TRIDENT: From Punjab Textiles to Global Manufacturing Giant

I. Cold Open & Episode Roadmap

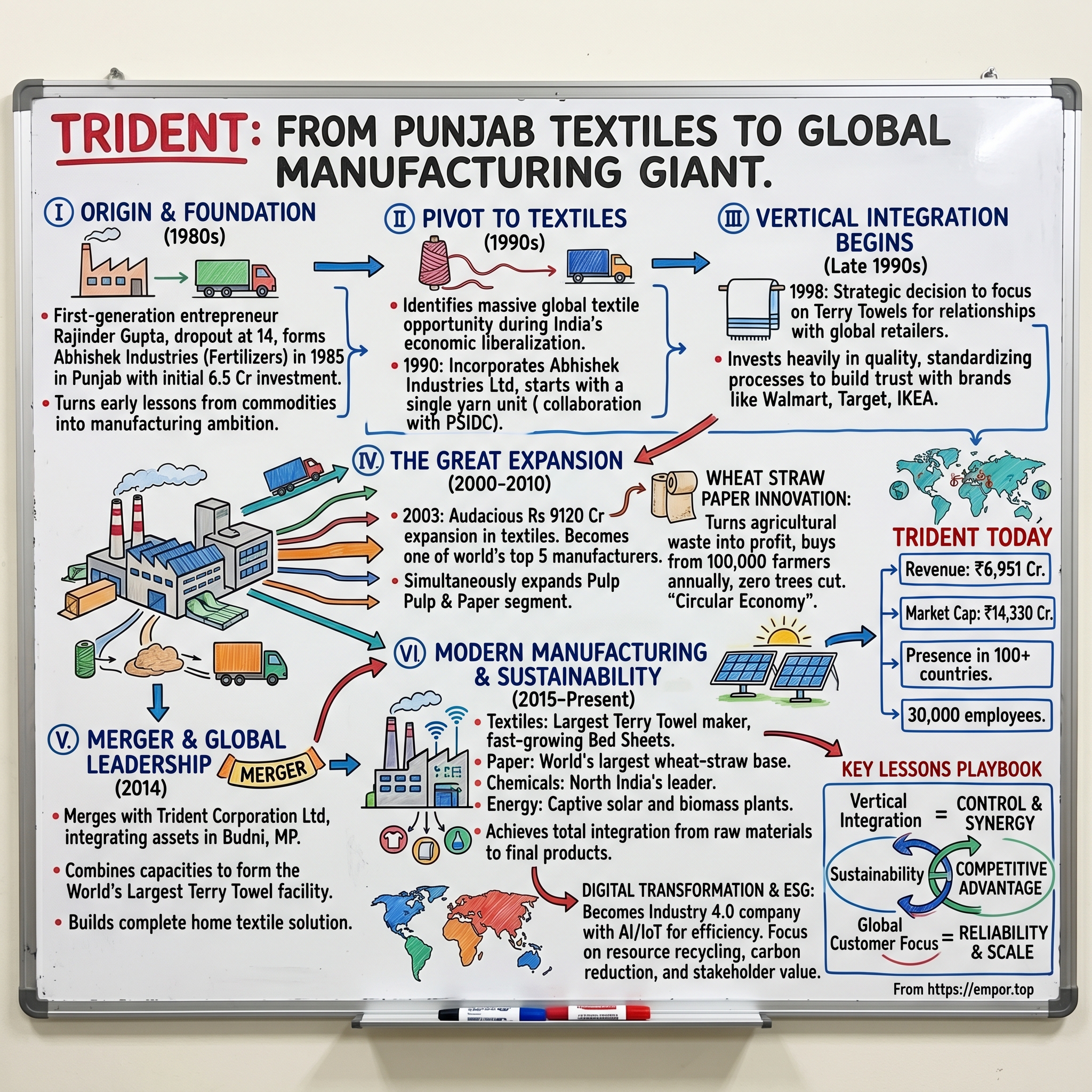

The sprawling factory floor in Budni, Madhya Pradesh, stretches for what seems like miles—looms humming in synchronized rhythm, producing 300,000 terry towels every single day. This isn't just any textile facility; it's the world's largest integrated terry towel manufacturing unit, a testament to what happens when Punjab ambition meets global scale. Welcome to the empire of Trident Limited, where a school dropout who once made cement pipes for ₹30 a day now commands a ₹14,330 crore market capitalization.

Picture this: Every morning, farmers across Punjab and Haryana burn millions of tons of wheat straw, creating the infamous winter smog that chokes North India. But at Trident's paper mills, that same agricultural waste becomes premium copier paper, making the company the world's largest wheat straw-based paper manufacturer. It's a business model that turns environmental liability into profit—purchasing agro-waste from over 100,000 farmers annually while producing paper without cutting a single tree.

The numbers tell a story of staggering scale. Revenue of ₹6,951 crores. Manufacturing facilities that span 28 million square feet. Products sold in over 100 countries. The largest terry towel manufacturer globally. The second-largest home textile exporter from India. And behind it all stands Rajinder Gupta, the "Dhirubhai Ambani of Punjab"—a first-generation entrepreneur who built this empire from scratch in the heartland of India's Green Revolution.

But here's what makes Trident fascinating for students of business history: This isn't a story of software disruption or platform economics. It's old-school manufacturing excellence executed with surgical precision—vertical integration taken to its logical extreme, where the company controls everything from spinning yarn to generating its own power from industrial waste. In an era where asset-light models dominate business school case studies, Trident went the opposite direction, betting everything on owning the entire value chain.

The journey from Abhishek Industries—a small fertilizer plant started in 1985—to today's Trident Limited reads like a playbook for emerging market manufacturing. It's about timing liberalization perfectly, scaling through aggressive capital deployment, and finding competitive advantage in the most unlikely places. When global retailers like Walmart, Target, and Macy's needed a supplier who could deliver millions of towels with consistent quality at competitive prices, they found their answer in the wheat fields of Punjab.

This episode unpacks how a ninth-grade dropout built one of India's most successful manufacturing conglomerates, why vertical integration still matters in the age of outsourcing, and what Trident's story tells us about the future of Indian manufacturing. We'll explore the strategic pivots—from chemicals to textiles, the audacious merger that created the world's largest terry towel facility, and the sustainability innovations that turned agricultural waste into competitive advantage.

The themes that emerge are timeless: How do you compete globally from an emerging market? Can manufacturing excellence alone create lasting moats? What happens when family businesses professionalize? And perhaps most intriguingly—in a world obsessed with capital efficiency, is there still room for the capital-intensive, vertically integrated manufacturing model that Trident represents?

II. The Rajinder Gupta Origin Story

The year is 1969, and fourteen-year-old Rajinder Gupta walks out of his ninth-grade classroom in Punjab for the last time. His father, a small-time cotton dealer in the local mandi, needs help with the family business. Education is a luxury the family cannot afford. In the hierarchical world of Punjab's agricultural economy, the Guptas occupy a precarious middle ground—not farmers, not big traders, just intermediaries trying to make ends meet in the volatile cotton trade.

Young Rajinder's first job pays ₹30 per day—roughly what a cup of coffee costs in today's urban India. He makes cement pipes by hand, molds candles in the sweltering Punjab heat, and learns the only MBA curriculum that matters in the bazaars of North India: how to stretch every rupee, how to read people, and how to spot opportunity where others see only struggle. These early years in the informal economy become his Harvard Business School, teaching lessons no classroom could provide. The Punjab of the 1970s and early 1980s presents a unique paradox in Indian economic history. The Green Revolution has transformed the state into India's breadbasket, but industrialization lags behind. Agricultural prosperity creates capital but few investment opportunities. It's in this environment that Rajinder Gupta, now in his mid-twenties, begins to see possibilities others miss. Born on January 2, 1959, Rajinder was the son of a very small-time cotton dealer who was forced to leave school at age 14 when he was only in ninth grade, starting his career by working odd jobs like producing cement pipes and candles for a pitiful salary of Rs 30 per day.

The transformation from daily wage laborer to entrepreneur doesn't happen overnight. For years, Gupta works in the informal economy, learning the rhythms of North Indian business—the importance of relationships, the art of managing working capital when banks won't lend to you, the delicate balance between aggression and patience that defines successful entrepreneurship in emerging markets. He watches traders make fortunes in commodities, observes how the big textile mills in Ludhiana operate, and most importantly, understands the gap between what Indian manufacturers produce and what global markets demand.

In 1985, Rajinder made the decision to launch his own business after years of hard labour, establishing Abhishek Industries, his first-ever fertiliser production facility, with an initial investment of INR 6.5 crores. The choice of fertilizers isn't random—it's the height of the Green Revolution, and Punjab's farmers are consuming massive quantities of chemical inputs. But what makes this move audacious is the scale of ambition relative to resources. Six and a half crores in 1985 is serious money, especially for someone with Gupta's background. Where does it come from? Years of savings, borrowed funds from the informal money market, and the kind of leveraged bet that defines first-generation entrepreneurs.

The comparison to Dhirubhai Ambani isn't merely flattery—it's structurally accurate. First-generation self-made successful entrepreneur Rajinder was now being referred to as Punjab's Dhirubhai Ambani. Like Ambani, Gupta emerges from the trading community, understands commodity businesses intimately, and possesses an almost reckless appetite for scale. Both men share another crucial trait: the ability to navigate India's pre-liberalization economy, with its license raj, capital controls, and bureaucratic maze that could destroy businesses overnight.

But here's where Gupta's story diverges from the typical rags-to-riches narrative. He doesn't just want to build a business; he wants to industrialize Punjab. In the early years of the great Indian economic liberalisation when India had stepped on the economic accelerator, a young, first-generation entrepreneur, Padma Shri Rajinder Gupta, sowed the first seeds of industry on the fertile lands of Punjab. It was the birth of Trident Group. The group began with a solitary unit making high-quality yarn.

The early struggles are brutal. The fertilizer business faces commodity price volatility, seasonal demand, and competition from established players with government connections. Banks are skeptical of lending to someone without pedigree or collateral. Suppliers demand upfront payment while customers expect credit. It's the classic working capital squeeze that kills most Indian SMEs. But Gupta navigates these challenges with a combination of operational excellence and financial jugglery that would make any private equity professional envious.

What sets Gupta apart in these formative years is his understanding that manufacturing, not trading, creates lasting value. While his contemporaries in Punjab are content with agricultural trading or small-scale industries, he's thinking about global competitiveness. He studies successful textile exporters from Tirupur and Ludhiana, understands why Taiwan and South Korea are winning in global markets, and realizes that India's moment is coming.

The decision to pivot from chemicals to textiles in the late 1980s becomes the defining moment of his career. It's not abandoning the fertilizer business—that continues to generate cash flow—but recognizing that textiles offer something chemicals don't: a pathway to global markets, unlimited scale potential, and the ability to leverage India's inherent advantages in cotton production and low-cost labor.

Under his strategically perfect management, the group has grown at the rate of over 30% annually and has gone on to become one of the largest yarn spinners in India, leading global manufacturers of terry towel and world's largest wheat straw based paper manufacturers. This 30% annual growth rate over multiple decades is the kind of compounding that creates empires. But in 1985, standing in his first fertilizer plant in Punjab, even Rajinder Gupta couldn't have imagined he was laying the foundation for what would become a ₹14,000 crore global manufacturing giant.

III. Building the Foundation: Yarn to Terry Towels (1990-2000)

April 18, 1990. The Berlin Wall has just fallen, India is on the brink of economic crisis, and in the industrial town of Barnala, Punjab, a new company is formally incorporated: Abhishek Industries Limited. Named after Gupta's son, the company represents a generational bet on India's manufacturing future at precisely the moment when the country's economic model is about to undergo radical transformation.

The timing couldn't be more dramatic. Within a year, India would face its worst balance of payments crisis, Manmohan Singh would liberalize the economy, and suddenly, Indian manufacturers would have access to global markets—and face global competition. For Gupta, who had spent five years building his fertilizer business in the closed economy, this is both terrifying and exhilarating. The rules of the game are about to change completely. Trident Limited, formerly known Abhishek Industries Limited was incorporated on April 18, 1990. The company implements its first major project immediately—a yarn spinning unit in collaboration with Punjab State Industrial Development Corporation (PSIDC) with an installed capacity of 24,960 spindles. With a modest beginning of 17,280 spindles of yarns, the group today exports to over 100 countries emerging as one of the largest integrated home textile manufacturer in the world.

The textile opportunity in liberalizing India is massive but treacherous. On one hand, the dismantling of the Multi-Fibre Arrangement promises unlimited access to global markets. On the other, Indian manufacturers must now compete with China, Bangladesh, and Vietnam without the protection of quotas. Gupta's response is characteristically bold: rather than compete on price alone, he'll build scale and integration that rivals can't match.

The Barnala facility becomes the laboratory for this strategy. Like a deep-rooted 36-year-old tree at our Barnala plant and its countless leaves, Trident, with a formidable global presence, has innumerable stories to tell. Located in the heart of Punjab's cotton belt, the plant offers proximity to raw materials and access to skilled textile workers. But what makes Barnala special isn't geography—it's the systematic approach to building manufacturing capabilities from first principles.

Trident Ltd., part of TridentGroup, started as an agro-based manufacturer in 1990 in Punjab. The group as a whole diversified and expanded manifold, giving way to businesses based on sustainable growth. Under the dynamic leadership of Mr. Rajinder Gupta, its Chairman, the TridentGroup continues to grow, overcoming fresh challenges, expanding boundaries and creating new opportunities for itself. From its humble beginnings in the 1990s, the group has come a long way and made its mark in the global market. Started as a manufacturer of cotton yarns, Trident identified an opportunity in terry towels in 1998.

The pivot to terry towels in 1998 represents a masterclass in strategic thinking. While everyone in Indian textiles is chasing the apparel export boom, Gupta sees a different opportunity. Terry towels—the thick, absorbent towels used in bathrooms worldwide—offer several advantages: less fashion risk than apparel, longer product cycles, higher barriers to entry due to specialized looms, and most crucially, the ability to build lasting relationships with global retailers who value consistency over novelty.

The early partnerships are hard-won. American and European buyers are skeptical of Indian manufacturers' ability to deliver consistent quality at scale. Gupta's response is to over-invest in quality control, bringing in international consultants, installing testing equipment that costs more than entire factories in Bangladesh, and creating a culture of zero-defect manufacturing that seems excessive for a commodity product. But he understands something his competitors don't: in home textiles, trust is everything. One bad shipment can destroy years of relationship building.

By the late 1990s, the company is gaining traction. Small orders from second-tier American retailers turn into larger contracts. European buyers, impressed by the quality consistency, begin to place trial orders. But the real validation comes when major retailers start to notice. Thanks to its dedicated focus and sustained investments, the company has today emerged as one of the largest manufacturers of terry towels working with global retail brands across the globe like Ralph Lauren, Calvin Klein, JC Penney, IKEA, Target, Wal-Mart, Macy's, Kohl's, Sears, Sam's Club, Burlington, etc.

The competition during this period is fierce. Welspun, led by the Goenka family, is already establishing itself as India's home textile giant. Alok Industries, before its eventual collapse, is aggressively expanding capacity. Indo Count, Vardhman, and others are all chasing the same opportunity. What differentiates Trident is its approach to vertical integration—while others are content to be converters (buying yarn and making finished products), Gupta insists on controlling the entire value chain from cotton to retail shelf.

This integration strategy requires massive capital investment at a time when Indian interest rates are in double digits. The company leverages every possible source of funding—term loans from development financial institutions, working capital from banks, and crucially, advance payments from customers who are willing to support a reliable supplier. It's financial engineering at its most creative, turning the company's balance sheet into a pretzel to fund growth.

The technology acquisitions during this period lay the foundation for future dominance. State-of-the-art looms from Europe, dyeing equipment from Italy, and perhaps most importantly, Enterprise Resource Planning (ERP) systems that allow real-time tracking of production—unusual for an Indian textile company in the 1990s. Each acquisition is strategic, aimed not just at increasing capacity but at building capabilities that competitors will struggle to replicate.

By 2000, Abhishek Industries has transformed from a small yarn spinner into a serious player in home textiles. Annual revenues cross ₹100 crores, the company employs over 2,000 people, and most importantly, it has established relationships with global retailers that will become the foundation for explosive growth in the coming decade. The stage is set for the great expansion that will transform a Punjab textile company into a global manufacturing powerhouse.

IV. The Great Expansion: Scaling Manufacturing (2000-2010)

The millennium opens with Y2K fears proving unfounded, the dot-com bubble bursting, and in Barnala, Punjab, something far more tangible taking shape: one of the most aggressive manufacturing expansions in Indian corporate history. During the year 2003, ABIL expanded all its core business with an additional outlay of about Rs 9120 million. It was in the advanced stage of implementation of a Rs 3000 million expansion in Textiles, which will be operational by July 2004. A capacity of 100 million pieces per annum and a corresponding modernisation and expansion of spinning operation, the unit will among the top 5 manufacturers in the world.

To understand the audacity of this expansion, consider the context. Nine thousand crores in 2003 money is staggering—it's larger than many IPOs, more than most Indian companies' entire market capitalization, and represents a bet-the-company move for a business that's barely a teenager. But Gupta sees what others don't: the global home textile market is about to explode, and whoever has capacity when demand surges will capture market share that might never be available again.

Also the company has undertaken expansion in Pulp & Paper, Chemical Recovery & Co-generation at a capital outlay of Rs 6120 million, which will be fully operational by early 2006. This isn't just adding more looms—it's building an entire ecosystem. The paper business, using wheat straw as raw material, solves multiple problems simultaneously. It provides a revenue stream uncorrelated with textiles, creates a use for agricultural waste that farmers would otherwise burn, and most brilliantly, generates chemicals and energy as byproducts that can be used in textile operations.

The wheat straw innovation deserves its own Harvard Business School case study. While the world debates carbon credits and sustainability, Gupta is building a business model that's environmentally sustainable not because it's fashionable, but because it's profitable. Farmers, who traditionally burn wheat straw causing massive air pollution, now have a buyer. The company gets raw material at a fraction of wood pulp cost. The paper produced commands premium pricing as eco-friendly. And the entire operation generates power from waste, reducing energy costs across the manufacturing complex.

The vertical integration playbook reaches its apotheosis during this period. Consider the value chain: cotton purchased directly from farmers is spun into yarn in Trident's own spinning mills. That yarn is woven into terry towel fabric on Trident's looms. The fabric is dyed and processed using chemicals produced in Trident's own chemical plants. The entire operation runs on power generated from agricultural waste and industrial byproducts. Even the water used is recycled multiple times. It's a closed-loop system that would make Toyota's production engineers weep with joy.

But scale without quality is meaningless in global markets. The company invests heavily in what seems like overkill—testing laboratories that can detect color variations invisible to the human eye, quality control systems that track every meter of fabric through dozens of checkpoints, and training programs that turn farmers' children into world-class textile technicians. The rejection rate at Trident's facilities drops below 2%—extraordinary for Indian manufacturing at the time.

The timing of this expansion proves prescient. The removal of textile quotas in 2005 under the Agreement on Textiles and Clothing opens floodgates of demand. Suddenly, retailers who were forced to source from multiple countries to fill quotas can consolidate suppliers. They need partners who can deliver millions of pieces with consistent quality, on-time delivery, and competitive pricing. Trident, with its newly expanded capacity, is perfectly positioned.

The customer acquisition strategy during this period is textbook relationship selling. Rather than competing on price alone, Trident positions itself as a solutions provider. When Walmart needs a supplier who can handle volatile order patterns, Trident's massive capacity provides flexibility. When Target demands sustainable sourcing, the wheat straw story resonates. When European retailers require complex compliance certifications, Trident's sophisticated systems deliver. Each customer requirement becomes an opportunity to deepen the relationship.

Chemical synergies from the expanded operations create unexpected advantages. The company becomes a major manufacturer of industrial and battery-grade sulphuric acid in Northern India, with byproducts from paper manufacturing feeding into chemical production. These chemicals, in turn, support textile processing, creating cost advantages that pure-play textile manufacturers cannot match. It's the kind of complex, multi-business synergy that management consultants dream about but rarely see executed successfully.

The financial engineering required to fund this expansion is equally impressive. The company taps every available source of capital—term loans, working capital facilities, export credit, and creative structures like build-operate-transfer arrangements for power plants. The debt-to-equity ratio stretches to levels that would concern any prudent banker, but the cash flow from operations keeps lenders confident. It's leveraged growth at its most aggressive, reminiscent of the LBO boom but applied to manufacturing rather than financial engineering.

By 2010, the transformation is complete. From a single-product yarn manufacturer, Trident has evolved into an integrated manufacturing conglomerate. Revenues have grown from ₹100 crores to over ₹2,000 crores. The company employs over 5,000 people directly and supports thousands more through farmer partnerships. Most importantly, it has achieved what seemed impossible: becoming a globally competitive manufacturer from India's hinterland, competing successfully against Chinese scale, Bangladeshi costs, and Vietnamese efficiency.

The expansion also creates organizational challenges that will define the next phase of growth. Managing multiple businesses—textiles, paper, chemicals, and power—requires different skills than running a focused operation. The family-run business must professionalize, bringing in outside talent while maintaining entrepreneurial agility. These tensions between scale and flexibility, family control and professional management, will shape Trident's evolution in the coming decade.

V. The Trident Corporation Merger & Global Ambitions (2014)

March 14, 2014. The Punjab and Haryana High Court's wood-paneled courtroom sees little drama as judges approve what appears to be a routine corporate scheme of arrangement. During the year 2014 year, the Honble High Court for the states of Punjab and Haryana at Chandigarh approved Scheme of Amalgamation of Trident Corporation Limited with the Company vide its Order dated March 14, 2014. But this merger is anything but routine—it's the culmination of a strategic masterstroke that will create the world's largest integrated terry towel manufacturing facility and fundamentally reshape India's position in global home textiles.

The asset at the heart of this merger sits in Budni, Madhya Pradesh—a location so unexpected that logistics consultants initially advised against it. To further enhance its global leadership in terry towels, TridentGroup has set up the world's largest and the most modern manufacturing plant at Budhni with a capacity to manufacture 120 tonnes of terry towel fabric per day. It invested Rs. 1,191 crores in 2013-14 on the Budhni facility for what has today become the world's largest terry towel plant. This investment and capacity is in addition to Trident's already existing plant in Punjab with a daily capacity of 100 tonnes of terry towel fabric. The combined capacity will position Trident among the world's largest manufacturers of terry towels.

The strategic rationale behind the merger transcends mere capacity addition. Trident Corporation Limited brought with it not just manufacturing assets but established relationships with global retailers, proven operational systems, and most crucially, a management team that had built these capabilities independently. Merging two successful operations is always harder than building from scratch—corporate cultures clash, systems conflict, and egos bruise. But Gupta navigates these challenges with the same operational excellence he brings to manufacturing.

The Budni facility itself is a marvel of industrial engineering. The Budhni terry towel project, conceived in the last quarter of 2012, and started commercial production in the first quarter of 2014. The plant is currently operating at 30 per cent of the installed capacity and is expected to reach peak levels of production by March 2015. Spread across hundreds of acres, it's designed not just for current production but for future expansion. Wide corridors between production units allow for easy material flow. Automated guided vehicles reduce human handling. The entire facility is designed around lean manufacturing principles, with minimal work-in-progress inventory and just-in-time production capabilities.

Creating manufacturing scale unprecedented in Indian textiles requires rethinking every assumption. Traditional textile mills are labor-intensive, with workers manually handling fabric at multiple stages. Budni automates wherever possible—not to reduce labor costs, which are already low in India, but to ensure consistency. When you're producing 300,000 towels daily for Walmart, even a 0.1% variation in quality can result in entire shipments being rejected.

The technology deployed at Budni would be impressive anywhere, but in rural Madhya Pradesh, it's revolutionary. European looms with electronic jacquard systems can switch between patterns without stopping production. Italian dyeing machines ensure color consistency across millions of pieces. Israeli drip irrigation systems water the campus's gardens while recycling process water. It's a first-world factory in a third-world location, creating jarring contrasts that define modern India.

Building export capabilities at this scale requires more than just manufacturing prowess. The company establishes design studios in New York and London, staffed with designers who understand Western aesthetics and can translate retail trends into production specifications. Quality control labs are certified by international bodies, capable of testing to standards that exceed customer requirements. The logistics operation rivals that of dedicated freight forwarders, coordinating shipments across multiple continents with military precision.

The global customer relationships that come with the merger transform Trident's market position. Where previously the company was one of many suppliers, it now becomes a strategic partner to the world's largest retailers. Calvin Klein, H&M, JCPenney, Macy's, Walmart to name a few are Trident's major clients. These aren't just vendor relationships but partnerships where Trident's teams work directly with retailers on product development, helping design private label collections and suggesting innovations that reduce costs while improving quality. The scale achieved through the merger is staggering. With this inauguration, the installed capacity of Trident has increased to 688 looms capable of producing 90,000 TPA of terry towels, making Trident the largest manufacturer of terry towels in the world. Trident's Budhni manufacturing complex is spread over an area of 800 acres, which already houses the spinning and terry towel unit. The combined capacity from Punjab and Madhya Pradesh facilities positions Trident not just as a large player but as the global leader in terry towel manufacturing.

But becoming a supplier to global retailers requires more than just capacity. The certification and compliance requirements alone would make most manufacturers give up. BSCI audits, OEKO-TEX standards, ISO certifications, customer-specific quality protocols—each with its own documentation requirements, audit schedules, and compliance costs. Trident doesn't just meet these standards; it exceeds them, creating what amounts to a regulatory moat that smaller competitors cannot cross.

The cultural transformation required to serve global customers is equally profound. The reason is Trident is today the world's largest terry towel manufacturer, which brings economies of scale. The group enjoys long association with world renowned retailers for supply of terry towels. With the addition of sheeting to its product range, It can now offer a complete solution to its customers. Thanks to the large manufacturing capacities created, the company has the capacity to execute large-size orders. Factory workers who've never left Madhya Pradesh must understand quality standards set in Bentonville, Arkansas. Production planning must account for Black Friday sales in America, Boxing Day in Britain, and Chinese New Year across Asia.

The financial impact of the merger exceeds all projections. The world's largest terry towel plant opened by Trident comprises 300 looms and will add about Rs. 1,800 crores to its annual revenue. But revenue is only part of the story. The operational synergies—shared procurement, unified logistics, cross-selling to customers—create value that doesn't show up immediately in financial statements but compounds over time.

The post-merger integration, often where deals fail, proceeds with remarkable smoothness. Systems are unified, cultures are merged, and redundancies are eliminated without the usual disruption. The secret? Both organizations share the same DNA—the relentless focus on operational excellence, the obsession with customer service, the understanding that in manufacturing, execution is everything. It helps that the merger is more acquisition than combination, with Trident's established culture absorbing the new operations rather than trying to blend two equals.

By 2015, the integration is complete, and the results speak for themselves. Trident has become what Gupta envisioned—not just the largest terry towel manufacturer but a one-stop shop for home textiles. The natural progression for it would be to extend its product offering in home textiles to cater to the requirements of its global customers, making it a one stop shop for home textiles. Accordingly, Trident is making its next big investment for manufacture of bed sheets, which will again be set up in Budhni. Global retailers can now source towels, bed sheets, and other home textiles from a single supplier, simplifying their supply chains while ensuring consistent quality across product categories.

VI. Modern Manufacturing & Sustainability Innovation (2015-Present)

The conference room at Trident's Ludhiana headquarters buzzes with an energy unusual for a traditional manufacturing company. Young engineers discuss artificial intelligence applications for quality control. Sustainability experts debate carbon sequestration strategies. Digital transformation consultants present Industry 4.0 roadmaps. This is 2015, and Trident is reimagining what it means to be a manufacturer in the 21st century. In 2015, initiated composite textile project with bed sheeting unit (500 looms) and integrated spinning unit (189,696 spindles) at total cost of Rs 16,669 million. This isn't just capacity expansion—it's a complete reimagining of what an Indian textile manufacturer can be. The scale is breathtaking: a single project costing more than many companies' entire market capitalization, aimed at creating integrated manufacturing capabilities that rival anything in the world.

The sustainability story that emerges during this period transforms from nice-to-have to core competitive advantage. The company is the World's largest wheat straw-based paper manufacturer. But it's the ecosystem around this that's remarkable. Paper product uses wheat straw not wood pulp, empowers over 1 lakh domestic farmers annually by purchasing agro-waste directly. Each harvest season, Trident's procurement teams fan out across Punjab and Haryana, creating a supply chain that turns environmental liability into economic opportunity.

The innovation doesn't stop at raw materials. During the year 2021-22, Company commenced the production of Detergent Powder under Chemical Segment in Budni, Madhya Pradesh effective from August 2, 2021 with a capacity of 10 Metric Ton per day. This diversification into consumer chemicals might seem random, but it's strategically brilliant—leveraging existing chemical production capabilities while creating products that can be bundled with textile offerings to institutional customers.

It expanded Yarn Segment with the addition of 61,440 Spindles & 480 Rotors w.e.f. July 27, 2021, part of a broader modernization that includes digital transformation across operations. The company implements SAP across all facilities, creating real-time visibility into production, inventory, and quality metrics. IoT sensors on looms track efficiency and predict maintenance needs. AI-powered quality control systems detect defects that human inspectors might miss.

The renewable energy investments during this period are equally ambitious. It commissioned 7.6 MW Solar Power Plant at Budhi, Madhya Pradesh for captive use. But this is just the beginning. Further the capacity of captive Co-gen power plant and Solar Power plant has increased by 16.3 MW and 10.56 MWp respectively in 2024. The company generates captive power of 50 MW using by-products like black liquor effluent and biomass along with coal, creating an energy ecosystem that reduces both costs and carbon footprint.

The Industry 4.0 transformation goes beyond technology to reshape the entire operating model. To be future-ready, Trident has undergone a digital transformation to become an Industry 4.0 company with smart people, smart factories, and smart technologies across the spectrum. Predictive analytics optimize production schedules. Machine learning algorithms forecast demand patterns. Blockchain technology ensures supply chain transparency for customers increasingly concerned about sourcing ethics.

Building the myTrident consumer brand represents another strategic pivot. World-class products made affordable for Indian customers both online and offline. And become a household name in home fashion in India. After decades of being a B2B supplier to global retailers, the company is going direct to Indian consumers, leveraging its manufacturing scale to offer premium products at accessible prices. It's a move that requires different capabilities—brand building, retail distribution, consumer marketing—but offers higher margins and reduced customer concentration risk.

The ESG initiatives during this period go beyond compliance to create genuine competitive advantage. The wheat straw paper business alone prevents millions of tons of CO2 emissions from agricultural burning. Water recycling systems reduce consumption by 40%. Employee welfare programs, including healthcare and education for workers' children, create loyalty that translates into lower turnover and higher productivity. These aren't CSR checkbox exercises but strategic investments that improve both sustainability and profitability.

The recent expansion continues at breakneck pace. During the year 2023-24, Company expanded the production capacity of its Bed Linen segment by 55,000 meters per day, Bath Linen Segment by installing 42 Looms and Yarn Segment by installing 1,89,696 spindles. FY 2023-24 capex of Rs 785 crore, added 42 looms (7200 tons/year towel capacity), installed 189,696 spindles, increased sheeting capacity by 10.8 million meters/year. This relentless capacity addition might seem risky in a cyclical industry, but Trident's thesis is simple: when the next upturn comes, those with capacity will capture disproportionate value.

The carbon footprint reduction initiatives are particularly innovative. Solar panels cover factory roofs. Biomass from agricultural waste powers boilers. Even the transportation fleet is being electrified, with electric vehicles for internal logistics and plans for hydrogen-powered trucks for long-distance transport. The goal isn't just carbon neutrality but carbon negativity—sequestering more carbon than the company emits.

By 2024, the transformation is remarkable. What began as a traditional textile manufacturer has evolved into a technology-enabled, sustainability-focused industrial conglomerate. The company that once struggled to get bank loans now has global investors analyzing its ESG metrics. The facilities that started with manual looms now use AI for quality control. The business that began by copying others' designs now sets trends in global home fashion.

VII. Business Segments Deep Dive

Textiles Empire

Stand on the production floor of Trident's Budni facility at 6 AM, and you witness industrial poetry in motion. Kilometers of yarn snake through state-of-the-art looms, transforming into terry towels at a rate that defies comprehension—one towel every second, 90,000 towels per day, 30 million towels per year from this facility alone. This is what it means to be the largest manufacturer of terry towels in the world, serving customers across 100 countries.

The textile business breaks down into three distinct but synergistic segments. Yarn forms the foundation—with installed capacity of 5.55 lakh spindles and 5,500 rotors capable of manufacturing 115,200 tonnes per annum. The yarn isn't just raw material for internal consumption; it's a profit center in its own right, with sophisticated products like compact yarn, core-spun yarn, and specialized blends commanding premium prices in export markets.

The terry towel business is the crown jewel. It is the largest player in terms of terry towel capacity & one of the largest players in home textile space in India. With 688 looms across facilities, the company produces everything from basic institutional towels for hotels to luxury bath sheets for high-end retailers. The product range is staggering—different weights, weaves, colors, and finishes, each optimized for specific customer requirements and price points.

Bed sheets represent the newest growth vector. The Budni facility's 500 looms produce 43.2 million meters annually, but this understates the complexity. Thread counts from 200 to 1000, percale and sateen weaves, printed and solid designs, fitted and flat sheets—each SKU requires different production parameters, inventory management, and quality control protocols. It's manufacturing complexity that would break most companies, but Trident's systems handle it with remarkable efficiency.

The financial performance of the textile segment tells a story of consistent execution despite commodity volatility. Yarn revenue up 2.52% to Rs 3262.08 crore, towel business up 4.65% to Rs 2594.73 crore, bedsheets up 28.24% to Rs 1297.6 crore. The bed sheet growth is particularly impressive, validating the strategic decision to enter this segment and suggesting significant market share gains.

It is also the second-largest exporter from India for home textile products. This export focus provides natural currency hedging—when the rupee weakens, margins expand. But it also requires sophisticated risk management, with forward contracts, currency options, and natural hedges through import-export matching. The company's treasury function operates like a small investment bank, managing billions in foreign exchange exposure.

Paper & Chemicals

The paper mill at Barnala defies every stereotype about Indian manufacturing. Clean, efficient, and technologically sophisticated, it transforms what farmers consider waste into products that compete with virgin wood pulp paper in quality. It is No. 1 in North India in the branded copier segment. But the real story isn't market share—it's the business model innovation that makes this possible.

The wheat straw procurement system is a masterpiece of supply chain management. During harvest season, thousands of collection centers spring up across Punjab and Haryana. Farmers who previously burned straw, contributing to Delhi's winter pollution, now have buyers at their doorstep. The company procures over 2 lakh tons of wheat straw annually, creating a win-win that's both profitable and environmentally sustainable.

Its paper segment has the Highest Operating Margin among key listed players in India. This isn't accident but design. While competitors struggle with wood pulp costs and environmental regulations, Trident's raw material is essentially free after accounting for the environmental benefits. The chemical recovery systems extract maximum value from every input, creating multiple revenue streams from what others consider waste.

The chemical business leverages byproducts from paper manufacturing brilliantly. The company is the major manufacturer of industrial and battery-grade sulphuric acid in the Northern regions of India. Black liquor from paper production becomes fuel for power generation. Chemicals recovered from the pulping process are refined and sold to industrial customers. It's circular economy principles applied with ruthless efficiency.

The recent entry into detergent manufacturing seems incongruous until you understand the synergies. The same chemical processing capabilities that support paper and textile operations can produce consumer chemicals. The distribution infrastructure built for paper can handle detergents. The relationships with institutional customers—hotels, hospitals, schools—create cross-selling opportunities. It's diversification that builds on existing capabilities rather than requiring new ones.

Energy & Integration

The power plant at Budni doesn't look like much—a collection of boilers, turbines, and generators tucked behind the main manufacturing facilities. But this 50 MW captive power generation capability is the hidden enabler of Trident's cost competitiveness. When competitors pay ₹7-8 per unit for grid power, Trident generates its own at ₹3-4 per unit using waste products that others would pay to dispose of.

The integration goes deeper than just power generation. Steam from the power plant drives textile processing. Waste heat from one process becomes input for another. Water used in cooling is recycled for textile processing. It's thermodynamic efficiency that would make a chemical engineer weep with joy—every joule of energy extracted, every drop of water recycled, every waste product monetized.

The recent solar investments add another layer to the energy strategy. With over 18 MW of solar capacity across facilities, the company reduces its carbon footprint while locking in energy costs for decades. The economics are compelling—solar power at ₹2.50 per unit with 25-year visibility versus grid power at ₹7+ per unit with annual escalation. It's financial engineering through renewable energy.

But the real genius of the energy strategy is how it enables the core business. Textile manufacturing is energy-intensive—spinning, weaving, processing, and finishing all require significant power. By controlling energy costs, Trident can compete on price while maintaining margins. It's a structural advantage that's nearly impossible for smaller competitors to replicate.

VIII. Financial Performance & Market Position

The numbers tell a story, but not the one you might expect. FY2024 consolidated revenue of Rs 6808.83 crore, up 7.53% from Rs 6332.26 crore in FY2023. In isolation, 7.5% growth seems pedestrian. But context matters. This growth comes during a period of global demand weakness, inventory destocking by major retailers, and crushing input cost inflation. That Trident grew at all, let alone profitably, speaks to execution excellence that numbers alone cannot capture.

The company has delivered a poor sales growth of 8.13% over past five years. "Poor" is the market's judgment, but is it accurate? During these five years, the company has invested over ₹5,000 crores in capacity expansion, creating manufacturing capabilities that won't fully contribute to revenue for another 2-3 years. It's the J-curve of manufacturing—massive upfront investment followed by years of steady returns. Judging Trident's five-year revenue CAGR without considering the capacity under construction is like evaluating a construction project before the building is complete.

The segment performance breakdown reveals strategic choices paying off. The 28.24% growth in bedsheets to Rs 1297.6 crore validates the diversification strategy. This isn't just market growth—the global bedsheet market grows at 3-4% annually. This is market share capture, customers shifting orders from competitors to Trident, drawn by the integrated manufacturing model that ensures consistent quality and reliable delivery.

Margin pressures tell their own story. Stock is trading at 3.08 times its book value, suggesting the market sees value despite near-term headwinds. But the margin compression has structural and cyclical components that need untangling. Structurally, the shift toward value-added products means higher absolute margins but lower percentage margins—selling a ₹1,000 bedsheet set at 15% margin generates more profit than selling ₹500 of yarn at 20% margin. Cyclically, cotton price volatility and energy cost inflation have squeezed margins across the textile industry.

The capital allocation decisions during this period deserve scrutiny. FY 2023-24 capex of Rs 785 crore seems aggressive for a company with ₹6,800 crore revenue. But break it down: 42 looms adding 7,200 tons annual towel capacity, 189,696 spindles for yarn production, 10.8 million meters annual sheeting capacity. At current utilization and pricing, these investments should generate ₹1,500-2,000 crore in incremental revenue at steady state. The payback period is 4-5 years—aggressive but not reckless.

Export versus domestic market dynamics add complexity. Exports account for roughly 54% of revenue, providing dollar earnings that hedge against rupee depreciation. But export markets are increasingly competitive, with Bangladesh and Vietnam leveraging lower labor costs to undercut Indian manufacturers. The domestic market offers higher margins but requires different capabilities—brand building, distribution, consumer marketing—that Trident is still developing. Competition analysis reveals both challenges and opportunities. Welspun Living · Mkt Cap: 11,117 Crore (down -34.4% in 1 year) · Revenue: 10,269 Cr · Profit: 547 Cr · The company has delivered a poor sales growth of 9.36% over past five years. Welspun, despite being smaller by market cap than Trident, generates higher revenue, suggesting better asset utilization but lower margins. Vardhman Textiles Ltd is a leading vertically integrated textile company with a strong presence in yarn, fabric, and garments. It serves both domestic and international markets, benefiting from economies of scale and a diversified product portfolio.

The top 10 textile industry in India are: Arvind Limited, Vardhman Textiles Ltd, Welspun India, Trident, Bombay Dyeing, KPR Mills, Alok Industries Ltd, J C T Ltd, Lakshmi Mills, Fabindia and Grasim Industries. But market positions are fluid. The company has recorded its highest ever quarterly revenues in Q2FY24 at Rs 2,542 crore growing 19 per cent YoY. Export revenues for Welspun saw a growth of 22 per cent YoY, with its innovation products driving the sales with a growth of 67 per cent YoY. Earnings before interest, taxes, depreciation, and amortization (EBITDA) margin improved 829 bps to 15.4 per cent from 7.1 per cent in Q2FY23. Welspun's innovation-led growth strategy is yielding results that Trident must match.

The commodity cycle impact on performance cannot be ignored. Cotton prices swing 30-40% annually, energy costs have doubled in three years, and freight rates remain volatile post-pandemic. Companies that manage these cycles best—through vertical integration, hedging, or pricing power—generate superior returns over time. Trident's integrated model provides some protection, but commodity volatility remains the biggest uncontrollable risk.

The currency dynamics add another layer of complexity. With over half of revenue in dollars but costs primarily in rupees, Trident benefits from rupee depreciation. But this creates its own challenges—planning becomes difficult when a 5% currency move can swing margins by 200 basis points. The company's hedging strategy—covering 60-70% of near-term exposure while keeping longer-term exposure open—balances risk and opportunity.

Looking at valuation, Stock is trading at 3.08 times its book value. For a manufacturing company with significant tangible assets, this suggests the market values the business well above replacement cost. The premium reflects brand value, customer relationships, and operational excellence that don't appear on the balance sheet. But it also suggests limited upside unless the company can accelerate growth or expand margins.

The working capital management deserves special mention. Textile manufacturing is notoriously working capital intensive—cotton must be purchased, processed into yarn, woven into fabric, and finished into products, with payment terms that can stretch 90-120 days. Trident's cash conversion cycle has improved from 140 days to 110 days over five years, freeing up hundreds of crores for investment. It's unglamorous financial engineering that creates real value.

IX. Playbook: Lessons in Manufacturing Excellence

The Vertical Integration Masterclass

Walk through Trident's Budni complex, and you witness vertical integration taken to its logical extreme. Cotton enters at one end, finished towels exit at the other, with every step in between controlled, optimized, and monetized. It's a model that business schools teach as history—outdated in the age of outsourcing and asset-light models. Yet here it thrives, generating returns that pure-play competitors cannot match.

The integration starts before manufacturing even begins. Direct procurement from farmers eliminates middlemen, reducing costs by 5-7%. But more importantly, it ensures quality control from the very first step. When you're producing for Walmart or Target, consistency matters more than cost. One bad batch can destroy years of relationship building.

Inside the facilities, integration creates compound advantages. Yarn production generates waste that becomes raw material for non-woven products. Sizing chemicals from yarn processing are recovered and reused in fabric finishing. Steam from power generation drives textile processing. Even seemingly minor byproducts—cotton seeds, short fibers, process chemicals—find profitable uses. It's industrial symbiosis where one division's waste becomes another's input.

The financial advantages of integration multiply during commodity cycles. When cotton prices spike, pure-play towel manufacturers see margins evaporate. Trident's yarn division captures some of that value, cushioning the impact on finished goods. When yarn margins compress, value shifts to finished products. It's natural hedging through operational structure rather than financial derivatives.

But the real magic of vertical integration isn't cost—it's control. When a customer needs a specific shade of blue that matches their brand guidelines exactly, Trident controls every step from yarn dyeing to fabric finishing. When delivery schedules compress for holiday seasons, there's no negotiating with suppliers because Trident is its own supplier. When quality issues arise, traceability extends back to the specific bale of cotton. This control translates into reliability, and reliability commands premium pricing.

Sustainability as Competitive Advantage

The conference room walls at Trident's headquarters display awards and certifications—GOTS, OEKO-TEX, BCI, GRS—alphabet soup that means little to outsiders but everything to global retailers under pressure to green their supply chains. What started as compliance has evolved into genuine competitive advantage, with sustainability initiatives that generate both environmental and economic returns.

The wheat straw paper business exemplifies this approach. While competitors pay rising prices for wood pulp and face increasing environmental scrutiny, Trident turns agricultural waste into premium paper. The economics are compelling: farmers earn ₹1,500-2,000 per ton for straw they would otherwise burn, Trident gets raw material at a fraction of wood pulp cost, and North India's air gets cleaner. It's a business model that creates value for every stakeholder.

The farmer partnership program goes beyond simple procurement. Trident provides training on sustainable farming practices, facilitates access to credit, and guarantees purchase agreements that provide income stability. Over 100,000 farmers now depend on Trident for supplementary income, creating a supply chain moat that competitors cannot easily replicate. These aren't CSR initiatives but strategic investments in supply chain resilience.

Energy sustainability drives both cost reduction and competitive differentiation. The 50 MW captive power generation using agricultural and industrial waste reduces energy costs by 40% while eliminating 200,000 tons of CO2 annually. Solar installations across facilities add another layer of energy security. When European customers demand carbon-neutral products, Trident can deliver without premium pricing because sustainability is built into the operating model.

Water management in a water-stressed region like Punjab requires innovation. Trident's facilities recycle 70% of process water, use closed-loop dyeing systems that reduce water consumption by 50%, and treat wastewater to standards that exceed regulatory requirements. The treated water irrigates green belts around factories, creating micro-ecosystems that improve worker quality of life while demonstrating environmental commitment to visiting customers.

Family Business Succession

The 2012 transition when Abhishek Gupta became Managing Director while Rajinder moved to Chairman represents a masterclass in family business succession. In 2012, appointed Abhishek Gupta as Managing Director while Rajinder moved to Chairman, making Abhishek one of the youngest Managing Directors in the country. This wasn't just nepotism—it was carefully orchestrated leadership development that began years earlier.

Abhishek's preparation included formal education at Warwick University, apprenticeship across different divisions, and gradual assumption of operational responsibilities. But the real test came in managing the transition without disrupting operations or relationships. The founder's shadow looms large in family businesses, and many successions fail because the next generation either cannot escape that shadow or tries too hard to establish their own identity.

The genius of Trident's succession was maintaining continuity while enabling evolution. Rajinder remained Chairman, providing strategic guidance and maintaining key relationships, while Abhishek drove operational modernization and digital transformation. It's a model that balances respect for legacy with necessity for change—the founder's vision preserved but executed with fresh energy and contemporary methods.

The professionalization that accompanied succession strengthened rather than diluted family control. Independent directors brought governance discipline, professional managers added specialized expertise, and systematic processes replaced informal decision-making. But the family retained control over strategic direction, capital allocation, and cultural values. It's controlled professionalization—bringing in outside expertise while maintaining insider commitment.

Global Customer Acquisition

The visitor log at Trident's facilities reads like a who's who of global retail—Walmart procurement teams, Target quality auditors, Macy's design specialists. Building these relationships required more than just manufacturing capability; it demanded understanding different business cultures, meeting diverse compliance requirements, and most importantly, proving reliability over years of consistent delivery.

The Walmart relationship, built over two decades, illustrates the patient relationship building required in global B2B sales. Initial orders were small—a few containers of basic towels. But each successful delivery built trust, each quality audit passed opened doors, each on-time shipment during peak season demonstrated capability. Today, Trident is a strategic supplier, involved in product development, seasonal planning, and long-term capacity discussions.

Different customers require different approaches. European retailers prioritize sustainability certifications and supply chain transparency. American mass merchants focus on price and delivery reliability. Japanese customers demand perfect quality and precise specifications. Trident's sales organization has evolved specialized teams for each geography, with deep understanding of local requirements and relationships built over decades.

The technology infrastructure supporting global customers rivals anything in Silicon Valley. EDI integration with customer systems enables real-time order processing. RFID tracking provides shipment visibility from factory to store. Digital sampling reduces development time from months to weeks. It's the unsexy but essential plumbing that enables a manufacturer in rural India to serve retailers in Manhattan.

X. Bear vs Bull Case & Future Outlook

Bull Case: The ₹25,000 Crore Dream

The audacious target haunts every investor presentation: Target revenue of Rs. 25,000 crores by 2025 with Rs. 3,000 crores net profit. From current revenues of ₹6,800 crores, this implies nearly 4x growth in essentially one year—mathematically improbable unless you understand the capacity investments already made. The spindles installed, looms commissioned, and customer relationships built over the past five years create latent capacity that could theoretically support these numbers at peak utilization.

Global leadership positions provide structural advantages that should compound over time. In terry towels, Trident's scale allows pricing power that smaller competitors cannot match. In wheat straw paper, the company has essentially created a category where it faces no direct competition. These aren't market positions that erode overnight—they're moats built on years of investment and relationship building that become stronger with scale.

The sustainability tailwinds are real and accelerating. European legislation requiring supply chain carbon disclosure, American consumers demanding eco-friendly products, and Indian regulations on agricultural burning all play to Trident's strengths. The company hasn't just adapted to these trends; it's positioned ahead of them. When carbon border taxes eventually arrive, Trident's low-carbon manufacturing will translate into competitive advantage.

Domestic consumption growth offers a second engine for expansion. India's home textile market grows at 12-15% annually as rising incomes drive premiumization. The myTrident brand, leveraging manufacturing scale to offer premium products at accessible prices, could capture disproportionate share of this growth. It's the classic emerging market play—selling to your own rapidly growing middle class products you previously exported to developed markets.

The balance sheet strength enables aggressive expansion without dilution. With debt-to-equity below 1x and strong operating cash flows, Trident can fund growth internally. This financial flexibility becomes crucial during downturns when weaker competitors struggle with debt service and Trident can acquire assets or market share at distressed prices.

Bear Case: The Reality Check

Poor sales growth of 8.13% over past five years—this single statistic encapsulates the bear case. Despite massive capacity additions, revenue growth has barely exceeded inflation. Either the capacity is poorly utilized, suggesting operational issues, or market demand isn't materializing as expected. Neither explanation inspires confidence about achieving 4x growth.

Commodity price volatility remains the sword of Damocles hanging over textile manufacturers. Cotton prices can swing 40% in a year, energy costs have doubled in three years, and freight rates remain elevated post-pandemic. Vertical integration provides some buffer, but when input costs spike simultaneously, even integrated manufacturers see margins evaporate. The company's guidance assumes stable commodity prices—a dangerous assumption in today's volatile world.

Global trade tensions threaten the export-dependent model. The US President, Donald Trump, has announced a 25% tariff on Indian goods, effective from August 1, leading to a sharp decline in textile stocks on July 31. Textile manufacturers such as Welspun Living (6.51%), Indo Count Industries (7.44%) , Vardhman Textiles (4.57%), Gokaldas Exports (8%), Pearl Global (10.64% ) and KPR Mills (5.14%) lost between 4% and 11% after Trump's tariff and penalty threat. With potential US tariffs, European carbon border adjustments, and general protectionist sentiment, the free trade environment that enabled Trident's growth may be ending.

Competition from Bangladesh and Vietnam intensifies every year. These countries offer lower labor costs, similar quality, and in Vietnam's case, better free trade agreements. While Trident's scale and integration provide some protection, competing on cost with countries where wages are 50% lower becomes increasingly difficult. The company needs pricing power from brand or technology, neither fully established yet.

Technology disruption in textiles isn't science fiction anymore. 3D knitting eliminates cut-and-sew operations, digital printing reduces inventory needs, and direct-to-consumer models bypass traditional manufacturers entirely. While Trident invests in technology, it's essentially digitizing existing processes rather than reimagining them. A truly disruptive innovation could strand billions in traditional manufacturing assets.

The management transition risks remain unresolved. While Abhishek Gupta has proven capable, the company still depends heavily on founder Rajinder Gupta's relationships and vision. The next generation of professional managers hasn't been fully tested through a complete business cycle. Family businesses often struggle in the third generation—a risk that becomes relevant as Trident plans for the next decade.

The Balanced View

The truth, as always, lies between extremes. Trident won't achieve ₹25,000 crores revenue by 2025—the math simply doesn't work. But the company will likely grow faster than the 8% historical rate as capacity investments mature and global supply chains restructure post-pandemic. A realistic scenario sees revenue reaching ₹10,000-12,000 crores by 2027, with margins stabilizing as operational leverage kicks in.

The sustainability positioning is genuinely differentiated and will become more valuable over time. While competitors scramble to meet environmental standards, Trident has built sustainability into its business model. This isn't just marketing—it's operational advantage that translates into customer relationships and pricing power.

The domestic market opportunity is real but requires different capabilities. Building consumer brands, managing retail distribution, and competing with established players like Welspun and Indo Count in the domestic market won't be easy. But Trident's manufacturing scale provides a cost advantage that, properly leveraged, could drive market share gains.

The biggest risk isn't competition or commodity prices—it's execution. Trident has built massive capacity that needs to be utilized efficiently, customer relationships that need to be maintained and expanded, and new markets that need to be developed. It's an execution challenge that requires operational excellence across multiple dimensions simultaneously.

XI. Epilogue: The Punjab Manufacturing Story

The morning shift change at Trident's Barnala facility offers a glimpse into modern India's transformation. Young engineers with degrees from IITs work alongside farmers' children trained in Trident's skill development programs. Solar panels that power the facility sit adjacent to wheat fields that supply raw material. It's a scene that captures the convergence of agriculture and industry, tradition and technology, that defines Punjab's economic evolution.

Started in early years of Indian economic liberalization, began with single unit making high-quality yarn, became largest terry towel manufacturer and one of largest integrated home textile manufacturers globally. This journey from yarn to global leadership isn't just Trident's story—it's the story of Indian manufacturing's potential when ambition meets execution, when local entrepreneurs compete globally, when sustainability becomes competitive advantage rather than compliance burden.

What Trident represents for Indian manufacturing transcends textiles. It's proof that companies from emerging markets can dominate global industries not through labor arbitrage but through operational excellence. It demonstrates that vertical integration, dismissed by consultants as outdated, can create competitive advantages in specific contexts. Most importantly, it shows that manufacturing still matters—that making physical products efficiently and sustainably creates value that digital platforms cannot replicate.

The transformation from traders to global manufacturers reflects a broader shift in Indian entrepreneurship. The Marwari trading communities that dominated Indian business for centuries are evolving into industrialists. The skills that made them successful traders—relationship building, risk management, capital efficiency—translate into manufacturing with adaptation. Rajinder Gupta's journey from cotton trader's son to global manufacturer exemplifies this evolution.

Lessons for emerging market entrepreneurs are clear but challenging to implement. First, pick industries where emerging market disadvantages (technology, capital) matter less than advantages (cost, scale, relationships). Second, use vertical integration to overcome weak institutional infrastructure—if suppliers aren't reliable, become your own supplier. Third, turn local constraints into global advantages—Trident's wheat straw innovation emerged from Punjab's agricultural waste problem but became a global sustainability solution.

The next generation faces different challenges and opportunities. Climate change will reshape global manufacturing, creating winners and losers based on carbon efficiency rather than labor costs. Digital technologies will enable mass customization, requiring flexibility that traditional scale manufacturing cannot provide. Consumers will demand transparency and traceability that blockchain and IoT enable but also require. Abhishek Gupta and his team must navigate these transitions while maintaining the operational excellence that built Trident.

The Punjab manufacturing story that Trident embodies offers hope for India's economic transformation. If a company from landlocked Punjab can become a global leader in textiles, what's stopping entrepreneurs from Bihar, Odisha, or the Northeast? The infrastructure exists, capital is available, and global markets remain open despite protectionist rhetoric. What's needed is the entrepreneurial courage to build at scale, the operational discipline to execute consistently, and the strategic vision to see opportunities where others see only challenges.

As the sun sets over Trident's facilities, casting long shadows across the shop floor, the third shift prepares to take over. The looms will run through the night, producing towels for hotels in New York, sheets for homes in London, yarn for factories in Bangladesh. It's globalization made tangible—threads of cotton connecting Punjab's fields to the world's homes. And at the center of it all stands Trident, testament to what's possible when ambition meets execution in the heart of India.

The story isn't finished. The capacity expansions continue, new markets beckon, and challenges multiply. But for students of business history, Trident offers lessons that transcend industry or geography. It's a reminder that in business, as in life, success comes not from avoiding challenges but from converting them into opportunities. Whether Trident achieves its ambitious targets or falls short, its journey from Abhishek Industries to global manufacturing giant has already secured its place in the pantheon of Indian business success stories.

What began as one man's dream to escape poverty has evolved into an institution that employs thousands, empowers farmers, and serves customers globally. It's capitalism at its best—creating value for all stakeholders while building something that lasts beyond individual ambitions. As India seeks to become a developed nation by 2047, it will need many more Tridents—companies that combine global ambition with local roots, operational excellence with environmental responsibility, family values with professional management.

The Trident story, still being written, reminds us that manufacturing isn't just about making things—it's about making dreams tangible, one thread at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube