AAVAS Financiers: Building Dreams in Bharat's Heartland

I. Introduction & Setting the Stage

The Null Value

Picture a two-room house going up on the edge of a small town in Rajasthan. There is no builder, no architect, no glossy brochure. The owner is a man who runs a hardware shop off the main bazaar. He buys cement forty bags at a time, when he has the cash. The roof goes on in the third year. His income exists — it is real, it is steady, and his neighbours could vouch for it — but it does not exist on paper. He has never filed an income tax return. He has no salary slip. To the credit-scoring engine of a large commercial bank, he is not a risky borrower; he is an empty field. A null value.

That null value is the entire business of Aavas Financiers Limited.

From its headquarters in Jaipur, Aavas has built one of India's most-watched affordable housing finance companies out of the borrowers the formal system cannot see. As of the quarter ended June 30, 2026, the company managed assets of ₹239.3 billion — roughly $2.9 billion — across 440 branches in 15 states and more than 260 districts, served by 7,706 employees and about 275,869 live loan accounts.1 The average housing loan is ₹1.12 million. Eighty-three per cent of the book sits below ₹1.5 million. Sixty-two per cent of assets under management are lent to the self-employed.1 This is not mortgage lending as a Mumbai banker understands it. It is closer to small-business underwriting with a house attached as collateral.

What This Story Tests

The question this story asks is a hard one, and mid-2026 is exactly the right moment to ask it. How did a regional subsidiary — spun out of a Jaipur vehicle financier because a banking licence made it inconvenient to keep — build a fortress in India's un-underwritten heartland, survive the 2018 non-bank liquidity freeze that killed several of its peers, deliver a twelve-fold increase in assets for its private equity owners, attract global buyout house CVC Capital Partners as its controlling shareholder, and then, within eighteen months of that handover, lose its chief executive, chief financial officer, chief risk officer and chief business officer in the space of ten weeks while the National Housing Bank ran an inspection of how it had been classifying loans?

Both halves of that sentence are true. Holding them together is the analytical work.

The roadmap runs roughly chronologically. First, the genesis: how Sushil Kumar Agarwal built a housing arm inside Sanjay Agarwal's AU Financiers, and why the parent's ambition to become a bank forced the child out of the house. Then the private equity era, when Kedaara Capital and Partners Group bought control in 2016 and spent two years converting a promoter-run lender into an institution. Then the public markets chapter — an IPO that listed at a discount into the worst possible week for Indian non-bank finance, and the liability architecture that let Aavas keep lending while others stopped. Then the deep dive into the underwriting method itself, which is the only thing here that plausibly qualifies as a durable advantage. Then the CVC transaction, which replaced two financial owners with one control owner. And finally the events of April to July 2026, which are still unresolved as of this writing.

A Word on Posture

Aavas has, on the reported numbers, an unusually clean book: gross non-performing assets of 1.11% and net NPAs of 0.71% at the end of June 2026, with early-delinquency (1+ days past due) at 3.76%, improved 39 basis points year on year.1 Those are good numbers for any lender, and excellent ones for a lender whose customers have no tax returns. But 2026 has introduced a specific and uncomfortable problem: a regulator was looking at how loans were classified, several of the executives who ran the classification-relevant functions left, and two rating agencies responded by putting the company's long-term debt on watch.2 Reported asset quality is an output of a process. When the process is under external review and the people who ran it have gone, the output deserves less automatic trust than usual — not because the numbers are presumed wrong, but because the ordinary reasons to presume them right have weakened.

That tension is the story. It begins in Jaipur, fifteen years ago, inside somebody else's company.

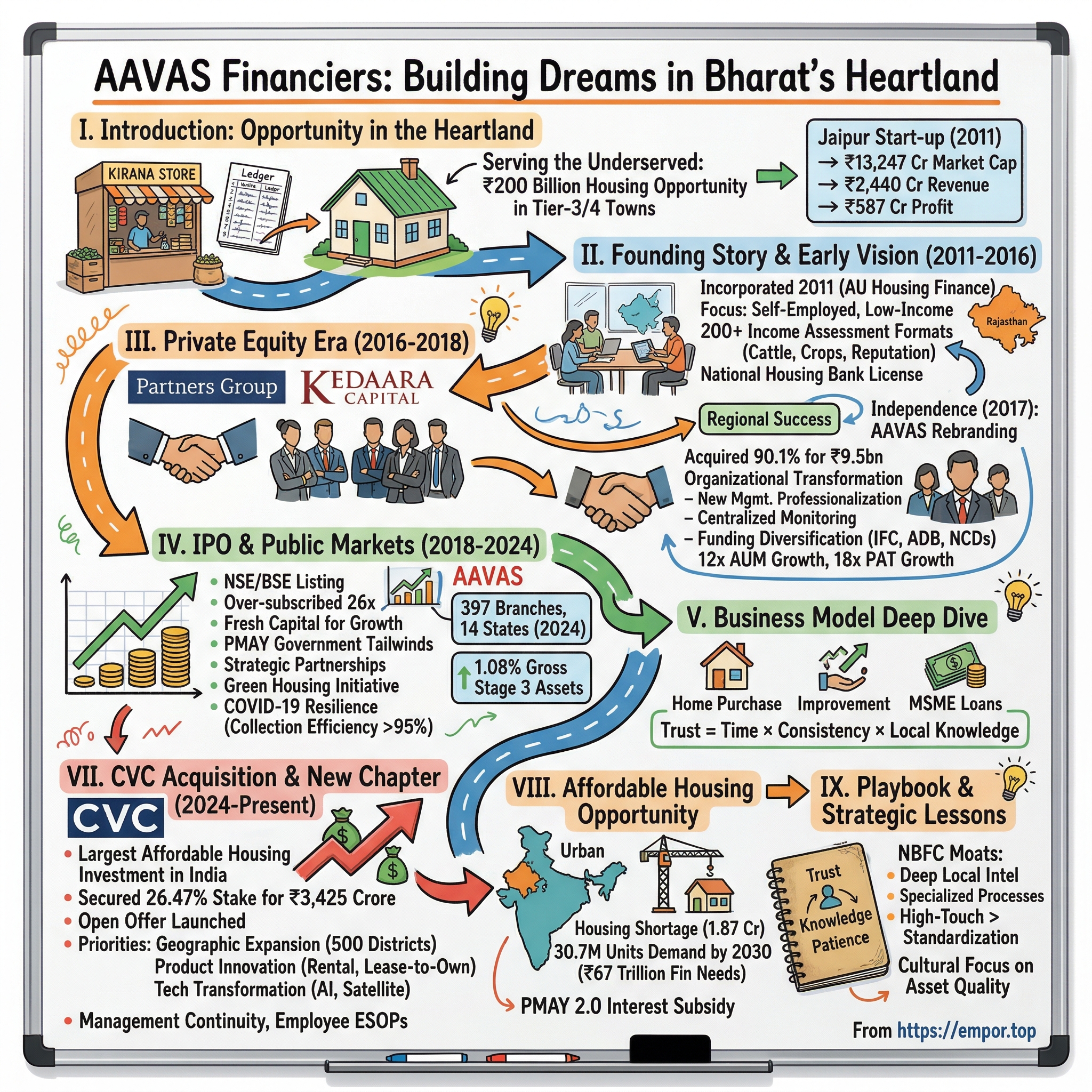

II. The Origins & The Spinoff: Spanning from AU Financiers (2011–2016)

Jaipur, Before It Was a Financial Centre

In the late 2000s, Jaipur was not where you went to build a financial institution. Mumbai had the capital markets, Delhi had the policy, Bangalore had the technology. Jaipur had a vehicle finance company called AU Financiers, run by Sanjay Agarwal, which had made a specialty of something the big banks found unattractive: lending against used commercial vehicles to small operators in Rajasthan's district towns. It was gritty, high-touch, feet-on-the-ground credit. It worked because AU's people knew the roads, the routes and the transporters personally.

The Man Who Saw the Gap

Inside that company was a chartered accountant named Sushil Kumar Agarwal — no relation in the corporate sense, though the shared surname has confused people for years. He had ranked tenth in the country in his CA examinations, also qualified as a company secretary, and had spent roughly two decades in financial services across Kotak Mahindra Prime, ICICI Bank and then AU, where he ran a business line.4 He was, by background, a credit person who had seen how large institutions make lending decisions from the inside — which mattered, because his central insight was about what those institutions could not do.

The insight was not that poor Indians wanted houses. Everyone knew that. The insight was subtler and more commercial: there existed a very large population of creditworthy Indians who were systematically excluded not by risk but by documentation. A shopkeeper turning over ₹80,000 a month in cash, a dairy farmer with fourteen buffaloes, a tailor with three machines and two employees — these people had cash flows a careful underwriter could measure. What they did not have was the paperwork a centralised credit process requires. Banks like HDFC, State Bank of India and ICICI were not being irrational in declining them; their cost structures and their underwriting architectures simply could not economically evaluate an applicant whose income had to be reconstructed by visiting the shop. Rejection was cheaper than diligence.

That gap — creditworthy but undocumented — is the founding thesis, and it is worth pausing on because it determines everything Aavas later became. If the gap had been about risk, the answer would have been higher pricing. Because the gap was about information cost, the answer had to be a distribution and appraisal machine. Aavas is, at its core, a bet that you can profitably industrialise the manual gathering of information that computers cannot gather.

Building Inside Someone Else's House

AU Housing Finance Limited was incorporated on February 23, 2011 as a subsidiary of AU Financiers, received its licence from the National Housing Bank in August 2011, and began lending in March 2012.[^3]21 The early years were slow by design. A branch would open in a district town; officers would learn the local property market, the local trades, the local reputational networks; the branch would take years to reach scale. Growth in this model is not a marketing decision. It is a hiring-and-training decision, and it compounds slowly at first.

It helped enormously that the business grew up inside AU. Vehicle finance to small transporters and mortgage finance to small shopkeepers are different products with the same underlying discipline: you are lending against a cash flow that only exists in the borrower's daily life, and the only way to know it is to go and look. The housing team inherited that instinct fully formed. It also inherited something less obvious — a tolerance for slow branches. In a bank, a branch that takes three years to break even is a problem to be escalated. In AU's world it was normal, because the entire model assumed that a location's value came from relationships built over years rather than footfall captured in months.

What Aavas did not inherit was a funding franchise. AU could fund itself against a diversified, fast-amortising vehicle book with plenty of banks willing to lend against it. A start-up mortgage lender making fifteen-year loans has the opposite profile: assets that return capital slowly, and a balance sheet that must therefore be funded with patient money it has not yet earned the right to raise. Through 2012 to 2015, this was the binding constraint. The company could find more good borrowers than it could fund.

The Licence That Forced a Separation

Then, in 2015, the Reserve Bank of India changed the landscape. It granted in-principle small finance bank licences to a set of non-bank lenders, AU Financiers among them. That approval was a triumph for Sanjay Agarwal — and a structural problem for his housing subsidiary. RBI's licensing conditions required the applicant to restructure its group holdings; a small finance bank could not simply carry on owning a separate housing finance company with its own regulator and its own capital needs. The housing arm had to go.

There was also a genuine business logic buried inside the regulatory compulsion, and it is the more interesting half. A bank funds itself with deposits, most of which are short-dated and callable. A housing finance company funds fifteen-year mortgages. Running both inside one balance sheet creates a permanent asset-liability mismatch that management must actively suppress — which in practice means the mortgage business gets rationed whenever the bank's treasury gets nervous. Separating them let each entity match its liabilities to its assets. The spin-off, in other words, was not merely compliance. It handed the housing business the right to build its own funding structure for its own duration, which is precisely the capability that saved it three years later.

Enter Kedaara and Partners Group

In February 2016, Partners Group and Kedaara Capital agreed to acquire control of the housing arm, with completion expected in April 2016 subject to National Housing Bank clearance.5 The two firms took a 90.1% stake for approximately ₹950 crore. Kedaara — a Delhi-headquartered private equity firm founded by former General Atlantic and Temasek executives — took the larger position and the operational lead; Partners Group, the Swiss-listed global private markets manager, came in alongside. In March 2017, the company dropped its parent's name and became Aavas Financiers Limited. Aavas means dwelling.

At the moment of separation, the business managed roughly ₹17 billion of assets and earned ₹328 million of profit after tax.6 It had a founder, a method, a regional footprint, and almost nothing else that an institutional investor would recognise as infrastructure. What happened over the next two years is a fairly pure demonstration of what good control-stage private equity is actually for.

III. The Private Equity Playbook: Scaling and Institutionalizing (2016–2018)

The Scaling Paradox

The stereotype of private equity in a founder-led company is a cost-cutting exercise with a leverage kicker. What Kedaara and Partners Group did at Aavas was close to the opposite: they spent money adding people and process to a business that was already growing, on the theory that the constraint was not demand but the company's ability to underwrite demand without breaking.

Consider the problem they inherited. A lender that evaluates borrowers by physically inspecting their businesses has a scaling paradox at its heart. Every new branch requires officers who can make judgement calls with no algorithm to fall back on. Judgement scales badly. Left alone, a business like this either grows slowly and stays clean, or grows fast and quietly rots — the rot invisible for two or three years because mortgages default late, not early. Indian financial history is littered with lenders that discovered this in year four.

Three Decisions That Became an Operating System

The owners' answer had three parts, and each is worth understanding on its own terms because together they became the operating system.

First, they separated who sells from who approves. Under a promoter-run structure, the person who found the customer often had significant influence over whether the loan got made. Kedaara and Partners Group built independent risk containment and credit functions reporting up a separate line, so that a branch could not approve its own business. This sounds like elementary governance. In practice it is the single most reliable predictor of whether a high-growth Indian lender survives its first credit cycle, because it removes the mechanism by which growth pressure converts into underwriting laxity.

Second, they built an in-house legal and technical capability rather than renting one. Title verification in semi-urban India is genuinely hard: records are inconsistent, ownership chains are informal, and a property that looks financeable can turn out to be encumbered in ways a fee-per-file external lawyer has no incentive to discover. Aavas built its own legal team — over a hundred people — and its own technical valuation staff. The economics are counterintuitive. It is more expensive per file than outsourcing. It is far cheaper per default.

Third, and most consequentially, they made a rule that Aavas would source one hundred per cent of its loans in-house. No direct selling agents. No brokers.

Why No DSAs, Ever

That third decision deserves proper explanation because it is the closest thing Aavas has to a philosophy. Across Indian retail lending, the dominant distribution model is the DSA — an independent agent who finds borrowers and hands them to whichever lender pays the best commission. DSAs are efficient. They are also structurally misaligned: the agent is paid on origination and bears no consequence for repayment. In a documented, salaried market, that misalignment is manageable, because the lender can independently verify the borrower's income from tax records. In an undocumented market, the DSA controls the only information the lender has — the borrower's story — and is paid to make that story fundable.

By refusing DSAs entirely, Aavas accepted a permanently higher operating cost and a permanently slower growth ceiling in exchange for owning the customer relationship and the information about that customer end to end. Its sales officers are the company's employees; their incentives are tied to collections as well as to origination, so the person who wrote the loan is still around when the loan has to be repaid. That is not a moral position. It is a design choice about where to put the information risk in a market where information is the scarce good.

Software as a Checklist

Alongside this, the company built its own loan origination and loan management systems rather than buying packaged software. The reason was mundane and important: field-based credit in districts with patchy connectivity needs applications that work offline, sync later, and force the officer through a structured data-capture sequence at the customer's premises rather than back at the branch from memory. Off-the-shelf systems built for urban salaried mortgages do not do this.

It is worth being precise about what this technology is and is not, because "proprietary LOS and LMS" is the kind of phrase that gets read as a moat when it is really plumbing. Aavas did not build an algorithm that predicts default better than anyone else's. It built a set of digital forms and workflows that make it very hard for a field officer to skip a step. Think of it less as artificial intelligence and more as a pilot's pre-flight checklist rendered in software: the value is not in any individual item but in the impossibility of proceeding without completing them. In a business where the failure mode is a tired officer in a hot district town taking a shortcut on a Friday afternoon, that is worth more than a clever model.

The final piece of the institutionalisation was the least visible: hiring professional executives with large-institution experience into functions that had previously been run informally. Finance, risk, technology and audit all acquired senior leaders in this period, several of whom stayed for the better part of a decade. That continuity became part of the investment case — and, as 2026 has demonstrated, part of the fragility.

What Two Years Bought

The results showed up in the footprint. The branch network went from roughly 50 to more than 165 by the end of FY18, concentrated deliberately in a contiguous block — Rajasthan, Maharashtra, Gujarat, Madhya Pradesh — rather than scattered across India.[^3] Contiguity matters more than it sounds: it lets a regional credit head physically visit branches, lets officers transfer between locations without relearning property markets, and keeps supervision costs low. Over FY14 to FY20, assets compounded at 63.6% annually and profit after tax at 81.9%, off a small base.4

By mid-2018, the owners had what they had paid for: a company with a repeatable method, institutional controls, and a growth runway. What they needed next was a public market willing to pay for it. They picked, as it turned out, the worst month in a decade.

IV. The IPO & Public Markets Juggernaut (2018–2024)

The Worst Fortnight in a Decade to List

The Aavas offering opened on September 25, 2018 and closed on September 27, with a price band of ₹818 to ₹821 a share, combining a fresh issue with a large offer for sale by the private equity owners.7 It raised roughly ₹1,640 crore in total. The book was subscribed just under one times. On October 8, the shares listed on the BSE and the NSE at ₹758 — a debut about 7.7% below the offer price.7

To understand why, you have to look at what else was happening that fortnight. On September 21, 2018, the infrastructure conglomerate IL&FS defaulted on a commercial paper obligation. Within days, a company that had been rated AAA was rated as junk, and the Indian mutual fund industry — the marginal buyer of short-term non-bank paper — stopped rolling over exposure to anything that was not a bank. The result was an instant, system-wide liquidity freeze for India's non-bank financial companies and housing finance companies. Several large names discovered that they had been funding long-dated assets with three-month paper, and that the three months had ended.

Aavas thus arrived in the public market carrying a label — housing finance company — that had just become radioactive, and with private equity sellers on the register whose eventual exit everyone could see coming. It is one of the least auspicious listings imaginable, and the flat pricing reflected exactly that.

What happened next is the most genuinely instructive episode in the company's history, because it was a test the business either passed or failed on architecture rather than on narrative.

The Liability Fortress

Aavas's liabilities were not concentrated in short-term wholesale paper. The funding mix leaned on term loans from commercial banks, refinance lines from the National Housing Bank, and non-convertible debentures, deliberately spread across tenors so that no single market's closure could stop the company from lending.[^3] This is unglamorous treasury work with a real cost: long-dated, diversified funding is more expensive than rolling cheap short paper, and in calm markets a lender that does it looks slightly less profitable than a lender that does not. The 2018 freeze converted that apparent inefficiency into survival. Peers that had optimised for the last basis point of funding cost spent 2019 selling loan portfolios; Aavas kept originating.

Funders Who Don't Read the Newspapers

The company then did something more strategic than simply surviving: it went and found funders whose motivations were not market sentiment at all. In December 2020, it signed an agreement with the International Finance Corporation, the World Bank Group's private sector arm, alongside the UK-IFC Market Accelerator for Green Construction programme, to build a green affordable housing finance business using IFC's EDGE building certification standard, with a stated focus on low-income and women borrowers.8 In February 2026 — much more recently, and materially — the Asian Development Bank signed a senior secured financing package of up to $108 million, including an $8 million concessional tranche through the Canadian Climate and Nature Fund for the Private Sector in Asia, with covenants requiring at least 70% of the money to fund lower-income housing loans and half of those loans to have women as sole or joint property owners.9

The analytical point is not that development finance is virtuous. It is that development finance institutions underwrite mandate fit, not quarterly sentiment. A lender with IFC and ADB in its liability stack has a source of long-dated money that does not disappear when Indian credit markets have a bad week — and, because those institutions do their own extensive diligence, their presence functions as a slow-moving third-party endorsement of the company's systems. It is a real and somewhat underrated asset. It is also, notably, an asset that becomes more valuable precisely when domestic ratings are under question, as they are today.

The Pandemic Test

Through this period the operating engine did what it was built to do. Over Kedaara's holding period from 2016 to its final exit, assets under management compounded from ₹17 billion to ₹204 billion — a twelve-fold increase at about 32% annually — while profit after tax rose from ₹328 million to ₹5.74 billion, roughly eighteen-fold at 37% annually.6 Gross stage 3 assets stayed close to one per cent throughout, including through the pandemic, when a portfolio of self-employed borrowers in district India was supposed to be the most vulnerable book in the country.

That last fact is the strongest single piece of evidence in the bull case, and it should be stated precisely rather than loosely. COVID-19 was a natural experiment on informal-sector underwriting: incomes stopped, moratoria were granted, and the sceptical view held that affordable housing books were a slow-motion accident. Aavas's book did not behave that way. Either the underwriting was genuinely selecting for resilient borrowers, or the loan-to-value cushion was doing the work, or restructuring was masking stress. The subsequent five years of normalised delinquency data are more consistent with the first two explanations than the third — which is a meaningful, if not conclusive, vote of confidence in the method.

There is a second-order lesson buried in the 2018–2024 stretch that is easy to skip past. The stock spent much of that period trading at a premium to most Indian lenders, and the reason was not growth alone — plenty of non-banks grew faster. It was that Aavas had, in public, under stress, demonstrated that its reported credit quality was not an artefact of a benign environment. Markets pay a great deal for that kind of proof, and they take it away quickly when it comes into doubt. Holding the premium required the company to keep supplying evidence quarter after quarter.

By FY24, assets stood above ₹170 billion. The private equity owners had a mature, proven, listed asset, and their funds were reaching the end of their natural lives. It was time for someone else to own it.

V. The Secret Sauce: Underwriting the Informal Sector

A Day in the Field

Follow a credit officer for a day and the abstraction becomes concrete.

The applicant runs a kirana shop — a neighbourhood grocery. He wants ₹1.1 million to complete a house on a plot he already owns. He has a bank account with irregular deposits, no tax returns, no audited accounts, and a handwritten ledger. The officer does not ask for documents he knows do not exist. Instead he sits in the shop for two hours in the late afternoon and counts. How many customers walk in. What the average basket looks like. Then he asks to see the purchase bills from the wholesaler — because a shop's inputs are far harder to fake than its claimed revenue, and a trader who buys ₹4 lakh of stock a month is selling something close to ₹5 lakh. He looks at the electricity bill, which correlates with refrigeration and therefore with turnover. He talks to the neighbouring shopkeepers, the wholesaler, the landlord. He photographs the ledger.

Then, separately, a technical officer visits the property with a mobile application that requires geo-tagged photographs before the file can proceed, so that the collateral the credit committee sees is verifiably the collateral that exists.[^3] And then, crucially, a different person — in a different reporting line, sitting elsewhere — decides whether to approve.

That is the "secret sauce." It is not clever. It is expensive, repetitive fieldwork, systematised.

For a dairy farmer, the proxies change: the number and health of the animals, the milk yield, the cooperative's payment records. For a tailor, it is machines, employees and order books. For a small transport operator, it is the vehicle, the route and the diesel purchases. Each trade has its own arithmetic, and the institutional knowledge of those arithmetics — held across thousands of officers, refined over fourteen years, embedded in checklists and training and scorecards — is what Hamilton Helmer would call Process Power: an advantage that lives in an organisation's accumulated way of doing things, is not visible on the balance sheet, and cannot be bought.

The useful analogy is medical. A general practitioner in a large hospital works from test results; if the tests come back empty, there is no diagnosis. A rural doctor who has practised in the same district for twenty years works from what they can observe — colour, gait, the family's history, what the neighbours say — and reaches a conclusion the hospital's machine could not. Neither is better in the abstract. The rural doctor's method is unscalable, unverifiable from head office, and entirely dependent on the individual's accumulated experience. That is Aavas's underwriting exactly, with one addition: the company has spent fourteen years trying to convert the rural doctor's intuition into a written protocol that a newly hired officer can execute in year one. How successfully it has done so is the central unknowable in the investment case, because the evidence — a clean loan book — takes five to seven years to arrive and is confounded by collateral values in the meantime.

Why a Large Bank Cannot Simply Copy It

Why can't a large bank simply copy this? Not because the technique is secret — it is described in every affordable-housing investor presentation in India. Because of cost structure and organisational fit. A bank underwriting a ₹5 crore urban mortgage can afford almost any diligence, but the same bank running a ₹11 lakh loan through a process that requires two field visits and a locally knowledgeable officer earns a fraction of the revenue per file. Worse, the process is illegible to a centralised credit committee: it produces judgements, not scores. Large institutions are built to standardise judgement out of lending, which is exactly why they cannot do this and exactly why the gap has persisted for fifteen years.

The Cross-Subsidy Nobody Talks About

The portfolio arithmetic makes the model work. As of June 2026, home loans accounted for 64% of assets, mortgage-backed MSME business loans 23%, and loan against property 13%.1 The self-employed were 62% of the book, and customers in the economically weaker and low-income groups were 54%.1 Housing loans grew 38% year on year in the quarter — a deliberate mix shift, and one with a consequence discussed below.

The MSME piece is the least understood and most important part of the economics. These are not unsecured small-business loans; they are business loans fully secured by residential or commercial property, made to the same kind of borrower, through the same appraisal process. They carry higher yields than home loans. That higher yield is what lets Aavas price core home loans competitively while still earning a spread of about 5% and a net interest margin of 7.70% as of the June 2026 quarter.1 In effect, the business-loan book cross-subsidises the housing book. It also means that when the mix shifts toward home loans — as it did sharply this year — yields compress mechanically, regardless of how well the company is executing. Management told analysts on the July 21, 2026 call to expect spreads to compress to below 5% for FY27, and separately noted a 10 basis point cut in the prime lending rate.2 That is an honest disclosure of a real trade-off, and investors should read the housing-mix growth and the spread guidance as the same fact seen from two sides.

The 45% Cushion

The other structural protection is loan-to-value. Aavas originates at an average LTV of about 55%.1 Read that number properly: the borrower has put up 45% of the property's value in equity, usually accumulated over years and often representing most of the family's net worth. Two things follow. Recovery in a default is very likely to cover principal, so severity of loss is low. And the borrower's incentive to keep paying is enormous, so frequency of default is low too. Conservative LTV is doing an extraordinary amount of the work in this business model — arguably as much as the appraisal method — and it is worth being clear that this is a collateral moat as much as a credit moat.

The results, as reported: gross NPAs of 1.11%, net NPAs of 0.71%, credit costs of 0.24%, and early-stage delinquency of 3.76%, all improving year on year.1 Return on assets of 3.19% and return on equity of 13.34%, the latter suppressed by an extremely well-capitalised balance sheet at 44.7% capital adequacy.1

There is a third leg to the system that gets less attention than underwriting and collateral, and it is collections. In a book of self-employed borrowers with lumpy cash flows, some proportion of customers will miss a payment in any given month for entirely benign reasons — a wedding, a bad monsoon, a delayed receivable. The difference between a lender with 1% NPAs and one with 4% is very often not who they lent to but how quickly and how personally they follow up. Aavas's field officers are compensated on collection efficiency as well as origination, which means the person chasing the missed instalment is frequently the person who sat in the borrower's shop and counted customers. That relationship is worth more in this segment than any call-centre script, and it is another reason the in-house sourcing rule and the low NPA figure are causally linked rather than merely correlated.

The Unused Balance Sheet

That capital ratio is itself an analytical fact worth naming. Carrying capital at nearly three times the regulatory floor means the company is nowhere near levered enough to earn a high return on equity. A 13% ROE from a 3.2% ROA is what you get when you refuse to use the balance sheet. For a lender under regulatory scrutiny in 2026, that fortress is comforting. For an owner like CVC, it is also an obvious, unexercised lever — and one worth watching, because deploying it is the single easiest way to raise returns and the single easiest way to change the risk profile of a business whose entire appeal has been conservatism.

VI. The CVC Buyout: Transitioning Promoters (2024–2025)

The Clock Runs Out

Every private equity investment has an end date written into the fund documents, and by 2024 Kedaara's and Partners Group's clocks had run down. They had already been selling into the market — including a 12.6% block in March 2024 — but the residual stake was large enough that dribbling it out through the exchange would have hung over the stock for years. What they needed was a single buyer for a control block.

On August 10, 2024, CVC Capital Partners announced that funds it manages had agreed to acquire 26.47% of Aavas — 20,949,112 shares — from Lake District Holdings Limited, an affiliate of Kedaara, and from Partners Group entities, triggering a mandatory open offer under SEBI's takeover regulations and positioning CVC to become the company's promoter.3 The block was priced at ₹1,635 per share, for approximately ₹3,425 crore, and the follow-on open offer for a further 26% was made at ₹1,767.11 per share, taking the combined transaction to roughly $1.3 billion.1011

What CVC Bought, and What It Paid

Two features of the deal structure are worth drawing out, because they say more than the headline number.

The first is who was buying. CVC is not a growth investor taking a minority ride; it is a control-oriented buyout firm. The distinction shapes everything that follows. Kedaara and Partners Group had spent eight years building an institution and then harvesting a listed multiple — their interest was in a company that compounded steadily and traded well. A control buyer's interest is in a company it can direct: change management, redeploy capital, reshape the growth algorithm, and exit at a multiple justified by something it did. The 2026 leadership turnover, whatever else was going on, is exactly what control ownership looks like in operation.

The second is what was paid. On the numbers available at the time, the entry valued Aavas at roughly 3.3 to 3.5 times book value.12 For context, peers in the affordable housing space were carrying meaningfully richer multiples: Home First Finance in the mid-3s to 4 times book, and Aptus Value Housing — whose return on assets ran near 7%, more than twice Aavas's — closer to 4.5 to 5 times.12 CVC, in other words, did not pay up. It bought the largest and most conservatively underwritten asset in the category at a discount to the faster-growing and more profitable ones.

Whether that was discipline or a signal is the genuinely open question. The bullish reading: CVC identified a business whose returns were artificially depressed by excess capital and a low-leverage philosophy, and bought the cheapest route to a category-leading franchise. The sceptical reading: the market was already pricing Aavas at a discount for a reason — slower growth than Home First, structurally lower returns than Aptus, and a heavier cost structure than either — and CVC paid a fair price for a good but not exceptional asset. On the evidence to date, both readings survive.

From Two Owners to One

The transaction proceeded through the Competition Commission of India and the mandatory tender process. Aquilo House Pte. Ltd., the CVC-controlled acquisition vehicle, picked up a further 17.8 million shares — about 22.5% — through the open offer, which settled on March 21, 2025.3 Kedaara completed the sale of its residual holding on July 2, 2025, closing a nine-year investment.6 Partners Group exited alongside. By the end of FY26, CVC's holding stood at approximately 49%, and it was the registered promoter of Aavas Financiers.[^3]

Something subtle changed in that handover that is easy to miss. From 2016 to 2024, Aavas was owned by two financial investors who between them had a majority but neither of whom ran it — a structure that, whatever its inefficiencies, gave professional management substantial operating autonomy and made abrupt strategic reversals unlikely. From 2025, it has had a single owner with just under half the register, full promoter status, and a house style of active intervention. Governance quality did not obviously fall. But the distribution of possible outcomes widened considerably, in both directions.

The market's initial reaction was positive; the stock reached its highest level since 2022 in early 2025. Within a year, the picture looked very different.

VII. The 2026 Leadership Reset & NHB Refinancing Shock

May 2026: A Calm Set of Results

On May 5, 2026, Aavas held its FY26 earnings call. It was, on the face of it, an unremarkable event: assets of ₹234.5 billion, up about 15%; net interest income of ₹13.56 billion, up 17%; profit after tax of ₹6.56 billion, up 14%; a full-year spread of 5.20% and a net interest margin of 7.93%; incremental borrowing raised at 7.61%, contributing to a 62 basis point improvement in the overall cost of funds; and 435 branches across 15 states, with 31 added in the final quarter alone, concentrated in Tamil Nadu, Uttar Pradesh and Gujarat.20[^22] Full-year disbursements were ₹67.75 billion, up 11%.[^22] Analysts asked about competition, balance transfers, prepayment behaviour, the MSME mix and the new leadership's direction; management pointed to asset quality and sustainable growth.20

What made the call unremarkable is what makes it striking in hindsight. Two weeks earlier, the chief executive had left. Six weeks later, the chief financial officer who presented those numbers and the chief risk officer who signed off on that asset quality would both be on garden leave. The operating results and the organisational reality had come apart, and for a period only one of them was visible.

The Sequence

Start with the sequence, because the sequence is the story.

On April 20, 2026, Aavas announced that the board had accepted the resignation of Sachinderpalsingh Jitendrasingh Bhinder as Managing Director and Chief Executive Officer with effect from the close of business that day, citing professional and personal commitments, with Bhinder continuing as a senior advisor. In the same announcement, the company named Manu Yeshpal Singh as MD & CEO effective April 21, 2026, subject to Reserve Bank of India and shareholder approvals.13 Bhinder had joined as CEO in February 2023 and become managing director later that year, succeeding founder Sushil Kumar Agarwal — a three-year tenure.

In May 2026, Chief Business Officer Selvin Uthaman departed.

On June 21, 2026, the board accepted the resignations of Ghanshyam Rawat, President and Chief Financial Officer, and Ashutosh Atre, President and Chief Risk Officer, effective September 21, 2026. Both were placed on garden leave immediately. Ghanshyam Gupta was appointed interim CFO and Punit Purushottam Agarwal interim Chief Risk Officer with effect from June 22.14

Rawat and Atre were not ordinary hires. Rawat had been the company's CFO since the AU Housing days — he appears as a trustee of the Aavas Foundation in the 2020 IFC announcement — and Atre had run risk through the entire scaling phase.8 These were the two people most closely identified with the twin pillars of the equity story: the funding architecture and the credit process. Losing both, on immediate garden leave, three months before their formal exit dates, is not a routine succession event. Garden leave is what an organisation does when it does not want the departing executive in the building.

The NHB Thread

Now the second thread. On or around June 22, 2026, press reports — originating with the Economic Times — stated that the National Housing Bank had been investigating loan classification at Aavas and had recalled refinancing support of nearly ₹500 crore. The reported allegations were specific and had three strands: that concessional refinance earmarked for scheduled caste and scheduled tribe borrowers had been drawn against loans to borrowers outside those categories; that properties had been recorded as located in hilly regions, which carry their own refinance benefits, when the underlying assets were elsewhere; and that non-housing loans had been reclassified as home loans to access preferential funding.15

Aavas responded through the exchanges the same day. The company called the reports "misleading, malicious, speculative and not an accurate characterisation of the Company's engagement with NHB," stated that NHB inspections are "a routine part of the regulatory framework," said that no refinance facility had been recalled or reversed, and added that it would make disclosures if developments warranted them under SEBI's listing regulations but believed none was necessitated at that stage.14 The stock fell as much as 8.2% intraday to ₹1,351 before recovering to close down about 3%; it was down roughly 34.5% for the calendar year to that point, and roughly a third below its 52-week high of ₹2,152.1415

It is important to be precise about what is established and what is not. Established: an NHB inspection occurred; four senior executives left within ten weeks; the company denies the specific allegations; two rating agencies took action. Not established: whether misclassification occurred, in what amount, whether any refinance was in fact recalled, and whether the executive departures were connected to the inspection at all. Aavas's denial is on the record and is unambiguous. The reported allegations are, at this writing, reported allegations. Both facts should be held simultaneously.

The Rating Agencies Respond

What is not in dispute is that the market's independent arbiters responded. On July 1, 2026, ICRA placed Aavas's long-term ratings — covering bank lines of ₹3,398 crore and non-convertible debentures of ₹800 crore — on Rating Watch with Developing Implications, citing frequent senior management changes during 2026, and specifically listing the CEO, CBO, CFO and CRO departures. Its ₹250 crore commercial paper rating was left unchanged at [ICRA]A1+.16 The same day, CARE Ratings placed facilities and NCDs totalling ₹13,521.92 crore on Rating Watch with Developing Implications, citing the same management transitions, and noting alongside them the company's geographic concentration — 64% of assets in three states — and its ongoing engagement with NHB on audit matters. CARE also noted the stabilising factors: capital adequacy of 44.6% and gross NPAs of 1.05% as of March 31, 2026.17

"Developing Implications" is deliberately non-committal — the rating can move up, down or nowhere once clarity emerges. But the mechanism matters more than the label. Aavas's cost of borrowing was 7.64% in the June quarter.1 A lender whose entire model depends on borrowing long and cheap, and lending to borrowers who cannot go elsewhere, is exposed at exactly this joint. Even without a downgrade, a watch designation gives every treasury desk a reason to ask for a few extra basis points on the next line — and against a spread already guided to compress below 5%, a small increase in funding cost is not a rounding error.

Aavas 3.0

Into this walked Manu Yeshpal Singh. He arrived from Kotak Mahindra Bank, where he was President and Business Head for Housing Finance, with more than 25 years in the sector including roles at Tata Capital and ICICI Bank.13 The résumé is genuinely relevant: he has run a large, prime, bank-owned mortgage business — precisely the kind of institution that competes with Aavas for its best-seasoned borrowers. He knows how balance transfers are won, which is the single most pressing commercial threat to Aavas's book.

His first earnings call as CEO, on July 21, 2026, was a study in leading with operations. Disbursements were up 41% year on year to ₹16.1 billion, with monthly assets additions up nearly 50%; net profit rose 23% to ₹1.71 billion on 18% net interest income growth; the cost-to-income ratio fell 254 basis points to 43.7%.12 Guidance was set at 22–23% disbursement growth and 17–18% assets growth for FY27, with a long-term aspiration of 20% sustainable growth.1 On competition and margins, management said it anticipated spread compression to below 5% for the year but expressed confidence that operating leverage on the cost-to-income line would keep return on equity stable. Asked about a jump in repayment rates to above 19% — a potentially alarming signal — management attributed the uptick to early-fiscal-year activity in segments priced above 14% and said it had normalised by June, adding that no alarming balance transfer trends had been observed.2

Alignment, for what it is worth, runs through equity. Aavas maintains employee and performance stock option programmes approved in recent years, which give incoming senior management a claim on long-run share price rather than annual growth alone; the specific grant terms for the current leadership have not been broken out in a way that allows outside assessment of the performance hurdles.[^3] This matters more than usual under a private equity promoter, because option economics are the mechanism by which a control owner converts "grow faster" from an instruction into an incentive. A reader who wants to understand what the new team is actually being paid to do should read the option disclosures in the next annual report rather than the strategy slides.

One further second-layer note belongs here. Neither rating agency, nor the company, has flagged an auditor issue, a restatement, or a change in accounting policy in connection with these events, and the FY26 accounts were signed in the ordinary course.161720 The question raised by the reported allegations is about how loans were tagged for refinance eligibility, which is a regulatory-reporting matter rather than a financial-statement one. Those are different things, and conflating them would overstate the case. But they run through the same data pipes, which is why the market treated the news as more than a compliance footnote.

That is a confident set of answers, and the underlying operating numbers back a good deal of it. It is also worth noting what the call, on the available record, did not dwell on: the NHB engagement and the executive exits did not feature prominently in the disclosed highlights.2 For a company whose ratings were placed on watch three weeks earlier explicitly because of management churn, the absence of a substantial forward-looking discussion of governance remediation is itself a data point. Investors assessing management credibility here have very little tenure to judge — Singh has been in the chair for three months — so the fair standard is not "has he delivered" but "is he telling us what he will be measured on." On growth and cost, yes, specifically. On the regulatory question, considerably less so.

VIII. Affordable Housing Industry Structure & Strategic Landscape

Zoom out from Jaipur and the competitive picture becomes clearer — and less comfortable.

The Demand Side Is Not the Problem

India's affordable housing loan market stood at roughly ₹19.5 trillion of outstanding loans as of the first half of FY26, representing about 46% of total housing loan value but 82% of all active housing loan accounts.19 That asymmetry is the whole industry in one statistic: enormous account volume, small average size, and therefore an economics that only works for lenders with genuinely low cost-to-serve or genuinely high yields. Mortgage penetration in India remains near 12% of GDP, against roughly 76% in the United States, and the housing shortage runs to tens of millions of units concentrated in exactly the income segments Aavas serves.19 The demand side of the bull case is not seriously contestable.

The supply side is where it gets difficult. Public sector banks have been losing share — from 42.4% of affordable housing outstandings in FY21 to 38.6% by H1 FY26 — while housing finance companies gained, and specialist NBFCs grew fastest of all.19 Capital has noticed that this segment earns double-digit yields on secured, small-ticket, granular collateral, which is close to an ideal risk-adjusted profile, and capital has responded the way it always does.

Porter, Applied Honestly

Run Porter's framework across it honestly.

Threat of new entrants: medium to high, and rising. The barrier is not capital — there is plenty. The barrier is the branch-and-officer network, which takes years to build and cannot be bought. But "years" is not "never," and the last five have produced several credible challengers. A new entrant with a fund behind it can hire experienced credit officers away from incumbents and be at scale in a decade. Aavas's fourteen-year head start is a real lead, not a permanent one.

Bargaining power of buyers: low at origination, high at seasoning. A first-time borrower with no documents has essentially no negotiating leverage; that is why yields above 12% are sustainable. But three years later, that same borrower has a repayment record on the credit bureau, possibly a GST registration, and a much better story to tell. At that point a large bank will happily refinance at 200 to 300 basis points less. This is the balance transfer problem, and it is the structural tax on the entire affordable model: the business systematically converts invisible borrowers into visible ones and then loses them to institutions that could never have originated them. Aavas's own repayment-rate uptick in early FY27, concentrated in loans priced above 14%, is the mechanism showing up in the data.2

That tax became heavier on January 1, 2026. The Reserve Bank of India (Pre-payment Charges on Loans) Directions, issued in July 2025 and effective for loans sanctioned or renewed from the start of this year, prohibit regulated lenders from levying pre-payment or foreclosure charges on floating-rate loans to individuals and micro and small enterprises.18 The friction that used to slow balance transfers — a 2% exit penalty that made switching uneconomic for a borrower with modest savings — is gone for new lending. This is a permanent, structural reduction in the stickiness of Aavas's best assets, and it is the single most underappreciated item in the bear case.

Rivalry: high, and differentiated. Aptus Value Housing dominates southern India with a high-yield, heavily self-employed book and returns on assets near 7% — meaningfully better than Aavas's 3.2%, achieved through higher pricing and a leaner cost structure. Home First Finance runs a more technology-forward, more salaried-weighted model with faster turnaround times. India Shelter Finance has been expanding aggressively through the northern corridors that Aavas considers home. None of these is a copy of Aavas, which is itself informative: the market has fragmented into distinct operating philosophies, and Aavas occupies the most conservative, most capital-heavy, most labour-intensive corner of it.

Supplier power in lending means funding, and here Aavas is comparatively strong — diversified bank lines, NHB refinance, NCDs, and multilateral money — except that the rating watch is precisely an attack on that strength. Substitutes are limited: the informal moneylender charges far more, and the alternative to a mortgage for this customer is building the house over a decade out of savings, which is what happened before companies like Aavas existed.

Seven Powers, Two Held

On Helmer's Seven Powers, Aavas plausibly holds two. Process Power, described earlier, is the strongest claim, and it is supported by fourteen years of sub-1.2% NPAs through a pandemic. Scale Economies are the second and weaker claim: at ₹239.3 billion of assets the company borrows at 7.64%, cheaper than smaller competitors can, which supports its spread even when it prices aggressively.1 But scale economies in lending are a shallow moat, because they rest on a credit rating — and a credit rating, as July 2026 demonstrated, can be placed under review in a single afternoon.

A word on the technology question, because it is asked about every lender now. Could artificial intelligence collapse Aavas's advantage by making informal-income assessment cheap? The honest answer is: partially, eventually, and not in the way most people assume. Account aggregator frameworks, UPI transaction histories and GST filings are steadily converting India's informal economy into a documented one, and every year some slice of Aavas's addressable customer base becomes legible to a bank's algorithm. That is a genuine long-run erosion of the moat. But it is erosion from the top — the most formalised customers become bankable first — which means the effect shows up not as a collapse in Aavas's origination but as a steady increase in the balance transfer rate on its best borrowers. Which is precisely the mechanism already described. The technology risk and the competition risk are the same risk wearing different clothes.

The cost side deserves a similar honesty. Aavas's cost-to-income ratio of 43.7% is improving but remains high relative to a technology-led originator, because the model is people-heavy by design — 7,706 employees for a ₹239 billion book.1 That is the price of the underwriting method. It also means operating leverage is the primary lever management has to defend returns as spreads compress, and management has said as much.2 The bet being made, in effect, is that the branch network can carry more volume per officer without loosening the process. That is a testable proposition, and the cost-to-income line is where it will be tested.

Myth vs Reality

Three consensus statements about this company deserve examination, because each is half right in a way that misleads.

Myth: Aavas is a housing finance company. Reality: roughly a third of the book is mortgage-backed business and property lending, and even the housing loans are underwritten off business cash flows rather than salary.1 The correct mental model is a secured small-business lender whose collateral happens to be homes. This matters because the risk factors that move the book are small-business conditions in district India, not urban property prices or interest-rate-driven housing demand.

Myth: the moat is technology. Reality: the technology is a workflow-enforcement layer, valuable but not proprietary in any deep sense. The moat, to the extent one exists, is the branch network, the officer training pipeline, and the fourteen years of institutional habit that sit behind them — none of which appear on the balance sheet, and all of which depend on the continuity of the people who carry them.

Myth: low NPAs prove superior underwriting. Reality: low NPAs prove that underwriting plus a 45% equity cushion plus a rising property market together produced few losses. Disentangling those three has not been possible in any environment India has offered since 2016, because collateral values have not fallen materially. The method has been tested by an income shock (2020) but not by a collateral shock. That is a meaningful gap in the evidence, and it is the reason the reported credit metrics, however good, cannot fully settle the question.

What Aavas Does Not Have

What Aavas does not have is worth stating plainly: no network effects, no switching costs (the RBI just removed the last of them), no cornered resource, no branding power that lets it charge more than Aptus. The company is defended by operational excellence and a conservative balance sheet. Those are genuine defences. They are also the kind that erode quietly if execution slips, which is exactly what a four-person C-suite exodus makes harder to rule out.

IX. Bull vs. Bear Case & Investment Analysis

Set the two cases against each other properly, because both are serious.

The Bull Case

The bull case starts with a demand pool that does not depend on anyone's forecast. Tens of millions of Indian households want to build or improve a home, cannot document their income, and have no alternative to a lender that will come and look. PMAY 2.0, launched in September 2024, targets 30 million additional homes through FY2029 with a 4% interest subsidy for economically weaker and low-income borrowers and a materially increased subsidy allocation in FY26.19 Aavas sits directly in the subsidy's path with 54% of customers in exactly those categories.1

Second, the operating engine is currently running well, not badly. Forty-one per cent disbursement growth, a cost-to-income ratio improving by more than 250 basis points, monthly asset additions up by half, and asset quality improving on every disclosed measure are not the signature of a business in distress.12 Whatever is happening in the boardroom has not yet reached the branches.

Third, capital. Capital adequacy at 44.7% against a regulatory requirement far below that means Aavas could grow substantially without raising a rupee, and a control owner with global funding relationships sits behind it.1 The balance sheet is not a constraint; it is unused capacity.

Fourth, the new chief executive's background is precisely matched to the company's most pressing problem. Someone who ran housing finance at Kotak understands the balance-transfer attack from the attacker's side.13

The Bear Case: An Activist's Stress Test

The bear case is not the mirror image of any of that — it is a different argument, and it turns on the reliability of the reported picture.

Begin where an activist would begin: with the people. Four senior executives, including the two who owned funding and credit, left within ten weeks, two of them on immediate garden leave.14 That is not attrition; that is a break. The most benign explanation is a new controlling owner installing its own team, which happens constantly in buyouts and says nothing about the underlying book. The least benign is that the departures and the NHB inspection are connected. An outside investor cannot currently distinguish between these, and the company has not provided information that would allow the distinction to be made. That is the core problem: not that something is known to be wrong, but that the normal machinery of assurance — a long-tenured CFO, a long-tenured CRO, an unremarked-upon regulator — has all gone offline at once.

Second, the specific nature of the reported allegations matters more than the amount. ₹400–500 crore is small against a ₹239 billion book. But loan classification is not a treasury issue; it is a data-integrity issue. If loans were mis-tagged to obtain concessional refinance — by borrower category, by geography, by product type — then the question naturally extends to whether classification elsewhere in the system is reliable, including the classification that produces the 1.11% gross NPA figure the entire equity story rests on. Aavas denies the allegations, and no adverse regulatory finding has been made public.14 But the reason the market reacted the way it did is that the alleged failure sits at the join between "the numbers are good" and "the numbers are what the company says they are."

Third, funding cost. A rating watch does not raise borrowing costs by itself, but it removes negotiating power at renewal. With spreads already guided below 5% for FY27 and a mix shift toward lower-yielding home loans, there is less cushion than there was.12

Fourth, the prepayment rules. This one is certain, not speculative. Aavas's most profitable loans are its seasoned ones, and the RBI has just made them cheaper to take away.18 Management said no alarming balance transfer trend has appeared.2 That is worth believing for now and worth re-testing every quarter, because the rule applies only to loans sanctioned from January 2026 — meaning the full effect will not be visible in the data for another two to three years, by which time it will be very hard to reverse.

Fifth, and most quietly, geographic concentration: 64% of assets in three states, as CARE noted.17 Contiguity was a strength in the building phase. It is a correlated-risk exposure in a downturn.

Where does that leave the "why win / why not" spine? Aavas wins from here if the Process Power thesis is real — if the appraisal method and the 55% LTV discipline genuinely produce a book that behaves better than its yield implies, and if the new management can run that machine at 17–18% growth without loosening it. The evidence for that thesis is fourteen years of low delinquency across a pandemic, which is not nothing. Aavas does not win if the informational advantage was partly an artefact of classification and reporting choices now under review, or if the combination of prepayment deregulation and a bank-led balance-transfer assault strips out seasoned assets faster than new origination replaces them. Both failure paths would show up in the same place: the growth rate holding while the quality of growth deteriorates.

Three KPIs, and Only Three

Three metrics deserve continuous tracking.

The first is the 1+ days past due ratio, currently 3.76%.1 Not gross NPAs — those are a lagging, definition-dependent measure, and in a book where the collateral is worth twice the loan, they understate stress for years. Early delinquency is where informal-sector underwriting reveals itself first, and it is the number that would move if standards had quietly slipped.

The second is the run-off or repayment rate on the existing book, which management disclosed rose above 19% before normalising.2 This is the direct measure of the balance transfer tax under the new prepayment regime. A book growing 17% while running off at 25% is a fundamentally different business from one growing 17% while running off at 15%, even though the headline growth is identical.

The third is spread, currently around 5.06% and guided below 5%.1 It captures the cost-of-borrowing consequence of the rating watch and the yield consequence of the mix shift toward home loans in a single number. If spread erodes faster than the cost-to-income ratio improves, the return-on-equity stability management promised does not happen.

Everything else — branch count, disbursement growth, profit after tax — is downstream of these three.

X. Playbook & Strategic Lessons

Strip away the specifics and three transferable lessons remain, each of which is being tested in real time.

Lesson One: Own the Information Channel

Lesson one: in an information-poor market, own the information channel or accept that you don't have one. The decision to source every loan in-house — no direct selling agents, ever — looked for years like an expensive eccentricity. It cost Aavas growth relative to peers who rented distribution, and it meant every new district required hiring and training before it could produce a rupee of loans. What it bought was that the story a borrower told was told to an Aavas employee, verified by an Aavas employee, and collected on by an Aavas employee whose pay depended on both origination and repayment. In markets where the lender can independently verify income from records, outsourcing distribution is fine. In markets where the intermediary controls the only information that exists, outsourcing distribution means outsourcing credit judgement to someone paid on volume. That distinction explains a large share of the difference between Indian lenders that survived 2018 and 2020 and those that did not.

Lesson Two: Separation Buys the Right Balance Sheet

Lesson two: spin-offs create focus, and focus is a real, if unglamorous, source of advantage. Aavas exists because a regulator made AU Financiers choose between being a bank and owning a mortgage lender. The forced separation turned out to be the making of it — not because the parent was a bad owner, but because a fifteen-year mortgage book and a deposit-funded bank want fundamentally different treasuries, different capital plans and different risk appetites. Freed to build a liability structure matched to its assets, Aavas assembled the long-dated, diversified funding base that carried it through the IL&FS freeze. The general principle: when a business unit's optimal capital structure differs sharply from its parent's, the strategic case for separation is usually stronger than the synergy case for keeping it.

Lesson Three: Build the Liability Base Before the Storm

Lesson three: diversify liabilities before you need to, and prefer lenders whose motivations aren't correlated with market sentiment. The cost of Aavas's funding conservatism was visible every quarter in slightly lower margins than a lender rolling cheap short-term paper. The benefit arrived all at once, in one week of September 2018, and again through the pandemic. The addition of IFC and, this February, ADB to the funding stack extends the same logic: development finance institutions lend against mandate fit and multi-year diligence, not against the mood of the domestic bond market.89 For any emerging-market non-bank lender, the question is not "what is my cost of funds today" but "who will still lend to me in the worst month of the next decade."

Lesson Four: A People-Based Moat Is Only as Durable as the People

And a fourth lesson, less comfortable, that this company is currently supplying: operating excellence built on people is only as durable as the people. Aavas's advantage was never a patent or a network. It was a way of working, held in the heads and habits of an organisation and enforced by a small number of senior executives who had been doing it for over a decade. When a founder, then a CEO, then a CFO, a CRO and a CBO all leave within a few years — the last four within a single quarter — the institutional memory that constitutes the moat is exactly what is at risk. Process Power is real, but it is not automatic. It has to be transmitted.

Where the Story Stands

Which brings the story back to the present. Manu Yeshpal Singh has inherited a business that, on every operating metric disclosed for the June 2026 quarter, is performing well: growing faster than it has in years, improving its cost structure, and reporting the best asset quality in its peer group.1 He has also inherited an unfinished regulatory engagement the company describes as routine and the press has described as anything but, an interim CFO and an interim CRO, two rating agencies waiting for clarity, and a shareholder base that has watched the stock fall by roughly a third from its high while the fundamentals it can see have improved.14151617

The next few quarters will settle which of those two pictures is the real one. If the NHB matter closes without material finding, the permanent CFO and CRO appointments land well, and early delinquency and run-off rates hold where they are, then 2026 will read in hindsight as an ownership transition that looked messier than it was — and Aavas will still be the company that figured out how to lend money to people no algorithm can see. If instead the classification questions widen, or seasoned borrowers begin walking out the door that the RBI opened in January, then the fourteen-year record will have to be re-read with a more sceptical eye.

Neither outcome is knowable today. What is knowable is exactly where to look.

References

-

Aavas Financiers Q1 FY27 slides: 41% disbursement surge, margins expand — Investing.com, 2026-07-21 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

AAVAS Financiers Ltd (BOM:541988) Q1 2027 Earnings Call Highlights — GuruFocus via Yahoo Finance, 2026-07-21 ↩↩↩↩↩↩↩↩↩↩↩

-

CVC Funds to acquire 26.47% stake in Aavas Financiers from Kedaara Capital and Partners Group's Affiliate — CVC Capital Partners, 2024-08-10 ↩↩

-

Sushil Kumar Agarwal — EY Entrepreneur Of The Year India, Winners 2020 ↩↩

-

Partners Group and Kedaara acquire housing finance arm — Private Equity International, 2016-02-16 ↩

-

Kedaara Capital completes the sale of its residual stake in Aavas Financiers — Kedaara Capital, 2025-07-02 ↩↩↩

-

IFC, Aavas Financiers to Help Catalyze Affordable Green Housing Finance for Low-income Borrowers in India — International Finance Corporation, 2020-12-02 ↩↩↩

-

ADB partners with Aavas Financiers to expand affordable housing, MSME lending in India — The Tribune, 2026-02-24 ↩↩

-

Anagram Partners represents CVC in the acquisition of a majority stake in Aavas Financiers — Anagram Partners, 2024-08-14 ↩

-

Aavas Financiers Limited — Open Offer Public Announcement, CVC Capital Partners, 2024-08-10 ↩

-

Affordable Housing Finance Company Valuation Comps — Ambit Capital Research, 2026-01-15 ↩↩

-

Leadership transition announcement — Aavas Financiers, Ref. AAVAS/SEC/2026-27/2360, 2026-04-20 ↩↩↩

-

AAVAS Financiers shares slip 8%; company clarifies on 'discrepancies' in certain loan classifications — Business Today, 2026-06-22 ↩↩↩↩↩↩

-

Aavas Financiers' ₹500 Crore Refinance Recall: NHB Probe Exposes Classification Failures, Says Report — Moneylife, 2026-06 ↩↩↩

-

Aavas Financiers' key debt ratings placed on watch by ICRA amid senior management exits — Whalesbook, 2026-07-01 ↩↩↩

-

Aavas Financiers' Ratings on Watch by CARE Amidst Leadership Changes — Whalesbook, 2026-07-01 ↩↩↩↩

-

RBI bans pre-payment penalties on floating rate loans for MSEs, individuals from Jan 1 — News on AIR (Prasar Bharati), 2025-07-03 ↩↩

-

India Affordable Housing Finance Market 2026: Size, Growth & Outlook — Home First Finance, 2026 ↩↩↩↩

-

Aavas Financiers Limited Q4 FY26 Earnings Conference Call Transcript — Aavas Financiers, 2026-05 ↩↩↩

-

National Housing Bank — Refinance Schemes and Regulatory Directives ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube