India Shelter Finance Corporation: Democratizing Home Ownership in India

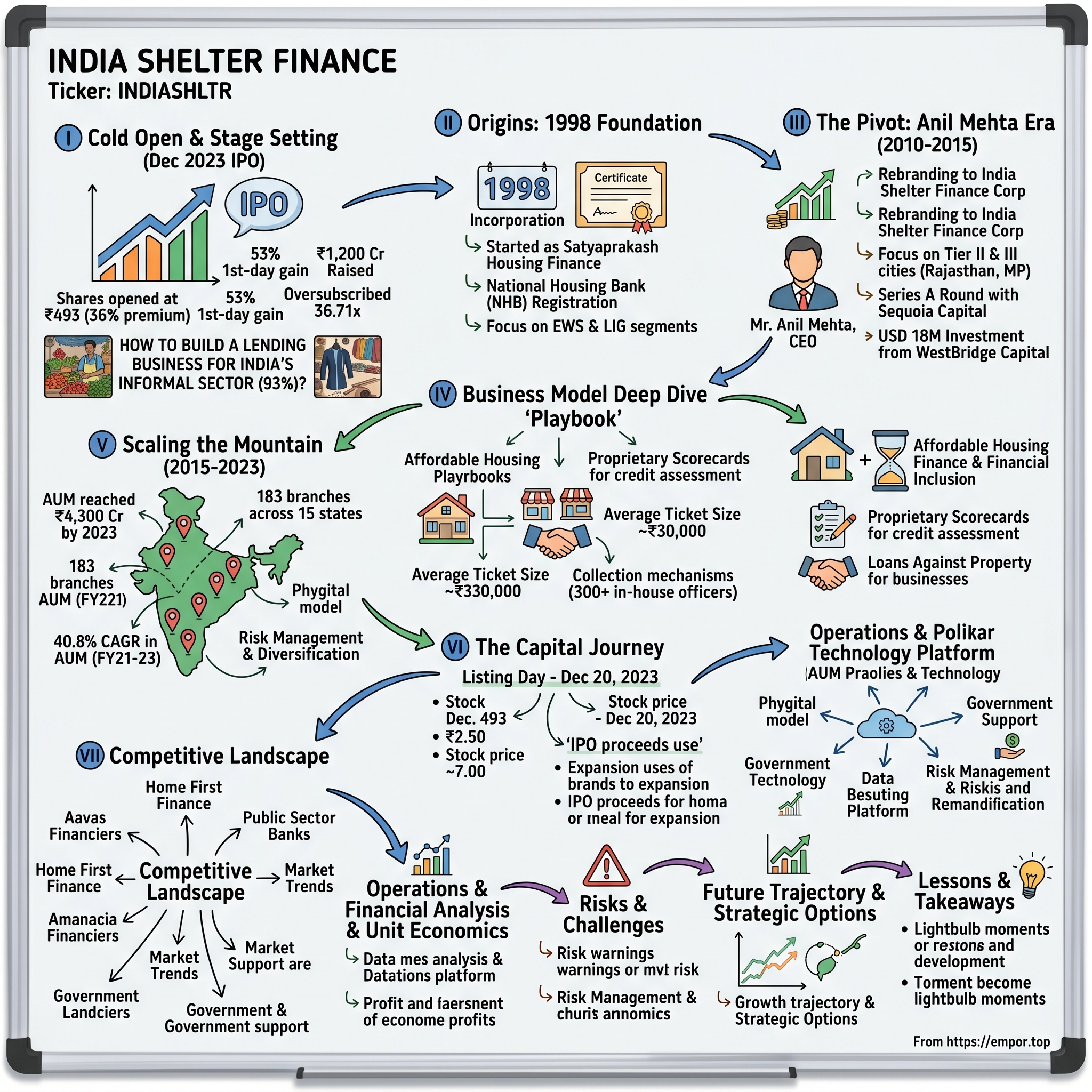

I. Cold Open & Stage Setting

The trading floor at the National Stock Exchange erupted at 10 AM on December 20, 2023. India Shelter Finance Corporation's shares opened at ₹493—a 36% premium to its IPO price of ₹363. Within minutes, the stock hit the upper circuit, locking in a 53% gain on its first day. For a company that most Indians had never heard of, this was a remarkable debut.

But the real story wasn't in the trading terminals. It was in the small towns of Rajasthan, where a vegetable vendor had just received approval for his first home loan. In the narrow lanes of Indore, where a tailor running a small shop could finally dream of owning rather than renting. This is the story of how India Shelter Finance Corporation built a ₹9,972 crore company by serving customers that traditional banks wouldn't touch.

The IPO itself told a compelling tale: ₹1,200 crore raised, with the issue oversubscribed 36.71 times. Qualified institutional buyers scrambled for shares, oversubscribing their portion by 89.70 times. The fresh issue of ₹800 crore would fuel expansion, while the ₹400 crore offer for sale gave early investors their payday. But these numbers only hint at the deeper transformation—how a company incorporated in 1998 as Satyaprakash Housing Finance became the gateway to homeownership for India's informal economy.

The question that drives this narrative: In a country where 93% of the workforce operates in the informal sector, where income proof is a luxury and credit histories are non-existent, how do you build a lending business? How do you assess risk when your customer's income comes from selling vegetables, tailoring clothes, or running a small tea stall? And perhaps most importantly, how do you scale this model from a handful of branches to 183 locations across 15 states?

This is not just a story about finance. It's about the architecture of aspiration in modern India—where technology meets tradition, where algorithms assess creditworthiness alongside personal visits, and where a housing finance company becomes a social infrastructure provider. As we'll discover, India Shelter's journey from obscurity to public markets reveals fundamental truths about financial inclusion, the limits of digital disruption, and the enduring power of patient capital in emerging markets.

II. Origins: The 1998 Foundation

October 26, 1998. The Asian Financial Crisis was still reverberating through emerging markets. India's GDP growth had slowed to 4.8%. In this environment of economic uncertainty, Satyaprakash Housing Finance India Limited quietly incorporated in New Delhi. The timing seemed almost perverse—launching a housing finance company when liquidity was tight and consumer confidence shaken.

But India's housing crisis didn't pause for macroeconomic headlines. By 1998, urban India faced a shortage of 19 million homes, with 95% of this deficit concentrated in the economically weaker sections and low-income groups. The formal banking system, still recovering from the bad loans of the early 1990s, showed little interest in serving customers who couldn't provide salary slips or income tax returns. This wasn't a gap in the market—it was a chasm.

The National Housing Bank, established in 1988 as the apex institution for housing finance, granted Satyaprakash its certificate of registration that same year. This wasn't just bureaucratic approval; it was entry into one of India's most regulated financial sectors. The NHB's dual mandate—promoting housing finance institutions while protecting depositors—created a framework that was both enabling and constraining. Capital adequacy requirements, provisioning norms, and exposure limits would shape every strategic decision for the next two decades.

The early years were marked by what can only be described as institutional anonymity. Satyaprakash operated in the shadows of larger housing finance companies like HDFC and LIC Housing Finance. Annual reports from this period—if they existed—have been lost to time. What we know comes from regulatory filings and the occasional mention in industry reports. The company experimented with different customer segments, struggled with collections, and learned painful lessons about risk assessment in India's informal economy.

By 2005, Satyaprakash had built a small portfolio concentrated in North India. But it was clear that incremental growth wouldn't unlock the opportunity. The company needed fresh thinking, new capital, and most importantly, leadership that understood both the complexity of informal sector lending and the discipline required to build a scalable financial institution. The stage was set for transformation, though it would take another five years for the catalyst to arrive.

The regulatory landscape itself was evolving. The NHB introduced new guidelines for asset classification, tightened provisioning norms, and pushed for better corporate governance. These changes, while challenging for smaller players, also created opportunity. Companies that could meet higher standards would gain credibility with institutional investors and rating agencies. For Satyaprakash, compliance became a competitive advantage—a signal that despite its small size, it was building for the long term.

What made this period particularly challenging was the fundamental mismatch between housing finance economics and customer reality. Traditional models assumed stable, verifiable income—the domain of salaried employees. But India's housing shortage was concentrated among daily wage earners, small business owners, and self-employed professionals whose income patterns were volatile and largely undocumented. The company that could crack this puzzle wouldn't just capture market share; it would essentially create a new market. As the decade ended, Satyaprakash stood at an inflection point, ready for the transformation that would redefine its identity and trajectory.

III. The Pivot: Anil Mehta Era & Transformation (2010-2015)

The year 2010 marked not just a rebranding but a complete reimagining of what the company could become. In March, Satyaprakash Housing Finance officially became India Shelter Finance Corporation—a name change that signaled ambition beyond nomenclature. Started in current form by Mr. Anil Mehta, the transformation went far deeper than corporate cosmetics.

Anil Mehta brings experience from previous roles at Max Life Insurance Company Limited, ANZ and Bank of America—a pedigree that mattered in an industry where credibility was currency. His arrival coincided with a fundamental strategic pivot: forget competing with HDFC in Mumbai's tony suburbs; instead, focus on Bhilwara, Bharatpur, and Bhopal—cities where a ₹5 lakh home loan could change a family's trajectory.

The capital structure tells its own story of ambition meeting opportunity. Sequoia Capital made their first investment in India Shelter Finance Corporation on Jul 30, 2010 in its Series A round, marking the beginning of institutional validation. This wasn't charity—Sequoia doesn't do charity. They saw what Mehta saw: an addressable market of 100 million households that banks considered unbankable.

India Shelter Finance Corporation is a public company based in Gurugram (India), founded in 2010 by Srinath Mukherji, Sanjaya Gupta, Anjali Metha and Chandra Prakash Sanadhya. This founding team brought complementary skills—Mehta's banking experience, coupled with co-founders who understood ground-level operations and technology infrastructure. The company obtained a fresh certificate from the National Housing Bank in 2010, essentially starting with a clean regulatory slate.

The initial geography choice was deliberate: Operations in Raj. & MP—Rajasthan and Madhya Pradesh. These states represented the perfect laboratory for India Shelter's thesis. Large informal economies, growing aspirational middle class, minimal competition from traditional banks, and state governments increasingly focused on affordable housing. In Rajasthan's textile markets and Madhya Pradesh's agricultural mandis, India Shelter found its first customers—small traders, shop owners, and service providers who had never walked into a bank branch.

Building the operational foundation required rethinking every assumption about housing finance. Traditional banks relied on salary slips and Form 16s. India Shelter's customers had neither. Instead, loan officers learned to assess creditworthiness through business cash flows, community reputation, and asset ownership patterns. They developed proprietary scorecards that weighted factors like years in business, family structure, and local market dynamics—metrics that would make a traditional credit analyst nervous but reflected ground reality.

WestBridge Capital, an investment company with offices in India, Mauritius and the US, is making its first investment in the India Shelter Finance Corporation. WestBridge will invest USD 18 million in the firm, and Sequoia Capital and Nexus Venture Partners, which are previous shareholders in India Shelter, will invest an additional total of USD 12 million. This January 2015 funding round wasn't just about capital—it was about patient capital. WestBridge's involvement signaled a long-term commitment to building infrastructure for financial inclusion.

The technology strategy during this period was pragmatic rather than revolutionary. While fintech startups were promising to digitize everything, India Shelter recognized that their customers needed human touch points. The company invested in basic loan origination systems, simple mobile applications for field officers, and centralized underwriting platforms. But the real innovation was in process design—creating standardized workflows that could assess informal income, verify property titles in areas with unclear documentation, and manage collections in cash-dominant economies.

Culture became the invisible differentiator. India Shelter wasn't hiring from HDFC or ICICI Bank. They recruited locally, trained intensively, and created career paths for people who understood their markets intimately. A branch manager in Kota wasn't just processing loans; they were embedded in the local economy, attending community functions, understanding seasonal income patterns, and building trust networks that no algorithm could replicate.

By 2015, the foundation was set. The firm holds a loan portfolio of INR 1.4 billion (USD 23 million) disbursed via 32 branches. These numbers seem modest compared to what would come, but they represented proof of concept. India Shelter had demonstrated that you could lend profitably to India's informal economy at scale. The next phase would test whether this model could grow from dozens of branches to hundreds, from millions in assets to billions, all while maintaining the discipline that made the model work. The transformation from Satyaprakash to India Shelter was complete—now came the real challenge of scaling the mountain.

IV. Business Model Deep Dive: The Affordable Housing Playbook

Picture a typical India Shelter customer: Ramesh runs a small hardware shop in Jodhpur, earning ₹30,000 monthly but with no salary slip to prove it. His wife Sunita teaches at a local school, adding ₹15,000 to the household income. They've been renting for twelve years, paying ₹8,000 monthly to a landlord who raises rent every year. The dream of owning a home seemed impossible—until India Shelter's loan officer walked into their shop one afternoon.

This is the genius of India Shelter's model: they built a business around customers that traditional banks actively avoided. The company operates as a retail-focused affordable housing finance provider, offering services such as home loans, loans against property, and more. But calling it just "housing finance" misses the sociological transformation at play. This is financial inclusion wrapped in mortgage documentation.

The customer segmentation data reveals the strategy's precision. Company specializes in providing affordable housing finance solutions and promoting financial inclusion, with a focus on serving low-income and informal-income individuals and families to help them achieve homeownership. But the real tell is in the demographics: 97.5% of borrowers had one or more women borrowers, and 71.3% were first-time home loan takers. These aren't just statistics—they represent fundamental shifts in property ownership patterns in small-town India.

The product suite seems simple on paper. Home loans for purchase and construction, loans against property for business expansion, and home improvement loans for renovation. India Shelter offers loans for housing improvements and construction that average INR 330,000 (USD 5,300) with terms of up to 15 years. But the average ticket size tells the story—these aren't loans for luxury apartments in Gurgaon. They're financing 500-square-foot homes in cities where ₹5 lakh can still buy dignity and security.

Why weren't banks serving this market? The answer lies in the economics of traditional banking. For a bank, processing a ₹5 lakh home loan costs almost the same as processing a ₹50 lakh loan—same documentation, same approvals, same compliance. But the revenue is one-tenth. Add the complexity of assessing informal income, the higher perceived risk, and the need for intensive field operations, and banks simply couldn't make the math work. Their cost structures, built for urban salaried customers, broke down in Tier III markets.

India Shelter flipped this equation through operational innovation. Instead of centralized processing centers in metros, they embedded operations in local markets. Instead of relying on credit bureau scores (often non-existent for their customers), they developed proprietary assessment models. Instead of standard documentation requirements, they accepted alternate proofs of income—bank account statements showing regular deposits, GST returns for small businesses, even rental receipts as proof of payment capacity.

The unit economics reveal why this model works. While banks might charge 8-9% for home loans to prime customers, India Shelter could charge 13-14% to subprime segments—not predatory pricing, but risk-adjusted returns that their customers gladly paid for access to formal credit. The cost of funds might be 8-9%, giving them a 5-6% spread versus 2-3% for traditional banks. Higher spread compensates for higher operational costs and credit risks.

Collection mechanisms became the secret sauce. With over 300 in-house collection officers, the company built a physical infrastructure that technology couldn't replace. These officers didn't just collect EMIs; they understood customer cash flows, provided financial counseling, and often helped customers through temporary difficulties. The relationship was pastoral, not transactional—a critical difference when dealing with volatile income streams.

The risk management philosophy deserves special attention. Traditional lenders view informal income as risky by definition. India Shelter recognized that a vegetable vendor who's operated the same stall for 15 years might be more stable than a software engineer in a startup. They looked at business vintage, community standing, asset ownership, and family structures. A joint family with multiple earning members represented lower risk than a nuclear family with single income—insights that emerged from thousands of field observations.

Technology played a supporting, not leading role. The company developed iServe, a customer service app, but the real innovation was in process technology—standardizing field assessments, creating centralized underwriting models, and building early warning systems for portfolio management. This wasn't about eliminating human judgment but augmenting it with data and consistency.

The competitive moat emerged from this operational complexity. A new entrant couldn't just throw capital at this market. They needed thousands of trained field officers, deep local knowledge, sophisticated risk models calibrated to informal economies, and patient investors willing to accept J-curve returns. By the time competitors recognized the opportunity, India Shelter had already built dense networks in their core markets—networks that took years to develop and couldn't be replicated quickly.

V. Scaling the Mountain: Growth Story (2015-2023)

The conference room at India Shelter's Gurgaon headquarters in early 2015 had a map of India covering an entire wall. Red pins marked existing branches—32 clusters mainly in Rajasthan and Madhya Pradesh. Yellow pins showed potential markets. By 2023, almost the entire map would be red. The transformation from regional player to national force happened not through blitzkrieg expansion but through what management called "concentric growth"—expanding outward from strength rather than scattered presence.

The numbers tell a story of extraordinary momentum. From that initial portfolio of ₹140 crore in 2015, India Shelter reached AUM reached 4300 Cr by 2023. This represents a 40.8% CAGR in assets under management between FY 2021-2023 alone—growth rates that would make Silicon Valley jealous, achieved in the decidedly unsexy business of small-ticket mortgages.

The branch expansion strategy revealed methodical thinking. By March 2023, the company operated 183 branches across 15 states, covering 94% of India's affordable housing finance market. But the sequence mattered more than the speed. Each new state entry followed a playbook: establish a hub in the state capital, understand local regulations and property registration processes, recruit from regional rural banks and microfinance institutions, then expand to Tier II and III cities in concentric circles.

Maharashtra came after Rajasthan. Gujarat followed Madhya Pradesh. Each expansion leveraged learnings from previous markets while respecting local nuances. In Tamil Nadu, joint family structures meant different risk assessments than in Punjab. In West Bengal, the company had to navigate different political economies than in Karnataka. This wasn't copy-paste expansion—it was localized adaptation within a standardized framework.

The "Phygital" model—a portmanteau that would normally induce eye-rolls—actually captured something essential about India Shelter's evolution. While fintech competitors promised fully digital lending, and traditional players remained stubbornly physical, India Shelter found the productive middle. Loan origination started digitally with mobile apps for lead capture and initial documentation. Field verification happened physically because you can't assess property quality through photos. Underwriting combined algorithmic scoring with human judgment. Disbursement went digital through bank transfers. Collections remained primarily physical because relationship management couldn't be automated.

Technology infrastructure investment accelerated during this period. The company built centralized underwriting hubs that could process applications from across the country while maintaining local market knowledge. They developed early warning systems that could flag potential delinquencies based on payment patterns, seasonal factors, and local economic indicators. The iServe app gave customers digital access while maintaining human touchpoints for complex queries.

But the real scaling challenge wasn't technology—it was human capital. Growing from 500 employees to over 3,000 meant institutionalizing what had been informal knowledge. India Shelter created detailed training programs that went beyond credit assessment to include local market dynamics, customer psychology, and even basic financial counseling. They built career paths that allowed successful field officers to become branch managers, creating internal mobility that retained institutional knowledge.

Risk management evolved with scale. What worked for a ₹500 crore portfolio wouldn't suffice for ₹4,000 crore. The company implemented three lines of defense: field officers as the first line, regional credit managers as the second, and centralized risk management as the third. They created portfolio concentration limits—no single branch could exceed 3% of total AUM, no single state could cross 25%. Geographic diversification became a risk mitigation strategy, not just a growth imperative.

The collection infrastructure scaled remarkably. Those 300+ collection officers weren't just collecting payments—they were data gathering nodes, early warning systems, and customer relationship managers rolled into one. The company maintained collection efficiency above 98% even as the portfolio grew exponentially—a testament to operational discipline in markets where cash still dominated and digital payments remained sporadic.

Funding sources diversified alongside growth. While equity capital from WestBridge, Sequoia, and Nexus provided the foundation, debt became the growth fuel. The company accessed funding from banks, financial institutions, and eventually the National Housing Bank. Cost of funds improved with scale and track record—from 11% in early years to 8-9% by 2023, directly improving unit economics.

Competition intensified during this period. Aavas Financiers went public in 2018, validating the affordable housing finance model. Home First Finance and Aptus Value expanded aggressively. Banks started creating specialized affordable housing verticals. But India Shelter's first-mover advantage in many markets, combined with deep operational expertise, created defensible positions. In many Tier III cities, India Shelter wasn't just a lender—they were the only formal lending option for informal sector customers.

The cultural challenge of scaling deserved special mention. How do you maintain entrepreneurial energy while building institutional processes? How do you preserve customer intimacy while standardizing operations? India Shelter's answer was radical decentralization within strict frameworks. Branch managers had significant autonomy in customer acquisition and relationship management but operated within rigid risk parameters. Regional heads could adapt products to local needs but couldn't breach pricing guidelines. This balance—freedom within framework—enabled scaled intimacy.

By 2023, India Shelter had proven something important: financial inclusion could be profitable at scale. The ₹4,300 crore AUM wasn't just a number—it represented approximately 100,000 families who owned homes they couldn't have afforded through traditional channels. The company had cracked the code on serving India's vast informal economy profitably, setting the stage for the next chapter—taking this proven model to public markets.

VI. The Capital Journey: From Private to Public

The board meeting in early 2023 had an air of inevitability. India Shelter had exhausted the private capital playbook—multiple funding rounds, blue-chip investors, steady growth. The public markets beckoned not just as a liquidity event but as a validation of the affordable housing finance model itself. The decision to IPO wasn't just financial engineering; it was a statement that serving India's informal economy could create institutional-grade returns.

The private equity years had been formative beyond just capital injection. India Shelter Finance Corporation has raised $111M in funding from investors like WestBridge Capital, Sequoia Capital and Nexus Venture Partners. But more than money, these investors brought discipline. Sequoia pushed for technology infrastructure. WestBridge insisted on governance standards. Nexus demanded operational metrics that went beyond traditional financial reporting. This institutional grooming prepared India Shelter for public market scrutiny.

The anchor investor round in December 2023 became a telling moment. ₹360 crore raised from institutional investors before the public offering opened—this wasn't just pre-IPO funding but a vote of confidence from sophisticated investors who had done deep diligence. The anchor book included domestic mutual funds who understood India's financial inclusion story and global investors betting on consumption growth in Tier II/III India.

Why December 2023? The timing seemed counterintuitive—global markets were volatile, interest rates were elevated, and tech IPOs were struggling. But India Shelter's leadership recognized a window. The affordable housing narrative was peaking with government support, the company's metrics were robust, and most importantly, there was genuine institutional appetite for quality financial services IPOs after years of tech-heavy listings.

The IPO structure itself revealed strategic thinking. The ₹800 crore fresh issue would fund expansion—new branches, technology upgrades, and regulatory capital for growth. The ₹400 crore offer for sale gave early investors partial exits while maintaining skin in the game. This wasn't a complete cash-out; major investors retained significant stakes, signaling continued confidence in the growth trajectory.

The subscription data became its own narrative. Overall subscription of 36.71 times meant investors bid for ₹44,000 crore worth of shares against ₹1,200 crore on offer. But the composition mattered more than the multiple. Qualified Institutional Buyers oversubscribed 89.70 times—smart money was scrambling for allocation. Retail investors, often seen as momentum chasers, showed more measured interest with 3.67 times subscription. This inversion—institutions more enthusiastic than retail—suggested fundamental rather than speculative interest.

The pricing discovery process exposed market dynamics. At ₹363 per share, the company was valued at approximately ₹6,000 crore at listing—nearly 3 times book value. For context, established housing finance companies traded at 1.5-2 times book. The premium reflected growth expectations, but also scarcity value—pure-play affordable housing finance companies were rare in public markets.

December 20, 2023: listing day delivered drama worthy of the buildup. Opening at ₹493 against the issue price of ₹363—a 36% premium—the stock hit upper circuit within minutes, closing the day up 53%. Trading volumes suggested this wasn't just operator-driven price discovery but genuine institutional accumulation. The market cap crossed ₹9,000 crore on day one, instantly making India Shelter one of the most valuable affordable housing finance companies in India.

Post-IPO shareholding patterns revealed the new reality. Promoters held approximately 2%, a remarkably low percentage that raised governance questions but also suggested professional management rather than promoter-driven operations. Institutional investors—both domestic and foreign—held over 70%, creating a sophisticated shareholder base that would demand performance but understand the business model's nuances.

The use of IPO proceeds followed through on promises. Within six months, India Shelter announced expansion into three new states, launched digital initiatives for customer acquisition, and strengthened its capital adequacy ratio to support future growth. The company didn't just raise capital; it deployed it strategically, validating investor confidence.

Market reception in subsequent quarters proved the IPO wasn't just listing day euphoria. The stock found support above ₹450 levels, maintaining valuations that reflected continued confidence. Quarterly results showing consistent growth in AUM and maintained asset quality reinforced the narrative that India Shelter represented a structural play on financial inclusion rather than a cyclical bet on real estate.

The competitive implications were significant. The successful IPO validated the affordable housing finance model for other players and potential new entrants. It also raised the bar—India Shelter now had permanent capital advantages that would be hard for private competitors to match. The company could access debt markets more efficiently, attract talent with stock options, and pursue acquisitions if opportunities arose.

For the founders and early employees, the IPO represented more than financial rewards. It validated a decade-long bet that serving India's underserved could create sustainable value. The journey from struggling to establish credibility with first institutional investors to commanding premium valuations in public markets exemplified how patient capital and operational excellence could transform niche opportunities into mainstream businesses. The public listing wasn't an exit—it was an entry into the next phase of institutional growth.

VII. Competitive Landscape & Market Dynamics

The map on the conference room wall at India Shelter's headquarters had many red pins—one for each branch. But the competitive landscape map on the adjacent wall told a different story. India's mortgage market can be broadly divided into two segments: loans with a ticket size above ₹15 lakh (normal mortgage market) and loans with a ticket size of ₹15 lakh and below (Affordable Housing). Affordable Housing focused loans constituted around ₹4.3 lakh crore as of March 2023—a massive addressable market where India Shelter competed with an increasingly sophisticated set of players.

The affordable housing market, valued at $300 billion, had attracted everyone from public sector banks to nimble fintech startups. But the real competition came from a cohort of specialized affordable housing finance companies that had emerged alongside India Shelter. Aavas Financiers major competitors are Home First Finance, Aptus Value Housing, Sammaan Capital, Can Fin Homes, PNB Housing Finance, Repco Home Finance, GIC Housing Fin. Each had carved out niches, developed unique strengths, and competed for the same customer base.

Aavas Financiers, perhaps India Shelter's most direct competitor, had taken a different path to similar outcomes. AAVAS FINANCIERS LIMITED was incorporated as a private limited Company in Jaipur, Rajasthan, under the Companies Act, 1956 on February 23, 2011. It formally started its operations in March 2012. In October 2018, the Company got listed on BSE and NSE. Going public five years before India Shelter gave Aavas first-mover advantage in capital markets. AAVAS is engaged in the business of providing housing loans, primarily, in the un-served and un-reached markets which include the States of Rajasthan, Maharashtra, Gujarat, Madhya Pradesh, Haryana, Uttar Pradesh, Chhattisgarh, Uttarakhand, Punjab, Himachal Pradesh, Delhi, Odisha, Karnataka and Tamil Nadu. Currently, we are operating in 14 states with a total of 397 branches.

The operational overlap was striking—both companies targeted similar geographies, served comparable customer segments, and faced identical challenges. Yet their approaches diverged in subtle but important ways. Aavas focused more heavily on rural markets, while India Shelter maintained stronger urban and semi-urban presence. Aavas's average ticket size skewed slightly lower, suggesting deeper penetration into lower income segments.

Aptus Value Housing Finance India Ltd is a Home Loan Company. Aptus has been formed to primarily address the housing finance needs of self-employed, low and middle income families primarily from semi-urban and rural areas. Company targets first-time home buyers where collateral is self- occupied residential property. Their southern India focus complemented rather than competed with India Shelter's northern and western concentration, though both were expanding into each other's territories.

Home First Finance brought technology differentiation to the competition. Home First Finance Company India Limited is an India-based housing finance company. The Company is a technology-driven lender that provides loans to customers from low and middle-income groups. Their emphasis on digital processes and data analytics represented a different philosophy—could technology replace the high-touch model that India Shelter had perfected?

The market dynamics revealed structural tailwinds that benefited all players. India's housing finance market, currently valued at Rs. 33,00,000 crore (US$ 379.7 billion), is projected to grow at a 15-16% compound annual growth rate (CAGR) to reach Rs. 77,00,000-81,00,000 crore (US$ 886.1-932.3 billion) by 2029-30, according to CareEdge Ratings. The growth is driven by strong structural fundamentals and government incentives, making housing finance an attractive sector for lenders.

But within this growing pie, competition intensified along multiple dimensions. Public Sector Banks (PSBs) currently dominate the home loan market with a 40% share, followed by Housing Finance Companies – HFCs (34%), Private Banks (20%), Others (4%), and NBFCs (2%). However, HFCs are significant players with a growing presence. This growing competition benefits borrowers by potentially driving down interest rates and improving loan terms.

The government's role as market maker cannot be overstated. Government schemes like Pradhan Mantri Awas Yojana (PMAY) and Affordable Housing Fund (AHF) play a pivotal role in boosting the housing finance market. These initiatives aim to promote affordable housing for low-income groups and offer subsidies and incentives to both homebuyers and developers. Such support encourages lending institutions to extend credit to underserved segments of the population, thereby driving market growth.

The competitive dynamics created interesting strategic choices. Pure-play affordable housing companies like India Shelter, Aavas, and Aptus competed on operational excellence and local market knowledge. Banks leveraged lower cost of funds but struggled with last-mile connectivity. NBFCs brought innovation but lacked the patient capital for long-gestation mortgage assets. Each model had trade-offs that prevented any single player from dominating.

The performance metrics revealed competitive positioning. Even as these companies together have grown at a compound annual growth rate of 25% over last five years, outpacing Industry growth of 15%, their combined market share remains a paltry 2% versus 40% share of low-ticket size loan (less than 2.5 million) in Rs 29 trillion housing loan industry. This paradox—rapid growth yet minimal market share—highlighted both the opportunity and the challenge. The market was so vast that even aggressive expansion barely moved market share needles.

Valuation differentials told their own story. Market Cap of Aavas Financiers is ₹13,302 Crs. While the median market cap of its peers are ₹10,484 Crs. India Shelter's post-IPO market cap of ₹9,972 crore positioned it competitively but not dominantly. The market was valuing execution capability and growth potential rather than current market position.

The interest rate environment added another layer of complexity. Rising rates hurt affordability but improved spreads. Falling rates increased demand but compressed margins. Each company's asset-liability management, cost of funds, and pricing power determined their ability to navigate these cycles. India Shelter's diversified funding sources and strong capital position provided buffers that smaller competitors lacked.

Technology emerged as both battleground and enabler. While India Shelter maintained its "phygital" approach, pure digital players were testing whether affordable housing could be fully digitized. Early evidence suggested that while digital could handle lead generation and initial processing, the complexity of property verification, income assessment for informal sector customers, and collection management still required human intervention.

Looking forward, the competitive landscape would likely consolidate. India has a low penetration rate for housing finance compared to other emerging markets, reflected in its low mortgage-to-GDP ratio of 12.3%. This indicates significant potential for growth in the Indian housing finance market. However, the low penetration rate presents an opportunity for HFCs and other lenders to expand their businesses, and the government's focus on affordable housing could further increase mortgage finance penetration in India. The companies that could scale efficiently while maintaining asset quality would emerge as winners in this marathon. India Shelter's challenge was clear: maintain its operational excellence while defending against both traditional competitors expanding down-market and new-age players attempting to disrupt the category entirely.

VIII. Operations & Technology Platform

The morning collection run in Jodhpur started at 6 AM. Ramesh Kumar, one of India Shelter's 300+ collection officers, checked his mobile app for the day's route—47 customers to visit, optimized for minimal travel time. But the app was just the starting point. Success in collections required something algorithms couldn't provide: understanding that the textile trader would have cash after the Monday market, that the auto-rickshaw driver's income peaked during school hours, and that the vegetable vendor preferred to pay at her stall rather than at home.

This blend of technology and human insight defined India Shelter's operational philosophy. While competitors debated digital versus physical, India Shelter had chosen both—building what they called a "phygital" infrastructure that leveraged technology where it added value while maintaining human touchpoints where relationships mattered.

The branch model remained the cornerstone of operations. Each of the 183 branches functioned as a micro-bank, deeply embedded in local communities. But these weren't traditional bank branches with tellers behind glass windows. India Shelter branches were designed for accessibility—ground floor locations in busy market areas, open layouts that felt welcoming to first-time borrowers, and staff who spoke local dialects. The average branch served a 30-kilometer radius, close enough for regular contact but large enough to achieve scale.

Branch managers wielded significant autonomy within strict parameters. They could approve loans up to ₹10 lakhs based on local assessment, adjust collection schedules for seasonal income patterns, and customize marketing for local festivals. But they couldn't breach pricing guidelines, relax documentation standards, or exceed portfolio concentration limits. This balance—freedom within framework—enabled local responsiveness without compromising institutional discipline.

The underwriting process revealed operational sophistication. When a potential customer approached India Shelter, the journey began digitally with the iServe app capturing basic information and documents. But then it turned intensely physical. Field officers visited homes, verified properties, observed business operations, and most importantly, talked to neighbors. In India's informal economy, community reputation often mattered more than credit scores.

The company developed proprietary scorecards that weighted unconventional factors. How long had the family lived in the area? Did they own gold jewelry (indicating savings behavior)? Were children attending private schools (suggesting stable income)? Did they participate in local chit funds (demonstrating payment discipline)? These seemingly random data points, when combined, created remarkably accurate risk profiles.

Technology infrastructure evolved to support this hybrid model. The loan origination system could handle applications from 183 branches simultaneously, process documents in 11 languages, and integrate with 23 banks for disbursement. But the real innovation was in edge computing—branch-level servers that could operate independently during internet outages, common in Tier III cities, then sync when connectivity resumed.

The collection mechanism deserved special attention. Those 300+ collection officers weren't just payment collectors; they were relationship managers, early warning systems, and financial counselors. Each officer managed approximately 300 accounts, visiting 40-50 customers daily. They used tablets to record payments, update customer information, and flag concerns. But success came from soft skills—knowing when a customer needed restructuring versus when they needed firmness, understanding family dynamics that affected payment capacity, and building trust that prevented willful defaults.

The collection app used behavioral analytics to optimize routes and timing. It learned that certain customers paid more reliably on specific days, that some markets had weekly closing days, and that collection success rates varied by time of day. The algorithm continuously refined these patterns, improving collection efficiency by 15% over manual routing.

But technology also enabled proactive risk management. Natural language processing analyzed field notes to identify early stress signals—mentions of medical emergencies, business downturns, or family disputes that could affect repayment. Machine learning models predicted delinquency probability 60 days in advance with 73% accuracy, allowing preventive interventions.

The digital transformation accelerated during COVID-19, though not in ways originally planned. Video KYC, initially seen as futuristic, became necessary during lockdowns. WhatsApp emerged as a powerful collection tool—not for payments but for maintaining customer contact when physical visits weren't possible. UPI integration finally gave customers digital payment options, though adoption remained below 30% even by 2023.

Data analytics capabilities grew sophisticated. India Shelter could now track portfolio performance by geography, customer segment, vintage, and dozens of other parameters in real-time. Heat maps showed delinquency patterns, helping identify problematic regions before they became crisis zones. Cohort analyses revealed that customers acquired during certain months performed better—insights that shaped acquisition strategies.

Yet the company resisted full automation in crucial areas. Loan approval remained human-dependent because algorithms couldn't assess the subtleties of informal income. Collection strategies stayed relationship-based because automated reminders annoyed customers accustomed to personal interaction. Property valuation required physical inspection because photos could hide structural issues.

The scalability challenge was real. As the portfolio grew from ₹1,000 crore to ₹4,300 crore, operational complexity increased exponentially. Each new state meant different property registration processes, documentation requirements, and legal frameworks. Each new branch required recruiting and training staff who understood local markets. Each new customer segment demanded refined risk models.

Training became a critical operational component. India Shelter established regional training centers that put new hires through 45-day programs covering everything from informal income assessment to smartphone app usage. Continuing education happened through e-learning modules, delivered via mobile apps that field staff could access during downtime. The company tracked training completion rates as closely as collection efficiency.

Quality control mechanisms evolved with scale. Random audits verified field assessments. Mystery shoppers tested branch service quality. Call centers conducted post-disbursement surveys to ensure customer satisfaction. These checks and balances prevented the operational drift that often accompanied rapid growth.

The vendor ecosystem required careful management. India Shelter worked with local property valuers, legal advisors, and document verification agencies. Managing quality and consistency across hundreds of vendors while maintaining cost efficiency demanded sophisticated vendor management systems. The company created preferred vendor panels, standardized service agreements, and performance scorecards that ensured service quality.

Looking ahead, the operational challenge was maintaining this intricate balance while scaling further. Could India Shelter preserve its high-touch service model while doubling its branch network? Could technology enhance rather than replace human judgment? Could the company maintain 98% collection efficiency as the portfolio grew beyond ₹10,000 crore? These operational questions would determine whether India Shelter could sustain its competitive advantages as it entered its next growth phase. The answer lay not in choosing between human and digital, but in orchestrating both into a symphony that served India's aspirational millions.

IX. Financial Analysis & Unit Economics

The spreadsheet on the CFO's screen told a story of transformation. In FY2023, India Shelter reported revenue of ₹1,274 crore and profit of ₹413 crore—numbers that would have seemed fantastical when the company was restructured in 2010. But beyond the headline figures lay the intricate machinery of housing finance economics, where basis points mattered and asset-liability mismatches could destroy decades of work.

The revenue growth trajectory revealed disciplined execution. Revenue growth of 31.84% between FY2022-23 outpaced the industry significantly, but this wasn't reckless growth. Each percentage point of expansion came with careful attention to asset quality, geographic diversification, and customer selection. The company had learned that in housing finance, growing too fast was often more dangerous than growing too slow.

The interest spread mathematics drove everything. India Shelter borrowed at 8-9% and lent at 13-14%, generating gross spreads of 5-6%. This seemed generous compared to banks earning 2-3% spreads, but the economics were different. Operating expenses consumed 2-3% due to the high-touch model. Credit costs took another 1-1.5% given the customer profile. That left 1.5-2.5% for shareholders—healthy but not excessive, requiring scale to generate meaningful absolute returns.

Cost of funds had improved dramatically with institutional maturity. From borrowing at 11-12% in early years, India Shelter now accessed funds at 8-9%, with further improvement post-IPO. The funding mix had diversified—bank loans at 8.5%, NCDs at 9%, NHB refinance at 7.5%, and the occasional external commercial borrowing at lower rates. This diversification wasn't just about cost; it was about ensuring liquidity during crisis periods when single sources might dry up.

The asset quality metrics stood out in an industry often plagued by NPAs. Gross NPA below 2% and net NPA below 1% seemed almost too good for a lender focused on informal sector customers. But these numbers reflected the power of community-based lending, intensive collection efforts, and conservative underwriting. The company maintained provision coverage above 60%, conservative for the asset quality but prudent given customer profiles.

Capital adequacy told a story of preparedness. With Tier-1 capital above 40% and total capital adequacy above 45%, India Shelter operated with buffers that seemed excessive. But management remembered 2008, 2016's demonetization, and COVID-19. In housing finance, capital wasn't just regulatory requirement—it was survival insurance. The fresh capital from IPO pushed these ratios even higher, providing dry powder for growth without leverage stress.

The efficiency ratios revealed operational leverage beginning to kick in. Cost-to-income ratio had declined from 45% to 35% over five years as fixed costs spread across a larger asset base. But this wasn't just scale benefits—it reflected conscious efforts to optimize branches, digitize processes where possible, and improve employee productivity. The company now generated ₹2.5 crore of AUM per employee versus ₹1.5 crore five years ago.

Return on equity painted a nuanced picture. At 15-18%, ROE seemed modest compared to some financial services businesses. But this reflected conscious choices—maintaining high capital buffers, investing in infrastructure for future growth, and pricing loans competitively rather than extractively. Management believed sustainable 15-18% ROE was better than volatile 25% returns that attracted regulatory scrutiny and competitive response.

The stock's valuation at 3.68 times book value seemed rich by traditional metrics. Banks traded at 1-2 times book. Even high-quality NBFCs rarely exceeded 3 times. But markets were valuing India Shelter's growth runway, asset quality track record, and exposure to India's financial inclusion theme. The premium also reflected scarcity—few pure-play affordable housing finance companies with institutional quality governance.

Disbursement patterns revealed business seasonality often missed by casual observers. Q4 consistently showed highest disbursements as customers rushed to complete property transactions before fiscal year-end. Monsoon quarters saw slowdowns in construction loans. Festival seasons drove property purchases. Understanding and planning for these patterns was crucial for liquidity management and growth planning.

The unit economics at branch level showed why physical infrastructure still mattered. A typical branch required ₹50 lakh initial investment and ₹25 lakh annual operating cost. Break-even came at ₹25 crore AUM, typically achieved in 18 months. Mature branches generated ₹75-100 crore AUM with 2.5-3% ROA—attractive economics that justified expansion. But success required patient capital, as branches typically showed losses for the first year.

Asset-liability management grew increasingly sophisticated. India Shelter matched asset and liability tenures to minimize interest rate risk. They maintained positive gaps in rising rate scenarios, benefiting from rate increases. The company used interest rate swaps selectively, though the underdeveloped derivative market in India limited options. Most importantly, they maintained pricing power—the ability to pass rate changes to customers without significant demand destruction.

The credit cost evolution told a learning story. Early years saw credit costs above 2% as the company learned hard lessons about informal sector lending. Gradual improvement to 1-1.5% reflected better underwriting, improved collections, and portfolio seasoning. Management guided for normalized credit costs of 1.25%, acknowledging that zero credit cost wasn't realistic or even desirable—some risk-taking was necessary for growth.

Productivity metrics showed continuous improvement. Disbursements per loan officer increased 30% over three years. Collection efficiency improved from 95% to 98%. Turnaround time from application to disbursement decreased from 15 days to 10 days. These operational improvements directly impacted financial performance, improving both growth and profitability.

The geographical contribution analysis revealed portfolio dynamics. Rajasthan and Madhya Pradesh, the oldest markets, contributed 40% of AUM but 50% of profits due to seasoned portfolios and operational efficiency. Newer states showed faster growth but higher costs and credit losses. This J-curve pattern was expected but required careful management to ensure new market investments didn't drag overall returns.

Funding cost dynamics post-IPO deserved attention. The listing immediately reduced borrowing costs by 25-50 basis points as institutional credibility improved. Rating upgrades followed, further reducing costs. Access to new funding sources—ECBs, subordinated debt, potentially retail NCDs—provided options beyond traditional bank borrowing. The company estimated 100 basis points reduction in funding costs over the next two years.

The competitive response to India Shelter's margins was inevitable. As the company demonstrated that 5-6% spreads were sustainable in affordable housing, competition intensified. New entrants accepted lower spreads to gain market share. Banks created specialized verticals to capture this opportunity. But India Shelter's operational excellence and risk management capabilities provided moats that pure pricing competition couldn't breach.

Looking at forward projections, the path to ₹10,000 crore AUM seemed clear. Assuming 25% annual growth, maintaining current asset quality, and gradual improvement in operational efficiency, the company could achieve 18-20% ROE by FY2026. The key sensitivities were interest rate cycles, competitive intensity, and regulatory changes—variables management could influence but not control.

The financial model's resilience had been tested through multiple cycles. India Shelter survived demonetization, thrived through GST implementation, and navigated COVID-19. Each crisis proved the model's antifragility—the ability to grow stronger through stress. This track record gave investors confidence that future challenges, while unpredictable in specifics, wouldn't derail the fundamental business model. The numbers told a story, but the real narrative was about building financial infrastructure for India's next billion aspirations.

X. Risks & Challenges: High Promoter Share Pledge Risk

The risk register at India Shelter's board meeting ran to 47 pages. At the top, highlighted in red: Promoters have pledged or encumbered 97.0% of their holding. This wasn't just a technical detail buried in footnotes—it represented a sword of Damocles hanging over the company's governance structure. In a margin call scenario, control could shift overnight, destabilizing operations built over decades.

The pledge structure emerged from historical necessities. Anil Mehta, WestBridge Crossover Fund, LLC, and Aravali Investment Holdings are the company's promoters, but their 47.9% holding came with strings attached. Early-stage funding often required personal guarantees, and promoters had pledged shares to secure working capital lines when institutional funding was scarce. Now, despite the successful IPO, these pledges remained—a legacy risk that sophisticated investors flagged immediately.

Geographic concentration posed another challenge. Despite expansion to 15 states, Rajasthan and Madhya Pradesh still contributed 40% of the portfolio. A drought in Rajasthan, political instability in Madhya Pradesh, or regional economic shock could disproportionately impact asset quality. The company's response—aggressive geographic diversification—came with its own risks as new markets meant new learning curves and potential missteps.

Interest rate sensitivity cut both ways. Rising rates improved spreads but reduced affordability for target customers. A 200 basis point rate increase could push EMIs beyond many customers' capacity, potentially triggering delinquencies. Conversely, falling rates compressed margins while increasing competition from banks suddenly interested in affordable housing. The company estimated that every 100 basis point rate change impacted ROE by 150 basis points—material sensitivity for a leveraged business.

Credit risks in the informal economy defied traditional modeling. A vegetable vendor's income could halve overnight due to unseasonal rain. A small manufacturer might lose his primary client without warning. These weren't gradual deteriorations that early warning systems could catch—they were cliff events that turned performing assets into NPAs instantly. While India Shelter's community-based model mitigated some risks, black swan events remained unpredictable.

Regulatory changes loomed large. The Reserve Bank of India's takeover of housing finance regulation from the National Housing Bank in 2019 brought stricter norms. New guidelines on income recognition, asset classification, and provisioning could impact profitability. Proposed regulations on interest rate caps for affordable housing, while well-intentioned, could destroy unit economics. The company maintained regulatory buffers, but rules could change faster than business models could adapt.

Competition from fintech and digital lenders represented an existential question. Could a pure-digital player crack the code of informal sector lending without physical infrastructure? Early evidence suggested challenges—digital lenders struggled with collections, couldn't assess property quality remotely, and lacked the community relationships that enabled India Shelter's model. But technology evolved rapidly, and a breakthrough in alternative data or AI-driven assessment could obsolesce traditional models overnight.

Macro-economic headwinds multiplied risks. India's GDP growth directly impacted informal sector incomes. A slowdown meant reduced business for small traders, lower demand for services, and consequently, stress in loan repayment. The company's portfolio performed well during COVID-19, but that was partly due to regulatory forbearance and moratoriums. The next crisis might not come with similar support.

Operational risks scaled with growth. Managing 3,000+ employees across 183 branches created challenges in maintaining culture and standards. A few rogue employees engaging in aggressive collection practices could trigger regulatory action and reputational damage. The company invested heavily in training and monitoring, but perfect control was impossible in such a distributed model.

Technology risks emerged as digitization increased. Cyber attacks on financial institutions were rising. A breach exposing customer data could trigger regulatory penalties and destroy trust painstakingly built over years. The company's hybrid model—part digital, part physical—created additional vulnerabilities as data moved between systems. Investments in cybersecurity were necessary but represented cost without direct revenue benefit.

Funding risks persisted despite diversification. While the IPO provided capital buffer, India Shelter remained dependent on debt markets for growth. A liquidity crisis like 2018's NBFC squeeze could constrain growth even if the company remained fundamentally sound. Asset-liability mismatches, while managed, could become critical during systemic stress. The company maintained credit lines and diversified funding sources, but systemic risks couldn't be fully mitigated.

Political and social risks deserved consideration. Loan waivers, populist promises of debt forgiveness, created moral hazard. Why repay if politicians might waive loans before elections? State-level political dynamics impacted collection efficiency. The company's response—focusing on customer education about credit scores and future borrowing ability—helped but couldn't eliminate politically-induced delinquency.

ESG (Environmental, Social, Governance) risks grew in importance. Climate change impacted both borrowers (through extreme weather affecting incomes) and collateral (flooding or drought affecting property values). Social risks included potential backlash against collection practices in economically stressed regions. Governance risks, particularly given the promoter pledge situation, remained under scrutiny.

Succession planning represented long-term risk. The company's success was closely tied to its founding team's vision and relationships. While professional management had been instituted, the transition from founder-led to institution-led growth was always challenging. Key person risk extended beyond the CEO to regional heads who had built local franchises over decades.

Market perception risks could become self-fulfilling. If investors lost confidence due to any trigger—rising NPAs, regulatory action, competitive pressure—the stock price decline could impact funding costs, employee morale, and customer confidence. In financial services, perception often became reality as confidence was the ultimate currency.

Despite this litany of risks, India Shelter's track record suggested resilience. The company had navigated demonetization, GST implementation, and COVID-19 without material deterioration in asset quality or profitability. Risk management wasn't about elimination but intelligent acceptance—understanding which risks were worth taking for growth and which could destroy the franchise. The challenge ahead was maintaining this balance while scaling from ₹4,300 crore to ₹10,000 crore and beyond. In affordable housing finance, growth without prudence was a path to destruction, but prudence without growth meant irrelevance. Walking this tightrope would determine India Shelter's next chapter.

XI. Future Trajectory & Strategic Options

The strategy presentation to the board in early 2024 opened with a simple question: "What does India Shelter look like at ₹25,000 crore AUM?" This wasn't idle speculation—at current growth rates, they'd reach this milestone by 2028. The answer would shape every decision from branch expansion to technology investment, from product development to talent acquisition.

Geographic expansion represented the most obvious growth lever. With presence in 15 states covering 94% of the affordable housing market, the remaining white spaces were either genuinely unviable or required different operating models. The Northeast, with its unique land ownership patterns and cultural dynamics, demanded localized approaches. Southern states like Kerala, with high literacy but emigrant-dependent economies, needed products designed for NRI remittances. Each new geography wasn't just pin on a map but a multi-year commitment to understanding local nuances.

The deeper opportunity lay in penetration within existing markets. India Shelter operated 183 branches, but India had 4,000+ towns with population above 20,000. The company could triple its branch network without entering a single new state. The unit economics supported expansion—mature branches generated 25-30% ROE, justifying investment in new locations. The constraint wasn't capital but organizational capacity to maintain quality while scaling.

Product diversification offered another vector. The affordable housing opportunity: Size of the prize was estimated at $300 billion, but adjacent opportunities beckoned. Micro-enterprise loans to the same customer base leveraged existing relationships and assessment capabilities. Education loans for customers' children addressed lifecycle needs. Insurance distribution provided fee income without balance sheet risk. Each adjacency had to pass a simple test: did it leverage existing strengths without diluting focus?

Digital transformation presented both opportunity and necessity. While the core model would remain high-touch, digital could enhance every aspect. AI-powered pre-screening could identify high-potential customers before human intervention. Blockchain-based property records could reduce fraud and accelerate processing. Satellite imagery could assess property development remotely. The challenge was investing ahead of returns while maintaining profitability.

Partnership strategies could accelerate growth without proportional risk. Co-lending with banks leveraged their low-cost funds with India Shelter's origination capability. Tie-ups with property developers provided customer acquisition at source. Partnerships with fintechs could bring technological capabilities without massive internal investment. But each partnership required careful structuring to ensure aligned incentives and protected economics.

The consolidation opportunity was intriguing. India's affordable housing finance sector had dozens of small players struggling with scale, technology, and funding. India Shelter's public currency and operational platform made it a natural consolidator. Acquiring portfolios or entire companies could provide instant scale in new markets. But integration risks were real—culture clashes, asset quality surprises, and operational disruptions had destroyed value in many financial services mergers.

International expansion seemed premature but wasn't impossible. Countries like Bangladesh, Sri Lanka, and Nepal faced similar housing finance gaps with comparable informal economies. India Shelter's model could theoretically port to these markets. But regulatory complexities, currency risks, and the bandwidth required to manage international operations argued for domestic focus, at least for the next five years.

The role in India's urbanization story was fundamental. The current shortage of housing in urban areas is estimated to be ~10 million units. An additional 25 million units of affordable housing are required by 2030 to meet the growth in the country's urban population. India Shelter wasn't just financing homes; it was enabling urbanization, supporting economic mobility, and creating middle-class wealth. This narrative resonated with policymakers, potentially unlocking regulatory support and government partnerships.

Technology infrastructure investments would determine competitive positioning. The company needed to move from digitizing existing processes to reimagining them. Could underwriting happen in hours instead of days? Could collections be predicted and prevented rather than managed post-delinquency? Could customer acquisition costs be reduced through digital channels? These weren't IT projects but strategic transformations requiring CEO-level commitment.

The talent strategy required evolution. India Shelter had succeeded with locally recruited, intensively trained staff. But scaling to ₹25,000 crore AUM required different capabilities—data scientists alongside loan officers, product managers alongside branch managers, risk modelers alongside collection agents. Creating career paths for traditional employees while attracting new-age talent demanded careful cultural management.

Capital allocation would shape returns. The IPO provided growth capital, but deployment required discipline. Each rupee could go toward new branches, technology, acquisitions, or be returned to shareholders. The board's framework was clear: invest where returns exceeded 20%, maintain capital buffers for stability, and return excess to shareholders. But execution required resisting temptations—the hot new technology, the transformative acquisition, the aggressive expansion that could destroy value.

Regulatory engagement strategy mattered more as size increased. India Shelter was approaching systemically important status—large enough that its failure could impact the sector. This brought stricter oversight but also a seat at policy discussions. The company needed to balance compliance with advocacy, supporting regulations that promoted financial inclusion while resisting those that damaged economics.

The sustainable growth rate calculation was sobering. Assuming 15% ROE, 50% dividend payout, and maintaining current capital adequacy, India Shelter could grow at 20-22% annually without raising capital. Faster growth required either higher ROE (through operational leverage or risk-taking), lower dividends (disappointing investors), or capital raising (diluting returns). This trilemma would shape strategic choices.

ESG integration wasn't optional anymore. Institutional investors increasingly demanded environmental and social impact metrics alongside financial returns. India Shelter's model inherently promoted social good—enabling homeownership for underserved populations. But measuring and communicating this impact required investment in systems and reporting. Green housing finance, supporting environmentally sustainable construction, could differentiate while accessing cheaper international funding.

The competitive response to India Shelter's success was inevitable and already visible. Banks were creating affordable housing verticals. Fintechs were raising venture capital to disrupt the sector. Regional players were consolidating to achieve scale. India Shelter's moat—operational excellence in informal sector assessment—remained defensible but required continuous investment to maintain.

Looking at the five-year horizon, the path seemed clear if challenging. Grow AUM to ₹15,000-20,000 crore through geographic and product expansion. Improve ROE to 18-20% through operational leverage and technology. Maintain asset quality through cycle-tested risk management. Build digital capabilities while preserving high-touch strengths. Create institutional resilience beyond founder dependence.

The ten-year vision was more transformative. India Shelter could become the financial supermarket for India's informal economy—providing not just housing finance but comprehensive financial services to 500,000+ families. Technology would enable mass customization, offering personalized products at scale. The company could pioneer new asset classes—rental housing finance, senior living loans, sustainable housing products—that didn't exist today.

But execution would determine outcomes. Many companies had similar visions; few achieved them. India Shelter's advantages—first-mover position, operational excellence, patient capital, and experienced management—provided a head start. But in India's dynamic economy, advantages eroded quickly without continuous innovation. The next chapter would test whether India Shelter could evolve from a successful regional player to a national champion of financial inclusion, fulfilling its promise of democratizing homeownership while creating sustainable shareholder value.

XII. Lessons & Takeaways

The conference room at IIM Ahmedabad was packed with MBA students, entrepreneurs, and finance professionals. Anil Mehta had been invited to deliver the keynote on "Building Financial Services for Bharat." His opening slide showed two images: a glass-fronted bank branch in Mumbai's Bandra-Kurla Complex and a India Shelter branch in a Jodhpur market, sandwiched between a sari shop and a mobile repair store. "The distance between these images," he said, "is not just geographic. It's the gap between India and Bharat, between the served and underserved, between assumption and reality."

Building in underserved markets requires fundamentally different thinking. India Shelter's journey demonstrated that traditional financial metrics—credit scores, salary slips, IT returns—were luxuries in informal economies. Success came from developing alternative assessment methods that captured economic reality rather than documentary evidence. The lesson extended beyond financial services: serving underserved markets meant questioning every assumption inherited from developed market models.

The importance of patient capital cannot be overstated. India Shelter's transformation from struggling Satyaprakash to public market success took 13 years from relaunch. Early investors like Sequoia and WestBridge committed for the long haul, understanding that building distribution, training staff, and developing risk models required time. The pressure for quick returns that destroyed many financial services companies was notably absent. This patience wasn't philanthropy—it was recognition that sustainable competitive advantages took time to build.

Balancing growth and asset quality emerged as the critical discipline. Every housing finance company that failed had one thing in common: they prioritized growth over quality during good times, only to pay the price during downturns. India Shelter's steady 25-30% growth might have seemed pedestrian compared to fintech unicorns, but it came with sub-2% NPAs. The company proved that in financial services, boring consistency beat exciting volatility.

Creating distribution moats in financial services required more than branch networks. India Shelter's moat came from thousands of micro-relationships—the loan officer who knew every shopkeeper in his territory, the branch manager who attended local weddings, the collection agent who understood seasonal income patterns. These relationships couldn't be replicated by technology or capital alone. They required time, trust, and cultural embedding that created switching costs beyond economics.

The India playbook for financial inclusion had unique characteristics. Unlike developed markets where financial inclusion meant bringing the poor into existing systems, India required building new systems for the majority. This wasn't about charity or corporate social responsibility—it was about recognizing that 93% of India's workforce operated informally, representing a massive commercial opportunity for those willing to develop appropriate models.

Technology as enabler, not replacement proved crucial. While pure-digital evangelists promised to revolutionize financial inclusion through apps and algorithms, India Shelter demonstrated that technology worked best when augmenting human capabilities rather than replacing them. The iServe app didn't eliminate loan officers; it made them more productive. Data analytics didn't replace field assessment; it made it more consistent. This hybrid model—neither fully digital nor entirely physical—represented practical innovation.

The power of focus versus diversification created strategic tension. India Shelter resisted temptations to become a full-service NBFC, to enter corporate lending, or to pursue high-ticket housing loans. This focus on affordable housing for informal sector customers enabled deep expertise, operational excellence, and brand recognition that generalists couldn't match. Yet pure focus risked concentration—geographic, sectoral, and customer segment. The balance between focus for excellence and diversification for resilience required constant calibration.

Organizational culture as competitive advantage seemed soft but proved hard. India Shelter's culture—customer-centric, execution-focused, ethically grounded—wasn't created through mission statements but through thousands of daily decisions. Promoting field officers to branch managers created role models. Celebrating collection officers alongside sales teams balanced priorities. Maintaining simple offices even after the IPO signaled values. In financial services, where products were commodities and regulations were uniform, culture became the ultimate differentiator.

The importance of regulatory navigation extended beyond compliance. India Shelter worked with regulators rather than around them, often exceeding requirements to build credibility. This approach paid dividends—during COVID-19, when regulatory forbearance was essential, companies with strong compliance track records received more flexibility. The lesson: in highly regulated industries, regulatory capital was as important as financial capital.

What this means for investors requires nuanced understanding. India Shelter traded at premium valuations not because it was a technology company or had network effects, but because it had solved a hard problem—profitably serving customers that others couldn't. For fundamental investors, the lesson was clear: sustainable competitive advantages could come from operational excellence in difficult markets, not just technological innovation or scale economies.

For entrepreneurs, India Shelter demonstrated that massive opportunities existed in solving real problems for underserved segments. But success required patient capital, deep market understanding, and willingness to build physical infrastructure even in digital ages. The glamour of B2B SaaS or consumer tech shouldn't obscure opportunities in essential services for the masses.

The role of founders versus institutions evolved through India Shelter's journey. Anil Mehta's vision and relationships were crucial in early stages, but building institutional capabilities—systems, processes, governance—enabled scaling beyond founder limitations. The transition from founder-dependent to institution-driven wasn't binary but gradual, requiring founders secure enough to build organizations larger than themselves.

Risk management as value creation, not value protection, marked sophisticated financial services companies. India Shelter's risk management didn't just prevent losses; it enabled growth into segments others feared. By understanding and pricing risks appropriately, the company could serve customers profitably where others saw only danger. This reframing—risk management as enabler rather than constraint—was crucial for financial inclusion.

The importance of timing and market readiness couldn't be ignored. India Shelter's model might have failed in 1998 or succeeded faster in 2018. The convergence of factors—government focus on affordable housing, digital infrastructure for operations, institutional capital seeking inclusion themes—created conditions for success. Entrepreneurs needed to assess not just whether their solution worked but whether the market was ready.

Building ecosystems versus companies represented evolved thinking. India Shelter didn't just lend money; it educated customers about property documentation, connected them with developers, and helped navigate government schemes. This ecosystem approach created value beyond transactions, building relationships that transcended economic exchange. In markets with trust deficits, companies that built ecosystems created sustainable advantages.

Looking forward, India Shelter's lessons suggested principles for building in emerging markets: Start with deep customer understanding rather than product innovation. Build physical infrastructure even in digital ages when customer segments demand it. Seek patient capital aligned with long-term value creation. Focus on operational excellence in chosen segments rather than pursuing every opportunity. Create cultures that balance growth with sustainability. Navigate regulations proactively rather than reactively. And most importantly, recognize that financial inclusion wasn't just social good but sound business when executed properly.

The ultimate lesson from India Shelter's journey was both simple and profound: in a country where hundreds of millions remained excluded from formal financial systems, the greatest opportunities lay not in serving the wealthy better but in serving the masses at all. This required different models, metrics, and mindsets than those taught in business schools or practiced in corporate boardrooms. But for those willing to challenge orthodoxy, build patiently, and execute relentlessly, the rewards—both financial and social—were transformational. India Shelter proved that democratizing access to capital wasn't just possible; it was profitable. And in that proof lay hope for financial inclusion not just in India but across emerging markets worldwide.

XIII. Recent News

Latest Quarterly Results

India Shelter Finance Corporation delivered exceptional performance in Q4FY25, with profit after tax growing 38% YoY to ₹108 crore. Return on Assets improved to 5.8% while Return on Equity reached 16.3%. These metrics demonstrated the company's ability to maintain profitability even as it scaled aggressively.

During a recent quarter, the company witnessed strong AUM growth of 37% YoY, driven by a 23% YoY increase in disbursements. Margins remained stable at 6.1%, in line with medium-term guidance. Return ratios stayed healthy at 5.6% RoA and 14.3% RoE.