SBFC Finance: From Bootstrap NBFC to MSME Lending Powerhouse

I. Introduction & Episode Setup

Picture this: A small business owner in Jaipur, running a textile shop for fifteen years, walks into a bank seeking a ₹10 lakh loan to expand inventory before the wedding season. Despite steady cash flows and a spotless repayment history with suppliers, he walks out empty-handed—no formal credit history, insufficient collateral, too much paperwork. This scene plays out millions of times across India's tier-2 and tier-3 cities, where the backbone of the economy—the micro, small, and medium enterprises—remains starved of formal credit.

Enter SBFC Finance, a company that spotted this massive gap and built an entire lending empire around it. Today, SBFC stands as a ₹11,149 crore market cap entity, having grown its assets under management at a blistering 46% CAGR over the past five years. With revenue of ₹1,396 crores and profit of ₹367 crores, this isn't just another NBFC success story—it's a masterclass in finding inefficiencies in India's financial system and building a scalable solution.

The question that drives this deep dive: How did a company founded in the depths of the 2008 financial crisis transform from a small non-banking financial company into one of India's fastest-growing MSME lenders? More importantly, what can SBFC's journey teach us about building in regulated spaces, serving underserved markets, and creating value in India's complex financial landscape?

What makes SBFC particularly fascinating is its timing and approach. While global financial institutions were collapsing in 2008, a group of professionals saw opportunity in India's credit-starved small businesses. They built not just a lending business, but a financial services platform that combines secured MSME loans, gold loans, and loan management services—a trinity that serves entrepreneurs, individual customers, and the vast universe of micro, small, and medium enterprises that form 30% of India's GDP yet receive less than 15% of formal credit.

This isn't a story of Silicon Valley-style blitzscaling or venture capital-fueled growth. It's about patient capital, deep market understanding, and the unglamorous work of building credit infrastructure in markets that others ignored. It's about creating what SBFC calls a "PhyGital" model—a portmanteau that captures their philosophy of combining digital efficiency with the human touch that's essential in relationship-based lending.

As we unpack this journey, we'll explore how SBFC navigated multiple rebrands, built a 135-branch network across 104 cities, went public in a challenging market, and positioned itself at the intersection of India's formalization drive and digital revolution. We'll examine the unit economics of MSME lending, the strategic pivot to gold loans, and the delicate balance between growth and risk management that defines success in the NBFC space.

For investors, SBFC presents a fascinating study in contrasts—stellar growth metrics paired with relatively modest returns on equity, geographic diversification balanced against concentration risk, and the perpetual tension between serving underserved markets profitably while maintaining asset quality. For entrepreneurs, it's a playbook on building in highly regulated industries where trust is currency and distribution is destiny.

II. The Founding Story & Early Years (2008-2017)

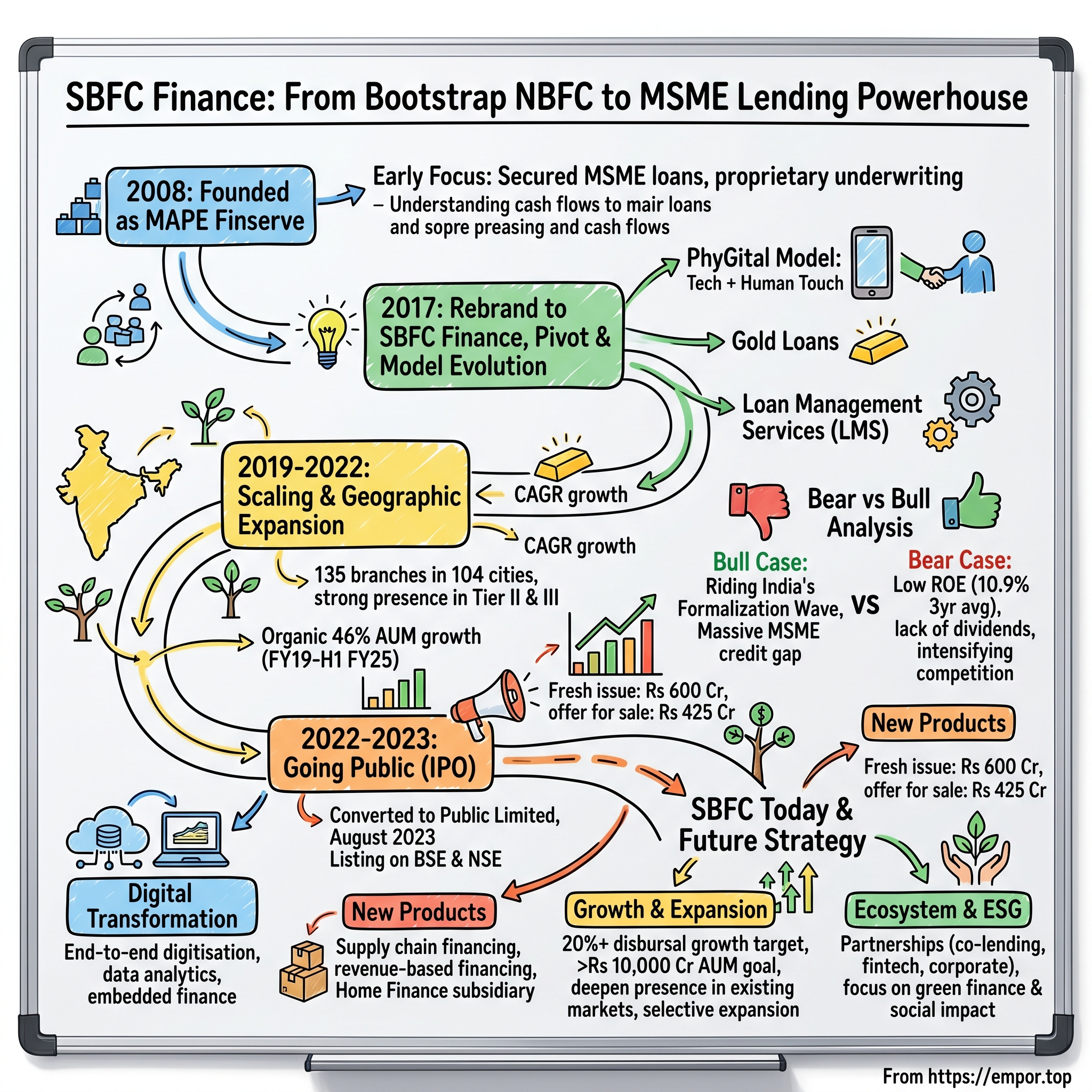

The date was January 25, 2008. Lehman Brothers was still six months away from collapse, but cracks in the global financial system were already visible to those paying attention. In India, inflation was running hot, the RBI was tightening monetary policy, and credit was becoming scarce. It was precisely in this environment that MAPE Finserve Private Limited—the entity that would eventually become SBFC Finance—was quietly incorporated.

The timing seemed almost contrarian. As global financial giants were deleveraging and Indian banks were turning conservative, here was a new NBFC being born. But the founders saw what others missed: a massive structural gap in India's credit markets that no amount of global turmoil could close. India's MSME sector, employing over 110 million people and contributing nearly a third of the country's GDP, was chronically underserved by formal financial institutions. Less than 20% had access to institutional credit, relying instead on informal moneylenders charging usurious rates.

The founding structure itself tells a story of ambition meeting pragmatism. This wasn't a bootstrap startup in the traditional sense—it was a professionally managed organization from day one, with institutional backing from Clermont Group (through SBFC Holdings Pte. Ltd. and Clermont Financial Pte. Ltd.) and Arpwood Group as co-promoters. The Singapore-based Clermont Group brought international financial services expertise, while Arpwood brought deep local market knowledge. This combination of global sophistication and local understanding would prove crucial in navigating India's complex lending landscape. The founding team brought a unique blend of skills to the table. Founded by Aseem Dhru and Mahesh Dayani, the company combined financial services expertise with deep operational knowledge. Aseem Dhru, who serves as CEO, brought a vision of reimagining lending for India's underserved segments. The backing from Arpwood Partners, The Clermont and later Malabar Investments provided not just capital but credibility in a market where trust is everything.

In those early years from 2008 to 2017, SBFC operated under the radar as MAPE Finserve, methodically building what would become its competitive moat. While fintech was still a nascent concept in India and digital payments were years away from mainstream adoption, the company focused on unglamorous but essential groundwork: understanding the cash flow patterns of small businesses, developing proprietary underwriting models that could assess creditworthiness beyond traditional metrics, and building relationships in markets where formal credit was viewed with suspicion.

The company's early strategy was deliberately focused. Rather than trying to be everything to everyone, they concentrated on secured MSME loans—loans backed by property that provided a safety net while they learned the intricacies of lending to India's informal economy. This wasn't the sexy, high-margin unsecured lending that would later make companies like Bajaj Finance household names. It was patient, relationship-based lending that required boots on the ground and deep local knowledge.

Consider the typical SBFC customer in those early days: a small manufacturer in Surat running a textile unit, a trader in Indore dealing in agricultural commodities, or a services provider in Coimbatore. These entrepreneurs had been in business for years, often decades, but existed in a parallel financial universe—maintaining impeccable repayment records with suppliers and informal lenders but invisible to the formal banking system. SBFC's innovation wasn't technological; it was methodological. They developed ways to assess these businesses based on actual cash flows rather than formal financial statements, on business relationships rather than credit scores.

The 2008-2017 period was also marked by significant regulatory evolution in India's NBFC sector. The RBI was tightening oversight following the global financial crisis, introducing stricter capital adequacy norms and governance standards. For a young NBFC, this meant higher compliance costs and operational complexity. But it also created barriers to entry that would later protect established players from fly-by-night operators.

By 2017, after nearly a decade of patient building, MAPE Finserve had established a solid foundation. They had developed proprietary underwriting capabilities, built a small but growing loan book, and most importantly, proven that lending to underserved MSMEs could be done profitably and at scale. The company was ready for its next phase—a transformation that would begin with something as simple yet significant as a name change.

The Board approved the change in the name of Company from MAPE Finserve Private Limited to Small Business Fincredit India Private Limited dated July 3, 2017. This wasn't just cosmetic rebranding. It was a declaration of intent, a signal to the market about exactly what space the company intended to own. The name "Small Business Fincredit" left no ambiguity about their target market or value proposition. After nearly a decade of operating in relative obscurity, the company was ready to step into the spotlight.

III. The Pivot & Business Model Evolution (2017-2020)

The summer of 2017 marked a watershed moment in Indian finance. The dust from demonetization was settling, GST was rolling out, and the government's push toward financial formalization was creating unprecedented opportunities for NBFCs focused on the MSME segment. It was against this backdrop that MAPE Finserve made its boldest move yet—completely reinventing itself as Small Business Fincredit India Private Limited.

But the real transformation went far deeper than a name change. This period saw SBFC develop what would become its signature innovation: the PhyGital model. In an era when fintech startups were promising to eliminate human interaction from lending, SBFC went the opposite direction. They developed a "PhyGital" model which uses technology and authentic in-person service to create loans which support the ambitions of customers.

The PhyGital approach wasn't born in a strategy consulting presentation—it emerged from thousands of customer interactions in India's tier-2 and tier-3 cities. The team discovered a fundamental truth about MSME lending in India: while technology could dramatically improve efficiency and reduce costs, the trust required for a business owner to pledge their property as collateral couldn't be built through an app. They engage directly with small business owners and work through loan applications together, in person, at the customer's pace.

Consider a typical loan origination under this model. When a textile shop owner in Erode needs working capital, an SBFC relationship manager doesn't just collect documents and run credit checks. They visit the business, understand its seasonal patterns, meet key suppliers and customers, and build a comprehensive picture that no algorithm could capture. Technology handles the heavy lifting—credit scoring, document verification, risk assessment—but the human relationship manager remains the face of the transaction.

This period also saw SBFC dramatically expand its product portfolio beyond traditional secured MSME loans. They identified gold loans as a massive opportunity, particularly in South India where gold ownership is high and using it as collateral is culturally accepted. Unlike secured business loans that required extensive documentation and property verification, gold loans could be disbursed within hours. It was the perfect complement to their MSME focus—serving the same customer base but addressing different needs and occasions.

The third pillar of their evolved business model was perhaps the most innovative: Loan Management Services (LMS). SBFC recognized that many banks and financial institutions wanted exposure to the MSME segment but lacked the operational infrastructure to service these loans effectively. In addition to providing loans direct to customers, SBFC offers specialist loan management services to third party financial institutions. SBFCs LMS clients benefit from their experienced customer care team managing statements of accounts, repayment schedules, interest certificates and other vital administrative processes on their behalf.

This wasn't just about diversifying revenue streams—it was about positioning SBFC as the infrastructure layer for MSME lending in India. By managing loans for other institutions, they gained insights into different underwriting approaches, expanded their market understanding, and built relationships that would prove valuable for future funding and partnerships.

The rebranding journey continued to evolve. The name was changed from Small Business Fincredit India Private Limited to SBFC Finance Private Limited dated October 24, 2019. This final iteration—SBFC Finance—was cleaner, more memorable, and better suited for a company with ambitions beyond just small business lending. It retained the core identity while allowing room for expansion into adjacent segments.

During this period, SBFC also made crucial decisions about what not to do. While peers were rushing into unsecured personal loans and consumer finance, SBFC stayed focused on secured lending. While others were opening hundreds of branches in a land-grab strategy, SBFC expanded methodically, ensuring each branch achieved profitability before moving to the next market. This discipline would prove crucial when the COVID-19 pandemic struck in early 2020.

The pandemic was the ultimate stress test for SBFC's business model. MSMEs were among the hardest hit, with lockdowns decimating cash flows overnight. Many NBFCs saw their asset quality deteriorate dramatically. But SBFC's focus on secured lending provided a buffer—even if borrowers struggled to repay, the underlying collateral provided protection. More importantly, their PhyGital model proved its worth. While purely digital lenders lost touch with customers during lockdowns, SBFC's relationship managers maintained connections, working with borrowers to restructure loans and navigate the crisis together.

The company's technology investments during this period deserve special mention. They built a proprietary loan origination system that could handle the complexity of MSME lending while remaining simple enough for field staff to use. They invested in data analytics capabilities that could identify early warning signals of stress in loan portfolios. They created digital channels for loan servicing that complemented their physical presence without replacing it.

One of the most telling metrics from this period was employee productivity. Despite the challenging environment, SBFC managed to increase loans per employee while maintaining asset quality. This wasn't achieved through aggressive targets or cost-cutting but through systematic process improvements and technology adoption. Every step of the loan journey was examined and optimized—from lead generation to disbursement to collection.

The unit economics that emerged from this evolution were compelling. While unsecured lenders chased volumes with thin margins and high credit costs, SBFC built a model with healthy spreads, manageable credit costs, and strong operational leverage. Their cost-to-income ratio improved steadily even as they invested in technology and expansion. Their return on assets might not have matched the headline numbers of consumer finance companies, but the consistency and sustainability of returns attracted a different class of investors—those who understood that in financial services, slow and steady often wins the race.

By the end of 2020, SBFC had transformed from a traditional NBFC into something unique in Indian finance—a specialized MSME lender with technology at its core but relationships at its heart, a company that could serve the smallest businesses profitably while building institutional-grade capabilities. The foundation was set for the next phase: aggressive expansion.

IV. Scaling & Geographic Expansion (2019-2022)

In the summer of 2019, as SBFC was finalizing its rebranding, the leadership team gathered for a critical strategy session in Mumbai. The question on the table: How aggressively should they expand? Conservative voices argued for consolidation—perfect the model in existing markets before venturing into new territories. But the data told a different story. Less than 15% of India's 70 million MSMEs had access to formal credit. The opportunity wasn't just large; it was urgent.

The decision they made would transform SBFC from a regional player into a national force. Over the next three years, they would execute one of the most ambitious geographic expansions in India's NBFC sector, growing from a handful of branches to 135 branches as of June 30, 2022, with an expansive footprint in 104 cities spanning 16 Indian states and two union territories.

But this wasn't expansion for expansion's sake. Each new market was chosen deliberately, using a data-driven framework that evaluated multiple factors: MSME density, competitive intensity, availability of collateral, local business culture, and regulatory environment. They discovered, for instance, that textile clusters in Tamil Nadu had fundamentally different financing needs than light engineering units in Punjab, requiring customized products and underwriting approaches.

The numbers from this period tell a remarkable story. The company achieved a CAGR growth of 46% in AUM from FY19 to H1 FY25. To put this in perspective, SBFC was adding more to its loan book every quarter than it had managed in entire years during its early phase. Yet this hypergrowth came with a twist—it was entirely organic.

With a sales team of 1,911 personnel, SBFC maintained 100% in-house loan portfolio origination, reducing reliance on direct selling agents. This was a contrarian bet in an industry where DSAs (Direct Selling Agents) were the norm. While competitors could scale faster using third-party originators, SBFC believed that controlling the entire customer journey was essential for maintaining quality and building lasting relationships.

The gold loan business emerged as a particular bright spot during this expansion. Loan against Gold achieved AUM of Rs 1000 Crore in FY 2025. What made SBFC's approach to gold loans different was their integration with the core MSME business. The same customer who took a secured business loan for capital expenditure could walk into the same branch and get an instant gold loan for working capital needs. It was cross-selling at its most elegant—not pushing products but providing solutions.

Technology became the enabler of this rapid scaling. SBFC developed what they called the "branch-in-a-box" model—a standardized template that could be deployed in any new location within weeks. This included not just physical infrastructure but entire operational workflows, from customer acquisition to loan servicing. New branch managers could tap into centralized underwriting expertise through video calls, combining local knowledge with institutional wisdom.

The company's approach to credit underwriting during this expansion phase deserves special attention. Rather than loosening standards to drive growth—a common trap in financial services—SBFC actually strengthened their risk management. They invested heavily in alternative data sources, partnering with GST networks, bank account aggregators, and industry databases to build a 360-degree view of borrower creditworthiness. They developed sector-specific scorecards that could differentiate between a profitable garment manufacturer and a struggling one, even when both had similar financial statements.

One innovation that proved particularly valuable was their "cluster-based lending" approach. Instead of evaluating businesses in isolation, SBFC mapped entire business ecosystems. In Tirupur's textile cluster, for example, they understood the interconnections between yarn suppliers, fabric processors, garment manufacturers, and exporters. This ecosystem view allowed them to identify both opportunities and risks that individual credit assessments would miss.

The human capital story during this period was equally impressive. SBFC grew from 2,826 employees in March 2023 to 3,758 employees in March 2024, a 33% increase. But more important than the numbers was the quality. SBFC recruited relationship managers from local communities who understood the nuances of regional business practices. They invested heavily in training, creating "SBFC University"—an internal academy that certified employees in everything from credit assessment to customer service.

The geographical diversification strategy paid dividends in risk management. As of March 31, 2023, SBFC's AUM was distributed with 30.84% in North, 38.53% in South, and 30.63% in West and East regions. This balanced portfolio meant that regional economic shocks—whether floods in Kerala or industrial slowdowns in Gujarat—couldn't derail the entire business.

But perhaps the most remarkable achievement of this period was maintaining asset quality despite rapid growth. While industry observers expected credit costs to spike as SBFC entered new markets and segments, the opposite happened. Their gross NPA ratios remained among the best in the industry, validating their thesis that careful underwriting and strong customer relationships could scale without compromising quality.

The operational efficiency gains during this period were substantial. Despite adding hundreds of branches and thousands of employees, SBFC's cost-to-income ratio actually improved. They achieved this through intelligent automation—not replacing humans but augmenting them. Routine tasks like document verification and data entry were automated, freeing relationship managers to focus on what they did best: building trust and understanding businesses.

An interesting subplot during this expansion was SBFC's approach to competition. Rather than engaging in price wars with banks or other NBFCs, they positioned themselves as the specialist—the lender who understood MSMEs better than anyone else. When a small business owner compared offers, SBFC might not always have the lowest rate, but they had the fastest turnaround, the most flexible terms, and the deepest understanding of business needs.

The expansion wasn't without challenges. Entering new markets meant navigating different regulatory requirements, building relationships with local stakeholders, and adapting to regional business practices. In some markets, SBFC faced resistance from entrenched local lenders. In others, they had to overcome skepticism about NBFCs following failures of other players. But each challenge became a learning opportunity, strengthening their playbook for future expansion.

By early 2022, SBFC had achieved something remarkable: they had built one of India's largest MSME-focused lending franchises while maintaining the agility of a startup. They were simultaneously hyperlocal—with deep roots in each market—and truly national in scale and ambition. The stage was set for their next big leap: going public.

V. The IPO Story & Going Public (2022-2023)

The boardroom at SBFC's Mumbai headquarters was unusually quiet on a September morning in 2022. After years of deliberation, the decision had been made: SBFC would go public. The status of the Company converted into a Public Limited Company and the name was changed from SBFC Finance Private Limited to SBFC Finance Limited vide fresh Certificate of Incorporation dated September 30, 2022.

The timing seemed counterintuitive. Global markets were in turmoil—inflation was surging, central banks were hiking rates, and tech stocks were crashing. The IPO market in India had turned decidedly cold after the euphoria of 2021. Yet SBFC's leadership saw opportunity where others saw risk. Their thesis was simple: in uncertain times, investors would gravitate toward businesses with real profits, proven models, and exposure to India's structural growth stories.

The IPO was structured ambitiously: ₹1,025 crores comprising a fresh issue of 105,328,548 equity shares aggregating to Rs 600 Crore and 74,561,402 equity shares aggregating to Rs 425 crore through offer for sale. The fresh capital would fuel the next phase of growth, while the offer for sale would provide partial exits to early investors who had backed the company through its journey.

The roadshow that preceded the IPO was revealing. SBFC's management team crisscrossed Mumbai, Delhi, Singapore, and London, meeting hundreds of institutional investors. The questions were predictable but probing: How sustainable was the 46% CAGR growth? What about asset quality in a rising rate environment? How would they compete with banks getting aggressive in MSME lending?

The answers lay in SBFC's track record. They weren't selling a promise; they were showcasing a proven model. The company had navigated demonetization, GST implementation, and COVID-19 while maintaining growth and profitability. Their secured lending focus provided downside protection. Their PhyGital model created competitive moats that pure digital or pure physical players couldn't replicate.

The IPO opened for bidding from August 3-7, 2023, priced at ₹57 per share. The price band had been carefully calibrated—aggressive enough to reflect SBFC's growth potential but reasonable enough to leave something on the table for investors. The response was closely watched as a barometer of investor appetite for the NBFC sector.

Behind the scenes, the IPO process had been transformative for SBFC as an organization. The preparation required upgrading every aspect of operations—from financial reporting to corporate governance. The company implemented sophisticated MIS systems, strengthened its board with independent directors, and created institutional mechanisms for transparency and accountability. This wasn't just compliance; it was building the infrastructure for the next phase of growth.

The institutional book-building process revealed interesting dynamics. Long-only funds liked the structural MSME opportunity and SBFC's execution track record. Growth investors were attracted by the expansion potential and improving unit economics. Value investors appreciated the reasonable valuations compared to consumer finance peers. The diversity of investor interest validated SBFC's positioning as a unique play on India's formalization story.

On August 16, 2023, SBFC's shares began trading on both BSE and NSE. The listing day performance would set the tone for the company's journey as a public entity. More importantly, it marked SBFC's transition from a privately-held NBFC to a public institution with broader stakeholder responsibilities.

The post-IPO capital allocation strategy revealed management's priorities. Rather than aggressive expansion into new products or geographies, SBFC focused on deepening presence in existing markets. They invested in technology infrastructure, particularly in risk management systems and digital customer interfaces. They strengthened their balance sheet, maintaining capital adequacy well above regulatory requirements.

One interesting development was the company's approach to investor relations post-listing. Unlike many newly listed companies that minimize disclosure, SBFC embraced transparency. They provided detailed operational metrics, conducted regular investor calls, and maintained open channels of communication. This approach helped build credibility with the institutional investor community.

The IPO also catalyzed internal changes. Employee stock options created wealth for long-serving team members, improving retention and motivation. The public market scrutiny pushed operational excellence—every basis point of margin, every percentage of cost reduction, every improvement in asset quality now had direct market impact.

An underappreciated aspect of going public was the signaling effect on customers and partners. Banks became more willing to provide credit lines. Corporate customers saw SBFC as a more credible long-term partner. Even retail customers—the small business owners—took comfort from the regulatory oversight and transparency that came with being a listed entity.

The market's initial reception was just the beginning. The real test would come in delivering on the growth promises made during the IPO while maintaining the discipline that had brought them this far. The proceeds from the fresh issue provided the war chest, but capital was just one ingredient. The bigger challenge was scaling the organization, maintaining culture, and navigating an increasingly competitive landscape.

Looking back, the IPO represented more than a fundraising event. It was SBFC's coming-of-age moment—a validation of their business model, a platform for future growth, and most importantly, a commitment to building one of India's premier MSME lending franchises. The journey from a 2008 startup to a 2023 public listing had been remarkable, but in many ways, the real story was just beginning.

VI. The MSME Lending Opportunity in India

To understand SBFC's trajectory, you must first grasp the sheer magnitude of India's MSME credit gap. Picture this: approximately 70 million micro, small, and medium enterprises operate across India, from the narrow lanes of Chandni Chowk to the industrial estates of Coimbatore. These businesses employ over 110 million people and contribute roughly 30% to India's GDP. Yet, less than 15% of these approximately 70 million MSMEs have access to formal credit as of March 2022.

The math is staggering. If we assume an average credit requirement of just ₹10 lakhs per MSME, the total addressable market exceeds ₹70 trillion. The current formal credit penetration of roughly ₹15 trillion leaves an unaddressed gap of over ₹55 trillion—larger than the entire Indian banking system's loan book. This isn't just a market opportunity; it's a structural inefficiency that constrains India's economic potential.

But why does this gap exist? The reasons are both simple and complex. Traditional banks, designed for either large corporate lending or mass retail products, struggle with the MSME segment's unique characteristics. These businesses often lack formal financial statements, their cash flows are irregular, and the ticket sizes—typically ₹5-50 lakhs—are too small for corporate banking but too complex for retail banking's standardized products.

SBFC positioned itself precisely in this sweet spot. The company focuses on disbursing loans with ticket size of ₹0.50 million to ₹3.00 million, targeting tier II and tier III cities. This wasn't arbitrary—it was based on deep market analysis. Loans below ₹5 lakhs could be served by microfinance institutions, while those above ₹30 lakhs attracted banks' attention. The ₹5-30 lakh segment was the orphan child of Indian finance.

The geographic focus on tier-2 and tier-3 cities was equally strategic. While Mumbai and Delhi grabbed headlines, the real entrepreneurial energy in India pulsed through places like Surat, Rajkot, Coimbatore, and Visakhapatnam. These cities housed thousands of small manufacturers, traders, and service providers who formed the backbone of India's economy but remained invisible to formal financial institutions.

The average secured MSME loan size of less than ₹10 lakhs in FY 2022 tells another story. SBFC wasn't cherry-picking the largest, safest borrowers in the MSME space. They were going deep, serving the true micro and small enterprises that others ignored. This required a fundamentally different operating model—one that could profitably serve smaller ticket sizes through operational efficiency and technology leverage.

The competitive landscape in MSME lending presents a fascinating study in contrasts. On one side, public sector banks hold the largest share but struggle with bureaucracy and risk aversion. Private banks focus on the creamy layer—the larger, more formal MSMEs. Microfinance institutions serve the bottom of the pyramid but lack the products for growth capital. Fintech lenders promise disruption but struggle with credit assessment and collection in the absence of physical presence.

SBFC carved out a unique position in this landscape. Unlike banks, they could move fast and customize solutions. Unlike MFIs, they could provide larger, longer-tenure loans. Unlike pure fintech players, they had the physical presence to build trust and handle collections. They became what one might call a "Goldilocks lender"—not too big, not too small, but just right for the vast middle of India's MSME segment.

The regulatory environment added another layer of complexity and opportunity. The RBI's evolving framework for NBFCs created both challenges and competitive advantages. Stricter capital requirements and governance norms raised entry barriers, protecting established players like SBFC from fly-by-night operators. Priority sector lending requirements for banks created partnership opportunities, where banks could meet their targets by funding NBFCs focused on MSMEs.

Government initiatives like GST and digital payments were gradually formalizing the MSME sector, making credit assessment easier and reducing risk. The Udyam registration portal was creating a verified database of MSMEs. The Account Aggregator framework was enabling consent-based financial data sharing. These developments were expanding the addressable market for formal credit while improving the economics of serving it.

But perhaps the most compelling aspect of the MSME opportunity was its resilience and growth potential. Unlike consumer lending, which is discretionary and cyclical, MSME lending serves productive purposes—working capital to buy inventory, term loans to expand capacity, equipment finance to improve productivity. These loans create economic value, generating the cash flows to repay them.

The social impact dimension added another layer of appeal. Every MSME loan from SBFC didn't just generate returns for shareholders; it created jobs, enabled entrepreneurship, and contributed to economic development. In a country where job creation remains the paramount challenge, MSME lending was both profitable and purposeful.

SBFC's loan management services offering revealed another dimension of the opportunity. They help institutional lenders manage all aspects of loan servicing including client relations, collections, payments, porting, and data storage. This positioned SBFC not just as a lender but as infrastructure for the broader MSME credit ecosystem. Banks and financial institutions that wanted MSME exposure without operational complexity could leverage SBFC's capabilities.

The unit economics of MSME lending, when done right, were compelling. Interest rates of 12-16% provided healthy spreads over funding costs. Secured lending kept credit costs manageable. The relationship-based model created switching costs and enabled cross-selling. Operating leverage improved with scale as fixed costs were spread over a larger book.

Yet challenges remained. Credit assessment required sophisticated models and deep market knowledge. Collection required extensive field force and persistent follow-up. Competition was intensifying as everyone from banks to fintechs recognized the opportunity. Regulatory changes could alter economics overnight.

SBFC's approach to these challenges revealed their strategic thinking. Rather than competing on price, they competed on service—faster turnaround, flexible terms, and deeper understanding. Rather than avoiding competition, they welcomed it as validation of the market opportunity. Rather than fearing regulation, they embraced it as a barrier to entry for weaker players.

The MSME lending opportunity in India wasn't just large; it was transformative. It represented the financial inclusion story beyond retail microfinance, the productivity unlock for India's economy, and the sustainable growth engine for financial institutions. SBFC had positioned itself at the center of this opportunity, with the capabilities to capture it and the discipline to do so profitably.

VII. Current Business & Operating Model

Walk into any SBFC branch in early 2024, and you'll witness a fascinating dance between old and new India. In the waiting area, a textile trader from the local market sits next to a young entrepreneur running an e-commerce fulfillment center. One has brought cloth-bound ledgers; the other shows cash flows on a tablet. Both need credit, both have collateral, and both represent SBFC's evolved operating model—serving traditional businesses while capturing new economy opportunities.

The numbers tell a story of controlled aggression. With 28% YoY growth in AUM reaching INR 8,747 crores, the company is targeting over 20% growth in disbursals and aiming to cross INR 10,000 crores in AUM. This isn't hypergrowth by fintech standards, but for a secured lender maintaining asset quality, it represents impressive execution.

The geographic footprint has evolved into a sophisticated portfolio strategy. The concentration isn't in the metros where competition is fierce and customers are over-banked. Instead, SBFC has built density in India's economic workhorses—the tier-2 and tier-3 cities where real businesses make real products. A branch in Tirupur serves textile exporters, one in Rajkot caters to engineering units, another in Kanpur focuses on leather goods manufacturers. Each branch becomes a specialized node in a national network.

The technology story at SBFC challenges conventional wisdom about digital transformation. Rather than replacing human interaction, technology amplifies it. The paperless gold loan process doesn't eliminate the branch visit—it makes it faster and more pleasant. AI-assisted credit assessments don't replace relationship managers' judgment—they augment it with data-driven insights. The philosophy is consistent: technology should reduce friction, not relationships.

Consider the loan origination process. When a ceramic tile manufacturer in Morbi needs expansion capital, the journey begins with a relationship manager who speaks Gujarati, understands the ceramic industry's cycles, and knows the local market dynamics. But behind this familiar face lies sophisticated technology. The RM's tablet pulls GST data to verify revenues, analyzes bank statements through APIs, and runs the application through AI models trained on thousands of similar cases. Documents are uploaded digitally, verification happens through blockchain-based systems, and credit decisions that once took weeks now happen in days.

The product portfolio has evolved thoughtfully. Secured MSME loans remain the core, but with increasing sophistication. There are specific products for different industries, tenure options aligned with business cycles, and flexibility in repayment structures. The gold loan business has emerged as more than just a side product—it's become a customer acquisition tool, a liquidity solution for existing clients, and a counter-cyclical hedge when business loans slow.

The company incorporated a subsidiary, SBFC Home Finance Private Limited, on December 6, 2022. This wasn't random diversification—it was logical extension. The same customers who borrowed for business expansion also needed home loans. The same property evaluation capabilities used for business loans could assess residential collateral. The same distribution network could serve both needs.

The loan management services business reveals SBFC's ambition to be more than just a lender. Apart from handling the porting of repayment modes (NACH/ECS) and transferring EMIs between accounts, for delinquent loans, they provide complete support including phone calls, SMS outreach and field visits. Moreover, SBFCs loan Management Service initiates and executes all legal cases relating to delinquent and non-performing asset accounts. This positions SBFC as the operating system for MSME lending—others provide capital, SBFC provides capability.

Risk management has evolved from defensive to strategic. Rather than avoiding risk, SBFC prices it appropriately. They've developed granular scorecards for different segments—a kirana store in Bihar has different risk characteristics than an auto parts manufacturer in Chennai. Early warning systems flag stress before it becomes delinquency. Portfolio limits ensure no single industry or geography can destabilize the book.

The funding strategy showcases financial sophistication. SBFC doesn't rely on a single source—they tap banks, issue NCDs, securitize portfolios, and access capital markets. This diversification ensures they're never held hostage by funding constraints. More importantly, they match assets and liabilities carefully, avoiding the ALM mismatches that have felled many NBFCs.

The organizational structure balances centralization with autonomy. Credit policies are set centrally, but execution happens locally. Technology platforms are standardized, but product features can be customized. Risk frameworks are non-negotiable, but business development strategies vary by market. It's a federated model that combines the best of both worlds—institutional strength with entrepreneurial agility.

With 3,758 employees as of March 31, 2024, SBFC has built significant human capital. But more impressive than the number is the composition. There are engineers building technology platforms, MBAs designing products, chartered accountants managing risk, and most importantly, thousands of feet-on-street personnel who understand local markets intimately. The average employee age skews young, bringing energy and adaptability to a traditional industry.

The customer experience philosophy permeates every interaction. Loan applications are designed to be simple without being simplistic. Documentation requirements are minimized without compromising risk management. Disbursement happens quickly but not carelessly. Collections are persistent but not aggressive. It's a delicate balance that requires constant calibration.

The financial performance reflects operational excellence. Net interest margins remain healthy despite competitive pressure. Operating expenses grow slower than assets, demonstrating operating leverage. Credit costs stay controlled despite rapid growth. Return ratios might not match aggressive unsecured lenders, but the consistency and sustainability appeal to long-term investors.

Innovation at SBFC happens in small, continuous improvements rather than big bang disruptions. They've introduced WhatsApp-based servicing for customer convenience. They've created industry-specific loan products based on customer feedback. They've implemented tablet-based applications to reduce paperwork. Each innovation is tested, measured, and scaled methodically.

The partnership ecosystem extends SBFC's reach without expanding its balance sheet. Tie-ups with equipment manufacturers enable vendor financing. Collaborations with e-commerce platforms facilitate merchant lending. Relationships with corporate help serve their supplier networks. These partnerships create win-win situations—partners get financial solutions for their ecosystems, SBFC gets pre-qualified customer leads.

Competition has intensified, but SBFC's response has been strategic rather than reactive. When banks cut rates, SBFC emphasizes speed and flexibility. When fintechs tout technology, SBFC highlights relationships and trust. When peers expand aggressively, SBFC focuses on quality and sustainability. They've learned that in financial services, there's no single winning strategy—success comes from consistent execution of a chosen approach.

Looking at SBFC's current operations, what emerges is a picture of maturity without complacency. They've built significant scale but maintain startup-like agility. They've embraced technology but haven't abandoned human touch. They've diversified products but maintained focus on core strengths. It's an operating model built for the long haul—resilient enough to weather storms, flexible enough to capture opportunities, and disciplined enough to generate sustainable returns.

VIII. Playbook: Building an NBFC in India

If you wanted to build the next SBFC, where would you start? Not with capital or technology or even a banking license. You'd start with a fundamental insight that SBFC's founders grasped early: in India, credit isn't just about risk and return—it's about trust, relationships, and deep market understanding. The playbook that emerges from SBFC's journey offers lessons that transcend the NBFC sector.

Capital Efficiency and the Art of Patient Growth

Most NBFCs fail not because they can't grow but because they grow too fast. SBFC's approach to capital has been almost Buddhist in its mindfulness. They understood that in lending, capital isn't just fuel for growth—it's a buffer against mistakes. Every rupee of equity supports roughly 5-6 rupees of lending, but also absorbs losses when loans go bad.

The discipline starts with pricing. SBFC doesn't chase market share with below-market rates. They price for risk, operations, and reasonable returns. A 14% interest rate might seem high compared to bank rates, but when you factor in the cost of serving small tickets, managing cash-based businesses, and maintaining field forces, the economics become clear. The question isn't "What's the lowest rate we can offer?" but "What rate ensures sustainable service to this segment?"

Funding strategy reveals another layer of sophistication. SBFC maintains relationships with multiple banks, ensuring no single institution can choke their growth. They access capital markets through NCDs, but carefully manage rollover risk. They securitize portfolios to free up capital, but retain skin in the game. Each funding source is optimized for cost, stability, and flexibility.

Building Trust in the India That Doesn't Trust

Here's a paradox: the customers who most need formal credit are often the most suspicious of it. The small businessman who's been borrowing from local moneylenders for generations doesn't trust banks. The family that's pledged gold to neighborhood jewelers doesn't understand NBFCs. SBFC cracked this code through what might seem like an old-fashioned approach: presence and persistence.

Every SBFC branch is deliberately located not in glass towers but in the commercial hearts of cities—near wholesale markets, industrial areas, and business clusters. The branch managers aren't fresh MBAs but often local residents who understand the community. They attend business association meetings, sponsor local events, and gradually become part of the ecosystem. Trust isn't downloaded; it's earned through repeated interactions.

The PhyGital model isn't just operational philosophy—it's trust architecture. Technology handles the objective aspects (document verification, credit scoring, disbursement), while humans manage the subjective elements (understanding business cycles, family dynamics, future plans). Customers trust the efficiency of technology but need the reassurance of human judgment.

When to Use Tech vs Human Touch

SBFC's technology adoption follows a clear principle: automate the mundane, humanize the critical. Document collection? Digital. But the conversation about why the business needs money? Always human. Credit scoring? AI-powered. But the final decision on a borderline case? Experienced credit manager. EMI collection? Automated NACH. But when payments are missed? Relationship manager's phone call.

This selective digitization has profound implications. It keeps costs low without sacrificing service quality. It scales operations without losing local touch. It attracts tech-savvy young entrepreneurs while retaining traditional businessmen. Most importantly, it creates defensible moats—any pure tech player can replicate SBFC's digital infrastructure, but combining it with thousands of trained relationship managers takes years.

Risk Management: The Boring Stuff That Matters

In lending, risk management isn't a department—it's a culture. SBFC's approach starts with selection. They don't lend to everyone who qualifies; they lend to those they understand. A profitable business in an unfamiliar industry might get rejected, while a struggling business in a known sector might get supported. This isn't arbitrary—it's recognition that in MSME lending, industry knowledge matters more than financial metrics.

Portfolio construction follows similar discipline. No single industry exceeds 15% of the book. No geographic region dominates. No customer segment becomes oversized. This diversification isn't just risk management—it's learning strategy. Each new segment teaches something about credit behavior, business cycles, and market dynamics.

Early warning systems catch problems before they become NPAs. A delay in GST filing might signal cash flow stress. Frequent requests for restructuring might indicate deeper problems. Changes in transaction patterns could suggest business disruption. These signals trigger proactive engagement—not aggressive collection but supportive intervention.

Navigating India's Regulatory Labyrinth

Working in India's financial sector means navigating between multiple regulators, changing rules, and varying state-level requirements. SBFC's approach has been to stay ahead of compliance rather than catching up to it. They implemented corporate governance standards before going public. They strengthened capital adequacy before RBI mandated it. They adopted technology standards before digital lending guidelines emerged.

This proactive compliance has strategic value. It builds regulatory comfort, enabling faster approvals for new initiatives. It attracts institutional investors who value governance. It creates operational discipline that improves efficiency. Most importantly, it avoids the disruptions that regulatory actions can cause.

Distribution Economics and the Branch Paradox

In an age of digital everything, SBFC's investment in physical branches seems anachronistic. But the economics tell a different story. A branch in a tier-2 city might cost ₹50 lakhs annually to operate. If it originates ₹25 crores in loans generating 4% net interest margin, that's ₹1 crore in annual revenue. Add fee income, cross-selling, and operating leverage, and branches become profit centers, not cost centers.

But branches aren't just about economics—they're about ecosystem presence. They become gathering places for local businesses, information nodes for market intelligence, and trust anchors for communities. The branch manager becomes more than a banker—they become advisor, connector, and sometimes counselor to local entrepreneurs.

Building Institutional Capabilities While Staying Nimble

As organizations grow, they typically face a tradeoff between scale and agility. SBFC has managed this through what might be called "structured flexibility." Core processes (credit approval, risk management, compliance) are standardized and centralized. But execution (customer acquisition, relationship management, problem resolution) remains decentralized and flexible.

Technology platforms enable this balance. A centralized loan origination system ensures consistency, but local teams can configure products for market needs. Risk models are developed centrally but calibrated locally. Training is standardized but contextualized for regional variations.

The Talent Equation

Building an NBFC isn't just about capital and technology—it's about people. SBFC's HR strategy reflects this understanding. They hire for attitude and train for skills. A relationship manager needs empathy more than Excel skills. A branch manager needs leadership more than lending expertise.

The training investment is substantial. New joiners undergo weeks of classroom and field training. Existing employees receive continuous skill upgrades. High performers are rotated across functions to build holistic understanding. This isn't cost—it's investment in organizational capability.

Lessons on Scaling Lending Businesses

The SBFC playbook ultimately reveals that scaling a lending business isn't about choosing between growth and quality, technology and touch, efficiency and effectiveness. It's about finding the right balance for your chosen segment and executing consistently.

Some principles emerge clearly: Start with a segment you deeply understand. Build trust before you build book. Invest in technology that enhances human capability rather than replacing it. Manage risk through knowledge, not just models. Stay ahead of regulation rather than reacting to it. Create economics that work at small scale but improve with size. Most importantly, remember that in lending, reputation is the ultimate asset—built over years, destroyed in moments.

The playbook isn't complete—it's still being written as SBFC navigates new challenges and opportunities. But the chapters written so far offer valuable lessons for anyone trying to build in India's complex, competitive, but ultimately rewarding financial services landscape.

IX. Bear vs Bull Case & Analysis

Let's strip away the corporate speak and examine SBFC with the cold, calculating eye of a fundamental investor. Every investment thesis has two sides, and SBFC's story—compelling as it might be—is no exception.

The Bull Case: Riding India's Formalization Wave

Bulls see SBFC as perfectly positioned at the intersection of multiple structural trends. India's formalization drive isn't slowing down—if anything, it's accelerating. GST has brought millions of businesses into the tax net. Digital payments have made cash flows visible. Credit bureaus are capturing more data. Each development expands SBFC's addressable market while reducing their risk.

The numbers support the optimism. Among MSME-focused companies, SBFC Finance has one of the highest AUM growth rates in the industry. The company has achieved a CAGR growth of 46% in AUM from FY19 to H1 FY25. This isn't a flash in the pan—it's sustained execution over multiple years through various economic cycles.

The market opportunity remains massively underpenetrated. Even if formal credit penetration to MSMEs doubles from 15% to 30% over the next decade, that represents a tripling of the current market. SBFC needs to capture just a tiny slice of this growth to deliver substantial returns. Their proven execution capabilities, established distribution network, and strong brand in target markets position them to capture more than their fair share.

The business model has proven its resilience. SBFC navigated demonetization, GST implementation, and COVID-19 not just surviving but growing. Their secured lending focus provides a buffer against credit losses. Their diversified geographic and sectoral presence prevents concentration risks. Their PhyGital model creates competitive moats that neither pure digital nor pure physical players can easily replicate.

Operational leverage is kicking in. As the branch network matures and technology investments bear fruit, costs are growing slower than revenues. The company is generating increasing returns on assets and equity. This isn't hypothetical—it's visible in the improving cost-to-income ratios and expanding margins.

The management team has demonstrated execution excellence. They've delivered on IPO promises, maintained asset quality during rapid growth, and navigated regulatory changes successfully. This track record builds confidence that future targets are achievable.

The Bear Case: Storm Clouds Gathering

Bears point to several red flags that bulls might be overlooking. Start with the fundamental concern: Company has a low return on equity of 10.9% over last 3 years. For a financial services company in a high-growth phase, this is disappointing. If SBFC can't generate better returns during good times, what happens when the cycle turns?

The dividend policy—or lack thereof—raises questions. Though the company is reporting repeated profits, it is not paying out dividend. This might signal that management sees better reinvestment opportunities, or it could indicate that profits aren't as robust as they appear. For income-focused investors, this is a deal-breaker.

Competition is intensifying from every direction. Banks are aggressively pushing into MSME lending, armed with lower funding costs and established relationships. Fintech players are using technology to slash operating costs and improve customer experience. New-age NBFCs are raising massive venture funding to grab market share. SBFC's moats might not be as deep as they appear.

The macro environment poses risks. Rising interest rates increase funding costs faster than lending rates can be adjusted. Economic slowdown hits MSMEs first and hardest. Regulatory changes could alter economics overnight—remember how RBI's guidelines transformed microfinance economics? SBFC operates in a sector where rules can change dramatically with little warning.

Asset quality concerns lurk beneath the surface. Rapid growth often masks credit problems that only emerge during downturns. SBFC's secured lending provides some protection, but property values can fall, businesses can fail, and even secured loans can become NPAs. The true test of their underwriting will come during the next economic downturn.

The technology transition risk is real. While SBFC talks about PhyGital, pure digital players are building AI-powered lending platforms that could make traditional models obsolete. If someone cracks the code on fully digital MSME lending—combining lower costs with good risk management—SBFC's branch-heavy model could become a liability.

Geographic concentration in certain markets could backfire. While SBFC has expanded nationally, they still have significant exposure to specific regions and industries. A localized economic shock—like the Kerala floods or Gujarat's industrial slowdown—could disproportionately impact their portfolio.

The Analytical Middle Ground

Stepping back from bull and bear extremes, several key questions emerge for investors:

Sustainability of Growth: Can SBFC maintain 20%+ growth without compromising asset quality? History suggests this is difficult in financial services. The company will need to continuously find new pockets of growth while maintaining underwriting discipline.

Competitive Positioning: Is SBFC's PhyGital model a sustainable differentiator or a temporary advantage? As technology improves and customer behavior evolves, the need for physical presence might diminish. Alternatively, the relationship aspect might become even more valuable as lending becomes commoditized.

Return Profile: Will returns on equity improve with scale, or is 10-12% the structural ceiling for this business model? This determines whether SBFC is a growth story or a value trap. Investors need clarity on the path to 15%+ ROEs that justify premium valuations.

Capital Allocation: How will management balance growth investment with shareholder returns? The lack of dividends might be justified during high growth, but at what point do shareholders see cash returns? The capital allocation track record post-IPO will be crucial.

Regulatory Evolution: How will changing regulations impact SBFC's business model? The RBI is increasingly focused on digital lending, customer protection, and systemic risk. New guidelines could either create opportunities or impose constraints.

The Verdict: Measured Optimism with Eyes Wide Open

The weight of evidence tilts bullish, but with important caveats. SBFC operates in an attractive market with proven execution capabilities and a differentiated model. The structural opportunity in MSME lending is real and lasting. The company has demonstrated resilience through multiple cycles.

However, the low returns on equity, intensifying competition, and regulatory uncertainties warrant caution. This isn't a "buy and forget" investment—it requires continuous monitoring of execution, competition, and market dynamics.

For long-term investors, SBFC represents a play on India's formalization and financial inclusion story. But success isn't guaranteed—it will require continued execution excellence, strategic evolution, and some luck with the economic cycle. The bull case is compelling, but the bear concerns are valid. As always in investing, the truth likely lies somewhere in between.

X. Future Outlook & Strategic Priorities

The conference room at SBFC's headquarters buzzes with controlled energy as the leadership team maps out the next five years. The whiteboard is covered with arrows, circles, and ambitious numbers. But the real story isn't in the targets—it's in the strategic choices that will determine whether SBFC becomes a defining institution in Indian finance or merely another successful NBFC.

The Digital Transformation Imperative

SBFC's digital journey isn't about replacing branches with apps—it's about reimagining the lending experience for the next generation of entrepreneurs. The young manufacturer in Coimbatore running a 3D printing business has different expectations than his father who ran a traditional engineering unit. He wants instant decisions, seamless documentation, and digital servicing—but still values the relationship and trust that SBFC provides.

The roadmap focuses on three pillars. First, end-to-end digitization of the customer journey. Loan applications through video KYC, AI-powered instant decisions for pre-approved customers, and API-based disbursements directly to vendor accounts. Second, data analytics for deeper customer understanding. Transaction analysis to predict credit needs, early warning systems to prevent NPAs, and personalized product recommendations based on business patterns. Third, platform approach to lending. Open APIs that allow partners to embed SBFC's lending capabilities, white-label solutions for corporate supply chain financing, and marketplace models connecting borrowers with multiple funding sources.

But technology alone isn't the answer. SBFC's insight is that in MSME lending, technology should eliminate friction, not relationships. The future model might see AI handling routine decisions while relationship managers focus on complex cases, advisory services, and customer success.

New Product Opportunities: Beyond Traditional Lending

The product pipeline reveals ambitious thinking. Supply chain financing emerges as a natural extension—SBFC already understands small suppliers; partnering with large corporates to finance their vendor networks is logical evolution. Revenue-based financing for digital-first businesses, where repayments flex with sales, addresses new-economy entrepreneurs who don't fit traditional lending models.

Embedded finance represents another frontier. Instead of customers coming to SBFC, SBFC's lending gets embedded where customers already are—accounting software, e-commerce platforms, payment systems. Imagine a Shopify seller getting working capital offers based on real-time sales data, or a restaurant on Zomato accessing loans tied to order volumes.

The home finance subsidiary opens doors to comprehensive financial solutions. The same customer who takes business loans, gold loans, and home loans from SBFC becomes deeply embedded in the ecosystem. Cross-selling isn't about pushing products—it's about being the complete financial partner for India's entrepreneurs.

Geographic Expansion: Depth vs Breadth

The expansion strategy faces a classic dilemma: go deeper in existing markets or enter new geographies? SBFC's choice is nuanced—selective expansion into adjacent markets while building density in strongholds. This isn't about planting flags but building sustainable franchises.

The focus shifts eastward. States like Odisha, Jharkhand, and the North-East remain underserved by formal credit. These markets require patience—understanding local business practices, building trust with communities, and adapting products for regional needs. But they offer virgin territory where SBFC can establish dominant positions before competition arrives.

Urban expansion takes a different form. Instead of competing in saturated metros, SBFC targets emerging satellite cities—Gurugram's Manesar, Chennai's Sriperumbudur, Pune's Chakan. These industrial corridors house thousands of MSMEs serving large manufacturers, creating concentrated lending opportunities.

Partnership and Ecosystem Play

The future of financial services isn't about solo excellence but ecosystem orchestration. SBFC's partnership strategy reflects this understanding. Co-lending with banks combines their capital with SBFC's origination capabilities. Fintech collaborations bring technological innovation without building everything in-house. Corporate partnerships open access to pre-qualified customer bases.

The loan management services business positions SBFC as infrastructure for the broader ecosystem. As more institutions recognize the MSME opportunity but lack operational capabilities, SBFC becomes the execution partner. This capital-light, fee-based model provides steady returns while building strategic relationships.

Government partnerships could unlock massive opportunities. As schemes like MUDRA and Stand-Up India expand, efficient execution partners become crucial. SBFC's ground presence and operational expertise position them as natural implementation partners for public sector initiatives.

Competition from New-Age Fintechs

The fintech challenge is real and evolving. Players like Lendingkart, Capital Float, and NeoGrowth have raised massive funding to disrupt MSME lending. Their advantages are clear: lower operating costs, superior customer experience, and data-driven decision-making. But SBFC's response isn't defensive mimicry—it's strategic differentiation.

While fintechs excel at small-ticket, short-tenure loans, SBFC focuses on larger, longer-term funding that requires deeper underwriting. While fintechs rely on digital channels, SBFC's physical presence provides comfort for collateral-based lending. While fintechs optimize for growth, SBFC balances growth with profitability and sustainability.

The real competition might not be head-to-head but segment-by-segment. Fintechs might dominate sub-₹5 lakh unsecured lending, while SBFC owns the ₹10-30 lakh secured space. The market is large enough for multiple winners if each finds their niche and executes well.

The ESG and Impact Narrative

Environmental, Social, and Governance considerations are moving from compliance to strategy. SBFC's inherent model—financing small businesses, creating employment, and enabling entrepreneurship—has strong social impact. But articulating and measuring this impact becomes crucial for attracting ESG-focused capital.

Green financing emerges as opportunity and responsibility. Funding solar installations for MSMEs, supporting electric vehicle adoption in commercial transportation, and enabling energy-efficient equipment upgrades align profit with purpose. These aren't CSR initiatives but core business opportunities that happen to have positive environmental impact.

Governance strengthening continues post-IPO. Independent board oversight, transparent disclosure, and stakeholder engagement build institutional credibility. This isn't just about compliance—strong governance attracts quality capital, enables strategic partnerships, and builds long-term sustainability.

The 2030 Vision

Looking toward the decade's end, SBFC's ambition crystallizes. They envision becoming the definitive MSME lending platform in India—not necessarily the largest but certainly the most trusted and innovative. This means:

- AUM crossing ₹25,000 crores through organic growth and strategic expansion

- Technology platform that others want to plug into rather than compete against

- Product suite covering the complete financial lifecycle of an MSME

- Geographic presence in 200+ cities with digital reach everywhere

- Return on equity consistently above 15% demonstrating sustainable profitability

- Market leadership in 2-3 specialized segments where they have unique expertise

But beyond numbers, the vision is about institutional building. Creating an organization that outlasts founders, survives cycles, and continuously evolves. Building a brand that becomes synonymous with MSME lending. Developing capabilities that become competitive moats. Most importantly, having meaningful impact on millions of entrepreneurs who power India's economy.

The Path Forward: Execution Amid Uncertainty

The future won't unfold linearly. Economic cycles will test resilience. Regulatory changes will force adaptation. Competition will intensify. Technology will disrupt. But SBFC's strategic priorities provide a framework for navigating uncertainty:

- Maintain the balance between growth and quality—rapid expansion without compromising underwriting discipline

- Invest in technology and talent—building capabilities for tomorrow while delivering results today

- Deepen customer relationships—becoming indispensable partners rather than mere lenders

- Strengthen the balance sheet—maintaining capital buffers and funding diversity for all scenarios

- Evolve the business model—staying relevant as customer needs and market dynamics change

The outlook is optimistic but grounded. SBFC has the market opportunity, execution capabilities, and strategic clarity to build something significant. But success isn't guaranteed—it requires continued focus, disciplined execution, and ability to evolve with changing times.

XI. Epilogue & Key Takeaways

As our deep dive into SBFC Finance draws to a close, it's worth stepping back to contemplate what this journey reveals—not just about one company, but about building in India's financial services landscape, serving the underserved profitably, and creating lasting institutions in rapidly evolving markets.

What SBFC Teaches Us About Financial Inclusion

Financial inclusion isn't charity—it's a massive business opportunity waiting for the right approach. SBFC proved that serving MSMEs, often considered too risky or unprofitable by traditional lenders, can generate sustainable returns. But success requires patience, deep market understanding, and willingness to build capabilities that others haven't.

The key insight: financial inclusion isn't about lowering standards or accepting lower returns. It's about developing new ways to assess creditworthiness, building distribution that reaches underserved segments, and creating products that match actual needs. SBFC's secured lending model, PhyGital approach, and relationship focus weren't compromises—they were innovations tailored to their market.

Building in Regulated Spaces: Constraints as Competitive Advantages

Operating as an NBFC in India means navigating complex, evolving regulations. Many see this as a burden. SBFC turned it into strategic advantage. By staying ahead of compliance, building institutional governance early, and maintaining conservative practices, they created trust with regulators, investors, and customers.

The lesson extends beyond financial services. In any regulated industry, companies that view compliance as strategic capability rather than cost center often win long-term. Regulations create barriers to entry, customer trust, and operational discipline. SBFC's journey from startup NBFC to listed company demonstrates how regulatory navigation can become competitive moat.

The India Opportunity: Beyond Unicorns and Startups

While media celebrates unicorns and disruptors, SBFC represents another kind of India opportunity—building substantial, profitable businesses by solving real problems for real customers. No fancy business models, no blitzscaling, no venture capital steroids. Just disciplined execution in a large, underserved market.

This approach might seem old-fashioned, but the results speak for themselves. SBFC built a ₹11,000+ crore market cap company while maintaining profitability, without raising excessive venture capital, and without burning cash for growth. It's a reminder that in India's diverse economy, there are multiple paths to building significant businesses.

The Biggest Surprises from the Research

Several findings challenged conventional wisdom:

First, the low return on equity (10.9% over three years) despite strong growth and market position. This suggests that MSME lending, even when done well, might have structural return limitations that investors must factor into valuations.

Second, the resilience through multiple economic shocks. From demonetization to COVID-19, events that should have devastated an MSME lender instead became proof points for SBFC's model. This wasn't luck—it was the result of conservative underwriting and strong customer relationships.

Third, the power of physical presence in an increasingly digital world. While everyone preaches digital-first, SBFC's branch-based model continues delivering growth and profitability. The lesson: in India, the future isn't digital or physical—it's both, intelligently integrated.

Fourth, the lack of dividend payments despite repeated profits. This suggests either exceptional reinvestment opportunities or management's preference for growth over shareholder returns—a crucial consideration for investors.

Lessons for Founders

Entrepreneurs building in India can extract several lessons from SBFC's playbook:

Start narrow, expand deliberately: SBFC began with secured MSME loans in select markets before expanding products and geography. Depth before breadth builds expertise and economics.

Build trust before scale: In markets where formal institutions have limited credibility, trust becomes the ultimate differentiator. SBFC invested years building relationships before aggressive expansion.

Technology amplifies but doesn't replace human judgment: In complex, relationship-driven businesses, technology should enhance human capability rather than eliminate it.

Patient capital enables patient building: SBFC's institutional backing allowed long-term thinking. Quick returns and sustainable businesses often don't mix.

Regulatory compliance is strategic capability: Building ahead of regulation rather than catching up creates competitive advantages and avoided disruption.

Lessons for Investors

For those evaluating opportunities in India's financial services sector, SBFC offers a framework:

Market size doesn't guarantee returns: The MSME lending opportunity is massive, but structural factors might cap returns. Understanding unit economics matters more than addressable market.

Execution quality differentiates winners: In commoditized products like lending, operational excellence, risk management, and distribution create sustainable advantages.

Growth and profitability can coexist: SBFC proved that 30-40% growth doesn't require burning cash. Sustainable growth might be slower but creates more value long-term.

Management quality matters enormously: In financial services, where leverage amplifies both returns and mistakes, leadership judgment becomes crucial.

Patience pays: SBFC took 15 years from founding to IPO. Significant value creation in complex sectors takes time.

The Unanswered Questions

Despite comprehensive analysis, questions remain:

Will SBFC's returns on equity improve with scale, or is 10-12% the structural ceiling? Can the PhyGital model remain relevant as digital natives become business owners? How will the competitive landscape evolve as everyone from banks to Big Tech enters MSME lending? Will regulatory changes help or hinder SBFC's model?

These uncertainties aren't weaknesses in the analysis—they're inherent to investing. SBFC's future depends on execution choices, competitive dynamics, and macroeconomic factors that can't be fully predicted.

Final Reflections

SBFC Finance isn't just another NBFC—it's a case study in building financial institutions for the India that exists, not the India we imagine. While others chase affluent consumers in metros, SBFC serves textile traders in Tirupur. While others pursue unsecured lending's high margins, SBFC maintains discipline with secured loans. While others optimize for valuation multiples, SBFC focuses on sustainable growth.

This isn't to say SBFC's approach is superior—different strategies work for different companies. But in a market often dominated by hype and headlines, SBFC represents something valuable: proof that boring businesses solving real problems for underserved segments can create substantial value.

The journey from 2008 startup to 2024 public company wasn't smooth or predetermined. It required navigating financial crises, regulatory changes, competitive threats, and pandemic disruptions. But through disciplined execution, strategic focus, and deep market understanding, SBFC built something significant—a platform for MSME lending that serves customers, generates returns, and contributes to India's economic development.

As India's economy formalizes and MSMEs increasingly access institutional credit, companies like SBFC will play crucial roles. They're the bridges between informal and formal economies, the enablers of entrepreneurship, and the builders of India's economic foundation. Understanding their models, challenges, and opportunities becomes essential for anyone interested in India's financial future.

The SBFC story continues to unfold. New chapters will be written as technology evolves, competition intensifies, and markets develop. But the lessons from their journey so far—about building in regulated markets, serving underserved segments, and creating sustainable value—will remain relevant for founders, investors, and observers of India's remarkable economic transformation.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube