Lupin Limited: The Indian Generic Giant's American Dream

I. Introduction & Episode Roadmap

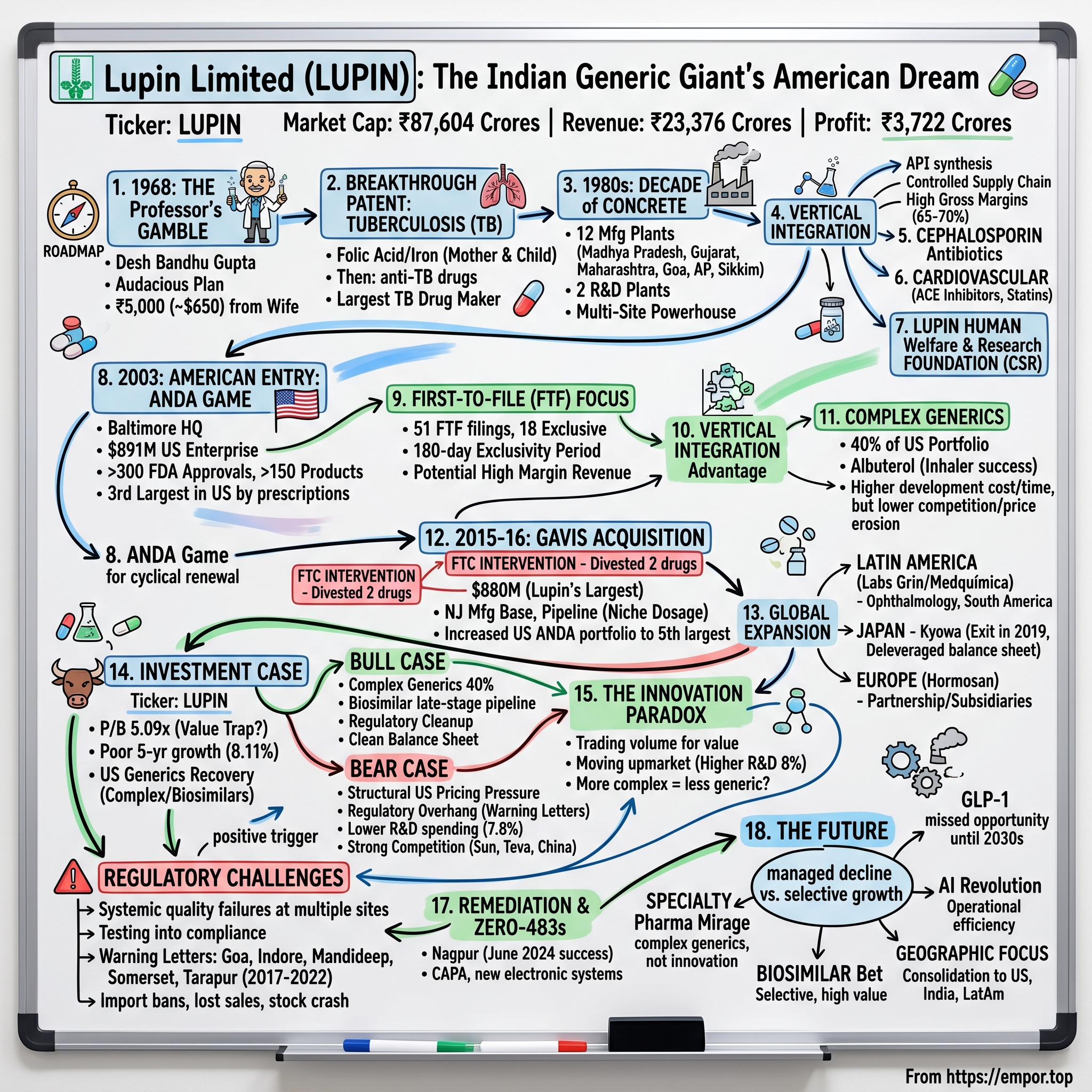

Picture this: A chemistry professor in dusty Rajasthan, 1968, walking into his modest home with an audacious plan. He needs 5,000 rupees—about $650 in those days—to start a pharmaceutical company. His wife, perhaps seeing something in his eyes that spreadsheets could never capture, hands over their savings. That professor was Desh Bandhu Gupta, and that moment would birth Lupin Limited, today a $3 billion revenue pharmaceutical powerhouse trading on the NSE with a market cap of ₹87,604 crores.

But here's what makes Lupin fascinating: unlike the Silicon Valley garage startup myth, this wasn't about disrupting an industry with technology. This was about mastering the unglamorous art of reverse-engineering molecules, navigating byzantine regulatory frameworks, and winning in the brutal economics of generic drugs—where your product is literally identical to your competitor's by definition. From a Rs. 5,000 startup to becoming India's third-largest pharmaceutical company by US prescriptions—this is a story about the unglamorous grind of generic drug manufacturing, where winning means mastering FDA regulations, optimizing API synthesis, and squeezing basis points from commodity-like margins. Lupin today generates ₹23,376 crores in revenue with profits of ₹3,722 crores, and is the third-largest pharmaceutical company in the U.S. by prescriptions.

How does a company from Mumbai become a dominant force in Baltimore pharmacies? How do you build competitive advantage when your product is, by law, identical to everyone else's? And in an industry where a single FDA warning letter can crater your stock price, how has Lupin navigated the treacherous waters of global pharmaceutical regulation?

This is the Lupin story—structured as building blocks, from those early tuberculosis contracts in India to today's complex biosimilar ambitions. We'll explore the Gavis acquisition that nearly got blocked by the FTC, the vertical integration playbook that created fortress economics, and the perpetual tension between remaining a generic manufacturer versus chasing the branded pharma dream. Along the way, we'll decode the ANDA game, understand first-to-file economics, and examine whether Lupin can transcend its generic roots.

So what for investors? With the stock trading at 5.09 times book value but delivering poor sales growth of 8.11% over five years, Lupin presents a classic value-versus-growth conundrum. The company's US generics recovery story and complex product pipeline offer upside, but persistent pricing pressure and regulatory overhang keep multiples compressed.

II. The Chemistry Professor's Gamble (1968–1980s)

The year is 1968. India has been independent for just 21 years. The country faces a healthcare crisis of staggering proportions: infant mortality rates hover around 146 per 1,000 births, life expectancy barely touches 47 years, and tuberculosis ravages entire communities. Into this landscape steps Desh Bandhu Gupta, a chemistry professor at BITS Pilani, one of India's premier technical institutions.

Gupta wasn't your typical entrepreneur. He was an academic, comfortable with molecular structures and reaction mechanisms, not balance sheets and cash flows. But he saw something others didn't: India's pharmaceutical industry was dominated by multinationals who had little interest in the diseases of the poor. Tuberculosis, malaria, basic nutritional deficiencies—these weren't profitable enough for Big Pharma's attention.

That Rs. 5,000 from his wife wasn't just seed capital; it was a vote of confidence in a radical idea. Gupta believed India could manufacture its own medicines, breaking free from expensive imports and multinational monopolies. The name "Lupin" itself came from the Lupin flower—hardy, resilient, able to grow in poor soil. Perhaps Gupta saw a metaphor there. The breakthrough came through an unlikely patron: the Central Bank of India. With funding from the Central Bank of India, the company was able to start their manufacturing facility for producing folic acid and iron tablets for the Indian government's mother and child health program. This wasn't venture capital chasing unicorns—this was public-sector banking supporting public health. The first Lupin facility wasn't producing blockbuster drugs; it was making basic nutritional supplements for government distribution programs.

But Gupta's masterstroke came with tuberculosis. In the 1970s, TB was India's silent killer, claiming hundreds of thousands of lives annually. The disease disproportionately affected the poor, making it commercially unattractive for multinationals. Gupta saw both mission and market. Lupin started manufacturing anti-tuberculosis (TB) drugs which at one point formed 36% of the company sales and was considered as the largest TB drugs manufacturer in the world.

Think about the strategic brilliance here: TB drugs required long treatment cycles (6-9 months), creating predictable revenue streams. Government procurement meant large-volume orders with assured payment. And most critically, success in TB established Lupin's credibility in anti-infectives—a therapeutic area that would later prove invaluable in global markets.

The company's early culture reflected Gupta's academic background. Unlike the wheeler-dealer pharmaceutical entrepreneurs of that era, Gupta approached drug manufacturing like a chemistry problem set. Process optimization, yield improvement, impurity profiles—these were the metrics that mattered. In the initial days, the company had only two employees—a peon-cum-packer and a part-time typist. From this humble beginning, Gupta built not just a company but an institution.

By 1979, Lupin had established its first formulations facility and R&D center in Aurangabad. The 1980s would see the company master cephalosporin antibiotics—a decision that would reshape its destiny. But in these early years, the foundation was being laid: a focus on essential medicines, deep government relationships, and an unwavering commitment to quality even when serving price-sensitive markets.

So what for investors? The TB focus wasn't just altruistic—it created a defensible niche with high barriers to entry (WHO prequalification, government relationships) and stable cash flows that funded future expansion. This pattern of finding underserved therapeutic areas would become Lupin's playbook.

III. Building the Indian Fortress (1980s–1990s)

By 1983, Lupin had outgrown its startup phase. Revenue had crossed ₹10 crores, the company employed over 200 people, and Gupta faced a critical decision: remain a domestic player focused on government contracts, or build the infrastructure for global ambitions. He chose the latter, embarking on what insiders called "the decade of concrete"—a massive capacity expansion that would transform Lupin from a single-plant operation into a multi-site pharmaceutical powerhouse.

The Mandideep facility in Madhya Pradesh, commissioned in 1987, became Lupin's crown jewel. This wasn't just another manufacturing plant; it was India's first dedicated cephalosporin facility with seven ACCA (7-Aminocephalosporanic acid) plants. Why cephalosporins? Gupta had identified a global supply gap. These broad-spectrum antibiotics were complex to manufacture, requiring fermentation technology and stringent contamination controls. Most Indian companies lacked the technical expertise or capital commitment. Lupin dove in headfirst. The geographical spread of Lupin's manufacturing empire reveals Gupta's strategic thinking. It has 12 manufacturing plants and 2 Research plants in India, as Jammu(J&K), Mandideep & Indore (Madhya pradesh), Ankaleswar & Dabasa (Gujarat), Tarapur, Aurangabad and Nagpur (Maharashtra), Goa, Visakhapatnam (Andhra Pradesh) and Sikkim. Each location was chosen deliberately: Madhya Pradesh for its central location and government incentives, Gujarat for chemical industry ecosystem, Maharashtra for proximity to Mumbai's financial center and ports.

The real game-changer was vertical integration. While competitors were content buying APIs from China and formulating finished drugs, Lupin went backwards into the value chain. The Ankleshwar facility in Gujarat, built in the late 1980s, became one of the world's largest integrated cephalosporin complexes. Lupin could now control everything from fermentation of the base molecule to the final tablet—a capability that would prove invaluable when FDA inspections became more stringent in later years.

Financial performance during this period tells the story: revenues grew from ₹10 crores in 1983 to over ₹100 crores by 1990, then exploded to ₹500 crores by 1995. The 1993 IPO of Lupin Laboratories Ltd. raised critical growth capital, valuing the company at ₹300 crores—a 60,000x return on that original ₹5,000 investment.

But numbers don't capture the operational excellence being built. Lupin's Mandideep plant achieved something remarkable: It has received the International Sustainability Rating System (ISRS) level 7 certification, the highest score in pharma manufacturing globally. This wasn't just about meeting standards; it was about setting them.

The cardiovascular portfolio became Lupin's second pillar alongside antibiotics. The company identified that ACE inhibitors and statins would become the world's largest drug categories as lifestyle diseases exploded globally. By the mid-1990s, Lupin was producing Lisinopril, Ramipril, and Atorvastatin APIs—molecules that would later generate billions in the US market.

In 1988 Gupta founded the group's CSR arm, the Lupin Human Welfare & Research Foundation (LHWRF). The project began with a set of rural development projects centred around 35 villages in Bharatpur District, Rajasthan. Later this expanded to other regions and states. The initiative has so far reached out to over 2.8 million people across over 3,400 villages in eight states of India.

This wasn't corporate whitewashing—Gupta understood that sustainable business required sustainable communities. The foundation's work in rural healthcare created grassroots brand loyalty that no advertising could buy. Village health workers became Lupin's unofficial ambassadors, recommending the company's antibiotics and creating pull-through demand at rural pharmacies.

So what for investors? The vertical integration strategy created significant barriers to entry and margin protection. When API prices spiked or supplies tightened (as would happen during COVID), Lupin maintained steady gross margins while competitors scrambled. The 12-plant network also provided regulatory redundancy—if one facility faced FDA issues, others could compensate.

IV. The American Entry: From Zero to Hero (2003–2010)

March 2003. The FDA's Orange County offices process yet another ANDA (Abbreviated New Drug Application) from an Indian company most Americans have never heard of. The drug: Cefuroxime Axetil tablets, a second-generation cephalosporin antibiotic. The applicant: Lupin Limited. This moment would mark the beginning of one of the most successful Asian pharmaceutical entries into the US market. To understand Lupin's US entry, you need to grasp the ANDA game. Unlike new drug applications that can cost billions and take a decade, ANDAs (Abbreviated New Drug Applications) are the generic drug pathway—prove bioequivalence to the brand, demonstrate manufacturing capability, and you can launch. But here's the catch: everyone else is doing the same thing. The first company to file often gets 180 days of exclusivity, during which they're the only generic on the market. Miss that window by a day, and your blockbuster opportunity becomes a commodity slugfest.

Since entering the pharmaceutical generics market in 2003 with ANDA approval for Cefuroxime Axetil Tablets, we have received over 300 FDA approvals and currently market more than 150 generics products in the U.S. The trajectory was remarkable—from zero to 300+ approvals in two decades.

But the real genius was in market selection. Rather than chase the crowded cardiovascular or diabetes segments where every Indian company was competing, Lupin focused on complex oral solids and niche therapeutic areas. The company targeted products with limited competition, higher barriers to entry, and stable pricing dynamics.

Headquartered in Baltimore, Maryland, Lupin Pharmaceuticals Inc. (LPI), the company's US subsidiary is a $891 million enterprise. It has a presence in the branded and generics markets of the US. The Baltimore headquarters wasn't just a sales office—it became a nerve center for understanding American pharmacy dynamics, insurance formularies, and the intricate dance between manufacturers, distributors, and pharmacy benefit managers.

The numbers tell the story of explosive growth. By 2007, Lupin had 18 ANDA approvals. By 2010, this had grown to over 50. But more importantly, Lupin was building relationships with the Big Three wholesalers—McKesson, AmerisourceBergen, and Cardinal Health—who control 90% of US drug distribution. Without their blessing, you could have the best generic drug in the world and it wouldn't reach a single pharmacy shelf.

Lupin's US strategy had three pillars:

-

First-to-File Focus: The company invested heavily in paragraph IV certifications, challenging brand patents. Win one of these, and you get 180 days of duopoly with the brand—margins can be 60-70% instead of the usual 15-20% for commoditized generics.

-

Vertical Integration Advantage: While competitors sourced APIs from China, Lupin's backward integration meant stable supply and quality control—critical when a single FDA warning letter could shut down your entire US business.

-

Customer Stickiness: Rather than being just another supplier, Lupin positioned itself as a reliable partner, never going on backorder, always meeting delivery commitments. In an industry plagued by shortages, reliability became a competitive advantage.

We are the 3rd largest generic company in the U.S. by the number of unbranded and branded generic prescriptions filled. This wasn't achieved through price wars but through strategic product selection and flawless execution.

The regulatory challenges were immense. The FDA inspected Indian facilities with increasing scrutiny, and Lupin faced its share of warning letters and 483s. But unlike some competitors who saw facilities banned from the US market, Lupin managed to remediate issues while maintaining supply continuity—a delicate balance that required significant investment in quality systems and compliance infrastructure.

So what for investors? The US market would eventually account for 37% of Lupin's global revenues, with EBITDA margins significantly higher than the corporate average. The ANDA portfolio became a moat—each approval representing 3-4 years of development work and $1-2 million in filing costs. With 300+ approvals, Lupin had built a $300-600 million replacement cost barrier that new entrants couldn't easily replicate.

V. The Gavis Acquisition: Lupin's Bold US Manufacturing Play (2015–2016)

February 2015. Lupin's board room in Mumbai. The discussion: whether to bet $880 million—nearly 40% of the company's market cap—on acquiring a New Jersey-based generic manufacturer most Indians had never heard of. GAVIS Pharmaceuticals wasn't a household name, but to Lupin's leadership, it represented something invaluable: a beachhead in US manufacturing and a pipeline of complex, high-margin products. The numbers were staggering: GAVIS Pharmaceuticals LLC and Novel Laboratories Inc. (GAVIS), subject to certain closing conditions, in a transaction valued at USD 880 million, cash free and debt free. For perspective, Gavis had revenues of just $96 million in FY2014—Lupin was paying 9.2 times annual revenue. In the frothy M&A market of 2015, this raised eyebrows even among bullish analysts.

But Lupin's management saw what others missed. Gavis wasn't just a revenue stream—it was a capabilities platform. The company had 66 ANDA filings pending approval with the US FDA and a pipeline of over 65 products under development. More critically, 72% of these filings were in niche dosage forms with limited competition. Gavis had filed 25 Para IVs (patent challenges) and eight first-to-file applications. Each successful FTF could generate $50-100 million in high-margin revenues during the exclusivity period.

GAVIS's New Jersey based manufacturing facility will become Lupin's first manufacturing site in the US. This wasn't just symbolic—it was strategic. Having US-based manufacturing meant faster response times to customer needs, reduced supply chain risk, and most importantly, credibility with the FDA. "Made in USA" still carried weight in the American pharmaceutical market, especially for controlled substances where DEA regulations made imports complex.

The FTC intervention added drama to the deal. Generic drug manufacturers Lupin Ltd. and Gavis Pharmaceuticals LLC will sell the rights and assets for two generic drugs, one used to treat bacterial infections and the other to treat ulcerative colitis, in order to settle FTC charges that Lupin's proposed $850 million acquisition of Gavis would likely be anticompetitive. The doxycycline monohydrate divestiture was particularly painful—this was a profitable product with limited competition.

But here's where Lupin's strategic thinking shone through. Rather than walking away or renegotiating, they accepted the divestitures. Why? Because the real value wasn't in the current portfolio but in the pipeline and capabilities. The acquisition creates the 5th largest portfolio of ANDA filings with the US FDA, addressing a USD 63.8 billion market. The combined company will have a portfolio of 101 in-market products, 164 cumulative filings pending approval and a deep pipeline of products under development for the US.

The integration challenges were significant. Gavis had a entrepreneurial, fast-moving culture—its founder, Dr. Veerappan Subramanian, had built the company as a nimble player that could out-execute larger competitors. Lupin, with its more structured Indian corporate culture, had to be careful not to stifle what made Gavis successful. The solution was semi-autonomy: Gavis continued to operate as a distinct unit within Lupin, maintaining its R&D focus while leveraging Lupin's global infrastructure.

The acquisition also accelerated Lupin's entry into complex generics. Gavis had expertise in controlled substances (Schedule II-V drugs), dermatology products, and modified-release formulations—all areas with higher barriers to entry and better pricing dynamics than simple oral solids. The Coral Springs, Florida inhalation R&D center complemented Gavis's New Jersey operations, creating a US-based innovation hub.

Financially, the deal was structured cleverly. At $880 million cash, it was Lupin's largest acquisition ever, but the company maintained a conservative debt-to-equity ratio by using accumulated cash and short-term bridge financing. The acquisition was expected to be accretive from the first full year—and it was, contributing significantly to Lupin's US revenues growing to over $900 million.

So what for investors? The Gavis acquisition transformed Lupin from an Indian company selling in America to an American company with Indian roots. The 164 pending ANDAs represented a shadow pipeline worth potentially $2-3 billion in peak sales. More importantly, US-based manufacturing and R&D capabilities created optionality for future growth, including potential entry into the branded specialty pharma market.

VI. Complex Generics & The Innovation Paradox

- A Lupin scientist in Coral Springs, Florida, holds up a small inhaler device. It looks identical to GlaxoSmithKline's Advair Diskus—and that's precisely the point. After seven years of development and over $100 million in R&D spending, Lupin has cracked one of the holy grails of generic pharmaceuticals: a generic version of a complex inhalation product. The FDA approval, when it comes, will unlock a market worth billions. Complex generics represent the innovation paradox of the generic drug industry. These aren't simple tablets where you prove bioequivalence and launch. We're talking about inhaled drugs, long-acting injectables, liposomal formulations, and biosimilars—products that blur the line between generic and innovative pharmaceuticals.

Over the past few years, we have made significant inroads in this space and launched products such as Filgrastim, Pegfilgrastim, Etanercept and Albuterol, among others, in different geographies around the world. The inhalation R&D center in Coral Springs, Florida, became Lupin's crown jewel of innovation. Here, scientists weren't just copying molecules—they were reverse-engineering complex delivery devices, matching particle size distributions, and ensuring identical lung deposition patterns.

Consider the economics: A simple oral generic might cost $1-2 million to develop and take 3-4 years. A complex inhaled product? Try $30-100 million and 7-10 years. But the payoff is proportional—while simple generics face immediate price erosion with multiple competitors, complex generics often have only 2-3 players, maintaining 40-50% of brand pricing instead of the typical 10-15%.

Our evolution into complex generics, particularly in inhalation and complex injectables, has been substantial, with these now making up 40% of our U.S. portfolio. This wasn't accidental—it was a deliberate strategic pivot recognizing that the era of easy generic wins was ending.

The biosimilar journey showcases both the promise and peril of this strategy. Lupin's etanercept biosimilar (for rheumatoid arthritis) gained approval in Japan and Europe, but the US market remained elusive. Why? Biosimilars face unique challenges: physician skepticism about switching stable patients, aggressive brand defense through patent thickets and rebate strategies, and the need for expensive clinical trials that traditional generics don't require.

We have made tremendous progress in our injectables portfolio, and are focused on four areas — iron products, peptides, depot injectables and partnered products. Each category represents different technical challenges and market opportunities. Depot injectables, for instance, require mastering polymer chemistry and release kinetics—capabilities that took years to build but create significant competitive moats.

The Albuterol inhaler success story deserves special attention. Albuterol, our key rescue inhalation product, has already garnered significant market share in the US. This seemingly simple asthma rescue inhaler required Lupin to crack the code on matching the reference product's plume geometry, spray pattern, and dose delivery—measured in micrograms across thousands of actuations. The FDA's bioequivalence requirements for inhaled products are among the most stringent in the world.

But here's the innovation paradox: The more complex and innovative Lupin's products became, the less they looked like traditional generics. R&D spending increased from 6% of sales to over 8%. Development timelines stretched. The company started hiring PhDs in aerosol physics and protein engineering—expertise you don't need for making generic statins.

This created tension within the organization. The old guard, who built Lupin on high-volume, low-cost manufacturing, questioned the ROI on these complex products. Why spend $50 million developing a biosimilar when you could develop 25 simple generics for the same cost? The answer lay in portfolio theory: complex products provided differentiation and margin protection even as the simple generics business commoditized.

The regulatory pathway for complex generics also differed fundamentally. Instead of simple ANDA filings, many required 505(b)(2) applications—a hybrid between generic and new drug applications. This meant more interactions with FDA, longer review times, but also potential for 3-year exclusivity periods that traditional generics don't receive.

So what for investors? The complex generics pivot is classic portfolio rebalancing—trading volume for value. With 40% of the US portfolio now in complex products, Lupin has partially insulated itself from generic pricing pressure. However, the higher R&D intensity (8% of sales vs. 4-5% for pure-play generics) and longer development cycles create a different risk-return profile that requires patience and deeper pockets.

VII. Global Expansion: Beyond US and India

The boardroom in Mumbai, 2014. Lupin's leadership faces a map dotted with acquisition targets: a Mexican ophthalmology specialist, a Brazilian generics manufacturer, a Japanese injectables company. The question isn't whether to expand globally—it's how to do it without losing focus or overpaying in the frothy M&A market. The answer would involve a series of calculated bets that would transform Lupin from a US-India bilateral player into a true multinational. The company's drugs reach 70 countries with a footprint that covers advanced markets such as USA, Europe, Japan, Australia as well as emerging markets including India, the Philippines and South Africa. But the real story is how Lupin built this presence—not through organic expansion but through a series of targeted acquisitions that provided instant market access and local expertise.

Latin America: The Ophthalmology Beachhead

In 2014, Lupin acquired 100% equity stake in Laboratories Grin, S.A. De C.V. (Grin), Mexico, a specialty pharmaceutical company engaged in the development, manufacturing and commercialization of branded ophthalmic products. At $28 million in revenues, Grin wasn't a blockbuster acquisition, but it provided something invaluable: a 60-year-old brand trusted by Mexican ophthalmologists.

Mexico represented a $13.5 billion pharmaceutical market growing at 9-10% annually. More importantly, it was a branded generics market where relationships with doctors mattered more than lowest price. Grin's specialized ophthalmic portfolio—eye drops, ointments, surgical preparations—gave Lupin a differentiated entry point rather than competing in crowded primary care segments.

The Brazil entry came through Medquímica in May 2015. In May 2015, Lupin entered the Brazilian market with its acquisition of 100% stake in Medquímica Indústria Farmacêutica S.A., Brazil, (Medquímica). With 550 employees and a 40-year history, Medquímica brought credibility in South America's largest pharmaceutical market. Brazil's unique regulatory environment—requiring local manufacturing for many government tenders—made acquisition the only viable entry strategy.

Japan: The Failed ExperimentJapan represents Lupin's most instructive failure. After acquiring Kyowa Pharmaceutical in 2007 and growing it to become Japan's fifth-largest generic company, Lupin threw in the towel in 2019. In 2019, Lupin exited the generic pharmaceuticals business in Japan by divesting its stake in Kyowa to private equity firm Unison for an enterprise value of Japanese 57,361 million yen (Rs 3,702.4 crore).

The Japan story illuminates the challenges of global expansion. Despite government initiatives to increase generic penetration from 30% to 80%, foreign companies struggled with Japan's unique requirements: local clinical trials even for approved generics, complex distribution through multiple wholesalers, and physician preference for branded originals. Lupin's Kyowa generated revenues of JPY 28,335 million in FY2019, but growth had stalled and margins were compressing.

The divestiture decision was strategic portfolio management at its best. Rather than doubling down on a struggling market, Lupin took the proceeds—approximately Rs 2,100 crores post-tax—to deleverage the balance sheet and redeploy capital to higher-return opportunities. Net debt dropped from Rs 4,361 crores to Rs 1,129 crores, giving the company firepower for future acquisitions in more attractive markets.

Europe and Rest of World: The Partnership Model

Rather than acquisitions, Lupin's European strategy relied on partnerships and licensing deals. The company established subsidiaries in Germany (Hormosan) and the UK, but focused on niche products rather than broad portfolios. The strategy was capital-light but also growth-constrained—Europe remained less than 10% of global revenues.

South Africa and the Philippines represented different approaches. In South Africa, Lupin built an organic presence, leveraging the country's role as a gateway to sub-Saharan Africa. The Philippines operation focused on branded generics, where doctor relationships and medical representative networks still mattered more than price.

The Portfolio Effect

By 2019, Lupin's global footprint looked impressive on paper but revealed strategic tensions: - The US remained the profit engine (40%+ of revenues, higher margins) - India provided volume and cash flow stability (35% of revenues) - Latin America showed promise but required continued investment - Japan had been abandoned after years of trying - Europe remained subscale despite multiple attempts

The lesson? Geographic diversification sounds good in investor presentations but execution complexity multiplies exponentially. Each market has unique regulatory requirements, distribution channels, pricing dynamics, and competitive landscapes. Lupin learned that being subscale in multiple markets is often worse than being dominant in a few.

So what for investors? The global expansion story is mixed. Latin American acquisitions (Grin, Medquímica) provide beachheads in growing markets with reasonable returns. The Japan exit showed management discipline in cutting losses. But the scattered geographic presence increases complexity without delivering the portfolio diversification benefits that investors seek. The company remains fundamentally dependent on US and India—everything else is optionality, not core value.

VIII. Business Model & Unit Economics

Strip away the corporate speak and Lupin's business model is deceptively simple: buy raw chemicals for $X, transform them into FDA-approved medicines, and sell them for $10X—if you're lucky. The entire generic drug industry operates on this arbitrage, but the devil, as always, lurks in the details. Understanding Lupin's unit economics requires peeling back layers of complexity that most investors never see.

We are vertically integrated, from process development of the API to the submission of dossiers for finished dosages. This provides control over the supply chain and the ability to offer quality products at the right time—and the right price. But what does vertical integration actually mean in practice?

The API-to-Formulation Value Chain

Consider a typical generic drug like Lisinopril (for blood pressure). The value chain looks like this:

- Basic chemicals (~$10/kg): Commodity inputs from China/India

- Intermediates (~$50/kg): Multi-step synthesis requiring specialized equipment

- API (~$200/kg): Final active ingredient meeting pharmacopoeia standards

- Formulation (~$2,000/kg equivalent): Tablets with excipients, coating, packaging

- Finished product (~$10,000/kg equivalent at wholesale): FDA-approved, branded bottles

At each step, value multiplies but so does complexity. Most generic companies operate only in steps 4-5, buying APIs from China and formulating tablets. Lupin operates across steps 2-5, capturing more value but requiring massive capital investment in fermentation tanks, clean rooms, and quality systems.

ANDA Economics: The 180-Day Lottery

The Abbreviated New Drug Application (ANDA) process is where fortunes are made or lost. Here's the math:

- Development cost: $1-3 million for simple oral solid, $10-50 million for complex generics

- Timeline: 3-4 years for simple products, 7-10 years for complex

- FDA approval probability: ~90% for established players like Lupin

- Market dynamics post-approval:

- First-to-file with 180-day exclusivity: 60-80% of brand price

- Second entrant: 40-50% of brand price

- Third entrant: 20-30% of brand price

- Fourth+ entrant: 10-15% of brand price (commodity pricing)

The company now has 51 First-to-File (FTF) filings including 18 exclusive FTF opportunities. Each exclusive FTF represents a potential $50-200 million revenue opportunity during the exclusivity period. Do the math: 18 exclusive FTFs could mean $900-3,600 million in high-margin revenues—but only if Lupin successfully challenges patents and launches first.

The Price Erosion Reality

Generic drug pricing follows a predictable decay curve: - Launch year: 100% of initial generic price - Year 2: 70-80% - Year 3: 50-60% - Year 4+: 30-40%

This erosion accelerates with more competitors. A product with two players might maintain 60% of launch pricing after three years. The same product with six players might drop to 20%. This is why Lupin focuses on complex generics—fewer competitors mean slower price erosion.

Manufacturing Scale Economics

Lupin's 15 manufacturing facilities represent both strength and burden:

Fixed costs (annual): - Facility maintenance: $5-10 million per plant - Quality/regulatory compliance: $3-5 million per plant - Base staffing: $10-15 million per plant - Total: ~$20-30 million per plant regardless of utilization

Variable costs (per batch): - Raw materials: 30-40% of sales - Direct labor: 5-10% of sales - Utilities: 3-5% of sales - Total: ~40-55% of sales

The math is brutal: each facility needs $50-100 million in annual revenue just to break even. Run at 50% capacity? Your unit costs double. This is why Lupin's focus on supply reliability becomes a competitive advantage—consistent volumes mean better capacity utilization and lower unit costs.

R&D Allocation: The Portfolio Approach

The company invested 7.8% of its revenue in research and development in FY24. But not all R&D is equal:

- Simple generics (30% of R&D): $1-2 million per ANDA, 3-year timeline, 10-15% IRR

- Complex generics (40% of R&D): $10-30 million per product, 5-7 year timeline, 20-25% IRR

- Biosimilars (20% of R&D): $50-100 million per product, 7-10 year timeline, 25-30% IRR

- 505(b)(2) products (10% of R&D): $20-50 million per product, 5-7 year timeline, 30%+ IRR

The portfolio approach means accepting that 30-40% of products will fail or generate minimal returns, 40-50% will meet hurdle rates, and 10-20% will be blockbusters that pay for everything else.

Channel Economics and Working Capital

The US generic distribution model adds another layer of complexity:

- Lupin sells to Big 3 wholesalers at WAC (Wholesale Acquisition Cost) minus 40-50% discount

- Wholesalers sell to pharmacies at WAC minus 15-20%

- Pharmacies get reimbursed by insurance at MAC (Maximum Allowable Cost) plus dispensing fee

- Lupin pays rebates to GPOs/buying groups (another 10-15% of WAC)

Net result: Lupin realizes only 35-45% of the list price. Working capital requirements are massive—wholesalers pay in 30-60 days, but Lupin must maintain 3-6 months of inventory. Cash conversion cycles stretch to 120-150 days.

The Vertical Integration Advantage

Because our manufacturing is also integrated, we are able to closely monitor the integrity of our generic products, a competitive advantage in an industry where customer trust and safety are non-negotiable. But the real advantage is economic:

- Gross margins: 65-70% for integrated players vs. 45-50% for formulation-only

- Supply security: No dependence on Chinese API suppliers during disruptions

- Regulatory leverage: Single quality system from API to finished product

- Cost advantage: 20-30% lower total costs versus non-integrated competitors

So what for investors? Lupin's business model creates high barriers to entry (vertical integration, regulatory expertise) but also high fixed costs that pressure margins during downturns. The ANDA portfolio of 300+ approvals represents $300-600 million in sunk development costs—a massive moat but also trapped capital. The key metric to watch: contribution margin per product. When this drops below $1 million annually, products become value-destructive regardless of volumes.

IX. Regulatory Challenges & Quality Control

March 2019. FDA investigators walk into Lupin's Tarapur facility for a routine inspection. What they find leads to a warning letter that will wipe out $2 billion in market value in a single day. This wasn't Lupin's first regulatory rodeo—and it wouldn't be the last. Understanding Lupin's regulatory challenges requires understanding the FDA's evolution from quality checker to global pharmaceutical police force.

The regulatory landscape for Indian pharma has transformed dramatically. In 2000, FDA conducted 50 inspections in India. By 2019, that number exceeded 400. The scrutiny isn't just about tablet weight or dissolution rates anymore—it's about data integrity, quality culture, and documentation practices that can differ vastly between Indian and American approaches.FDA has cited similar CGMP violations at two other facilities in your company's manufacturing network. On November 6, 2017, we issued a warning letter to your facilities Lupin Limited, Goa, (FEI 3004819820) and Lupin Limited, Indore (FEI 3007549629). These repeated failures at multiple sites demonstrate that management oversight and control over the manufacture of drugs are inadequate.

This damning statement from a 2019 warning letter encapsulates Lupin's regulatory challenges: systemic quality issues across multiple facilities, suggesting corporate-level failures rather than isolated incidents.

The Data Integrity Crisis

The most serious violations centered on data integrity—the pharmaceutical equivalent of accounting fraud. At Lupin's plant in Indore, analysts ignored nearly all of the initial out-of-spec testing results, 134 of 139 in a two-year period, the FDA said. Think about that: when a test showed a product failing specifications, Lupin's response 96% of the time was to invalidate the test rather than investigate the product.

The practice, known as "testing into compliance," involves retesting samples until you get a passing result, then using statistical gymnastics to declare the failing results as "outliers." It's like flipping a coin until you get heads, then declaring all the tails don't count. The FDA doesn't find this amusing.

The Warning Letter Cascade

Lupin's regulatory troubles followed a predictable cascade:

- Initial 483 observations (minor violations noted during inspection)

- Escalation to Warning Letter (serious violations requiring immediate correction)

- Import Alert (products from facility banned from US market)

- Consent Decree (court-supervised remediation—the nuclear option)

Between 2017 and 2022, Lupin facilities received multiple warning letters: - November 2017: Goa and Indore facilities - September 2019: Mandideep Unit 1 - June 2021: Somerset, New Jersey (the prized US facility from Gavis acquisition) - September 2022: Tarapur API facility

Each warning letter triggers a cascade of consequences: new product approvals freeze, customer confidence erodes, remediation costs explode, and stock price craters.

The Cultural Divide

The root cause often traces to fundamental cultural differences in quality philosophy:

Indian approach (historically): - Quality as a cost center to be minimized - Documentation as bureaucratic burden - Testing as a hurdle to overcome - Inspections as events to prepare for

FDA expectations: - Quality as integral to operations - Documentation as real-time truth - Testing as scientific investigation - Continuous state of inspection readiness

Lupin has spent millions trying to bridge this gap, hiring ex-FDA officials as consultants, implementing electronic batch records, and creating "quality councils." But changing culture is harder than changing SOPs.

The Cost of Compliance

The financial impact of regulatory issues extends far beyond remediation costs:

Direct costs: - Remediation consultants: $10-20 million per facility - System upgrades: $5-10 million per facility - Additional quality staff: $3-5 million annually per facility - Lost product sales during import bans: $50-100 million per event

Indirect costs: - Delayed product launches: $100-200 million in lost opportunity - Customer switching to competitors: 10-20% volume loss - Stock price impact: 20-30% decline per warning letter - Management distraction: Immeasurable

The Remediation Playbook

Lupin's response follows the industry playbook:

- Hire consultants (preferably ex-FDA officials)

- Implement CAPA (Corrective and Preventive Actions)

- Retrain personnel (often the same training, again)

- Upgrade systems (electronic everything)

- Request reinspection (and pray)

The June 2024 success story—zero 483 observations at the Nagpur injectable facility—shows remediation can work. But it takes years and millions of dollars per facility.

The Competitive Impact

Regulatory issues create a vicious cycle. While Lupin remediates facilities, competitors launch products. When Lupin returns to market, pricing has eroded and market share has been lost. The opportunity cost often exceeds the direct remediation cost.

Consider the Tarapur facility, which manufactured key APIs. We acknowledge your commitment to suspend production of drugs for the U.S. market. Every day of suspension means lost sales, idle capacity, and customers finding alternative suppliers who may never return.

So what for investors? Regulatory issues are the sword of Damocles hanging over every Indian pharma investment. Lupin's multiple warning letters suggest systemic issues that will take years and hundreds of millions to fully resolve. The recent zero-483 inspection offers hope, but with 15 facilities globally, the company remains one bad inspection away from another crisis. Factor in a 20-30% "regulatory discount" to valuations until Lupin achieves multiple years of clean inspections across all facilities.

X. Competitive Landscape & Market Dynamics

The global generics industry resembles a giant game of musical chairs where the music never stops but chairs keep disappearing. Prices erode 10-20% annually, new competitors emerge from China and Eastern Europe, and consolidation creates behemoths that dwarf individual players. In this environment, Lupin's position as the 3rd largest generic company in the U.S. by prescriptions sounds impressive—until you realize what that actually means in economic terms.

The Indian Pharma Hierarchy

Within India's pharmaceutical elite, pecking order matters:

- Sun Pharma (Market cap: ~₹400,000 crores): The undisputed king, built through serial acquisitions including Ranbaxy and Taro

- Dr. Reddy's (Market cap: ~₹150,000 crores): The pioneer in Indian pharma's US journey

- Cipla (Market cap: ~₹130,000 crores): Respiratory specialist with strong emerging market presence

- Lupin (Market cap: ~₹87,000 crores): The former high-flyer now playing catch-up

- Aurobindo (Market cap: ~₹75,000 crores): The quiet executor with minimal regulatory issues

Each company carved out different niches. Sun Pharma pursued specialty dermatology, Dr. Reddy's focused on complex generics and biosimilars, Cipla dominated respiratory, while Lupin bet on cardiovascular and diabetes. The strategies diverged, but the destination remained the same: the lucrative US market.

The Global Giants

Internationally, Lupin faces different beasts entirely:

- Teva (Israel): Despite its debt troubles, still 3x Lupin's size with unmatched distribution

- Viatris (Mylan + Upjohn): The merger created a $17 billion revenue giant

- Sandoz (Novartis spinoff): European leader with biosimilar expertise

- Hikma (Jordan/UK): Focused on injectables and the Middle East

These players operate at a different scale. Teva launches 300+ products annually; Lupin manages 20-30. When Teva enters a market, pricing drops 30-40% overnight. Lupin must pick its battles carefully.

The China Threat

The elephant in the room is China. Companies like Huahai Pharmaceutical and Zhejiang Hisun aren't just API suppliers anymore—they're moving up the value chain into finished dosages. Their cost structure is 30-40% below Indian players:

- Labor costs: 50% of India

- Electricity: 60% of India costs

- Environmental compliance: "Flexible" (though tightening)

- Government support: Substantial subsidies and tax breaks

When Chinese players enter a market, it's game over for pricing. Lupin's response has been to move upmarket into complex products where regulatory barriers protect margins—for now.

The Consolidation Wave

Since entering the pharmaceutical generics market in 2003 with ANDA approval for Cefuroxime Axetil Tablets, we have received over 300 FDA approvals and currently market more than 150 generics products in the U.S. We are the 3rd largest generic company in the U.S. by the number of unbranded prescriptions. But market share doesn't equal profitability.

The consolidation math is brutal: - Top 3 wholesalers control 90% of US distribution - Top 3 PBMs control 80% of covered lives - Top 3 retail chains control 40% of prescriptions

This concentration gives buyers unprecedented pricing power. Lupin might be #3 by prescriptions, but it has zero leverage in price negotiations.

The PBM/GPO Squeeze

Pharmacy Benefit Managers (PBMs) and Group Purchasing Organizations (GPOs) have become the de facto gatekeepers of the US generic market:

- Formulary placement requires rebates of 30-50% off list price

- Exclusive contracts demand additional 10-20% discounts

- Failure to supply penalties can reach millions per incident

- Price protection clauses prevent any increases

Lupin's response has been to focus on products where it's one of only 2-3 suppliers, maintaining some pricing power. But these opportunities are shrinking.

Portfolio Analysis: Where Lupin Stands

Breaking down Lupin's competitive position by category:

Strong positions (Top 3 market share): - Certain cardiovascular generics (legacy strength) - Select diabetes products (though facing erosion) - Niche respiratory products (limited competition) - Some women's health products (from Gavis)

Weak positions (Outside top 5): - Pain management (dominated by Teva, Mylan) - Oncology generics (late entry, established competition) - Most CNS products (except specific niches) - Basic antibiotics (commoditized)

Emerging positions (Potential growth): - Complex respiratory generics - Biosimilars (early stage) - Specialty injectables - Ophthalmic products (from Grin acquisition)

The Differentiation Dilemma

How do you differentiate when your product is legally required to be identical to competitors'? Lupin's answers:

- Supply reliability: Never going on backorder (easier said than done)

- Customer service: Dedicated account management (table stakes now)

- Portfolio breadth: One-stop shopping (but others have broader portfolios)

- Speed to market: First-to-file positions (highly valuable but rare)

- Manufacturing location: US-made from Somerset facility (some value)

The harsh reality: in commodity generics, the only real differentiation is price.

Biosimilar Battleground

Biosimilars represent both opportunity and threat. Lupin's biosimilar pipeline includes high-value targets, but competition is fierce:

- Development costs: $100-200 million per biosimilar

- Timeline: 7-10 years

- Competitive field: Big Pharma entering aggressively

- Market dynamics: Only 2-3 players can survive per product

Lupin lacks the deep pockets of Pfizer or Amgen in biosimilars. It must choose targets carefully and likely needs partnerships to compete.

Market Share Reality Check

Let's decode what "3rd largest by prescriptions" actually means:

- Prescription volume: High (millions of scripts)

- Revenue per prescription: Low and declining ($10-20 average)

- Market value share: Much lower than volume share (probably 5-7%)

- Profitability rank: Likely outside top 5

Volume leadership without pricing power is a recipe for working harder to stay in the same place—the Red Queen problem.

So what for investors? Lupin operates in one of the world's most competitive industries where moats are narrow and temporary. The company's #3 position by US prescriptions is misleading—it's like being the third-largest seller of bottled water by volume. The real competitive advantage lies in the complex generics pipeline and first-to-file positions, not in the commodity portfolio. Watch for portfolio mix shift toward complex products as the key driver of competitive positioning, not market share headlines.

XI. Analysis & Investment Case

Let's cut through the noise. Lupin trades at ₹1,934 per share with a market cap of ₹87,604 crores. The stock is down 9.25% over the past year while the Nifty Pharma index is up 35%. Something isn't working. The question for investors: is this a value trap or a turnaround story trading at a discount?

The Numbers That Matter

Mkt Cap: 87,604 Crore (down -9.25% in 1 year) · Revenue: 23,376 Cr · Profit: 3,722 Cr · Stock is trading at 5.09 times its book value · The company has delivered a poor sales growth of 8.11% over past five years. Promoter Holding: 46.9%

Let's add context to these numbers:

Valuation Metrics: - P/E ratio: ~23x (vs. industry average of 28x) - P/B ratio: 5.09x (expensive for a manufacturing business) - EV/EBITDA: ~12x (reasonable for pharma) - Dividend yield: 2.1% (400% dividend payout) - Net Debt-Equity as on March 31, 2024 stands at 0.03.

The balance sheet is clean post-Kyowa divestment, but growth has stalled.

The Bull Case

The optimists see multiple triggers:

-

Complex generics traction: Our evolution into complex generics, particularly in inhalation and complex injectables, has been substantial, with these now making up 40% of our U.S. portfolio. Higher margins, less competition.

-

US recovery: After years of pricing pressure, the US generics market is stabilizing. Lupin's reliability during COVID shortages strengthened customer relationships.

-

Biosimilar optionality: Late-stage pipeline in high-value biologics. One successful launch could add ₹1,000+ crores in annual revenue.

-

Regulatory cleanup: Recent zero-483 inspections suggest quality issues are being resolved. Each clean inspection removes discount from valuation.

-

India growth: Lupin is the 7th largest company in the Indian Pharmaceutical Market (IQVIA MAT Mar 2024). Domestic market growing at 10-12% annually with improving margins.

-

Hidden assets: The Company now has 51 First-to-File (FTF) filings including 18 exclusive FTF opportunities. Each exclusive FTF could generate ₹200-500 crores during exclusivity period.

The Bear Case

The pessimists have their own ammunition:

-

Structural headwinds: US generic pricing pressure is structural, not cyclical. No amount of complexity can fully offset commoditization.

-

Regulatory overhang: Multiple warning letters suggest deep-rooted quality issues. One bad inspection could trigger another crisis.

-

Innovation deficit: The company invested 7.8% of its revenue in research and development in FY24. Below industry leaders spending 10-12%. Innovation pipeline is thin.

-

Execution issues: The company has delivered a poor sales growth of 8.11% over past five years. Management has consistently over-promised and under-delivered.

-

Competitive disadvantage: Smaller than Sun Pharma, less innovative than Dr. Reddy's, more regulatory issues than Cipla. Stuck in the middle.

-

Gavis disappointment: The $880 million acquisition hasn't delivered promised returns. Integration challenges and market dynamics disappointed.

The Realist's View

Strip away the optimism and pessimism, and here's what remains:

Lupin is a decent company in a terrible industry. The generic drug business model is fundamentally broken—prices decline perpetually, development costs rise continuously, and regulatory requirements tighten relentlessly. It's like running up a down escalator that accelerates every year.

accounting for 37% of Lupin's global sales. Q4 FY2024 sales were INR 19,006 mn, up 0.6% compared to INR 18,885 mn in Q3 FY2024; up 22.6% compared to INR 15,503 mn in Q4 FY2023; accounting for 39% of Lupin's global sales. US FY2024 sales were USD 815 mn compared to USD 632 in FY2023.

The US business shows recovery, but from a low base. India provides stability but limited growth. Everything else is subscale.

The Investment Framework

Think of Lupin as three businesses:

-

Cash cow (60% of value): Existing generic portfolio generating steady but declining cash flows. Value this at 8-10x EBITDA.

-

Growth option (30% of value): Complex generics and biosimilar pipeline. High risk, high reward. Value using probability-weighted NPV.

-

Regulatory liability (−10% of value): Ongoing compliance costs and risk of future issues. Apply a permanent discount.

Scenario Analysis

Best case (20% probability): - Clean regulatory slate achieved - 2-3 biosimilar launches successful - US pricing stabilizes - Stock re-rates to ₹3,000 (15x EV/EBITDA)

Base case (60% probability): - Gradual improvement in operations - Mixed success in complex generics - Regulatory issues contained but not eliminated - Stock ranges ₹1,800-2,200 (current multiples)

Worst case (20% probability): - Another major warning letter - Biosimilar failures - Accelerated US pricing pressure - Stock drops to ₹1,200 (8x EV/EBITDA)

Expected value: ₹2,040 (roughly current price)

The Capital Allocation Question

Based on the long-term outlook the Board has recommended a dividend of 400%. This signals confidence but also lack of growth opportunities. If management saw high-return projects, why return so much capital?

The company sits on minimal net debt but isn't deploying capital aggressively. This suggests either: 1. Management is disciplined (good) 2. No attractive opportunities exist (bad) 3. Regulatory issues prevent expansion (ugly)

Relative Valuation

Versus peers, Lupin looks neither cheap nor expensive: - Trades at discount to Sun Pharma (deserved given scale difference) - Premium to Aurobindo (questionable given regulatory issues) - In-line with Dr. Reddy's (despite inferior innovation pipeline)

The market is pricing Lupin as a middle-of-the-pack player, which seems fair.

The Verdict

Lupin is a "show me" story. Management must prove they can: 1. Keep facilities inspection-ready 2. Successfully launch complex generics 3. Stabilize US pricing through mix improvement 4. Generate returns above cost of capital

Until then, it's dead money for growth investors and too risky for value investors—stuck in no-man's land.

So what for investors? At current valuations, Lupin offers limited upside with significant downside risk. The stock is appropriate only for investors who believe in the complex generics transformation story and can stomach regulatory volatility. For others, better risk-reward exists elsewhere in pharma. The 400% dividend suggests even management sees limited reinvestment opportunities. This is a trading stock, not a compounder.

XII. The Future: What's Next for Lupin?

- Lupin stands at a crossroads familiar to every successful generic company: remain a fast follower or attempt the leap to innovation. The company's future hinges on navigating three fundamental tensions: specialty versus generic, global versus focused, and innovation versus imitation.

The Specialty Pharma Mirage

Every generic company dreams of becoming a specialty pharma player. Higher margins, patent protection, pricing power—it's the promised land. Lupin is no different. Generic manufacturers are shifting towards hybrid models, investing in complex generics, inhalation therapies, injectables, and specialty pipelines. This transition is driven by margin pressures, regulatory complexity, and the need for differentiation in global markets.

But here's the uncomfortable truth: the graveyard of pharma is littered with generic companies that tried and failed to make this transition. Teva's Copaxone success was the exception, not the rule. Most generic companies lack the clinical development expertise, regulatory experience, and deep pockets required for innovative drug development.

Lupin's approach is more measured—what they call "specialty lite": - Complex generics that require some innovation but not full clinical trials - 505(b)(2) products that leverage existing safety data - Biosimilars where the reference product provides a development roadmap - Specialty generics in niche therapeutic areas

It's not true innovation, but it's a step up from commodity generics.

The AI Revolution Question

AI is revolutionizing pharma across the value chain—from drug discovery and clinical trials to commercial analytics and supply chain optimization. GenAI is expected to deliver up to 11% value relative to revenue in biopharma, with applications in molecule design, patient stratification, and predictive modeling.

But AI in pharma faces the "last mile" problem. You can use AI to identify drug targets, optimize molecules, even predict clinical trial outcomes. But you still need to run the actual trials, navigate regulatory approval, and manufacture at scale. AI accelerates discovery but doesn't eliminate the fundamental time and cost of drug development.

For Lupin, AI represents more opportunity in operational efficiency than drug discovery: - Predictive maintenance in manufacturing - Supply chain optimization - Pharmacovigilance automation - Regulatory document generation

These aren't sexy applications, but they could reduce costs by 10-15%—meaningful in a margin-compressed industry.

The Biosimilar Bet

Looking forward, Multicare has a robust pipeline of new product launches scheduled for FY25 and FY26, which include biosimilars and specialty products. This strategic focus on expanding and diversifying its product offerings is expected to drive continued growth and solidify its market position.

Biosimilars represent Lupin's biggest swing for the fences. Unlike small molecule generics, biosimilars maintain 70-80% of originator pricing and face limited competition. But the challenges are immense:

- Development costs of $100-200 million per product

- Manufacturing complexity requiring dedicated facilities

- Physician education to overcome switching reluctance

- Originator companies fighting back with authorized biosimilars

Lupin's biosimilar strategy appears selective—focusing on products where they have existing commercial relationships and can leverage their manufacturing infrastructure. It's not trying to compete with Samsung Bioepis or Celltrion in every biosimilar; it's picking its spots.

Geographic Focus vs. Global Ambitions

The U.S. pharmaceutical market is the largest in the world, with a net value of USD 487 Bn in 2024, and is expected to grow at a CAGR between 3% and 6% from 2025 to 2030. North America remains a cornerstone of Lupin's global strategy.

The geographic strategy appears to be consolidating around core markets: - US: Remain focused on complex generics and niche products - India: Leverage brand equity and distribution for steady growth - Europe: Selective participation through partnerships - Latin America: Build on Grin/Medquímica base - Rest of World: Opportunistic only

This is portfolio rationalization, not expansion. After the Japan exit, expect more pruning of subscale markets.

The Next Generation Leadership Question

The founder, Desh Bandhu Gupta died in June 2017 and was subsequently replaced as chairman by his wife, Manju Deshbandhu Gupta. The second generation—Vinita Gupta (CEO) and Nilesh Gupta (MD)—have been running operations for years. But founder-led companies often struggle with third-generation transitions.

The leadership challenge for Lupin: - Maintaining entrepreneurial culture in a regulated industry - Balancing family control with professional management - Attracting top talent when competing with MNCs - Making hard decisions about underperforming assets

The 46.9% promoter holding provides stability but also limits strategic flexibility. Will the family double down or gradually dilute?

The Innovation Reality Check

Let's be honest about Lupin's innovation capabilities: - No novel drug has ever emerged from Lupin's labs - The biosimilar pipeline is me-too, not first-in-class - Complex generics are still generics, just harder to make - R&D spending at 7.8% is below industry leaders

This isn't necessarily bad. Pure innovation is a casino where even Big Pharma loses more often than wins. Lupin's "fast follower" strategy might be more appropriate for its capabilities and capital.

The Strategic Options

Looking forward, Lupin has four strategic paths:

-

Double down on complex generics (Most likely) - Focus resources on respiratory, injectables, and difficult formulations - Accept lower growth but higher margins - Become a niche player rather than broad portfolio

-

Pursue transformative M&A (Possible but risky) - Acquire innovative pipeline or specialty company - Requires significant capital raise or debt - Integration risk given past mixed record

-

Gradual pivot to CDMO (Dark horse option) - Leverage manufacturing expertise for contract manufacturing - Stable revenues, lower risk - Admits defeat in branded ambitions

-

Financial engineering (If all else fails) - Break up company into focused units - Dividend recap or aggressive buybacks - Milk the cash cow while it lasts

The 2030 Vision

By 2030, Lupin will likely be: - Smaller but more profitable (₹25,000 crore revenue, 20% EBITDA margins) - Focused on 3-4 core markets (US, India, maybe Brazil) - 60% complex generics, 30% traditional generics, 10% specialty - Either acquired or acquirer (standalone unlikely)

The blockbuster GLP-1 agonists alone are forecast to reach USD 74 Bn in spending by 2028. Lupin won't participate in this bonanza—it lacks the innovation capability. Instead, it will pick up the crumbs when these products go generic in the 2030s.

So what for investors? Lupin's future is one of managed decline in traditional generics offset by selective growth in complex products. This isn't a growth story or a turnaround story—it's a value realization story. The company will generate steady cash flows, maintain its dividend, and slowly transform its portfolio. Exciting? No. Investable for income-seekers? Perhaps. The next decade will determine whether Lupin transcends its generic roots or accepts its fate as a well-run but ultimately commoditized manufacturer.

XIII. Epilogue & Lessons

After 15,000 words dissecting Lupin's journey from a Rs. 5,000 loan to an ₹87,000 crore enterprise, what have we learned? Not just about one company, but about value creation in commoditized industries, the challenges of emerging market companies going global, and the perpetual tension between ambition and capability.

Lesson 1: In Commodities, Execution Is Everything

Generic drugs are the ultimate commodity—your product is legally required to be identical to competitors'. In this environment, competitive advantage comes not from what you make but how you make it. Lupin's success in becoming the 3rd largest generic company in the U.S. by prescriptions wasn't about innovation; it was about: - Never going on backorder when competitors couldn't supply - Filing ANDAs correctly the first time while others got rejected - Maintaining FDA compliance when peers got warning letters - Managing working capital when others ran out of cash

The lesson extends beyond pharma: in commodity businesses, operational excellence isn't just important—it's the only thing that matters.

Lesson 2: Vertical Integration Is a Double-Edged Sword

We are vertically integrated, from process development of the API to the submission of dossiers for finished dosages. This gave Lupin control, quality assurance, and margin protection. During COVID, when China shut down API supplies, Lupin kept manufacturing while competitors scrambled.

But vertical integration also means: - Higher capital requirements - More regulatory touchpoints - Greater operational complexity - Reduced flexibility to switch suppliers

The lesson: vertical integration makes sense when supply security and quality control outweigh flexibility and capital efficiency. In pharma, with lives at stake and regulators watching, the tradeoff usually favors integration.

Lesson 3: Geographic Expansion Has Diminishing Returns

The company's drugs reach 70 countries, but meaningful profits come from just two: US and India. The Japan exit after spending 12 years trying to crack that market reveals a harsh truth: being subscale in multiple markets is worse than being dominant in a few.

Each new geography brings: - Unique regulatory requirements - Different competitive dynamics - Local relationship building - Separate supply chains

Unless you can achieve critical mass, you're just spreading resources thin. The lesson: expand geographically only when you have a sustainable competitive advantage, not just because the market exists.

Lesson 4: Regulatory Compliance Is a Capability, Not a Checkbox

Lupin's multiple warning letters reveal a fundamental misunderstanding many emerging market companies have about quality: it's not about passing inspections, it's about building a culture where quality is embedded in every action.

The real cost of regulatory failures isn't the remediation expense—it's: - Lost customer trust - Delayed product launches - Management distraction - Permanent valuation discount

The lesson: in regulated industries, compliance isn't a cost center—it's the foundation that everything else builds upon. Underinvest at your peril.

Lesson 5: The Innovation Trap Is Real

Every successful generic company eventually faces the same question: should we become an innovative pharmaceutical company? The allure is obvious—higher margins, patent protection, pricing power. The reality is sobering—different capabilities, massive capital requirements, high failure rates.

Lupin's measured approach to innovation—complex generics, biosimilars, 505(b)(2) products—represents a middle path. Not true innovation, but a step up from pure commodities. The lesson: know your capabilities and play within them. Better to excel at fast-following than fail at pioneering.

Lesson 6: Family Businesses Face Unique Challenges

Promoter Holding: 46.9%. The Gupta family's continued control provides stability but also constraints. Family businesses often excel at long-term thinking but struggle with: - Hard decisions about underperforming assets - Attracting non-family talent to top roles - Separating business from personal relationships - Managing succession beyond the second generation

The lesson: family ownership can be a competitive advantage in building for the long term, but governance structures must evolve as companies grow.

Lesson 7: Industry Structure Matters More Than Strategy

Lupin could execute flawlessly and still face declining prices, consolidated buyers, and new competition. The generic drug industry structure—concentrated buyers, fragmented suppliers, regulatory barriers, and patent cliffs—determines outcomes more than individual company strategy.

This doesn't mean strategy doesn't matter, but it means recognizing which games are worth playing. The lesson: before crafting strategy, understand whether industry structure allows for sustainable profits. Some races aren't worth winning.

Lesson 8: Cash Flow Is King in Cyclical Industries

Based on the long-term outlook the Board has recommended a dividend of 400%. In a declining price environment, generating and returning cash becomes more important than reported earnings. Lupin's focus on working capital management and capacity utilization drives cash generation even as margins compress.

The lesson: in cyclical or declining industries, optimize for cash flow, not accounting profits. Cash can be redeployed or returned; paper profits can evaporate.

Lesson 9: Timing Matters as Much as Execution

Lupin entered the US market in 2003, just as the generic penetration was accelerating and before Chinese competition intensified. Had they entered five years earlier, they would have lacked scale. Five years later, the opportunity would have been diminished.

Similarly, the Gavis acquisition in 2015 came just as complex generics were becoming viable but before the market was saturated. The lesson: in business, being early is the same as being wrong, but being late means missing the opportunity entirely.

Lesson 10: There Are No Permanent Moats in Pharma

Lupin's 51 First-to-File positions sound impressive, but each provides only 180 days of exclusivity. Patents expire, regulations change, new competitors emerge. What seems like a fortress today becomes a commodity tomorrow.

The lesson: in pharmaceuticals, and perhaps all industries, competitive advantages are temporary. The only sustainable advantage is the ability to continuously develop new advantages.

The Ultimate Question: Was It Worth It?

From Rs. 5,000 in 1968 to ₹87,000 crores in 2024—a 174 million times return. By any measure, Lupin is a success story. But step back and consider: - Thousands of employees dependent on its success - Millions of patients relying on affordable medicines - Investors seeking returns in a difficult industry - A family's legacy tied to its future

Lupin embodies the contradictions of modern capitalism: creating enormous value while operating in an industry with structural challenges, improving global health while maximizing profits, building a global company while remaining rooted in Indian values.

The Final Word

Lupin's story isn't finished. At 56 years old, the company is middle-aged by corporate standards. It faces the classic mid-life crisis: accept what you are or chase what you might become. The next decade will determine whether Lupin remains a successful generic company, transforms into something more, or gradually fades into irrelevance.

For entrepreneurs, Lupin offers inspiration—proof that with Rs. 5,000 and determination, you can build a global enterprise. For investors, it provides caution—even successful companies in difficult industries face perpetual challenges. For students of business, it presents a masterclass in navigating complexity, managing stakeholders, and creating value in unlikely places.

The company has delivered a poor sales growth of 8.11% over past five years. Yet it survives, employs thousands, serves millions, and generates billions. In the end, perhaps that's enough. Not every company needs to change the world. Sometimes, making essential medicines affordable and accessible is contribution enough.

As Desh Bandhu Gupta might have said, walking through those monsoon-soaked Mumbai streets decades ago: we didn't set out to build a pharmaceutical empire. We set out to solve a problem—making medicines accessible to those who needed them most. That Lupin became what it is today is less important than the fact that it continues to serve that original mission, one generic tablet at a time.

So what for investors? Lupin teaches us that value creation doesn't require breakthrough innovation or monopolistic positions. Sometimes, it's about finding an underserved need, executing relentlessly, and adapting continuously. The company may never achieve the margins of innovative pharma or the growth of biotechs, but it has created enormous value for all stakeholders over five decades. In a world obsessed with disruption, there's something to be said for the patient accumulation of incremental advantages. That's the real Lupin lesson: success doesn't always look like Silicon Valley. Sometimes it looks like a chemistry professor with Rs. 5,000 and a belief that medicines should be affordable for all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube