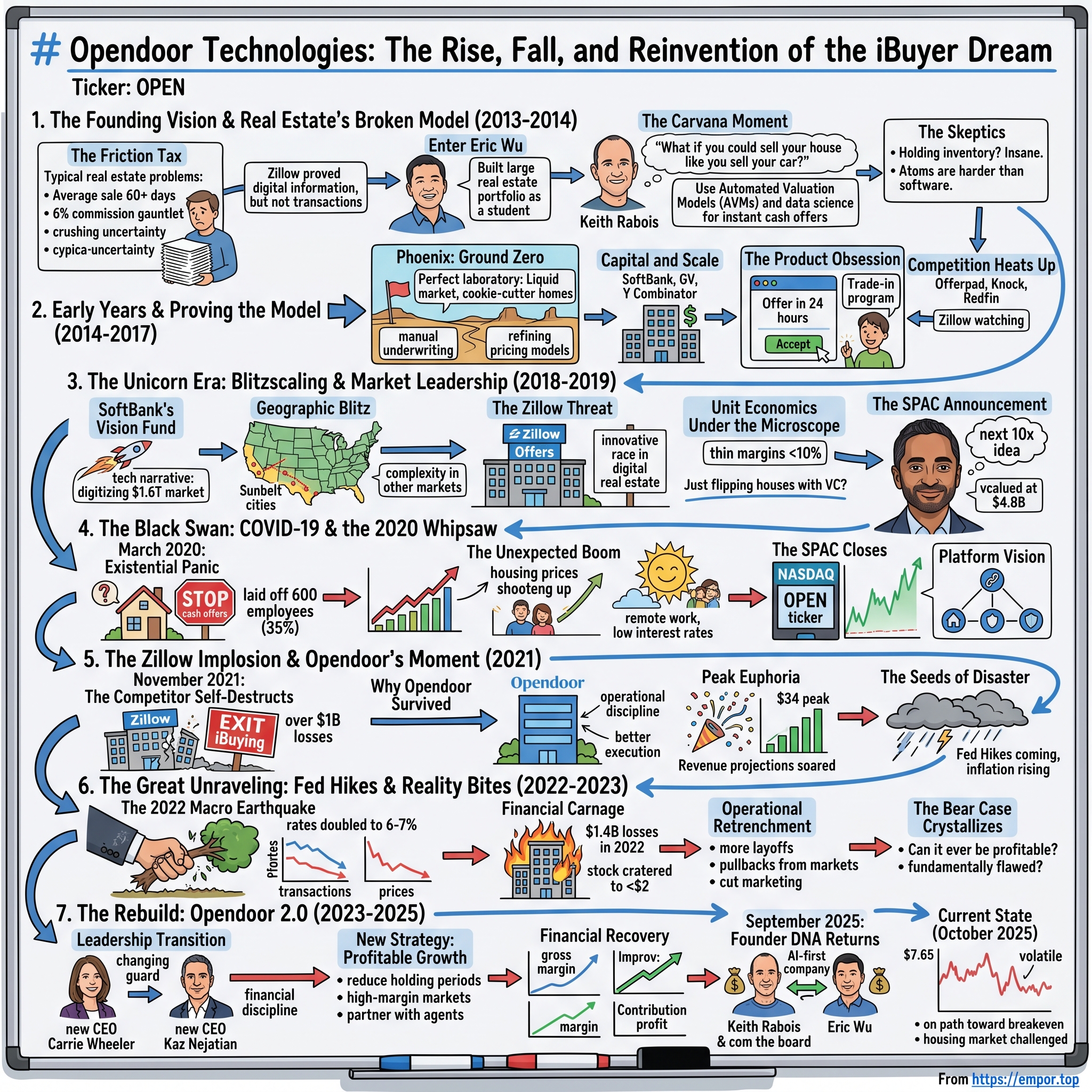

Opendoor Technologies: The Rise, Fall, and Reinvention of the iBuyer Dream

I. Introduction & Episode Roadmap

Picture this: You're standing in front of your house—the one where you've hosted Thanksgivings, watched your kids grow up, argued about paint colors. Now life's throwing you a curveball. New job. Divorce. Inheritance. You need to move. Fast.

The traditional path? Six months of hell. Staging. Open houses. Tire-kickers tracking mud through your living room. Negotiations with buyers who ghost you after inspection. Real estate agents taking 6% off the top. And the crushing uncertainty—will this even sell?

Then someone whispers: "What if you could sell your house like you sell your car?"

This is the story of Opendoor Technologies—the company that convinced Silicon Valley it could make real estate as liquid as stocks. Founded in March 2014 by serial entrepreneurs Keith Rabois, Eric Wu, Ian Wong, and JD Ross, Opendoor pioneered "iBuying"—algorithmically buying homes with a click, holding them for 90 days, and flipping them for profit.

The big question we're exploring: How did a Y Combinator startup persuade Wall Street to give it a $4.8 billion valuation, survive a near-death experience during COVID, watch its biggest competitor spectacularly implode, then lose $1.4 billion in a single year before clawing its way back from the brink?

This is a story about the limits of "software eating the world." About what happens when venture-backed tech models collide with the oldest, most illiquid asset class in America. About survival, reinvention, and whether convenience can ever justify the cost of certainty.

II. The Founding Vision & Real Estate's Broken Model (2013–2014)

The Friction Tax

In 2013, real estate was ripe for disruption—and everyone knew it. The average home sale took 60+ days, cost sellers 6% in commissions, and subjected them to a gauntlet of uncertainty. Would buyers get financing? Would inspection kill the deal? How long would you carry two mortgages?

Zillow had already proven you could digitize the information layer of real estate—the Zestimate made home values transparent. But Zillow didn't touch transactions. They sold ads to agents. The actual buying and selling? Still stuck in 1985.

Meanwhile, the on-demand economy was exploding. Uber let you summon a car with a tap. Airbnb turned spare bedrooms into hotels. The iPhone had trained consumers to expect instant gratification. So the question hanging in the air was obvious: Why couldn't you sell your house with the same ease you'd sell your car?

Enter Eric Wu

Eric Wu spent his college scholarship money building an impressive real estate portfolio that included roughly 25 properties by the time he graduated in 2005. The son of Taiwanese immigrants raised by a single mother in Glendale, Arizona after his father died when he was four, Wu understood real estate at a visceral level.

His startup Movity analyzed neighborhood data to help home-buyers decide where to live, launched out of Y Combinator in 2009, raised $1.3 million, and sold a year later to Trulia. At Trulia, Wu worked as head of geo-data and social products until 2013, watching the real estate industry's digital transformation from the inside.

But Wu had experienced firsthand the pain of selling a home traditionally. The friction. The uncertainty. The wasted time. There had to be a better way.

The Carvana Moment

Around 2013, fellow Y Combinator peer Keith Rabois raised the idea of Opendoor to Wu. Rabois, the former Khosla Ventures managing director who'd been part of the PayPal mafia, saw the opportunity clearly: "What if you could sell your house like you sell your car on Carvana?"

The insight was elegant. Carvana had cracked instant used-car buying by building pricing algorithms, taking on inventory risk, and offering convenience at scale. Cars depreciate, but they're also liquid—millions trade hands every year with relatively standardized pricing. Houses? Illiquid as hell. But maybe, just maybe, data science could solve that.

In 2014, Wu co-founded Opendoor with Ian Wong and Rabois. The vision: Use automated valuation models (AVMs), data science, and machine learning to make instant cash offers on homes. Buy them sight-unseen (or with minimal inspection). Hold for 60-90 days. Make light repairs. Resell. Capture the spread.

The value proposition to sellers: Trade 3-5% off market value for absolute certainty and zero hassle. No staging. No showings. No negotiations. Close on your timeline—as fast as two weeks.

The Skeptics

When Wu pitched this at Y Combinator, the reaction was predictable: "You're going to hold inventory? In real estate? That's insane."

Real estate isn't software. It's atoms. Physical assets that sit on balance sheets. Assets subject to local market dynamics, weather, contractor availability, and the whims of the Federal Reserve. Houses can't be shipped overnight or drop-shipped. They decay. They require maintenance. And if the market turns, you're stuck holding billions in depreciating inventory.

But Wu and Rabois had an answer: algorithmic home buying could work if you had enough data, moved fast enough, and operated at scale. The unit economics were thin—maybe 5-8% gross margin after fees, repairs, and holding costs—but paper-thin margins multiplied across thousands of transactions could build a massive business.

The target customer was clear: people in life transitions. Divorce. Job relocations. Inheritance. Death. The moments when speed and certainty matter more than squeezing out every last dollar.

III. Early Years & Proving the Model (2014–2017)

Phoenix: Ground Zero

The company launched in the Phoenix market and soon expanded to others. Why Phoenix? The perfect laboratory. Liquid market. Suburban sprawl meant cookie-cutter homes—easier for algorithms to price. Post-financial crisis, data was plentiful. And Phoenix's steady appreciation gave Opendoor a tailwind.

The first transactions were hardly the algorithmic marvel they'd eventually become. Early underwriting was manual, disguised as automated. Teams worked around the clock refining pricing models, learning which repairs moved homes faster, figuring out holding costs down to the dollar.

But the "we'll buy your home" guarantee worked. Sellers loved it. The certainty, the speed, the lack of weekend open houses—it felt like magic.

Capital and Scale

After raising a $9.95 million venture capital round led by Khosla Ventures in May 2014, the company began operations. But buying homes at scale requires more than equity—it demands debt. Lots of it.

Opendoor raised progressively larger rounds—GGV Capital, Andreessen Horowitz, and others betting big. Investors included SoftBank, GV, Uber founder Travis Kalanick, Reddit co-founder Alexis Ohanian, and Y Combinator president Sam Altman.

The company expanded methodically: Dallas, Las Vegas, Atlanta—all Sunbelt markets with similar characteristics to Phoenix. Each launch refined the playbook: automated pricing, centralized operations, standardized renovation processes.

By 2019, the company reported that the average time a property was held was 90 days. The faster they turned homes, the better the returns. Speed became everything.

The Product Obsession

Opendoor's product was deceptively simple: Submit your address online. Answer questions about condition. Get an offer in 24 hours. Accept it. Pick your close date. Done.

Behind the scenes, an army of data scientists, contractors, photographers, and local market experts made it work. Every transaction fed the algorithm. Every renovation taught them what buyers wanted. The flywheel was spinning.

They even added a trade-in program: Buy your next home through Opendoor while they buy your old one. It was the closest thing to CarMax for housing America had seen.

Competition Heats Up

Success breeds imitators. Offerpad launched in 2015. Knock entered the market. Others circled. And looming largest: Zillow, watching from the sidelines, studying Opendoor's every move.

But Opendoor had first-mover advantage, the deepest pockets, and the best algorithms. By 2017, they were the clear leader in iBuying—a term they'd essentially invented.

The dream was no longer theoretical. It was working.

IV. The Unicorn Era: Blitzscaling & Market Leadership (2018–2019)

The Capital Deluge

In 2018, Opendoor raised $400 million from the SoftBank Group Vision Fund. In 2019, it raised $300 million in a funding round led by General Atlantic. The 2019 round valued the company at a $3.5 billion pre-money valuation.

SoftBank's involvement signaled something important: Opendoor wasn't just a real estate company anymore. It was a technology company. A platform. The "AWS of real estate," as pitches claimed.

The narrative shifted from "home flipping with algorithms" to "digitizing the $1.6 trillion residential real estate market." Opendoor's target: capture 4% of U.S. home sales by 2024. That would mean tens of billions in revenue.

Geographic Blitz

By 2019, the company had bought and sold 50,000 houses in 23 cities across the U.S. That year alone, Opendoor was on pace to purchase $5 billion in homes.

But moving beyond Sunbelt markets introduced complexity. California's price volatility. Midwest seasonality. Northeast's older housing stock. Each market had unique dynamics. The algorithm that worked in Phoenix might fail in Philadelphia.

Still, Opendoor pressed forward. Each new market meant more data, more scale, theoretically better unit economics. The playbook was clear: blitzscale now, optimize later.

The Zillow Threat

In 2018, Zillow launched its own iBuyer: Zillow Offers. This changed everything.

Zillow had massive brand recognition—100 million monthly users searching for homes. They had deeper pockets. And they had legitimacy. When Zillow enters your market, it validates the business model. But it also brings existential competition.

Redfin also entered the space, fueling an innovation race in digital real estate. Suddenly, iBuying wasn't Opendoor's exclusive domain. It was an arms race.

The capital intensity became existential. To compete with Zillow's scale, Opendoor needed billions. Not just to buy homes, but to market, to hire, to expand faster than rivals.

Unit Economics Under the Microscope

Here's where things got uncomfortable. Opendoor's gross margin was under 10% for most quarters, and even during the 2020 boom it was only 15.4% in Q4 2020.

Critics asked the obvious question: "You're just flipping houses with venture capital, aren't you?"

The bull case depended on three assumptions: 1. Scale would drive efficiency and margin expansion 2. Adjacency services (mortgage, title, insurance) would boost take rates 3. The market was so massive that even thin margins at scale meant huge profits

But those were bets, not certainties. And the business was burning cash.

The SPAC Announcement

In September 2020, Chamath Palihapitiya's SPAC Social Capital Hedosophia II announced it would acquire Opendoor, valuing the company at $4.8 billion.

The deal provided Opendoor with $414 million from the SPAC's trust and a $600 million PIPE, with $100 million coming from Palihapitiya himself.

Chamath called it his "next 10x idea," comparing Opendoor's potential to Amazon or Tesla in their early days. The pitch: Opendoor wasn't a real estate company. It was a technology platform poised to transform a $1.6 trillion market.

Public markets beckoned. The unicorn was about to become a public company.

V. The Black Swan: COVID-19 & the 2020 Whipsaw (March–December 2020)

March 2020: Existential Panic

When COVID hit, Opendoor faced immediate catastrophe. The company stopped making cash offers on homes. Shelter-in-place orders froze the housing market overnight.

The nightmare scenario: Opendoor held roughly 4,000 homes worth approximately $1.5 billion. If home prices cratered like in 2008, the company would be insolvent.

In April 2020, the company laid off 600 employees—35% of its workforce. Laid-off employees received eight weeks of full pay and 16 weeks of health insurance reimbursement. CEO Eric Wu donated his 2020 salary to a relief fund for struggling employees.

In March, Opendoor announced they would suspend home buying during the COVID-19 pandemic out of concerns for the safety of their customers. The company that promised "instant liquidity" for homeowners had just shut down its core product.

Lenders pulled back. Liquidity crunched. Every day felt like it might be the last.

While Opendoor claimed it was well-capitalized, it wasn't healthy enough to avoid layoffs like arch-competitor Zillow, which outlined cost-cutting without layoffs. Opendoor's deep pockets allowed it to weather the storm albeit smaller, while Zillow's deeper pockets gave it a potential advantage in the recovery.

The Unexpected Boom

Then something miraculous happened. The company resumed operations in May 2020 by introducing a contact-free platform to help people buy and sell homes digitally.

And the housing market didn't crash—it exploded.

Remote work revolution. Ultra-low interest rates. Americans fleeing cities for suburbs. Suddenly everyone wanted a house. Bidding wars erupted. Prices soared.

Opendoor's inventory—the homes they'd been terrified would sink them—became gold. Properties appreciated rapidly. The $1.5 billion liability became an asset.

By summer 2020, Opendoor carefully restarted acquisitions. They'd learned to operate in chaos. The company that nearly died in March was printing money by July.

The SPAC Closes

On December 17, 2020, shareholders of Social Capital Hedosophia Holdings Corp II approved the merger. On December 21, 2020, the merger was finalized and the company began trading on the NASDAQ under the ticker OPEN.

The stock surged. From the ~$10 SPAC price, shares climbed past $30 by early 2021. Bulls proclaimed: "They survived COVID. Housing is booming. iBuying is inevitable."

Opendoor had over $1 billion cash on its balance sheet. A war chest to dominate.

Strategic Pivot: The Platform Vision

Survival changed the company. In August 2019, Opendoor had launched mortgage services through Opendoor Home Loans. In September 2019, it acquired national title and escrow company OS National.

The thesis evolved: Don't just flip homes. Become a platform. Attach mortgage, title, insurance. Earn fees across the entire transaction. Boost unit economics from 5% to 10%+ through adjacencies.

Opendoor was positioning itself not as a home flipper, but as the operating system for residential real estate. The tech narrative intensified.

VI. The Zillow Implosion & Opendoor's Moment (2021)

November 2021: The Competitor Self-Destructs

In November 2021, Zillow announced it was exiting its iBuyer business, Zillow Offers, after racking up over $1 billion in losses over 3.5 years.

The company disclosed it lost about $304 million in the third quarter from the program after purchasing homes at higher prices than it expected to sell them at. It bought 9,680 homes in Q3 but sold only 3,032.

CEO Rich Barton said "we've determined the unpredictability in forecasting home prices far exceeds what we anticipated and continuing to scale Zillow Offers would result in too much earnings and balance-sheet volatility".

What went wrong? Zillow Offers ended up buying a lot of houses and overpaying for many because they didn't see the market start to cool. It appears that Zillow's competitors Opendoor and Offerpad used AI models that detected the cooling housing market and reacted appropriately, pricing their offers more accurately.

Zillow's algorithm had failed spectacularly. The company purchased more homes in Q3 2021 than in the previous 18 months combined—at much higher prices than the competition.

CEO Rich Barton said "We just determined that being an iBuyer was too risky, too volatile and ultimately addressed too few customers".

Why Opendoor Survived When Zillow Failed

The difference came down to operational discipline. Opendoor had more conservative pricing models. Better execution. Local market managers who understood nuances algorithms might miss. They'd been in iBuying since 2014; Zillow launched Offers in late 2019. That experience mattered.

Earlier in 2021, when home price appreciation was at record highs and other iBuyers flirted with profitability, Zillow continued posting massive losses. While its peers managed incremental operational improvements over time, Zillow did not.

Peak Euphoria

Opendoor's stock hit over $34 per share in 2021 not long after its IPO, giving it a market cap north of $25 billion. Trading volume exploded. Retail investors piled in.

The narrative was irresistible: Opendoor survived COVID. Zillow validated iBuying by entering—then validated Opendoor by failing and exiting. Opendoor was the last iBuyer standing with real scale.

In 2021, the company bought 37,000 homes. Revenue projections soared—analysts talked about $50 billion+ by 2025. Comparisons to Carvana and Airbnb flew freely.

Redfin also entered the iBuying space but would later scale back, as would others, leaving the market consolidating around Opendoor and Offerpad.

The Seeds of Disaster

But beneath the euphoria, warning signs flickered. The Federal Reserve was hinting at rate hikes. Inflation was rising. The housing market's red-hot streak—the very thing that saved Opendoor in 2020—couldn't last forever.

And Opendoor's unit economics remained stubbornly thin. Even with home price appreciation gifting them gains, gross margins stayed below 10%. The business model still hadn't proven it could work in a flat or declining market.

That test was coming.

VII. The Great Unraveling: Fed Hikes & Reality Bites (2022–2023)

The 2022 Macro Earthquake

The Federal Reserve began raising rates aggressively in March 2022. Mortgage rates, which had been below 3%, doubled to 6% within months, then climbed to 7%.

The housing market seized. Transaction volumes collapsed. The lock-in effect emerged—homeowners with 3% mortgages refused to sell and refinance at 7%. Supply dried up. Buyers vanished.

For Opendoor, the nightmare scenario unfolded: They'd been buying homes at 3% rates, now had to sell into a 7% rate environment. Homes they bought in April 2022 for $420,900 were listing for $480,000 in May, but by January 2023 sold for only $346,000—a 17.8% loss.

Financial Carnage

In Q3 2022, Opendoor announced losses of $928 million. About 62%—$573 million—came from lowering home values in its inventory.

The company warned investors it expected to lose as much as $175 million in adjusted EBITDA in Q3. The losses didn't include fees or expenses from renovating and marketing, and had been mounting as the housing market declined.

Bloomberg research from YipitData found Opendoor lost money on 42% of its August 2022 transactions nationally. Real estate analyst Mike DelPrete said "Opendoor's metrics are in the danger zone. They are very close to where Zillow was in its worst moments".

Full year 2022: Opendoor reported a loss of $1.4 billion, after a loss of $662 million in 2021. Sales were $15.6 billion.

While revenues grew 94% to $15.6 billion in 2022, losses grew from $662 million in 2021 to $1.4 billion in 2022. Adjusted net loss climbed 394% from $116 million in 2021 to $574 million in 2022.

The stock cratered. From $30+, shares plunged below $2—a 94%+ decline. Ahead of its 2020 IPO, the company's market cap was around $18 billion. By early 2023 it was slightly above $1 billion.

Operational Retrenchment

In November 2022, Opendoor cut 18% of its workforce, or 550 jobs. This followed the 35% cut in 2020.

In April 2023, Opendoor laid off 560 employees—22% of the company—mainly hitting the operations unit. The company said new listings had dropped by around 30% since their 2022 peak due in part to rising mortgage interest rates.

The company pulled back from unprofitable markets. Slashed marketing spend. Tightened underwriting. The focus shifted from growth to survival.

Management acknowledged: "Fed action to raise target rates by 300 basis points in less than five months catalyzed the fastest shift in housing conditions in four decades. We constantly track conditions and adjust strategies, but we did not predict the speed of decline".

The Bear Case Crystallizes

Critics felt vindicated. iBuying doesn't work in volatile markets. You can't algorithmically underwrite risk in illiquid assets. This is just house flipping with fancy branding.

Existential questions emerged: Is the business model fundamentally flawed? Can Opendoor ever be profitable? How long can they survive burning cash?

The dream of making real estate as liquid as stocks felt further away than ever.

VIII. The Rebuild: Opendoor 2.0 (2023–2025)

Leadership Transition

In late 2022, co-founder Eric Wu stepped down as CEO. He was replaced by Carrie Wheeler, the former CFO, in early 2023.

On December 14, 2023, Wu announced he would step down from the company entirely, though remaining an advisor. He stated: "After ten years, I am called to get back to my startup roots and create and build again. I'm humbled by this accomplishment and grateful for all my teammates".

Wheeler, a CFO taking the reins in a crisis, signaled one thing: financial discipline. No more blitzscaling. The priority was survival, then profitability.

New Strategy: Profitable Growth

The playbook changed completely: - Prioritize unit economics over growth at all costs - Focus on high-margin, liquid markets - Reduce holding periods - Tighten pricing models - Boost take-rate services (mortgage attach rates, exclusivity fees)

By Q4 2023, Opendoor had 2,118 homes in inventory, down from 4,460 at the end of 2022. They were systematically clearing out the toxic inventory bought at peak prices.

Technology Refinement

The algorithms improved. Machine learning got better at detecting market shifts faster. Renovation workflows became more integrated—control costs, reduce cycle time.

Most importantly: Partner with agents, don't try to replace them. "We've always worked with, and wanted to work with, agents," said Tyler Hixson, head of real estate industry strategy. "They're repeat customers, so they're a really great ally".

Financial Recovery

Full year 2023: Revenue of $6.9 billion, down 55% versus 2022, with 18,708 homes sold, down 52%. Gross profit of $487 million versus $667 million in 2022; Gross Margin improved to 7.0% versus 4.3% in 2022.

Full year 2024: Revenue of $5.2 billion, down 26% versus 2023, with 13,593 homes sold, down 27%. Gross profit of $433 million versus $487 million in 2023; Gross Margin of 8.4% versus 7.0% in 2023.

The key shift: Contribution Profit improved drastically from $(258) million in 2023 to $242 million in 2024, highlighting substantial recovery in operational performance.

Adjusted Net Loss decreased from $(778) million in 2023 to $(258) million in 2024. Adjusted EBITDA improved from $(627) million in 2023 to $(142) million in 2024.

The company wasn't profitable yet, but the trajectory had reversed. They were losing less money on every transaction.

September 2025: Founder DNA Returns

In August 2025, CEO Carrie Wheeler resigned after activist investors drove up Opendoor's stock price, helping the company avoid Nasdaq delisting. Though Opendoor had reported its first quarter of adjusted EBITDA profitability since 2022, some investors questioned Wheeler's leadership.

On September 10, 2025, Opendoor announced Kaz Nejatian, Chief Operating Officer of Shopify, as its new CEO. Co-founders Keith Rabois and Eric Wu returned to the Board of Directors, with Rabois taking on the role of Chairman.

Khosla Ventures and Wu invested $40 million in equity capital through a private investment in the company.

Rabois said Nejatian "is a decisive leader who has driven product innovation at scale, ruthlessly reduced G&A expenses to drive profitability and deeply understands the potential for AI to radically reshape a company's entire operations. He is the right leader to unlock Opendoor's unique data and assets as we build on Opendoor's original mission, now enhanced as an AI-first company".

The founders were back. The AI-first positioning signaled a new chapter.

Current State (October 2025)

As of October 29, 2025, OPEN shares trade at $7.65, with a 52-week high of $10.87 and 52-week low of $0.508. The stock has been volatile—up 365% year-to-date according to some measures, though still 78% below its 2021 peak.

The stock hit $10.87 in September 2025 but has declined about 20% in the past month. Retail interest appears to be waning after a meme-stock surge earlier in the year.

The company remains unprofitable but is on a path toward breakeven. The housing market remains challenged—high mortgage rates continue suppressing transaction volumes.

IX. The Business Model Deep Dive & Playbook

How iBuying Actually Works

The customer-facing experience is simple: Submit your address online. Answer questions about your home. Get an offer in 24 hours. Accept it. Choose your close date.

Behind the scenes, complexity abounds.

Pricing Algorithms: Opendoor analyzes comparables, neighborhood data, macro trends. The algorithm factors in square footage, bedrooms, bathrooms, lot size, school district, days on market for similar homes. Machine learning refines predictions based on thousands of past transactions.

The tradeoff: Speed versus accuracy. A slower, more detailed appraisal might be more accurate. But speed is the product.

Holding Costs: Once Opendoor buys a home, the clock starts ticking. Mortgage interest, property taxes, insurance, utilities—roughly 1-2% of the home's value per month in carrying costs. Every extra day of ownership erodes margins.

Renovation: Opendoor makes standardized repairs designed to appeal to the broadest buyer base. Fresh paint. Minor fixes. Landscaping. Nothing fancy. The goal: speed and cost control, not maximizing value.

Resale: Price to move, not maximize margin. List it. Market it. Sell it fast. The longer it sits, the more it costs.

Unit Economics Breakdown

Target gross margin: 5-8% (comparable to the 6% traditional agent commission).

Revenue components: - Home sale price - Service fee charged to seller (typically 5%) - Ancillary services (title, escrow, maybe mortgage)

Cost components: - Home purchase price - Renovation (2-3% of value) - Holding costs (1-2% per month) - Transaction fees (1-2%) - Corporate overhead

The math is tight. A $300,000 home might generate $15,000 in service fee revenue, cost $9,000 in renovations and holding, $3,000 in transaction costs. That leaves maybe $3,000 in gross profit—1% gross margin.

Scale benefits help: lower cost of capital through warehouse lines, faster turns through better contractor networks, better pricing through more data.

Why It's Hard

Illiquidity: Houses aren't stocks. You can't exit instantly. If the market turns, you're stuck.

Local complexity: Every ZIP code is different. School district changes can swing prices 20%. A new highway announcement can tank a neighborhood overnight.

Macro sensitivity: Interest rates matter enormously. A 2-point rate increase can freeze the entire market.

Operational intensity: Physical assets require human touch. Contractors, photographers, local managers, customer service. This isn't a pure software play.

The Bull Case for iBuying

Convenience is valuable. Customers will pay for certainty. The market is $2 trillion annually—capturing even 1-2% is huge.

Technology creates moats. Better data. Better pricing models. Better operational excellence. Adjacency revenue can boost margins from 5% to 10%+ if you can sell mortgage, title, insurance.

Demographics favor this model. Millennials and Gen-Z expect digital-first, on-demand experiences. They're less loyal to traditional agents.

The winner-take-most dynamic: The iBuyer with the best data, most scale, and lowest cost of capital wins. Opendoor has survived when bigger, richer competitors failed.

The Bear Case

Structurally low margins. Physics matters—you can't escape the gravity of buying and holding physical assets. Even at scale, gross margins stay thin.

Catastrophic downside in downturns. 2022 proved this. When the market turns, the model breaks.

Limited competitive moat. Zillow tried and failed. But others could try again. The technology isn't defensible enough.

Market size illusion. Maybe only 1-2% of sellers actually want this product. Most people want to maximize value, not trade dollars for convenience. As of 2025, iBuyers account for less than 0.5% of home sales nationwide.

Better alternatives exist. Agent-light models. Flat-fee brokers. They offer savings without the inventory risk.

X. Competitive Landscape & Market Context

The iBuyer Wars

In 2024, Offerpad purchased fewer than 2,500 homes compared to nearly 15,000 homes acquired by Opendoor. Opendoor has the largest market share of 79%, while Offerpad makes up 20% of the iBuyer market.

Offerpad, founded in 2015, remains Opendoor's primary competitor. But both companies face similar headwinds: high interest rates, low transaction volumes, compressed margins.

For Q3 2025, Offerpad expects revenues between $130-150 million, down from $208.1 million a year ago. Homes sold are expected to be 360-410 units, down from 615 units.

Both companies are shifting strategies—Opendoor toward an agent-led multi-product platform, Offerpad toward asset-light services through its HomePro program.

Why Zillow Failed

Zillow's failure offers crucial lessons. CEO Rich Barton said Zillow's ultimate failure was its inability to predict housing prices accurately. The company realized it couldn't accurately forecast home prices six months out "within a narrow margin of error".

While other iBuyers slowed their pace and median prices, Zillow plowed full-speed ahead. The company purchased more homes in Q3 2021 than in the previous 18 months combined—at much higher prices than competition.

Operational chaos compounded algorithmic failures. Zillow couldn't coordinate contractors, couldn't turn inventory fast enough, couldn't adjust to market shifts.

The lesson: This business requires operational excellence, not just algorithmic sophistication.

Traditional Real Estate Response

Realtors fought back, emphasizing the human touch that algorithms can't replicate. Discount brokers like Redfin offered agent-assisted transactions at lower commissions.

About 90% of Opendoor buyers use agents, on par with the industry. But fewer than 10% of sellers are agent-represented thanks to Opendoor's ease.

iBuying proved complementary, not replacement. It serves a specific segment—people who value convenience and certainty over maximizing price. For complex transactions, luxury homes, or sellers wanting to squeeze out every dollar, traditional agents remain relevant.

XI. Analysis: Bull vs. Bear Case Today

The Bull Case (October 2025)

Survival = Positioning Advantage. Opendoor survived when Zillow didn't. Redfin retreated. Others exited. Being the last iBuyer standing with scale matters.

Improving Unit Economics. Contribution Profit swung from negative $258 million in 2023 to positive $242 million in 2024. Gross margins have improved from negative levels in 2022 to around 5-6% in 2024, driven by better pricing algorithms and shorter holding periods.

The path to profitability is visible. The company is losing less money each quarter.

Housing Market Will Normalize. The lock-in effect won't last forever. Eventually, mortgage rates will stabilize. Life events—divorce, death, job changes—will force transactions. When the market thaws, Opendoor is positioned to benefit.

Valuable Optionality. Opendoor sits on proprietary data, brand recognition, and operational infrastructure that took a decade to build. That's worth something, even if current financials are weak.

Long-term TAM. In 2023 alone, more than four million existing homes were sold, representing approximately $1.6 trillion in transactions. Capturing 1-2% of that market means $16-32 billion in revenue potential.

Deeply Discounted Stock. Trading at $7-8 per share versus a $34 peak, the stock prices in significant pessimism. Asymmetric upside if the model works.

The Bear Case (October 2025)

Fundamentally Unprofitable Model. Opendoor has incurred net losses on an annual basis since founding. Net losses of $275 million, $1.4 billion, and $662 million for 2023, 2022, and 2021 respectively. The company has a cumulative net deficit of $3.2 billion since founding. A company that will never generate a profit is worth less than zero.

Next Downturn Could Be Fatal. Balance sheet remains fragile. Over 90% of Opendoor's $8 billion borrowing capacity extends through 2026, but accessing that capital depends on market conditions. Another 2022-style downturn could be existential.

Limited Moat. The technology isn't defensible. Others have tried and could try again. Zillow failed due to execution, not because iBuying is impossible.

Market May Never Be Big Enough. If iBuyers only appeal to 0.5% of sellers, the addressable market is tiny. You're fighting over scraps.

Dilution Risk. The company granted new CEO Kaz Nejatian massive equity awards including 1,580,611 RSU shares and two performance-based awards each relating to 40,886,344 shares. Existing shareholders get diluted.

Competitors Fragment Market. Even if Offerpad is smaller, they still compete for the same narrow slice of sellers, fragmenting an already small market.

Key Risks

Interest Rates Stay Elevated. If the Fed keeps rates high through 2026, housing remains frozen. Low transaction volumes strangle iBuyers.

Recession Triggers Price Declines. Opendoor holds billions in inventory. Even a modest 5-10% price decline across that inventory wipes out equity.

Regulatory Challenges. Realtor lobbying. State-level restrictions on iBuying. The FTC already fined Opendoor $62 million in August 2022 over charges of misleading home sellers in marketing campaigns.

Technology Failures. Algorithm mispricing at scale. One bad quarter of acquisitions can take years to work through.

Key Opportunities

Housing Market Thaw. When rates stabilize and lock-in effect fades, transaction volumes recover. Opendoor is positioned to capture that rebound.

Financial Services Revenue. Opendoor's Title & Escrow has an 83% attach rate adding $1,500 or 0.6% to contribution margin. They've identified home loans, buy/list services, home warranty, remodeling, insurance, and moving services as opportunities. In all, they estimate juicing another 8% or $20,000 of contribution margin from these services.

B2B Pivot. Power buying for builders, institutional buyers. Lower marketing costs, more predictable volumes.

XII. Epilogue: Lessons & The Road Ahead

What We Learned About Disrupting Real Estate

"Software Eats the World" Has Limits. Marc Andreessen's famous maxim meets its match in physical assets. Atoms are hard. Software can optimize operations, improve pricing, streamline processes. But it can't eliminate the fundamental capital intensity and market risk of owning homes.

Convenience is Valuable But Has a Price Ceiling. Sellers will pay for certainty and speed—but only up to a point. Most people will sacrifice convenience to capture an extra $20,000 in home value.

Timing and Macro Matter More Than Tech. Opendoor's near-death in March 2020 and resurrection by July had nothing to do with technology improvements. The Federal Reserve mattered more than the algorithm. iBuying is a levered bet on housing markets, dressed up as technology.

Survival Matters. Opendoor outlasted Zillow not because their technology was dramatically superior, but because they executed better operationally and managed risk more conservatively. In shakeouts, staying power wins.

Lessons for Founders

Capital Intensity Creates Fragility. Asset-heavy businesses require massive amounts of capital. When markets turn, that capital evaporates. Plan for downturns, not just upside.

Unit Economics Must Work at Scale. You can't grow your way out of negative unit economics. Opendoor's margins remain thin even after a decade of optimization. If the math doesn't work at small scale, scale probably won't fix it.

Operational Excellence Matters as Much as Algorithms. Zillow had better algorithms (debatable) and more brand recognition. They failed because they couldn't execute operationally—couldn't coordinate contractors, couldn't turn inventory fast. Technology is necessary but not sufficient.

Market Timing and Luck Are Underrated. Opendoor nearly died in March 2020. They survived because of luck—COVID triggered a housing boom, not bust. Don't discount the role of fortune.

Lessons for Investors

Beware "Technology Company" Narratives on Asset-Heavy Businesses. Opendoor is a real estate company that uses technology, not a technology company that happens to touch real estate. Valuing it like a SaaS business was investor malpractice.

Cyclical Businesses Deserve Cyclical Valuations. Housing is cyclical. iBuying is cyclical squared. Paying 20x revenue at peak cycle was irrational. The stock got properly repriced in 2022.

Disruption Doesn't Mean Winner-Take-All. Just because you're disrupting an industry doesn't mean you capture all value. iBuying might be a niche product serving 1% of sellers. That's fine—but value it accordingly.

Sometimes the Best Outcome is Survival, Not Dominance. Opendoor won't dominate residential real estate. But surviving as a profitable niche player serving specific customer segments might be enough to justify today's valuation.

What's Next for Opendoor?

2025-2026: The Profitability Test. Can they reach sustained profitability? CEO Carrie Wheeler and now CEO Kaz Nejatian have emphasized focusing on reaching sustained profitability in the coming years. Management expects to significantly reduce adjusted net losses in 2025 relative to 2024, and the volume/revenue needed for breakeven is significantly lower than prior frameworks.

Strategic Options. Stay independent? Merge with Offerpad for cost synergies? Get acquired by a financial services company for distribution? All are on the table.

Long-term: 10% of Market or Niche Player? The bull case requires iBuying to reach 5-10% market share. The bear case says it stays below 1%. Which materializes determines whether Opendoor becomes a $10 billion company or struggles to survive.

The AI-first positioning under new CEO Kaz Nejatian signals renewed ambition. Whether AI can truly transform iBuying's economics remains to be seen.

Final Reflection

Opendoor pioneered something genuinely new—instant home liquidity. The idea of selling your house with a click wasn't crazy. It was visionary.

The execution? More complicated. Opendoor proved the model could work in narrow circumstances—stable markets, modest appreciation, specific property types, specific seller segments. But scaling it to dominate residential real estate proved much harder than anyone imagined.

The dream was bigger than reality. Selling your house will never be as easy as selling your car, because houses aren't cars. They're illiquid, heterogeneous, emotionally charged, locally complex assets.

But Opendoor did change real estate. They forced the industry to modernize. They proved convenience has value. They survived competitors with deeper pockets and bigger brands.

This story isn't over. This is halftime, not the end.

Whether Opendoor becomes a profitable niche player or a cautionary tale about the limits of software disruption remains to be determined. The next 12-24 months will tell us which ending we get.

For investors seeking exposure to PropTech innovation without the volatility of Opendoor, the lesson is clear: Disruption is real, but so is execution risk. The best opportunities often lie in picks-and-shovels plays—the companies selling tools to the disruptors—rather than the disruptors themselves.

Watch the housing market. Watch interest rates. And watch whether Opendoor can finally prove that algorithmic home buying works not just in theory, but in practice across full market cycles.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube