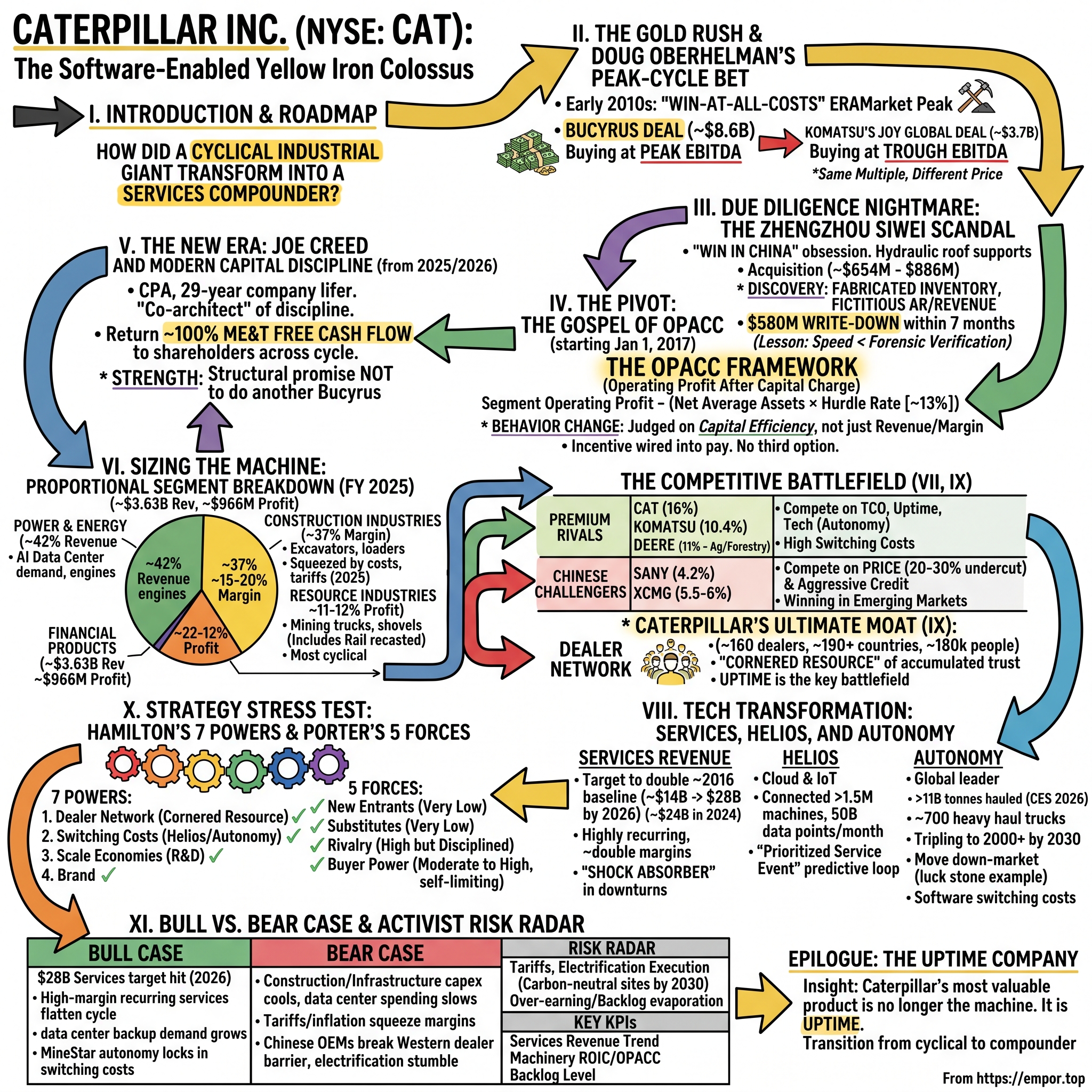

Caterpillar Inc. (NYSE: CAT): The Software-Enabled Yellow Iron Colossus

I. Introduction & Episode Roadmap

Somewhere on Earth right now, at this exact moment, a Caterpillar machine is moving. A D11 dozer is ripping through overburden in the Pilbara. A 797 haul truck the size of a two-story house is climbing out of a copper pit in Chile. A 3516 reciprocating engine, big enough to fill a shipping container, is spinning up to keep a hyperscale data center alive through a grid hiccup in northern Virginia. The yellow paint is so consistent across continents that it has become a kind of visual shorthand for civilization under construction. Where there is concrete being poured, coal being pulled out of the ground, or an AI cluster being stood up to train the next frontier model, there is almost always a piece of yellow iron with a black "CAT" stenciled on the side.

And yet the most interesting thing about Caterpillar in 2026 is not the iron. It is the question of what kind of company actually owns that iron's economics. Because the story we are going to tell is not really a story about machines. It is a story about a 100-year-old industrial giant that spent the early 2010s nearly destroying itself chasing volume at the top of a commodity cycle — and then, humbled and bruised, rebuilt its entire corporate operating system around a single unforgiving question: does this dollar of capital earn its keep?

Here is the central tension of this episode. How does a company famous for 400-ton steel dump trucks and diesel engines that you can hear from a mile away transform into something that looks, financially, more like a software-enabled services compounder? How does a business this cyclical, this capital-heavy, this exposed to the price of copper and the mood of the Federal Reserve, learn to throw off recurring, high-margin cash through the bottom of a cycle?

The arc runs through three CEOs and three completely different philosophies. First, the high-flying, aggressive, "win-at-all-costs" era of Doug Oberhelman in the early 2010s — an era defined by a top-of-the-cycle mega-acquisition and a due-diligence catastrophe in China that became a Harvard Business School cautionary tale. Then the quiet, almost monastic discipline of Jim Umpleby, the Solar Turbines engineer who took over on January 1, 2017, and rewrote the company's DNA around an internal economic-profit metric most outsiders have never heard of. And finally the modern era under Chairman and CEO Joe Creed — a CPA and 29-year company lifer who ascended to CEO in May 2025 and to the chairmanship in April 2026, and who was, quite literally, one of the co-architects of the discipline he now enforces.410

Our roadmap has six movements. The Cycle Trap — the mining super-cycle peak, the Bucyrus deal, and the Zhengzhou Siwei fraud. The Gospel of OPACC — how Caterpillar re-engineered its incentives around a brutal capital-charge metric. Proportionality & Economics — a segment-by-segment look at where the cash actually flows today, and the surprising answer (it is not where you think). The Moat — the legendary dealer network, the Helios cloud, and Caterpillar's lead in autonomous haulage. The Battlefield — the disciplined duel with 株式会社小松製作所 Komatsu Ltd. and the looming price war with Chinese OEMs. And finally The Stress Test — bull versus bear, the activist's case, and a hard look through Hamilton's 7 Powers and Porter's 5 Forces.

We will keep an independent posture throughout. Caterpillar's investor relations machine is excellent, and management tells a clean story. Our job is to separate what is proven from what is asserted, and to ask, at every turn, what evidence supports the claim and what would falsify it. Let us begin where the trouble started — at the very top of the mountain.

II. The Gold Rush & Doug Oberhelman's Peak-Cycle Bet

Picture the mood inside Caterpillar's Peoria headquarters around 2010 and 2011. China was pouring more concrete in three years than the United States poured in the entire twentieth century. Iron ore, copper, and coal prices were screaming upward. The great mining houses — BHP, Rio Tinto, Vale — were not just buying machines; they were ordering fleets, years in advance, and competing with each other for delivery slots. For a company that sells the picks and shovels of the global commodity rush, this was the closest thing to printing money that heavy industry ever sees.

Doug Oberhelman, who became CEO in 2010, read the moment the way most of corporate America read it: as a secular boom, not a cyclical peak. The directive that radiated out from the C-suite was unambiguous. Build more capacity. Grab more volume. Win. The fear that haunted Peoria was not that the cycle would turn — it was that Komatsu, the Japanese number two, would steal the mining crown while Caterpillar hesitated. In that climate, caution looked like cowardice.

So Caterpillar made the biggest acquisition in its history. In November 2010 it agreed to buy Bucyrus International — the storied Milwaukee maker of giant electric rope shovels, draglines, and underground mining gear — for roughly $8.6 billion in cash and assumed debt, paying $92.00 per share, a premium of about 32% over where Bucyrus had been trading.5 The strategic logic was genuinely seductive. Caterpillar was strong in surface mining trucks but thin in the enormous shovels that load them and in underground longwall systems. Bucyrus filled both holes at once. Overnight, Caterpillar could walk into any mine on Earth and offer the entire flow sheet — the truck, the shovel that fills it, the underground gear that feeds it — as a single yellow ecosystem. It was the ultimate one-stop-shop play, designed to leapfrog Komatsu in one decisive stroke.

Here is where the analysis gets uncomfortable. The deal was struck at roughly 12 times Bucyrus's peak 2010 EBITDA — and the operative word is peak. Caterpillar was buying a cyclical business at the top of its cycle and capitalizing those cycle-high earnings as if they were the new normal. That is the cardinal sin of industrial M&A, and the contrast with how the rival handled the same problem is the cleanest tuition-paid lesson in the whole story.

Consider what Komatsu did with the near-identical asset. In 2016 and 2017, after commodity prices had collapsed and stayed down, Komatsu bought Joy Global — Bucyrus's twin, the other great American mining-equipment house — for about $3.7 billion.7 Both deals were struck at a similar multiple of roughly 12 times EBITDA. But Komatsu was applying that multiple to depressed, bottom-of-the-cycle earnings. Because the denominator was trough EBITDA rather than peak EBITDA, Komatsu acquired a comparable competitive footprint for less than half the absolute dollars Caterpillar laid out. Same multiple, radically different price — because the two companies timed the cycle in opposite directions. Caterpillar bought the boom; Komatsu bought the bust.

The bust came on schedule. By 2013, commodity prices had rolled over, the mining houses slammed the brakes on capital spending, and the order book that had looked like a secular boom revealed itself as a cyclical spike. Caterpillar's Resource Industries segment — the mining business Bucyrus was supposed to crown — saw sales collapse by well over 60% from peak. What followed were years of factory consolidations, mass layoffs, idle capacity, and write-offs, as Caterpillar discovered the brutal operating leverage of a heavy-fixed-cost business running at half volume.

The deeper lesson for investors is not "Bucyrus was a bad company." Bucyrus made excellent machines, and much of that technology lives on inside Caterpillar's mining lineup today. The lesson is about when you deploy capital in a cyclical industry, and about the institutional psychology that makes good companies pay peak prices precisely when caution feels most dangerous. Oberhelman's Caterpillar was not reckless by the standards of 2011 — it was perfectly in tune with the consensus. That is exactly the problem. And the consensus was about to deliver a second, more humiliating blow, this time from an underground coal mine in central China.

III. The Due Diligence Nightmare: The Zhengzhou Siwei Scandal

If Bucyrus was a sin of timing, the next disaster was a sin of credulity — and it remains one of the most instructive due-diligence failures in modern corporate history.

The obsession driving it was "win in China." In 2011, Caterpillar looked at the Chinese underground coal market, saw enormous demand for hydraulic roof supports — the massive steel powered shields that hold up the roof over a working coal face so miners aren't crushed — and decided it needed a local champion fast. The target was a Hong Kong-listed shell called ERA Mining Machinery, whose crown jewel was a mainland manufacturer named Zhengzhou Siwei Mechanical & Electrical Manufacturing. Caterpillar agreed to acquire ERA for up to roughly $886 million, a deal that ultimately closed at around $654 million in June 2012.6[^9]

Seven months. That is how long it took for the whole thing to unravel. In January 2013, Caterpillar managers physically on the ground in China at Siwei's facilities discovered something that should have been impossible: the inventory simply was not there. Warehouses that the balance sheet said were stacked with roof supports and components were, in reality, largely empty. The gap between the paper and the physical world was not a rounding error — it was the company.6

What Caterpillar had bought, it turned out, was a multi-year, coordinated accounting fraud orchestrated by Siwei's local management. The playbook was textbook and comprehensive: fabricated purchase orders, physical inventory values that were systematically overstated, revenue recognized on products that were never built and never shipped, and accounts receivable conjured from transactions that did not exist.6[^9] This was not a single bad quarter that slipped through. It was a deliberate, sustained fabrication of the company's economic reality.

The financial reckoning came fast and brutal. In January 2013 Caterpillar announced a non-cash goodwill impairment charge of roughly $580 million — wiping out more than 80% of the acquisition's value in a single stroke, barely half a year after the ink dried.6 The stock took the hit, and shareholders sued, alleging the board and its tier-one legal and accounting advisers had waved through enormous red flags. The most damning of those flags, surfaced in the litigation and press coverage, was that Siwei had reportedly been begging for emergency cash infusions in the weeks just before the deal closed — the kind of liquidity desperation that should make any acquirer stop the presses and send forensic accountants to count the actual boxes in the actual warehouse.[^9]

Why does this matter beyond the embarrassment? Because it reveals something structural about the Oberhelman-era operating philosophy. When the organizing principle is speed and volume and winning the region before the competition does, due diligence becomes a box to check on the way to the prize rather than a genuine adversarial search for reasons to walk away. The two disasters share a single root cause: a culture that treated capital deployment as a race. Bucyrus was paying peak prices because slowing down felt like losing; Siwei was skipping forensic verification because slowing down felt like losing. Different failures, same disease.

Together, the mining write-downs and the China fraud sealed Oberhelman's fate. By the time he handed over the reins, Caterpillar had learned — at a cost measured in billions and in years of restructuring — that growth without capital discipline is not growth at all. It is the slow-motion destruction of shareholder value dressed up in the language of ambition. The man who would translate that hard lesson into a permanent operating system came not from the construction or mining side of the house, but from a quiet, profitable corner most outsiders had never heard of: gas turbines.

IV. The Pivot: Jim Umpleby and the Gospel of OPACC

On January 1, 2017, the CEO job passed to Jim Umpleby, and almost nobody outside Peoria saw it coming. Umpleby was not a charismatic empire-builder. He was a soft-spoken mechanical engineer who had spent decades at Solar Turbines — Caterpillar's San Diego–based gas turbine division inside the Energy & Transportation segment, a business known internally for steady margins, long customer relationships, and a relentless service attach rate. He was, in other words, the cultural opposite of the volume-at-all-costs mindset that had just blown two enormous holes in the balance sheet. That was precisely the point.

Umpleby's central act was to introduce what Caterpillar calls the Operating & Execution (O&E) Model, and it is impossible to understand modern Caterpillar without understanding the metric at its heart. For decades, divisions inside Caterpillar — like divisions inside most industrial conglomerates — were judged largely on operating margin and revenue growth. Grow the top line, hold the margin, get promoted. The problem with that scorecard is that it is blind to capital. A business can post a respectable 15% operating margin while quietly consuming enormous amounts of plant, inventory, and receivables to generate every dollar of that profit — and on a margin scorecard, nobody notices the capital being incinerated underneath.

So Umpleby changed the scorecard to OPACC — Operating Profit After Capital Charge. The concept is economic profit, and the formula is conceptually simple even if the internal accounting is not. You take a segment's Machinery, Energy & Transportation operating profit, and then you subtract a capital charge — calculated as the net average assets that business consumes, multiplied by a strict pre-tax hurdle rate that has historically sat around 13%. The capital charge is the rent the division pays for the balance sheet it ties up. If a business earns a fat margin but hoards capital, the charge eats the profit and its OPACC collapses toward zero or goes negative. If a business earns a thinner margin but barely touches the balance sheet — say, a parts-and-service operation — its OPACC can be enormous.

This single change in arithmetic rewired the company's behavior, because it forced every business unit through a brutal sieve into one of two buckets. Value Creators are the high-OPACC lines — the ones generating economic profit well above their capital charge. They get the R&D dollars, the growth capital, the management attention. Value Consumers are the low- or negative-OPACC lines, and for them the mandate is stark and unsentimental: fix it, restructure it, or exit it. There is no third option where a perpetually capital-hungry, low-return business gets to keep cruising along because it happens to post positive accounting profit. OPACC strips away that comfort.

The genius — and the part worth respecting analytically — is that Umpleby did not just preach the metric; he wired it into the pay. The executive Annual Incentive Plan was rebuilt so that bonuses keyed off enterprise operating profit, OPACC performance, and — critically — services revenue growth. Volume, the old religion, simply stopped paying. Capital efficiency started paying. When you change what makes people rich, you change what they do, and over the back half of the 2010s Caterpillar's behavior visibly shifted: tighter inventory, more disciplined factory footprints, a hard pivot toward the high-return services and power businesses, and a conspicuous absence of the kind of cycle-top mega-deals that had defined the prior era.

A skeptic should still ask the hard question: is OPACC a genuine governing discipline, or a piece of investor-relations theater that gets quietly overridden when a tempting deal comes along? The honest answer is that the proof is in the absence — the absence of another Bucyrus, the absence of another Siwei, the steady return of cash to shareholders instead of its redeployment into empire. For nearly a decade now, Caterpillar's capital allocation has behaved consistently with what OPACC would dictate. That consistency is itself the evidence. And the man who helped build the model, and who would inherit the job of defending it, was sitting in the CFO's chair of the very segment Umpleby came from.

V. The New Era: Joe Creed and Modern Capital Discipline

The succession was choreographed with the kind of deliberateness you would expect from a company that had learned its lessons the hard way. On May 1, 2025, Jim Umpleby moved up to Executive Chairman and Joseph E. (Joe) Creed became CEO and joined the board. Then, effective April 1, 2026, Creed added the chairman's title, consolidating both roles and completing the handoff.10 There was no drama, no outside-hire shock, no strategic U-turn — which, given Caterpillar's history, was precisely the message.

Creed is the embodiment of continuity, and his résumé reads like a deliberate refutation of the Oberhelman archetype. He is a 29-year Caterpillar lifer who joined the company in 1997, fresh out of Western Illinois University with an accounting degree.4 He is a CPA, and he climbed the entire financial ladder of the company: CFO of the Energy & Transportation segment, corporate vice president of Finance Services, corporate VP of the Oil & Gas business, then Group President of Energy & Transportation, and finally Chief Operating Officer before the top job.4 Read that path carefully and the significance jumps out: this is a man whose native language is capital allocation, return on invested capital, and the OPACC framework he helped operationalize alongside Umpleby. Where Oberhelman was a salesman and a builder, Creed is an accountant and an allocator. For a company whose near-death experience came from undisciplined capital deployment, putting a CPA who co-authored the discipline in the CEO chair is not an accident. It is the thesis.

The incentive structure reinforces the alignment. Creed's total 2025 compensation came in at roughly $17.01 million, of which the overwhelming majority — well over 85% — was tied to performance equity and non-equity incentive plans rather than guaranteed cash; his base salary was about $1.38 million, with the bulk arriving as stock awards and performance-based pay.9 The structural point matters more than the headline number: this is not a pay package that rewards simply showing up or growing revenue. It rewards the metrics that nearly killed the company when they were ignored.

Ownership tells the same story. Caterpillar's stock-ownership guideline requires the CEO to hold equity worth six times base salary — against a roughly $1.38 million base, that is an $8.28 million holding floor. Creed clears it with room to spare; his directly and beneficially held position of roughly 46,311 shares was worth somewhere in the range of $35 million to $42 million at early-2026 prices.4 When a CEO has eight figures of personal net worth riding on the same stock you own, the interests are, at least mechanically, aligned around long-term per-share value rather than short-term flash.

Which brings us to the capital allocation playbook that defines the modern company. Under Creed, Caterpillar has committed to returning substantially 100% of its Machinery, Energy & Transportation free cash flow to shareholders across the cycle, through dividends and buybacks.2 Read that commitment against the history we just walked through and its meaning is unmistakable: it is a structural promise not to do another Bucyrus. The cash that might once have funded a cycle-top acquisition spree is now contractually pointed back at owners. The era of risky, empire-building M&A is, by design and by incentive, over. Modern Caterpillar presents itself as a disciplined, cash-generating compounder.

But a promise to return free cash flow is only as good as the cash flow itself — and the most important question for an investor is not whether Caterpillar returns its cash, but where that cash now comes from. The answer has shifted dramatically, and it is not where the company's reputation would lead you to guess.

VI. Sizing the Machine: Proportional Segment Breakdown

Here is the single most counterintuitive fact about Caterpillar in 2026, and it reframes the entire investment case. The company whose brand is built on yellow earthmoving machines now makes more revenue — and considerably more profit — from power generation and engines than from the construction equipment that made it famous.

In fiscal 2025, Caterpillar reported total revenues of roughly $67.6 billion, up about 4% from $64.8 billion in 2024, with consolidated operating profit of about $11.2 billion.9 Strip out the financing arm and the company's industrial heart breaks into three machinery segments, and their relative weights are the story.

Power & Energy — the segment formerly badged Energy & Transportation — is now the crown jewel. At roughly $28.6 billion in revenue, it is the largest segment by sales at about 42% of machinery revenue, and because it carries the highest margins in the portfolio, north of 22%, it punches even harder on profit, contributing something on the order of half of the company's operating value.9 This is the part of Caterpillar that most casual observers don't even know exists. It is the reciprocating diesel and gas engines, the Solar Turbines gas turbines, the generator sets — the equipment that keeps the lights on. And right now its single hottest demand driver is the most important capital-expenditure story on the planet: generative AI. Hyperscale data centers training and serving large models need vast, reliable backup and prime power, and that means arrays of large reciprocating gensets standing by for the moment the grid stutters. On top of that sits the traditional book of oil-and-gas compression engines, marine propulsion, and industrial power. The analytical takeaway is important and double-edged: Caterpillar has, almost by accident of its turbine and engine heritage, become a direct beneficiary of the AI infrastructure boom — which is wonderful while hyperscaler capex is climbing, and a concentration risk if that capex ever rolls over.

Construction Industries — the traditional core, the literal yellow iron — came in at about $25.06 billion, roughly 37% of machinery revenue.9 This is the excavators, backhoes, skid-steer loaders, compactors, and asphalt pavers that build roads, subdivisions, and commercial sites. It is a steady, enormous cash generator, but it is also the most exposed to the ordinary business cycle and to input costs. In 2025 the strain showed: even as construction sales held up, segment profit margins compressed hard — Caterpillar disclosed that Construction Industries profit margin fell from about 19.6% to 14.9%, squeezed by higher manufacturing costs, tariffs, and unfavorable price realization.9 That single data point is a window into the whole 2025 margin story, which we will come back to.

Resource Industries — the mining segment, the direct descendant of that fateful Bucyrus deal, now including Rail after an early-2026 segment recast — was the smallest of the three at roughly $14.66 billion, about 22% of machinery revenue, but it punched below its weight on profit, contributing only around 11–12% of operating value at margins that slid toward 10% in 2025.9 This is the big mining haul trucks, the electric rope shovels and draglines, the hydraulic mining excavators — sold to the BHPs and Rio Tintos and Vales of the world, whose capital budgets swing with commodity prices. It is the most cyclical part of the company and, in 2025, the most pressured, hit by manufacturing inflation and shifting global tariffs.

Sitting alongside the three machinery segments is Financial Products, or Cat Financial, which generated about $3.63 billion in revenue and roughly $966 million in segment profit.9 Cat Financial provides retail financing and leases to the customers buying the machines, plus wholesale financing to the dealers. Run with conservative underwriting, it is not a flashy business, but it is a powerful one: it lubricates machine sales, deepens the customer relationship, and throws off close to a billion dollars of steady income. Crucially, it is also a low-capital-intensity profit relative to building factories — exactly the kind of return profile OPACC rewards.

So what should an investor take from this map? Two things. First, the "cyclical mining giant" mental model of Caterpillar is roughly a decade out of date; the company's profit center has migrated to power and energy, and its fortunes are now tied as much to data-center buildouts and engine demand as to the price of copper. Second, the margin compression of 2025 — consolidated operating margin falling from 20.2% in 2024 to 16.5% in 2025 — was real and concentrated in the construction and mining segments, driven by tariffs and manufacturing-cost inflation rather than collapsing demand.9 That distinction matters enormously for the bull-bear debate, and we will return to it. But the deepest source of Caterpillar's durability isn't in any single segment. It is in the distribution system that wraps around all of them.

VII. The Competitive Battlefield: Premium Rivals vs. Chinese Challenger Incursions

Imagine a copper mine 4,000 meters up in the Andes, where a single haul truck sitting idle costs the operator something on the order of $100,000 an hour in lost production. Now imagine the part that truck needs is a four-day flight and a mountain road away. That scenario — not the sticker price of the truck — is the battlefield on which the heavy-equipment war is actually fought. Understanding that reframes the entire competitive landscape.

The global heavy-equipment market is roughly $150–170 billion in annual revenue, and Caterpillar is the undisputed number one with about 16% share — a remarkable position for a fragmented, global, capital-intensive industry.8 But the field below it is getting more crowded and more interesting.

The premium challenger, the worthy rival, is 株式会社小松製作所 Komatsu Ltd. — the global number two at roughly 10.4% share, with annual revenue around $28.5 billion and a construction-and-mining segment of about $24.9 billion.8 Komatsu is the company we already met as the disciplined cycle-timer that bought Joy Global at the bottom. It is deeply engineering-led, commands premium pricing, and earns excellent residual values on its used machines. Crucially, Komatsu pioneered Autonomous Haulage Systems and its "Smart Construction" digital offering, which means the technology frontier is genuinely contested rather than a Caterpillar walkover. The two premium players compete the way disciplined oligopolists do — not on slashing upfront price, but on total cost of ownership, durability, uptime, and technology. That restraint is itself a feature of the industry's economics and a meaningful part of why both companies earn good returns.

Then there are the Chinese value challengers, and this is where the long-term tension lives. 三一重工 Sany Heavy Industry is the global number six at about 4.2% share, with revenue around $10.88 billion.8 What makes Sany dangerous is not its domestic Chinese business, which has been hammered by the country's property slump, but its pivot. Facing a brutal home market, Sany has thrown itself at exports — reporting that international sales reached about $6.78 billion, roughly 64% of its revenue, in its 2024 results.[^11] And it builds those machines in heavily automated "Lighthouse" factories that let it hit aggressive price points on increasingly high-spec equipment. Alongside it, 徐工集团 XCMG Group sits at global number four, with roughly 5.5–6% share and approximately $12 billion in revenue.8

The threat vector from Sany and XCMG is specific and worth stating precisely. They are not, today, taking premium contracts from Caterpillar at a Pilbara iron-ore mine. They are winning in the emerging markets — Latin America, Africa, Southeast Asia — by undercutting the premium players by 20–30% on upfront price and pairing that with aggressive credit terms. In price-sensitive markets where a mine or contractor cannot stomach the premium and downtime is less catastrophically expensive, that combination is genuinely competitive. The open question, the one that should keep a Caterpillar bull honest, is whether the Chinese OEMs can ever replicate the one thing they currently lack: a dense, trusted, local service network in Caterpillar's core Western strongholds. So far they cannot. But "so far" is doing a lot of work in that sentence.

Rounding out the field are the non-premium and adjacent competitors. Deere & Company is the global number three at roughly 11% share, though its dominance is concentrated in North American agriculture and forestry rather than head-to-head with Caterpillar's core earthmoving.8 Volvo Construction Equipment, with around $10 billion in revenue, is strong in European wheel loaders and articulated haulers.

Which brings us back to the mine on the mountain. The reason Caterpillar wins the ground war is not that its machines are categorically better than Komatsu's — they are roughly peers — and it is certainly not that they are cheaper than Sany's. Caterpillar wins because when a machine breaks on a remote job site at 2 a.m., a Cat dealer's parts and a Cat dealer's technician arrive in hours, not days, almost anywhere on Earth. That is not a product advantage. It is a distribution advantage, and it is the deepest moat in the entire business. It deserves its own chapter.

VIII. The Tech Transformation: Services, Helios, and Autonomy

For most of its history, Caterpillar's business had a simple, painful rhythm: when the economy boomed, customers bought machines and profits soared; when the economy cooled, customers stopped buying and profits cratered. The entire stock was a bet on the cycle. The most important — and least appreciated — change of the last decade is that Caterpillar has been deliberately building a second business on top of the machines, one that keeps earning money even when nobody is buying new iron. That business is services, and it is the financial spine of the modern investment case.

The target was laid out publicly back at the 2019 investor day and reaffirmed since: roughly double Machinery, Energy & Transportation services revenue from a 2016 baseline of about $14 billion to $28 billion by 2026.212 And the progress has been real and verifiable, not aspirational. Services revenue reached about $22 billion in 2023 and roughly $24 billion in 2024, which means services now account for something like 39% of machinery revenue, up from around 25% in 2016.12 The 2026 target is, on the company's own reporting, within reach.

Why does this matter so much? Because of the economics and the timing. Services — parts, maintenance, rebuilds, repair, digital subscriptions — are highly recurring and carry operating margins roughly double those of basic equipment manufacturing. And here is the magic against the cycle: in a downturn, a construction firm will absolutely delay buying a new $400,000 excavator. But it will not stop running the excavators it already owns — those machines still need filters, hydraulic seals, undercarriage parts, and scheduled rebuilds, or they stop making money. So as new-machine sales fall in a recession, the installed base keeps demanding service. Services act as a shock absorber, buffering cash flow through exactly the troughs that used to gut Caterpillar's earnings. If this engine performs as designed, it structurally lowers the cyclicality of the whole company — and that, more than any single product, is the reason a heavy-equipment maker can credibly call itself a compounder.

The technological backbone making this possible is Helios, Caterpillar's proprietary cloud and IoT platform. Helios connects over 1.5 million active machines and engines worldwide — including, notably, some non-Caterpillar equipment — and processes more than 50 billion data points a month.13 Think of it as a continuous medical telemetry feed for a global fleet of iron. It watches fluid levels, vibration signatures that betray bearing wear, fuel burn, and load cycles, and it converts that raw telemetry into something genuinely valuable: a "Prioritized Service Event," which is essentially the system telling a local dealer that a specific hydraulic seal on a specific excavator working a specific site in Peru is likely to fail within, say, the next 50 operating hours — before it strands the machine. That predictive loop is what turns a one-time machine sale into a decades-long service annuity, and it is why Caterpillar's digital parts commerce has scaled to more than $15 million in daily digital transactions.13

The most spectacular expression of the technology, though, is autonomy. Caterpillar is the undisputed global leader in heavy-vehicle autonomous haulage, and the scale is staggering. At CES 2026 the company disclosed that its autonomous fleets had safely hauled over 11 billion tonnes of material globally to date — up from about 8.62 billion tonnes in late 2024, implying a run-rate around 2 billion tonnes a year.11 That is being done by roughly 700 fully autonomous heavy haul trucks operating across three continents, with a stated strategic ambition to roughly triple the fleet toward 2,000-plus trucks by 2030.11 These are not golf carts; they are 200- and 300-ton trucks running 24 hours a day with no driver in the cab, coordinated by Cat MineStar Command for hauling.

What's strategically newer is the move down-market — from giant remote mines to ordinary aggregate quarries. The lighthouse example is the partnership with Luck Stone at its Bull Run quarry in Virginia, where autonomous Cat 777 trucks have hauled over 2 million tons of material — proof that the technology can leave the rarefied world of mega-mining and work in the thousands of localized quarries that dot every developed economy.3 And here is the moat lock-in that makes autonomy so strategically potent: once a mine or quarry has woven its entire digital architecture — scheduling, haul routes, safety systems, fleet management — into Caterpillar's MineStar software, the cost and operational risk of ripping it out for a competitor's system becomes almost prohibitive. The machines become switchable; the operating system does not. That is how a hardware company quietly acquires software-like switching costs. Whether those switching costs are as durable as management implies is a fair question — but the direction of travel is unmistakable, and it is what we will test next.

IX. The Strategy Stress Test: Hamilton's 7 Powers & Porter's 5 Forces

Strip away the narrative and ask the structural question: why does Caterpillar earn the returns it earns, and how durable is that advantage really? Two frameworks — Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces — let us pressure-test the moat rather than simply admire it.

Start with the single most important Power, and the one competitors find genuinely impossible to copy: the Cornered Resource of the Cat dealer network. Caterpillar sells almost entirely through roughly 160 independently owned dealers operating in 190-plus countries, employing close to 180,000 people — a dealer workforce larger than Caterpillar's own corporate base of around 115,000.1 These are not company stores. They are independent, often multi-generational family businesses, many more than 50 years old, with decades-deep local relationships with mining operators, contractors, and governments. The reason this is a cornered resource rather than just a big sales channel is that it cannot be bought or rebuilt at any price on a relevant timescale. A Chinese OEM with all the capital in the world cannot conjure a profitable, trusted, 50-year-old dealer in rural Peru or outback Australia next quarter. The network is the accumulated trust of a century, and trust does not have a spot price. This is the deepest reason Caterpillar's premium pricing survives the assault from cheaper rivals.

The second Power is Switching Costs, and we just watched it being manufactured. Embedding a customer's fleet into Helios telemetry and, especially, into MineStar autonomous command wires Caterpillar into the customer's daily operations — maintenance scheduling, parts replenishment, even the ERP and safety systems of an autonomous mine. The more of a customer's operation runs on Caterpillar's software, the more painful it becomes to leave. These switching costs are high and, critically, growing as autonomy and connectivity penetrate the installed base — a Power that barely existed a decade ago and is now compounding.

The third Power is Scale Economies, most visibly in R&D. Caterpillar spends on the order of $2 billion a year on research and development — electrification, alternative fuels, autonomy, digital — and because it spreads that spend across the largest installed base and manufacturing footprint in the industry, its per-unit R&D burden is lower than Komatsu's, Sany's, or Volvo's.1 Scale lets the leader out-invest the field while charging customers less per machine for the privilege, which is the self-reinforcing logic that keeps leaders in the lead. (The 7 Powers framework also nods to Caterpillar's Brand — that yellow paint genuinely commands a price premium — but Brand here is downstream of the dealer network and reliability, so we treat it as reinforcing rather than primary.)

Now Porter's Forces, which test the same durability from the industry-structure angle. Threat of new entrants is very low: the capital intensity is brutal, emissions regulation is a moat in itself, and — as we have hammered — you cannot enter seriously without a global distribution network that takes generations to build. Threat of substitutes is very low: there is simply no near-term substitute for a 400-ton mining truck or a multi-megawatt backup genset; you cannot replace high-horsepower earthmoving with human labor or lightweight battery tools. Rivalry is high but disciplined: the premium tier competes ferociously on technology and uptime but shows real pricing restraint, while the value tier competes on price but lacks Western dealer support — a segmented standoff rather than a margin-destroying free-for-all.

The most interesting force is buyer power, which is moderate to high but self-limiting. The mega-miners — BHP, Rio Tinto, Vale — order in such volume that they have genuine leverage on price. But that leverage runs straight into the wall of downtime economics. Saving 5% on the purchase price of an excavator is meaningless if a single breakdown costs $100,000 an hour in lost production, and that arithmetic shoves even the most powerful buyers back toward the premium supplier with the parts on the shelf and the technician in the truck. The buyers have the power; the physics of their own operations stop them from fully using it. That is as elegant a moat as exists in heavy industry — and it is exactly the dynamic a skeptic must argue against to make the bear case.

X. The Activist Risk Radar & Bull vs. Bear Case

So let's make the bear case properly, because a moat this celebrated deserves a genuine adversary rather than a strawman. Put on the hat of a skeptical long-short investor and ask the uncomfortable questions.

Is Caterpillar over-earning? The single most important number in the bear's brief is the margin slide: consolidated operating margin fell from 20.2% in 2024 to 16.5% in 2025, a 370-basis-point drop driven by tariff drag and manufacturing-cost inflation.9 The bull says this is a transitory, externally-imposed cost shock — tariffs and inflation, not demand collapse. The bear says it exposes how much of the 2024 peak margin was cycle-high and how fragile pricing power really is when input costs move against the company. Both can point to the same data; the disagreement is about what 16.5% represents — a temporary dip or a reversion toward a more normal mid-cycle reality. Layered on top is the backlog question. Caterpillar has been carrying a record backlog in the range of $51–63 billion, which the bull reads as visibility and the bear reads as a number that could evaporate quickly if global infrastructure and data-center capex cool, since backlog is orders, not signed-in-blood revenue.

Is the buyback strategy actually smart? Caterpillar returned billions through buybacks in 2024 and 2025 — years when the stock traded near record highs.29 The activist critique writes itself: buying back stock at peak valuations is the mirror image of buying Bucyrus at peak EBITDA, and that capital might be better spent out-investing Komatsu in battery-electric and zero-emission mining machines before the rival establishes a lead in the technology that mining customers say they will demand. The counter is that the 100%-of-free-cash-flow return commitment is precisely the discipline that prevents another empire-building blunder — but a fair observer notes the tension: a promise of capital discipline and a critique of buyback timing are not so easily reconciled.

Can the Chinese OEMs break in? Sany and XCMG are improving quality fast. If they ever build credible dealer-and-service networks in North America and Western Europe, Caterpillar's premium pricing — the thing the entire return profile rests on — faces structural erosion rather than the contained, emerging-markets pressure it sees today. That is the long-tail risk that, if it materializes, attacks the moat at its foundation.

The current risk radar beyond those holds two material items. First, tariffs and input costs are not a one-off; ongoing trade disputes represent a multi-hundred-million-dollar headwind that management has repeatedly flagged, and they bite hardest in the construction and mining segments. Second, electrification execution risk: mining customers want carbon-neutral sites by 2030, which requires multi-megawatt battery packs or hydrogen fuel cells in machines that work brutal duty cycles. This demands enormous capex, and if Caterpillar's zero-emission machines suffer reliability problems or lag on performance, the company risks surrendering exactly the premium positioning the dealer network has spent a century building. Reliability is the brand; a stumble in electric reliability is a stumble in the brand.

Net it out into a clean bull versus bear. The bear case: construction and infrastructure capex cools, hyperscaler spending on backup data-center power slows, tariffs grind margins toward the low-double-digits and stay there, and Chinese value OEMs finally crack the Western dealer barrier. In that world the record backlog shrinks and the "compounder" reverts to being a high-quality cyclical. The bull case: the $28 billion services target is hit in 2026 and keeps compounding, high-margin recurring services genuinely flatten the cycle, data-center backup-power demand keeps climbing, and MineStar autonomy spreads into hundreds of aggregate quarries, locking in switching costs the value players cannot match. In that world Caterpillar earns a re-rating as a structurally less cyclical business than its history suggests.

For investors who want to cut through the noise, three KPIs carry most of the signal. First, the services revenue trend — the single cleanest read on whether the de-cyclicalization thesis is real; watch the quarterly march toward and beyond $28 billion. Second, machinery ROIC / OPACC versus the ~13% hurdle — the direct test of whether capital discipline is being maintained or quietly abandoned. Third, backlog level and pricing realization — specifically whether the $51–63 billion backlog holds and whether price increases are offsetting the tariff drag that gutted 2025 margins. Those three, tracked over time, will tell you which case is winning long before the headlines do.

XI. Epilogue & Outro

Step back from the iron and the segment tables, and the Caterpillar story resolves into one of the cleanest case studies in corporate self-correction that American industry has to offer. This is a company that walked right into the classic growth trap — paying a peak-cycle price for Bucyrus, skipping forensic diligence on a fraudulent Chinese acquisition, mistaking a commodity spike for a secular boom — and then, instead of papering over the wreckage, rebuilt its entire operating system around the brutal arithmetic of economic profit. The OPACC discipline, the services pivot, the dealer network turned into a software moat: none of it was inevitable, and all of it was a deliberate response to nearly destroying shareholder value at the top of the last cycle.

The surprising insight, the one that reframes how to think about the whole enterprise, is this: Caterpillar's most valuable product is no longer the machine. It is uptime. The yellow iron is the razor; the parts, the service, the Helios telemetry, and the MineStar autonomy are the blades — recurring, high-margin, and increasingly sticky. A company that the market once priced as a pure bet on global GDP and the copper price has spent a decade trying to become something more durable: a seller of operational certainty to the people who keep the physical world running.

Whether it fully succeeds is genuinely unresolved. The margin compression of 2025 is a real warning that pricing power has limits and that tariffs and input costs can still bite hard. The Chinese challengers are improving, the electrification transition is expensive and unforgiving, and a record backlog is only as good as the cycle that stands behind it. But the direction is unmistakable, the discipline is now wired into the incentives, and the dealer network remains the kind of advantage that money simply cannot buy in any reasonable timeframe. The next chapter — written by a CPA who helped author the discipline he now enforces — will be a test of whether operational uptime can finally tame a century-old cycle. That is the story worth watching.

References

-

Caterpillar 2022 Investor Day Strategy Presentation — Caterpillar Inc. ↩↩↩

-

Caterpillar and Luck Stone Reach Milestone in Autonomous Quarrying — Caterpillar Inc. ↩

-

Caterpillar Executive Leadership Profile: Joseph E. Creed — Caterpillar Inc. ↩↩↩↩

-

Caterpillar to Buy Mining Equipment Maker Bucyrus for $8.6 Billion — Reuters, 2010-11-15 ↩

-

Caterpillar Suffers $580 Million Write-down Due to Chinese Unit Fraud — Bloomberg, 2013-01-18 ↩↩↩↩

-

Komatsu to Acquire Joy Global for $3.7 Billion in Mining Play — Reuters, 2016-07-21 ↩

-

Yellow Table 2025: Global Construction Equipment Rankings — International Construction, 2025-05-15 ↩↩↩↩↩

-

Caterpillar Reports Fourth-Quarter and Full-Year 2025 Results — Caterpillar Inc. / PR Newswire, 2026 ↩↩↩↩↩↩↩↩↩↩

-

Caterpillar Chief Executive Officer Joe Creed Elected Chairman of the Board — Caterpillar Inc., 2026 ↩↩

-

Scaling a Proven Autonomy System to Support New Industries — Caterpillar Inc., 2026 ↩↩

-

Caterpillar Aims for $28 Billion in Services Revenue Using Digital Technologies — Digital Commerce 360, 2025-07-18 ↩↩

-

Caterpillar Unveils AI-Powered Future and Invests in the Workforce Building It — Caterpillar Inc., 2026 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube