OneSource Specialty Pharma: India's CDMO Bet on the GLP-1 Gold Rush

I. Introduction & Episode Setup (5-10 min)

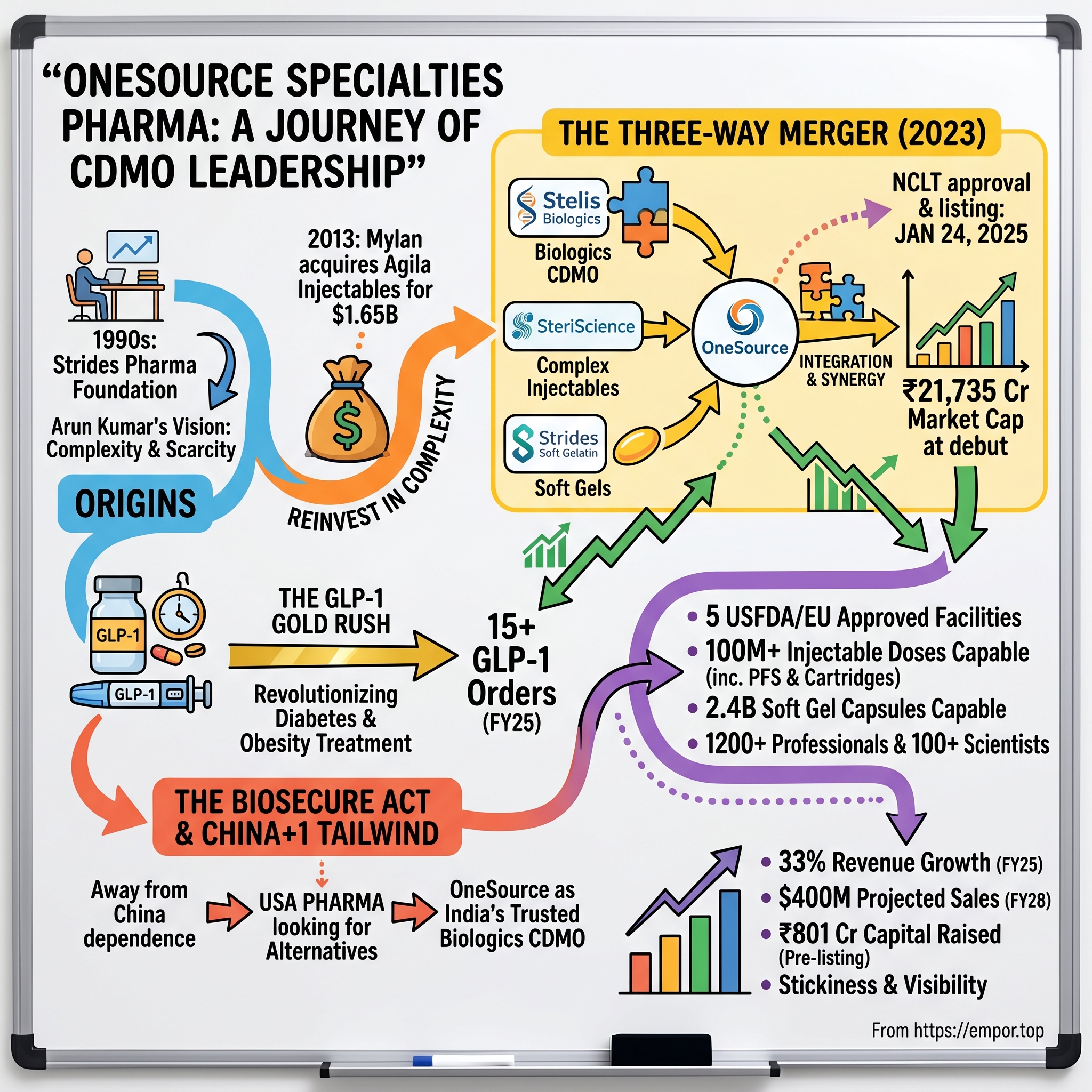

Picture this: It's January 24, 2025, and the opening bell rings at the National Stock Exchange in Mumbai. A new ticker symbol—ONESOURCE—flashes across trading screens for the first time. Within hours, the stock commands a market cap of ₹21,735 crore, making it one of India's most valuable pharmaceutical debuts in recent memory. But this isn't just another IPO story. This is the culmination of a three-decade journey that began in a small office in Vashi, Navi Mumbai, where a young entrepreneur named Arun Kumar first dreamed of building a global pharmaceutical empire.

OneSource Specialty Pharma Ltd is in the research, development, manufacture and commercialisation of biological drug products in various injectable formats. The company represents something unprecedented in Indian pharma: a pure-play contract development and manufacturing organization (CDMO) focused exclusively on the most complex, highest-value segments of modern medicine—biologics, drug-device combinations, and the exploding market for GLP-1 obesity drugs.

The timing couldn't be more perfect—or more precarious. On one side, the market for GLP-1 drugs is slated to touch $100-130 billion in the next few years, driven by rising demand for diabetes and obesity treatments. On the other, geopolitical tensions between the U.S. and China are creating what might be the greatest supply chain reshuffling in pharmaceutical history. The BIOSECURE Act is continuing to drive significant interest as pharma partners look to increase supply chain diversity and security, potentially redirecting billions in CDMO contracts away from China.

The central question driving our story today: How did a subsidiary of Strides Pharma, operating in the shadows of global pharmaceutical giants, position itself to become India's leading biologics CDMO at precisely the moment when the world needs alternatives to Chinese manufacturing? It's a story that involves strategic spin-offs, bold capital allocation decisions, and a bet that the future of medicine would be injected, not swallowed—delivered through sophisticated pen devices, not simple pills.

II. The Strides Origin Story & Arun Kumar's Empire (30-40 min)

Hailing from Kerala but brought up in Ooty, the son of a government servant, Kumar left home at 21 to seek his fortune in Mumbai. He worked with a couple of pharma companies for eight years before setting up Strides at Vashi, Navi Mumbai, in 1990. This wasn't Silicon Valley garage startup mythology—this was grinding it out in the industrial outskirts of India's financial capital, learning the pharmaceutical trade from the ground up.

What set Arun apart wasn't just ambition—it was his ability to spot scarcity. "We look at areas where there is scarcity," he says. "It could be in manufacturing, around a particular domain or a particular technology, or it could be in a particular market. We also look for high capex, long-gestation businesses." This philosophy would guide every major decision for the next three decades.

The early years of Strides were marked by rapid expansion and near-disaster. The company expanded rapidly in the decade 1996 to 2006 but piled on debt as well. With some corrections and refocusing, Strides recovered to build success stories. By 2013, Arun had built something remarkable: Agila Specialties, Strides' injectables business. When Mylan came calling with an offer, the number was staggering: $1.65 billion. This was more than three times Strides' revenue of around $500 million at the time and indeed more than the $1.3 billion Mylan garnered from the Asia Pacific region.

But Arun wasn't content to be a one-hit wonder. Besides founding Strides, Arun's family office (setup in the early 2000s) ran a differentiated set of investments spread across several companies with a combined revenue base of over a billion dollars and an invested capital of over half a billion dollars. His entrepreneurial DNA expressed itself through constant building, buying, and spinning off assets.

Perhaps his most impressive feat outside of Strides was SeQuent Scientific. Arun is credited to have co-founded and built India's largest fully integrated Animal Health Company, SeQuent Scientific Limited, in less than five years. Arun's stake in SeQuent was divested to the Carlyle Group in May 2020. The transaction valued SeQuent at approximately $210 million, with CA Harbor Investments proposing to acquire a majority stake in SeQuent via private share purchase agreements, for a purchase price of INR 86 per share.

This wasn't just financial engineering—it was strategic vision. Each business Arun touched followed the same playbook: identify complexity that others avoided, build capabilities that took years to replicate, and exit when strategic buyers recognized the value. "Being an entrepreneur, and especially a first-generation entrepreneur, calls for strong character," says Kumar.

The sale of Agila funded Strides' next act. Rather than simply returning capital to shareholders or pursuing me-too generic drugs, Arun saw the future: biologics, complex injectables, and the convergence of drugs with delivery devices. While the rest of Indian pharma was racing to the bottom on pricing for simple generics, Arun was betting on complexity—and preparing to build what would become OneSource.

What's remarkable about Arun's journey is how he consistently zagged when others zigged. When Indian pharma was focused on the U.S. generics gold rush, he built capabilities in Africa. When others chased volume, he chased complexity. And when the world was mesmerized by oral medications, he bet the future would be injectable.

III. Building the CDMO Platform: The Three-Way Merger (35-45 min)

The creation of OneSource wasn't a simple spin-off—it was architectural origami of the highest order. OneSource was incorporated in 2007 as a subsidiary of Strides Pharma Ltd. The company is a Contract Development and Manufacturing Organisation that caters to several biopharma and biotech companies. It covers the entire CDMO value chain, from clinical development to technology transfer to commercial manufacture and regulatory assistance.

But the real story begins in September 2023, when Arun and his team unveiled their masterstroke. Last September, Strides created OneSource—a specialty pharma pure-play CDMO—by integrating Stelis Biologics' CDMO, SteriScience's complex injectables, and Strides' soft gelatine businesses into a single entity. This wasn't just combining three businesses—it was creating India's first dedicated specialty pharma CDMO from complementary pieces that, together, would be worth far more than their sum.

Consider the strategic logic: Stelis brought biologics capabilities—the ability to manufacture the large molecule drugs that represent the future of medicine. SteriScience contributed complex injectable expertise—the knowledge to create sophisticated drug-device combinations. And Strides' soft gelatin business added high-volume manufacturing capabilities for specialized oral dosage forms. Each piece filled a gap the others couldn't address alone.

The regulatory navigation alone was a Herculean task. The scheme required approval from multiple stakeholders: shareholders of three different entities, creditors, stock exchanges, SEBI, and ultimately the National Company Law Tribunal. Following NCLT approval, OneSource is set to list its equity shares on the BSE and NSE, subject to regulatory clearances. The NCLT Mumbai Bench sanctioned the scheme on November 14, 2024, paving the way for what would become one of the most watched listings of 2025.

But here's where it gets interesting: even before the merger was complete, sophisticated investors were circling. OneSource Specialty Pharma Limited has secured commitments to raise ₹8,010 million (~USD 95 million) from prominent domestic and international investors, as well as family offices, ahead of its listing. The fundraising deal is based on a pre-money equity valuation of USD 1.65 billion.

This wasn't just financial validation—it was a bet on India's pharmaceutical future. The investment valued the company at a pre-money equity valuation of $1.65 billion, before OneSource had even begun trading as an independent entity. The message was clear: smart money believed this combination of assets, at this moment in pharmaceutical history, was worth betting on.

The technical capabilities that emerged from this merger were formidable. OneSource has capabilities spanning supply-constrained drug-device combinations, biologics, and soft gelatin capsules – with the capacity to produce more than 100 million injectable doses including cartridges and pre-filled-syringes and 2.4 billion soft gelatin capsules. These weren't just numbers—they represented the ability to serve the most sophisticated pharmaceutical companies in the world with their most complex products.

The merger also brought together over 1,200 professionals, including more than 100 scientists and technical experts. This brain trust wasn't accumulated overnight—it represented decades of capability building across three organizations, now united under a single mission: to become the CDMO of choice for specialty pharmaceuticals.

What made this three-way merger particularly brilliant was its timing. The pharmaceutical industry was undergoing a fundamental shift from small molecule drugs to biologics, from simple pills to complex drug-device combinations. OneSource emerged from this merger with capabilities spanning the entire spectrum—positioned perfectly for where the industry was heading, not where it had been.

IV. The GLP-1 Opportunity: Right Place, Right Time (45-55 min)

If you want to understand the GLP-1 phenomenon, start with a simple number: The global GLP-1 receptor agonist market size was estimated at USD 53.46 billion in 2024 and is projected to reach USD 156.71 billion by 2030, growing at a CAGR of 17.46% from 2025 to 2030. This isn't just growth—it's a gold rush, and OneSource positioned itself perfectly at the intersection of capability and opportunity.

The story of GLP-1 drugs—medications like Ozempic and Wegovy that have revolutionized diabetes and obesity treatment—is really a story about manufacturing complexity. These aren't simple pills you can stamp out by the millions. They're sophisticated biologics that require precise temperature control, complex formulation, and most critically, integration with advanced delivery devices. The average patient doesn't want to draw up a syringe—they want to click a pen.

OneSource Specialty Pharma's managing director and CEO Neeraj Sharma said, "One of our key service offerings is around drug-device combinations, especially in the generic GLP space, and we already have significant capacity in terms of cartridge and fill-finish, as well as full assembly of GLP-1 devices." This wasn't opportunistic positioning—it was the result of years of strategic investment in exactly the capabilities the market would need.

Consider what OneSource brings to the table: OneSource expects significant growth in its order book over the next three years, driven by rising demand for weight-loss drugs. The company added 15 orders related to obesity and diabetes drugs in fiscal year 2025 and anticipates a 30% compound annual growth rate through fiscal year 2028. These aren't speculative projections—they're based on actual orders from pharmaceutical companies scrambling to meet unprecedented demand.

The Ozempic/Wegovy phenomenon has created something unprecedented in pharmaceutical history: a supply-constrained blockbuster. Novo Nordisk and Eli Lilly, despite massive manufacturing expansions, still can't meet global demand. After a manufacturing expansion spree over the past two years, Novo is looking to build out capacity even more in 2024. Specifically, the company plans to add "significant additional volumes" for Wegovy over the next year.

This is where OneSource's capabilities become critical. OneSource has clients in America, Europe, the Middle East, Africa, and India, all looking at GLP-1 opportunities. The company isn't just manufacturing—it's providing end-to-end CDMO services that include formulation development, regulatory support, and most importantly, the ability to integrate drugs with sophisticated pen devices.

The technical challenges are immense. GLP-1 drugs are peptides—chains of amino acids that are incredibly sensitive to temperature, pH, and mechanical stress. Getting them into a pre-filled pen that a patient can carry around and self-administer requires expertise in formulation science, materials science, mechanical engineering, and quality control. It's the pharmaceutical equivalent of putting a Ferrari engine in a Toyota Corolla body and making it work perfectly every time.

The company is proactively expanding its capacity for drug-device combinations and cartridge filling assembly, which will take up most of the capital expenditure investment. This isn't speculative capacity building—it's responding to actual demand from global pharmaceutical companies who need alternatives to constrained Chinese suppliers.

What makes OneSource particularly attractive to GLP-1 manufacturers is its integrated capabilities. A pharmaceutical company doesn't need to coordinate between multiple suppliers for drug substance, drug product, and device assembly. OneSource can handle the entire chain, reducing complexity, cost, and critically, time to market. In a market where every month of delay means hundreds of millions in lost revenue, this integration is invaluable.

The company's positioning in India also provides cost advantages without the geopolitical risks of China. Labor costs are competitive, the regulatory environment is stable, and critically, India has a long history of successful pharmaceutical manufacturing for global markets. OneSource isn't asking customers to take a leap of faith—it's offering a proven alternative at exactly the moment the industry needs it most.

V. Manufacturing Excellence & Technical Capabilities (40-50 min)

Walk into OneSource's flagship facility in Bengaluru, and you're not in a typical Indian pharmaceutical plant. Following the NCLT process and listing, OneSource Specialty Pharma will operate five state-of-the-art facilities in Bengaluru, India, all approved by major regulatory bodies, including the USFDA and EU authorities. These aren't just manufacturing sites—they're cathedrals of complexity, designed to handle some of the most challenging pharmaceutical products in the world.

The numbers tell part of the story, but only part. The company can produce over 100 million injectable doses annually, including cartridges and pre-filled syringes. It can manufacture 2.4 billion soft gelatin capsules. But what really matters is what those numbers represent: the ability to handle everything from microliter-precision filling of expensive biologics to high-volume production of complex oral dosage forms.

OneSource is in the research, development, manufacture and commercialisation of biological drug products in various injectable formats. This isn't just contract manufacturing—it's the full spectrum from early development through commercial production. When a biotech company comes to OneSource with a promising molecule, they can take it from preclinical studies all the way through to commercial launch.

The regulatory credentials are crucial. The newly combined CDMO has five world-class facilities approved by major regulatory agencies, including the US FDA, EU, and TGA. These approvals aren't paperwork—they represent years of inspections, quality system implementations, and continuous improvement. Each FDA inspection is a high-wire act where a single observation can shut down production for months. OneSource's track record speaks to a quality culture that goes beyond compliance to genuine excellence.

Consider the device assembly capabilities. The company operates over 20 automatic and semi-automatic flexible assembly stations supporting multiple device formats. This isn't simple mechanical assembly—it's precision engineering where tolerances are measured in microns and every device must deliver exactly the right dose, every time. A failure rate of even 0.1% would be catastrophic when dealing with life-saving medications.

The soft gelatin capability deserves special attention. While the world focuses on injectables, soft gels remain a critical dosage form for many medications, particularly those requiring enhanced bioavailability or precise dosing of liquid formulations. OneSource's 2.4 billion capsule capacity makes it one of the largest soft gel manufacturers globally—a capability that perfectly complements its injectable offerings.

But perhaps most impressive is the integration of these capabilities. A client developing a complex therapy might need multiple dosage forms—an injectable for acute treatment and an oral formulation for maintenance therapy. OneSource can handle both, providing integrated development and manufacturing that reduces complexity and accelerates time to market.

The human capital is equally impressive. Along with a team of over 1,200 professionals, including 200+ techno-commercial experts, we specialize in diverse dosage formats and advanced biologics platforms. These aren't just workers—they're scientists, engineers, and quality professionals who understand the nuances of biological manufacturing, the complexities of drug-device integration, and the regulatory requirements of global markets.

The company's approach to technology transfer is particularly sophisticated. When a pharmaceutical company develops a new process, transferring it to commercial manufacturing is often where projects fail. OneSource has developed systematic approaches to tech transfer that reduce risk and accelerate timelines—critical capabilities when every month of delay can cost hundreds of millions in lost revenue.

Quality systems deserve special mention. In biologics manufacturing, contamination or deviation can destroy entire batches worth millions of dollars. OneSource's quality infrastructure—from environmental monitoring to analytical testing to deviation management—represents decades of accumulated expertise. This isn't something you can build overnight or buy off the shelf.

VI. The Biosecure Act Tailwind & China Plus One Strategy (30-40 min)

The BIOSECURE Act might be the most important piece of U.S. legislation that most people have never heard of. The bill aims to prevent federally funded US pharmaceutical companies from working with Chinese services firms. Its writers have cited concerns about national security. The legislation would give US drugmakers until 2032 to dissociate from those Chinese companies. For OneSource, it represents a generational opportunity.

To understand why, you need to grasp the depth of Western pharma's dependence on China. A survey published in May 2024 by the pharma trade group Biotechnology Innovation Organization (BIO) found that 79% of the 124 US biotechnology companies surveyed contract with at least one Chinese firm. This isn't just cost optimization—it's structural dependence built over two decades.

The named companies in the BIOSECURE Act aren't bit players. The original draft bill named four Chinese firms—WuXi AppTec, BGI Group, MGI, and Complete Genomics—as potential threats, and in May, an amended version added WuXi Biologics to the list. WuXi AppTec alone employs over 20,000 chemists—more than all major Indian CDMOs combined. In 2023, WuXi Apptec generated around $26.13 billion from U.S. contracts, accounting for 65% of its total revenue.

But geography has become destiny in pharmaceutical manufacturing. Some are turning to Indian drug services firms, which are preparing for an influx of business. OneSource isn't just hoping to catch some overflow—it's positioning itself as the premium alternative for companies that need sophisticated capabilities, not just cheap capacity.

The timing of OneSource's emergence as an independent entity couldn't be better. OneSource is strategically positioned – with the remarkable growth of GLP-1s and the BIOSECURE Act – to address the increasing demand for drug-device combinations and biologics drug substances and product. This isn't opportunistic marketing—it's the convergence of capability and market need.

Consider what OneSource offers that Chinese CDMOs cannot: genuine independence from geopolitical risk. When a U.S. pharmaceutical company partners with OneSource, they're not worried about intellectual property ending up in the wrong hands or sudden regulatory changes disrupting their supply chain. Reuters reported that in February, US intelligence officials briefed senators that WuXi AppTec had transferred a US client's intellectual property to China without the customer's consent. These aren't theoretical risks—they're real concerns driving real decisions.

The "China Plus One" strategy that many multinationals have adopted is evolving into something more nuanced. It's not just about having a backup to China—it's about building resilient, diversified supply chains that can withstand geopolitical shocks. OneSource offers not just an alternative to China, but arguably a superior option for complex, high-value products where quality and reliability matter more than rock-bottom costs.

India's advantages go beyond just being "not China." The country has a 50-year history of supplying pharmaceuticals to global markets. The regulatory framework, while sometimes challenging, is transparent and aligned with international standards. English is the business language. The legal system, inherited from British common law, provides predictable commercial dispute resolution. These "soft" factors matter enormously when you're trusting a partner with products worth billions.

The Indian government has also recognized the opportunity. Policy support for the pharmaceutical sector, including Production Linked Incentive (PLI) schemes and infrastructure investments, is creating an ecosystem that supports sophisticated manufacturing. This isn't just about OneSource—it's about India positioning itself as the alternative to China for global pharmaceutical manufacturing.

For OneSource specifically, the BIOSECURE Act creates urgency among potential customers. Many US companies are already looking for alternatives. When a pharmaceutical company needs to transfer a critical product from a Chinese CDMO, they need a partner with proven capabilities, regulatory approvals, and available capacity. OneSource checks all three boxes.

VII. Financial Performance & Growth Trajectory (35-45 min)

The numbers tell a compelling story, but you have to read between the lines to understand the real narrative. Revenue rose 33% to ₹1,445 crore in FY25, with a net profit of ₹93 crore. For a CDMO emerging from a complex merger, these aren't just good numbers—they're validation that the strategy is working.

Let's put this in context. OneSource is projected to achieve a remarkable 32% revenue growth in 2025, with sales anticipated to reach $400 million by 2028. This isn't hockey stick projection based on hope—it's based on contracted business and visible pipeline. In the CDMO world, where relationships are multi-year and switching costs are high, revenue visibility is remarkably strong.

The capital story is equally important. OneSource Specialty Pharma recently raised Rs 801 crore through equity issuance. This wasn't distressed fundraising—it was growth capital raised at a premium valuation from sophisticated investors who understood exactly what they were buying. The fundraising deal is based on a pre-money equity valuation of USD 1.65 billion.

The unit economics of the CDMO business are compelling once you reach scale. Unlike branded pharmaceuticals where you need massive marketing spending, or generics where you're in constant price competition, CDMO relationships are sticky, long-term, and relatively high-margin once you've absorbed the initial technology transfer costs. When a pharma company spends two years transferring a product to your facility and getting regulatory approvals, they're not switching for a 5% price difference.

The company anticipates a CAGR of over 30% through FY28, supported by increased operational efficiency and expansion into high-value biologics and drug-device combinations. This growth isn't coming from market share gains in commoditized products—it's coming from moving up the value chain into more complex, higher-margin products.

The margin story is particularly interesting. In Q2FY25, OneSource reported its third consecutive EBITDA positive quarter. For a business that was assembled from three different entities, achieving operational profitability this quickly suggests strong underlying unit economics and effective integration. The company is targeting an exit EBITDA of over $20 million by Q4FY25—aggressive but achievable given the current trajectory.

Capital allocation will be critical going forward. The company is proactively expanding its capacity for drug-device combinations and cartridge filling assembly, which will take up most of the capital expenditure investment. This isn't speculative capacity addition—it's responding to specific customer needs and market opportunities.

The working capital dynamics of the business are also favorable. Unlike branded pharma where you need to maintain inventory across multiple markets, or generics where customer payment terms can stretch, CDMO contracts typically include favorable payment terms and sometimes even customer-funded capacity expansions. This capital-light growth model, paradoxically in a capital-intensive industry, is part of what makes the business model so attractive.

What's not captured in the current numbers but crucial for the investment thesis is the value of the pipeline. When OneSource announces 15 new orders for GLP-1 related products, each of those represents a multi-year revenue stream. The lifetime value of a successful CDMO relationship can run into hundreds of millions of dollars. The current P&L only reflects the tip of the iceberg.

Risk-adjusted returns in the CDMO space can be exceptional. While the business requires significant upfront investment in facilities and quality systems, once you've achieved regulatory approvals and established customer relationships, the cash flow characteristics are excellent: high visibility, limited customer concentration risk if managed well, and natural growth as customers' products grow.

VIII. Strategic Investors & Market Validation (25-35 min)

Follow the smart money, and you'll find yourself at OneSource's door. A few weeks ago, asset management firm 360 ONE Asset invested in OneSource Specialty by acquiring a stake from an existing investor for an undisclosed amount. Market sources have pegged the deal at around $200 million. This wasn't a venture capital spray-and-pray investment—this was a calculated bet by sophisticated investors who understood the strategic positioning.

The investor roster reads like a who's who of smart Indian capital. 360 ONE Asset (formerly IIFL Wealth) manages money for India's ultra-high-net-worth individuals—people who made their fortunes building businesses and know how to evaluate them. When they write a $200 million check, they're not chasing momentum—they're buying into a thesis.

Promoter holding stands at 29.8%, decreased over last quarter by -4.46%. This might concern some investors, but it actually signals confidence. The promoters are reducing stake not through distressed selling but through premium transactions to strategic investors. They're crystallizing value while maintaining enough skin in the game to ensure alignment.

The pre-listing fundraise tells its own story. OneSource has secured commitments to raise ₹8,010 million (~USD 95 million) from prominent domestic and international investors, as well as family offices. Family offices—the investment vehicles of successful entrepreneurs—are particularly telling validators. These investors have built businesses themselves and understand the difference between financial engineering and genuine value creation.

Market validation extends beyond just financial investors. The customer list—while confidential—includes some of the world's most sophisticated pharmaceutical companies. When a company trusts you with a billion-dollar molecule, that's the ultimate validation. These aren't price shoppers—they're quality buyers who understand that in biologics manufacturing, the difference between 99% and 99.9% quality can be the difference between success and catastrophe.

The listing itself has been fascinating to watch. OneSource shall start trading on NSE and BSE from Friday, January 24, 2025 onwards. Strides shareholders will receive one OneSource equity share for every two Strides shares held. This structure—giving existing Strides shareholders direct ownership in OneSource—aligns interests and ensures a distributed, engaged shareholder base from day one.

The institutional investor interest speaks volumes. Institutional investors hold 47% stake, including 39.46% held by foreign investors - one of the highest in the pharma sector. Foreign institutional investors don't take concentrated positions in Indian companies lightly. They've done the work—facility visits, customer reference checks, regulatory due diligence—and concluded this is a bet worth making.

What's particularly interesting is who's not investing—or rather, who can't. Chinese capital, which has been aggressive in Indian markets, is notably absent. Strategic investors from Big Pharma are also missing, probably because OneSource serves multiple competing companies. This independence—not being captive to any single customer or geography—is actually a strength, even if it means forgoing certain sources of capital.

The valuation metrics are demanding but defensible. At a $1.65 billion pre-money valuation for a company with roughly $180 million in forward revenues, OneSource is priced for growth. But in the CDMO space, where relationships are long-term and switching costs are high, revenue multiples can be misleading. What matters is the quality of the revenue—its stickiness, growth potential, and margin structure.

IX. Playbook: The CDMO Business Model (25-30 min)

The CDMO business model is one of the great paradoxes of modern pharma: it's simultaneously capital-intensive and capital-efficient, commodity-like and highly differentiated, dependent and independent. Understanding these contradictions is key to understanding OneSource's strategy.

Start with the fundamental value proposition. Pharmaceutical companies face a build-versus-buy decision for manufacturing. Building requires massive capital investment, years of construction, regulatory approvals, and ongoing fixed costs whether you're at 20% or 80% utilization. Buying from a CDMO means variable costs, shared infrastructure, and the ability to scale up or down based on demand. In a world where drug development is increasingly risky and expensive, outsourcing manufacturing is often the only rational choice.

But not all CDMOs are created equal. At the bottom of the pyramid are simple API manufacturers—commodity producers competing on price. Move up, and you find sterile fill-finish providers, formulators, and specialized dosage form manufacturers. At the apex—where OneSource plays—are integrated CDMOs capable of handling complex biologics, drug-device combinations, and end-to-end development from preclinical through commercial manufacturing.

The moat in this business isn't just capital or capability—it's trust. When a pharmaceutical company hands over a molecule worth potentially billions of dollars, they're not just buying manufacturing capacity. They're buying quality systems, regulatory expertise, project management, and most importantly, the confidence that their partner won't compromise their product or intellectual property. Trust takes years to build and seconds to destroy.

Customer concentration is the Achilles' heel of many CDMOs. Lose one major customer, and revenues can crater. OneSource's strategy of serving multiple customers across multiple therapeutic areas and geographies provides diversification, but it also requires careful management. You can't have Pfizer and Merck's competing products in the same facility. Information barriers, physical separation, and operational discipline are essential.

Technology transfer—the process of moving a product from development to commercial manufacturing—is where CDMOs really earn their keep. It's part science, part art, and part project management. A successful tech transfer can shave months off a product launch. A failed one can kill a program entirely. OneSource's experience across hundreds of tech transfers is intellectual property that doesn't show up on the balance sheet but drives the P&L.

The importance of regulatory excellence cannot be overstated. A single FDA warning letter can shut down a facility for months or years. OneSource's clean regulatory track record across multiple facilities and jurisdictions isn't luck—it's the result of systematic investment in quality systems, training, and culture. In the CDMO world, your regulatory history is your resume.

Building trust with Big Pharma requires more than just capability—it requires cultural alignment. These companies have their own ways of working, their own quality standards, their own expectations. A CDMO that can adapt to different corporate cultures while maintaining its own standards is rare. It's the difference between being a vendor and being a partner.

The global CDMO landscape offers lessons and warnings. Lonza, the Swiss giant, shows the value of technological leadership and premium positioning. Catalent's recent struggles demonstrate the risks of over-leverage and operational complexity. Samsung Biologics proves that deep pockets and government support help but aren't sufficient without operational excellence. Each offers a playbook—or a cautionary tale—for OneSource's journey.

X. Risks, Competition & Bear Case (20-30 min)

Let's confront the uncomfortable truths. Company has low interest coverage ratio. Company has a low return on equity of -18.2% over last 3 years. These aren't just numbers to gloss over—they're red flags that demand explanation. The bear case for OneSource starts here: a company with weak historical financial metrics asking investors to believe in a transformation story.

The integration risk is real and present. Merging three distinct businesses—each with its own culture, systems, and processes—while maintaining GMP compliance and customer relationships is like performing heart surgery while running a marathon. One major quality issue during integration, one key customer loss, one regulatory setback, and the entire narrative unravels.

Competition isn't sleeping. Global giants like Lonza, Catalent (despite recent challenges), and Samsung Biologics have deeper pockets, longer track records, and established relationships with Big Pharma. Chinese CDMOs, even with BIOSECURE Act pressures, aren't disappearing—they're adapting, potentially setting up facilities in third countries or restructuring ownership to circumvent restrictions.

Customer concentration remains a structural risk. While OneSource serves multiple clients, the CDMO industry's reality is that a handful of products often drive the majority of revenues. If one major GLP-1 program gets cancelled, if one key customer decides to in-source manufacturing, the impact could be severe. The company hasn't disclosed customer concentration metrics, which itself is concerning.

The technology risk in biologics is particularly acute. The industry is moving toward increasingly complex modalities—cell therapies, gene therapies, mRNA vaccines. Does OneSource have the scientific depth to stay current? Can it afford the R&D investment required to maintain technological relevance? The company's current capabilities might be perfect for today's products but obsolete for tomorrow's.

Regulatory risks extend beyond just maintaining compliance. A single contamination event in biologics manufacturing can destroy entire batches worth tens of millions. A data integrity issue can trigger FDA scrutiny that takes years to resolve. The company operates in one of the most regulated industries on earth, where perfection is expected and anything less can be catastrophic.

The cyclical nature of CDMO demand is often underappreciated. When pharma companies are flush with cash, they outsource aggressively. When times get tough, they might pull manufacturing in-house to maintain utilization at their own facilities. OneSource is benefiting from a perfect storm of demand drivers—GLP-1 explosion, BIOSECURE Act, post-COVID supply chain diversification. What happens when these tailwinds fade?

Geopolitical risk cuts both ways. While OneSource benefits from the U.S.-China tensions, it's not immune to broader geopolitical dynamics. India-U.S. relations, while currently strong, aren't guaranteed to remain so. Trade policies, tax treaties, regulatory mutual recognition agreements—all could change with political winds.

The capital intensity of the business model is a persistent challenge. While CDMO relationships are sticky, winning new business requires continuous investment in capabilities and capacity. The company's current capex plans focused on drug-device combinations represent a bet that might not pay off if the market evolves differently than expected.

Finally, there's valuation risk. At a $1.65 billion pre-money valuation, OneSource is priced for perfection. The company needs to execute flawlessly on integration, capture share from Chinese competitors, ride the GLP-1 wave successfully, and avoid operational mishaps. That's a lot of things that need to go right to justify current valuations.

XI. Bull Case & Future Vision (20-25 min)

But here's why the bulls might be right: we're witnessing a structural shift in pharmaceutical manufacturing that happens perhaps once in a generation. The convergence of biological innovation, geopolitical realignment, and manufacturing technology is creating opportunities for those positioned correctly. OneSource isn't just in the right place at the right time—it's built the right capabilities for what's coming.

The structural shift to outsourcing in biopharma isn't a trend—it's a paradigm change. Drug development costs now routinely exceed $1 billion. No company, not even Big Pharma giants, can afford to build manufacturing capacity for every molecule in their pipeline. The make-versus-buy decision increasingly favors "buy," especially for complex biologics where the expertise required is so specialized.

OneSource expects significant growth in its order book over the next three years, driven by rising demand for weight-loss drugs. The company added 15 orders related to obesity and diabetes drugs in fiscal year 2025. This isn't speculative hope—it's contracted business that validates the bull thesis. The GLP-1 opportunity alone could drive growth for the next decade.

India's emergence as a trusted pharmaceutical manufacturing hub is accelerating. The COVID vaccine experience, where Indian manufacturers supplied billions of doses globally, demonstrated capability at scale. The PLI schemes, infrastructure investments, and regulatory harmonization efforts are creating an ecosystem that supports sophisticated manufacturing. OneSource is riding this wave, not fighting against it.

The expansion into drug-device combinations represents a massive opportunity that's still early innings. As biologics become more complex and patients demand more convenient delivery methods, the integration of drug and device becomes critical. OneSource's capabilities here—from cartridge filling to device assembly—position it for the next generation of pharmaceutical products.

The long runway for biologics is perhaps the most compelling part of the bull case. We're still in the early stages of the biological revolution in medicine. Cell therapies, gene therapies, bi-specific antibodies, antibody-drug conjugates—each represents massive markets that barely existed a decade ago. OneSource's platform can evolve to serve these emerging modalities.

The operational leverage in the model is just beginning to show. Once you've built the quality systems, achieved the regulatory approvals, and established the customer relationships, incremental revenue drops through at very high margins. The company's path to $400 million in revenue by 2028 might prove conservative if demand materializes as expected.

Network effects in the CDMO business are underappreciated. As OneSource successfully delivers for more customers, its reputation builds. As reputation builds, customer acquisition becomes easier and cheaper. As the customer base expands, the company can invest in more capabilities, attracting more customers. It's a virtuous cycle that, once spinning, is hard to stop.

The management team's track record suggests they know how to create value. Arun Kumar didn't build and sell Agila for $1.65 billion by accident. He didn't create and exit SeQuent Scientific to Carlyle by luck. This is a team that has repeatedly identified value, built capabilities, and crystallized returns. Betting against their ability to do it again might be unwise.

XII. Epilogue & Reflections (10-15 min)

As OneSource begins its journey as a public company, it's worth stepping back to consider what this means—not just for investors, but for India's pharmaceutical ambitions and the global industry's evolution.

The transformation from Strides subsidiary to standalone powerhouse isn't just a corporate restructuring—it's a case study in strategic vision and patient capital allocation. For three decades, Arun Kumar and his team have been building toward this moment, accumulating capabilities that would only reveal their full value when combined and unleashed at exactly the right time.

What OneSource represents for India is profound. For decades, Indian pharma was synonymous with cheap generics—necessary medicines made affordable for the world's poor, but not exactly cutting-edge innovation. OneSource is part of a new narrative: Indian companies as innovation partners, as builders of complex capabilities, as trusted manufacturers of the world's most sophisticated medicines.

For founders and investors, the OneSource story offers several key lessons. First, complexity is a moat if you can master it. While others raced to the bottom on simple generics, OneSource built capabilities in the most complex areas of pharmaceutical manufacturing. Second, timing matters more than being first. OneSource didn't invent CDMOs or biologics manufacturing, but it assembled the right capabilities at the right moment. Third, patient capital and strategic vision can create extraordinary value. The three-decade journey from a Navi Mumbai startup to a $1.65 billion valuation wasn't linear, but it was deliberate.

The future of specialized CDMOs in the biologics age looks bright but demanding. Success will require continuous innovation, flawless execution, and the ability to evolve with the science. OneSource has positioned itself well, but the race is just beginning. The winners will be those who can combine scientific excellence with operational discipline and strategic vision.

As we close this episode, consider this: OneSource's story is really three stories intertwined. It's a story about Indian entrepreneurship, about the evolution of pharmaceutical manufacturing, and about the opportunities created when geopolitics reshapes global supply chains. Each thread is compelling on its own. Woven together, they create a narrative that might just define the next chapter of global pharma.

The stock market will render its verdict daily on whether OneSource can deliver on its ambitious promises. But regardless of short-term price movements, what Arun Kumar and his team have built represents something significant: proof that Indian companies can compete at the highest levels of pharmaceutical complexity, serving the world's most demanding customers with the world's most sophisticated medicines.

For long-term fundamental investors, OneSource presents a fascinating proposition. It's not without risks—integration challenges, competition, and execution requirements are all real. But it's also not without remarkable opportunity—riding multiple secular trends with demonstrated capabilities and strategic positioning. Time will tell whether this bet on complexity, capability, and timing pays off. But one thing is certain: the story of OneSource is just beginning.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube