Sarda Energy & Minerals: From Raipur Steel to Integrated Energy Powerhouse

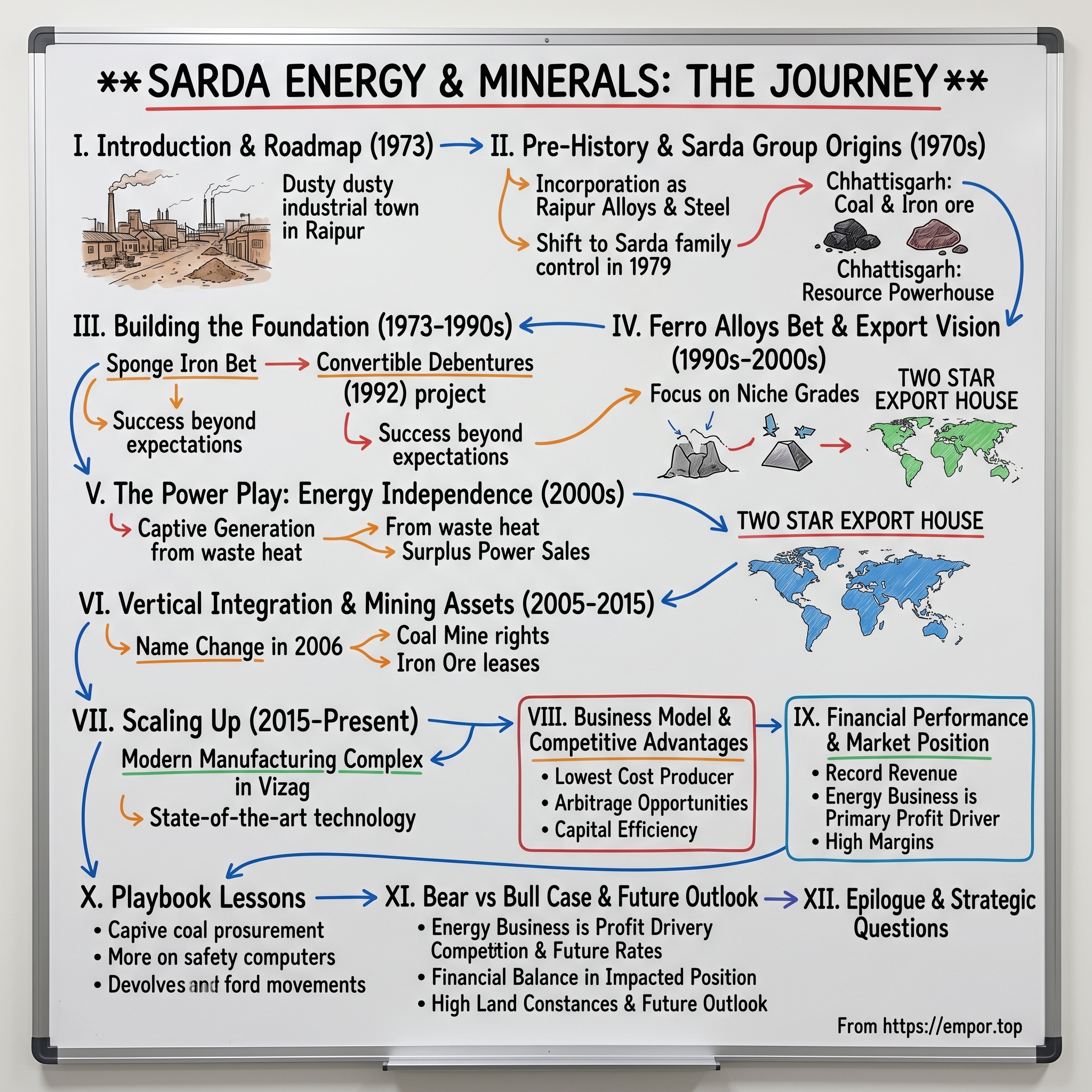

I. Introduction & Episode Roadmap

Picture this: It's 1973 in Raipur, a dusty industrial town in what was then Madhya Pradesh. The License Raj is in full swing, India's steel shortage is chronic, and a group of entrepreneurs see opportunity where others see only red tape and infrastructure gaps. They're about to build what will become Sarda Energy & Minerals—not in Mumbai or Delhi, but in the mineral-rich heartland that most industrialists overlooked.

Fast forward to 2024: Sarda Energy & Minerals Limited commands a ₹19,760 crore market capitalization, generates ₹5,350 crore in revenue, and delivers ₹941 crore in profit. It's a vertically integrated powerhouse spanning steel, ferro alloys, power generation, and mining—all built from that original Raipur base. The stock has surged 99% in the past year alone, hitting all-time highs of ₹607.75 in August 2025.

But here's what makes this story compelling for students of business strategy: Sarda didn't follow the playbook of India's steel giants. While Tata Steel and SAIL were building massive integrated plants with government backing, Sarda quietly assembled a different kind of machine—one optimized for capital efficiency, energy independence, and export competitiveness from India's second-tier cities.

The central question we're exploring isn't just how a small Chhattisgarh steel company became an integrated conglomerate. It's about understanding a uniquely Indian model of industrial development—one that thrives on vertical integration, self-sufficiency, and the arbitrage opportunities that exist between India's resource-rich hinterlands and its infrastructure-poor reality. This is a story about building backwards from the market, integrating upstream when others were content to trade, and finding competitive advantage in geography that others dismissed.

Three themes will guide our journey through Sarda's evolution. First, the power of radical vertical integration in emerging markets where supply chains are unreliable. Second, how energy independence became the secret weapon for manufacturing competitiveness in power-deficit regions. And third, the delicate balance between serving volatile domestic markets and building a global export franchise from an unlikely base.

As we'll discover, Sarda's path offers a masterclass in patient capital allocation, family business governance in public markets, and the art of building industrial empires far from India's commercial capitals. It's a blueprint that challenges conventional wisdom about where and how to build manufacturing excellence—and why sometimes the best opportunities lie where others aren't looking.

II. Pre-History & The Sarda Group Origins

The year is 1976. Emergency has just been declared across India. Industrial licenses are gold dust. And in this environment of extreme government control, a company called Raipur Alloys & Steel Limited gets incorporated—not by the Sarda family, but by an entity called the Tejpaul Group. This detail matters because it reveals something fundamental about Indian business in the 1970s: even starting a steel company required navigating a maze of permissions, partnerships, and political economy that would be unrecognizable today.

The Tejpaul Group's tenure was brief—a mere three years. By 1979, control shifted to what would become the Sarda Group, led by entrepreneurs who understood something others missed: Chhattisgarh (then part of Madhya Pradesh) wasn't a backwater—it was India's future resource powerhouse. The region held 17% of India's coal reserves, vast iron ore deposits, and crucially, it was far enough from established industrial centers that land was cheap and labor available.

The founding vision, as articulated in early company documents, was deceptively simple: "fine-tune the edges of industry dynamics" through cost-efficient products. But unpacking this corporate speak reveals sophisticated thinking. The Sarda founders weren't trying to compete with SAIL or Tata Steel on scale. They were identifying specific market inefficiencies—grades of steel that were imported, ferro alloys that commanded premiums, sponge iron that downstream processors needed—and building targeted capacity to serve these niches.

Consider the context of post-independence India that shaped this strategy. The License Raj didn't just restrict who could produce what; it created massive distortions in supply and demand. Steel was perpetually short. Imports were restricted to conserve foreign exchange. Quality specifications for infrastructure projects were rising, but domestic capacity in specialized grades lagged. Every one of these distortions represented an arbitrage opportunity for those willing to navigate the bureaucracy.

The choice of Chhattisgarh as a base wasn't romantic—it was ruthlessly practical. While the Birlas and Tatas were concentrated in Bihar's coal belt or near port cities, Chhattisgarh offered a different value proposition. Raw materials were literally at the doorstep. The state government, eager for industrial development, was more accommodating than established industrial states. Labor costs were a fraction of those in Mumbai or Kolkata. And perhaps most importantly, being far from India's industrial centers meant less competition for resources and attention.

The Sarda Group's approach to ownership and governance also departed from typical Indian business houses of the era. Rather than creating a web of cross-holdings and pyramid structures, they maintained clean, concentrated ownership. This would prove crucial decades later when accessing capital markets—investors could understand exactly what they were buying.

By the early 1980s, the foundations were set. The company had its licenses, its land, and its strategic vision. But what came next would test whether provincial entrepreneurs could really build something substantial from India's heartland. The answer would reshape not just Sarda, but offer a template for industrial development that dozens of companies would later follow.

III. Building the Foundation: Steel & Sponge Iron (1973–1990s)

The first major strategic move came in 1985 with a name change from Raipur Alloys & Steel Ltd to Raipur Alloys Steel—dropping the "Limited" might seem trivial, but it signaled something important about the company's ambitions. This wasn't going to remain a small, limited operation. The vision was already expanding beyond the initial boundaries.

But the real transformation began with a bet on sponge iron—a product most Indians had never heard of, yet one that would become the cornerstone of Sarda's integrated strategy. Sponge iron, or direct reduced iron (DRI), is iron ore that's been reduced to metallic iron without melting. It's the crucial intermediate product between raw ore and finished steel. And in the 1980s, India was desperately short of it.

The economics were compelling. Blast furnaces—the traditional route from ore to steel—required massive capital investment, coking coal (which India imports), and scale that only government-backed enterprises could afford. But sponge iron could be produced in smaller, modular plants using non-coking coal (which Chhattisgarh had in abundance). For a company Sarda's size, it was the perfect entry point into steelmaking.

In 1992, the company issued convertible debentures to finance its sponge iron project—a surprisingly sophisticated financial instrument for a Raipur-based company. This wasn't just about raising capital; it was about bringing in investors who understood the long-term value of backward integration. The debentures offered investors a hedge: debt-like returns if the project struggled, equity upside if it succeeded.

The project succeeded beyond expectations. By the mid-1990s, Sarda wasn't just producing sponge iron for captive consumption—it was selling to other steel producers who lacked their own DRI capacity. This created an interesting dynamic: Sarda was simultaneously a supplier to and competitor with larger steel companies. It could arbitrage between selling intermediate products when prices were high and converting to finished steel when vertical integration offered better margins.

Building in resource-rich but infrastructure-poor regions brought unique challenges that shaped the company's DNA. Power was unreliable—the state electricity board could barely meet demand, and industrial consumers faced frequent load-shedding. Roads were terrible—transporting finished products to markets or ports required careful logistics planning. Skilled workers were scarce—the company had to invest heavily in training local talent.

Each of these constraints forced innovation. Unreliable power led to early investments in captive generation. Poor roads meant optimizing product mix for value-to-weight ratios. Lack of skilled workers created a culture of long-term employment and internal development that would become a competitive advantage.

The backward integration into sponge iron also revealed something crucial about Indian steel economics that many missed. The government's steel pricing policies created artificial floors and ceilings, but intermediate products like sponge iron traded more freely. By controlling its own sponge iron production, Sarda could capture margins that integrated producers like SAIL often left on the table due to internal transfer pricing policies.

By the late 1990s, the foundation was complete. The company had established itself as a reliable producer of sponge iron and basic steel products. It had demonstrated that profitable steel production was possible outside India's traditional industrial centers. Most importantly, it had validated the core thesis: vertical integration in Indian commodities wasn't just about cost control—it was about creating optionality in volatile markets.

The stage was set for the next phase of expansion, one that would take Sarda from a regional steel producer to an international player in specialized alloys.

IV. The Ferro Alloys Bet & Export Vision (1990s–2000s)

The pivot to ferro alloys manufacturing in the 1990s wasn't obvious. Most Indian steel companies were focused on tonnage—producing more basic steel for India's infrastructure boom. But Sarda's leadership saw a different opportunity: the global market for specialized ferro alloys was fragmented, quality-sensitive, and paid premiums for reliability. It was a market where a company from Raipur could compete with producers from South Africa or Brazil—if they got the economics and execution right.

Ferro alloys are the vitamins of steelmaking—small additions that dramatically change steel properties. Manganese alloys improve strength and workability. Chrome alloys provide corrosion resistance. Silicon alloys enhance magnetic properties. Global steel producers need these specialty ingredients, but most lack the expertise or scale to produce them efficiently. This created a global trading market worth billions, dominated by a handful of specialized producers.

Sarda's entry started with manganese-based ferro alloys, leveraging India's manganese ore reserves and the company's existing infrastructure. But what distinguished their approach was the focus on niche grades rather than commodity products. While competitors chased volume in standard ferro manganese, Sarda invested in producing refined grades with specific chemistry that commanded 20-30% premiums.

The export strategy that emerged was remarkably sophisticated for a company still based in Chhattisgarh. By the early 2000s, Sarda was shipping to 60 countries—from specialty steel producers in Japan to tool manufacturers in Germany. Each market had different specifications, payment terms, and logistics requirements. Managing this complexity from Raipur required building capabilities that many Mumbai-based companies lacked.

The achievement of TWO STAR EXPORT HOUSE status from India's Ministry of Commerce in this period wasn't just a certificate—it came with tangible benefits including priority credit access, simplified customs procedures, and most importantly, credibility with international buyers who were initially skeptical of an unknown Indian supplier.

The strategic positioning in niche grades versus commodity play reveals sophisticated thinking about competitive advantage. Commodity ferro alloys compete on cost—a game where scale always wins. But specialized grades compete on consistency, chemistry precision, and supply reliability. Sarda could never match the scale of Chinese producers in commodity grades, but they could deliver exact specifications, on time, with metallurgical support—services that commanded premium pricing.

Building a reputation as supplier of choice internationally required overcoming significant trust barriers. European and Japanese buyers had established relationships with South African and Brazilian suppliers. Why risk switching to an unknown Indian company? Sarda's answer was systematic: ISO certifications, regular customer visits to Raipur facilities, metallurgical testing labs that matched international standards, and crucially, a willingness to customize products for specific applications.

The company also pioneered an interesting commercial innovation: back-to-back contracts linking raw material costs to finished product pricing. This reduced currency and commodity risk for both Sarda and its customers, making long-term supply agreements more attractive. In volatile commodity markets, this risk-sharing approach differentiated Sarda from traders who simply tried to maximize spot margins.

By 2005, ferro alloys exports had transformed Sarda's financial profile. Foreign exchange earnings provided natural hedging for imported equipment and technology. International customers demanded quality standards that improved domestic operations. Most importantly, the export franchise provided revenue diversification—when Indian steel markets slumped, international demand often remained robust.

The ferro alloys bet validated a crucial insight: in globalized commodity markets, location disadvantages could be overcome through specialization and service. Raipur might be far from ports, but if you're shipping high-value ferro alloys where transport costs are a small percentage of product value, geography matters less than chemistry.

This international success would prove crucial for the next phase of Sarda's evolution—one that would require massive capital investment and technological sophistication.

V. The Power Play: Captive Generation & Energy Independence (2000s)

If steel was Sarda's foundation and ferro alloys its differentiation, power generation would become its secret weapon. The vision for complete energy self-sufficiency that emerged in the early 2000s wasn't just about cost control—it was about recognizing that in India's power-deficit economy, reliable electricity was the ultimate competitive advantage.

The numbers told the story. Chhattisgarh in the 2000s faced power deficits of 15-20% during peak demand. Industrial consumers faced not just load-shedding but wild tariff variations—electricity costs could swing 30% year-to-year based on state electricity board finances and political decisions. For energy-intensive businesses like steel and ferro alloys, where power represents 20-30% of production costs, this volatility was existential.

Sarda's approach to captive power began with waste heat recovery—using hot gases from sponge iron kilns and ferro alloy furnaces to generate steam for turbines. This wasn't cutting-edge technology globally, but implementing it efficiently in Indian conditions required significant innovation. The 30 MW turbine commissioned in 2008-09, coupled with a 90 TPH FBC (Fluidized Bed Combustion) boiler, represented one of the most efficient waste heat recovery systems in India's steel industry at the time.

The economics of captive power in Indian manufacturing created compelling arbitrage opportunities. State electricity boards charged industrial consumers ₹6-8 per unit while subsidizing agricultural and residential users. But generating your own power from waste heat cost ₹2-3 per unit. Coal-based captive generation cost ₹3-4 per unit. Every megawatt of captive capacity translated directly to competitive advantage.

But Sarda didn't stop at thermal power. The entry into renewable energy through solar and hydro projects via Special Purpose Vehicles (SPVs) showed strategic foresight that wouldn't fully pay off for another decade. In 2009, when solar power cost ₹15+ per unit, investing in renewable energy seemed irrational. But Sarda's leadership understood something crucial: energy independence wasn't just about current economics but future optionality.

The hydro projects in particular revealed sophisticated thinking about resource utilization. Chhattisgarh's seasonal rivers were considered unsuitable for large hydro projects, but perfect for small run-of-river systems that could provide baseload power during monsoons when coal-based generation became expensive due to transportation challenges. By combining thermal, waste heat, solar, and hydro, Sarda created an internal power portfolio that could optimize across seasons, fuel costs, and regulatory regimes.

The regulatory landscape around captive power generation also created interesting opportunities. The Electricity Act of 2003 allowed captive generators to sell surplus power to the grid or directly to other consumers through open access. Sarda structured its power investments to maintain captive status (requiring 51% self-consumption) while maximizing third-party sales during high-tariff periods. This regulatory arbitrage added another layer of returns to power investments.

Technology partnerships became crucial as power generation grew more sophisticated. Collaborations with companies like Siemens for turbine optimization and Doosan Babcock for boiler efficiency brought global best practices to Raipur. These weren't just vendor relationships but knowledge transfers that upgraded Sarda's technical capabilities across all operations.

The transformation into an energy-independent manufacturer had second-order effects that weren't immediately obvious. Reliable power meant production planning could ignore grid constraints. Surplus power generation created a new profit center with different cyclicality than steel markets. Most importantly, energy assets provided collateral for funding future expansion—banks understood and valued power plants even when they struggled to evaluate ferro alloy market dynamics.

By 2010, Sarda had achieved something remarkable: complete energy independence with surplus generation capacity. In a country where industrial consumers regularly curtailed production due to power shortages, Sarda could run full capacity year-round while selling excess power at premium rates during deficit periods.

This energy independence would prove crucial for the next phase of vertical integration—one that would take Sarda all the way back to the mines.

VI. Vertical Integration & Mining Assets (2005–2015)

The name change in 2006 from Raipur Alloys Steel to Sarda Energy & Minerals Limited wasn't just rebranding—it was a declaration of intent. The company was no longer just a steel producer with some power assets. It was positioning itself as an integrated player across the entire value chain from mining to finished products. This transformation would require navigating India's complex mining regulations, joint venture politics, and the delicate balance between resource security and capital efficiency.

The 2007 merger with Chhattisgarh Electricity Company Limited was the opening move in this broader strategy. CECL brought not just additional power generation capacity but more importantly, coal linkages and mining leases that were becoming increasingly valuable as India's coal allocation policies tightened. In one stroke, Sarda acquired assets that would have been impossible to develop organically given the regulatory environment.

But the real coup came with the Madanpur South Coal Company joint venture. Securing rights to 36 million tonnes of coal reserves sounds straightforward in hindsight, but the execution required navigating a maze of stakeholders. The mine was allocated through a government process that prioritized end-users over traders. Sarda had to demonstrate not just financial capacity but technical capability to develop and operate the mine efficiently. The JV structure—with other industrial consumers—spread risk while ensuring coal security for decades.

The economics of captive mining in India created massive value that public markets initially underappreciated. Imported coal cost $100-150 per tonne delivered to plant. Domestic coal from Coal India cost ₹2,000-4,000 per tonne depending on grade and transportation. But captive coal cost only ₹800-1,200 per tonne including mining and logistics. For a company consuming millions of tonnes annually, this differential was transformative.

Iron ore mining leases acquired during this period followed a different logic. Unlike coal, where the goal was cost reduction, iron ore mining was about quality control. Sarda's pellet and sponge iron operations required consistent Fe content and specific gangue chemistry. Captive mines ensured this consistency while also providing optionality—selling ore externally when prices spiked or converting to pellets when integration offered better margins.

The international expansion through Singapore and Hong Kong subsidiaries might seem incongruous for a Chhattisgarh-based company, but it served specific strategic purposes. These entities facilitated equipment imports, managed foreign exchange hedging, and most importantly, provided platforms for international coal sourcing. The Indonesian coal interests acquired through these vehicles gave Sarda access to high-calorific value coal that complemented domestic supplies for specific applications.

The regulatory environment during this period was increasingly challenging. The "Coalgate" scandal of 2012 led to cancellation of many coal block allocations. Environmental clearances became more stringent. Mining leases faced public interest litigation. Sarda navigated these challenges through a combination of regulatory compliance, community engagement, and strategic patience—maintaining clean records that survived scrutiny when many peers faced cancellations.

Technology adoption in mining operations distinguished Sarda from traditional Indian miners. GPS-based fleet management, real-time grade control systems, and automated loading infrastructure might be standard globally, but were revolutionary in Indian mining contexts. These investments improved recovery rates by 15-20% while reducing environmental impact—crucial for maintaining social license to operate.

The vertical integration achieved by 2015 was remarkable in scope. From coal and iron ore mines through power generation and steel production to specialized ferro alloys, Sarda controlled its entire value chain. This integration provided multiple benefits: cost advantages from eliminating middleman margins, quality control from mine to market, operational flexibility to optimize across the value chain based on market conditions, and importantly, reduced working capital requirements as internal transfers replaced market transactions.

But perhaps the most valuable outcome was strategic optionality. When ferro alloy prices crashed, Sarda could focus on steel. When steel margins compressed, power sales provided cushion. When power tariffs declined, low-cost coal from captive mines maintained profitability. This portfolio effect—different businesses with different cycles—provided resilience that pure-play competitors lacked.

The transformation from steel producer to integrated energy and minerals company was complete. But the next phase would test whether this integrated platform could support ambitious capacity expansion and technological upgrading.

VII. Scaling Up: The Modern Manufacturing Complex (2015–Present)

The scale of modern manufacturing that Sarda has achieved by 2024 would have seemed fantastical to its founders in 1973. The numbers tell only part of the story: 9 lakh MT pellet capacity, 3.6 lakh MT sponge iron, 3 lakh MT billets, 2.5 lakh MT wire rod, and 0.45 lakh MT H.B. wire. What these capacities represent is a fully integrated steel complex that can take iron ore from mine to finished wire products—all within a single corporate structure.

But the crown jewel of Sarda's modern expansion is the Vishakhapatnam complex, developed through its wholly-owned subsidiary Sarda Metals & Alloys Limited (SMAL). Set up as a greenfield state-of-the-art complex near Vishakhapatnam in 2013-14 with 1 X 80 MW Captive Power Plant and 3 X 36 MVA Ferro Alloys Submerged Arc Furnaces, this facility represents a strategic departure from Sarda's traditional Chhattisgarh base.

The Vizag location wasn't chosen randomly. The plant is strategically located just 40-45 KM from Vishakhapatnam & Gangavaram Ports and only 2 Kms from Kantakapalli Railway siding on Chennai-Kolkata main line. For a company that had built its empire in landlocked Chhattisgarh, establishing a coastal manufacturing base opened new possibilities—direct access to export markets, easier import of specific raw materials, and proximity to southern Indian customers.

The technology partnerships for Vizag reveal Sarda's ambition to build world-class facilities. SMAL has partnered with state-of-the-art technology providers such as Tenova Pyromet, Tamini, SGL Carbon, RHI for the construction of its 36 MVA furnaces. For its Captive Power Plant it has partnered with Siemens, Germany for Turbine & Generator and with Doosan Babcock, South Korea. These weren't just vendor relationships but technology transfers that brought global best practices to Indian ferro alloy production.

The expansion trajectory shows remarkable consistency. In May 2021, the Board of Sarda Metals & Alloys approved expansion project of Ferro Alloys by adding one more furnace of 36 MVA (with capacity addition of 50,000 MT p.a.) with an estimated capex of Rs. 135 crore. By December 2022, the third ferro alloys furnace was commissioned and started production. This disciplined capacity addition—one furnace at a time, ensuring each is operational before starting the next—reflects capital allocation wisdom rare in Indian manufacturing.

The eco-friendly initiatives deserve special mention. Converting fly-ash from captive power plants into eco-bricks isn't just environmental compliance—it's turning waste into revenue. When you generate 80+ MW of coal-based power, fly-ash disposal becomes a major challenge. By converting this to construction materials, Sarda solved an environmental problem while creating a new profit center.

Quality certifications accumulated during this period tell their own story. ISO 9001, ISO 14001, ISO 45001, and ISO 50001 certifications reflect the company's commitment to quality, environmental management, occupational health and safety, and energy management, with products meeting international quality benchmarks through NABL-accredited lab and BIS certification. More importantly, Sarda has been recognized with a 3 Star Export House status by the Ministry of Commerce, Government of India—an upgrade from its earlier Two Star status.

The implementation of Total Productive Maintenance (TPM) with aims to achieve the Japan Institute of Plant Maintenance (JIPM) Award shows ambitions beyond mere capacity expansion. This is about building manufacturing excellence that can compete globally, not just in commodity products but in operational efficiency and quality consistency.

Recent expansion approvals suggest the scaling up is far from over. In September 2024, the company secured Chhattisgarh Environment Conservation Board nod to expand coal production from 1.44 MTPA to 1.68 MTPA. This seemingly modest 17% increase in coal mining capacity has outsized importance—it ensures raw material security for expanded steel and power operations while maintaining cost advantages.

The geographic diversification achieved through this expansion phase is strategically important. Raipur remains the integrated steel hub with backward integration to mines. Vizag has become the ferro alloy and export hub with port proximity. This dual-center model provides operational flexibility—if regulatory or market conditions challenge one location, the other can compensate.

The financial impact of this scaling up has been dramatic. The integrated model now generates economies of scale that smaller competitors cannot match. Fixed costs are spread across larger production volumes. Capacity utilization can be optimized across products based on market conditions. Most importantly, the company has achieved the scale necessary to invest in continuous technological upgrading—a virtuous cycle where scale enables technology investments that further improve competitiveness.

VIII. Business Model & Competitive Advantages

Understanding Sarda's business model requires appreciating a fundamental truth about Indian commodity businesses: in markets where products are largely undifferentiated, the only sustainable advantages are cost, integration, and financial flexibility. Sarda has systematically built all three, creating a business model that thrives on volatility rather than despite it.

The positioning as "one of the lowest cost producers of steel" isn't marketing rhetoric—it's mathematical reality. Consider the cost structure: captive coal reduces energy costs by 60% versus grid power. Captive iron ore eliminates mining company margins. Waste heat recovery generates free power from production processes. Vertical integration eliminates working capital locked in inter-company transactions. Add these up, and Sarda's cost per tonne is structurally lower than non-integrated competitors.

The integrated model spanning mining → power → steel → ferro alloys creates multiple arbitrage opportunities. When ferro alloy prices spike, Sarda can shift furnace capacity from steel to alloys. When steel margins improve, sponge iron can be converted to billets rather than sold externally. When power tariffs rise, surplus generation can be sold to grid rather than used for incremental production. This optionality—the ability to optimize across the value chain based on relative prices—is worth more than any single efficiency improvement.

Capital efficiency metrics reveal disciplined management. With 73.2% promoter holding and dividend payout at just 7.69% of profits over the last 3 years, the company retains most earnings for growth. This is classic owner-operator behavior—prioritizing long-term compounding over short-term distributions. The high promoter stake also aligns management incentives with minority shareholders, reducing agency costs that plague many Indian companies.

Geographic advantages often go unappreciated. Chhattisgarh's mineral wealth isn't just about raw material proximity—it's about being the large fish in a smaller pond. In Mumbai or Kolkata, Sarda would compete with dozens of established players for everything from skilled workers to government attention. In Raipur, they're among the largest employers and taxpayers, commanding priority access to resources and regulatory support. This "home court advantage" translates to faster approvals, better infrastructure support, and preferential treatment in resource allocation.

The export-domestic balance deserves careful analysis. With exports to more than 30-60 countries, Sarda has built natural hedging into its business model. When Indian steel demand weakens, international ferro alloy demand often remains robust. When the rupee depreciates, export realizations improve. When domestic prices are regulated or suppressed, international markets provide outlets. This geographic diversification of revenue reduces cyclical volatility.

Management philosophy, while harder to quantify, shapes every strategic decision. The focus on "fine-tuning the edges of industry dynamics" rather than revolutionary disruption reflects pragmatic understanding of commodity businesses. You don't win by inventing new products—you win by producing existing products more efficiently. This philosophy drives continuous incremental improvements rather than bet-the-company transformations.

The capital allocation track record speaks volumes. Every major investment—from backward integration into mining to forward integration into wire products—has been self-funded through internal accruals. No dilutive equity raises. No aggressive leverage. Just patient reinvestment of earnings into adjacent opportunities. This conservative financing approach means Sarda has never been forced to sell assets or dilute shareholders during downturns.

Working capital management, though showing some stress with days increasing from 78.1 to 119 days, reflects strategic choices rather than operational weakness. Holding higher raw material inventory when prices are low, extending credit to capture export orders, and maintaining finished goods stock for quick delivery—these decisions trade working capital efficiency for commercial advantage.

The competitive moat isn't any single factor but the combination of multiple reinforcing advantages. Integrated operations create cost advantages. Cost advantages enable pricing flexibility. Pricing flexibility wins market share. Market share justifies capacity expansion. Capacity expansion improves economies of scale. It's a flywheel that becomes stronger with each rotation.

What's often missed is how these advantages compound over time. A 10% cost advantage might seem modest, but when reinvested over decades, it creates an insurmountable lead. Sarda's 50-year journey from a small Raipur steel unit to an integrated conglomerate demonstrates this compounding in action.

IX. Financial Performance & Market Position

The financial performance numbers for 2024 tell a story of transformation. Q1 FY26 record revenue INR1633 Cr, profit INR435 Cr, representing a 76% YoY increase in revenue. But the headline numbers only hint at the structural shift happening beneath the surface.

The energy segment now contributes 47% of the company's consolidated revenue and a staggering 67% of EBITDA, delivering ₹800 crores in revenue and ₹467 crores in EBITDA in Q1. This isn't the same company that was primarily a steel producer even five years ago. The energy business—once built for captive consumption—has become the primary profit driver.

The EBITDA performance deserves special attention. EBITDA for the quarter more than doubled YoY to Rs 697 crore, marking a robust 108% increase from Rs 336 crore in Q1FY25. On a sequential basis, EBITDA surged 120% from Rs 317 crore in the previous quarter. More importantly, the company's EBITDA margin expanded to 38%, reflecting operational efficiency and improved realizations. For a commodity business, 38% EBITDA margins are exceptional—typically seen only during super-cycles or in highly differentiated products.

The valuation metrics present an interesting puzzle. With a P/E ranging from 21.3-27.77 and Book Value at ₹178, the market is pricing Sarda closer to a growth company than a commodity producer. The stock performance validates this optimism—99.17% increase over the last year with an all-time high of ₹607.75 in August 2025. But is this justified?

Comparing with peers provides context. JSW Steel trades at similar multiples but with lower margins. Tata Steel commands premium valuations based on brand and scale. SAIL, despite government backing, trades at discounts due to operational inefficiencies. Sarda sits in an interesting middle ground—the operational efficiency of private sector, the integration advantages of larger players, but the agility of a mid-cap.

Cash profit, a key indicator of a company's internal accrual strength, leapt 161% YoY to Rs 642 crore and 154% QoQ. This cash generation ability explains how Sarda funds expansion without dilution or excessive leverage. In capital-intensive industries, the ability to self-fund growth is a massive competitive advantage.

Working capital management shows both strength and stress. The increase from 78.1 to 119 days reflects strategic inventory building and extended credit terms to capture market share. In commodity businesses, working capital often expands during growth phases as companies build inventory during price troughs and extend credit to win contracts.

The operational metrics reveal impressive execution. Iron ore pellet production rose 9% year-on-year to 230,000 tonnes, with sponge iron and billet output up 4% and 17% respectively. Wire rod production surged 54% to 42,000 tonnes, while ferro alloys and HB wire output grew 9% each. This isn't just capacity addition—it's balanced growth across the product portfolio.

The power generation numbers are particularly impressive. Independent power production saw thermal generation touch 1,182 million units, up 13% QoQ. Captive thermal power generation rose 15% YoY to 355 million units, while hydropower output surged 37% YoY to 120 million units. The diversification across thermal and hydro provides seasonal balance—hydro peaks during monsoons when coal transport becomes challenging.

The market's reaction to these results was swift and decisive. Shares of Sarda Energy & Minerals surged nearly 14% to ₹500.40 on August 4, making it one of the top gainers on the NSE. This wasn't just algorithmic trading—it reflected fundamental revaluation as investors recognized the energy business transformation.

Sarda Energy's standalone net sales for March 2025 reached Rs 1,013.09 crore, up 51.21% YoY. Net profit rose 14.03% to Rs 115.25 crore, while EBITDA increased by 67%. The divergence between revenue growth and profit growth in some periods reflects commodity price volatility, but the long-term trend is clear—rising volumes, improving margins, and accelerating cash generation.

The financial performance isn't just about growth—it's about quality of earnings. The high contribution from the energy segment provides stability. The balanced product mix reduces concentration risk. The strong cash generation funds growth without dilution. And the improving margins suggest operational leverage is kicking in as scale increases.

X. Playbook: Lessons from the Chhattisgarh Model

The Sarda story offers a masterclass in building industrial enterprises in Tier 2/3 India—a playbook that challenges conventional wisdom about location, scale, and strategy. The lessons extend beyond steel and power to any capital-intensive business contemplating where and how to build in emerging markets.

Building in Tier 2/3 India: Challenges and Advantages

The decision to build in Raipur rather than established industrial centers wasn't romantic provincialism—it was calculated arbitrage. Land costs were 70% lower. Labor was available and trainable. State government support was enthusiastic rather than transactional. But most importantly, being the big fish in a smaller pond meant priority access to everything from railway capacity to environmental clearances.

The challenges were real. Skilled engineers had to be convinced to relocate. Equipment vendors needed persuasion to provide service support. Banking relationships required patient cultivation. But each challenge overcome became a competitive moat—competitors would face the same hurdles trying to replicate Sarda's model.

The Power of Backward Integration in Commodities

Sarda's systematic backward integration—from finished steel to sponge iron to pellets to iron ore mining—demonstrates the compound value of controlling your supply chain. Each step backward didn't just reduce costs; it provided optionality. When sponge iron prices spiked, Sarda could sell externally. When they crashed, captive consumption ensured utilization. This optionality has value beyond simple cost savings—it's insurance against supply disruptions and price volatility.

The integration philosophy extended beyond obvious linkages. Captive power wasn't just about energy security—it was about converting waste heat to electricity, turning a disposal problem into a profit center. Coal mining wasn't just about fuel security—it was about capturing the entire value chain from extraction to electron.

Export-Domestic Balance in Volatile Markets

The 60-country export franchise in ferro alloys provides crucial portfolio balance. Domestic markets follow Indian economic cycles. Export markets follow global dynamics. Exchange rates provide natural hedging. This geographic diversification smooths revenue volatility in ways that product diversification alone cannot achieve.

The export capability also enforced discipline. International customers demand consistent quality, reliable delivery, and competitive pricing. Meeting these standards for exports elevated domestic operations. The spillover benefits—from quality systems to logistics capabilities—improved the entire organization.

Family Business Governance in Listed Companies

The 73.2% promoter holding could be seen as limiting float, but it's enabled long-term thinking rare in widely-held companies. No activist investors demanding breakups or special dividends. No quarterly earnings pressure driving short-term decisions. The family's wealth concentration in one company aligns their interests with long-term value creation.

Yet the governance isn't nepotistic. Professional managers run operations. Independent directors provide oversight. Disclosure standards meet listing requirements. The balance—family vision with professional execution—offers lessons for other promoter-driven companies navigating public markets.

Environmental Compliance and Sustainability in Heavy Industry

In an era of increasing environmental scrutiny, Sarda's approach offers a pragmatic template. Rather than seeing compliance as cost, they've turned it into competitive advantage. Fly-ash becomes eco-bricks. Waste heat becomes power. Mining rehabilitation becomes community development. This isn't greenwashing—it's recognizing that sustainable operations are ultimately more profitable operations.

The recent environmental clearances for capacity expansion, when many competitors face closure orders, validates this approach. Regulators are more likely to approve expansion for companies with strong compliance track records. Environmental leadership becomes license to grow.

When to Diversify vs When to Integrate

Sarda's journey reveals crucial timing insights. They integrated backward (into mining and power) when those assets were available and cheap. They integrated forward (into wire products) when market demand emerged. They diversified geographically (Vizag plant) when the Raipur base was stable. Each move built on existing strengths rather than abandoning them.

The discipline to not diversify is equally instructive. Despite opportunities, Sarda hasn't entered unrelated businesses. No real estate ventures. No financial services. No consumer products. The focus remains on the core value chain where their capabilities create competitive advantage.

The Chhattisgarh model ultimately demonstrates that competitive advantage in commodities doesn't require revolutionary technology or massive scale. It requires patient capital allocation, systematic capability building, and relentless focus on controlling what you can control. In markets where most players chase the same opportunities in the same locations, doing something different in somewhere different can be the ultimate differentiation.

XI. Bear vs Bull Case & Future Outlook

Bull Case: The Integrated Advantage in India's Infrastructure Decade

The optimistic view starts with a simple observation: India's steel consumption per capita is still only 75 kg versus China's 650 kg and the global average of 230 kg. Even reaching global average implies tripling of demand. Sarda, with its integrated model and cost advantages, is positioned to capture disproportionate share of this growth.

The integrated model provides structural cost advantages that only strengthen over time. While standalone steel producers face margin pressure from raw material inflation, Sarda's captive mines and power generation insulate it from input cost volatility. The company's cost per tonne is structurally 20-30% below non-integrated peers—a gap that widens during inflationary periods.

India's infrastructure story remains in early innings despite decades of discussion. The government's ₹100 trillion infrastructure pipeline through 2025 isn't just political rhetoric—projects are being tendered, funded, and executed. Each kilometer of highway, railway, and metro requires steel, ferro alloys, and power. Sarda supplies all three.

The strong promoter backing with 73.2% holding ensures patient capital and long-term thinking. Unlike widely-held companies pressured for quarterly performance, Sarda can make decade-long bets on capacity expansion and integration. The execution track record—from successfully commissioning the Vizag plant to ramping up power generation—demonstrates ability to deliver on ambitious plans.

Energy independence in power-deficit regions provides sustainable competitive advantage. While competitors curtail production during power shortages or pay peak tariffs, Sarda runs full capacity with surplus power to sell. This reliability premium becomes more valuable as customers prioritize supply security over marginal price differences.

Bear Case: Structural Headwinds and Concentration Risks

The pessimistic view focuses on structural challenges that no amount of operational excellence can overcome. Commodity cycles are inevitable, and Sarda's current margins reflect cyclical peaks rather than sustainable levels. When China's property crisis fully unfolds and global steel demand corrects, even the most efficient producers will face margin compression.

Environmental regulations are tightening globally and India won't remain an exception indefinitely. Sarda's dependence on coal-based power and carbon-intensive steel production faces existential threat from carbon taxes and emission norms. The capital required to transition to green steel and renewable energy could destroy returns for a decade.

Competition from imports remains a perpetual threat. When global steel prices crash, international producers dump excess capacity in India. Despite government protection through duties, imported steel often remains cheaper than domestic production. Sarda's cost advantages matter less when competing against subsidized Chinese or distressed global capacity.

Geographic concentration in Chhattisgarh creates multiple risks. A single adverse regulatory change, environmental crisis, or political shift could disrupt operations. Unlike diversified players with assets across states and countries, Sarda has most eggs in one geographic basket.

The technology transition to green steel poses particular challenges for smaller players. While Tata Steel and JSW can afford billion-dollar investments in hydrogen-based steel production, mid-sized players like Sarda may lack the scale to justify such investments. Being stuck with obsolete technology while larger players move to green steel could create permanent disadvantage.

Future Outlook: Navigating the Transition

The next decade will test whether Sarda can navigate multiple transitions simultaneously. The shift from coal to renewable energy isn't optional—it's existential. But the company's early investments in solar and hydro, plus the massive cash generation from current operations, provide resources for this transition.

The question of what happens when India's steel demand matures is crucial but perhaps premature. Even optimistic projections suggest India won't reach global average steel consumption until 2040. That's fifteen years of growth runway—enough time to build next generation capabilities while harvesting current investments.

Can regional champions compete with national consolidation? The global steel industry suggests mixed outcomes. While consolidation creates scale advantages, regional players with specific advantages—location, product mix, customer relationships—continue to thrive. Sarda's integrated model and cost position suggest it could be an acquirer rather than target in future consolidation.

The ESG transition challenge for coal-dependent operations is real but manageable. The company's track record of environmental compliance, early renewable investments, and strong cash generation provide tools for transition. The key is timing—moving fast enough to maintain legitimacy but not so fast as to destroy returns.

International expansion remains an option but not necessity. The Singapore and Hong Kong subsidiaries provide platforms for overseas growth if Indian markets saturate. But with domestic demand growth trajectory, international expansion seems more optionality than imperative.

The bear and bull cases aren't mutually exclusive—elements of both will likely materialize. Sarda will face commodity cycles, environmental challenges, and competitive pressures. But its integrated model, execution capability, and financial strength provide tools to navigate these challenges. The question isn't whether challenges will emerge but whether Sarda's advantages are sufficient to overcome them.

XII. Epilogue & Strategic Questions

As we conclude this deep dive into Sarda Energy & Minerals, we're left with strategic questions that extend beyond one company to the future of Indian manufacturing, commodity businesses, and industrial development in emerging markets.

What happens when India's steel demand matures?

History suggests no country maintains high steel consumption growth indefinitely. Japan's steel demand peaked in the 1970s. America's flattened in the 1980s. China's is peaking now. When India reaches this inflection—whether in 2040 or 2050—what happens to companies built for growth? Sarda's answer appears to be value-addition rather than volume. The progression from sponge iron to billets to wire rods to specialty wires shows a path toward higher value products that can grow even when tonnage plateaus.

Can regional champions compete with national consolidation?

The global steel industry has seen waves of consolidation creating giants like ArcelorMittal and China Baowu. Yet regional champions persist—Nucor in America, Salzgitter in Germany, BlueScope in Australia. These survivors share characteristics: operational excellence, local market knowledge, and strategic niches. Sarda exhibits all three, suggesting survival and prosperity are possible even amid consolidation.

The ESG transition challenge for coal-dependent operations

The hardest question facing Sarda—and hundreds of similar companies globally—is how to transition from carbon-intensive operations without destroying shareholder value. The answer isn't simple replacement of coal with renewables; it's systematic transformation of entire production processes. Early moves into hydro and solar provide foundations, but the real transition requires technologies still being developed—hydrogen-based steel production, carbon capture, circular economy models. Sarda's strong cash generation provides resources for this transition, but execution will determine survival.

Lessons for other emerging market manufacturers

The Sarda model offers several transferable lessons. First, building away from commercial centers can create sustainable advantages if you solve the infrastructure and talent challenges. Second, vertical integration in emerging markets provides value beyond cost savings—it's about reliability in unreliable environments. Third, patient capital and concentrated ownership enable long-term thinking that public markets rarely tolerate. Fourth, environmental compliance and community engagement aren't costs but investments in license to operate.

The next decade: green steel, renewable energy, international expansion?

Looking forward, Sarda faces three major strategic choices. The green steel transition isn't optional but its timing and technology choices are. Moving too early risks stranded assets; too late risks obsolescence. The renewable energy expansion must balance captive needs with merchant opportunities. Being 100% renewable sounds appealing but may not be economically optimal. International expansion offers growth beyond India but requires capabilities and capital that might be better deployed domestically.

The deeper question is whether Sarda represents the past or future of Indian industry. Is it the last generation of coal-based, commodity-focused, regionally concentrated companies? Or is it a template for building industrial champions from India's heartland, leveraging local resources and relationships to compete globally?

The answer likely lies in execution over the next decade. If Sarda successfully navigates the energy transition, maintains cost leadership through technology adoption, and continues disciplined capital allocation, it could emerge as a case study in industrial transformation. If it fails to adapt, it becomes a cautionary tale about the limits of operational excellence in structurally challenged industries.

What makes Sarda fascinating isn't just its past achievement in building an integrated empire from provincial beginnings. It's the strategic choices ahead that will determine whether this Chhattisgarh champion becomes a national leader or remains a regional success story. The tools are in place—integrated operations, strong balance sheet, proven execution capability. The question is whether vision and leadership can deploy these tools to navigate an uncertain future.

For investors, Sarda represents a bet on execution in transition. The current valuation assumes successful navigation of multiple challenges while maintaining competitive advantages. Whether this optimism proves justified depends on factors both within and beyond management control—global commodity cycles, environmental regulations, technology evolution, and India's development trajectory.

The story of Sarda Energy & Minerals is far from over. In many ways, the most interesting chapters are just beginning to be written. The transformation from Raipur Alloys to integrated energy and minerals company was impressive. The next transformation—to sustainable, technology-enabled, globally competitive enterprise—will determine whether Sarda becomes a footnote or case study in Indian industrial history.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube