and development during the Great Depression. In fact, during the depths of the Great Depression, when many other chemical companies were cutting back on research, Dow continued to expand its investment in R&D. In the depths of the Depression, Willard H. Dow expanded Dow research at a time when other companies cut back.

The centerpiece of this strategy was the Physics Laboratory, which under the leadership of John J. Grebe became known as "an idea factory." Over a 20-year span beginning in the mid-1920s, the Physics Lab was responsible for a long list of innovations, which laid the base of knowledge for product lines that remain key markets for Dow decades later. These products included a range of chemistries for the agricultural, pharmaceutical, water purification, building, energy and automotive industries.

Grebe's management philosophy was revolutionary for its time. Anyone with an idea needed to write it down on a card, sign and date it, and then pin it to the bulletin board to be discussed. He even carefully thought through the physical layout of the laboratory space to encourage open dialogue, making sure his team members had to walk past their colleagues to get anywhere. "I find talking over a project with others enhances its value, develops its progress more swiftly, focuses light on obscure aspects," he said. "No mere man should walk alone among ideas."

The Plastic Revolution

The payoff from Willard's Depression-era research investments came faster than anyone expected. In the 1930s, Dow began producing plastic resins, which would grow to become one of the corporation's major businesses. Its first plastic products were ethylcellulose, made in 1935, and polystyrene, made in 1937.

These weren't just incremental improvements on existing products—they were entirely new materials that would reshape American life. Midland's Physics Lab, headed by its brilliant director, John Grebe, was responsible for a long list of innovations, including automatic controls, DOWTHERM™ products, waste disposal bacteria, ethylene research, styrene, STYROFOAM™, PVC, Saran, ion exchange resins, polystyrene and Ethafoam.

The development of Styrofoam in particular showcased Dow's approach to innovation. The material was discovered almost by accident when a Dow scientist was trying to create a flexible rubber-like substance. Instead, he created a rigid foam that was 98% air but incredibly strong and insulating. Rather than discard this "failure," Dow's researchers recognized its potential. By the late 1930s, Styrofoam was being tested for everything from building insulation to flotation devices.

Foreign Expansion Begins

As war clouds gathered in Europe and Asia, Willard Dow made another contrarian decision. In 1942, Dow began its foreign expansion with the formation of Dow Chemical of Canada in Sarnia, Ontario to produce styrene for use in styrene-butadiene synthetic rubber. This wasn't just about market access—it was about building redundancy into Dow's production system as the world prepared for war.

The transformation from Depression survivor to wartime supplier would complete Dow's evolution from regional chemical producer to national industrial champion. By the time Willard Dow died in a tragic plane crash in 1949, he had grown company revenue 700%—a seven-fold increase that positioned Dow for the post-war chemical boom that was about to transform the world.

IV. Post-War Expansion & The Plastics Age (1945–1970s)

The Accidental Dynasty

On March 31, 1949, a DC-3 carrying Willard Dow and his wife Martha crashed in freezing rain near London, Ontario. In an instant, Dow Chemical lost its visionary leader, the man who had navigated the company through Depression and war. The board faced a crisis: Who could possibly replace a Dow at Dow Chemical?

Their answer was surprising—Leland "Lee" Doan, Willard's brother-in-law, a man with no formal chemistry training who had married into the Dow family. Wall Street was skeptical. How could a non-chemist run one of America's most sophisticated chemical companies? But Doan understood something his critics didn't: The post-war economy wouldn't be won in laboratories alone, but in boardrooms, marketing departments, and on factory floors around the world. In the year of Willard's death, 1949, sales were $200 million, but ten years later they had nearly quadrupled. In the year of Willard's death, 1949, sales were $200 million, but ten years later they had nearly quadrupled. Under Doan's leadership, employment at Dow more than doubled to 31,000 from 14,000, and sales soared to $890 million from $200 million during his 13-year tenure.

The Suburban Chemical Revolution

What Doan understood was that the post-war American Dream ran on chemicals. As wartime production gave way to a peacetime economy, residential construction boomed. By 1960, 62 percent of Americans owned their own homes. As the consumer economy grew, so did the demand for household products. Every new ranch house in Levittown needed insulation (Styrofoam), every kitchen needed food wrap (Saran Wrap), every refrigerator needed plastic shelving (Styron).

Dow, a company accustomed to selling its products to other companies, recognized the opportunity and soon developed a wealth of products fit for mass consumption, from Styron refrigerator shelves to Saran Wrap®. The company that had supplied bromides to photography companies now sold directly to housewives. Dow launched its first consumer product, Saran Wrap, in 1953. Saran Wrap, a thin plastic film, was sold in rolls and used primarily for wrapping food. This product binds tightly to the wrapped food and keeps water and gas from getting through the thin plastic, thus keeping the material that is inside fresh over a longer period of time.

The marketing transformation was radical. Dow embarked on a major consumer push during the 1940s and 1950s, connecting its plastics materials and products with everyday household needs – from food preservation and presentation to toys. This trend continued into the 1970s, and along the way advertising moved into new media like television.

The Infrastructure of Growth

While Madison Avenue sold the dream, Dow's engineers were building the infrastructure to support it. During his tenure, Lee Doan built a larger sales force trained to become market and production analysts and serve Dow's industrial customers. He also invested in an expansion program focused on plastics and invested in plants outside of Midland and Texas. Doan's goal was to build new plants as near as possible to the consumers of the plants' products, avoiding the risks associated with a too-great concentration of resources in the older divisions.

The crown jewel of this expansion was Freeport, Texas. What started as a magnesium extraction plant had evolved into something unprecedented: The Freeport plant is Dow's largest site, and the largest integrated chemical manufacturing site in the country. The site grew quickly – with power, chlorine, caustic soda and ethylene also soon in production. This wasn't just a factory—it was a city of chemistry, where the waste products of one process became the feedstock for another, creating an ecosystem of efficiency that competitors struggled to replicate.

Going Global: The International Chess Game

The 1950s and 1960s marked Dow's transformation from American chemical company to global powerhouse. After World War II, Dow's export department in Midland consisted of only an export sales manager and two salesmen – each of whom divided the world between them. This soon changed in the 1950s, as Dow gradually evolved from a domestic company into an international operation. In the early 1950s, the Company began to emphasize foreign sales with the formation of Dow Chemical Inter-American, responsible for trade in Latin America, and Dow Chemical International, responsible for trade in all other parts of the world.

The expansion strategy was sophisticated. In 1952, Dow entered into a joint venture to form its first overseas subsidiary, Asahi-Dow Limited in Japan, where it developed into a major supplier of plastics for the nation. Rather than simply exporting products, Dow built local partnerships and manufacturing capabilities. When Dow realized that constructing manufacturing facilities in other countries created demand, they began producing plastics in Germany, Greece, Spain and Italy. The largest investment was in the Netherlands, at Terneuzen. That chemical complex opened in 1965.

By 1965, the company had grown so large and complex that traditional management structures were breaking down. With extensive operations all around the world, Doan and his managers had a meeting in 1965 where they acknowledged the need to decentralize. They established a headquarters on every continent to manage business. Dow Europe, Dow Latin America and Dow Pacific were established in 1966.

The Numbers Tell the Story

The financial transformation under the Doan family was staggering. By 1964, Dow sales exceeded $1 billion for the first time and reached $2 billion in 1971, less than a decade later. In 1964, it reached sales of $1 billion, but its sales had doubled to $2 billion by 1971. It subsequently hit $10 billion in sales in 1980.

This wasn't just growth—it was an explosion. Throughout the 1960s, Dow's earnings increased approximately 10 percent each year. The company that Herbert Dow had started with a second-hand generator and some Michigan brine was now by 1974, Dow was the most profitable chemical company in the world.

But success came with complications. The very plastics that made Dow wealthy were about to make it infamous.

V. Controversies & Corporate Responsibility (1960s–1990s)

When Chemistry Meets Conscience

In 1965, a Dow sales representative received an unusual order from the U.S. Department of Defense: 10 million pounds of something called "napalm B." The compound—polystyrene thickened gasoline that stuck to skin and burned at 1,500 degrees Fahrenheit—wasn't new to Dow. They'd been making incendiary materials since World War II. But this order was different. This was for Vietnam, and soon everyone would know Dow's name.

Among the company's hundreds of products, however, one began to receive an inordinate amount of publicity—napalm. Beginning in 1966 the company became the target of anti-Vietnam War protests. Company recruiters were overrun on college campuses by large numbers of placard-waving students. Dow defended its manufacture of the searing chemical by saying that it was not responsible for U.S. policy in Indochina and that it should not deprive American fighting men of a weapon that the Pentagon thought was necessary.

The protests were unlike anything corporate America had seen. Students didn't just boycott Dow products—they physically blocked recruiters from entering campus buildings. At the University of Wisconsin in 1967, a Dow recruitment session sparked a riot that left 65 students injured. The company that had helped win World War II was now cast as a merchant of death. "Dow shalt not kill" became a rallying cry. The images of children running from napalm attacks, particularly the Pulitzer Prize-winning photograph of Phan Thi Kim Phuc, became inextricably linked with Dow's corporate identity.

Agent Orange: The Ghost That Haunts

But napalm was just the beginning. During the Vietnam War the company produced napalm, a jellied incendiary reported to have been used indiscriminately against civilians and soldiers. Dow was also one of several makers of Agent Orange, a defoliant containing the toxic substance dioxin. The U.S. military sprayed 20 million gallons of Agent Orange over Vietnam, Laos, and Cambodia to destroy jungle cover. Dow executives insisted they were simply fulfilling government contracts, providing materials the Pentagon deemed essential.

The real reckoning came years later, when Vietnam veterans began developing cancers, neurological disorders, and children with birth defects. In 1984 Dow and the other chemical companies settled a class-action lawsuit out of court by agreeing to establish a $180 million fund for the use of veterans and the families of veterans exposed to Agent Orange. The settlement covered 250,000 veterans, but it was just the beginning of Agent Orange litigation that would stretch for decades.

The Silicone Breast Implant Crisis

Just as Dow was recovering from the Vietnam controversies, another crisis emerged from an unexpected source: its joint venture, Dow Corning. Founded in 1943 as a 50-50 partnership between Dow Chemical and Corning Glass, Dow Corning had become the world's largest manufacturer of silicone products. In the early 1960s, Dow Corning began collaborating with two Texas plastic surgeons, Frank Gerow and Thomas Cronin, on silicone breast implants. By the early 1990s, over a million women had received these implants.

Then the lawsuits began. In 1984, Maria Stern won $211,000 in compensatory damages and $1.5 million in punitive damages from silicone breast implant manufacturer Dow Corning after claiming that her breast implants caused autoimmune disease. In February Dow Corning released confidential internal memoranda that acknowledged that the company had known for decades that silicone gel would seep out of the implants.

The financial tsunami was devastating. When a 1994 class-action settlement set aside $4.25 billion to pay damages, a quarter of a million women—20 percent of implant recipients—claimed to be ill and therefore eligible for compensation. The largest manufacturer, Dow Corning, filed for bankruptcy protection in 1995. Dow Corning Corp. has agreed to pay $3.2 billion to settle claims of about 170,000 women who say their silicone breast implants made them sick. If the proposed settlement is approved, individual women could receive from $12,000 to $60,000 apiece.

The bankruptcy protection lasted an astounding nine years. Dow Corning Corp. emerged Tuesday after nearly a decade of bankruptcy protection related to thousands of silicone breast implant liability lawsuits. The irony was bitter: scientific studies eventually showed no link between silicone implants and the systemic diseases claimed by plaintiffs. In June of 1994, the New England Journal of Medicine published a study by Mayo Clinic epidemiologists that found no increased risk of connective tissue disease in women with silicone gel breast implants. In 1995, the Journal followed with yet another study—this one larger and more refined—that found no association between implants and connective tissue disorders.

Strategic Transformation: From Controversy to Specialization

The cumulative effect of these controversies forced a fundamental reckoning at Dow. The company that had proudly supplied materials for national defense was now seen by many as a corporate villain. Campus recruiters faced protests. Consumer boycotts threatened retail products. The Dow brand, once associated with American innovation, had become toxic in some circles.

The response was a gradual but decisive shift in business strategy. Rather than abandon controversial products entirely, Dow began a systematic transformation from commodity chemicals toward specialty materials. This wasn't just about public relations—it was about margin enhancement and strategic positioning. Specialty chemicals commanded higher prices, required deeper customer relationships, and were less vulnerable to the boom-bust cycles that plagued commodity markets.

The transformation accelerated in the 1980s and 1990s. Research spending remained at almost 90 percent of cash flow. Extra-strong ceramics and plastics for the electronics industry are among the numerous specialty chemicals that Dow hoped would account for two-thirds of its sales in the 1990s. The company still placed a premium on innovation, however, and stated that it anticipated placing 15 to 25 new products on the market each year.

This strategic pivot represented more than a business decision—it was an acknowledgment that chemical companies could no longer operate in isolation from social concerns. The controversies of the 1960s through 1990s had taught Dow a painful lesson: in the modern world, corporate success required not just technical excellence but social license to operate. The company that emerged from this crucible was different—more cautious, more sophisticated, and more aware that every molecule it produced carried not just chemical properties but social and ethical implications.

VI. Union Carbide Acquisition & Transformation (1999–2015)

The Deal That Changed Everything

On August 4, 1999, Dow Chemical CEO William Stavropoulos stood before a packed conference room at the St. Regis Hotel in New York. The financial press had been summoned for what Dow called a "major strategic announcement." Stavropoulos, a chemical engineer who had risen through Dow's ranks over 32 years, dropped the bombshell: In August 1999, Dow agreed to acquire Union Carbide Corporation (UCC) for $9.3 billion in stock.

The room erupted. Union Carbide wasn't just any chemical company—it was the company forever associated with Bhopal, site of history's worst industrial disaster. On December 3, 1984, a gas leak at Union Carbide's pesticide plant in Bhopal, India, had released methyl isocyanate into the surrounding shantytown, killing thousands immediately and affecting hundreds of thousands more. The disaster had become shorthand for corporate irresponsibility, the subject of documentaries, books, and ongoing litigation. Wall Street loved the deal. Dow Chemical announced the purchase of Carbide in 1999 for $8.89 billion in stock. The deal was consummated in 2001 and valued at $11.6 billion. The acquisition would create the world's second-largest chemical company, giving Dow access to Union Carbide's specialty chemicals portfolio and strengthening its position against rivals like BASF and DuPont.

But the moral calculus was troubling. More than 16 years after the Bhopal gas leak, TDCC acquired all of the shares of UCC stock, and UCC became a wholly owned subsidiary of TDCC in February 2001. By acquiring Union Carbide, Dow was inheriting not just assets but also the ghost of Bhopal—ongoing litigation, environmental contamination, and the fury of survivors who still sought justice.

The Legal Architecture of Denial

Dow's lawyers had constructed an elaborate legal firewall. The Dow Chemical Company (TDCC) never owned or operated the Bhopal plant, they argued. The plant was owned and operated by Union Carbide India Limited (UCIL), a Indian company in which Union Carbide (UCC) held just over half the stock. When UCC became a subsidiary of TDCC in 2001, TDCC did not assume UCC's liabilities. Dow and UCC did not merge and did not become the same company. Since the 2001 transaction, UCC has operated as a wholly-owned subsidiary of TDCC, with its own assets and liabilities distinct and separate from TDCC's.

The legal sophistication was impressive, but it couldn't hide an uncomfortable reality. UCC has paid dividends to Dow since completion of the acquisition in 2001. From 2009-2011 these dividends amounted to $2200m. Indeed, Dow was quick to pay off an outstanding claim against Union Carbide soon after it acquired the company, setting aside $2.2 billion to compensate former Union Carbide asbestos workers in Texas. Though swift to accept historical liabilities inherited from Union Carbide in North America, Dow stringently maintains that it isn't liable for Union Carbide's historical actions in Bhopal.

Andrew Liveris and the Transformation Strategy

In 2004, Dow brought in Andrew Liveris, an Australian chemical engineer who had spent 28 years rising through Dow's ranks in Asia. The Company's longest-serving CEO, during his more than 14-year tenure as Chairman and CEO, Andrew N. Liveris transformed Dow from a cyclical chemicals manufacturing company into one powered by science, driven by innovation and delivering solutions to the world.

Liveris understood that Dow couldn't outrun its controversies—it had to transform beyond them. His strategy was bold: move Dow up the value chain from commodity chemicals to specialty materials, innovation-driven products with higher margins and deeper customer relationships. During nearly a decade as Dow's CEO, Liveris has led the Company's transformation from a cyclical chemicals manufacturing company into a novel enterprise – one powered by science, driven by innovation and delivering solutions to the world.

The centerpiece of this transformation was audacious. Liveris' strongest move to implement the strategy came with the purchase of Rohm and Haas in the summer of 2008 for $16.2 billion. This Fortune 500 company, a leader in speciality chemicals, was the subject of a global auction, which Dow won with a bid of $16.2 billion. The timing couldn't have been worse—or perhaps better, depending on your perspective.

The Kuwait Crisis and Near-Death Experience

The acquisition closed during the 2008 financial crisis. The credit crisis caused one of Dow's joint venture partners, Petrochemical Industries Company (PIC) of the State of Kuwait, a wholly owned subsidiary of Kuwait Petroleum Corporation (KPC), to withdraw from a planned partnership in basic plastics, despite an agreed contract, depriving Dow of $9 billion in proceeds designated to fund the Rohm and Haas deal.

Dow was suddenly facing financial catastrophe. The company had committed to the largest acquisition in its history just as credit markets froze and a major funding source evaporated. Liveris and his team scrambled to save the company. In March 2009, Liveris and his management team organized a plan to implement the Rohm and Haas integration, focusing on growth and cost synergies, but also reducing costly debt from the transaction through public offerings, along with equity offers. The plan also called for the divestiture of non-strategic assets, which was accomplished through a sales process that assured maximum valuation.

The near-death experience forced Dow to accelerate its transformation. Non-core assets were sold, costs were slashed, and the integration with Rohm and Haas was executed with military precision. The acquisition proved to be synergistic in terms of growth, allowing a broader and deeper presentation to clients with regard to value-added chemicals, plastics, and materials, but also in terms of costs.

By the time Liveris stepped down in 2018, he had fundamentally reshaped Dow. The company that had acquired Union Carbide with all its baggage had transformed itself into a materials science innovator, setting the stage for the most ambitious corporate restructuring in chemical industry history—the DowDuPont merger and three-way split.

VII. The DowDuPont Mega-Merger & Three-Way Split (2015–2019)

The $130 Billion Chess Move

On December 11, 2015, at 6:00 AM Eastern Time, two press releases hit the wires simultaneously. They announced what seemed impossible: On Dec. 11, 2015, The Dow Chemical Company and E. I. du Pont de Nemours and Company announced entry into an Agreement and Plan of Merger. The two titans of American chemistry—fierce rivals for over a century—would merge in a deal valued at $130 billion, creating the world's largest chemical company.

But this wasn't a typical merger. From the beginning, the plan was to merge only to split apart. The companies would combine, reorganize their portfolios, and then separate into three focused companies: an agricultural giant (Corteva), a materials science leader (new Dow), and a specialty products innovator (new DuPont). It was corporate surgery on an unprecedented scale.

Wall Street was skeptical. How do you merge two companies with combined revenues of $85 billion, 110,000 employees, and operations in 180 countries—only to split them apart 18 months later? The complexity was staggering. Every product, every plant, every employee had to be assigned to one of three buckets. Supply chains had to be untangled. IT systems had to be separated. Customer relationships had to be maintained through the chaos.

The Rationale: Why Merge to Split?

The logic, while counterintuitive, was compelling. Both Dow and DuPont were conglomerates with overlapping but not identical portfolios. Both had agricultural divisions competing with Monsanto and Syngenta. Both had specialty chemical businesses fighting for the same customers. Both had commodity operations suffering from Chinese overcapacity.A merger allowed them to combine similar businesses, achieve massive scale, and capture synergies before splitting into focused pure-plays. The transaction is expected to result in run-rate cost synergies of approximately $3 billion and the potential for approximately $1 billion in growth synergies. The merger created significant value for shareholders through cost synergies estimated at $3 billion and potential growth synergies of $1 billion.

The Execution Marathon

The execution was even more complex than anticipated. Effective Aug. 31, 2017, the Merger Transaction was completed and each of Dow and DuPont became subsidiaries of DowDuPont Inc. But this was just the beginning. "We had literally 700 cost actions we were taking with the synergies between Dow and DuPont," says Ed Breen, DuPont's CEO who would become executive chairman of DowDuPont.

The organizational structure was unique. We had to make a choice: Do we create one company and later spin out three, or do we immediately upon close go from two companies to three divisions with a thin holding-company structure on top? We did the latter, which meant that DowDuPont essentially had no employees. DowDuPont officers were the two CEOs of legacy companies, me as the CFO of both, the three COOs of the divisions who would become CEOs of the new companies, and the two general counsels.

This structure allowed the three future companies to begin operating independently from day one, reducing uncertainty for employees and customers. It took about 90 days to make sure everybody knew where they would land, but that one decision helped streamline the decision making and figure out who was accountable for what.

The Cost of Transformation

The human cost was significant. DowDuPont Chief Executive Officer Ed Breen is shutting down research and development projects that are expensive, require years of work and may have poor investment returns. He calls these projects, "moonshots," and considers them a waste of money. They say they will run the merged organization "lean and mean" by shutting down plants, eliminating jobs, laying-off employees and reducing the number of suppliers.

The cost-cutting was brutal but effective. Before splitting into three independent segments, the material sciences and agriculture divisions each are eliminating over $1 billion in costs and the specialties segment is expected to save just under $1 billion. Nearly 60 percent of DuPont's corporate overhead costs have been eliminated.

The Three-Way Split: Birth of New Giants

After 18 months spun off the merged entity's material science divisions into a new corporate entity bearing Dow Chemical's name and agribusiness divisions into the newly created Corteva. The execution took longer than originally planned. DowDuPont remains on track to separate the Materials Science division (Dow) by April 1, 2019, and the Agriculture (Corteva Agriscience) and Specialty Products (DuPont) divisions by June 1, 2019.

On March 12, 2018, Jim Fitterling was named the CEO of the new Dow Inc., which was split, on April 1, 2019, from DowDuPont. Dow separated from DowDuPont in April. On June 1, DowDuPont separated its agricultural chemical and seed business into a standalone company called Corteva Agriscience. The remaining entity became the new DuPont, focused on specialty materials.

Each company emerged with distinct identities and strategies: - New Dow: Focused on materials science, commodity and specialty plastics, with $43 billion in revenues - Corteva Agriscience: Combined agriculture businesses with $14.3 billion in 2018 sales, 56% from seeds, balance from crop protection - New DuPont: Four business segments (transportation and advanced polymers, electronics and imaging, safety and construction, and nutrition and biosciences) with $22.6 billion in 2018 sales

The financial engineering worked. The breakup into three companies aimed to unlock greater shareholder value by allowing each entity to focus on its core business. Investors applauded the focused strategies, cleaner portfolios, and elimination of conglomerate discounts.

But the real test would come in the following years, as each company faced its own challenges in increasingly competitive and regulated markets.

VIII. The New Dow: Materials Science Focus (2019–Present)

Jim Fitterling's Vision

When Jim Fitterling took the helm of the newly independent Dow Inc. on April 1, 2019, he faced a daunting challenge. After the corporate gymnastics of the DowDuPont merger and split, Dow needed to prove it could stand alone and thrive. Fitterling, who had joined Dow in 1984 as a co-op student and worked his way up through engineering and commercial roles, brought both institutional knowledge and fresh perspective.

Fitterling led Dow's transformation from a lower-margin, commodity company to one deeply focused on higher-growth markets that value innovation. His strategy was clear: leverage Dow's massive scale and integration advantages while pivoting toward sustainability and circular economy solutions. This wasn't greenwashing—it was a fundamental reimagining of what a chemical company could be in the 21st century.

The Sustainability Transformation

Under Fitterling's leadership, Dow has accelerated environmental sustainability targets to put the Company on a path to achieving carbon neutrality and eliminating plastic waste. By 2030 Dow will reduce its net annual carbon emissions by 5 million metric tons – a 15% reduction vs. its 2020 baseline. These weren't just aspirational goals—they came with concrete investments and technological innovations. The centerpiece of this strategy is the Path2Zero project. Dow announced today its plan to build the world's first net-zero carbon emissions integrated ethylene cracker and derivatives site with respect to scope 1 and 2 carbon dioxide emissions. The project would more than triple Dow's ethylene and polyethylene capacity from its Fort Saskatchewan, Alberta site, while retrofitting the site's existing assets to net-zero carbon emissions. Decarbonizes ~20% of Dow's global ethylene capacity while growing polyethylene supply by ~15% and supporting ~$1 billion of EBITDA growth by 2030.

Decarbonize and Grow: The Business Case for Sustainability

In 2024, we continued to implement our Decarbonize & Grow strategy and launched our Water & Nature strategy. Both are critical for long-term business growth. The genius of Dow's approach is that it treats decarbonization not as a cost but as an investment opportunity. We are investing $1 billion per year on average across the economic cycle to drive growth and decarbonization of our manufacturing assets.

The financial logic is compelling. We remain on track to deliver $3 billion in underlying EBITDA improvements, as we reduce Scope 1 and 2 net annual GHG emissions by 5 million metric tons versus our 2020 baseline by 2030. This isn't greenwashing—it's a fundamental redesign of Dow's business model where sustainability drives profitability.

The strategy encompasses multiple initiatives: - Clean Energy Integration: Integrate clean energy including renewables and nuclear for power and steam. Selected Seadrift, TX site for safe, reliable and emissions free advanced SMR nuclear energy project. Secured access to >1000 MW of renewable power for Dow's sites. - Circular Economy Leadership: By 2030, Dow will transform plastic waste and other forms of alternative feedstock to commercialize 3 million metric tons of circular and renewable solutions annually. - Water Stewardship: By 2030, Dow will implement a robust land management strategy, our top 20 water-dependent sites will have water stewardship plans, and 10 of those sites will be water-resilient.

Current Market Position and Competitive Dynamics

Despite the transformation efforts, Dow faces significant headwinds. The chemical industry is experiencing overcapacity, particularly from Chinese producers who have built massive facilities regardless of global demand. Commodity chemical margins are under pressure. Environmental regulations are tightening globally. And the specter of Dow's controversial past—from Agent Orange to Bhopal—continues to complicate its social license to operate.

Yet Dow's position is stronger than it might appear. The company's integrated production model—where the waste of one process becomes the feedstock for another—provides cost advantages that are difficult to replicate. Its scale allows for investments in sustainability technologies that smaller competitors can't afford. And ironically, tightening environmental regulations may actually benefit Dow by raising barriers to entry and forcing out less efficient competitors.

The transformation under Fitterling represents a bet that the chemical industry's future lies not in producing more stuff cheaper, but in producing better stuff more sustainably. It's a vision where Dow becomes not just a supplier of materials but a partner in the circular economy, where every molecule is designed for reuse, where carbon neutrality isn't an aspiration but a business model.

IX. Playbook: Business & Strategic Lessons

Innovation Through Adversity: The Dow Pattern

Throughout its 127-year history, Dow has displayed an almost uncanny ability to transform crises into catalysts for innovation. When German cartels tried to destroy Herbert Dow with predatory pricing, he turned their weapon against them, buying their cheap bromides and reselling them at a profit. When the Depression crushed demand, Willard Dow doubled down on R&D, hiring the best scientists at bargain prices. When credit markets froze during the 2008 financial crisis, threatening the Rohm and Haas acquisition, Dow executed one of the fastest and most successful integrations in chemical industry history.

This pattern reveals a deeper truth: Adversity forces choices that prosperity allows you to avoid. In good times, companies can afford inefficiency, redundancy, and strategic drift. Crisis strips away these luxuries, forcing brutal prioritization. Dow's repeated success in these moments suggests an organizational culture that doesn't just survive pressure but requires it to reach peak performance.

The Power of Vertical Integration and Feedstock Advantage

Dow's integrated production model represents one of the most underappreciated competitive advantages in industrial history. The Freeport complex isn't just a collection of chemical plants—it's an ecosystem where ethylene becomes polyethylene, where chlorine combines with ethylene to make vinyl chloride, where every waste stream becomes someone else's raw material.

This integration provides three distinct advantages: 1. Cost Leadership: By eliminating transportation costs between production steps and capturing value at every stage of the chain, Dow achieves costs that standalone producers can't match 2. Supply Security: When global supply chains break, integrated producers keep running 3. Innovation Acceleration: Having all production steps under one roof allows for rapid experimentation and process optimization

The model is extraordinarily difficult to replicate. Building an integrated complex requires billions in capital, decades of operational expertise, and access to competitive feedstocks. Once established, these complexes become nearly impregnable competitive moats.

Managing Complexity: From Single Product to Global Conglomerate

Dow's evolution from a single-product bromide extractor to a global materials science company offers a masterclass in complexity management. The company didn't just add products—it built systems. Each new chemistry wasn't viewed in isolation but as part of an expanding network of possibilities.

The key insight was recognizing that chemical companies don't really sell molecules—they sell solutions to problems. Farmers don't want pesticides; they want higher yields. Automakers don't want plastics; they want lighter, stronger materials. By organizing around customer needs rather than chemical categories, Dow could leverage its broad portfolio more effectively than specialists could leverage their depth.

Portfolio Transformation: Knowing When to Divest vs. Acquire

Dow's history is littered with bold acquisitions and equally bold divestitures. The company bought Union Carbide despite its Bhopal liability, merged with DuPont only to split apart, and sold consumer brands like Saran Wrap that had defined it for generations. Each move reflects a disciplined approach to portfolio management:

Acquire when: - Assets are undervalued due to temporary distress - Integration can unlock significant synergies - The purchase strengthens existing market positions - Technology or market access justifies the premium

Divest when: - Assets no longer fit the strategic focus - Someone else can extract more value - Capital can be redeployed at higher returns - Regulatory or reputational costs exceed benefits

The Union Carbide acquisition exemplified this calculus. Despite Bhopal's reputational baggage, Dow saw undervalued specialty chemical assets that could be integrated into its existing operations. The legal structure kept liabilities at arm's length while allowing operational integration.

The Merge-and-Split Strategy: Creating Focused Pure-Plays

The DowDuPont transaction pioneered a new model for corporate restructuring: the merge-and-split. Rather than each company trying to optimize its conglomerate portfolio independently, they combined forces to create scale, captured synergies, then separated into focused entities.

The strategy offers several advantages: - Scale for Synergies: Combined companies can eliminate more costs than either could alone - Clean Portfolio Construction: Starting fresh allows optimal business unit allocation - Market Timing: Different businesses can be spun out when market conditions are favorable - Regulatory Approval: Easier to get approval for a merger with planned divestitures

The execution complexity is enormous, requiring precise choreography of legal structures, IT systems, customer relationships, and employee morale. But when executed well, it can unlock billions in value that traditional restructuring can't access.

Sustainability as Business Strategy, Not Just CSR

Dow's current transformation treats sustainability not as a cost center but as a profit driver. This isn't corporate altruism—it's recognition that the chemical industry's license to operate depends on addressing environmental concerns, and that customers increasingly demand sustainable solutions.

The Path2Zero project exemplifies this approach. By building the world's first net-zero ethylene cracker, Dow isn't just reducing emissions—it's creating a premium product category. Customers will pay more for plastics with lower carbon footprints. Governments will provide incentives. Competitors will struggle to match the offering without similar investments.

Leadership Through Controversy and Reputation Management

Perhaps no major corporation has faced more reputational challenges than Dow—from napalm to Agent Orange to Bhopal's ongoing legacy. Yet the company has not only survived but thrived, offering lessons in crisis management:

- Legal Structure as Shield: Keeping controversial assets in separate legal entities limits contagion

- Time as Ally: Public memory fades; operational excellence endures

- Strategic Patience: Don't make dramatic moves during peak controversy

- Continuous Transformation: New achievements eventually overshadow old controversies

- Local Engagement: Strong community relationships provide resilience during global criticism

The approach is morally complex but strategically effective. By maintaining legal distance from historical liabilities while focusing on future innovation, Dow has managed to rebuild its reputation without fully resolving its past.

X. Analysis & Investment Case

Current Financials and Market Position

Dow Inc. today stands as a $43 billion revenue materials science leader, manufacturing in 31 countries with approximately 35,900 employees. The company has emerged from the DowDuPont restructuring as a more focused, more profitable enterprise. The portfolio is cleaner, the strategy is clearer, and the balance sheet is stronger than it's been in decades.

But the numbers only tell part of the story. Dow operates in an industry where success is measured not in quarters but in decades, where a single plant can cost billions and take years to build, where competitive advantages are built on proprietary processes developed over generations.

Competitive Positioning vs. BASF, SABIC, LyondellBasell

In the global chemical oligopoly, Dow occupies a unique position. Companies such as BASF (Germany), Dow (U.S.), SABIC (Saudi Arabia), Exxon Mobil Corporation (U.S.), and DuPont (U.S.) and among others, are the major companies in the chemical market. Each competitor brings distinct advantages:

BASF: The German giant remains the world's largest chemical company by revenue, with unmatched portfolio breadth and European market dominance. However, Europe's severing of ties with Russia after the invasion of Ukraine cut the industry off from an abundant supply of natural gas and exacerbated the sector's weakness. European companies like BASF, Ineos, Covestro, Arkema, and Evonik Industries posted sharp declines in chemical sales.

SABIC: Backed by Saudi Aramco's feedstock advantage, SABIC enjoys some of the lowest production costs globally. Sabic, a subsidiary of Saudi Aramco since 2020, is also parting with a business it has run for more than 40 years. It is moving forward with a $6.4 billion petrochemical joint venture in Fujian Province, China, with a local partner.

LyondellBasell: Pure-play petrochemical focus provides operational efficiency but limits growth options. The petrochemical sector is facing its own downturn, primarily driven by new capacity in China and the US. Declines in chemical sales and profits at Dow, ExxonMobil, LyondellBasell Industries, Indorama Ventures, and Braskem reflect that.

Dow's competitive advantages rest on three pillars: 1. Geographic Balance: Unlike European competitors struggling with energy costs or Middle Eastern players dependent on oil prices, Dow's global footprint provides resilience 2. Integration Depth: Few competitors match Dow's level of vertical integration from basic feedstocks to specialty products 3. Sustainability Leadership: Dow's Path2Zero and circular economy initiatives position it ahead of competitors in meeting customer sustainability demands

Bull Case: Decarbonization Leader, Innovation Pipeline, Circular Economy

The bull case for Dow rests on its transformation from commodity chemical producer to sustainability solutions provider. The Path2Zero project alone could generate $1 billion in EBITDA by 2030 while positioning Dow as the preferred supplier for customers with net-zero commitments. The company's innovation pipeline, focused on circular economy solutions and bio-based materials, addresses growing regulatory and consumer pressure for sustainable products.

The numbers support this optimism. Global chemical production is projected to grow 3.5% in 2025. The global specialty chemicals market is expected to grow from $800 billion in 2023, to reach $1040.9 billion in 2029, at a CAGR of 4.48%. Dow's positioning in high-growth segments like packaging, infrastructure, and renewable energy provides exposure to secular growth trends.

Moreover, Dow's disciplined capital allocation—targeting returns above 13% through the cycle—ensures that growth investments enhance rather than dilute returns. The company's commitment to returning cash to shareholders through dividends and buybacks provides downside protection while maintaining upside optionality.

Bear Case: Commodity Exposure, China Competition, Regulatory Pressures

The bear case is equally compelling. Despite transformation efforts, Dow remains significantly exposed to commodity chemicals subject to brutal price cycles. The biggest structural change by far to the sector in recent years is the rise of several Chinese petrochemical producers. Chinese overcapacity in basic chemicals continues to pressure margins globally.

Regulatory pressures are intensifying. Extended producer responsibility laws, plastic taxes, and chemical bans threaten traditional business models. Dow's historical liabilities—from Bhopal to PFAS contamination—create ongoing legal and reputational risks that are difficult to quantify but impossible to ignore.

The macroeconomic environment adds further uncertainty. Interest rate volatility, trade tensions, and recession risks all disproportionately impact capital-intensive, cyclical businesses like chemicals. Dow's high fixed costs and operational leverage amplify both upside and downside movements.

Capital Allocation Strategy and Shareholder Returns

Dow's capital allocation framework balances growth investment with shareholder returns. The company targets: - Growth Capex: ~$1 billion annually for decarbonization and capacity expansion - Maintenance Capex: ~$1.5 billion annually to sustain operations - Dividend: Sustainable and growing, currently yielding ~5% - Share Buybacks: Opportunistic, dependent on cash generation and market conditions

This framework reflects a mature company generating substantial cash flow but facing limited high-return growth opportunities. The emphasis on dividends over buybacks suggests management's confidence in sustainable cash generation but acknowledgment of cyclical volatility.

Long-term Growth Drivers and Risks

The investment case ultimately depends on one's view of several long-term trends:

Growth Drivers: - Sustainability regulations driving demand for low-carbon materials - Circular economy creating new markets for recycled and bio-based chemicals - Infrastructure investment requiring advanced materials - Electrification and renewable energy demanding specialty chemicals

Key Risks: - Structural overcapacity in commodity chemicals - Breakthrough technologies disrupting traditional materials - Accelerating deglobalization fragmenting markets - Climate change impacts on coastal production facilities - Ongoing liability from historical operations

For long-term fundamental investors, Dow presents a complex but potentially rewarding opportunity. The company offers exposure to essential materials markets with improving sustainability credentials, backed by substantial cash generation and shareholder returns. However, success requires navigating commodity cycles, managing legacy liabilities, and executing a transformation strategy in an increasingly complex global environment.

XI. Epilogue & Future Outlook

The Future of Materials Science and Chemical Industry

As we stand at the intersection of the digital and physical worlds, the chemical industry faces its most profound transformation since the polymer revolution of the 1950s. The convergence of artificial intelligence, biotechnology, and materials science is creating possibilities that Herbert Dow could never have imagined—self-healing materials, programmable plastics, chemicals that capture carbon as they cure.

For Dow Inc., this future presents both existential challenges and unprecedented opportunities. The company that once extracted bromine from brine now must extract value from data, sustainability from circularity, and growth from a planet with finite resources. The skills that built Dow—chemical engineering, process optimization, scale economics—remain necessary but no longer sufficient.

Dow's Positioning for Energy Transition and Sustainability

Dow's bet on the energy transition is bold but not without precedent. Just as the company pivoted from inorganic to organic chemistry in the 1920s, from commodities to specialties in the 1980s, it now pivots from linear to circular, from carbon-intensive to carbon-neutral. The Path2Zero project isn't just a plant—it's a statement of intent, a $6.5 billion wager that customers will pay premiums for sustainable materials.

The evidence suggests this bet may pay off. Major consumer brands have made public commitments to reduce Scope 3 emissions—the emissions from their supply chains. For these companies, Dow's low-carbon plastics aren't a nice-to-have but a must-have. Regulations in Europe and increasingly in North America are creating markets for recycled and bio-based materials that didn't exist five years ago.

But transformation is never smooth. The Fort Saskatchewan Path2Zero project has already faced delays, with construction pushed back due to market conditions. The tension between growth and decarbonization remains unresolved—can you really grow a petrochemical business while eliminating petroleum? Dow says yes, through electrification, hydrogen, and carbon capture. Skeptics point to the enormous energy requirements and uncertain economics of these technologies.

Key Questions: Can Dow Lead in Both Returns and Responsibility?

The fundamental question facing Dow—and indeed the entire chemical industry—is whether you can simultaneously deliver competitive returns to shareholders while meeting increasingly stringent environmental and social expectations. Can a company with Dow's history transcend its past? Can an industry built on fossil fuels lead the transition beyond them?

The early evidence is mixed but intriguing. Dow's stock has outperformed the broader market since the DowDuPont split, suggesting investors believe in the transformation story. The company's sustainability-linked bonds were oversubscribed, indicating capital markets are willing to fund the transition. Customer demand for sustainable materials is growing faster than overall chemical demand.

Yet challenges abound. Chinese competitors, unconstrained by Western ESG expectations, continue to gain market share. The economics of many sustainable technologies remain dependent on government subsidies. And Dow's own Scope 3 emissions—from the use of its products—dwarf its Scope 1 and 2 emissions, raising questions about whether true carbon neutrality is achievable for a plastics producer.

Final Reflections on 127 Years of Chemical Innovation

Looking back across Dow's 127-year history, certain patterns emerge with startling clarity. The company has consistently thrived when it embraced radical change—whether Herbert Dow's electrochemical innovations, Willard's Depression-era research investments, or the current sustainability transformation. It has struggled when it clung to the status quo, whether in the commodity chemical downturns or the reputational crises of the Vietnam era.

The company's greatest strength has always been its ability to see value where others see waste—bromine in brine, magnesium in seawater, energy in plastic waste. This alchemical vision, transforming the worthless into the essential, remains Dow's core competency. In an age where waste itself has become humanity's greatest challenge, this capability may be more valuable than ever.

But Dow's history also carries warnings. The company's technological optimism has sometimes blinded it to human costs—from workplace accidents in the early years to the ongoing controversies over chemical safety. The belief that chemistry can solve any problem has occasionally become the conviction that chemistry causes no problems, a dangerous delusion in an interconnected world.

As Dow enters its second century, it faces a world dramatically different from the one Herbert Dow knew, yet surprisingly similar in its challenges. Then as now, new technologies disrupted established industries. Then as now, global competition threatened American manufacturing. Then as now, society demanded that business serve broader purposes than profit alone.

The difference lies in scale and urgency. Climate change presents an existential challenge that dwarfs any previous crisis. The circular economy demands not just new products but new business models. Stakeholder capitalism requires balancing competing interests in ways that would have puzzled earlier generations of managers.

Can Dow navigate these challenges? History suggests it can—the company has reinvented itself repeatedly, survived seemingly fatal crises, and emerged stronger from each transformation. But history also warns that past performance doesn't guarantee future results. The very capabilities that enabled Dow's success—scale, integration, technological focus—may become liabilities in a world demanding agility, collaboration, and systems thinking.

Perhaps the most important lesson from Dow's history is that corporate longevity requires constant evolution. The Dow of 2050 will likely bear as little resemblance to today's Dow as today's bears to Herbert's original bromide business. The question isn't whether Dow will change but whether it will change fast enough, smart enough, and responsibly enough to remain relevant in a rapidly transforming world.

For investors, customers, employees, and communities, Dow represents both the promise and peril of industrial capitalism. It embodies humanity's ability to transform nature into prosperity, but also our capacity to damage what we depend upon. Its future success will depend not just on chemical innovation but on social innovation—finding ways to create value that enhances rather than degrades the systems that sustain us all.

The story of Dow is far from over. The next chapter is being written now, in laboratories working on carbon capture, in boardrooms debating sustainability strategies, in communities demanding environmental justice. Whether that chapter tells of transformation or decline, leadership or obsolescence, will depend on choices being made today. The one certainty is that the world will be watching, because in many ways, Dow's journey mirrors our own—from exploitation to sustainability, from isolation to integration, from mere survival to the possibility of thriving within planetary boundaries.

The chemical formula for success in the 21st century remains unwritten. But if history is any guide, it will be discovered not through defending the past but through imagining—and creating—a radically different future.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube