Shakti Pumps (India) Limited: From Local Pumps to Solar Leadership

I. Introduction & Episode Roadmap

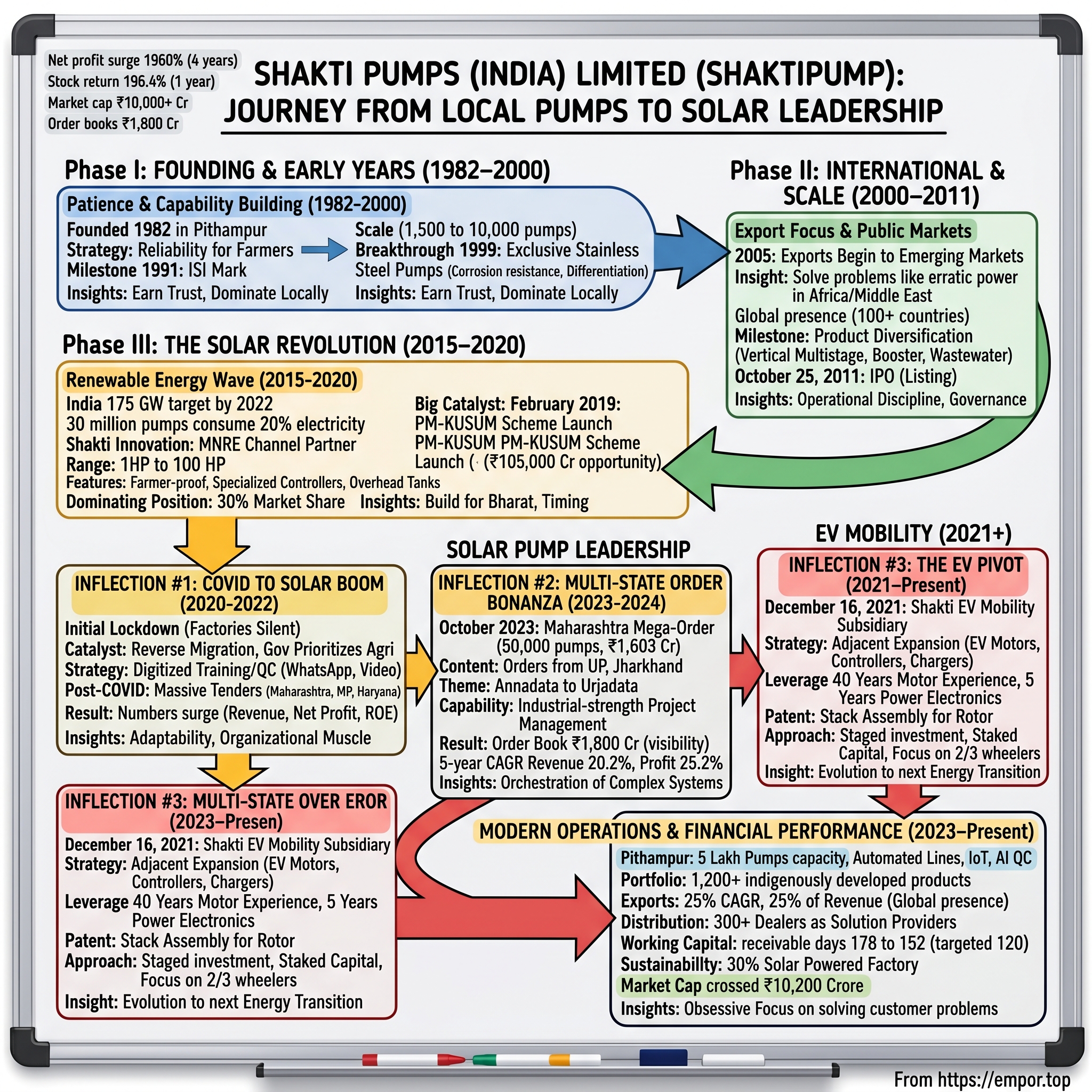

Picture this: A company's net profit surges 1960% in just four years. Not a tech unicorn. Not a pharmaceutical breakthrough. But a pump manufacturer from Madhya Pradesh that most investors had never heard of until recently. This is the story of Shakti Pumps—a 42-year-old company that transformed from a local submersible pump maker into India's solar pump champion, now exporting to over 100 countries while quietly building an electric vehicle subsidiary that might reshape its future yet again.

The numbers tell one story: From struggling with negative returns in FY20 to delivering a 196.4% stock return in the past year alone. Market cap crossing ₹10,000 crore. Order books swelling to ₹1,800 crore. But the real story—the one that matters for understanding how industrial companies create lasting value in India—lies in how a small manufacturer from Pithampur cracked the code on government partnerships, rode the renewable energy wave at exactly the right moment, and built operational excellence in one of the most challenging sectors imaginable: rural infrastructure.

Founded in 1982, when India's industrial landscape looked nothing like today, Shakti Pumps began with a simple premise: build reliable pumps for India's farmers. Four decades later, it dominates 30% of India's solar pump market under the PM-KUSUM scheme—a ₹105,000 crore opportunity that's still in early innings. The company that once made 1,500 pumps annually now has capacity for 500,000, with technology ranging from basic submersibles to sophisticated solar-powered systems that turn farmers from "Annadata" (food providers) into "Urjadata" (energy providers).

How did a traditional manufacturing company navigate India's complex policy landscape, survive multiple economic cycles, and emerge as a renewable energy leader? How did it build trust with state governments from Maharashtra to Uttar Pradesh, securing multi-hundred crore contracts when competitors with deeper pockets struggled? And perhaps most intriguingly—why is this pump manufacturer now investing heavily in electric vehicle motors, potentially setting up its next transformation?

This is more than a corporate success story. It's a masterclass in reading India's policy tea leaves, building for Bharat rather than just India, and understanding that in infrastructure, timing isn't just important—it's everything. We'll trace Shakti's journey from its humble beginnings through international expansion, the solar revolution that changed everything, the COVID crisis that became an unexpected catalyst, and the current moment where government orders flow like monsoon rain while the company quietly builds what might become its next act in electric vehicles.

The structure ahead: We'll start with those early years in Madhya Pradesh's industrial heartland, move through the patient building of capabilities that would matter decades later, examine the inflection points that transformed the business, and end with what this all means for India's infrastructure story. Along the way, we'll extract the playbook—because Shakti's strategy of partnering with government, building for rural markets, and diversifying at precisely calibrated moments offers lessons that extend far beyond pumps and solar panels.

II. Founding Story & Early Years (1982–2000)

The industrial estate of Pithampur in early 1982 was little more than promise and red dirt. Madhya Pradesh's government had just begun developing what would become one of India's most successful Special Economic Zones, but at the time, it was a gamble—far from established manufacturing hubs, lacking basic infrastructure, with only the state's assurance that this would become something significant. Into this uncertainty stepped the founders of what began as Shakti Electrical Industries, a name that would undergo three reconstitutions before emerging as Shakti Pumps (India) Limited.

The choice of Pithampur wasn't accidental—it was strategic chess played decades before the payoff. While competitors clustered in Gujarat's established industrial corridors or Tamil Nadu's manufacturing belts, Shakti's founders saw opportunity in Madhya Pradesh's centrality. Geographic center meant equidistant access to markets north and south. State government incentives meant lower capital requirements. And being early meant relationships—with local officials, with emerging suppliers, with the farming communities that would become not just customers but evangelists.

That first manufacturing unit was almost quaint by today's standards: capacity for 1,500 submersible pumps annually. The founders weren't thinking global scale—they were solving a local problem. Madhya Pradesh's farmers needed reliable irrigation, but existing pumps either came from distant manufacturers with little service support or local assemblers with questionable quality. Shakti positioned itself in between: industrial-grade manufacturing with local presence and commitment.

The early product focus revealed DNA that would define the company for decades: submersible pumps and motors designed specifically for Indian conditions. Not imported designs adapted for local use, but ground-up engineering for wells that ran dry seasonally, power supply that fluctuated wildly, and maintenance skills that varied dramatically across rural regions. This wasn't glamorous innovation—it was patient, iterative improvement based on feedback from mechanics in Indore's villages and farmers in Bhopal's periphery.

By 1991, nine years in, came the first validation that mattered in India's quality-conscious but price-sensitive market: the ISI mark certification. For industrial buyers, particularly government departments, this wasn't just a stamp—it was permission to be considered serious. Shakti leveraged this immediately, becoming a major supplier to Madhya Pradesh's government, the Public Health Engineering Department, and irrigation departments. These weren't just customers; they were references that opened doors across state boundaries.

The 1995 expansion marked a mindset shift from survival to scale. Capacity jumped from 1,500 to 10,000 pumps annually—a 6.6x increase that required not just capital but confidence that demand would follow supply. The company added control panels (8,000 per annum capacity) and entered monoblock pumps, diversifying within its core competency. This wasn't random product proliferation—each addition solved an adjacent problem for the same customer base. Farmers who bought submersible pumps needed control panels. Those with different water table depths needed monoblock options. What happened in 1998-1999 revealed prescient strategic thinking. The ISO 9002 certification wasn't just another quality badge—it was internationalization groundwork laid years before actual exports began. But the real masterstroke came in 1999: Shakti became the exclusive manufacturer of motor pump sets purely of stainless steel in the nation. This wasn't incremental improvement—it was category creation. While competitors fought on price with cast iron, Shakti chose differentiation through material science. Stainless steel meant corrosion resistance crucial for India's varied water conditions, longer life reducing total cost of ownership, and premium positioning that would matter when government tenders looked beyond L1 pricing.

The period from 1982 to 2000 wasn't glamorous. No venture funding. No media coverage. No hockey-stick growth charts. Just patient building of capabilities that would compound over decades. The founders understood something fundamental about Indian industrial success: before you can scale, you must earn trust. Before you expand geographically, you must dominate locally. Before you innovate radically, you must execute flawlessly on basics.

By 2000's end, Shakti had built four critical assets that money alone couldn't buy: relationships with government departments that would become massive customers two decades later, manufacturing expertise in stainless steel that competitors would struggle to replicate, understanding of rural markets that urban-focused companies missed, and most importantly, a reputation for reliability in sectors where failure meant crop loss and livelihood destruction. The foundation was set. The next phase would test whether this Madhya Pradesh manufacturer could transform regional success into national relevance—and eventually, global ambition.

III. Going International & Building Scale (2000–2011)

The early 2000s found India's industrial landscape in flux. China had just entered the WTO, flooding global markets with cheap manufacturing. Indian companies faced an existential choice: retreat into protected domestic markets or venture into the very global arena where Chinese competition seemed insurmountable. For Shakti Pumps, sitting in Pithampur with a decade of steady but unspectacular growth, the decision would define its next chapter.

By 2005, Shakti began what seemed almost naive—exporting pumps from India when the world was buying everything from China. But the company had identified an insight others missed: emerging markets didn't just need cheap pumps; they needed pumps that worked in conditions similar to India's. African farmers faced the same erratic power supply as their counterparts in Madhya Pradesh. Middle Eastern installations dealt with similar heat and dust. Latin American agricultural regions had comparable maintenance skill gaps. Shakti exports a wide range of pumping products to over 100 countries globally—but this eventual reach started with careful selection of markets where "Made in India" meant "Made for conditions like yours."

The export strategy revealed sophisticated thinking about product-market fit. Rather than competing with European manufacturers on precision engineering or Chinese players on cost, Shakti positioned itself in the middle: robust enough for harsh conditions, affordable enough for developing markets, with service philosophy that understood irregular maintenance schedules and variable operator skills. The company didn't just export products—it exported solutions designed for the realities of emerging market infrastructure.

"Shakti" brand products are well received in the market as they are conforming to national international standards coupled with superior quality and durability. This wasn't marketing speak—it was systematic brand building in markets where word-of-mouth mattered more than advertising. Each international installation became a reference point. Each successful deployment in Nigeria's agricultural belt or Bangladesh's shrimp farms became proof that Indian engineering could compete globally—not on price alone, but on understanding customer context.

Product diversification during this period followed a careful logic. Beyond the core submersible pumps, the company expanded into vertical multistage centrifugal pumps for industrial applications, pressure booster pumps for commercial buildings, and specialized wastewater pumps for urban infrastructure. Each addition leveraged existing manufacturing capabilities while opening new customer segments. This wasn't random proliferation—it was systematic market expansion using the same stainless steel expertise and motor technology as competitive advantages.

The building toward public markets began around 2008-2009, as the company recognized that international expansion and product diversification would require capital beyond what traditional banking could provide. The preparation for IPO forced operational discipline that would pay dividends later: formal financial reporting systems, institutional governance structures, and transparent procurement processes—all requirements for listing that coincidentally made the company more competitive for large government contracts. The IPO on October 25, 2011, marked Shakti's entry into India's capital markets at an interesting moment. The listing date was October 25, 2011, when markets were still recovering from the 2008 crisis aftershocks and European debt concerns dominated headlines. Yet for a pump manufacturer from Madhya Pradesh with limited brand recognition among retail investors, the timing proved fortuitous—institutional investors were seeking exposure to India's infrastructure story, and Shakti represented a pure play on rural development.

The immediate post-IPO period tested management's ability to balance market expectations with operational realities. Public markets demanded quarterly performance, transparent communication, and growth narratives—foreign concepts for a company accustomed to multi-year government contracts and relationship-based business. The adjustment wasn't just financial; it was cultural. Board meetings shifted from operational discussions to strategic planning. Management information systems upgraded from tracking production to monitoring working capital cycles. Investor relations became a function, not an afterthought.

What emerged from this 2000-2011 period was a company fundamentally transformed yet still rooted in its core mission. International expansion hadn't diluted focus on Indian farmers; it had validated that Shakti's solutions worked globally. Product diversification hadn't scattered resources; it had created a portfolio serving the same customers more comprehensively. The IPO hadn't just raised capital; it had imposed disciplines that would prove crucial when government opportunities exploded in the coming decade.

By 2011's end, Shakti stood at an inflection point. It had manufacturing scale, international credibility, product breadth, and now public market access to capital. What it couldn't have known was that India's renewable energy revolution was about to begin—and a small-town pump manufacturer would find itself at the epicenter of a transformation that would reshape Indian agriculture. The foundation was built. The stage was set. The solar age was about to dawn.

IV. The Solar Revolution: PM-KUSUM & Government Push (2015–2020)

In 2015, when Prime Minister Modi announced India's ambitious renewable energy targets at the Paris Climate Summit—175 GW by 2022—most observers focused on utility-scale solar farms and rooftop installations. Few noticed a small line item about "solarization of agricultural pumps." Yet for Shakti Pumps, sitting on decades of pump manufacturing expertise and recently acquired capital market credibility, this represented the opportunity of a lifetime. The convergence of climate policy, agricultural economics, and energy security was about to transform their business in ways that traditional pump manufacturers could barely imagine.

India's renewable energy awakening wasn't just about global commitments—it was about brutal domestic realities. Over 30 million agricultural pumps consumed nearly 20% of India's electricity, most running on heavily subsidized power that states could no longer afford. Farmers faced erratic supply, often getting power only at night, forcing them to irrigate in darkness. State electricity boards bled money on agricultural subsidies while farmers suffered from unreliable irrigation. The solution seemed obvious in hindsight: replace electric pumps with solar ones. But execution would require manufacturers who understood both solar technology and the peculiarities of Indian farming.

As a channel partner for the Ministry of New & Renewable Energy (MNRE), Shakti Pumps developed a range of Solar pumps between 1HP to 100 HP that were simple and easy to operate, offering 40% more discharge than other ordinary pumps. This wasn't incremental product development—it was reimagining the pump from first principles. Traditional pumps were designed for consistent grid power; solar pumps needed to work with variable sunshine. Conventional pumps assumed trained operators; solar pumps needed to be farmer-proof. Standard pumps prioritized efficiency at optimal conditions; solar pumps needed resilience across diverse scenarios.

The technical challenges were substantial. Solar panels generate DC power; pumps traditionally run on AC. Solution: develop specialized controllers that could maximize water output across varying solar conditions. Solar power peaks at noon; irrigation needs vary by crop cycle. Solution: design systems that could pump to overhead tanks during peak sunshine for later use. Rural areas lack technical support; farmers can't troubleshoot complex electronics. Solution: build diagnostic systems simple enough that a phone call could resolve most issues.

Then came February 2019: the launch of Pradhan Mantri Kisan Urja Suraksha evam Utthaan Mahabhiyan (PM-KUSUM), a tongue-twister of a scheme that would reshape Indian agriculture. With targeted installation of 30,800 MW of solar capacity by 2022 and central financial assistance of 30-60%, this wasn't just policy—it was transformation at scale. The scheme created an estimated market of around Rs 105,000 crore for solar pumps in India, with states competing to maximize installations and manufacturers scrambling to build capacity.

Shakti's strategic positioning for PM-KUSUM revealed years of careful preparation finally paying off. While competitors rushed to form joint ventures with Chinese solar manufacturers or scrambled to understand agricultural applications, Shakti had already spent years developing solar pump technology specifically for Indian conditions. Their controllers could handle the voltage fluctuations common in rural areas. Their pumps were designed for the high silt content of Indian groundwater. Their service network already reached the villages where installations would happen. With Shakti Pumps holding a dominating market share of 30% under the PM-KUSUM scheme, the company had positioned itself as the go-to partner for state governments looking to implement the program.

Building capacity for massive scale became the operational challenge of 2019-2020. The state-of-the-art manufacturing facility expanded to an installed capacity of 5 lakh pumps per annum while maintaining its export operations to over 100 countries. But scale wasn't just about production—it was about ecosystem development. Training programs for installation teams who could work in remote areas. Quality control systems that could ensure reliability when service visits might take days. Supply chain management that could deliver to districts with limited transportation infrastructure. Financial systems that could handle the complex subsidy mechanisms where farmers paid 10%, state and center contributed 30% each, and banks financed the remaining 30%.

The competition landscape during this period revealed why Shakti won where others struggled. Large conglomerates entered with financial muscle but lacked ground-level understanding—their pumps failed in field conditions they hadn't anticipated. Chinese manufacturers offered cheaper products but couldn't navigate the complex stakeholder management required for government schemes. Regional players understood local markets but lacked the financial strength to handle delayed government payments. Shakti occupied the sweet spot: technically competent, financially stable, politically connected, and operationally experienced in exactly the markets where PM-KUSUM would roll out.

By 2020's end, as COVID began disrupting global supply chains, Shakti had established itself as synonymous with solar pumps in India's agricultural heartland. The company that once made 1,500 pumps annually was now shipping that many in three days. The transformation from mechanical pump manufacturer to renewable energy player was complete. But the real test—executing at scale during a global pandemic while government orders multiplied—was just beginning. The solar revolution had arrived; now came the challenge of delivering on its promise.

V. Inflection Point #1: COVID Crisis to Solar Boom (2020–2022)

March 24, 2020, 8 PM: Prime Minister Modi announces a nationwide lockdown with four hours' notice. In Pithampur, Shakti's factory floor fell silent. Workers rushed home to villages before transport shut down. Supply chains froze mid-shipment. Government offices—the source of most orders—closed indefinitely. For a company that had just positioned itself at the center of India's solar pump revolution, the timing couldn't have been worse. Or so it seemed.

The pandemic's initial impact was brutal. Manufacturing operations that required hundreds of workers on assembly lines couldn't function with social distancing. Component imports from China—solar panels, electronic controllers—stopped abruptly. Installation teams couldn't travel to villages where farmers waited for solar pumps. State governments, overwhelmed by health emergencies, suspended infrastructure programs. Revenue recognition halted as projects couldn't be commissioned. Working capital stretched as receivables extended but payables remained fixed. The carefully constructed growth story of 2019 seemed to evaporate overnight.

Yet within this crisis, subtle shifts were occurring that would transform temporary disruption into lasting opportunity. Rural India, less affected by COVID's first wave, saw reverse migration as millions returned from cities. These returning workers brought awareness of solar technology from urban exposure. State governments, recognizing agriculture's importance for economic recovery and food security, began prioritizing rural infrastructure. The central government, seeking to stimulate demand while supporting farmers, increased PM-KUSUM allocations. Most critically, the narrative shifted from solar pumps as climate solution to solar pumps as livelihood protection—a subtle but powerful reframing that accelerated adoption.

The operational transformation Shakti underwent during the pandemic months of 2020-2021 would define its next chapter. Unable to rely on traditional practices, the company digitized processes that had remained manual for decades. Installation training moved online, with WhatsApp becoming the primary support channel for field technicians. Quality control shifted from physical inspection to video verification. Order processing, historically requiring multiple government office visits, transformed into digital workflows. Customer service, previously limited to business hours, became 24/7 through automated response systems. These weren't temporary adjustments—they were permanent improvements that increased efficiency while reducing costs.

By late 2020, as India emerged from the first lockdown, something remarkable happened. States flush with central stimulus funds and focused on rural employment generation began announcing massive solar pump tenders. Maharashtra, Madhya Pradesh, Haryana—each trying to outdo others in installation targets. The extension of PM-KUSUM until March 2026 signaled government commitment despite pandemic pressures. Suddenly, the order pipeline that had dried up in March began flooding in by December. But this wasn't the gradual growth of previous years—this was a deluge that would test every aspect of Shakti's operations.

The company maintained around 30% market share in the domestic solar pump market under the PM KUSUM scheme during this tumultuous period, but maintaining share in an exploding market meant absolute volumes were multiplying. Manufacturing lines that had operated single shifts moved to round-the-clock production. The workforce, reduced during lockdown, needed rapid expansion—but now with COVID protocols adding complexity. Component procurement, already stressed by global supply chain disruptions, required daily crisis management. Installation capacity, the ultimate bottleneck, needed creative solutions like partnering with local electrical contractors and training rural youth.

The financial turnaround story of 2020-2022 reads like fiction, but the numbers are real. From negative ROE of -5.1% in FY20 to positive territory by FY21, then accelerating to double digits by FY22. Revenue growth resumed after the pandemic pause, but more importantly, margins expanded as operational efficiency improved and solar pump mix increased. Working capital management, forced to improve during the crisis, continued delivering benefits as the company learned to operate with leaner inventory and faster collections. The crisis had forced organizational muscle that good times might never have built.

Competition during this period took on different dynamics. Several players, unable to manage pandemic disruptions, exited the market. Others, particularly those dependent on imported components, struggled with cost escalations and supply uncertainties. Pure-play solar companies without agricultural expertise failed to execute rural installations. Traditional pump manufacturers without solar capabilities couldn't participate in tenders. Shakti's integrated approach—manufacturing both pumps and controllers, understanding both solar technology and agricultural applications—proved to be the winning combination.

By early 2022, as India declared victory over COVID's worst waves, Shakti emerged transformed. Not just survived but strengthened. Not just recovered but accelerated. The pandemic that threatened to derail the solar pump story had instead catalyzed it. Government commitment had deepened, farmer acceptance had accelerated, and Shakti's operational capabilities had evolved to handle complexity at scale. The crisis had become a crucible, and what emerged was a company ready for its next phase of growth. The stage was set for what would become an extraordinary period of order flow that would test the very limits of execution capability.

VI. Inflection Point #2: The Multi-State Order Bonanza (2023–2024)

October 2023 began like any other month in Shakti's Pithampur headquarters, with management reviewing quarterly results and planning capacity expansion. Then the phone rang. And rang again. And kept ringing. Within weeks, order confirmations would cascade in from multiple states, each worth hundreds of crores, transforming the company's trajectory in ways that spreadsheet projections had never captured. This wasn't gradual growth—this was step-change transformation compressed into quarters.

The first domino fell with an October 2023 announcement: ₹149.71 crore for replacing conventional electric pump sets with energy-efficient BLDC (brushless DC) solar pump sets. But the significance went beyond the order value. The accompanying statement revealed a paradigm shift in how governments viewed solar pumps: "This revolutionary action changes 'Annadata' (food providers) into 'Urjadata' (energy providers). Discoms would recover the pump set cost within 5 years, and farmers can earn substantial income by selling excess power to discoms." Solar pumps were no longer just irrigation tools—they were income generation assets.

Then came the Maharashtra mega-order, also in October 2023: 50,000 off-grid solar photovoltaic pumps worth ₹1,603 crore including GST. To understand the scale, consider that this single order represented more pumps than many manufacturers produced annually. Maharashtra, India's richest state and second-largest by area, was making a statement—solar pumps weren't pilot projects anymore but mainstream agricultural infrastructure. The order's structure revealed sophisticated thinking: off-grid systems that wouldn't strain existing electrical infrastructure while providing reliable irrigation to remote areas.

The momentum continued into 2024. August brought two major wins: Uttar Pradesh contracted 12,537 solar pumps worth approximately ₹558.16 crore ($66.65 million), while Jharkhand added ₹94 million under PM-KUSUM. Each state brought unique challenges. UP's vast Gangetic plains required pumps that could handle varying water tables. Jharkhand's tribal areas needed simple systems that could be maintained with minimal technical support. Maharashtra's diverse topology demanded pumps that worked efficiently from coastal Konkan to drought-prone Vidarbha. The ability to customize solutions while maintaining standardized production revealed operational sophistication built over decades.

The company maintained its leadership in the PM-KUSUM scheme with an estimated 25 per cent market share across major agricultural states, including Maharashtra, Madhya Pradesh, Rajasthan, Haryana, Punjab, Uttar Pradesh, and Jharkhand. But maintaining share while absolute volumes exploded required fundamental operational restructuring. Production planning transformed from monthly to daily cycles. Procurement expanded from single-source to multi-vendor strategies. Logistics evolved from truck-based to multi-modal transportation. Installation scaling meant training thousands of technicians across hundreds of districts simultaneously.

Execution capabilities at this scale separated winners from mere participants. Consider the Maharashtra order: 50,000 pumps meant roughly 200 installations daily for a year, across a state larger than Italy, in villages often lacking proper roads, requiring coordination with district collectors, agriculture departments, local banks, and village panchayats, while maintaining quality standards that could withstand government audits and farmer expectations. This wasn't manufacturing—this was orchestration of complex systems where a delay in any component could cascade into project penalties.

The financial impact was transformative. Between FY20 and FY24, the company reported 5-year CAGR in revenue and net profit of 20.2% and 25.2%, respectively. But these backward-looking numbers understated the forward momentum. Order books swelling to ₹1,800 crore by September 2024 provided visibility that most manufacturing companies could only dream of. More importantly, the order mix—dominated by government contracts with defined payment terms—reduced market risk while improving capital allocation decisions.

Project management evolution during this period deserves special attention. Shakti developed what could be called "industrial-strength project management"—systems robust enough to handle government bureaucracy yet flexible enough for ground realities. Each major order was broken into district-level projects with dedicated teams. Real-time dashboards tracked everything from component inventory to installation progress. WhatsApp groups connected field teams with technical support. Automated escalation systems flagged delays before they became critical. This wasn't software company agile; this was manufacturing company reliability scaled to infrastructure project complexity.

The human story within these numbers often gets lost. In villages across Maharashtra, farmers who had irrigated at night for decades suddenly had water during the day. In UP's bundelkhand region, where diesel pumps drained savings, solar pumps made farming viable again. In Jharkhand's tribal areas, reliable irrigation meant families didn't need to migrate for work. Each installed pump represented not just revenue for Shakti but transformation for rural communities—a responsibility the company took seriously, reflected in service response times and system reliability metrics that exceeded tender requirements.

By late 2024, as order execution continued at breakneck pace, Shakti had transformed from a pump manufacturer into an infrastructure solutions provider. The company that once celebrated single-crore orders now managed multi-hundred crore projects across multiple states simultaneously. The operational capabilities built during this period—project management, supply chain orchestration, stakeholder coordination—would prove valuable beyond solar pumps. Which perhaps explains why, even as solar pump orders dominated headlines, management quietly invested in what might become the next transformation: electric vehicles.

VII. The EV Pivot: Diversification or Distraction? (2021–Present)

December 16, 2021, marked an intriguing departure from script. While solar pump orders dominated earnings calls and investor presentations, Shakti quietly announced entry into electric vehicles through a wholly-owned subsidiary, Shakti EV Mobility Private Limited. The timing seemed odd—why divert focus when solar pumps were exploding? The answer lay in pattern recognition that only insiders could see: the same convergence of government policy, technological disruption, and market transformation that created the solar pump opportunity was beginning in electric vehicles.

The strategic logic, once examined closely, was compelling. The subsidiary would manufacture EV Motors with Controllers, Chargers, and VFD (Variable Frequency Drives) to optimize battery performance, leveraging Shakti group's 40 years of experience in making motors and 5 years of manufacturing Power Electronics Equipment. This wasn't random diversification—it was adjacent expansion into a market where core competencies transferred directly. Motors? Shakti had manufactured them for four decades. Controllers? Already designing sophisticated ones for solar pumps. Power electronics? Core to their solar pump technology. The technical synergies were obvious; the market synergies would emerge over time.

The investment trajectory revealed measured confidence rather than reckless ambition. ₹110 crore pledged over five years, with ₹32 crore infused initially. By February 2025, another ₹6 crore raised total investment to ₹45 crore—careful capital deployment that wouldn't strain the booming solar pump business while building optionality for the future. This wasn't betting the company; it was placing strategic chips on a trend too significant to ignore, in a market projected to grow at 49% CAGR between 2022 and 2030, reaching 10 million annual unit sales by decade's end.

The technology development within Shakti EV Mobility focused on pragmatic innovation rather than moonshot ambitions. The recent patent for "Stack Assembly for Permanent Magnet Rotor" addressed a specific challenge in EV motors: improving efficiency while reducing manufacturing complexity. This wasn't competing with Tesla on cutting-edge battery chemistry; it was solving bread-and-butter problems that Indian two- and three-wheeler manufacturers faced. The approach mirrored what worked in solar pumps: understand local requirements, design for local conditions, manufacture at competitive costs.

Early revenue numbers told a story of patient building rather than hockey-stick growth. As of March 31, 2024, the subsidiary had total assets valued at ₹372.39 crore and turnover of ₹43.09 crore. These weren't transformative numbers—yet. But for students of Shakti's history, they echoed the early days of solar pumps: small revenue, significant investment, careful capability building, waiting for the market moment. The difference now was that Shakti had capital, credibility, and confidence earned from the solar pump success.

The market opportunity in EV components revealed interesting dynamics. While headlines focused on passenger vehicles and companies like Ola Electric, the real volume in India would come from two- and three-wheelers—the workhorses of last-mile delivery, urban commuting, and small goods transportation. These vehicles needed robust, cost-effective motors that could handle Indian conditions: heat, dust, overloading, minimal maintenance. Exactly the kind of engineering challenge Shakti had solved before in pumps. The customers were different, but the value proposition remained consistent: reliability at reasonable cost.

Risk management in this diversification showed institutional maturity. The subsidiary structure insulated the core business from EV-related risks. Investment was staged rather than front-loaded. Technology development focused on components rather than complete vehicles, reducing capital requirements and market risk. Customer development began with smaller contracts, building credibility before pursuing larger opportunities. This wasn't the playbook of venture-funded startups; it was the approach of a profitable company extending into adjacent markets.

The potential synergies extended beyond obvious technical overlaps. Government relationships built through solar pumps could facilitate EV component supply to state transport undertakings. Manufacturing expertise in electronics and motors applied directly. Quality certifications and export capabilities transferred seamlessly. Even seemingly unrelated capabilities—like managing working capital in government contracts—would prove valuable in the EV space where payment cycles could be extended.

Industry observers began speculating about a potential demerger to unlock value, especially after the company announced a 5:1 bonus issue. Separating solar pumps from EV operations could theoretically create two focused entities, each with distinct valuations appropriate to their growth profiles and risk characteristics. The solar pump business, with established market position and steady government orders, might command infrastructure-like multiples. The EV subsidiary, with higher growth potential but greater uncertainty, could attract growth capital at technology valuations.

By 2024, while solar pumps still dominated revenue and profits, the EV initiative had evolved from experiment to serious second act. The subsidiary was no longer just manufacturing components but developing integrated solutions for specific vehicle segments. Partnerships with OEMs were progressing from trials to commercial contracts. The technology portfolio expanded from motors to complete powertrain solutions. What started as diversification was beginning to look like transformation.

The question—diversification or distraction—had an emerging answer: neither. It was evolution. Just as Shakti evolved from mechanical pumps to solar solutions when the market shifted, it was now preparing for the next energy transition. The company that understood how to help farmers move from diesel to solar was positioning to help transporters move from petrol to electric. Different products, same insight: energy transitions create infrastructure opportunities, and those who build capabilities before the market fully develops capture disproportionate value when it does.

VIII. Modern Operations & Global Expansion (2023–Present)

Inside Shakti's Pithampur facility in 2024, the contrast with that original 1982 unit couldn't be starker. Where manual assembly once produced 1,500 pumps annually, automated lines now churned out that many in days. The state-of-the-art manufacturing facility with installed capacity of 5 lakh pumps per annum represented not just scale but sophistication—IoT sensors tracking production efficiency, AI-powered quality control systems, and digital twins optimizing assembly sequences. Yet amidst this technology, the core philosophy remained unchanged: build products that work in India's toughest conditions.

The product portfolio expansion to over 1,200 indigenously developed products revealed systematic market coverage rather than random proliferation. Each product addressed specific use cases: shallow well pumps for Bengal's high water tables, high-head submersibles for Rajasthan's deep aquifers, corrosion-resistant models for coastal areas, silt-handling variants for Gangetic plains. This wasn't catalog padding—it was precision engineering for India's diverse hydrogeology. The R&D investment of 3-4% of net profits consistently plowed back into development showed commitment to innovation that went beyond marketing rhetoric.

Export performance continued as a significant growth driver, with approximately 25% CAGR over the past four years, contributing roughly 25% to total revenue. But the export story had evolved from opportunistic sales to strategic market development. Operations in more than 100 countries weren't just pins on a map—they represented careful selection of markets with similar agricultural conditions to India. African countries facing water scarcity found Shakti's drought-resistant pumps invaluable. Middle Eastern farms dealing with high salinity appreciated the corrosion resistance. Latin American smallholders valued the simple maintenance requirements.

The distribution architecture—over 300 dealers across India—had transformed from traditional wholesale relationships to partnership ecosystems. Dealers weren't just order-takers but solution providers, trained in system design, equipped with configuration tools, and supported by technical teams. In export markets, the approach adapted to local requirements: direct presence in key countries, distributors in others, and project-based engagement for large installations. This wasn't one-size-fits-all distribution but carefully calibrated market access strategies.

Working capital management emerged as an unexpected competitive advantage. Receivable days improved from 178 in FY24 to 152 in FY25, with further reduction to 120 days targeted by FY26. In a business dominated by government contracts with notoriously slow payments, this improvement released hundreds of crores for growth investment rather than financing receivables. The techniques were prosaic but powerful: better documentation reducing payment disputes, dedicated government liaison teams expediting approvals, and selective factoring for large receivables without recourse.

Digital transformation, accelerated during COVID, had become embedded in operations. Every pump now carried QR codes linking to installation videos and service history. Field service teams used mobile apps for diagnostics and spare parts ordering. Farmers could register complaints through WhatsApp and track resolution in real-time. Production planning integrated with supply chain management, automatically adjusting procurement based on order pipeline. This wasn't digitization for its own sake but technology solving real operational friction.

The quality evolution from ISI certification in 1991 to current international standards reflected journey from local manufacturer to global supplier. ISO certifications were table stakes; the real differentiation came from product reliability in extreme conditions. Mean Time Between Failures (MTBF) for Shakti pumps exceeded industry averages by 30-40%, reducing lifecycle costs even if initial prices were higher. This reliability premium, invisible in tender L1 pricing, became evident in repeat orders and word-of-mouth recommendations.

Manufacturing excellence extended beyond the factory floor to supply chain orchestration. Single-source dependencies that could have crippled production during COVID were eliminated through vendor development programs. Local suppliers were trained and certified, reducing logistics costs while improving response times. Critical components had buffer stocks calibrated by algorithm rather than intuition. The entire supply chain was stress-tested quarterly, identifying vulnerabilities before they became crises.

The human capital story within this operational transformation often goes unnoticed. The company that started with dozens of workers now employed thousands, but more importantly, it had evolved from providing jobs to building careers. Engineers recruited from tier-2 colleges found themselves managing multi-crore projects within years. Diploma holders from industrial training institutes became production supervisors overseeing sophisticated automation. Rural youth trained as installation technicians earned more than many urban graduates. This wasn't corporate social responsibility—it was building capabilities where they were needed.

Sustainability initiatives, initially driven by compliance, had evolved into competitive advantage. Solar panels powered 30% of factory operations. Water recycling systems reduced consumption by 40%. Packaging moved from plastic to biodegradable alternatives. Even pump designs optimized for recyclability, anticipating regulations that didn't yet exist. International customers, particularly in Europe, increasingly valued these credentials in vendor selection. What started as cost actually became revenue enabler.

The modern Shakti Pumps of 2024 bore little resemblance to its 1982 ancestor except in one crucial aspect: obsessive focus on solving customer problems. Technology, scale, and sophistication were means, not ends. The company that once helped farmers irrigate fields now helped them generate income from solar power. The manufacturer that started with simple submersibles now produced sophisticated systems integrating IoT monitoring and remote diagnostics. Yet at its core, success still came from understanding that in India, products must work not in laboratories but in fields, not in ideal conditions but in reality, not for trained operators but for everyday users.

IX. Financial Performance & Market Position

The numbers tell a story of transformation so dramatic that they strain credibility—until you examine the underlying drivers. From revenue of ₹841.93 crore in FY2022-2023, growing 22.78% to reach ₹2,571 crore by 2024, with profits surging to ₹413 crore. The market cap crossing ₹10,208 crore represented a valuation multiple that would have seemed fantasy just years earlier. Yet behind these headlines lay a more nuanced narrative of operational excellence translating into financial outperformance.

The profitability transformation from FY20 to FY24 reads like a textbook turnaround. ROE improving from negative 5.1% to 24.2%. ROCE rising from negative 0.2% to 31.5%. These weren't cosmetic improvements through financial engineering—they reflected fundamental operational changes. Higher margin solar pumps replacing commodity mechanical pumps. Government contracts providing predictable cash flows. Export markets offering better realizations. Working capital efficiency releasing trapped value. Each percentage point of improvement represented countless operational decisions compounding over time.

The stock performance—196.4% return in one year—captured market recognition of this transformation, but also revealed interesting dynamics about investor perception. Trading at a P/E ratio of 30x, above its 5-year median of 24.4x, suggested markets were pricing in continued growth rather than just celebrating past performance. The 5:1 bonus issue announced in 2024, combined with ₹1 dividend per share, signaled management confidence while improving stock liquidity for retail investors who had largely missed the institutional accumulation phase.

Order book strength provided unusual visibility for a manufacturing company. Outstanding orders around ₹1,800 crore as of September 2024 represented nearly 9-10 months of revenue visibility—luxury in a sector where most companies operated with 2-3 month pipelines. But order books told only part of the story. The quality of orders—government contracts with sovereign guarantee, export orders with letters of credit, repeat customers with payment history—mattered more than quantum. This wasn't speculative backlog but executable pipeline.

The revenue mix evolution revealed strategic positioning paying off. Domestic government sales under PM-KUSUM provided volume and stability. Exports offered currency hedge and margin premium. Aftermarket services generated recurring revenue with minimal capital employed. The emerging EV business, while still small, added growth optionality. This portfolio approach—different segments contributing different values—reduced concentration risk while maintaining focus on core competencies.

Cash flow characteristics had transformed from typical manufacturing patterns to something resembling infrastructure assets. Operating cash flows turned consistently positive. Capital expenditure, while substantial for capacity expansion, was self-funded rather than debt-dependent. Working capital cycles, though extended due to government payments, were predictable and manageable. Free cash flow generation allowed simultaneous investment in growth and returns to shareholders—a balance few achieved.

The margin story went beyond gross numbers to reveal operational leverage at work. Fixed costs spread across higher volumes. Procurement scale driving better component pricing. Vertical integration capturing value previously leaked to suppliers. Service revenue with 40%+ margins mixing favorably. Even transportation costs per unit decreased as route optimization and load consolidation improved. These weren't one-time gains but structural improvements that would sustain unless volumes collapsed.

Peer comparison revealed Shakti's unique position. Against traditional pump manufacturers, it showed superior growth and margins due to solar mix. Compared to solar EPC players, it demonstrated better return ratios through manufacturing focus. Versus infrastructure companies, it offered higher growth with similar cash flow stability. This categorical ambiguity—industrial manufacturer, renewable energy player, infrastructure provider—made conventional valuation frameworks challenging, contributing to valuation dispersion among analysts.

The demerger speculation added another dimension to financial analysis. If solar pumps and EV operations separated, combined valuations might exceed consolidated entity due to pure-play premiums and distinct investor bases. Solar pumps could attract infrastructure funds seeking stable yields. EV business might appeal to growth investors willing to accept J-curve returns. The bonus issue, improving float, potentially prepared for such restructuring, though management remained noncommittal.

Capital allocation decisions revealed evolving sophistication. Growth capex focused on debottlenecking rather than greenfield expansion. Technology investments emphasized automation and digitization over capacity addition. EV subsidiary funding stayed measured despite market excitement. Dividend policy balanced retention for growth with shareholder returns. Even small decisions—like maintaining higher cash despite borrowing facilities—showed risk management maturity earned through cycles.

By late 2024, Shakti's financial position represented more than just strong numbers—it reflected a business model that had found product-market fit at scale. Government relationships provided demand visibility. Manufacturing excellence ensured execution capability. Financial strength enabled working capital funding. Technical competencies created competitive moats. The convergence of these factors, built over decades but crystallizing in recent years, explained why a pump manufacturer from Madhya Pradesh traded at multiples typically reserved for technology companies.

X. Playbook: Business & Strategy Lessons

The Shakti Pumps story offers a masterclass in building industrial businesses in India, with lessons that extend far beyond pumps or solar panels. The playbook that emerges isn't about brilliant moves or breakthrough innovations but about patient building, strategic positioning, and relentless execution in unglamorous sectors where others saw only commoditization.

Government Partnership as a Moat

While others viewed government contracts as bureaucratic nightmares with delayed payments, Shakti recognized them as strategic assets worth cultivating. The insight: government business in India isn't just about L1 pricing but about trust, earned through decades of reliable delivery. Every successful execution became a reference for the next tender. Every relationship with district collectors and department secretaries compounded into network effects. The moat wasn't technology or capital but reputation—impossible to replicate quickly, invaluable when multi-hundred crore contracts were awarded.

Building for Bharat: Rural-First Product Strategy

Shakti understood something Silicon Valley often misses: India isn't a market but multiple markets with dramatically different needs. Their rural-first approach meant products designed for users who might be illiterate, service networks reaching villages without proper roads, and pricing models accommodating seasonal agricultural income. While competitors designed for urban showcase installations, Shakti optimized for rural reality. This wasn't corporate social responsibility but hard-nosed strategy—rural markets offered volume, government support, and competitive insulation that urban markets never could.

Capital Efficiency in a Capital-Intensive Business

Manufacturing pumps requires significant fixed investment, yet Shakti achieved returns that asset-light businesses would envy. The secret lay in systematic capital allocation. Capacity additions were modular, expanding only after demand was proven. Technology investments focused on productivity over prestige. Working capital optimization released funds without dilution. Even facility locations—in SEZs with tax benefits, near component suppliers, accessible to target markets—reflected capital consciousness. The discipline to say no to empire building while saying yes to strategic investment separated Shakti from peers who confused scale with success.

Managing Cyclicality Through Diversification

Agricultural demand, government spending, and rural income—all cyclical factors affecting Shakti's business. The response wasn't hoping for stability but building portfolio resilience. Domestic and export markets moved on different cycles. Solar pumps and mechanical pumps served different segments. Government and retail sales had distinct dynamics. The EV initiative added another uncorrelated stream. This wasn't random diversification but calculated portfolio construction, ensuring that when one segment slowed, others could compensate.

Export as a Hedge Against Domestic Policy Changes

The decision to build export capabilities when domestic demand was sufficient seemed unnecessary—until it wasn't. Export markets provided currency hedging when the rupee depreciated. International standards forced quality improvements that benefited domestic products. Global exposure brought technology awareness before local competition recognized trends. Most critically, export revenue provided stability when domestic policies shifted—a insurance policy whose premium was paid through patient market development over decades.

The Demerger Option Value

The speculation about potential demerger reveals sophisticated corporate strategy. By maintaining clear subsidiary structures while building distinct businesses, management created optionality without commitment. If markets rewarded focus, they could separate. If synergies dominated, they could integrate further. This structural flexibility—unusual for traditional manufacturers—showed learning from modern corporate finance while respecting operational realities. The bonus issue improving float, the subsidiary maintaining separate financials, the careful communication about distinct businesses—all preserved options for future value creation.

Execution at Scale

The ability to execute thousands of installations across multiple states simultaneously wasn't built overnight. It required systems thinking that went beyond manufacturing. Project management capabilities borrowed from construction companies. Supply chain orchestration learned from FMCG players. Service networks inspired by automotive models. Training systems adapted from IT services. Shakti became a learning organization, absorbing best practices from diverse industries and adapting them to their context.

Brand Building in B2B and B2G Markets

"Shakti" became synonymous with reliability in markets where brand seemingly didn't matter. The strategy was subtle but effective. Every pump carried visible branding that farmers would see daily. Service technicians wore uniforms that stood out in villages. Success stories were shared in regional languages through WhatsApp. Government engineers were invited to factory visits. Awards and certifications were prominently displayed. This wasn't consumer marketing but reputation building—slower but more durable in markets where word-of-mouth determined success.

Technology Adoption: Fast Follower Advantage

Shakti rarely pioneered technology but excelled at adaptation. Solar pumps weren't their invention, but they perfected them for Indian conditions. IoT monitoring wasn't novel, but their implementation was pragmatic. Digital payments weren't revolutionary, but their adoption was comprehensive. This fast-follower approach avoided bleeding-edge risks while capturing proven benefits. The discipline to wait until technology was ready, then move decisively, proved more valuable than first-mover advantage.

Lessons in Stakeholder Management

Success in Indian infrastructure requires managing complex stakeholder matrices. Shakti mastered this through systematic engagement. Government relations went beyond Delhi to district levels. Farmer feedback was collected through dealers, not surveys. Banking relationships were cultivated before capital was needed. Employee development created internal ambassadors. Investor communication balanced transparency with conservatism. Each stakeholder was understood, engaged, and aligned—creating ecosystem support that competitors couldn't quickly replicate.

The playbook that emerges isn't about disruption but about evolution, not about shortcuts but about patience, not about brilliance but about consistency. In markets where others saw commoditization, Shakti found differentiation. Where others avoided complexity, they built capabilities. Where others chased quick returns, they invested for decades. The result: a business that looks simple from outside but reveals sophisticated strategy upon examination—perhaps the ultimate moat in transparent markets.

XI. Bear vs. Bull Case & Future Outlook

Bull Case: The Convergence Continues

The optimistic view for Shakti Pumps rests on multiple growth drivers converging simultaneously. Management's guidance of 25-30% revenue growth in FY26, sustained over the next 3-4 years, seems achievable given the order book visibility and market dynamics.

PM-KUSUM's extension until March 2026 is just the beginning. With only 10-15% of India's agricultural pumps currently solarized, the addressable market remains enormous. State governments, facing fiscal pressure from power subsidies and climate commitments, have no choice but to accelerate solar pump adoption. The economic logic—farmers saving on diesel/electricity, states reducing subsidy burden, discoms improving financial health—creates irreversible momentum. Shakti's established position as the trusted partner makes them the default beneficiary.

The export opportunity is entering a new phase. Climate change and water scarcity are global phenomena, making efficient irrigation critical worldwide. Shakti's products, battle-tested in India's harsh conditions, are perfectly suited for emerging markets in Africa, Asia, and Latin America. As these countries develop agricultural policies similar to India's, Shakti's experience navigating government programs becomes invaluable competitive advantage. Export revenue growing at 25% CAGR could accelerate as international climate funding flows toward agricultural adaptation.

The EV business represents optionality with asymmetric upside. If India's two-wheeler electrification follows China's trajectory, the component market will explode. Shakti's focus on motors and controllers—the highest value components after batteries—positions them to capture significant value without the capital intensity of vehicle manufacturing. Early customer wins, patent development, and manufacturing capability suggest this isn't speculation but strategic preparation for an inevitable transition.

Operational improvements have further runway. Working capital days reducing to 120 could release hundreds of crores for growth investment. Automation and digitization are still in early stages, with potential for margin expansion as processes optimize. Service revenue, currently small, could become significant as installed base grows and pumps require maintenance. Each improvement compounds, creating a virtuous cycle of profitability enabling investment driving growth.

The demerger possibility adds another dimension of value creation. Separate entities could unlock 30-50% valuation upside as focused businesses attract appropriate investors. The solar pump business could re-rate as an infrastructure play with stable cash flows. The EV subsidiary could command technology multiples with growth potential. Even without demerger, the optionality creates a floor on valuations as activists or strategic buyers might force value realization.

Bear Case: The Risks Accumulate

The pessimistic view acknowledges multiple risks that could derail the growth story, some within management control but many external.

Government dependency is the obvious vulnerability. PM-KUSUM could face budget constraints as fiscal priorities shift. State governments, notorious for payment delays, might stretch working capital beyond manageable levels. Policy changes—subsidy reduction, tender modifications, or preference shifts—could disrupts business model overnight. The concentration risk is real: government contracts dominate revenue, and government is an unpredictable customer.

Competition is intensifying from multiple directions. Large conglomerates like Tata and Adani are entering renewable energy aggressively, with capital and political connections that Shakti can't match. Chinese manufacturers, temporarily constrained by import restrictions, might find ways to enter through local assembly or partnerships. Regional players are upgrading capabilities, competing for the same tenders with local political advantages. The 30% market share might prove to be peak rather than sustainable position.

The EV business remains unproven despite investment and promises. Technology risk is real—battery chemistry evolution could make current motor designs obsolete. Customer concentration with few OEMs creates vulnerability. Competition from established auto component manufacturers with deeper pockets and relationships could marginalize Shakti's offerings. The subsidiary bleeding cash while solar pump profits subsidize experiments might frustrate investors expecting capital efficiency.

Valuation concerns are legitimate with the stock trading at 30x P/E, above historical averages. Any disappointment—order delays, execution challenges, or margin pressure—could trigger significant correction. The retail investor enthusiasm that drove recent gains might reverse quickly if momentum breaks. Institutional investors, attracted by the growth story, might retreat if quality of earnings deteriorates or governance concerns emerge.

Execution risks multiply with scale. Managing thousands of installations across multiple states strains organizational capability. Quality issues, inevitable at this scale, could damage reputation built over decades. Working capital stretched by government delays might force expensive financing. Key person dependency, with founding family still controlling operations, creates succession uncertainties. Even small execution failures could cascade into larger crises given the operational complexity.

Future Catalysts: Known and Unknown

Several near-term catalysts could swing the narrative either direction:

Solar manufacturing integration could transform economics if import restrictions on Chinese panels continue. Backward integration into panel assembly or partnership with domestic manufacturers might improve margins while ensuring supply security. Conversely, any liberalization of solar imports could pressure margins as Chinese competition returns.

The EV subsidiary reaching profitability would validate the diversification strategy and potentially trigger re-rating. Customer announcements, particularly with marquee OEMs, could shift perception from experiment to growth driver. However, continued losses might force difficult decisions about additional investment or strategic alternatives.

The potential demerger remains the wildcard. If announced, it could unlock immediate value as separate entities attract focused investors. If rejected, it might disappoint speculators while allowing operational synergies to continue. The decision timing and structure would significantly impact near-term stock performance.

New government schemes beyond PM-KUSUM could open additional markets. Programs for drinking water supply, urban infrastructure, or industrial applications might leverage Shakti's capabilities in new segments. Alternatively, policy focus shifting from hardware subsidies to service delivery might reduce order flow.

The broader narrative—India's infrastructure build-out, renewable energy transition, and agricultural transformation—supports long-term optimism despite near-term uncertainties. Shakti sits at the intersection of multiple megatrends, with capabilities built over decades that new entrants can't quickly replicate. Whether this positioning translates into sustained outperformance depends on execution excellence, strategic choices, and external factors beyond anyone's complete control.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube