Honeywell Automation India: From Tata JV to Industrial Automation Powerhouse

I. Introduction & Episode Roadmap

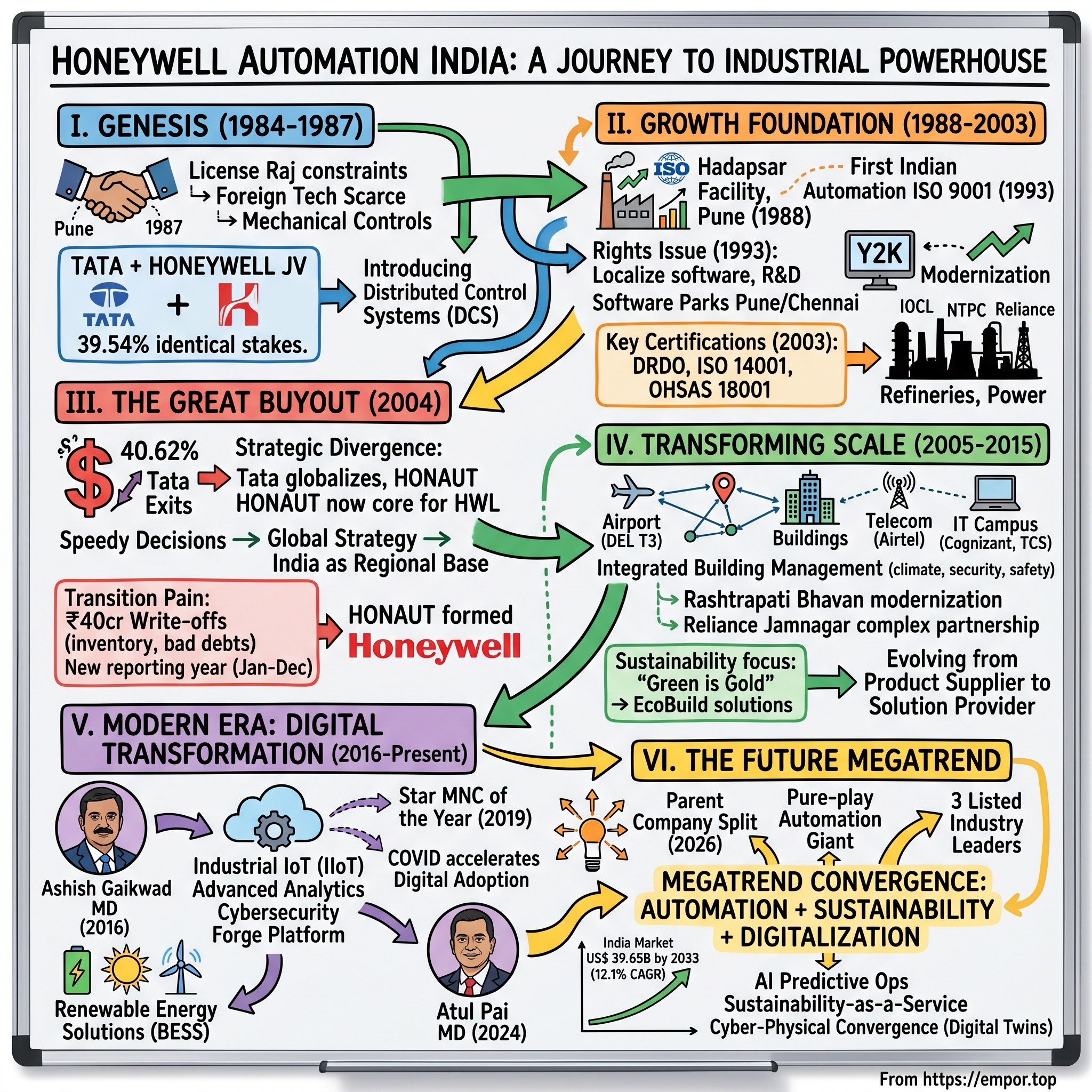

Picture this: It's 1987, and India's industrial landscape looks nothing like today. The License Raj still grips the economy, foreign technology is scarce, and most Indian factories run on mechanical controls that haven't changed since independence. In a modest office in Pune, two unlikely partners—the Tata Group, India's most trusted business house, and Honeywell, an American automation pioneer—shake hands on a venture that would fundamentally reshape how India's industries operate.

Today, that handshake has evolved into Honeywell Automation India Limited (HONAUT), a ₹31,700+ crore market cap behemoth that controls the nerve centers of India's largest refineries, powers the climate systems of its most prestigious buildings, and orchestrates the complex ballet of chemicals through the nation's petrochemical plants. From Rashtrapati Bhavan to Reliance's Jamnagar refinery, from Delhi's gleaming T3 terminal to Cognizant's sprawling campuses—HONAUT's technology pulses through the infrastructure that powers modern India.

But here's what makes this story truly fascinating: Unlike the typical foreign subsidiary playbook of market entry and gradual localization, HONAUT's journey is marked by three distinct acts of transformation. First, the delicate dance of a joint venture navigating India's pre-liberalization maze. Second, a dramatic buyout that saw Tata exit completely—rare for a successful JV. And third, the current race toward autonomous operations powered by AI and Industry 4.0.

The question that drives our exploration today isn't just how a joint venture became India's automation backbone. It's this: In an era where every industrial company claims to be "digital-first" and "AI-powered," how did a company born in the analog age of 1984 position itself at the forefront of India's $40 billion automation opportunity? And more intriguingly, why did Tata—known for holding assets for generations—walk away from what would become one of India's most valuable industrial technology companies?

This is a story about technology transfer and cultural fusion, about betting on India before liberalization made it fashionable, and about the unglamorous but essential business of making machines talk to each other. It's about how selling automation in India meant first selling the very idea that automation wasn't about replacing workers but amplifying human potential. Most importantly, it's about recognizing that in the race toward autonomous operations, the winners won't be those with the best technology alone, but those who understand the delicate interplay between global innovation and local execution.

As we journey through HONAUT's evolution—from that first Pune facility to today's AI-enabled solutions—we'll uncover the patterns that separate enduring industrial franchises from mere technology vendors. We'll examine why some joint ventures flourish while others flounder, why Honeywell succeeded where other multinationals struggled, and what HONAUT's trajectory tells us about India's next chapter in industrial development.

The stage is set not just by India's industrial awakening, but by a global megatrend that's accelerating: the convergence of automation, sustainability, and digitalization. As Honeywell's parent company prepares to split into two focused entities—one pure-play automation giant and one aerospace leader—HONAUT finds itself at an inflection point. The next decade will determine whether it remains a steady performer in India's industrial landscape or transforms into the platform that powers the country's leap toward autonomous operations.

II. The Joint Venture Genesis: Tata Meets Honeywell (1984–1987)

The monsoon of 1984 brought more than rain to India's industrial landscape. In a conference room overlooking the sprawling Tata headquarters in Bombay House, representatives from two vastly different corporate cultures sat across a mahogany table, navigating the delicate choreography of forming what would become one of India's most consequential industrial partnerships. On one side sat the Tata Group, embodiment of Indian industrial pride, carrying the legacy of Jamsetji Tata's vision of self-reliant India. On the other, Honeywell executives from Minneapolis, armed with automation technology that most Indian factories had only read about in trade journals.

The entity they birthed—Tata Process Controls Private Limited, incorporated in January 1984 in Maharashtra—would become the vessel through which India's factories would leap from mechanical controls to digital automation. But the story of how these two giants came together reveals as much about India's economic constraints as it does about corporate strategy.

Consider the context: This was Rajiv Gandhi's India, where the winds of change were beginning to blow but the License Raj still dictated who could manufacture what, in what quantity, and with whose technology. Foreign companies couldn't simply set up shop; they needed Indian partners who could navigate the byzantine corridors of Delhi's bureaucracy. For Honeywell, already a global automation powerhouse with operations from Houston refineries to Rotterdam chemical plants, India represented both enormous potential and enormous complexity. The country's industrial base—steel plants, refineries, power stations—desperately needed modernization, but accessing this market required more than technology. It required trust, patience, and most importantly, the right partner.

The partnership structure reflected this reality: when the company became operational as Tata Honeywell Limited in 1987, both Tata Group and Honeywell Asia Pacific Inc held identical 39.54% stakes. This wasn't just financial symmetry—it was diplomatic precision. Neither partner could claim dominance; both had equal skin in the game. The remaining shares were held by Indian financial institutions and the public, a structure that satisfied both regulatory requirements and nationalist sensitivities.

But why automation, and why then? For Tata, the logic was compelling. The group's own steel plants, chemical facilities, and power operations needed the kind of process control systems that Honeywell had perfected over decades. Rather than remain perpetual technology importers, why not manufacture these systems in India, for India? The import substitution philosophy that had driven Indian industrial policy since independence found a willing champion in the Tatas.

The venture started operations with a small team of engineers and technicians at its facility in Hadapsar, Pune, primarily focusing on providing automation and control solutions to industries such as refineries, petrochemicals, and power generation. The choice of Pune was strategic—close enough to Bombay's commercial hub, but with lower costs and access to engineering talent from the city's numerous technical institutes.

The early team faced a peculiar challenge: selling the very concept of automation to Indian industry. In 1987, many Indian plant managers still relied on analog gauges, manual valve controls, and armies of operators taking readings every hour. The idea of distributed control systems (DCS)—where sensors, controllers, and computers worked in concert to manage entire plants—seemed like science fiction. More threatening still was the perception that automation meant job losses, a politically explosive notion in a country where industrial employment was sacrosanct.

Honeywell brought more than just technology to this partnership. They brought a fundamentally different approach to industrial operations—one where data, not intuition, drove decisions; where predictive maintenance replaced reactive repairs; where a single operator could monitor what previously required dozens. But translating this vision required more than installing equipment. It required changing mindsets.

The American partner's technology portfolio in 1987 was already impressive: TDC 3000 distributed control systems that had revolutionized refinery operations globally, smart transmitters that could self-diagnose problems, and safety systems that prevented the kind of industrial disasters that haunted the developing world. But Honeywell's executives understood that success in India wouldn't come from simply transplanting American solutions. The technology needed to be tropicalized—adapted for India's extreme heat, monsoon humidity, and frequent power fluctuations.

Meanwhile, Tata brought something equally valuable: credibility. When Tata Honeywell's sales engineers knocked on doors at Indian Oil, Bharat Petroleum, or NTPC, they weren't seen as foreign vendors pushing expensive imports. They were part of the Tata family, inheritors of a trust built over a century. This mattered immensely in an environment where purchase decisions involved not just technical evaluation but also navigating complex webs of bureaucratic approval.

The joint venture also benefited from an unexpected tailwind: the Bhopal disaster of 1984. The tragedy at Union Carbide's pesticide plant, which killed thousands and remains one of history's worst industrial accidents, had fundamentally altered India's attitude toward industrial safety. Suddenly, conversations about safety systems, emergency shutdowns, and process control weren't luxuries—they were necessities. Tata Honeywell found itself at the intersection of technology and conscience, offering solutions that could prevent another Bhopal.

By the end of 1987, the joint venture had established its engineering center in Pune, begun localizing Honeywell's global products for Indian conditions, and started the slow process of building a sales and service network across the subcontinent. The company's first major wins came from the oil and gas sector—refineries that needed to modernize to meet new environmental standards and improve yields. Each project was a proving ground, demonstrating that automation could deliver tangible returns: higher production efficiency, lower emissions, fewer accidents, and paradoxically, more skilled jobs as operators became system managers rather than valve turners.

The cultural fusion within the company was fascinating to observe. American engineers accustomed to working in climate-controlled labs learned to design systems that could survive 45-degree Celsius heat and dust storms. Indian engineers trained in theoretical excellence learned the relentless focus on field reliability and customer service that Honeywell demanded globally. The Pune facility became a melting pot where Minnesota met Maharashtra, where Six Sigma met jugaad, where global standards met local ingenuity.

As 1987 drew to a close, Tata Honeywell had laid the foundation for what would become a decades-long transformation of Indian industry. But neither partner could have predicted how dramatically India's economic landscape would change in just four years, when P.V. Narasimha Rao and Manmohan Singh would unleash liberalization, fundamentally altering the dynamics of foreign investment, technology transfer, and industrial growth. The joint venture that began as a careful navigation of the License Raj would soon find itself racing to capitalize on India's economic awakening.

III. Building the Foundation: Growth Under Joint Control (1988–2003)

The morning of March 15, 1993, marked a watershed moment for Tata Honeywell. As the certification auditor from Bureau Veritas handed over the ISO 9001 certificate to the management team in Pune, the company became the first and only Indian automation company to receive ISO 9001 certification in 1993-94. This wasn't just a piece of paper to frame on the wall—it was validation that an Indian company could match global quality standards in the demanding field of industrial automation.

The achievement came five years after the company had established an impressive 36,000 square feet state-of-the-art manufacturing, design and engineering facilities in the industrial city of Pune in 1988. This facility wasn't merely an assembly unit; it was equipped with system integrated services, testing facilities, systems assembly & staging centre, printed wiring assembly manufacturing facility and a smart technology centre. In an era when most Indian industrial companies were still importing control systems, Tata Honeywell was manufacturing them to international standards.

The path to ISO certification had required a fundamental transformation in how the company operated. Every process, from component sourcing to system testing, had to be documented, standardized, and continuously improved. For engineers accustomed to Indian industrial practices where flexibility often trumped standardization, this was a cultural revolution. But it paid dividends immediately—when Tata Honeywell engineers walked into a refinery control room carrying the ISO certification, they weren't selling promises; they were offering proven quality.

The timing of the 1993 rights issue couldn't have been better. The company came out with a Rights Issue of 2,080,000 equity shares at a premium of Rs. 25 per share, aggregating Rs. 7.28 crores to part finance normal capital expenditure and long term working capital requirements, totaling Rs. 13.8 crores. The issue was fully subscribed. This capital infusion came just as India's economy was opening up post-1991 liberalization, and industrial investment was accelerating.

The funds raised weren't just for capacity expansion—they represented a strategic bet on India's industrial future. Part of the capital went toward establishing Software Technology Park (STP) in Pune, which would later expand to Chennai in 1998-99. This wasn't just about writing code; it was about developing the software backbone for distributed control systems tailored to Indian industrial conditions. While global competitors were trying to sell off-the-shelf solutions, Tata Honeywell was building capabilities to customize systems for Indian refineries that processed different crude grades, power plants that dealt with varying coal quality, and chemical plants operating in extreme weather conditions.

The late 1990s brought a new dimension to the company's growth story. As Y2K fears gripped the global industrial sector, Tata Honeywell found itself in an unexpected position of strength. Indian companies, terrified that their aging control systems might fail when the calendar flipped to 2000, suddenly had budgets for modernization. The company's engineers worked round the clock, upgrading legacy systems, installing new controllers, and essentially future-proofing India's industrial infrastructure.

Then came 2003, a year that would showcase the company's evolution from a technology provider to a strategic partner for India's most critical sectors. The Company's GPS Manufacturing was certified by the DRDO, the premier defense research organization in India. This certification opened doors that had remained firmly shut to private companies—defense installations, strategic petroleum reserves, nuclear power plant auxiliaries. The trust implicit in DRDO certification meant that Tata Honeywell could now bid for projects that touched national security.

The same year brought another first: HAIL became the first automation company in India to have received a double certification of ISO 14001 and OHSAS 18001. While ISO 14001 demonstrated environmental management capabilities, OHSAS 18001 proved occupational health and safety excellence. For a company whose systems controlled hazardous processes in refineries and chemical plants, this dual certification was more than corporate responsibility—it was a competitive differentiator.

The period also saw the company's client list evolve into a who's who of Indian industry. Indian Oil Corporation's refineries began standardizing on Tata Honeywell systems. NTPC's power plants relied on their controls for efficient combustion and emissions management. Reliance Industries, then building what would become the world's largest refining complex at Jamnagar, chose Tata Honeywell for critical automation systems. Each project wasn't just a sale; it was a reference that opened more doors.

But success brought its own challenges. By 2003, the company employed over 1,300 people and generated revenues approaching $70 million. The joint venture structure, which had served well during the establishment phase, was beginning to show strains. Decision-making required consensus between Tata and Honeywell representatives, slowing response times in an increasingly competitive market. Global product roadmaps had to be negotiated with local market requirements. Investment decisions needed approval from two corporate headquarters with different risk appetites and strategic priorities.

The expansion during this period also reflected changing market dynamics. In 2003-04, Honeywell decided to expand its existing facility to accommodate additional 300 people and started to construct a new building in the existing premises. This wasn't just about adding desks; it was about building capabilities for the next generation of automation technologies. The facility would house testing centers for Experion, Honeywell's new process knowledge system that represented a leap from distributed control to integrated operations management.

Competition was intensifying too. ABB, leveraging its strong power sector presence, was aggressively pursuing process automation opportunities. Siemens brought German engineering excellence and deep pockets. Yokogawa offered Japanese precision and reliability. Emerson pitched integrated solutions. In this environment, being good wasn't enough—you had to be exceptional.

The company's response was to double down on its strengths: local engineering capabilities that could deliver global technology with Indian cost structures, service networks that could reach remote plant locations within hours, and most importantly, the trust that came from being part of both the Tata and Honeywell families. By 2003, when automation engineers in Indian companies thought about upgrading their control systems, Tata Honeywell wasn't just an option—it was often the default choice.

Yet beneath this success story, fundamental questions were emerging. Could a 50-50 joint venture structure (effectively, given the identical stakes) continue to serve both partners' interests as the market evolved? How would the company navigate the next wave of technological change—from proprietary systems to open architectures, from hardware to software, from products to solutions? And most intriguingly, what would happen if one partner decided the joint venture had served its purpose?

As 2003 drew to a close, these questions were no longer theoretical. Behind closed doors in Mumbai and Minneapolis, executives were already discussing what would become one of the most significant ownership transitions in Indian industrial history. The joint venture that had introduced cutting-edge automation to India was about to transform into something entirely different—a fully owned subsidiary of a global giant, with all the opportunities and challenges that entailed.

IV. The Great Buyout: Honeywell Takes Full Control (2004)

The boardroom at Bombay House on July 9, 2004, witnessed the end of an era. After seventeen years of partnership, Honeywell Asia Pacific Inc. acquired Tata Group's 40.62% stake in their former joint venture, Tata Honeywell Ltd, with the transaction announced in July 2004 and completed after all necessary regulatory approvals were received. The handshake that had created one of India's most successful industrial joint ventures was now being unwound with a different kind of handshake—one that transferred complete control to the American partner.

The numbers told only part of the story: Tata Honeywell had approximately 1,300 employees and had $70 million in revenues for the year that ended March 31, 2004. But behind these figures lay a more complex narrative of strategic divergence, changing priorities, and the evolution of India's business environment post-liberalization.

For Tata, the decision to exit wasn't about failure—quite the opposite. The joint venture had succeeded beyond initial expectations, establishing itself as India's premier automation company. But by 2004, the Tata Group was undergoing its own transformation under Ratan Tata's leadership. The conglomerate was globalizing aggressively—acquiring Tetley, eyeing Corus Steel, dreaming of Jaguar Land Rover. Capital was needed for these grand ambitions, and non-core holdings, even successful ones, became candidates for divestment.

More fundamentally, the automation business had evolved from a strategic necessity in 1987 to a financial investment by 2004. Tata's own companies—Tata Steel, Tata Chemicals, Tata Power—were now sophisticated buyers of automation technology with multiple vendor options. The exclusive relationship that once justified the joint venture had given way to arm's length commercial transactions.

For Honeywell, acquiring full control represented a different calculation. India was no longer the difficult, closed market of 1987. It was one of the world's fastest-growing economies, with industrial investment booming and infrastructure projects multiplying. Having a subsidiary rather than a joint venture meant faster decision-making, direct implementation of global strategies, and most importantly, the ability to use India as a base for regional expansion.

The company changed its reporting year from April-March to Jan-Dec to align its reporting practices with the international Honeywell group. As a result, in 2004, the company reported only 9 months financials. This seemingly mundane accounting change symbolized a deeper transformation—from an Indian company with American technology to an American company with Indian operations.

But the real drama emerged when Honeywell's new management team began examining the books more closely. After the takeover, Honeywell noticed that lot of receivables were unrecoverable but still shown as good. In addition, the company noticed that significant amount of inventory was non-usable; however, it was not written off. This was despite the management of the company being in the hands of reputed groups like Tata and Honeywell since 1987. As a result, in FY2004-FY2005, Honeywell Automation India Ltd wrote off about ₹40 cr of receivables and inventory.

This discovery revealed an uncomfortable truth about joint venture governance. When two partners share control, accountability can sometimes fall through the cracks. The Indian practice of carrying receivables for years—hoping that government customers would eventually pay—clashed with American expectations of clean balance sheets. Inventory that was "might need someday" by Indian standards was "obsolete" by Honeywell's global metrics.

The ₹40 crore write-off was painful but necessary. It represented not just bad debts and dead stock, but the price of transformation from a protected market player to a global competitor. The company moved towards a more conservative provisioning regime, with this transition taking place from Dec 04 to Dec 05.

Vinayak Deshpande continued serving as the firm's managing director through the transition, providing crucial continuity. His presence reassured customers that while ownership had changed, relationships built over seventeen years would endure. This mattered immensely in an industry where project cycles stretched over years and trust was earned through decades of reliable service.

The name change from Tata Honeywell Limited to Honeywell Automation India Limited in November 2004 was more than rebranding. For customers, it meant dealing with a subsidiary of a $25 billion global corporation rather than a local joint venture. For employees, it meant career paths that could extend to Minneapolis, Phoenix, or Shanghai. For competitors, it meant facing an entity with deeper pockets and direct access to global R&D.

The cultural transformation was equally significant. The joint venture had operated with a unique blend of Tata's relationship-based approach and Honeywell's process-driven culture. Now, pure Honeywell systems took over. Performance metrics aligned with global standards. Pricing decisions followed worldwide guidelines. Investment approvals went through regional headquarters in Singapore rather than Bombay House.

The company supplied industrial automation and control solutions to core industries such as petrochemicals, refining, oil and gas, mining, metals and power, and also offered building automation and security solutions. This portfolio positioning would prove prescient as India's economy entered a new growth phase, demanding exactly these capabilities.

The market's reaction to the buyout was mixed. Some investors worried about losing the Tata name's credibility. Others saw opportunity in a focused multinational committed to the Indian market. The stock price volatility in the months following the announcement reflected this uncertainty.

But Honeywell's commitment was clear. In 2003-04, Honeywell decided to expand its existing facility to accommodate additional 300 people and started to construct a new building in the existing premises. A state of the art Experion testing centre was housed in this building. During 2005, Honeywell completed construction of new building, which provided additional seating space for 425 people and also provides space for the test labs.

This expansion wasn't just about adding capacity. It was about building capabilities for next-generation products. Experion represented Honeywell's vision of unified operations—where process control, safety systems, and business applications worked seamlessly together. Having a testing center in India meant local customers could see demonstrations, run pilots, and get comfortable with technology that represented millions in investment.

The buyout also triggered a subtle but important shift in competitive dynamics. When Tata was a shareholder, certain Indian companies preferred dealing with what they saw as a "swadeshi" company. Now, Honeywell Automation India Limited had to compete purely on merit—technology, service, price. This forced the company to become more aggressive, more innovative, more customer-focused.

For Honeywell globally, the India subsidiary became a test bed for emerging market strategies. If you could succeed in India—with its price sensitivity, diverse requirements, and challenging operating conditions—you could succeed anywhere in Asia. The lessons learned in selling to Indian refineries would prove valuable in Indonesia, Thailand, and Vietnam.

As 2004 ended, the transformation from joint venture to subsidiary was complete on paper. But the real work of cultural integration, strategic alignment, and market positioning had just begun. The company that had introduced distributed control systems to India now had to prove it could lead India's next wave of industrial automation—not as a foreign transplant, but as an Indian company that happened to be owned by Americans.

V. The Transformation Years: Building Scale (2005–2015)

The decade from 2005 to 2015 would prove to be Honeywell Automation India's golden era of transformation. Armed with complete control and a clean balance sheet post-write-offs, the company embarked on an aggressive expansion that would see it evolve from an industrial automation specialist to the technological backbone of India's infrastructure boom.

The first major breakthrough came from an unexpected quarter. In 2006, when Delhi International Airport embarked on its massive modernization ahead of the 2010 Commonwealth Games, they needed more than just an air conditioning system—they needed an integrated building management platform that could handle everything from climate control to security, from energy management to fire safety. Honeywell's solution for Terminal 3, which would become one of the world's largest and most advanced terminals, set a new benchmark for infrastructure automation in India.

Major wins / customers include Bharti Airtel, Cognizant Technology Solutions, Delhi International Airport, IOCL, Kolkata Airport, Leighton Welspun, Reliance Industries, Tata Consultancy Services. But these names only hint at the transformation underway. Each of these projects represented a different facet of India's economic evolution, and Honeywell positioned itself at the intersection of all these trends.

The IT services boom created an entirely new market for building automation. When Cognizant and TCS built their sprawling campuses—each housing tens of thousands of engineers—they needed sophisticated systems to manage energy consumption, ensure 24/7 cooling for server rooms, and create comfortable working environments. Honeywell's building solutions weren't just about installing thermostats; they were about creating intelligent ecosystems where every sensor, every controller, every piece of equipment communicated seamlessly to optimize both comfort and costs.

Bharti Airtel's requirements were different but equally complex. As the telecom giant expanded its network across India, each cell tower, each switching center, each data facility needed precise climate control and power management. In a country where power cuts were routine and diesel generators were backup necessities, Honeywell's systems ensured seamless transitions, optimal fuel consumption, and most importantly, uninterrupted service to millions of mobile subscribers.

The crown jewel of this period came from an unexpected source. As a mark of recognition of our Performance Contracting business, a prestigious order was received from BEE (Bureau of Energy Efficiency, Government of India) for Rashtrapati Bhavan. The President's Estate—a 340-room palace built in 1929—needed modernization without compromising its heritage character. Honeywell's solution was a masterclass in discrete automation: sensors hidden behind historic facades, controllers that respected architectural integrity while delivering 21st-century efficiency.

But it was in the industrial sector where Honeywell's transformation was most profound. When Reliance Industries expanded its Jamnagar refinery to become the world's largest refining complex, the scale was staggering: 1.24 million barrels per day capacity, hundreds of process units, thousands of control loops. Honeywell didn't just supply equipment; they became Reliance's technology partner, providing everything from basic instrumentation to advanced process control, from safety systems to enterprise-wide optimization software.

The Indian Oil Corporation projects revealed another dimension of Honeywell's evolution. IOCL's refineries, many built in the 1960s and 70s, needed modernization without shutdowns. Honeywell pioneered "hot cutover" techniques—replacing entire control systems while plants continued operating, like performing heart surgery while the patient ran a marathon. This capability, refined in India's challenging conditions, would later become a global differentiator for Honeywell.

The period also saw significant leadership evolution. New leaders from Honeywell's global ranks brought international best practices while respecting local market dynamics. They understood that selling to Indian customers required more than technical excellence—it required patience for long sales cycles, flexibility in commercial terms, and most importantly, commitment to long-term relationships rather than transactional deals.

The company's approach to talent development during this period laid the foundation for future growth. Engineers hired in 2005 as fresh graduates were, by 2015, leading complex projects across Asia. The Pune facility became a training ground where global Honeywell employees learned about emerging market dynamics. The phrase "if you can make it work in India, you can make it work anywhere" became a company mantra.

Competition during this decade was fierce and multifaceted. ABB leveraged its power sector dominance to push into process automation. Siemens brought German engineering and deep pockets. Yokogawa offered Japanese precision. Emerson pitched integrated solutions. Local players like L&T began developing indigenous capabilities. In this environment, Honeywell's strategy was clear: compete on value, not price; sell outcomes, not products; build partnerships, not vendor relationships.

The financial crisis of 2008 tested this strategy. As global markets crashed and Indian growth slowed, industrial investment dried up. Projects were cancelled, payments delayed, budgets slashed. But Honeywell used this period to deepen customer relationships. When customers couldn't afford new systems, Honeywell helped them optimize existing ones. When capital budgets disappeared, Honeywell pioneered service models that improved efficiency without upfront investment. This approach built loyalty that would pay dividends when growth returned.

By 2010, as India's economy roared back, Honeywell was perfectly positioned. The company had evolved from a product supplier to a solution provider, from a technology vendor to a trusted advisor. The portfolio now spanned the entire automation pyramid—from field instruments to enterprise software, from discrete manufacturing to continuous processes, from greenfield projects to brownfield modernization.

The company's work on infrastructure projects during this period was particularly noteworthy. Metro rail systems in Delhi and Bangalore, airports in Hyderabad and Mumbai, smart city initiatives in Gujarat and Maharashtra—each project expanded Honeywell's footprint beyond traditional industrial automation into the broader infrastructure space. These projects required new capabilities: integration with multiple vendors, compliance with government specifications, and navigation of complex stakeholder environments.

The rise of sustainability as a business imperative created new opportunities. Indian companies, under pressure from both regulations and global customers to reduce emissions and improve efficiency, turned to automation as the answer. Honeywell's EcoBuild solutions for commercial buildings and advanced process control for industries promised—and delivered—significant reductions in energy consumption and emissions. The marketing tagline "Green is Gold" resonated with CFOs who saw sustainability investments delivering measurable returns.

By 2015, Honeywell Automation India had transformed from the joint venture of 2004 into something far more significant. With over 3,000 employees, expanding facilities, and a client list that read like a who's who of corporate India, the company had established itself as indispensable to India's industrial and infrastructure ecosystem. But more importantly, it had built capabilities that would prove crucial for the next phase of transformation—the digital revolution that was about to reshape industrial automation globally.

VI. Modern Era: Digital Transformation & Industry 4.0 (2016–Present)

The appointment of Ashish Gaikwad as managing director effective from October 1, 2016, marked more than a leadership transition—it symbolized the coming of age of homegrown talent in multinational corporations. Mr. Ashish Gaikwad had joined the company as a software engineer. He was appointed as managing director in 2016. His journey from coding automation solutions in the 1990s to leading the company in the era of artificial intelligence embodied the transformation of both the individual and the institution.

With more than 25 years of experience in automation, control, and advanced software applications in the process industry, Ashish brings a successful track record from a career spanning more than 26 years with a mix of operations, sales, strategic marketing, and general management. He holds a bachelor's degree in electrical and electronics engineering from Birla Institute of Technology and Science (BITS), Pilani. This wasn't just another CEO appointment—it was validation that India could produce global leaders who understood both bits and bytes as well as balance sheets.

The timing of Gaikwad's appointment coincided with a global inflection point. It is a great time for me to take on this responsibility in India, especially as Honeywell continues its evolution as a cyber-industrial company. This "cyber-industrial" vision wasn't marketing speak—it represented a fundamental reimagining of what an automation company could be in the age of cloud computing, artificial intelligence, and the Industrial Internet of Things (IIoT).

Under Gaikwad's leadership, Honeywell Automation India began its most ambitious transformation yet. The company that had introduced distributed control systems to India in the 1980s now had to lead the country's journey toward connected plants, predictive maintenance, and autonomous operations. This required not just new technology but a complete rethinking of the value proposition—from selling products to selling outcomes, from providing systems to enabling digital transformation.

The portfolio evolution during this period reflected changing market dynamics. Process solutions now went beyond traditional DCS to include advanced analytics, cloud-based monitoring, and cybersecurity solutions. Building solutions evolved from simple HVAC controls to integrated smart building platforms that optimized everything from energy consumption to space utilization to occupant wellness. The emergence of comprehensive lifecycle services transformed the business model from one-time sales to recurring revenue streams.

With his hands-on knowledge of the latest in automation and control solutions, including software solutions, digital transformation, the Industrial Internet of Things (IIoT), and his understanding of the Indian market, I am confident Ashish will take HAIL to new heights. This confidence proved well-founded as the company navigated multiple disruptions—from GST implementation to demonetization, from the global shift to renewable energy to the acceleration of digital adoption post-COVID.

The government's Make in India and Digital India initiatives created unprecedented opportunities. Industrial automation wasn't just about efficiency anymore—it was about national competitiveness. Smart factories, digital twins, predictive analytics—these weren't futuristic concepts but immediate necessities for Indian manufacturers competing globally. Honeywell positioned itself as the bridge between global technology and local implementation, between aspiration and execution.

The company's work in renewable energy during this period deserves special mention. Honeywell's Renewable Energy solutions, especially Battery Energy Storage Solution (BESS), help the renewable energy sector produce energy more efficiently, lower Total Cost of Ownership, Boost Revenue Streams, and to Optimize Asset Performance while reducing the environmental impact and improving safety and regulatory compliance. As India committed to ambitious renewable targets, Honeywell's solutions for grid stability, energy storage, and intelligent load management became critical infrastructure.

Competition in this era came from unexpected quarters. IT services giants like TCS and Infosys began offering IoT and analytics solutions. Cloud providers like AWS and Azure pitched platform-as-a-service models. Startups promised AI-powered optimization at fraction of traditional costs. In this environment, Honeywell's response was to leverage its domain expertise—you might be able to analyze data, but do you understand the thermodynamics of a distillation column? You might offer cloud storage, but can you ensure millisecond response times for safety-critical systems?

The financial performance during Gaikwad's tenure reflected both opportunities and challenges. Since thereof the company showed significant tighter WC management, better Margins, better FCF management. It seems that it was the change of the management at both domestic and holding company level, which brought the fortunes good for HAIL. The company witnessed better focus, better utilization, tighter control and discipline that changed the fortunes of the company since 2015.

Under his leadership, Honeywell Automation was recognized as India's Best Multi-National Company and was awarded 'Star MNC of the Year 2019', by Business Standard. This recognition wasn't just corporate vanity—it validated the company's evolution from a foreign subsidiary to an integral part of India's industrial ecosystem.

The COVID-19 pandemic, arriving in early 2020, tested every assumption about industrial automation. Suddenly, remote monitoring wasn't a nice-to-have but a necessity. Plants had to operate with skeleton crews. Supply chains needed real-time visibility. Buildings required sophisticated air quality management. Honeywell's solutions—developed over years for efficiency—suddenly became essential for business continuity.

The pandemic also accelerated digital adoption by years. Companies that had resisted cloud-based solutions suddenly demanded them. Organizations that had postponed digital transformation suddenly fast-tracked it. The market for industrial IoT, estimated to grow steadily over a decade, compressed into quarters. Honeywell, with its established platforms and proven solutions, was positioned to capture this accelerated demand.

By 2024, as Atul Pai was appointed as Managing Director, effective May 16, 2024, succeeding Ashish Gaikwad who is taking on a broader responsibility as India Leader for Industrial Automation, one of Honeywell International Inc's strategic business groups, the company had transformed yet again. It was no longer just an automation company but a digital industrial leader, no longer just a technology provider but a transformation partner.

The modern era also brought new challenges. Cybersecurity became paramount as industrial systems connected to the internet. Talent retention became crucial as tech giants poached automation engineers. Margin pressure intensified as customers demanded more value for less cost. Regulatory complexity increased as data localization and privacy laws evolved. Each challenge required not just tactical responses but strategic evolution.

Looking at the current landscape, India's industrial automation market is expected to reach $39.65 billion by 2033, growing at a CAGR of 12.10%. The drivers are clear: manufacturing competitiveness, infrastructure modernization, sustainability mandates, and labor productivity imperatives. But the real opportunity lies in the convergence of operational technology (OT) and information technology (IT), where Honeywell's dual heritage—industrial domain expertise and software capabilities—provides unique advantage.

The Industry 4.0 revolution isn't just about technology—it's about reimagining how industries operate. Smart factories that self-optimize, supply chains that self-heal, buildings that learn from occupant behavior, power grids that balance renewable intermittency—these aren't distant dreams but emerging realities. And at the center of this transformation stands Honeywell Automation India, no longer the joint venture of 1987 but a critical enabler of India's industrial future.

VII. Financial Performance & Market Position

The numbers tell a story of paradox. Current metrics: ₹31,726 Cr market cap, ₹4,412 Cr revenue, ₹512 Cr profit—impressive on the surface, yet Trading at 7.86 times book value, P/E ratio of 62.0 reveals the market's expectations far outpacing current performance. This valuation premium for a company with The company has delivered a poor sales growth of 4.95% over past five years presents a fundamental question: Is the market pricing in a transformation that hasn't yet materialized, or is it recognizing value that traditional metrics fail to capture?

The ownership structure provides clarity on control but raises questions about minority interests. Promoter Holding: 75.0% by Honeywell ensures strategic alignment with the parent but limits float, potentially explaining some of the valuation volatility. The almost debt-free status represents both strength and conservatism—strength in financial flexibility, conservatism in not leveraging cheap debt for growth in a capital-intensive industry.

The dividend policy—Company has been maintaining a healthy dividend payout of 18.1%—strikes a balance between rewarding shareholders and retaining capital for growth. But in a market where competitors are investing aggressively in digital transformation and emerging technologies, is this prudent capital allocation or missed opportunity?

The 5-year sales CAGR of merely 4.95% stands in stark contrast to the market opportunity. India Industrial Automation market is expected to reach US$ 14.18 billion in 2024 to US$ 39.65 billion by 2033, with a CAGR of 12.10% from 2025 to 2033. Alternative estimates suggest even higher growth, with The India Industrial Automation Market is expected to reach USD 17.28 billion in 2025 and grow at a CAGR of 14.26% to reach USD 33.64 billion by 2030. This disconnect between market growth and company performance suggests either execution challenges or strategic choices that prioritize margins over market share.

The stock's journey has been equally volatile. From an all-time high of ₹59,994 in June 2024 to a 52-week range of ₹31,025-53,072, the price swings reflect both market exuberance about automation's future and concerns about near-term delivery. The current market cap of ₹31,726 crores represents a -30.9% decline over one year, suggesting the market is recalibrating expectations.

Analyzing the financial health reveals a business model in transition. The project-based nature of industrial automation creates inherent lumpiness in revenues—a single large refinery project can spike quarterly numbers, while delays in government infrastructure spending can depress them. This volatility makes traditional valuation metrics less reliable and requires investors to look beyond quarterly fluctuations to long-term positioning.

The competitive landscape explains some of the growth challenges. The key players operating in the India industrial process automation market are Rockwell Automation, Honeywell, Emerson, Hitachi, ABB Ltd, Schneider Electric, Siemens, Fanuc Corporation, Mitsubishi Electric, Omron Corporation, Yokogawa India Ltd., Valmet, Azbil Corporation, Toshiba Corporation, General Electric, and others. In this crowded field, differentiation becomes crucial, and price competition can erode margins even as the market expands.

The transformation of revenue mix tells a deeper story. While traditional process automation remains the cash cow, new revenue streams from software, services, and digital solutions are growing but not yet at scale to move the needle significantly. The shift from capital expenditure-driven sales to operational expenditure-based models—subscription software, managed services, performance contracts—requires different selling motions, different financial metrics, and most importantly, different investor expectations.

Working capital management has emerged as a bright spot. The tighter control implemented since 2015 has improved cash conversion, crucial for a business where customer payment cycles can stretch across quarters. But this efficiency gain has limits—you can only optimize working capital so much before it impacts customer relationships or growth investments.

The geographic concentration risk often goes unnoticed. While HONAUT dominates certain segments in India, its limited international footprint means it's essentially betting everything on India's industrial growth story. Compare this to global peers who can offset regional slowdowns with geographic diversification, and the vulnerability becomes apparent.

The recent quarterly performance adds nuance to the growth story. Q1 FY26 unaudited results showing Revenue ₹11,831M, PAT ₹1,246M, EPS ₹140.95 suggest resilience but not acceleration. The numbers indicate a business maintaining profitability while struggling to capture the market's explosive growth.

The margin profile deserves scrutiny. In an industry where software and services typically command higher margins than hardware, HONAUT's margin stability suggests either excellent execution in commoditizing segments or inability to scale higher-margin businesses. Given the parent company's global capabilities in software and analytics, the latter explanation raises questions about technology transfer and local market adaptation.

The valuation premium—P/E of 62 compared to global automation peers trading at 20-30 times—reflects India's growth premium but also incorporates significant execution risk. Investors are essentially paying for a future where HONAUT successfully transforms from a project-based automation vendor to a digital industrial platform player. The track record suggests capability but questions remain about timing and execution.

Looking at capital allocation, the company faces a classic innovator's dilemma. Investing aggressively in emerging technologies like AI, IoT, and cloud platforms requires significant upfront costs with uncertain returns. Yet not investing risks obsolescence as nimble competitors and well-funded startups attack specific verticals with focused solutions.

The parent company's strategic decisions cast a long shadow. Honeywell's planned separation into focused entities—automation and aerospace—could be transformative for HONAUT, providing clearer strategic direction and potentially more investment. But it could also mean less support, less technology transfer, and more pressure for standalone performance.

The currency dynamics add another layer of complexity. As a subsidiary importing technology and components while selling in rupees, HONAUT faces constant currency hedging challenges. The rupee's depreciation benefits export competitiveness but increases input costs, creating a natural hedge that's never perfect.

Customer concentration, while not explicitly disclosed, likely follows industrial patterns—a few large projects contributing disproportionate revenues. This creates vulnerability to project delays, scope changes, or customer financial stress. The economic sensitivity of capital-intensive industries means HONAUT's fortunes are tied closely to India's industrial investment cycles.

The rise of Make in India and Atmanirbhar Bharat presents both opportunity and challenge. While these initiatives drive automation demand, they also encourage local competition and sometimes mandate local content that may conflict with HONAUT's global supply chains.

As we examine the financial performance, the question isn't whether HONAUT is profitable—it clearly is. The question is whether it's capturing its fair share of a exploding market opportunity, and whether its current trajectory justifies premium valuations. The numbers suggest a solid business navigating transformation, but not yet the explosive growth story the market opportunity would suggest possible.

VIII. The Automation Megatrend & Future Strategy

The February 6, 2025 announcement dropped like a strategic bombshell: Honeywell announced that its Board of Directors completed the comprehensive business portfolio evaluation launched a year ago by Chairman and CEO Vimal Kapur and intends to pursue a full separation of Automation and Aerospace Technologies. Combined with the previously announced Advanced Materials spin-off, The planned separation, coupled with the previously announced plan to spin Advanced Materials, will result in three publicly listed industry leaders with distinct strategies and growth drivers.

For Honeywell Automation India Limited, this represents the most significant strategic shift since the 2004 buyout. Honeywell Automation will maintain global scale, with 2024 revenue of $18 billion. Honeywell Automation will connect assets, people and processes to power digital transformation, building on decades-long technology leadership positions, deep domain experience, and a vast installed base to serve a variety of high-growth verticals. This isn't just corporate restructuring—it's the birth of a pure-play automation giant freed from the capital allocation tensions of a conglomerate.

The strategic logic is compelling. Honeywell Automation will be better able to capitalize on the global megatrends underpinning its business, from energy security and sustainability to digitalization and artificial intelligence. For the Indian subsidiary, this means clearer strategic focus, dedicated investment capital, and most importantly, alignment with the three megatrends reshaping industrial landscapes globally: automation, sustainability, and digitalization.

Consider what this means for technology development. Currently, Honeywell's R&D budget gets allocated across aerospace (high margin, long cycles), automation (rapid evolution, competitive pressure), and materials (commodity exposure, cyclical). Post-separation, the automation entity can invest aggressively in AI, machine learning, and autonomous systems without competing for capital with aircraft engine development or specialty chemical plants.

The AI revolution stands at the center of this transformation. 2025 is emerging as the year AI revolutionizes the industrial sector at scale—not as pilot projects or proof-of-concepts, but as production-ready systems that fundamentally alter how factories operate. Honeywell's Forge platform, combining decades of domain expertise with modern cloud architecture and AI capabilities, positions the company to lead this transition. But success requires more than technology; it requires reimagining the very nature of industrial operations.

The path to autonomous operations addresses multiple converging pressures. Skilled labor shortages plague industries globally—experienced operators retiring faster than replacements can be trained. Regulatory demands for safety, environmental compliance, and operational transparency grow stricter annually. Customer expectations for quality, consistency, and customization reach new heights. Autonomous operations promise to address all these challenges simultaneously, but the journey from today's supervised automation to tomorrow's self-optimizing plants requires careful orchestration.

For HONAUT, the parent company's transformation creates both opportunities and challenges. On the opportunity side, being part of a pure-play automation company means access to more focused investment, clearer strategic direction, and stronger market positioning. The company can pursue aggressive growth strategies in emerging areas like battery energy storage systems, green hydrogen production, and carbon capture without competing for mindshare with aerospace priorities.

The India-specific opportunities are particularly compelling. As the country commits to net-zero targets, every industrial facility needs modernization. The shift from fossil fuels to renewable energy requires sophisticated grid management and storage solutions. The semiconductor fabrication plants being established need ultra-precise environmental controls. Data centers proliferating across the country demand sophisticated cooling and power management. Each of these represents not just a sale but a long-term relationship opportunity.

The digitalization imperative creates another growth vector. Indian companies, having leapfrogged certain technological generations in consumer technology, are increasingly willing to do the same in industrial technology. Why progress through incremental automation improvements when you can jump directly to AI-enabled autonomous systems? This mindset, coupled with relatively newer industrial infrastructure compared to developed markets, positions India as an ideal testbed for next-generation automation technologies.

But challenges loom equally large. The separation means HONAUT loses the financial cushion of being part of a diversified conglomerate. Economic downturns that previously might have been offset by aerospace strength will hit directly. The company must stand on its own merits, compete for capital in public markets, and deliver consistent performance without the safety net of corporate reallocation.

Technology transfer mechanisms may also change. Currently, HONAUT benefits from innovations across all Honeywell divisions—sensor technology from aerospace finding applications in industrial settings, materials science from chemicals improving equipment durability. Post-separation, these synergies may require formal partnerships or licensing agreements, potentially increasing costs or slowing innovation adoption.

The competitive landscape will intensify post-separation. Pure-play automation companies like Rockwell and Emerson have spent years honing their strategies while Honeywell balanced multiple priorities. Digital natives like PTC and Aveva attack from the software side. Chinese competitors offer increasingly sophisticated solutions at aggressive price points. Standing alone, Honeywell Automation must prove it can compete not just on legacy and installed base, but on innovation and value delivery.

The sustainability imperative represents both the greatest opportunity and the most complex challenge. "The formation of three independent, industry-leading companies builds on the powerful foundation we have created, positioning each to pursue tailored growth strategies, and unlock significant value for shareholders and customers" For the automation business, this means becoming the enabler of global sustainability goals—helping industries reduce emissions, optimize resource usage, and transition to circular economy models.

Three specific technology areas will likely define success in this new era:

First, AI-powered predictive operations that don't just prevent failures but optimize entire value chains in real-time. This goes beyond traditional automation to create systems that learn, adapt, and improve autonomously.

Second, sustainability-as-a-service offerings that guarantee emission reductions and efficiency improvements through outcome-based contracts. This shifts the business model from selling products to delivering measurable environmental impact.

Third, cyber-physical convergence that seamlessly blends digital twins, augmented reality, and physical operations into unified management platforms. This represents the full realization of Industry 4.0 vision.

The separation is intended to be completed in the second half of 2026 and in a manner that is tax-free to Honeywell shareholders. This timeline gives HONAUT roughly 18 months to prepare for life as part of a standalone automation company. The preparation involves not just operational adjustments but fundamental strategic positioning—defining what unique value the Indian operation brings to the global automation entity and how it can leverage India's unique position in global supply chains.

The megatrend convergence—automation meeting sustainability meeting digitalization—creates a once-in-a-generation opportunity. Companies that successfully navigate this convergence won't just survive; they'll define the next era of industrial operations. For HONAUT, with its established base, technical capabilities, and market position, the question isn't whether it can participate in this transformation, but whether it can lead it.

IX. Playbook: Business & Investing Lessons

The HONAUT story offers a masterclass in navigating emerging market complexities, with lessons that extend far beyond automation into the broader dynamics of technology transfer, market development, and value creation in developing economies.

Lesson 1: Joint Ventures as Market Entry—The Critical Timing Window

The Tata-Honeywell partnership from 1987 to 2004 exemplifies both the power and limitations of joint ventures in emerging markets. The initial logic was impeccable: Honeywell needed local credibility and regulatory navigation; Tata needed technology and global best practices. But here's the critical insight: Joint ventures have an optimal lifespan. They work brilliantly for market entry and establishment—typically 10-15 years—but can become constraints when markets mature and strategies diverge.

The 2004 buyout timing was nearly perfect. India had liberalized, foreign ownership restrictions had eased, and Honeywell had built sufficient local credibility to stand independently. Tata, meanwhile, could redeploy capital to its global acquisition spree. Investors should watch for similar inflection points—when the benefits of partnership diminish relative to the constraints of shared control.

Lesson 2: Parent Company Commitment—Beyond Capital

Post-2004, Honeywell's commitment went beyond maintaining ownership. They invested in local manufacturing, established R&D centers, and most critically, developed local talent into global leaders. The current managing director of Honeywell Automation India Ltd, Mr. Ashish Gaikwad had joined the company as a software engineer. He was appointed as managing director in 2016. This isn't just good corporate citizenship—it's strategic wisdom. Local leaders understand market nuances, navigate regulatory complexity, and build trust in ways expatriate managers cannot.

The contrast with other multinationals who treat emerging market operations as sales outposts is stark. Honeywell's approach—developing India as a capability center, not just a market—created competitive advantages that pure capital investment couldn't buy.

Lesson 3: Reputation as Competitive Moat

Major wins / customers include Bharti Airtel, Cognizant Technology Solutions, Delhi International Airport, IOCL, Kolkata Airport, Leighton Welspun, Reliance Industries, Tata Consultancy Services. As a mark of recognition of our Performance Contracting business, a prestigious order was received from BEE (Bureau of Energy Efficiency, Government of India) for Rashtrapati Bhavan. These aren't just customer names—they're proof points that create a virtuous cycle. Prestigious projects attract talent, build credibility for the next sale, and create barriers competitors cannot easily overcome.

In B2B industrial markets, reference selling is everything. One successful project at a Reliance refinery opens doors at every other refinery. One smooth implementation at Rashtrapati Bhavan signals capability for any government project. This dynamic creates winner-take-most markets where early leaders compound advantages over time.

Lesson 4: Economic Cycles and Project Business—The Resilience Test

Project-based businesses face unique challenges. Revenue recognition is lumpy, working capital needs are significant, and economic downturns can devastate order books. HONAUT's navigation through 2008's financial crisis, 2016's demonetization, and COVID-19 reveals important patterns.

First, service revenues provide stability when capital expenditure freezes. Second, operational efficiency improvements sell even in downturns—especially in downturns when companies need cost reduction. Third, government infrastructure spending often counter-cycles private investment, providing natural hedging. Investors should evaluate industrial companies not just on growth metrics but on their ability to maintain profitability through cycles.

Lesson 5: Growth Versus Margins—The Mature Market Dilemma

The company has delivered a poor sales growth of 4.95% over past five years. Yet margins remained stable and returns on capital stayed healthy. This represents a strategic choice: prioritize profitability over market share in a competitive, mature market. But is this the right choice?

The answer depends on market dynamics. In winner-take-all platform businesses, growth at any cost might make sense. But in industrial automation, where switching costs are high and relationships matter more than technology, profitable growth—even if modest—might be the wiser path. The challenge is communicating this to growth-obsessed markets that might undervalue stability.

Lesson 6: Technology Transfer and Localization

Successful technology transfer requires more than shipping products and manuals. It demands adapting solutions to local conditions—tropicalizing equipment for heat and humidity, modifying software for local regulations, creating service models that work with local infrastructure realities. HONAUT's success came from recognizing that automation in India isn't just automation at lower cost—it's fundamentally different automation shaped by unique operational contexts.

The broader lesson: technology companies entering emerging markets must choose between two models. Either maintain global standardization and accept limited market penetration, or invest in deep localization and accept complexity. Half-measures typically fail.

Lesson 7: Building Trust in B2B Markets

Industrial buying decisions involve enormous risk. A failed automation system can shut down a refinery, costing millions daily. In this context, trust matters more than technology, relationships more than price. HONAUT built trust through multiple mechanisms: the Tata association initially, consistent project delivery subsequently, and local presence continuously.

The trust equation in B2B markets has three components: capability (can you do it?), reliability (will you do it?), and alignment (are our interests aligned?). Marketing can signal capability, track records prove reliability, but alignment requires structural choices—local investment, long-term commitment, skin in the game.

Lesson 8: Managing Strategic Transitions

The upcoming Honeywell separation represents HONAUT's third major transition—from joint venture to subsidiary, and now to part of a pure-play automation company. Each transition risked customer defection, employee exodus, and strategic confusion. Yet the company navigated previous changes successfully. How?

The key lies in maintaining operational continuity while evolving strategic positioning. Customers care less about ownership structures than about service quality. Employees care less about corporate logos than about career prospects. By keeping operations stable during ownership transitions, companies can evolve strategies without disrupting relationships.

Lesson 9: The Valuation Paradox

Trading at P/E of 62 despite modest growth presents a paradox that teaches important valuation lessons. Markets sometimes price option value rather than current performance. HONAUT's valuation embeds multiple options: India's industrial growth acceleration, successful digital transformation, benefits from parent company separation. Whether these options realize value depends on execution, but their existence justifies premium valuations even amid modest current performance.

Lesson 10: Competitive Dynamics in Technical Markets

Industrial automation isn't a commodity market where lowest price wins. It's a technical market where total cost of ownership, lifecycle support, and risk mitigation matter more than purchase price. This creates interesting competitive dynamics. New entrants can't simply undercut prices; they must build entire ecosystems of support, service, and trust. Incumbents can't simply rely on installed base; they must continuously innovate or risk disruption.

For investors, this means looking beyond market share statistics to evaluate competitive position. Who has the strongest service network? Who invests most in R&D? Who has the deepest customer relationships? These intangibles often matter more than financial metrics.

The Meta-Lesson: Patience and Persistence

Perhaps the most important lesson from HONAUT's journey is the value of patience and persistence in industrial markets. Unlike consumer technology where winners emerge quickly, industrial markets evolve over decades. Relationships built over years matter more than brilliant strategies. Consistent execution trumps dramatic pivots.

For long-term investors, this suggests a different evaluation framework. Instead of asking "will this company disrupt the market?" ask "can this company compound advantages over time?" Instead of seeking explosive growth, look for sustainable competitive positions. Instead of focusing on quarterly results, evaluate decade-long trajectories.

The HONAUT playbook ultimately teaches that in industrial markets, success comes not from revolution but from evolution—careful, considered, consistent progress that builds trust, capability, and value over time. In an era obsessed with disruption, there's profound wisdom in this approach.

X. Bear vs. Bull Case Analysis

The investment case for HONAUT presents a fascinating study in contrasts—compelling strategic positioning shadowed by execution concerns, massive market opportunity tempered by competitive realities, premium valuations challenged by modest growth. Let's examine both sides with the rigor this complexity demands.

The Bear Case: Why Skeptics See Risk

Sluggish Growth in a Booming Market The most damning bear argument centers on the growth disconnect. India Industrial Automation market is expected to reach US$ 14.18 billion in 2024 to US$ 39.65 billion by 2033, with a CAGR of 12.10% from 2025 to 2033. Against this backdrop, HONAUT's 5-year revenue CAGR of 4.95% looks anemic. If you can't grow faster than GDP in a high-growth vertical, are you really a growth story or just a value trap with a growth multiple?

This underperformance suggests either execution issues or strategic misalignment. Perhaps the company prioritizes margins over market share, a defensible strategy but not one that justifies premium valuations. Or perhaps competitive dynamics have intensified beyond what financial statements reveal, with customers increasingly choosing alternatives despite HONAUT's reputation.

Valuation Stretched Beyond Fundamentals Trading at 62 times earnings and 7.86 times book value, HONAUT commands valuations typically reserved for high-growth technology companies. Yet this is a company growing at 5% annually, heavily dependent on project-based revenues, and operating in an increasingly competitive market. The valuation implies either massive acceleration ahead or significant multiple compression coming.

Compare HONAUT to global automation peers: Rockwell Automation trades at ~25x earnings, Emerson at ~22x, ABB at ~24x. Even adjusting for India's growth premium, a 2.5x valuation differential seems excessive for a company not demonstrably outperforming on growth or margins.

Dependency Dynamics and Strategic Constraints The 75% promoter holding by Honeywell creates both stability and strategic rigidity. Major decisions require alignment with global priorities that may not optimize for India. Technology development happens primarily outside India, creating dependency on parent company R&D priorities. The upcoming separation might help, but it also removes the diversification benefits of being part of a larger conglomerate.

This dependency extends to technology access. While HONAUT benefits from Honeywell's global innovations, it also pays for this access through royalties and technology fees that impact margins. Post-separation, these arrangements might become more transparent but not necessarily more favorable.

Competitive Intensity Accelerating The competitive landscape has evolved dramatically. The key players operating in the India industrial process automation market are Rockwell Automation, Honeywell, Emerson, Hitachi, ABB Ltd, Schneider Electric, Siemens, Fanuc Corporation, Mitsubishi Electric, Omron Corporation, Yokogawa India Ltd., Valmet, Azbil Corporation, Toshiba Corporation, General Electric, and others. This isn't just a long list—it represents deep-pocketed multinationals investing aggressively in India.

Moreover, new competition emerges from unexpected quarters. Indian IT services companies leverage software expertise to offer automation solutions. Chinese companies bring cost advantages. Startups attack specific verticals with focused solutions. The moat that protected HONAUT for decades is narrowing.

Project Volatility and Economic Sensitivity Industrial automation remains tied to capital expenditure cycles. When the economy slows, automation projects get deferred first. When credit tightens, industrial expansion freezes. This cyclicality makes earnings unpredictable and valuations volatile. The current premium valuation provides little margin of safety for the next downturn.

The Bull Case: Why Believers See Opportunity

Massive Market Opportunity Still Early The headline market numbers deserve deeper examination. India's industrial base remains significantly under-automated compared to global standards. The $39.65 billion market size by 2033 might prove conservative if India achieves its manufacturing ambitions. More importantly, the nature of demand is evolving from simple automation to intelligent systems, playing to HONAUT's strengths.

Consider specific verticals: India plans to add 500GW of renewable energy by 2030, each MW requiring sophisticated control systems. The semiconductor fabrication plants being established need ultra-precise automation. The pharmaceutical industry, post-COVID, is investing heavily in automation for both capacity and compliance. Each of these represents multi-year revenue opportunities.

Balance Sheet Strength Enables Strategic Flexibility Being almost debt-free in a capital-intensive industry provides enormous strategic flexibility. HONAUT can pursue aggressive growth investments, weather economic downturns, or return capital to shareholders as conditions warrant. This financial strength becomes particularly valuable during uncertainty—exactly when weaker competitors struggle.

The strong balance sheet also enables new business models. Performance-based contracts, where payment depends on efficiency improvements, require financial strength to bridge timing differences. Lease models for expensive equipment need balance sheet capacity. These emerging models favor financially strong incumbents.

Market Leadership with Deep Moats Despite competition, HONAUT maintains leadership in integrated automation solutions. This isn't just about market share—it's about the installed base creating switching costs, the service network providing rapid response, and decades of project experience reducing implementation risk. Honeywell Automation India Ltd is one of the best in its job of implementing automation & control systems. This helps it win prestigious large clients.

The reference customer list reads like a who's who of Indian industry. These relationships, built over decades, don't shift easily. When a refinery needs a new unit automated, they call the company that successfully automated their last three units. This incumbency advantage is under-appreciated by growth-focused investors.

Government Support Accelerating Adoption Make in India, Digital India, and PLI schemes create unprecedented policy support for automation. The government recognizes that manufacturing competitiveness requires world-class automation. This translates into accelerated depreciation benefits, subsidized financing, and sometimes direct purchase support. Policy tailwinds can overcome economic headwinds.

Furthermore, infrastructure spending—airports, metros, smart cities—directly drives automation demand. Government projects might have longer sales cycles but offer better payment certainty and larger contract sizes. HONAUT's track record with government projects positions it well for this opportunity.

Parent Company Transformation Unlocks Value Honeywell Automation will maintain global scale, with 2024 revenue of $18 billion. Honeywell Automation will connect assets, people and processes to power digital transformation, building on decades-long technology leadership positions, deep domain experience, and a vast installed base to serve a variety of high-growth verticals. The separation creates a focused automation pure-play with clearer strategy and dedicated resources.

For HONAUT, this means better technology access, more investment support, and clearer strategic direction. The parent company can now pursue automation-specific acquisitions, develop automation-focused technologies, and optimize for automation market dynamics without balancing aerospace or materials priorities.

The Synthesis: Beyond Binary Outcomes

The bear-bull debate often assumes binary outcomes—either HONAUT captures the growth opportunity and re-rates higher, or it fails and valuations compress. Reality will likely prove more nuanced. The company might succeed in maintaining market position and profitability without achieving explosive growth. It might benefit from parent company separation while facing increased competition. It might see certain verticals boom while others stagnate.

For investors, this suggests a barbell approach might be appropriate. The downside seems limited by asset value, market position, and balance sheet strength. The upside depends on execution, market dynamics, and strategic choices. At current valuations, the market prices in significant success—perhaps too much for conservative investors but possibly appropriate for those believing in India's automation imperative.

The critical variables to monitor aren't just financial metrics but strategic indicators: win rates in competitive bids, technology partnerships announced, new vertical penetration, and service revenue growth. These leading indicators will signal whether HONAUT successfully navigates its transformation well before financial statements confirm the outcome.

XI. Epilogue: The Next Chapter

As we stand at the threshold of 2025, Honeywell Automation India Limited finds itself at the most consequential inflection point in its four-decade journey. The company that began as a hesitant handshake between Indian industrial ambition and American technological capability now faces a future where it must define its own destiny as part of a soon-to-be-independent global automation giant.

The vision for 2030 isn't difficult to imagine, but achieving it requires navigating contradictions that define modern industrial businesses. HONAUT must be simultaneously global and local—leveraging worldwide R&D while solving uniquely Indian challenges. It must be both digital and physical—selling software and analytics while maintaining deep mechanical and process expertise. It must serve both the future and the present—enabling autonomous factories while supporting decades-old control systems that still run critical infrastructure.