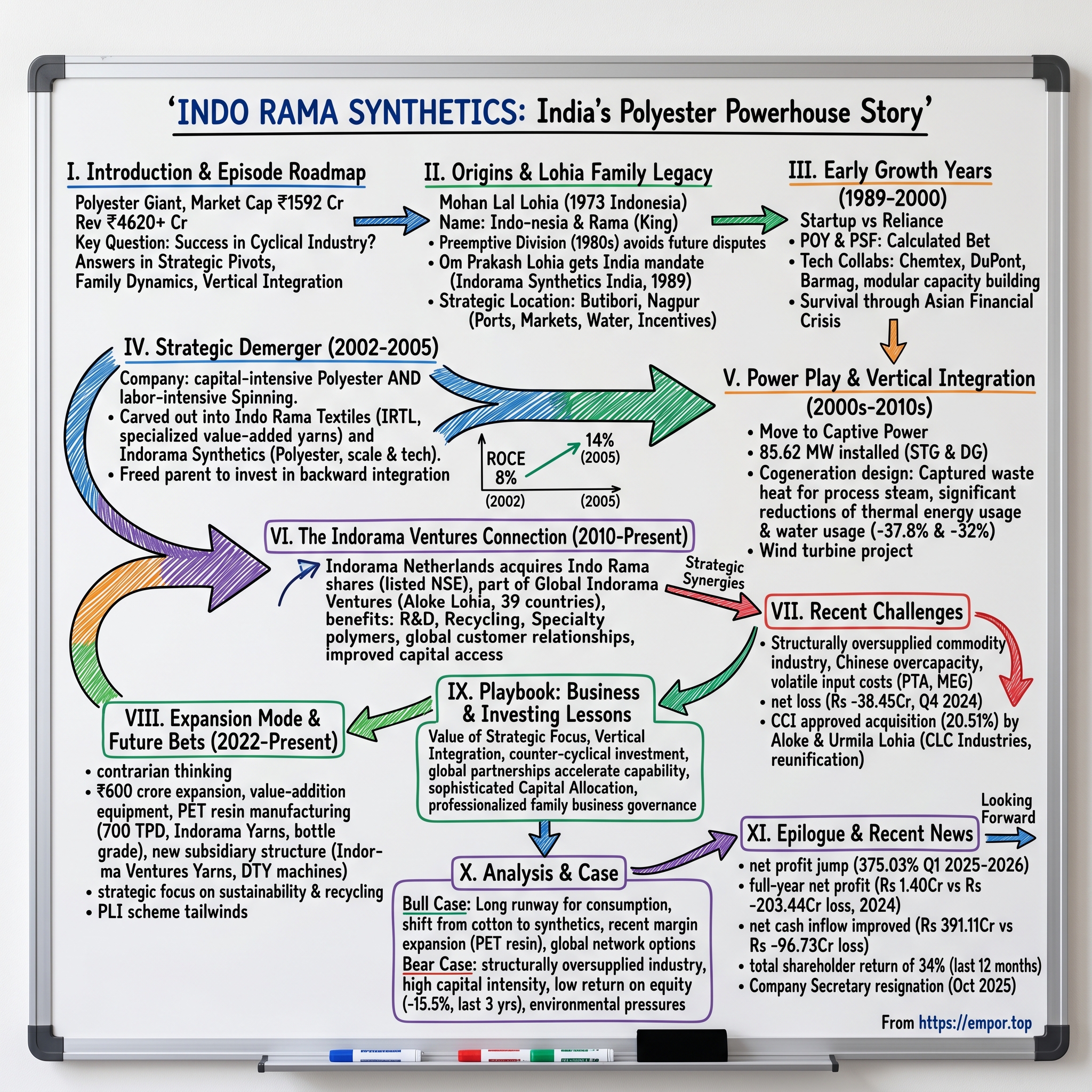

Indo Rama Synthetics: India's Polyester Powerhouse Story

I. Introduction & Episode Roadmap

In the sprawling industrial landscape of Butibori, near Nagpur, stands a testament to India's synthetic textile revolution. Indo Rama Synthetics, with its towering polymerization units and spinning facilities, represents more than just another manufacturing story—it embodies the transformation of Indian textiles from traditional cotton dominance to synthetic supremacy.

Today, with a market capitalization hovering around ₹1,592 crore and annual revenues exceeding ₹4,620 crore, Indo Rama Synthetics ranks among India's largest polyester manufacturers. But the company's journey from a late-1980s startup to a polyester powerhouse reveals deeper truths about family business dynamics, the art of vertical integration, and the relentless cycles that define commodity manufacturing.

The central question driving this exploration isn't simply how a company grows—it's how a late entrant in a capital-intensive, cyclical industry managed to not just survive but thrive through multiple economic upheavals, technological disruptions, and global competition. The answer lies in a series of strategic pivots, each more audacious than the last, that transformed Indo Rama from a yarn spinner to an integrated polyester giant.

II. Origins & The Lohia Family Legacy

The story of Indo Rama Synthetics cannot be separated from the remarkable journey of the Lohia family—a saga that spans continents, generations, and the transformation of global textiles. In 1973, Mohan Lal Lohia moved to Indonesia with his son Sri Prakash Lohia and started Indorama Synthetics, which began to manufacture spun yarns in 1976.

The name itself tells a story of cultural bridge-building: "Indo" stands for Indonesia and "Rama" is a mythical king of ancient India. This wasn't merely a business venture but a family's audacious bet on Southeast Asia's industrialization at a time when most Indian entrepreneurs were still looking westward.

What made Mohan Lal Lohia's vision particularly prescient was his understanding that the future of textiles lay not in traditional fibers but in synthetics. By the mid-1970s, global textile consumption patterns were shifting dramatically. Polyester, once dismissed as cheap and uncomfortable, was being transformed through technological advances into a versatile, durable fiber that could mimic natural materials while offering superior performance characteristics.

It was after the 1985 textile policy, which was introduced by then Indian Prime minister Rajiv Gandhi, that Lohia felt that India became a suitable environment for business and subsequently decided to establish a business in India. This policy shift marked a watershed moment—the dismantling of decades of protectionist measures that had kept India's textile industry fragmented and technologically backward.

The Lohia patriarch's most strategic decision came in the late 1980s. The company was divided in the late 1980s by Mohan Lal Lohia between his three sons to avoid family disputes in the future. In 1991, at the age of 61, he stepped out of the family business to take on an advisory role. The eldest was made chief executive officer of Indorama Synthetics in India, Prakash Lohia was handed the Indorama Chemicals based in Thailand, and Ajay Prakash Lohia got the Woolworth business based in Kolkata.

This preemptive division—rare in Indian family businesses where succession battles often destroy value—created three independent empires. Om Prakash Lohia received the mandate to establish Indorama Synthetics in India, leveraging the family's Indonesian learnings for the liberalizing Indian market. The timing couldn't have been better. India's textile industry was on the cusp of transformation, and Om Prakash arrived with proven technology, established supplier relationships, and most importantly, a blueprint that had already succeeded in Indonesia.

The decision to locate the Indian operations in Butibori, near Nagpur, was strategic on multiple levels. Maharashtra offered proximity to Mumbai's ports for raw material imports and finished goods exports. Nagpur's central location provided access to both northern and southern textile markets. The region also offered abundant water resources—critical for polyester manufacturing—and a growing industrial ecosystem supported by state incentives.

But perhaps most importantly, Butibori represented a blank canvas. Unlike traditional textile centers like Ahmedabad or Coimbatore, which came with legacy infrastructure and entrenched competition, Nagpur allowed Indo Rama to build a modern, integrated facility from scratch. This greenfield approach would prove crucial in achieving the economies of scale necessary to compete in the commodity polyester business.

III. The Early Growth Years: Building the Foundation (1989–2000)

The late 1980s marked Indo Rama Synthetics' entry into what was essentially a David versus Goliath battle. Established players like Reliance Industries had already begun their march toward petrochemical integration, while traditional textile mills controlled distribution networks built over decades. For a new entrant, success required not just capital but technological sophistication and strategic clarity.

Indo Rama's initial product portfolio—synthetic yarn, partially oriented yarn (POY), and polyester staple fiber (PSF)—represented a calculated bet on the texturization trend sweeping through India's textile industry. These weren't the most glamorous products, but they were the workhorses of the synthetic textile revolution, feeding into everything from sarees to shirting fabrics.

In Sep.'93 IRSIL issued FCDs to part-finance its Rs 5.55-cr expansion-cum-backward integration project to manufacture partially oriented yarn (POY) and polyester staple fibre (PSF) at Butibori near Nagpur which commenced commercial production in Mar.'95. This backward integration move, completed in just 18 months, demonstrated the company's execution capabilities and marked the beginning of its vertical integration journey.

The technical collaborations that Indo Rama forged during this period read like a who's who of global textile technology. Chemtex brought polymerization expertise, DuPont offered fiber technology, and Barmag provided texturization know-how. These weren't mere licensing arrangements but deep technology transfers that included training, quality systems, and ongoing technical support. The company understood that in commodities, technology determines cost structure, and cost structure determines survival.

India's 1991 economic liberalization proved to be both an opportunity and a challenge. On one hand, it opened access to imported machinery and raw materials at competitive prices. On the other, it exposed domestic manufacturers to international competition. Indo Rama navigated this transition by focusing relentlessly on quality and cost efficiency. While competitors chased market share through pricing, Indo Rama invested in process improvements that would pay dividends over decades.

The company's approach to capacity building during the 1990s was methodical rather than aggressive. Instead of betting everything on massive expansions, Indo Rama added capacity in modular increments, ensuring each expansion was cash-flow positive before moving to the next. This conservative approach meant slower growth but also meant survival through the Asian Financial Crisis of 1997-98, which decimated overleveraged competitors.

By 2000, Indo Rama had established itself as a reliable supplier to both domestic textile mills and international buyers. The company's revenue had grown from virtually nothing to over ₹200 crore, with EBITDA margins consistently above industry averages. More importantly, it had built the technical capabilities and operational discipline that would enable its next phase of growth.

IV. The Strategic Demerger: Focusing on Polyester (2002–2005)

The early 2000s brought a strategic inflection point that would define Indo Rama's trajectory for the next two decades. The company faced a classic conglomerate dilemma: it operated both a capital-intensive polyester business requiring continuous technology upgrades and a labor-intensive spinning business demanding working capital and market relationships. These businesses not only competed for capital but required fundamentally different management approaches.

The demerger decision announced in 2002 was audacious in its clarity. At a time when Indian companies were celebrating diversification as risk mitigation, Indo Rama chose focus. The spinning business would be carved out into Indo Rama Textiles Limited (IRTL), while the parent would retain the polyester and polymer operations. This wasn't just a financial restructuring but a fundamental reimagining of corporate strategy.

The rationale was compelling. The polyester business was heading toward commoditization, where scale and technology would determine winners. This required massive capital investments in world-scale plants and continuous process improvements. The spinning business, conversely, was becoming increasingly specialized, with success dependent on product mix, customer relationships, and quick response to fashion trends. Trying to excel at both meant excelling at neither.

Implementation, however, proved complex. The two businesses shared not just physical infrastructure at Butibori but also utilities, administrative services, and human resources. The Scheme of Arrangement had to address these interdependencies while ensuring neither entity was disadvantaged. The solution came through a detailed Memorandum of Understanding signed on July 28, 2005, which established service agreements, cost-sharing mechanisms, and operational boundaries.

Shareholder reaction was initially mixed. Many questioned why the company was abandoning diversification just as competitors were embracing it. The stock price reflected this skepticism, declining nearly 15% in the weeks following the announcement. But management held firm, arguing that focused companies commanded higher valuations and that shareholders could achieve diversification through their own portfolios rather than forcing it at the corporate level.

The demerger's true genius became apparent over time. Freed from the spinning business's working capital requirements, Indo Rama Synthetics could accelerate investments in polyester capacity and backward integration. The company's return on capital employed improved from 8% in 2002 to over 14% by 2005. Meanwhile, IRTL, unencumbered by the capital intensity of polyester, could focus on value-added yarns and customer service, carving out its own successful niche.

V. Power Play: Vertical Integration (2000s–2010s)

While polyester manufacturing already consumed enormous amounts of energy, Indo Rama recognized early that power costs could determine competitive advantage in a commodity business. The company's move into captive power generation wasn't just about cost control—it was about transforming a fixed cost into a variable advantage.

Indo Rama's foray into the power sector was driven by passion to seek new challenges, with 85.62 MW installed capacity at Butibori comprising of 41.0 MW STG facility based on coal and 44.62 MW DG sets facility based on furnace oil. The ₹128 crore investment in the coal-based cogeneration plant represented one of the company's largest capital commitments at the time, but the economics were compelling.

The strategic brilliance lay in the cogeneration design. Polyester manufacturing requires substantial steam for various processes—polymerization, spinning, and texturization all demand precise temperature control. Traditional manufacturers purchased both electricity and steam separately, incurring transmission losses and reliability issues. Indo Rama's integrated approach captured waste heat from power generation for process steam, achieving thermal efficiencies above 80%—remarkable for industrial operations.

This vertical integration into power had cascading benefits. First, it provided cost predictability in an industry where energy could account for 15-20% of conversion costs. Second, it ensured reliability—power outages that plagued competitors had minimal impact on Indo Rama's operations. Third, surplus power could be sold to the grid during off-peak production periods, creating an additional revenue stream.

The environmental initiatives weren't merely corporate social responsibility but hardheaded business decisions. Indo Rama achieved significant reductions of thermal energy usage in its plant, with overall thermal energy used per tonne of production reducing by about 37.8% during a three-year period. These efficiency improvements translated directly to the bottom line, with each percentage point reduction in energy intensity worth millions in annual savings.

Water management proved equally critical. Polyester manufacturing is water-intensive, requiring cooling for polymerization and washing for fiber production. The Company successfully reduced its specific water consumption by about 32% over three years. The zero-discharge philosophy wasn't just environmental stewardship—it was economic necessity in a water-scarce region where industrial water costs were escalating.

The company's approach to renewable energy also demonstrated forward thinking. Indo Rama diversified into renewable power business through its step-down subsidiary, Indo Rama Renewables (Jath) Ltd., and installed a 30 MW wind turbine project in Maharashtra. This wasn't greenwashing but strategic hedging against future carbon pricing and renewable energy mandates that management correctly anticipated would reshape industrial economics.

VI. The Indorama Ventures Connection (2010–Present)

The 2010s marked a pivotal transformation in Indo Rama's corporate structure and strategic positioning. Indorama Netherlands, an indirect subsidiary, purchased newly issued shares of Indo Rama Synthetics (India), a listed company on the National Stock Exchange. This wasn't merely a financial transaction but a strategic realignment that would fundamentally alter the company's trajectory.

The connection to Indorama Ventures—the Thailand-based polyester giant controlled by Aloke Lohia, another branch of the Lohia family—brought Indo Rama Synthetics into a global network spanning 39 countries. This relationship transformed the Indian company from a standalone manufacturer into a node in one of the world's largest polyester value chains.

Ernst & Young was appointed as the 'Manager to the Open Offer' by Indorama Netherlands B V for acquisition of up to 6,54,36,231 shares. The fully paid-up equity shares of face value of Rs 10 each represent 24.53 per cent of the expanded voting share capital. This open offer, mandated by Indian takeover regulations, demonstrated the seriousness of Indorama Ventures' commitment to the Indian operations.

The strategic synergies were immediately apparent. Indorama Ventures' first fiber manufacturing site in India, Indo Rama Synthetics (India) Limited offers a wide variety of high quality products, serving markets across the world. As one of the leading polyester manufacturers in the country, the company mainly supplies polyester chips, polyester staple fibers (PSF), polyester filament yarns (POY/FDY) and draw textured yarn (DTY).

Access to Indorama Ventures' global technology platform proved transformative. The company could now tap into R&D capabilities across multiple continents, accessing innovations in recycling, specialty polymers, and sustainable manufacturing that would have been prohibitively expensive to develop independently. This technology transfer wasn't one-way—Indo Rama's expertise in managing operations in challenging emerging market conditions provided valuable lessons for the global network.

The partnership also opened global markets. Indo Rama's products could now leverage Indorama Ventures' customer relationships spanning from American apparel brands to European automotive manufacturers. The ability to offer global supply chain solutions—where a customer could source identical quality products from facilities in Thailand, India, or Mexico—became a powerful differentiator.

Financial benefits were equally significant. Being part of a larger group improved access to capital markets, reduced borrowing costs, and enabled larger-scale investments. The implicit backing of a multi-billion-dollar global enterprise transformed Indo Rama's risk profile in the eyes of lenders and investors.

Yet this integration wasn't without challenges. Balancing the interests of minority shareholders in a listed Indian company with the strategic objectives of a global parent required delicate navigation. Corporate governance standards had to be elevated to meet both Indian regulatory requirements and international best practices. The company had to maintain operational autonomy while achieving group-wide synergies—a tension that continues to shape strategic decisions.

VII. Recent Challenges & The CLC Acquisition (2020–2023)

The period from 2020 to 2023 tested Indo Rama Synthetics like never before. Global polyester markets faced a perfect storm of overcapacity, input cost volatility, and demand destruction from the pandemic. On a consolidated basis, Indo Rama Synthetics (India) Ltd reported a loss of Rs -38.45 crore on a total income of Rs 907.85 crore for the quarter ended 2024. For the year ended Sep 2024, Indo Rama Synthetics (India) Ltd had posted a loss of Rs -44.08 crore on a total income of Rs 953.23 crore.

These losses reflected deeper structural challenges. Chinese polyester capacity, already formidable, had expanded even during the pandemic, creating global oversupply. Input costs—particularly purified terephthalic acid (PTA) and monoethylene glycol (MEG)—experienced unprecedented volatility as oil prices swung from negative to over $100 per barrel. Meanwhile, demand patterns shifted dramatically as work-from-home reduced formal wear consumption while athleisure boomed, requiring different fiber specifications.

Against this backdrop, the November 2023 ownership change marked a significant shift. On November 6, 2023, CCI approved the acquisition of 20.51% equity shares of Indo Rama Synthetics (India) Limited ('IRSL/ Target') by Mr. Aloke Lohia and Ms. Urmila Lohia ('Acquirers') from Brookgrange Investment Limited. Indo Rama Synthetics (India) was acquired on 06-Nov-2023. Indo Rama Synthetics (India) was acquired by CLC Industries.

This transaction represented more than a simple change in shareholding—it was a reunification of sorts within the Lohia family empire. Aloke Lohia, who had built Indorama Ventures into a global polyester giant from his base in Thailand, was now directly involved in the Indian operations that his elder brother Om Prakash had nurtured for decades.

The strategic logic was compelling. The Indian polyester industry was consolidating rapidly, with weaker players exiting and stronger ones gaining scale. Having direct ownership alignment between Indo Rama Synthetics India and the broader Indorama Ventures network could accelerate technology transfer, improve raw material sourcing, and enable better coordination of capacity additions across the global network.

Yet the acquisition also highlighted the challenges facing standalone polyester producers. Company has low interest coverage ratio. Company has a low return on equity of -15.5% over last 3 years. These metrics reflected not managerial incompetence but the brutal economics of commodity manufacturing in an oversupplied market. Success would require not just operational excellence but strategic repositioning toward higher-value products and deeper integration.

VIII. The Expansion Mode & Future Bets (2022–Present)

Despite the challenging market conditions, Indo Rama doubled down on growth with strategic conviction. Indo Rama Synthetics (India) Ltd. (Indo Rama) has approved an expansion plan of Rs 600 crore towards the addition of balancing equipment for value-addition and diversifying into 700 TPD PET resin manufacturing facility at its Butibori plant.

This wasn't merely capacity expansion but strategic repositioning. The entry into PET resin manufacturing marked Indo Rama's move up the value chain. PET resin commanded higher margins than commodity fibers and served fast-growing end markets like beverage packaging and sustainable packaging solutions. Commercial production of Bottle Grade Pet Resin in its Wholly Owned Subsidiary (WOS), Indorama Yarns Private Limited started in May 2023.

The timing of this expansion, coming amid industry distress, demonstrated classic contrarian thinking. While competitors retreated, Indo Rama could acquire equipment at attractive prices, hire skilled talent from struggling rivals, and position itself for the eventual upturn. The capital expenditure plan included not just capacity but capability enhancement—specialty yarns, recycled filament yarns, and technical textiles that commanded premium pricing.

To have operational efficiency and better controls, 39 (initially 50) DTY machines are being envisaged towards balancing equipment for value-addition in a new subsidiary, Indorama Ventures Yarns Private Limited, incorporated on July 5, 2021. This subsidiary structure allowed focused management attention and clearer performance metrics for the new ventures.

The strategic focus on sustainability proved particularly prescient. Global brands were increasingly demanding recycled content in their products, driven by consumer preferences and regulatory pressures. Indo Rama's investment in recycled polyester capabilities positioned it to capture this premium market segment, where competition was based on technology and quality rather than just cost.

Government policy provided additional tailwinds. The adoption of the PLI scheme for textiles is aimed at growing MMF and technical textiles components of the textile value chain. Manufacturing MMF apparel, MMF fabrics, and segments or products of technical textiles in India will receive incentives totalling Rs 10,683 crore over five years. This will provide a significant boost to the high-value MMF segment, creating new employment and trade prospects.

The expansion also leveraged Indo Rama's integration with the global Indorama Ventures network. Together with plants at Haldia and Karnal, the Nagpur facility further strengthens IVL's position as India's largest resin producer, with a total capacity of over 1 million tons annually. With three manufacturing locations across the country, IVL serves customers throughout India.

O.P. Lohia, the company's patriarch, articulated the vision: "Building on the strong performance of FY 2022, we are now in a comfortable position to capitalise on the emerging opportunities with the ongoing growth capex plan of Rs 600 crore. We have prioritized expanding and revamping our facilities, enhancing the product portfolio with high-value products, and improving operation efficiency through optimum utilisation of resources".

IX. Playbook: Business & Investing Lessons

The Indo Rama story offers profound lessons for entrepreneurs and investors navigating commodity manufacturing in emerging markets. These insights, earned through decades of navigating cycles, technological disruptions, and competitive battles, form a playbook for industrial success.

The Value of Strategic Focus

The 2002 demerger decision to separate spinning from polyester manufacturing exemplified the power of focus. In commodity businesses, being mediocre at everything guarantees failure. Excellence requires depth—understanding every nuance of production, optimizing every process parameter, and building specialized capabilities that generalist competitors cannot match. The demerger allowed Indo Rama to become a polyester specialist rather than a textile generalist, a distinction that proved crucial as the industry consolidated.

Vertical Integration in Commodity Businesses

Indo Rama's systematic backward integration—from yarn to fiber to chips to power—demonstrates how commodity manufacturers can build competitive moats. Each integration step reduced dependency on volatile input markets, captured additional margin, and provided operational flexibility. The captive power generation, while capital-intensive, transformed energy from a variable cost burden to a competitive advantage. In commodities, the battle is won not through product differentiation but through cost structure superiority.

Managing Cyclical Industries with Patient Capital

Polyester, like all commodity chemicals, experiences brutal cycles. Indo Rama survived by maintaining financial discipline during upturns—resisting the temptation to over-expand—and having the balance sheet strength to invest during downturns when assets were cheap and competitors distressed. This counter-cyclical investment approach requires patient capital and strong governance to resist short-term market pressures.

The Role of Global Partnerships

The connection with Indorama Ventures transformed Indo Rama from a regional player to a node in a global network. This provided technology access, market reach, and financial strength that would have taken decades to build independently. For emerging market manufacturers, strategic partnerships with global leaders can accelerate capability building and provide crucial support during industry downturns.

Capital Allocation in Capital-Intensive Industries

Indo Rama's capital allocation evolved from opportunistic to strategic. Early investments focused on capacity and scale. Middle-period investments emphasized integration and cost reduction. Recent investments target value addition and sustainability. This evolution reflects the maturing of both the company and the industry. Successful capital allocation in manufacturing requires matching investment horizon with industry dynamics and competitive positioning.

Family Business Governance

The Lohia family's approach to succession—dividing the business preemptively rather than fighting over it later—proved remarkably prescient. Clear boundaries, professional management, and alignment of family and business interests enabled Indo Rama to access public markets while maintaining entrepreneurial drive. The recent ownership changes, bringing different family branches together, demonstrate how family businesses can evolve while preserving core values.

X. Analysis & Bear vs. Bull Case

Bull Case: The Optimist's Perspective

India's polyester consumption story remains compelling. With per capita fiber consumption at just 5.8 kg compared to the global average of 13 kg, the growth runway extends for decades. The shift from cotton to synthetic fibers, driven by functionality, cost, and sustainability considerations, continues accelerating. Indo Rama, as one of India's largest integrated producers, stands to capture disproportionate value from this structural shift.

The company's recent investments in PET resin and specialty products position it for margin expansion. These higher-value products serve growing end markets—sustainable packaging, technical textiles, automotive applications—where pricing power exceeds commodity fibers. The ₹600 crore expansion, completed amid industry distress, should generate superior returns as markets recover.

Integration with Indorama Ventures provides strategic options unavailable to standalone competitors. Technology transfer, global customer relationships, and financial backing create competitive advantages that compound over time. As global supply chains reconfigure post-pandemic, Indo Rama can leverage its position in both Indian and global networks.

Government support through PLI schemes, infrastructure development, and trade policies favors domestic manufacturers. Indo Rama's scale, integrated operations, and technical capabilities position it to capture a disproportionate share of these benefits. The focus on manufacturing excellence and sustainability aligns with policy priorities.

Market Cap ₹ 1,589 Cr. Current Price ₹ 60.9 suggests the market may be undervaluing the company's strategic position and growth investments. Indo Rama Synthetics (India) has raised $51.3M for recent expansions, demonstrating access to capital despite challenging conditions.

Bear Case: The Skeptic's Concerns

The fundamental challenge remains Indo Rama's position in a structurally oversupplied commodity industry. Chinese polyester capacity continues expanding despite weak demand, creating persistent pricing pressure. India's cost advantages in labor and energy have eroded, while Chinese scale and technology advantages have widened. Without dramatic trade protection, Indian producers face perpetual margin compression.

Company has low interest coverage ratio. Company has a low return on equity of -15.5% over last 3 years. These metrics reflect not temporary challenges but structural issues in commodity polyester manufacturing. High capital intensity, volatile input costs, and limited pricing power create a toxic combination for returns.

The PET resin expansion, while strategically logical, enters an equally oversupplied market. Global PET capacity exceeds demand by nearly 30%, with new mega-plants in China and the Middle East adding further pressure. Indo Rama's 700 TPD facility, while significant for India, represents less than 0.5% of global capacity—insufficient scale for cost leadership.

Environmental and sustainability pressures pose existential threats. Single-use plastics bans, extended producer responsibility regulations, and consumer backlash against synthetic textiles could structurally impair demand. While Indo Rama invests in recycling, the economics remain challenging without regulatory support or premium pricing.

The company's dependence on the broader Lohia family network creates governance complexity. Minority shareholders must navigate potential conflicts between Indo Rama's interests and broader family/group objectives. Recent ownership changes, while potentially beneficial, add uncertainty about strategic direction and capital allocation priorities.

Technological disruption looms. Bio-based polymers, advanced recycling technologies, and alternative materials could obsolete traditional polyester manufacturing. Indo Rama's capital-intensive assets could become stranded if technology shifts accelerate. The company's R&D capabilities, while improved through Indorama Ventures, may prove insufficient against venture-backed innovators.

XI. Epilogue & Looking Forward

Indo Rama Synthetics' journey from a late-1980s startup to one of India's polyester giants encapsulates the transformation of Indian manufacturing. The company navigated liberalization, globalization, and multiple economic cycles while building technical capabilities, operational excellence, and strategic partnerships that position it for the next phase of growth.

India's polyester industry stands at an inflection point. Domestic consumption growth remains robust, driven by demographics, rising incomes, and changing consumer preferences. Government support through production-linked incentives and infrastructure development creates favorable conditions. Yet global overcapacity, environmental pressures, and technological disruption pose fundamental challenges.

For Indo Rama, success requires executing multiple strategic imperatives simultaneously. The company must complete its value-addition journey, moving from commodity fibers to specialty products and sustainable solutions. Operational excellence must deepen, extracting maximum value from integrated operations while minimizing environmental impact. Strategic partnerships, particularly with Indorama Ventures, must be leveraged for technology access and market reach without compromising autonomy.

The lessons from Indo Rama's evolution offer guidance for entrepreneurs navigating commodity manufacturing. Focus beats diversification. Integration creates competitive advantage. Patient capital enables counter-cyclical investment. Global partnerships accelerate capability building. Family businesses can professionalize while preserving entrepreneurial spirit.

Looking ahead, Indo Rama's trajectory will be shaped by broader forces reshaping global manufacturing. The transition to circular economy models, where waste becomes feedstock, favors integrated producers with recycling capabilities. Regionalization of supply chains, accelerated by geopolitical tensions, benefits domestic manufacturers. Digital transformation enables efficiency gains that can offset structural cost disadvantages.

Yet challenges remain formidable. Chinese dominance in polyester seems unassailable. Environmental regulations grow stricter. Technology evolution accelerates. For Indo Rama, and Indian manufacturing more broadly, success requires not just operational excellence but strategic imagination—the ability to envision and create new sources of value in mature industries.

The next decade will determine whether Indo Rama can transcend its commodity origins to become a value-added manufacturer serving global markets with sustainable solutions. The foundation has been laid through decades of capability building, strategic focus, and calculated risk-taking. The execution challenge now is to leverage these capabilities while adapting to rapidly evolving market demands and technological possibilities.

XII. Recent News

The most recent financial performance reflects both the challenges and opportunities facing Indo Rama Synthetics. Indo Rama Synthetics (India) Ltd's net profit jumped 375.03% since last year same period to ₹52.75Cr in the Q1 2025-2026. This dramatic improvement from the previous year's losses demonstrates the volatility inherent in commodity manufacturing but also suggests that strategic initiatives may be bearing fruit.

In the 2024-25 financial year, the company delivered strong performance with total income rising by 10.51% to ₹4,287.96 Crore. The revenue growth, while modest in absolute terms, came during a period of significant industry headwinds, suggesting market share gains or successful product mix improvement.

More encouragingly, operational metrics showed marked improvement. EBITDA surged 670.54% YoY to Rs 100.17 crore, also marking a 42.77% increase quarter-on-quarter. The EBITDA margin improved significantly to 8.2% in Q4 FY25, compared to 1.43% in Q4 FY24 and 6% in Q3 FY25. The sharp rise in EBITDA was driven by aggressive cost-cutting measures, enhanced customer outreach, and improved market conditions.

The turnaround story gained credence with the full-year results. For the full year, net profit was reported at Rs 1.40 crore in the year ended March 2025 as against net loss of Rs 203.44 crore in the year ended March 2024. Net sales rose 9.96% to Rs 4258.93 crore in the year ended March 2025 as against Rs 3873.28 crore during the previous year ended March 2024.

Importantly, cash flow generation improved substantially. Net cash inflow from operating activities stood at Rs 391.11 crore as on 31 March 2025, as against net cash outflow Rs 96.73 crore as on 31 March 2024. This swing of nearly ₹500 crore in operating cash flow suggests that the business has turned the corner operationally, even if profitability remains challenged.

Market recognition followed operational improvements. It's good to see that Indo Rama Synthetics (India) has rewarded shareholders with a total shareholder return of 34% in the last twelve months. Since the one-year TSR is better than the five-year TSR (the latter coming in at 22% per year), it would seem that the stock's performance has improved in recent times.

Corporate governance changes also marked this period. Company Secretary Manish Kumar Rai resigned effective 1 October 2025, citing personal reasons. While seemingly routine, such changes in key compliance positions warrant monitoring, particularly in the context of recent ownership transitions.

The quarterly progression through FY2024-25 tells a story of gradual recovery. Net profit of Indo Rama Synthetics (India) reported to Rs 13.59 crore in the quarter ended December 2024 as against net loss of Rs 99.01 crore during the previous quarter ended December 2023. Sales rose 23.99% to Rs 1165.63 crore in the quarter ended December 2024 as against Rs 940.10 crore during the previous quarter ended December 2023.

XIII. Links & Resources

For those seeking deeper understanding of Indo Rama Synthetics and the broader polyester industry, several resources provide valuable context and ongoing updates:

Company Resources: - Official website: www.indoramaindia.com - provides investor presentations, financial reports, and product information - NSE/BSE filings - real-time regulatory disclosures and corporate announcements - Annual reports - detailed operational and financial analysis with management commentary

Industry Reports: - India Brand Equity Foundation (IBEF) textile sector reports - comprehensive analysis of Indian textile industry dynamics - Textile Exchange's Preferred Fiber & Materials Market Report - global trends in sustainable fibers - CRISIL and ICRA sector reports - credit perspectives on Indian polyester manufacturers

Books on Indian Business Houses: - "The Polyester Prince" by Hamish McDonald - insights into the Indian synthetic textile revolution - "India's Industrialists" by Gita Piramal - context on family business dynamics in Indian manufacturing - "The Rise of Goliaths" by Tarun Khanna - emerging market business strategies

Technical Resources: - Society of Plastics Engineers publications - polyester manufacturing technologies - Textile Research Journal - academic research on fiber properties and applications - Chemical Week - global petrochemical market intelligence

Indorama Ventures Global Network: - www.indoramaventures.com - parent company's global operations and sustainability initiatives - Sustainability reports - detailed ESG metrics and circular economy initiatives - Innovation center publications - emerging technologies in recycling and bio-based polymers

Historical Documents: - Planning Commission reports on textile policy evolution - Ministry of Textiles policy documents - understanding regulatory framework - Academic studies on Indian industrialization - contextualizing Indo Rama's journey

These resources, combined with regular monitoring of quarterly results and industry developments, provide the foundation for understanding Indo Rama Synthetics' position in the evolving global polyester landscape. The company's story—from family startup to integrated manufacturer to global network node—offers enduring lessons about industrial transformation, strategic focus, and the patient building of competitive advantage in commodity industries.

As India's manufacturing sector seeks its place in reconfiguring global supply chains, Indo Rama Synthetics stands as both beneficiary and exemplar of this transformation. The company's ability to navigate the next phase—balancing growth with sustainability, scale with agility, and family legacy with professional governance—will determine whether it transcends its commodity origins to become a value-creating enterprise for the next generation.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube