KEI Industries: From Partnership Firm to Power Cable Giant

I. Introduction & Episode Roadmap

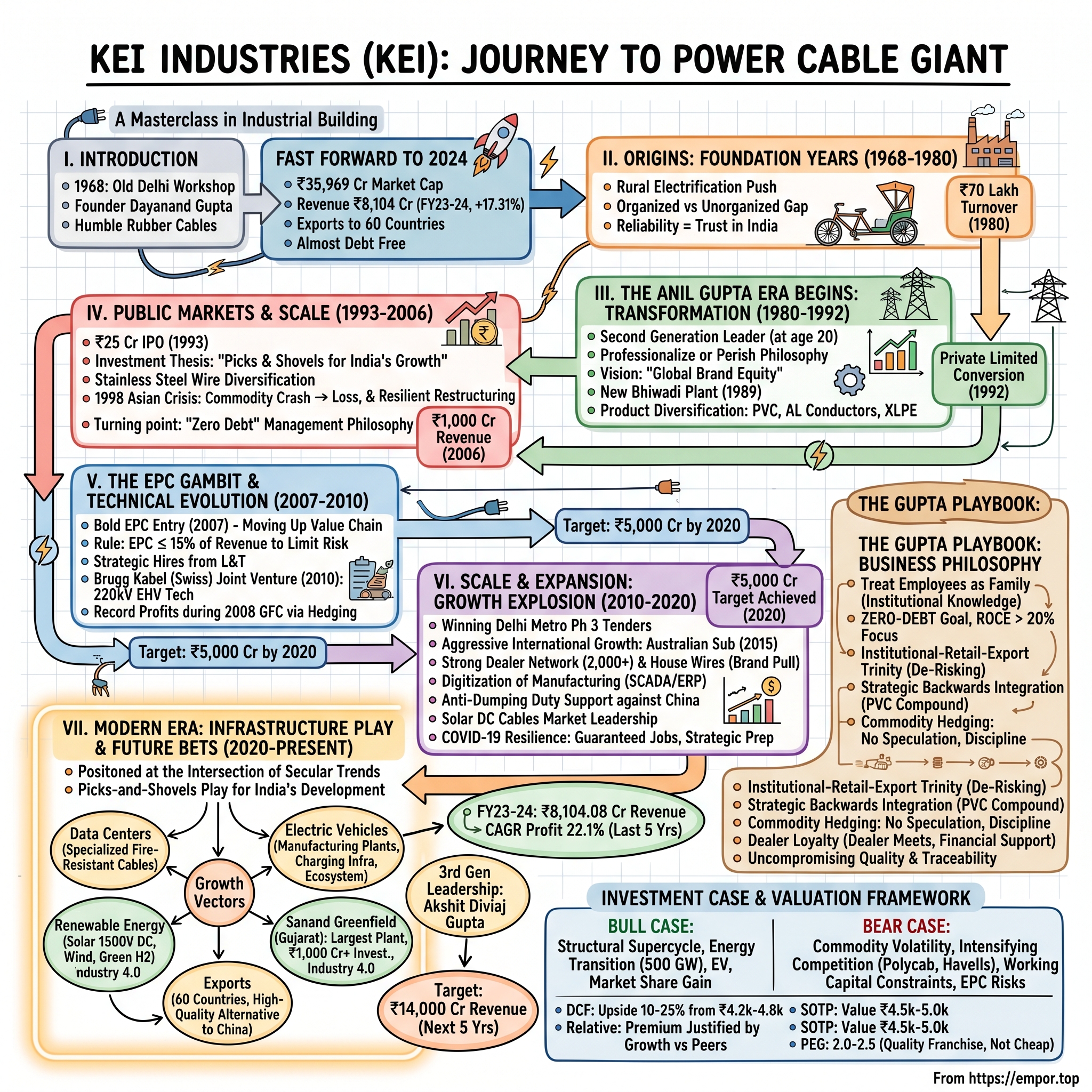

Picture this: It's 1968 in Old Delhi's Bara Hindu Rao area. The narrow lanes are filled with the cacophony of cycle rickshaws, street vendors hawking their wares, and the occasional Ambassador car honking its way through the crowd. In a modest workshop, a man named Dayanand Gupta is melting rubber, twisting copper wires, and dreaming of electrifying India—one cable at a time. He calls his venture Krishna Electrical Industries, a partnership firm with barely 100 employees and ambitions that seem almost quaint by today's standards.

Fast forward to 2024. That small workshop has morphed into KEI Industries Limited—a ₹35,969 crore market cap behemoth manufacturing cables for 60 countries, from the scorching deserts of the Middle East to the frozen landscapes of Russia. The company's cables power Delhi Metro's sprawling network, light up India's smart cities, and increasingly, charge the electric vehicles zipping through Bangalore's tech corridors. The staggering transformation story is best captured in numbers: ₹35,969 crore market cap today, revenue of ₹8104.08 crore in FY 2023-24, growing at 17.31%, and almost debt free. But these metrics only hint at the deeper narrative—how a family business navigated India's License Raj, survived the 1990s liberalization shock, and emerged as a critical infrastructure player in Asia's third-largest economy.

This is not just another manufacturing success story. It's a masterclass in patient capital deployment, crisis management, and the art of building industrial capabilities in an emerging market. It's about reading India's infrastructure cycles, making counter-intuitive bets during downturns, and understanding that in the cable business, your real customers aren't just buying copper and plastic—they're buying reliability for mission-critical applications where failure isn't an option.

What makes KEI particularly fascinating for investors is its positioning at the intersection of multiple secular trends: India's massive infrastructure buildout, the energy transition, rapid urbanization, and the electric vehicle revolution. The company has quietly become the picks-and-shovels play for India's development story—whether it's metros, airports, data centers, or solar farms being built, they all need KEI's cables.

Over the next several hours, we'll unpack how the Gupta family built this empire, the strategic pivots that defined each era, the near-death experiences that shaped management philosophy, and most importantly, what the next decade might hold. We'll explore why Warren Buffett might appreciate this business (hint: it's about competitive moats and rational capital allocation), why Peter Lynch would find it interesting (the growth-at-reasonable-price characteristics), and what Charlie Munger would say about its corporate culture.

Buckle up. This is the KEI Industries story—where rubber meets the road, or rather, where copper meets PVC, and transforms into the nervous system of a rapidly modernizing nation.

II. Origins: The Foundation Years (1968-1980)

The year was 1968. India Gandhi had just become Prime Minister for the second time. The country was still finding its economic footing, two decades after independence. Industrial licenses were gold dust, foreign exchange was scarcer than rain in the Thar Desert, and the phrase "self-reliance" wasn't just policy—it was survival.

In this environment, Dayanand Gupta saw an opportunity that others missed. Post-independence India was embarking on its rural electrification dreams. Villages that had known only kerosene lamps for centuries were about to experience their first electric bulb. But there was a problem: who would make the cables to carry this electricity?

The multinational players were focused on high-value industrial applications. The unorganized sector made products of questionable quality. Dayanand positioned Krishna Electrical Industries right in the middle—better than the local players, more accessible than the multinationals.

Starting with rubber-insulated cables for house wiring seems almost primitive by today's standards. The manufacturing process was labor-intensive: workers would manually wind copper conductors, apply rubber insulation through a crude extrusion process, and vulcanize the cables in steam chambers. Quality control meant visual inspection and basic electrical testing. The entire operation could fit in a space smaller than a modern McDonald's outlet.

But Dayanand understood something fundamental about the Indian market that many missed. In a country where a tube light going off could mean a child couldn't study for exams, where a fan stopping in May's heat was a family crisis, reliability mattered more than sophistication. His rubber cables might not have been pretty, but they worked. And in 1970s India, working was enough.

The Bara Hindu Rao facility in Old Delhi tells you everything about the era's constraints and ingenuity. Located in the heart of the old city, getting raw materials in meant navigating narrow gullies on cycle rickshaws. Getting finished products out required similar logistics gymnastics. The 120 employees weren't just workers; they were craftsmen who understood that each cable they made would light up someone's home.

By 1980, the company had achieved ₹70 lakh in turnover—roughly $875,000 at the exchange rates of that time. In Silicon Valley terms, this would barely qualify as a lifestyle business. But in License Raj India, where getting an industrial license could take years and importing machinery required navigating byzantine regulations, this represented solid, sustainable growth.

The broader context is crucial here. India's per capita electricity consumption in 1980 was just 172 kWh—compare that to 2,500 kWh in developed countries. The electrical cable market was fragmented beyond belief: hundreds of small players making substandard products, a handful of large players focused on industrial applications, and massive unmet demand in between. The organized sector controlled less than 40% of the market.

What Dayanand had built wasn't just a cable company. He had created a foundation for something bigger—a platform that understood Indian market realities, had relationships with suppliers who actually delivered, and most importantly, had begun building a reputation for reliability in a market where trust was the scarcest commodity.

The stage was set for transformation. But first, tragedy would strike, and from that tragedy would emerge a leader who would reimagine what Krishna Electrical Industries could become. The year 1980 wouldn't just mark the end of a decade—it would mark the beginning of the Anil Gupta era.

III. The Anil Gupta Era Begins: Transformation (1980-1992)

Twenty-year-old Anil Gupta wasn't supposed to be running a cable company. Fresh out of Dr. Zakir Hussain College with his M.Com degree, he had the academic credentials for a comfortable corporate job. His friends were joining the Tatas and Birlas of the world. But when his father Dayanand passed away suddenly in 1980, Anil faced a choice that would define not just his life, but the trajectory of what would become a multi-billion-dollar enterprise.

"I had been visiting the factory since I was 15," Anil would later recall in interviews. "My father would take me along during school holidays. While my friends were playing cricket, I was learning how to test cable insulation and calculate copper requirements." This early exposure would prove invaluable, but nothing quite prepares a 20-year-old for inheriting a business with 120 employees looking to him for leadership.

The India that Anil inherited the business in was fundamentally different from his father's era. Indira Gandhi's socialist policies were reaching their zenith. The Sixth Five Year Plan (1980-85) had ambitious targets for power generation—adding 20,000 MW of capacity. But between government targets and ground reality lay a chasm, and in that chasm lay opportunity.

Anil's first insight was deceptively simple: professionalize or perish. The partnership firm structure that had served his father well was inadequate for the ambitions Anil harbored. He began hiring professionally qualified engineers—a radical move in an industry dominated by family members and trusted lieutenants. These engineers brought something critical: the ability to reverse-engineer and improve upon existing products.

By 1985, the company had crossed ₹2 crore in revenue. But more importantly, Anil had begun articulating a vision that seemed audacious for a small Delhi-based firm: "To become a leading name in business and create brand equity, not only in India but internationally." His senior managers thought he was dreaming. The international cable market was dominated by giants like Pirelli, Nexans, and Prysmian. What chance did a company from Bara Hindu Rao have?

The transformation strategy had three pillars. First, expand the product portfolio beyond basic rubber cables. By 1987, KEI was manufacturing PVC insulated cables, aluminum conductors, and had begun experimenting with XLPE (cross-linked polyethylene) insulation—technology that was just beginning to gain acceptance in India.

Second, move beyond Old Delhi. The Bara Hindu Rao facility had maxed out its potential. Anil identified Bhiwadi in Rajasthan—close enough to Delhi for logistics, but with space to build a modern manufacturing facility. The first Bhiwadi plant, commissioned in 1989, was a statement of intent: 10 acres of land, automated extrusion lines, and testing facilities that rivaled anything in the country.

Third, and most crucially, build a brand. In an industry where buying decisions were made by electrical contractors based on margins, Anil insisted on quality that commanded a premium. "KEI" began appearing on cables, marketing materials started emphasizing technical specifications, and slowly, architects and consultants began specifying KEI cables in their projects.

The decision to convert from a partnership to a private limited company in 1992 wasn't just legal restructuring—it was philosophical transformation. Anil was preparing for something bigger. He had been watching the winds of change. The Soviet Union had collapsed, P.V. Narasimha Rao had become Prime Minister, and whispers of economic liberalization were growing louder.

The 1992 conversion also brought in professional governance. Board meetings replaced family discussions. Annual reports replaced informal accounting. Strategic planning replaced intuitive decision-making. For employees who had worked under Dayanand, this was culture shock. But Anil persisted, knowing that the company's next phase would require institutional credibility.

By the end of 1992, KEI had 350 employees, two manufacturing facilities, and revenue approaching ₹10 crore. The product range had expanded from basic rubber cables to include power cables up to 1.1 kV, control cables, and instrumentation cables. More importantly, the company had begun supplying to institutional clients—Delhi Vidyut Board, Northern Railways, and several public sector undertakings.

But Anil knew this was just the beginning. The real test would come with going public—exposing the company to market scrutiny, shareholder expectations, and the brutal discipline of quarterly results. As 1992 drew to a close, the documentation for the IPO was being prepared. The boy who had inherited a small cable company at 20 was about to bet everything on India's liberalization story.

The transformation from Krishna Electrical Industries to KEI Industries Limited was complete. But the transformation from a family business to an industrial powerhouse had just begun.

IV. Public Markets & Manufacturing Scale (1993-2006)

The timing was either perfect or terrible, depending on your perspective. As KEI's IPO documents were being finalized in early 1993, Anil Gupta received news that would have broken a lesser man: his father Dayanand, who had been suffering from illness, passed away. The patriarch who had started it all was gone, just as the company was about to take its biggest leap.

The Bombay Stock Exchange in 1993 was a different beast. The Harshad Mehta scam had just shaken investor confidence. New issues were viewed with suspicion. And here was KEI—a cable company from Delhi, in an unglamorous sector, asking investors to trust a 33-year-old CEO. The IPO was priced at ₹10 per share, valuing the company at roughly ₹25 crore.

The roadshows were grueling. Fund managers in Mumbai's Nariman Point offices would ask pointed questions: "Why cables? Why not get into IT services like everyone else?" Anil's answer was consistent: "India will need 10x the power infrastructure over the next two decades. Every megawatt of power generation needs kilometers of cables. We're selling the picks and shovels for India's infrastructure gold rush."

The IPO was subscribed 1.2 times—not spectacular, but enough. KEI Industries Limited was now a public company, with all the scrutiny and expectations that entailed. The first annual general meeting as a public company was telling. Shareholders ranged from retired government employees who had invested ₹5,000 to institutional investors managing crores. Anil promised them all one thing: consistent growth with capital discipline.

The mid-1990s brought an unexpected opportunity. The telecom revolution was beginning, and the new cellular towers needed specialized cables. But more interesting was what was happening in India's industrial landscape. The Bajaj family was restructuring, spinning off their steel division. KEI saw an opportunity and in 1994, entered into stainless steel wire manufacturing—a seemingly unrelated diversification that would prove prescient.

The Bhiwadi plant expansion of 1994-1996 was KEI's first major capacity bet as a public company. The investment: ₹25 crore. The target: manufacturing capabilities for cables up to 11 kV. The risk: the power sector was still dominated by state electricity boards, notorious for delayed payments. But Anil had noticed something others hadn't—private industrial consumers were growing rapidly, and they paid on time.

Then came 1998, and with it, a crisis that would test every assumption. The Asian Financial Crisis had crashed commodity prices. Copper fell 40% in six months. KEI was sitting on high-cost inventory as prices plummeted. The company reported its first loss as a public entity. Stock price crashed from ₹45 to ₹12. Financial newspapers wrote obituaries: "KEI's Diversification Disaster."

But inside the Bhiwadi facility, a different story was unfolding. Instead of panicking, Anil used the crisis to restructure. Unprofitable product lines were shut down. The sales team was reorganized around customer segments rather than geography. Most importantly, a new risk management framework was implemented—never again would the company be caught with excessive commodity exposure.

The turnaround was swift. By 2000, KEI was back in the black. But more importantly, the company had learned vital lessons about commodity cycles, working capital management, and the importance of diversification within core competence. The stainless steel wire business, which analysts had mocked, provided stability when cable demand softened.

The 2001 decision to set up a facility in Silvassa was strategic genius disguised as geographic expansion. Silvassa, a Union Territory, offered tax benefits. But more importantly, it was close to Mumbai—India's commercial capital and largest consumer of cables. The facility was designed for flexible manufacturing, able to switch between different cable types based on demand.

By 2002, KEI had quietly become one of India's top 5 cable manufacturers. Revenue crossed ₹500 crore. But Anil wasn't satisfied. International competitors were entering India with superior technology. Chinese manufacturers were dumping cheap cables. The company needed a technological moat.

The answer came in 2006 with the triple extrusion process for XLPE cables. This technology, licensed from a European company at significant cost, allowed simultaneous extrusion of conductor screen, insulation, and insulation screen. Only three other companies in India had this capability. KEI could now manufacture cables up to 33 kV with quality matching international standards.

The period from 1993 to 2006 had seen KEI transform from a ₹10 crore company to a ₹1,000 crore enterprise. The employee count had grown from 350 to 2,000. Manufacturing facilities had expanded from one to three. But most importantly, KEI had survived and thrived through the Asian Financial Crisis, the dot-com bust, and multiple commodity cycles.

As 2006 drew to a close, India's infrastructure boom was about to begin in earnest. The government was talking about $500 billion in infrastructure investment. Power generation capacity additions were being planned at unprecedented scale. And KEI, battle-tested and technologically ready, was perfectly positioned to capture this opportunity.

But first, Anil had one more strategic card to play—entering the EPC business, a move that would transform KEI from a product company to a solutions provider. The stakes had never been higher.

V. The EPC Gambit & Technical Evolution (2007-2010)

The conference room at KEI's Okhla headquarters was tense. It was late 2006, and Anil Gupta had just proposed what seemed like corporate suicide to his board. "We're going to become an EPC company," he announced. The directors, mostly industry veterans, were incredulous. Engineering, Procurement, and Construction was a different beast altogether—fixed-price contracts, execution risks, and working capital requirements that could sink a company.

"Look at L&T's struggles with EPC margins," one director argued. "Why enter a business where even the giants bleed?" But Anil had done his homework. He'd noticed that 40% of cable procurement decisions were being influenced by EPC contractors. KEI was making excellent products but losing orders because contractors preferred suppliers who could provide complete solutions. It was time to move up the value chain.

The first EPC project was a disaster waiting to happen. A 33 kV substation for a steel plant in Chhattisgarh, contract value ₹15 crore. KEI had never done civil construction, never managed third-party equipment procurement, never dealt with the maze of clearances required for commissioning. Six months into the project, they were behind schedule and over budget.

That's when Anil made a crucial decision. Instead of trying to build all capabilities in-house, he hired a core team from L&T's transmission division. The salary bill shocked shareholders—these engineers commanded packages that were 3x KEI's average. But they brought something invaluable: knowledge of how to execute.

By mid-2007, the Chhattisgarh project was back on track. More importantly, KEI had learned the EPC playbook: strict project management protocols, milestone-based billing, and most crucially, the discipline to walk away from bad contracts. The company established a rule: EPC would never exceed 15% of total revenue. This wasn't about becoming L&T; it was about protecting the cable business.

Then came the Brugg Kabel moment. In 2009, Anil was visiting the Hannover Industrial Fair when he stopped at a small Swiss company's booth. Brugg Kabel had developed technology for extra-high voltage cables up to 400 kV, but lacked presence in Asia. KEI had market access but lacked EHV technology. Over Swiss coffee and Indian chai in Hannover, the contours of a joint venture emerged.

The Brugg partnership, finalized in 2010, was transformative. For a technology transfer fee and ongoing royalties, KEI gained access to Swiss precision engineering. The first product: 220 kV XLPE cables, which only two other companies in India could manufacture. The market opportunity was massive—India's transmission network was being upgraded from 132 kV to 220 kV and 400 kV to reduce transmission losses.

Setting up EHV manufacturing wasn't just about buying machines. The Chopanki facility in Rajasthan, commissioned in 2010, looked more like a pharmaceutical plant than a cable factory. Clean rooms for jointing, nitrogen-filled curing chambers, and testing facilities that could simulate lightning strikes. The investment: ₹200 crore, the largest in KEI's history.

The first 220 kV cable order came from Power Grid Corporation. The testing requirements were brutal: the cable had to withstand 318 kV for 30 minutes, undergo 1,000 heat cycles, and maintain properties after accelerated aging tests. When KEI's cable passed all tests on the first attempt, even the Brugg engineers were surprised. Indian manufacturing had come of age.

But 2008 had brought the Global Financial Crisis, and with it, a familiar challenge. Commodity prices crashed again—copper fell from $8,000 to $3,000 per ton. But this time, KEI was prepared. The commodity hedging framework developed after the 1998 crisis kicked in. The company actually reported record profits in 2009, while competitors struggled with inventory losses. The milestone of crossing ₹1,000 crore in revenue in 2010 wasn't celebrated with champagne. Anil Gupta marked it by announcing the next target: ₹5,000 crore by 2020. The number seemed impossible—it implied 17% CAGR for a decade in a cyclical, commodity-dependent business. But KEI now had something it lacked before: capability across the entire value chain.

The EPC business, despite early struggles, had become a strategic weapon. When Delhi Metro needed cables laid through congested urban areas with minimal disruption, KEI could offer not just cables but complete installation and commissioning. When private developers needed substations for IT parks, KEI provided turnkey solutions. The discipline of limiting EPC to 15% of revenue meant it enhanced margins without adding undue risk.

As 2010 drew to a close, KEI Industries stood transformed. From rubber cables in Old Delhi to EHV cables tested in Swiss laboratories. From a partnership firm to a company with institutional processes. From ₹70 lakh to ₹1,000 crore. But the real transformation was in capability—KEI could now compete with anyone, anywhere, on technology and execution.

The next decade would test these capabilities like never before. India's infrastructure boom was about to begin in earnest, and KEI was ready to wire the nation's growth story.

VI. Scale & Expansion: The Growth Explosion (2010-2020)

The PowerPoint slide that Anil Gupta presented to his board in January 2011 had just three numbers: ₹2,000 crore by 2012, ₹3,000 crore by 2015, ₹5,000 crore by 2020. The board members exchanged glances. The company had just crossed ₹1,000 crore after four decades. Now Anil was proposing to add the next ₹1,000 crore in two years, and then accelerate from there.

"The India growth story isn't a forecast anymore," Anil argued. "It's happening. Metro systems in every major city. Power generation capacity doubling. Industrial corridors being built. Smart cities being planned. Every one of these needs kilometers of cables. The question isn't whether demand will come—it's whether we'll be ready to supply it."

The first test came sooner than expected. In 2011, Delhi Metro Phase 3 tenders were floated—300 kilometers of metro lines, hundreds of kilometers of cables needed. But there was a catch: the specifications required cables that could withstand Delhi's extreme temperatures (2°C to 48°C), moisture from monsoons, and vibrations from trains running every 3 minutes. Only companies with proven track records would be considered.

KEI's bid was aggressive but calculated. The 2012 milestone wasn't just a number—it was validation. When results were announced in March 2012, KEI had won 40% of the cable contracts for Delhi Metro Phase 3. Revenue for FY 2011-12: ₹2,147 crore. Anil's ambitious target had been exceeded.

But growth at this pace brought its own challenges. Working capital requirements exploded. The company needed ₹400 crore just to fund receivables and inventory. Traditional funding sources—banks—were willing but expensive. That's when KEI made a clever move: supplier credit programs with copper suppliers, backed by international banks at LIBOR plus 100 basis points. The cost of capital dropped by 400 basis points overnight.

The international expansion started almost by accident. In 2013, an Australian distributor visited KEI's Chopanki plant. Australia's mining boom had created massive demand for specialized cables that could withstand harsh outback conditions. Chinese suppliers were cheap but unreliable. European suppliers were reliable but expensive. KEI offered a middle path.

The first Australian order was small—A$2 million for mining cables. But KEI over-delivered, providing technical support that European suppliers charged extra for. By 2014, Australian orders had grown to A$20 million. In 2015, KEI incorporated KEI Cables Australia Pty Ltd, its first international subsidiary. The timing was perfect—Australia's infrastructure spending was accelerating, and "Made in India" was gaining credibility.

Back home, the retail strategy was yielding unexpected dividends. While competitors focused on large institutional orders, KEI had quietly built a network of 2,000 dealers and distributors. House wires—the simplest product in KEI's portfolio—were generating 20% EBITDA margins because of brand pull. Electricians preferred KEI because the company ran training programs, teaching them about new wiring standards and safety protocols.

The ₹3,000 crore milestone came in FY 2014-15, a year ahead of schedule. But Anil wasn't celebrating. He had noticed something concerning: Chinese cable manufacturers were entering India aggressively, offering prices 20% below Indian manufacturers. The government's anti-dumping duties provided temporary relief, but Anil knew protectionism wasn't a long-term strategy.

The answer was technology and scale. In 2016, KEI announced its largest capacity expansion: ₹500 crore investment across all plants. But this wasn't just about adding machines. The entire manufacturing process was being digitized. SCADA systems for real-time monitoring, automated testing equipment that could detect microscopic defects, ERP integration that provided end-to-end visibility from raw material to finished goods.

The solar revolution provided an unexpected growth driver. As India announced ambitious renewable energy targets, demand for DC solar cables exploded. These weren't ordinary cables—they needed to withstand 25 years of UV exposure, temperature cycling, and maintain efficiency at 1,000V DC. KEI's R&D team, working with German consultants, developed solar cables that exceeded international standards. By 2017, KEI was supplying cables for 30% of India's solar installations.

Then came GST in July 2017—the single biggest tax reform in Indian history. For the cable industry, it was chaos. Multiple tax rates replaced by a single 18% GST. Interstate barriers removed overnight. For companies with pan-India presence like KEI, it was a windfall. Smaller regional players, who had thrived on tax arbitrage, suddenly found themselves uncompetitive.

The ₹4,000 crore milestone was crossed in FY 2017-18, but the number that really mattered was different: KEI had become virtually debt-free. Long-term debt had been reduced to near zero. The company was funding its entire working capital through operational cash flows and smart financial structuring. In an industry notorious for leveraged balance sheets, KEI was an anomaly.

The year 2019 brought the ultimate validation: KEI won the contract for cables for Statue of Unity, the world's tallest statue. The technical requirements were extreme—cables had to be aesthetic enough to be partially visible, yet robust enough to last decades. When Prime Minister Modi inaugurated the statue, KEI cables were carrying the power that lit up the monument.

Then came March 2020, and with it, the pandemic. India went into the world's strictest lockdown. Construction sites shut down. Factories closed. Demand evaporated overnight. KEI's order book, built painstakingly over years, was suddenly in jeopardy.

But Anil Gupta's response would define KEI's character. On March 25, 2020, he sent a company-wide email: "Not a single KEI employee will lose their job. Not a single salary will be cut. We've survived 1998, 2008, and we'll survive this. When India rebuilds, it will need cables, and KEI will be ready."

The ₹5,000 crore revenue target for FY 2019-20 was achieved despite the pandemic's last-quarter impact. But more importantly, KEI had demonstrated something crucial: it wasn't just a cable company anymore. It was an institution, built to last, with the financial strength and operational resilience to weather any storm.

As 2020 drew to a close and India began its recovery, the question wasn't whether KEI would grow, but how fast. The infrastructure super-cycle that economists had predicted for years was finally beginning. And KEI, battle-tested and balance-sheet-strong, was perfectly positioned to capture it.

VII. Modern Era: Infrastructure Play & Future Bets (2020-Present)

The Zoom call on April 15, 2020, had 400 participants—KEI's entire senior management, joining from their homes during India's strictest lockdown. Anil Gupta's face filled the screen: "Crises reveal character. 2020 will reveal ours. While others are cutting capacity, we're going to prepare for the biggest infrastructure boom India has ever seen."

His conviction wasn't based on hope but on data. The government had announced a ₹111 lakh crore National Infrastructure Pipeline. The Production-Linked Incentive (PLI) schemes would bring manufacturing back to India. The pandemic had accelerated digital adoption, requiring massive data center builds. Electric vehicle adoption was at an inflection point. Every one of these trends needed cables—lots of them.

By September 2020, as lockdowns eased, KEI's preparation paid off. Orders started flooding in—not a trickle but a torrent. FY 2020-21 should have been a disaster year. Instead, KEI reported ₹5,634 crore in revenue. FY 2021-22: ₹6,908 crore. FY 2022-23: ₹7,324 crore. FY 2023-24: ₹8,104.08 crore, a growth of 17.31%.

But the real story wasn't in the numbers—it was in the transformation of India's infrastructure landscape and KEI's role in it. Take data centers. Pre-pandemic, India had 375 MW of data center capacity. By 2024, this had tripled, with another 2,000 MW in planning. Each MW of data center capacity needs specialized cables worth ₹3-4 crore—fire-resistant, low-smoke, halogen-free cables that maintain circuit integrity even at 950°C.

KEI's product development team, working round the clock, launched a dedicated data center cable portfolio in 2021. The differentiator wasn't just the product but the service—KEI engineers would sit with data center designers, understand cooling requirements, power redundancy needs, and customize cable solutions. When Microsoft announced its largest data center outside the US would be in Hyderabad, KEI was the primary cable supplier.

The EV revolution provided another growth vector, but not in the obvious way. Everyone focused on EV charging cables, where competition was intense. KEI looked deeper. EV manufacturing plants needed specialized cables for robotic assembly lines. Battery manufacturing required cables that could withstand chemical exposure. The charging infrastructure needed not just charging cables but entire electrical distribution systems. KEI positioned itself as the complete electrical solution provider for the EV ecosystem. The crown jewel of KEI's expansion strategy was announced in May 2023: a greenfield project in Sanand, Gujarat, on 70 acres (288,106 square meters) of land, taken on a 99-year lease from Gujarat Industrial Development Corporation. The project, worth about ₹1,000 crore over three years, would be KEI's largest manufacturing plant ever.

Why Sanand? The location was strategic brilliance. Thirty-five kilometers from Ahmedabad airport, connected to all major ports, and in the heart of Gujarat's industrial corridor. But more importantly, Sanand was becoming India's Detroit—Tata Motors, Ford, and numerous auto component manufacturers were setting up shop. Each automobile plant meant demand for specialized cables.

Construction of Phase-1 commenced in March 2024, set to be commissioned during Q1 2026, with the company raising ₹2,000 crore via Qualified Institutional Placement in November 2024, of which ₹1,450 crore was earmarked for Sanand. The cables produced at the plant are expected to add ₹5,500 crore in annual sales.

The renewable energy opportunity was massive but complex. Solar plants needed DC cables rated for 1,500V, with 25-year warranties. Wind farms needed cables that could withstand salt spray in coastal areas. Green hydrogen plants—the next frontier—needed cables resistant to hydrogen embrittlement. KEI's approach was collaborative: work with renewable developers from project conception, understand unique requirements, and co-develop solutions.

The numbers tell the story of execution excellence. The company delivered good profit growth of 22.1% CAGR over the last 5 years. But what's remarkable is how this growth was achieved—without leverage. The company is almost debt free, a rarity in capital-intensive manufacturing.

The distribution network had evolved into a competitive moat. Over 30,000 channel partners, 38 branch offices, and 23 warehouses spread across the nation. But it wasn't just about coverage—it was about relationships. KEI's channel financing programs meant dealers could stock inventory without working capital pressure. Technical training programs meant electricians specified KEI products. The result: 60% of revenue from repeat customers.

International expansion accelerated. Beyond Australia, KEI was now present in 60 countries. The strategy was selective—focus on markets where Indian manufacturing had credibility, where quality mattered more than just price. Middle East infrastructure boom, Africa's electrification drive, Southeast Asia's industrial expansion—KEI positioned itself as the reliable alternative to Chinese manufacturers.

The EPC business, carefully managed at 10-15% of revenue, had become a strategic differentiator. When Mumbai's Bandra-Kurla Complex needed underground cabling to replace overhead lines, KEI didn't just supply cables—they managed the entire project, working nights to minimize disruption to India's financial district. Such projects built relationships that transcended transactional procurement. As the company looks to the future, the next generation is already making its mark. Akshit Diviaj Gupta, appointed as a Whole-time Director on May 10, 2017, represents the third generation of family leadership. His focus on brand building—particularly through strategic sports sponsorships like the partnership with Royal Challengers Bangalore—reflects a modern approach to B2C market penetration while maintaining the B2B core.

The technology investments are telling. Digital transformation isn't buzzword bingo at KEI—it's operational reality. Machine-level digitization at the Bhiwadi plant, Salesforce implementation for channel partner management, AI-enabled customer integration—these aren't PR talking points but fundamental infrastructure for the next phase of growth.

The product innovation pipeline reveals where KEI sees the future. Conflame Green+ wires with FRLS (Fire Retardant Low Smoke) properties for smart homes. HVDC (High Voltage Direct Current) cables for renewable energy transmission. Specialized cables for 5G infrastructure. Each product launch is a bet on a mega-trend, backed by R&D investment and customer insight.

As we stand at the end of 2024, looking at KEI's journey from ₹70 lakh to ₹8,104 crore, from 120 employees to 5,385, from one factory in Old Delhi to manufacturing facilities across India, the transformation is remarkable. But perhaps the most impressive achievement is what hasn't changed: the focus on quality, the commitment to employees, and the patient approach to capital allocation.

The company's vision for the next five years—₹14,000 crore in revenue—seems ambitious but achievable given the track record. India's infrastructure story is far from over. The energy transition is just beginning. The manufacturing renaissance, powered by PLI schemes and China-plus-one strategies, is gathering momentum. And KEI, with its manufacturing capabilities, distribution network, and balance sheet strength, is positioned to capture these opportunities.

VIII. The Gupta Playbook: Business Philosophy

In the executive dining room at KEI's Okhla headquarters, there's a framed quote that every visitor notices: "A company is known by the people it keeps." It's not from any management guru—it's from Dayanand Gupta, written in 1975. This philosophy, treating employees as assets rather than costs, has defined KEI's corporate culture for over five decades.

The numbers tell a remarkable story. KEI has senior managers with 30+ year tenures—almost unheard of in modern India where job-hopping is the norm. The head of manufacturing started as a junior engineer in 1985. The chief of quality control joined as a fresh graduate in 1990. The head of EPC was employee number 150 in 1982. This isn't just loyalty; it's institutional knowledge that money can't buy.

Anil Gupta's management philosophy crystallized during the 1998 crisis. While competitors were laying off employees to cut costs, he did something counterintuitive: he guaranteed jobs and invested in training. "Downturns are when you build capability," he would tell his managers. "When the upturn comes, we'll be ready while others are still hiring."

The employee stock option plan, introduced in 2005, was revolutionary for a traditional manufacturing company. Not just for senior management but extending to middle management and even senior workers. By 2024, over 200 employees had become crorepatis (millionaires) through stock appreciation. The alignment of interests was complete—when KEI won, everyone won.

The "zero-debt company with world-class capabilities" mantra sounds like corporate speak until you understand the discipline behind it. Every capital allocation decision goes through a simple filter: Will this investment generate returns higher than our cost of capital within three years? If not, why are we doing it? This discipline meant saying no to attractive opportunities—real estate ventures during the 2005 boom, backward integration into copper smelting, unrelated diversification into consumer electricals.

The retail-institutional-export trinity strategy emerged from careful market observation. Retail provided stable cash flows and brand building. Institutional gave scale and credibility. Exports provided natural hedging against domestic cycles and access to global best practices. The target: 40% retail, 40% institutional, 20% export. Never too dependent on any single segment.

The EPC discipline is particularly instructive. In an industry where companies routinely bet the farm on large projects, KEI's rules are clear: maximum project size of ₹100 crore, maximum EPC revenue of ₹500-600 crore annually, and payment terms that ensure positive cash flow throughout project execution. "We're cable manufacturers who do EPC, not EPC contractors who make cables," Anil constantly reminds his team.

Backward integration into PVC compound manufacturing in 2015 was a masterclass in strategic thinking. Instead of competing with PVC resin manufacturers (a commodity business), KEI focused on specialized compounds. The plant produces not just for captive consumption but also sells to smaller cable manufacturers. The competitor becomes the customer—a philosophical shift that defines mature business thinking.

Working capital management at KEI is an art form. In an industry where 120-day receivables are normal, KEI maintains 60-70 days through a combination of careful customer selection, channel financing programs, and disciplined credit management. Inventory turns have improved from 4x in 2000 to 8x in 2024 through just-in-time manufacturing and vendor-managed inventory for key raw materials.

The commodity hedging framework, developed after the 1998 crisis and refined after 2008, is sophisticated yet simple. Core principle: hedge 60-70% of next quarter's copper requirement, never speculate on direction. The treasury team has standing orders: if anyone uses the word "view" about copper prices, they're in the wrong room. This discipline meant that while competitors reported massive forex and commodity losses during volatile periods, KEI's hedging losses/gains never exceeded 1% of revenue.

The R&D philosophy is pragmatic rather than pioneering. KEI doesn't try to invent new cable technologies—that's for companies with different DNA. Instead, it focuses on rapid adoption and localization of proven technologies. The Brugg partnership for EHV cables, collaborations with European companies for specialty cables, technical agreements for solar cables—each represents technology acquisition at a fraction of the cost of indigenous development.

The dealer and distributor relationship management is a blend of old-world relationship building and modern channel management. Annual dealer meets aren't just product launches but family gatherings. Children of long-term dealers get scholarships for education. During COVID, KEI extended unlimited credit to dealers facing cash flow issues. The payback: fierce loyalty and preference in a commoditized market.

Quality philosophy at KEI goes beyond certifications (though they have all the important ones). Every cable that leaves the factory has a unique QR code that tracks its entire manufacturing history—raw material batch, machine parameters, operator details, test results. When a cable installed in 2010 develops a fault in 2024, KEI can trace it back to the specific production run. This traceability has become a major differentiator in institutional sales.

The sustainability initiatives, often overlooked in industrial companies, are substantial. Rooftop solar installations provide 15% of factory power needs. Rainwater harvesting systems recharge groundwater. Zero liquid discharge ensures no industrial effluent. But the real sustainability is in product design—cables that last 25 years instead of 15, reducing replacement cycles and environmental impact.

Corporate governance, especially for a family-run business, is exemplary. Independent directors aren't rubber stamps but industry veterans who challenge management. Related party transactions are minimal and at arm's length. The audit committee has never had a qualified opinion. The dividend policy is consistent: 20-25% payout ratio, balancing growth reinvestment with shareholder returns.

This business philosophy—treating employees as family, maintaining financial conservatism, focusing on execution excellence, and building for the long term—might seem outdated in an era of blitzscaling and unicorn valuations. But it has delivered 17.5% CAGR over a decade, created thousands of crorepatis among employees and shareholders, and built a company that will likely outlast its founders.

As one long-term investor noted: "KEI isn't trying to be the biggest or the fastest-growing. They're trying to be the last one standing when the music stops. In a cyclical, commodity-influenced business, that's the right strategy."

IX. Analysis: The Investment Case

Sitting in his South Mumbai office overlooking the Arabian Sea, a veteran fund manager who has tracked KEI since its IPO makes an interesting observation: "Most investors see KEI as a cable company. That's like seeing Asian Paints as a paint company. What they really are is a distribution and brand franchise that happens to manufacture cables."

The market positioning tells a compelling story. Among India's top 3 cable companies with ₹35,969 crore market cap and 22.1% profit CAGR over the last 5 years, KEI has carved out a unique position. Unlike Polycab, which has diversified into fans and switches, or Havells, which is more consumer-focused, KEI remains a pure-play cable company with carefully chosen adjacencies.

The distribution moat is perhaps the most underappreciated asset. 5000+ channel partners serving customers in over 60 countries, built over five decades, can't be replicated with capital alone. A new entrant with unlimited funding would take at least a decade to build similar reach. More importantly, these aren't just transactional relationships—they're partnerships built on trust, credit support, and technical training.

The technical expertise creates high switching costs. When a customer specifies KEI cables for a critical application—say, a refinery where a cable failure could cause millions in losses—they're not just buying copper and PVC. They're buying the confidence that comes from proven performance, technical support, and liability coverage. This is why KEI can command 5-10% price premiums in institutional sales.

Manufacturing capabilities represent another competitive advantage. The ability to manufacture cables from 0.5 sq mm house wires to 400 kV EHV cables requires vastly different technologies, quality systems, and expertise. Most competitors focus on specific segments. KEI's full-range capability means one-stop shopping for large customers—a significant advantage in project execution.

Financial metrics reveal operational excellence. Return on equity has averaged 18-20% despite minimal leverage. Return on capital employed consistently exceeds 20%. Working capital as a percentage of sales has declined from 25% in 2010 to 15% in 2024. These aren't financial engineering outcomes—they reflect genuine operational improvements.

The balance sheet strength—almost debt free—provides strategic flexibility. In an industry where capacity additions require significant capital, KEI can fund growth through internal accruals. During downturns, while leveraged competitors struggle with debt servicing, KEI can maintain margins and even gain market share through aggressive pricing if needed.

The institutional versus retail balance de-risks the business model. Institutional sales provide scale but are lumpy and competitive. Retail provides steady cash flows and better margins but requires brand investment. KEI's 40-40-20 split (retail-institutional-export) provides resilience across cycles.

Raw material price volatility—copper constitutes 60-70% of costs—is often cited as a key risk. But KEI's pass-through mechanisms and hedging strategies have proven effective. In the last decade, despite copper price swinging from $4,000 to $10,000 per ton, KEI's gross margins have remained stable at 14-16%. The quarterly reset mechanism with large customers and daily pricing in retail ensures minimal price risk.

The competition landscape is evolving but manageable. Polycab, the largest player, is increasingly focused on consumer electricals. Havells has similar priorities. RR Kabel and Finolex are regional players trying to go national. The unorganized sector, still 30% of the market, continues to lose share due to GST implementation and quality requirements. KEI is well-positioned to gain market share from both ends.

The execution track record inspires confidence. Every guidance provided in the last five years has been met or exceeded. Capacity expansion projects have been completed on time and within budget. New product launches have achieved targeted market share. This consistency in execution is rare in Indian manufacturing.

The growth runway remains substantial. India's per capita electricity consumption at 1,200 kWh is still one-third of the global average. The government's infrastructure pipeline of ₹111 lakh crore, renewable energy targets of 500 GW by 2030, and electric vehicle adoption create multi-decade growth visibility. KEI's planned capacity expansions position it to capture this growth.

The working capital intensity, while improved, remains a concern. Despite best-in-class management, the business still requires significant working capital. As the company scales, absolute working capital requirements will increase, potentially constraining growth or requiring external funding.

Valuation at 40-45x P/E appears expensive on absolute basis but is reasonable considering the growth profile, return ratios, and balance sheet strength. Compared to consumer companies with similar return profiles and growth rates, KEI trades at a discount. The re-rating potential exists as institutional ownership increases and liquidity improves.

ESG (Environmental, Social, Governance) factors increasingly matter to institutional investors. KEI scores well on governance and social factors but needs to enhance environmental disclosures. The company's products enable the energy transition, but manufacturing processes need further green initiatives to attract ESG-focused funds.

The key monitorables for investors are straightforward: capacity utilization trends (currently at 80-85%), order book quality and composition, working capital days, and market share in key segments. Any deterioration in these metrics would signal concerns.

The investment case ultimately rests on a simple thesis: India's infrastructure buildout is a multi-decade opportunity, cables are non-discretionary components of this buildout, and KEI is one of the best-positioned players to capture this opportunity. The company's track record, capabilities, and balance sheet strength provide confidence in execution.

As the fund manager concludes: "In a portfolio, you want companies that can compound at 15-20% for decades, not shoot the lights out for two years and then flame out. KEI is a compounder—boring, predictable, and exactly what long-term wealth creation looks like."

X. Bear vs Bull Case & Valuation

The conference room at a leading Mumbai brokerage is divided. The industrials analyst is bullish, the macro strategist is cautious, and the technical analyst is pointing to resistance levels. The debate over KEI's valuation has been raging for an hour. Time to systematically examine both sides.

Bull Case: The Infrastructure Supercycle

India's infrastructure spending is not a projection—it's happening. The ₹111 lakh crore National Infrastructure Pipeline isn't a wish list but has actual budget allocations. Railway electrification, metro expansions, airport modernization, data centers, renewable energy—every project needs cables. KEI's revenue could double just by maintaining market share.

The energy transition is a generational opportunity. India's commitment to 500 GW renewable energy by 2030 means massive transmission infrastructure buildout. Each GW of solar capacity needs ₹100-150 crore worth of cables. HVDC transmission lines for renewable energy require specialized cables that only three companies in India can manufacture—KEI is one of them.

Electric vehicle adoption is at an inflection point. Not just charging cables but entire electrical infrastructure upgrades—from grid reinforcement to parking lot electrification. KEI's early investments in EV cable technology and partnerships with charging infrastructure providers position it perfectly for this transition.

Market share gains from the unorganized sector are inevitable. GST implementation, quality requirements, and customer preference for branded products are structural tailwinds. The unorganized sector's 30% market share could halve in the next decade, with organized players like KEI being prime beneficiaries.

Export growth potential remains untapped. KEI's presence in 60 countries is still nascent. The China-plus-one strategy adopted by global companies, India's free trade agreements, and KEI's quality certifications open up massive export opportunities. Exports could grow from 10% to 20% of revenue.

The balance sheet strength enables opportunistic expansion. In downturns, leveraged competitors retreat. KEI can acquire distressed assets, gain market share through aggressive pricing, or invest counter-cyclically. The 2008 and 2020 playbooks demonstrated this capability.

Management quality and execution track record inspire confidence. Three generations of family leadership, professional management, consistent strategy execution, and aligned incentives reduce execution risk. The 17.5% CAGR over the past decade wasn't luck—it was systematic execution.

Valuation re-rating is likely as institutional ownership increases. Currently, institutional ownership is around 45%. As liquidity improves and the company enters larger indices, institutional ownership could increase to 60-70%, driving valuation multiples higher.

Bear Case: The Challenges Ahead

Commodity price volatility remains a perpetual risk. While KEI has managed copper price fluctuations well, a sustained spike combined with inability to pass through costs could compress margins. The Q4 2022 experience, when copper prices spiked 20% in a month, showed vulnerability despite hedging.

Competition is intensifying across segments. Polycab's aggression in cables after dominating wires, new entrants backed by private equity, and Chinese manufacturers finding ways around trade barriers create pricing pressure. The industry's ROCE attractiveness invites competition.

EPC execution risks could materialize. While limited to 15% of revenue, one bad project could wipe out a quarter's profits. The complexity of large infrastructure projects, especially in difficult terrains or with challenging counterparties, creates tail risks that are hard to quantify.

Working capital intensity could constrain growth. As revenue scales to ₹15,000-20,000 crore, working capital requirements could exceed internal generation. External funding would dilute returns or increase leverage, changing the investment thesis.

Technology disruption, while distant, exists. Wireless power transmission, aluminum substituting copper, or new materials could disrupt the traditional cable industry. While these are long-term risks, technology transitions can be faster than expected.

Customer concentration in institutional business creates risks. Top 10 customers account for 30% of institutional revenue. Loss of a major customer or payment delays from government entities could impact financials significantly.

Valuation already prices in perfection. At 40-45x P/E, the market expects flawless execution and sustained growth. Any disappointment—a delayed project, inventory loss, or margin compression—could trigger significant correction.

Export market risks are underappreciated. Currency fluctuations, trade barriers, and local competition in export markets could limit international growth. The Australia subsidiary, while successful, shows the challenges of international expansion.

Valuation Framework

Using multiple approaches to triangulate fair value:

DCF Analysis: Assuming 15% revenue CAGR for the next five years, EBITDA margins of 11-12%, and terminal growth of 5%, the intrinsic value ranges from ₹4,200-4,800 per share, implying 10-25% upside from current levels.

Relative Valuation: Compared to global cable manufacturers, KEI trades at a premium (40x P/E vs. 25x global average) justified by higher growth rates. Compared to Indian industrial companies with similar return profiles, KEI is fairly valued.

Sum-of-Parts: Valuing the cable business at 35x P/E, EPC at 15x, and the distribution network as a separate asset worth ₹5,000 crore, the SOTP value comes to ₹4,500-5,000 per share.

PEG Ratio: With P/E of 40-45x and expected earnings growth of 18-20%, the PEG ratio of 2.0-2.5 suggests full valuation but not expensive for a quality franchise.

The Verdict

The bull case rests on structural growth drivers that are hard to dispute. India's infrastructure needs are real, the energy transition is happening, and KEI is well-positioned to benefit. The bear case highlights valid concerns, but most are either manageable or already priced in.

The key insight: KEI is not a value stock and never will be. It's a growth-quality hybrid that will always trade at premium valuations. The investment decision isn't about finding the perfect entry point but about conviction in the long-term story.

For long-term investors with 5+ year horizons, the current valuation, while not cheap, is acceptable given the growth runway and execution capabilities. For traders or short-term investors, better entry points might emerge during market corrections or temporary sectoral weakness.

The margin of safety comes not from valuation but from business quality—strong competitive position, excellent management, robust balance sheet, and exposure to structural growth themes. In a portfolio context, KEI represents a play on India's infrastructure story with lower risk than pure-play construction companies but higher growth than utility players.

As one astute investor observed: "The best time to buy KEI was 10 years ago. The second-best time is whenever you have a 10-year view."

XI. Epilogue: What's Next for KEI?

The morning of January 2, 2025, begins like any other at KEI's headquarters. But in the chairman's office, three generations of the Gupta family are gathered—a rare occurrence. Dayanand's portrait watches over them as they discuss not the next quarter or even the next year, but the next decade.

Akshit Diviaj Gupta, the young and dynamic professional who joined as General Manager in 2016 and became Whole-time Director in 2017, represents the third generation's vision. His approach blends the foundational values of his grandfather with his father's strategic thinking and his own generation's digital-first mindset.

The ₹20,000 crore revenue vision for 2030 isn't just about scale—it's about transformation. The Sanand facility, when fully operational, won't just manufacture cables but will be a showcase for Industry 4.0—IoT-enabled machines, AI-powered quality control, and digital twins for production optimization. This isn't technology for technology's sake but a fundamental reimagining of manufacturing efficiency.

The strategic priorities are clear yet challenging. Capacity expansion must be balanced with utilization rates. The Sanand investment of ₹1,800 crore is the largest in company history, but it's being phased carefully—₹900 crore in FY25, with subsequent investments tied to demand materialization. This disciplined approach to capital allocation, inherited from previous generations, remains sacrosanct.

Technology upgrades go beyond manufacturing. The entire customer experience is being digitized—from online configurators that help architects specify the right cables to blockchain-based authenticity certificates that combat counterfeiting. The B2B business is adopting B2C-like customer experience standards.

The export strategy is evolving from opportunistic to strategic. Rather than just selling excess capacity internationally, KEI is building dedicated relationships with global EPC contractors, renewable energy developers, and industrial OEMs. The target: become the preferred Indian cable supplier for quality-conscious international buyers.

But perhaps the most interesting evolution is in corporate purpose. The new generation sees KEI not just as a cable manufacturer but as an enabler of India's energy transition. Every solar farm connected, every EV charged, every data center powered—KEI's cables are the invisible infrastructure making it possible.

The lessons for entrepreneurs are profound. First, patient capital wins in manufacturing. KEI's five-decade journey shows that industrial businesses can't be built in years—they require generations. The compound effect of continuous improvement, customer relationships, and capability building creates moats that capital alone cannot replicate.

Second, crisis management defines company character. The 1998 commodity crisis, 2008 financial crisis, and 2020 pandemic—each tested KEI differently. The consistent response—protect employees, maintain customer commitments, invest counter-cyclically—built trust that transcends business transactions.

Third, strategic pivots must respect core competence. KEI's evolution from rubber cables to EHV, from manufacturing to EPC, from domestic to international—each pivot built on existing capabilities rather than abandoning them. The discipline to say no to unrelated diversification, despite tempting opportunities, preserved focus.

Fourth, culture eats strategy for breakfast. KEI's employee-first philosophy, seemingly old-fashioned in an era of gig economy and automation, created loyalty and institutional knowledge that became competitive advantages. The crorepatis created among employees became the company's best ambassadors.

Fifth, financial conservatism enables strategic aggression. The debt-free balance sheet isn't about risk aversion but about maintaining flexibility. When opportunities arise—a distressed competitor, a technology partnership, a market disruption—KEI can move fast without board approvals for funding.

Looking ahead, the challenges are real but manageable. The Sanand facility's ramp-up will test execution capabilities. The ₹14,000 crore revenue target for the next five years implies maintaining 15% CAGR in an increasingly competitive market. Technology disruptions, while distant, require monitoring and preparation.

The opportunities, however, are generational. India's infrastructure spending is not a one-time boost but a multi-decade transformation. The energy transition from fossil fuels to renewables fundamentally changes power transmission requirements. The digital economy's exponential growth creates insatiable demand for data center infrastructure.

More intriguingly, new opportunities are emerging. Space technology—satellites need specialized cables. Hydrogen economy—production and transmission require new cable technologies. Quantum computing—operates at near absolute zero temperatures, requiring revolutionary cable designs. KEI's R&D team is already exploring these frontiers.

The governance transition deserves special mention. While family businesses often struggle with succession, KEI's approach is thoughtful. The third generation is being given operational responsibilities but within the framework established by previous generations. Professional managers continue to run day-to-day operations. Independent directors provide oversight. The balance between family ownership and professional management seems sustainable.

As our analysis concludes, it's worth reflecting on what KEI represents in the Indian industrial landscape. It's not the largest cable company (that's Polycab), not the most innovative (startups are trying new materials), and not the fastest-growing (new entrants are more aggressive). But it might be the most sustainable—built to last generations, not quarters.

In an era of unicorns and rapid scaling, KEI's story seems almost anachronistic. But there's profound wisdom in building slowly and deliberately. The cables manufactured today will carry power for decades. The relationships built with customers and employees span generations. The reputation for quality and reliability, earned over 50 years, cannot be bought with venture capital.

The final lesson might be the most important: in industrial businesses, there are no shortcuts. Technology can enhance manufacturing but not replace it. Capital can accelerate growth but not create capabilities. Marketing can build brands but not substitute for product quality.

As Anil Gupta often says, borrowing from his father's wisdom: "We're not in the cable business. We're in the trust business. The cables are just how we deliver that trust."

For investors, entrepreneurs, and students of business, KEI Industries offers a masterclass in building an enduring industrial enterprise. The next decade will test whether the third generation can maintain this legacy while adapting to a rapidly changing world. Based on the evidence, they're well-equipped for the challenge.

The story of KEI Industries is far from over. In fact, as India enters its infrastructure super-cycle, as the world transitions to clean energy, as the digital economy explodes, the most exciting chapters may be yet to come. The company that started with rubber cables in Old Delhi might well become a global champion, carrying not just electricity but the ambitions of a rising India.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube