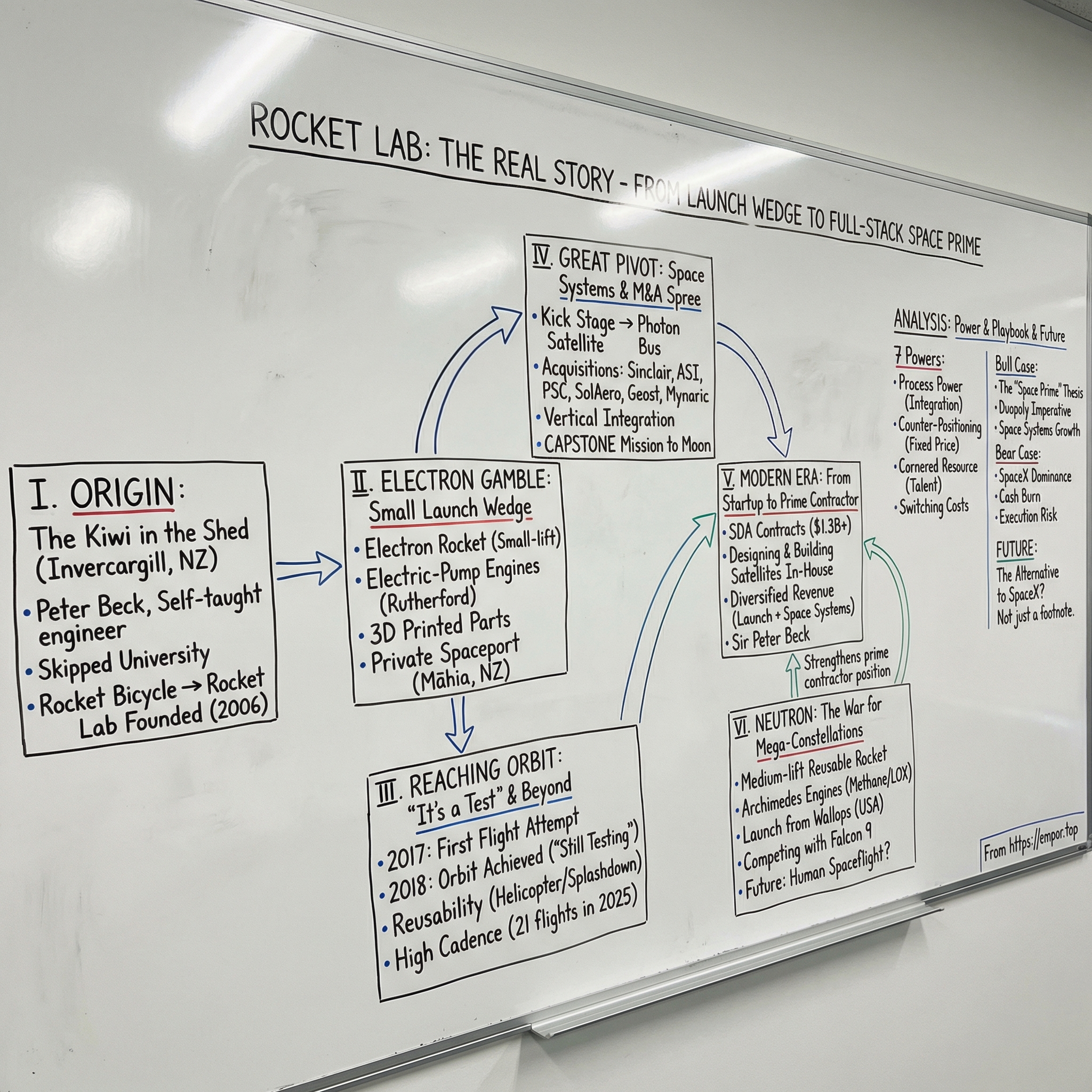

Rocket Lab: Building the Next-Generation Space Prime

I. Introduction & Episode Roadmap [00:00 - 00:12] (12 Mins)

On the morning of June 29, 2026, a company that had spent two decades defining itself as a rocket manufacturer announced an acquisition akin to buying a telecommunications carrier.

While not literally a consumer phone operator, the target was close enough to surprise observers who thought they understood Rocket Lab. Iridium Communications, operator of a 66-satellite low Earth orbit constellation, holder of globally licensed L-band spectrum, and connectivity provider to roughly 2.55 million subscribers across maritime, aviation, defense, and consumer safety markets, agreed to be acquired for about $8.0 billion in enterprise value.12 Rocket Lab shareholders had spent five years underwriting a strategy centered on launch vehicles and satellite buses. They awoke to a transaction that positions satellite services—recurring subscription revenue with a 57% EBITDA margin—as the largest single profit pool in the combined business.2

The market's initial reaction was euphoria: Rocket Lab shares surged roughly 16% on the day, while Iridium's jumped about 25%.3 The subsequent reaction was far harsher. By the end of July 2026, Rocket Lab stock had declined to around $64, falling roughly 58% from its 52-week high of $151 and bringing its market capitalization to near $39 billion. That drawdown coincided with investors digesting the capital structure required for the deal, including a $3.6 billion bridge loan and a still-unfunded equity component, alongside the pending maiden launch of an unproven rocket scheduled for the back half of the same year.4

A broader industry shift also influenced trading. On June 12, 2026, SpaceX completed its initial public offering on the Nasdaq, pricing at $135 a share, raising $75 billion in the largest IPO in Wall Street history, and closing its debut session at $161 for a market capitalization above $2 trillion.5 For five years, public-market investors seeking commercial space exposure had a short list, with Rocket Lab positioned near the top. The arrival of a massive, liquid direct peer reshapes where institutional capital resides, regardless of Rocket Lab's execution. Rocket Lab's addition to the Nasdaq-100 index effective June 22, 2026, and the associated passive index buying, failed to offset the capital rotation.6 Determining how much of the stock's decline reflects transaction skepticism, how much stems from Neutron schedule uncertainty, and how much represents a sector re-weighting around a new mega-cap benchmark is a central analytical challenge.

That operational and financial balance defines the enterprise. Rocket Lab Corporation—the holding company that succeeded Rocket Lab USA, Inc. in a corporate reorganization effective May 23, 2025, and trades on the Nasdaq under ticker RKLB—has executed one of the most ambitious industrial roll-ups in modern aerospace.7 Yet on a trailing financial basis, it remains unprofitable, reporting full-year 2025 revenue of $601.8 million against a net loss of $198.2 million.[^8]

The core thesis worth testing. The prevailing retail framing positions Rocket Lab as merely "the other launch company" operating in SpaceX's wake. That framing is outdated. In the first quarter of 2026, Rocket Lab generated $200.3 million of revenue, of which $136.6 million—roughly 68%—came from Space Systems, the segment building satellites, solar cells, star trackers, separation systems, flight software, infrared missile-warning payloads, and laser communications terminals.8 Launch, the business commanding most public attention, contributed $63.7 million.8 Furthermore, Rocket Lab's largest single contract is not a launch award, but an $816 million prime contract from the U.S. Space Development Agency to design and build 18 missile-tracking satellites.9

Consequently, the essential questions surrounding the company extend beyond simple comparisons with SpaceX:

- How did a self-taught toolmaker from New Zealand's South Island build the only Western enterprise besides SpaceX delivering routine, commercial orbital access—and what does that track record reveal about future operational execution?

- Was the company's early acquisition strategy from 2020 to 2023 a source of durable structural advantage, or primarily capital deployment into distressed assets during a low-interest-rate environment—and does that same financial discipline translate to transaction scales of $275 million, and now $8 billion?

- Can Neutron, a partially reusable medium-lift rocket yet to fly, avoid the high historical failure rates associated with maiden orbital launch vehicles, and how would schedule slippage impact the equity valuation?

- Is Rocket Lab successfully compounding a vertically integrated operational advantage, or is it accumulating balance-sheet leverage and execution complexity faster than verifiable returns?

These questions lack simple answers. The primary evidence follows.

II. The Genesis: Peter Beck & The New Zealand Roots (2006–2013) [00:12 - 00:27] (15 Mins)

Invercargill sits near the southern tip of New Zealand's South Island, closer to Antarctica than to the centers of the global aerospace industry. A town of roughly 50,000 people known for oysters, coastal winds, and a motorcycle museum, it was an unlikely setting for a ten-year-old to decide to build orbital rockets.

Peter Beck grew up there as the son of a museum director and a teacher in a household where the workshop was a central part of daily life. Rather than attending university, he completed a toolmaking apprenticeship at Fisher & Paykel, the New Zealand appliance manufacturer. Learning manufacturing on a lathe rather than aerospace engineering in a lecture theater established a practical foundation that became central to Rocket Lab's culture: the primary engineering question was rarely whether a component could be designed, but whether it could be produced repeatedly and economically in-house. Machining propulsion hardware builds a different operational instinct than simulating it.

Beck spent his twenties building rocket motors independently before working at Industrial Research Ltd, a New Zealand government research institute. A trip to the United States clarified the market gap he intended to fill. In 2006, he founded Rocket Lab in Auckland with seed backing from Mark Rocket, a New Zealand internet entrepreneur.

Atea-1 and the first proof point

The company established its initial credibility on November 30, 2009, launching Atea-1, a suborbital sounding rocket, from Great Mercury Island. Reaching space, Rocket Lab became, by its own account and contemporary reporting, the first private company in the Southern Hemisphere to do so.[^11]

Although small, carrying minimal payload, and unrecovered, Atea-1 served an essential strategic function: it converted Beck from an enthusiast into a founder with a demonstrated flight record. In an industry where customer and investor trust presents a major barrier to entry, that flight validation proved crucial. Every subsequent capital raise relied on the fact that the team had put a vehicle above the Kármán line on a fraction of a standard aerospace campaign budget.

The insight: taxis, not buses

Rocket Lab's strategic pivot stemmed from analyzing satellite market trends rather than traditional launch dynamics.

Throughout the 2000s and early 2010s, satellite components shrank rapidly. Sensors, radios, processors, and reaction control systems that previously required a satellite bus the size of a delivery van scaled down to fit within filing cabinets or small CubeSat modules. Suddenly, universities, startups, and government agencies could construct functional spacecraft for a few million dollars.

However, orbital deployment remained a structural bottleneck. Small satellites flew primarily as secondary payloads on heavy rockets, tying launch timing and orbital destination to the primary customer's schedule. Smallsat operators often waited up to two years for a launch slot, only to be dropped into orbits offset by 15 degrees or more from their target inclinations. Beck framed the issue through an intuitive analogy: the launch industry offered a city bus when customers needed a taxi. The bus offered lower costs per passenger, but the taxi delivered specific payloads to exact orbits on demand.

That framing dictated the company's design strategy. A dedicated small-satellite launcher could succeed only if unit costs remained low enough for a single customer and launch cadence proved dependable. Those twin requirements—cost per unit and frequency—shaped the architecture of the Electron rocket.

Moving the company to America without moving the factory

In 2013, Rocket Lab restructured as a U.S. entity, establishing its corporate home in Huntington Beach, California, while keeping engineering, manufacturing, and testing operations in New Zealand. The rationale was practical: U.S. defense and intelligence agencies rarely procure launch services from foreign entities, and U.S. venture capital firms strongly prefer domestic corporate structures.

Capital followed the reorganization. Khosla Ventures led early institutional funding, Bessemer Venture Partners joined subsequent rounds, and defense prime Lockheed Martin took a strategic equity position. A major defense contractor investing in a New Zealand startup with a single suborbital flight served as strong market validation for the small-launch thesis.

The dual-nation structure established in 2013 remains a key operational asset. Controlling a private, sovereign launch site in New Zealand allowed Rocket Lab to bypass the scheduling bottlenecks of crowded U.S. government ranges like Cape Canaveral. Over the subsequent decade, the company set out to demonstrate that an unknown startup from a country without a legacy aerospace sector could execute orbital launches on a reliable schedule.

III. The Electron Revolution & Small-Lift Market Validation (2013–2020) [00:27 - 00:47] (20 Mins)

The engineering challenge of small-lift launch is that physics does not scale down linearly.

A traditional rocket engine turbopump—the machinery forcing propellant into the combustion chamber under extreme pressure—is driven by a gas generator, a small pre-burner that consumes a fraction of the propellant to spin a turbine. While highly effective at large scale, gas generators introduce immense complexity into small engines, where plumbing, valves, and startup sequencing fail to shrink proportionally. The result is an engine dominated by mechanical complexity.

Rutherford: batteries in a rocket engine

Rocket Lab's solution was to eliminate the gas generator entirely. Its Rutherford engine uses electric motors—brushless DC motors powered by lithium-polymer batteries—to drive the turbopumps. Rather than using a high-pressure pre-burner, Rutherford powers its fuel pumps electrically, operating much like high-output electric motors driving propellant into the combustion chamber.

The design involves a clear engineering trade-off. Batteries are heavy and remain onboard throughout ascent, spending a portion of the rocket's performance carrying the power source for its own pumps. In exchange, the system yields mechanical simplicity, precise throttle response, and superior manufacturability. Rutherford's primary components are 3D-printed, dramatically reducing part counts and production lead times. By printing engines rather than machining and hand-assembling thousands of individual parts, Rocket Lab produced propulsion systems at rate on a modest budget.

The vehicle's airframe represented a second structural choice. Electron, standing roughly 18 meters tall, is constructed from carbon composite rather than the aluminum-lithium alloys common in launch structures. Carbon composite provides high strength for its weight—a crucial advantage for a small vehicle where dry mass directly reduces payload capacity. However, composite manufacturing demands strict quality control, introducing production challenges that would reemerge years later during the development of larger vehicles.

Māhia: the launch site nobody else could have

In 2016, Rocket Lab opened Launch Complex 1 on the Māhia Peninsula on the east coast of New Zealand's North Island, establishing the world's first private orbital launch site.

Much of Rocket Lab's subsequent operational record stems from this location. U.S. commercial launch providers typically operate on federal ranges, sharing airspace, radar infrastructure, and range-safety personnel with national security missions that hold priority. Range scheduling creates chronic bottlenecks. By contrast, Māhia sits on remote farmland surrounded by sparse air and maritime traffic, operating under bespoke space legislation enacted by the New Zealand government. Control over the pad, range, and calendar gave Rocket Lab a distinct operational footprint.

This control functioned as a strategic counter-positioning advantage that traditional launch providers could not easily duplicate without departing federal range structures. It also established the baseline credibility of Rocket Lab's launch cadence commitments.

Three flights that defined the company

May 2017 — "It's a Test." The initial Electron flight reached space but failed to attain orbit. An investigation traced the issue not to the rocket itself, but to misconfigured ground contractor telemetry equipment that prompted range safety officers to terminate an otherwise nominal flight. The finding exonerated the launch vehicle's core architecture.

January 2018 — "Still Testing." Electron reached orbit and deployed its payloads on its second attempt, achieving orbital capability faster than most legacy development programs.

November 2018 — "It's Business Time." The company completed its first fully commercial operational flight, transitioning Electron from a developmental vehicle into a commercial product.

The graveyard around them

Electron's operational record is best measured against peer ventures targeting the same market segment.

Virgin Orbit spent over $1 billion developing air-launch capabilities from a modified Boeing 747 before filing for bankruptcy in 2023 after failing to establish operational cadence or reliability. Astra Space reached orbit but suffered repeated launch failures and was taken private following a steep equity decline. Relativity Space flew its 3D-printed Terran 1 rocket once before abandoning the vehicle class to pursue a larger launcher. Firefly Aerospace reached orbit but struggled for years to maintain a consistent launch schedule.

Rocket Lab succeeded where peers stumbled by prioritizing manufacturing rate and launch cadence over technological novelty. Printed engines, composite airframes designed for repeatable tooling, and a dedicated private range were all decisions engineered for cadence. The company ended 2025 having flown 21 missions in a single year with a 100% mission success rate, and closed the year with its 79th Electron flight overall.10

That operational record—79 flights for a launcher once viewed skeptically by industry observers—forms the empirical foundation of Rocket Lab's execution track record. Yet by 2020, Beck had recognized a broader strategic reality: small-sat launch alone was insufficient to build an enduring, large-scale aerospace enterprise.

IV. Capital Deployment & The M&A Playbook: Building Space Systems (2020–2023) [00:47 - 01:12] (25 Mins)

The realization that reframed Rocket Lab’s strategy was rooted in basic economics: global orbital launch represents roughly a $10 billion annual market, while the satellites, ground systems, applications, and services operating above it form a market an order of magnitude larger. Remaining exclusively a launch provider meant selling the lowest-margin component of any mission—the taxi fare rather than the overall journey. Furthermore, launch revenues are inherently volatile, capital-intensive, and exposed to pricing pressure from SpaceX.

Beginning in 2020, Chief Executive Peter Beck initiated an aggressive acquisition strategy. Rocket Lab's capital allocation track record splits cleanly into two distinct phases.

Era one: buying bottlenecks cheaply (2020–2023)

Sinclair Interplanetary (2020). Rocket Lab announced the acquisition of Toronto-based satellite component manufacturer Sinclair Interplanetary in March 2020 and closed the transaction in April.11 The financial terms were modest, totaling roughly $12.3 million in cash according to a subsequent registration statement.12 The deal gave Rocket Lab control over essential reaction wheels and star trackers—the precision hardware that orients spacecraft in orbit. Sinclair was a critical supplier across the small-satellite sector, allowing Rocket Lab to capture a high-margin component business that served its own competitors.

Advanced Solutions, Inc. (2021). Rocket Lab acquired Colorado-based Advanced Solutions for $40 million, bringing flight software, simulation tools, and guidance, navigation, and control systems in-house.13 Flight software represents a critical operational dependency and a common source of program delays; acquiring Advanced Solutions eliminated an external bottleneck while adding software capabilities Rocket Lab could commercialize independently.

Planetary Systems Corporation (2021). Rocket Lab acquired Planetary Systems Corporation in a cash-and-stock transaction detailed alongside its other 2021 acquisitions in regulatory filings.12 The company produced separation mechanisms and dispensers—hardware responsible for deploying satellites into orbit cleanly without imparting unwanted rotation.

SolAero Technologies (2022). Closed for $80 million in cash in January 2022, SolAero represented the most strategically significant early transaction.[^16] Based in Albuquerque, SolAero was one of only two domestic manufacturers of high-efficiency, space-grade solar cells. Rocket Lab executed the acquisition during pandemic-era supply chain disruptions, when solar array shortages caused widespread satellite schedule slippage, acquiring a critical industry bottleneck at roughly twice annual revenue. The federal government later supported an expansion of SolAero’s facilities through CHIPS Act funding to boost domestic space solar cell manufacturing.14

Virgin Orbit assets (2023). At a May 2023 bankruptcy auction, Rocket Lab secured Virgin Orbit’s 140,000-square-foot Long Beach manufacturing facility, including high-capacity 3D printers, CNC machinery, and specialized tooling, for $16.1 million.15 The purchase price represented a small fraction of the equipment's replacement value, and the site was repurposed as the primary production facility for the medium-lift Archimedes engine.

Evaluating the initial M&A strategy. Rocket Lab's early acquisitions focused on established, revenue-generating component makers occupying key supply chain positions during a period of depressed valuations across commercial space. Each transaction either secured an essential internal input or expanded external product offerings. Unlike SPAC-era peers that purchased pre-revenue concepts at inflated valuations, Rocket Lab prioritized operational track records and attractive entry prices. However, integrating small, accretive component suppliers presents fewer operational risks than managing larger, more complex enterprises—a distinction that became relevant as deal sizes expanded.

Era two: buying capability at scale (2025–2026)

Geost (2025). Announced in May 2025 and finalized later that year, Rocket Lab acquired Geost for $275 million before adjustments, structured as roughly $125 million in cash and about 3.06 million shares.16 Geost manufactures electro-optical and infrared payloads for missile warning and defense tracking. The transaction marked a shift from basic satellite bus manufacturing to complete mission payload integration.

Mynaric (2026). Rocket Lab signaled intent to acquire German optical communications specialist Mynaric in March 2025, navigating a corporate restructuring process completed in August 2025 before closing the acquisition on April 14, 2026, for an aggregate consideration of $155.3 million—a nominal cash payment plus roughly 2.28 million shares.1718 Mynaric produced laser communication terminals critical for interconnected defense satellite constellations, providing Rocket Lab with both key optical technology and a European operational presence.

Motiv Space Systems (2026). In May 2026, alongside its first-quarter financial results, Rocket Lab announced a definitive agreement to acquire Motiv Space Systems, a robotics and precision-mechanisms firm whose engineering lineage includes the robotic arm on NASA’s Mars Perseverance rover.8

On Rocket Lab's first-quarter 2026 earnings call, Beck framed the acquisition series in operational terms, noting that the deals were driven by past supplier delays and cost overruns, and stating that all acquired technologies were "already being built into our platforms or supplied to others."8 That claim finds support in the company's contracting results: Chief Financial Officer Adam Spice attributed Rocket Lab’s $816 million Space Development Agency Tranche 3 award in part to vertical integration, which produced a superior financial profile compared to non-integrated competitors.8

The Iridium deal: a different kind of transaction entirely

On June 29, 2026, Rocket Lab agreed to acquire Iridium Communications for $54.00 per share—consisting of $27.00 in cash plus Rocket Lab stock governed by an exchange ratio collar between $67.50 and $112.50—implying an enterprise value of approximately $8.0 billion and a 24% premium over Iridium's prior closing price.12 Deutsche Bank and Wells Fargo committed a $3.6 billion 364-day senior secured bridge term loan facility, with the remainder of the cash funding expected from balance sheet cash, additional debt, and new equity.2 Closing is expected in mid-2027, subject to approval by Iridium shareholders and regulatory clearance.2

The strategic rationale is clear: acquiring an active satellite constellation with licensed global spectrum offers a "shortcut" around the years required to secure orbital spectrum and deploy a network.1 In 2025, Iridium generated $871.7 million in revenue and roughly $495 million in operational EBITDA—a 57% margin—across approximately 2.55 million subscribers.2 Under Rocket Lab’s ownership, future replacement satellites would be manufactured and launched in-house, capturing margins previously paid to third-party providers like SpaceX.

However, market skepticism centers on the combined execution and financial risks. Investors are evaluating multiple concurrent challenges: the maiden flight of the unproven Neutron rocket, the integration of four acquisitions within an eighteen-month window, the execution of two large fixed-price defense contracts, and the absorption of a leveraged acquisition roughly ten times Rocket Lab's trailing annual revenue in a mobile satellite service sector with lower growth rates than its core business. The financing requirements present tangible balance-sheet risks: the equity portion remains unraised, and the $3.6 billion bridge loan is a short-term 364-day facility that must be refinanced.24

A broader question remains regarding capital discipline. Rocket Lab’s initial 2020 to 2023 playbook relied on purchasing distressed component suppliers at modest valuations. In contrast, acquiring Iridium involves buying a mature, publicly traded satellite operator at a premium using significant debt leverage. Managing large-scale corporate integration and debt servicing represents a fundamentally different operational task, leaving Rocket Lab’s expanded acquisition strategy without a historical precedent in its execution record.

V. The De-SPAC, Eating the Hat, & The Medium-Lift Gambit: Neutron (2021–Present) [01:12 - 01:37] (25 Mins)

Before any of this could be funded, Rocket Lab had to become a public company — and it chose the most 2021 way imaginable to do it.

$777 million and a blank-cheque sponsor

In August 2021, Rocket Lab completed a merger with Vector Acquisition Corporation, a special purpose acquisition company sponsored by Vector Capital's Alex Slusky, raising gross proceeds of approximately $777 million at an enterprise valuation near $4.1 billion.19

De-SPACs from that vintage have a deservedly poor reputation, and it is worth being precise about why Rocket Lab's has aged better than most. The typical 2021 space SPAC monetised a projection: a hockey-stick revenue forecast for a product that did not exist and customers who had not signed. Rocket Lab went public with an operating launch business, real revenue, and a specific, disclosed use of proceeds. It also, like every one of its peers, missed its original projections badly on launch cadence — a fact management has never disputed and which is visible in the gap between the de-SPAC forecast and what actually happened. What differentiated Rocket Lab was that the shortfall was substantially offset by a business line the original model barely contemplated: Space Systems, grown largely through the acquisitions described above.

That is an important nuance for judging management. Rocket Lab did not hit its plan. It hit a different, larger number by changing the plan — which is better than missing, and worse than delivering what was promised.

The blender

On March 1, 2021, alongside the announcement of the SPAC merger and the Neutron programme, Beck released a video in which he put a Rocket Lab cap into a kitchen blender, pulverised it, and ate a spoonful of the result.

The context: for years, Beck had publicly and repeatedly insisted Rocket Lab would never build a reusable rocket and never build a larger vehicle, arguing that small launch demanded absolute focus. Enough people had thrown the quotes back at him that he had promised to eat his hat if he ever reversed.

It is easy to dismiss this as a marketing stunt, and it partly was. But it functioned as something more useful: an unusually legible act of public accountability from a founder-CEO, at a moment when the company was asking public shareholders to fund a strategy reversal. The cost of admitting error was paid up front and in a currency investors could see. Five years later, that episode is still the single best data point in Rocket Lab's favour on the question of whether management will tell you when it has changed its mind. As we will see, the Neutron programme has given them repeated opportunities to demonstrate whether that instinct survived contact with a hard schedule.

What Neutron actually is

Neutron is a partially reusable medium-lift launch vehicle: roughly 43 metres tall, designed to deliver about 13,000 kg to low Earth orbit in expendable configuration, with a recoverable and reflyable first stage.20 It is powered by nine Archimedes engines on the first stage — a liquid oxygen and liquid methane, oxidizer-rich staged combustion design — producing approximately 1.5 million pounds of thrust at liftoff, with a vacuum-optimised Archimedes on the second stage.20

Two design choices distinguish it, and both are best explained without jargon.

The captive fairing — "Hungry Hippo." On a conventional rocket, the nose cone that protects the payload during ascent splits into two halves and is thrown away — or, in SpaceX's case, fished out of the ocean by boat and refurbished. Neutron's fairing instead stays attached to the first stage. It opens like a set of jaws, releases the second stage and payload, then closes again and comes home with the booster. The engineering benefit is that Rocket Lab never has to recover, clean, dry, and requalify a piece of salt-soaked structure. The engineering risk is that a large moving mechanism must work perfectly, twice, on every flight, in the highest-load region of the trajectory.

Composite everything. Neutron's structures are carbon composite, built on automated fiber placement machines — the same manufacturing philosophy as Electron, scaled up. This is the source of both Neutron's mass efficiency and, as it turned out, its most damaging setback.

Where it flies. Archimedes is tested at NASA's Stennis Space Center in Mississippi. Neutron launches from Launch Complex 3 at the Mid-Atlantic Regional Spaceport on Wallops Island, Virginia — Rocket Lab's second U.S. pad and the one that makes it a domestic medium-lift provider in the eyes of the Pentagon.

Why the Pentagon cares before the rocket flies

On March 27, 2025, the U.S. Space Force on-ramped Neutron to the National Security Space Launch Phase 3 Lane 1 programme — a firm-fixed-price IDIQ vehicle with a maximum value of $5.6 billion and an ordering period running to June 2029, alongside a $5 million task order for a capabilities assessment.21 Rocket Lab became one of only a handful of providers eligible to bid the Lane 1 manifest, on the basis of a vehicle that had not yet left the ground.

That is a genuine option, and it is also a reminder of the structure of this industry: the U.S. government is actively subsidising the existence of a second and third medium-lift provider because a monopoly supplier of national security launch is an unacceptable strategic condition. Rocket Lab's addressable market in defence launch is therefore not purely a function of being better than SpaceX. It is partly a function of not being SpaceX. Investors should count that as real, and should also recognise that a policy-created advantage can be un-created by policy.

Neutron's actual development record — the delays, the tank rupture, and what management said about both — is a management-credibility question, and belongs in that section. First, the financial engine as it exists today.

VI. Segment Breakdown & Financial Engine: Space Systems vs. Launch Services [01:37 - 02:02] (25 Mins)

Behind the corporate narrative, Rocket Lab in 2026 operates as two core business segments moving at different speeds—Launch Services and Space Systems—with a third, satellite services, slated to arrive through the pending acquisition of Iridium.

The scoreboard

Full-year 2025 revenue reached $601.8 million, up 38% year over year.[^8] GAAP gross margin improved to 34.4% from 26.6%, while non-GAAP gross margin rose to 39.7% from 32.0%.[^8] The company reported a GAAP net loss of $198.2 million and an adjusted EBITDA loss of roughly $101 million.[^8] Year-end backlog stood at $1.85 billion, a 73% increase.[^8]

First-quarter 2026 results accelerated that growth trajectory, as revenue grew 63.5% year over year to $200.3 million, GAAP gross margin reached a record 38.2%, non-GAAP gross margin hit 43.0%, net loss narrowed to $45.0 million, and adjusted EBITDA loss shrank to $11.8 million—topping management's guidance.8 Backlog roughly doubled year over year to $2.2 billion, allocated 41.5% to launch and 58.5% to Space Systems.8

The primary analytical takeaway lies in the margin trajectory accompanying that expansion. Generating 63.5% top-line growth while expanding gross margins by several hundred basis points indicates that incremental revenue was not achieved through price discounting, though Rocket Lab still consumed $77.4 million in free cash flow during the quarter.8

Space Systems: the actual business

Space Systems generated $136.6 million in the first quarter of 2026, up 57.2% year over year, spanning a distinct hierarchy of hardware and services.8

At the foundational level are components: reaction wheels, star trackers, separation systems, solar cells, optical terminals, and electric thrusters. These high-margin products are sold across the commercial space sector, including to direct launch competitors, while shortening Rocket Lab's internal supply chain. In the first quarter of 2026, the company introduced Gauss, a new electric propulsion product supported by a 200-unit production line, explicitly to relieve an internal supply chain bottleneck.8

At the middle layer sit spacecraft platforms—the Photon and Lightning bus architectures, alongside Flatellite, announced in February 2025 as a flat, stackable satellite designed for rapid constellation deployment.22 Flatellite signaled management's strategy to expand beyond hardware sales into constellation operations—an ambition later expanded through the proposed acquisition of Iridium.

At the top layer sits prime contracting, where segment economics become more complex.

The two SDA programmes. In December 2023, the Space Development Agency awarded Rocket Lab a $515 million contract to design, build, and operate 18 Transport Layer Beta satellites for the Proliferated Warfighter Space Architecture.[^26][^27] Two years later, on December 19, 2025, the SDA awarded Rocket Lab an $816 million prime contract—comprising an $806 million base plus roughly $10.45 million in options—to construct 18 Tracking Layer Tranche 3 missile-warning satellites featuring Rocket Lab's Phoenix infrared sensor payload and StarLite protection sensors, with final delivery expected in 2029.9

Combined, these awards represent over $1.3 billion in prime defense work, demonstrating that vertical integration has allowed Rocket Lab to win major defense contracts previously reserved for legacy primes.

However, the margin structure of prime contracting differs from component sales. Chief Financial Officer Adam Spice noted on the fourth-quarter 2025 earnings call that larger defense programs carry lower gross margins while delivering higher contribution dollars, as foundational R&D expenses are already absorbed.23 On the first-quarter 2026 call, Spice stated that SDA Tranches 2 and 3 contribute lower-margin revenue at scale, while newly acquired Mynaric requires operational integration to reach target margin levels.8 Second-quarter 2026 guidance reflected this margin pressure, projecting GAAP gross margins of 33% to 35%—below the 38.2% delivered in the first quarter—on revenue of $225 million to $240 million.8

Consequently, as Rocket Lab scales its prime contracting footprint, top-line growth and gross margin expansion remain in near-term tension.

Launch: smaller, and the reason everything else exists

Launch Services generated $63.7 million in the first quarter of 2026, up 78.9% year over year but down 16.1% sequentially due to fewer completed flights—reflecting launch revenue as a step function rather than a recurring annuity.8

Unit economics have steadily improved. On the first-quarter 2026 call, management noted that average Electron flight pricing increased from $5 million to $6 million in early operations to near $8.5 million—reflecting pricing power gained through launch schedule reliability.8

Two additional operational factors shape the segment's outlook.

HASTE. The Hypersonic Accelerator Suborbital Test Electron, a modified vehicle executing suborbital test missions for the Department of Defense, commands premium pricing and higher margins. In the first quarter of 2026, Rocket Lab booked a 20-launch, $190 million block order for HASTE, with management stating that hypersonic missions represent roughly one-third of launch backlog, alongside three dedicated HASTE launches signed with Anduril scheduled no earlier than November 2026.8

Capacity. Management stated that existing Electron manufacturing and launch infrastructure can support up to 52 missions annually with minimal additional capital expenditure.8 Compared with 21 launches completed in 2025, that infrastructure offers operational leverage if customer demand materializes.

What this all funds

Cash and marketable securities stood at approximately $1.48 billion at the end of the first quarter of 2026, with management citing total available liquidity exceeding $2 billion.8 That cash position was built primarily through equity offerings, with roughly $1.1 billion raised through at-the-market programs in 2025 and an additional $450.3 million raised in the first quarter of 2026, alongside the conversion of most of its 4.25% convertible notes into equity, which reduced remaining principal to $37.6 million.[^8]8

While funding operations through equity during periods of higher valuation preserved cash, it expanded the share count. With the stock down over 50% from its peak, the equity component needed to complete the Iridium acquisition will require issuing shares at a significantly lower valuation than during earlier capital raises.

VII. Competitive Landscape, Industry Structure, & Strategic Frameworks [02:02 - 02:22] (20 Mins)

Imagine the launch market as a strategic war map. There is one fortified position controlling most of the terrain, a handful of contested outposts, and a large graveyard of failed ventures.

The map

Small launch is effectively over as a contest. Virgin Orbit's assets sit inside Rocket Lab. Astra retreated to satellite propulsion. Firefly's Alpha flies infrequently. Relativity abandoned Terran 1 to pursue a larger vehicle that has yet to fly. Rocket Lab won this category by outlasting its peers, leaving Electron with virtually no dedicated small-launch competition in the West—facing pressure primarily from rideshare missions.

Medium and heavy launch remain dominated by SpaceX. Falcon 9 continues to serve as the industry benchmark and price setter, with SpaceX raising its list price to roughly $74 million in early 2026. Its cadence is measured in hundreds of flights a year, driven largely by its own Starlink deployments. Starship, the vehicle that could redefine launch economics entirely, has experienced continued schedule slips through 2026 and has not yet entered operational commercial service. Meanwhile, United Launch Alliance flies Vulcan Centaur, Arianespace operates Ariane 6, and Blue Origin's New Glenn suffered a pad explosion during a 2026 hot-fire test and is working toward a return to flight.

That last point cuts against the assumption that Neutron is entering an overcrowded market. Western medium-lift alternatives to Falcon 9 are either operating at low flight rates, recovering from serious setbacks, or still unproven. Neutron is running behind its management's original schedule, but it is not falling behind a field of runaway competitors.

Space Systems is the more genuinely contested arena. York Space Systems competes directly for Space Development Agency constellation awards. Terran Orbital was absorbed by Lockheed Martin, removing an independent producer and reinforcing that major primes view small-satellite manufacturing as strategic infrastructure. L3Harris, Northrop Grumman, and BAE's Ball Aerospace business all bid on the same government programs, while companies like Planet Labs compete in downstream data services. Rocket Lab's differentiation in this segment stems less from proprietary technology alone than from owning a larger portion of its internal bill of materials.

Seven Powers, honestly scored

Counter-positioning — strong, and the company's best power. Against SpaceX, Rocket Lab does not compete strictly on price per kilogram; it competes on orbit destination and schedule control. A rideshare launch drops secondary payloads into a fixed orbit dictated by the primary customer's timeline. For a defense operator replacing a critical orbital asset or a constellation operator filling a precise plane, rideshare is not a direct substitute. Against legacy primes, Rocket Lab offers fixed-price, vertically integrated spacecraft delivered on timelines that traditional cost-plus supply chains struggle to match—without the legacy prime's risk of cannibalizing subcontractor margins. The Space Development Agency contract wins serve as concrete evidence of this advantage.

Process power — real but narrower than claimed. Rocket Lab's accumulated operational knowledge in 3D-printed engines, automated composite layup, and high-tempo launch management is genuine and difficult to replicate quickly. However, the Neutron Stage 1 tank rupture in January 2026—caused by a defect introduced during a third-party hand layup before the company's automated fiber placement machine was commissioned—presents a direct counterexample.23 Process power that relies on machinery not yet fully operational represents an aspiration rather than an established moat. Transitioning production entirely to the automated fiber placement machine addresses the root cause, but it highlights that the internal capability was not fully in place when needed.

Cornered resource — concentrated, and therefore a risk as much as an asset. Peter Beck, knighted in 2024 as a Knight Companion of the New Zealand Order of Merit for services to aerospace, combines hands-on propulsion engineering, capital allocation, and executive leadership.24 Founder-led organizations of this structure gain speed and decisiveness, but they also carry key-person risk and a governance structure in which top conviction is rarely challenged internally. The ambitious Iridium transaction serves as a case study in both dynamics.

Scale economies — emerging, not yet demonstrated. Manufacturing solar cells, reaction wheels, separation systems, sensors, thrusters, and optical terminals in-house should theoretically lower satellite production costs relative to competitors purchasing components on the open market. Chief Financial Officer Adam Spice asserted precisely that, attributing the Space Development Agency Tranche 3 contract win to vertical integration.8 However, consolidated gross margins remain in the 30% range, and the company's largest prime programs carry lower gross margins than individual component sales. Scale economies remain a logical strategic thesis supported by early awards, but not yet a fully proven cost position.

Switching costs and branding — modest. Flight heritage provides meaningful credibility in satellite manufacturing and launch services, but direct network effects are essentially absent.

Porter's Five Forces

Supplier power: low, by design and by acquisition. This is the direct payoff of the M&A strategy. Notably, on the fourth-quarter 2025 earnings call, Spice identified subcontractor deliveries as the binding constraint on how fast Space Development Agency revenue could be recognized—which is simultaneously an argument for further integration and evidence that integration remains incomplete.23

Threat of new entrants: low. The 2021–2022 collapse in space SPAC financing, followed by a series of industry bankruptcies, has left private capital cautious toward pre-revenue launch ventures. While startups like Stoke Space persist, the broad funding window that enabled the previous cohort has closed.

Buyer power: moderate to high, and rising. The Space Development Agency and defense customers award large fixed-price contracts and maintain strong programmatic leverage. Fixed-price structures require Rocket Lab to absorb cost overruns. Commercial constellation operators, meanwhile, retain a credible alternative in SpaceX for most missions.

Substitutes: the central strategic risk. Rideshare services substitute for dedicated small launch at the margin, while Starship, if it achieves high launch cadence at low cost, presents a potential substitute across all payload classes.

Rivalry: intense in Space Systems, asymmetric in launch. Rocket Lab competes against defense prime contractors many times its size in satellite manufacturing, while facing a single, vastly larger dominant competitor in launch.

The framework verdict: Rocket Lab's competitive position is strongest where it is least emphasized in public discussions—in individual components and integrated defense spacecraft—and weakest where mainstream narrative attention concentrates.

VIII. Management Credibility, Conference Call Q&A Audit, & Governance [02:22 - 02:37] (15 Mins)

The most revealing test of a management team is not how it communicates when a development program proceeds smoothly, but how it accounts for operational setbacks in the aftermath of a failure.

February 26, 2026: the tank

On its third-quarter 2025 conference call in November, Rocket Lab informed investors that Neutron would arrive at Launch Complex 3 in the first quarter of 2026, with the maiden launch to follow—already a delay from an earlier target of late 2025.2526 Chief Executive Peter Beck emphasized at the time that additional testing and qualification were required, reiterating that the company would avoid learning critical operational lessons in flight rather than on the ground.25

In January 2026, however, a Neutron Stage 1 propellant tank ruptured during hydrostatic pressure testing.

On the fourth-quarter 2025 call, Beck addressed the failure with greater technical specificity than is customary in the launch industry. The tank had satisfied anticipated flight loads; the rupture occurred when engineers expanded the test envelope to characterize structural margins. The root cause was a manufacturing defect at a critical joint, introduced during a hand layup performed by a third-party supplier while Rocket Lab's automated fiber placement (AFP) machine was still being commissioned. Beck stated that the replacement tank was "being built on the AFP machine, completely eliminating the possibility of this hand defect reoccurring," alongside design modifications to improve structural margin and manufacturability.23 The target for the maiden launch moved to the fourth quarter of 2026, with Beck maintaining that "the priority will always be to bring a reliable rocket to market, even if it means taking a few extra months."23

Evaluating this disclosure reveals two opposing interpretations. The immediate communication was transparent: management disclosed a specific root cause, a targeted engineering fix, and an explicit schedule adjustment within the quarter the event occurred, rather than allowing details to emerge via media leaks. During the call, Stifel analyst Erik Rasmussen questioned whether a fourth-quarter 2026 launch remained realistic and whether producing a replacement tank would increase capital expenditures. Chief Financial Officer Adam Spice responded that the incremental expense was modest because, with the automated fiber machine commissioned, only variable material costs applied.23

Conversely, the setback represented the third schedule revision for Neutron, occurring in composite manufacturing—a core competency highlighted by the company. By the end of 2025, cumulative Neutron development spending was tracking toward approximately $360 million against an original budget of $250 million to $300 million, with management estimating that each quarter of delay added roughly $15 million in ongoing staffing costs.25

May 7–8, 2026: the credibility rebuild

The first-quarter 2026 conference call delivered the strongest quarterly financial results in company history. Beck outlined parallel qualification milestones: Stage 1 tank refinements using AFP-produced components on the shop floor, stage-separation testing completed under full flight loads and advancing to off-nominal conditions, Archimedes engines undergoing testing at NASA's Stennis Space Center in both first-stage and vacuum configurations, thermal protection installed on the reusable fairing, and construction of the recovery barge targeting sea trials later in 2026.8

Beck also provided analysts with specific operational parameters for the maiden mission, clarifying: "On flight one, we will attempt soft splashdown to test reentry engine relights. Provided all goes well, we slip the barge under it and attempt landing on flight two."8 This framework established clear public expectations by separating a successful orbital debut from booster recovery.

Regarding launch cadence, Beck projected a gradual scale-up of "one, three, five" launches, mirroring Electron's operational ramp.8 Program execution delivered a key physical milestone on July 13, 2026, when Rocket Lab announced a successful full-duration burn of a vacuum-configured Archimedes engine lasting just under five and a half minutes.27 Because engine qualification often represents the primary schedule constraint in launch development, a full-duration hot fire provided concrete physical progress.

Despite those operational milestones, Beck declined to narrow the maiden launch target beyond year-end 2026, stating that schedule estimates would refine as the launch date approached.8 Given three prior schedule revisions, the lack of a tighter launch window leaves investors without a firm timeline for the vehicle's orbital debut.

Narrative consistency across the record

Across conference calls from 2024 through 2026, Rocket Lab's strategic thesis has remained consistent: launch serves as a customer acquisition channel, Space Systems acts as the primary economic driver, vertical integration provides cost advantages, and end-to-end satellite services represents the long-term destination.[^33] While management has maintained this strategic framing, the capital required to execute it has expanded significantly—a shift reflected in increased balance-sheet leverage, larger acquisition scales, and ongoing equity issuance.

Governance: the parts that should make investors uncomfortable

Insider selling. Between July 6 and July 8, 2026, Beck's family entity, the Equatorial Trust, sold 3,275,779 shares for approximately $286.4 million at weighted-average prices ranging from roughly $81.59 to $101.57, executed under a Rule 10b5-1 trading plan adopted on March 27, 2026.28 Because the 10b5-1 plan was established three months before the Iridium acquisition announcement, the sales were pre-scheduled rather than discretionary. A concurrent Schedule 13D filing disclosed a five-million-share trading plan alongside the cancellation of certain restricted stock units.29 Nevertheless, the transaction involved the founder selling $286 million in stock within a week of announcing an $8.0 billion leveraged acquisition—the largest and highest-risk transaction in company history—shortly before Rocket Lab shares experienced a steep drawdown.

Ownership and control. As of March 20, 2026, Beck and affiliated New Zealand entities held 46,443,180 shares, representing approximately 7.51% of common stock, with most of that exposure held through Series A convertible participating preferred stock in the Equatorial Trust.29 While this represents meaningful financial alignment, it falls below the 10% equity threshold common among founder-led technology firms, and the governance terms associated with preferred share structures warrant ongoing investor examination.

Structural complexity. The May 2025 corporate reorganization established Rocket Lab Corporation as the top-level holding entity—a restructuring management attributed to U.S. government security requirements.7 However, when combined with international manufacturing operations, four acquisitions within an eighteen-month span, and a pending $8.0 billion transaction, the consolidated corporate structure increases analytical complexity. For investors, this operational and reporting complexity places added importance on accounting judgments involving purchase price allocations, goodwill valuations, and percentage-of-completion revenue recognition on long-term fixed-price defense programs in future financial filings.30

IX. Material Risk Radar & The Skeptical Investor Stress Test [02:37 - 02:50] (13 Mins)

Every risk in this business ultimately reduces to two fundamental questions: does the rocket work, and does the capital last?

1. Neutron execution — the binary

Maiden flights of new orbital launch vehicles fail at a historically high rate. Rocket Lab's own Electron failed to reach orbit on its debut. Chief Executive Peter Beck stated that the goal for Neutron is orbit on the first attempt and, on the third-quarter 2025 conference call, was explicit about the rationale: "We've seen what happens when others rush to the pad with an unproven product, and we just refuse to do that."26

The specific operational risks are clear. The Stage 1 propellant tank was redesigned and rebuilt on new automated tooling and must complete structural qualification. Archimedes must demonstrate reliable ignition and performance across nine clustered first-stage engines, having so far demonstrated full-duration operation on a single second-stage unit.27 The captive fairing mechanism must actuate correctly under aerodynamic loads. Furthermore, the reusability economics—the foundation of Neutron's ability to compete on price with Falcon 9—will not begin testing until the second flight.8

An initial flight failure would not be fatal, but it would prove costly in both consumed cash and schedule delay. A second consecutive failure would raise structural questions about the program.

2. Capital and the financing stack

This financing risk represents the core driver of the stock's recent repricing. Rocket Lab is consuming free cash flow, guiding toward further adjusted EBITDA losses, funding Neutron's development, and committing to a $3.6 billion bridge facility whose cash draw is scheduled for a mid-2027 closing.82 The bridge loan is a 364-day instrument that must be refinanced with permanent debt and equity in future credit and equity markets.

The company's $1.48 billion cash position provides liquidity, but it is insufficient on its own to fund the cash consideration for the Iridium transaction.8 Issuing equity at a share price roughly 58% below its peak results in significantly greater dilution than an offering executed at earlier valuation highs.4 The exchange-ratio collar operates symmetrically: if Rocket Lab shares trade below $67.50, the company must issue additional shares to satisfy the transaction value.2

3. Starship and the technology-disruption tail

If SpaceX achieves operational cadence with Starship at dramatically lower costs per kilogram, the pricing structure supporting Neutron's commercial margins will narrow. While this disruption risk is real, it is often framed too broadly. Starship's development timeline through 2026 has extended Neutron's market window, and a significant portion of Rocket Lab's defense awards is driven by customer requirements for assured access, supplier diversity, and sovereign capability that lower launch costs alone do not override. The precise risk is not that Starship eliminates Neutron, but that it reduces the long-term return on the roughly $360 million invested in Neutron's development.

A secondary financial risk stems from market structure. With SpaceX publicly listed and added to the Nasdaq-100 index in early July 2026, Rocket Lab no longer holds scarcity value as the sole liquid pure-play commercial space stock.531 This shift directly affects cost of capital: a company planning to issue equity as part of an $8.0 billion transaction now competes for institutional allocations against a market-dominant peer during a period when its own share price has halved.

4. Government concentration and programme risk

Contract awards from the Space Development Agency, HASTE missions, National Security Space Launch eligibility, and missile interceptor research position the U.S. government as Rocket Lab's primary customer. On May 7, 2026, Rocket Lab and Raytheon were selected to demonstrate capabilities for the Space Force's Space Based Interceptor program, with Raytheon serving as one of twelve prime awardees sharing agreements worth up to a combined $3.2 billion and targeting an initial demonstration in 2028.3233 The contract structure is distinct: Rocket Lab serves as a subcontractor to Raytheon on that program rather than a prime contractor, representing a developmental option tied to defense priorities rather than booked backlog.

Defense programs remain vulnerable to cancellation, budget adjustments under continuing resolutions, and shifting political priorities. A substantial portion of Rocket Lab's $2.2 billion backlog depends on federal appropriations beyond corporate control. Furthermore, because major defense awards are structured as fixed-price contracts, any cost overruns must be absorbed directly by Rocket Lab.

5. Integration and attention

Executing four completed acquisitions within eighteen months, managing a pending $8.0 billion transaction, preparing for a maiden medium-lift flight, and building out two satellite constellations create significant operational complexity. Chief Financial Officer Adam Spice acknowledged that newly acquired Mynaric requires margin remediation.8 Managing multiple complex integrations simultaneously represents an execution challenge that financial statements do not fully capture.

The activist stress test

A skeptical investment case highlights several interconnected vulnerabilities:

"Rocket Lab's launch segment represents 32% of revenue and cannot scale without a rocket that has never flown. Space Systems is growing primarily through lower-margin prime contracts. Management funded this expansion by issuing over $1.5 billion in equity across 2025 and early 2026, and with the stock down over 50%, committed to a leveraged acquisition of a mature communications operator that risks diluting top-line growth and compressing valuation multiples. Meanwhile, the founder sold $286 million in stock in the same period. What specific risk-adjusted return does this structure offer shareholders?"

This perspective reflects verifiable financial disclosures.

Arguments that hold up under examination. Rocket Lab is not an unproven launch startup. Space Systems operates as an established segment with substantial backlog, key positions in solar cells and optical terminals, and $1.3 billion in prime defense contracts.9[^26] Gross margins have expanded alongside revenue growth rather than compressing.8 Electron's pricing history demonstrates realized pricing power on an established launch vehicle. Furthermore, Iridium generates roughly $495 million in annual operational EBITDA, introducing significant cash flow to a combined entity that currently reports net losses.2

Arguments that do not hold up. Past success in integrating small component suppliers does not guarantee the successful integration of a large leveraged enterprise. A single engine test milestone does not establish Neutron's operational schedule reliability. Finally, defense contract backlog cannot be treated as realized revenue until program milestones are successfully delivered.

X. The Investment Spine: Bull vs. Bear Case & What to Watch [02:50 - 03:00] (10 Mins)

Peter Beck built Rocket Lab over two decades by challenging industry assumptions regarding small launch and vertical integration. However, the company has now taken on a set of operational and financial commitments where engineering execution is necessary but no longer sufficient. The next twelve months will resolve more of the enterprise's long-term trajectory than the previous five years did.

The three things that actually matter

Evaluating Rocket Lab requires focusing on three primary operational and financial metrics:

1. Neutron: flight-one outcome, followed by the timeline to flight two and the first booster reflight. The maiden launch serves as a binary test of whether the company's medium-lift capability exists. However, the more economically consequential milestone is what occurs afterward. Management has stated that a landing attempt will occur on the second flight, and that rapid reusability underpins Neutron's projected cost structure.8 An orbital rocket that flies successfully but cannot be recovered and reused promptly yields a lower return on capital than current valuation models assume. The key metric to watch is the interval between the first three flights relative to management's "one, three, five" annual launch cadence framework.

2. Space Systems gross margins as the Space Development Agency programs scale. This provides the clearest indicator of whether vertical integration produces a genuine structural cost advantage. Rocket Lab has committed to delivering large fixed-price constellations at gross margins management described as below the corporate average, while simultaneously contending that in-house component manufacturing yields superior economics compared to non-integrated competitors.823 As Tranche 2 and Tranche 3 hardware deliveries peak, segment gross margins will clarify whether scale generates margin expansion or persistent margin compression.

3. The Iridium financing structure: fully diluted share count and pro forma net debt. While strategic debates over the transaction will persist until closing, the financial mechanics are immediate. Investors must track how the $3.6 billion bridge loan facility is refinanced into permanent debt, the prevailing interest rates, and the number of new equity shares issued to complete funding. This capital structure outcome will exert a larger influence on per-share equity value over the near term than any single operational milestone.24

The bull case

Under the optimistic thesis, Neutron achieves orbit on its debut and successfully recovers a first-stage booster within its initial flight sequence. Rocket Lab then emerges as the primary Western alternative to SpaceX's Falcon 9 for medium-lift commercial and national security payloads—benefiting from customer demand for supplier diversity and government policy favoring multiple launch providers.

Space Systems accelerates through execution on $1.3 billion in Space Development Agency prime contracts, HASTE hypersonic missions accounting for one-third of the launch backlog, and high-margin component sales to external market participants.89 Vertical integration translates into measurable unit-cost advantages at higher production volumes, sustaining the gross margin expansion established in early 2026.

Upon closing the Iridium acquisition, Rocket Lab absorbs roughly $495 million in annual operational EBITDA, globally licensed spectrum, and approximately 2.55 million active subscribers.2 This transaction transforms a capital-consuming hardware manufacturer into a cash-generative space systems operator capable of manufacturing, launching, and operating its own satellite constellations.

The bear case

Conversely, the cautious thesis highlights schedule and balance-sheet risks. If Neutron encounters an initial flight failure or struggles to demonstrate rapid reusability, commercial launch revenue slides into 2028 while ongoing operational expenditures consume additional capital. Refinancing the Iridium transaction in a volatile equity market risks significant shareholder dilution at depressed valuations or high-cost debt servicing, burdening the enterprise with substantial balance-sheet leverage while core operations continue to generate GAAP losses.4

Additionally, fixed-price defense contracts carry potential cost overrun risks, while recent acquisitions such as Mynaric may require longer integration timelines before reaching target margins. As Iridium's mature growth profile blends into consolidated revenue, top-line growth could decelerate, prompting public markets to value the combined business as a leveraged satellite operator rather than a high-growth technology platform.

In the background, if SpaceX achieves operational cadence and cost reductions with Starship, industry pricing across medium-lift launch could compress just as Rocket Lab attempts to recoup Neutron's development investment.

The unresolved question

The analytical consensus on Rocket Lab in mid-2026 rests on a clear dichotomy: the company has demonstrated an ability to manufacture complex aerospace hardware reliably and economically, but it is now asking investors to underwrite execution across three unproven domains—large-scale leveraged acquisitions, medium-lift launch operations, and subscription satellite services.

Management's overarching objective is to construct a modern defense prime: using launch as a customer acquisition vehicle, integrating the satellite supply chain through targeted acquisitions, establishing medium-lift launch as access to national security infrastructure, and operating an active orbital constellation. The strategy forms a vertically integrated architecture where operational segments reinforce one another.

The central debate centers on whether this architecture can be assembled at a pace supported by the company's capital structure. The maiden flight of Neutron will address operational capability, while the finalized Iridium financing terms will clarify capital structure durability. For an enterprise that began in Invercargill with suborbital sounding rockets, the remaining questions remain centered on execution.

References

-

Rocket Lab to Acquire Iridium in Historic Deal, Creating A Fully Vertically Integrated Space Powerhouse Primed for Growth — PR Newswire, 2026-06-29 ↩↩↩↩↩↩↩↩↩↩↩↩

-

Rocket Lab pops 16%, Iridium soars 25% on $8 billion space consolidation deal — CNBC, 2026-06-29 ↩

-

Rocket Lab Has Fallen 58% From Its High While Wall Street's Average Target Sits 79% Above the Price — The Motley Fool, 2026-07-28 ↩↩↩↩↩

-

SpaceX market cap tops $2 trillion after shares of Elon Musk's rocket company gain 19% on debut — CNBC, 2026-06-12 ↩↩

-

Rocket Lab To Join The Nasdaq-100 Index — GlobeNewswire, 2026-06-12 ↩

-

Rocket Lab Corporation Form 8-K on Holding Company Reorganization — SEC EDGAR, 2025-05-23 ↩↩

-

Rocket Lab (RKLB) Q1 2026 Earnings Call Transcript — The Motley Fool, 2026-05-08 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Rocket Lab Awarded $816M Prime Contract to Build Missile-Defense Satellite Constellation for U.S. Space Force — Rocket Lab Investor Relations, 2025-12-19 ↩↩↩↩

-

Rocket Lab Successfully Launches for iQPS, Ends 2025 With 21 Launches and 100% Mission Success — Barchart, 2025-12 ↩

-

Rocket Lab to Acquire Satellite Hardware Manufacturer Sinclair Interplanetary — Rocket Lab, 2020-03-16 ↩

-

Rocket Lab's Interplanetary Focus Expands With New $40M Buy — Forbes, 2021-10-14 ↩

-

DoD Awards CHIPS Act Funding to Rocket Lab to Expand Domestic Solar Cell Production — U.S. Department of Defense, 2024-06-11 ↩

-

Rocket Lab buys Virgin Orbit's California headquarters in asset auction — Reuters, 2023-05-23 ↩

-

Rocket Lab Closes Acquisition of Geost, Expanding Its National Security Capabilities with Launch, Spacecraft, and Now Payloads — Rocket Lab, 2025 ↩

-

Rocket Lab Announces Intention to Acquire Mynaric, Leading Laser Communications Provider — Rocket Lab, 2025-03-11 ↩

-

Mynaric Completes StaRUG Process Amid Rocket Lab Acquisition Deal — Via Satellite, 2025-08-19 ↩

-

Vector Acquisition Corp / Rocket Lab De-SPAC Prospectus (Form S-4/A) — SEC EDGAR, 2021-07-21 ↩

-

Rocket Lab delays debut of powerful, partially reusable Neutron rocket to 2026 — Space.com, 2025-11-11 ↩↩

-

Rocket Lab's Neutron Rocket On-Ramped to U.S. Space Force's $5.6b National Security Space Launch (NSSL) program — Business Wire, 2025-03-27 ↩

-

Rocket Lab Announces Flatellite: A New Satellite Designed for Mass Manufacture and Tailored for Large Constellations — Business Wire, 2025-02-27 ↩

-

Rocket Lab (RKLB) Q4 2025 Earnings Call Transcript — The Motley Fool, 2026-02-26 ↩↩↩↩↩↩↩

-

Sir Peter Beck: Ambitions interplanetary and down-to-Earth — RNZ, 2024 ↩

-

Rocket Lab delays debut of Neutron rocket to 2026 — Spaceflight Now, 2025-11-11 ↩↩↩

-

Rocket Lab delays first Neutron launch to 2026 — SpaceNews, 2025-11-11 ↩↩

-

Watch Archimedes burn! Rocket Lab fires up engine for its powerful next-gen Neutron launcher — Space.com, 2026-07-13 ↩↩

-

Rocket Lab CEO Peter Beck sells $286.4m in company stock — Investing.com, 2026-07-09 ↩

-

Schedule 13D/A — Rocket Lab Corp, Beck beneficial ownership — StockTitan, 2026 ↩↩

-

Rocket Lab Corporation Form 10-K for fiscal year 2025 — SEC EDGAR, 2026-02-26 ↩

-

SpaceX stock closes below debut price at $148 in two-day slide after Nasdaq-100 inclusion — CNBC, 2026-07-08 ↩

-

Rocket Lab and Raytheon Selected To Demonstrate Advanced Capabilities For U.S. Space Force's Space Based Interceptor Program — GlobeNewswire, 2026-05-07 ↩

-

Rocket Lab joins Raytheon on space interceptor program for Golden Dome — SpaceNews, 2026-05-07 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube