OLECTRA: India's Electric Bus Revolution

I. Introduction & Episode Roadmap

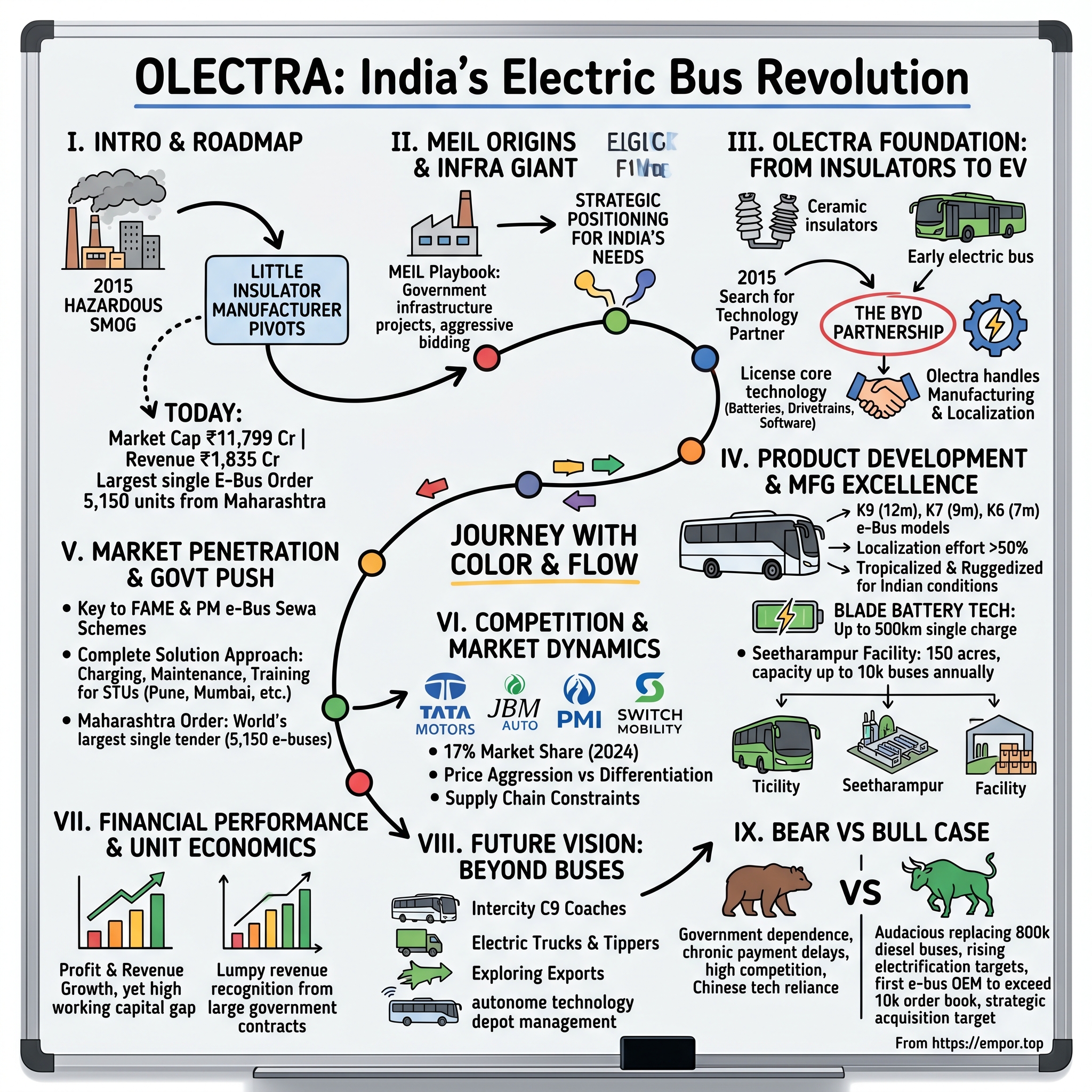

Picture this: It's 2015, and the skies above Delhi are so thick with smog that schools are shutting down, flights are being diverted, and the city's air quality index has crossed 900—categorized simply as "hazardous." The Supreme Court calls it a "living hell," and India's urban pollution crisis has become a global headline. In the midst of this environmental catastrophe, a little-known insulator manufacturer from Hyderabad is quietly preparing to pivot its entire business toward what seems like an impossible dream: building India's first electric buses.

Fast forward to today, and Olectra Greentech commands a market capitalization of ₹11,799 crore with revenues touching ₹1,835 crore. The company that once made composite polymer insulators for power lines now rolls out sleek, silent electric buses from its state-of-the-art facility near Hyderabad. It's secured the world's largest single electric bus order—5,150 units from Maharashtra alone—and has become the poster child for India's electric mobility ambitions.

But here's what makes this story truly fascinating: Olectra isn't backed by any of India's automotive giants. It's not a Tata or a Mahindra spinoff. Instead, it's the unlikely offspring of MEIL, a ₹35,000 crore infrastructure conglomerate better known for building irrigation projects and power plants than cutting-edge vehicles. And its technology? Licensed from BYD, the Chinese electric vehicle giant, in a partnership that has survived geopolitical tensions, border conflicts, and investment restrictions that would have killed most cross-border collaborations.

This is a story about how government policy can create entire industries overnight, how emerging market companies navigate technology transfer in an increasingly fractured world, and why sometimes the most unlikely players end up winning the biggest prizes. It's about the messy, complicated, often contradictory path of industrial transformation in the world's most populous nation. The themes we'll explore cut across classic business school case studies: technology transfer between nations, the role of industrial policy in creating new markets, conglomerate advantages in emerging economies, and how companies navigate the treacherous waters of geopolitical tensions while maintaining crucial partnerships. As we'll see, the company's net order book stands at over 10,000 as of March 31, 2025, making it a critical player in India's ambitious electric mobility transformation.

II. MEIL Origins & The Infrastructure Giant

The year is 1989. India is still two years away from economic liberalization, the Soviet Union hasn't yet collapsed, and in a small workshop in Hyderabad, a farmer's son named P.P. Reddy is welding together municipal water pipes with borrowed equipment and boundless ambition. He calls his venture Megha Engineering Enterprises—"megha" meaning cloud in Sanskrit, perhaps an unconscious nod to the lofty heights he would eventually reach.

Reddy had no engineering degree, no family connections in business, no venture capital. What he had was an acute understanding of India's infrastructure deficit and the political savvy to navigate the byzantine world of government contracts. His nephew, P.V. Krishna Reddy, joined the fledgling operation in 1991, just as India was opening its economy to the world. Together, they would transform a fabrication unit into what would become Megha Engineering & Infrastructures Limited (MEIL)—a $5 billion infrastructure colossus with over 25 group companies and projects valued at approximately $30 billion.

The MEIL playbook was deceptively simple: bid aggressively for government infrastructure projects, execute with military precision, and reinvest profits into increasingly complex ventures. From municipal water pipes, they graduated to irrigation projects. From irrigation, they moved to power plants. Each step up the complexity ladder brought new capabilities, new relationships, and critically, new insights into where India's infrastructure needs were heading.

By the 2000s, MEIL had become what Indians call a "master of all trades"—building everything from the world's largest lift irrigation project (Kaleshwaram in Telangana) to metro rail systems, from oil refineries to smart cities. The company's structure resembled less a traditional corporation and more a confederation of specialized units, each focused on a different aspect of India's infrastructure buildout. This diversification wasn't random; it was strategic positioning for whatever mega-projects the government would prioritize next.

The infrastructure context in India during this period cannot be overstated. While China was pouring concrete at unprecedented rates, India's infrastructure spending lagged desperately behind its economic growth. Roads, power, water, transportation—everything needed upgrading simultaneously. For companies like MEIL, this represented not a challenge but an generational opportunity. The government needed private partners who could execute complex projects at scale, and MEIL had proven it could deliver.

But why would an infrastructure giant suddenly pivot to electric vehicles? The answer lies in understanding how Indian conglomerates think differently from their Western counterparts. In mature markets, conglomerate diversification is often viewed with suspicion—a sign of management empire-building or lack of focus. In emerging markets like India, it's a survival strategy. Government priorities shift, new sectors receive sudden policy support, and the companies that thrive are those that can rapidly redeploy capital and capabilities toward whatever the nation needs built next.

For MEIL's leadership, the signs were becoming clear by the early 2010s. India's urban air pollution was reaching crisis levels. The country was importing over $100 billion worth of oil annually. Climate change commitments were looming. Most importantly, the government was beginning to signal that electric mobility would be a national priority. When you've built your empire on anticipating and serving government infrastructure needs, you don't ignore such signals.

The vehicle for this electric ambition wouldn't be MEIL directly—that would be too much of a stretch for a company known for concrete and steel. Instead, they would use a smaller subsidiary that most investors had never heard of, one that manufactured an obscure but essential component of India's power grid. The transformation of that subsidiary would become one of the most unlikely pivots in Indian corporate history.

III. OLECTRA's Foundation: From Insulators to EVs

In 2000, while the world was recovering from the dot-com crash and India's IT boom was just beginning, a small company called Goldstone Infratech was quietly incorporated in Hyderabad. Its mission was unglamorous but essential: manufacturing composite polymer insulators—those ceramic-looking devices you see on power lines that prevent electricity from jumping to the ground. It was precisely the kind of boring, industrial business that never makes headlines but forms the backbone of modern infrastructure.

The company—which would later become Olectra Greentech Limited—spent its first decade perfecting the art of insulator manufacturing. These weren't simple ceramic discs; they were sophisticated composite polymers designed to withstand extreme weather, pollution, and electrical stress. The technology was cutting-edge for India at the time, replacing traditional porcelain insulators with lighter, stronger, more reliable alternatives. By 2010, they had become one of India's leading manufacturers, supplying to power utilities across the country.

Then came the pivot moment—though "moment" undersells what was actually a gradual realization spread across several years. By 2015, India's urban air quality had become an international embarrassment. The World Health Organization listed Delhi as the world's most polluted city. School children were developing respiratory problems at alarming rates. The Supreme Court was issuing increasingly harsh directives about vehicular emissions. Something had to give.

Within MEIL's corporate planning rooms, executives were connecting dots that others hadn't yet seen. India's government was about to embark on one of the world's largest transportation electrification programs. Someone would need to build these electric buses—lots of them, quickly, and at price points that cash-strapped state transport corporations could afford. The opportunity was massive, but the challenges were equally daunting.

Olectra had no automotive experience whatsoever. They had never built a vehicle, never managed a supply chain for moving parts, never dealt with the complex safety regulations that govern passenger transportation. What they did have was MEIL's backing, deep relationships with government entities, and critically, an understanding that they didn't need to invent the technology—they needed to find it.

The search for a technology partner began in earnest in 2015. The requirements were specific: proven electric bus technology, willingness to transfer knowledge to India, ability to localize production, and most importantly, a partner who understood that this wasn't just about selling buses—it was about building an industry. Several global players were approached. Most were skeptical. India's electric vehicle market was essentially non-existent. There was no charging infrastructure, no trained mechanics, no ecosystem of component suppliers.

But one company saw what others didn't. BYD—Build Your Dreams—the Chinese battery maker turned electric vehicle giant, was looking for an entry point into India's vast market. They had the technology, having already deployed thousands of electric buses in Chinese cities. What they lacked was local manufacturing capability and the political relationships necessary to navigate India's complex regulatory environment. In Olectra, they found the perfect partner.

The announcement of the partnership in 2015 sent ripples through India's automotive industry. Here was a composite insulator manufacturer claiming it would build electric buses with Chinese technology. The skepticism was palpable. Established players like Tata Motors and Ashok Leyland, with decades of bus-building experience, watched with a mixture of amusement and concern. Surely this experiment would fail?

What the skeptics underestimated was the power of focused execution backed by patient capital. MEIL poured resources into Olectra, funding new facilities, hiring automotive engineers, and most critically, giving the company time to learn. The first buses, rolled out in 2016, were essentially BYD buses assembled in India. But with each batch, the localization increased, the quality improved, and the costs came down.

The early challenges were immense. Indian road conditions were nothing like the smooth highways of Shenzhen. The buses needed to handle potholes, flooding, extreme heat, and overloading—because in India, a 40-seat bus routinely carries 60 passengers. The battery management systems, designed for China's temperate climate, had to be reconfigured for India's extreme temperatures. Every component had to be tropicalized, ruggedized, and cost-optimized.

But perhaps the biggest challenge was market education. State transport corporations, used to diesel buses they could repair with basic tools, were deeply suspicious of electric technology. Olectra had to become not just a manufacturer but an evangelist, conducting pilot programs, training drivers and mechanics, and gradually building confidence in electric propulsion. The transformation from insulator manufacturer to EV pioneer was complete, setting the stage for one of the most important international partnerships in India's automotive history.

IV. The BYD Partnership: Technology Transfer & Scale

The meeting took place in a nondescript conference room in Shenzhen in late 2014. On one side sat Wang Chuanfu, the enigmatic founder of BYD who had transformed a battery manufacturer into the world's largest electric vehicle company. On the other, representatives from Olectra and MEIL, armed with spreadsheets showing India's bus market potential and a vision for electric transformation. What transpired in that room would reshape India's public transportation landscape.

BYD in 2014 was at an inflection point. They had conquered the Chinese electric bus market, with over 10,000 units on the road. But international expansion was proving challenging. Europe and America viewed Chinese technology with suspicion. Emerging markets lacked the infrastructure and purchasing power. India represented a unique opportunity—massive scale, government support for electrification, but also significant barriers to entry. Setting up a wholly-owned subsidiary would face regulatory hurdles and local resistance. They needed a partner.

The structure of the partnership was carefully crafted to navigate both countries' sensitivities. This wasn't a joint venture in the traditional sense—that would have required regulatory approvals that might never come. Instead, it was structured as a technology licensing arrangement with deep collaboration. BYD would provide the core technology—battery systems, electric drivetrains, control software. Olectra would handle manufacturing, localization, and crucially, the relationship with Indian government customers.

The technology transfer began with BYD's K9 model, a 12-meter electric bus that had become the workhorse of Chinese cities. But bringing the K9 to India wasn't simply a matter of shipping blueprints. Indian engineers spent months at BYD's facilities, learning not just how to assemble the buses but understanding the underlying engineering principles. BYD's engineers, in turn, came to India to understand local conditions and requirements.

The company is India's largest pure electric bus manufacturer, offering e-bus models like 7m, 9m, and 12m, including inter-city coach variants. It is broadening its product portfolio in the e-mobility sector by introducing electric trucks and tippers. The K9 became the template, but what emerged from Olectra's facilities was increasingly indigenized. The K7 (9-meter) and K6 (7-meter) variants were developed specifically for Indian conditions—narrower for congested city streets, with enhanced ground clearance for rough roads.

Then came 2020 and the Galwan Valley clash—a deadly border confrontation between Indian and Chinese forces that sent bilateral relations into a deep freeze. Suddenly, having a Chinese partner became a massive liability. The Indian government began scrutinizing all Chinese investments. Olectra Greentech unveiled its latest blade battery technology, promising longer ranges and faster charging times. Public sentiment turned sharply anti-Chinese, with calls to boycott Chinese products trending on social media.

The partnership faced its biggest test when MEIL and BYD jointly proposed a $1 billion electric four-wheeler manufacturing facility in India. The proposal promised to bring cutting-edge EV technology to India's passenger vehicle market. The government's response was swift and unequivocal: rejected on security grounds. The message was clear—Chinese investments in critical sectors would face intense scrutiny.

Lesser partnerships would have crumbled. But Olectra and BYD had built something more resilient than a typical vendor relationship. They had created a framework for technology transfer that could survive geopolitical turbulence. Olectra Greentech announced that it is ramping up its manufacturing capacity to meet a large order book of over 10,200 electric buses. For FY 2024-25, Olectra is targeting the delivery of 1,200 buses, with a conservative target of 2,500 buses for FY 2025-26.

The key was progressive localization. By 2021, Olectra had achieved over 50% local content in its buses. Indian suppliers were providing chassis, bodies, seats, and increasingly, even electronic components. The most sensitive component—the battery—remained imported, but even here, Olectra was working on alternatives. The goal wasn't to eliminate BYD from the equation but to reduce dependence to a level that wouldn't trigger security concerns.

The partnership's success can be measured not just in buses sold but in technology absorbed. Indian engineers who had never worked on electric vehicles were now designing battery management systems. Local suppliers who had only made diesel engine components were now manufacturing electric motor parts. An entire ecosystem was emerging, catalyzed by the technology transfer from BYD.

The renewal of the collaboration agreement until December 31, 2030, despite the geopolitical tensions, speaks to the mutual dependence that has developed. BYD needs Olectra to access the Indian market; Olectra needs BYD's continuous technology upgrades to stay competitive. It's a partnership born of pragmatism, sustained by mutual benefit, and tested by geopolitical fire. The fact that it has survived and thrived offers lessons for how technology transfer can work even in an increasingly fragmented global economy.

V. Product Development & Manufacturing Excellence

The factory floor in Seetharampur, just outside Hyderabad, spreads across 150 acres—roughly the size of 115 football fields. The company has placed orders for robots from leading manufacturers like Fanuc and Kuka, planning to commence commercial production using robotic assembly by the end of this financial year. In one corner, sheets of aluminum are being pressed into bus body panels. In another, workers in blue overalls are installing leather seats with the precision of Swiss watchmakers. The smell of welding mingles with the antiseptic cleanliness of the battery assembly area. This is where India's electric bus revolution takes physical form.

The evolution of Olectra's manufacturing capability is a masterclass in industrial climbing. The first buses in 2016 were essentially "screwdriver assembly"—SKD (Semi-Knocked Down) kits from BYD that were put together in India. The value addition was minimal, maybe 20%. Critics dismissed it as "Made in India" in name only. But that was just the beginning.

It operates K9 buses (12-meter), K7 (nine-meter) and K6 (seven-meter). All these buses have customizable seating capacity and are designed for long-range operations. Each model represents a step up in localization and sophistication. The K6, designed specifically for narrow Indian streets, couldn't simply be a shrunken K9. It needed a completely different turning radius, a reconfigured battery placement for better weight distribution, and windows designed for India's intense summer heat.

The real breakthrough came with battery technology. Early models used lithium iron phosphate batteries that provided a range of about 250 kilometers per charge—adequate for city operations but limiting for intercity routes. The introduction of BYD's Blade Battery technology changed everything. These new batteries, with their unique cell-to-pack design, offered 30% more energy density while actually being safer than conventional lithium-ion batteries. An Olectra bus could now travel up to 500 kilometers on a single charge, opening up entirely new use cases.

But batteries were just one piece of the puzzle. Indian buses face unique challenges that would destroy vehicles designed for developed markets. During monsoons, buses wade through knee-deep water. In summer, interior temperatures can reach 50°C. Dust infiltrates everything. Overloading is not exceptional; it's standard operating procedure. Every component had to be re-engineered for these conditions.

The air conditioning system provides a perfect example. Chinese buses used roof-mounted AC units designed for moderate climates. In India, these units would fail within months, overwhelmed by the heat and dust. Olectra developed a split system with enhanced cooling capacity and military-grade dust filters. The penalty was slightly reduced passenger capacity, but the gain in reliability was worth it.

As of 9M FY25, the company has delivered about 2,448 electric buses and 51 electric tippers, covering 30+ Cr km across the length and breadth of the country. Each kilometer driven provided data that fed back into the design process. Suspension systems were reinforced after buses on rural routes reported excessive wear. Battery cooling systems were upgraded after units in Rajasthan showed thermal stress. Software updates were pushed over-the-air to optimize energy consumption based on route patterns.

The manufacturing process itself evolved from labor-intensive assembly to increasingly automated production. The new Seetharampur facility, with an investment of over ₹700 crore, represents a quantum leap in capability. When fully operational, it will have the capacity to produce 10,000 buses annually—more than India's entire electric bus market in 2023. The scale seems ambitious, even hubristic. But Olectra's management sees something others don't: the inflection point is coming.

The plant is designed for flexibility as much as scale. Production lines can switch between different bus models with minimal downtime. The same facility that produces a 7-meter city bus in the morning can roll out a 12-meter intercity coach by afternoon. This flexibility is crucial in a market where orders come in large, irregular chunks from state transport corporations with varying requirements.

Quality control happens at multiple stages, but the final test is the most dramatic. Each bus undergoes a "monsoon simulation" where it's bombarded with high-pressure water jets from every angle. Then comes the "pothole test" on a specially designed track that simulates twenty years of Indian road conditions in twenty minutes. Buses that survive this torture test are deemed ready for Indian roads.

The push toward manufacturing excellence isn't just about building better buses; it's about changing perceptions. Every Olectra bus that completes a million kilometers without major breakdown chips away at the skepticism surrounding electric vehicles. Every successful deployment makes the next sale easier. In the infrastructure business, reputation is everything, and Olectra is methodically building a reputation for buses that simply don't quit.

VI. Market Penetration & Government Push

The announcement came at 3 PM on a humid Mumbai afternoon in August 2023: Olectra had won the world's largest single electric bus tender—5,150 buses for Maharashtra State Road Transport Corporation (MSRTC). The order value: ₹10,000 crore. The timeline: aggressive. The implications: transformational. In one stroke, Olectra's order book had doubled, and India's electric bus adoption had shifted from pilot phase to massive rollout.

But the road to this moment was paved with years of patient relationship building and policy navigation. The story really begins in 2015 with FAME—Faster Adoption and Manufacturing of Hybrid and Electric Vehicles—India's first serious attempt at electric vehicle promotion. FAME-I, with its modest budget of ₹895 crore, was more gesture than game-changer. But it signaled government intent, and for companies like Olectra, that signal was enough to justify massive investments.

It serves state and central government bodies across cities like Pune, Mumbai, Hyderabad, and others, including MSRTC, BEST, PMPML, and TSRTC. Each of these relationships was cultivated over years, starting with pilot deployments of just 5-10 buses. Pune was first, taking a chance on Olectra's buses for its Bus Rapid Transit system. The buses performed well, but more importantly, Olectra provided something diesel bus manufacturers never had: real-time data on operations, energy consumption, and maintenance needs.

The relationship with state transport corporations (STUs) is unique in the Indian context. These aren't normal commercial customers. They're government entities, perpetually cash-strapped, politically sensitive, and deeply conservative in their procurement. Convincing an STU to buy electric buses wasn't just about price and performance; it was about handholding through the entire transition.

Olectra developed what they called the "complete solution approach." They didn't just sell buses; they helped STUs set up charging infrastructure, trained drivers and maintenance staff, and even assisted in route planning to maximize battery efficiency. When BEST (Mumbai's bus service) complained that drivers were anxious about battery range, Olectra installed real-time monitoring systems and conducted week-long training programs to build confidence.

Then came FAME-II in 2019, with a budget of ₹10,000 crore—a tenfold increase that suddenly made electric buses financially viable for STUs. The scheme offered a capital subsidy of up to ₹50 lakh per bus, bringing the effective cost below that of diesel buses when total cost of ownership was considered. The policy design was clever: subsidies were tied to operational performance, ensuring that manufacturers couldn't just dump substandard vehicles.

The PM e-Bus Sewa scheme, launched in 2023, took this even further. The government would support 10,000 electric buses across 169 cities, with a focus on cities lacking organized public transport. The scheme's structure favored companies that could deliver at scale, quickly, with proven technology. Olectra, with its established manufacturing capacity and operational track record, was perfectly positioned.

Olectra Greentech Ltd reports a 70% revenue increase and a 156% rise in profit after tax, driven by robust electric bus deliveries and a growing order book. But growth at this pace brings its own challenges. State transport corporations, while enthusiastic about electric buses, often lack the technical expertise to manage large-scale electric fleet operations. Payment cycles are notoriously long—sometimes stretching to six months or more. The company's receivables are high, currently at about five months, although efforts are being made to reduce this.

The competitive dynamics in government tenders are brutal. Price is paramount, but it's not everything. Olectra's strategy has been to position itself as the "safe choice"—the company with the most buses on the road, the longest operational track record, and the backing of a major infrastructure conglomerate. When you're a bureaucrat making a ₹1,000 crore purchasing decision, "nobody got fired for buying Olectra" becomes a powerful argument.

The Maharashtra order exemplifies this dynamic. Olectra wasn't the lowest bidder—JBM Auto was. But Olectra's technical scores, delivery track record, and financial strength gave it the edge. The Maharashtra government reinstated an order for 5,150 electric buses, with revised delivery timelines. The order faced challenges, with reports of potential cancellations causing stock price volatility, but the company has not received any official communication regarding order cancellations and has clarified this with stock exchanges while remaining optimistic about order commitments.

The government's target is audacious: replace approximately 800,000 diesel buses with electric ones by 2030. At current production rates, this seems impossible. But policy support is accelerating, technology is improving, and critically, the economics are beginning to work even without subsidies. The market penetration phase is giving way to market expansion, and Olectra has positioned itself at the center of this transformation.

VII. Competition & Market Dynamics

In 2024, something remarkable happened in India's electric bus market: it became a real market. For years, the sector had been a government-supported experiment with a handful of players. But with 3,616 electric buses registered in a single year and order books swelling into the tens of thousands, the gold rush was officially on. Olectra Greentech faces challenges in the competitive tendering process, as seen in the Chennai bus tender where they were not successful.

The competitive landscape reads like a who's who of Indian automotive and engineering companies. Tata Motors, India's largest commercial vehicle manufacturer, leveraged its decades of bus-building experience and vast service network. JBM Auto, a relatively unknown player until recently, emerged as a fierce competitor with aggressive pricing and rapid capacity expansion. PMI Electro Mobility and Switch Mobility (Ashok Leyland's EV arm) rounded out the major players, each with their own strategy for capturing market share.

In this intensifying battlefield, Olectra held a 17% market share in 2024—respectable, but not dominant. The market dynamics were shifting from "can you build an electric bus?" to "can you build 1,000 electric buses, deliver them in six months, and price them at ₹80 lakh?" The game was becoming about scale, speed, and razor-thin margins.

Tata Motors represented the most formidable competition. Their strategy was classic incumbent playbook: leverage existing dealer networks, offer electric variants of popular diesel models, and bundle maintenance contracts that STUs were already familiar with. Their Starbus EV, while technologically less sophisticated than Olectra's offerings, had the advantage of familiarity. STU mechanics who had worked on Tata buses for decades found the transition easier.

JBM Auto took a different approach—pure price aggression. Backed by the deep pockets of the Neel Metal Products group, they were willing to bid at losses to gain market share. Their ECO-LIFE buses, manufactured in partnership with European company Solaris, were positioned as "European technology at Indian prices." They won several high-profile tenders, including a significant portion of Delhi's electric bus orders, by undercutting competitors by 10-15%.

But the most interesting competitive dynamic wasn't between manufacturers—it was the race for differentiation in an increasingly commoditized market. Government tenders specified technical requirements in minute detail: battery capacity, range, passenger capacity, even the color of seats. This left little room for product differentiation. Everyone was essentially building the same bus to the same specifications.

Olectra's response was to compete on dimensions beyond the product itself. OGL achieved a significant milestone by surpassing 10,000 units in its e-bus order book, solidifying its position as the first e-bus OEM in India to achieve this feat. This wasn't just about bragging rights; it was about signaling to customers that Olectra had the scale and financial strength to deliver on large orders.

The technology differentiation that did exist centered on batteries and drivetrains. Olectra's BYD-sourced Blade Battery technology offered advantages in energy density and safety. Tata's partnership with Cummins brought different strengths in power electronics. JBM's European partnerships provided advantages in lightweight construction. But for most STU procurement officers, these differences were academic. What mattered was price, delivery timeline, and payment terms.

The competitive dynamics were further complicated by the entrance of new players. Infraprime Logistics, a company nobody had heard of two years ago, suddenly won a 1,400-bus order from Delhi. Chinese manufacturers like Foton and Yutong were circling, looking for Indian partners to circumvent investment restrictions. Even traditional diesel bus body builders were trying to enter the market by partnering with electric drivetrain suppliers.

The entire industry is facing supply constraints, particularly with chassis and battery components. This supply chain bottleneck created an interesting dynamic: having manufacturing capacity was worthless without secured component supplies. Olectra's partnership with BYD provided some advantage here, with preferential access to batteries, but even they faced challenges in scaling up production.

The market structure was evolving toward a stable oligopoly. The capital requirements for setting up manufacturing, the complexity of technology integration, and the importance of government relationships created high barriers to entry. But within this oligopoly, competition was fierce. Every tender was a battle, with bidders sometimes pricing below cost just to keep factories running and workers employed.

Looking ahead, the basis of competition is likely to shift. As the market matures and subsidies potentially phase out, factors like total cost of ownership, uptime reliability, and service quality will become more important than initial purchase price. Companies that can offer innovative financing models, superior after-sales service, or breakthrough technology improvements will gain an edge. For now, though, it's a knife fight for every order, and Olectra is fighting with the biggest blade it can find.

VIII. Financial Performance & Unit Economics

The numbers tell a story of explosive growth coupled with the grinding realities of a capital-intensive, government-dependent business. Revenue of ₹1,835 Cr and Profit of ₹141 Cr might seem modest for a company with a market capitalization exceeding ₹11,000 crore, but understanding Olectra's financials requires looking beyond the headline numbers to the underlying unit economics and cash flow dynamics.

Quarterly Revenue of ₹523.67 crores, up 70% from ₹307.16 crores in Q2 last year. EBITDA of ₹85.69 crores, up 90% from ₹45.06 crores in Q2 last year. Profit After Tax (PAT) of ₹47.65 crores, up 156% from ₹18.58 crores in Q2 last year. These growth rates would make any Silicon Valley startup jealous, but they come with a catch: the working capital requirements are crushing.

Consider the unit economics of a single electric bus. The typical selling price to an STU ranges from ₹80 lakh to ₹1.2 crore, depending on specifications. The bill of materials—batteries, chassis, motors, controllers—accounts for roughly 70% of this price. Manufacturing overhead adds another 10-12%. Sales and administrative expenses consume 5-7%. That leaves EBITDA margins in the 15-18% range—healthy for a manufacturing business, but not spectacular.

But here's where it gets complicated. The payment terms with STUs are typically 30% advance, 60% on delivery, and 10% after satisfactory operation for six months. In practice, that "delivery" payment often gets delayed by 2-3 months as buses go through inspection and registration. The final 10% can take a year or more to collect. Meanwhile, Olectra must pay its suppliers—especially for imported batteries—within 60-90 days.

This working capital gap means that rapid growth actually consumes cash rather than generating it. Every bus delivered represents a cash outflow that won't be fully recovered for 6-12 months. The company is working on localization efforts to reduce costs and improve margins, which are currently at 15.6% for the quarter. Localization helps not just with margins but also with working capital, as local suppliers often offer better payment terms than international ones.

The capital intensity extends beyond working capital to fixed assets. The new Seetharampur facility represents a ₹700 crore investment for a capacity of 10,000 buses annually. At full utilization, that's ₹7 lakh of capex per unit of annual capacity—a significant upfront investment that needs to be amortized over thousands of buses to make economic sense.

For the quarter ended 30 June 2025, the company reported revenue from operations of ₹347.22 crore, a notable 10.6% increase from ₹313.94 crore in the same quarter last year. Net profit for the quarter stood at ₹26.03 crore, which is 8.5% higher than the ₹24.25 crore recorded in Q1 FY25. The quarterly volatility in revenues reflects the lumpy nature of bus deliveries—a few weeks' delay in completing a large order can shift hundreds of crores of revenue from one quarter to the next.

The stock market's valuation of Olectra reflects both the growth potential and the execution risks. Trading at over 80 times trailing earnings, the market is clearly not valuing Olectra based on current profitability. Instead, investors are betting on the convergence of several factors: sustained government support for electric buses, Olectra's ability to maintain market share as the sector grows, and eventual margin expansion through scale and localization.

Company has a low return on equity of 10.6% over last 3 years. This seemingly disappointing ROE actually reflects the capital-intensive nature of the business and the heavy investments made in anticipation of future growth. As capacity utilization improves and working capital cycles normalize, ROE should improve significantly.

The financial engineering required to manage this business is sophisticated. Olectra uses a combination of term loans for capex, working capital facilities for operations, and increasingly, structured financing arrangements where banks provide loans directly to STUs for bus purchases. These tripartite agreements reduce Olectra's working capital burden but add complexity to revenue recognition and collection processes.

Looking ahead, the path to improved financial performance is clear but challenging. First, achieve better capacity utilization—running the factory at 70-80% capacity versus the current 30-40% would dramatically improve fixed cost absorption. Second, reduce working capital cycles through better payment terms or financial innovations. Third, improve margins through localization and scale economies. Fourth, diversify the revenue base beyond STUs to reduce customer concentration risk.

The bull case for Olectra's financials rests on the assumption that electric bus adoption in India is still in its infancy. If even 20% of India's bus fleet goes electric by 2030—a conservative estimate given government targets—that represents a market opportunity of over 160,000 buses. At Olectra's current market share and ASPs, that's a revenue opportunity exceeding ₹15,000 crore. The bear case worries about subsidy withdrawal, competition intensifying to the point where margins evaporate, and execution risks in scaling up production 5x from current levels.

IX. Future Vision: Beyond Buses

The conference room at Olectra's headquarters features a wall-sized screen displaying a map of India dotted with moving icons—each representing one of their buses in operation, updating location and battery status in real-time. But CEO P. Rajesh Reddy isn't looking at the buses. He's pointing to a corner of the screen showing a different icon: a truck symbol marked "Prototype Testing - Pune-Mumbai Highway." This is Olectra's next act.

The company has deployed its C9 buses as Puri Bus Service. The 12-meter bus is a 49-seater and is designed for long distance and intercity operations. The intercity segment represents a natural evolution from urban buses. The technology requirements are actually more demanding—longer range, higher speeds, enhanced passenger comfort for multi-hour journeys. But the market opportunity is enormous. India's intercity bus market is three times larger than the urban segment, and currently, almost entirely diesel-powered.

The Olectra-BYD C9 coach is their answer to this opportunity. With seating for 49 passengers and batteries storing 360 kWh of energy, it can cover 500 kilometers on a single charge—enough for most intercity routes in India. The economics are compelling: while the upfront cost is higher than diesel coaches, the operating cost per kilometer is less than half. For route operators running buses 400 kilometers daily, the payback period is under four years.

But buses, even intercity coaches, are just the beginning. The company's R&D is working on various products, including electric trucks, with order materialization expected in this financial year. The commercial vehicle electrification opportunity in India extends far beyond passenger transportation. Trucks, especially for last-mile delivery and urban goods movement, are ripe for electrification.

The truck market presents different challenges and opportunities. Unlike buses, which are largely purchased by government entities, trucks are bought by private operators who care obsessively about total cost of ownership. They don't care about environmental benefits unless it impacts their bottom line. But with diesel prices rising and cities increasingly restricting diesel vehicle entry during peak hours, electric trucks are becoming economically attractive.

Olectra's approach to the truck market leverages their existing capabilities while acknowledging new requirements. The battery technology and power electronics transfer directly from buses. The manufacturing processes are similar. But the use cases are vastly different. A garbage truck needs massive torque for frequent stops and starts. A delivery van prioritizes cargo space over battery placement. A mining tipper requires ruggedization that makes even Indian buses look delicate.

The technology roadmap extends beyond vehicle types to fundamental improvements in electric propulsion. Battery technology is evolving rapidly, with solid-state batteries promising double the energy density of current lithium-ion cells. Olectra is working with BYD and Indian research institutions to stay at the forefront of these developments. The goal is to be ready to integrate new battery technologies as soon as they become commercially viable.

Charging infrastructure represents both a challenge and an opportunity. Olectra has so far relied on customers to set up charging facilities, providing technical support but not infrastructure investment. That's beginning to change. The company is exploring models where they provide charging-as-a-service, installing and operating charging stations for fleet operators. This would create a recurring revenue stream and deeper customer relationships.

The export opportunity is tantalizing but complicated. Southeast Asian and African countries face similar urban transportation challenges as India—growing cities, air pollution, limited financial resources. Olectra's buses, designed for Indian conditions, are well-suited for these markets. But exporting requires different certifications, service infrastructure, and financing arrangements. The company is taking baby steps, participating in international tenders and exploring partnership opportunities.

Perhaps the most ambitious vision is for autonomous electric buses. While fully autonomous vehicles remain years away in India's chaotic traffic conditions, limited automation—like depot management systems where buses can park and charge themselves—is achievable in the near term. Olectra is collaborating with Indian technology companies to develop these capabilities, potentially creating a differentiator in an increasingly commoditized market.

The diversification strategy isn't without risks. Each new product category requires investment in R&D, manufacturing capabilities, and market development. The company must balance the growth opportunities against the risk of losing focus on their core bus business. The insulator business is growing slowly compared to the electric bus segment, with no current plans to demerge it. This legacy business, while small, provides stable cash flows that support the electric vehicle investments.

Looking at the broader vision, Olectra is positioning itself not just as a bus manufacturer but as an electric commercial vehicle company. The addressable market expands from thousands of crores to tens of thousands of crores. The customer base diversifies from government to private enterprises. The technology moat deepens as the company moves from assembly to innovation. It's an ambitious vision, requiring flawless execution, continued government support, and a bit of luck. But for a company that successfully pivoted from making insulators to building India's electric bus industry, perhaps nothing is impossible.

X. Playbook: Lessons for Emerging Market Innovation

The Olectra story, stripped of its specifics, reveals a playbook for how emerging market companies can build new industries through a combination of government alignment, strategic partnerships, and pragmatic execution. These lessons extend far beyond electric buses or even India—they're applicable wherever companies in developing economies are trying to leapfrog technological generations.

Lesson 1: Ride the Policy Wave, Don't Fight It

Olectra's entire strategy was predicated on anticipating and aligning with government policy. They didn't try to create demand for electric buses through superior technology or marketing; they positioned themselves to capture demand that policy would create. This requires a different mindset from Silicon Valley-style disruption. Instead of asking "how can we change consumer behavior?", the question becomes "what infrastructure will the government prioritize next?"

The company's deep relationships with government entities, inherited from parent MEIL, provided early signals about policy direction. When bureaucrats started discussing electric mobility in 2014-15, before any formal policy announcement, Olectra was already searching for technology partners. By the time FAME-II was announced, they had manufacturing capacity ready. This anticipatory positioning is crucial in markets where government procurement drives adoption.

Lesson 2: Technology Transfer vs. Indigenous Development

The decision to partner with BYD rather than develop electric bus technology indigenously was pragmatic, not glamorous. Indigenous development would have taken a decade and hundreds of crores with uncertain outcomes. Technology transfer got them to market in two years with proven solutions. The key was structuring the partnership to enable progressive localization and knowledge absorption rather than perpetual dependence.

This approach challenges the notion that emerging market companies must choose between being technology creators or forever remaining assemblers. Olectra shows a third path: start with assembly, learn through doing, progressively localize, and eventually innovate on top of the transferred technology. It's not as intellectually satisfying as pure innovation, but it's far more likely to succeed commercially.

Lesson 3: The Conglomerate Advantage

In developed markets, conglomerate structures are often seen as inefficient, destroying value through complexity and lack of focus. But in emerging markets, conglomerate backing provides crucial advantages: patient capital, government relationships, and the ability to absorb early losses. MEIL's support allowed Olectra to invest heavily before revenues materialized, weather the uncertainty of policy implementation, and credibly bid for large government contracts.

The conglomerate structure also provides risk diversification. If electric buses had failed to take off, MEIL had dozens of other businesses to fall back on. This portfolio approach to innovation—place multiple bets, support the winners, quietly shut down the losers—is particularly suited to emerging markets where policy shifts can make or break entire sectors overnight.

Lesson 4: Stakeholder Complexity Management

Olectra had to manage an unusually complex set of stakeholders: Chinese technology partners viewed with suspicion, government customers with Byzantine procurement processes, investors expecting Silicon Valley growth rates, and competitors eager to paint them as foreign pawns. Managing these contradictions required exceptional stakeholder communication and alignment skills.

The company's approach was to give each stakeholder what they valued most. BYD got market access and revenues. Government customers got reliable buses and local job creation. Investors got growth and future potential. Competitors were kept at bay through rapid capacity expansion and aggressive bidding. It's a delicate balance, constantly at risk of tipping over, but when it works, it creates a defensible position.

Lesson 5: Building Manufacturing Capability

The progression from SKD assembly to sophisticated manufacturing didn't happen overnight. It required systematic capability building: hiring experienced engineers from the automotive industry, sending teams to China for training, investing in testing facilities, and most importantly, learning from every failure. Each bus that broke down became a learning opportunity. Each customer complaint drove product improvement.

This iterative approach to capability building is different from the "moon shot" approach often celebrated in innovation literature. There were no breakthrough moments, no eureka discoveries. Just gradual, systematic improvement in hundreds of small processes that collectively transformed a novice assembler into a credible manufacturer.

Lesson 6: Capital Allocation in Policy-Dependent Sectors

Investing in sectors dependent on government policy requires a different approach to capital allocation. Traditional NPV models break down when the key variable—policy support—is binary and unpredictable. Olectra's approach was to stage investments based on policy milestones. Small pilot facility when FAME-I was announced. Larger investment when FAME-II confirmed sustained support. Major capacity expansion only after securing large orders.

This milestone-based investment approach manages risk while maintaining optionality. If policy support wavers, losses are contained. If support strengthens, capacity can be rapidly scaled. It's a real-options approach to capital allocation, particularly suited to policy-dependent sectors in emerging markets.

The Meta-Lesson

The overarching lesson from Olectra's journey is that emerging market innovation doesn't follow Silicon Valley rules. It's not about disrupting incumbents with superior technology or creating entirely new markets. It's about recognizing where government priorities and technological possibilities intersect, then executing with discipline and pragmatism to capture the opportunity.

This might seem less revolutionary than creating the next unicorn, but the impact can be equally transformational. Olectra's electric buses are reducing air pollution in Indian cities, providing livelihood to thousands of workers, and building technological capabilities that will benefit India for decades. It's innovation suited to the realities and needs of emerging markets—practical, scalable, and aligned with national development priorities.

XI. Bear vs. Bull Case Analysis

The Bull Case: India's Electric Bus Champion

The optimistic view of Olectra starts with a simple observation: India's electric bus penetration is less than 2% today, while China's exceeds 80% in new sales. This gap represents not a failure but an opportunity—perhaps the largest addressable market for electric buses anywhere in the world over the next decade.

The numbers are staggering. India operates approximately 800,000 buses, and the government has committed to full electrification by 2030. Even if only half this target is achieved, it represents 400,000 electric buses—a market opportunity exceeding ₹3 trillion. Olectra's position as the first e-bus OEM in India to achieve a 10,000-unit order book gives it pole position in this race.

The competitive advantages appear durable. The BYD partnership, despite geopolitical tensions, provides continuous technology upgrades that would take competitors years to develop independently. The manufacturing scale—10,000 units annual capacity when fully operational—creates cost advantages through bulk procurement and operational leverage. The track record of over 2,400 buses delivered builds customer confidence in a market where reliability is paramount.

Government support shows no signs of weakening. The PM e-Bus Sewa scheme is just getting started. State governments are announcing their own electric vehicle policies with additional incentives. City-level initiatives like Delhi's complete electrification of public transport by 2025 create guaranteed demand. Climate commitments made at COP summits necessitate transport electrification. The policy tailwind could blow for a decade or more.

The financial trajectory in the bull case is compelling. As volumes scale from hundreds to thousands of buses annually, fixed costs get absorbed, working capital cycles normalize, and margins expand. The current 15-16% EBITDA margins could expand to 20%+ through localization and operational efficiency. ROE, currently suppressed by heavy investment, could exceed 25% once capacity utilization improves.

Diversification provides additional upside. Electric trucks, intercity coaches, and eventually export markets could double or triple the addressable market. Recurring revenues from charging infrastructure and service contracts could transform the business model from one-time sales to lifetime customer value. Technology improvements—solid-state batteries, autonomous features—could command premium pricing.

The strategic value might exceed the financial returns. As India's largest pure-play electric bus manufacturer, Olectra could become an acquisition target for global OEMs looking to enter the Indian market. Or it could become the platform for India's electric vehicle ambitions, similar to how BYD became central to China's EV strategy. The option value embedded in this strategic position is hard to quantify but potentially enormous.

The Bear Case: Structural Challenges and Execution Risks

The pessimistic view starts with an uncomfortable truth: Olectra is essentially a contract manufacturer dependent on government orders and Chinese technology. Remove either pillar, and the business model collapses.

The dependence on government orders is near-total, with STUs accounting for over 90% of revenues. These customers are financially weak—most STUs lose money even with heavily subsidized operations. Payment delays are chronic and getting worse as state finances strain under post-COVID debt burdens. A single policy change—reduction in FAME subsidies, shift to hydrogen buses, or simple budget constraints—could evaporate demand overnight.

The company is dependent on foreign technology for certain components, which could pose risks given geopolitical tensions. The BYD partnership, while providing technology, also creates vulnerability. If India-China relations deteriorate further, the partnership could become untenable. BYD could decide to enter India independently once regulations ease, competing directly with Olectra. The technology transfer might plateau, leaving Olectra with aging technology as global competitors advance.

Competition is intensifying rapidly. Tata Motors has the brand, service network, and balance sheet to dominate once it decides to. New entrants backed by global OEMs are inevitable as the market grows. Chinese manufacturers, despite current restrictions, will find ways to access the Indian market. Price competition has already compressed margins, and it will only get worse as capacity exceeds demand.

The execution challenges in scaling from 1,000 to 10,000 buses annually are enormous. The company faces industry-wide supply chain challenges, particularly with components related to chassis and batteries. Quality issues at scale could destroy the carefully built reputation. Working capital requirements could spiral out of control, necessitating dilutive equity raises or expensive debt.

Technology commoditization is accelerating. Electric bus technology isn't rocket science—it's batteries, motors, and controllers assembled into a bus body. As component suppliers mature, anyone can assemble an electric bus. The moats that exist today—technology access, manufacturing capability, government relationships—could erode rapidly. In five years, electric buses might be as commoditized as diesel buses are today.

The financial returns might never materialize. The current valuation at 80x earnings assumes perfect execution, sustained government support, and limited competition—a trifecta that rarely occurs. More likely, competition and subsidy reduction will compress margins just as volumes scale. The capital intensity means that even with growth, returns on invested capital might remain pedestrian.

The bear case ultimately sees Olectra as a transitional player—important in establishing India's electric bus industry but eventually marginalized as established automotive giants and global OEMs take over. It's a bridge between the diesel past and electric future, valuable for a time but not enduringly so.

The Verdict

The truth, as always, likely lies between these extremes. Olectra has built something real and valuable—manufacturing capability, customer relationships, and early-mover advantage in a massive market. But the structural challenges are equally real—government dependence, technology reliance, and intensifying competition.

The investment case depends on time horizon and risk tolerance. For those believing in India's electric mobility transformation and willing to weather policy volatility and execution challenges, Olectra offers exposure to a generational shift in transportation. For those seeking predictable returns and sustainable competitive advantages, the risks might outweigh the rewards.

What's certain is that Olectra's next five years will look nothing like its last five. The company will either emerge as India's electric vehicle champion or fade as global giants dominate. There's little middle ground in platform shifts of this magnitude.

XII. Epilogue: What This Means for India's EV Future

As our story draws to a close, it's worth stepping back from Olectra's specific journey to consider what it represents for India's broader electric vehicle ambitions and industrial development strategy.

Olectra is, in many ways, a test case for industrial policy in the 21st century. Unlike the heavy-handed license raj of India's socialist past, the electric bus sector shows a more sophisticated approach: set ambitious targets, provide time-bound incentives, and let private companies compete for implementation. It's industrial policy via procurement rather than protection, using government's purchasing power to create markets that wouldn't otherwise exist.

The results so far are encouraging. India has gone from zero electric buses in 2015 to thousands on the road today. An entire ecosystem—from battery suppliers to charging infrastructure providers—has emerged. Technical capabilities that didn't exist in India five years ago are now routine. It's proof that with the right policy framework, emerging markets can rapidly build new industries.

But Olectra's story also reveals the limitations and dependencies inherent in this model. The industry exists because of subsidies and would likely collapse without them. The technology remains largely imported, with true indigenous innovation still years away. The financial sustainability depends on continued government support that could evaporate with changing political priorities or fiscal constraints.

The question for India is whether electric buses are the beginning of a broader electric vehicle revolution or a one-off success in a narrow segment. Can the capabilities built in commercial vehicles transfer to passenger cars, where India has struggled to gain traction? Can the supply chain developed for buses support two-wheelers and three-wheelers, where electrification makes even more economic sense? Can India move from assembly to innovation, developing electric vehicle technologies that compete globally?

The lessons for other emerging markets are particularly relevant. Countries from Indonesia to Nigeria face similar challenges: growing transportation needs, urban pollution, and dependence on imported oil. The Olectra model—government-led demand creation, international technology partnerships, and progressive localization—could be replicated. But it requires patient capital, consistent policy, and companies willing to invest ahead of demand.

The broader implications for industrial strategy are profound. In an era of deglobalization and friend-shoring, the ability to rapidly build domestic capabilities in strategic sectors becomes crucial. Electric vehicles are just one example; the same playbook could apply to semiconductors, renewable energy, or biotechnology. The key is identifying sectors where government procurement can catalyze private investment and where international partnerships can accelerate capability building.

For investors, Olectra represents a new category of opportunity: policy-driven platform shifts in emerging markets. These aren't traditional value investments based on current cash flows, nor are they venture investments in unproven technologies. They're bets on government commitment to sectoral transformation and companies' ability to execute at scale. The risk-reward profile is unique—binary outcomes with potentially massive returns.

The environmental implications cannot be ignored. Every electric bus deployed removes approximately 100 tons of CO2 emissions annually. If India achieves even partial electrification of its bus fleet, the impact on air quality and carbon emissions would be transformational. Olectra and its competitors aren't just building businesses; they're engineering public health improvements that will benefit millions.

Looking ahead, the next five years will be crucial. Either electric buses become normalized—as routine as diesel buses are today—or the experiment fails, leaving stranded assets and broken promises. The technology will improve, costs will decline, and infrastructure will expand. But the critical variable remains policy commitment. Will successive governments maintain support through electoral cycles and fiscal pressures?

Olectra's journey from insulator manufacturer to electric bus pioneer encapsulates both the promise and peril of industrial transformation in emerging markets. It shows that with vision, partnership, and execution, companies can build entirely new industries. But it also reveals the fragility of such transformations, dependent on government support, international partnerships, and favorable economics that could change overnight.

As India stands at the cusp of potentially massive electric vehicle adoption, Olectra stands as both beneficiary and symbol of this transformation. Its success or failure won't just determine shareholder returns; it will influence whether emerging markets can successfully navigate the energy transition while meeting their development needs. In that sense, every Olectra bus quietly humming through India's streets carries more than passengers—it carries the hopes of a nation trying to build a cleaner, more sustainable future while lifting millions out of poverty.

The story isn't over. In fact, for India's electric vehicle industry and for Olectra, it's just beginning. The next chapters will be written not in corporate boardrooms or government policy documents, but on the streets of Indian cities, where electric buses either become the new normal or remain an ambitious experiment that couldn't quite scale. Time, and perhaps a bit of that Indian jugaad (innovative problem-solving), will tell.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube