Geely: The Global Automotive Alchemist

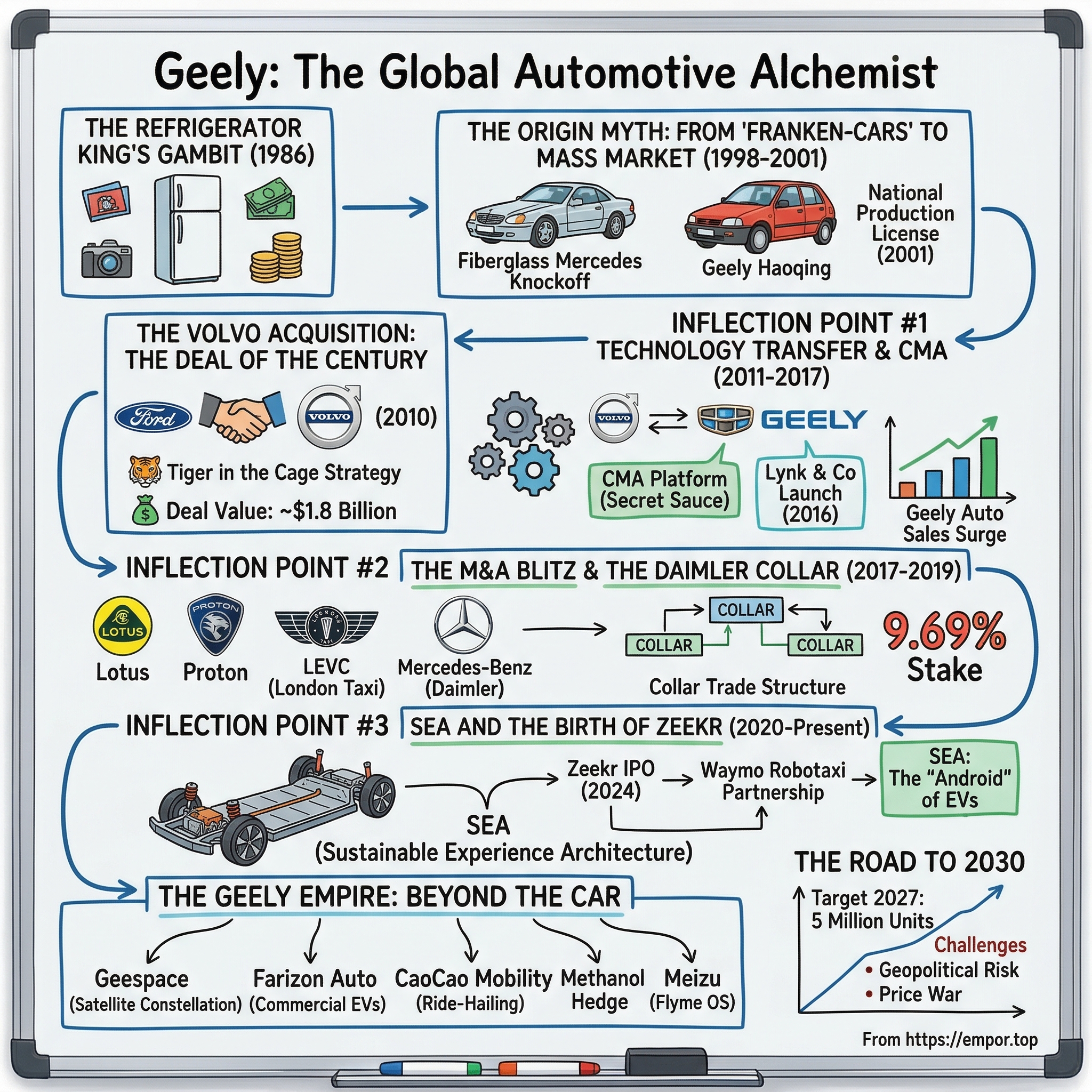

I. The Refrigerator King's Gambit

Picture a twenty-three-year-old farmer's son in Taizhou, Zhejiang Province, in 1986. He has a hundred yuan from his father — about sixteen dollars — a Seagull camera he bought with it, and the hustle of a man who has already figured out that tourists at scenic spots will pay for photographs. By the time he is twenty-five, that camera has generated his first million renminbi. By the time he is thirty, he is making refrigerators. By forty-seven, he owns Volvo. By fifty-five, he is the single largest shareholder in Mercedes-Benz.

Li Shufu's story is, on its surface, a rags-to-riches tale of the Chinese economic miracle. But that framing misses what makes it genuinely extraordinary. This is not a story about cheap labor or government subsidies. This is a story about a man who studied a Mercedes-Benz by literally taking one apart in a shed, who was laughed out of the Detroit Auto Show, and who then executed one of the most audacious merger-and-acquisition strategies in the history of the global automobile industry — all while running a company that most Western analysts had never heard of.

The mystery at the heart of Geely is this: how did a company that started making fiberglass-bodied knockoff sedans in a converted prison van factory become the most sophisticated acquirer of automotive assets on the planet? How did it buy Volvo from Ford for seventy-two cents on the dollar, revive it into a genuine BMW competitor, and then use that playbook to snap up Lotus, Proton, a stake in Mercedes, and the iconic London black cab — all while building an electric vehicle platform that Waymo now uses for its robotaxis?

The answer involves three interlocking themes.

First, what Li Shufu calls the "Tiger in the Cage" strategy — the conviction that Western automotive brands are extraordinary assets trapped inside dysfunctional corporate structures, and that a patient Chinese buyer can unlock their value simply by setting them free.

Second, the SEA platform — Geely's multi-billion-dollar bet on becoming the "Android of electric vehicles," licensing a single skateboard chassis to everyone from Baidu to a Polish national car project.

And third, the quiet transformation of Geely from a low-cost manufacturer into something the world has never quite seen before: a Chinese conglomerate that operates luxury European brands, launches its own satellite constellation, builds robotaxis for American tech companies, and runs one of the largest ride-hailing platforms in Asia — all under the umbrella of a founder who still owns roughly forty percent of the holding group and makes decisions with the speed of a startup founder.

Geely Automobile Holdings, listed on the Hong Kong Stock Exchange as 0175.HK, delivered over three million vehicles in 2025 and generated RMB 345 billion in revenue. Its parent, the Zhejiang Geely Holding Group, targets five million units by 2027. At a market capitalization of roughly HKD 200 billion, the question for investors is whether this is a company that deserves to trade at ten times earnings — or whether the market is fundamentally mispricing the most ambitious automotive empire assembled since Ferdinand Piëch built the Volkswagen Group.

To answer that question, we need to go back to a shed in Zhejiang where a young man was pulling apart a refrigerator compressor and dreaming about cars.

II. The Origin Myth: Photography, Fridges, and "Franken-Cars" (1963–2001)

Every great business story has a moment where you can trace the founder's DNA back to a single defining trait. For Jeff Bezos, it was an obsession with long-term thinking. For Steve Jobs, it was an obsession with design. For Li Shufu, the defining trait is an almost preternatural ability to see what a thing could become rather than what it currently is — and the stubbornness to pursue that vision through a dozen failures, regulatory roadblocks, and the universal ridicule of people who thought they knew better.

Li Shufu was born on June 25, 1963, into a farming family in Taizhou, a coastal city in Zhejiang Province that sits in the heart of China's most entrepreneurial region. Zhejiang is to China what Lombardy is to Italy or what the Ruhr Valley once was to Germany — a place where making things is in the cultural DNA. Wenzhou, the city that produced China's first private airlines and first private banks, is just down the coast. Taizhou itself was already known for producing small-parts manufacturers and scrappy traders long before the economic reforms of the 1980s.

After graduating from high school in 1982, Li received a hundred yuan from his father. He bought a Seagull-brand camera — a popular Chinese knockoff of a Soviet design — and set up shop photographing tourists at local scenic spots. It was pure hustle: find the customers, take the photo, develop the film, deliver the print. Within two years, he had saved enough to open a camera shop. By the mid-1980s, he had earned his first million renminbi, a sum that in that era and that province made him a genuine local celebrity — a "Bai Wan," or ten-thousand-fold rich man.

But Li was not interested in photography. He was interested in manufacturing. In 1984, he began producing refrigerator parts, and by 1986 he had formally founded the Zhejiang Geely Holding Group in Ningbo. He and his brother Li Xubing launched the "Arctic" brand of refrigerators, and for a few years it looked like Geely's destiny was to be a white-goods company. Then, in 1989, the central government began requiring production licenses for refrigerator manufacturers. Arctic was not selected. Just like that, the refrigerator business was over.

This is the first example of a pattern that would define Li Shufu's career: getting shut out by regulators and finding a way around.

Li pivoted to aluminum-magnesium decoration boards — the kind of material used in building facades — and ran that business profitably through the early 1990s. But his real fascination was with vehicles. In 1993, he visited a state-owned motorcycle factory and immediately saw an opportunity: motorcycles were simpler than cars, the margins were decent, and the licensing requirements were less punishing.

By 1994, he had purchased a small state-owned motorcycle company and inaugurated a new plant in Taizhou with capacity for fifty thousand units per year. The Geely Group Zhejiang Motorcycle Company was formally founded on April 8, 1995, producing under the Jiming brand. These were cheap mopeds and scooters in the 50-to-250cc range, but they sold. By 2002, the factory could produce three hundred thousand units annually, and Geely was exporting to Southeast Asia and South America.

The motorcycle business was profitable, but Li's ambition was always cars. The problem was that in 1990s China, private companies were not allowed to manufacture automobiles. The industry was reserved for state-owned enterprises. When Li petitioned government officials for permission, one Communist Party official famously dismissed him.

Li's response has become one of the most quoted lines in Chinese business history: "A car is really just two sofas with four wheels." To another official, he pleaded: "I would not regret even if we fail, but could you please give us an opportunity first?"

The officials said no. They said it politely, they said it firmly, and they said it repeatedly. China's automobile industry was considered a strategic sector — too important to be left to the unpredictable ambitions of private entrepreneurs. The state-owned enterprises — FAW, SAIC, Dongfeng, Changan — had the government's backing, the production licenses, and the joint-venture partnerships with Toyota, Volkswagen, and General Motors that gave them access to foreign technology. Private companies were, in the government's view, best suited to making screws, toys, and small appliances. Not cars.

So Li found another way.

He learned that the Deyang No. 95 Factory, a prison-run vehicle manufacturer in Sichuan Province, had gone out of business but still held a valid vehicle manufacturing license. The factory, which had once produced five-ton trucks based on the Dongfeng EQ140 platform, was essentially a shell. Li invested twenty-four million renminbi, took seventy percent of the shares, and created the Sichuan Geely Boyin Automotive Company. When the elderly prison director passed away, Li bought the remaining thirty percent. In March 1997, the factory equipment was relocated to Linhai in Zhejiang, and Geely was officially — if only technically — in the car business.

What happened next has become the stuff of Chinese automotive legend. Li purchased a Mercedes-Benz and had it completely disassembled in a workshop. He also obtained a Hongqi CA7200, a Chinese sedan that was itself based on the FAW-Volkswagen Audi 100 platform. His team stripped the Hongqi down to its front and rear subframes, then built a new body out of fiberglass and steel panels styled to look like a Mercedes-Benz W210 E-Class. The interior components — seats, dashboard — came from the Hongqi. Audi wheel covers were fitted.

The result was christened the "Geely Number 01."

Li reportedly slept only two hours a night for weeks to complete the project. When the car was driven through downtown Taizhou, it generated enormous excitement. He advertised it in the Taizhou Daily News and received numerous inquiries about pricing. But the Geely Number 01 was a prototype — a franken-car that proved Li could physically assemble something that looked like a luxury sedan, even if the technology to actually engineer one was years beyond his reach.

In a 2009 CCTV interview, Li called it "a very foolish effort." By then, the original prototype had rusted and rotted in a corner of the old factory; when the building was demolished, the car was destroyed with it.

The real breakthrough came when Li admitted what he could not yet do and focused on what he could. He pivoted from imitating Mercedes to building the cheapest possible car for the Chinese mass market. On August 8, 1998, the first Geely Haoqing rolled off the assembly line in Linhai. It was modeled on the Daihatsu Charade — produced in China as the Tianjin Xiali — and powered by a Daihatsu three-cylinder engine. Only two hundred cars were produced that year, and Geely still did not have a national production license. The cars were sold locally, almost underground.

It was a scrappy, unglamorous beginning. The Haoqing was not a good car by any standard — fit and finish were poor, the engine was underpowered, and early quality issues were rampant. But it was cheap. Priced at under forty thousand renminbi — roughly five thousand dollars — it cost less than half of what a Tianjin Xiali charged and a fraction of what the joint-venture brands like Volkswagen and Toyota offered. In a country where the average urban household income was barely above ten thousand dollars, Geely had found a market: buyers who could not afford anything else but desperately wanted four wheels and a roof.

Everything changed on November 9, 2001. China had just acceded to the World Trade Organization, and the government was loosening restrictions on private enterprise. Geely finally received its national production license, becoming China's first private automaker authorized to sell cars across the country.

The timing was exquisite: China was about to enter the greatest automotive boom in human history. Between 2001 and 2010, the Chinese car market would grow from two million units per year to eighteen million — and Geely, with its ultra-cheap sedans priced at a fraction of what state-owned rivals charged, was perfectly positioned to ride the wave.

But Li Shufu had no intention of remaining a maker of cheap cars. The Geely Number 01 — that fiberglass Mercedes built in a shed — was not a fluke. It was a statement of intent. Li had always wanted to build something worthy of the name, and the motorcycle profits and mass-market car sales were just the means to get there.

By 2006, Geely was selling nearly two hundred thousand cars per year and had listed on the Hong Kong Stock Exchange in 2005, giving it access to international capital markets. It had also entered motorsport, sending a team to the 2006 Detroit Auto Show — where its display was widely mocked by Western media as amateurish — and competed in the Rally of China. These were branding exercises aimed at gaining international visibility, even if the visibility was not always flattering. Li understood that being laughed at was better than being ignored. A punchline today could become a competitor tomorrow.

The question was how a company with virtually no engineering capability, no brand equity outside China, and no experience in international markets could possibly make the leap from Daihatsu knockoffs to genuine global competition.

III. Inflection Point #1: The Volvo Acquisition — The Deal of the Century (2007–2010)

There are certain moments in business history where a single transaction changes everything — not just for the companies involved, but for an entire industry's understanding of what is possible. The leveraged buyout of RJR Nabisco in 1988 defined an era of financial engineering. Google's acquisition of Android in 2005 reshaped the mobile phone industry. Geely's purchase of Volvo in 2010 belongs in this category, not because of its size — the price was modest by automotive standards — but because of what it proved: that a Chinese company with no global brand recognition, no advanced engineering capability, and no experience managing a Western workforce could acquire a storied European brand and make it better.

In January 2007, Li Shufu walked into Ford Motor Company's headquarters in Dearborn, Michigan, and asked to buy Volvo. He was given a polite meeting with Ford's chief financial officer, Don Leclair, and treated as a curiosity — a courtesy call from an obscure Chinese motorcycle-and-cheap-car manufacturer that no one at Ford had ever heard of. Later that year, Geely sent an official letter to Ford expressing its desire to acquire the Swedish brand. Ford never replied.

To understand why Li was laughed off, you need to understand the context. Ford was in crisis, but it was still Ford. Alan Mulally had arrived as CEO in September 2006 and inherited a company that had just posted a twelve-and-a-half-billion-dollar loss. Mulally's "Way Forward" plan called for selling off the luxury brands that Ford had assembled in the late 1990s under the Premier Automotive Group: Aston Martin, Jaguar, Land Rover, and Volvo.

Ford had paid six billion four hundred fifty million dollars for Volvo Cars in January 1999, and Forbes estimated the company had spent seventeen billion dollars building its PAG acquisitions in total. The strategy had been a disaster — the brands operated as independent fiefdoms with minimal synergies, and the Jaguar X-Type became an industry punchline for slapping a Jaguar badge on a Ford Mondeo platform.

Mulally began selling. Aston Martin went to a consortium led by David Richards in 2007. Jaguar and Land Rover went to Tata Motors in March 2008 for roughly one and a half billion dollars. Volvo was last. And when the credit markets froze in late 2008 and General Motors and Chrysler lurched toward bankruptcy, Mulally found himself with very few potential buyers. Ford had priced Volvo at six billion. No one was paying that.

Li Shufu, who had spent a year preparing a detailed acquisition proposal, showed up at the Detroit Auto Show in early 2008 and presented it to Ford. He was rejected again. But this time, something had changed in the power dynamic. Ford was desperate. And John Thornton — a Ford board director and former Goldman Sachs president who had been living and working in China — met Li in Beijing in December 2008, just days after Ford publicly announced its openness to selling Volvo.

Thornton recognized what Ford's management had missed: Li Shufu was not a tourist. He was a serious buyer with access to Chinese capital at a moment when Western credit markets were frozen solid.

In January 2009, Li led a delegation to meet Ford's top management and received an official invitation letter to submit a binding bid. Ford's internal code name for the negotiations was "Delta." Over the next twelve months, a team of bankers and lawyers on both sides worked through a transaction of staggering complexity. The deal document ran to ten thousand pages, because untangling Volvo from Ford required separating shared technology platforms, engine intellectual property, supply contracts, and cross-licensing agreements that had been woven together over a decade.

Li's advisory team was formidable. Rothschild led the financial advisory, with Meyrick Cox — an Eton-educated engineer turned senior banker — as the point person. Jennifer Yu, Rothschild's head of investment banking for China, helped navigate the political dimensions of the deal. Hans-Olov Olsson, a former Volvo CEO, joined as a strategic advisor. Freshfields Bruckhaus Deringer handled the legal work.

The financing structure was as creative as the negotiation. The total consideration was approximately one billion eight hundred million dollars — less than a third of what Ford had paid in 1999. Of that amount, Geely put up roughly two hundred million in equity. Chinese state-linked entities including the China Development Bank and the city of Daqing provided loans and guarantees. Goldman Sachs co-invested.

The structure meant Geely acquired an automaker with four times its revenue using less equity than a midsize American home cost in San Francisco. From Ford's perspective, the deal was painful but rational. Ford recovered roughly twenty-eight cents on every dollar it had paid for Volvo — a massive loss, but it generated cash to fund Mulally's turnaround of the core Ford brand, which would prove to be one of the great corporate rescues of the twenty-first century.

On March 28, 2010, the stock purchase agreement was signed. On August 2, 2010, the deal closed with a handshake between Li Shufu and Ford's Lewis Booth.

Li's promise to the Swedish workforce became famous. In meetings with Volvo's unions and employees in Gothenburg — a deeply skeptical audience that feared Chinese owners would strip the brand and ship the jobs east — he used a vivid metaphor: "Volvo is a tiger. It belongs in the forest, but Ford has put it in a cage. I want to let the tiger go back to the forest."

The implication was profound and counterintuitive. Most acquirers promise "synergies" — corporate code for layoffs and consolidation. Li promised the opposite: autonomy. Volvo would remain headquartered in Gothenburg. It would retain its Swedish management team, its engineering staff, and its design identity. Geely's role would be to provide capital, access to the Chinese market, and supply-chain support. The Swedish brain would remain Swedish. The Chinese muscle would make it affordable.

This was not altruism. It was not sentimentality. It was strategic genius born from studying exactly how previous cross-border automotive acquisitions had failed.

The most instructive cautionary tale was Daimler-Chrysler, the "merger of equals" in 1998 that became a textbook case of cultural destruction. Daimler's German engineers imposed their standards on Chrysler's American operations, killing the speed and creativity that had made Chrysler profitable. The merged company hemorrhaged value, and Daimler eventually sold Chrysler to Cerberus Capital for six billion dollars — a fraction of the thirty-six billion it had paid. BMW's acquisition of Rover followed a similar pattern of cultural collision and value destruction.

Li studied these failures obsessively and drew a simple conclusion: the best way to get value from a European automotive brand is to leave it alone.

There was also a political dimension that is often overlooked. The Volvo acquisition required approval from both Swedish and Chinese regulators, and Li navigated both with remarkable skill. In Sweden, he personally met with union leaders, toured factories, and made commitments about employment levels that he has largely kept. In China, the acquisition was celebrated as a national triumph — proof that Chinese companies could compete on the global stage — and Li received tacit government support that smoothed the regulatory path.

He understood something that many cross-border acquirers miss: the deal does not close when the lawyers sign the papers. It closes when the people on the factory floor believe that the new owner is serious.

The question that every analyst asked in August 2010 was whether this promise of autonomy would survive contact with reality. The answer would take a decade to fully reveal itself, and it would come in the form of a modular vehicle platform that changed the trajectory of the entire Geely empire.

IV. The Great Leap Forward: Technology Transfer and CMA (2011–2017)

The best acquisitions in business history are not the ones that generate immediate headlines. They are the ones that generate compounding returns over a decade. Amazon's purchase of Kiva Systems did not make the front page, but it gave Amazon the robotic fulfillment capability that now underpins its entire logistics empire. Disney's acquisition of Pixar was criticized as overpriced, but it rejuvenated Disney Animation and generated tens of billions in franchise value. The Geely-Volvo deal belongs in this category. The real value was not in the transaction — it was in what happened after.

The first five years after the Volvo acquisition were quiet — conspicuously so for an industry that usually demands immediate returns from blockbuster deals. Li Shufu kept his promise. Volvo stayed in Gothenburg. The Swedish management team was not replaced. No factories were shuttered, and no jobs were shipped to China. Instead, Geely did something that would prove far more valuable than any short-term cost-cutting: it invested.

The numbers tell the story. Geely committed approximately eleven billion dollars in total investment into Volvo over the decade following the acquisition. This funded three new vehicle architectures — the Scalable Product Architecture (SPA) for larger models, the Compact Modular Architecture (CMA) for smaller ones, and the electrified derivatives of both.

It paid for new factories: a plant in Chengdu opened in 2013, and a second Chinese facility in Daqing followed in 2014, giving Volvo manufacturing capacity inside the world's largest car market for the first time. It funded the complete renewal of Volvo's product lineup — the XC90, S90, XC60, XC40, and their electrified variants — replacing a generation of aging, Ford-platform vehicles with cars that were genuinely competitive with Audi, BMW, and Mercedes in technology, design, and safety.

The results were dramatic, though they came slowly at first. In the early years, Geely's investment went largely into R&D and factory construction — activities that generated no immediate revenue but laid the foundation for everything that followed. The outside world saw little change, and skeptics continued to predict that Geely would eventually strip Volvo's technology and abandon the autonomy promise.

They were wrong.

Volvo sold 373,525 cars in 2010, the year of the acquisition. By 2017, that figure had grown to 571,577 — a fifty-three percent increase. By 2023, it reached 708,716. Revenue doubled. Profitability was restored and then expanded. The brand, which had been perceived as "safe but boring" under Ford, was repositioned as a Scandinavian luxury brand with a focus on sustainability, minimalist design, and advanced safety technology.

The XC90 deserves its own moment because it was when the world realized Geely had not ruined Volvo — it had unleashed it. Launched in 2014 as the first vehicle on the new SPA platform, the XC90 was a revelation. Thomas Ingenlath, Volvo's head of design (later the CEO of Polestar), had created something that was both unmistakably Scandinavian and thoroughly modern — clean lines, Thor's Hammer LED headlights, and an interior that prioritized calm and simplicity over the button-heavy cockpits that German rivals favored.

Car and Driver called it "the best Volvo ever made." It was reviewed by critics as one of the best luxury SUVs in the world and sold out for months after launch. The XC90 proved that Geely's investment was not just a financial transaction — it was a creative liberation. Under Ford, Volvo had been forced to share platforms and components with cheaper Ford and Mazda vehicles, compromising its ability to develop truly differentiated products. Under Geely, with dedicated SPA and CMA architectures, Volvo could finally build vehicles that were engineered from the ground up to express the brand's values.

But the real strategic prize was not Volvo's resurgence. It was what happened when Volvo's engineering capability was connected to Geely's mass-market ambitions.

In 2013, Geely and Volvo established the China Euro Vehicle Technology Centre, or CEVT, in Gothenburg. This was the architectural joint that connected the two companies. CEVT's mandate was to develop shared vehicle platforms that could be used by both Geely and Volvo brands — combining Swedish engineering standards with Chinese manufacturing costs. The first product of this collaboration was the CMA platform.

Think of CMA as the "secret sauce" of the Geely-Volvo relationship. It was a compact vehicle architecture that met Volvo's safety and quality standards but was designed to be manufactured at Chinese cost structures. The platform was flexible enough to support sedans, SUVs, and hatchbacks, with both internal combustion and plug-in hybrid powertrains. For Volvo, CMA underpinned the XC40 — the brand's entry-level SUV and one of its best-selling models. For Geely, it became the basis for an entirely new brand.

That brand was Lynk & Co, and its launch tells you everything about how Li Shufu was thinking about the future of automotive retail.

The Berlin debut in October 2016 was one of the most unusual brand introductions in automotive history. Rather than positioning itself as a traditional car company, Lynk & Co was presented as a "mobility subscription" service — more Netflix than BMW. The brand's proposition was that you did not need to own a car; you could subscribe to one on a monthly basis, share it with other members through an app, and swap vehicles as your needs changed.

The cars themselves — designed at CEVT and manufactured in Geely's Zhangjiakou factory — were sharp-looking compact SUVs with prominent grilles and tech-forward interiors. They looked nothing like anything Geely had ever made.

The Berlin launch was deliberate and tells you something about Li Shufu's understanding of brand psychology. He wanted Lynk & Co to be perceived as a European brand, not a Chinese one. The company established a flagship "club" in Amsterdam — part showroom, part co-working space, part coffee shop — and opened pop-up locations in Berlin, Barcelona, and Antwerp. In Europe, the subscription model was the primary sales channel. In China, the cars were sold through traditional dealerships as well, and they sold remarkably well: Lynk & Co moved over 220,000 units in China in 2021.

The deeper significance of the CMA platform and Lynk & Co was what they proved about the Geely-Volvo synergy model. Geely had not stripped Volvo's technology and slapped it onto cheap Chinese cars. Instead, it had created a shared engineering center that elevated both companies — Volvo got a cost-effective compact platform, and Geely got access to world-class engineering. The relationship was additive, not extractive. This was the vindication of the "Tiger in the Cage" philosophy: the tiger was back in the forest, and it was hunting with a pack.

The CMA story also highlights a subtle but important point about how technology transfer works in practice. Geely did not simply copy Volvo's blueprints and stamp them onto cheaper cars. The knowledge transfer happened through people, process, and co-development.

Swedish engineers at CEVT worked alongside Chinese engineers, and the learning went both ways. The Chinese team brought manufacturing pragmatism — how to design components that could be sourced from Chinese suppliers at a fraction of European costs without sacrificing the safety and performance standards that Volvo demanded. The Swedish team brought systems engineering discipline — how to integrate hundreds of subsystems into a vehicle that behaves predictably in every driving condition. Over time, the Geely-side engineers absorbed capabilities that would have taken decades to develop independently.

This human capital transfer — not the drawings or the specifications, but the tacit knowledge embedded in the people — was the real return on the Volvo acquisition.

By 2017, the transformation was visible in the numbers. Geely Auto's branded sales surged to 1.25 million units — a sixty-three percent year-over-year increase — up from around 330,000 units just five years earlier. Models like the Boyue SUV and the Emgrand sedan, engineered with technology and practices that traced back to the CEVT collaboration, were among the best-selling vehicles in China. The Geely brand had shed its reputation for cheap, unreliable cars and was competing credibly in the Chinese mass market against joint-venture brands like Volkswagen and Toyota. Gross margins were healthy. The stock price had quintupled.

For an acquisition that critics had called "a snake trying to swallow an elephant," the results were unambiguous.

The significance for investors went beyond the sales numbers. Geely had demonstrated a repeatable formula: acquire a distressed Western brand, preserve its autonomy, connect it to Chinese manufacturing scale through shared platforms, and use the technology transfer to elevate the entire portfolio. It was a playbook that could be run again. And Li Shufu had already identified his next targets.

V. Inflection Point #2: The M&A Blitz and the Daimler "Collar" (2017–2019)

Most companies would have spent 2017 celebrating. Geely Auto had just posted the best year in its history. Volvo was thriving. The CMA platform was entering production. Lynk & Co was generating global buzz. Any reasonable CEO would have declared victory, consolidated the gains, and focused on execution.

Li Shufu is not a reasonable CEO. He is a man who built a Mercedes out of fiberglass in a shed. And in 2017, he decided that the Volvo deal was not the culmination of his ambitions — it was merely the proof of concept.

If the years from 2011 to 2017 were about patient engineering work behind closed doors, the period from 2017 to 2019 was when Li Shufu stepped onto the global stage and announced — in the most dramatic way possible — that Geely was no longer a Chinese company with a Swedish subsidiary. It was a global automotive empire.

The shopping spree began in June 2017 with a single transaction that delivered two prizes. Geely acquired a 49.9 percent stake in Proton Holdings, the Malaysian national carmaker, from DRB-HICOM. Bundled into the same deal was a 51 percent controlling stake in Lotus Cars, the legendary British sports car manufacturer that Proton had owned since 1996 and had never figured out how to properly fund or manage.

The Proton deal was strategic geometry. Malaysia offered Geely a manufacturing base in Southeast Asia, right-hand-drive production capability, and access to the ASEAN market — a region with six hundred million consumers and rapidly growing automotive demand. Proton had been in decline for over a decade, hemorrhaging market share to Toyota and Honda, but it still had brand recognition, a dealer network, and government support.

Geely applied the playbook it had perfected with Volvo: inject capital, introduce Geely-engineered vehicles adapted for the local market, and let the local team run operations. The Proton X70, based on Geely's Boyue SUV, launched in 2018 and became the first new Proton SUV in years. It was followed by the X50, and Proton posted five consecutive years of sales growth through 2023, reclaiming the number-two position in Malaysia with roughly twenty percent market share.

Lotus was a different kind of bet entirely. If Proton was about market access and manufacturing capacity, Lotus was about heritage, prestige, and the transformative power of a legendary name.

The brand had been starved of investment for decades under a succession of owners who admired it but could never figure out how to fund it. Lotus was selling only a few thousand cars a year — the Elise, Exige, and Evora, all brilliant driver's cars built in tiny numbers at the company's factory in Hethel, Norfolk. But it possessed something money could not easily buy: one of the most storied names in motorsport history, with engineering DNA that traced back to Colin Chapman's revolutionary lightweight designs of the 1950s and 1960s. Chapman's motto — "Simplify, then add lightness" — had defined a philosophy of engineering excellence that influenced everyone from Gordon Murray to Adrian Newey.

Geely poured approximately three billion dollars into Lotus, including over one billion for a new factory in Wuhan, China. The strategy was to transform Lotus from a niche sports car maker into an electric performance brand — launching the Eletre, a hyper-SUV, and the Emeya, a hyper-GT, while keeping the Emira, the last internal-combustion Lotus, in production at the historic Hethel factory. Lotus Technology completed a SPAC merger with L Catterton Asia Acquisition Corp and listed on the Nasdaq in February 2024 under the ticker LOT, valued at approximately seven billion dollars.

Meanwhile, Geely was transforming the London black cab. The company had acquired the London Taxi Company — the manufacturer of the iconic hackney carriage — in 2013 and rebranded it as the London Electric Vehicle Company, or LEVC. Geely invested three hundred twenty-five million pounds in a new manufacturing facility at Ansty Park near Coventry, and the result was the LEVC TX: an extended-range electric vehicle with over seventy miles of pure electric range and a total range of three hundred thirty-three miles with its gasoline range extender. It still had the six passenger seats, rear-hinged doors, and wheelchair ramp that Transport for London required, but it was now fundamentally an electric vehicle. By late 2023, over half of London's taxi fleet was zero-emission capable, with the majority being LEVC TXs.

The common thread connecting all these acquisitions — Proton, Lotus, LEVC — was the same logic that had driven the Volvo deal: buy undervalued brands with strong heritage and loyal niche followings, inject Geely's capital and Chinese manufacturing capability, and extract technology synergies that benefited the entire portfolio. Each time, the brand was kept operationally independent. Each time, the technology flowed in both directions. And each time, the asset was worth dramatically more within Geely's ecosystem than it had been under its previous owner.

Then came the Daimler shock.

In late 2017, Li Shufu quietly approached Daimler AG — the parent of Mercedes-Benz — and asked the company to issue new shares so Geely could buy a direct stake. Daimler refused. What Li did next was one of the most audacious financial maneuvers in modern corporate history.

Working with Bank of America and Morgan Stanley, Li constructed a collar trade — a derivatives structure that is worth understanding because it reveals the sophistication of Geely's financial operations. In simple terms, a collar involves simultaneously buying shares in the open market while purchasing put options (downside protection) and selling call options (capping your upside). The net effect is that you accumulate a large position without the full capital outlay or the market impact that a traditional block purchase would create.

The banks act as intermediaries, absorbing the risk in exchange for substantial fees. Critically, the collar structure allowed Li to accumulate shares without triggering the German mandatory disclosure rules that would have required him to announce his position publicly once it crossed certain thresholds. It was, by some accounts, the largest collar trade ever executed in a single stock globally.

On February 24, 2018, the world learned that Li Shufu had built a 9.69 percent stake in Daimler AG — roughly nine billion dollars' worth — making him the company's single largest shareholder. Markets, regulators, and Daimler's own management were caught completely off guard. Germany's financial regulator, BaFin, investigated whether disclosure rules had been violated. Chancellor Angela Merkel stated there were "no obvious violations." The structure was technically legal, but it exposed gaps in European financial regulation that prompted an extended policy debate.

The strategic rationale was layered. On the surface, it was about technology access — a seat at the table for discussions about electric powertrains, autonomous driving, and battery technology. More concretely, the stake led to the formation of a fifty-fifty joint venture between Geely and Mercedes-Benz to produce electric Smart cars in China, manufactured on Geely's SEA platform. Smart, the historic Mercedes microcar brand, was reborn as a global electric vehicle brand headquartered in Ningbo, with engineering in both China and Germany. The Smart #1 compact SUV launched in 2022, followed by the Smart #3 crossover coupe in 2023.

But the deeper significance of the Daimler stake was what it revealed about Li Shufu's strategic ambition. This was not a financial investment seeking dividends. It was a statement that Geely intended to be a peer of the world's greatest automotive companies — not a supplier, not a junior partner, but an equal sitting at the same table.

It is worth pausing to note what the Daimler stake cost relative to what it bought. Nine billion dollars for a 9.69 percent stake in Mercedes-Benz is, by any measure, an enormous bet for a company that was selling mass-market cars in China for under twenty thousand dollars. But the strategic return — the Smart joint venture, the technology sharing discussions, the seat at the table with one of the world's most prestigious automotive brands — would have been nearly impossible to achieve through any other means. You cannot call Mercedes-Benz and ask for a technology partnership when you are an unknown Chinese manufacturer. You can when you are their largest shareholder.

By 2019, Li Shufu had assembled an automotive portfolio that no other executive in the world could match in breadth or audacity: a Swedish luxury brand, a British sports car icon, a Malaysian national carmaker, London's black cabs, the largest shareholding in Mercedes-Benz, and a Chinese mass-market brand that was now selling over a million vehicles a year. The shopping spree was over. Now came the question of whether Geely could build something even more ambitious: a technology platform that would tie all of these assets together and position the company for the electric age.

VI. Inflection Point #3: SEA and the Birth of Zeekr (2020–Present)

The automotive industry has a saying: "The platform is the strategy." BMW's CLAR platform, Toyota's TNGA, Volkswagen's MQB — these modular architectures are the foundations upon which entire product lines are built, and the companies that get them right achieve structural cost advantages that persist for a generation. What Geely did with SEA was take this principle to its logical extreme: build a platform so flexible and so capable that it could underpin not just your own brands, but anyone else's.

In September 2020, as the world was still reeling from the pandemic, Geely unveiled the Sustainable Experience Architecture — SEA — at an event in Beijing. It was, on the surface, just another electric vehicle platform announcement in an industry that was churning them out by the dozen. But the ambition behind SEA was fundamentally different from anything a legacy automaker had attempted.

The platform had been in development for more than four years at CEVT in Gothenburg, at a cost of more than eighteen billion renminbi — roughly two and a half billion dollars. To understand what SEA is, imagine a skateboard — a flat floor containing the battery pack, electric motors, suspension, and wiring — onto which you can place any body style you want. SEA's modularity meant it could support wheelbases from 1,800 millimeters to 3,300 millimeters, meaning it could underpin everything from a compact city car to a full-size SUV, a sports car, or a pickup truck.

But the real innovation was not technical. It was strategic.

Geely described SEA as the world's first "open-source" electric vehicle platform — a deliberate analogy to Google's Android operating system. Just as Android allowed any smartphone manufacturer to build on Google's software without developing its own mobile OS from scratch, SEA would allow any automaker to build electric vehicles on Geely's engineering foundation. The company would license the platform to external partners, generating revenue from its R&D investment while establishing SEA as an industry standard.

Think of what this means in competitive terms. Most automakers treat their vehicle platforms as proprietary crown jewels — the architecture is the competitive advantage, and sharing it would be unthinkable. Geely flipped this logic. By opening the platform, it could achieve economies of scale that no single brand could match, spread R&D costs across a vastly larger production base, and create switching costs for partners who built their product pipelines around SEA. The more partners who adopted the platform, the more investment Geely could justify in improving it, which made it more attractive to new partners — a classic network-effects flywheel.

The internal adoption was immediate and comprehensive. Every Zeekr model — the 001, 007, 009, X, 7X, and Mix — is built on SEA. The Smart electric vehicles from the Geely-Mercedes joint venture use SEA. Jidu Auto, the joint venture between Geely and Baidu for autonomous electric vehicles, builds on SEA. And in November 2022, ElectroMobility Poland — the company behind the Izera national electric vehicle project — became the first confirmed external licensee.

The highest-profile external adoption, however, came from an unexpected direction: Waymo, Alphabet's autonomous driving subsidiary. The partnership, first struck in 2021, produced the Zeekr RT — a purpose-built autonomous vehicle based on a derivative of SEA called SEA-M, specifically designed for robotaxi and logistics applications. The vehicle bristles with sensors: thirteen cameras, four lidar units, six radar modules, and external audio receivers.

At CES 2026, Waymo rebranded it as the "Ojai" — pronounced "oh-hi," named after a village in the mountains above Los Angeles — because American consumers were unfamiliar with the Zeekr name. As of early 2026, Waymo employees and their families can hail the Zeekr-built van in San Francisco and Phoenix, which is typically the last step before public commercial availability.

Zeekr itself deserves its own narrative arc. Founded in March 2021 as Geely's premium battery-electric vehicle brand, it was conceived as a direct competitor to Tesla, NIO, and Xpeng. An Conghui, one of Li Shufu's longest-tenured and most trusted lieutenants, was named CEO. The first model, the Zeekr 001, was a shooting-brake style sedan — an unusual body style that immediately differentiated it from the crossovers and sedans that dominated the Chinese EV market. With its 800-volt architecture, over 400 kilometers of real-world range, and sub-four-second zero-to-hundred acceleration, the 001 was a statement vehicle.

What set Zeekr apart from the crowded field of Chinese EV startups was speed of execution. NIO had taken years to scale production past fifty thousand units. Xpeng struggled with quality issues in its early models. Zeekr, by contrast, had the full weight of Geely's manufacturing infrastructure behind it — existing factories, proven supply chains, and a platform that had already been validated through years of development and billions of dollars of investment. This was not a startup building from scratch. It was a startup with the resources of a three-million-unit automaker.

The growth trajectory was staggering. Zeekr delivered roughly seventy-two thousand vehicles in 2022, its first full year. That jumped to 118,685 in 2023, then to 222,123 in 2024 — an eighty-seven percent year-over-year increase. It was the fastest a Chinese new-energy vehicle company had ever gone from founding to a US public listing: the NYSE IPO in May 2024 priced at twenty-one dollars per ADS, the top of its range, raising approximately four hundred forty-one million dollars and valuing the company at over five billion dollars.

But the Zeekr IPO story has a second chapter that reveals something important about how Li Shufu thinks about capital allocation. In May 2025, barely a year after the IPO, Geely proposed taking Zeekr private. The merger was completed in December 2025 at a price of two dollars and sixty-eight cents in cash plus 1.23 new Geely shares per Zeekr ADS, making Zeekr a wholly owned subsidiary of Geely Auto. The rationale was consolidation: the "Taizhou Declaration" of September 2024 called for streamlining the multi-brand structure, eliminating duplicate R&D spending, and bringing Zeekr's technology fully under the Geely Auto umbrella.

This capital recycling — IPO a subsidiary to raise external funding and establish a public valuation, then re-absorb it when the strategic logic demands consolidation — is a move straight out of the private equity playbook. The same pattern played out with Volvo Cars, which IPO'd on the Nasdaq Stockholm in October 2021 at a valuation of roughly eighteen and a half billion dollars, raising over two billion in proceeds. Polestar listed via a SPAC merger with Gores Guggenheim in June 2022 at an implied enterprise value of twenty billion dollars, though the stock subsequently declined sharply.

The Zeekr product lineup expanded rapidly. The 009 luxury MPV arrived in early 2023. The Zeekr X compact crossover brought the brand's starting price below RMB 200,000. The 007 sedan, launched in late 2023 to compete directly with the Tesla Model 3 and BYD Seal, became the volume driver. The 7X mid-size SUV and the Mix compact MPV with its innovative sliding-door design followed in 2024. Each model was built on SEA but targeted a different use case, demonstrating the platform's versatility.

The Geely Galaxy sub-brand, launched in February 2023, addressed the mass-market NEV segment that sat between the Geely core brand's combustion-era positioning and Zeekr's premium ambitions. Galaxy models — including the L7 plug-in hybrid SUV and the E5 pure electric sedan — incorporated styling and technology derived from the Zeekr and Volvo platforms but at significantly lower price points. Galaxy contributed substantially to Geely's NEV mix improvement, helping accelerate the transition away from internal combustion engines.

The consolidated numbers tell the story of transformation. By 2025, Geely Auto delivered 3.02 million vehicles — exceeding its target of 2.71 million — and generated RMB 345 billion in revenue, up twenty-five percent year-over-year. Net profit was RMB 16.85 billion, and gross margins expanded to 16.6 percent. New-energy vehicle sales reached 1.69 million units, representing 55.8 percent of total sales — a remarkable shift for a company that was overwhelmingly an internal-combustion-engine manufacturer just five years earlier.

VII. Current Management and the Geely Empire Structure

Geely's corporate structure is often described as confusing, and that description is generous. The Zhejiang Geely Holding Group, Li Shufu's private holding company, sits at the top and controls a web of publicly listed entities, joint ventures, and wholly owned subsidiaries that span the globe. Understanding who runs what — and how they are incentivized — is essential to understanding the company's strategic logic.

Li Shufu remains the chairman and controlling shareholder, owning approximately forty percent of the holding group. Now sixty-two years old, he holds a master's degree from Yanshan University and a net worth of roughly fifteen billion dollars. His management style has been described as "visionary but hands-off" — he sets the strategic direction and approves major capital allocation decisions, but delegates operational execution to a small circle of trusted lieutenants.

Li is fond of military metaphors and historical allusions. He has compared Geely's multi-brand strategy to the Chinese concept of "zheng qi" — the orthodox force that holds the line while the unorthodox force flanks the enemy. Geely Auto is the orthodox force: reliable, high-volume, cash-generating. Zeekr, Polestar, and Lotus are the flanking maneuvers — smaller, more agile, attacking premium segments where margins are higher and brand perception shapes the entire portfolio's image.

The most important figure in Geely's financial architecture was Daniel Li Donghui, who joined Geely in April 2011 as vice president and CFO. Daniel Li — no family relation to Li Shufu — was the man who structured the Volvo and Daimler deals, managed the IPOs of Volvo Cars, Zeekr, Polestar, and Lotus Technology, and built the capital-recycling strategy that has become Geely's signature financial innovation.

His background tells you everything about the role he played: an MBA from Indiana University's Kelley School of Business, prior CFO roles at Liugong Machinery, Cummins Inc., and BMW Brilliance Automotive. He served as CEO of Geely Holding Group from November 2020 until December 2025.

An Conghui is the operational counterweight to Daniel Li's financial engineering. He joined Geely in 1996, making him one of the earliest employees, and rose through the ranks by overseeing the creation of CEVT, the development of the CMA platform, and the launch of Lynk & Co. When Zeekr was founded in 2021, An was named CEO. Following the December 2025 merger that brought Zeekr back under Geely Auto, An assumed the position of CEO of Geely Holding Group.

An is known inside the company as the "product guy" — the executive who understands both the engineering and the consumer experience, and who bridges the gap between what Geely's factories can build and what Chinese and global consumers actually want.

The incentive structure across the Geely empire is worth noting for investors. Management at each subsidiary has been heavily incentivized through equity in their respective entities, creating a "venture capital-like" structure within what is nominally a legacy conglomerate. When Zeekr went public, its management team held meaningful stakes. When Volvo Cars IPO'd, Swedish executives participated in the upside. This creates alignment between the operating units and the parent company while preserving the entrepreneurial energy that large conglomerates typically kill.

The risk, of course, is that subsidiary-level incentives can create misaligned priorities — a subsidiary CEO optimizing for their own unit's share price may resist consolidation that benefits the parent. The Zeekr privatization tested this tension directly, and the fact that it was completed relatively smoothly suggests the governance structure is robust enough to handle these moments.

There is also the question of the Geely family. Li Shufu's son, Li Xingxing (also known as Eric Li), has been quietly rising through the ranks. While Li Shufu has not publicly designated a successor, the presence of a next-generation Li in the organization adds a dynastic dimension that is common in Asian conglomerates but carries both continuity advantages and governance risks that outside investors should monitor.

The organizational structure reflects a deliberate design philosophy. Each brand operates with substantial autonomy — Volvo in Gothenburg, Lotus in Hethel and Wuhan, Polestar across European and American markets, Smart from its Ningbo base. But they are connected through shared platforms (CMA, SEA), shared supply chains, and increasingly shared technology stacks.

Think of it as a federation rather than a centralized empire — each state governs itself, but they share a common defense infrastructure and trade freely with each other. Whether this federation can sustain coherence as it grows toward five million annual units remains one of the key questions for investors.

VIII. The "Hidden" Businesses: Beyond the Car

Warren Buffett once said that you should invest in businesses simple enough to be run by an idiot, because eventually one will. By that standard, Geely is the anti-Buffett investment — a sprawling conglomerate whose business model spans seven continents and extends into outer space. But the individual pieces, when examined closely, reveal a surprisingly coherent strategic logic.

If all Geely did was make and sell cars, it would already be one of the most interesting companies in the global automotive industry. But Li Shufu has built something far more ambitious — an ecosystem of businesses that extend from low-earth orbit to city streets, and that collectively represent a bet on what mobility looks like in the 2030s.

The most striking of these is Geespace, Geely's satellite subsidiary. Founded in 2018, Geespace is building the "Geely Future Mobility Constellation" — a network of low-orbit satellites integrating communication, navigation, and remote sensing capabilities. The target is 240 satellites, and the launch cadence has accelerated rapidly: nine satellites in June 2022, eleven more in February 2024, ten more in September 2024.

To understand why a car company is launching satellites, think about what autonomous driving actually requires. A self-driving car needs to know its position on the road within centimeters, not meters. Standard GPS is accurate to about three to five meters — fine for telling you which street you are on, useless for telling a robot which lane to occupy. By building its own satellite constellation optimized for high-precision positioning, Geely is vertically integrating the navigation layer of autonomous mobility. It is the same impulse that led Tesla to develop its own chips and BYD to build its own batteries — the recognition that if a component is critical to your product's core function, you cannot afford to depend on someone else to supply it.

Farizon Auto, established in 2016, is Geely's commercial vehicle subsidiary and has been the market leader for new-energy light trucks in China for three consecutive years. Its flagship product is the Homtruck, available in both pure-electric (with battery-swap capability) and methanol fuel-cell hybrid versions. Commercial vehicles are less glamorous than premium EVs, but they represent an enormous addressable market: China's logistics sector operates tens of millions of trucks and vans, and the electrification of commercial fleets is still in its early stages.

The commercial segment also generates steadier, more predictable revenue than the consumer market — fleet operators make purchasing decisions based on total cost of ownership rather than brand sentiment, and once a fleet commits to a platform, switching costs are high.

CaoCao Mobility is Geely's ride-hailing platform, operating across Chinese cities with three service tiers. In February 2025, CaoCao launched robotaxi pilot operations in Suzhou and Hangzhou, using Geespace's satellite network for positioning.

The strategic value of CaoCao extends beyond its own revenue: it functions as a captive customer for Geely's electric vehicles, a real-world testing ground for autonomous driving technology, and a data source for understanding mobility patterns and vehicle performance. Every CaoCao vehicle generates data on driving conditions, battery degradation, maintenance needs, and customer preferences — data that feeds back into Geely's product development cycle. It is a closed loop that competitors without their own ride-hailing platforms cannot easily replicate.

Then there is methanol — and this is where the Geely story gets genuinely weird in the best possible way.

This might sound like a niche curiosity buried in a PowerPoint footnote, but it represents a serious strategic hedge that has been twenty years in the making. Geely has invested in methanol vehicle technology since 2005 — over two decades of development, more than twenty vehicle models, and 256 patents filed. In Guiyang, China, over ninety percent of the city's taxi fleet runs on methanol-powered Geely Emgrands.

What makes methanol interesting is not just its emissions profile — ninety-nine percent less sulfur oxides, sixty percent less nitrogen oxides, and seventy-five percent less particulate matter than petrol — but its strategic implications. If the world eventually decides that lithium battery supply chains are too concentrated, too environmentally destructive, or too geopolitically risky, methanol offers an alternative pathway to decarbonization.

Geely's latest methanol engine achieves thermal efficiency exceeding forty-six percent, and in a fifteen-month trial in Denmark, methanol vehicles achieved average well-to-wheel emissions of forty-six grams of CO2 per kilometer — lower than battery-electric vehicles in most countries when accounting for the carbon intensity of electricity generation. Geely also invested in Carbon Recycling International, an Icelandic company that produces green methanol using carbon capture. This is not a primary strategy — Geely is clearly betting on battery electric as the dominant powertrain. But it is one of the most thoughtful hedges in the industry against a single-technology future.

Finally, there is the Meizu acquisition — the one that made automotive analysts scratch their heads the hardest.

In June 2022, Geely acquired a 79 percent controlling stake in Meizu Technology, a Chinese consumer electronics company based in Zhuhai. Meizu was once a serious competitor to Xiaomi and Huawei in the Chinese smartphone market but had faded into irrelevance by the early 2020s. Geely did not buy Meizu for its phone business — the phones were almost irrelevant. It bought it for Flyme, Meizu's mobile operating system, and for the team of software engineers who built it.

Flyme now powers the infotainment systems in Lynk & Co and other Geely vehicles, creating a seamless "phone plus car" ecosystem that mirrors what Xiaomi and Huawei are pursuing from the opposite direction — starting with phones and adding cars. Li Shufu bet that the integration would be more effective starting from the car side, because the car is a more complex product with higher switching costs.

Taken together, these businesses form a picture that is either visionary or hubristic, depending on your perspective. Satellites provide centimeter-precision positioning. The SEA platform provides the vehicle architecture. Meizu provides the software. CaoCao provides the mobility service. Farizon handles commercial logistics. And methanol provides a hedge against an all-lithium future. Whether any single piece justifies its investment on a standalone basis is debatable. Whether the ensemble represents a genuinely differentiated strategic position in the global automotive industry is harder to dismiss.

IX. Analysis: Porter's 5 Forces and Hamilton's 7 Powers

Now that the narrative arc is complete — from refrigerator parts in Zhejiang to satellite constellations in low-earth orbit — it is time to step back and ask the hard question: does any of this amount to a durable competitive moat? A great story does not automatically make a great investment. Plenty of companies have assembled impressive asset portfolios only to see their competitive positions erode under the weight of their own complexity or the relentless pressure of better-capitalized rivals.

To understand Geely's competitive moat — or lack thereof — it helps to apply two frameworks that sophisticated investors use to evaluate durable competitive advantage.

Start with Hamilton Helmer's 7 Powers, the framework that asks: what gives a business pricing power and protects it from competitive erosion?

Scale Economies are Geely's most obvious power. The SEA platform is the ultimate scale play — a single R&D investment amortized across seven brands (Geely, Volvo, Polestar, Zeekr, Smart, Lotus, and Jiyue) and potentially external licensees. When Geely spends a billion dollars improving SEA's battery management system or crash structure, that cost is spread across more than three million vehicles annually. A competitor developing a proprietary platform for a single brand must absorb the same R&D cost across a fraction of the volume.

This is the same dynamic that made Volkswagen's MQB platform one of the most successful in automotive history — and Geely is pursuing it with even more brand diversity. The critical question is whether this scale advantage is real or theoretical. Volkswagen achieved genuine platform sharing because its brands — from Skoda to Audi — ultimately converged on similar components and manufacturing processes. Geely's brands are more diverse in their market positioning and geographic footprint, which creates complexity that can offset scale savings.

Cornered Resource is the most interesting and least obvious power. Geely possesses something no other automotive company in the world can replicate: the combination of European brand equity with Chinese supply-chain speed. It has Swedish engineering and design (Volvo, CEVT), British motorsport heritage (Lotus), German luxury partnerships (Mercedes/Smart), Malaysian manufacturing (Proton), and Chinese production costs and speed-to-market.

No Western company has the Chinese supply chain. No Chinese company has the European brands. This "East-West DNA" is a genuine cornered resource — it took fifteen years and tens of billions of dollars to assemble, and no competitor can replicate it quickly. The question is how durable this advantage is. BYD is building its own European brand presence through aggressive export pricing. Xiaomi brings consumer electronics brand power and software sophistication. The window in which Geely's unique combination is unmatched may be closing.

Process Power — the ability to do something that competitors cannot easily copy even when they can see what you are doing — is another lens worth applying. Geely's process power lies in its cross-border M&A playbook. The company has now executed half a dozen major international acquisitions, each time navigating different regulatory environments, labor relations, cultural contexts, and technology transfer challenges. The organizational capability to manage these transactions has been built over fifteen years and constitutes a genuine process advantage.

Switching Costs are emerging through the "Geely Ecosystem." The Meizu phone connects to the car's Flyme infotainment system. The car connects to Geespace's satellite network. CaoCao's ride-hailing service creates habitual user engagement. As these systems become more tightly integrated, the cost of switching away from a Geely vehicle — not just in money but in convenience and data continuity — increases.

This is the same playbook Apple uses with its hardware-software-services ecosystem, adapted for mobility. The honest assessment, however, is that these switching costs are still nascent. Most car buyers in China do not yet choose vehicles based on ecosystem integration the way they choose smartphones. Whether this changes in a world of software-defined vehicles and over-the-air updates is one of the most important questions in the industry.

Now turn to Porter's Five Forces, which provide a more immediate read on competitive dynamics.

Threat of New Entrants is the most pressing competitive challenge. The Chinese automotive market has seen an unprecedented wave of new entrants: Xiaomi delivered its first car in 2024 and targeted three hundred thousand units in 2025. Huawei, while not manufacturing directly, provides intelligent driving systems to partners like Seres and Chery, and Huawei-powered brands saw explosive sales growth in late 2025. BYD, already dominant with roughly twenty-nine percent of China's new-energy vehicle market, continues to expand aggressively.

Geely's defense is its multi-brand portfolio — the ability to compete simultaneously at multiple price points and in multiple segments makes it harder for any single new entrant to displace it. When Xiaomi attacks the premium sedan segment, Zeekr fights back. When BYD pressures the mass market, Geely Galaxy responds. This "multi-brand shield" is expensive to maintain but provides strategic flexibility that single-brand competitors lack.

Bargaining Power of Suppliers is mitigated by Geely's vertical integration. The company develops its own batteries and electric motors, manufactures its own transmissions, and controls key components through its supply chain. In an industry where battery costs represent thirty to forty percent of vehicle cost, controlling the supply chain is not just a margin advantage — it is an existential necessity. That said, Geely is less vertically integrated in battery production than BYD, which manufactures its own Blade Battery cells at massive scale. This gap represents both a cost disadvantage and a strategic vulnerability.

Rivalry Among Existing Competitors is the most intense it has ever been in the Chinese market. The price war that erupted in 2023 and continued through 2025 compressed margins across the industry and forced dozens of smaller players into bankruptcy or acquisition. Geely's gross margin of 16.6 percent — while improving — reflects the intense competitive pressure.

Bargaining Power of Buyers is high and increasing — arguably higher in China than in any other major automotive market. Chinese consumers are among the most well-informed and price-sensitive car buyers in the world, with access to detailed comparison tools and a cultural willingness to switch brands that would be unusual in Western markets.

Threat of Substitutes is perhaps the most interesting long-term force, and the one that gets the least attention in sell-side research. In Chinese cities, the substitute for car ownership is not another car — it is the combination of ride-hailing, public transit, e-bikes, and shared mobility that makes car ownership unnecessary for many urban consumers. Geely's CaoCao ride-hailing platform and its investment in autonomous driving through the Waymo partnership are hedges against this threat, positioning the company on both sides of the ownership-versus-mobility equation.

Stepping back from the framework analysis, the overarching picture that emerges is of a company with genuine but contested competitive advantages. The scale economies and cornered resource powers are real, but they are under constant attack from competitors who are themselves scaling rapidly. The switching costs are still theoretical rather than proven. Geely's bet is that it can survive the war of attrition currently raging in the Chinese market and emerge as one of the three or four players with the scale, technology, and brand portfolio to dominate the global industry in the 2030s.

For investors tracking Geely's ongoing performance, two KPIs matter more than any others.

First, NEV mix — the percentage of total sales that are new-energy vehicles. This metric captures the speed of Geely's transition from internal combustion to electrification, which directly determines its competitiveness in China's rapidly shifting market. The NEV mix reached 55.8 percent in 2025, up from 41 percent in 2024 — the trajectory needs to continue accelerating toward a target that approaches eighty or ninety percent by the end of the decade.

Second, gross margin trajectory. In an industry undergoing a vicious price war, the ability to maintain or expand gross margins while growing volume is the single best indicator of whether a company's scale advantages are translating into durable profitability. Geely's gross margin improved from 15.3 percent in 2023 to 15.9 percent in 2024 to 16.6 percent in 2025 — a positive trend, but still below the levels that would signal true pricing power in a brutally competitive market.

X. Playbook: Lessons for Founders and Investors

Beyond the investment thesis, the Geely story offers several lessons that extend well beyond the automotive industry — lessons about acquisitions, about patience, about brand management, and about the art of financial engineering in service of industrial strategy.

The first is what might be called "asset-light M&A" — the art of buying distressed assets and using their R&D to fuel mass-market growth. When Geely bought Volvo, it was not buying a car company. It was buying an engineering capability — the safety technology, the platform architecture, the design language — that would have cost tens of billions of dollars and a decade of time to develop organically. The purchase price was a fraction of Volvo's cumulative R&D investment.

By keeping Volvo operationally independent while connecting it to Geely's platforms, Li captured the engineering value without inheriting the operational dysfunction that had depressed the asset's price. The same playbook was applied to Lotus, Proton, and LEVC. The critical insight is that Li was not buying revenue or market share — he was buying knowledge and brand equity, which are infinitely more valuable per dollar when transferred into a fast-growing ecosystem. Every founder contemplating an acquisition should ask themselves Li's question: am I buying a business, or am I buying a capability? The answer determines everything about how you should structure, price, and manage the deal.

The second lesson is strategic patience. Li Shufu first approached Ford about Volvo in January 2007. The deal did not close until August 2010 — three and a half years of rejection, persistence, and careful preparation. He was laughed off, ignored, and dismissed before finally being taken seriously.

Many acquirers would have moved on after the first rejection. Li waited for the market cycle to turn in his favor — the 2008 financial crisis destroyed Ford's alternatives — and was ready to move when the moment arrived. This patience extended to the post-acquisition period: Geely invested in Volvo for years before the CMA platform began generating returns. The willingness to deploy capital with a five-to-ten-year payoff horizon is rare in any industry and almost unheard of in the Chinese automotive market, where the competitive clock runs fast and investors demand quarterly results.

The third lesson is about multi-brand portfolio management — specifically, the question of when to launch a new brand versus extending an existing one. Geely has never killed a brand, though the Taizhou Declaration suggested some streamlining may come. It has spawned new ones with remarkable frequency: Lynk & Co in 2016, Zeekr in 2021, Geely Galaxy as a sub-brand in 2023.

Each brand targets a specific segment and customer persona — mass market, urban mobility, premium EV, performance, luxury — and each has its own identity, pricing, and retail experience. The risk of this approach is brand proliferation and cannibalization. The advantage is that each brand can compete aggressively in its segment without diluting the positioning of the others.

It is the multi-brand strategy that made the Volkswagen Group the most profitable automotive conglomerate in history, adapted for the Chinese and electric-vehicle era. The open question is whether Geely has the management bandwidth and capital to sustain this many brands simultaneously — or whether the Taizhou Declaration's call for streamlining was an admission that the portfolio had grown too complex.

The fourth lesson is perhaps the most distinctive: capital recycling. The genius of taking sub-brands public is not just about raising external capital — it is about creating price discovery, establishing standalone valuations for embedded assets, and generating liquidity that can be redeployed into the next phase of growth.

Volvo's Stockholm IPO raised over two billion dollars. Zeekr's NYSE IPO raised over four hundred million. Lotus Technology's Nasdaq listing raised capital at a multi-billion-dollar valuation. Each of these events validated the parent company's asset value while providing external funding that reduced Geely's capital burden.

When Zeekr was re-absorbed in late 2025, Geely brought back an entity whose value had been tested by public markets and funded by external capital. This "IPO-and-reabsorb" cycle is a form of financial engineering that generates real liquidity and real price discovery without permanently diluting the parent's control. For investors in the parent company, it means that the intrinsic value of Geely Holding is always greater than the sum of its public market capitalizations — because the unlisted and recently re-absorbed entities carry value that the market has validated but not fully priced into the parent.

XI. The Road to 2030

The final question is whether the Geely story's best chapters are behind it or ahead of it.

Geely enters the second half of the 2020s as one of the most complex and ambitious automotive companies on the planet — and one that faces an equally complex set of challenges and opportunities. Its 2026 targets call for 3.45 million units across Geely Auto, with 2.22 million new-energy vehicles and 640,000 exports. The broader Geely Holding Group targets five million units by 2027. These are aggressive numbers, but the trajectory — from 1.69 million in 2023 to 3.02 million in 2025 — suggests they are achievable if the market cooperates.

The risks are substantial, specific, and worth enumerating clearly.

China's automotive price war shows no sign of abating, and the industry is likely to see further consolidation as weaker players exit. Geely's margins, while improving, remain under pressure from competitors like BYD who can leverage superior vertical integration in battery manufacturing to undercut on price.

The geopolitical risk of being a Chinese company that owns Western crown jewels like Volvo and Lotus is real and growing — the European Union's evolving stance on Chinese EV imports, including anti-subsidy investigations and proposed tariffs, adds regulatory uncertainty that could constrain Geely's ability to operate seamlessly across borders. Political sentiment in Europe and the United States toward Chinese-owned brands could shift quickly, and Geely's exposure to this risk is greater than any of its Chinese peers precisely because of the acquisitions that have been its greatest strategic achievement.

The management succession question is also worth watching. Li Shufu is sixty-two and has shown no signs of stepping back, but the transition from An Conghui as CEO of Zeekr to CEO of Geely Holding Group in late 2025 suggests a generational handoff is being quietly prepared. Whether An — or any successor — can replicate Li's unique combination of entrepreneurial vision, M&A instinct, and political navigation skill is unknowable but critical to the company's long-term trajectory.

There is also the "conglomerate discount" risk — the possibility that investors will never give Geely full credit for the sum of its parts because the structure is too complex, the cross-holdings too opaque, and the related-party transactions between listed and unlisted entities too difficult to evaluate from the outside. Conglomerate discounts are a persistent feature of Asian holding companies, and Geely's structure — with Geely Auto (0175.HK) as the primary listed entity, Volvo Cars on Nasdaq Stockholm, Polestar on Nasdaq, Lotus Technology on Nasdaq, and various unlisted entities within Geely Holding Group — makes consolidated valuation genuinely difficult. The Taizhou Declaration's emphasis on simplification may be partly motivated by a desire to reduce this discount.

On the other side of the ledger, the opportunities are extraordinary.

Geely has assembled a collection of assets — brands, platforms, technologies, and market positions — that no other automotive company possesses. The SEA platform has the potential to become an industry standard if external licensing gains traction beyond the initial partners. The Waymo partnership positions Geely at the center of the autonomous mobility revolution in the United States. The methanol technology provides optionality in a world where battery supply chains face increasing scrutiny. And the combination of Chinese manufacturing costs with European brand equity gives Geely a structural advantage in fast-growing markets — Southeast Asia, the Middle East, Latin America — where both factors are valued.

The export story deserves attention as well. Geely exported over 400,000 vehicles in 2025 and is targeting 640,000 in 2026. The primary export markets include Southeast Asia, the Middle East, Latin America, and increasingly Europe through the Volvo, Polestar, and Smart brands.

The European export channel is particularly important because it represents the highest-value market where the Geely ecosystem's European brands carry natural advantages. However, it is also where geopolitical risk is most acute — the European Commission's anti-subsidy investigation into Chinese EV imports, launched in late 2023, has cast a shadow over the growth trajectory. If additional tariffs are imposed on Chinese-manufactured vehicles, Geely's strategy of manufacturing some Volvo and Polestar models in China for European export could be disrupted.

Is Geely the next Volkswagen Group? The comparison is tempting but incomplete. Volkswagen built its empire over decades in a relatively stable regulatory and technological environment. Geely is building in a world where the internal combustion engine is being phased out, where autonomous driving is reshaping the value chain, and where geopolitical competition between China and the West threatens to fragment the global automotive market. What Li Shufu has built is not a copy of anything that came before. It is something new — a Chinese-owned, globally operated, technology-forward automotive conglomerate that defies easy categorization.

Consider the sheer improbability of the journey. In 1997, a man who had never built a car used a defunct prison factory license to assemble a fiberglass Mercedes knockoff in coastal Zhejiang. In 2010, he bought the real Volvo. In 2018, he became the largest shareholder in the real Mercedes. In 2024, his company launched satellites into orbit and built robotaxis for Waymo.