Procter & Gamble Health Limited: From Merck's Asian Outpost to P&G's Vitamin Powerhouse

I. Introduction & Episode Teaser

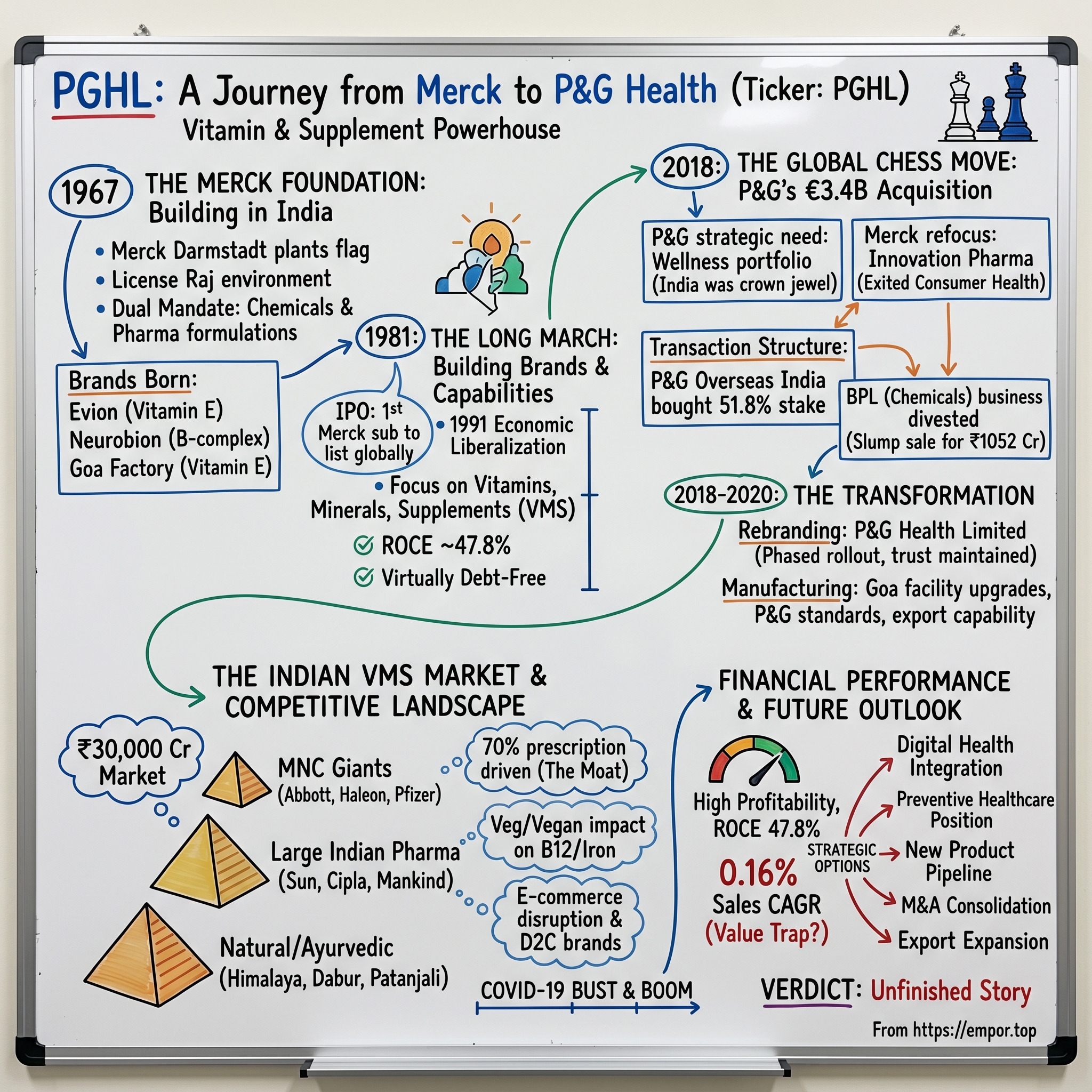

Picture this: A German pharmaceutical giant plants its flag in newly independent India in 1967, builds a chemicals-and-pharma empire over five decades, then sells it to an American consumer goods behemoth for €3.4 billion. The Indian subsidiary—now worth ₹10,517 crore on the NSE—becomes the crown jewel of vitamins and supplements in one of the world's fastest-growing health markets.

This is the story of Procter & Gamble Health Limited (PGHL), a company that has lived three distinct lives: as Merck's Asian experiment, as India's vitamin powerhouse, and now as P&G's gateway to the global supplements boom. It's a tale that spans the License Raj, economic liberalization, and the modern wellness revolution—a masterclass in patient capital, strategic pivots, and the art of building consumer trust in a B2B2C market.

The numbers tell one story: market cap of ₹10,517 crore, ROCE of 47.8%, virtually debt-free. But the real narrative lies deeper—in a Goa factory that produces 260 million ampoules annually, in doctor relationships built over decades, and in brands like Neurobion and Seven Seas that have become household names across Indian medicine cabinets.

What makes PGHL fascinating isn't just its financial performance—it's how a company manufacturing industrial chemicals in the 1960s transformed into India's leading vitamins, minerals, and supplements (VMS) player. It's about navigating India's complex pharmaceutical regulations while building consumer brands. It's about being the strategic linchpin in a global €3.4 billion acquisition that reshaped P&G's health portfolio worldwide.

Today, PGHL sits at the intersection of multiple megatrends: India's rising health consciousness, the shift from treatment to prevention, the graying population seeking wellness solutions, and the post-COVID vitamin boom. Yet it faces headwinds too—sluggish revenue growth of just 0.16% over five years, fierce competition from both multinational giants and nimble local players, and the disruption of traditional pharmacy channels by e-commerce upstarts.

This episode traces an unlikely journey from Merck's 1967 bet on post-independence India through the company's 1981 IPO (the first Merck subsidiary globally to go public), its survival through 1991's economic liberalization, and its eventual transformation under P&G's ownership. We'll explore how a B2B chemicals business built consumer health brands, why P&G paid billions for this portfolio, and what the future holds for India's VMS market.

The roadmap ahead: We'll start in 1967 with Merck's arrival in India, walk through five decades of building capabilities and brands, dissect the 2018 acquisition that changed everything, analyze the current competitive landscape, and evaluate whether PGHL can reignite growth in its new avatar. Along the way, we'll extract lessons on patient capital, global M&A with local implications, and the unique dynamics of India's healthcare market.

II. The Merck Foundation: Building in India (1967–1981)

The year was 1967. India had been independent for just two decades, Indira Gandhi had recently become Prime Minister, and the country was in the throes of the License Raj—that Byzantine system of permits, quotas, and regulations that governed every aspect of business. Foreign companies needed government approval for everything from factory locations to product pricing. Yet it was precisely in this environment that E. Merck of Darmstadt, Germany, decided to establish its Asian beachhead.

The timing wasn't accidental. Post-independence India desperately needed pharmaceuticals and industrial chemicals. The government, while suspicious of foreign capital, recognized the technology transfer imperative. For Merck, India offered something irresistible: a protected market of 500 million people, nascent local competition, and the promise of English-speaking technical talent at a fraction of German costs.

Merck's Indian subsidiary started with a dual mandate that would define its character for decades: pharmaceuticals and chemicals. This wasn't typical for Merck subsidiaries elsewhere, but India demanded flexibility. The chemicals business—producing everything from laboratory reagents to industrial compounds—provided steady cash flows and government contracts. The pharmaceutical side focused on formulations and eventually, the vitamin products that would become its calling card.

The early product portfolio reflected this duality. On one side: analytical reagents for India's growing network of laboratories, specialty chemicals for the textile and leather industries concentrated in Mumbai and Tamil Nadu. On the other: vitamin formulations, initially imported but increasingly manufactured locally as the company built capabilities. The strategy was deliberate hedging—if pharmaceutical regulations tightened, chemicals would cushion the blow; if industrial demand weakened, healthcare products would compensate. The company's decision to go public in 1981 was unprecedented—the first Merck subsidiary globally to list on a stock exchange. In its first year, the company had 115 employees, which rose to more than 1,000 the following year. This wasn't just about raising capital; it was a strategic masterstroke. By becoming a listed Indian company with local shareholders, Merck preempted potential nationalization threats that haunted foreign firms in socialist India. The public listing also provided transparency that helped navigate bureaucratic scrutiny and gave the company a distinctly Indian identity despite German parentage.

Consider the context: This was still License Raj India, where Coca-Cola had been expelled in 1977 for refusing to dilute foreign ownership and share its formula. IBM would leave in 1978 over similar issues. Merck's preemptive public listing in 1981 looked prescient—it secured the company's future while competitors were being shown the door.

The early manufacturing strategy was equally calculated. Rather than import finished products (which attracted prohibitive duties), Merck focused on building local production capabilities. The Goa location wasn't random—the state offered tax incentives, educated workforce from Portuguese-era institutions, and crucially, port access for importing raw materials and eventually, exporting finished goods. What started as a small vitamin E production unit would evolve into something far more significant, but in these early years, it was about establishing a foothold and earning trust.

By 1981, Merck Limited had laid three critical foundations: operational flexibility through the dual pharma-chemical model, local legitimacy through public listing, and manufacturing capability through the Goa facility. These would prove invaluable as India transformed from a closed economy to a liberalized market, setting the stage for the company's long march toward market leadership.

III. The Long March: Building Brands & Capabilities (1981–2010)

The midnight hour of July 24, 1991, changed everything. Finance Minister Manmohan Singh stood before Parliament and announced the dismantling of the License Raj. Foreign brands could now enter India. Import duties would fall. The rupee would be devalued. For Merck Limited, which had spent a decade building behind India's protectionist walls, this was both existential threat and unprecedented opportunity.

The immediate aftermath was brutal. Multinationals flooded in with deep pockets and global brands. Local players scrambled to form joint ventures. The pharmaceutical market, once a cozy club of licensed manufacturers, became a battlefield. Yet Merck had something others lacked: a decade of relationships with Indian doctors, established manufacturing, and crucially, local shareholders who provided political cover against the "foreign invader" narrative.

The company's response was counterintuitive—instead of competing on price with local generics or on brand glamour with new MNC entrants, Merck doubled down on a specific niche: vitamins, minerals, and supplements. This wasn't where the headline growth was (that was in antibiotics and lifestyle drugs), but it offered something valuable: complexity barriers. Manufacturing high-quality vitamins required sophisticated technology, quality control, and formulation expertise that fly-by-night operators couldn't replicate.

The brand portfolio that emerged during this period reads like a medicine cabinet inventory of middle-class India: Evion (Vitamin E), Neurobion (B-complex for "nerve health"), Seven Seas (cod liver oil), Nasivion (nasal decongestant), Polybion (another B-complex variant), Cosome (Vitamin C), and Livogen (iron supplements). Each brand came with a carefully crafted narrative—not just vitamins, but solutions to specific Indian health anxieties. Neurobion wasn't just B12; it was for "tingling sensations" that Indian patients frequently reported. Livogen wasn't just iron; it was for the widespread anemia that plagued Indian women.

The Goa factory underwent a dramatic transformation during these decades. From its humble beginnings as a vitamin E unit, it evolved into what the company would later describe as "the largest sterile facility in the Company with capacity of 260 million ampoules per annum and the only softgel site with a capacity of over 744 million capsules per annum." This wasn't just capacity expansion—it was capability building. Sterile manufacturing for injectables required clean room technology, stringent quality controls, and regulatory compliance that created formidable entry barriers.

But the real moat wasn't manufacturing—it was the doctor relationships. In India's pharmaceutical market, especially for vitamins and supplements, doctor recommendation trumped everything else. While Western markets saw vitamins as over-the-counter consumer products, in India they remained quasi-pharmaceutical, prescribed by physicians and dispensed by pharmacists. Merck invested heavily in medical education programs, sponsoring conferences, funding research, and most importantly, building trust with the medical community. The distribution strategy during this period was equally sophisticated. Reforms in India in the 1990s and 2000s aimed to increase international competitiveness in pharmaceuticals, and India's exports in pharmaceuticals saw remarkable growth. But domestically, Merck focused on building a network that reached beyond metros into Tier 2 and Tier 3 cities where competition was less intense and doctor loyalty stronger. The company invested in training pharmacists, ensuring product availability, and maintaining cold chains for temperature-sensitive products—unglamorous work that created competitive advantages.

The 2000s brought new challenges and opportunities. India's pharmaceutical market was booming, growing at double digits annually. The middle class was expanding, health awareness rising, and chronic diseases becoming more prevalent. Yet Merck's growth during this period was steady rather than spectacular. The company seemed content to build capabilities rather than chase market share at any cost. In retrospect, this patient approach—focusing on quality, building trust, investing in manufacturing—would prove invaluable when a German parent company decided it was time to exit consumer health.

By 2010, Merck Limited had transformed from a foreign subsidiary navigating socialist bureaucracy into a uniquely Indian pharmaceutical company with German DNA. The vitamin portfolio had become synonymous with quality in Indian medical circles. The Goa factory had evolved into a world-class facility. The distribution network reached every corner of the country. Most importantly, the company had survived and thrived through India's economic transformation, positioning itself perfectly for what would come next: the biggest strategic shift in its five-decade history.

IV. The Global Chess Move: P&G's €3.4 Billion Acquisition (2018)

The announcement came on April 19, 2018, catching even industry insiders by surprise. Procter & Gamble would acquire Merck KGaA's global consumer health business for €3.4 billion ($4.2 billion)—giving the Cincinnati-based consumer goods giant vitamin brands like Seven Seas and greater exposure to Latin American and Asian markets. But the real story wasn't in the headline number. It was in a specific line item: Merck Limited, the publicly listed Indian subsidiary, would be the crown jewel of the Asian portfolio.

To understand why P&G paid billions for a business growing in low single digits globally, you need to understand P&G's strategic predicament in 2018. The company's traditional categories—diapers, razors, laundry detergent—were under assault from private labels and direct-to-consumer brands. Growth in developed markets had stalled. Meanwhile, the global wellness trend was exploding, particularly in Asia. Vitamins and supplements represented a $140 billion global market growing at 6% annually, with Asia-Pacific growing even faster.

For Merck KGaA, the logic was equally compelling but opposite in direction. The Darmstadt-based company wanted to focus on innovation-intensive pharmaceuticals, not consumer products requiring massive marketing budgets. Consumer health, while profitable, was becoming increasingly competitive and required capabilities—brand building, digital marketing, e-commerce—that weren't core to Merck's pharmaceutical DNA.

The Indian component was crucial to the deal's economics. While Merck's consumer health business generated €860 million in sales globally, the growth was concentrated in emerging markets, particularly India. PGHL (then still Merck Limited) wasn't just manufacturing vitamins; it had built an entire ecosystem—doctor relationships spanning decades, pharmacy networks covering 600,000 outlets, brands that Indian consumers trusted implicitly, and manufacturing capabilities that could serve not just India but export to other markets.

The transaction structure in India was particularly complex. Since Merck Limited was publicly listed with 48.19% public shareholding, P&G couldn't simply acquire it as part of the global deal. Instead, Merck's promoters signed an agreement to sell their 51.80% stake to P&G's Dutch subsidiary, Procter & Gamble Overseas India B.V., for ₹1,290.19 crore. This triggered mandatory open offer regulations, requiring P&G to offer to buy shares from public shareholders at the same price—₹4,100 per share, a 23% premium to the prevailing market price.

But there was another wrinkle: the BPL (Biological Products Laboratory) business. This chemicals division, manufacturing everything from laboratory reagents to industrial compounds, didn't fit P&G's consumer health vision. In a separate but simultaneous transaction, Merck Limited's board signed a slump sale agreement with a Merck group entity to divest the BPL business for ₹1,052 crore. This surgical separation required careful orchestration—employee transfers, customer contracts, regulatory approvals—all while maintaining business continuity.

The strategic rationale for P&G went beyond just adding vitamin brands. The company saw an opportunity to leverage its global R&D capabilities, marketing expertise, and supply chain excellence to accelerate growth in the VMS category. More importantly, PGHL provided something P&G desperately needed: credibility in healthcare. While P&G had successful OTC brands like Vicks and Pepto-Bismol, it lacked presence in vitamins and supplements, a category increasingly blurring the lines between pharmaceuticals and consumer goods.

From PGHL's perspective, becoming part of P&G offered access to resources and capabilities that Merck KGaA, focused on prescription pharmaceuticals, couldn't provide. P&G's expertise in brand building, its digital marketing capabilities, its relationships with modern retail chains, and its global distribution network could potentially unlock growth that had remained elusive under Merck's ownership.

The timing was particularly fortuitous. India's per capita spending on vitamins and supplements was still a fraction of developed markets, suggesting enormous headroom for growth. The population was aging, chronic diseases were rising, and health consciousness was increasing—all tailwinds for the VMS category. Moreover, the Indian government's push for universal health coverage and preventive healthcare aligned perfectly with PGHL's portfolio.

On December 1, 2018, the acquisition closed. P&G had successfully navigated regulatory approvals across multiple jurisdictions, completed the complex Indian transaction, and integrated a business spanning 100 countries. For €3.4 billion, P&G had acquired not just brands and factories, but a platform for growth in the fastest-growing segment of healthcare. And at the center of this global chess move sat PGHL—no longer Merck's Asian outpost, but P&G's gateway to the vitamins and supplements opportunity in emerging markets.

V. The Transformation: From Merck to P&G Health (2018–2020)

The first challenge facing P&G was deceptively simple: what to call the company? "Merck Limited" carried five decades of trust with Indian doctors and pharmacists, but it belonged to a competitor. The solution—"Procter & Gamble Health Limited"—seemed obvious in retrospect, but the rebranding exercise that followed was anything but simple.

Consider the scope: thousands of product packages, hundreds of marketing materials, pharmacy signages across 600,000 outlets, doctor education materials, regulatory filings, and perhaps most critically, the mental transition in the minds of stakeholders who had known the company as "Merck" for generations. P&G approached this with characteristic precision, rolling out the rebrand in phases to minimize disruption while investing heavily in communication to reassure doctors and pharmacists that only the name was changing, not the products or the company's commitment to quality.

The BPL divestiture, executed simultaneously with the P&G acquisition, was a masterclass in surgical precision. The chemicals business, contributing roughly 30% of revenues but operating on entirely different dynamics than pharmaceuticals, needed to be separated without disrupting either operation. This meant splitting shared services, allocating employees (giving them choices where possible), separating IT systems, and ensuring that customers of both businesses experienced no interruption. The ₹1,052 crore consideration helped smooth the transition, providing capital for P&G to invest in the health business while giving Merck funds to support the separated chemicals operations.

The cultural integration proved more nuanced than anyone anticipated. Merck Limited had operated with Germanic precision—methodical, process-oriented, conservative in decision-making. P&G brought American corporate culture—data-driven but faster-moving, brand-focused, with elaborate systems for everything from performance management to innovation pipelines. The company had to navigate between these worlds while maintaining its unique Indian character that had been key to its success.

One early friction point was the sales approach. Merck's model relied heavily on medical representatives visiting doctors, a high-touch, relationship-driven approach that had worked for decades. P&G's global playbook emphasized brand pull—creating consumer demand through advertising that would drive patients to ask doctors for specific products. In India's VMS market, both approaches were needed, but finding the right balance required months of experimentation and adjustment.

The manufacturing transition was smoother, largely because P&G recognized the Goa facility's excellence and chose enhancement over transformation. The company invested in upgrading quality systems to P&G's global standards, which were even more stringent than Merck's already high bar. New equipment was installed to increase automation, reduce variability, and improve efficiency. The facility's export capabilities were expanded, with P&G leveraging it to supply not just the 13 countries Merck had been serving, but potentially P&G's entire Asian network.

Perhaps the most significant change was in innovation and product development. Under Merck, new product launches had been infrequent, with the company preferring to focus on its established brands. P&G brought a different philosophy—constant innovation, line extensions, new delivery formats. The company began exploring gummies, effervescent tablets, and other formats popular in Western markets but nascent in India. The R&D team, previously focused on formulation improvements, was now tasked with adapting global innovations for Indian consumers.

The integration of systems and processes was a massive undertaking. P&G operates with globally standardized systems—SAP for enterprise resource planning, standardized marketing processes, global procurement contracts. PGHL needed to be integrated into these systems while maintaining the flexibility to serve the unique Indian market. This meant months of data migration, process mapping, training, and parallel running of old and new systems to ensure no disruption.

The transformation wasn't without casualties. Some long-time employees, comfortable with Merck's steady pace, found P&G's performance-driven culture jarring. The company lost some institutional knowledge as people retired or moved on. Some doctor relationships, built over decades, needed to be carefully managed as the company's approach evolved. But P&G was playing a long game, willing to accept short-term disruption for long-term gain.

By early 2020, the transformation was largely complete. PGHL had shed its chemicals business, adopted a new identity, integrated into P&G's global systems, and begun to leverage its new parent's capabilities. The company was poised for growth, with plans for new product launches, distribution expansion, and increased marketing investment. Then, in March 2020, COVID-19 arrived in India, and suddenly, a company selling vitamins and immunity boosters found itself at the center of a global health crisis that would fundamentally alter consumer behavior.

VI. The Indian VMS Market & Competitive Landscape

To understand PGHL's position, you need to first grasp the peculiar dynamics of India's vitamins, minerals, and supplements market—a ₹30,000 crore arena where prescription habits meet consumer marketing, where ancient Ayurveda competes with modern formulations, and where trust matters more than clinical trials.

The Indian VMS market defies Western categorization. In the U.S. or Europe, vitamins are consumer products, bought off shelves based on personal research or advertising influence. In India, 70% of VMS sales still flow through prescriptions. A patient doesn't decide they need Vitamin D; their doctor tells them they're deficient and prescribes a specific brand. This prescription-driven model creates enormous entry barriers—you can't just launch a vitamin brand with clever marketing; you need thousands of doctors to trust and prescribe it. The Indian Nutritional Supplements Market was valued at USD 42.97 billion in 2024 and is projected to reach USD 68.43 billion by 2030, growing at an 8.1% CAGR. Yet within this massive market, PGHL operates in a specific high-value segment—the prescription VMS space where trust and medical endorsement matter more than mass marketing.

The competitive landscape resembles a three-tier pyramid. At the top sit the multinational giants: Abbott with its Ensure range, GSK Consumer Healthcare (now Haleon) with brands like Caltrate and Centrum, Pfizer with its calcium supplements. These companies have deep pockets, global R&D capabilities, and established doctor relationships. PGHL competes directly in this tier, leveraging its Merck-era trust and P&G's resources.

The middle tier comprises large Indian pharmaceutical companies that have entered VMS: Sun Pharma, Cipla, Mankind Pharma. These players leverage their existing distribution networks and doctor relationships but often lack specialized VMS expertise. They compete on price and accessibility rather than innovation or brand premium.

The bottom tier—but increasingly disruptive—consists of Ayurvedic and natural players like Himalaya, Dabur, and Patanjali. India is witnessing a shift toward health consciousness and fitness, which has increased the demand for nutritional supplements. These growth opportunities are attracting several international companies and new products. These companies tap into India's cultural preference for "natural" remedies, often positioning their products as side-effect-free alternatives to "chemical" vitamins.

What makes PGHL's position defensible? First, the prescription moat. Brands like Neurobion and Evion aren't just recommended by doctors—they're specifically prescribed, by name, millions of times annually. This isn't easily replicable; it requires decades of medical education, clinical evidence, and trust-building. A patient might experiment with consumer vitamins, but when a doctor writes "Neurobion" on a prescription, that's what they buy.

Second, the manufacturing complexity. PGHL's Goa facility doesn't just produce tablets—it manufactures sterile injectables, softgels, and specialized formulations that require sophisticated technology and quality control. India has a large vegetarian and vegan population, which significantly impacts the Vitamins & Minerals market. Vegetarians and vegans often have limited dietary sources of certain vitamins and minerals, such as vitamin B12 and iron, leading to higher demand for supplements. Furthermore, India has a high prevalence of micronutrient deficiencies, especially in rural areas. This capability barrier prevents commoditization.

Third, the portfolio breadth. While competitors might excel in specific categories—Abbott in nutrition drinks, Himalaya in herbal supplements—PGHL offers a comprehensive range from basic vitamins to specialized formulations. This allows the company to be a one-stop solution for doctors and pharmacies.

The market dynamics are shifting rapidly. E-commerce, which barely existed in pharma a decade ago, now accounts for a growing share of VMS sales. E-commerce platforms are becoming a key distribution channel offering a wide range of products at competitive prices with home delivery convenience. India has gained 125 million online shoppers in the past three years with another 80 million expected by 2025. India's e-commerce market is expected to reach 111 billion USD by 2024 and 200 billion USD by 2026. Young consumers bypass doctors entirely, ordering supplements based on influencer recommendations or online research. Direct-to-consumer brands like HealthKart and Wellbeing Nutrition offer personalized supplements, subscription models, and aggressive digital marketing that traditional players struggle to match.

The COVID-19 pandemic accelerated several trends. Indian population has begun to believe in immunity-boosting supplements and has led to a significant shift in buying patterns. Vitamin capsules, chewable tablets and gummies are examples of the open-minded buying behaviour. Preventive healthcare has become an important line of defence during the pandemic. Immunity became a national obsession, driving explosive growth in Vitamin C, D, and Zinc supplements. Preventive health moved from niche to mainstream. Digital adoption accelerated by years. PGHL benefited from these trends but also faced intensified competition as every player rushed to launch immunity products.

The regulatory environment adds another layer of complexity. Unlike pharmaceuticals with clear approval pathways, nutraceuticals operate in a grey zone—not quite food, not quite drug. FSSAI regulations are evolving, quality standards are tightening, and advertising claims are under scrutiny. This regulatory uncertainty favors established players like PGHL who can afford compliance costs and have the credibility to navigate changing rules.

Looking at market share, PGHL claims to be "one of India's largest VMS companies," but exact rankings are disputed and data is fragmented. What's clear is that no single player dominates—the market remains fragmented with the top 10 players controlling less than 40% share. This fragmentation presents both opportunity (room for consolidation) and challenge (intense competition for every percentage point of share).

The pricing dynamics are particularly interesting. PGHL's products command premium pricing—a Neurobion strip costs significantly more than generic B-complex vitamins. Yet patients pay willingly because of the brand trust and doctor endorsement. This pricing power is crucial for margins but also limits market expansion as price-conscious consumers opt for cheaper alternatives.

VII. Financial Performance & Market Position

The numbers tell a story of paradox: exceptional profitability metrics coupled with anemic growth, premium valuations despite stagnant revenues, and a fortress balance sheet that isn't translating into market share gains. PGHL's financial profile reads like a value investor's dream and a growth investor's puzzle.

Start with the headline metrics: Market capitalization of ₹10,276 crore, stock price around ₹6,197, P/E ratio of 34.2, book value per share of ₹323. The valuation multiple immediately stands out—34 times earnings for a company that has delivered just 0.16% sales CAGR over the past five years. The market is clearly pricing in something beyond current performance, but what?

The profitability metrics provide one answer. ROCE of 47.8% and ROE of 36.4% place PGHL in the elite tier of Indian companies. These aren't pharmaceutical industry returns; they're software company returns achieved in a manufacturing business. The drivers are multiple: premium pricing power from branded products, operational efficiency from the focused portfolio, minimal capital requirements for growth, and the inherited manufacturing excellence from the Merck era.

The dividend yield of 2.02% might seem modest, but it reflects a conservative payout policy that prioritizes reinvestment. More importantly, the company is virtually debt-free—a rarity in Indian pharmaceuticals where companies typically leverage balance sheets for growth. This financial conservatism provides flexibility but also raises questions about capital allocation efficiency.

Breaking down the revenue composition reveals the growth challenge. The domestic formulations business, contributing roughly 85% of revenues, has been growing in low single digits. The export business, despite the Goa facility's capabilities to serve 13 countries within P&G's network, remains subscale. The company's dependence on mature brands like Neurobion and Evion means growth must come from either market expansion or new product launches—both proving difficult.

The margin profile is where PGHL truly shines. Gross margins exceed 65%, reflecting the premium pricing of branded VMS products versus generic competition. Operating margins in the mid-20s demonstrate efficient operations despite significant spending on doctor engagement and trade margins. The lack of debt means virtually all operating profit flows to the bottom line, resulting in net margins that make PGHL one of the most profitable pharmaceutical companies in India.

But profitability without growth is a recipe for value trap. The 0.16% five-year revenue CAGR is particularly concerning given the underlying market is growing at 8-10% annually. PGHL is losing market share even as the pie expands. Several factors explain this underperformance: mature brand portfolio with limited innovation, conservative marketing spend relative to aggressive competitors, distribution gaps in emerging channels like e-commerce, and the disruption period during the Merck-to-P&G transition.

The working capital management deserves special mention. PGHL operates with negative working capital in many quarters—collecting from customers faster than paying suppliers. This cash generation machine requires minimal capital for operations, freeing resources for other investments. Yet this efficiency hasn't translated into growth investments, raising questions about strategic priorities.

Comparing PGHL's metrics with peers reveals both strengths and weaknesses. Abbott India trades at similar valuations but delivers consistent high-single-digit growth. Pfizer India has lower margins but stronger revenue momentum. Indian companies like Mankind Pharma operate at lower margins but grow faster through aggressive expansion. PGHL's premium valuation seems to rest on its profitability and P&G parentage rather than growth prospects.

The stock performance reflects this paradox. While delivering decent returns to shareholders through dividends and buybacks, the stock has been a market performer rather than outperformer. Institutional investors appreciate the quality metrics but remain concerned about growth. Retail investors are attracted to the P&G brand but puzzled by the stagnant revenues.

The recent quarterly results show tentative signs of improvement. Management has indicated that integration challenges are behind them and growth initiatives are taking hold. New product launches are in the pipeline. Distribution expansion is underway. Digital initiatives are being rolled out. But the market has heard these promises before and awaits concrete evidence of sustained growth revival.

The export opportunity remains largely untapped. Despite manufacturing products that meet global quality standards and having access to P&G's international network, exports remain a small contributor. The company exports to 13 countries, but this could potentially expand to P&G's entire global footprint. The question is whether management has the ambition and P&G has the strategic intent to make PGHL a global manufacturing hub.

The capital allocation framework post-P&G acquisition is evolving. With no debt and strong cash generation, PGHL has multiple options: increase marketing spend to drive growth, pursue acquisitions in adjacent categories, expand manufacturing capacity for exports, or return more cash to shareholders. The choices made here will determine whether PGHL remains a profitable niche player or transforms into a growth story.

The financial strength provides a cushion for strategic experiments. Unlike leveraged competitors who must generate cash to service debt, PGHL can afford to invest for the long term. The question is whether the company will use this strength aggressively or continue its conservative approach. The market's premium valuation suggests investors are betting on the former, but the track record points to the latter.

VIII. Playbook: Lessons from the PGHL Story

Every business story contains lessons, but PGHL's five-decade journey from Merck's Indian subsidiary to P&G's health platform offers a masterclass in several strategic principles that transcend industries and geographies.

The Power of Patient Capital

Merck's 50-year commitment to India before divesting represents patient capital at its finest. The company entered in 1967, weathered the License Raj, survived liberalization, and built capabilities brick by brick. There was no rushed exit during the difficult 1970s, no panic during the 1991 reforms, no hastiness to monetize during the 2000s boom. This patience allowed the development of deep assets—doctor relationships, brand equity, manufacturing expertise—that couldn't be replicated quickly regardless of capital deployed.

The lesson extends beyond timeframes to expectations. Merck didn't demand that its Indian subsidiary match German margins immediately or grow at venture capital rates. It understood that building trust in healthcare, especially in a complex market like India, required generations not quarters. This patience was rewarded when P&G paid billions for assets that would take decades to rebuild from scratch.

Global Acquisitions with Local Implications

The €3.4 billion global deal demonstrates how multinational M&A has profound local consequences. For P&G, acquiring Merck's consumer health was about global category expansion. But in India, it meant navigating public market regulations, managing minority shareholders, executing complex separations, and maintaining stakeholder trust. The Indian subsidiary wasn't just a line item in a global deal—it required bespoke structuring, separate negotiations, and careful integration.

This complexity multiplier in cross-border deals is often underestimated. Acquirers focus on global synergies while local complexities—regulatory approvals, labor laws, tax implications, minority shareholder rights—can derail value creation. PGHL's successful transition required P&G to treat the Indian component as a deal within a deal, with dedicated resources and specialized expertise.

Managing Complexity: The Multi-Business Challenge

For decades, Merck Limited successfully operated across pharmaceuticals, chemicals, and consumer health—three businesses with different customers, regulations, and success factors. This complexity was managed through organizational design (separate divisions), operational discipline (distinct supply chains), and strategic clarity (each business had defined role in portfolio).

The BPL separation during the P&G acquisition showcased the flip side—how to surgically separate intertwined businesses without destroying value. The ₹1,052 crore separation wasn't just about dividing assets; it required untangling shared services, splitting customer relationships, managing employee transitions, and ensuring neither business was compromised. The lesson: complexity can be a competitive advantage if managed well, but unwinding complexity requires exceptional execution.

Manufacturing as Moat

In an era obsessed with asset-light models, PGHL's Goa facility represents the enduring value of manufacturing excellence. The ability to produce 260 million sterile ampoules and 744 million softgels annually isn't just about capacity—it's about capabilities that create competitive advantage. Regulatory approvals, quality certifications, process knowledge, and technical expertise embedded in the facility create barriers that pure marketing companies can't overcome.

The manufacturing moat extends beyond physical assets to institutional knowledge. The decades of experience in vitamin formulation, stability testing, quality control, and regulatory compliance represent intellectual property that doesn't appear on balance sheets but drives competitive advantage. When P&G acquired PGHL, it wasn't just buying brands—it was acquiring manufacturing capabilities that would take years to replicate.

Brand Equity Transfer

The transformation from B2B chemicals to B2C health products illustrates how brand equity can transcend categories—but only with careful management. The "Merck" name carried trust from industrial customers to doctors to consumers. Each transition required different messaging, channels, and proof points, but the underlying equity—German quality, scientific rigor, reliability—transferred across segments.

The rebranding to P&G Health showcased the reverse challenge: transferring equity from consumer goods to healthcare. P&G's strength in shampoo and detergents doesn't automatically translate to vitamins and supplements. The company had to build healthcare credibility while leveraging consumer marketing expertise—a delicate balance that's still evolving.

Regulatory Navigation

Operating in Indian pharmaceuticals requires mastering regulatory complexity that would challenge any multinational. Drug price controls, advertising restrictions, quality standards, doctor engagement rules, distribution regulations—each with federal and state variations. PGHL's success came from treating regulatory compliance not as a cost center but as competitive advantage.

The company's approach—proactive engagement with regulators, investment in compliance infrastructure, conservative interpretation of grey areas—might seem expensive and slow. But it built trust that proved invaluable during transitions. When ownership changed from Merck to P&G, regulatory approvals came smoothly because of decades of credibility. The lesson: in highly regulated industries, reputation with regulators is as important as reputation with customers.

The Trust Architecture

Perhaps the most important lesson from PGHL's story is the architecture of trust in healthcare. The company built multiple layers: trust with regulators through compliance, trust with doctors through education and evidence, trust with pharmacists through consistent supply and margins, trust with patients through quality and efficacy. Each layer reinforced the others, creating a system more powerful than any individual component.

This trust architecture took decades to build and survived ownership changes, market disruptions, and competitive attacks. It's the reason why doctors still prescribe Neurobion despite cheaper alternatives, why pharmacists stock PGHL products despite lower margins than generics, why patients pay premium prices despite budget constraints. Trust, carefully constructed and maintained, is the ultimate moat.

IX. Bear vs. Bull Case

Bull Case: The Wellness Megatrend Play

The optimist sees PGHL as perfectly positioned for India's wellness revolution. Start with demographics: 1.4 billion people, median age of 28, rising life expectancy, and growing disease burden. According to the INDIA AGING REPORT 2023, the elderly population aged above 60 years is expected to grow from 149 million in 2022 to 347 million in 2050. The addressable market isn't just growing—it's exploding.

The health consciousness shift is structural, not cyclical. COVID-19 didn't create health awareness; it accelerated a trend already underway. Middle-class Indians are shifting from treatment to prevention, from reactive to proactive health management. This isn't a fad—it's a generational change in how Indians think about health. PGHL's portfolio of preventive health products positions it at the center of this shift.

P&G's global capabilities are just beginning to impact PGHL. The parent company brings world-class R&D, digital marketing expertise, e-commerce capabilities, and access to innovations from developed markets. P&G's success in building billion-dollar brands in India (Whisper, Pampers, Gillette) demonstrates its ability to understand and serve Indian consumers. Applied to health products, these capabilities could unlock significant growth.

The financial fortress provides optionality. With virtually no debt and strong cash generation, PGHL can invest aggressively without financial constraints. It can acquire complementary businesses, launch new categories, expand distribution, or increase marketing—all without diluting returns or taking financial risk. This flexibility is valuable in a rapidly evolving market.

The brand equity remains undermonetized. Neurobion, Evion, and Seven Seas have built trust over decades but remain underpenetrated. The prescription-driven model, while limiting growth, ensures sticky revenues and pricing power. As these brands expand from prescription to consumer awareness, the revenue opportunity multiplies without proportional cost increase.

Regulatory tailwinds are emerging. The government's focus on preventive healthcare, insurance coverage expansion, and Ayushman Bharat (national health protection scheme) all favor increased VMS consumption. As healthcare access improves, diagnosis of deficiencies will increase, driving supplement demand. PGHL's established position allows it to capture disproportionate share of this growth.

Bear Case: The Growth Trap

The skeptic sees structural challenges that P&G's ownership hasn't solved. Five years of 0.16% revenue growth isn't a temporary blip—it reflects fundamental issues. Mature brands in mature categories with mature customer bases don't suddenly accelerate. The prescription-driven model that created the moat also limits the growth potential.

Competition is intensifying from every direction. Global giants like Abbott and GSK bring similar capabilities to P&G. Indian companies like Mankind and Sun Pharma have lower costs and deeper local networks. D2C brands like Wellbeing Nutrition move faster and connect better with young consumers. Ayurvedic players tap into cultural preferences PGHL can't match. The competitive space is getting more crowded, not less.

The valuation leaves no room for error. At 34 times earnings, PGHL trades at premium multiples despite inferior growth. Any disappointment—a failed product launch, regulatory change, competitive loss—could trigger significant multiple compression. The market is pricing in acceleration that hasn't materialized for five years.

Channel disruption threatens the core model. PGHL's strength lies in traditional channels—doctor prescriptions and pharmacy sales. But e-commerce, D2C brands, and modern retail are growing faster. Young consumers don't visit doctors for vitamin recommendations; they research online and buy from apps. PGHL's traditional strengths become weaknesses in digital channels.

The innovation pipeline appears weak. While P&G has global R&D capabilities, the local pipeline seems limited to line extensions and format variations. True innovation in VMS—personalized nutrition, genetic testing, microbiome-based supplements—is happening at startups and specialized companies, not at large corporations. PGHL risks being disrupted by new science it's not pursuing.

Integration challenges may persist. Cultural differences between P&G's consumer goods DNA and PGHL's pharmaceutical heritage create ongoing friction. The aggressive growth culture of P&G clashes with the conservative, compliance-focused approach inherited from Merck. These cultural conflicts can paralyze decision-making and slow execution.

The prescriber base is aging. Doctors who prescribe brands like Neurobion learned about them decades ago. Younger doctors, trained in evidence-based medicine and influenced by international guidelines, may be less brand-loyal. As the prescriber base turns over generationally, traditional brand advantages erode.

The Verdict

Both cases have merit, but the balance tilts toward cautious optimism. PGHL possesses undeniable strengths—brand equity, manufacturing capability, financial strength, and P&G parentage. The market opportunity is real and growing. But execution remains the variable. Can management accelerate growth without sacrificing profitability? Can P&G's capabilities translate to Indian healthcare? Can traditional strengths adapt to digital disruption?

The answer likely lies in the middle: PGHL will grow, but not spectacularly. It will remain highly profitable but face margin pressure. It will benefit from market growth but lose some share to nimbler competitors. For investors, it represents a quality compounder rather than a multibagger—steady wealth creation rather than explosive returns.

X. Future Outlook & Strategic Options

The path forward for PGHL requires navigating between its heritage strengths and future imperatives. The company stands at an inflection point where incremental improvements won't suffice—strategic choices must be made about where to play and how to win in the evolving Indian health market.

Digital Health Integration

The convergence of healthcare and technology presents both PGHL's biggest opportunity and greatest threat. Digital health platforms are intermediating the doctor-patient relationship, creating new decision points for supplement recommendations. Apps like Practo and 1mg don't just facilitate consultations—they influence prescription behavior through algorithms and partnerships.

PGHL needs a digital strategy beyond e-commerce presence. This could involve partnerships with health-tech platforms for personalized nutrition recommendations, development of proprietary apps for medication adherence and health tracking, or integration with wearable devices for real-time health monitoring. The company's credibility with healthcare professionals provides an advantage in digital health that pure tech players lack.

Preventive Healthcare Positioning

The shift from treatment to prevention accelerates post-COVID, but PGHL hasn't fully captured this narrative. While its products are inherently preventive, the messaging remains medicinal. There's an opportunity to reposition from "vitamin deficiency treatment" to "wellness optimization"—a subtle but significant shift that expands the addressable market from sick people to healthy people who want to stay healthy.

This requires new product formats (gummies, effervescents, functional foods), new channels (gyms, wellness centers, corporate wellness programs), and new messaging (performance enhancement, not just deficiency treatment). P&G's expertise in consumer marketing could be leveraged to build wellness brands that complement the medical heritage.

New Product Pipeline

The global P&G portfolio includes innovations not yet launched in India—personalized vitamins, beauty-from-within supplements, cognitive enhancement products. Adapting these for Indian consumers, at Indian price points, with Indian regulatory approvals, represents a multi-year opportunity.

But innovation shouldn't just flow from global to local. India's unique disease burden (high diabetes, widespread vitamin D deficiency, endemic anemia) creates opportunities for India-first innovation that could eventually go global. PGHL's manufacturing capabilities and market knowledge position it to develop products for Indian health challenges that affect billions across emerging markets.

M&A Possibilities

PGHL's strong balance sheet and P&G's global expertise make it a natural consolidator in the fragmented VMS market. Potential targets include regional brands with strong doctor relationships but weak marketing, Ayurvedic companies with authentic positioning but need modernization, or D2C brands with digital expertise but lacking credibility and scale.

Acquisitions could also be capability-driven rather than just brand-focused. Buying a digital health startup, a personalized nutrition company, or a clinical testing laboratory could provide capabilities that would take years to build organically. The key is ensuring cultural fit and integration capability—areas where many pharmaceutical M&As fail.

Export Expansion

The Goa facility's capabilities remain underutilized for exports. While serving 13 countries, the potential extends to P&G's presence in 180+ markets. Positioning PGHL as P&G's global VMS manufacturing hub could drive significant growth without proportional investment.

The export opportunity extends beyond just P&G networks. India's reputation as the "pharmacy of the world" in generics could extend to VMS. Countries across Africa, Southeast Asia, and Latin America face similar nutrition challenges as India. PGHL's experience in developing affordable, high-quality supplements for Indian consumers could translate to these markets.

Strategic Choices

Ultimately, PGHL must choose its strategic identity. Is it a pharmaceutical company leveraging P&G's consumer expertise, or a consumer health company with pharmaceutical heritage? Is growth the priority, or profitability preservation? Is the focus domestic or global? Is the model prescription-driven or consumer-pull?

These aren't binary choices but require clear prioritization. The current strategy appears to be "all of the above," which risks being none of the above. Clear strategic choices, consistently executed, would provide the direction that seems lacking since the P&G acquisition.

The market opportunity is undeniable. India's VMS market will likely double by 2030. The question is whether PGHL will capture its fair share of this growth or continue losing ground to more focused competitors. The assets are in place—brands, manufacturing, distribution, parentage. What's needed is strategic clarity and execution excellence to unlock the value that the market's premium valuation anticipates but recent performance hasn't delivered.

XI. Recent News & Developments

Recent quarterly results show signs of recovery. In Q2 FY25, PGHL reported a 25.5% increase in net profit YoY to ₹82.3 crore, while Q3 FY25 saw net profit surge 26.1% to ₹90.9 crore. Revenue growth remains modest, with Q2 FY25 revenues growing just 2.8% to ₹313.4 crore. However, margin expansion has been significant—EBITDA margin expanded to 36.4% in Q2 FY25 from 29.1% in the previous year's quarter.

Management commentary from Milind Thatte, Managing Director, reflects cautious optimism. "Our strategy, centered on a focused portfolio of quality, trusted, and highly recommended brands where performance drives brand choice; superiority (across product, package, brand communication, retail execution, and value), constructive disruption and an agile accountable organization." The emphasis on "constructive disruption" suggests awareness of the need for innovation while maintaining core strengths.

Q3 FY25 was described as "a period of strategic reinforcement as we took proactive steps to strengthen our supply network." This focus on supply chain enhancement reflects lessons learned from pandemic-era disruptions and preparation for potential export expansion.

The dividend policy remains shareholder-friendly. The Board declared an interim dividend of ₹80 per equity share for FY25, with record date of February 21, 2025. This consistent dividend distribution, despite modest revenue growth, reflects confidence in cash generation capabilities and commitment to shareholder returns.

Stock performance has been volatile but positive. PGHL hit a 52-week high of 6,500 on August 1, 2025, and a 52-week low of 4,863 on October 29, 2024. The stock is up 7% over the last month and 18.31% over the last year. This outperformance relative to business fundamentals suggests market optimism about future prospects.

The cost structure improvements are noteworthy. Total expenses fell 7.91% YoY in Q2 FY25, with cost of materials consumed down 44.82% and employee benefits expenses down 23.77%. These efficiency gains, whether from procurement optimization or automation, are driving margin expansion despite tepid revenue growth.

Looking ahead, the company faces the challenge of converting operational improvements into revenue growth. The market's premium valuation and recent stock performance suggest expectations of acceleration. Whether PGHL can deliver on these expectations while maintaining its exceptional profitability will determine its trajectory in the coming quarters.

XII. Conclusion: The Unfinished Story

Procter & Gamble Health Limited stands as a testament to the power of patient building in emerging markets. From Merck's 1967 entry into License Raj India to P&G's 2018 acquisition, this company has navigated economic liberalization, regulatory complexity, and market transformation while building enduring competitive advantages. The Goa factory, doctor relationships, and brand equity represent assets that took decades to build and would take decades to replicate.

Yet the story remains unfinished. The company possesses all the ingredients for success—trusted brands, manufacturing excellence, financial strength, and global parentage—but hasn't yet found the recipe to blend them into sustained growth. The 0.16% five-year revenue CAGR in a market growing at 8-10% annually represents both failure and opportunity. Failure to capture the market's growth so far, but opportunity because the assets to accelerate remain intact.

The strategic crossroads ahead will define PGHL's next chapter. Will it remain a profitable niche player, content with high margins and steady dividends? Or will it leverage P&G's capabilities and its own strengths to become a growth story? The Indian VMS market's expansion from $43 billion to potentially $68 billion by 2030 provides the canvas. Whether PGHL paints a masterpiece or remains a sketch will depend on strategic clarity, execution excellence, and the willingness to disrupt itself before others disrupt it.

For investors, PGHL represents a classic quality-versus-growth dilemma. The exceptional profitability metrics, debt-free balance sheet, and steady dividends offer safety and compounding. But the premium valuation assumes growth acceleration that hasn't materialized. The bet on PGHL is ultimately a bet on management's ability to unlock the latent potential in its portfolio while navigating the disruption of traditional pharmaceutical distribution.

The broader lessons from PGHL's journey transcend the company itself. In an era of quick flips and growth-at-any-cost strategies, PGHL demonstrates the enduring value of patient capital, deep capabilities, and trust-building in complex markets. The company's transformation from industrial chemicals to consumer health, through multiple ownership changes and market disruptions, showcases the importance of strategic flexibility while maintaining core strengths.

As India's health consciousness rises, chronic diseases proliferate, and preventive care mainstreams, the opportunity for VMS companies has never been greater. PGHL's challenge is converting its historical advantages into future growth while adapting to digital disruption, changing consumer behaviors, and intensifying competition. The company that emerges from this transformation—whether still recognizable as the Merck subsidiary of old or reimagined as P&G's health platform—will write the next chapter of this continuing story.

The journey from Merck's Asian outpost to P&G's vitamin powerhouse has been remarkable. But in the dynamic Indian market, past success guarantees nothing. PGHL must earn its future through innovation, execution, and the courage to change. The assets are in place, the opportunity is clear, and the market is waiting. What remains to be seen is whether PGHL will seize the moment or let it pass, whether it will lead the market transformation or follow others who do.

For a company that has survived and thrived through India's economic evolution, adapted to ownership changes, and built irreplaceable assets, the future should be bright. But brightness requires more than heritage—it requires vision, strategy, and execution. As PGHL enters its sixth decade, now under P&G's ownership, the question isn't whether it will survive but whether it will soar. The answer lies not in its distinguished past but in the choices it makes today for tomorrow. The story of Procter & Gamble Health Limited continues, and its most important chapters may yet be unwritten.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube