The Phoenix Mills: From Cotton to Consumption

I. Introduction and Episode Roadmap

Picture Lower Parel in Mumbai today. Glass towers rise above streets clogged with Ubers and auto-rickshaws. The St. Regis hotel gleams forty stories high. Below it, Palladium Mall hums with Gucci, Burberry, and the kind of polished marble floors that make you instinctively lower your voice. Somewhere inside, a family browses Apple products at an authorized reseller while their teenager eats at a Japanese restaurant that would not be out of place in Ginza. On the upper floors, Standard Chartered bankers tap away at terminals overlooking a cityscape that would have been unrecognizable to their predecessors who worked in the same compound three decades ago.

Now rewind to 1990. This same plot of land was a shuttered cotton mill. Idle looms sat in cavernous sheds. Soot-stained chimneys pointed at a sky that no longer needed them. The workers who once operated those machines had been dispersed years earlier by the longest textile strike in Indian history. The compound smelled of rust, damp cotton, and abandonment. Stray dogs dozed in the shade of walls that had once vibrated with the clatter of industrial machinery. No one walking past would have guessed that this decaying industrial campus would become the single most valuable piece of retail real estate in the country.

The distance between those two images is the story of The Phoenix Mills Limited. It is not, despite appearances, a real estate story. It is a platform story. The Ruia family took a dying industrial asset in the heart of India's financial capital and turned it into the physical operating system for the country's consumption boom.

Every global luxury brand that wanted to enter India eventually had to come through their doors. Apple chose a Phoenix mall for its third Indian retail store in September 2025. Starbucks, Zara, H&M, and dozens of international names established their India beachheads in Phoenix properties. When luxury conglomerates sit in Paris or Milan debating where to plant their flag in the world's fastest-growing major consumer market, the conversation inevitably turns to Phoenix.

The numbers tell only part of the tale. The Phoenix Mills today operates twelve malls spanning roughly eleven million square feet of retail space across India's top cities. Its market capitalization hovers around five hundred and sixty billion rupees, roughly six and a half billion dollars.

But the company is far more than malls. It manages an additional five million square feet of commercial office space. It runs two luxury hotels totaling nearly six hundred keys. It has developed ultra-luxury residential projects that sell at eye-watering premiums. Total consumption across its malls reached nearly fourteen thousand crore rupees in fiscal year 2025 alone, an amount that grew twenty-one percent year over year.

By 2027, management targets fourteen million square feet of retail space. By 2030, eighteen million.

But the real story is how they got here.

It involves a family that refused to sell when every rational incentive pointed toward cashing out. It involves a devastating fire that leveled a factory building with no cause ever established. It involves a year-long labor strike that killed an entire industry. It involves byzantine land regulations that trapped Mumbai's mill owners in regulatory purgatory for decades. And it involves a slow, painful pivot from selling cotton to selling experiences, with bowling alleys and nightclubs serving as unlikely stepping stones toward Gucci and Louis Vuitton.

Along the way, sovereign wealth fund partnerships with Canada's CPPIB and Singapore's GIC gave Phoenix access to global cost-of-capital in one of the world's highest interest-rate environments. A rare thing happened in Indian family-run businesses: professional management was empowered to actually run the company. And the "Long India" consumer thesis found its most direct physical expression in a chain of malls that became destinations, not just shopping centers.

This is the story of how a hundred-year-old textile mill became India's most dominant luxury mall owner, and what it tells us about the biggest consumption story of the twenty-first century.

To tell it properly, we need to start with the raw material of the story, literally. Cotton. And the city that cotton built.

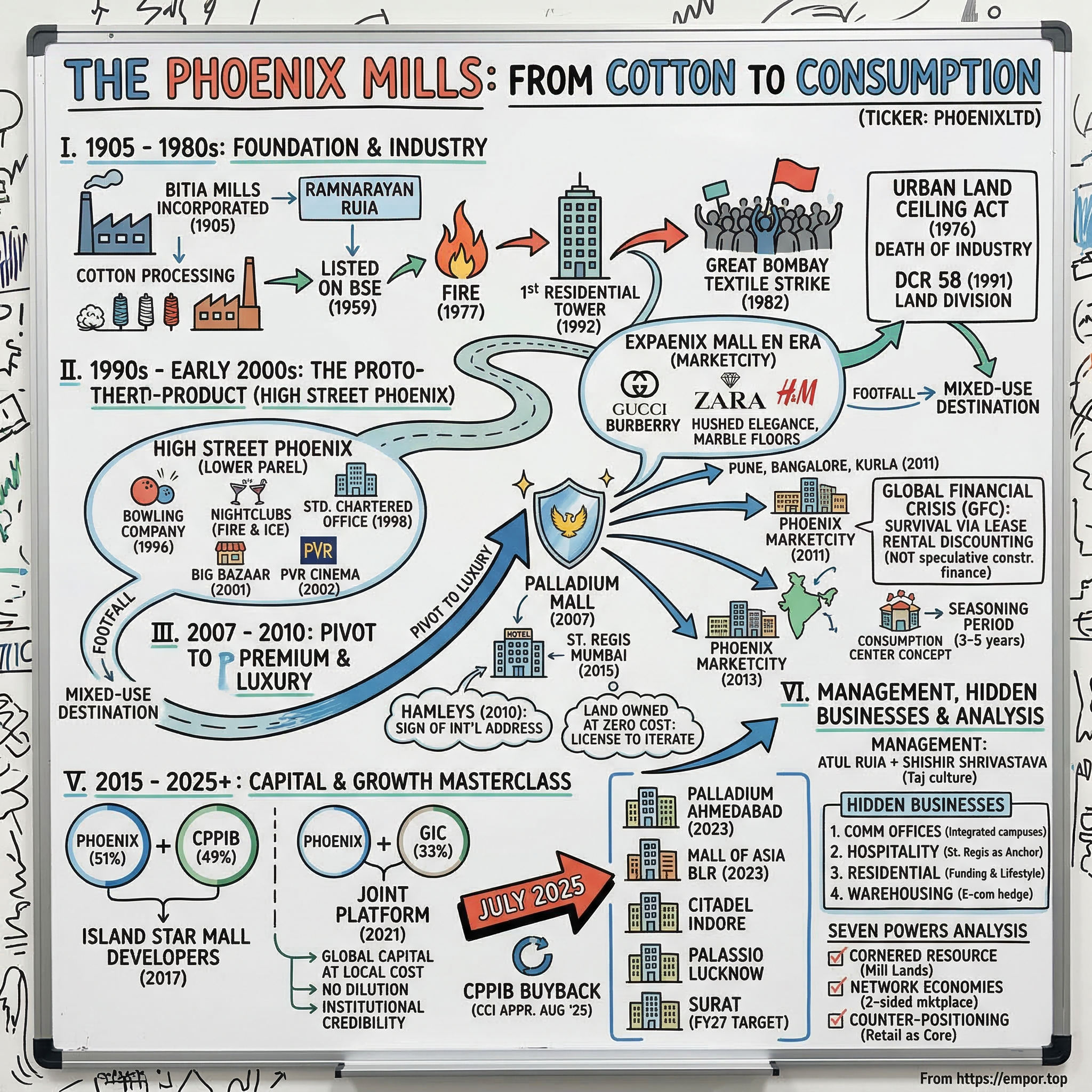

II. History: The Mill Lands and The Fire (1905 to 1990s)

To understand Phoenix Mills, you first have to understand what happened to Mumbai's textile district, because it is one of the great industrial collapses of the twentieth century, and the land it freed up reshaped the entire city.

Bombay in the early 1900s was the Manchester of the East. Dozens of cotton mills stretched across a belt from Lalbaug to Lower Parel in the city's central spine, employing hundreds of thousands of workers in a vast industrial ecosystem.

The mills were not just factories; they were communities. Workers lived in chawls, the dense tenement housing blocks, steps away from where they worked. The mills had their own hospitals, schools, and social clubs. The entire neighborhood pulsed with the rhythm of industrial life. At the peak of the industry, more than sixty mills operated within a few square miles of central Bombay. The chimneys were landmarks. The noon whistle was the neighborhood clock. Mill workers were a political constituency that could make or break state governments.

The Phoenix Mills was incorporated on January 27, 1905, originally under the name Bitia Mills, by Ramnarayan Ruia. For the better part of eight decades, it did what every other mill in the Parel-Lower Parel belt did: it processed cotton. Bleaching, dyeing, mercerizing, printing, calendering, copper roller engraving, foundry work. The Ruia family, a prominent Marwari business clan, maintained control throughout. The company listed on the Bombay Stock Exchange in 1959. It was, by any measure, an unremarkable enterprise in an industry that seemed permanent.

The first crack came in 1977, when a fire destroyed the Blower Department of Phoenix Mills. The entire four-story structure was razed. No cause was ever established, an unsettling detail that hinted at the murky politics of Bombay's industrial landscape. Approximately seven hundred mill workers and four hundred office staff were suddenly without work for three years.

The company eventually decided to replace the destroyed structure with a twenty-eight-story residential tower, completed in 1992. That decision, almost accidental, planted the first seed of the idea that this land could be something other than a factory floor. A cotton mill building goes down in flames; a residential tower goes up in its place. It was an early lesson in the alchemy of Mumbai land conversion.

But the real cataclysm was the Great Bombay Textile Strike of 1982. Led by firebrand union leader Datta Samant, it shut down virtually every mill in the city for over a year. At its peak, more than two hundred and fifty thousand workers walked off the job. The strike was ostensibly about wages, but it became an existential battle between organized labor and mill owners who were already struggling with competition from powerlooms in Gujarat and cheaper production elsewhere. Samant had earned a fearsome reputation by winning workers massive pay raises at other companies through aggressive tactics, and the textile workers believed he could do the same for them.

He could not. The strike dragged on for months, then a year, then beyond. Workers exhausted their savings. Families went hungry. And one by one, mill owners realized that this was not a negotiation; it was a farewell. The strike did not end with a victory for either side. It ended with the death of the industry itself.

Mill after mill declared itself "sick" under Indian industrial law, a designation that allowed owners to halt operations and begin the long process of shutting down. Workers drifted away to other cities or into the informal economy. The great sheds fell silent. Families who had lived in the mill neighborhoods for generations lost their livelihoods. It was a human tragedy of enormous proportions, and it left behind something that would prove equally consequential: vast tracts of urban land in the heart of what was rapidly becoming one of the most expensive real estate markets on earth.

But the land remained trapped, and this is where the story gets complicated in a uniquely Indian way. Mumbai's mill lands were subject to the Urban Land (Ceiling and Regulation) Act of 1976, which set limits on surplus urban land development. Mill owners could not simply sell their compounds to developers and walk away.

Then in 1991, the Maharashtra government introduced Development Control Regulation 58, a rule that would shape the destiny of every mill owner in the city. DCR 58 mandated that mill lands be divided into three equal parts: one-third for the mill owner to develop or sell with limited floor space index, one-third for worker housing through the state housing authority MHADA, and one-third for public open spaces.

Think of it this way: if you owned a hundred acres of mill land, you could only develop a third of it, you had to give a third to the government for public housing, and a third had to become parks. For a family sitting on prime urban land worth thousands of crore, this was a straitjacket.

The Urban Land Ceiling Act was not repealed in Maharashtra until 2007, which meant that for roughly two decades, mill owners sat on some of the most valuable urban land in Asia without a clear path to monetize it. The political battles over these regulations were fierce. Every conversion of mill land to commercial use required navigating a thicket of approvals from municipal, state, and central authorities, with labor unions, political parties, and community organizations all staking claims. The process could take years, and every step was contested.

This is the context in which Ashok Ruia, Atul Ruia's father, made the decision that would define the family's fortune. While many mill owners eventually sold their land parcels to real estate developers for quick cash, pocketing money that seemed enormous at the time but would prove to be a fraction of the land's eventual value, the Ruias decided to develop theirs themselves.

It was, on its face, an irrational choice. The Ruias were textile people, not real estate developers. They had no experience building consumer-facing properties. They did not know how to negotiate with retail tenants, manage foot traffic, or curate a brand mix. The regulatory environment was hostile and unpredictable. And the capital requirements of real estate development were enormous compared to running a mill.

But they had one advantage that turned out to be decisive: they owned the land outright, and their cost basis was effectively zero. The compound in Lower Parel, stretching across multiple acres in what was rapidly becoming one of Mumbai's most central neighborhoods as the city's commercial center migrated south from Fort and Nariman Point, was a legacy inheritance from generations of mill ownership. This meant they could afford to experiment, make mistakes, and iterate in ways that a developer who had paid market price for the land simply could not. If a bowling alley failed, they would not go bankrupt. If a nightclub concept did not work, they could try something else.

The Ruias did not arrive at a vision overnight. The pivot from B2B commodity to B2C experience happened gradually, almost organically. The residential tower built on the site of the fire was proof of concept. But the real question was what to do with the rest of the sprawling industrial campus. The answer would take another decade to fully materialize, and it would start not with luxury retail but with bowling alleys and nightclubs, in the most improbable origin story of any major Indian corporation.

III. The Proto-Product: High Street Phoenix (1999 to 2010)

Walk into a premium Phoenix mall today and you see curated luxury, gleaming surfaces, and international brands displayed with the precision of a museum exhibition. The origins of this empire looked nothing like that. They looked like a Friday night in late-1990s Mumbai, loud, messy, and full of the chaotic energy that defines the city.

In 1996, the Ruias opened South Asia's largest bowling alley inside the old mill compound. Twenty lanes. The Bowling Company, they called it, India's first bowling company and sports bar. It was a wild bet for a textile family, but it tapped into something real. Mumbai in the mid-nineties was a city where the new economy was creating wealth but the infrastructure of leisure had not caught up. Young, affluent South Mumbai residents who had nowhere to go on weekends suddenly had a destination.

The old mill sheds, with their high ceilings and industrial character, provided atmospheric spaces that no new construction could replicate. Nightclubs followed: Fire and Ice became one of the city's hottest spots. Discotheques with names like Ra and Aaziano filled the industrial spaces with bass-heavy music and strobe lights. Standard Chartered Bank moved its offices into part of the compound in 1998, taking thirty thousand square feet, the first sign that the compound could attract serious corporate tenants.

The compound was becoming a neighborhood. Not a planned one, but an organic, evolving ecosystem where entertainment, dining, banking, and socializing coexisted in converted industrial spaces. It was messy, but it was alive in a way that no other part of Mumbai could match. The high ceilings and raw industrial character of the old mill buildings gave the spaces a distinctive atmosphere, almost a proto-Brooklyn aesthetic before Brooklyn itself had become fashionable. Young professionals who worked in the nearby office towers of Lower Parel came for happy hour. Families came on weekends. College students came to bowl. The compound was drawing foot traffic from across the city, and foot traffic, as any retailer will tell you, is the lifeblood of commerce.

Then came Big Bazaar in 2001, Kishore Biyani's revolutionary hypermarket concept. Its very first location was at Phoenix's compound. This was not luxury retail. This was mass-market, pile-it-high, sell-it-cheap Indian retail at its most chaotic and energetic. Housewives from across Mumbai made pilgrimages to Big Bazaar during its Wednesday sales events. The crowds were enormous, the aisles were packed, and the energy was electric. But from Phoenix's perspective, what mattered was footfall, the sheer number of people walking through the compound every day.

An eight-screen PVR cinema multiplex followed, along with Galaxy Entertainment gaming arcade, sports bars, and a growing roster of restaurants. By the mid-2000s, the compound had grown to approximately three million square feet and had become, almost by accident, Mumbai's most vibrant mixed-use destination.

But here is where the story takes its most important turn, the one that separates Phoenix from every other mall owner in India. The Ruias looked at what they had built and realized they were playing in the wrong lane.

Mass-market retail was a commodity. Anyone with enough square footage could put in a Big Bazaar and a cinema. The margins were thin, the tenants had leverage because they could relocate to any number of comparable spaces, and the experience was not defensible.

What nobody in India was doing well was premium and luxury retail. The international brands wanted in. India's growing upper-middle class, flush with IT salaries and stock market gains, wanted to shop like they did on trips to Singapore and Dubai. But there was nowhere for these two groups to meet.

The malls that existed in India in the mid-2000s were either too downmarket or too poorly managed to attract genuine luxury tenants. International luxury brands have exacting standards: precise climate control, ceiling heights above a certain minimum, corridor widths that create a feeling of spaciousness, security arrangements, and neighboring tenants that enhance rather than diminish their brand perception. Most Indian malls of that era could not meet these requirements. The buildings were functional but uninspired, the common areas were poorly maintained, and the tenant mix was haphazard.

The Ruias saw this gap and drove straight through it. The creation of Palladium Mall in 2007, built within the same Lower Parel compound, was not just another floor of shops. It was a deliberate repositioning of the entire property toward premium consumption.

The compound was bifurcated into two distinct worlds. Palladium handled luxury and premium brands in an environment of hushed elegance, marble floors, and carefully designed lighting. The Grand Galleria, on the other side, continued to serve the broader market with its mass-market retailers and entertainment anchors.

Burberry came in. Zara arrived. Over five hundred stores eventually populated the complex. High Street Phoenix became the undisputed center of gravity for South Mumbai's retail ecosystem, the place where a Goldman Sachs analyst could buy a bespoke suit on one floor and her driver could shop at Big Bazaar two buildings away.

The hotel partnership deepened the strategy further. Phoenix partnered with Shangri-La Hotels and Resorts in 2007 to operate a five-star hotel on the property. That deal would eventually evolve into The St. Regis Mumbai under Marriott's management, opening in 2015 with three hundred and ninety-five keys, ten restaurants, and over forty thousand square feet of banquet space. The hotel was not just a hospitality asset. It was an anchor that cemented the compound's identity as a premium destination and brought a constant stream of affluent business travelers through the retail floors below.

When Hamleys, the legendary British toy retailer, opened its first Indian store at High Street Phoenix in 2010, it was a symbolic milestone that signaled to international retailers: this is the address in India.

The capital efficiency of this entire evolution cannot be overstated. Because the Ruias owned the land with an effective cost basis of zero, inherited from their textile mill forebears, they could absorb the years of experimentation with bowling alleys and nightclubs, the pivot to premium, and the massive construction costs of Palladium without the crushing debt burden that would have destroyed a developer who had purchased the land at market rates. Their legacy ownership of mill land was not just an asset; it was a license to iterate. They could afford to be wrong multiple times and still arrive at the right answer, which is exactly what happened.

There is an important lesson here about how great businesses are often built. The Ruias did not start with a twenty-year strategic plan for luxury retail dominance. They started with a bowling alley. They iterated. They watched what worked and what did not. They noticed that the premium positioning generated higher margins and more defensible competitive advantages than mass-market retail. And they pivoted, not all at once, but gradually, letting the market teach them where the opportunity lay. The best strategies are often discovered, not designed.

By 2010, the proof of concept was complete. High Street Phoenix had demonstrated that a single compound could combine retail, entertainment, dining, hospitality, and commercial office space into an integrated ecosystem that was worth more than the sum of its parts. The question every ambitious operator eventually faces had arrived: could this model travel beyond its original home?

IV. The Expansion Era: Marketcity and the GFC (2010 to 2015)

The decision to expand beyond Mumbai was made years before the first Phoenix Marketcity mall opened its doors. In 2005, management began acquiring land parcels in four cities: Kurla in Mumbai's eastern suburbs, Viman Nagar in Pune, Whitefield in Bangalore, and Velachery in Chennai. The strategy was straightforward in concept but audacious in execution: copy the High Street Phoenix model, adapt it for different micro-markets, and create a branded chain of consumption centers across India's top cities. Four simultaneous land acquisitions. Four different regulatory environments. Four different consumer demographics. For a company that had only ever operated in one location, it was a bet-the-company moment.

The timing was terrible, and then it was perfect.

The land acquisitions happened during India's real estate boom of the mid-2000s, when prices were reasonable and optimism was high. Credit was flowing freely. India's GDP was growing at nine percent. Property prices in major cities were doubling every few years. Everything seemed possible.

Then the Global Financial Crisis hit in 2008, and the Indian real estate sector went into cardiac arrest.

To understand how Phoenix survived the GFC while so many peers did not, you need to understand the dominant business model of Indian real estate at the time. Most developers operated on what amounted to a Ponzi-like structure, even if it was entirely legal. They would take construction loans from banks, use those loans to build residential towers, sell apartments off-plan to generate cash before construction was finished, and use the proceeds to service debt and fund new projects. As long as apartment prices kept rising and buyers kept showing up with down payments, the model worked beautifully. When credit markets seized up in 2008 and buyers vanished, it imploded spectacularly.

DLF, India's largest real estate company, had listed at astronomical valuations in 2007 and then watched its stock collapse by over eighty percent as the debt-fueled residential boom unraveled. Unitech, another major developer, would eventually face criminal charges against its founders for diverting homebuyer funds. Jaypee Group, Amrapali, HDIL, the list of casualties was long. The entire sector was built on a model of rolling short-term debt against long-term assets, and when the music stopped, there were not enough chairs.

Phoenix was different, and the difference came down to the type of debt it carried. While its peers had loaded up on construction finance for speculative residential projects, Phoenix's borrowings were primarily structured as lease rental discounting.

This is a concept worth understanding because it explains not just Phoenix's GFC survival but its entire financial philosophy. In lease rental discounting, a bank lends against the steady stream of rental income from occupied commercial properties. The bank looks at the signed lease agreements, the track record of rental payments, and the quality of the tenants, and lends a multiple of that annual rental income.

This is a fundamentally different risk profile from construction finance. A construction loan is a bet on a future outcome: will the building get finished, and will buyers show up? Lease rental discounting is a bet on an existing reality: tenants are already paying rent. The cost of capital is lower, the terms are longer, and the likelihood of a sudden margin call is dramatically reduced. Think of it as the difference between a bank lending against your salary versus lending against your business plan. One is predictable; the other is a prayer.

This did not mean Phoenix emerged from the crisis unscathed. The expansion timeline was delayed, and the early years of the new malls were challenging as consumer confidence took time to recover. But Phoenix survived, and in real estate, survival during a credit crisis is not just survival. It is competitive advantage. When the dust settled, many of Phoenix's would-be competitors had been wiped out or severely weakened, leaving fewer players to compete for premium tenants and consumer attention in the recovery.

In 2011, three Phoenix Marketcity malls opened simultaneously in Pune, Bangalore, and Kurla. It was a bold statement: three new malls in three different cities, all in the same year. The logistics alone were staggering, coordinating hundreds of tenants, thousands of construction workers, and millions of square feet of fit-out across three states with different regulatory regimes and labor markets.

Chennai followed in 2013. By the end of fiscal year 2013, the operating retail portfolio had reached approximately five million square feet of gross leasable area. The company had gone from a single-asset operator in South Mumbai to a multi-city platform in just two years. The "Phoenix" brand, previously synonymous only with Lower Parel, now meant something in Pune, Bangalore, and Chennai as well.

The Marketcity brand represented a deliberate positioning choice, and it is important to understand what it was and what it was not.

These were not replicas of Palladium. Marketcity malls were larger, more mass-market oriented, designed to serve the broad middle class of India's Tier-1 cities rather than the ultra-affluent South Mumbai crowd. The tenant mix leaned toward popular fashion brands, mid-range restaurants, and family entertainment rather than luxury boutiques. They combined fashion retail with heavy food and beverage components and entertainment anchors, particularly PVR cinema multiplexes.

The thesis was what management called the "Consumption Center" concept. The idea is deceptively simple but strategically profound: a mall should not be a place you go to buy a shirt. It should be a place you go to spend an afternoon or an evening, eating, watching movies, bowling, shopping, and socializing. The longer a visitor stays, the more they spend. Every anchor tenant that drives footfall, whether a cinema or a food court, creates spillover traffic for every other store in the mall. The cinema does not need to be hugely profitable on its own; it needs to put five thousand people into the building every evening who then walk past a hundred stores on their way in and out.

The Kurla mall provided an important lesson in the difficulty of replicating success. Location for a mall is not just about the pincode. It is about micro-market accessibility: how easy is it for your target customer to actually get there? Kurla, despite being technically in Mumbai, sits in a congested part of the city where traffic patterns and public transit connectivity are fundamentally different from the easy access that Lower Parel enjoys from South Mumbai's affluent neighborhoods. Getting to Kurla from Bandra or Andheri during rush hour could take an hour. Getting to Lower Parel from those same neighborhoods took twenty minutes.

The mall performed well over time but took significantly longer to ramp up than its peers, teaching management that not all Mumbai locations are created equal and that a catchment area's accessibility matters as much as its demographics.

The period from 2013 to 2016 was one of consolidation. The four new malls needed time to "season," a retail real estate concept describing the process by which a mall transitions from being a new and uncertain venue to an established part of the local landscape. Seasoning typically takes three to five years. During this period, rental rates are below long-term potential, occupancy may fluctuate as initial tenants churn, and the operator is essentially investing in building a brand and a community around the property.

Phoenix used this seasoning period to refine its operational playbook. They learned which tenant categories drove the most footfall. Fast fashion brands like Zara and H&M were magnets for younger shoppers. Multiplex cinemas drove evening and weekend traffic. Food courts needed to be large enough and diverse enough to serve as destinations in their own right, not afterthoughts tucked into a basement corner.

They learned how to structure lease agreements with the right mix of minimum guaranteed rent, which provides baseline income security, and revenue-sharing, which gives the landlord upside when tenants do well. They learned how to manage the complex logistics of a large retail property where everything from air conditioning to parking to security has to work seamlessly for the tenant and consumer experience to succeed.

By the mid-2010s, Phoenix had proven that its model could work beyond Lower Parel. But it had also reached the limits of what it could do with its own balance sheet. The next phase of growth would require a different kind of capital, and finding it would become the defining chapter of the Phoenix story.

V. The Capital Allocation Masterclass (2015 to 2025)

If there is a single chapter in the Phoenix Mills story that separates it from every other Indian real estate company, it is how management raised and deployed capital during the decade from 2015 to 2025. This is where the company transitioned from being a "developer" to being an "asset manager," and it happened through a series of partnerships that were elegant in structure and decisive in impact.

The fundamental problem facing any Indian real estate company that wants to grow is the cost of capital. India's benchmark lending rates have historically hovered between eight and twelve percent. If you are building a mall that takes three to four years to construct and another three to five years to season, you are paying high-cost interest on an asset that will not generate meaningful cash flow for six to eight years.

Run the math: if you borrow a thousand crore at ten percent and generate no income for six years, your principal has compounded to nearly eighteen hundred crore before the first rent check arrives. Your mall has to generate eighty percent more rental income than you originally projected just to break even on the financing costs.

The math is brutal. It is the central challenge of commercial real estate in a high-interest-rate emerging market. It is why so many Indian developers load up on residential sales to cross-subsidize their commercial builds, and it is why so many of them eventually get into trouble when the residential cycle turns.

Phoenix Mills found a different path. In 2017, Canada Pension Plan Investment Board, one of the world's largest pension funds managing over five hundred billion dollars in assets for Canadian retirees, partnered with Phoenix to create Island Star Mall Developers Private Limited. The structure was notable. CPPIB took a forty-nine percent stake, Phoenix retained fifty-one percent, keeping operational control.

This was not a passive financial investment where a fund writes a check and checks back in five years. It was a strategic platform designed to develop and operate retail-led mixed-use projects across India. The initial portfolio included Phoenix Marketcity Bangalore, with subsequent additions in Wakad (Pune), Hebbal (Bangalore), and Indore.

The genius of this structure was threefold, and each element addressed a specific weakness in Phoenix's strategic position.

First, it brought in capital at a cost dramatically below what Phoenix could access in Indian debt markets. Canadian pension money costs perhaps three to four percent, less than half the rate Phoenix would pay at an Indian bank. Over a six-to-eight-year development and seasoning cycle, that difference in cost of capital is the difference between a project that generates twenty percent returns and one that generates ten percent.

Second, the partnership did not dilute the listed entity. The partnership existed at the project level, not at the holding company level, so public shareholders were not affected. Phoenix kept its listed share count unchanged while gaining access to hundreds of millions of dollars in development capital.

Third, it brought global institutional credibility. When CPPIB puts its name on a deal, it signals to every other global investor, every international tenant, and every Indian bank that the governance, the accounting, and the asset quality have been vetted to international standards.

In 2021, CPPIB committed an additional one hundred and thirty-one million dollars to the platform, funding the expansion into new cities. That same year, Singapore's sovereign wealth fund GIC entered the picture with an even larger deal. GIC and Phoenix established a retail-led mixed-use investment platform with an initial portfolio valued at seven hundred and thirty-three million dollars. GIC acquired a twenty-six percent equity stake, later increased to roughly thirty-three percent in a second tranche in July 2022, with Phoenix contributing its Marketcity malls in Mumbai and Pune along with commercial assets including Art Guild House, Phoenix Paragon Plaza, and Centrium in Mumbai, totaling approximately three and a half million square feet.

Step back and consider what had happened. Two of the world's most sophisticated institutional investors, managing a combined two trillion dollars in assets, had effectively validated Phoenix's operating model and management team. These are investors who perform months of due diligence, who scrutinize governance structures with forensic intensity, and who can put money anywhere in the world. They chose Phoenix.

For a mid-cap Indian real estate company with a legacy as a textile mill, this was an extraordinary endorsement. It was also a powerful competitive advantage. Try getting a meeting with a global luxury brand to pitch your mall as their India launch location. Now try it with "our partners include the Canadian and Singaporean sovereign wealth funds" on your slide deck. The credibility effect was immediate and measurable.

But the truly interesting capital allocation decision came in July 2025, when Phoenix announced it would buy back CPPIB's entire forty-nine percent stake in Island Star Mall Developers for approximately five thousand four hundred and forty-nine crore rupees, roughly eight hundred and seventy million Canadian dollars. The Competition Commission of India approved the deal in August 2025, with the first tranche completed before November 2025 and subsequent tranches structured over three years.

Why buy back a stake that had served the company so well? The answer reveals management's confidence in the current phase of the business, and it is worth dwelling on because the logic is instructive.

When Phoenix brought in CPPIB in 2017, it needed growth capital and institutional validation. The assets were in development or early-stage operation. The risk was high, the cash flows were uncertain, and Phoenix could not afford to fund the build-out alone. Sharing forty-nine percent of the upside with a partner was a rational trade for survival and scale.

By 2025, the calculus had changed completely. The assets in the ISMDPL portfolio were mature, generating strong rental income, and no longer required partner capital for development. The risk had been substantially de-risked. Buying back the stake meant Phoenix would capture one hundred percent of the cash flows from these assets going forward, at a price that reflected mature asset values rather than speculative future potential.

It was a signal that management believed the "harvest phase" was just beginning, the phase where completed, seasoned malls throw off growing rental income year after year with relatively modest ongoing capital requirements. CLSA, the Asia-focused brokerage, upgraded Phoenix's stock rating following the announcement, recognizing the accretive nature of the buyback.

The company's recent expansion tells a consistent story of aggressive but disciplined growth. Palladium Ahmedabad opened in February 2023, bringing over thirty-five luxury brands to Gujarat for the first time. Phoenix Mall of Asia, a massive thirteen-acre property in Hebbal, north Bangalore, with 1.2 million square feet of retail space and over four hundred and forty brands, opened in October 2023. Phoenix Citadel Indore became central India's largest shopping destination. Phoenix Palassio Lucknow became operational in a record twenty-four months from acquisition, featuring architecture blending European and Awadhi influences.

A seven-acre parcel in Surat acquired in December 2022 for approximately five hundred and ten crore rupees is earmarked for a premium retail destination expected by fiscal year 2027. In fiscal year 2025 alone, the company invested approximately twenty-six hundred crore rupees on acquisitions and construction, with an additional sixteen hundred crore going into land purchases in Coimbatore, Chandigarh, Bangalore, and Mumbai.

The company's approach to acquisitions is distinctive and worth understanding: Phoenix rarely buys finished assets. Instead, it acquires brownfield or greenfield land parcels and builds from scratch. This carries higher execution risk, as construction timelines, regulatory approvals, and cost overruns can all go wrong.

But it creates a massive yield-on-cost advantage. Think of it like the difference between buying a rental property that is already leased versus buying an empty lot and building the rental property yourself. In the first case, you pay a price that reflects the full value of the existing rental stream, and your yield is modest. In the second case, your all-in cost may be a fraction of the completed asset's value, and the yield on your invested capital can be dramatically higher. Management has targeted returns on capital employed of twenty percent or higher on new developments, a number that would be impossible to achieve by buying stabilized assets at market prices.

The capital structure today reflects a company that has learned how to use different pools of capital for different purposes: sovereign wealth fund partnerships for growth-phase assets, internal accruals for land acquisition, and lease rental discounting from Indian banks for stabilized properties. Net debt to EBITDA sits at approximately one point eight times, a comfortable level for an asset-heavy business that provides room to absorb the inevitable construction delays and economic cycles that come with large-scale development.

The key financial question for investors to monitor is the trajectory of capital expenditure relative to operating cash flow. This is a company in investment mode, spending aggressively to build the next generation of malls in cities where premium retail space is virtually non-existent. The question is whether the new assets can ramp up quickly enough to convert investment into positive free cash flow before the next inevitable economic downturn tests the balance sheet. The CPPIB buyback adds near-term leverage, and the three-year payment structure reflects management's awareness of this dynamic.

VI. Management and Governance: The Ruia Plus Shrivastava Model

In Indian real estate, governance is often the weakest link. Family-run companies with opaque related-party transactions, aggressive accounting, and promoters who treat the listed entity as a personal piggy bank have given the sector a well-deserved reputation for poor corporate governance. The horror stories are legion: diverted homebuyer funds, shell company transactions, undisclosed liabilities, and promoters who live like maharajas while minority shareholders watch their investments evaporate.

Phoenix Mills has not been perfect, but it has distinguished itself through a management structure that is unusually professional for the industry, and understanding that structure is essential to understanding the investment case.

Atul Ruia is the architect of the modern Phoenix Mills. Educated at the University of Pennsylvania with a chemical engineering degree and an MBA from the Wharton School of Finance, he joined the family business in 1994 and was appointed to the board in 1996. He was in his mid-twenties when he took charge, inheriting a shuttered textile mill and a regulatory morass that would have discouraged most people from even trying.

The fact that he chose to build a consumption center rather than sell the land to a developer reflects both ambition and an instinct for the long game that is rare in Indian business families, where the temptation to monetize assets quickly is enormous. Every few months, a developer or private equity fund would have shown up with a check for the land. Every time, the Ruias said no.

Atul's most important decision may have been stepping back. He retired as Managing Director in December 2019 at the age of forty-eight, remaining as Non-Executive Chairman. This was not a forced exit or a health-related decision. It was a deliberate choice to transition the company from founder-led to professionally managed while the founder was still young and healthy enough to provide strategic guidance.

In the Indian context, where business patriarchs routinely cling to executive roles into their seventies and eighties, a forty-eight-year-old chairman stepping back to let professionals run the show is genuinely remarkable. His family's promoter holding, at approximately forty-seven percent through Ruia International Holding Company and related entities, ensures alignment between the controlling family and minority shareholders. His net worth, estimated at approximately twelve hundred crore rupees, is overwhelmingly tied to Phoenix Mills stock.

The person who ran the day-to-day operations for over two decades was Shishir Shrivastava, and his story is equally important. Shrivastava is not a Ruia. He is not related to the family. He is a hotel management graduate from IHM Bangalore, class of 1997, who started his career as a catering assistant and management trainee at the Taj Hotels.

The Taj is India's most storied hospitality brand, and its training program is legendary for instilling a culture of meticulous service and attention to detail. Shrivastava absorbed that culture before joining the Phoenix Group in 2000, when the compound was still more bowling alley than luxury mall.

Over twenty-five years at Phoenix, he rose through every meaningful role: Vice President of Business Development and Projects, Chief Executive of Hospitality and New Initiatives, Executive Director, Joint Managing Director, and finally Managing Director and CEO. Think of the Atul-Shishir dynamic as analogous to the Steve Jobs and Tim Cook partnership at Apple. Atul was the visionary who saw what the mill compound could become. Shishir was the operator who figured out how to make it work at scale, city after city, mall after mall.

He was instrumental in shaping the tenant mix at High Street Phoenix, orchestrating the hotel development, managing the pan-India Marketcity rollout, and structuring the complex capital partnerships with CPPIB and GIC. His hospitality background gave him an instinct for service quality and customer experience that most real estate executives lack. When a visitor walks into a Phoenix mall and notices that the air conditioning is perfect, the restrooms are spotless, and the security guards are polite, that is the Taj Hotels training expressing itself through a different medium.

In October 2025, Shrivastava was elevated to Non-Executive Vice Chairman, effective until September 2027, with operational responsibilities transitioning to Rajesh Kulkarni and Rashmi Sen, designated as Whole-time Directors and Key Managerial Personnel. This was a carefully managed succession, not an abrupt change, and it signals that Phoenix is building institutional depth rather than remaining dependent on one or two individuals.

The compensation structure at Phoenix has been notable for its reliance on equity-linked incentives. Heavy ESOP allocations and performance-linked pay for senior management create alignment between executives and shareholders in a way that fixed-salary structures do not.

Why does this matter? Because in most Indian real estate companies, the professional manager is a hired hand who executes the promoter's vision but has no real stake in the outcome. Their incentive is to keep the boss happy, not to maximize long-term value. At Phoenix, the ESOP structure means that when the stock does well, senior managers benefit directly. When it does not, they feel the pain. This is rare in Indian real estate, where promoter families often micromanage operations and resist empowering professional managers with meaningful equity stakes, fearing dilution of control.

There is a cultural dimension here that matters enormously for the long-term investment case. Real estate in India is traditionally a "builder" business: you build something, you sell it, you move on to the next project. Every incentive in the system, from how banks lend to how customers buy to how tax laws work, is oriented toward the transaction.

Phoenix has deliberately cultivated an "operator" culture: you build something, you maintain it, you upgrade it, you optimize the tenant mix, you invest in the customer experience year after year. The difference is the difference between a contractor and a brand. Contractors compete on price. Brands compete on trust and experience. It is this cultural shift, more than any single financial decision, that separates Phoenix from the pack and makes its competitive advantages durable rather than transient.

VII. The Hidden Businesses

When most investors think of Phoenix Mills, they think of malls. That is understandable, as retail is the core business and the brand's public identity. But the company has quietly built three additional business lines that are increasingly material, and understanding them reveals the full strategic picture.

The first and most strategically important is commercial offices. Phoenix has been systematically building office space on top of and adjacent to its mall properties, creating integrated campuses where people can live, work, shop, and socialize without leaving the compound.

The completed office portfolio now spans approximately four point eight million square feet across Mumbai, Pune, Bangalore, and Chennai. Key assets include Art Guild House, an eight-hundred-thousand-square-foot premium office complex at Phoenix Marketcity Kurla distinguished by elaborate art installations throughout the building that make it feel more like a gallery than a corporate tower. Phoenix Paragon Plaza and Centrium in Mumbai round out the portfolio. Office income reached approximately two hundred and ten crore rupees in fiscal year 2025, up ten percent year over year, with EBITDA of one hundred and thirty-one crore, up nineteen percent.

Why does a mall company want to be in the office business? The strategic logic is straightforward but powerful. Retail is inherently cyclical. Consumer spending fluctuates with economic conditions, festive seasons, and sentiment. A bad monsoon, a stock market correction, or a national mood of austerity can all dent mall revenues.

Office leases, by contrast, are typically three to nine years in duration with built-in annual escalation clauses of five to fifteen percent. They provide a steady, predictable stream of annuity income that stabilizes the company's cash flows when retail is volatile. Moreover, office tenants create a captive daytime population for the mall: thousands of professionals who eat lunch, grab coffee, shop during breaks, and bring their families on weekends. Every office building is a footfall generator for the retail asset below it.

Management targets seven million square feet of office space by 2027, which would make the commercial portfolio nearly as large as the retail one by area, though not by revenue. If they hit that target, Phoenix will be running a dual-engine business: retail for growth and excitement, offices for stability and predictability. It is a hedge that most pure-play mall operators do not have.

The second hidden business is hospitality, and it centers on what is arguably the crown jewel of the entire Phoenix portfolio. The St. Regis Mumbai, located atop Palladium Mall in Lower Parel, is a three-hundred-and-ninety-five-key uber-luxury hotel operated by Marriott International under its most prestigious brand. It features ten restaurants, over forty-two thousand square feet of banquet space, a spa, pool, nightclub, and business club. It is widely regarded as one of the best-performing hotels in Mumbai, a city with no shortage of luxury hotels.

The Courtyard by Marriott in Agra, with one hundred and ninety-three keys located two kilometers from the Taj Mahal, rounds out the hospitality portfolio at five hundred and eighty-eight keys across two properties, owned through subsidiary Pallazzio Hotels and Leisure Limited.

The hotel business is not primarily a standalone profit center, though it generates healthy returns. Its primary function is strategic, and this is a distinction that many investors miss. A world-class hotel anchors the entire Lower Parel compound at the premium end. Business travelers staying at The St. Regis walk downstairs to Palladium for shopping. Corporate events held in the banquet halls drive traffic to restaurants. Wedding receptions bring hundreds of affluent guests into the compound who might not otherwise visit.

The hotel creates a halo effect that elevates every other asset in the compound. It is the reason Gucci is comfortable being there: a five-star hotel next door signals that this is a location worthy of their brand. No amount of marble flooring in a mall can substitute for an actual St. Regis connected by an elevator. The hotel is not a separate business; it is a force multiplier for the entire ecosystem.

The third business, and the one that has most directly supported Phoenix's capital-intensive expansion, is residential development. The key projects are One Bangalore West and Kessaku, both in Rajajinagar, Bangalore.

Kessaku is the more remarkable and worth describing because it encapsulates the Phoenix approach. Spread over four and a half acres, it features five exclusive towers with names drawn from the five natural elements in Japanese: Sora, Niwa, Mizu, Faia, and Zefa. The name itself, Kessaku, means "masterpiece" in Japanese. Units range from four to six bedrooms, priced from four and a half crore to over twenty-three crore rupees. These are not mass-market apartments; they are lifestyle statements.

The residential strategy at Phoenix is distinctive because the company only builds residential projects around its existing mall and hotel properties. It sells the "Phoenix Lifestyle," where your home is a short walk from the best mall, the best restaurants, and a five-star hotel. This allows it to command a significant premium over standalone residential projects.

More importantly, residential sales generate immediate cash flow, cash that arrives years before a new mall starts generating meaningful rental income. It is a self-funding ecosystem: sell apartments to finance the mall, use the mall to drive hotel occupancy, use the hotel to attract premium tenants, use the premium tenants to justify higher residential prices for the next project. Each piece of the puzzle feeds the others.

The fourth and newest business line is warehousing and logistics. Phoenix incorporated Phoenix Logistics and Industrial Parks Private Limited in September 2022 and acquired Janus Logistics and Industrial Parks Private Limited in January 2023. This is a nascent bet on India's rapidly growing logistics infrastructure needs, driven by e-commerce growth and supply chain modernization.

It is too early to assess whether this will become a material business. The risk is that it represents a distraction from core competencies, pulling management attention and capital away from what Phoenix does best. The opportunity is that Phoenix's land acquisition skills and construction capabilities could translate effectively into a sector with enormous demand-supply gaps, as India's warehousing infrastructure struggles to keep pace with the explosion of e-commerce. Management has not yet disclosed detailed plans or financial targets for this vertical, so investors should watch for clarity in coming quarters.

There is an irony here worth noting: the very e-commerce trend that threatens Phoenix's retail malls is also the force driving demand for the warehousing business. If online shopping continues to grow, warehousing needs grow with it. Phoenix may be hedging its bets, building physical infrastructure for both sides of the retail equation.

What ties all four businesses together is the integrated mixed-use model. Phoenix does not build standalone malls or standalone hotels or standalone office parks. It builds ecosystems where each component reinforces the others, creating a flywheel of footfall, spending, and brand equity that is very difficult for single-purpose competitors to replicate.

VIII. Analysis: The Seven Powers

Hamilton Helmer's Seven Powers framework provides a useful lens for analyzing whether Phoenix Mills' competitive advantages are durable or transient. For readers unfamiliar with the framework, Helmer identified seven types of strategic power that enable a company to earn persistently higher returns than its competitors: Scale Economies, Network Economies, Counter-Positioning, Switching Costs, Branding, Cornered Resource, and Process Power. Not every company possesses all seven, and not every power is equally relevant. Phoenix has a strong case for at least three of them.

The most obvious power is Cornered Resource. The mill land in Lower Parel is a classic non-reproducible asset. You cannot create more land in the heart of Mumbai. The specific plot that houses High Street Phoenix, Palladium, and The St. Regis exists because of a century of industrial history, a devastating textile strike, byzantine regulatory frameworks, and a family that chose development over sale.

No competitor can replicate this combination. Anyone wanting to build a comparable retail destination in South Mumbai would need to acquire land at current market prices, which in Lower Parel now run into the tens of thousands of rupees per square foot. At those prices, the economics of building a new premium mall are virtually impossible. The rent you would need to charge to earn a reasonable return on the land cost alone would be higher than what even the most premium tenants would pay.

The land is the moat, and it is a moat that gets deeper every year as Mumbai grows denser and more expensive. Every new skyscraper built nearby, every new metro line opened, every corporate office that relocates to Lower Parel makes Phoenix's existing asset more valuable and a competitor's hypothetical new entry more prohibitively expensive.

The second power is Network Economies, and it operates in a subtle but powerful way. A premium mall is a two-sided marketplace, much like a dating app or a credit card network. On one side are brands, which need foot traffic and the right demographic. On the other side are consumers, who want access to the brands they aspire to. Each side reinforces the other.

When Apple chose Phoenix Mall of Asia in Bangalore for its third Indian retail store in September 2025, leasing eight thousand square feet at an annual rent of approximately two crore rupees, it was making a statement about where affluent Indian consumers shop. That statement, in turn, attracts more affluent consumers, which attracts more premium brands, which attracts more consumers. The flywheel is self-reinforcing.

This network effect is visible in the pricing data. Phoenix malls reportedly command rental rates thirty to fifty percent above market averages for comparable retail space. That is an astonishing premium in an industry where landlords typically compete aggressively on price to fill vacancies.

Brands pay this premium not because the physical space is thirty percent better, but because the network of other brands and consumers in the mall creates value that no individual tenant could generate on its own. A Louis Vuitton store in a standalone location draws one type of traffic. A Louis Vuitton store next to Gucci, Burberry, and an Apple store, inside a mall connected to The St. Regis hotel, draws a fundamentally different and more valuable audience. The network is the product.

The third power is Switching Costs, which operate primarily on the tenant side. Once a luxury brand has invested in fitting out a store in a Phoenix mall, with custom interiors that might cost several crore rupees, trained staff who know the local clientele, established customer relationships, and integrated inventory management, the cost of leaving is enormous.

Beyond the sunk financial cost, there is the relationship cost: the brand has built a customer base that associates it with that specific location. Moving to a different mall means starting that relationship-building process from scratch, with no guarantee that the new location will deliver comparable footfall or the right demographic mix. For a luxury brand, the wrong location is not just unprofitable; it is brand-damaging.

There is also a compelling case for Counter-Positioning relative to Phoenix's primary competitors, and this is perhaps the most underappreciated of its competitive advantages.

Consider the competitive landscape. DLF has significant retail assets like Mall of India in Noida and Emporio in Delhi, but retail is a supporting business for its massive residential and office portfolio. When DLF's management team wakes up in the morning, they are thinking about residential launches and office leasing. Mall operations are a secondary priority.

Prestige Estates in Bangalore is diversified across residential, commercial, and retail with no singular focus on malls. Brigade Enterprises is similar. Both are excellent companies, but neither has organized its entire corporate strategy around being the best mall operator in the country.

Nexus Select Trust, backed by Blackstone, is the closest comparable as India's only listed retail-focused REIT with seventeen malls, but its REIT structure requires distributing most of its income to unitholders, limiting its ability to reinvest aggressively in new development.

Phoenix's counter-position is that it treats retail as the core, not the appendage. Others build malls to help sell houses. Phoenix builds houses to help fund malls.

This inversion of priorities has profound operational consequences. Phoenix invests more heavily in mall operations, tenant curation, and consumer experience than competitors for whom retail is a secondary business line. It hires differently, budgets differently, and makes capital allocation decisions differently. The result is higher occupancy, higher rental rates, and stronger tenant retention, which compounds over time into a quality gap that becomes increasingly difficult to close. A competitor would have to reorganize its entire business model to match Phoenix's focus, which is precisely what counter-positioning is designed to prevent.

What Phoenix lacks, at least for now, is Scale Economies in the traditional sense. With twelve operational malls, it is not so large that its purchasing power or operational scale creates meaningful cost advantages. It also does not have a clear Process Power advantage, and Brand power, while strong domestically, has not been tested internationally.

The framework suggests that Phoenix's advantages are durable but concentrated: the land, the network effect, and the tenant switching costs create a defensible position in existing markets, while counter-positioning relative to diversified developers gives it an operational edge.

The critical question is whether these powers travel. In Lower Parel, the cornered resource is unassailable. In Bangalore, where Phoenix Mall of Asia has quickly established itself as a premium destination, the network effects are building. But in newer markets like Indore, Lucknow, and the planned developments in Coimbatore and Chandigarh, the company is starting from scratch. It must build network effects from zero in cities where the luxury consumer base is thinner and the brand recognition is lower. The Seven Powers analysis suggests that Phoenix's existing assets are deeply moated, while its expansion assets carry more risk and will take years to develop comparable defensive strength.

IX. Bear Case Versus Bull Case

Every great company has a bear case, and the quality of a bear case often reveals how well you understand the bull case. Phoenix Mills is no exception.

The company's recent stock performance serves as a useful starting point for this debate. Shares declined roughly twenty-one percent from the fifty-two-week high, and three consecutive quarters of earnings misses have given ammunition to skeptics. Both the bull and bear arguments deserve serious examination.

The bear case begins with the existential question that hangs over every physical retailer on the planet: can brick-and-mortar retail survive the e-commerce onslaught? Amazon, Flipkart, and Myntra have transformed how Indians shop. The convenience of home delivery, aggressive discounting, and endless selection are structural advantages that physical stores cannot match on utilitarian purchases.

Every year, a larger share of Indian consumer spending moves online, and this trend will not reverse. If a significant enough portion of luxury and premium retail shifts to e-commerce, and there are early signs that it might as platforms like Tata CLiQ Luxury and Ajio Luxe grow rapidly, the fundamental demand for physical mall space weakens and rental growth slows or turns negative.

Phoenix's counter-argument is that premium retail is experiential in a way that e-commerce cannot replicate. You do not buy a Gucci handbag on Amazon. You walk into the store, touch the leather, try it on, and make a purchase that is as much about the experience as the product. You certainly do not try on a Cartier bracelet through a screen.

The malls are also evolving into food, beverage, and entertainment destinations that are inherently physical. You cannot eat at a restaurant through an app. You cannot watch a movie on IMAX from your couch. You cannot take your children to a play zone through a browser.

This argument has held up well so far, with consumption in Phoenix malls growing twenty-one percent year over year even as e-commerce penetration deepens. But it requires continuous investment in keeping the mall experience compelling enough to justify the trip. The moment a mall feels tired, dated, or inconvenient, the experiential advantage evaporates.

The second bear concern is key-person risk. Despite the succession from Shrivastava to Kulkarni and Sen, the company's strategy and culture were shaped by Atul Ruia and Shishir Shrivastava over two decades. Whether the next generation can maintain the same quality of capital allocation and operational excellence is an open question. The promoter holding of forty-seven percent ensures family alignment, but family alignment does not automatically translate into management competence.

Third, there is the macro risk of an Indian consumption slowdown. Phoenix's entire thesis is predicated on India's rapidly growing middle and upper-middle class spending more on discretionary consumption. If the much-discussed K-shaped recovery deepens, premium retail could feel the impact as aspirational consumers pull back. The company's recent earnings misses may be early signals that the consumption story is not as linear as the bull case assumes.

Fourth, valuation. At an enterprise value to EBITDA multiple of approximately twenty-six times, Phoenix is priced for significant growth. The stock price already reflects a lot of good news. If that growth materializes more slowly than expected, if the new malls in Ahmedabad, Indore, and Lucknow take longer to season and reach target rental yields, the stock has meaningful downside from current levels.

The market is paying a premium for execution, and execution risk in construction-heavy businesses is real. Cost overruns, regulatory delays, tenant acquisition challenges, and macroeconomic headwinds can all compress returns below expectations. When you pay a premium for perfection, anything less than perfection hurts.

Now for the bull case, and it is a powerful one.

It starts with the most important structural tailwind in global economics: India's per capita GDP trajectory. There is a well-documented pattern in economic development. As per capita income crosses the two thousand five hundred to three thousand dollar threshold, historical patterns from every Asian economy, from Japan in the 1960s to South Korea in the 1980s to China in the 2000s, show that discretionary spending explodes. This is the inflection point where a population transitions from spending almost everything on food, shelter, and basic necessities to having meaningful disposable income for branded goods, experiences, dining out, and lifestyle consumption.

India is at or near this inflection point, and Phoenix is positioned directly in the path of the resulting spending wave. The question is not whether this wave is coming. It is whether Phoenix can build fast enough to capture it.

The supply side reinforces the case dramatically. India has a staggering shortage of high-quality, professionally managed retail space. There are only about seventy to eighty operational malls in the country that would meet international standards, serving a population of one point four billion. By comparison, the United States has roughly a hundred and fifteen thousand shopping centers for three hundred and thirty million people. The denominator is enormous, and the numerator is tiny.

Phoenix, with its twelve operational malls and a pipeline targeting eighteen million square feet by 2030, commands an estimated twenty percent share of India's premium mall segment. Every new mall it opens in an underserved city is entering a market where demand dramatically exceeds supply. This is not like opening a mall in suburban New Jersey where three competitors are already within driving distance. This is like being the first company to build a proper supermarket in a town that has only ever had corner shops. The latent demand is enormous, and the supply is essentially zero.

Then there is the REIT optionality, a potential value unlock that is not yet priced into the stock. Phoenix Mills has not yet converted any of its assets into a Real Estate Investment Trust. A REIT listing would allow the company to securitize its stabilized, income-generating malls at yields that global institutional investors find attractive, unlocking significant value and providing a new source of low-cost capital.

Nexus Select Trust, backed by Blackstone, demonstrated that the market for retail REITs exists in India. Analysts have estimated that India's retail REIT market could reach eighty thousand crore rupees by 2030. If Phoenix were to REIT its mature assets while retaining ownership of development-stage properties, it could create a dual structure that offers both income through the REIT and growth through the listed development company. This optionality exists because management has not committed to a timeline, but the strategic logic is compelling and the precedent has been set.

Through the lens of Porter's Five Forces, Phoenix operates in a relatively favorable competitive environment.

Start with the threat of new entrants: it is limited by the scarcity of suitable land in prime urban locations, the massive capital requirements, and the five-to-eight-year gestation period required to develop and season a premium mall. A new competitor cannot simply decide to enter the market next quarter. They need land, capital, regulatory approvals, construction capability, tenant relationships, and years of patience.

Supplier power from construction companies and building materials providers is fragmented and manageable. No single contractor has pricing power over Phoenix.

Buyer power from tenants is moderated by the network effects discussed earlier: premium brands need to be in the best malls, giving Phoenix pricing power that would not exist in a more fragmented market.

The threat of substitutes, primarily e-commerce, is real but so far limited in the premium and luxury segments where the purchase experience matters as much as the product itself.

Competitive rivalry exists primarily with Nexus Select Trust and DLF's select retail assets, but the market is large enough and supply-constrained enough that direct head-to-head competition is limited. Phoenix and Nexus can both grow rapidly without taking market share from each other because the total addressable market is so underserved.

For investors tracking Phoenix Mills' ongoing performance, two key performance indicators stand out above all others.

The first is consumption growth: the total value of goods and services sold across Phoenix's mall portfolio. This metric, reported quarterly, captures the fundamental health of the retail ecosystem and answers the most basic question: are consumers spending more in Phoenix malls? In fiscal year 2025, total consumption reached thirteen thousand seven hundred and fifty crore rupees, representing twenty-one percent year-over-year growth. In the first nine months of fiscal year 2026, consumption hit twelve thousand one hundred and twenty-two crore, up fifteen percent. Any sustained deceleration in this metric would signal weakening demand.

The second critical KPI is gross retail collections: the total rental and revenue-share income Phoenix collects from its tenants. This metric, which reached thirty-three hundred and ten crore rupees in fiscal year 2025, up twenty-two percent, directly measures the company's ability to convert consumer spending into landlord income.

The relationship between these two KPIs is revealing. If consumption grows faster than collections, it means tenants are capturing more of the value and Phoenix is losing pricing power. If collections grow faster than consumption, Phoenix is extracting a larger share of tenant revenue, a sign of strengthening competitive position. Tracking both numbers together, quarter by quarter, gives investors the clearest possible picture of whether the Phoenix platform is getting stronger or weaker.

X. Carve Outs and Conclusion

Every now and then, a company's story reads like a novel that no editor would approve because the plot twists seem too improbable.

The arc of Phoenix Mills traces one of those stories. A cotton mill founded in 1905, devastated by a fire in the late 1970s, crippled by the longest textile strike in Indian history, trapped for decades by regulatory frameworks designed for a manufacturing economy that no longer existed, reinvented itself as the platform through which India's consumption revolution reaches its most aspirational consumers.

The Ruia family's decision to develop rather than sell was the foundational bet. Atul Ruia's Wharton-trained strategic vision set the direction. Shishir Shrivastava's twenty-five years of operational excellence, rooted in Taj Hotels discipline, turned that vision into eleven million square feet of functioning retail ecosystems across a dozen cities. The CPPIB and GIC partnerships provided global capital at local cost, enabling expansion that would have been impossible on the company's balance sheet alone. And the recent buyback of CPPIB's stake signals that management believes the best returns are still ahead.

The company is not without risks, and they are material.

E-commerce is a permanent competitive pressure that will not go away. Recent earnings misses have raised questions about near-term growth momentum. The heavy capital expenditure cycle required to reach eighteen million square feet by 2030 will continue to pressure free cash flow for years to come. Valuation multiples leave limited margin for error. And the transition from the founding leadership to the next generation of management is still in its early stages, with the true test of whether institutional culture survives the departure of its architects yet to come.

But the structural position is extraordinary, and it is worth stating plainly what Phoenix has that almost no other Indian company can claim.

It owns irreplaceable assets in India's most valuable urban markets. It has built network effects that make its malls the default destination for international brands entering the country. It has demonstrated capital allocation discipline that is genuinely rare in Indian real estate, as evidenced by the sovereign wealth fund partnerships and the disciplined expansion into new cities. And it sits at the intersection of the most powerful secular trend in the global economy: the rise of the Indian consumer, a trend that has decades of runway ahead of it.

Whether Phoenix Mills is the best way to play the "Long India" consumer story is a question each investor must answer for themselves. What is not in question is that the Ruia family took a pile of ruins in Lower Parel and built something that Gucci, Apple, and the Canadian pension system all consider essential infrastructure for the Indian century.

There is a final thought worth sitting with. In 1905, when Ramnarayan Ruia incorporated Bitia Mills, he was building infrastructure for an economy that turned raw cotton into finished textiles. A hundred and twenty-one years later, his descendants run a company that turns raw land into finished consumption experiences. The raw material changed. The skill, turning a physical asset into something more valuable than its constituent parts, stayed exactly the same.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube