RACL Geartech: The Indian Gear Maker That Powers BMW, KTM & Porsche

I. Introduction: The Noida Outfit Supplying Europe's Finest

Picture the factory floor of a premium motorcycle manufacturer in Munich or Mattighofen. When an engineer at BMW Motorrad signs off on a new transmission component, or when KTM's quality team validates a gear set for their flagship 1290 Super Duke, the parts that emerge from the shipping containers often bear a rather unexpected origin: Noida, India.

RACL is a ₹1,000 crore market cap company delivering to KTM, BMW Motorrad, Aston Martin, Porsche, and Mercedes AMG. RACL is amongst the most unique auto ancillary companies.

How does a company from India's National Capital Region—a place more associated with call centers and IT parks than precision engineering—end up becoming a trusted supplier to Europe's most demanding luxury automakers? The answer involves a bankruptcy rescue that reads like corporate fiction, a management buyout orchestrated by a plant manager who refused to let the company die, and a decades-long patient climb up the value chain.

Its client roster includes ZF, BMW, KTM, Kawasaki, and TVS, and it boasts what is arguably one of the cleanest quality records in the business: zero product recalls in its four-decade history.

Think about that for a moment: zero product recalls. In an industry where a single defective gear can cause catastrophic mechanical failure, where the tolerance requirements measure in microns, and where European OEMs are notoriously unforgiving, this Indian company has delivered flawless quality for over forty years.

The RACL Geartech story carries several themes that make it worthy of deep examination. There's the near-death experience and management buyout—a narrative arc more common in private equity case studies than in Indian manufacturing. There's the export-led transformation strategy that positioned the company in premium, low-volume segments long before "Make in India" became a government slogan. And there's the ongoing pivot from component supplier to drivetrain systems partner, a rare evolutionary leap in the Indian auto ancillary context.

Over the last two decades, the company has evolved from supplying basic gears for mass motorcycles and tractors to becoming a trusted drivetrain solutions partner for some of the world's most demanding OEMs.

What follows is the story of how patience, precision, and a stubborn refusal to chase volume over value created one of India's most distinctive manufacturing businesses—and what lies ahead as RACL navigates the complex transition toward electric vehicles, faces the bankruptcy of a major customer, and attempts to scale without sacrificing the quality-first culture that made its reputation.

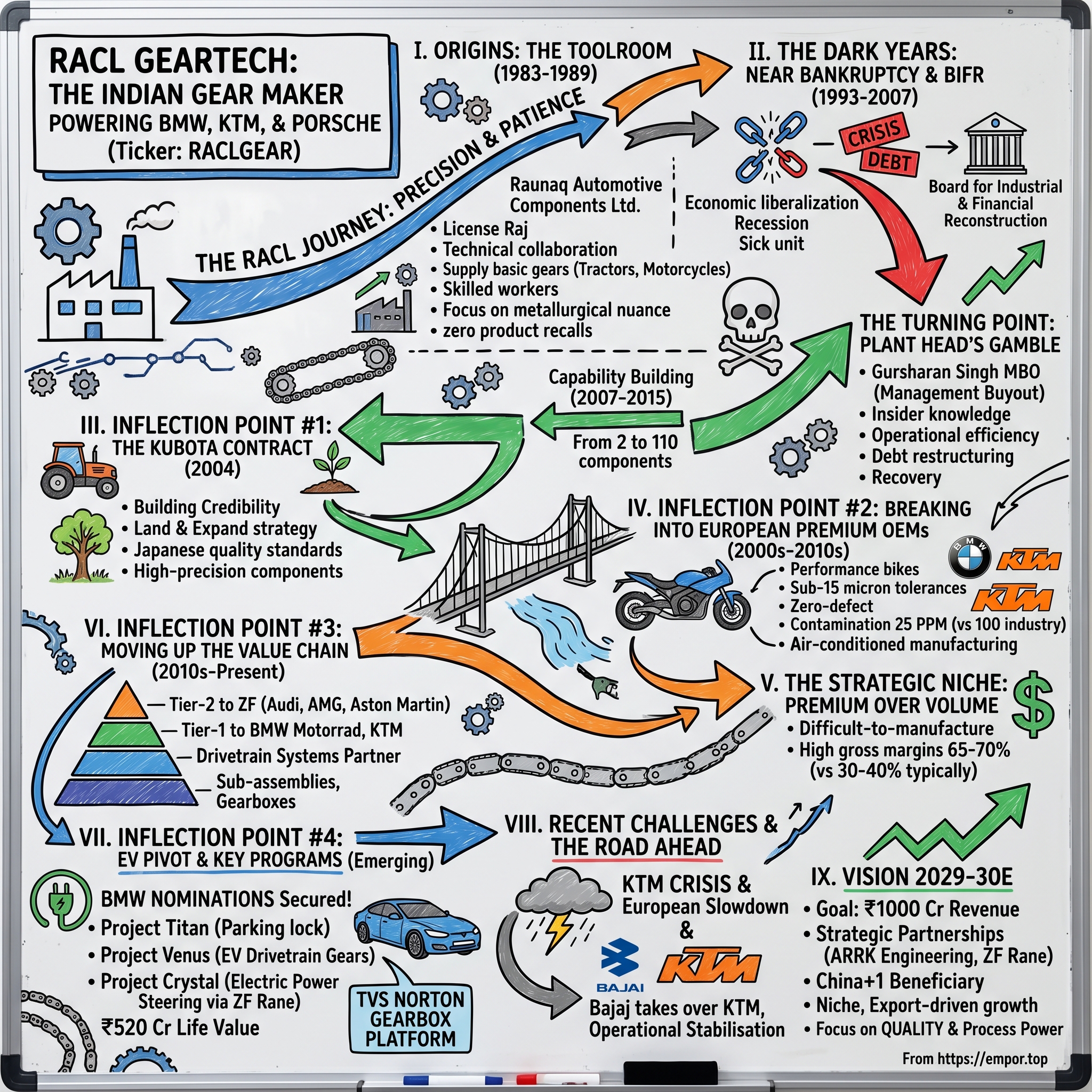

II. Origins: The Toolroom That Could (1983–1989)

The License Raj era of 1980s India was not, by any stretch of imagination, a hospitable environment for precision manufacturing. Import restrictions kept foreign machinery out. Technology transfer agreements were Byzantine affairs requiring multiple government approvals. And the domestic auto industry, protected from foreign competition, had little incentive to demand world-class component quality.

It began in 1983 as a modest toolroom outfit, supplying jigs, fixtures, and loose gears to Indian two-wheeler manufacturers.

RACL Geartech Ltd. was originally incorporated in 1983 as Raunaq Automotive Components Ltd. (RACL), part of the Raunaq Group, with technical collaboration from DAB Industries, USA. The company was set up to manufacture precision-engineered gears and transmission components for automotive OEMs in India and abroad.

The Raunaq Group connection is noteworthy. Raunaq Singh, the group's founder, had built a conglomerate spanning engineering, auto components, and industrial products. The auto components venture was meant to capitalize on India's nascent two-wheeler boom—Hero Puch (later Hero Honda) and Bajaj were ramping up, and the demand for transmission components was rising.

The company was formerly known as Raunaq Automotive Components Limited and changed its name to RACL Geartech Limited in October 2015. RACL Geartech Limited was incorporated in 1983 and is headquartered in Noida, India.

The technical collaboration with DAB Industries provided the initial know-how, but building genuine manufacturing capability in 1980s India required something more fundamental: skilled workers who could actually operate precision machinery and understand metallurgical processes. This is where a young mechanical engineer named Gursharan Singh entered the picture.

RACL has more than three and a half decades of presence in the automobile component industry. Mr. Gursharan Singh, CMD (Chairman & Managing Director) of the company, joined the company as a plant head and has been associated with the company since its inception.

Singh had cut his teeth at Escorts Tractors—then associated with Ford—before joining RACL as plant head. Mr. Gursharan Singh, a Diploma holder in Mechanical Engineering with a Post Graduate Diploma in Export Management, brings over four decades of industry experience in the auto component sector. He began his career with Escort Tractors Ltd. (then associated with Ford), before moving to RACL where he has now spent more than 32 years.

The company started commercial production in 1989, manufacturing transmission gears for a variety of vehicles including two-wheelers, tractors, cars, jeeps, light commercial vehicles, and heavy vehicles. In those early years, there was nothing to distinguish RACL from dozens of other gear manufacturers serving the Indian auto industry. The business was primarily domestic, the customers were price-sensitive Indian OEMs, and the margins reflected the commodity nature of the work.

Over time, it built strong technical know-how in the production of transmission gears, shafts, reduction gear sets, sprockets, ratchets, synchronizers, and axle assemblies, catering to motorcycles, passenger cars, tractors, ATVs, and industrial equipment.

What separated RACL from its peers, even in these early days, was an unusual obsession with process control. While other manufacturers focused on churning out volume, Singh and his team invested in understanding the metallurgical nuances that separated adequate gears from exceptional ones. This foundation—invisible in the financial statements of the 1990s—would prove decisive in the decades to come.

III. The Dark Years: Near Bankruptcy & BIFR (1993–2007)

The early 1990s brought India's economic liberalization, but for RACL, the transition from protected market to open competition proved nearly fatal. The recession that hit Indian auto manufacturing in the late 1990s exposed the company's structural weaknesses: too much debt, insufficient differentiation, and customers who treated gear suppliers as interchangeable commodities.

The company's early years were turbulent. By the late 1990s and early 2000s, RACL faced serious financial difficulties, caused by a mix of recessionary pressures, a slowdown in the automotive industry, and internal inefficiencies.

The crisis deepened to a point where the company could no longer service its debts. The company (formerly known as Raunaq Auto) went bankrupt and was referred to the erstwhile BIFR in 2001.

For those unfamiliar with Indian corporate law of that era, being referred to the Board for Industrial and Financial Reconstruction (BIFR) was essentially a corporate death sentence for most companies. In 2001, it was referred to the Board for Industrial and Financial Reconstruction (BIFR), effectively meaning the company was deemed "sick" and required restructuring. During this period, RACL's very survival was at risk.

The BIFR process, designed to rehabilitate "sick" industrial units, more often served as a way station to liquidation. Banks would take haircuts on their loans, workers would lose jobs, and assets would be sold off to repay what could be recovered. The statistics were grim: most companies that entered BIFR never emerged as going concerns.

The Turning Point: A Plant Head's Gamble

What happened next defies the typical BIFR narrative. Rather than accepting the company's decline or waiting for external restructuring, Gursharan Singh—the plant head who had been with RACL since its inception—orchestrated a management buyout.

Gursharan Singh joined the company as a plant head in 1983. Mr. Gursharan Singh orchestrated a management buy-out and successfully took RACL out of the BIFR purview in November 2007.

The management buyout concept was unusual in Indian manufacturing at the time. Unlike private equity-led buyouts in Western markets, this was a case of insider knowledge meeting entrepreneurial conviction. Singh knew the machines, knew the customers, and—crucially—knew what the company could become if freed from its corporate parent's troubles and given focused leadership.

A turning point came with the leadership of Mr. Gursharan Singh, who assumed charge as Chairman & Managing Director. Through his strategic initiatives, the company refocused on operational efficiency, tighter cost control, and most importantly, securing critical OEM contracts.

RACL Geartech's CEO is Gursharan Singh, appointed in April 2004, with a tenure now exceeding 20 years. He directly owns 36.57% of the company's shares. The significant ownership stake aligned Singh's interests completely with the company's long-term success—a rarity in Indian manufacturing where promoter-manager agency problems frequently undermine performance.

The process wasn't quick. From the 2001 BIFR referral to the November 2007 discharge took six years of negotiations with banks, operational restructuring, and—perhaps most importantly—proving that the company could win and retain high-quality customers.

Thanks to these efforts, RACL successfully completed its Rehabilitation Scheme under BIFR and was formally discharged in November 2007. This marked the end of its insolvency phase and the beginning of a sustained revival.

The bankruptcy experience shaped RACL's culture in ways that persist today. The company developed an almost paranoid focus on financial discipline, quality control, and customer relationships. When you've stared at liquidation, you don't take shortcuts on the things that keep customers loyal.

IV. Inflection Point #1: The Kubota Contract (2004) – Building Credibility

Before RACL could emerge from BIFR, it needed a customer win that would validate its turnaround thesis and provide the cash flows to service restructured debt. That validation came from an unexpected source: a chance encounter that turned into a decade-long partnership.

Due to a stroke of good luck, he met a potential client (Kubota, a leading Japanese player in tractors) on a flight and convinced them to give a small order. And that resulted in a domino effect of being able to thrive in a sector that is famous for a lack of pricing power.

The Kubota relationship began in 2004, and the timing was fortuitous. Japanese OEMs were beginning to explore sourcing from India as part of their cost optimization strategies, but they were notoriously demanding about quality. For Kubota, quality wasn't just about meeting specifications—it was about consistent performance over millions of cycles in demanding agricultural applications.

One notable breakthrough was winning a contract from Kubota of Japan, which gave RACL both credibility and financial lifeline at a critical stage. Slowly, the company built a reputation for delivering high-precision, safety-critical components—something only a handful of Indian firms could achieve at the time.

The philosophy that emerged from this period was deceptively simple: quality over volume. Rather than chasing scale in commodity segments where Indian manufacturers would always compete on price against Chinese and Southeast Asian rivals, RACL would focus on technically demanding applications where process excellence commanded premium pricing.

RACL Kubota relationship starting with 2 components in 2004 to supplying over 110 components today. This expansion from 2 to 110 components with a single customer illustrates the "land and expand" strategy that would become RACL's signature approach. Get a foot in the door with one or two components, deliver flawlessly, and gradually earn the right to supply additional parts.

The Kubota relationship also taught RACL how to work with demanding global OEMs. Japanese quality standards were unforgiving. Documentation requirements were extensive. Lead times were non-negotiable. This education proved invaluable when RACL began approaching European customers with even more stringent requirements.

The company used the 2007-2015 period primarily for capability building rather than aggressive growth. The company built a reputation for delivering high-precision, safety-critical components—something only a handful of Indian firms could achieve at the time.

This patient approach—spending eight years building capabilities before accelerating growth—runs counter to the typical emerging market manufacturing playbook of "grow fast, fix quality later." But for RACL, the quality-first approach was existential. Given that it takes 2-3 years of work with an OEM before a product launches, the seeds planted in this period began bearing fruit from FY18 onward.

V. Inflection Point #2: Breaking into European Premium OEMs (2000s–2010s)

If the Kubota contract was RACL's proof of concept, the European premium motorcycle contracts were its coming-of-age moment. Winning business from BMW Motorrad and KTM represented something fundamentally different from supplying agricultural equipment: it meant producing components for vehicles where performance and reliability were matters of life and death.

The big break came in the 2000s when it began supplying critical gear components to European performance bike makers like BMW Motorrad, KTM, and Piaggio, directly from its Noida plant. This wasn't just about making parts; RACL was involved from the design and prototyping stage, building components with sub-15 micron tolerances and zero-defect reliability. At a time when "Make in India" was still a slogan on the horizon, RACL was already on the shop floors of Europe's finest OEMs.

Sub-15 micron tolerances. To put that in perspective, a human hair is approximately 70 microns in diameter. RACL was manufacturing gears with dimensional accuracy measured in fractions of a hair's width. At these tolerances, temperature fluctuations in the manufacturing environment can affect outcomes. Dust particles become contaminants. The difference between a perfect gear and a rejected one is invisible to the naked eye.

The Quality Edge

While typical contamination levels are set at a threshold of 100 per million (PPM) by OEMs, RACL is operating at 25 PPM - primary reason for it emerging as the preferred supplier to many premium customers.

Product quality in highly critical components—while customers have an acceptable tolerance rate of up to 50-100 PPM, the company has been able to consistently deliver within contamination rates of 25-50 PPM leading to quality reliability. This the company has been able to deliver by importing machines and operating the manufacturing locations in an air-conditioned environment (which reduces entry of dust particles).

Air-conditioning a manufacturing facility in India might seem like a trivial detail, but it's precisely these kinds of process investments that separate premium suppliers from commodity manufacturers. When European quality engineers audit a facility, they're not just looking at machine capabilities—they're assessing whether the entire environment supports consistent precision manufacturing.

The 10-year exclusive BMW bike contract mentioned in earlier investor analyses illustrates the depth of these relationships. Highly regarded process design innovations from RACL have won it exclusive contracts like the 10 year single vendor BMW bike contract.

From Tier-2 to Tier-1

Recently made headways towards becoming a Tier-2 supplier to Mercedes, Porsche, BMW cars via ZF (started in 2020).

The ZF relationship deserves particular attention. ZF Friedrichshafen is the world's second-largest automotive supplier, and becoming a component supplier to ZF opens doors to multiple premium OEM platforms. In exports, BMW Motorrad, KTM, BRP-Rotax, Man trucks, Escorts Kubota, ZF, Piaggio are the key customers. For ZF the company is supplying chassis and chassis components (high margin) in Austria which goes in BMW 7 series.

In addition to BMW 7 series the company supplies components to ZF which goes into Aston Martin, Porsche and Mercedes AMG.

The progression is noteworthy: from supplying gears for motorcycles (which, while demanding, involve relatively small production volumes) to supplying chassis components for BMW's flagship 7 Series sedan. This represents a step-function increase in both the complexity of components and the scale of the opportunity.

VI. The Strategic Niche: Premium Over Volume

Most auto component companies in India have followed a predictable path: start with domestic OEMs, chase volume, compete on price, and gradually squeeze out margins in an endless race to the bottom. RACL's strategy represents a deliberate counter-positioning: focus on difficult-to-manufacture niche luxury products, accept lower volumes, and capture the margin premium that comes with complexity.

The company primarily is in high-end 2 wheelers ranging from 300CC+ to ~1250 CC+.

Consider the implications. A mass-market 125cc commuter scooter sold in India might cost ₹70,000. A BMW R 1250 GS costs €15,000+. The gear set that goes into the BMW transmission commands pricing that reflects both its technical complexity and the value proposition of the end product. More importantly, the customer's purchasing decision isn't driven by the component's price—nobody comparison shops BMW motorcycle gears.

BMW Motorrad and KTM in high-end 2 wheelers, ZF—second largest Auto-OEM in the world, BMW—4W and BRP-Rotax. The company has amongst the highest gross margins in the entire space owing to a specialized portfolio. Gross margins range between 65-70% for the company, amongst the highest in the industry.

Gross margins of 65-70% are extraordinary in auto components, where 30-40% is more typical. These margins reflect the technical barriers to entry, the switching costs for OEMs, and the reality that in premium applications, price sensitivity is dramatically lower than in mass-market segments.

Process R&D, Not Product R&D

The company invests in process R&D and not product R&D.

This distinction matters enormously. Product R&D—designing new component types, developing proprietary technologies—requires massive investment and carries significant risk. For a company of RACL's size (roughly ₹420 crore in revenue), competing on product innovation against global giants would be futile.

Process R&D, by contrast, focuses on manufacturing excellence: how to achieve tighter tolerances, reduce contamination, improve consistency, and lower costs while maintaining quality. This is where RACL can compete—and win—against much larger rivals. The company's air-conditioned manufacturing environments, imported machinery, and decades of accumulated know-how create a capability moat that competitors cannot easily replicate.

VII. Current Business Model & Geographical Diversification

The company that emerged from bankruptcy is now a geographically diversified precision manufacturing business with operations spanning multiple continents and customer relationships across diverse automotive segments.

For FY2024-2025, exports contributed 68% and domestic sales 32% of total revenue. The regional business share shows Europe at approximately 56% and India & Asia Pacific at 42%.

The product distribution for FY24-25 reflects deliberate diversification: Two Wheelers (39%) remain the largest segment, followed by Commercial Vehicles (18%), Passenger Cars including EV (14%), Recreational Vehicles (13%), Tractors and Agriculture (11%), Three Wheelers (3%), and Industrial (2%).

It operates in India, Austria, Japan, Germany, Switzerland, Italy, Thailand, Vietnam, the United States, China, and Sweden.

With two manufacturing facilities in Noida and Gajraula, four warehouses in Europe and one 100% wholly owned subsidiary in Austria to support European clients, the company operates as a tier-1 and tier-2 supplier to global OEMs across premium motorcycles, passenger cars, tractors, and industrial equipment.

The Austrian subsidiary is strategically important. Having a European presence allows RACL to provide local service and just-in-time delivery to demanding European customers. The four European warehouses enable inventory positioning closer to customer facilities, reducing lead times and providing supply chain flexibility.

Customer Concentration

Though RACL has moderate concentration risk with top five customers contributing ~57% of total revenue in FY24 (PY: ~58%), comfort is drawn from the fact that the company is a preferred vendor for many of its premium segment export customers with whom it has long-term relationships. Also, the management as a part of its strategy ensures that sales does not exceed 20% of total revenue to any single customer. The largest contributor during FY24 was ~15% of the total revenue.

The 20% revenue cap per customer is a deliberate risk management strategy. It means RACL will occasionally say no to additional volume from large customers—a discipline that many growth-focused companies fail to maintain. The KTM situation (discussed later) validates this approach: when a major customer experiences difficulties, the impact is painful but not existential.

Largest customers include KTM (~15%), BMW Motorrad (~15%), BRP-Rotax (~15%), Kubota (11%), ZF (9%), MAN Trucks (7%), Piaggio (6%), and TVS (5%).

VIII. Inflection Point #3: Moving Up the Value Chain – From Gears to Systems

The journey from gear supplier to transmission specialist to drivetrain partner is rare in the Indian context, especially for a company of RACL's size. Yet this transformation represents the company's most strategically significant evolution—and its best chance at sustained profitable growth.

In auto ancillaries, what starts as a high-volume, low-margin commodity gradually morphs into a precision-critical, platform-embedded product. Key requirement is getting the engineering, quality, and consistency right. That's exactly the story playing out at RACL Geartech. Over the last two decades, the company has evolved from supplying basic gears for mass motorcycles and tractors to becoming a trusted drivetrain solutions partner for some of the world's most demanding OEMs.

The value chain migration looks something like this:

- Phase 1 (1983-2000s): Loose gears, individual components, commodity manufacturing

- Phase 2 (2000s-2010s): High-precision components for premium applications, co-development with OEMs

- Phase 3 (2010s-present): Sub-assemblies, gear boxes, integrated systems

- Phase 4 (emerging): Complete drivetrain solutions, EV components, engineering services

For ZF the company is supplying chassis and chassis components (high margin) in Austria which goes in BMW 7 series. In FY23 PV exposure was 0%, now is around ~10% of revenues.

The passenger vehicle segment barely existed in RACL's revenue three years ago. Today it represents roughly 10% of sales, with components going into luxury vehicles like the BMW 7 Series, and through ZF to Aston Martin, Porsche, and Mercedes AMG.

In domestic the company caters to TVS (Apache + 300 CC BMW) and Kawasaki along with Escorts Kubota. Recently launched high end bikes such as Piaggio RS 457 and Aprilia 450 CC are supplied by RACL Geartech.

The domestic market positioning mirrors the export strategy: premium segments, technically demanding applications, customers who value quality over price. The TVS relationship is particularly interesting because TVS manufactures BMW's sub-500cc motorcycles in India—so RACL supplies both the Indian and German ends of that partnership.

IX. Inflection Point #4: EV Pivot & The BMW "Project Titan"

The electric vehicle transition poses existential questions for traditional powertrain component suppliers. A battery electric vehicle has no transmission in the traditional sense, no gear boxes, none of the mechanical complexity that defines RACL's core business. How does a gear manufacturer survive in an EV world?

The answer, it turns out, is that EVs still need precision mechanical components—just different ones. Parking lock mechanisms, reduction gears for electric motors, electric power steering components, and drivetrain integration elements all require the same manufacturing capabilities that RACL has spent decades developing.

RACL Geartech nominations secured from BMW AG for contributions to the development of components of electric sports cars, with Rs. 520 crore revenue projected over its lifecycle.

₹520 crore over the project lifecycle. For context, RACL's total annual revenue in FY25 was approximately ₹417 crore. This single BMW EV nomination represents more than a full year's current revenue—and it's focused on components for BMW's next-generation electric sports car platform.

Project Titan where the company has started pilot supplies and where the company is a series supplier for BMW for supply of Parking Lock Mechanism for its next generation electric sports car. First phase is complete and the second trial phase of the samples was scheduled in February 2025 and the company expects mass production from August 2026.

The Project Portfolio

RACL has a robust order book anchored by Project Titan and Venus (BMW EV programs) and Project Crystal (ZF Rane → US). RACL has secured a strong orderbook with significant SOPs wins from 2026, including high value projects like BMW's EV drivetrain gears (Project Venus) & parking lock systems (Project Titan) with a lifetime value of ₹520 crore, along with electric power steering components (Project Crystal) which is in collaboration with ZF Rane for a major US OEM for pick-up truck platform.

Three distinct high-value programs position RACL for the EV transition:

- Project Titan: Parking lock mechanisms for BMW's next-generation electric sports car

- Project Venus: EV drivetrain gears for BMW's electric sports car platform

- Project Crystal: Electric Power Steering components through ZF Rane for a major US pickup truck manufacturer

Several recently announced programs like BMW's electric sports car drivetrain to TVS Norton's complete gearbox platform, are expected to contribute meaningfully over the next 12–24 months.

The TVS Norton gearbox platform deserves attention. Norton, the iconic British motorcycle brand now owned by TVS, provides another avenue for RACL to supply complete transmission systems rather than individual components. This represents the highest level of value chain integration—essentially becoming a Tier-0.5 supplier responsible for entire functional systems.

X. Recent Challenges: KTM Bankruptcy & European Slowdown

No success story is without setbacks, and RACL faced significant headwinds in FY25. The combination of European market slowdown and the near-collapse of a major customer tested the company's resilience.

KTM contributed 6-8% of sales in FY25 versus 15% historically. PMAG (KTM)—largest customer—announced bankruptcy in FY25 which resulted in sales slumping. Bajaj Auto has since taken over KTM, which may give some comfort for recovery in FY26.

The KTM Crisis

In late 2024, KTM teetered on the brink of collapse, filing for court-led restructuring and replacing its long-time CEO in an effort to cut costs. Bajaj's financial lifeline enabled KTM to resume full production by mid-2025.

On November 29, 2024, KTM filed for restructuring under self-administration. That's the Austrian version of bankruptcy protection. The hole was a "very high three-digit million" euro gap.

The KTM bankruptcy resulted from a combination of overproduction, ill-advised expansion into e-bicycles, and a post-pandemic demand normalization that left the company with massive unsold inventory. For RACL, this meant dramatically reduced orders from what had been approximately 15% of revenue.

Bajaj Auto, which had already injected €800 million (RM3.84 billion) into KTM in May 2025 to stave off bankruptcy, has now completed the acquisition of KTM's parent companies. On 18 November 2025, Bajaj's subsidiary purchased all 50,100 shares of Pierer Bajaj AG, officially ending the Pierer family's control.

The resolution—Bajaj Auto's full takeover of KTM—potentially benefits RACL. Bajaj already manufactures KTM's smaller-displacement motorcycles in India, and Bajaj's financial discipline should stabilize KTM's operations. The company has adopted a "precautionary approach" regarding confirmed delivery schedules until KTM is fully stabilized.

Financial Impact

PAT declined 65% in FY25 primarily on account of lower sales and high debt (~300 crores). RACL at the start of the year guided for ~550 crores revenue (~30% increase from FY24), due to slowdown in Europe + higher delivery inventories, the company revised guidance downwards to 460-490 crores (~10-15% growth). Company delivered a revenue of 428 crores.

The gap between initial guidance (₹550 crore) and actual delivery (₹428 crore) represents a significant miss that tested investor confidence. The causes were external—European demand weakness, KTM's production halt, and shipping disruptions—but the impact on profitability was severe.

For the full year, net profit declined 35.69% to Rs 25.60 crore in the year ended March 2025 as against Rs 39.81 crore during the previous year ended March 2024. Sales rose 0.02% to Rs 417.37 crore in the year ended March 2025 as against Rs 417.29 crore during the previous year ended March 2024.

The silver lining: RACL's diversification strategy—no customer exceeding 20% of revenue—prevented what could have been an existential crisis. With the recent fund raise of 79 crores (from Malabar and other investors), debt is not a challenge for near term.

XI. Strategic Partnerships: ARRK Engineering & ZF Rane

Two recent partnerships signal RACL's strategic direction: moving beyond component manufacturing toward integrated engineering and manufacturing solutions.

ARRK Engineering Partnership

RACL Geartech Limited has entered into a strategic technical agreement with German firm ARRK Engineering GmbH. This partnership aims to transform RACL from a component supplier to an end-to-end engineering and industrialization solution provider for the automotive and E-Mobility markets. The collaboration combines ARRK's expertise in product design, prototyping, and testing with RACL's manufacturing capabilities.

Under the agreement, RACL Geartech will leverage ARRK's expertise in product design, prototyping, virtual simulation, and testing & validation, combined with its own capabilities in high-precision gears, shafts, and machined components. The partnership aims to deliver next-generation drivetrain and transmission solutions for the global automotive and e-mobility markets. With this alliance, RACL Geartech plans to move up the value chain by offering end-to-end engineering and industrialisation services—from concept design and testing to mass production.

The ARRK partnership addresses a capability gap. RACL excels at manufacturing but lacks the sophisticated design, simulation, and validation capabilities that OEMs increasingly expect from Tier-1 suppliers. By partnering with ARRK rather than building these capabilities internally, RACL gains access without the massive investment and learning curve.

ZF Rane Partnership

RACL Geartech Limited has partnered with ZF Rane (a ZF Group Company) to develop and supply key components for Electric Power Steering (EPS) systems in passenger cars, including ring gears, sun gears, drive gears, and planetary gear assemblies. This collaboration supports a customised steering system for a leading American pickup truck manufacturer, marking a significant step in RACL Geartech's North American expansion and entry into the EPS market for domestic and export purposes. Prototype production and testing are set for Q2 FY 2025-2026 at the RACL Gajraula plant.

Additionally, RACL Geartech is engaged with Project Crystal, involving electric power steering (EPS) components for a major US OEM for pickup truck platform, through ZF Rane, a globally reputed automotive systems supplier. The project includes supplying high-precision, compact reduction gearsets critical for EPS systems that replace traditional hydraulic steering, providing torque assistance.

The ZF Rane partnership is particularly significant because it represents entry into the North American market—RACL's first major penetration of that geography—and positions the company in the fast-growing electric power steering segment. The "major US pickup truck manufacturer" likely means Ford, GM, or Stellantis, each of which represents enormous volume potential.

XII. Organizational Culture & Management Philosophy

Manufacturing excellence isn't just about machines and processes—it's about people. RACL's culture has been shaped by its near-death experience and the decades-long tenure of key employees.

He is a mechanical engineer with Post-Graduate Diploma in Export Management. He is ably supported by a team of professionals who have been with the company for more than two decades.

The long tenure of senior professionals creates institutional memory that can't be easily replicated. When employees have spent 20+ years perfecting specific manufacturing processes, their knowledge becomes embedded in organizational capability rather than documented procedures.

RACL Geartech Limited is a Great Place to Work-Certified™ organization. Great Place to Work® Certification is recognized world over by employees and employers alike and is considered the 'Gold Standard' in identifying and recognizing Great Workplace Cultures.

The machinery is prohibitively expensive for new entrants, but even if another ancillary company puts up the money to buy costly machinery, they would need to go through a learning curve that could take many years. The other option—poaching employees from RACL—is less likely because many of RACL's employees have been around for decades and appear quite loyal to the company. The loyalty may stem from the shared experience of surviving potential bankruptcy, which created a closely knit team.

This cultural cohesion creates a soft moat that's harder to value than financial metrics but equally important for sustained competitive advantage.

XIII. Playbook: Business & Investing Lessons

The RACL story offers several generalizable lessons for business and investing:

1. Turnaround Through Focus

From near-bankruptcy to premium supplier by doubling down on quality over volume. When everything is at risk, constraints force clarity about what truly matters.

2. Niche Over Scale

Choosing premium, low-volume segments creates margin protection. In commoditized industries, the alternative to differentiation is perpetual margin pressure.

3. Patient Capability Building

The 2007-2015 period of capability building before growth acceleration demonstrates that sustainable competitive advantage requires investment horizons measured in decades, not quarters.

4. The Kubota Model

Use one marquee client to build credibility, then expand. The initial customer becomes a reference, a proving ground, and a template for future relationships.

5. Process R&D Over Product R&D

For small companies in capital-intensive industries, competing on process excellence is more sustainable than competing on product innovation. Let larger players bear the R&D risk while you perfect execution.

6. Export-Led Growth

Using Indian cost advantage for global premium markets rather than competing in domestic mass-market segments where price competition is most intense.

7. Management Buyout Success

Insider knowledge combined with ownership incentives creates alignment that's difficult to replicate with external management. Singh's 36%+ ownership ensures his interests match shareholders'.

XIV. Competitive Analysis: Porter's Five Forces

Understanding RACL's competitive position requires analyzing the industry structure through Michael Porter's framework.

Threat of New Entrants: LOW

The barriers to entry in precision gear manufacturing are substantial. The machinery is prohibitively expensive—a single high-precision CNC gear hobbing machine can cost upward of ₹5-10 crore. Even if a competitor invests in equipment, the learning curve takes years. Long OEM qualification cycles (2-3 years) and precision requirements at sub-15 micron tolerances create high barriers that protect incumbent positions.

Bargaining Power of Suppliers: MODERATE

Raw material (primarily steel) price volatility is a concern but largely pass-through—RACL's contracts typically include price adjustment clauses. Specialized machinery suppliers are limited, creating some dependency on equipment vendors like Gleason and other precision tooling manufacturers.

Bargaining Power of Buyers: MODERATE-HIGH

Large global OEMs have negotiating power, but RACL is a preferred vendor for many of its premium segment export customers with whom it has long-term relationships. Management as a strategy ensures that sales does not exceed 20% of total revenue to any single customer. The no-single-customer-above-20% policy provides negotiating leverage.

Threat of Substitutes: LOW-MODERATE

Precision gears remain critical in EVs, contrary to popular belief. Drivetrains still need mechanical components even in electric vehicles. The EV transition changes the product mix but doesn't eliminate demand for precision engineering capabilities.

Industry Rivalry: MODERATE

Despite differentiated product, this is not a wide moat business. RACL core products are differentiated (transmission related parts have more stringent vibration/noise parameters so need high-precision engineering). However, while competition is not intense, there is no unique technology edge that others cannot replicate.

XV. Hamilton's 7 Powers Analysis

Applying Hamilton Helmer's "7 Powers" framework provides additional strategic insight:

Scale Economies: WEAK

At approximately ₹420 crore revenue, RACL is sub-scale compared to global giants. Scale benefits exist in precision manufacturing, but RACL competes on quality differentiation rather than cost leadership.

Network Effects: ABSENT

No network effects exist in component manufacturing. Each customer relationship is bilateral rather than multi-sided.

Counter-Positioning: MODERATE

RACL has pursued a strategy that focuses on difficult-to-manufacture niche luxury products. This has resulted in a higher margin profile than most auto component players. Larger players focused on volume would cannibalize their existing low-margin business to compete in RACL's premium segments—an unattractive strategic trade-off.

Switching Costs: MODERATE-STRONG

Long qualification cycles (2-3 years) and zero product recalls in four decades make switching risky for OEMs. Process integration at the design stage creates stickiness. When a component is co-developed with the OEM, the validation and testing investments create reluctance to re-qualify alternative suppliers.

Branding: WEAK-MODERATE

As a B2B component supplier, RACL has no consumer brand, but strong reputation among OEMs for quality provides analogous benefits within its customer base.

Cornered Resource: MODERATE

The skilled workforce with decades of experience represents a cornered resource that competitors cannot easily replicate. The air-conditioned manufacturing facilities and imported precision machinery also constitute differentiated physical resources.

Process Power: MODERATE

RACL's process excellence—achieving 25 PPM contamination rates versus industry standards of 50-100 PPM—represents genuine process power. This capability emerged from decades of accumulated learning and cannot be quickly copied.

XVI. Key Performance Indicators to Watch

For investors monitoring RACL's ongoing performance, three metrics matter most:

1. Export Revenue Growth & Geographic Mix

With 68% of revenue from exports, the health of European premium automotive markets directly impacts RACL's topline. Watch for shifts in geographic mix—particularly penetration of the US market through the ZF Rane partnership and continued European stability as KTM recovers.

2. Customer Concentration & New Customer Additions

The company targets adding 8-10% new business through customer onboarding every 2-3 years. Monitor whether this diversification continues and whether any single customer breaches the 20% revenue cap.

3. Program Execution: Start of Production (SOP) Dates

Project Titan (BMW parking lock mechanism) and Project Crystal (ZF Rane EPS) have SOPs scheduled for 2026. Meeting these dates would validate RACL's capability to execute large, complex programs. Delays would extend the already-long payback cycle on program-related capex.

XVII. Bull and Bear Cases

The Bull Case

Multiple growth vectors converging: Projects Titan, Venus, and Crystal represent over ₹600 crore in lifetime value, with SOPs from 2026. The ARRK partnership enables engineering services revenue. KTM's recovery under Bajaj ownership could restore lost volumes. Domestic premiumization (TVS Norton, Aprilia, Kawasaki) provides India-sourced growth.

EV transition as opportunity, not threat: RACL's precision manufacturing capabilities transfer directly to EV drivetrain components. The BMW EV programs demonstrate that OEMs value RACL's quality standards for next-generation platforms.

Industry tailwinds: The auto component industry accounted for 2.3% of India's GDP in FY25 and provided direct employment to over 1.5 million people, a figure expected to rise as the sector's GDP contribution reaches 5-7% by 2026. India's emergence as a global sourcing hub benefits quality-focused exporters like RACL.

China+1 beneficiary: European and American OEMs are actively diversifying supply chains away from China. RACL's established quality track record positions it to capture share from Chinese competitors.

The Bear Case

Customer concentration risk persists: Despite diversification efforts, top five customers still represent ~57% of revenue. Another major customer disruption (like KTM) would significantly impact results.

Execution risk on large programs: The company's growth thesis depends on successful execution of complex programs with long development cycles. These require upfront capex (~₹45–50 Cr FY26E), engineering validation, and timely SOPs (Start of Production). Delays in customer launches or validation failures can stretch payback cycles, particularly as most programs have 3–5-year development lead times.

European demand uncertainty: With 56% of revenue from Europe, any sustained economic weakness in the Eurozone—or specific softness in premium vehicle demand—would pressure growth.

Working capital challenges: RACL operates in niche, export-driven programs with long production and shipping cycles, leading to structurally high inventory days (123) with receivable days (102) and payables days (148) in FY25. High working capital requirements constrain cash flow generation.

No wide moat: While competition is not intense, there is no unique technology edge that others cannot replicate. A determined competitor with capital and patience could eventually match RACL's capabilities.

XVIII. Conclusion: The Long Road from Bankruptcy to BMW

The RACL Geartech story defies easy categorization. It's not a typical Indian manufacturing success story of labor arbitrage and scale. It's not a technology-driven disruptor. It's something rarer: a patient, quality-obsessed company that bet against the industry's commodity trajectory and won.

From the brink of liquidation in 2001 to supplying drivetrain components for BMW electric sports cars in 2025, the company's trajectory reflects choices that seemed counterintuitive at each step. Focus on quality when the market rewarded volume. Target premium segments when domestic demand beckoned. Build capabilities for years before accelerating growth. Refuse customers who would concentrate revenue too heavily.

RACL Geartech's topline witnessed a steady CAGR of ~14.4% in the past 5 years. This growth has been propelled by the company's diversification efforts and product innovation. For RACL, multi-year order inflow from marquee clients is expected to contribute to the revenue milestone of ~₹1,000 crores by FY29-30E.

The path to ₹1,000 crore revenue requires flawless execution of programs currently in development. It requires KTM's recovery under Bajaj ownership. It requires continued trust from European OEMs navigating their own transitions to electric platforms. None of these are guaranteed.

But RACL has navigated existential threats before. A company that survived BIFR, orchestrated a management buyout, built relationships with the world's most demanding manufacturers, and maintained zero product recalls across four decades has demonstrated resilience that transcends any single quarterly result.

The next chapter—whether RACL becomes a ₹1,000 crore precision manufacturing leader or faces new challenges that test its culture—will be written by the same patient, quality-first approach that brought it from a Noida toolroom to the shop floors of Munich and Mattighofen. In an industry where many companies compete on price alone, RACL has bet that precision and patience compound over time. So far, that bet has paid off.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube