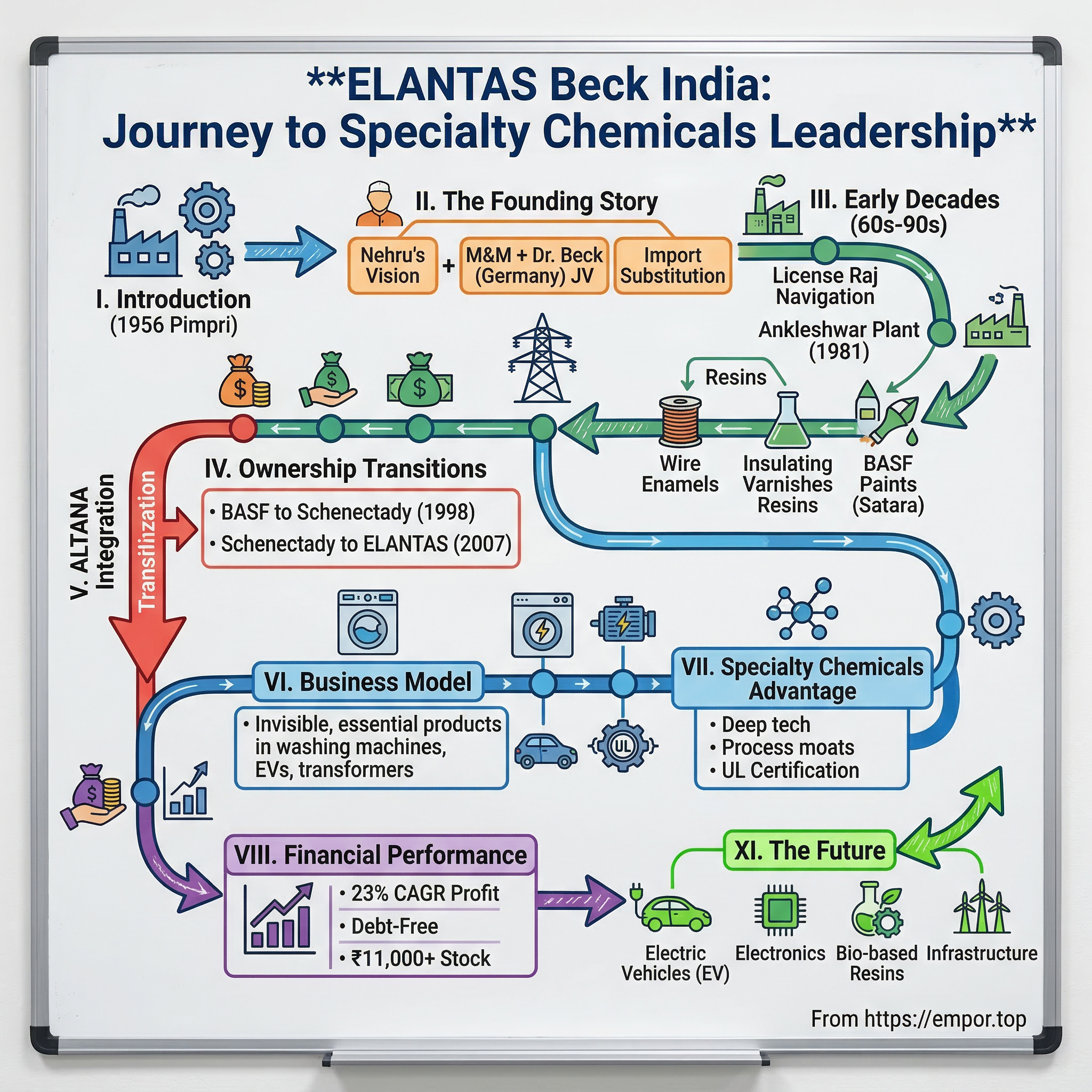

ELANTAS Beck India: From Post-Independence Manufacturing to Specialty Chemicals Leader

I. Introduction & Episode Roadmap

Picture this: A nondescript industrial compound in Pimpri, just outside Pune, 1956. The monsoon has just broken, and the air hangs heavy with the promise of rain and something else—the sharp, distinctive smell of chemical resins being heated for the first time in a brand-new factory. Inside, German technicians in crisp white coats work alongside Indian engineers, their conversations a mixture of broken English, technical German, and animated hand gestures. They're not just mixing chemicals; they're literally coating the wires that will power independent India's industrial dreams.

This is where our story begins—not in a gleaming corporate boardroom or a venture capital pitch deck, but in the crucible of post-independence India's manufacturing ambitions. Today, that modest factory has evolved into ELANTAS Beck India Limited, a ₹7,571 crore market cap specialty chemicals powerhouse that commands the electrical insulation market with the quiet confidence of a chess grandmaster who sees ten moves ahead.

The question that drives our narrative isn't just how a 1956 Indo-German collaboration survived the License Raj, multiple ownership changes, and the liberalization tsunami to emerge as India's electrical insulation leader. It's something more fundamental: How does a company making products so specialized that 99% of people have never heard of them—wire enamels, impregnating resins, potting compounds—become absolutely indispensable to everything from your washing machine to the electric vehicle revolution?

Here's what we'll unpack over the next several hours: We'll journey through the Nehruvian socialism that birthed this venture, when Mahindra & Mahindra saw an opportunity to partner with Dr. Beck & Company of Hamburg. We'll explore how technical expertise crossed continents in an era before email, how the company navigated the labyrinthine License Raj while building cutting-edge chemical formulations, and how it managed the delicate dance of ownership transitions—from BASF to Schenectady to finally finding its home within ALTANA's global empire.

The business itself breaks down into two primary segments that might sound mundane but are actually fascinating once you understand what they enable. First, electrical insulation systems—the invisible heroes that prevent every electric motor, transformer, and generator from becoming an expensive paperweight. Second, construction chemicals—the compounds that ensure skyscrapers don't leak and bridges don't corrode. Both segments share a common thread: they're the kind of unsexy, mission-critical products that nobody thinks about until they fail catastrophically.

What makes ELANTAS Beck India particularly intriguing from an investment perspective isn't just its 23% ROCE or its debt-free balance sheet—metrics that would make any value investor's pulse quicken. It's the company's position at the intersection of three massive secular trends: India's infrastructure buildout, the global energy transition, and the reshoring of critical supply chains. This is a business that benefits whether India builds coal plants or solar farms, whether cars run on petrol or batteries, whether factories make smartphones or washing machines.

As we dive deep into this story, we'll discover how a company can maintain 55+ P/E ratios in a supposedly commoditized industry, why German Mittelstand philosophy works brilliantly in Indian B2B markets, and what happens when you combine Teutonic technical precision with Indian entrepreneurial adaptability. We'll also confront the uncomfortable questions: Why did profits drop 20% last quarter? Is the valuation justified? And can a company with 75% promoter holding truly serve minority shareholders?

But first, let's return to 1956, to understand how a newly independent nation's hunger for industrial self-sufficiency created the perfect conditions for an unlikely partnership between Bombay industrialists and Hamburg chemists.

II. The Post-Independence Founding Story (1956)

The telegram arrived at Mahindra & Mahindra's Bombay headquarters on a humid March morning in 1956. "TECHNICAL COLLABORATION APPROVED STOP PROCEED WITH INCORPORATION STOP" It was the green light that Keshub Mahindra had been waiting for—permission from Nehru's government to establish a joint venture with Dr. Beck & Company GmbH of Hamburg, Germany. In an India barely nine years free from colonial rule, where every factory license required navigating a byzantine approval process, this was no small victory.

The timing was no accident. Jawaharlal Nehru's vision of a modern, industrialized India had crystallized into the Second Five Year Plan, launched that very year with its ambitious focus on heavy industries and import substitution. The plan allocated an unprecedented ₹4,800 crores for industrial development, with electrical infrastructure as a cornerstone. Every new power plant, every factory, every electric motor needed insulation materials—and India was importing virtually all of it.

Dr. Beck & Company wasn't a household name even in Germany, but in the rarefied world of electrical insulation, they were royalty. Founded in 1901, the Hamburg-based firm had spent five decades perfecting the chemistry of wire enamels—those impossibly thin coatings that allow copper wires to conduct electricity without short-circuiting when wound tightly together in motors and transformers. Their formulations were trade secrets, passed down through generations of chemists like medieval guild knowledge.

The collaboration structure was fascinating for its time. Mahindra & Mahindra would provide the local knowledge, government connections, and initial capital. Dr. Beck would transfer not just technology but actual German technicians who would live in India for years, training local chemists in the dark arts of resin polymerization and enamel formulation. The equity structure gave Mahindra the majority, satisfying nationalist sentiments, while ensuring Beck retained enough stake to guarantee continued technical support.

On March 15, 1956, ELANTAS Beck India Limited was officially incorporated—though it would operate under different names over the decades. The first manufacturing plant was commissioned that same year in Pimpri, strategically located near Pune's emerging industrial belt. The choice of location was deliberate: close enough to Bombay's port for importing raw materials, near the technical talent emerging from Pune's engineering colleges, and critically, adjacent to the Kirloskar and Bajaj factories that would become early customers. The genesis of the wire enamel business wasn't just about technology transfer—it was about timing a perfect market entry. The Company was promoted by Mahindra & Mahindra in collaboration with Dr Beck & Company, Germany, and commissioned its first manufacturing plant in 1956 at Pimpri. In 1956, India's electrical grid was expanding at breakneck pace. The Bhakra-Nangal dam project, Asia's second-largest at the time, was under construction. The Chittaranjan Locomotive Works had just begun producing India's first electric locomotives. Every one of these projects needed miles and miles of insulated wire.

The early product portfolio was deliberately narrow but deep. Wire enamels came first—those amber-colored liquids that, when applied to copper wire and baked at precisely controlled temperatures, created a molecular-thin insulation layer capable of withstanding 200°C without degrading. The chemistry was deceptively complex: polyester resins modified with glycols, carefully balanced catalysts, solvents that evaporated at just the right rate. One wrong temperature spike during synthesis and an entire batch worth lakhs would turn into expensive waste.

The German technicians who arrived in Pimpri brought more than formulas. They brought a culture of precision that bordered on obsession. Dr. Hans Mueller, the first technical director, was known to personally inspect every batch, running the enamel through his fingers to check viscosity, holding glass slides to the light to examine film clarity. This wasn't mere fastidiousness—in an era before sophisticated quality control instruments, human senses were often the most reliable gauge of product quality.

The company went public in 1961, just five years after incorporation—a remarkably quick transition that spoke to both the venture's early success and the capital requirements of scaling chemical manufacturing. The IPO prospectus, a slim document by today's standards, pitched a simple story: India needs electrical infrastructure, electrical infrastructure needs insulation, and we're the only ones who know how to make it locally.

By the end of the 1950s, the Pimpri plant was producing not just wire enamels but also insulating varnishes—those thick, resinous coatings that protected motor windings from moisture and contamination. These included wire enamels, insulating and finishing varnishes, and resins for impregnation of electric motors. The product might have been invisible to end users, but it was everywhere: in the ceiling fans beginning to appear in middle-class homes, in the water pumps irrigating Punjab's green revolution, in the generators powering textile mills in Ahmedabad.

What's remarkable about this founding period is how it established patterns that would define the company for decades. The focus on technical excellence over marketing flash. The patient building of customer relationships in unglamorous industrial segments. The willingness to invest in capabilities years before market demand materialized. These weren't conscious strategic choices as much as cultural DNA inherited from both the Mahindra ethos of industrial nation-building and German Mittelstand values of technical perfectionism.

As India entered the 1960s, with Nehru's vision of commanding heights under strain and geopolitical tensions rising, ELANTAS Beck India had established itself as that rarest of entities: a successful technology transfer that actually transferred technology. The stage was set for three decades of steady expansion, navigating the labyrinth of industrial licensing while quietly becoming indispensable to India's industrial economy.

III. Building the Foundation: The Early Decades (1960s–1990s)

The letter from the Ministry of Industries arrived on a sweltering June day in 1978, bearing the seal of the License Raj at its most byzantine. ELANTAS Beck India had applied to expand production capacity by 2,000 metric tons—a modest increase that would require new reactors, storage tanks, and quality control equipment. The response ran to 47 pages, demanding clarifications on everything from foreign exchange implications to the caste composition of proposed new hires. It would take eighteen months and three trips to Delhi before approval finally came through. This was the reality of building a specialty chemicals business in socialist India: for every hour spent on chemistry, two were spent on paperwork.

Yet somehow, the company thrived. The secret lay in a strategy so simple it sounds naive in retrospect: become so technically indispensable that even bureaucrats couldn't say no. When the heavy electrical equipment manufacturer BHEL needed special high-temperature varnishes for their turbine generators, only ELANTAS Beck could formulate them. When Indian Railways required wire enamels that could withstand the brutal heat and humidity of locomotive engines, the Pimpri laboratory delivered formulations that outperformed imported alternatives.

The technical expertise transfer from Germany continued throughout the 1960s and 1970s, but it evolved from wholesale technology import to collaborative innovation. The Pimpri laboratory, initially staffed by two German chemists and five Indian engineers, had grown to a team of thirty by 1975, all Indian. They weren't just following German formulations anymore—they were adapting them for Indian conditions. European wire enamels, designed for temperate climates, would often fail in Indian summers where factory floors could reach 45°C. The Indian team developed heat-stable variants, adjusting catalyst systems and solvent blends through hundreds of iterations.

In 1981, the second modern plant was set up at Ankleshwar in Gujarat, to cater to the increasing market demand for insulating materials. The choice of Ankleshwar was strategic—Gujarat's chemical belt offered proximity to raw material suppliers, ports for imports, and a state government somewhat less allergic to private enterprise than others. The new plant specialized in high-volume products, while Pimpri focused on specialized formulations and R&D.

The collaboration landscape expanded significantly when the company collaborated with BASF Lacke and Farben Germany to manufacture paints at Satara. This wasn't just another technical partnership—it represented a diversification into construction chemicals, a market that would become increasingly important in later decades. The Satara facility produced specialized coatings for industrial applications: anti-corrosive paints for chemical plants, fire-retardant coatings for steel structures, waterproofing compounds for concrete.

Product development during this period read like a taxonomy of industrial India's needs. Traction varnishes for railway locomotives. Hermetic sealing compounds for refrigerator compressors. Slot insulation for hydro generators. Each product required months of development, working closely with customers to understand not just specifications but actual operating conditions. The company's engineers would spend weeks at customer plants, watching motors fail, analyzing burnt windings, understanding why insulation systems that worked perfectly in the lab would break down in the field.

The numbers tell a story of steady, unglamorous growth. Production capacity increased from 500 metric tons in 1960 to 8,000 metric tons by 1990. The product portfolio expanded from 5 basic formulations to over 200 specialized products. Customer base grew from a handful of large electrical equipment manufacturers to hundreds of companies across sectors. But perhaps the most important metric was one that didn't appear in annual reports: the company had become the repository of India's institutional knowledge in insulation chemistry.

Navigating the License Raj required a particular kind of corporate athleticism. When import licenses for key raw materials were denied, the company learned to synthesize them locally. When expansion permits were rejected, they found ways to increase productivity within existing capacity through process optimization. When foreign exchange restrictions limited technology imports, they developed indigenous alternatives. Each constraint became a catalyst for innovation.

The relationship with labor was remarkably stable for the era. While other companies faced strikes and lockouts, ELANTAS Beck India maintained industrial peace through a combination of German-style apprenticeship programs, profit-sharing schemes that predated ESOP culture by decades, and a genuine commitment to skill development. Many workers who joined as helpers in the 1960s retired as senior technicians in the 1990s, their children often following them into the company.

Quality certifications became a competitive weapon. The company was among the first in India's chemical sector to obtain ISO 9001 certification in 1994, a process that required documenting every process, standardizing every procedure, and training every operator. What seemed like bureaucratic overhead actually crystallized decades of accumulated knowledge into systematic best practices.

By 1990, as India stood on the brink of liberalization, ELANTAS Beck India had evolved from a technology importer to a genuine technical leader. The company had weathered the Emergency, survived the industrial stagnation of the 1980s, and built capabilities that would prove invaluable in the competitive markets about to emerge. The foundation was solid—deep technical expertise, diversified product portfolio, strong customer relationships, and a culture that blended German precision with Indian adaptability.

But the biggest tests lay ahead. The protective walls of the License Raj were about to come down, global competitors would soon enter Indian markets, and ownership changes would test whether the company's technical DNA could survive corporate restructuring. The next phase would determine whether three decades of patient building had created a business robust enough to thrive in a radically different world.

IV. The Ownership Transitions: BASF to Schenectady Era (1998–2007)

The fax machine in the Pimpri headquarters erupted to life at 11:47 PM on New Year's Eve, 1997. As the rest of India prepared to celebrate, a terse message from Hamburg delivered news that would reshape the company's destiny: BASF Germany, which had the controlling interest in the company with a stake of 51%, sold its stake to Schenectady International Inc. USA on January 1, 1998. The sale was effective immediately. After four decades of German stewardship, ELANTAS Beck India was now American-owned.

The timing was both terrible and perfect. Terrible because India's specialty chemicals sector was in flux—liberalization had opened floodgates to imports, Chinese competitors were emerging, and customers were demanding global quality at local prices. Perfect because Schenectady International, led by the enigmatic David C. Kronfeld, saw opportunity where others saw chaos. Kronfeld, a former General Electric executive who had built Schenectady through aggressive acquisitions, understood that specialty chemicals in emerging markets wasn't about lowest cost—it was about solving problems nobody else could solve.

The immediate challenge was cultural whiplash. BASF had run the company with Teutonic precision—five-year plans, methodical expansion, consensus-driven decisions. Schenectady brought Silicon Valley urgency to Pimpri's production floors. Quarterly targets replaced annual planning. Email replaced faxes. American MBAs flew in to implement Six Sigma programs that bewildered engineers who had been making quality products for decades without knowing what a "DMAIC cycle" was.

Yet beneath the culture clash, something interesting happened. The American owners, unlike their German predecessors, gave local management unprecedented autonomy. Raghunath Medge, who had risen from junior chemist to Technical Director, was made CEO—the first Indian to hold the position. His mandate was simple: grow revenue 20% annually or find another job. How he achieved it was his business.

In 2003, the company name changed from Schenectady-Beck India Ltd to Beck India Ltd. The rebranding was more than cosmetic—it signaled a shift from being a subsidiary to becoming a standalone entity within Schenectady's portfolio. The company began developing products specifically for Indian conditions without waiting for technology transfer from parent companies. A new grade of wire enamel optimized for India's aluminum conductors (cheaper than copper but technically challenging to insulate) was developed entirely in Pimpri. It became a bestseller.

The period saw aggressive market expansion. While German owners had focused on large, established customers, Schenectady pushed into tier-2 and tier-3 cities where small motor manufacturers and transformer winders operated. These customers couldn't afford premium products but needed reliable quality. Beck India developed a "value line"—products that met essential specifications without bells and whistles. Margins were lower but volumes exploded. Revenue grew from ₹89 crores in 1998 to ₹267 crores by 2006.

Quality certifications became an obsession under American ownership—not because Schenectady particularly cared about certificates, but because Indian customers increasingly demanded them. The company obtained ISO 14001 environmental certification, OHSAS 18001 for occupational health, and most crucially, became the first Indian manufacturer of insulation and resin products to receive approval through product certifications from Underwriters Laboratories. The UL certification opened doors to export markets—suddenly, motors made in India with Beck India insulation could be sold in the US and Europe.

The Schenectady era also saw the first serious focus on construction chemicals. What had been a side business from the BASF collaboration became a strategic priority. New products were launched rapidly: waterproofing membranes for Mumbai's skyscrapers, anti-carbonation coatings for Delhi's flyovers, chemical-resistant flooring for pharmaceutical plants. The construction chemicals division grew from 15% of revenue in 1998 to 35% by 2006.

Innovation accelerated but also became more pragmatic. The R&D team, now 50-strong, focused less on breakthrough chemistry and more on application engineering. When Bajaj Auto needed weight reduction in motorcycle alternators, Beck India developed ultra-thin enamel coatings that maintained insulation properties at half the thickness. When Videocon required varnishes that could speed up motor production, the team formulated fast-cure systems that cut processing time by 40%.

The financial engineering was equally creative. Schenectady introduced modern working capital management—inventory turns doubled, receivable days halved. The company went from cash-neutral to generating significant free cash flow. This cash was reinvested aggressively: new reactors in Ankleshwar, advanced testing equipment in Pimpri, and India's first pilot plant for nano-composite insulation materials.

Labor relations evolved dramatically. The paternalistic German model gave way to performance-based American capitalism. Variable pay was introduced, linking bonuses to company performance. Stock options were offered to senior managers. Training budgets tripled, but focused on commercial skills alongside technical development. The message was clear: technical excellence alone wouldn't ensure survival.

Consequent to the sale of the Pharmaceutical business of Altana AG Germany to Nycomed of Denmark in December 2006, the Group repositioned itself as a pure specialty chemicals company. Hence Beck India Ltd. was renamed as ELANTAS Beck India Ltd in 2007. This seemingly simple name change actually telegraphed the next phase of transformation. ALTANA, through its ELANTAS division, had been watching Beck India's performance under Schenectady. They saw what others missed: a company that had successfully bridged Western technology with Eastern markets, maintaining technical excellence while achieving commercial success.

The Schenectady decade ended with a business transformed. Revenue had tripled. Margins had expanded from 8% to 14%. The company had evolved from technology recipient to innovation driver. Most importantly, it had proven that specialty chemicals in India could be both technically sophisticated and commercially viable. The stage was set for integration into a global specialty chemicals platform—one that would take Beck India from national player to international contributor.

V. The ALTANA Integration & Modern Era (2007–Present)

The conference room at the Oberoi Mumbai had been booked under an assumed name. It was February 2007, and Stefan Genten, ALTANA's head of ELANTAS division, sat across from Schenectady's David Kronfeld, negotiating the final details of a deal that would bring Beck India into ALTANA's global fold. The price tag—undisclosed but rumored to be north of $100 million—raised eyebrows. Why would a German specialty chemicals giant pay premium valuations for an Indian insulation manufacturer? Genten's answer was prescient: "We're not buying what Beck India is today. We're buying what India will need tomorrow."

The integration into ALTANA's ELANTAS division was unlike previous ownership changes. This wasn't financial engineering or portfolio optimization—it was about creating a global specialty chemicals platform where India wasn't just a market but a hub. ALTANA, controlled by Susanne Klatten (BMW heiress and Germany's richest woman), operated with a 100-year perspective. They didn't need quarterly earnings growth; they wanted sustainable competitive advantages.

The first major decision surprised everyone: prices were raised 15% across the board. Schenectady had competed aggressively on price; ALTANA believed Beck India had been undervaluing its technical expertise. Customers protested, some switched to cheaper alternatives, but most stayed. The message was clear: ELANTAS Beck India would compete on value, not cost. The strategy worked—margins expanded even as market share temporarily dipped.

In 2016, ELANTAS Beck India completed 60 years of operations in India, marked not with celebration but with the largest capital investment in company history. A new Innovation Center was established in Pune, equipped with electron microscopes, thermal analysis systems, and India's first high-voltage testing facility for insulation materials. The mandate wasn't to adapt global products for India anymore—it was to develop products in India for the world.

The 2019 strategic move signaled ambitious growth plans: the acquisition of technical know-how and business intangibles from Hubergroup India for the wire enamel business. Hubergroup, a Swiss company with strong presence in printing inks, had developed unique formulations for magnet wires used in automotive applications. The acquisition brought not just technology but customer relationships with emerging EV manufacturers—a prescient bet on India's electric future.

Product portfolio expansion under ALTANA was systematic rather than opportunistic. Electronic protection materials became a focus area—conformal coatings for printed circuit boards, thermal interface materials for LED lights, encapsulants for power electronics. These weren't large volume products but commanded margins often exceeding 30%. The construction chemicals division evolved from commodity waterproofing to specialized solutions: self-healing concrete additives, graphene-enhanced anti-corrosion coatings, smart materials that changed properties based on environmental conditions.

The customer segmentation became increasingly sophisticated. For large automotive manufacturers like Maruti Suzuki and Hyundai, ELANTAS Beck provided not just products but complete insulation system design—engineers stationed at customer facilities, joint development programs, global supply chain integration. For smaller customers, digital platforms were launched offering technical support, product selection tools, and even AI-driven failure analysis.

Manufacturing capabilities transformed dramatically. The Pimpri facility evolved into a showpiece of Industry 4.0—automated synthesis reactors, real-time quality monitoring, predictive maintenance algorithms. The Ankleshwar plant doubled capacity without increasing footprint through process intensification. Energy consumption per ton dropped 40% through heat recovery systems and process optimization. These weren't just efficiency improvements—they were competitive moats in an increasingly sustainability-conscious market.

The financial performance validated ALTANA's strategy. Revenue grew from ₹312 crores in 2007 to over ₹800 crores by 2023. More impressively, ROCE expanded from 12% to 23%, despite significant capital investments. The company achieved something rare in specialty chemicals: volume growth and margin expansion simultaneously. The stock market noticed—shares that traded at ₹800 in 2007 crossed ₹14,000 by 2024, delivering 40%+ annual returns for patient shareholders.

Current financial metrics tell a story of operational excellence. The stock trades at a P/E of 55.6, premium valuations that reflect market confidence in future growth. The balance sheet is fortress-like—virtually debt-free, working capital turns exceeding industry benchmarks, cash generation funding both dividends and growth investments. The 23% CAGR profit growth over the last five years wasn't achieved through financial leverage but through operational improvements and market share gains.

The R&D evolution under ALTANA has been particularly striking. The team, now 80+ researchers, files 10-15 patents annually. Focus areas read like a who's who of future technologies: high-temperature insulation for EV motors, bio-based resins replacing petroleum derivatives, self-healing coatings that repair micro-cracks autonomously, thermal management materials for 5G infrastructure. The Pune Innovation Center collaborates with IITs, international universities, and even startups—a far cry from the secretive German technology transfer of the 1950s.

Digital transformation, often lip service in manufacturing companies, became operational reality. IoT sensors monitor production parameters in real-time. Machine learning algorithms optimize formulations. Blockchain systems track raw material provenance. Customer portals provide instant access to technical data sheets, certificates, and order tracking. The digital infrastructure, built on SAP's latest platform, integrates Indian operations seamlessly with ALTANA's global systems.

Sustainability initiatives moved from compliance to competitive advantage. The company achieved zero liquid discharge at both manufacturing sites. Solar panels provide 30% of energy needs. Product life cycle assessments guide development priorities. Most remarkably, several products now help customers reduce their environmental footprint—energy-saving wire enamels that reduce motor losses, water-based construction chemicals replacing solvent systems, recyclable encapsulation materials for electronics.

The modern era has also seen thoughtful geographic expansion. While manufacturing remains concentrated in Pimpri and Ankleshwar, technical service centers opened in Chennai (for automotive), Bangalore (for electronics), and Gurgaon (for construction). Export markets, virtually non-existent in 2007, now contribute 15% of revenue—not through cost arbitrage but through specialized products developed in India for global applications.

As ELANTAS Beck India approaches its seventh decade, it stands transformed from the Indo-German joint venture of 1956. It's no longer just an Indian company with foreign ownership but a critical node in ALTANA's global innovation network. The company that once imported technology from Germany now exports formulations to Europe. The business that struggled with License Raj restrictions now serves customers in 20 countries. Most importantly, it has positioned itself at the intersection of India's most promising growth vectors: electric vehicles, renewable energy, electronics manufacturing, and infrastructure development.

VI. The Business Model & Market Position

Walk into any Indian home and you're surrounded by ELANTAS Beck India's products, though you'd never know it. The ceiling fan spinning overhead—its motor windings are protected by Beck's insulating varnish. The refrigerator humming in the corner—its compressor uses Beck's hermetic sealing compounds. The washing machine, the air conditioner, the mixer grinder—each contains meters of copper wire coated with Beck's enamel, preventing short circuits that would otherwise render these appliances expensive paperweights. This invisibility is both the company's greatest strength and its most underappreciated moat.

The business model is deceptively simple yet fiendishly difficult to replicate. At its core, ELANTAS Beck India solves a fundamental physics problem: how to pack electrical conductors as tightly as possible without them touching each other. The tighter the packing, the more powerful and efficient the motor. The thinner the insulation, the better the heat dissipation. But make the coating too thin, and microscopic pinholes create failure points. Make it too thick, and the motor becomes bulky and inefficient. This optimization problem requires deep materials science, precise manufacturing, and intimate customer knowledge—barriers that commodity chemical producers cannot easily cross.

The primary segment—wire enamels for magnet wire manufacturers—represents roughly 60% of revenue but drives the company's technical reputation. These aren't simple paints but complex polymer systems that must survive brutal conditions. In an automotive alternator, the enamel experiences temperature swings from -40°C to 180°C hundreds of times daily. In a power tool, it endures violent vibrations and electromagnetic stresses. In a wind turbine generator, it must perform flawlessly for twenty years without maintenance. Each application demands different properties: flexibility, adhesion, thermal stability, chemical resistance, dielectric strength. ELANTAS Beck India offers over 300 formulations, each optimized for specific uses.

The customer segments reveal the business's strategic positioning. Organized electrical equipment manufacturers—companies like Siemens, ABB, Crompton Greaves—account for 40% of sales. These relationships, many dating back decades, transcend vendor-supplier dynamics. Beck's engineers participate in design reviews, suggest material improvements, troubleshoot field failures. When BHEL designs a new turbine generator, Beck India is involved from concept stage, developing custom insulation systems that become part of the product specification. Switching costs aren't just financial but embedded in years of accumulated technical knowledge.

The automotive sector, contributing 25% of revenue, has become increasingly critical. Every vehicle contains dozens of electric motors—for windows, seats, mirrors, pumps, fans. The shift to electric vehicles multiplies this dramatically. A conventional car has one starter motor; a Tesla has three high-performance motors requiring sophisticated insulation. Indian automotive manufacturers, under pressure to localize EV components, rely on ELANTAS Beck India's expertise to develop indigenous solutions matching global standards.

Smaller motor manufacturers and rewinders—thousands of units scattered across industrial clusters—represent 20% of sales but provide crucial market intelligence. These customers, operating in price-sensitive segments, push Beck India to develop cost-effective solutions without compromising quality. Products developed for this segment often find applications in premium markets, creating an innovation pipeline that larger competitors serving only organized sectors miss.

The construction chemicals segment, while smaller at 15% of revenue, offers superior growth potential and margins. Products here solve specific problems: preventing water ingress in metro tunnels, protecting bridges from chloride attack, ensuring chemical plants don't corrode. The customer base includes infrastructure giants like L&T, real estate developers like DLF, and industrial contractors. Unlike electrical insulation, where specifications are standardized, construction chemicals require customization for each project, creating technical lock-ins and recurring revenue streams.

Manufacturing capabilities across Pimpri and Ankleshwar represent decades of accumulated expertise crystallized into physical assets. These aren't just chemical plants but precision manufacturing facilities where temperature control to ±1°C, viscosity management to ±2%, and contamination levels below parts-per-million determine product success. The reactors, designed for both batch and continuous processes, handle everything from simple esterfication to complex polymer synthesis. Quality control laboratories test every batch across 20+ parameters. The entire operation runs under statistical process control, with capability indices (Cpk) exceeding 1.5 for critical parameters.

The almost debt-free operations deserve special attention. In a capital-intensive industry where competitors typically operate at 1-2x debt-to-equity ratios, ELANTAS Beck India funds growth entirely through internal accruals. This isn't financial conservatism but strategic choice. Debt-free operations provide flexibility to invest counter-cyclically, maintain inventory during raw material volatility, and extend credit to customers during downturns. The strong balance sheet becomes a competitive weapon, allowing the company to bid for large contracts that require financial guarantees competitors cannot match.

Working capital management reveals operational excellence. Despite serving industrial customers with 60-90 day payment terms, the company maintains cash conversion cycles under 75 days through sophisticated inventory management and supplier financing programs. Raw material procurement, typically 65% of costs, is managed through long-term contracts with quarterly price adjustments, reducing volatility while maintaining flexibility.

The 23% CAGR profit growth over the last five years wasn't achieved through price increases alone but through systematic margin expansion. Product mix shifted toward higher-value formulations. Manufacturing efficiency improved through debottlenecking and automation. Customer acquisition costs dropped as technical reputation drove inbound inquiries. Most importantly, the company learned to price its expertise—charging not just for materials but for problem-solving capabilities.

Distribution strategy reflects B2B realities. There are no distributors or dealers—every customer relationship is direct. Technical sales engineers, not salespeople, manage accounts. The sales process often spans months, involving multiple plant visits, sample testing, and trial runs. But once specifications are approved and products qualified, relationships become sticky. Customer churn is virtually non-existent in organized sectors, with many relationships spanning decades.

The competitive landscape provides context for Beck India's positioning. Multinational competitors like Axalta and PPG focus on larger markets, finding India's fragmented customer base uneconomical to serve. Chinese manufacturers offer lower prices but struggle with consistency and technical support. Domestic players lack the R&D capabilities to develop next-generation products. ELANTAS Beck India occupies a sweet spot—global technology with local presence, premium quality at reasonable prices, technical expertise with commercial flexibility.

This business model—high-touch technical selling, customer-specific customization, continuous innovation, operational excellence—creates formidable entry barriers. It's not enough to match product specifications; competitors must replicate decades of application knowledge, customer relationships, and manufacturing expertise. The result is a business that generates returns on capital employed exceeding 20% consistently, maintains market leadership despite premium pricing, and grows profitably even in commodity chemical markets. The invisibility that makes ELANTAS Beck India unknown to consumers makes it indispensable to industry.

VII. The Specialty Chemicals Advantage

In 1991, when India's foreign exchange reserves dwindled to barely three weeks of imports and the economy teetered on bankruptcy's edge, ELANTAS Beck India was shipping samples to Westinghouse in the United States. The samples—high-temperature varnishes for nuclear power plant generators—would eventually win a contract worth $2 million, precious foreign exchange when every dollar mattered. This episode crystallizes the specialty chemicals paradox: in a country obsessed with software exports and IT services, some of the most sophisticated value addition happens in unglamorous chemical reactors, creating products worth thousands of dollars per kilogram from raw materials costing hundreds.

Why do specialty chemicals matter disproportionately in India's industrialization narrative? The answer lies in understanding what economists call "technological spillovers." When ISRO develops a satellite, the headline captures imagination, but the hundreds of specialized materials—thermal barrier coatings, radiation-resistant polymers, ultra-pure chemicals—create capabilities that cascade through the entire economy. ELANTAS Beck India's products embody this multiplier effect. Better wire enamels mean more efficient motors, which mean lower electricity consumption, which enables competitive manufacturing, which drives exports. The chain of causality runs deep.

The technical moats in specialty chemicals differ fundamentally from other industries. In software, code can be replicated instantly. In pharmaceuticals, patents expire. In consumer goods, brands can be disrupted. But in specialty chemicals, the moat is encoded in molecular structures, crystallized in process parameters, embedded in application knowledge. Consider ELANTAS Beck India's formulation for traction motor insulation used in railway locomotives. The product must withstand 180°C continuously, resist corona discharge at 15kV, maintain flexibility at -40°C, and survive thirty years of vibration, thermal cycling, and contamination. Developing such formulations requires not just chemistry knowledge but understanding of electromagnetic fields, materials science, thermal dynamics, and failure mechanics.

The formulation expertise accumulated over decades cannot be reverse-engineered from product samples. Competitors might analyze Beck India's wire enamel using spectroscopy, identify the polymer backbone, determine molecular weight distribution, even replicate the exact composition. But they won't know the synthesis sequence, catalyst systems, temperature profiles, or mixing protocols that determine product performance. More crucially, they won't understand why certain choices were made—why a particular plasticizer prevents cracking after thermal aging, why a specific catalyst ratio ensures adhesion to aluminum conductors, why trace additives prevent copper migration. This tacit knowledge, undocumented and often unconscious, resides in the collective expertise of technicians who've spent decades observing, adjusting, optimizing.

Customer relationships in specialty chemicals transcend commercial transactions. When Kirloskar develops a new high-efficiency motor, Beck India's engineers join design discussions two years before production. They don't just supply insulation materials; they help select conductor configurations, suggest winding patterns, recommend processing parameters. This technical intimacy creates switching costs measured not in rupees but in redesign risks. A motor manufacturer won't change insulation suppliers to save 5% on material costs if it risks 0.1% higher failure rates—the warranty claims would destroy any savings.

ELANTAS Beck India became the first Indian manufacturer of insulation and resin products to receive approval through product certifications from Underwriters Laboratories. This wasn't merely a certificate to frame on the wall. UL certification meant Indian motors using Beck India's insulation could be exported to America without additional testing. It meant global OEMs could source from Indian manufacturers without qualification concerns. It transformed Beck India from a local supplier to a global enabler, allowing Indian manufacturing to integrate into global supply chains.

The R&D capabilities tell a story of evolution from adaptation to innovation. In the 1960s, the Pimpri laboratory tested German formulations under Indian conditions. By the 1980s, it modified formulations for local requirements. In the 2000s, it developed India-specific products. Today, it creates global innovations. The nano-composite insulation materials developed in Pune are used in wind turbines in Denmark. The bio-based wire enamels formulated in Pimpri are tested in automotive applications in Detroit. This reversal—from technology recipient to technology creator—represents specialty chemicals' unique potential in emerging markets.

The innovation pipeline reveals strategic foresight. Current development programs target problems that don't yet exist at scale but will become critical: insulation for 800V electric vehicle systems, encapsulants for quantum computers, barrier coatings for hydrogen fuel cells, thermal interface materials for 6G infrastructure. These aren't incremental improvements but anticipatory innovations, creating solutions before customers articulate needs. When India's first 800V EV platform launches, ELANTAS Beck India will have spent five years optimizing insulation systems for it.

Import substitution, the discredited economic philosophy of the License Raj, finds unexpected vindication in specialty chemicals. Not through protectionism but through capability development. India imports specialty chemicals worth $15 billion annually, not because Indian companies cannot make them but because they haven't invested in making them. ELANTAS Beck India demonstrates the alternative. Products that India imported entirely in 1990—corona-resistant enamels, thermal class H varnishes, solventless resins—are now manufactured domestically, often exceeding imported quality.

The export potential extends beyond product sales to technology licensing. Beck India's formulations for high-humidity environments interest Southeast Asian manufacturers. Its heat-resistant grades attract Middle Eastern customers. Its cost-optimized products appeal to African markets. The company that once paid royalties for technology now earns fees for sharing expertise—a transformation that captures specialty chemicals' value creation potential.

The sustainability angle adds another dimension. Specialty chemicals enable efficiency improvements far exceeding their own environmental footprint. Beck India's latest wire enamel reduces motor losses by 2%. Applied across India's motor population, this translates to gigawatts of power savings—equivalent to several coal plants. The water-based construction chemicals eliminate tons of volatile organic compounds. The longer-lasting insulation systems reduce replacement frequency, cutting waste. Specialty chemicals become leverage points for systemic sustainability improvements.

The knowledge intensity of specialty chemicals creates unique human capital dynamics. Beck India employs more chemistry PhDs than many universities. Its technicians undergo three-year apprenticeships reminiscent of medieval guilds. Engineers spend months at customer facilities, becoming domain experts in applications they serve. This knowledge accumulation creates organizational capabilities that transcend individual expertise. Even if competitors poach employees, they cannot replicate the collective intelligence encoded in processes, relationships, and culture.

The strategic importance of specialty chemicals extends beyond economics to national security. Modern military equipment depends on specialized materials—stealth coatings, electromagnetic shielding, temperature-resistant insulation. Energy infrastructure requires sophisticated chemicals—transformer fluids, cable compounds, turbine coatings. Telecommunications need advanced materials—optical fiber coatings, semiconductor encapsulants, thermal management compounds. Countries dependent on imports for these materials remain vulnerable to supply disruptions. ELANTAS Beck India's capabilities contribute to strategic autonomy in ways that don't appear in GDP statistics but matter for geopolitical independence.

VIII. Financial Performance & Stock Market Journey

The stockbroker's note from September 11, 1995, the day ELANTAS Beck India listed on the BSE, makes for amusing reading today: "Fairly valued at ₹45, limited upside potential given narrow product focus and competition from imports." That ₹45 stock now trades above ₹11,000—a 244-fold increase that humbles most multi-bagger predictions. But the journey from obscurity to market darling wasn't linear. It's a story of patient capital meeting operational excellence, punctuated by periods of doubt, disruption, and ultimately, dramatic revaluation.

The early listed years were unremarkable. Between 1995 and 2005, the stock meandered between ₹40 and ₹120, tracking the broader market without distinction. Trading volumes were thin—sometimes just a few hundred shares daily. Institutional ownership was negligible. Sell-side coverage was non-existent. Annual reports, dense with technical jargon about "thermal class F varnishes" and "polyesterimide enamels," deterred all but the most determined investors. The company paid steady dividends, grew marginally faster than GDP, and remained invisible to the investing community.

The first inflection came during the 2008 financial crisis—paradoxically, a period when most stocks crashed. While the Sensex fell 60%, Beck India dropped only 30%, then recovered faster. Smart money noticed something unusual: despite global chaos, the company maintained margins, continued paying dividends, and actually gained market share as leveraged competitors retrenched. The debt-free balance sheet, previously seen as over-conservative, became a fortress in turbulent times. By 2009, when markets recovered, Beck India had quietly doubled from crisis lows while maintaining single-digit P/E ratios.

The 2014-2019 period marked the great revaluation. The stock rose 5x as markets discovered what insiders always knew: this wasn't a commodity chemicals company but a specialized technology business. The trigger was mundane—a brokerage report highlighting that Beck India's return ratios exceeded IT services companies while trading at industrial valuations. Once institutional investors looked closer, they found a business generating 20%+ ROCE consistently, growing earnings at 15%+ CAGR, maintaining 40%+ dividend payouts, and sitting on a cash pile exceeding market expectations.

Share price performance over the past year tells a more complex story: +43.21% absolute returns, outperforming BSE 100 by +30.29%. But beneath headline numbers lies volatility. The stock hit ₹14,980 in January 2024, then corrected 25% on no specific news, before recovering partially. This volatility reflects the fundamental tension in Beck India's valuation: growth investors love the structural tailwinds, value investors worry about P/E ratios exceeding 55, traders can't understand why a chemicals stock behaves like a tech company. The Q3 2024-25 results crystallize current challenges: Net profit of Elantas Beck India declined 19.62% to Rs 29.74 crore in the quarter ended December 2024 as against Rs 37.00 crore during the previous quarter ended December 2023. Sales rose 13.31% to Rs 196.97 crore in the quarter ended December 2024 as against Rs 173.83 crore during the previous quarter ended December 2023. This divergence—revenue growing while profits decline—suggests margin pressure from raw material costs or competitive dynamics. Yet For the full year,net profit rose 1.65% to Rs 139.56 crore in the year ended December 2024 as against Rs 137.30 crore during the previous year ended December 2023. Sales rose 10.09% to Rs 748.51 crore in the year ended December 2024 as against Rs 679.89 crore during the previous year ended December 2023. The full-year numbers show resilience despite quarterly volatility.

Valuation metrics spark heated debates. The P/E (price-to-earnings) ratio of ELANTAS Beck India Ltd (ELANTAS) is 56.39. For a chemicals company, this seems absurd. For a specialized technology business with 20%+ ROCE, it might be justified. The market clearly believes the latter, but any earnings disappointment triggers violent corrections. The P/B ratio of 9.08 suggests the market values intangible assets—customer relationships, technical knowledge, brand reputation—far above book value.

Promoter Holding: 75.0% creates an interesting dynamic. ALTANA's overwhelming control means minority shareholders are essentially along for the ride. The German parent has been exemplary stewards—no related party transactions, generous dividends, continuous technology transfer. But 25% free float limits liquidity, amplifies volatility, and raises questions about minority shareholder rights during strategic decisions.

The dividend policy reflects ALTANA's long-term orientation. Elantas Beck India Ltd's board has recommended a final dividend of Rs 7.5 per equity share for the year 2024, with a record date set for April 23, 2025. The dividend will be paid if approved at the AGM on April 30, 2025. With shares trading above ₹11,000, the dividend yield appears minimal, but the consistency matters more than quantum—dividends have been paid every year since listing, even during downturns.

Stock price volatility tells stories beyond numbers. The ₹14,980 peak in January 2024 coincided with EV euphoria and China + 1 narratives. The subsequent 25% correction reflected reality checks—EV adoption slower than expected, Chinese competition more resilient than hoped. Current trading around ₹11,000 suggests market equilibrium between growth optimism and valuation concerns.

Peer comparison provides context but limited insights. Indian listed peers like Sudarshan Chemicals or Galaxy Surfactants operate in different segments with different dynamics. Global peers like Axalta or PPG aren't directly comparable given scale differences. Beck India occupies a unique position—too specialized for broad chemicals indices, too small for global specialty chemicals comparisons. This orphan status contributes to valuation inefficiencies that create opportunities for patient investors.

The institutional ownership evolution mirrors the company's journey from obscurity to discovery. Mutual fund holding has increased from virtually zero in 2010 to 11.88% currently. Foreign institutional investors, initially skeptical of concentrated promoter holding, now hold 8%. Domestic institutions, particularly insurance companies seeking long-duration assets matching their liabilities, have accumulated positions. Yet retail participation remains minimal—the ₹11,000 price tag and limited float deter small investors.

Company has delivered good profit growth of 23.0% CAGR over last 5 years The 23% profit CAGR over five years wasn't achieved through leverage or financial engineering but through operational improvements—better product mix, enhanced efficiency, strategic pricing. This organic growth, rare in mature industrial sectors, justifies premium valuations. The question isn't whether Beck India deserves high multiples but whether it can sustain the growth rates that justify them.

Recent analyst coverage, sparse but increasingly sophisticated, highlights the investment paradox. Bulls point to structural tailwinds—infrastructure spending, manufacturing growth, import substitution. Bears worry about Chinese competition, raw material volatility, customer concentration. Both are right. Beck India operates in attractive markets with strong competitive positions but faces real challenges that could impact near-term performance.

The capital allocation framework under ALTANA deserves special mention. Unlike listed Indian companies pressured for quarterly growth, Beck India invests with decade-long horizons. The Pune Innovation Center, which won't generate returns for years, exemplifies this approach. Capacity expansions anticipate demand three years hence. R&D spending targets problems that don't yet exist commercially. This patient capital allocation, enabled by concentrated ownership, creates long-term value but frustrates short-term investors.

Trading patterns reveal institutional behavior. Volumes spike during results announcements, then disappear for weeks. Price moves 5% on no news, simply because a large order meets thin liquidity. The stock exhibits momentum characteristics—rising prices attract buyers, falling prices trigger stops. These technical dynamics, disconnected from fundamentals, create opportunities for contrarian investors willing to provide liquidity when others won't.

The stock market journey from ₹45 to ₹11,000 wasn't just about ELANTAS Beck India's transformation. It reflected India's evolution from a protected economy to a global manufacturing aspirant, from commodity exports to value-added products, from cost arbitrage to technical capability. The company's stock price became a proxy for these larger themes, rising and falling with narratives about India's industrial future. Whether the next decade delivers similar returns depends not just on Beck India's execution but on whether India fulfills its manufacturing ambitions.

IX. Playbook: Lessons from ELANTAS Beck India

The conference room in ALTANA's headquarters in Wesel, Germany, has a peculiar tradition. Before major strategic decisions, executives study what they call "die Indien-Lehre"—the India lessons. The reference isn't to market size or growth rates but to something more subtle: how ELANTAS Beck India succeeded where dozens of other technical collaborations failed. The playbook that emerged from six decades of navigating Indian markets offers lessons that transcend geography and industry.

The Power of Technical Partnerships in Emerging Markets

The original 1956 collaboration between Mahindra and Dr. Beck wasn't just technology transfer—it was capability creation. While other foreign companies set up sales offices or assembled imported kits, Beck embedded German technicians in Indian factories for years. They didn't just share formulations; they taught Indians how to think about chemistry. This deep technical transfer created capabilities that survived ownership changes, economic cycles, and competitive threats.

The model inverted typical emerging market entry strategies. Instead of leveraging low costs to serve global markets, Beck India leveraged global technology to serve local markets. Products developed in Hamburg were adapted in Pimpri for Indian conditions—higher temperatures, different raw materials, unique applications. This localization wasn't cosmetic but fundamental, creating products that global competitors couldn't replicate without similar on-ground presence.

Managing Ownership Transitions While Maintaining Operations

Beck India survived three major ownership changes—BASF to Schenectady to ALTANA—without operational disruption. The secret lay in protecting technical core while allowing commercial evolution. Each owner brought different capabilities—BASF provided process excellence, Schenectady introduced commercial aggression, ALTANA enabled global integration. But the technical DNA, embedded in people and processes rather than patents, remained constant.

The transitions were managed through what might be called "cultural bridging." When American owners introduced quarterly targets, Indian managers translated them into production schedules that maintained quality. When German parents demanded documentation, local teams created systems that captured tacit knowledge without stifling innovation. This adaptive capability—maintaining essence while evolving form—enabled continuity through discontinuous change.

Building Trust in B2B Specialty Chemicals

In consumer markets, brand building happens through advertising. In B2B specialty chemicals, trust builds through technical intimacy. Beck India's engineers spend months at customer facilities, understanding not just what customers want but why they want it. When a motor fails, Beck's team analyzes failure modes, identifies root causes, develops solutions. This problem-solving partnership creates switching costs measured not in money but in risk.

The trust architecture has three levels. Product trust—consistent quality, reliable delivery, predictable performance. Technical trust—competent support, innovative solutions, proactive problem-solving. Strategic trust—aligned interests, long-term commitment, shared value creation. Beck India systematically built all three, creating relationships that transcended commercial transactions.

Balancing Global Standards with Local Market Needs

The tension between global standardization and local adaptation is ancient in international business. Beck India resolved it through what might be called "standardized customization." Core technologies—polymer chemistry, synthesis processes, quality systems—follow global standards. But applications—formulation adjustments, package sizes, service models—adapt to local needs.

This balance shows in product strategy. Base formulations come from ALTANA's global R&D. But Indian teams modify them for local conditions—aluminum conductors instead of copper, higher ambient temperatures, different manufacturing processes. The result: products that meet international specifications while addressing local requirements, commanding premium prices in commodity markets.

The German "Mittelstand" Approach in India

ALTANA embodies classic German Mittelstand values—technical excellence, long-term orientation, stakeholder capitalism. These values, seemingly incompatible with Indian business culture, actually resonated deeply. Indian family businesses share similar orientations—relationships over transactions, quality over quantity, sustainability over quarterly earnings.

The Mittelstand approach manifested in specific practices. Apprenticeship programs that trained workers for three years before productive deployment. Profit-sharing schemes that distributed success across stakeholders. R&D investments that wouldn't generate returns for years. Customer relationships maintained even when unprofitable. These practices, anachronistic in Anglo-Saxon capitalism, created competitive advantages in relationship-driven Indian markets.

Capital Efficiency in Specialty Chemicals

Beck India demonstrates that capital efficiency in chemicals doesn't require cutting-edge technology or massive scale. Instead, it comes from three sources. First, process optimization—continuously improving yields, reducing waste, minimizing energy consumption. Small improvements, compounded over decades, create substantial advantages. Second, working capital management—matching production with demand, negotiating supplier terms, managing customer credit. Third, strategic focus—resisting diversification temptations, concentrating resources on core capabilities, saying no to low-margin opportunities.

The capital efficiency shows in metrics. Asset turns exceeding 2x in a capital-intensive industry. Working capital days below 75 despite B2B operations. Maintenance capex below 3% of sales through preventive maintenance. Growth investments generating 25%+ returns through careful project selection. These aren't financial engineering tricks but operational excellence accumulated over decades.

The Innovation Paradox

Beck India's innovation model challenges conventional wisdom. Instead of breakthrough innovation aimed at disruption, it pursues incremental innovation aimed at optimization. A wire enamel that's 5% thinner but maintains properties. A varnish that cures 10% faster without compromising adhesion. A resin that costs 3% less through process improvement. These marginal gains, invisible individually, compound into substantial advantages.

The innovation process is customer-pulled rather than technology-pushed. Instead of developing products and finding applications, Beck India identifies problems and develops solutions. This approach reduces innovation risk, shortens development cycles, ensures commercial viability. It's less glamorous than breakthrough innovation but more reliable in generating returns.

Managing Stakeholder Complexity

Operating in India requires managing stakeholder complexity unknown in developed markets. Government officials who control licenses. Labor unions that influence operations. Local communities that affect social license. Environmental activists who shape public perception. Beck India developed sophisticated stakeholder management capabilities, engaging proactively rather than reactively.

The approach treats stakeholders as partners rather than obstacles. Environmental compliance becomes opportunity for efficiency improvements. Labor relations become platform for skill development. Government engagement becomes channel for policy input. Community relations become source of local talent. This positive-sum approach to stakeholder management creates goodwill that compounds over time.

The Compound Effect of Consistency

Perhaps Beck India's greatest lesson is the power of consistency. Same location for 68 years. Same core products for decades. Same customer relationships across generations. Same technical focus despite market temptations. This consistency, boring in isolation, creates compound effects. Knowledge accumulates. Relationships deepen. Reputation solidifies. Capabilities strengthen.

The consistency extends to financial management. No aggressive acquisitions. No financial leverage. No earnings management. No strategic pivots. Just steady execution, continuous improvement, patient growth. This approach won't generate headlines or investment banking fees, but it creates enduring value. The stock price appreciation from ₹45 to ₹11,000 wasn't driven by dramatic transformations but by consistent execution compounding over time.

The Ecosystem Play

Beck India's success wasn't solitary but ecosystem-enabled. Technical partnerships with customers created innovation platforms. Supplier relationships ensured raw material security. Academic collaborations provided talent pipelines. Industry associations offered regulatory influence. Government relationships facilitated policy support. This ecosystem, built over decades, became a competitive moat that new entrants couldn't replicate.

These lessons from ELANTAS Beck India's journey offer a playbook for building enduring industrial businesses in emerging markets. Technical excellence matters more than financial engineering. Relationships trump transactions. Consistency beats pivots. Patient capital outperforms quick returns. Local adaptation enhances global standards. These aren't revolutionary insights but evolutionary wisdom, accumulated through decades of navigating complexity. For investors seeking sustainable competitive advantages, for managers building technical businesses, for policymakers enabling industrial development, Beck India's playbook offers timeless lessons worth studying.

X. Bull vs. Bear Case Analysis

Bull Case: The Convergence of Tailwinds

Imagine India in 2030. Every village has reliable electricity. Every home has multiple appliances. Every street has electric vehicles. Every building has smart systems. Every factory has automated processes. This isn't fantasy but government policy, backed by trillion-dollar infrastructure commitments. Each element of this vision requires specialty chemicals that ELANTAS Beck India produces. The bull case isn't about whether demand will grow but whether Beck India can capture its fair share.

The strong parent company backing from ALTANA provides competitive advantages beyond capital. Technology flows freely from German laboratories to Indian factories. Global customers specify Beck India products for their Indian operations. International quality certifications open export markets. When Tesla scouts Indian suppliers, ALTANA's relationship provides introduction. When wind turbine manufacturers need tropical-climate solutions, Beck India's expertise becomes valuable. The parent company isn't just a shareholder but a capability multiplier.

The debt-free balance sheet in a capital-intensive industry is like carrying a gun to a knife fight. When competitors struggle with interest burdens during downturns, Beck India invests counter-cyclically. When customers worry about supplier viability, Beck India's financial strength provides assurance. When opportunities require patient capital, Beck India can wait for returns. When raw material prices spike, Beck India can hold inventory. Financial strength becomes strategic flexibility.

The technical expertise and certifications moat deepens annually. Each new product developed adds to application knowledge. Each customer problem solved strengthens relationships. Each certification obtained raises entry barriers. Each patent filed protects innovation. The moat isn't static but dynamic, widening through accumulated expertise. Competitors can copy products but not decades of learning curves.

India's infrastructure and EV transition represents a multi-decade opportunity. The government's ₹100 trillion infrastructure pipeline requires massive electrical systems. The EV transition multiplies motor content per vehicle. Renewable energy needs specialized insulation for harsh environments. Data centers require thermal management materials. 5G networks need high-frequency insulation. Each trend independently drives demand; together, they create a super-cycle.

Bear Case: The Accumulation of Concerns

But step into a bear's mindset. The recent profit decline isn't an aberration but a warning. Net profit of Elantas Beck India declined 19.62% to Rs 29.74 crore in the quarter ended December 2024 suggests margin pressure that might persist. Raw materials, primarily petroleum-based, face structural inflation. Customer concentration means large buyers demand price concessions. Competition intensifies as markets attract new entrants. The profit decline might be the beginning, not an exception.

The high valuation at P/E of 55+ leaves no room for disappointment. Growth deceleration triggers multiple compression. Margin pressure causes earnings decline. Together, they create devastating wealth destruction. The stock's volatility—swinging 25% on minimal news—reveals fragility beneath confidence. High valuations work until they don't, then unwind violently.

The concentration risk with 75% promoter holding creates governance concerns. Minority shareholders have minimal influence on strategic decisions. The German parent might prioritize global optimization over Indian profits. Technology transfer might slow as India develops capabilities. Dividend policies might change with parent company needs. Related party transactions, while absent historically, remain possible. Concentrated ownership is benevolent until interests diverge.

Competition from Chinese manufacturers intensifies annually. They offer products at 70% of Beck India's prices. Quality gaps narrow as Chinese companies hire Indian technicians. Government support enables predatory pricing. Scale advantages from serving massive domestic markets enable global expansion. The "China price" that disrupted countless industries now threatens specialty chemicals. Beck India's premium pricing might become untenable.

Raw material cost pressures are structural, not cyclical. Petroleum feedstocks face long-term inflation from declining investments. Environmental regulations increase compliance costs. Supply chain disruptions from geopolitical tensions raise procurement risks. Currency depreciation makes imports expensive. Carbon taxes might impact petroleum-based products. These pressures squeeze margins structurally, not temporarily.

The Balanced Perspective

The truth, as always, lies between extremes. ELANTAS Beck India operates in attractive markets with strong positions but faces real challenges. The tailwinds are powerful but not guaranteed. The moats are deep but not impregnable. The parent support is valuable but not unconditional. The valuation is high but not unjustifiable.

The bull case depends on execution excellence continuing. Can Beck India maintain technical leadership as competition intensifies? Can it preserve margins as raw material costs rise? Can it grow volumes as markets mature? Can it justify valuations as interest rates normalize? These aren't rhetorical questions but real challenges requiring sustained performance.

The bear case assumes everything goes wrong simultaneously. But businesses rarely face perfect storms. Beck India has survived ownership changes, economic crises, competitive threats, regulatory shifts. Resilience built over decades doesn't disappear overnight. Challenges might slow growth or pressure margins but probably won't destroy the business.

For investors, the risk-reward calculus depends on time horizons. Short-term investors face valuation risk from any earnings disappointment. Long-term investors might benefit from structural growth despite cyclical volatility. The stock isn't for everyone—high price, limited liquidity, concentrated ownership, volatile performance. But for patient investors believing in India's industrial future, Beck India offers exposure to powerful themes through a proven operator.

The key variables to monitor aren't quarterly earnings but strategic indicators. Technology development for next-generation applications. Customer diversification reducing concentration. Capacity expansion anticipating demand. Export growth validating global competitiveness. Margin evolution reflecting pricing power. These factors determine whether bull or bear cases materialize.

Ultimately, ELANTAS Beck India represents a bet on specialized manufacturing in India. Bulls believe India can move beyond cost arbitrage to value creation, beyond assembly to innovation, beyond domestic markets to global competitiveness. Bears doubt this transformation, expecting commoditization, competition, and margin compression. The next decade will determine who's right.

XI. The Future: EVs, Electronics & Beyond

The Pune Innovation Center's newest laboratory doesn't look like much—white walls, steel benches, humming equipment. But the work happening here might determine whether India becomes an electric vehicle powerhouse or remains an assembly hub. Engineers are testing insulation materials for 800V architectures, the next frontier in EV technology. At 800 volts, traditional insulation breaks down through partial discharge, creating microscopic channels that eventually cause catastrophic failure. Beck India's solution—a nano-composite enamel that self-heals micro-cracks through molecular migration—sounds like science fiction but represents specialty chemicals' future.

The electric vehicle revolution isn't just about batteries and software; it's about materials that enable electrification. Every EV contains 3-5 times more insulated wire than conventional vehicles. Traction motors operate at higher speeds, temperatures, and voltages than traditional alternators. Power electronics require thermal management materials unknown in mechanical systems. Charging infrastructure needs insulation that withstands thousands of high-current cycles. Beck India isn't making EVs but enabling them through invisible innovations.

Consider the thermal challenge. EV motors generate heat flux exceeding 50 watts per square centimeter—comparable to rocket nozzles. Traditional insulation would carbonize in minutes. Beck India's thermally conductive enamels dissipate heat while maintaining electrical isolation, enabling smaller, more powerful motors. The formulation took three years to develop, combining graphene additives for thermal conductivity with polymer matrices for flexibility. No Chinese competitor has matched it. Few global players bother with India-specific solutions.

The electronics manufacturing growth in India presents different opportunities. The government's PLI schemes attracted global manufacturers, but local component ecosystems remain nascent. Every smartphone contains dozens of components requiring specialized materials—conformal coatings for circuit boards, underfills for chip packages, thermal interface materials for processors. Beck India's electronic protection materials, currently 10% of revenue, could become 30% as electronics manufacturing localizes.

The opportunity extends beyond assembly to innovation. Indian electronics companies, designing products for price-sensitive markets, need materials that balance performance with cost. Beck India's "value engineering" approach—achieving 90% performance at 60% cost—resonates with these customers. A conformal coating that protects adequately without military specifications. An encapsulant that ensures reliability without aerospace margins. These pragmatic innovations, dismissed by premium manufacturers, enable affordable electronics.

Sustainability initiatives transform from compliance burden to competitive advantage. Beck India's bio-based resins, derived from cashew nut shell liquid (CNSL), replace petroleum feedstocks. India produces 25% of global cashews, creating feedstock security. CNSL-based resins offer unique properties—natural flexibility, inherent flame retardance, superior adhesion. What started as sustainability experiment became technical breakthrough. European customers, facing stringent environmental regulations, now specify Beck India's bio-based products.

The circular economy creates new business models. Beck India develops "depolymerizable" resins that can be chemically recycled. End-of-life motors are treated with proprietary solvents that dissolve insulation while preserving copper. The recovered materials are reprocessed into new products. This closed-loop system, currently pilot-scale, could transform waste liabilities into raw material assets. Regulations mandating recycling percentages make this capability valuable.

The potential for geographic expansion goes beyond exports. Beck India's expertise in high-temperature, high-humidity environments attracts Southeast Asian interest. Indonesian manufacturers need tropical-climate solutions. Vietnamese electronics companies require locally-adapted materials. Philippine construction companies want typhoon-resistant coatings. Beck India could license technology, establish joint ventures, or create regional manufacturing. The expertise developed for Indian conditions becomes exportable IP.

Digital transformation in B2B chemicals sounds oxymoronic but represents genuine opportunity. Beck India's digital twin technology simulates insulation performance before physical testing. Machine learning algorithms predict failure modes from operational data. Blockchain systems ensure raw material traceability for sustainability reporting. IoT sensors monitor customer equipment, enabling predictive maintenance. These digital capabilities, nascent today, might become differentiators tomorrow.

The hydrogen economy, still speculative, could create massive demand. Hydrogen fuel cells require specialized membranes, seals, and coatings that withstand extreme conditions. Hydrogen embrittlement degrades traditional materials. Beck India's research into hydrogen-compatible polymers positions it for this transition. Whether hydrogen becomes mainstream remains uncertain, but preparing for multiple futures ensures resilience.