Sandur Manganese & Iron Ores: From Princely Mining to Modern Metals

I. Introduction & Episode Setup

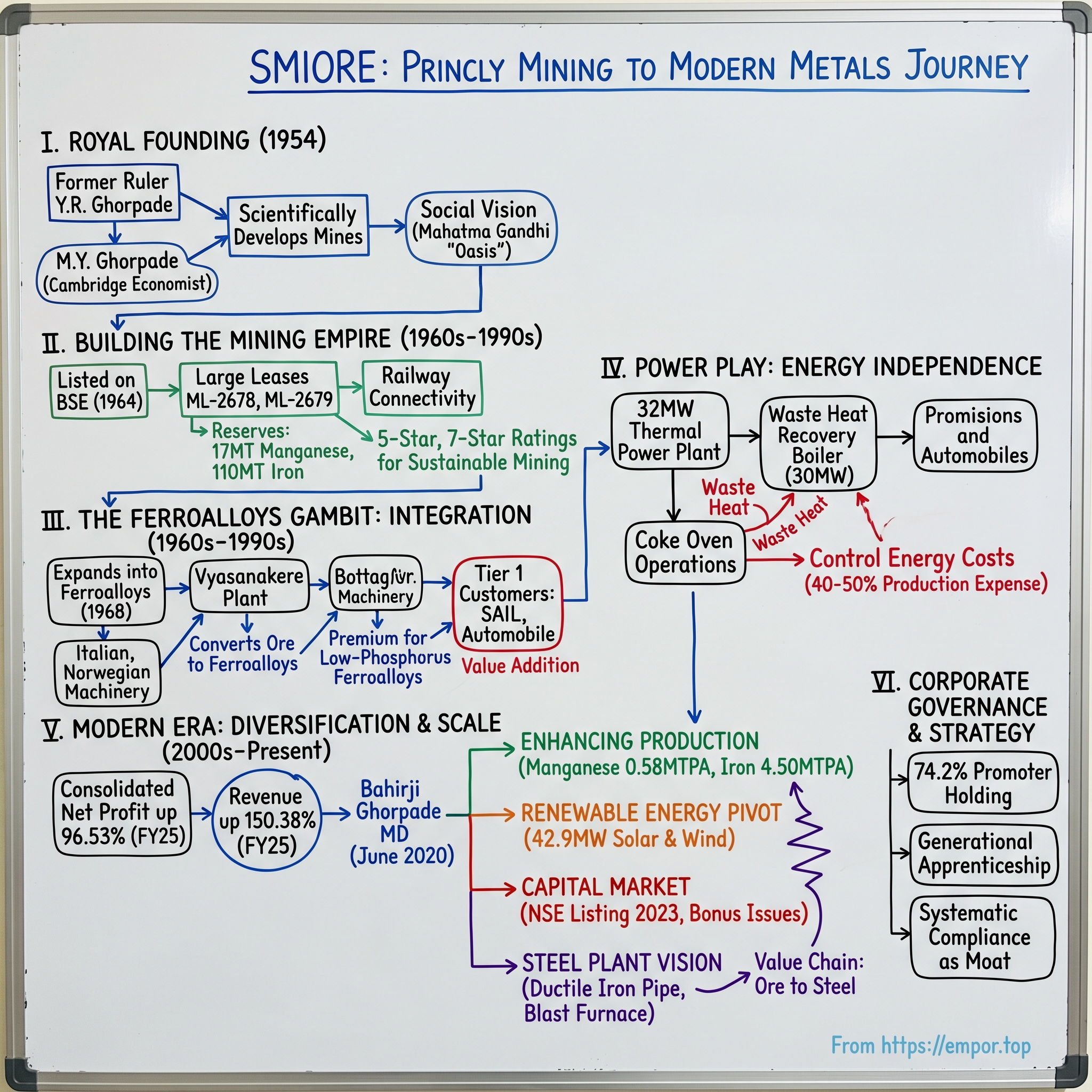

Picture this: In the dusty, iron-rich hills of Karnataka's Bellary district, where the earth bleeds rust-red and manganese veins snake through ancient rock formations, stands a company that embodies India's post-independence industrial dream. The year is 1954. India has been free for just seven years. The princely states—those 565 feudal kingdoms that once covered 40% of the subcontinent—are being absorbed into the new republic. Most maharajas are negotiating privy purses and fading into genteel obscurity. But in the small principality of Sandur, something different is happening.

The former ruler, Yeshwantrao Hindurao Ghorpade, isn't retreating to his palace. Instead, he's founding what would become Sandur Manganese & Iron Ores Limited (SMIORE)—a mining venture that would outlive the princely state system itself and evolve into a ₹7,272 crore metals powerhouse. Today, SMIORE stands as India's third-largest manganese ore producer, a vertically integrated metals company that spans mining, ferroalloys, coke production, and power generation. The puzzle that makes this story fascinating isn't just the transition from royal privilege to corporate success. It's how a small mining operation in one of India's poorest districts transformed into a company that today boasts a market cap of ₹7,272 crore, with full-year net profit rising 96.53% to ₹470.61 crore in FY2025 against ₹239.46 crore in FY2024, while sales rose 150.38% to ₹3,135.06 crore from ₹1,252.13 crore. The company trades at a P/E ratio of 15.45 with a dividend yield of 0.50%.

But numbers tell only part of the story. This is a tale of three generations of the Ghorpade family navigating India's labyrinthine mining regulations, surviving the Karnataka mining scams that destroyed many competitors, and building one of the country's most integrated metals businesses. It's about transforming a commodity extraction business into a sophisticated manufacturing operation with ferroalloys, coke ovens, and captive power generation. And it's about doing all this while maintaining 74.2% promoter holding—a testament to the family's long-term vision and control.

Think of SMIORE as India's answer to the great mining dynasties of the West—except instead of the Rockefellers or Carnegies, you have former royalty who traded their privy purses for pickaxes, their palaces for processing plants. They didn't just dig holes in the ground; they built an entire value chain from ore to alloy, creating what might be India's most vertically integrated manganese business.

The questions we'll explore: How did a princely family succeed where many industrial houses failed? What made manganese—that unglamorous cousin of iron ore—the foundation for a multi-thousand-crore empire? And in an era of ESG concerns and regulatory crackdowns, how does a 70-year-old mining company position itself for the next century?

As we'll see, the answer lies in a unique combination of aristocratic patience, engineering excellence, and an almost obsessive focus on downstream integration. While competitors fought over mining licenses, the Ghorpades were building furnaces. While others exported raw ore, they were making ferroalloys. And while the industry reeled from regulatory upheavals, SMIORE kept expanding—methodically, relentlessly, profitably.

This isn't just a business story. It's a window into how traditional Indian businesses can reinvent themselves, how family enterprises can professionalize without losing their soul, and how a company can thrive in one of the world's most challenging regulatory environments. Welcome to the unlikely empire built on manganese and managed by maharajas.

II. Royal Origins & Founding Story (1954)

The monsoon of 1954 brought more than rain to the dusty plateaus of Sandur. As India's new constitution was still finding its feet and Nehru's five-year plans were reshaping the economic landscape, a remarkable transformation was unfolding in this small corner of Karnataka. The last ruler of Sandur state, Yeshwantrao Hindurao Ghorpade, wasn't lamenting the end of princely privilege. Instead, he was laying the foundation stones—quite literally—for what would become one of India's most enduring mining enterprises. To understand the genesis of SMIORE, you need to understand the man behind it. M.Y. Ghorpade (Murarirao Yeshwantrao Ghorpade), eldest son of Y.R. Ghorpade, was incorporated by M.Y. Ghorpade, who was associated with the management of the Company from its inception and represented Sandur in the Karnataka Assembly for about four decades. He was an Economics Post Graduate from Cambridge University. Here was a man straddling two worlds: the feudal past of princely India and the socialist-industrial future that Nehru was architecting. Having completed his graduation in Bangalore and Masters in Economics Tripos from Cambridge University, he graduated from St Joseph's College, Bangalore, in 1950, and completed his MA (Economics Tripos) at Cambridge University in 1952.

The Cambridge economics degree wasn't just a credential—it was a worldview. While his contemporaries at Cambridge were debating Keynesian economics and the Marshall Plan, young Murarirao was thinking about how to transform a feudal economy into an industrial one. The theoretical became personal when he returned to Sandur and saw the Belgian mining company's operations that had been extracting manganese since 1907.

In 1904, the former ruler of Sandur, His Highness Y. R. Ghorpade, granted a mining lease over an area of 7,511 Ha to a Belgian company named General Sandur Mining Company for 25 years. The mining operations in the present area commenced in 1907. The Belgians had been content to extract and export raw ore—classic colonial economics. But the Ghorpades saw something different: an opportunity to build India's industrial base, one manganese deposit at a time.

The timing of SMIORE's founding in 1954 was no accident. India's first Five Year Plan (1951-1956) had just been launched, prioritizing heavy industry and infrastructure. Steel production was the holy grail—Nehru called steel plants the "temples of modern India." And what does steel need? Manganese. Every ton of steel requires 7-10 kg of manganese as an alloying element. Without manganese, steel is brittle and useless. The Ghorpades weren't just mining a mineral; they were mining India's industrial future.

His Highness Yeshwantrao Hindurao Ghorpade envisioned scientifically developing and professionally managing the mines. To realise this vision, he guided and supported his eldest son, Murarirao Yeshwantrao Ghorpade, in establishing SMIORE in 1954. The phrase "scientifically developing" is crucial here. This wasn't going to be the crude extraction methods of the colonial era. From day one, SMIORE adopted systematic mining practices, geological surveys, and proper ore grading—revolutionary for Indian mining in the 1950s.

The early operations centered in Deogiri village, where the earth revealed its treasures reluctantly. The manganese here had a special characteristic that would become SMIORE's competitive moat: low phosphorus content. In the steel-making world, phosphorus is the enemy—it makes steel brittle and prone to cracking. Indian steel plants desperately needed low-phosphorus manganese, and SMIORE had it in abundance.

But perhaps the most remarkable aspect of this founding story was the social vision embedded in the enterprise. Mahatma Gandhi called Sandur "an oasis" as he applauded the royal administration for abolishing the caste-based discrimination in the state and fostering equanimity amongst its people. This wasn't just about making money from mining; it was about creating employment, developing backward regions, and proving that Indian enterprise could match any in the world.

Shri M.Y.Ghorpade joined The Sandur Manganese & Iron Ores Limited as an Administrative Officer in 1956 and worked at the Mines office in Deogiri. In 1959, he was made the Joint Managing Director of SMIORE and worked in that capacity till 1972. In 1978, after finishing his term as Finance Minister of Karnataka, he returned to actively work for SMIORE and was appointed as Managing Director. The seamless movement between public service and private enterprise reflected a uniquely Indian model of development—where business leaders saw themselves as nation-builders, not just profit-maximizers.

By the late 1950s, SMIORE had established itself as more than just another mining company. It was becoming an institution—professionally managed, scientifically operated, and socially conscious. The seeds planted in 1954 were beginning to sprout, setting the stage for an aggressive expansion that would transform SMIORE from a regional mining operation into a national industrial force.

III. Building the Mining Empire (1960s-1990s)

The scorching summer of 1964 marked a turning point. As India mourned Nehru's death and Lal Bahadur Shastri took the reins of a food-scarce nation, SMIORE was making a bet that would define its next half-century. Under the visionary leadership of Murarirao Yeshwantrao Ghorpade, the Company became a public limited entity in 1964 and later listed on the BSE (Bombay Stock Exchange) Limited. Going public wasn't just about raising capital—it was a declaration that this princely mining venture was ready to play in the big leagues.

The decision to convert to a public limited company on July 29, 1964, came with a specific purpose: establishing an electro-metallurgical industry at Vyasanakere near Hospet. This wasn't diversification for its own sake. The Ghorpades understood a fundamental truth about commodity businesses: those who control the value chain control the profits. Why sell raw manganese ore for ₹100 when you could convert it to ferroalloys and sell for ₹1,000?The scale of what SMIORE controlled was staggering: large mines with two leases up to 2033, ML-2678 and ML-2679, with an area of 1860.10 hectares (ha) and 139.20 ha, respectively with reserves of Manganese Ore: 17MT & Iron Ore: 110 MT. To put this in perspective, that's roughly 2,000 hectares of mineral-rich land—about the size of 2,800 football fields. And they had the rights locked up until 2033, giving them a 70-year runway from the 1960s.

Since its inception in 1954, the Company has owned and operated the largest manganese ore mines in the private sector, along with sizeable iron ore reserves located in Sandur, Ballari district of Karnataka. This wasn't just big for Karnataka or even South India—SMIORE had become a national player. The low phosphorus manganese they were pulling out of the ground was exactly what India's nascent steel industry needed.

The infrastructure development during this period was remarkable. The SMIORE mines are well-connected to two railway sidings - Swamihalli (SMLI) and Sunderambencha (SDMG) on the Swamihalli - Hospet BG Line. Building railway connectivity in the 1960s and 70s wasn't just about logistics—it was about staking a claim to the future. While competitors were still loading ore onto bullock carts and trucks, SMIORE was moving thousands of tons by rail directly to steel plants and ports.

But the real genius of this era was the approach to mining itself. SANDUR was well lauded by the Vasudeva Committee for systematic mining and associations under the aegis of IBM and DGMS for safety and ecologically sustainable mining. In an industry notorious for crude extraction methods and environmental damage, SMIORE was playing a different game. They were mining scientifically—mapping ore bodies, maintaining proper benches, ensuring slope stability. This wasn't strip mining; it was surgical extraction.

The labor relations story during this period deserves special mention. The semi-mechanized and labour-intensive processes generate large-scale employment opportunities for the people living in and around the town of Sandur. In a region where agriculture was the only employment option, SMIORE created thousands of jobs. But more than jobs, they created a social contract. The company built hospitals, schools, and housing colonies. They turned Sandur from a sleepy princely backwater into a thriving mining town. The recognition came later, but it validated what SMIORE had been doing all along. The Company has been receiving 5 Star Rating awards from inception of this award by the Ministry of Mines, Government of India in the year 2014 -15 and this is the 8th consecutive year that the Company has received these awards. More remarkably, in 2025, the Ministry of Mines on Monday awarded seven-star ratings for the first time to three mines – Ultratech Cement's Naokari limestone mine, Tata Steel's Noamundi iron ore mine, and Sandur Manganese and Iron Ore Ltd.'s Kammatharu mine. This seven-star status—the highest possible rating—recognized mines that had maintained five-star ratings for five consecutive years and passed rigorous evaluation.

The iron ore side of the business was evolving too. Company produces iron ore with Fe content of 56-58%, with lump to fine production ratio of 1:2. This wasn't the highest-grade iron ore in the world, but it was perfectly suited for Indian blast furnaces. The lump-to-fine ratio mattered because lumps could go straight into furnaces while fines needed sintering—another value-addition opportunity SMIORE would later exploit.

By the 1990s, SMIORE had built something remarkable: a mining operation that combined scale with sustainability, volume with value addition, and profit with purpose. They weren't just extracting minerals; they were building an ecosystem. The railway sidings, the worker colonies, the systematic mining practices—all of these created barriers to entry that protected SMIORE's position even as India liberalized its economy in 1991.

The company's approach to community development during this period deserves special attention. While other mining companies faced labor strikes and local opposition, SMIORE enjoyed remarkable industrial peace. The secret? They treated mining not as extraction but as partnership. Local communities weren't just labor pools; they were stakeholders. The company built schools that educated the children of miners, hospitals that served entire villages, and training programs that turned unskilled laborers into mining technicians.

This period also saw the company navigate India's complex regulatory environment with remarkable skill. Mining in India has always been politically charged—land rights, environmental concerns, and corruption scandals regularly roiled the sector. But SMIORE's systematic approach and clean reputation helped it avoid the pitfalls that destroyed many competitors. When the Karnataka mining scams erupted in the 2000s and 2010s, SMIORE emerged unscathed, its licenses intact, its reputation enhanced.

The foundation built during these three decades—1960s through 1990s—would prove crucial for what came next. The company had ore reserves, infrastructure, reputation, and most importantly, the capital and credibility to move up the value chain. The stage was set for the great ferroalloy gambit.

IV. The Ferroalloys Gambit: Forward Integration

The year was 1968. India had just survived its worst drought in a century, the Green Revolution was taking root, and the country's steel plants were crying out for a critical ingredient: ferroalloys. Without ferromanganese and silicomanganese, you couldn't make quality steel. And without quality steel, you couldn't build the India that planners dreamed of. It was against this backdrop that SMIORE made its boldest move yet.SMIORE commenced ferroalloy operations in the year 1968 in its leading-edge manufacturing unit equipped with sophisticated Italian and Norwegian machinery at Vyasanakere, near Hospet, Karnataka. The first furnace was a 15 MVA electric reduction furnace supplied by Ing Leone Tagliaferri & C-Spa, Italy, with technical collaboration from Sadacem, Belgium, at a capital cost of about Rs. 30 million—a massive investment for that era. The furnace was capable of producing 36,000 tonnes of foundry grade pig iron or about 30,000 tonnes of ferromanganese/silicomanganese per annum.

But here's where it gets interesting. Our present Chairman Emeritus, Shivrao Yeshwantrao Ghorpade, helmed the Company's foray into the electro-metallurgical industry with the production of ferroalloys in 1968. A Metallurgical Engineer from the prestigious Colorado School of Mines in the USA, and an eminent metallurgy expert in the country, he guided in developing and building infrastructure of the SMIORE's Metal & Ferroalloy Plant from scratch to its commissioning and implementation of strong principles, scientific and systematic procedures and a performance-oriented approach to the manufacturing operations methodology.

Think about the audacity of this move. In 1968, most Indian mining companies were content to dig and ship. The technology for ferroalloy production was closely guarded by European and American companies. Electric arc furnaces required massive amounts of power in a country where electricity was scarce. The metallurgy was complex—get the temperature wrong by 50 degrees or the carbon ratio off by 0.5%, and you'd produce expensive slag instead of valuable ferroalloys.

The company went in for further expansion by installing two 20 MVA electric reduction furnaces (in 1977 and 1980), each capable of producing 12,000 tonnes of ferrosilicon per annum. These furnaces were supplied by Elkem Spigerverket, Norway—the gold standard in ferroalloy technology. By bringing in Norwegian expertise, SMIORE wasn't just buying equipment; they were buying knowledge, training, and a place in the global ferroalloy community.

By the year 1980, the Company's metal & ferroalloy plant was recognized as one of the finest metallurgical plants of the country and gained prominence for supplying quality low-phosphorous pig iron to the Indian foundry industry, especially for the quality-conscious automobile industry, and also ferroalloys to SAIL and other steel plants in India and overseas. The low-phosphorus advantage from their manganese ore carried through to their ferroalloys, creating a product that commanded premium prices.

The technical challenges of ferroalloy production deserve appreciation. You're essentially running controlled lightning through a mixture of ore, coke, and flux at temperatures exceeding 2000°C. The chemistry has to be perfect—too much silicon and you get silicomanganese instead of ferromanganese; too little carbon and the reduction doesn't happen; too much phosphorus and your customer's steel becomes brittle. It's industrial alchemy at its most demanding.

The capital intensity was staggering. Each furnace cost millions of rupees in an era when a middle-class salary was ₹500 per month. The power requirements were enormous—a single 20 MVA furnace could consume as much electricity as a small town. Which is why SMIORE's next move was so strategic: they built their own power plant. The Company embraced progress and innovation, expanding capacities for Silico Manganese and Ferro Manganese (SiMn/ FeMn) to 95,000/ 1,25,000 TPA from 48,000/ 66,000 TPA in 2022. This wasn't just incremental growth—it was a doubling down on the ferroalloy strategy that had proven so successful. The expanded capacity put SMIORE among India's top ferroalloy producers, competing with companies many times its size.

But perhaps the most important aspect of the ferroalloy gambit was how it changed SMIORE's business model. Instead of being price-takers in the volatile ore market, they became price-makers in the value-added ferroalloy market. When manganese ore prices crashed, ferroalloy margins often expanded as steel companies still needed their essential ingredients. When ore prices soared, SMIORE captured the full value chain profit.

The ferroalloy operations are powered by a captive 32 MW thermal power plant, which was set up as a strategic move to eliminate dependence on expensive and inadequate power. This captive power strategy would become increasingly important as India's power situation remained unpredictable through the 1980s and 1990s. While competitors faced production shutdowns during power cuts, SMIORE's furnaces kept running.

The risk management aspect of this forward integration cannot be overstated. Commodity businesses are notoriously cyclical—feast or famine. By moving into ferroalloys, SMIORE created multiple revenue streams with different demand drivers. Ferromanganese for steel production, silicomanganese for special steels, ferrosilicon for aluminum alloys—each had its own market dynamics, smoothing out the volatility.

The technical expertise built during this period became a moat. Running ferroalloy furnaces isn't something you learn from a manual. It requires years of experience, understanding how different ore grades behave at different temperatures, how to adjust the carbon-to-ore ratio for optimal reduction, how to manage the slag chemistry. This tacit knowledge, accumulated over decades, couldn't be easily replicated by new entrants.

The financial impact was transformative. While mining remained the volume business, ferroalloys became the margin business. A ton of manganese ore might sell for $100-150, but the ferromanganese made from it could command $1,000-1,500. Even accounting for the additional costs of production, the value addition was substantial.

By the 1990s, SMIORE had successfully transformed from a mining company that happened to make ferroalloys into an integrated metals producer where mining and manufacturing reinforced each other. The ferroalloy gambit had paid off spectacularly, setting the stage for the next phase of growth: energy independence through an even more ambitious expansion into power generation and coke production.

V. Power Play: Energy Independence Strategy

The furnaces at Vyasanakere glowed white-hot through the night, consuming electricity at rates that would make accountants weep. By the early 2000s, SMIORE faced a stark reality: in the ferroalloy business, your biggest competitor isn't another company—it's your electricity bill. Power costs could account for 40-50% of ferroalloy production expenses. In India's perpetually power-short economy, this wasn't just a cost issue; it was an existential threat.

The company's response would reshape its entire business model. Rather than remaining hostage to state electricity boards and their erratic supply, SMIORE embarked on an energy independence strategy that would eventually see it generating power through a 32-megawatt thermal power plant and recently adding Coke Oven operations producing 220 mu of energy per year.

But the real masterstroke came with the coke oven project. In 2018, the Company embarked on an ambitious Coke Oven expansion project, which commissioned in FY 2021. Coke Oven Plant operations of Batteries 1 & 2 was commissioned in January 2020. The new 24 MVA furnace was commissioned in March 2020. This wasn't just about making coke—it was about capturing waste heat and turning it into power.

The Stage I of the Iron and Steel (I&S) Project, which comprised of a 0.4 MTPA Coke Oven Plant (COP), 30 MW Waste Heat Recovery Boiler (WHRB) and Repair & Refurbishment of Ferroalloy Plant implemented got commissioned in FY 2020-21. The genius of this setup? The coke ovens produced metallurgical coke needed for ferroalloy production while generating waste heat that powered turbines to produce electricity. It was industrial symbiosis at its finest.

Completed coke oven expansion in FY21 with two plants having cumulative production capacity of 0.4 MTPA, four coke oven batteries with two waste heat recovery boilers (30 MW). This wasn't incremental improvement—it was a fundamental reimagining of SMIORE's energy architecture. The company was no longer just mining and manufacturing; it was orchestrating an intricate dance of materials and energy flows.

The environmental angle added another dimension. While the world was increasingly concerned about carbon emissions, SMIORE was capturing waste heat that would otherwise be lost to the atmosphere and converting it into useful energy. The coke ovens, traditionally seen as dirty technology, were being reimagined as part of an integrated, relatively cleaner production system.

The timing of this energy push was prescient. As India's economy boomed in the 2000s and 2010s, industrial power demand soared. State electricity boards, already stretched, began implementing savage power cuts for industrial users. Companies without captive power faced production losses, missed delivery schedules, and damaged customer relationships. SMIORE, with its integrated power generation, sailed through these disruptions.

The financial mathematics were compelling. The 32 MW thermal plant and 30 MW waste heat recovery system could generate approximately 500 million units of power annually. At industrial power rates of ₹6-8 per unit, this represented ₹300-400 crore of value creation annually—either through cost savings or through selling surplus power to the grid.

But perhaps more importantly, the energy independence strategy changed SMIORE's competitive position. In commodity businesses, the low-cost producer wins. By controlling their energy costs—the single largest variable expense in ferroalloy production—SMIORE could remain profitable even when market prices squeezed high-cost producers out.

The coke production added yet another revenue stream. The Company has approximately four coke oven batteries with a cumulative capacity of 0.4 million tons per annum (MTPA). Metallurgical coke is essential for steel production and commands premium prices. What started as an energy strategy had evolved into a profitable business segment in its own right.

The integration went even deeper. The coke ovens needed coal, which SMIORE could source alongside the coal for its thermal power plant, achieving economies of scale in procurement. The coke went into the ferroalloy furnaces, replacing expensive purchased coke. The waste gases from coke production fired the boilers, generating steam for power. Every waste stream became an input stream somewhere else.

This energy strategy also provided optionality. When power prices were high, SMIORE could sell surplus power to the grid. When ferroalloy demand was strong, they could consume all power internally for maximum production. This flexibility—the ability to optimize across multiple variables—is what separates sophisticated industrial enterprises from simple commodity producers.

The environmental compliance aspect, while challenging, became a competitive advantage. As India tightened pollution norms, many smaller players couldn't afford the investment in pollution control equipment. SMIORE's integrated approach, with waste heat recovery and modern pollution control systems, positioned it well for the regulatory future.

By 2021, SMIORE had achieved something remarkable: near-complete energy independence in one of the world's most energy-constrained industrial environments. The power play had transformed SMIORE from a mining company that made ferroalloys into an integrated materials and energy conglomerate. The stage was set for the modern era of diversification and scale.

VI. Modern Era: Diversification & Scale (2000s-Present)

The spreadsheet on Bahirji Ghorpade's laptop told a story of explosive growth. Q3 FY25 results had just been compiled: consolidated net profit surged to Rs 137.48 crore from Rs 9.07 crore in Q3 FY24. Revenue stood at Rs 951.87 crore, steeply higher than Rs 153.02 crore in the same quarter previous year. The numbers were staggering—a 1,416% increase in profit, 522% surge in revenue. But for the young Managing Director who had taken charge in June 2020, these numbers were just the beginning of a larger transformation story. The modern era of SMIORE began with a series of strategic expansions. SANDUR has obtained Environmental Clearance and other approvals to enhance Manganese ore production from 0.28 to 0.58 MTPA and Iron ore production from 1.60 to 4.50 MTPA along with 7 MTPA Beneficiation Plant and a Downhill Conveyor System. This wasn't just incremental growth—it was a tripling of iron ore capacity and doubling of manganese capacity, positioning SMIORE for a completely different scale of operations.

The segments now consist of Mining, Ferroalloys, and Coke and Energy, with the Mining Segment accounting for ~64% of 9MFY24 revenues. But the real story isn't in the segment breakdown—it's in how these segments reinforce each other. The mining provides raw materials for ferroalloys, the coke ovens provide reductants for the furnaces and generate power, and the power enables everything else. It's an industrial ecosystem, not just a collection of businesses.

For the full year FY2025, net profit rose 96.53% to Rs 470.61 crore against Rs 239.46 crore in FY2024. Sales rose 150.38% to Rs 3135.06 crore from Rs 1252.13 crore. These aren't just good numbers—they're transformational. The company had essentially doubled its profitability and more than doubled its revenues in a single year.

The regulatory victories were equally impressive. The EC permits iron ore production of 0.216 million tonnes per annum (MTPA) from the Ramghad mine, with existing manganese ore production of 0.05 MTPA remaining unchanged. The company also received approval to raise its iron ore production capacity from the current 3.81 million tonnes per annum (MTPA) to 4.36 MTPA. Each approval represented years of patient work navigating India's byzantine environmental clearance process.

But perhaps the most ambitious element of the modern expansion is the steel plant vision. SANDUR is working tirelessly to set up its Steel plant in Vyasanakere, Karnataka. This would complete the value chain—from ore to steel—making SMIORE one of the few fully integrated metals companies in India. The proposed plant includes a 0.3 MTPA Ductile Iron Pipe Plant, Blast Furnace, Sinter Plant, and associated facilities.

The renewable energy pivot adds another dimension to the modern strategy. A 42.9 MW renewable hybrid solar & wind energy project in collaboration with ReNew Sandur Green Energy Private Limited was commissioned on June 13, 2023. The 33 MW Solar Power Plant and 9.9 MW Wind Turbine Generators interconnect with the Karnataka Power Transmission Corporation Limited grid. This isn't greenwashing—it's a fundamental rethinking of energy sourcing as renewable power becomes cost-competitive with thermal.

The beneficiation plant deserves special attention. The proposed 7 MTPA Beneficiation Plant would allow SMIORE to upgrade low-grade ores into high-grade concentrates. In a world where high-grade deposits are increasingly rare, the ability to beneficiate low-grade ore is like having a technology that turns lead into gold. The Downhill Conveyor System would transport ore in a pollution-free and environment-friendly manner, reducing truck traffic and diesel consumption. The capital market moves added another dimension. The board has approved a bonus issue in the ratio of 2:1, allotting 2 new equity shares for every 1 existing share, with each share having a face value of ₹10 in August 2025. This follows the previous bonus issue announced in 2024 in a generous 5:1 ratio. The back-to-back bonus issues signal massive confidence in future growth—you don't dilute equity unless you're certain of generating proportionally higher profits.

The listing on the National Stock Exchange in September 2023 marked another milestone. The company shares got listed on National Stock Exchange of India (NSE) Limited on 7 September 2023. This wasn't just about liquidity—it was about institutional recognition. NSE listing opens doors to institutional investors, index inclusion, and enhanced visibility.

The modernization isn't just about scale—it's about sophistication. The company is implementing digital systems for mine planning, using drones for surveying, and employing IoT sensors for equipment monitoring. The downhill conveyor system represents next-generation thinking about logistics—using gravity instead of diesel to move ore.

Under the leadership of current Managing Director, Bahirji A. Ghorpade, SANDUR has achieved remarkable milestones such as commissioning Coke Oven Plant and Waste Heat Recovery Boiler ahead of schedule. Bahirji, who took charge in June 2020 after pursuing his master's degree in finance and management from Cranfield University, represents the third generation of Ghorpade leadership—bringing global perspective to a local enterprise.

The financial performance validates the strategy. The company achieved highest-ever Revenue, EBITDA and PAT in FY22, and has continued that momentum. With segments accounting for Mining (~64% of revenues), Ferroalloys (~25%), and Coke and Energy (~11%), SMIORE has transformed from a mining company into a diversified industrial enterprise.

The modern era isn't just about growth—it's about sustainable growth. The company has been consciously and generously contributing towards Social and Environmental improvement through community health centres, compensation to farmers, desilting of tanks, environment protection and forest conservation activities. The Sandur Kushala Kala Kendra nurtures traditional handicrafts, preserving and fostering traditional skills and art.

As we enter 2025, SMIORE stands at an inflection point. The expansions are approved, the capital is in place, and the market is hungry for both manganese and iron ore. The steel plant plans could transform SMIORE from a raw material supplier into a finished goods manufacturer. The renewable energy investments position it for a carbon-constrained future. And the family's continued commitment—maintaining 74.2% shareholding—ensures long-term thinking prevails over quarterly pressures.

VII. Family Business Evolution & Corporate Governance

Three photographs hang in the boardroom at Sandur House in Bangalore. The first, sepia-toned and formal, shows Y.R. Ghorpade in royal regalia—the last maharaja of Sandur. The second captures M.Y. Ghorpade at a mine site, hard hat on, examining ore samples with engineers. The third, in vivid color, shows Bahirji A. Ghorpade ringing the NSE bell in 2023. Three generations, three eras, one company. The visual narrative captures something profound about family businesses: how do you honor tradition while embracing transformation?

The Ghorpade family's 74.2% promoter holding tells only part of the story. In an era where promoter stakes are routinely diluted for growth capital, the family has maintained super-majority control while still expanding aggressively. How? Through a combination of internal accruals, judicious debt, and most importantly, patience—that rarest of commodities in modern capitalism. The succession planning at SMIORE offers a masterclass in family business transition. Bahirji A Ghorpade took on the charge of the company in June 2020, after serving the company across functions and roles, starting from the position of a Management Trainee. He pursued his Bachelors in Commerce from Christ University Bengaluru, began the journey in the Company as an Executive Trainee in 2015, where he understood the grass-root level functioning of the Company. After working for two years, he took a sabbatical and completed Masters in Finance & Management from Cranfield School of Management, UK.

This wasn't nepotism—it was apprenticeship. For the first two years, he spent time within all units and departments, determined to understand the grassroots functioning of the organisation. The Cranfield degree wasn't just credentialing; it was about bringing global best practices to a traditional Indian business. When he returned in 2018, he wasn't parachuted into the corner office. He worked in project accounting, corporate affairs, material management, finance, administration, and general management before taking the MD role.

The family's approach to governance evolved significantly over the decades. While maintaining control, they professionalized management. The board includes independent directors with expertise in mining, finance, and corporate governance. The audit committees, remuneration committees, and CSR committees function with genuine independence. This isn't window dressing—it's recognition that family control and professional governance aren't mutually exclusive.

The fourth generation promoter represents a fascinating evolution. Where the first generation brought royal authority, the second brought global education, and the third brought technical expertise, the fourth brings financial sophistication and sustainability consciousness. Bahirji's focus on ESG metrics, renewable energy, and sustainable mining practices reflects how family businesses must evolve to remain relevant.

The employee relationship deserves special attention. At present, the company has almost 3,000 employees. In most mining companies, labor relations are adversarial. At SMIORE, they're familial. A package of rice, jowar, wheat, 3 types of pulses, oil, chillies, jaggery, sugar, poha, groundnuts, fried gram, sooji, etc., is provided which meets the needs of a family for one full month at a total cost of ₹145, to every employee, largely insulating them from inflation and protecting their real wages and quality of life.

This paternalistic approach might seem outdated in the era of gig economy and at-will employment. But in rural Karnataka, where SMIORE operates, it creates loyalty that money can't buy. Multi-generational employment is common—grandfather, father, and son all working for the same company. This creates institutional memory and operational stability that's impossible to replicate.

The capital allocation philosophy reflects family ownership advantages. While public companies face quarterly earnings pressure, SMIORE can take decade-long bets. The coke oven project took three years to commission. The steel plant will take five years. The mining expansion approvals took seven years. No quarterly-focused management would have this patience.

But family ownership also brings challenges. The concentration risk is obvious—74.2% in family hands means minority shareholders have limited influence. Succession risk is real—what if the next generation isn't interested or capable? And there's always the risk of family disputes, though the Ghorpades have remarkably avoided the feuds that destroyed many Indian business families.

The professional management layer helps mitigate these risks. Key positions are held by non-family professionals. The CFO, the heads of mining, ferroalloys, and energy divisions—all are professionals hired for competence, not connections. This creates a meritocratic culture within a family-controlled structure.

The recent bonus issues signal confidence but also strategy. By issuing bonus shares rather than dividends, the family maintains capital within the company for growth while still rewarding shareholders. The 5:1 bonus in 2024 followed by 2:1 in 2025 effectively gave shareholders 12 shares for every original share—massive value creation without cash outflow.

The governance structure has evolved to handle complexity. With mining, manufacturing, and energy operations, plus planned steel production, SMIORE is essentially multiple businesses under one roof. Each division has operational autonomy while strategic decisions remain centralized. It's a federal structure—unified at the top, autonomous at the operating level.

The CSR initiatives aren't just compliance—they're part of the family's social compact. The Sandur Kushala Kala Kendra, supporting traditional handicrafts, the Sandur Residential School, providing education to rural children, the healthcare facilities for communities—these reflect a princely tradition of noblesse oblige adapted for corporate India.

As SMIORE enters its eighth decade, the family business model faces new tests. Can it maintain entrepreneurial agility at increased scale? Can it attract and retain top talent competing against MNCs? Can it navigate the transition to the fifth generation when that time comes? The answers will determine whether SMIORE remains a family business that happens to be public, or becomes a public company that happens to be family-controlled—a subtle but crucial distinction.

VIII. Mining in Modern India: Regulatory & Environmental Challenges

The Supreme Court order came down like a hammer in 2011. All mining in Karnataka's Bellary district—suspended. The devastating impact rippled through the industry: companies bankrupted, workers unemployed, government revenues vanished. In the eye of this storm stood SMIORE, watching competitors crumble while somehow keeping its operations intact. How did a 60-year-old mining company navigate India's most severe mining crisis? The answer reveals everything about surviving in one of the world's most complex regulatory environments.

Mining in India isn't just about geology and economics—it's about politics, environmental activism, judicial intervention, and social license. The Karnataka mining scam, which erupted in 2010-2011, involved illegal mining worth thousands of crores, implicated chief ministers and ministers, and led to a complete overhaul of how India regulates mining. For SMIORE, with its operations in the epicenter of the scandal, this was an existential moment.

The company's survival strategy was built on a foundation laid decades earlier: systematic and scientific mining practices. SANDUR was well lauded by the Vasudeva Committee for systematic mining. When investigators came calling, SMIORE could show clean paperwork going back decades—proper environmental clearances, accurate production records, legitimate royalty payments. In an industry where regulatory compliance was often treated as optional, SMIORE's obsessive documentation became its salvation.

But survival wasn't enough. SMIORE turned crisis into opportunity. While competitors remained shut or operated under severe restrictions, SMIORE received regulatory clearance for expanding mining operations, approval from Central Empowered Committee to increase iron ore production limit. The approvals didn't come easily—they required years of patient engagement with regulators, environmental groups, and local communities.

The environmental clearance process in India is Byzantine in its complexity. It involves the Ministry of Environment, Forest and Climate Change (MoEFCC), State Pollution Control Boards, the Indian Bureau of Mines, the Forest Department, district collectors, and often, the courts. Each has its own requirements, timelines, and political pressures. Navigating this requires not just legal expertise but diplomatic skill.

SMIORE's approach was methodical. For the expansion from 1.60 to 4.50 MTPA iron ore production, the company first obtained environmental clearance from MoEFCC, then consent from Karnataka State Pollution Control Board, then approval from the Supreme Court-appointed Central Empowered Committee, and finally, the maximum permissible annual production limit from the monitoring committee. Each step took months, sometimes years. A single misstep could reset the entire process.

The company's environmental management went beyond compliance. Honoured with Seven Star Rated Mine award by Ministry of Mines for outstanding efforts in green mining—the highest possible rating, achievable only after maintaining five-star ratings for five consecutive years and passing rigorous evaluation. This wasn't greenwashing but genuine operational excellence. The company implemented water harvesting, afforestation programs, and dust suppression systems that became industry benchmarks.

The social license dimension proved equally critical. Mining companies across India face local opposition—sometimes genuine environmental concern, often politically motivated, occasionally extortionate. SMIORE's deep roots in Sandur, its employment of local communities, and its extensive CSR programs created a buffer against such opposition. When activists targeted mining companies, local communities often defended SMIORE.

The regulatory framework kept evolving. The Mines and Minerals (Development and Regulation) Amendment Act, the National Mineral Policy, the District Mineral Foundation requirements—each brought new compliance burdens. The company needed dedicated teams just to track regulatory changes and ensure compliance. The cost of compliance often exceeded the cost of mining itself.

The Forest Rights Act added another layer of complexity. Mining leases often overlapped with forest lands, requiring separate forest clearances. Tribal rights, wildlife corridors, and biodiversity concerns all needed addressing. SMIORE's patient approach—engaging with communities, conducting detailed environmental impact assessments, implementing mitigation measures—turned potential opponents into stakeholders.

The political dimension couldn't be ignored. Mining licenses in India often become political footballs. Changes in state government could mean review of all clearances. SMIORE's strategy was political neutrality—maintaining relationships across party lines, focusing on compliance rather than connections, building reputation rather than relying on influence.

The downhill conveyor system exemplifies SMIORE's approach to regulatory challenges. Traditional ore transportation by trucks created pollution, damaged roads, and generated community opposition. The conveyor system eliminated truck traffic, reduced diesel consumption, and improved community relations. It also impressed regulators, demonstrating SMIORE's commitment to sustainable mining.

The renewable energy investments served multiple purposes. They reduced carbon footprint, satisfying environmental concerns. They provided energy security, addressing operational needs. And they positioned SMIORE as a progressive company, earning regulatory goodwill. In India's relationship-driven regulatory environment, reputation matters as much as compliance.

The recent approval to enhance manganese ore production from 0.28 to 0.58 MTPA and iron ore from 1.60 to 4.50 MTPA didn't happen overnight. It was the culmination of years of patient work—maintaining spotless compliance records, investing in environmental protection, building community support, and demonstrating that mining could be done responsibly.

The cost has been substantial. Environmental compliance, CSR spending, and regulatory management probably account for 15-20% of SMIORE's operational costs. But in an industry where one regulatory violation can shut down operations worth thousands of crores, this is insurance well worth paying.

Looking forward, the regulatory environment will only get more complex. Climate change concerns, ESG requirements, and international sustainability standards are adding new dimensions to compliance. But SMIORE's seven-decade track record suggests it will adapt, as it always has—methodically, patiently, and successfully.

IX. Playbook: Business Strategy & Lessons

What would Warren Buffett see in a princely Indian mining company? At first glance, SMIORE violates several Buffett principles—it's in a commodity business with no pricing power, it's capital intensive with huge environmental liabilities, and it operates in a challenging regulatory environment. Yet dig deeper, and you find a business with a moat as wide as the Bellary hills are high. The SMIORE playbook offers lessons that transcend mining, revealing universal principles about building enduring businesses in challenging environments.

Lesson 1: Vertical Integration as Risk Mitigation

The conventional wisdom says focus on core competence. SMIORE did the opposite, integrating from ore to alloy to energy. But this wasn't diversification for its own sake—it was risk mitigation through value chain control. When ore prices crash, ferroalloy margins often expand. When power costs spike, captive generation provides buffer. When coke prices soar, internal production ensures supply.

The integration creates operational synergies invisible to financial statements. The waste heat from coke ovens generates power. The power runs ferroalloy furnaces. The ferroalloys consume manganese ore. Each business supports the others, creating resilience that standalone operations lack. In commodity businesses where you can't control price, controlling costs through integration becomes the competitive advantage.

Lesson 2: Patient Capital's Competitive Advantage

The Ghorpade family's 74.2% ownership isn't just about control—it's about time horizon. While public companies optimize for quarterly earnings, SMIORE makes decade-long bets. The coke oven project had negative returns for three years before becoming profitable. The mining expansion approvals took seven years. The steel plant will take five years to commission.

This patience extends to market cycles. Commodity businesses are viciously cyclical. Most players leverage up during booms and collapse during busts. SMIORE's conservative balance sheet and family backing allow it to survive downturns and acquire assets when others are selling. As Buffett says, "Be fearful when others are greedy and greedy when others are fearful."

Lesson 3: Regulatory Compliance as Competitive Moat

In industries with complex regulation, compliance becomes a barrier to entry. SMIORE's seven-star environmental rating isn't just a certificate—it's a competitive weapon. New entrants must match these standards, requiring years of investment and operational excellence. Existing players who cut corners face shutdown risk, as the Karnataka mining crisis demonstrated.

The company treats regulatory relationships as strategic assets. Consistent compliance, transparent operations, and proactive engagement with regulators build trust capital. When regulations change—and in India, they always do—this trust provides flexibility and faster approvals. It's expensive insurance that pays off during crisis.

Lesson 4: Community Integration Beyond CSR

SMIORE's community engagement transcends mandatory CSR spending. Three generations of families working in the mines create stakeholder alignment impossible to replicate. The subsidized food programs, schools, and healthcare aren't charity—they're investments in social license. When activists protest mining, local communities defend SMIORE because their prosperity depends on it.

This extends to supplier relationships. Local contractors, transport operators, and service providers depend on SMIORE. This creates an ecosystem invested in the company's success. In India's relationship-driven business environment, these networks provide resilience that no amount of capital can buy.

Lesson 5: Technical Excellence as Differentiation

In commodity businesses, operational excellence is the only sustainable differentiation. SMIORE's low-phosphorus manganese ore commands premium pricing because steel makers need it. The systematic mining practices ensure consistent ore quality. The ferroalloy expertise allows customization for customer requirements.

This technical edge compounds over time. Decades of mining data inform extraction planning. Years of furnace operations optimize energy consumption. Generations of worker experience reduce operational risks. This tacit knowledge—impossible to document or transfer—becomes an appreciating asset.

Lesson 6: Capital Allocation Discipline

Despite massive growth, SMIORE maintained conservative leverage. The expansion has been funded through internal accruals and modest debt. No dilutive equity raises, no aggressive acquisitions, no unrelated diversification. Every investment connects to existing operations—mining feeds ferroalloys, ferroalloys need energy, energy requires coke.

The bonus shares instead of dividends reflect this discipline. Rather than cash dividends that leak capital, bonus shares reward shareholders while retaining capital for growth. The family's wealth remains tied to the business, aligning their interests with minority shareholders.

Lesson 7: Succession Planning as Institutional Building

The smooth transition across four generations didn't happen by accident. Each generation brought different skills—royal authority, global education, technical expertise, financial sophistication. But more importantly, each generation built institutions that outlast individuals.

Professional management in operational roles ensures continuity regardless of family involvement. Systematic processes reduce dependence on individual judgment. Corporate governance structures balance family control with stakeholder interests. The company is building to last centuries, not quarters.

Lesson 8: Optionality Through Scale

The approved expansion to 4.50 MTPA iron ore and 0.58 MTPA manganese ore creates optionality. SMIORE can sell ore when prices are high, process into ferroalloys when margins are better, or reserve for future steel production. Scale provides flexibility to optimize across market conditions.

This extends to energy strategy. Surplus power can be sold to the grid when prices are attractive or consumed internally when ferroalloy demand is strong. The renewable energy investments provide hedge against carbon taxes. Multiple options create value beyond any single path.

Lesson 9: Brand Building in B2B Markets

Mining companies rarely build brands, yet SMIORE has. The consistent quality, reliable supply, and ethical operations created reputation that commands premium pricing. Steel makers specify SMIORE ore. Ferroalloy customers pay advances. Regulators fast-track approvals. In commoditized markets, trust becomes the ultimate differentiation.

Lesson 10: Embrace Complexity as Barrier

SMIORE operates in one of the world's most complex business environments—Indian mining. Rather than avoiding this complexity, the company embraced it. The ability to navigate Karnataka politics, environmental clearances, Supreme Court committees, and local communities becomes a capability competitors can't replicate.

The playbook isn't about any single strategy but how multiple strategies reinforce each other. Vertical integration enables capital discipline. Patient capital allows regulatory compliance. Community integration supports expansion approval. Technical excellence justifies premium pricing. Each element strengthens the others, creating a business system rather than just a business.

For investors, the lesson is to look beyond financial metrics to competitive dynamics. For entrepreneurs, it's about building businesses that get stronger with time. For family businesses, it's about institutionalizing excellence while maintaining entrepreneurial spirit. The SMIORE playbook shows that even in the most challenging industries and environments, sustainable competitive advantage is possible—it just requires patience, discipline, and systematic execution over decades.

X. Analysis & Investment Case

The numbers tell a story of transformation. Trading at a P/E ratio of 15.45 with a current dividend yield of 0.50%, SMIORE appears fairly valued by conventional metrics. But conventional analysis misses the inflection point. With revenue surging 150% to ₹3,135 crore in FY2025 and net profit doubling to ₹470 crore, this isn't steady-state mining—it's a business in metamorphosis. The question for investors isn't whether SMIORE is cheap today, but what it becomes tomorrow.

The Bull Case: Structural Tailwinds and Operating Leverage

India's steel production is targeted to reach 300 million tonnes by 2030, up from 140 million tonnes today. Every tonne requires 7-10 kg of manganese. SMIORE's expanded capacity of 0.58 MTPA manganese ore positions it to capture this demand surge. With import dependence at 70% for manganese, domestic producers enjoy structural advantage through logistics costs and supply security.

The operating leverage is compelling. Mining has high fixed costs—once you've built infrastructure, incremental production has minimal variable costs. The approved expansion to 4.50 MTPA iron ore from 1.60 MTPA nearly triples output with proportionally lower cost increase. At current iron ore prices of ₹5,000-6,000 per tonne, this expansion alone could add ₹1,000+ crore to revenue.

The ferroalloy business provides pricing power unusual in commodities. SMIORE's low-phosphorus ferromanganese commands 10-15% premium over standard grades. With capacity expanded to 95,000 TPA silicomanganese and 125,000 TPA ferromanganese, and ferroalloy prices at historical highs, this segment could contribute ₹1,500+ crore revenue at full utilization.

The energy independence through 62 MW captive power (32 MW thermal + 30 MW waste heat recovery) saves ₹300-400 crore annually at current industrial power rates. The 42.9 MW renewable capacity adds another ₹150 crore value through carbon credits and renewable energy certificates.

The Bear Case: Commodity Cycles and Execution Risks

Commodity businesses are inherently cyclical. Iron ore prices have ranged from $40 to $220 per tonne over the past decade. Manganese ore prices are equally volatile. A China slowdown or global recession could crush prices and margins. SMIORE's operating leverage works both ways—high fixed costs mean losses mount quickly during downturns.

The expansion execution carries risks. The 7 MTPA beneficiation plant requires ₹500+ crore investment. The proposed steel plant could require ₹3,000+ crore. Cost overruns or delays could pressure balance sheet and returns. The company's limited experience in steel production adds execution uncertainty.

Regulatory risks remain elevated. A change in mining policy, environmental restrictions, or political upheaval in Karnataka could disrupt operations. The Supreme Court's continued oversight of Karnataka mining adds uncertainty. Any violation could trigger operational suspension, as competitors discovered.

The ESG concerns are structural. Mining is inherently environmentally destructive. As global investors increasingly exclude extractive industries, valuations could face permanent derating. Carbon taxes and environmental compliance costs will only increase, pressuring margins.

Competitive Positioning: David Among Goliaths

Against MOIL (market cap ₹3,000+ crore) in manganese and NMDC (market cap ₹40,000+ crore) in iron ore, SMIORE appears small. But size isn't everything. MOIL operates in underground mines with higher costs. NMDC focuses on volume over value addition. SMIORE's integrated model and premium products provide differentiation.

The private sector peers—Essel Mining, Rungta Mines, Serajuddin—lack SMIORE's downstream integration. Most are pure-play miners, vulnerable to price cycles. SMIORE's ferroalloy and energy businesses provide stability and margins these peers lack.

The real competition comes from imports. Indonesian and South African manganese, Brazilian and Australian iron ore set global prices. But logistics costs, import duties, and supply chain uncertainabilities provide domestic producers 15-20% landed cost advantage.

Valuation: Hidden Assets and Growth Options

The market values SMIORE at ₹7,272 crore market cap. But consider the replacement cost of assets: 2,000 hectares of mining leases (irreplaceable in today's regulatory environment), 95,000 TPA ferroalloy capacity (₹2,000+ crore replacement cost), 62 MW power generation (₹400+ crore), 0.4 MTPA coke ovens (₹800+ crore). The replacement value exceeds ₹5,000 crore for existing assets alone.

The growth pipeline adds substantial option value. At full expansion, SMIORE could generate ₹5,000+ crore revenue and ₹1,000+ crore EBITDA. At sector-average EV/EBITDA of 8-10x, this implies ₹8,000-10,000 crore enterprise value—40% upside from current levels.

The steel plant option is unvalued by markets. If executed successfully, a 1 MTPA steel plant could add ₹3,000 crore revenue and ₹500 crore EBITDA. This transforms SMIORE from mining company to integrated steel producer, deserving higher multiples.

Risk-Reward: Asymmetric Opportunity

The downside appears limited. At 0.5x book value and 7x P/E on trough earnings, SMIORE trades below replacement cost. The family's 74.2% ownership provides downside support—they won't let the company trade below intrinsic value indefinitely.

The upside is substantial. Successful expansion execution, favorable commodity cycles, and steel plant commissioning could drive 3-5x returns over 5 years. The operating leverage means small improvements in realization drive large profit increases.

The Investment Decision Framework

For value investors, SMIORE offers Benjamin Graham's "margin of safety"—trading below replacement cost with proven assets and cash generation. For growth investors, the expansion pipeline and steel plant option provide multi-year growth runway. For dividend investors, the improving cash generation suggests dividend increases ahead.

The key monitorables are execution milestones (beneficiation plant commissioning, production ramp-up), commodity prices (iron ore above $80/tonne, manganese ore above $150/tonne), and regulatory developments (forest clearances, environmental compliance).

The investment case ultimately rests on three beliefs: India's infrastructure build-out will drive steel demand; domestic mining will capture value from import substitution; and SMIORE's integrated model provides resilience through cycles. If these prove correct, SMIORE offers compelling risk-reward for patient investors willing to embrace complexity and cyclicality.

The market often mistakes complexity for risk. In SMIORE's case, complexity is the moat. Any investor willing to understand the business—really understand it—will find a company trading at reasonable valuations with substantial growth options and competitive advantages that compound over time. In a market obsessed with software and services, old-economy businesses like SMIORE offer contrarian opportunity for those willing to dig deep—literally and figuratively.

XI. Looking Forward & Reflections

As the morning mist clears over the Sandur hills, revealing the red earth scarred by seven decades of mining, a fundamental question emerges: What is the future of a 70-year-old mining company in a world racing toward net-zero emissions? The answer, paradoxically, might be brighter than ever. The energy transition doesn't eliminate the need for metals—it multiplies it. Every electric vehicle needs 4x more copper than a conventional car. Every wind turbine requires 500 kg of manganese for its steel structure. Every solar panel needs specialized alloys. The green revolution is, at its core, a mining boom in disguise.

SMIORE's manganese becomes even more critical in this new world. Beyond steel, manganese is essential for lithium-ion batteries—the manganese-rich NMC (Nickel Manganese Cobalt) cathodes that power Teslas and grid storage systems. As India builds its EV ecosystem, domestic manganese supply becomes a strategic imperative. SMIORE's expanded production couldn't be better timed.

The company's renewable energy pivot—42.9 MW of solar and wind—isn't just compliance; it's preparation. Carbon border taxes are coming. The EU's Carbon Border Adjustment Mechanism (CBAM) will penalize carbon-intensive imports. Steel and ferroalloys made with renewable power will command premiums. SMIORE's early investments position it ahead of the curve.

The steel plant ambition represents the biggest bet yet. India imports 50% of its steel despite being the world's second-largest producer. The government's production-linked incentive (PLI) scheme for specialty steel offers ₹6,322 crore in incentives. SMIORE's planned steel plant, integrated from ore to finished product, could capture both import substitution and PLI benefits.

But the real transformation might be technological. The beneficiation plant turning low-grade ore into high-grade concentrate is just the beginning. Future technologies—bio-leaching, plasma smelting, hydrogen-based reduction—could revolutionize metal extraction. SMIORE's technical expertise and capital resources position it to adopt and adapt these technologies.

The governance evolution continues with interesting possibilities. The bonus shares and NSE listing suggest preparation for something bigger. Perhaps acquisitions to consolidate India's fragmented mining sector. Maybe a strategic partner for the steel venture. Or possibly a generational transition that brings in professional CEOs while family remains as promoters.

The India story provides tailwind. As manufacturing shifts from China under "China Plus One" strategies, India needs raw materials. The Production Linked Incentive schemes across sectors—automobiles, electronics, textiles—all require metals. Domestic mining becomes critical for supply chain resilience.

Yet challenges loom large. Artisanal mining using technology could disrupt traditional operations. Recycling and circular economy models could reduce primary ore demand. Synthetic biology might create alternatives to mined materials. SMIORE must evolve from mining company to materials company to remain relevant.

The human dimension deserves reflection. Three thousand families depend on SMIORE for livelihood. Entire communities have grown around its operations. The company's success isn't just about shareholder returns—it's about sustaining ecosystems of human prosperity in one of India's most backward regions. The manganese-battery connection adds a compelling new dimension. According to BloombergNEF, demand for manganese from the battery sector is expected to increase ninefold by 2030. CPM Group expects the demand for high-purity manganese to increase 13 times between 2021 and 2031 (from 90 kt to 1.1 million tonnes of Mn contained) and 50 times between 2021 and 2050 (to 4.5 million tonnes of Mn contained). This isn't incremental growth—it's exponential transformation.

India's steel ambitions provide another growth vector. The Ministry of Steel, under the National Steel Policy (NSP), has set an ambitious target of reaching 300 MTPA capacity / 255 MTPA production by 2030. Every ton of steel requires manganese. SMIORE's location advantage—in Karnataka, close to steel clusters—becomes increasingly valuable as transportation costs rise.

The lessons from SMIORE's journey apply broadly to Indian business:

First, time horizons matter. The Ghorpades thought in generations, not quarters. This allowed investments that took years to pay off—the ferroalloy plant, the coke ovens, the mining expansions. In a world obsessed with quick returns, patient capital becomes competitive advantage.

Second, complexity can be a moat. SMIORE operates in one of the world's most challenging environments—Indian mining with its regulatory maze, environmental concerns, and social pressures. Rather than avoiding this complexity, they mastered it. What seems like a burden becomes a barrier that protects against competition.

Third, vertical integration in commodities works—if done right. The key is integration that creates operational synergies, not just financial engineering. SMIORE's model where waste from one process becomes input for another creates value that pure-play operations can't match.

Fourth, family businesses can professionalize without losing soul. The Ghorpades maintained control while bringing in professional management, modern governance, and institutional processes. This hybrid model—family values with professional execution—might be the optimal structure for long-term value creation.

Fifth, sustainable business is good business. SMIORE's environmental investments—initially seen as compliance costs—became competitive advantages. The seven-star rating, the renewable energy, the community programs—these aren't CSR theater but strategic assets.

Looking ahead, SMIORE faces choices that will define its next 70 years. Does it remain focused on mining and metals, or expand into new materials for the energy transition? Does it maintain family control, or dilute for growth capital? Does it stay Indian, or go global?

The answers matter not just for SMIORE but for Indian industry. As the country attempts its own transition from $3.7 trillion to $10 trillion economy, it needs companies that can operate at global scale while maintaining local roots. It needs businesses that can navigate complexity while maintaining integrity. It needs enterprises that think in decades while executing daily.

SMIORE's story suggests such companies exist—they just look different from Silicon Valley unicorns or Wall Street darlings. They're built over generations, not funding rounds. They measure success in sustainable value creation, not exit multiples. They see business not as extracting value but creating ecosystems of prosperity.

As the sun sets over the Sandur hills, painting the mining scars gold, one thing becomes clear: the future belongs not to those who extract resources fastest, but to those who transform them most thoughtfully. In that transformation—from ore to alloy, from family firm to institution, from princely privilege to public company—lies a blueprint for building businesses that last not just decades but centuries.

The manganese in your smartphone battery, the steel in your car, the ferroalloys in your buildings—they carry within them 70 years of patient building. That's the real treasure of Sandur: not what lies beneath the ground, but what's been built above it. A business, a community, a legacy. And in India's journey toward developed nation status, such enterprises—rooted yet reaching, traditional yet transforming—might just be the bedrock on which the future is built.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube