Elite Material: From PCB Supplier to AI Infrastructure Backbone

I. Introduction & Cold Open

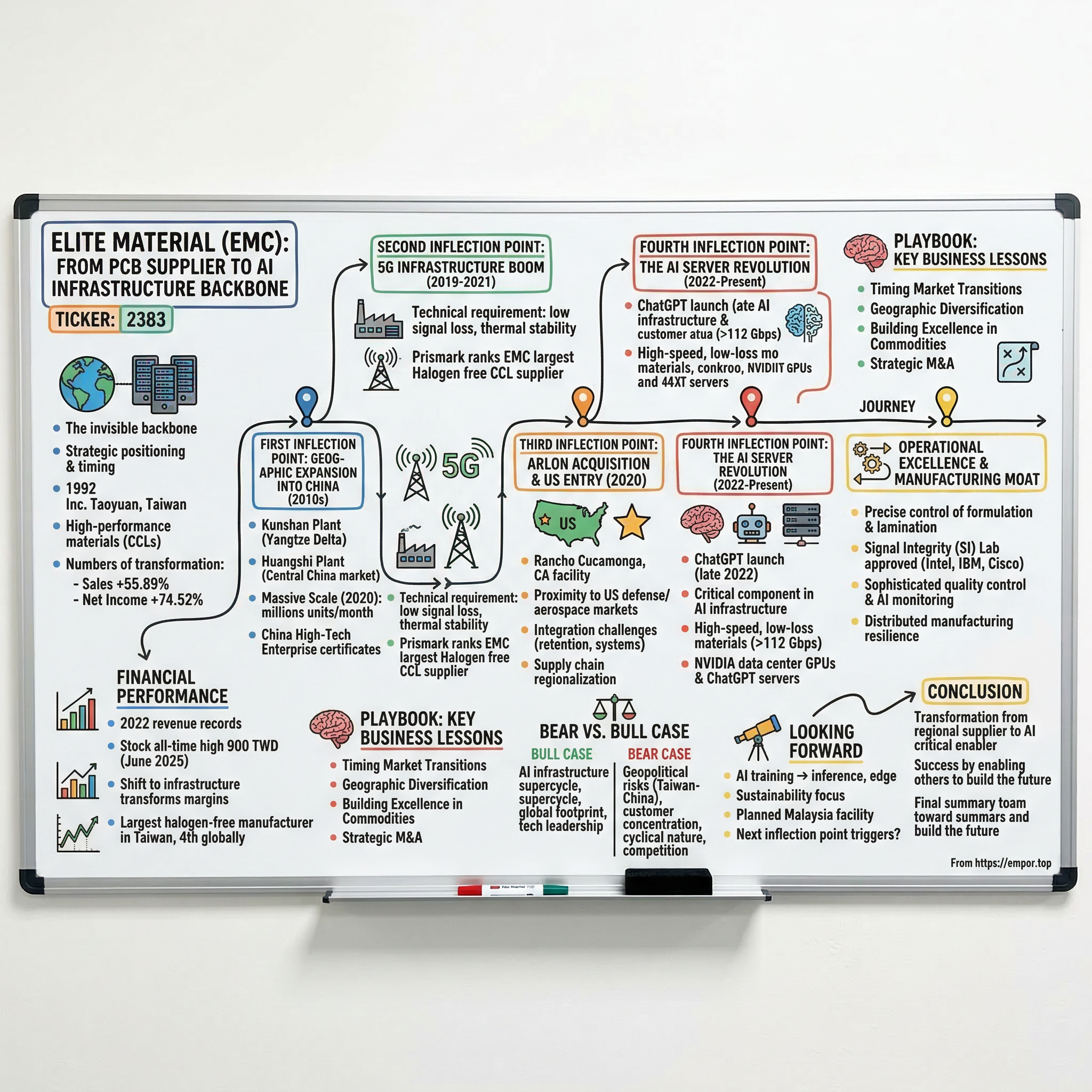

Picture this: In the heart of Taiwan's electronics manufacturing ecosystem, a company quietly producing the invisible backbone of our digital world—copper clad laminates—suddenly finds itself at the epicenter of the AI revolution. This is the story of Elite Material Company (EMC), whose journey from a regional PCB materials supplier to a critical player in global AI infrastructure reads like a masterclass in strategic positioning and timing.

The company was incorporated in 1992 and is based in Taoyuan City, Taiwan. What began as a conventional materials manufacturer has transformed into one of the most important suppliers enabling the AI boom, with their high-performance materials found in everything from NVIDIA's latest data center GPUs to the servers powering ChatGPT.

The numbers tell a compelling story of transformation. Sales growth of 55.89% and net income growth of 74.52% reflect not just a company riding a wave, but one that positioned itself perfectly to catch it. As we'll explore, EMC's journey involves four critical inflection points that fundamentally altered its trajectory: geographic expansion into China, the 5G infrastructure boom, the strategic Arlon acquisition establishing U.S. presence, and the current AI server revolution.

II. Origins & The Taiwan Electronics Context

EMC was founded in Taoyuan, Taiwan, for manufacturing conventional FR-4 copper clad thin core laminates and prepregs. This manufacturing operation received global recognition for its "exceptional" quality. The early 1990s Taiwan represented a unique moment in global electronics manufacturing—the island nation was transitioning from low-cost assembly to sophisticated component manufacturing, positioning itself as the critical link between design innovation in Silicon Valley and mass production capabilities in Asia.

The PCB industry in Taiwan during this period was highly fragmented, with hundreds of small manufacturers competing on price. EMC's founders recognized that competing purely on cost was a losing game. Instead, they focused obsessively on quality and reliability, building relationships with the emerging Taiwanese electronics giants who would later dominate global supply chains. This early decision to prioritize quality over volume would prove prescient as the industry consolidated and customers increasingly valued supply chain reliability.

III. The IPO and Early Public Years (2000s)

EMC launched its IPO on TAIEX with trading code "2383". EMC Taiwan went listed on the Taiwan Stock Exchange in 1998. The transition to public company status marked a fundamental shift in EMC's ambitions. With access to capital markets, the company could now pursue aggressive expansion strategies that would have been impossible as a private entity.

The early 2000s saw EMC begin its international expansion, recognizing that proximity to customers would become increasingly important as just-in-time manufacturing gained prominence. The company established sales offices across Asia and began laying the groundwork for what would become its most transformative strategic move: expansion into mainland China.

IV. First Inflection Point: Geographic Expansion into China (2010s)

The China expansion strategy represents EMC's first major inflection point, fundamentally altering its growth trajectory and market position. The Kunshan Plant at No.985, Luyang Jinmao Road, Zhoushi town, Kunshan City, Jiangsu Province, China became the company's first overseas manufacturing facility, strategically positioned to serve the booming electronics manufacturing cluster in the Yangtze River Delta.

The third manufacturing facility was set up in Huangshi China, with a view to supplying the Central China market. This wasn't just about adding capacity—it was about embedding EMC directly into the world's fastest-growing electronics manufacturing ecosystem. The Huangshi facility, located in Hubei Province, gave EMC access to the central China market, particularly the emerging automotive electronics sector.

By 2020, the scale of EMC's China operations had become massive. Monthly capacity in China reached 1.35 million units in Kunshan, 950,000 units in Zhongshan, and 300,000 units in Huangshi. In Taiwan, its capacity reached 650,000 units monthly. EMC's monthly capacity in Huangshi increased by another 300,000 units by the end of the third quarter with 600,000-unit monthly capacity in total in full operation by the end of the year.

The China expansion wasn't without risks. Geopolitical tensions between Taiwan and China, intellectual property concerns, and the challenge of maintaining quality standards across multiple facilities all posed significant challenges. EMC navigated these by maintaining strict technology transfer protocols, investing heavily in local talent development, and creating redundant quality control systems.

EMC China facilities received "China High-Tech Enterprise" certificates. This recognition wasn't just ceremonial—it provided tax benefits and preferential treatment that helped EMC compete with domestic Chinese manufacturers while maintaining its Taiwanese headquarters and R&D operations.

V. Second Inflection Point: 5G Infrastructure Boom (2019-2021)

The 5G revolution arrived just as EMC had completed its geographic expansion, and the company was perfectly positioned to capitalize. Applications of the company's products include, but are not limited to, communication devices, networking infrastructure products and the upcoming 5G communication products.

The technical requirements for 5G infrastructure materials were dramatically different from previous generations. Base stations required materials that could handle higher frequencies with minimal signal loss, while maintaining thermal stability in outdoor environments. EMC's decade of R&D investment in high-frequency, halogen-free materials suddenly became incredibly valuable.

Prismark ranked EMC as the world's largest Halogen free CCL supplier. This leadership position in environmentally friendly materials proved crucial as 5G infrastructure builders faced increasing scrutiny over environmental impact. EMC's halogen-free materials not only met performance requirements but also helped customers meet increasingly strict environmental regulations.

The financial impact was immediate and dramatic. Revenue growth accelerated, margins expanded as customers prioritized performance over price, and EMC's stock price began its multi-year ascent. The company went from being one of many CCL suppliers to a critical partner for 5G infrastructure deployment.

VI. Third Inflection Point: The Arlon Acquisition & US Entry (2020)

The Arlon acquisition in late 2020 represents perhaps EMC's boldest strategic move. Acquiring a U.S. manufacturer during the height of COVID-19 pandemic restrictions, amid escalating U.S.-China tensions, seemed risky. Yet this move would prove transformative.

The strategic rationale was compelling. As supply chain regionalization accelerated and "friend-shoring" became a priority for Western companies, having U.S. manufacturing capability became essential. Arlon's facility in Rancho Cucamonga, California, provided not just production capacity but also proximity to U.S. defense contractors and aerospace companies—markets that were essentially closed to Asian suppliers.

Integration challenges were significant. Arlon had been struggling financially, its equipment needed modernization, and cultural differences between Taiwanese management style and American workforce expectations required careful navigation. EMC approached these challenges methodically, retaining key technical talent while gradually implementing its quality systems and operational excellence practices.

The investment commitment was substantial, signaling EMC's long-term commitment to the U.S. market. This wasn't just about acquiring assets—it was about establishing EMC as a truly global supplier capable of serving customers regardless of geopolitical tensions.

VII. Fourth Inflection Point: The AI Server Revolution (2022-Present)

The AI revolution that began with ChatGPT's launch in late 2022 created unprecedented demand for high-performance computing infrastructure. EMC's materials suddenly became critical components in the AI arms race. The company's high-speed, low-loss materials were essential for the massive data throughput required by AI training clusters.

The technical requirements for AI server materials pushed the boundaries of what was possible. Signal integrity at speeds exceeding 112 Gbps, thermal management for densely packed GPUs, and reliability under 24/7 operation at maximum capacity all demanded materials innovation. EMC's years of investment in high-frequency materials for 5G infrastructure provided the foundation, but significant additional development was required.

Competition intensified as South Korean giants recognized the opportunity. The battle for AI server orders became a high-stakes game of technology leadership, manufacturing scale, and customer relationships. EMC leveraged its geographic diversification, with different facilities specializing in different aspects of the AI server supply chain.

VIII. Operational Excellence & Manufacturing Moat

The complexity of manufacturing high-performance CCL is often underestimated. The process requires precise control of resin formulation, glass fabric treatment, copper foil lamination, and curing conditions. Minor variations can result in catastrophic failure in end applications. EMC's three-decade refinement of these processes created a formidable competitive moat.

Developed Signal Integrity (SI) Lab approved with Intel/ Delta-L, IBM/ SPP and Cisco/ S3 measurement methodologies. This certification from industry leaders validated EMC's technical capabilities and opened doors to design partnerships with leading OEMs.

Quality control systems evolved from simple inspection to sophisticated statistical process control and predictive analytics. EMC implemented real-time monitoring across all production lines, with AI-powered systems detecting anomalies before they resulted in defects. This operational excellence enabled industry-leading yields and reliability metrics.

The 2023 plant fire in northern Taiwan tested EMC's operational resilience. The company's response—quickly shifting production to other facilities while accelerating recovery efforts—demonstrated the value of its distributed manufacturing footprint. Customer relationships strengthened as EMC maintained supply continuity despite the disruption.

IX. Financial Performance & Market Position

In 2022, the company set revenue records. EMC pointed out that its product combination has improved. The growth in infrastructure network product market share and delivery has resulted in a slight increase in sales and lessened the impact of the poor performance of consumer electronics.

The shift from consumer electronics to infrastructure transformed EMC's financial profile. Infrastructure customers valued reliability and performance over price, enabling margin expansion. Multi-year supply agreements provided revenue visibility and reduced cyclical volatility.

Stock performance reflected this transformation. Trading at just 4 TWD per share during the 2008 financial crisis, EMC shares reached an all-time high of 900 TWD in June 2025, delivering extraordinary returns for long-term shareholders. The company's market capitalization grew from a small-cap afterthought to a significant component of Taiwan's technology sector.

EMC is currently the largest manufacturer of halogen-free base material in Taiwan and the 4th largest manufacturer of halogen-free material in the world. This market position, combined with technological leadership in high-speed materials, positioned EMC as an essential supplier for next-generation electronics infrastructure.

X. Playbook: Key Business Lessons

EMC's journey offers several critical lessons for companies navigating technology transitions:

Timing Market Transitions: EMC consistently positioned itself ahead of major technology waves—5G infrastructure before the buildout began, AI server materials before the ChatGPT moment. This wasn't luck but systematic analysis of technology roadmaps and early engagement with leading customers.

Geographic Diversification as Competitive Advantage: While competitors focused on single-country manufacturing, EMC's distributed footprint across Taiwan, China, and the United States provided resilience and customer flexibility. This proved invaluable as geopolitical tensions reshaped global supply chains.

Building Excellence in "Commodities": CCL might seem like a commodity product, but EMC proved that operational excellence and technological innovation could create differentiation even in seemingly mature industries. The company's focus on quality and reliability built customer loyalty that transcended price competition.

Strategic M&A in New Geographies: The Arlon acquisition demonstrated how thoughtful M&A could accelerate geographic expansion. Rather than building from scratch, EMC acquired existing capabilities and relationships, then applied its operational excellence to transform performance.

Riding vs. Creating Waves: EMC succeeded by recognizing and riding technology waves rather than trying to create them. The company didn't invent 5G or AI, but it ensured its materials were essential for others' innovations.

XI. Bear vs. Bull Case

The Bull Case: The AI infrastructure supercycle is just beginning. As AI models grow exponentially in size and complexity, demand for high-performance computing infrastructure will continue expanding. EMC's established position with leading customers, proven ability to meet demanding specifications, and globally distributed manufacturing create significant competitive advantages.

The U.S. manufacturing presence via Arlon provides unique access to defense and aerospace markets while satisfying "made in America" requirements. As supply chain regionalization continues, this capability becomes increasingly valuable.

Technological leadership in high-speed, high-frequency materials creates barriers to entry. Years of R&D investment and accumulated manufacturing know-how cannot be easily replicated by new entrants.

The Bear Case: Geopolitical risks remain significant. Despite geographic diversification, EMC still has substantial exposure to China-Taiwan tensions. Any disruption to cross-strait relations could severely impact operations.

Customer concentration poses risks. While EMC serves multiple industries, a small number of large customers account for significant revenue. Loss of any major customer could materially impact financial performance.

The electronics industry's cyclical nature hasn't disappeared. While infrastructure spending provides some stability, eventual overcapacity in AI infrastructure could trigger a painful downturn.

Competition from Korean manufacturers continues intensifying. Companies like Doosan have deeper pockets and may be willing to sacrifice margins to gain market share.

Technology transitions create risks. If new interconnect technologies bypass traditional PCBs, demand for CCL could decline rapidly.

XII. Looking Forward: The Next Chapter

As we look toward EMC's future, several themes emerge:

The AI infrastructure buildout likely has years of growth ahead. As AI moves from training to inference, from cloud to edge, material requirements will evolve. EMC's ability to adapt its products to these changing needs will determine its continued success.

Sustainability considerations are becoming paramount. EMC's leadership in halogen-free materials positions it well, but increasing focus on circular economy principles may require fundamental changes to product design and manufacturing processes.

Capacity expansion decisions loom large. With demand exceeding supply for high-performance materials, EMC must balance aggressive expansion against the risk of overcapacity. The company's planned Malaysia facility represents a careful bet on continued growth while maintaining geographic diversification.

What could trigger the next major inflection point? Several possibilities exist: breakthrough in quantum computing requiring entirely new material systems, mainstream adoption of photonic interconnects, or geopolitical realignment fundamentally reshaping global supply chains.

Conclusion

Elite Material's transformation from a regional PCB materials supplier to a critical enabler of the AI revolution represents one of the most successful pivots in recent technology history. The company's journey illustrates how operational excellence, strategic foresight, and careful execution can create extraordinary value even in seemingly mature industries.

The four major inflection points—China expansion, 5G boom, Arlon acquisition, and AI revolution—each required different capabilities and created new opportunities. EMC's ability to navigate these transitions while maintaining operational excellence and customer trust proved the difference between modest success and exceptional performance.

As the digital infrastructure backbone continues evolving, EMC's role becomes ever more critical. The invisible materials in every server, switch, and base station may not capture headlines, but they enable the digital revolution reshaping our world. For investors and industry observers, EMC's story offers valuable lessons about timing, positioning, and the enduring value of manufacturing excellence.

The next chapter remains unwritten, but EMC's track record suggests the company will continue adapting and thriving as technology evolves. In an industry where today's innovation becomes tomorrow's commodity, EMC has proven that consistent execution and strategic positioning can create lasting competitive advantages. The journey from Taoyuan to the heart of the AI revolution demonstrates that in technology, as in life, success often comes not from inventing the future, but from enabling others to build it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube