Supreme Industries: The 82-Year Journey from Modi to Taparia - Building India's Plastics Empire

I. Introduction & Episode Roadmap

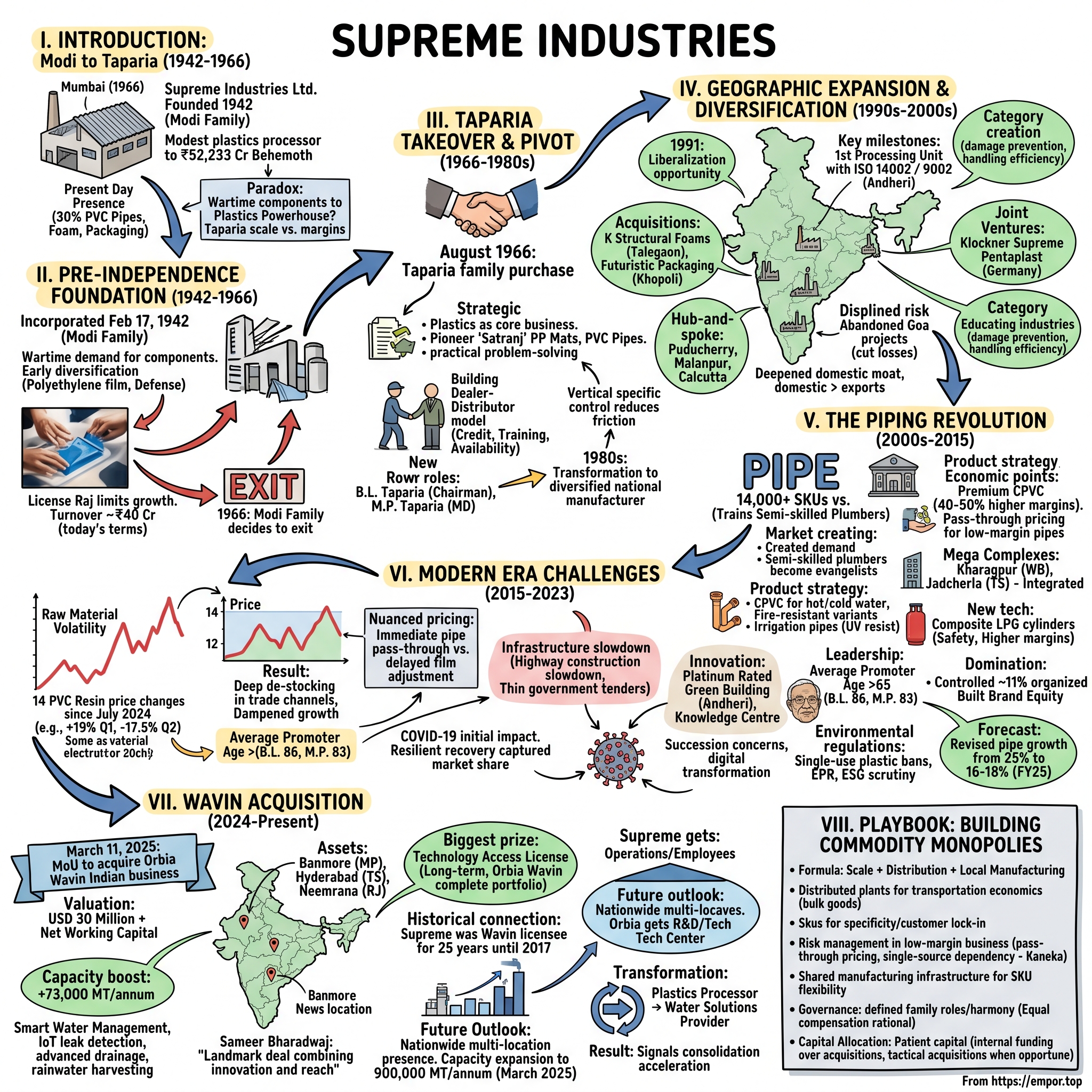

Picture this: A nondescript industrial compound in Mumbai's Andheri district, 1966. The monsoon rains hammer corrugated tin roofs while inside, workers mold plastic sheets on aging machinery. The Modi family, who'd built this business from scratch during World War II, are signing papers to hand over control to an ambitious Marwari family named Taparia. Neither party could have imagined that this modest plastics processor would become a ₹52,233 crore behemoth—India's undisputed emperor of engineered plastics.

Today, Supreme Industries commands a staggering presence across Indian households and infrastructure. Those PVC pipes snaking through your walls? There's a 30% chance they're Supreme's. The foam mattress in budget hotels, the industrial packaging protecting electronics, the composite LPG cylinders replacing rusty metal ones—Supreme touches Indian life in ways most never notice. With ₹10,419 crore in revenue and operations spanning 25+ plants nationwide, it's a classic "hiding in plain sight" monopoly.

The paradox at Supreme's heart fascinates: How does a company founded to supply defense components during British rule morph into a plastics powerhouse? Why did the original founders exit just as India's economy began opening up? And how did the Taparia family—relative unknowns in 1966—build competitive moats in what most consider a commodity business?

This is a story about timing markets across eight decades, the unglamorous path to market dominance, and why family businesses sometimes thrive precisely because they think in generations, not quarters. It's about building scale when others chase margins, going deep when competitors go broad, and why the most boring industries often create the most enduring wealth.

II. The Pre-Independence Foundation & Modi Era (1942-1966)

The year was 1942. British India teetered on the edge of chaos—Gandhi's Quit India movement had just launched, the Japanese army threatened from Burma, and wartime shortages plagued the subcontinent. In this tumultuous environment, a group of enterprising promoters led by the Modi family established Supreme Industries Limited in Mumbai's industrial heartland. While freedom fighters battled colonial rule in the streets, the Modis quietly built what would become one of India's most enduring industrial enterprises.

Incorporated on February 17, 1942 at Wadala, Mumbai, Supreme Industries Limited was promoted by the family of Kantilal K Modi. The timing seems almost deliberately contrarian—launching a manufacturing venture while the nation convulsed with independence fervor. Yet the Modis understood something fundamental: wars create demand for industrial components, and whoever controlled production capacity would thrive in the post-war reconstruction.

The company diversified early, manufacturing plastic moulded goods, cast polyethylene film, and defense components from two rented premises at Wadala and Naigaon in Mumbai. Picture these early facilities: corrugated tin sheds where workers molded plastics by hand, the acrid smell of polyethylene mixing with Mumbai's humid air. This wasn't glamorous work. The Modis weren't building the Tata Steel of their generation—they were making unglamorous components that others overlooked.

The post-independence years brought both opportunity and constraint. Nehru's License Raj meant every expansion required government approval, every import needed permits, and competition remained limited by design. For established players like Supreme, these restrictions became moats. By 1965-66, after 23 years of steady growth, the company's turnover reached ₹18.77 lakhs—equivalent to roughly ₹40 crores in today's terms.

Yet by 1966, the Modi family faced a crossroads. The first generation was aging, the second showed limited interest in plastics processing, and better opportunities beckoned in other industries. The family that would later build Modi Enterprises into sectors ranging from tobacco to entertainment decided Supreme's future lay elsewhere. They chose to exit entirely—a decision that would prove transformative for both seller and buyer.

What drove this exit? The Modis never publicly detailed their reasoning, but the timing suggests strategic calculation. India's economy was shifting, new industries beckoned, and perhaps they recognized that Supreme needed fresh vision to realize its potential. Sometimes the best entrepreneurial decision is knowing when to hand over the reins.

III. The Taparia Takeover & Strategic Pivot (1966-1980s)

August 1966. The monsoon has arrived early in Mumbai, and in a lawyer's office near Nariman Point, two families sit across a mahogany table. The Taparia family—Marwari businessmen with roots in Rajasthan—are taking over Supreme Industries from the Modi family through an outright purchase of shares. The amount isn't disclosed in public records, but for the Taparias, this represents a massive bet on India's industrial future.

Who were the Taparias? Unlike the established Modi clan, they were relative unknowns in Mumbai's business circles. B.L. Taparia would become Chairman while his brother M.P. Taparia assumed the role of Managing Director—a partnership that would drive Supreme for the next five decades. The brothers brought complementary skills: B.L. focused on strategic vision and capital allocation, while M.P. dove deep into operations and customer relationships.

Their first strategic decision proved prescient: defining plastic processing as the company's core business and pioneering the manufacture of 'Satranj' PP mats, PVC pipes, HMHDPE film and bags, and injection moulded plastic products. Why plastics in 1966 India? Consider the context: concrete and metal dominated construction, jute ruled packaging, and "plastic" still carried connotations of cheap Western imports. The Taparias saw what others missed—plastics offered durability at lower costs, lighter weights for transportation, and infinite moldability for diverse applications.

The 'Satranj' PP mats tell the story of their approach. Named after the chess-like pattern, these polypropylene floor coverings replaced traditional cotton durries in millions of Indian homes. They were washable, lasted years instead of months, and cost a fraction of woven alternatives. It wasn't glamorous innovation—it was practical problem-solving at scale.

In 1974, the company started manufacturing units at Andheri & Taloja, and during 1981-82, the Taloja unit began producing polyethylene foam. Each expansion followed a pattern: identify an imported product, reverse-engineer the manufacturing process, then produce it cheaper using local labor and distribution. The Andheri facility became their showpiece—visitors would see modern injection molding machines alongside workers hand-finishing products, a hybrid of automation and craftsmanship that defined Indian manufacturing in the License Raj era.

Building distribution in pre-liberalization India required particular ingenuity. Without modern logistics or communication networks, the Taparias created a dealer-distributor model that would become their biggest moat. They offered credit terms that smaller competitors couldn't match, conducted training programs for plumbers and contractors, and most importantly, guaranteed product availability even during raw material shortages.

The family structure—B.L. Taparia as Chairman, M.P. Taparia as Managing Director, with S.J. Taparia (nephew) and V.K. Taparia (B.L.'s son) joining later as Executive Directors—created clear hierarchies while maintaining family unity. Unlike many Indian business families that fractured over succession, the Taparias institutionalized roles early. Each family member controlled specific product verticals, reducing internal friction while maintaining central strategic control.

By the 1980s, Supreme had transformed from a small plastics molder into a diversified manufacturer with national ambitions. The foundation was set for geographic expansion that would define their next phase of growth.

IV. Geographic Expansion & Product Diversification (1990s-2000s)

July 1991. Finance Minister Manmohan Singh stands before Parliament announcing the end of the License Raj. For Supreme Industries, watching from their Mumbai headquarters, this moment represented both threat and opportunity. The protective walls that limited competition would crumble, but so would the constraints on expansion. The Taparias chose to see opportunity.

Their first major move in the liberalized economy was strategic acquisition. A K Structural Foams Ltd., the manufacturer of injection moulded products, at Talegaon near Pune in Maharashtra became Supreme's first significant purchase. Then came assets of M/s Futuristic Packaging Ltd., a company that specialised in manufacturing multilayer films at Khopoli (Maharashtra). These weren't glamorous deals—no investment bankers, no media coverage. Just the Taparias quietly buying distressed assets at attractive valuations and integrating them into their distribution network.

The pattern of these acquisitions reveals their strategy: buy manufacturing capacity in financial distress, inject working capital, leverage Supreme's distribution muscle, and watch revenues multiply. The Futuristic Packaging deal exemplified this—a company with good technology but poor market access suddenly gained reach to thousands of Supreme dealers nationwide.

Geographic expansion followed a hub-and-spoke model. Set up the Puducherry unit to manufacture industrial components, material handling, and consumer products, the unit at Malanpur (MP) for protective packaging products, and the Calcutta Unit to manufacture industrial moulded products and material handling crates. Each new facility served regional markets, reducing transportation costs while maintaining quality standards through centralized procurement and training.

The crown jewel of this period was becoming the first Plastics Processing Unit in the country to get an ISO 14002 / ISO 9002 certificate at their Andheri Unit. In an industry where quality perception mattered as much as actual quality, this certification became a powerful differentiator when bidding for institutional contracts.

Joint ventures marked Supreme's willingness to access technology while maintaining control. The partnership with Klockner Pentaplast GmbH of Germany created Klockner Supreme Pentaplast Ltd. at Malanpur—bringing European rigid film technology to India. When the Germans later wanted to exit, Supreme bought them out, rechristening it Supreme Vinyl Films Ltd. The technology stayed, the foreign partner left, and Supreme controlled another vertical.

Not every bet worked. Abandoned the project to manufacture foam polystyrene products in Goa, and later closed down the operations of Supreme Industries Limited (Goa) and divested the assets. The Taparias showed discipline in cutting losses—a rarity among promoter-driven Indian companies where ego often trumps economics.

The decision to focus on India rather than chase exports deserves examination. While competitors pursued global markets with thin margins, Supreme deepened its domestic moat. Handling volumes of over 6,40,000 tonnes of polymers annually effectively makes the country's largest plastics processors. By 2000, they operated from multiple facilities across Maharashtra, Madhya Pradesh, Tamil Nadu, West Bengal, Punjab, UP, and Rajasthan.

The masterstroke was creating product categories rather than just manufacturing products. When Supreme entered protective packaging, they didn't just make foam—they educated industries about transit damage prevention. When they launched industrial components, they taught factories about material handling efficiency. This consultative approach created switching costs beyond price.

By decade's end, Supreme had transformed from a regional player to a national force, setting the stage for their next act: dominating India's infrastructure boom through plastic piping systems.

V. The Piping Revolution & Market Leadership (2000s-2015)

The story of Supreme's dominance in plastic piping begins with a staggering number: 14,000+ SKUs across products like uPVC pipes, injection moulded PVC fittings, handmade fittings, HDPE pipe systems. To understand the audacity of this product proliferation, consider that most competitors offered perhaps 2,000 variants. Supreme didn't just enter the piping business—they carpet-bombed it with options.

The early 2000s coincided perfectly with India's infrastructure awakening. The Golden Quadrilateral highway project, urban expansion, and agricultural modernization all demanded piping solutions. But Supreme's masterstroke wasn't capturing this demand—it was creating demand where none existed. They established a one-of-a-kind 'Knowledge Centre' to train plumbing professionals, transforming semi-skilled workers into evangelists for modern piping systems.

Picture a typical training session at the Knowledge Centre: plumbers from small towns learning about pressure ratings, chemical resistance, installation techniques. Supreme didn't just teach them about products—they educated them about margins, customer objections, and upselling techniques. These plumbers returned to their markets as Supreme ambassadors, specifying Supreme products in every project.

The product strategy reflected deep market understanding. In irrigation-heavy states, they pushed agricultural pipes with special UV resistance. In chemical hubs like Gujarat, they emphasized CPVC's resistance to acids and bases. In metros undergoing real estate booms, they highlighted fire-resistant variants for high-rises. Lifeline C-PVC and CPVC fittings are designed for hot and cold water supply in residential, commercial and public projects, high and low rise buildings, corporate houses and academic institutes, solar heater applications, etc. CPVC pipes and CPVC pipe fittings are suitable for all uptakes and down take lines, terrace looping, and concealed pipe work applications.

The economics of the piping business revealed Supreme's genius. While competitors fought over price in commodity PVC pipes, Supreme created premium categories. Their CPVC pipes commanded 40-50% higher margins than standard PVC. The cross-laminated films business enjoyed even fatter margins. M.P. Taparia once explained their pricing philosophy: "Plastic piping, we pass on the price increase immediately. Because that is a low margin product, we immediately pass on. Similarly, on industrial products also we pass it on after one week's time and furniture, protective packaging and material handling we give a time lag between two to three weeks to transfer the increased cost including our operating margin. On Cross-Laminated Films, where we enjoy a strong margin, we do not change the price every time".

Building manufacturing moats required massive capital deployment. Supreme established two new multi-product mega complexes – the first one was at Kharagpur (West Bengal), spread across 59 Acres and another one was at Jadcherla (Telangana), spread across 50 acres. These weren't just factories—they were integrated complexes producing everything from raw material processing to finished goods, reducing dependency on external suppliers and capturing more value chain.

The 2014-15 period marked technological breakthroughs. First, Supreme secured exclusive global rights to produce and market cross laminated film products. Second, the company also began commercial production of composite cylinders in Halol, Gujarat. The composite LPG cylinders represented classic Supreme thinking—take a commodity product (metal cylinders), apply advanced materials technology, create a premium alternative with better safety features, and capture higher margins.

Market share data tells the story of dominance. By 2015, Supreme controlled approximately 11% of India's organized plastic pipes market—but the real moat was mindshare. Ask any plumber about quality pipes, Supreme featured in the top three. Ask contractors about reliable supply, Supreme topped the list. This brand equity, built over decades of consistent quality and availability, proved impossible for new entrants to replicate.

The infrastructure angle deserves special attention. Government-led initiatives such as the "Har Ghar Jal Yojna" and "Jal Jeevan Mission" are pivotal, aiming to provide tap water to rural households. This ambitious drive propels the demand for PVC pipes across the country. Additionally, rapid urbanization and extensive infrastructure projects demand reliable plumbing, sewage, and drainage systems, thus boosting the use of PVC pipes. Supreme positioned itself perfectly to capture this government-driven demand while maintaining pricing discipline in competitive tenders.

The piping revolution transformed Supreme from a diversified plastics company into India's piping powerhouse, setting up the next challenge: navigating modern complexities of raw material volatility and evolving competition.

Modern Era Challenges & Strategic Pivots (2015-2023)

If there's one image that captures Supreme Industries' modern era challenges, it's this: 14 PVC resin price changes since July 2024 alone. Imagine being M.P. Taparia, the octogenarian Managing Director, watching price alerts flash across his screen—up 19% in Q1, down 17.5% in Q2, each swing representing millions in inventory gains or losses. The price of PVC resin saw an increase of 19% between mid-April and the end of June, followed by a sharp decline of 17.5% between July 1st and August 16th.

The volatility story begins with a fundamental shift in global petrochemical markets. This rapid price fluctuation caused deep de-stocking in the trade channels, further dampening growth. When PVC prices rise, dealers stop buying, waiting for the inevitable correction. When prices fall, they dump inventory, crushing margins. Supreme found itself caught between protecting market share and preserving profitability—a balance that became increasingly precarious.

The company's response revealed operational sophistication. As M.P. Taparia explained their pricing philosophy during this turbulent period, different product categories received different treatment timelines. Piping products saw immediate price pass-through due to thin margins, while cross-laminated films with fatter margins absorbed some volatility. This nuanced approach protected relationships while maintaining overall profitability.

Infrastructure spending slowdowns compounded the raw material challenge. Government spending on infrastructure projects slowed down in the first half of the fiscal year, adding to the subdued market environment. The grand infrastructure projects that drove piping demand through the 2010s began drying up. Highway construction slowed, urban development projects stalled, and the once-reliable government tender pipeline thinned dramatically.

Competition evolved from predictable to existential. Organized players like Astral Poly and Prince Pipes expanded aggressively, while Chinese imports flooded lower-end segments. The unorganized sector—small regional manufacturers operating without quality certifications—captured price-sensitive rural markets. Supreme's premium positioning, once a strength, became a vulnerability as customers traded down during economic uncertainty.

COVID-19's arrival in March 2020 initially devastated operations. Plants shut, workers fled to villages, and demand evaporated overnight. Yet the recovery revealed Supreme's resilience. While competitors struggled with working capital, Supreme's strong balance sheet allowed them to restart quickly, capture market share from distressed players, and even accelerate capacity expansion when others retreated.

Innovation initiatives during this period reflected changing market dynamics. Supreme established a one-of-a-kind 'Knowledge Centre' to train plumbing professionals. The company also built Supreme Chambers, a Platinum Rated Green Building in Andheri. These weren't vanity projects—they represented strategic investments in market education and brand building when traditional growth levers weakened.

The succession question loomed largest. Mr B. L. Taparia (age 86 years), Non-executive Chairman, Mr M. P. Taparia (age 83 years, brother of Mr B. L. Taparia), Managing Director, Mr S. J. Taparia (age 75 years, nephew of Shri B. L. Taparia and Shri M. P. Taparia), Executive Director · Mr V. K. Taparia (age 65 years, son of Mr B. L. Taparia), Executive Director. The average promoter age above 65 created uncertainty about leadership transition. Unlike software companies where founders exit in their 40s, Supreme's octogenarian leadership raised questions about succession planning, strategic agility, and ability to navigate digital transformation.

Environmental regulations added another layer of complexity. Single-use plastic bans, EPR (Extended Producer Responsibility) requirements, and growing ESG scrutiny forced strategic pivots. Supreme invested in recycling capabilities, developed biodegradable alternatives, and emphasized the longevity of their products—but the fundamental challenge remained: plastics faced increasing societal pushback.

The company adapted its growth forecast accordingly. Supreme Industries Limited, a leading plastic products manufacturer, has revised its growth forecast for its Plastic Pipe Systems division from 25% to 16-18% for FY25. This dip is attributed to several challenges faced in the first half of the fiscal. This wasn't surrender—it was strategic recalibration, acknowledging new realities while positioning for the next growth phase.

By 2023, Supreme had weathered the worst but emerged changed. Margins compressed, growth slowed, and the easy wins of the infrastructure boom seemed distant memories. Yet the company's fundamental strengths—distribution reach, manufacturing scale, brand equity—remained intact, setting the stage for their boldest move yet.

VII. The Wavin Acquisition & Future Ambitions (2024-Present)

March 11, 2025. The announcement hit the wires before market opening: Supreme Industries Ltd has signed a Memorandum of Understanding (MoU) with Wavin Industries on March 10, 2025, for the acquisition of its Indian piping business. The transaction is valued at an aggregate consideration of USD 30 million, plus networking capital on the closing date. For a company that had grown organically for decades, this represented a strategic inflection point—Supreme's boldest acquisition in its 83-year history.

The Wavin deal wasn't just about buying assets. Supreme now owns and operates Orbia Wavin's manufacturing units in Banmore (Madhya Pradesh), Hyderabad (Telangana), and Neemrana (Rajasthan). With this acquisition, Supreme Industries aims to expand its presence in the plastic piping industry by increasing its production capacity by 73,000 metric tonnes per annum. This pushes total capacity toward the magical one million MT mark—a psychological barrier that separates industry leaders from also-rans.

But the real prize lay in technology access. As part of the broader agreement, Supreme also signed a long-term technology license with Orbia Wavin. This deal grants Supreme access to Orbia Wavin's complete portfolio of advanced water management solutions, along with fixed payments and royalty-based licensing terms. The partnership enables Supreme to harness Wavin's proven technologies and scale them across its vast distribution network throughout India and the SAARC region.

The technology portfolio reads like a wishlist for India's water infrastructure future: smart water management systems, IoT-enabled leak detection, advanced drainage solutions, rainwater harvesting technologies. Supreme Industries will have exclusive access to all existing technologies from Wavin BV – Netherlands, the parent Company on account of the acquisition. It will also gain access from us to all new technologies that we develop over the next seven years for India and SAARC countries.

M.P. Taparia's statement reveals the strategic thinking: "With this acquisition and agreement now complete, we are well-positioned to accelerate the next phase of growth for Supreme. Orbia Wavin's proven technologies and global expertise complement our strengths in manufacturing and market reach. Together, we will deliver reliable, sustainable and impactful water management solutions to meet the rising demands of India's infrastructure transformation".

The historical connection adds intrigue. Supreme was a Wavin licensee for 25 years until 2017 and we are deeply honored to renew our partnership and massively scale it through innovation to meet India's future needs. This wasn't a cold acquisition—it was rekindling an old relationship with dramatically different terms. Where Supreme once paid licensing fees as a junior partner, they now owned the Indian operations outright while securing exclusive regional technology rights.

Sameer Bharadwaj, CEO of Orbia, framed it from their perspective: "This is a landmark deal that begins a powerful collaboration to transform water management in India. By combining Orbia Wavin's innovation engine with Supreme's unmatched reach and footprint, we are creating a platform for long-term impact on India's water security and resilience". For Orbia, divesting physical assets while retaining technology licensing represented classic asset-light strategy—maintain innovation leadership while Supreme handles manufacturing and distribution complexity.

The deal structure reveals sophistication. As part of the deal, all India-based operations and employees of Orbia Wavin have officially transitioned to Supreme. This move ensures business continuity and service consistency for customers and stakeholders. Meanwhile, Orbia Wavin will continue operating its Technology & Innovation Center in India. Employees at the center will remain part of Orbia, focused on developing the next generation of high-performance water infrastructure technologies. Supreme gets the operations; Orbia keeps the R&D—both playing to their strengths.

The broader vision connects to India's infrastructure trajectory. Combining Orbia Wavin's technologies for water management and our manufacturing and distribution strengths, we are poised to secure India's water management needs with advanced solutions as India's economy is projected to more than double over the next decade. With government initiatives like Jal Jeevan Mission targeting piped water for every household by 2024, and smart cities demanding advanced water management, Supreme positioned itself at the intersection of policy push and technological capability.

With a nationwide presence of multi-location manufacturing as well and a capacity expansion to 900,000 metric tons per annum, by March 2025, Supreme is at the forefront of India's infrastructure growth, delivering innovative and reliable products to diverse sectors. The Wavin acquisition doesn't just add capacity—it adds capabilities that transform Supreme from a plastics processor to a water solutions provider.

The market implications extend beyond Supreme. This deal signals consolidation acceleration in India's fragmented piping industry. Smaller players lacking technology access or scale face existential questions. International technology providers must reconsider their India strategy—direct operations or licensing partnerships? Supreme's move forces everyone to recalibrate.

For the octogenarian Taparia brothers watching their creation evolve, this represents both culmination and transition—proving that even at 80-plus, they can execute transformative deals while potentially creating a platform robust enough to thrive beyond their tenure.

VIII. Playbook: Building Monopolies in Commodities

The Supreme Industries playbook reads like a masterclass in turning commodity manufacturing into a defensible moat. Start with an unglamorous product—plastic pipes, foam sheets, industrial crates. Products so boring that MBAs flee to software startups rather than sell PVC fittings. Yet Supreme built a ₹52,000+ crore market cap from these mundane materials. How?

Scale + Distribution + Local Manufacturing = The Supreme Formula

The formula seems simple, but execution complexity killed most competitors. Scale meant 25+ plants nationwide, not for prestige but for transportation economics. Plastic pipes are bulky and cheap—shipping them cross-country destroys margins. Supreme's distributed manufacturing meant they could serve Pune from Talegaon, Kolkata from Kharagpur, Chennai from nearby facilities. Competitors with centralized plants couldn't match delivered costs.

Distribution depth mattered more than breadth. While competitors boasted dealer counts, Supreme focused on dealer loyalty. Credit terms, training programs, exclusive territories, consistent supply during shortages—Supreme treated dealers as partners, not customers. A Supreme dealer in Nashik might stock 200 SKUs, knowing each would turn over predictably. This mutual dependency created switching costs that price competition couldn't overcome.

Local manufacturing went beyond geography. Each plant specialized in regional preferences—agricultural pipes for Punjab, industrial products for Gujarat's chemical belt, premium fittings for Mumbai's high-rises. The company is India's leading manufacturer of plastic piping solutions, offering 14,000+ SKUs across products like uPVC pipes, injection moulded PVC fittings, handmade fittings, HDPE pipe systems, etc for diverse applications in plumbing, water tanks, fire protection, drainage, and more. This SKU proliferation wasn't inefficiency—it was customer lock-in through specificity.

Managing Raw Material Volatility in a Low-Margin Business

PVC resin price volatility could destroy a quarter's profitability in days. Supreme's response involved multiple layers of risk management. First, the pricing discipline M.P. Taparia described—immediate pass-through for low-margin pipes, delayed adjustment for higher-margin products, stable pricing for premium categories. This segmented approach protected relationships while preserving margins.

Inventory management became algorithmic before algorithms were fashionable. Each product category had different inventory turns, price sensitivity, and demand patterns. Cross-laminated films might carry 60 days inventory given stable demand and high margins. PVC pipes turned every 15 days to minimize resin price exposure. This granular management required sophisticated IT systems when competitors still used paper ledgers.

Supplier relationships transcended transactional purchasing. Supreme Industries Ltd sources its CPVC requirements from a single company, Kaneka Corporation, Japan. M. P. Taparia: We are buying only from one company, Kaneka. Supreme Industries Ltd is dependent on a single supplier, Kaneka Corporation for the entire supply of CPVC resin, which in turn is the key raw material to manufacture plastic pipes that makeup 63% of sales of the company. This single-source dependency seems risky, but it guaranteed supply during shortages, technical support for new products, and first access to innovations.

Product Proliferation as a Moat

Those 14,000+ SKUs in piping alone represent a competitive weapon. A contractor working on a pharmaceutical plant needs specific chemical-resistant fittings in unusual dimensions. Supreme stocks them. A farmer in Maharashtra needs UV-resistant agricultural pipes in non-standard lengths. Supreme makes them. Each SKU might sell modestly, but collectively they create customer dependence.

The economics work because of shared infrastructure. The same injection molding machine producing standard elbows on Monday makes specialized chemical-resistant fittings on Tuesday. The same extrusion line running agricultural pipes switches to fire-sprinkler pipes with a die change. This manufacturing flexibility means Supreme can offer variety without proportional cost increase.

Quality consistency across this variety required process discipline. Every plant follows identical protocols, uses centrally-sourced raw materials, and submits to regular corporate audits. A contractor buying Supreme pipes in Assam gets the same quality as Mumbai. This predictability matters more than marginal price differences in professional markets.

The Taparia Model of Family Business Governance

Currently, four members of the Taparia family are present on the board of directors of the company. Mr B. L. Taparia (age 86 years), Non-executive Chairman, Mr M. P. Taparia (age 83 years, brother of Mr B. L. Taparia), Managing Director, Mr S. J. Taparia (age 75 years, nephew of Shri B. L. Taparia and Shri M. P. Taparia), Executive Director · Mr V. K. Taparia (age 65 years, son of Mr B. L. Taparia), Executive Director. This structure could spell disaster—family conflicts, unclear succession, competing power centers. Yet it worked for five decades.

The key: defined roles and mutual respect. B.L. Taparia handled strategy and capital allocation. M.P. Taparia managed operations and customer relationships. Next generation members ran specific divisions with P&L responsibility but within strategic parameters. Family meetings separated business from personal, with formal agendas and documented decisions.

Compensation philosophy reflected this discipline. remuneration is ₹26 crores in 2019, on profit before tax (PBT) of ₹664 crores. This is within the restrictions of the Companies Act. However, the remuneration drawn by the family is almost the same. Equal compensation regardless of role seems economically irrational but preserved family harmony—no one could claim unfair treatment.

Capital Allocation: Organic Growth vs. Acquisitions

Supreme's capital allocation history reveals strategic patience. For decades, they chose organic expansion over acquisitions. Each new plant, each capacity addition, each geographic expansion was internally funded and managed. This built organizational capability—Supreme people knew how to construct plants, ramp production, develop markets.

When acquisitions came, they were tactical and opportunistic. Distressed asset purchases like A K Structural Foams and Futuristic Packaging added capacity cheaply. Technology partnerships like Klockner brought capabilities Supreme couldn't develop internally. The Wavin acquisition combined both—distressed asset pricing with transformative technology access.

The balance sheet philosophy enabled this flexibility. Company is almost debt free. Low leverage meant Supreme could move quickly when opportunities arose, weather downturns without distress, and invest counter-cyclically when competitors retrenched.

Why Plastics Processing Creates Better Economics Than Most Realize

Plastics processing seems like a terrible business—commodity products, volatile raw materials, fragmented competition, low barriers to entry. Yet Supreme generated consistent returns on capital exceeding 20%. The secret lies in operational leverage and market position.

Once you achieve scale, incremental volume generates disproportionate profit. Fixed costs—plant depreciation, management overhead, distribution infrastructure—get spread across more units. Variable costs remain stable or even decline through purchasing power. A 10% volume increase might generate 20% profit growth.

Market position multiplies these advantages. As the largest player, Supreme gets first call on raw materials during shortages. Dealers prioritize Supreme products for prime shelf space. Contractors specify Supreme in tenders knowing availability is assured. These small advantages compound over time into insurmountable leads.

The playbook's brilliance lies not in any single element but in their reinforcement. Scale enables distribution depth which justifies local manufacturing which improves service which builds dealer loyalty which supports premium pricing which funds further scale. Competitors can copy tactics but not the decades of compound advantage—the true moat in commodity businesses.

IX. Bear vs. Bull Case Analysis

Bull Case: The Infrastructure Super-Cycle Thesis

Bulls see Supreme Industries as perfectly positioned for India's next decade of growth. Trading at 56.79 P/E and 9.64 P/B ratios, the valuation seems demanding until you consider the structural tailwinds. India needs $1.4 trillion in infrastructure investment through 2030. Every highway, metro line, airport, and smart city requires millions of meters of piping—and Supreme controls the market's premium segment.

The Wavin technology acquisition transforms the growth algorithm. Previously, Supreme competed on scale and distribution. Now they offer IoT-enabled smart water systems, advanced drainage solutions, and technologies even China lacks. Government contracts increasingly specify advanced capabilities that only Supreme can provide at scale. Imagine winning 40% of Jal Jeevan Mission contracts simply because competitors lack the technology to bid.

Promoter Holding: 48.9% signals skin in the game, but more importantly, it prevents hostile takeovers that might disrupt long-term strategy. The Taparia family thinks in decades, not quarters—rare in today's activist-driven markets. This patient capital enables investments in technology, capacity, and market development that public market pressure might otherwise prevent.

The capacity expansion to nearly 1 million MT positions Supreme for market share gains. As smaller players struggle with technology requirements, environmental compliance, and working capital needs, Supreme can acquire distressed assets cheaply or simply capture their market share. Industry consolidation typically benefits the largest player disproportionately—Supreme stands to capture 2-3% market share annually through competitive attrition alone.

Replacement demand provides a hidden growth driver. Pipes installed in the 1990s infrastructure boom need replacement. Metal pipes corrode, concrete pipes crack, but Supreme's installations from that era still function—building credibility for replacement contracts. This replacement cycle, worth potentially ₹50,000 crores over the next decade, favors established players with proven track records.

The balance sheet strength enables opportunistic moves. With minimal debt and strong cash generation, Supreme can fund organic expansion, pursue acquisitions, and weather downturns simultaneously. In a capital-intensive industry, financial flexibility becomes competitive advantage—Supreme can invest when others cannot.

Bear Case: Structural Headwinds and Succession Shadows

Bears point to multiple concerns that bulls conveniently ignore. Raw material volatility isn't getting better—it's getting worse. Climate change disrupts petrochemical supply chains, geopolitical tensions affect crude prices, and currency fluctuations amplify import costs. The price of PVC resin saw an increase of 19% between mid-April and the end of June, followed by a sharp decline of 17.5% between July 1st and August 16th. This rapid price fluctuation caused deep de-stocking in the trade channels, further dampening growth. These violent swings make business planning nearly impossible.

Competition from China represents an existential threat that protectionism can't permanently prevent. Chinese manufacturers operate at scales that dwarf Indian players, with government subsidies enabling predatory pricing. While anti-dumping duties provide temporary relief, WTO challenges and free trade agreements will eventually open floodgates. When Chinese pipes cost 30% less, even quality-conscious buyers reconsider.

The unorganized sector's resilience surprises many analysts. These small manufacturers operate without environmental clearances, quality certifications, or tax compliance—giving them 20-30% cost advantages. In price-sensitive rural markets, farmers choose these products over Supreme's premium offerings. As rural income growth slows, this down-trading accelerates.

Environmental regulations pose existential questions. Single-use plastic bans expand annually. European markets already restrict PVC in construction. Young consumers actively avoid plastic products. While Supreme invests in recycling and bio-plastics, the fundamental business model—converting petroleum into products that last centuries—faces societal opposition that technology can't fully address.

The succession planning concerns aren't just about age—they're about capability. Building Supreme required skills suited to License Raj India: government relations, manufacturing excellence, distribution management. Leading Supreme forward requires different capabilities: digital transformation, sustainability strategy, global competition. Can octogenarian leadership navigate these transitions? Can next-generation family members who've known only success handle adversity?

Margin pressure appears structural, not cyclical. Supreme Industries Limited, a leading plastic products manufacturer, has revised its growth forecast for its Plastic Pipe Systems division from 25% to 16-18% for FY25. This dip is attributed to several challenges faced in the first half of the fiscal. As competition intensifies and customers gain pricing power through transparency, margins face permanent compression. The 15-20% EBITDA margins of the past may prove unsustainable.

The Verdict: Priced for Perfection in an Imperfect World

At current valuations, Supreme needs everything to go right—continued infrastructure spending, successful technology integration, smooth succession, and competitive rationality. History suggests at least one assumption will prove wrong. The question becomes whether Supreme's fundamental strengths—distribution, scale, technology access—can overcome whichever challenge materializes.

The bull case requires belief in India's growth story and Supreme's ability to capture disproportionate value. The bear case simply requires recognition that commodity businesses face commodity economics, regardless of market position. With the stock trading at historically high multiples, the market clearly favors the bulls—but markets have been wrong before.

X. Epilogue & Investment Lessons

Standing in Supreme's Andheri headquarters, you might miss the lessons hidden in plain sight. The building itself—Supreme Chambers, a Platinum-rated green building—represents pragmatic excellence, not vanity. Like the company, it works better than it looks. This aesthetic philosophy—function over form, substance over style—permeates everything Supreme touches.

What Supreme Teaches About Building in "Boring" Industries

The first lesson: boring is beautiful when it's essential. Nobody dreams about PVC pipes, but everyone needs water. No entrepreneur pitches foam packaging to venture capitalists, but every electronics manufacturer requires it. Supreme understood that unsexy products with steady demand create better businesses than glamorous products with fickle customers.

The moat-building playbook differs in boring industries. Software companies build moats through network effects and switching costs. Consumer brands create moats through emotional attachment. Supreme built moats through physical presence—25 plants, thousands of dealers, millions of SKUs. This infrastructure moat proves harder to replicate than code or brand equity because it requires decades and massive capital.

Patience becomes competitive advantage in slow-moving industries. While tech companies measure progress in quarters, Supreme measures in decades. The Kharagpur complex took five years from land acquisition to full production. The dealer network required 30 years of relationship building. Competitors seeking quick returns abandon these markets, leaving them to patient capital.

The Power of Patient Capital and Multi-Decade Compounding

The Taparia family's 58-year ownership created compound advantages invisible in quarterly reports. Trust compounds—dealers stick with Supreme through cycles because the relationship spans generations. Knowledge compounds—workers become craftsmen, engineers become experts, salespeople become advisors. Scale compounds—each new plant makes the next one easier to justify, finance, and operate.

Consider the math: Supreme's revenues grew from ₹18.77 lakhs in 1965-66 to ₹10,419 crores in 2024—a 55,000x increase. But more impressive is consistency—positive profits for five consecutive decades, dividend payments through recessions, capacity expansion during downturns. This predictability attracts stakeholders who value stability over growth—suppliers, employees, customers who become partners in building the enterprise.

Patient capital enables contrarian moves. Supreme expanded capacity during the 2008 financial crisis when competitors retrenched. They invested in technology during COVID when others conserved cash. They acquired Wavin when plastics face environmental scrutiny. These contrarian bets work because patient capital can wait for cycles to turn.

Why Timing Matters Less Than Time in the Market

The Modis sold Supreme in 1966, just before India's industrial expansion. The Taparias bought at what seemed like the wrong time—License Raj constraints, limited demand, primitive infrastructure. Yet the "wrong" time proved right because they had time to build before competition intensified.

Every decade brought challenges that seemed existential. The 1970s oil crisis made petrochemicals unviable. 1991 liberalization brought foreign competition. The 2008 crisis crashed demand. COVID stopped production. Environmental concerns threaten the business model. Yet Supreme survived and thrived through all of it.

The lesson: In slow-changing industries, starting position matters less than staying power. Supreme wasn't first in plastics, best in technology, or cheapest in pricing. They simply stayed longer, invested more consistently, and accumulated advantages that time made insurmountable.

Final Reflections on Family Businesses and India's Growth Story

Supreme embodies the paradox of Indian family businesses—seemingly anachronistic yet surprisingly resilient. The Taparia family structure appears outdated: brothers as Chairman and MD, nephew and son as Executive Directors, decisions made over family dinners. Modern governance advocates would restructure immediately. Yet this structure generated superior returns for decades.

The strength lies in aligned incentives. The Taparias can't exit via stock options or golden parachutes. Their wealth remains tied to Supreme's success. Their reputation in Marwari business circles depends on Supreme's performance. Their children's inheritance depends on Supreme's sustainability. These interlocking incentives create focus that professional management might lack.

But succession remains the achilles heel. Supreme's octogenarian leadership navigated from License Raj to liberalization, from regional player to national champion. Can the next generation navigate from national champion to regional powerhouse? From manufacturing excellence to technology leadership? From family business to institution? These transitions prove harder than any market challenge.

India's growth story intertwines with Supreme's trajectory. As India urbanizes, Supreme provides urban infrastructure. As India industrializes, Supreme enables manufacturing. As India modernizes, Supreme supplies advanced solutions. This synchronization—company growth matching country growth—explains outperformance and suggests continued opportunity.

Yet questions remain. Can a plastics company thrive in an environmental age? Can family businesses compete with professional corporations? Can Indian manufacturing compete globally? Supreme's next chapter must answer these questions.

The investment lessons transcend Supreme:

- Boring businesses with essential products often beat exciting businesses with optional products

- Physical infrastructure moats prove more durable than technological moats

- Patient capital compounds advantages that impatient capital never sees

- Family ownership creates problems but also provides stability

- Timing market entry matters less than staying through cycles

- Scale advantages in commodity businesses create winner-take-most dynamics

- Technology can transform even traditional industries if applied strategically

For investors, Supreme represents a test case: Can an old-economy company navigate new-economy challenges? Can manufacturing businesses create software-like returns? Can family businesses professionalize without losing their essence?

The answers unfold daily in Supreme's plants, where workers mold plastic into products India needs. Whether those products generate returns investors want depends on factors beyond financial analysis—succession planning, environmental adaptation, competitive dynamics, and India's growth trajectory.

Supreme Industries' story continues, written in polymer and profit, shaped by family and market forces, building India's future from the most mundane materials. The next chapters remain unwritten, but the lessons from eight decades provide a foundation—sometimes boring builds best.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube